santiago exchange's guide to responsible …inter.bolsadesantiago.com/sitios/en/biblioteca...

TRANSCRIPT

1

Santiago Exchange's

GUIDE TO RESPONSIBLE

In collaboration with EYINVESTMENT

2017

2

Prologue Santiago Exchange Prologue Principles for RI

I. Introduction

II. Objectives of the RI Guide

III. Definition of Responsible Investment

III.1. RI in Capital Markets

III.1.1 The Role of Investors

III.1.2 The Role of Issuers

III.1.3 The Role of Exchanges

III.1.4 Role of Rating Agencies and External Assurance Firms

III.2. Benefits of Responsible Investment

IV. Responsible Investment in the World

IV.1. Global Context of Responsible Investment

IV.2. International RI Initiatives

0607

08

09

13

14

14

15

15

15

16

21

22

23

CONTENIDO

3

IV.3. Responsible Investment in Latin America

IV.4. Latin American RI Initiatives

IV.5. Responsible Investment in Chile

IV.5.1. Dow Jones Sustainability Chile Index (DJSI Chile)

IV.5.2. New Regulatory Developments

V. Decision Making in Responsible Investment

V.1. Responsible Investment Strategies

V.2. Examples of Applying these Strategies

V.3. Steps to Follow to Invest Responsibly

V.4. Access to Corporate ESG Information

Additional ResourcesReferencesAcknowledgemnts and Contact

24

25

26

27

28

31

32

33

36

37

43

48

50

4

PROLOGUE SANTIAGO EXCHANGE

One of our challenges at Santiago Exchange is to promote

responsible investment with a special emphasis on en-

couraging best practices in self-regulation, transparency

and innovation.

In capital markets, Responsible Investment is defined

as an investment approach that incorporates environ-

mental, social and corporate governance (ESG) factors.

With that definition in mind, the objective of this guide

is for these topics to be incorporated and considered in

decision making and investment practices.

The need to develop—together with EY—this guide arose

as part of Santiago Exchange's commitment to promote

sustainability in capital markets. We hope this guide serves

as a tool to help investors incorporate these topics and

to educate them on the implications that sustainability

has on all their decisions.

Santiago Exchange is committed to incorporating sus-

tainability in the capital markets and to playing a key

role as a promoter of ESG issues. These issues are being

integrated in response to the numerous benefits linked

to such practices, which include identifying new business

opportunities; improving access to capital; and keeping

ahead of regulatory and social changes, among others.

Today global markets have incorporated more and more

recommendations and products related to sustainability.

The fact that investors are demanding more and better

5

José Antonio Martínez Z.Chief Executive OfficerSantiago Stock Exchange

information on the topic prompted the creation of this

guide, which aims to support and guide investors in un-

derstanding Responsible Investment, identifying ESG risks

and opportunities and communicating the principles and

potential of Responsible Investment.

Stock exchanges currently play a unique role in building

more sustainable capital markets. In light of this role, our

exchange must work to ensure the sustainable develo-

pment of both our organization and the capital market.

This is achieved by implementing the highest standards

of transparency, responsible investment and corporate

governance in the Chilean market in order to meet the

expectations of the exchange's diverse stakeholders.

In terms of sustainability, our exchange has carried out

diverse initiatives to promote and incorporate ESG issues,

such as launching two versions of Chile's first Sustaina-

bility Index; organizing—together with UN Women and

UN Global Compact—a local version of Ring the Bell for

Gender Equality; and publishing this and other guides

to promote the incorporation of sustainability issues by

different market agents, to name a few.

We hope this document teaches you more about the sco-

pes, objectives and advantages of Responsible Investment

and enhances investor decision-making processes.

6

PROLOGUE PRINCIPLES FOR RI

At the UN-supported Principles for Responsible Invest-

ment, we work to create an economically efficient,

sustainable global financial system that supports long-

term value creation. We believe that such a system will

be more resilient, reward responsible investment and

benefit the environment and society as a whole.

As one of the four organizers of the UN Sustainable Stock

Exchanges (SSE) initiative, we see stock exchanges as

a fulcrum in the financial system; influencing market

practices and the application of financial regulation

that can either support or undermine a sustainable

financial system.

An important role for stock exchanges to play to support

a more sustainable system, is to educate and help close

the information gap between companies and investors

about sustainable business and investment practices.

Incorporating environmental, social and governance (ESG)

issues into the investment process allows investors to allo-

cate capital towards well-governed companies, that work to

create sustainable economies. This approach is consistent

with the increasingly global understanding that fiduciary

duty requires investors to take account of ESG issues in

their investment processes, in their active ownership un-

dertakings, and in their public policy engagement.

7

Investor practice on ESG issues is improving, but not suffi-

ciently to support a sustainable financial system. Guidance

documents and directives from stock exchanges and regu-

lators can play a critical role in helping investors advance in

this work.

As such, we applaud the work of Santiago Exchange in crea-

ting this guidance for investors, as well as the complementary

guidance for companies. The release of the two, complimentary

guides sends a signal that should help drive both transparen-

cy and long-term value creation. It is a strong example of the

actions an exchange can take to bolster the long-term health

and viability of its market and ensure the financial system is

contributing positively to society as a whole.

Nathan FabianDirector of Policy and ResearchUN-supported Principles for Responsible Investment

* Guía de Reportería en Temas de Sostenibilidad para Emisores.

8

New market demands and regulations emerging

from society and government bodies regarding the

activities of companies and financial institutions

have paved the way for the concept of responsible

investment (also known as RI) to gain increasing

strength and importance for investors.

Responsible investment involves the consideration

of environmental, social and governance (ESG)

matters, as well as other financial drivers, when

making investment decisions, which is also known

as sustainability performance. While ESG factors

are at times called “non-financial” or “extra-fi-

nancial”, how an investor manages them undoub-

tedly has financial consequences. An investment

that considers these factors is a responsible and

sustainable investment that seeks to ensure and

maximize medium- and long-term returns, incor-

porating risks and opportunities that arise from

corporate performance in these dimensions.

In order to provide a tool to guide investors on

ESG issues and support them in incorporating sus-

tainability into decision making and investment

practices, Santiago Exchange has developed this

Guide to Responsible Investment, in collaboration

with EY (formerly Ernst & Young), as part of an

agreement to generate information of interest to

the financial market, thus helping enhance trust

and transparency for stock market participants.

INTRODUCTIONI

9

This guide was also prepared as part of Santiago

Exchange's commitment arising from its involve-

ment in the Sustainable Stock Exchanges (SSE)

initiative, which it joined in 2014.

The guide is intended to provide information about

the concept of and context surrounding responsi-

ble investment to the general public as well as to

provide guidance for institutional investors and

financial and investment analysts to adopt this

new trend by incorporating ESG issues into the

investment process.

The guide was prepared using benchmarks and local

and international studies on responsible investment

to identify best practices and alternatives for im-

plementation in the Chilean financial market. The

contents of this document were developed in con-

junction with experts in responsible investment,

issuers and investors that took part in collaborati-

ve workshops to reach a consensus regarding the

right approach for responsible investment in the

Chilean market.

10

OBJECTIVES OF THE RI GUIDEII

11

The objective of this guide is to promote the main elements

for responsible investment among investors and the general

public, as well as to provide a tool to help investors incorpo-

rate ESG issues in their decision making and practices.

The guide was prepared with the help of financial market

stakeholders participating in three workshops held between

June and September 2016. These workshops brought toge-

ther issuers with experience in corporate sustainability, ex-

perts in responsible investment and private and institutional

investors that have incorporated or are interested in incor-

porating these issues in their investment decisions. These

opportunities for debate and consensus laid the foundation

for the content of the Chilean securities market's first Guide

to Responsible Investment.

In order to provide a tool that helps investors integrate ESG

issues into investment processes, the guide seeks to achieve

the following specific objectives:

Objective 1: Understand responsible investment

The second objective of this guide is to show how traditional financial

analysis, which does not consider ESG factors, neglects the potential return

associated with the performance of these variables.

ESG returns can be both positive and negative. Therefore, they must be

considered from a risk perspective when making investment decisions, but

they must also be considered as an opportunity factor for portfolio returns.

Objective 2: Identify ESG risks and opportunities Objective 4: Explore the potential of responsible investment

Lastly, the fourth objective of the guide is to demystify prejudices regarding

RI and the incorporation of “non-financial” variables in investment decisions,

in order to demonstrate that investing responsibly provides possibilities

for economic return with lower risk levels and a long-term outlook.

This guide aims to introduce the concept and definition of RI based on

current global consensus.

The guide's third objective is to provide readers with a series of perspec-

tives and actions to consider when deciding to incorporate ESG variables

in their investment decisions as well as useful information sources.

