santucci 2/10 1 finances for smarties: or, the half million dollar vacation santucci

TRANSCRIPT

Santucci 2/10Santucci 2/10 11

Finances for Smarties: Or, the Finances for Smarties: Or, the half million dollar vacationhalf million dollar vacation

SantucciSantucci

Santucci 2/10Santucci 2/10 22

How much will I need for retirement?How much will I need for retirement?

More than you thinkMore than you think Calculate living to age 100Calculate living to age 100 Inflation is a killerInflation is a killer

– Rule of 72Rule of 72– Divide the inflation rate (3%?) into 72 and that’s the Divide the inflation rate (3%?) into 72 and that’s the

number of years your money will be cut in halfnumber of years your money will be cut in half– 72/3%= 23 years72/3%= 23 years– So, 23 years after the day you retire you’ll need TWICE So, 23 years after the day you retire you’ll need TWICE

as much money to keep from eating ALPO as you as much money to keep from eating ALPO as you needed beforeneeded before

– Consumer price index more like 4.4% = 16 years!Consumer price index more like 4.4% = 16 years!

Santucci 2/10Santucci 2/10 33

How much will I spend in retirement?How much will I spend in retirement?

More than you thinkMore than you think The idea is you will be sitting at home The idea is you will be sitting at home

knitting and watching the bird feeders-NOTknitting and watching the bird feeders-NOT Likely you will be healthy, active, and Likely you will be healthy, active, and

EXPENSIVEEXPENSIVE Estimate 60-100% of your current income! Estimate 60-100% of your current income!

(meaning the income you will be earning (meaning the income you will be earning when you are an attending)when you are an attending)

Santucci 2/10Santucci 2/10 44

How much will I spend in retirement II?How much will I spend in retirement II?

Keep the inflation thing in mindKeep the inflation thing in mind Realize that even with decreased expenses Realize that even with decreased expenses

(house paid off, kids out of the house) certain (house paid off, kids out of the house) certain expenses will go up and upexpenses will go up and up– Property taxesProperty taxes– Health care costsHealth care costs

How much does your free Medicare cost you?How much does your free Medicare cost you?– Try 20% copay and most/all of your drug costsTry 20% copay and most/all of your drug costs

– Gasoline? Heating? AC? Global warming? Oil wars?Gasoline? Heating? AC? Global warming? Oil wars? Rule of Thumb: 80% of your “current” incomeRule of Thumb: 80% of your “current” income

– Make $400,000-40% taxes = $240,000/yearMake $400,000-40% taxes = $240,000/year– $240,000 X .80 = $192,000 $240,000 X .80 = $192,000 – X 35 years = $6.72 millionX 35 years = $6.72 million

Santucci 2/10Santucci 2/10 55

But I really want to go on vacationBut I really want to go on vacation

Consider a $2,000 IRA contributionConsider a $2,000 IRA contribution $40 a week only$40 a week only At 30 years compound interest, at “historic At 30 years compound interest, at “historic

stock market returns” you will have stock market returns” you will have $500,000. $500,000.

At 50 years, you will have $3,000,000 (but it At 50 years, you will have $3,000,000 (but it will be worth $750,000 due to inflation by will be worth $750,000 due to inflation by then)then)

Don’t blow your IRA on vacationDon’t blow your IRA on vacation

Santucci 2/10Santucci 2/10 66

Simple Rule: Take the easy savings Simple Rule: Take the easy savings route: Traditional IRAroute: Traditional IRA

$5,000 a person TAX FREE$5,000 a person TAX FREE– Do not overcontribute: they tax you extra 6% penaltyDo not overcontribute: they tax you extra 6% penalty

Traditional IRA goes in tax free but you have to pay taxes Traditional IRA goes in tax free but you have to pay taxes on the money lateron the money later

Anyone can contribute (no salary limit), if you don’t have Anyone can contribute (no salary limit), if you don’t have some other sort of work 401k or OTHER way to savesome other sort of work 401k or OTHER way to save

For now, probably go traditionalFor now, probably go traditional ROTH IRA you have to pay taxes now, but accrues tax freeROTH IRA you have to pay taxes now, but accrues tax free Later, may want to convert to ROTH (your $3 million will Later, may want to convert to ROTH (your $3 million will

come out tax free)come out tax free) Can take out at 59.5 years of age but MANDATORY Can take out at 59.5 years of age but MANDATORY

distributions begin at 70.5 yearsdistributions begin at 70.5 years 10% fine if you take out before 59.5 years10% fine if you take out before 59.5 years

