sap® financial consolidation 10.0 starter …sapidp/012002523100002462822015e/fc...list of...

TRANSCRIPT

List of Financial Accounts

1

SAP® FINANCIAL CONSOLIDATION 10.0

STARTER KIT FOR IFRS SP7 Simplified Configuration Description (Appendix)

2

Copyright © 2015 SAP® BusinessObjects™. All rights reserved. SAP BusinessObjects and its logos, BusinessObjects, Crystal Reports®, SAP BusinessObjects Rapid Mart™, SAP BusinessObjects Data Insight™, SAP BusinessObjects Desktop Intelligence™, SAP BusinessObjects Rapid Marts®, SAP BusinessObjects Watchlist Security™, SAP BusinessObjects Web Intelligence®, and Xcelsius® are trademarks or registered trademarks of Business Objects, an SAP company and/or affiliated companies in the United States and/or other countries. SAP® is a registered trademark of SAP AG in Germany and/or other countries. All other names mentioned herein may be trademarks of their respective owners.

Legal No part of this starter kit may be reproduced or transmitted in any form or for any purpose Disclaimer without the express permission of SAP AG. The information contained herein may be

changed without prior notice. Some software products marketed by SAP AG and its distributors contain proprietary software components of other software vendors. The information in this starter kit is proprietary to SAP. No part of this starter kit’s content may be reproduced, copied, or transmitted in any form or for any purpose without the express prior permission of SAP AG. This starter kit is not subject to your license agreement or any other agreement with SAP. This starter kit contains only intended content, and pre-customized elements of the SAP® product and is not intended to be binding upon SAP to any particular course of business, product strategy, and/or development. Please note that this starter kit is subject to change and may be changed by SAP at any time without notice. SAP assumes no responsibility for errors or omissions in this starter kit. SAP does not warrant the accuracy or completeness of the information, text, pre-configured elements, or other items contained within this starter kit. SAP DOES NOT PROVIDE LEGAL, FINANCIAL OR ACCOUNTING ADVISE OR SERVICES. SAP WILL NOT BE RESPONSIBLE FOR ANY NONCOMPLIANCE OR ADVERSE RESULTS AS A RESULT OF YOUR USE OR RELIANCE ON THE STARTER KIT. THIS STARTER KIT IS PROVIDED WITHOUT A WARRANTY OF ANY KIND, EITHER EXPRESS OR IMPLIED, INCLUDING BUT NOT LIMITED TO THE IMPLIED WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE, OR NON-INFRINGEMENT. SAP SHALL HAVE NO LIABILITY FOR DAMAGES OF ANY KIND INCLUDING WITHOUT LIMITATION DIRECT, SPECIAL, INDIRECT, OR CONSEQUENTIAL DAMAGES THAT MAY RESULT FROM THE USE OF THIS STARTER KIT. THIS LIMITATION SHALL NOT APPLY IN CASES OF INTENT OR GROSS NEGLIGENCE. The statutory liability for personal injury and defective products (under German law) is not affected. SAP has no control over the use of pre-customized elements contained in this starter kit and does not endorse your use of the starter kit nor provide any warranty whatsoever relating to third-party use of the starter kit.

List of Financial Accounts

3

Contents

Chapter 1 List of Financial Accounts ..................................................................................................... 4

Assets ....................................................................................................................................... 4

Equity and Liabilities ................................................................................................................. 7

Income Statement ..................................................................................................................... 9

Chapter 2 List of Package Schedules ................................................................................................... 11

Chapter 3 List of Accounting Flows ..................................................................................................... 13

Chapter 4 Package Controls .................................................................................................................. 14

Chapter 5 List of Audit IDs .................................................................................................................... 19

Chapter 6 Consolidation Journal Entries ............................................................................................. 21

Form 1 – Elimination of Intra-group Transactions ................................................................... 22

Form 2 – Elimination of Internal Provisions ............................................................................ 23

Form 3 – Elimination of Internal Dividends ............................................................................. 24

Form 4 – Elimination of Internal Capital Gains or Losses ...................................................... 25

Form 5 – Non-Controlling Interests ......................................................................................... 26

Form 6 – Elimination of Investments ...................................................................................... 27

Form 7 – Currency Translation Adjustment ............................................................................ 28

Form 8 – Goodwill and Bargain Purchase .............................................................................. 29

Chapter 7 List of Retrieval Schedules .................................................................................................. 30

C-0 Home Pages and Summary Reports ............................................................................... 30

C-1 Annual Report .................................................................................................................. 30

C-2 Analysis ............................................................................................................................ 31

C-3 Accounting Reports .......................................................................................................... 32

C-4 Control Reports ................................................................................................................ 32

C-5 IFRS Adoption .................................................................................................................. 34

List of Financial Accounts

4

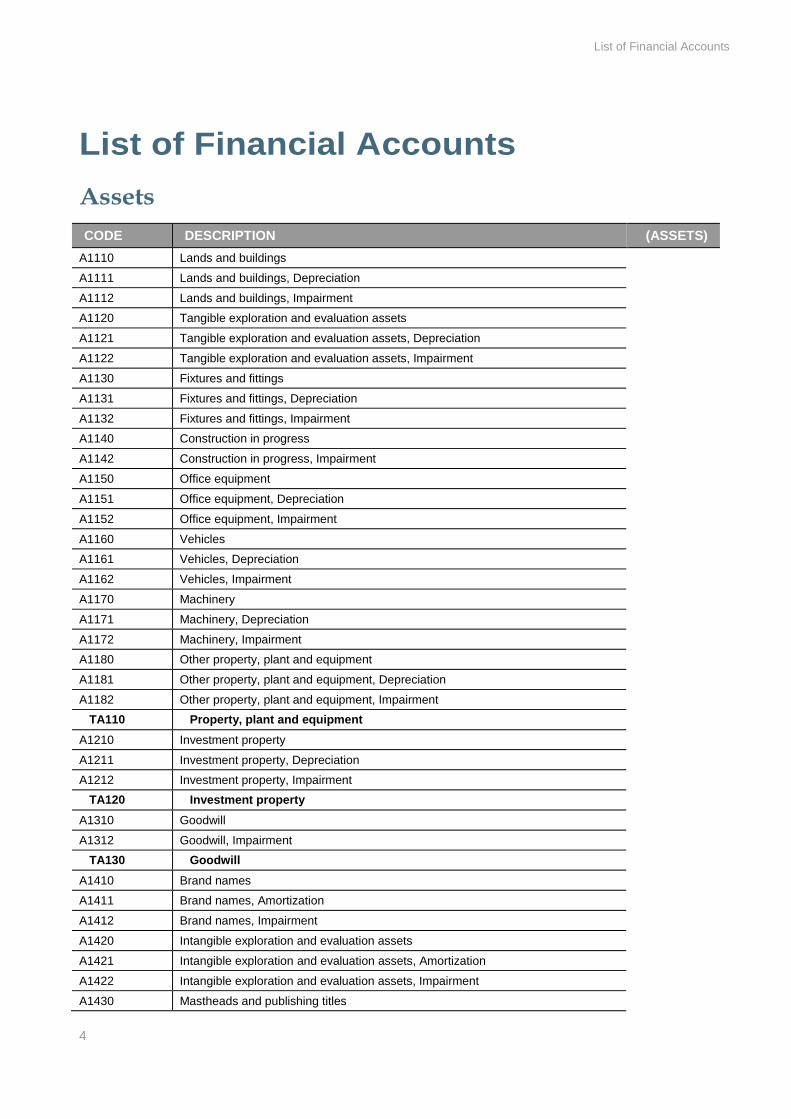

List of Financial Accounts

Assets

CODE DESCRIPTION (ASSETS)

