santos - paragonfg.com.au · macquarie research santos 23 october 2015 2 value on offer sto advised...

TRANSCRIPT

Please refer to page 9 for important disclosures and analyst certification, or on our website

www.macquarie.com/research/disclosures.

AUSTRALIA

STO AU Outperform

Price (at 05:44, 22 Oct 2015 GMT) A$6.32

Valuation A$ 11.96 - DCF (WACC 9.0%, beta 1.3, ERP 5.0%, RFR 3.8%)

12-month target A$ 7.50

12-month TSR % +23.6

Volatility Index High

GICS sector Energy

Market cap A$m 6,560

30-day avg turnover A$m 54.1

Number shares on issue m 1,038

Investment fundamentals Year end 31 Dec 2014A 2015E 2016E 2017E

Revenue m 4,037.0 3,314.5 4,245.3 4,904.0 EBIT m 845.0 537.0 1,216.5 1,694.8 Reported profit m -935.0 127.0 485.9 883.8 Adjusted profit m 533.0 122.0 485.9 883.8 Gross cashflow m 1,777.0 1,429.2 1,846.5 2,344.3 CFPS ¢ 182.3 143.8 174.9 207.8

CFPS growth % 11.9 -21.1 21.6 18.8 PGCFPS x 3.5 4.4 3.6 3.0 PGCFPS rel x 0.42 0.49 0.42 0.39 EPS adj ¢ 54.7 12.2 45.8 78.3 EPS adj growth % 5.4 -77.6 275.0 70.8 PER adj x 11.6 51.7 13.8 8.1 PER rel x 0.78 3.32 0.92 0.60

Total DPS ¢ 35.0 30.0 31.5 34.7 Total div yield % 5.5 4.7 5.0 5.5 Franking % 100 100 100 100 ROA % 3.9 2.3 5.1 7.2 ROE % 5.4 1.4 5.6 9.2 EV/EBITDA x 7.1 8.2 6.1 5.0

Net debt/equity % 79.4 123.8 112.8 70.2 P/BV x 0.7 0.8 0.8 0.7

STO AU vs ASX 100, & rec history

Note: Recommendation timeline - if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, October 2015

(all figures in AUD unless noted)

Analyst(s) Kirit Hira +61 2 8232 9692 [email protected]

23 October 2015 Macquarie Securities (Australia) Limited

Santos Value on offer Event

STO advised that it has rejected an indicative, highly conditional and non-

binding proposal from Scepter Partners to acquire the company for a cash

consideration of A$6.88/sh (representing a 26% premium to last close and a

more material 29% premium to 1 month VWAP).

Impact

A fairly opportunistic offer: At A$6.88/sh, we estimate this implies an oil

price discounted by core and risked NAV of ~U$59/bbl and U$54/bbl, which

compares to longer-term futures curve at U$64/bbl and our LT normalised

assumption of U$80/bbl. Indeed STO also suggested that it did not reflect the

"fair value of the asset base", let alone a premium for control. While offers for

OSH would likely attract a premium vs. STO (given the differing quality of

assets, growth prospects, balance sheet position, etc), a comparison of

Scepter’s offer vs. WPL initial offer for OSH perhaps highlights the

opportunistic nature of the Scepter proposal. Indeed we estimate that the

pricing terms imply a 15-50% discount to WPL’s offer for OSH (based on 1

month VWAP prior to the disturbed price) based on various valuation metrics.

Conditions could have also proved challenging: Despite the Board’s

quick decision to reject the offer, we believe that this decision would have

been better communicated if the formal conditions were also released (as was

the case with WPL’s offer for OSH). Nonetheless, it would be fair to assume

that the conditions included the typical “no shop, no talk”, exclusivity, subject

to financing and due diligence provisions. While the bidder appears well

funded, any clauses surrounding exclusivity could hamper ongoing asset

sales over an extended due diligence process. With no guarantees

surrounding a potential transaction post due diligence, agreeing to the offer

would significantly narrow STO’s options and leave the company exposed.

Asset sales appear the preferred option: With indicative offers for asset-

levels also likely received (with the press reporting that initial offers could be

announced in early November), we believe that the Board’s decision reflects

the level of interest that has been received regarding specific assets. In our

recent note, STO - No assets are sacred, we highlighted those potential asset

scenarios and how the residual business could look. With the industry willing

to buy assets at the forward curve and with STO reportedly receiving plenty of

interest in asset sales, we continue to see this as the more favourable option

to expose the value of STO’s asset base. That said, if Scepter were to

increase their offer by a mere 10% to ~A$7.58/sh, we believe such an offer

could not as easily be dismissed as opportunistic by the STO Board

(particularly if concessions were made surrounding specific conditions).

Earnings and target price revision

No change

Price catalyst

12-month price target: A$7.50 based on a DCF methodology.

Catalyst: STO reports 3Q15 operating results on 23 October and we expect

will announce initial asset sales in early-to-mid November.

Action and recommendation

Maintain an Outperform rating and a A$7.50/sh target.

Macquarie Research Santos

23 October 2015 2

Value on offer

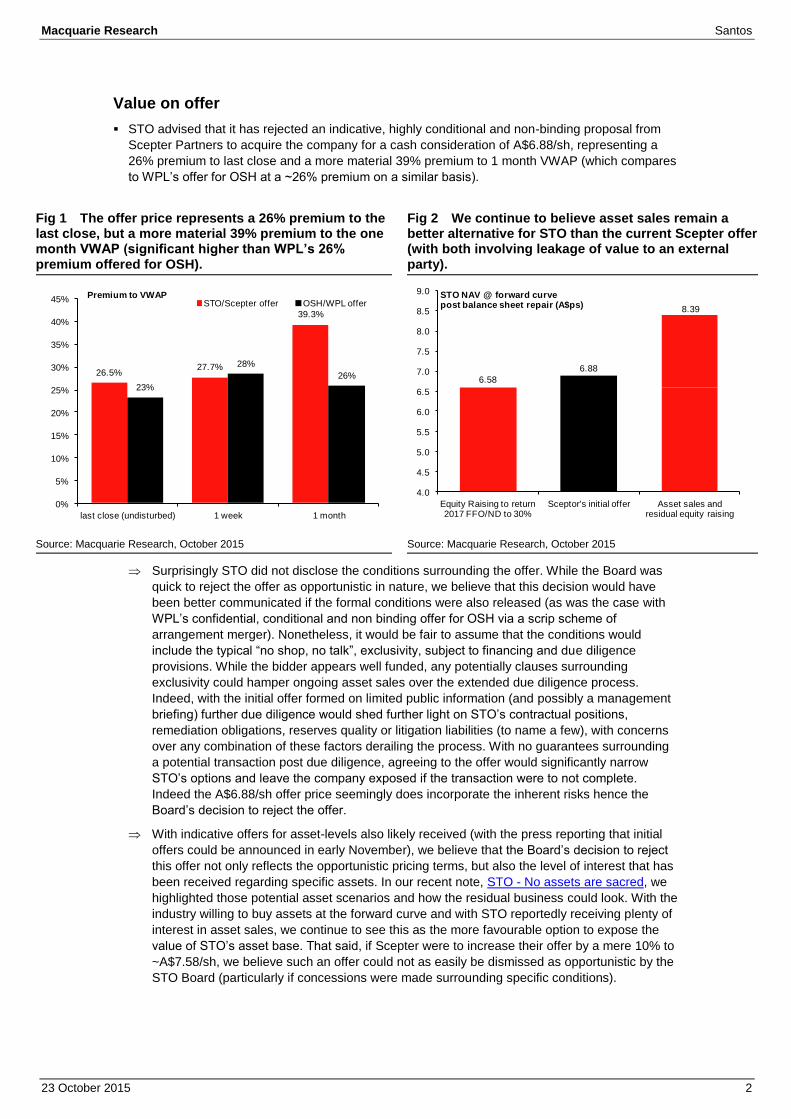

STO advised that it has rejected an indicative, highly conditional and non-binding proposal from

Scepter Partners to acquire the company for a cash consideration of A$6.88/sh, representing a

26% premium to last close and a more material 39% premium to 1 month VWAP (which compares

to WPL’s offer for OSH at a ~26% premium on a similar basis).