Objective 3: Determine strategies and steps to invest responsibly

12

DEFINITION OF RESPONSIBLE INVESTMENT

III

13

Responsible investment is an investment approach that

explicitly acknowledges the relevance for the investor of

ESG factors, and of the health and long-term stability of the

market as a whole. It recognizes that the generation of long-

term, sustainable returns depends on the stability, proper

functioning and good management of social, environmental

and economic systems. Responsible investment differs from

conventional investment approaches in two ways:

• The first is that timing is important. The main objective of

responsible investment is the creation of investment returns

that are sustainable over the long-term and not only focused

on the present.

• The second is that responsible investment requires investors

to pay attention to the context surrounding the investment, in-

cluding the stability and health of economic and environmental

systems and the evolution of societal values and expectations.

Making the analysis of ESG issues an integral part of the

investment process enables investors to comprehensively

evaluate the risks and opportunities associated with the

topic. This allows them to make better decisions and facili-

tates the investment valuation process in capital markets. It

also helps improve the quality of dialog between companies

and their investors in generating long-term value, offers

incentives for companies to improve their management

and encourages investors to actively seek opportunities

involving ESG factors.

The growing interest in responsible investment has been driven

by the financial industry's recognition that risks and opportuni-

ties associated with the performance and impact of ESG factors

are material. The industry has also deepened its understanding

of the integration of these aspects, mainly because effective

research, analysis and management of these areas have been

demonstrated to be a key part of evaluating an investment's

performance in the short-, medium- and long-term.

Furthermore, responsible investment incorporates active dialog

between investors and companies regarding their performan-

ce and the impact of ESG variables into decision making and

investment management practices, and integrates their risks

and opportunities into portfolio management.

In fact, it can be said that the growing global interest in res-

ponsible investment has been driven by the following factors:

• Recognition of the financial importance of ESG issues.

• The understanding that integrating these factors is part of

an investor's fiduciary duty with its clients and beneficiaries.

• Concern for the consequences of a short-term outlook on

company operations, investor returns and market behavior.

• Public policies that have begun to demand that inves-

tors exercise their rights and responsibilities as owners of

their investments.

• Pressure from competitors that seek to differentiate themsel-

ves through responsible investment and sustainability practices.

• Ethical motivations from investors, clients and beneficiaries.

III.1. RI in Capital MarketsIII.1.1. The Role of Investors

Strong financial performance is no longer the only criterion that

affects long-term investment returns. The management of ESG

issues, sometimes called “non-financial” or “extra-financial”

risks or opportunities, undoubtedly has financial consequen-

ces. For this reason, investors are called to fulfill their fiduciary

duty, which seeks to ensure that those that manage third-party

14

funds act responsibly, placing the interests of their clients or

beneficiaries over their own interests. By incorporating ESG

factors into investment practices and decisions, investors better

manage investment risks and opportunities, while contributing

to the country's sustainable economic development.

The trend toward responsible investment is growing and, the-

refore, the number of investors that consider ESG issues in the

investment process1, is increasing.

III.1.2. The Role of IssuersIssuers have begun to integrate ESG issues into their strategic

management, recognizing that society has increasingly higher

expectations regarding their conduct and behavior, acknowle-

dging that they are called to foster and play a leading role in

the sustainable development of the economy, balancing the

economic, social and environmental results of their operations.

Today, a company's role in sustainability is to continuously seek

the economic viability of the business, coexisting in harmony

with the environment and the neighboring community.

III.1.3. The Role of Exchanges

Exchanges have a fundamental role in building sustainable

capital markets. As a meeting point for the diverse players

that make up the market, exchanges play a leading role in

setting standards as well as developing and promoting good

practices that strengthen the capital market and society as a

“whole.” This is why Santiago Exchange works every day to

continuously develop the organization and the capital markets

through ongoing knowledge, understanding and practice of the

highest standards of transparency, responsible investment and

corporate governance.

Santiago Exchange began working with corporate sustaina-

bility and responsible investment by joining major initiatives

such as the United Nations Sustainable Stock Exchanges (SSE)

Initiative and the World Federation of Exchanges Sustainable

Working Group (SWG). Also, in its role as a promoter of best

practices in sustainability, it has proposed recommendations

for issuers listed with Santiago Exchange2 and prepared a

Sustainability Reporting Guide3, in order to strengthen the

stock market's transparency and enhance information provi-

ded by issuers to investors. In addition, it has developed tools

to encourage responsible investment in the capital market,

including the first local sustainability index, the Dow Jones

Sustainability Chile Index (DJSI Chile). Along with this guide,

these tools are helping raise the sustainability standard in

Chile and increase transparency about how sustainability

and responsible investment are being integrated by Chilean

capital market participants.

III.1.4. Role of Rating Agencies and External Assurance Firms

ESG corporate rating agencies are institutions specialized in

assessing issuers' performance in sustainability aspects. They

have been promoted mainly by investors that need ESG infor-

mation, in addition to financial information, for investment

decision making.

These ESG rating agencies evaluate issuers on their sustainabi-

lity performance based on publicly available information and, in

some cases, with assistance from the company being assessed.

The rating methods are based on industry-specific standards

that are comparable with each other in order to facilitate in-

vestment decision making. One example of these institutions

is RobecoSAM4, the rating agency for Chilean companies being

evaluated for Santiago Exchange's Dow Jones Sustainability

Chile Index (DJSI Chile).

1 2014 Global Sustainable Investment Review (2015) findings show that inves-tors who consider ESG factors in portfolio selection and management grew by 61% over the past two years, outpacing investment in conventional assets.2 Santiago Exchange identified a series of recommendations grouped into

three information categories: market operations, financial reporting and investor relations. For more information see web site of Santiago Exchange.3 The Sustainability Reporting Guide is an initiative from Santiago Exchange

designed to provide a tool to guide issuers on ESG issues and investors' re-

quirements for sustainable information. For more information see web site of Santiago Exchange4 RobecoSAM: http://www.robecosam.com/

15

The practical guide to ESG integration, of Principles of Respon-

sible Investment of United Nations (PRI)5, states that sell-side

brokers and rating agencies started integrating ESG factors

into research over 15 years ago. Their approach is to integra-

te ESG information with traditional financial information – by

leveraging their financial information systems, their access

to company management, and the expertise of mainstream,

sector-focused investment analysts – to improve research.

Recently, credit rating agencies have also expressed interest in

incorporating ESG aspects into their assessment methodology.

As a result, PRI brought together six credit rating agencies,

including S&P Global Rating, Dagong Global Credit Rating

Group and Moody's Corporation, to sign a statement that su-

pports systematic and transparent integration of ESG aspects

in their credit assessments. With support from The Rockefeller

Foundation, the statement was launched on May 26, 2016, and

initially signed by more than 100 investors (with US$15 billion

in assets under management - AUM). In the document, the

credit rating agencies recognize the need for greater clarity

about how ESG factors are considered in credit analysis and

reaffirm their commitment to more systematic and transpa-

rent consideration of these factors.The field of sustainability

and responsible investment is also home to external assurance

firms that confirm the information published by issuers in their

sustainability report, similar to assurance provided for compa-

nies' financial statements. External assurance of sustainability

disclosures can lend an added degree of trust, credibility and

recognition, just as financial auditing does. Auditing/accoun-

ting firms and sustainability risk rating agencies are the most

common third-party assurance providers.

III.2. Benefits of Responsible InvestmentLocal securities market participants have identified the following

benefits of responsible investment:

III.2.1. Maximizing risk-adjusted ReturnsResponsible investment helps investors to better manage

risk and generate sustainable, long-term returns. It is effi-

cient from a returns and risk perspective since it provides a

better understanding of companies' risks and opportunities

and the activities being invested in. Integrating ESG factors

into decision making enables investors to maximize long-term

risk-adjusted returns by including more information in their

decision-making process. This helps investors adjust for risk

and maximize potential opportunities.

5 Principles for Responsible Investment (2016), A Practical Guide to ESG

Integration for Equity Investing

16

The following section details the possible risks that can be

mitigated with a responsible investment approach:

• Environmental Aspects: The main risks are related to

managing natural resources and preventing pollution or con-

tamination. One key element is the reduction of greenhouse

gas emissions, given that climate change is a global challenge.

• Social Aspects: The social risks and opportunities to be

identified as matters that can impact a business's performance

are centered on the relations and policies that each company

has with its stakeholders: employees, customers, the commu-

nity, suppliers, public authorities, shareholders, among others.

Some possible risks and opportunities may include:

• Employees: The main indicators to address in this area inclu-

de: diversity, occupational health, adherence to labor laws and

optimum working conditions in the supply chain. Opportunities

for effective human resource management are related to im-

proved productivity, reduced turnover and absenteeism, talent

retention and openness to new ideas and business innovation.