A1110 Lands and buildings

A1111 Lands and buildings, Depreciation

A1112 Lands and buildings, Impairment

A1120 Tangible exploration and evaluation assets

A1121 Tangible exploration and evaluation assets, Depreciation

A1122 Tangible exploration and evaluation assets, Impairment

A1130 Fixtures and fittings

A1131 Fixtures and fittings, Depreciation

A1132 Fixtures and fittings, Impairment

A1140 Construction in progress

A1142 Construction in progress, Impairment

A1150 Office equipment

A1151 Office equipment, Depreciation

A1152 Office equipment, Impairment

A1160 Vehicles

A1161 Vehicles, Depreciation

A1162 Vehicles, Impairment

A1170 Machinery

A1171 Machinery, Depreciation

A1172 Machinery, Impairment

A1180 Other property, plant and equipment

A1181 Other property, plant and equipment, Depreciation

A1182 Other property, plant and equipment, Impairment

TA110 Property, plant and equipment

A1210 Investment property

A1211 Investment property, Depreciation

A1212 Investment property, Impairment

TA120 Investment property

A1310 Goodwill

A1312 Goodwill, Impairment

TA130 Goodwill

A1410 Brand names

A1411 Brand names, Amortization

A1412 Brand names, Impairment

A1420 Intangible exploration and evaluation assets

A1421 Intangible exploration and evaluation assets, Amortization

A1422 Intangible exploration and evaluation assets, Impairment

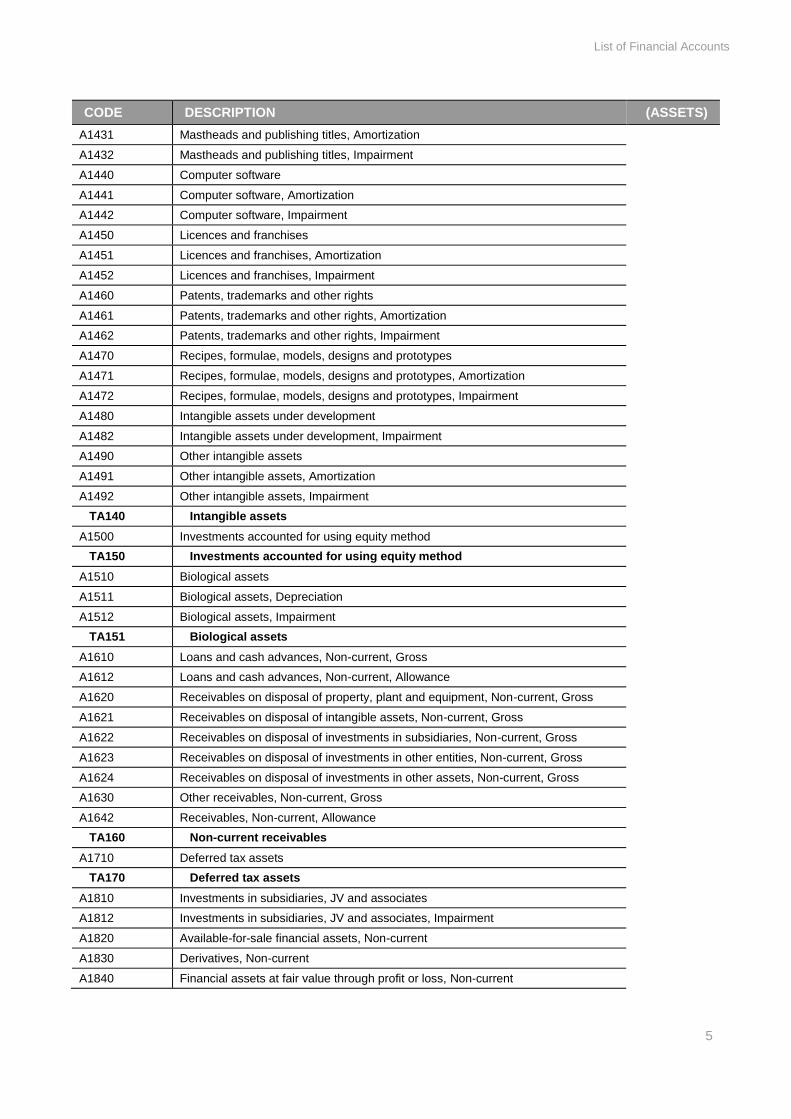

A1430 Mastheads and publishing titles

List of Financial Accounts

5

CODE DESCRIPTION (ASSETS)

A1431 Mastheads and publishing titles, Amortization

A1432 Mastheads and publishing titles, Impairment

A1440 Computer software

A1441 Computer software, Amortization

A1442 Computer software, Impairment

A1450 Licences and franchises

A1451 Licences and franchises, Amortization

A1452 Licences and franchises, Impairment

A1460 Patents, trademarks and other rights

A1461 Patents, trademarks and other rights, Amortization

A1462 Patents, trademarks and other rights, Impairment

A1470 Recipes, formulae, models, designs and prototypes

A1471 Recipes, formulae, models, designs and prototypes, Amortization

A1472 Recipes, formulae, models, designs and prototypes, Impairment

A1480 Intangible assets under development

A1482 Intangible assets under development, Impairment

A1490 Other intangible assets

A1491 Other intangible assets, Amortization

A1492 Other intangible assets, Impairment

TA140 Intangible assets

A1500 Investments accounted for using equity method

TA150 Investments accounted for using equity method

A1510 Biological assets

A1511 Biological assets, Depreciation

A1512 Biological assets, Impairment

TA151 Biological assets

A1610 Loans and cash advances, Non-current, Gross

A1612 Loans and cash advances, Non-current, Allowance

A1620 Receivables on disposal of property, plant and equipment, Non-current, Gross

A1621 Receivables on disposal of intangible assets, Non-current, Gross

A1622 Receivables on disposal of investments in subsidiaries, Non-current, Gross

A1623 Receivables on disposal of investments in other entities, Non-current, Gross

A1624 Receivables on disposal of investments in other assets, Non-current, Gross

A1630 Other receivables, Non-current, Gross

A1642 Receivables, Non-current, Allowance

TA160 Non-current receivables

A1710 Deferred tax assets

TA170 Deferred tax assets

A1810 Investments in subsidiaries, JV and associates

A1812 Investments in subsidiaries, JV and associates, Impairment

A1820 Available-for-sale financial assets, Non-current

A1830 Derivatives, Non-current

A1840 Financial assets at fair value through profit or loss, Non-current

List of Financial Accounts

6

CODE DESCRIPTION (ASSETS)