Fig 1 The offer price represents a 26% premium to the last close, but a more material 39% premium to the one month VWAP (significant higher than WPL’s 26% premium offered for OSH).

Fig 2 We continue to believe asset sales remain a better alternative for STO than the current Scepter offer (with both involving leakage of value to an external party).

Source: Macquarie Research, October 2015 Source: Macquarie Research, October 2015

Surprisingly STO did not disclose the conditions surrounding the offer. While the Board was

quick to reject the offer as opportunistic in nature, we believe that this decision would have

been better communicated if the formal conditions were also released (as was the case with

WPL’s confidential, conditional and non binding offer for OSH via a scrip scheme of

arrangement merger). Nonetheless, it would be fair to assume that the conditions would

include the typical “no shop, no talk”, exclusivity, subject to financing and due diligence

provisions. While the bidder appears well funded, any potentially clauses surrounding

exclusivity could hamper ongoing asset sales over the extended due diligence process.

Indeed, with the initial offer formed on limited public information (and possibly a management

briefing) further due diligence would shed further light on STO’s contractual positions,

remediation obligations, reserves quality or litigation liabilities (to name a few), with concerns

over any combination of these factors derailing the process. With no guarantees surrounding

a potential transaction post due diligence, agreeing to the offer would significantly narrow

STO’s options and leave the company exposed if the transaction were to not complete.

Indeed the A$6.88/sh offer price seemingly does incorporate the inherent risks hence the

Board’s decision to reject the offer.

With indicative offers for asset-levels also likely received (with the press reporting that initial

offers could be announced in early November), we believe that the Board’s decision to reject

this offer not only reflects the opportunistic pricing terms, but also the level of interest that has

been received regarding specific assets. In our recent note, STO - No assets are sacred, we

highlighted those potential asset scenarios and how the residual business could look. With the

industry willing to buy assets at the forward curve and with STO reportedly receiving plenty of

interest in asset sales, we continue to see this as the more favourable option to expose the

value of STO’s asset base. That said, if Scepter were to increase their offer by a mere 10% to

~A$7.58/sh, we believe such an offer could not as easily be dismissed as opportunistic by the

STO Board (particularly if concessions were made surrounding specific conditions).

26.5%27.7%

39.3%

23%

28%

26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

last close (undisturbed) 1 week 1 month

STO/Scepter offer OSH/WPL offerPremium to VWAP

6.58

6.88

8.39

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

9.0

Equity Raising to return 2017 FFO/ND to 30%

Sceptor's initial offer Asset sales and residual equity raising

STO NAV @ forward curvepost balance sheet repair (A$ps)

Macquarie Research Santos

23 October 2015 3

At A$6.88/sh, we estimate this implies an oil price discounted by core and risked NAV of

~U$59/bbl and U$54/bbl, which compares to longer-term futures curve at U$64/bbl and our LT

normalised assumption of U$80/bbl. Indeed STO also suggested that it did not reflect the "fair

value of the asset base", let alone a premium for control. While offers for OSH would likely

attract a premium vs. STO (given the differing quality of assets, growth prospects, balance

sheet position, etc), a comparison of Scepter’s offer vs. WPL initial offer for OSH perhaps

highlights the opportunistic nature of the Scepter proposal. Indeed we estimate that the pricing

terms imply a 15-50% discount to WPL’s offer for OSH (based on 1 month VWAP prior to the

disturbed price) based on various valuation metrics.

Fig 3 Scepter’s offer seemingly looks even more opportunistic than WPL’s offer for OSH, with the implied discount on various valuation metrics ranging from 15-50%.

WPL/OSH Scepter/STO Discount

Oil price discounted U$/bbl ~U$65/bbl ~U$54/bbl (15.6%) 2017 EV/prod U$/kboepd $116,355 $99,512 (14.5%) 2017 EV/EBITDA x 7.0 x 4.9 x (29.7%) 2017 EV/EBIT x 13.0 x 9.2 x (29.6%) EV/1P U$/boe $26.7 $21.2 (20.4%) EV/2P U$/boe $20.1 $10.6 (47.1%) EV/2P+2C U$/boe $9.1 $4.5 (51.0%)

Source: Macquarie Research, October 2015

Who is the bidder?

The bidder, Scepter Partners, is a Bermuda-based merchant bank and direct investment syndicate

for sovereign wealth led by the former Blackstone Advisor Partners Asian team. The group sponsors

the acquisition of large cap strategic assets with a focus on natural resources, infrastructure, real

estate and media/telecom (STO seems to tick two of these boxes).The core stakeholders include

high net worth senior members of Asian and Gulf-based ruling families (reportedly include ruling

families in Brunei and UAE). Scepter highlights that it invests with a long-term horizon, providing

businesses with capital to realise growth potential – indeed STO are seemingly in need of both.

With funds only recently allocated to the bidding party from high net worth individuals we

would expect that Scepter Partners remain keen to impress their key stakeholders with their

foundation transaction. Furthermore, with the key stakeholders supporting Scepter well known

(and publicised), we would suspect that management of Scepter (including Anthony Steains

the current CEO) would be keen to highlight their transaction experience to these

stakeholders. Consequently we do believe this is a creditable (albeit conditional) offer.

In mid-September the Board of Scepter stakeholders (led by HH Price Abdul Ali Kabier of

Brunei) allocated U$14b of discretionary assets. Scepter also claim that its key stakeholders

have net worth in excess of A$100bn, suggesting that the bidder is well funded.

STO always screened as the most obvious takeover target

In our recent note, Australian Energy Sector - The next M&A cycle set to commence, we painted a

picture of growing M&A against the backdrop of lower-for-longer oil prices. While we did not

necessarily believe that any of the locally listed large-cap E&P stocks were takeover targets in their

own right, we have now seen offers for two of the three stocks, namely STO and OSH. That said we

have always screened STO as the most obvious takeover target from a valuation perspective, albeit

there were stock specific challenges (namely the long-tail of assets).

Macquarie Research Santos

23 October 2015 4

Fig 4 Adopting average EV/2P transaction metrics for gas-weighted assets over the last 5 years and adjusting for sunk development costs, STO screened as the only possible takeover target

WPL STO OSH

Market EV/2P US$/bbl $8.26 $8.26 $8.26 5 year average of global gas focused transactions Developed EA gas mmboe 136 EV/2P U$/boe $10.00 Developed reserves justify slight premium Undeveloped EA gas mmboe 344 EV/2P U$/boe $2.07 25% of global avg EV/2P multiple Enterprise Value US$bn $0.00 $2.07 $0.00 Developed 2P Reserves mmboe 761 510 411 EV/2P U$/boe $14.46 $14.46 $14.46 Average capital intensity of Pluto, PNG LNG Undeveloped 2P Reserves mmboe 577 256 132 EV/2P U$/boe $8.26 $8.26 $8.26 5 year average of global gas focused transactions Enterprise Value US$bn $15.77 $9.48 $7.04 2C Resources mmboe 1,743 1,424 770 EV/2C U$/boe $1.65 $1.65 $1.65 20% of global avg EV/2P multiple Enterprise Value US$bn $2.88 $2.35 $1.27

Total Enterprise Value US$bn $18.65 $13.91 $8.31 Net Debt $3.82 $5.95 -$0.77 Excludes project financing for PNG LNG

Implied Market Cap A$ps $18.09 $11.01 $11.07 Issued shares 824 1,009 1,523

Implied share price $21.96 $10.91 $7.27

Premium to current share price -29% 73% -2%

Source: Macquarie Research, October 2015

Adopting average transaction metrics for gas-weighted transactions over the last five years

and making adjustments for the developed reserves base we estimate that the average

implied takeover premium vs. current share prices for Australian Energy stocks is merely 14%

- barely enough to build in a control premium. Indeed, as has historically been the case, STO

appears the only plausible takeover with the implied takeover price 70% above the current

share price.