• Customers: If the product or service provided by the company

meets quality and safety standards and employees and suppliers

are treated fairly, opportunities are related to brand loyalty, in-

creased sales, reduced risk of litigation and improved reputation.

• Community: A company's relationship with the community

has become a key element of both its operations and its grow-

th. Consideration of indigenous communities' rights, human

rights and practices that are generally responsible towards

neighboring communities are determining factors for obtaining

and maintaining social licenses to operate and protecting a

company's reputation and value.

• Governance Aspects: Corporate governance is managed

internally within organizations and the transparency of the

information is relevant in being accountable to shareholders,

regulators and the general public. A strategy that works acti-

vely to instill business ethics will prevent incidences of bribery

and corruption and will also have an influence on the company

or organization's reputation.

III.2.2. Strengthening the Fiduciary Role of Institutional Investors

Integrating ESG issues into investment processes will allow inves-

tors to make more informed decisions and, therefore, improve

the performance of their portfolio in line with their fiduciary

Worldwide interest in responsible investment has increased

among investors and has also broadened the scope and depth

of studies on the subject.

A growing number of studies make the business case for compa-

nies to fully integrate sustainability into their businessstrategy.

The evidence suggests that strong corporate performance on

ESG factors correlates positively with improved cost of capital

and financial performance6.

The study “Investing for a Sustainable Future” published in

May 2016 by MIT Sloan Management Review7, which surveyed

more than 3,000 executives from nearly 100 countries, found

that 75% of investors cited improved revenue performance

and operational efficiency from companies' sustainability

approaches, thus lending these considerations significant

weight in the investment decision.

By analyzing ESG factors for an investment portfolio, new

opportunities and risks are considered, which provides a new

risk-return perspective for an investment and contributes to

the investment portfolio's returns and diversification.

6 Deutsche Asset & Wealth Management (2015) ESG & Corporate Financial

Performance: Mapping the global landscape.7

MIT Sloan Management Review (2016) Investing for a Sustainable Future. MIT Sloan Management Review.

17

obligations, which will result in allocating capital to companies

with strong corporate governance and a vision of sustainability8.

III.2.3. Contributing to Sustainable Economic Development

Including the risks and opportunities related to ESG issues as

relevant factors in investment decisions gives investors a role

in the country's sustainable development.

The United Nations' “2030 Agenda for Sustainable Develop-

ment”, signed by Chile in 2015, identifies 17 Sustainable Deve-

lopment Goals (SDG)9 to transform our world. In addition to

eliminating global poverty, the SDGs include eradicating hun-

ger and ensuring food safety; guaranteeing good health and

quality education; achieving gender equality; ensuring access

to water and energy; promoting sustained economic growth;

adopting urgent measures against climate change; promoting

peace and facilitating access to justice.

An ESG approach in investors' investment practices helps

build a sustainable economy. By incorporating ESG factors,

investors take on a long-term development perspective and

contribute to the creation of value consistent with the coun-

try's sustainable development.

8 For more information, see Fiduciary Duty in the 21st Century

9 The 17 Sustainable Development Goals (SDGs) of the 2030 Agenda for

Sustainable Development, adopted by world leaders in September 2015 at an historic UN Summit officially came into force on 1 January 2016. Over the

next fifteen years, with these new Goals that universally apply to all, coun-tries will mobilize efforts to end all forms of poverty, fight inequalities and tackle climate change, while ensuring that no one is left behind. For more information, see the 17 Goals.

18

RESPONSIBLE INVESTMENT IN THE WORLD

IV

19

IV.1. Global Context of Responsible Investment

Responsible investment is a growing trend. Between 2012 and

2014, investment portfolios that incorporated ESG factors

increased by over 60%, from US$ 13.3 trillion to US$ 21.4

trillion, and accounted for 30.2 of all professionally managed

investments worldwide10.

The assets used to invest responsibly can vary considerably

from one market to the next. In Canada and Europe, most of

the assets used for this type of investment are concentrated in

variable income instruments (49.5%) and fixed income bonds

(39.5%), followed by other types of assets as shown below:

Equity

Bonds

Real Estate / Property

Alternative / Hedge Funds

Monetary / Deposit

Commodities

0.7%

0.4%

1.1%1.1%

5.0%2.7%

39.5% 49.5%

IV.2. International RI InitiativesWithin the global context of responsible investment, several

organizations promote sustainability and the inclusion of ESG

issues in capital markets, including:

SOURCE: GLOBAL SUSTAINABLE INVESTMENT ALLIANCE, 2015.

2012 2014

49.0% Europe 58.8%

20.2% Canada 31.3%

11.2% United States 17.9%

12.5% Australia 16.6%

0.6% Asia 0.8%

21.5% Global 30.2%

Table 4.1 1: Responsible Investment as a Percentage of Total Managed Investments. Chart 4.1 1: Responsible Investment Asset Allocation in Canada and Europe.

SOURCE: GLOBAL SUSTAINABLE INVESTMENT ALLIANCE, 2015.

Venture Cap / Private Equity Other

10 Global Sustainability Investment Alliance (2015) 2014 Global Sustainable

Investment Review.

20

Sustainable Stock Exchanges (SSE)

The Sustainable Stock Exchanges (SSE11) initiative aims to

explore how stock exchanges, in collaboration with investors,

regulators and companies, can enhance corporate transparency

and ultimately also improve performance on environmental,

social and corporate governance issues. Its main objective is

to promote sustainable economic development and long-term

responsible investment through stock exchanges.

The SSE was created by the United Nations in 2009 and inau-

gurated by UN Secretary-General Ban Ki-Moon, in New York

City. The SSE initiative invites exchanges globally to become a

Partner Exchange by making a voluntary public commitment to

promoting sustainability in their markets. Santiago Exchange

has belonged to this initiative since 2014.

Principles for Responsible Investment (PRI)In order to promote responsible investment around the world,

in 2006 the United Nations published six principles that were

developed by a group of investment professionals reflecting

the increasing relevance of environmental, social and corporate

governance issues to investment practices.

The Principles for Responsible Investment (PRI) seek to provide

a framework for investors and companies. The Principles are

voluntary and aspirational. Those adhering to the principles

commit to incorporate ESG criteria in their investment activities

by doing the following:

• Incorporating ESG issues into investment analysis and deci-

sion-making processes.

• Being active owners and incorporating ESG issues into their

ownership policies and practices.

• Seeking appropriate disclosure on ESG issues by the entities

in which they invest.

• Promoting acceptance and implementation of the Principles

within the investment industry.

70

1400

1600

April 06 April 12April 09 April 15April 07 April 13April 10 April 16April 08 April 14April 11

601200501000

40800

30600

20400

10 200

0 0

US$ TRILLION Nº SIGNATORIES

SOURCE: PRI

Number of Signatories

Total Assets Under Management (AUM)

Figure 4.2 1: Global PRI Signatories and Assets Under Management. Annual Count as of April 2016.

11 Sustainable Stock Exchanges Initiative: http://www.sseinitiative.org/

21

• Working together to enhance their effectiveness in imple-

menting the Principles.

• Reporting on their activities and progress towards imple-

menting the Principles.

PRI provides a Reporting Framework developed in conjunction

with investors that captures investors’ responsible investment

activity ad industry practice. It also offers a collaboration plat-

form that allows investors from around the world to compare

and share their experiences, as well as to engage in actions

involving responsible investment and sustainable development.

Currently, the initiative has more than 1500 signatories, repre-

senting more than USD $60 trillion assets under management,

in 57 countries.

Sustainable Investment Forum (SIF)Sustainable Investment Forums (SIF) are initiatives designed to

promote responsible investment and other forms of financing

that generate sustainable economic development, contribute to

social prosperity and take the environment into consideration.

The global SIF network for the promotion and progress of

responsible and sustainable investment extends to the Uni-

ted States, United Kingdom, Asia, Australia/NZ, the European

Union, Canada, Spain, Italy and Latin America, among others12.

Those invited to belong to the SIFs include financial institutions,

asset managers, suppliers of responsible investment services,

think tanks and non-profit organizations.