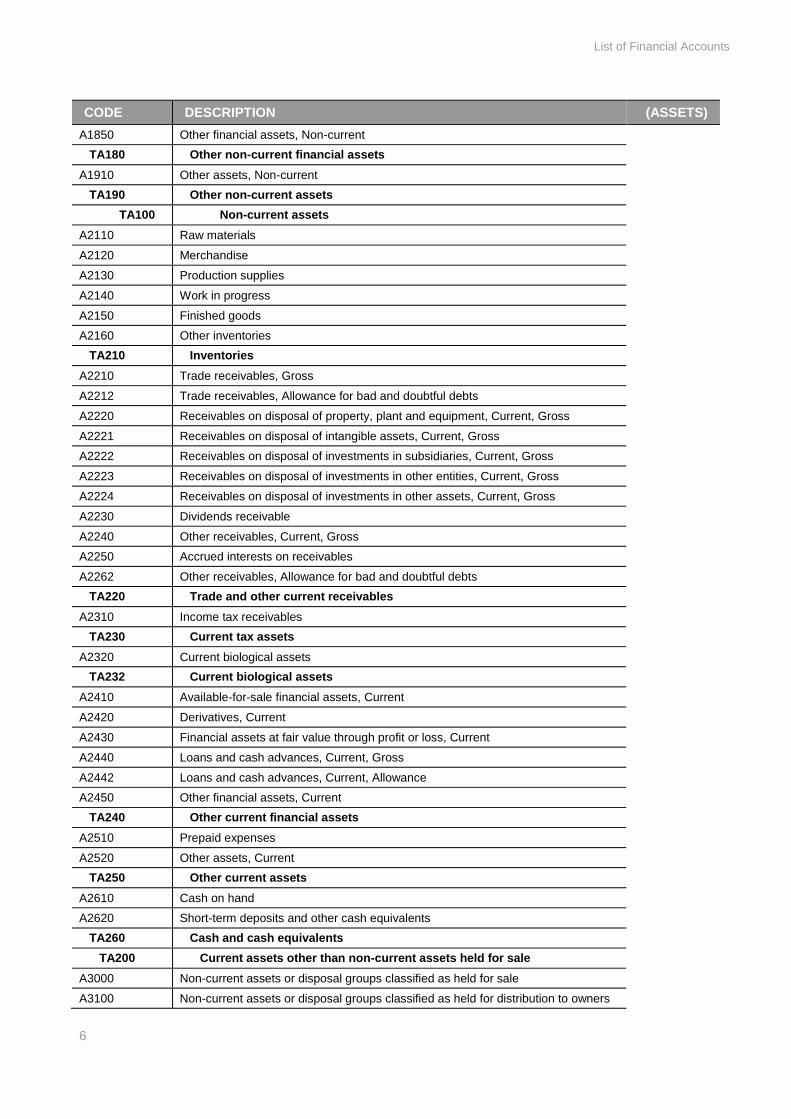

A1850 Other financial assets, Non-current

TA180 Other non-current financial assets

A1910 Other assets, Non-current

TA190 Other non-current assets

TA100 Non-current assets

A2110 Raw materials

A2120 Merchandise

A2130 Production supplies

A2140 Work in progress

A2150 Finished goods

A2160 Other inventories

TA210 Inventories

A2210 Trade receivables, Gross

A2212 Trade receivables, Allowance for bad and doubtful debts

A2220 Receivables on disposal of property, plant and equipment, Current, Gross

A2221 Receivables on disposal of intangible assets, Current, Gross

A2222 Receivables on disposal of investments in subsidiaries, Current, Gross

A2223 Receivables on disposal of investments in other entities, Current, Gross

A2224 Receivables on disposal of investments in other assets, Current, Gross

A2230 Dividends receivable

A2240 Other receivables, Current, Gross

A2250 Accrued interests on receivables

A2262 Other receivables, Allowance for bad and doubtful debts

TA220 Trade and other current receivables

A2310 Income tax receivables

TA230 Current tax assets

A2320 Current biological assets

TA232 Current biological assets

A2410 Available-for-sale financial assets, Current

A2420 Derivatives, Current

A2430 Financial assets at fair value through profit or loss, Current

A2440 Loans and cash advances, Current, Gross

A2442 Loans and cash advances, Current, Allowance

A2450 Other financial assets, Current

TA240 Other current financial assets

A2510 Prepaid expenses

A2520 Other assets, Current

TA250 Other current assets

A2610 Cash on hand

A2620 Short-term deposits and other cash equivalents

TA260 Cash and cash equivalents

TA200 Current assets other than non-current assets held for sale

A3000 Non-current assets or disposal groups classified as held for sale

A3100 Non-current assets or disposal groups classified as held for distribution to owners

List of Financial Accounts

7

CODE DESCRIPTION (ASSETS)

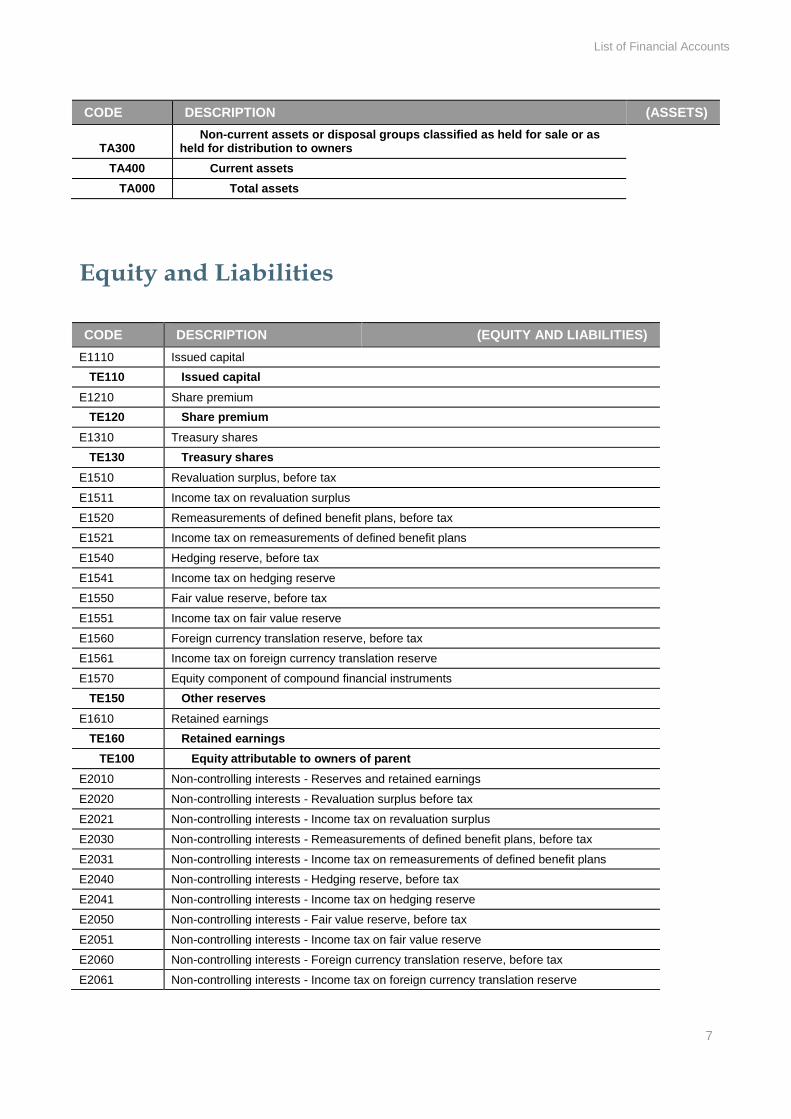

TA300 Non-current assets or disposal groups classified as held for sale or as held for distribution to owners

TA400 Current assets

TA000 Total assets

Equity and Liabilities

CODE DESCRIPTION (EQUITY AND LIABILITIES)

E1110 Issued capital

TE110 Issued capital

E1210 Share premium

TE120 Share premium

E1310 Treasury shares

TE130 Treasury shares

E1510 Revaluation surplus, before tax

E1511 Income tax on revaluation surplus

E1520 Remeasurements of defined benefit plans, before tax

E1521 Income tax on remeasurements of defined benefit plans

E1540 Hedging reserve, before tax

E1541 Income tax on hedging reserve

E1550 Fair value reserve, before tax

E1551 Income tax on fair value reserve

E1560 Foreign currency translation reserve, before tax

E1561 Income tax on foreign currency translation reserve

E1570 Equity component of compound financial instruments

TE150 Other reserves

E1610 Retained earnings

TE160 Retained earnings

TE100 Equity attributable to owners of parent

E2010 Non-controlling interests - Reserves and retained earnings

E2020 Non-controlling interests - Revaluation surplus before tax

E2021 Non-controlling interests - Income tax on revaluation surplus

E2030 Non-controlling interests - Remeasurements of defined benefit plans, before tax

E2031 Non-controlling interests - Income tax on remeasurements of defined benefit plans

E2040 Non-controlling interests - Hedging reserve, before tax

E2041 Non-controlling interests - Income tax on hedging reserve

E2050 Non-controlling interests - Fair value reserve, before tax

E2051 Non-controlling interests - Income tax on fair value reserve

E2060 Non-controlling interests - Foreign currency translation reserve, before tax

E2061 Non-controlling interests - Income tax on foreign currency translation reserve

List of Financial Accounts

8

CODE DESCRIPTION (EQUITY AND LIABILITIES)

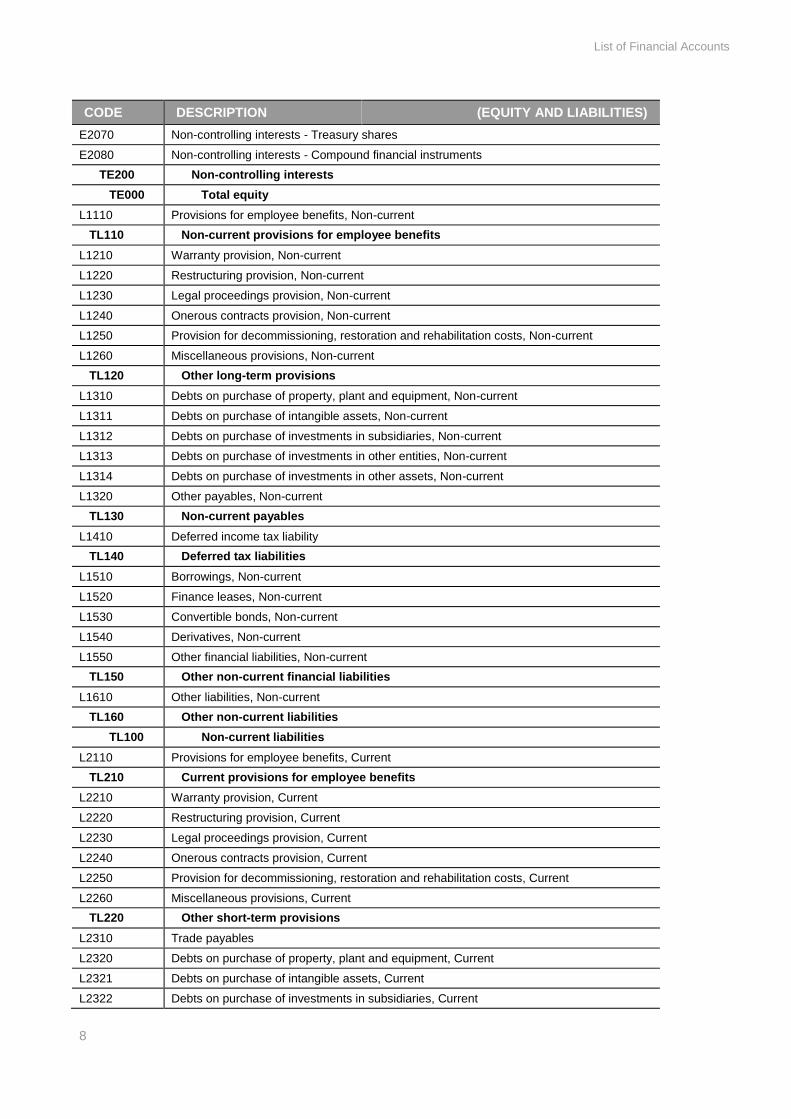

E2070 Non-controlling interests - Treasury shares

E2080 Non-controlling interests - Compound financial instruments

TE200 Non-controlling interests

TE000 Total equity

L1110 Provisions for employee benefits, Non-current

TL110 Non-current provisions for employee benefits

L1210 Warranty provision, Non-current

L1220 Restructuring provision, Non-current

L1230 Legal proceedings provision, Non-current

L1240 Onerous contracts provision, Non-current

L1250 Provision for decommissioning, restoration and rehabilitation costs, Non-current