STO continues to have a long-tail of assets which has historically dissuaded potential suitors

attracted to specific assets. However, with the offer price ascribing value for only STO’s five

most valuable assets under Macquarie assumptions (but closer to 20 assets under the

forward curve) and with the A&D market becoming more liquid, a risk-seeking buyer (such as

Scepter) could back itself to restructure STO’s portfolio (whether it be through asset sales or

carve-outs), leaving it with the most valuable assets.

Fig 5 STO has the largest portion of undeveloped reserves and largest resource-to-reserves ratio

Fig 6 While STO has a long-tail of assets, the most valuable 8 assets underpin the current enterprise value

Source: Company Data, Macquarie Research, August 2015 Source: Macquarie Research, August 2015

0

500

1,000

1,500

2,000

2,500

3,000

3,500

WPL STO OSH

Developed 2P Undeveloped 2P 2C2P+2C (mmboe)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

GL

NG

PN

G L

NG

Co

op

er

Re

ind

ee

rK

ipp

er

Ch

im S

ao

Spar

Da

rwin

L

NG

NAV @ MRE assumptions

NAV @ Forward Curve

Offer EV

Enterprise Value (A$m)

Macquarie Research Santos

23 October 2015 5

Asset sales still the preferred option

With indicative offers for asset-levels also likely received (with the press reporting that initial offers

could be announced in early November), we believe that the Board’s decision to reject this offer not

only reflects the opportunistic pricing terms, but also the level of interest that has been received

regarding specific assets. In our recent note, STO - No assets are sacred, we highlighted those

potential asset scenarios and how the residual business could look. With the industry willing to buy

assets at the forward curve and with STO reportedly receiving plenty of interest in asset sales, we

continue to see this as the more favourable option to expose the value of STO’s asset base.

Focusing on NAV and FCF yields even adjusting for the additional equity required in instances

where there is a funding shortfall, we estimate that the implied TERP is at up to a 9% discount

to post asset sale/equity raising core NAV or 25% discount to risked NAV, with a sale of PNG

LNG delivering the largest discount. Nonetheless a sale of the highest margin businesses

(PNG LNG and WA&NT) hits 2017 FCF yields, despite the limited additional equity required

with 2017 yields falling to 11.3% and 10.6% respectively

Fig 7 Assuming each asset sale in isolation (and any equity issuance to resolve the shortfall) we estimate the TERP is still at up to a 25% discount to our post asset sale/equity issuance risked NAV

Fig 8 However minimising the requirement for equity through asset sales comes at a cost in term of FCF yields (albeit with STO still offering healthy yields on a post asset sale & post money basis)

Source: Macquarie Research, October 2015 Source: Macquarie Research, October 2015

Sale of producing assets will have an obvious impact on pro-forma production, EBITDA,

NPAT and FCF. While this could rebase the size of the business lower, as the executive

chairman Peter Coates has articulated, the focus of the strategic review is to “restore and

maximise shareholder value” not preserve production for the sake of maximising the scale of

the business. Indeed we would argue that the market is far more focused on STO’s balance

sheet and preserving the value of the asset base, rather than retaining a production base.

Fig 9 Assuming assets sales and a shortfall raising the STO business will look difference, however the focus should remain on the balance sheet and value creation, not necessarily headline production and earnings

2017 forecasts Base Case (A$2bn

raising)

PNG LNG sale

WA&NT sale

Moomba infrastructure

sale

SE Asia (ex PNG LNG)

sale

GLNG pipeline sale

Production mmboe 67.4 56.4 51.9 67.7 62.5 67.7 Sales mmboe 75.7 67.7 62.7 78.2 73.0 78.2 Revenue A$m 4,072 3,369 3,338 4,092 3,840 4,096 EBITDA A$m 2,474 1,942 1,955 2,395 2,303 2,448 EBIT A$m 1,028 695 723 943 923 996 NPAT A$m 467 320 289 417 405 447 EPS Acps 29 29 25 32 31 31 Operating Cash Flow A$m 2,293 1,879 1,796 2,225 2,100 2,265 Free Cash Flow A$m 1,156 777 773 1,201 1,019 1,152 EV/EBITDA x 7.2 x 7.1 x 7.3 x 6.3 x 6.6 x 6.4 x PER x 21.5 x 21.6 x 25.4 x 19.9 x 20.7 x 20.3 x FCF Yield % 11.6% 11.3% 10.6% 14.5% 12.2% 12.8% * Forecasts assume the forward curve and spot fx. Based upon TERP assuming a the equity shortfall is raised at a 30% discount to closing price on 22 Oct(A$6.32/sh)

Source: Macquarie Research, September 2015

-30%

-25%

-20%

-15%

-10%

-5%

0%

4

5

5

6

6

7

7

8

8

9

9

Base Case (A$2bn

raise)

PNG LNG sale

WA / NT sale

Moomba sale

SE Asia sale

GLNG pipeline

sale

Core NAV

Risked NAV

TERP discount to Core NAV [RHS]

STO NAV (A$/sh) %

1.4%

0.3%

3.4%

1.6%

2.8%

11.3%10.6%

14.5%

12.2%12.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

PNG LNG sale

WA / NT sale Moomba sale SE Asia sale GLNG pipeline sale

2016 2017

Post asset sale and equity raising FCF Yield (based on TERP)

Macquarie Research Santos

23 October 2015 6

Fig 10 Santos financials

Source: Company data, Macquarie Research, October 2015

Santos (STO-AU) Share Price: A$6.32

Outperform Shares: 1004.4m

Profit & Loss 1H15A 2H15E 2014A 2015E 2016E 2017E Price Assumptions 1H15A 2H15E 2014A 2015E 2016E 2017E

Sales revenue A$m 1,611 1,711 4,037 3,322 4,245 4,904 US$/A$ ¢ 0.77 0.69 0.89 0.73 0.63 0.67

add other income A$m 44 43 81 87 81 76 Domestic gas A$/GJ 4.00 4.44 3.53 4.22 6.52 6.97

Total revenue A$m 1,655 1,753 4,118 3,408 4,326 4,980 Oil-Brent US$/bbl 57.53 52.00 100.08 54.76 58.25 67.00

less operating costs A$m (717) (829) (2,029) (1,546) (1,749) (1,825)

EBITDAX A$m 938 924 2,089 1,862 2,577 3,155 Production 1H15A 2H15E 2014A 2015E 2016E 2017E

less exploration expensed A$m (194) (90) (256) (284) (136) (140) Natural gas PJ 88.6 90.3 178.8 178.8 181.9 183.0

EBITDA A$m 744 834 1,833 1,578 2,441 3,015 Crude mmbbl 3.8 4.2 9.6 8.1 6.8 5.9

less dep. & amort. A$m (480) (543) (988) (1,023) (1,225) (1,320) Condensate mmbbl 1.9 2.0 3.2 3.9 3.9 3.9

less other non-cash costs A$m (13) - - (13) - - LPG k tonnes 74.3 91.3 167.4 165.6 180.0 183.9

EBIT A$m 251 291 845 542 1,217 1,695 LNG k tonnes 660.7 704.7 826.7 1365.4 1926.3 2367.7

less net interest A$m (125) (149) (97) (274) (444) (369) Total production mmboe 29.1 28.4 54.1 58.4 63.3 67.4

Pre-tax operating profit A$m 126 142 748 268 772 1,325 Third party sales mmboe 6.5 4.4 12.5 8.4 11.7 12.8

less tax expense (incl PRRT) A$m (94) (52) (215) (146) (286) (441) Total sales mmboe 34.8 31.0 63.7 64.8 70.8 75.7

Net operating profit A$m 32 90 533 122 486 884

add non-recurring items A$m 5 - (1,468) 5 - -

Reported profit A$m 37 90 (935) 127 486 884

add (goodw ill amm - pref div) A$m - - - - - -

Adjusted profit A$m 32 90 533 122 486 884

0% 0% 0%

EPS (Adjusted) Acps 3.3 9.0 54.7 12.3 46.1 80.1

EPS Grow th % -88% 177% 5% -78% 276% 74%

DPS (Ordinary & Special) Acps 15 15 35 30 32 35

Franking % 100% 100% 100% 100% 100% 100%

EFPOWA shares on issue m 984 1,004 975 994 1,050 1,103

Cashflow Analysis 1H15A 2H15E 2014A 2015E 2016E 2017E Reserves 2014A 2015E 2016E 2017E