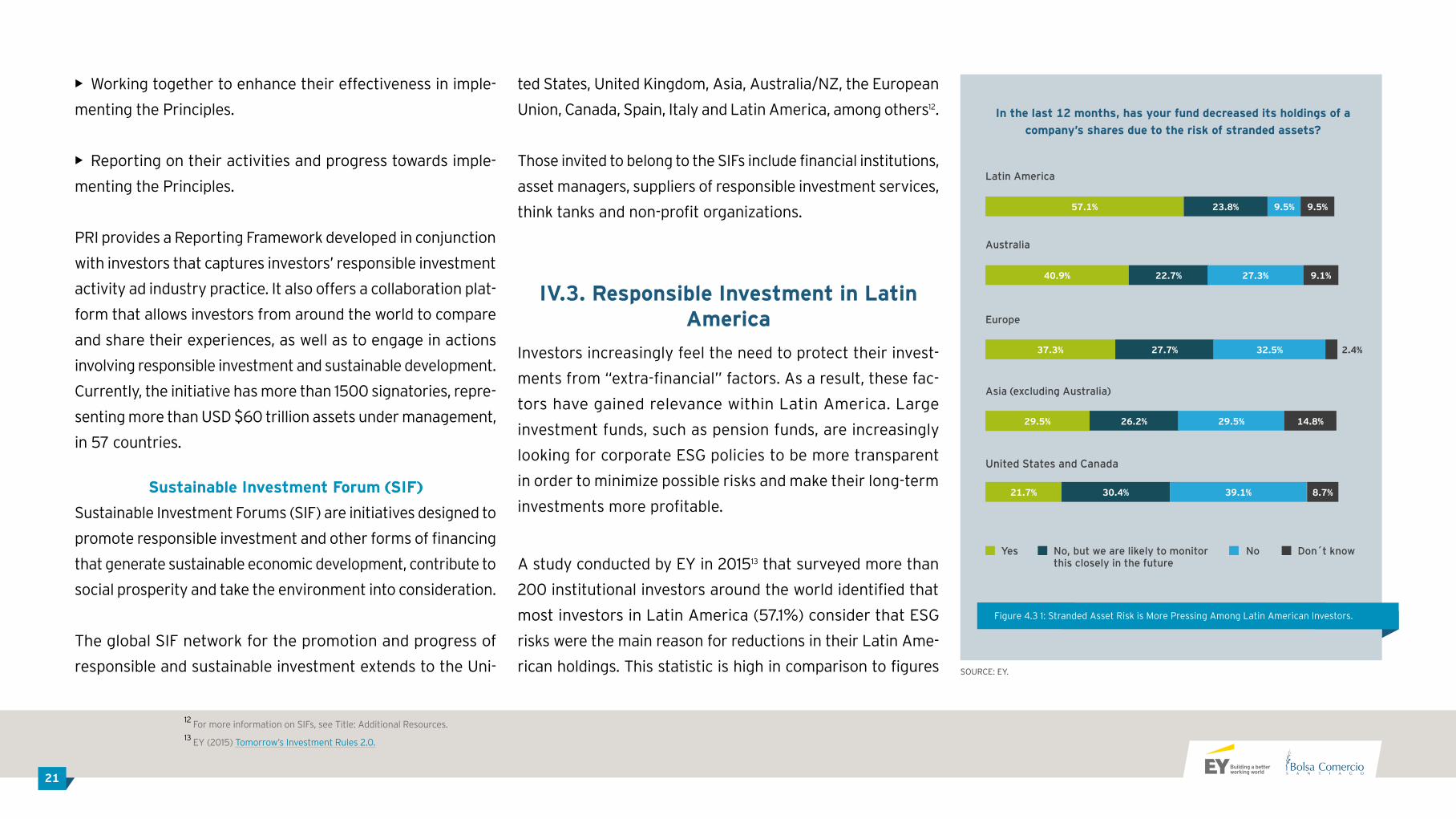

IV.3. Responsible Investment in Latin America

Investors increasingly feel the need to protect their invest-

ments from “extra-financial” factors. As a result, these fac-

tors have gained relevance within Latin America. Large

investment funds, such as pension funds, are increasingly

looking for corporate ESG policies to be more transparent

in order to minimize possible risks and make their long-term

investments more profitable.

A study conducted by EY in 201513 that surveyed more than

200 institutional investors around the world identified that

most investors in Latin America (57.1%) consider that ESG

risks were the main reason for reductions in their Latin Ame-

rican holdings. This statistic is high in comparison to figures

12 For more information on SIFs, see Title: Additional Resources.

13 EY (2015) Tomorrow’s Investment Rules 2.0.

In the last 12 months, has your fund decreased its holdings of a company’s shares due to the risk of stranded assets?

Australia

40.9% 22.7% 27.3% 9.1%

Europe

37.3% 27.7% 32.5% 2.4%

Asia (excluding Australia)

29.5% 26.2% 29.5% 14.8%

United States and Canada

21.7% 30.4% 39.1% 8.7%

Latin America

57.1% 23.8% 9.5% 9.5%

SOURCE: EY.

Yes No Don´t knowNo, but we are likely to monitor this closely in the future

Figure 4.3 1: Stranded Asset Risk is More Pressing Among Latin American Investors.

22

and financial sector players committed to financing sustaina-

ble development; it also offers its participants skill building

opportunities and tools to manage risks and opportunities that

take into consideration environmental, social and corporate

governance factors.

Responsible Investment Program (PIR)PIR emerges in Peru as part of the 20th International Climate

Change Conference (COP20). The initiative is promoted by the

private financial sector and spearheaded by SURA, the Lima Stock

Exchange (BVL) and the development bank of Peru (COFIDE)

with technical support from A2G14.

PIR provides a space for technical assistance and coordination

for its members to develop and implement instruments such as

responsible investment policies, strategies, plans and portfolios.

Its mission is to promote responsible investment practices in the

financial system in Peru as well as several other countries in the

region, through strategic partnerships, and to disseminate the

Principles of Responsible Investment.

Investment Products Developed by Exchanges in the RegionCurrently, there are several investment products that foster

responsible investment and corporate sustainability develo-

ped by exchanges in the Latin American market in keeping

with the role they play in capital markets.

Exchanges that have begun to introduce this type of products

include Santiago Exchange, the Colombian Stock Exchange,

the Lima Stock Exchange, the Mexican Stock Exchange and

the Brazilian Stock Exchange (BM&FBovespa), considered a

regional trailblazer.

Exchanges in the region have developed the following responsible

investment initiatives:

• Carbon bond trading platforms: MEXICO2, an initiative of

the Mexican Stock Exchange, responds to Mexico's needs

to address the effects of climate change.

• Sustainable/ESG indexes: The creation of sustainability

indexes certainly demonstrates the efforts put forth by ex-

changes in the region to promote the incorporation of ESG

factors by issuers. Latin America currently boasts an extensive

offering of sustainable indexes with four exchanges offering

ESG Indicies. Examples include the Dow Jones Sustainability

14 A2G: http://www.atwog.com/

reported in Europe, Asia or the United States. The importance

of including ESG factors in investment practices and decisions

has increased and, at present, they are more highly valued and

monitored by investors in the region.

IV.4. Latin American RI InitiativesProgress has been made in responsible investment initiati-

ves in Latin America through working platforms involving

investors and issuers, such as LatinSIF, and investment

products and services developed by exchanges related to

responsible investment.

LatinSIFIn 2015, the main organizations promoting responsible invest-

ment in Latin America signed an agreement to work together

through LatinSIF, part of the global network of Sustainable

Investment Forums (SIF), whose objective is to develop a colla-

boration network and generate knowledge for the implemen-

tation of responsible investment criteria and methodologies

in Latin America.

LatinSIF is a forum for debate and a work space for companies

23

Chile Index from Santiago Exchange; the Sustainable CPI In-

dex from the Mexican Stock Exchange, launched in December

2011; the Good Corporate Governance Index from the Lima

Stock Exchange, created in 2002 and the family of sustai-

nable indexes from BM&FBovespa, including the Corporate

Sustainability Index (ISE) launched in 2005, the Carbon Index

(ICO2), the family of Corporate Governance Indexes and the

Tag Along Stock Index (ITAG).

• High-impact investment funds: INVERSOR, a private capi-

tal fund founded by the Colombian Stock Exchange in 2009,

supports and strengthens companies that work to transform

the country's social and environmental problems through their

business models. Another example is BVSA, the Social Envi-

ronmental Stock Exchange, an initiative from BM&FBovespa.

Its mission is to mobilize donors to support carefully selected

environmental projects in order to build a more just and ega-

litarian society in Brazil

IV.5. Responsible Investment in ChileIn Chile, there are regulations, financial products and initia-

tives that foster and promote responsible investment and

sustainable development in the securities market as well

as among its participants.

An increasing number of issuers are publishing sustainability

reports. Currently, in the Chilean market close to 44% of the

securities market's most representative issuers15 disclose

ESG information or prepare an annual sustainability report,

based on Santiago Exchange data.

This new trend in management and responsible invest-

ment has stimulated the development of new standards

by regulators and new corporate assessment tools by

Santiago Exchange.