Santucci 2/10Santucci 2/10 77

More on RothMore on Roth

No mandatory distribution ageNo mandatory distribution age Can only contribute up to salary of $95,000 Can only contribute up to salary of $95,000

($150,000 filing jointly)($150,000 filing jointly) You can take out the principal anytime you You can take out the principal anytime you

wantwant Every once in a while, like this year and Every once in a while, like this year and

next, you can convert to a ROTH without next, you can convert to a ROTH without any income limit any income limit

Santucci 2/10Santucci 2/10 88

What is my tax rateWhat is my tax rate

If you make $50,000 a year, its 25%If you make $50,000 a year, its 25% So your traditional IRA starts off 25% richerSo your traditional IRA starts off 25% richerSingle Joint

$8,350 10% $16,700 10%

$33,950 15% $67,900 15%

$82,850 25% $137,050 25%

$171,550 28% $171,550 28%

$372,950 33% $372,950 33%

over 35% over $35

Santucci 2/10Santucci 2/10 99

Ok smart guy WHERE should I put Ok smart guy WHERE should I put my moneymy money

I have no ideaI have no idea 10 years ago: buy good stock and keep it10 years ago: buy good stock and keep it Now: buy stock and move it around. 10.5% historic gainsNow: buy stock and move it around. 10.5% historic gains Can buy inexpensive “index” funds that just mindlessly buy Can buy inexpensive “index” funds that just mindlessly buy

certain stock or bond indexes such as the S&P 500 fundcertain stock or bond indexes such as the S&P 500 fund Need age and RISK specific “asset allocation”Need age and RISK specific “asset allocation”

– Domestic stockDomestic stock Large/small cap (means “capitalization” and it means big or small Large/small cap (means “capitalization” and it means big or small

companies)companies)

– International stockInternational stock– BondsBonds

Usually the young keep most in stocks. 120-your age is Usually the young keep most in stocks. 120-your age is conservative. I will have 5 market cycles before retirement: conservative. I will have 5 market cycles before retirement: I keep most in stocksI keep most in stocks

Santucci 2/10Santucci 2/10 1010

Debt killsDebt kills

The average American has $8,000 in credit The average American has $8,000 in credit card debtcard debt

At 12%, it will cost you bout $10,000 over 9 At 12%, it will cost you bout $10,000 over 9 years ($400 a month)\years ($400 a month)\

Transfer to a 1 year 0% card will save Transfer to a 1 year 0% card will save $1,000 (final cost $9,000)$1,000 (final cost $9,000)

Santucci 2/10Santucci 2/10 1111

Santucci 2/10Santucci 2/10 1212

Cost of bad credit ICost of bad credit I

Home Mortgage Median Sales Price of Existing Single-Family Homes in the Midwest is $142,700

Credit Type Term Rate Payment

Cost of high interest rate

Perfect 30 6% $855 0

Medium 30 7.50% $997 $51,198

Bad 30 9% $1,148 $105,349

Santucci 2/10Santucci 2/10 1313

Cost of bad credit IICost of bad credit II

Auto Financing Average auto debt per borrower nationally is $12,738. Sources: TransUnion. An average rate for new and used auto loans with good credit is 6.41%. Sources: HSH Associates.

Credit Type Term Rate Payment

Cost of high interest rate

Perfect 6 6% $213 0

Medium 6 9.50% $232 $1,190

Bad 6 15% $269 $3,457

Santucci 2/10Santucci 2/10 1414

How is your credit score calculatedHow is your credit score calculated

35% - Your Payment History

– Number of accounts paid as agreed

– Negative public records or collections – Delinquent accounts: – total number of past due items– how long you've been past due– how long it's been since you had a past due payment

30% - Amounts You Owe

– How much you owe on accounts and the types of accounts with balances

– How much of your revolving credit lines you've used--looking for indications you are over-extended

– Amounts you owe on installment loan accounts vs. their original balances--to make sure you are you paying them down consistently

– Number of zero balance accounts

Santucci 2/10Santucci 2/10 1515

How is your credit score calculated IIHow is your credit score calculated II

15% - Length of Your Credit History

– Total length of time tracked by your credit report

– Length of time since accounts were opened

– Time that's passed since the last activity

– The longer your (good) history, the better your scores

10% - Types of Credit Used

– Total number of accounts and types of accounts (installment, revolving, mortgage, etc.)