Cash receipts from operations A$m 1,825 1,754 4,577 3,579 4,318 5,172 Natural gas PJ 6,786 6,607 6,425 6,242

less operating costs A$m (1,031) (833) (2,371) (1,864) (2,217) (1,771) Oil mmbbl 62 54 47 41

less gross interest paid A$m (83) (126) (49) (209) (389) (321) Condensate mmbbl 63 59 55 51

less tax paid A$m (77) (34) (164) (111) (111) (163) LPG k tonnes 3,022 2,856 2,676 2,492

Cashflow from operations A$m 634 761 1,993 1,395 1,601 2,917 Total 2P reserves mmboe 1,245 1,186 1,123 1,056

less development & exploration A$m (1,288) (1,160) (3,714) (2,448) (1,051) (1,138) Contingent resources mmbbl 1,721 1,721 1,721 1,721

less acq./inv. A$m (125) - (48) (125) - - Total reserves & resources mmboe 2,966 2,907 2,844 2,777

add divestment A$m 47 45 1 92 - -

less dividends paid A$m (107) (151) (196) (258) (315) (364) 2P reserve life years 23.1 20.3 17.7 15.7

add debt movements A$m 334 27 2,081 361 (150) (1,765) EV/ 1P reserves A$/boe 22.20 24.50 27.60 31.88

add equity movements/other A$m 106 151 10 257 315 364 EV / 2P reserves A$/boe 11.11 11.65 12.31 13.10

Net cashflow A$m (399) (327) 127 (726) 400 14 EV / Total resources A$/boe 4.66 4.76 4.86 4.98

add exchange rate adj. A$m 23 - 4 23 - - EV/ 1P reserves US$/boe 17.32 19.11 21.52 24.87

Increase in cash A$m (376) (327) 131 (703) 400 14 EV / 2P reserves US$/boe 8.66 9.09 9.60 10.21

Net debt at year end A$m 8,600 10,421 7,477 10,421 9,952 7,355 EV / Total resources US$/boe 3.64 3.71 3.79 3.88

Balance Sheet 1H15A 2H15E 2014A 2015E 2016E 2017E Per Barrel Statistics 1H15A 2H15E 2014A 2015E 2016E 2017E

Cash & cash eq. A$m 399 72 775 72 472 486 Sales revenue / boe US$/boe 56.63 57.04 66.44 41.31 42.43 48.95

Current assets A$m 1,662 1,340 2,065 1,340 1,751 1,582 EBIT / boe US$/boe 8.82 9.71 13.91 6.74 12.16 16.92

Fixed assets A$m 21,851 22,417 20,280 22,417 22,106 21,743 Profit / boe US$/boe 1.12 3.01 8.77 1.52 4.86 8.82

Total assets A$m 23,513 23,757 22,345 23,757 23,857 23,325 Opex/boe US$/boe 11.92 11.10 16.44 11.53 9.40 9.22

Current liabilities A$m 1,578 1,395 1,946 1,395 2,563 2,553 Capex/boe US$/boe 34.67 26.61 61.13 30.45 10.50 11.36

Total liabilities A$m 13,800 15,336 12,932 15,336 15,032 12,840 DDA/boe US$/boe 16.62 17.87 16.26 12.54 12.09 13.04

Shareholder equity A$m 9,713 8,421 9,413 8,421 8,824 10,485 Cash flow /boe US$/boe 22.29 25.37 32.80 17.35 16.00 29.12

Ratio Analysis 1H15A 2H15E 2014A 2015E 2016E 2017E NPV @ WACC of 9.0%

ND/ND+E % 47% 55% 44% 55% 53% 41% Producing assets A$m A$ps %

Interest cover x 2.1 x 2.5 x 8.7 x 2.0 x 2.7 x 4.6 x Cooper Basin Area 2,647 2.62

Dividend payout ratio % 461% 167% -37% 235% 68% 43% Onshore Queensland CSG Assets 79 0.08

ROA % 1% 1% 4% 2% 5% 7% Otw ay Gas 245 0.24

ROE % 0% 1% 5% 1% 6% 9% WA Gas 1,484 1.47

ROIC % 0% 0% 4% 2% 4% 6% WA Oil 522 0.52

Effective tax rate % 76% 33% 34% 53% 32% 31% South East Asia 868 0.86

EBITDA margin % 46% 49% 45% 48% 58% 61% Bayu-Undan 376 0.37

EBIT margin % 16% 17% 21% 16% 29% 35% PNG LNG trains 1 & 2 risked valuation @ 100% 2,964 2.94

Free cash f low A$m (607) (354) (1,720) (961) 550 1,779 Developing assets

Kipper risked valuation @ 100% 634 0.63

Valuation 1H15A 2H15E 2014A 2015E 2016E 2017E Glastone LNG train 1&2 risked valuation @ 100% 5,262 5.21

EV/EBITDAX ratio x 17.4 x 15.0 x 6.6 x 7.4 x 5.4 x 4.4 x Cooper Basin - 2C risked valuation @ 50% 509 0.50

EV/DACF ratio x 22.4 x 18.0 x 7.6 x 9.2 x 7.0 x 5.6 x PNG LNG debottleneck risked valuation @ 75% 124 0.12

P/E ratio x 242.2 x 70.2 x 11.6 x 51.6 x 13.7 x 7.9 x Static assets & exploration

P/CFPS ratio x 22.0 x 17.5 x 3.5 x 4.4 x 3.6 x 3.0 x PNG LNG train 3 risked valuation @ 75% 449 0.45

FCF yield % nmf nmf nmf nmf 8.2% 25.6% Discoveries 687 0.68

Dividend yield % 1.9% 2.4% 5.5% 4.7% 5.0% 5.5% Exploration 990 0.98

Financial assets

Sensitivities (Adjusted Earnings) Valuation 2014A 2015E 2016E 2017E Corporate/tariffs/other 185 0.18

Oil price (+US$1/bbl) A$m 12.11 533 144 524 942 Cash & Investments 444 0.44

delta 0.15 0 21 38 58 Debt (6,395) (6.34)

1.3% 0.0% 17.5% 7.8% 6.6% Risked NPV 12,074 11.96

Currency (+1c) A$m 11.69 533 122 469 871 Shareprice prem/(disc) to NPV -47%

delta (0.27) 0 (0) (17) (13) - core NPV per share (A$) 10.03

-2.3% 0.0% -0.4% -1.7% -1.2% - risked NPV per share (A$) 11.96

- unrisked NPV per share (A$) 15.34

0

10

20

30

40

50

60

70

80

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

Gas Crude Condensate LPG LNGmmboe

Macquarie Research Santos

23 October 2015 7

Fig 11 Santos NAV breakdown

Source: Macquarie Research, October 2015

Producing Assets Interest Unrisked Unrisked Risk Risked Risked USD/boe A$ps A$ps % NPV Sensitivity

mmmboe AUD (m) mmmboe AUD (m) risked unrisked -$10 Base +$10

Cooper Basin - 2P 63.0% 212 2,647 100% 212 2,647 9.4 2.62 2.62 22% 1.38 2.62 2.33