IV.5.1. Dow Jones Sustainability Chile Index (DJSI Chile)Santiago Exchange, in its role as promoter of good practices,

and in order to provide more information to investors on local

capital market issuers, decided to create the Chilean securities

market's first sustainability index. The motivations behind

this development are to strengthen financial and economic

development that is sustainable over time, to highlight the

companies that work to incorporate ESG issues into their

businesses, to foster profitability with respect for the envi-

ronment and the community and to recognize companies that

15 This 44% represents 25 of the 57 issuers on the IGPA as of year-end 2015

with a free-float adjusted market capitalization of more than USD100 million.

24

have robust and transparent corporate governance systems.

The Dow Jones Sustainability Chile Index (DJSI Chile), deve-

loped by Santiago Exchange in collaboration with S&P Dow

Jones Indices and RobecoSAM as an independent, external

assessor, presented its first results in 2015. This index is an

important tool for the decision-making process of investors

that consider ESG issues when making an investment.

The DJSI Chile—the first local sustainability index—offers a

standard global metric on ESG issues for Chilean companies.

The methodology for this index is described below:

• Eligibility criteria: In the index's first year, the 40 companies

on the IPSA were assessed . In 2016, the assessment16 was broade-

ned to include companies on the IGPA17 with a free-float adjusted

market capitalization of more than USD100 million as of year-end

2015. The assessment is expected to expand to more issuers in

the future. There are currently 21 companies on the index.

• Independent assessment: RobecoSAM, a Swiss company

that specializes in sustainability, was in charge of rating the

ESG performance of the companies invited to participate in the

DJSI Chile. The assessment was conducted using a voluntary,

sector-specific questionnaire given to issuers. The assessment

also considers public information such as financial statements,

press, corporate websites, sustainability reports and informa-

tion given to supervisors.

• Analysis process: The analysis included 24 sectors from the

Global Industry Classification Standard (GICS), with 59 groups of

issuers. It analyzed both generic dimensions and other factors

unique to the particular industry. The industry-specific elements

were the results of the questionnaire weighted differently based

on the sector or industry. For example, the banking sector was

evaluated on its asset laundering prevention policies, some-

thing that is less relevant for an energy company. Thus, at the

end of the evaluation the “Total Sustainability Score” (TSS) is

obtained. This is used to select the companies eligible for the

Index based on a minimum sustainability standard assigned

per industry sector by RobecoSAM. Based on the TSS obtained

by the companies, the best 40% per industry is selected using

the “Best-In-Class” methodology. The weight of each company

on the Index is determined by its free-float adjusted market

capitalization. No company may have a weight greater than

15% on the DJSI Chile.

IV.5.2. New Regulatory Developments

Governments around the world are responding to demands

for ESG information by taking action to drive corporate sustai-

nability disclosures. Authorities recognize the importance of

strengthening market mechanisms that will help the country

achieve its objectives related to sustainable development18.

As a result, a number of capital market regulators have

introduced regulatory requirements governing corporate

disclosure of ESG information. In examining instruments in

place in the world’s 50 largest economies per GDP according

the World Bank, as of November 2016, there were19.

• Over 100 regulations mandating the disclosure of environ-

mental, social or governance information

• Over 200 measures mandating or encouraging sustaina-

bility-related disclosure instruments (a threefold increase

since 2006).

• Nearly 300 instruments overall, spanning corporate disclo-

sure, investor stewardship codes and pension fund regulation

regarding sustainability factors.

16 Selective Stock Price Index: http://www.bolsadesantiago.com/mercado/

Paginas/indicesbursatiles.aspx17

General Stock Price Index http://www.bolsadesantiago.com/mercado/Paginas/indicesbursatiles.aspx

18 In September 2015, Chile committed to the Sustainable Development Goals

(SDG), as part of the 2030 Agenda for Sustainable Development approved by the Chiefs of State of the 193 United Nations member countries, which includes 17 goals and 169 targets.

19 For more information see PRI responsible Investment regulation

25

Establishing protocols for identifying, measuring and disclo-

sing ESG factors can help companies stay ahead of such new

regulatory developments.

The Chilean Superintendency of Securities and Insurance

(SVS) has not fallen behind on promoting sustainability and

the disclosure of ESG issues by issuers to investors. In June

2015, it issued two new standards (General Rules No. 385

and No. 386) that aim to improve the disclosures made by

issuers on matters of corporate governance, corporate social

responsibility and sustainable development, among others.

Although adoption of these practices is not mandatory for

issuers, the objective is to enhance corporate transparency

so that investors make investment decisions that favor com-

panies in which their interests are better protected.

The main objectives of Rule No. 385 are to:

• Foster the adoption of corporate social responsibility and

sustainable development policies, referring particularly to

the diversity of the company's board and senior executives.

• Encourage the disclosure of information to shareholders

and the general public regarding corporate social respon-

sibility and sustainable development policies and practices

and their effectiveness.

• Improve the quality and credibility of the information

contained in the board self-assessment through an external,

third-party evaluation.

• Promote the adoption of national and international princi-

ples, directives and recommendations such as, for example,

those developed by The Committee of Sponsoring Orga-

nizations (COSO) or those contained in Control Objectives

for lnformation and Related Technology (COBIT) created by

ISACA or ISO 31000:2009 and ISO 31004:2013.

• Specify measures for addressing conflicts of interest and

procedures for updating the Board Code of Conduct.

Therefore, the new Rule No. 386 calls for incorporating the

following information regarding corporate social respon-

sibility and sustainable development into the company's

annual report:

26

• Board diversity (gender, nationality, age and years in office).

• Diversity of chief executive officer and other divisions that

report to the CEO or board of directors.

• Organizational diversity (gender, nationality, age and years

of service).

• Salary gap by gender.

This chapter is designed to provide tools for developing

an investment strategy that incorporates ESG factors. It

also proposes seven basic steps that an investor can follow

starting from the decision to integrate it into its decision

making to the disclosure of the strategy used. Lastly, this

section identifies a series of information sources on the

ESG performance of issuers that can be accessed by inves-

tors that wish to incorporate these factors into their local

investment analysis.

27

DECISION MAKING IN RESPONSIBLE INVESTMENT

V

28

V.1. Responsible Investment Strategies As mentioned, selecting and managing assets with a respon-

sible investment approach is based on a combined analysis

of financial information and ESG variables. There are several

strategies that investors can use to incorporate ESG consi-

derations into investment asset management. In 2013, the

Global Sustainable Investment Alliance (GSIA)20 published

the following responsible investment strategies, which have

set the global standard in such matters.

V.1.1. Sustainability-themed InvestingInvestment in investment projects or assets specifically re-

lated to sustainability or the environment. Investor motiva-

tion may vary, but they tend to support industries that work

towards sustainable production and resource consumption.

In this investment approach, one can find non-conventional

renewable energies, projects that treat waste, green tech-

nologies that reduce pollution, energy or water efficiency

projects, among others (i.e. investment projects that have a

positive impact on the environment).

V.1.2. Positive/Best-in-Class Screening Investment in sectors, companies or projects selected for

positive ESG performance relative to industry peers.

V.1.3. Negative/Exclusionary Screening

The exclusion of companies or industries as investment options

based on environmental, social or ethical considerations. The

rationale for and ways of creating and applying filters vary

from ethical reasons to reasons related to risk management.

V.1.4. Norms-based Screening Screening of investments against minimum standards of bu-

siness practice based on international norms. This standard

can be based on international norms issued by one or several

organizations and institutions. A decision is made to either

exclude or incorporate assets from or into the investment

portfolio depending on whether or not companies comply

with the standards.

V.1.5. Integration of ESG Factors This method explicitly includes elements of ESG risks and

opportunities within financial analysis and investment de-

cision making, using processes and information sources

developed internally or by third parties such as risk rating

agencies and portfolios of sustainability indexes, in order to

identify companies' ESG performance.

V.1.6. Impact/Community Investing

Targeted investments, typically made in private markets, aimed

at solving social or environmental problems and generating

long-term returns for the investor. Impact investments include

community investments, where capital is specifically directed

to traditionally underserved individuals or communities, as

well as financing that is provided to businesses with a clear

social or environmental purpose. Impact investment brings

together all financial transactions carried out by investment

funds that invest large sums in profitable projects with posi-

tive social or environmental impacts (i.e. social enterprises)21.

V.1.7. Corporate Engagement and Shareholder Action This strategy uses shareholder power to influence corporate

behavior, including through direct corporate engagement

(i.e. communicating with senior management and/or boards

of companies), filing or co-filing shareholder proposals, and

proxy voting that is guided by comprehensive ESG guidelines.