– A mixture of account types usually generates better scores than reports with only numerous revolving accounts (credit cards)

10% - New Credit

– Number of accounts you've recently opened and the proportion of new accounts to total accounts

– Number of recent credit inquiries

– The time that's passed since recent inquiries or newly-opened accounts

– If you've re-established a positive credit history after encountering payment problemsIn general, checking to make sure you aren't attempting to open numerous new accounts

Santucci 2/10Santucci 2/10 1616

Credit ScoreCredit Score

Credit scores (usually) range from 340 to 850. The higher your score, the less risk a lender believes you will be. As your score climbs, the interest rate you are offered will probably decline.

Borrowers with a credit score over 700 are typically offered more financing options and better interest rates,

Credit scores among the US population in 2003:Up to 499: 1%500 - 549: 5%550 - 599: 7%600 - 649: 11%650 - 699: 16%700 - 749: 20%750 - 799: 29%Over 800: 11%

Santucci 2/10Santucci 2/10 1717

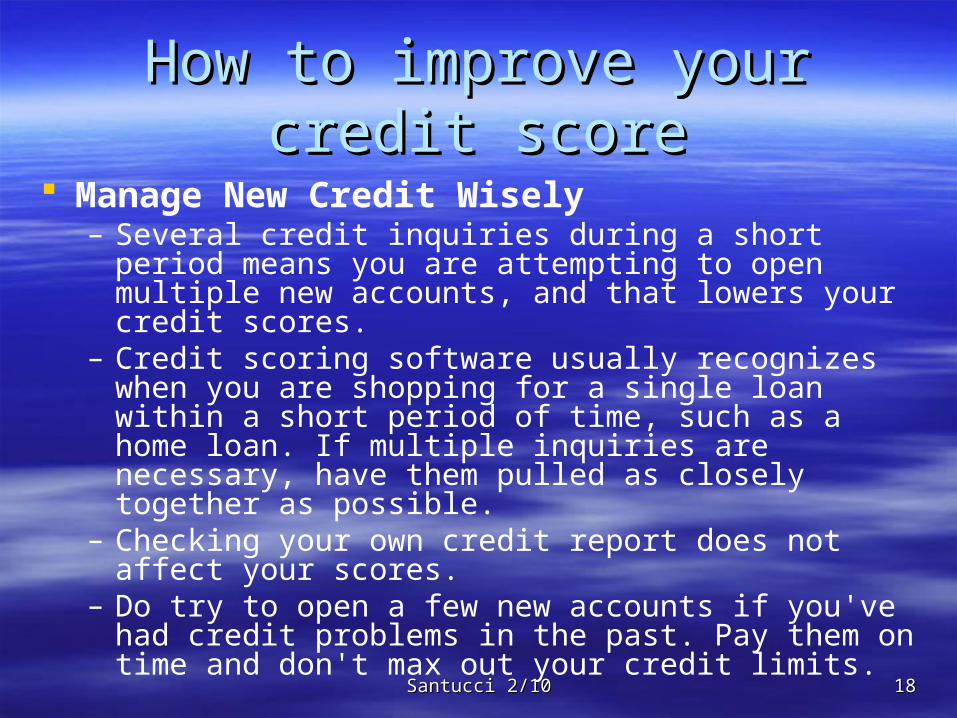

How to improve your credit scoreHow to improve your credit score

Improve Your Payment History– Always pay your bills on time. Late payments play a major role in

driving down your score. – If you have past-due bills now, get current and stay that way.

Keep Debt to a Minimum: no more than 30% of available credit– Keep your credit card balances low. High debt-to-credit-limit ratios

drive your scores down. – Pay off debt, don't move it around. Owing the same amounts, but

having fewer open accounts, can lower your score if you max out the accounts involved.

– Don't close unused accounts, because zero balance might help your score.

– Don't open new accounts that you don't need as a quickie approach to altering your debt-to-credit-limit ratios. That can lower your score.