Surat / Denison various 6 68 100% 6 68 8.9 0.07 0.07 1% 0.08 0.07 0.08

Fairview 30.0% 1 11 100% 1 11 11.0 0.01 0.01 0% - 0.01 -

Casino & Henry 50.0% 16 224 100% 16 224 10.8 0.22 0.22 2% 0.25 0.22 0.25

Minerva 10.0% 2 21 100% 2 21 6.5 0.02 0.02 0% 0.02 0.02 0.02

Bayu-Undan 11.5% 19 376 100% 19 376 14.6 0.37 0.37 3% 0.29 0.37 0.48

John Brookes 45.0% 47 328 100% 47 328 5.3 0.33 0.33 3% 0.27 0.33 0.28

Spar/Halyard (Aus) 45.0% 32 409 100% 32 409 9.6 0.41 0.41 3% 0.49 0.41 0.52

Reindeer/Carabou 45.0% 35 746 100% 35 746 15.9 0.74 0.74 6% 0.74 0.74 0.96

Barrow Island 28.6% 4 141 100% 4 141 26.9 0.14 0.14 1% 0.12 0.14 0.16

Stag 66.7% 6 238 100% 6 238 27.6 0.24 0.24 2% 0.20 0.24 0.28

Mutineer / Exeter 41.6% 1 30 100% 1 30 32.6 0.03 0.03 0% 0.02 0.03 0.03

Fletcher/Finucane 44.0% 3 113 100% 3 113 26.7 0.11 0.11 1% 0.08 0.11 0.12

Maleo & Peluang 67.5% 6 194 100% 6 194 26.5 0.19 0.19 2% 0.22 0.19 0.22

SE Gobe 9.4% 0 6 100% 0 6 27.4 0.01 0.01 0% 0.00 0.01 0.01

Chim Sao & Dua (Vietnam) 31.9% 13 599 100% 13 599 35.2 0.59 0.59 5% 0.56 0.59 0.79

Oyong & Wortel 45.0% 6 69 100% 6 69 9.3 0.07 0.07 1% 0.07 0.07 0.07

PNG LNG trains 1 & 2 13.5% 234 2,964 100% 234 2,964 9.5 2.94 2.94 25% 2.25 2.94 3.42

Sub Total 642 9,185 642 9,185 10.7 9.10 9.10 76% 7.04 9.10 10.04

Developing Assets

Gladstone LNG train 1&2 30.0% 451 5,262 100% 451 5,262 8.7 5.21 5.21 44% 3.64 5.21 5.43

PNG LNG debottleneck 13.5% 1 166 75% 0 124 239.6 0.12 0.16 1% 0.24 0.12 0.29

Kipper 35.0% 45 634 100% 45 634 10.6 0.63 0.63 5% 0.63 0.63 0.67

Cooper Basin - 2C 63.0% 212 1,017 50% 106 509 3.6 0.50 1.01 4% 0.00 0.50 0.37

Mereenie - 2P 50.0% 14 149 100% 14 149 8.2 0.15 0.15 1% 0.14 0.15 0.16

Gunnedah Basin (2P) 80.0% 133 736 20% 27 147 4.2 0.15 0.73 1% 0.16 0.15 0.16

Sub Total 855 7,964 643 6,825 8.0 6.76 7.89 57% 4.81 6.76 7.08

Static Assets

PNG LNG expansion train(s) 11.5% 66 599 75% 49 449 6.8 0.45 0.59 4% 0.37 0.45 0.54

Ande Ande Lumut - K-sand 50.0% 51 121 75% 38 91 7.4 0.09 0.12 1% 0.04 0.09 0.12

Sole - 2C 50.0% 18 30 75% 14 22 8.3 0.02 0.03 0% 0.04 0.02 0.04

Mereenie - 2C 50.0% 14 115 15% 2 17 6.4 0.02 0.11 0% 0.02 0.02 0.02

Caldita/Barossa 25.0% 125 666 30% 38 200 4.0 0.20 0.66 2% 0.09 0.20 0.28

Petrel/Tern 40.0% 152 202 30% 46 61 1.0 0.06 0.20 1% 0.06 0.06 0.06

Sub Total 273 1,530 141 779 4.2 0.83 1.52 6% 0.56 0.77 1.00

Exploration

Zola (Contingent) 24.8% 21 56 50% 10 28 3.0 0.03 0.06 0% 0.03 0.03 0.03

Bianchi (Prospective) 24.8% 12 20 50% 6 10 3.0 0.01 0.02 0% 0.01 0.01 0.01

Zola (Prospective) 24.8% 84 309 20% 17 62 3.0 0.06 0.31 1% 0.06 0.06 0.06

Burnside-1 (Aus) 47.8% 120 268 25% 30 67 2.0 0.07 0.27 1% 0.06 0.07 0.06

Winchester-1 (Aus) 75.0% 167 728 50% 83 364 3.5 0.36 0.72 3% 0.33 0.36 0.33

Crow n-1 (Aus) 30.0% 118 284 50% 59 142 2.0 0.14 0.28 1% 0.13 0.14 0.13

Lasseter-1 (Aus) 30.0% 144 353 50% 72 176 2.0 0.17 0.35 1% 0.16 0.17 0.16

Bestari-1 Block R PSC (Malay) 20.0% 40 245 50% 20 123 5.0 0.12 0.24 1% 0.11 0.12 0.11

Gunnedah Basin (2C) 50.0% 108 233 5% 5 12 1.8 0.01 0.23 0% 0.01 0.01 0.01

Cooper Basin - Shale 63.0% 26 69 10% 3 7 2.0 0.01 0.07 0% 0.01 0.01 0.01

Sub total 840 2,565 306 990 2.4 0.98 2.54 8% 0.82 0.98 0.82

Financial & Corporate

Cash & investments 444 0.44 0.44 4% 0.81 0.44 0.81

Debt & hybrid (6,395) (6.34) (6.34) -53% (5.92) (6.34) (5.92)

Base business carbon - - - 0% - - -

LNG projects carbon - - - - 0% - - -

ORR, Tariffs 440 0.44 0.44 4% 0.44 0.44 0.44

Third Party Sales 189 0.19 0.19 2% 0.25 0.19 0.25

Corporate overheads (445) (0.44) (0.44) -4% (0.50) (0.44) (0.50)

Sub Total (5,767) (5.71) (5.71) -48% (4.92) (5.71) (4.92)

Overall total 2,610 mmboe 12,013 AUDm 11.96 15.34 99% 8.36 11.96 14.07

-core NPV per share (A$) 833 10.03 6.69 10.03 11.91

-risked NPV per share (A$) 1,731 11.96 8.36 11.96 14.07

-unrisked NPV per share (A$) 2,610 15.34 11.86 15.34 18.47

Diluted number of shares (m) 1,009.3

Ordinary Shares on Issue (m) 1,004.4

In-the-money options outstanding (m) 4.9

Exchange Rate 0.75

WACC (post tax) 9.0%

Share Price 6.32

Price premium (discount) to NPV -47%

Proportion of NAV from LNG 75%

Franking credits (risked at 50% - A$ps) 0.40

Macquarie Research Santos

23 October 2015 8

Macquarie Quant View

The quant model currently holds a strong negative view on Santos. The

strongest style exposure is Growth, indicating this stock has good historic

and/or forecast growth. Growth metrics focus on both top and bottom line

items. The weakest style exposure is Price Momentum, indicating this

stock has had weak medium to long term returns which often persist into

the future.

Displays where the

company’s ranked based on

the fundamental consensus

Price Target and

Macquarie’s Quantitative

Alpha model.

Two rankings: Local market

(Australia & NZ) and Global

sector (Energy)

536/574 Global rank in

Energy

% of BUY recommendations 62% (8/13)

Number of Price Target downgrades 6

Number of Price Target upgrades 1

Macquarie Alpha Model ranking Factors driving the Alpha Model

A list of comparable companies and their Macquarie Alpha model score

(higher is better).

For the comparable firms this chart shows the key underlying styles and their

contribution to the current overall Alpha score.

Macquarie Earnings Sentiment Indicator Drivers of Stock Return

The Macquarie Sentiment Indicator is an enhanced earnings revisions

signal that favours analysts who have more timely and higher conviction

revisions. Current score shown below.

Breakdown of 1 year total return (local currency) into returns from dividends, changes

in forward earnings estimates and the resulting change in earnings multiple.

What drove this Company in the last 5 years How it looks on the Alpha model

Which factor score has had the greatest correlation with the company’s

returns over the last 5 years.

A more granular view of the underlying style scores that drive the alpha (higher is

better) and the percentile rank relative to the sector and market.