L1260 Miscellaneous provisions, Non-current

TL120 Other long-term provisions

L1310 Debts on purchase of property, plant and equipment, Non-current

L1311 Debts on purchase of intangible assets, Non-current

L1312 Debts on purchase of investments in subsidiaries, Non-current

L1313 Debts on purchase of investments in other entities, Non-current

L1314 Debts on purchase of investments in other assets, Non-current

L1320 Other payables, Non-current

TL130 Non-current payables

L1410 Deferred income tax liability

TL140 Deferred tax liabilities

L1510 Borrowings, Non-current

L1520 Finance leases, Non-current

L1530 Convertible bonds, Non-current

L1540 Derivatives, Non-current

L1550 Other financial liabilities, Non-current

TL150 Other non-current financial liabilities

L1610 Other liabilities, Non-current

TL160 Other non-current liabilities

TL100 Non-current liabilities

L2110 Provisions for employee benefits, Current

TL210 Current provisions for employee benefits

L2210 Warranty provision, Current

L2220 Restructuring provision, Current

L2230 Legal proceedings provision, Current

L2240 Onerous contracts provision, Current

L2250 Provision for decommissioning, restoration and rehabilitation costs, Current

L2260 Miscellaneous provisions, Current

TL220 Other short-term provisions

L2310 Trade payables

L2320 Debts on purchase of property, plant and equipment, Current

L2321 Debts on purchase of intangible assets, Current

L2322 Debts on purchase of investments in subsidiaries, Current

List of Financial Accounts

9

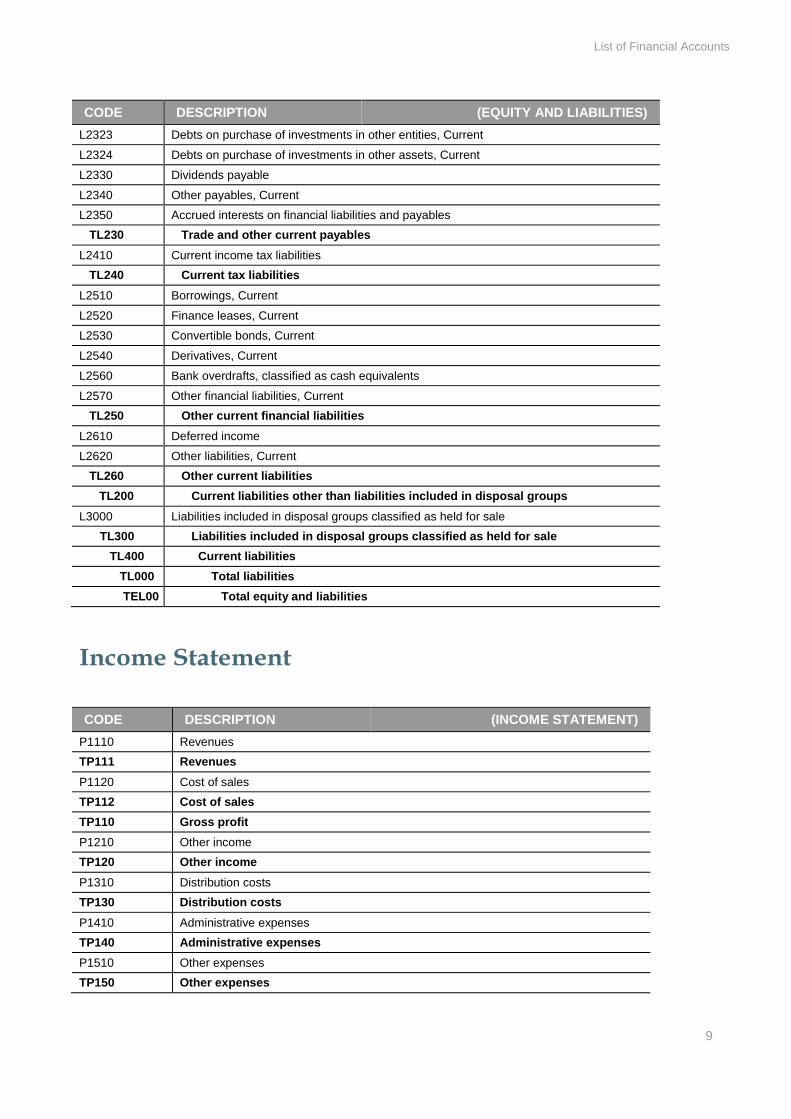

CODE DESCRIPTION (EQUITY AND LIABILITIES)

L2323 Debts on purchase of investments in other entities, Current

L2324 Debts on purchase of investments in other assets, Current

L2330 Dividends payable

L2340 Other payables, Current

L2350 Accrued interests on financial liabilities and payables

TL230 Trade and other current payables

L2410 Current income tax liabilities

TL240 Current tax liabilities

L2510 Borrowings, Current

L2520 Finance leases, Current

L2530 Convertible bonds, Current

L2540 Derivatives, Current

L2560 Bank overdrafts, classified as cash equivalents

L2570 Other financial liabilities, Current

TL250 Other current financial liabilities

L2610 Deferred income

L2620 Other liabilities, Current

TL260 Other current liabilities

TL200 Current liabilities other than liabilities included in disposal groups

L3000 Liabilities included in disposal groups classified as held for sale

TL300 Liabilities included in disposal groups classified as held for sale

TL400 Current liabilities

TL000 Total liabilities

TEL00 Total equity and liabilities

Income Statement

CODE DESCRIPTION (INCOME STATEMENT)

P1110 Revenues

TP111 Revenues

P1120 Cost of sales

TP112 Cost of sales

TP110 Gross profit

P1210 Other income

TP120 Other income

P1310 Distribution costs

TP130 Distribution costs

P1410 Administrative expenses

TP140 Administrative expenses

P1510 Other expenses

TP150 Other expenses

List of Financial Accounts

10

CODE DESCRIPTION (INCOME STATEMENT)