Santucci 2/10Santucci 2/10 1818

How to improve your credit scoreHow to improve your credit score

Manage New Credit Wisely– Several credit inquiries during a short period means you

are attempting to open multiple new accounts, and that lowers your credit scores.

– Credit scoring software usually recognizes when you are shopping for a single loan within a short period of time, such as a home loan. If multiple inquiries are necessary, have them pulled as closely together as possible.

– Checking your own credit report does not affect your scores.

– Do try to open a few new accounts if you've had credit problems in the past. Pay them on time and don't max out your credit limits.

Santucci 2/10Santucci 2/10 1919

Santucci 2/10Santucci 2/10 2020

How much does college cost?How much does college cost?

More than you thinkMore than you think Rises 6% a yearRises 6% a year

Type of School Without grants With

grants 4 years

Community college (live@home) $4,552 $2,352 $9,408

In-state public university $17,336 $13,336 $53,344

Private university $35,374 $27,674 $110,696

Santucci 2/10Santucci 2/10 2121

How much to save for college?How much to save for college?

$4551 per year, per child, starting at birth$4551 per year, per child, starting at birth $379/month$379/month

Santucci 2/10Santucci 2/10 2222

College savingsCollege savings Coverdale IRA or “education IRA”Coverdale IRA or “education IRA”

– $2,000 per year. Accrues tax free$2,000 per year. Accrues tax free 529 SAVINGS plan529 SAVINGS plan

– Accrues tax freeAccrues tax free– ““State run” plans still allow you to go to any State run” plans still allow you to go to any

collegecollege– Each state is different, but Michigan makes Each state is different, but Michigan makes

$10,000/year free of state taxes (4%) $10,000/year free of state taxes (4%) – If you don’t use it for college you a)pay taxes If you don’t use it for college you a)pay taxes

b)suffer 10% penaltyb)suffer 10% penalty– You can switch beneficiary to the other good kidYou can switch beneficiary to the other good kid

Santucci 2/10Santucci 2/10 2323

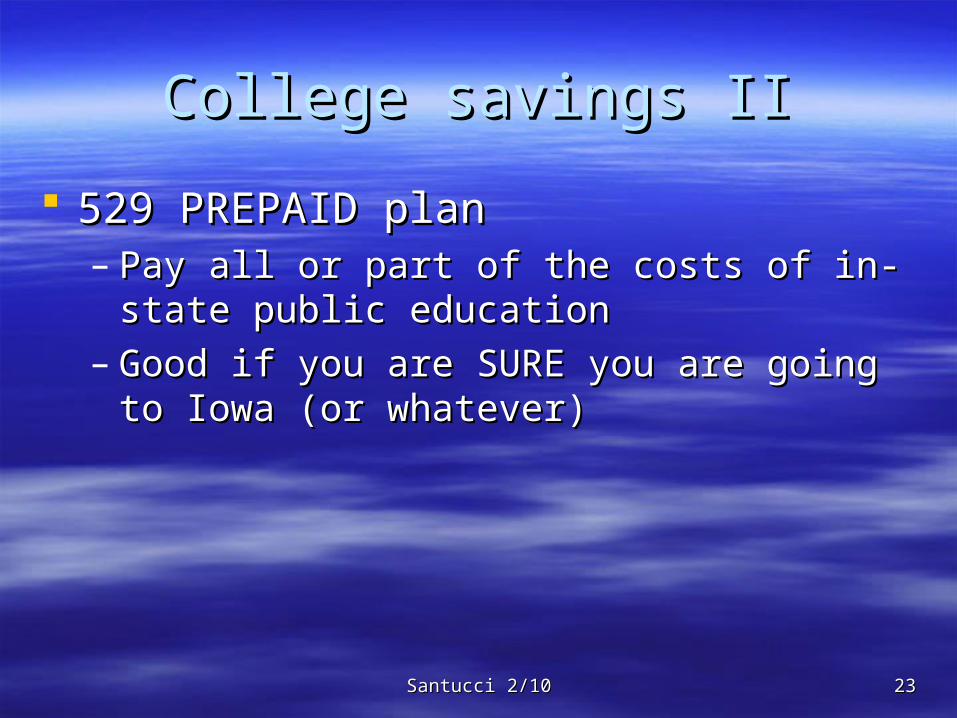

College savings IICollege savings II

529 PREPAID plan529 PREPAID plan– Pay all or part of the costs of in-state public Pay all or part of the costs of in-state public

educationeducation– Good if you are SURE you are going to Iowa (or Good if you are SURE you are going to Iowa (or

whatever)whatever)