Source (all charts): FactSet, Thomson Reuters, and Macquarie Research. For more details on the Macquarie Alpha model or for more customised analysis and screens, please contact the Macquarie Global Quantitative/Custom Products Group ([email protected])

Fu

nd

am

en

tals

Quant

Local market rank Global sector rank

Attractive

-2.7

-2.6

-1.3

-0.9

-0.3

0.3

-3.0 -2.0 -1.0 0.0 1.0 2.0 3.0

Beach Energy

Santos

WorleyParsons

Oil Search

Woodside Petroleum

Caltex Australia

-100% -80% -60% -40% -20% 0% 20% 40% 60% 80% 100%

Beach Energy

Santos

WorleyParsons

Oil Search

Woodside Petroleum

Caltex Australia

Valuations Growth Profitability Earnings

Momentum

Price

Momentum

Quality

-0.6

-1.0

-0.5

-0.7

-0.2

0.6

-3.0 -2.0 -1.0 0.0 1.0 2.0 3.0

Beach Energy

Santos

WorleyParsons

Oil Search

Woodside Petroleum

Caltex Australia

-70% -50% -30% -10% 10% 30% 50% 70%

Beach Energy

Santos

WorleyParsons

Oil Search

Woodside Petroleum

Caltex Australia

Dividend Return Multiple Return Earnings Outlook 1Yr Total Return

-31%

-31%

-21%

-20%

31%

31%

32%

34%

-40% -20% 0% 20% 40%

⇐ Negatives Positives ⇒

Operating Leverage NTM

PEG Ratio Inverted

Operating Leverage Inc.

EPS Growth FY1

Operating Margin NTM

EPS Growth 5yr Historic

Interest Cover

EV/EBITDA FY0

0 1

Technicals & TradingRisk

LiquidityCapital & Funding

QualityPrice Momentum

Earnings MomentumProfitability

Growth

ValuationAlpha Model Score

-0.11-1.40

-1.19 0.01

-0.73-1.62

-0.41-0.41-0.03

-1.09-2.59

0 1

Normalized

Score

0 50 100

Percentile relative

to sector(/574)

0 50 100

Percentile relative

to market(/395)

Macquarie Research Santos

23 October 2015 9

Important disclosures:

Recommendation definitions

Macquarie - Australia/New Zealand Outperform – return >3% in excess of benchmark return Neutral – return within 3% of benchmark return Underperform – return >3% below benchmark return Benchmark return is determined by long term nominal GDP growth plus 12 month forward market dividend yield

Macquarie – Asia/Europe Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie First South - South Africa Outperform – expected return >+10% Neutral – expected return from -10% to +10% Underperform – expected return <-10%

Macquarie - Canada Outperform – return >5% in excess of benchmark return Neutral – return within 5% of benchmark return Underperform – return >5% below benchmark return

Macquarie - USA Outperform (Buy) – return >5% in excess of Russell 3000 index return Neutral (Hold) – return within 5% of Russell 3000 index return Underperform (Sell)– return >5% below Russell 3000 index return

Volatility index definition*

This is calculated from the volatility of historical price movements. Very high–highest risk – Stock should be expected to move up or down 60–100% in a year – investors should be aware this stock is highly speculative. High – stock should be expected to move up or down at least 40–60% in a year – investors should be aware this stock could be speculative. Medium – stock should be expected to move up or down at least 30–40% in a year. Low–medium – stock should be expected to move up or down at least 25–30% in a year. Low – stock should be expected to move up or down at least 15–25% in a year. * Applicable to Asia/Australian/NZ/Canada stocks only

Recommendations – 12 months Note: Quant recommendations may differ from Fundamental Analyst recommendations

Financial definitions

All "Adjusted" data items have had the following adjustments made: Added back: goodwill amortisation, provision for catastrophe reserves, IFRS derivatives & hedging, IFRS impairments & IFRS interest expense Excluded: non recurring items, asset revals, property revals, appraisal value uplift, preference dividends & minority interests EPS = adjusted net profit / efpowa* ROA = adjusted ebit / average total assets ROA Banks/Insurance = adjusted net profit /average total assets ROE = adjusted net profit / average shareholders funds Gross cashflow = adjusted net profit + depreciation *equivalent fully paid ordinary weighted average number of shares All Reported numbers for Australian/NZ listed stocks are modelled under IFRS (International Financial Reporting Standards).

Recommendation proportions – For quarter ending 30 September 2015

AU/NZ Asia RSA USA CA EUR

Outperform 48.87% 59.96% 35.63% 42.13% 59.44% 42.11% (for US coverage by MCUSA, 3.54% of stocks followed are investment banking clients)

Neutral 33.44% 25.00% 39.08% 52.55% 37.06% 38.42% (for US coverage by MCUSA, 5.05% of stocks followed are investment banking clients)

Underperform 17.68% 15.04% 25.29% 5.32% 3.50% 19.47% (for US coverage by MCUSA, 0.51% of stocks followed are investment banking clients)

STO AU vs ASX 100, & rec history

(all figures in AUD currency unless noted)

Note: Recommendation timeline – if not a continuous line, then there was no Macquarie coverage at the time or there was an embargo period.

Source: FactSet, Macquarie Research, October 2015

12-month target price methodology

STO AU: A$7.50 based on a DCF methodology

Company-specific disclosures: STO AU: Macquarie and its affiliates collectively and beneficially own or control 1% or more of any class of Santos Limited's equity securities. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/disclosures.

Date Stock Code (BBG code) Recommendation Target Price 09-Sep-2015 STO AU Outperform A$7.50 14-Aug-2015 STO AU Outperform A$9.00 15-Apr-2015 STO AU Outperform A$10.00 09-Mar-2015 STO AU Outperform A$11.00 09-Dec-2014 STO AU Outperform A$12.00 02-Dec-2014 STO AU Outperform A$14.50 08-Oct-2014 STO AU Outperform A$15.50 27-Jun-2014 STO AU Outperform A$17.00 16-May-2014 STO AU Outperform A$16.50 16-Aug-2013 STO AU Outperform A$17.00 23-Feb-2013 STO AU Outperform A$16.50

Target price risk disclosures: STO AU: Any inability to compete successfully in their markets may harm the business. This could be a result of many factors which may include geographic mix and introduction of improved products or service offerings by competitors. The results of operations may be materially affected by global economic conditions generally, including conditions in financial markets. The company is exposed to market risks, such as changes in interest rates, foreign exchange rates and input prices. From time to time, the company will enter into transactions, including transactions in derivative instruments, to manage certain of these exposures.

Analyst certification: We hereby certify that all of the views expressed in this report accurately reflect our personal views about the subject company or companies and its or their securities. We also certify that no part of our compensation was, is or will be, directly or indirectly, related to the specific recommendations or views expressed in this report. The Analysts responsible for preparing this report receive compensation from Macquarie that is based upon various factors including Macquarie Group Ltd total revenues, a portion of which are generated by Macquarie Group’s Investment Banking activities. General disclaimers:

Macquarie Research Santos

23 October 2015 10

Macquarie Securities (Australia) Ltd; Macquarie Capital (Europe) Ltd; Macquarie Capital Markets Canada Ltd; Macquarie Capital Markets North America Ltd; Macquarie Capital (USA) Inc; Macquarie Capital Securities Ltd and its Taiwan branch; Macquarie Capital Securities (Singapore) Pte Ltd; Macquarie Securities (NZ) Ltd; Macquarie First South Securities (Pty) Limited; Macquarie Capital Securities (India) Pvt Ltd; Macquarie Capital Securities (Malaysia) Sdn Bhd; Macquarie Securities Korea Limited and Macquarie Securities (Thailand) Ltd are not authorized deposit-taking institutions for the purposes of the Banking Act 1959 (Commonwealth of Australia), and their obligations do not represent deposits or other liabilities of Macquarie Bank Limited ABN 46 008 583 542 (MBL) or MGL. MBL does not guarantee or otherwise provide assurance in respect of the obligations of any of the above mentioned entities. MGL provides a guarantee to the Monetary Authority of Singapore in respect of the obligations and liabilities of Macquarie Capital Securities (Singapore) Pte Ltd for up to SGD 35 million. This research has been prepared for the general use of the wholesale clients of the Macquarie Group and must not be copied, either in whole or in part, or distributed to any other person. If you are not the intended recipient you must not use or disclose the information in this research in any way. If you received it in error, please tell us immediately by return e-mail and delete the document. We do not guarantee the integrity of any e-mails or attached files and are not responsible for any changes made to them by any other person. MGL has established and implemented a conflicts policy at group level (which may be revised and updated from time to time) (the "Conflicts Policy") pursuant to regulatory requirements (including the FCA Rules) which sets out how we must seek to identify and manage all material conflicts of interest. Nothing in this research shall be construed as a solicitation to buy or sell any security or product, or to engage in or refrain from engaging in any transaction. In preparing this research, we did not take into account your investment objectives, financial situation or particular needs. Macquarie salespeople, traders and other professionals may provide oral or written market commentary or trading strategies to our clients that reflect opinions which are contrary to the opinions expressed in this research. Macquarie Research produces a variety of research products including, but not limited to, fundamental analysis, macro-economic analysis, quantitative analysis, and trade ideas. Recommendations contained in one type of research product may differ from recommendations contained in other types of research, whether as a result of differing time horizons, methodologies, or otherwise. Before making an investment decision on the basis of this research, you need to consider, with or without the assistance of an adviser, whether the advice is appropriate in light of your particular investment needs, objectives and financial circumstances. There are risks involved in securities trading. The price of securities can and does fluctuate, and an individual security may even become valueless. International investors are reminded of the additional risks inherent in international investments, such as currency fluctuations and international stock market or economic conditions, which may adversely affect the value of the investment. This research is based on information obtained from sources believed to be reliable but we do not make any representation or warranty that it is accurate, complete or up to date. We accept no obligation to correct or update the information or opinions in it. Opinions expressed are subject to change without notice. No member of the Macquarie Group accepts any liability whatsoever for any direct, indirect, consequential or other loss arising from any use of this research and/or further communication in relation to this research. Clients should contact analysts at, and execute transactions through, a Macquarie Group entity in their home jurisdiction unless governing law permits otherwise. The date and timestamp for above share price and market cap is the closed price of the price date. #CLOSE is the final price at which the security is traded in the relevant exchange on the date indicated. Country-specific disclaimers: Australia: In Australia, research is issued and distributed by Macquarie Securities (Australia) Ltd (AFSL No. 238947), a participating organisation of the Australian Securities Exchange. New Zealand: In New Zealand, research is issued and distributed by Macquarie Securities (NZ) Ltd, a NZX Firm. Canada: In Canada, research is prepared, approved and distributed by Macquarie Capital Markets Canada Ltd, a participating organisation of the Toronto Stock Exchange, TSX Venture Exchange & Montréal Exchange. Macquarie Capital Markets North America Ltd., which is a registered broker-dealer and member of FINRA, accepts responsibility for the contents of reports issued by Macquarie Capital Markets Canada Ltd in the United States and sent to US persons. Any US person wishing to effect transactions in the securities described in the reports issued by Macquarie Capital Markets Canada Ltd should do so with Macquarie Capital Markets North America Ltd. The Research Distribution Policy of Macquarie Capital Markets Canada Ltd is to allow all clients that are entitled to have equal access to our research. United Kingdom: In the United Kingdom, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated by the Financial Conduct Authority (No. 193905). Germany: In Germany, this research is issued and/or distributed by Macquarie Capital (Europe) Limited, Niederlassung Deutschland, which is authorised and regulated by the UK Financial Conduct Authority (No. 193905). and in Germany by BaFin. France: In France, research is issued and distributed by Macquarie Capital (Europe) Ltd, which is authorised and regulated in the United Kingdom by the Financial Conduct Authority (No. 193905). Hong Kong & Mainland China: In Hong Kong, research is issued and distributed by Macquarie Capital Securities Ltd, which is licensed and regulated by the Securities and Futures Commission. In Mainland China, Macquarie Securities (Australia) Limited Shanghai Representative Office only engages in non-business operational activities excluding issuing and distributing research. Only non-A share research is distributed into Mainland China by Macquarie Capital Securities Ltd. Japan: In Japan, research is Issued and distributed by Macquarie Capital Securities (Japan) Limited, a member of the Tokyo Stock Exchange, Inc. and Osaka Exchange, Inc. (Financial Instruments Firm, Kanto Financial Bureau (kin-sho) No. 231, a member of Japan Securities Dealers Association). India: In India, research is issued and distributed by Macquarie Capital Securities (India) Pvt. Ltd. (CIN: U65920MH1995PTC090696), formerly known as Macquarie Capital (India) Pvt. Ltd., 92, Level 9, 2 North Avenue, Maker Maxity, Bandra Kurla Complex, Bandra (East), Mumbai – 400 051, India, which is a SEBI registered Research Analyst having registration no. INH000000545. Malaysia: In Malaysia, research is issued and distributed by Macquarie Capital Securities (Malaysia) Sdn. Bhd. (Company registration number: 463469-W) which is a Participating Organisation of Bursa Malaysia Berhad and a holder of Capital Markets Services License issued by the Securities Commission. Taiwan: In Taiwan, research is issued and distributed by Macquarie Capital Securities Ltd, Taiwan Branch, which is licensed and regulated by the Financial Supervisory Commission. No portion of the report may be reproduced or quoted by the press or any other person without authorisation from Macquarie. Nothing in this research shall be construed as a solicitation to buy or sell any security or product. Research Associate(s) in this report who are registered as Clerks only assist in the preparation of research and are not engaged in writing the research. Thailand: In Thailand, research is produced, issued and distributed by Macquarie Securities (Thailand) Ltd. Macquarie Securities (Thailand) Ltd. is a licensed securities company that is authorized by the Ministry of Finance, regulated by the Securities and Exchange Commission of Thailand and is an exchange member of the Stock Exchange of Thailand. The Thai Institute of Directors Association has disclosed the Corporate Governance Report of Thai Listed Companies made pursuant to the policy of the Securities and Exchange Commission of Thailand. Macquarie Securities (Thailand) Ltd does not endorse the result of the Corporate Governance Report of Thai Listed Companies but this Report can be accessed at: http://www.thai-iod.com/en/publications.asp?type=4. South Korea: In South Korea, unless otherwise stated, research is prepared, issued and distributed by Macquarie Securities Korea Limited, which is regulated by the Financial Supervisory Services. Information on analysts in MSKL is disclosed at http://dis.kofia.or.kr/websquare/index.jsp?w2xPath=/wq/fundMgr/DISFundMgrAnalystStut.xml&divisionId=MDIS03002001000000&serviceId=SDIS03002001000. South Africa: In South Africa, research is issued and distributed by Macquarie First South Securities (Pty) Limited, a member of the JSE Limited. Singapore: In Singapore, research is issued and distributed by Macquarie Capital Securities (Singapore) Pte Ltd (Company Registration Number: 198702912C), a Capital Markets Services license holder under the Securities and Futures Act to deal in securities and provide custodial services in Singapore. Pursuant to the Financial Advisers (Amendment) Regulations 2005, Macquarie Capital Securities (Singapore) Pte Ltd is exempt from complying with sections 25, 27 and 36 of the Financial Advisers Act. All Singapore-based recipients of research produced by Macquarie Capital (Europe) Limited, Macquarie Capital Markets Canada Ltd, Macquarie First South Securities (Pty) Limited and Macquarie Capital (USA) Inc. represent and warrant that they are institutional investors as defined in the Securities and Futures Act. United States: In the United States, research is issued and distributed by Macquarie Capital (USA) Inc., which is a registered broker-dealer and member of FINRA. Macquarie Capital (USA) Inc, accepts responsibility for the content of each research report prepared by one of its non-US affiliates when the research report is distributed in the United States by Macquarie Capital (USA) Inc. Macquarie Capital (USA) Inc.’s affiliate’s analysts are not registered as research analysts with FINRA, may not be associated persons of Macquarie Capital (USA) Inc., and therefore may not be subject to FINRA rule restrictions on communications with a subject company, public appearances, and trading securities held by a research analyst account. Information regarding futures is provided for reference purposes only and is not a solicitation for purchases or sales of futures. Any persons receiving this report directly from Macquarie Capital (USA) Inc. and wishing to effect a transaction in any security described herein should do so with Macquarie Capital (USA) Inc. Important disclosure information regarding the subject companies covered in this report is available at www.macquarie.com/research/disclosures, or contact your registered representative at 1-888-MAC-STOCK, or write to the Supervisory Analysts, Research Department, Macquarie Securities, 125 W.55th Street, New York, NY 10019. © Macquarie Group