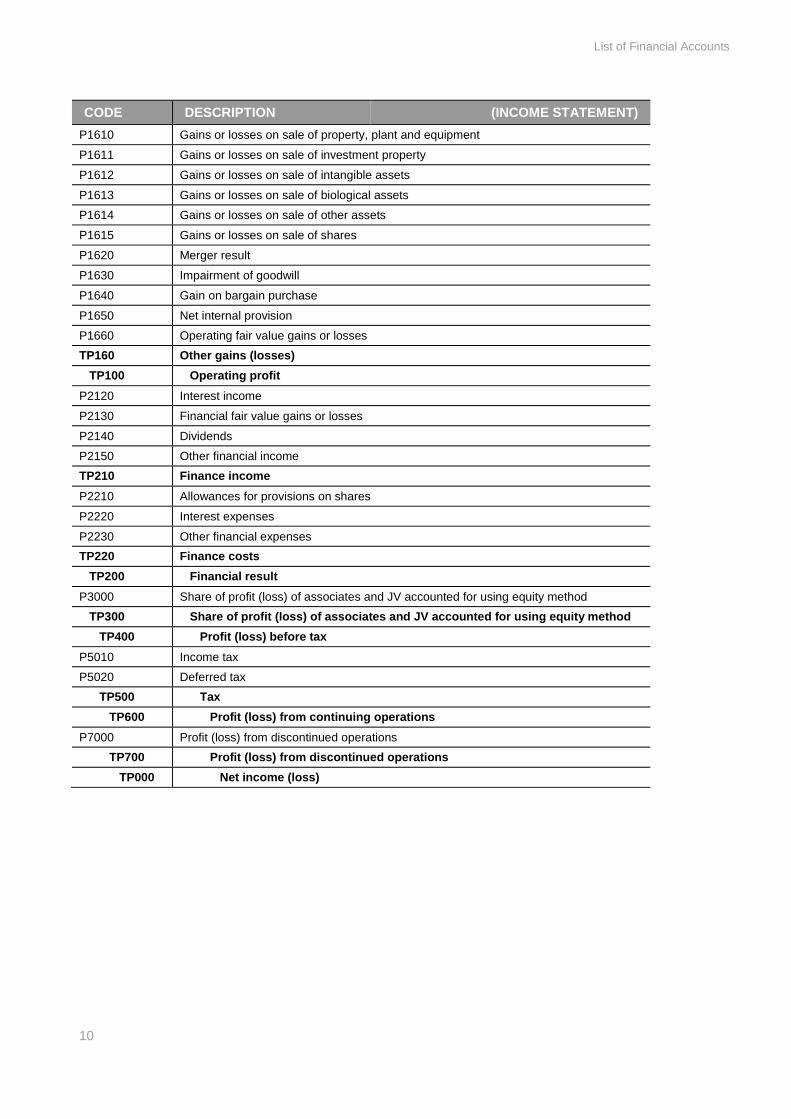

P1610 Gains or losses on sale of property, plant and equipment

P1611 Gains or losses on sale of investment property

P1612 Gains or losses on sale of intangible assets

P1613 Gains or losses on sale of biological assets

P1614 Gains or losses on sale of other assets

P1615 Gains or losses on sale of shares

P1620 Merger result

P1630 Impairment of goodwill

P1640 Gain on bargain purchase

P1650 Net internal provision

P1660 Operating fair value gains or losses

TP160 Other gains (losses)

TP100 Operating profit

P2120 Interest income

P2130 Financial fair value gains or losses

P2140 Dividends

P2150 Other financial income

TP210 Finance income

P2210 Allowances for provisions on shares

P2220 Interest expenses

P2230 Other financial expenses

TP220 Finance costs

TP200 Financial result

P3000 Share of profit (loss) of associates and JV accounted for using equity method

TP300 Share of profit (loss) of associates and JV accounted for using equity method

TP400 Profit (loss) before tax

P5010 Income tax

P5020 Deferred tax

TP500 Tax

TP600 Profit (loss) from continuing operations

P7000 Profit (loss) from discontinued operations

TP700 Profit (loss) from discontinued operations

TP000 Net income (loss)

List of Package Schedules

11

List of Package Schedules

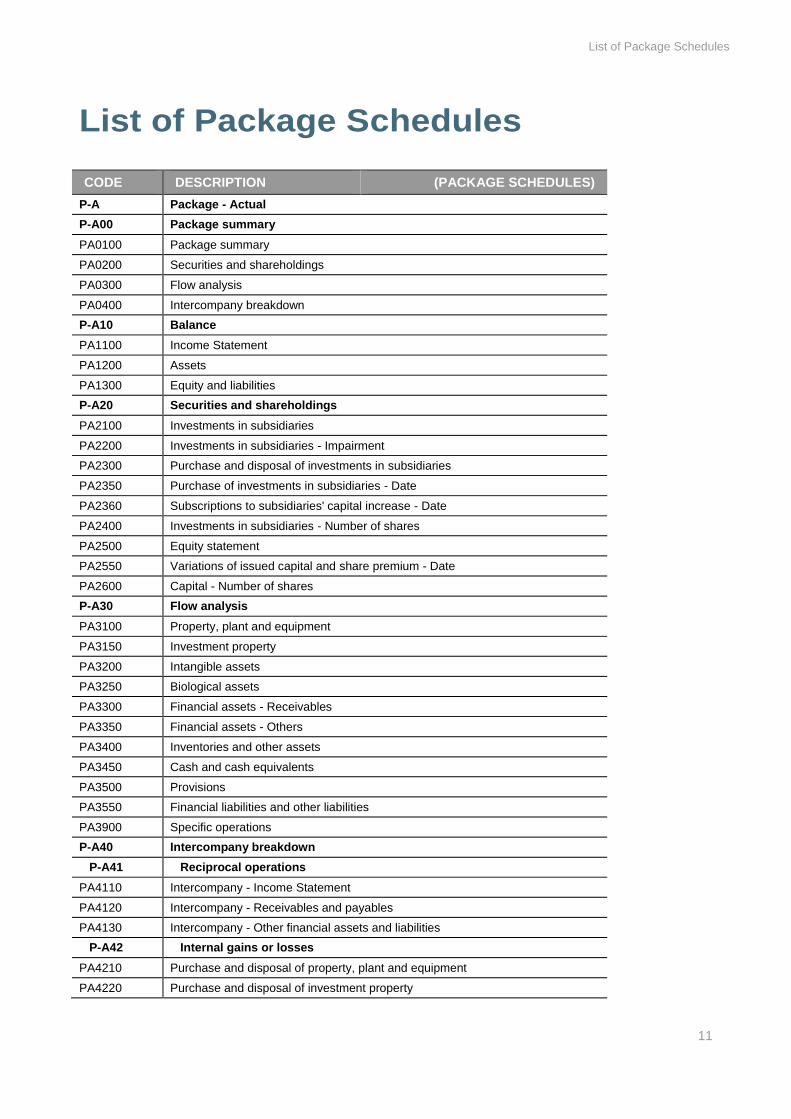

CODE DESCRIPTION (PACKAGE SCHEDULES)

P-A Package - Actual

P-A00 Package summary

PA0100 Package summary

PA0200 Securities and shareholdings

PA0300 Flow analysis

PA0400 Intercompany breakdown

P-A10 Balance

PA1100 Income Statement

PA1200 Assets

PA1300 Equity and liabilities

P-A20 Securities and shareholdings

PA2100 Investments in subsidiaries

PA2200 Investments in subsidiaries - Impairment

PA2300 Purchase and disposal of investments in subsidiaries

PA2350 Purchase of investments in subsidiaries - Date

PA2360 Subscriptions to subsidiaries' capital increase - Date

PA2400 Investments in subsidiaries - Number of shares

PA2500 Equity statement

PA2550 Variations of issued capital and share premium - Date

PA2600 Capital - Number of shares

P-A30 Flow analysis

PA3100 Property, plant and equipment

PA3150 Investment property

PA3200 Intangible assets

PA3250 Biological assets

PA3300 Financial assets - Receivables

PA3350 Financial assets - Others

PA3400 Inventories and other assets

PA3450 Cash and cash equivalents

PA3500 Provisions

PA3550 Financial liabilities and other liabilities

PA3900 Specific operations

P-A40 Intercompany breakdown

P-A41 Reciprocal operations

PA4110 Intercompany - Income Statement

PA4120 Intercompany - Receivables and payables

PA4130 Intercompany - Other financial assets and liabilities

P-A42 Internal gains or losses

PA4210 Purchase and disposal of property, plant and equipment

PA4220 Purchase and disposal of investment property

List of Package Schedules

12

CODE DESCRIPTION (PACKAGE SCHEDULES)