Santucci 2/10Santucci 2/10 2424

Santucci 2/10Santucci 2/10 2525

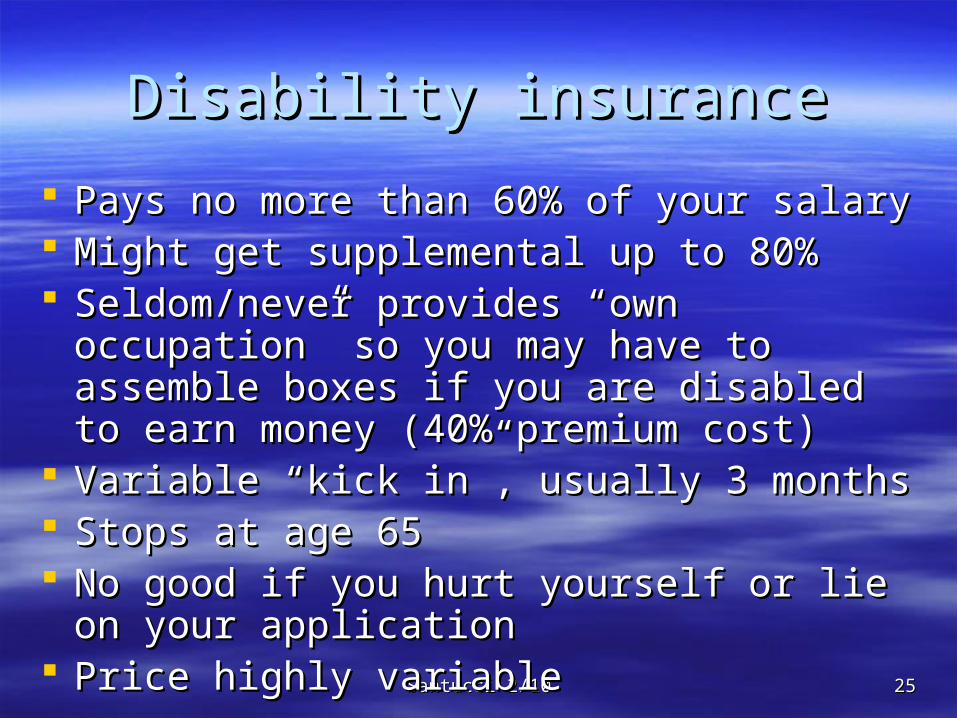

Disability insuranceDisability insurance

Pays no more than 60% of your salaryPays no more than 60% of your salary Might get supplemental up to 80%Might get supplemental up to 80% Seldom/never provides “own occupation” so Seldom/never provides “own occupation” so

you may have to assemble boxes if you are you may have to assemble boxes if you are disabled to earn money (40% premium cost)disabled to earn money (40% premium cost)

Variable “kick in”, usually 3 monthsVariable “kick in”, usually 3 months Stops at age 65Stops at age 65 No good if you hurt yourself or lie on your No good if you hurt yourself or lie on your

applicationapplication Price highly variablePrice highly variable

Santucci 2/10Santucci 2/10 2626

Santucci 2/10Santucci 2/10 2727

Term life insuranceTerm life insurance

CheapestCheapest Look for 20 year fixed cost (costs the same each Look for 20 year fixed cost (costs the same each

year)year) After 20 years, you’ll have enough savings to bury After 20 years, you’ll have enough savings to bury

you, your kids and house MAY be mostly paid for, you, your kids and house MAY be mostly paid for, and your saved but unused retirement may help to and your saved but unused retirement may help to pay costspay costs

Different than “whole life” which is good “forever” Different than “whole life” which is good “forever” and requires yearly payments. Builds up a cash and requires yearly payments. Builds up a cash value which you don’t lose. 30% pure profit to value which you don’t lose. 30% pure profit to company. Advanced info: save for later.company. Advanced info: save for later.

Santucci 2/10Santucci 2/10 2828

How much life insurance do I need?How much life insurance do I need?