Macquarie Research Santos

23 October 2015 11

Auckland

Tel: (649) 377 6433

Jakarta Tel: (62 21) 515 1818

Munich Tel: (089) 2444 31800

Sydney Tel: (612) 8232 9555

Bangkok

Tel: (662) 694 7999

Johannesburg Tel: (2711) 583 2000

New York Tel: (1 212) 231 2500

Taipei Tel: (886 2) 2734 7500

Calgary

Tel: (1 403) 294 9541

Kuala Lumpur Tel: (60 3) 2059 8833

Paris Tel: (33 1) 7842 3823

Tokyo Tel: (81 3) 3512 7900

Denver

Tel: (303) 952 2800

London Tel: (44 20) 3037 2000

Perth Tel: (618) 9224 0888

Toronto Tel: (1 416) 848 3500

Frankfurt

Tel: (069) 509 578 000

Manila Tel: (63 2) 857 0888

Seoul Tel: (82 2) 3705 8500

Vancouver Tel: (1 604) 605 3944

Geneva

Tel: (41) 22 818 7777

Melbourne Tel: (613) 9635 8139

Shanghai Tel: (86 21) 6841 3355

Hong Kong

Tel: (852) 2823 3588

Mumbai Tel: (91 22) 6653 3000

Singapore Tel: (65) 6601 1111

Available to clients on the world wide web at www.macquarieresearch.com and through Thomson Financial, FactSet, Reuters, Bloomberg, and CapitalIQ.

Research

Head of Equity Research

Peter Redhead (Global) (852) 3922 4836

Paul Checchin (Australia & NZ) (612) 8232 4197

Retail / Consumer / Food & Bev

Bryan Raymond (612) 8232 2740

Energy

Kirit Hira (612) 8232 9692

ESG

Deana Mitchell (612) 8232 4576

Financials

Banks

Brendan Carrig (612) 8237 6043

Anita Stanley (Maternity leave) (612) 8232 9869

Insurance & Diversified Financials

Tim Lawson (612) 8237 7332

Bryan Raymond (612) 8232 2740

Andrew Buncombe (612) 8232 0629

Healthcare

Dr Craig Collie (612) 8232 4130

Industrials

Capital Goods

John Purtell (612) 8232 8633

Niraj Shah (612) 8237 0750

Infrastructure

Ian Myles (612) 8232 4157

Transportation

Sam Dobson (612) 8232 9986

Chemicals, D&C, Packaging, Builders, Steel

John Purtell (612) 8232 8633

Niraj Shah (612) 8237 0750

Peter Steyn (612) 8232 5144

Resources

Hayden Bairstow (618) 9224 0838

Ben Crowley (618) 9224 0839

Andrew Hodge (612) 8237 0321

Real Estate

Paul Checchin (612) 8232 4197

Rob Freeman (612) 8237 1152

Telcos / Media / Tourism & Leisure

Andrew Levy (612) 8232 5165

Andrew Russell (612) 8232 9390

Utilities

Ian Myles (612) 8232 4157

Commodities & Precious Metals

Colin Hamilton (Global) (44 20) 3037 4061

Jim Lennon (London) (44 20) 3037 4271

New Zealand

Stephen Hudson (649) 363 1414

Warren Doak (649) 363 1416

Daniel Frost (649) 363 1474

Nick Mar (649) 363 1476

Andrew Levy (Telecommunications) (612) 8232 5165

Emerging Leaders – Industrials

Adam Simpson (612) 8232 4439

Andrew Wackett (618) 9224 0867

Jodie Bannan (612) 8232 2999

Jennifer Kruk (612) 8232 6422

Michael Higgins (612) 8232 3208

Quantitative

Gurvinder Brar (Global) (44 20) 3037 4036

John Conomos (Australia) (612) 8232 5157

Jeremy Lamplaugh (612) 8232 1060

Data Services

Sheridan Duffy (612) 8232 9786

Economics and Strategy

Jason Todd (612) 8237 3134

James McIntyre (Australia) (612) 8232 8930

Find our research at

Macquarie: www.macquarie.com.au/research

Thomson: www.thomson.com/financial

Reuters: www.knowledge.reuters.com

Bloomberg: MAC GO

Factset: http://www.factset.com/home.aspx

CapitalIQ www.capitaliq.com

Contact Gareth Warfield for access (612) 8232 3207

See and hear our analysts at www.macquarie.com.au/macquariedigital

Toll free from overseas

Canada 1800 989 8159

Hong Kong 800 96 2049

Japan 0053 161 6437

New York 1888 622 7862

Singapore 800 616 1037

Email addresses

Sales Equities

Dan Ritchie (Australia) (612) 8232 3124

Dave Roberton (New Zealand) (649) 363 1498

Sales

Kristen Edmond (Desk Head – Sydney) (612) 8232 3111

Gavin Maher (Australia) (612) 8232 4151

Nick Rehak (Australia) (612) 8232 4053

Charlotte Edelman (Australia) (612) 8232 4565

Kurt Dalton (Australia) (612) 8232 5943

Mike Johnson (Desk Head – Hong Kong & International Sales) (852) 3922 2050

Adam Millhouse (Hong Kong) (852) 3922 2055

Dan Pittorino (Desk Head - London) (44 20) 3037 4831

Andrew Haigh (London) (44 20) 3037 4843

Clare McCartney (London) (44 20) 3037 4833

Brendan Waller (Desk Head - Melbourne) (613) 9635 8177

Leighton Patrick (Desk Head - New York) (1 212) 231 2552

Rowly Hirst (New York) (1 212) 231 2553

Michael McNair (New York) (1 212) 231 2571

Sales Trading

Ben Clifford (Head of Sales Trading) (612) 8232 4012

Sam Molina (Sydney) (612) 8232 5935

John Ogle (Sydney) (612) 8232 3118

Francis Sarks (Sydney) (612) 8232 4458

Antony Kirwan (Sydney) (612) 8232 4003

Ben McIntyre (Sydney) (612) 8237 2833

Philip Sellaroli (Sydney) (612) 8232 2029

John Alessi (Melbourne) (613) 9635 9183

Andrew Donald (Melbourne) (613) 9635 8270

Natalie Rachele (Melbourne) (613) 9635 8595

Jon Holland (Auckland) (649) 363 1471

Mike Keen (London) (44 20) 3037 4905

Electronic Execution

Valerie Kingsmill (612) 8237 2230

Darren Miller (612) 8232 8261

James Giarratano (612) 8237 0878

Portfolio Trading

Garth Leslie (612) 8232 9982

Kathryn Koutouzis (612) 8237 5456

Block Trading

Tim Shaw (Desk Head – Sydney). (612) 8232 4386

Specialist Sales

Julia Thomas (Property) (613) 9635 9323

Phil Zammit (Emerging Leaders) (612) 8232 3122

Owen Johnston (Emerging Leaders) (612) 8232 3328

Alternative Strategies

Greg Mann (Equity Finance) (612) 8232 1820

Shannon Donohoe (Stock Borrow & Loan) (612) 8232 6997

Syndication

Paul Staines (612) 8232 7781

Angus Firth (612) 8232 4039

Tiffany Ward (612) 8232 5151

Corporate Access

Julie Loring (612) 8232 7543

Asha Walsh (612) 8237 8464

Transition Management & Portfolio Solutions

Mick Larkin (612) 8232 0639

David Goodman (612) 8232 5245

Scott Macaulay (612) 8232 4782