20 Global Sustainable Investment Alliance: http://www.gsi-alliance.org/

21 Latin American Impact Investing Forum: http://www.inversiondeimpacto.org/

29

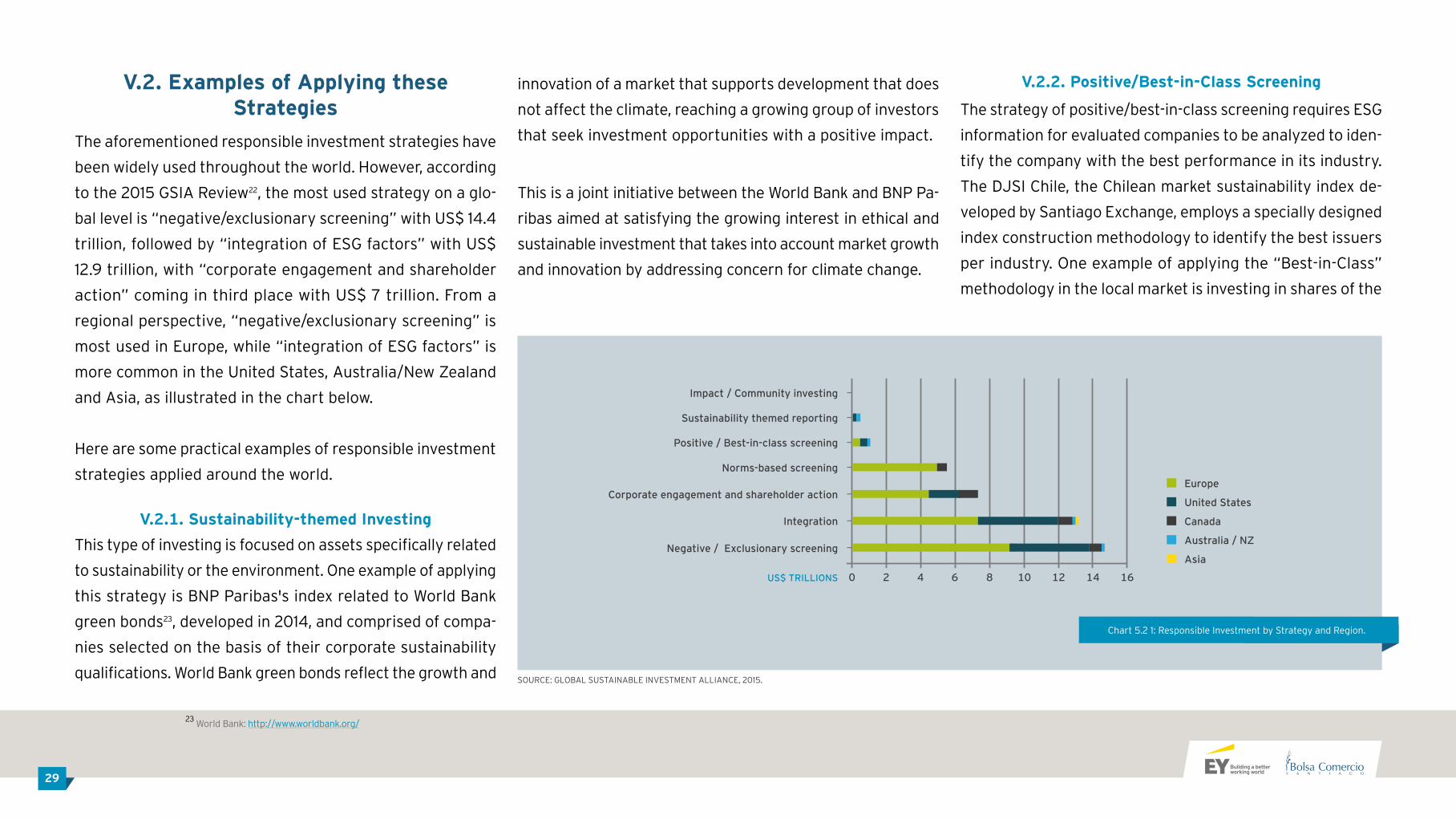

V.2. Examples of Applying these Strategies

The aforementioned responsible investment strategies have

been widely used throughout the world. However, according

to the 2015 GSIA Review22, the most used strategy on a glo-

bal level is “negative/exclusionary screening” with US$ 14.4

trillion, followed by “integration of ESG factors” with US$

12.9 trillion, with “corporate engagement and shareholder

action” coming in third place with US$ 7 trillion. From a

regional perspective, “negative/exclusionary screening” is

most used in Europe, while “integration of ESG factors” is

more common in the United States, Australia/New Zealand

and Asia, as illustrated in the chart below.

Here are some practical examples of responsible investment

strategies applied around the world.

V.2.1. Sustainability-themed InvestingThis type of investing is focused on assets specifically related

to sustainability or the environment. One example of applying

this strategy is BNP Paribas's index related to World Bank

green bonds23, developed in 2014, and comprised of compa-

nies selected on the basis of their corporate sustainability

qualifications. World Bank green bonds reflect the growth and

innovation of a market that supports development that does

not affect the climate, reaching a growing group of investors

that seek investment opportunities with a positive impact.

This is a joint initiative between the World Bank and BNP Pa-

ribas aimed at satisfying the growing interest in ethical and

sustainable investment that takes into account market growth

and innovation by addressing concern for climate change.

V.2.2. Positive/Best-in-Class Screening

The strategy of positive/best-in-class screening requires ESG

information for evaluated companies to be analyzed to iden-

tify the company with the best performance in its industry.

The DJSI Chile, the Chilean market sustainability index de-

veloped by Santiago Exchange, employs a specially designed

index construction methodology to identify the best issuers

per industry. One example of applying the “Best-in-Class”

methodology in the local market is investing in shares of the

Impact / Community investing

0 2 4 6 8 10 12 14 16

Sustainability themed reporting

Positive / Best-in-class screening

Norms-based screening

Corporate engagement and shareholder action

Integration

Negative / Exclusionary screening

Europe

United States

Canada

Australia / NZ

Asia

US$ TRILLIONS

SOURCE: GLOBAL SUSTAINABLE INVESTMENT ALLIANCE, 2015.

Chart 5.2 1: Responsible Investment by Strategy and Region.

23 World Bank: http://www.worldbank.org/

30

companies that comprise the DJSI Chile basket, which were

selected for the index because of their outstanding perfor-

mance in sustainability as compared to their peers. In other

words, they are the best in their class.

Another example of responsible investment using the positi-

ve screening strategy is that employed by the international

asset management company, Amundi24. It has a research

team dedicated to ESG analysis of companies using a “Best-

in-Class” approach based on its patented ESG rating system

to evaluate ESG performance by industry. This rating system

is fed with ESG data supplied by third-party research sources,

combined with internal analysis prepared by the company.

V.2.3. Negative / Exclusionary Screening Exclusion of a sector or companies from an investment por-

tfolio for a variety of reasons that lead to bad management

of ESG issues. One example occurred with the international

investment company Barclays25, which announced in mid-

2015 that it would no longer finance coal mining projects

due to the negative environmental and social impacts of the

extraction method used by the industry. This decision was

made despite the fact that Barclays was one of the financial

backers of this mining method in the United States in 2013.

V.2.4. Norms-based Screening

This responsible investment method contrasts each com-

pany with an international standard or norm, analyzing their

compliance level and making this the decisive variable when

deciding whether to invest. One example of this type of in-

vestment can be seen in a study by Novethic in 201326, which

analyzed the influence that investors can have when they

refuse to invest in multinational companies that violate la-

bor rights, show disregard for freedom of speech and/or are

complicit in human rights abuses.

The study shows that "norms-based exclusion" leads investors

to question business models, excluding companies involved

in human rights violations from its investment decisions.

The perception of investors is that in the long term it is too

costly to invest in controversial companies and in order to

protect their reputation and make responsible investments,

shareholders are saying "no" to these companies.

V.2.5. Integration of ESG FactorsOne example of the “integration of ESG factors” in traditional

investment assessment is used by RBC Global Asset Manage-

ment, the asset management division of Royal Bank of Canada,

24 Amundi: https://www.amundi.com/int?nr=1

25 Barclays: https://www.home.barclays/

26 Novethic (2013) Controversial companies: Do investor blacklists make a

difference?

31

which identifies and integrates ESG factors into the funda-

mental analysis of stocks using multiple information sources.

The process begins with a fundamental analysis to identify

any positive or negative ESG factors. This assessment is then

embedded into an analysis of the competitive position and

the sustainability of the business, which we then put into

our valuation models. RBC invests only in companies that

perform strongly in four areas: business model; market share

opportunity; end-market growth; and management & ESG.

RBC's analysis and assessment process is detailed in the prac-

tical guide to ESG integration for equity investing prepared

by PRI. This guide contains information and case studies on

the integration of ESG aspects into traditional investment

tools and techniques, including fundamental, quantitative,

beta and passive investment analysis.