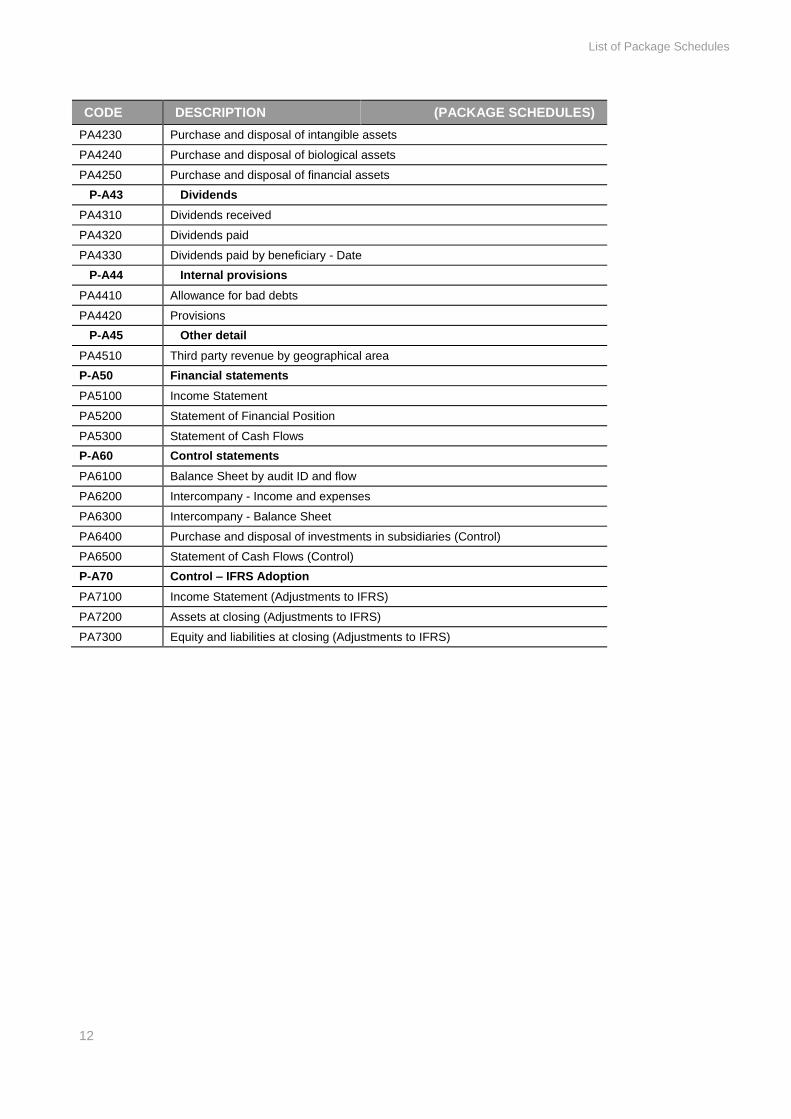

PA4230 Purchase and disposal of intangible assets

PA4240 Purchase and disposal of biological assets

PA4250 Purchase and disposal of financial assets

P-A43 Dividends

PA4310 Dividends received

PA4320 Dividends paid

PA4330 Dividends paid by beneficiary - Date

P-A44 Internal provisions

PA4410 Allowance for bad debts

PA4420 Provisions

P-A45 Other detail

PA4510 Third party revenue by geographical area

P-A50 Financial statements

PA5100 Income Statement

PA5200 Statement of Financial Position

PA5300 Statement of Cash Flows

P-A60 Control statements

PA6100 Balance Sheet by audit ID and flow

PA6200 Intercompany - Income and expenses

PA6300 Intercompany - Balance Sheet

PA6400 Purchase and disposal of investments in subsidiaries (Control)

PA6500 Statement of Cash Flows (Control)

P-A70 Control – IFRS Adoption

PA7100 Income Statement (Adjustments to IFRS)

PA7200 Assets at closing (Adjustments to IFRS)

PA7300 Equity and liabilities at closing (Adjustments to IFRS)

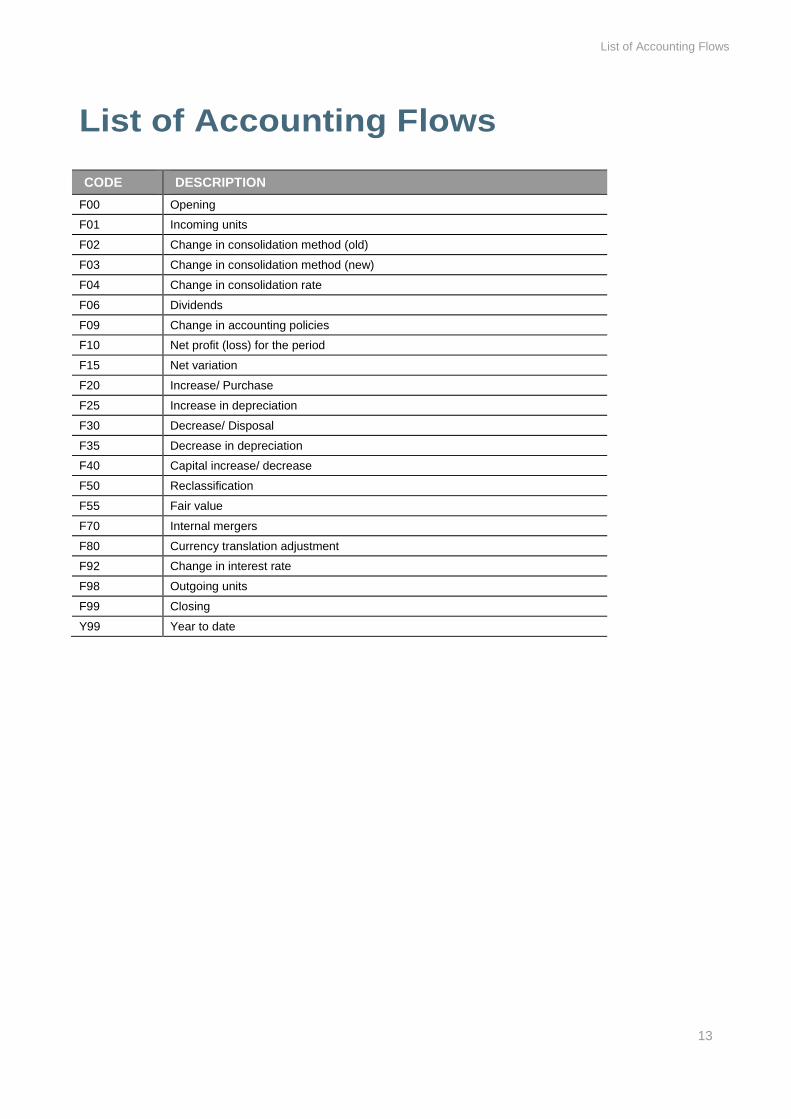

List of Accounting Flows

13

List of Accounting Flows

CODE DESCRIPTION

F00 Opening

F01 Incoming units

F02 Change in consolidation method (old)

F03 Change in consolidation method (new)

F04 Change in consolidation rate

F06 Dividends

F09 Change in accounting policies

F10 Net profit (loss) for the period

F15 Net variation

F20 Increase/ Purchase

F25 Increase in depreciation

F30 Decrease/ Disposal

F35 Decrease in depreciation

F40 Capital increase/ decrease

F50 Reclassification

F55 Fair value

F70 Internal mergers

F80 Currency translation adjustment

F92 Change in interest rate

F98 Outgoing units

F99 Closing

Y99 Year to date

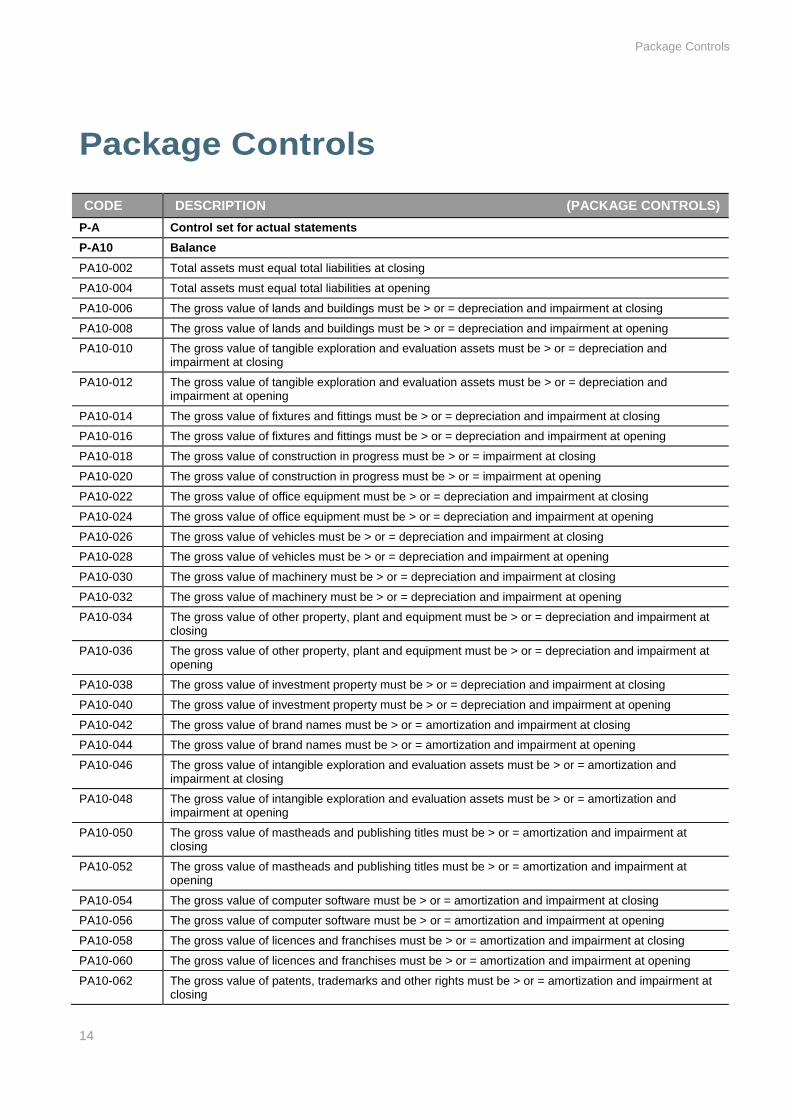

Package Controls

14

Package Controls

CODE DESCRIPTION (PACKAGE CONTROLS)