DependsDepends To get $5,000 a month for 20 years is To get $5,000 a month for 20 years is

$1,000,000 of insurance$1,000,000 of insurance

Santucci 2/10Santucci 2/10 2929

Santucci 2/10Santucci 2/10 3030

What is umbrella insuranceWhat is umbrella insurance

Remember you are a rich doctorRemember you are a rich doctor A type of liability insurance policy that A type of liability insurance policy that

covers EXTRA on car accidents, and home covers EXTRA on car accidents, and home accidentsaccidents

Provides an “umbrella” of often $1 million + Provides an “umbrella” of often $1 million + against your neighbor slipping on your against your neighbor slipping on your drivewaydriveway

Not expensiveNot expensive

Santucci 2/10Santucci 2/10 3131

Santucci 2/10Santucci 2/10 3232

Emergency FundEmergency Fund

Variable amountVariable amount Cash (can put into Certificate of Deposit)Cash (can put into Certificate of Deposit) 3-4 months of living expenses3-4 months of living expenses 6 months if you have kids6 months if you have kids

Santucci 2/10Santucci 2/10 3333

Santucci 2/10Santucci 2/10 3434

Children as employeesChildren as employees

Can gift each kid $11,000 per (you and your Can gift each kid $11,000 per (you and your spouse can each gift) tax freespouse can each gift) tax free

If they are believably old enough, you can If they are believably old enough, you can employ them for as much as you can justify employ them for as much as you can justify to the IRS ($6,000 a year for teens?)to the IRS ($6,000 a year for teens?)

UGMA (uniform gift to minors act)UGMA (uniform gift to minors act) They can use this to double-pay into college They can use this to double-pay into college

funds, but at their low 15% tax rate not your funds, but at their low 15% tax rate not your high tax rate high tax rate

Santucci 2/10Santucci 2/10 3535

Santucci 2/10Santucci 2/10 3636

Random rules to followRandom rules to follow

If you can lower your interest rate by 1% with If you can lower your interest rate by 1% with refinance of your home, do it.refinance of your home, do it.

Spend no more than 250% of your income on a Spend no more than 250% of your income on a home. Downpayment 20%. (Max 28% of gross home. Downpayment 20%. (Max 28% of gross income= housing payment)income= housing payment)

DO NOT INFLATE YOUR SPENDING AS YOUR DO NOT INFLATE YOUR SPENDING AS YOUR SALARY INFLATESSALARY INFLATES

Maximize your 401k (often matched) when offeredMaximize your 401k (often matched) when offered Save at least 10% of salary when starting out, Save at least 10% of salary when starting out,

much more latermuch more later Buy used cars: new car = 30% loss of value in the Buy used cars: new car = 30% loss of value in the

first yearfirst year

Santucci 2/10Santucci 2/10 3737

Santucci 2/10Santucci 2/10 3838

Stuff you need to know laterStuff you need to know later

Estate taxesEstate taxes You’ll have to optimize your estate LATERYou’ll have to optimize your estate LATER Up to 46% Up to 46% Once in a lifetime $1 million dollar exclusion Once in a lifetime $1 million dollar exclusion

(not totally accurate but will do)(not totally accurate but will do)

Santucci 2/10Santucci 2/10 3939

Santucci 2/10Santucci 2/10 4040

Stuff you need nowStuff you need now

An insurance agentAn insurance agent A financial plannerA financial planner

– If only for your education at this timeIf only for your education at this time– They’ll calculate how much insurance you need, They’ll calculate how much insurance you need,

how much you need to save for college and how much you need to save for college and retirementretirement

Santucci 2/10Santucci 2/10 4141

rulesrules Eliminate debtEliminate debt Create an emergency fundCreate an emergency fund Mind your credit scoreMind your credit score Save $5,000 a year in traditional IRA nowSave $5,000 a year in traditional IRA now Buy enough life insurance to bury yourself, OR keep you Buy enough life insurance to bury yourself, OR keep you

family secure “forever”family secure “forever” Buy disability insuranceBuy disability insurance Consider “umbrella insurance”Consider “umbrella insurance” Start saving for collegeStart saving for college Forget social securityForget social security Forget using your home equity as retirement moneyForget using your home equity as retirement money Later when you are rich, optimize your estate tax burdenLater when you are rich, optimize your estate tax burden Live below your meansLive below your means