V.2.6. Impact InvestmentImpact investment, in addition to seeking long-term returns

for investors, looks to solve social and environmental pro-

blems. This strategy was employed by Danone and Mars27,

two multinational food companies, that created an innovative

investment fund (Livelihoods 3F) in 2015 to help small-scale

farmers and, therefore, boost their companies' productivity.

An investment of 120 million euros over the next 10 years

to implement projects in Africa, Asia and Latin America is

expected to help over 200,000 small-scale farmers and 2

million people to increase the sustainability of their crops.

Livelihoods 3F (The Livelihoods Fund for Family Farming)

will set in motion projects to restore the environment and

deteriorated ecosystems in order to improve the productivity,

income and living conditions of small-scale rural farmers.

V.2.7. Corporate Engagement / Shareholder ActionThis strategy uses shareholder power to influence corporate

behavior, acting through decisions made by boards. One

example of this occurred in November 2014 with the oil com-

pany Exxon Mobil28, where shareholders asked the company

to protect their shares from the climate risks forecasted by

the International Energy Agency (IEA)29.

Shareholders, through a proposal, asked Exxon Mobil to

protect the investors' value by increasing the amount au-

thorized for capital distributions (dividends or share buy-

backs) to shareholders instead of investing in costly projects

with a high carbon content. This proposal reflects investors'

growing concern regarding the impact of ESG factors in the

companies where they invest and how they exercise power

to change their practices.

V.3. Steps to Follow to Invest ResponsiblyIn order to promote and encourage investors in the local

market to join the responsible investment trend and play an

active role in society's sustainability objectives, seven steps

are listed below for investors or asset managers to follow to

invest responsibly and sustainably.

The following steps are intended to assist investors with the

financial opportunity to integrate a responsible investment

focus into their portfolios, maintaining balance in their ma-

nagement processes and contractual relations with their own

investment managers30.

• Know the Investment EnvironmentIt is important to research RI trends and be familiar with the

27 Danone: http://www.danone.com/

Mars: http://www.mars.com/global28

Exxon Mobil: http://corporate.exxonmobil.com/

29 International Energy Agency: https://www.iea.org/

30 Principles for Responsible Investment (2016) How asset owners can drive

responsible Investment. Bolsa de Valores de Colombia (2014) Inversión Responsable y Sostenible

32

approaches and practices being used by other industry pla-

yers. This step can also include reviewing relevant laws for

ESG factors. Important networks or collaborative initiatives

such as PRI are other good sources to research. In this stage,

it is also important to be familiar with RI/ESG terminology

and regional and international ESG norms.

• Establish Considerations and ObjectivesAfter exploring the RI scene, investors should develop a

perspective on RI. This process involves establishing con-

siderations and assumptions about the materiality of ESG

factors and how relevant they are to different investment

strategies, different types of assets and, more generally

speaking, to the organization's goals. These goals can vary

between the different types of investment assets and can

depend on the investor's role in the industry (asset ma-

nagers versus asset owners). In addition to determining

considerations, investors must define objectives, which

are usually based on financial measures, such as liquidity

requirements and risk-return ratios. Asset owners must

also decide which risks to manage and identify the market

conditions in which there may be losses.

• Build Consensus and Guarantee Board Approval In order for an RI strategy to be successful, it is important for

there to be a common understanding of and organization-wide

support for the broad RI goals. This requires ongoing com-

munication, consultation and collaboration among an orga-

nization's key decision makers and stakeholders regarding

its plans and RI strategy during the process of establishing

and implementing an RI strategy.

• Create an RI PolicyA responsible investment policy is a key document that provi-

des a foundation for an investor's RI activities and approach.

It establishes the principles and strategies that an investor

has chosen to achieve their investment objectives. A respon-

sible investment policy seeks to complement and support an

investor's declaration on investment policies and procedures

and must be referenced in this declaration31.

• Establish an Internal Governance StructureThe successful implementation of an RI strategy32 is facilitated

by a responsible investment governance structure with clear-

ly defined roles, responsibilities and lines of communication.

This guarantees clarity and responsibility with respect to im-

plementation and responsible investment goals, and provides

mechanisms for dealing with challenges as they arise. Many

investors have designated managerial roles, analysts specia-

lizing in ESG, and committees that supervise and participate

in making critical or important decisions that must be made.

• Develop CapacitiesOnce the responsible investment policy has been released and

governance structures have been established, it is important

to develop internal capacities within the organization to im-

plement RI. This can involve, for example, developing internal

learning modules for employees or having ESG analysts work

directly with key teams within the organization, from port-

folio management teams to communications and marketing

teams, to foster awareness and understanding.

• CollaborationThe advancement of RI depends on constructive, peer-to-

peer collaboration in order to share knowledge and resources

and participate in collective actions to help solve complex

problems. The PRI, for example, fosters and facilitates such

collaboration through its collaboration platform for the de-

velopment of responsible investment initiatives.

31 Principles for Responsible Investment (2016) Investment Policy: Process

& Practice – A Guide for Asset Owners32

Responsible Investment (2016) Crafting an investment strategy – A process guidance for asset owners

33

V.4. Access to Corporate ESG Information

Once the responsible investment strategy is clear and the

organization has decided how ESG criteria will be incorpo-

rated into the investment decision, it is important to be able

to identify and access information on environmental, social

and corporate governance performance on companies where

investors are considering investing.

Information on ESG performance can be provided by com-

panies themselves, through their sustainability reports or

integrated reports, or by third-party organizations. Some

other tools that provide information include sustainability

indexes developed by exchanges, which are supplemented

by information prepared by ESG risk rating agencies through

rankings and evaluations of companies within a given mar-

ket, together with information developed and published by

regulators, which can be in the form of questionnaires or

specific regulatory assessments.

The resources or tools offered by the capital market to assess

corporate ESG performance include:

V.4.1. Corporate Reports

When thinking about where to invest, it is important to be

able to identify the quality of reporting and how ESG factors

are involved in the company's management and operations.

A good report can help build an understanding of the perfor-

mance risks and opportunities that will affect the investor

in the short and long term. Similarly, it can help increase

transparency, responsibility and effective communication

between the issuer and the investor.

Information must reflect the organization's relevant econo-

mic, environmental and social performance and substantially

influence the assessments and decisions of stakeholders.

There are several resources that focus on reporting ESG in-

formation and on performance in ESG dimensions, including:

• UN Global Compact’s best practices related to the GC Ad-

vanced Communication on Progress in the areas of human

rights, labor, environment and anti-corruption.

• Indicators from the Carbon Disclosure Project (CDP) regar-

ding climate change, water consumption and deforestation.

• Climate Disclosure Standards Board’s (CDSB) Framework

for reporting environmental information and natural capital

in mainstream financial reports.

• GRI Sustainability Reporting Guidelines, with over 140 in-

dicators that address ESG issues across all sectors, defined

by their relevance to stakeholders.

• The International Integrated Reporting Framework (IIRC).

• The Sustainability Accounting Standards Board’s (SASB)

standards identify relevant factors by industry sector that

are comparable with each other.

To learn more about the companies that promote these stan-

dards, please see Title: Additional Resources for this Guide.

Reports prepared by companies, regardless of the format and

standard used, are public and can be found and downloaded

directly from each company's website.