P-A Control set for actual statements

P-A10 Balance

PA10-002 Total assets must equal total liabilities at closing

PA10-004 Total assets must equal total liabilities at opening

PA10-006 The gross value of lands and buildings must be > or = depreciation and impairment at closing

PA10-008 The gross value of lands and buildings must be > or = depreciation and impairment at opening

PA10-010 The gross value of tangible exploration and evaluation assets must be > or = depreciation and impairment at closing

PA10-012 The gross value of tangible exploration and evaluation assets must be > or = depreciation and impairment at opening

PA10-014 The gross value of fixtures and fittings must be > or = depreciation and impairment at closing

PA10-016 The gross value of fixtures and fittings must be > or = depreciation and impairment at opening

PA10-018 The gross value of construction in progress must be > or = impairment at closing

PA10-020 The gross value of construction in progress must be > or = impairment at opening

PA10-022 The gross value of office equipment must be > or = depreciation and impairment at closing

PA10-024 The gross value of office equipment must be > or = depreciation and impairment at opening

PA10-026 The gross value of vehicles must be > or = depreciation and impairment at closing

PA10-028 The gross value of vehicles must be > or = depreciation and impairment at opening

PA10-030 The gross value of machinery must be > or = depreciation and impairment at closing

PA10-032 The gross value of machinery must be > or = depreciation and impairment at opening

PA10-034 The gross value of other property, plant and equipment must be > or = depreciation and impairment at closing

PA10-036 The gross value of other property, plant and equipment must be > or = depreciation and impairment at opening

PA10-038 The gross value of investment property must be > or = depreciation and impairment at closing

PA10-040 The gross value of investment property must be > or = depreciation and impairment at opening

PA10-042 The gross value of brand names must be > or = amortization and impairment at closing

PA10-044 The gross value of brand names must be > or = amortization and impairment at opening

PA10-046 The gross value of intangible exploration and evaluation assets must be > or = amortization and impairment at closing

PA10-048 The gross value of intangible exploration and evaluation assets must be > or = amortization and impairment at opening

PA10-050 The gross value of mastheads and publishing titles must be > or = amortization and impairment at closing

PA10-052 The gross value of mastheads and publishing titles must be > or = amortization and impairment at opening

PA10-054 The gross value of computer software must be > or = amortization and impairment at closing

PA10-056 The gross value of computer software must be > or = amortization and impairment at opening

PA10-058 The gross value of licences and franchises must be > or = amortization and impairment at closing

PA10-060 The gross value of licences and franchises must be > or = amortization and impairment at opening

PA10-062 The gross value of patents, trademarks and other rights must be > or = amortization and impairment at closing

Package Controls

15

CODE DESCRIPTION (PACKAGE CONTROLS)

PA10-064 The gross value of patents, trademarks and other rights must be > or = amortization and impairment at opening

PA10-066 The gross value of recipes, formulae, models, designs and prototypes must be > or = amortization and impairment at closing

PA10-068 The gross value of recipes, formulae, models, designs and prototypes must be > or = amortization and impairment at opening

PA10-070 The gross value of intangible assets under development must be > or = impairment at closing

PA10-072 The gross value of intangible assets under development must be > or = impairment at opening

PA10-074 The gross value of other intangible asssets must be > or = amortization and impairment at closing

PA10-076 The gross value of other intangible asssets must be > or = amortization and impairment at opening

PA10-078 The gross value of biological assets must be > or = depreciation and impairment at closing

PA10-080 The gross value of biological assets must be > or = depreciation and impairment at opening

PA10-082 The gross value of investments in subsidiaries, JV and associates must be > or = impairment at closing

PA10-084 The gross value of investments in subsidiaries, JV and associates must be > or = impairment at opening

PA10-086 The gross value of loans and cash advances, non-current must be > or = impairment at closing

PA10-088 The gross value of loans and cash advances, non-current must be > or = impairment at opening

PA10-090 The gross value of receivables, non-current must be > or = allowance for bad and doubtful debts at closing

PA10-092 The gross value of receivables, non-current must be > or = allowance for bad and doubtful debts at opening

PA10-094 The gross value of trade receivables must be > or = allowance for bad and doubtful debts at closing

PA10-096 The gross value of trade receivables must be > or = allowance for bad and doubtful debts at opening

PA10-098 The gross value of other receivables must be > or = allowance for bad and doubtful debts at closing

PA10-100 The gross value of other receivables must be > or = allowance for bad and doubtful debts at opening

PA10-102 The gross value of loans and cash advances, current must be > or = impairment at closing

PA10-104 The gross value of loans and cash advances, current must be > or = impairment at opening

P-A20 Securities and shareholdings

PA20-002 Changes in investments in subsidiaries must be analyzed

PA20-004 Changes in investments in subsidiaries detailed by share must be analyzed by flow

PA20-006 Breakdown of investments in subsidiaries by share must equal account total at closing

PA20-008 Breakdown of investments in subsidiaries by share must equal account total at opening

PA20-010 Breakdown of investments in subsidiaries by share must equal account total in movement flows

PA20-012 Changes in impairment on investments in subsidiaries must be analyzed

PA20-014 Changes in impairment on investments in subsidiaries detailed by share should be analysed by flow

PA20-016 Breakdown by share of impairment on investments in subsidiaries must equal account total at closing

PA20-018 Breakdown by share of impairment on investments in subsidiaries must equal account total at opening

PA20-020 Breakdown by share of impairment on investments in subsidiaries must equal account total in movement flows

PA20-021 Flows for impairment of investments in subsidiaies must be the same on the balance sheet and on the income statement

PA20-022 Breakdown by share of profit or loss on sale of shares must equal account total

PA20-026 The analysis of the disposal of investments in subsidiaries by partner must equal account total

PA20-028 The analysis of the purchase of investments in subsidiaries by partner must equal account total

PA20-029 The number of shares in securities held has to be filled in at opening

PA20-030 The number of shares in securities held has to be filled in at closing

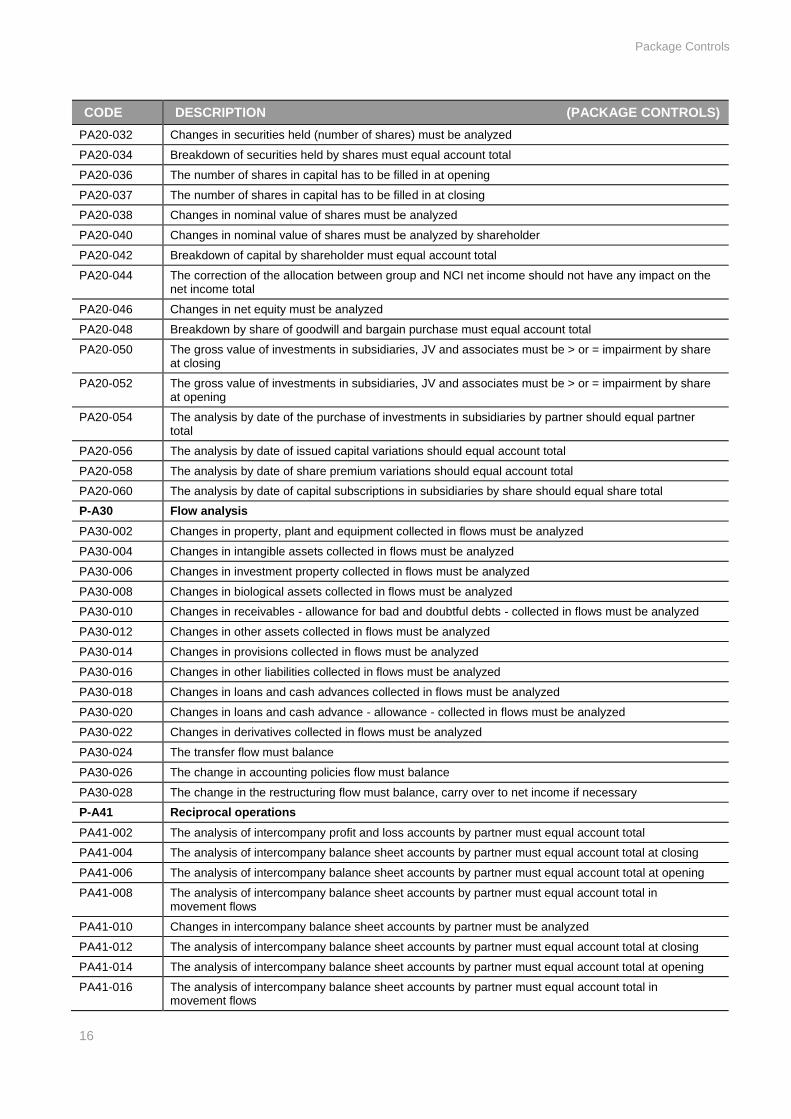

Package Controls

16

CODE DESCRIPTION (PACKAGE CONTROLS)