34

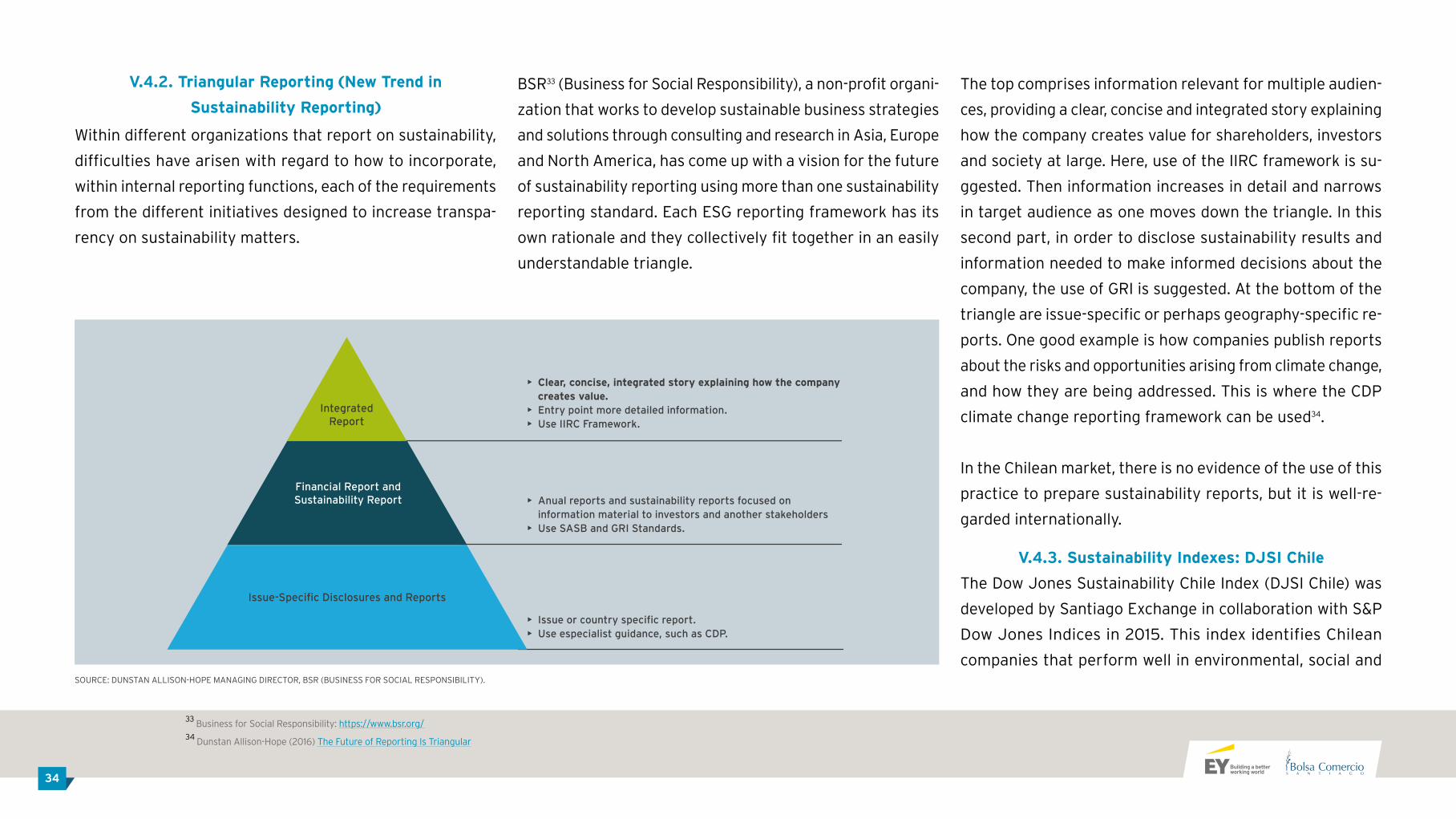

V.4.2. Triangular Reporting (New Trend in Sustainability Reporting)

Within different organizations that report on sustainability,

difficulties have arisen with regard to how to incorporate,

within internal reporting functions, each of the requirements

from the different initiatives designed to increase transpa-

rency on sustainability matters.

BSR33 (Business for Social Responsibility), a non-profit organi-

zation that works to develop sustainable business strategies

and solutions through consulting and research in Asia, Europe

and North America, has come up with a vision for the future

of sustainability reporting using more than one sustainability

reporting standard. Each ESG reporting framework has its

own rationale and they collectively fit together in an easily

understandable triangle.

The top comprises information relevant for multiple audien-

ces, providing a clear, concise and integrated story explaining

how the company creates value for shareholders, investors

and society at large. Here, use of the IIRC framework is su-

ggested. Then information increases in detail and narrows

in target audience as one moves down the triangle. In this

second part, in order to disclose sustainability results and

information needed to make informed decisions about the

company, the use of GRI is suggested. At the bottom of the

triangle are issue-specific or perhaps geography-specific re-

ports. One good example is how companies publish reports

about the risks and opportunities arising from climate change,

and how they are being addressed. This is where the CDP

climate change reporting framework can be used34.

In the Chilean market, there is no evidence of the use of this

practice to prepare sustainability reports, but it is well-re-

garded internationally.

V.4.3. Sustainability Indexes: DJSI ChileThe Dow Jones Sustainability Chile Index (DJSI Chile) was

developed by Santiago Exchange in collaboration with S&P

Dow Jones Indices in 2015. This index identifies Chilean

companies that perform well in environmental, social and

33 Business for Social Responsibility: https://www.bsr.org/

34 Dunstan Allison-Hope (2016) The Future of Reporting Is Triangular

SOURCE: DUNSTAN ALLISON-HOPE MANAGING DIRECTOR, BSR (BUSINESS FOR SOCIAL RESPONSIBILITY).

IntegratedReport

• Clear, concise, integrated story explaining how the company creates value.• Entry point more detailed information.• Use IIRC Framework.

• Anual reports and sustainability reports focused on information material to investors and another stakeholders• Use SASB and GRI Standards.

• Issue or country specific report.• Use especialist guidance, such as CDP.

Financial Report and Sustainability Report

Issue-Specific Disclosures and Reports

35

governance issues in comparison to their industry peers

(Best-in-Class methodology). It also provides financial incen-

tive for incorporating sustainable and socially responsible

processes at companies that take part in the market and

creates an environment of responsible investment consistent

with society's demands.

For more information on the performance of the DJSI Chile

and the companies on the index, visit Santiago Exchange's

website35.

V.4.4. ESG Ranking and AssessmentThere are institutions specialized in assessing issuer perfor-

mance in sustainability aspects. They generate information

on corporate performance in these areas to develop sus-

tainable indexes or rankings, among other measurement

initiatives. These initiatives have been promoted mainly by

investors that need ESG information in addition to financial

information for investment decision making.

One example is RobecoSAM and its annual assessment process,

the Corporate Sustainability Assessment (CSA), performed glo-

bally on over 3,000 companies. The assessment process is based

on an industry-specific questionnaire and publicly disclosed

information. The results of the evaluation are used to update

the companies included in the Dow Jones sustainability indexes.

Information in aggregate is published on its website and those

of other securities market data suppliers. For more information

on RobecoSAM's assessment process, visit its website36.

Another organization providing ESG performance informa-

tion is ALAS20, which recognizes companies, investors and

professionals each year that stand out for their leadership

in ESG issues. For more information, see its website37.

Regarding the quality of information that companies on

Santiago Exchange's IPSA index make available to their sha-

reholders and stakeholders, Informe Reporta38 analyzes the

set of financial and ESG disclosures that companies make

available to their shareholders and stakeholders on the day

of their annual general meetings, placing special emphasis

on voluntary information provided by companies.

V.4.5. National Environmental Oversight Information System (SNIFA)

The Superintendency of the Environment (SMA in Spanish) is

a decentralized, public entity with authority to oversee and

enforce environmental matters. It is exclusively responsible

for executing, organizing and coordinating the monitoring and

oversight of Environmental Qualification Resolutions, mea-

sures in Prevention and/or Environmental Decontamination

Plans, the content of Environmental Quality and Emissions

Standards, and Management Plans, when appropriate, as well

as all other environmental instruments established by law.

In addition, the SMA must work to ensure that environmen-

tal information is available and easy to access. This is done

through the National Environmental Oversight Information

System (SNIFA in Spanish). This publicly-accessible website

provides information on the SMA's oversight and enforcement

processes, organized geographically, together with rulings,

judgments and resolutions from authorities on environmental

matters. It also includes access to public records of environ-

mental instruments and enforcement actions.

With this platform, the SMA provides relevant, public and im-

partial information regarding the environmental performance

of companies to be considered by investors in their invest-

ment processes. The data can be reviewed on the website39.

35 Santiago Exchange: http://www.bolsadesantiago.com/Paginas/Home.aspx

36 RobecoSAM: http://www.robecosam.com/en/sustainability-insights/

about-sustainability/corporate-sustainability-assessment/review.jsp

37 Alas 20: http://web.alas20.com/

38 Informe Reporta: http://informereporta.com/cl

39

SNIFA: http://snifa.sma.gob.cl/v2/

36

V.4.6. NCG 385 Questionnaires

The Superintendency of Securities and Insurance (SVS), the

autonomous public institution charged with overseeing the

activities and participants of the Chilean securities and insu-

rance markets, issued General Character Standard (NCG in

Spanish) 385 in 2015. This standard aims to improve disclo-

sures by local publicly listed companies on corporate gover-

nance matters and incorporates the disclosure of practices

related to social responsibility and sustainable development.

Although adopting such practices is not mandatory, an entity

must report whether or not it has implemented them and how.

This standard requires publicly listed companies to complete

a form stating whether they have implemented 97 corpora-

te governance best practices grouped into four categories:

board functioning and operations; relations between the

company, shareholders and the general public; risk mana-

gement and control; and a third-party assessment of board

compliance with the practices. 23 of these best practices

are related to performance in ESG dimensions.

The SVS aims to create incentives for investors to make

investment decisions that favor companies in which their

interests are better protected. The year 2016 was the first