PA20-032 Changes in securities held (number of shares) must be analyzed

PA20-034 Breakdown of securities held by shares must equal account total

PA20-036 The number of shares in capital has to be filled in at opening

PA20-037 The number of shares in capital has to be filled in at closing

PA20-038 Changes in nominal value of shares must be analyzed

PA20-040 Changes in nominal value of shares must be analyzed by shareholder

PA20-042 Breakdown of capital by shareholder must equal account total

PA20-044 The correction of the allocation between group and NCI net income should not have any impact on the net income total

PA20-046 Changes in net equity must be analyzed

PA20-048 Breakdown by share of goodwill and bargain purchase must equal account total

PA20-050 The gross value of investments in subsidiaries, JV and associates must be > or = impairment by share at closing

PA20-052 The gross value of investments in subsidiaries, JV and associates must be > or = impairment by share at opening

PA20-054 The analysis by date of the purchase of investments in subsidiaries by partner should equal partner total

PA20-056 The analysis by date of issued capital variations should equal account total

PA20-058 The analysis by date of share premium variations should equal account total

PA20-060 The analysis by date of capital subscriptions in subsidiaries by share should equal share total

P-A30 Flow analysis

PA30-002 Changes in property, plant and equipment collected in flows must be analyzed

PA30-004 Changes in intangible assets collected in flows must be analyzed

PA30-006 Changes in investment property collected in flows must be analyzed

PA30-008 Changes in biological assets collected in flows must be analyzed

PA30-010 Changes in receivables - allowance for bad and doubtful debts - collected in flows must be analyzed

PA30-012 Changes in other assets collected in flows must be analyzed

PA30-014 Changes in provisions collected in flows must be analyzed

PA30-016 Changes in other liabilities collected in flows must be analyzed

PA30-018 Changes in loans and cash advances collected in flows must be analyzed

PA30-020 Changes in loans and cash advance - allowance - collected in flows must be analyzed

PA30-022 Changes in derivatives collected in flows must be analyzed

PA30-024 The transfer flow must balance

PA30-026 The change in accounting policies flow must balance

PA30-028 The change in the restructuring flow must balance, carry over to net income if necessary

P-A41 Reciprocal operations

PA41-002 The analysis of intercompany profit and loss accounts by partner must equal account total

PA41-004 The analysis of intercompany balance sheet accounts by partner must equal account total at closing

PA41-006 The analysis of intercompany balance sheet accounts by partner must equal account total at opening

PA41-008 The analysis of intercompany balance sheet accounts by partner must equal account total in movement flows

PA41-010 Changes in intercompany balance sheet accounts by partner must be analyzed

PA41-012 The analysis of intercompany balance sheet accounts by partner must equal account total at closing

PA41-014 The analysis of intercompany balance sheet accounts by partner must equal account total at opening

PA41-016 The analysis of intercompany balance sheet accounts by partner must equal account total in movement flows

Package Controls

17

CODE DESCRIPTION (PACKAGE CONTROLS)

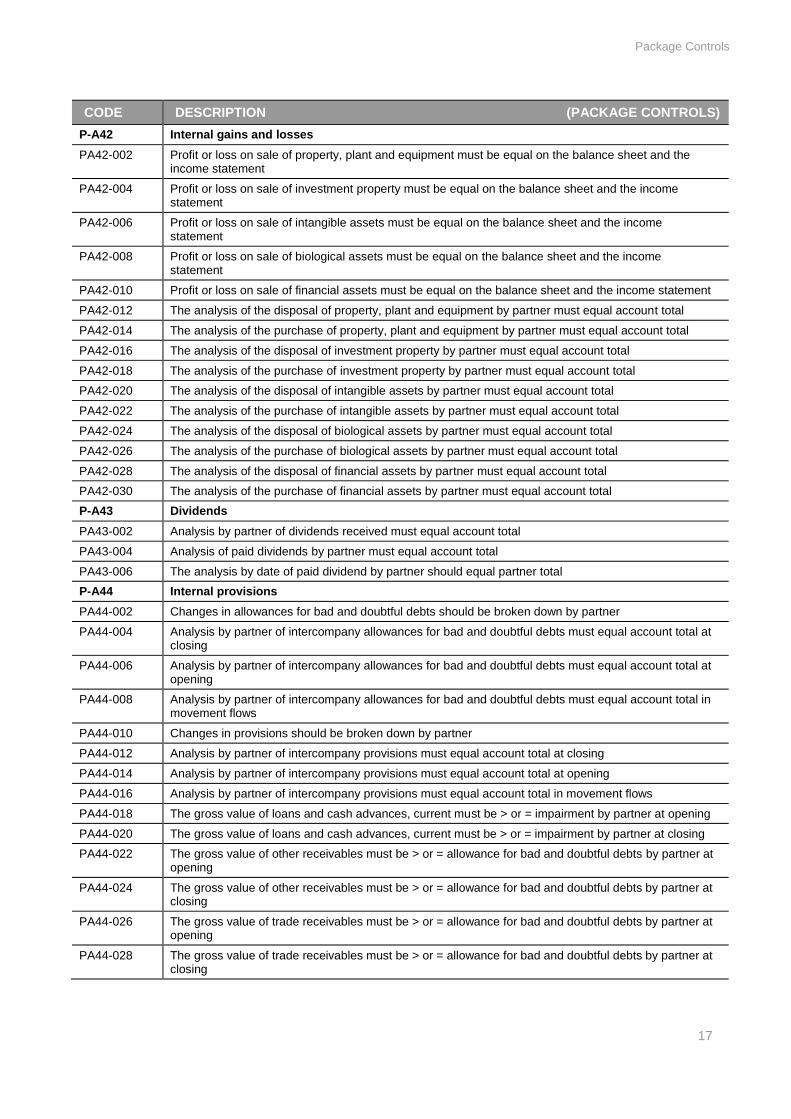

P-A42 Internal gains and losses

PA42-002 Profit or loss on sale of property, plant and equipment must be equal on the balance sheet and the income statement

PA42-004 Profit or loss on sale of investment property must be equal on the balance sheet and the income statement

PA42-006 Profit or loss on sale of intangible assets must be equal on the balance sheet and the income statement

PA42-008 Profit or loss on sale of biological assets must be equal on the balance sheet and the income statement

PA42-010 Profit or loss on sale of financial assets must be equal on the balance sheet and the income statement

PA42-012 The analysis of the disposal of property, plant and equipment by partner must equal account total

PA42-014 The analysis of the purchase of property, plant and equipment by partner must equal account total

PA42-016 The analysis of the disposal of investment property by partner must equal account total

PA42-018 The analysis of the purchase of investment property by partner must equal account total

PA42-020 The analysis of the disposal of intangible assets by partner must equal account total

PA42-022 The analysis of the purchase of intangible assets by partner must equal account total

PA42-024 The analysis of the disposal of biological assets by partner must equal account total

PA42-026 The analysis of the purchase of biological assets by partner must equal account total

PA42-028 The analysis of the disposal of financial assets by partner must equal account total

PA42-030 The analysis of the purchase of financial assets by partner must equal account total

P-A43 Dividends

PA43-002 Analysis by partner of dividends received must equal account total

PA43-004 Analysis of paid dividends by partner must equal account total

PA43-006 The analysis by date of paid dividend by partner should equal partner total

P-A44 Internal provisions

PA44-002 Changes in allowances for bad and doubtful debts should be broken down by partner

PA44-004 Analysis by partner of intercompany allowances for bad and doubtful debts must equal account total at closing

PA44-006 Analysis by partner of intercompany allowances for bad and doubtful debts must equal account total at opening

PA44-008 Analysis by partner of intercompany allowances for bad and doubtful debts must equal account total in movement flows

PA44-010 Changes in provisions should be broken down by partner

PA44-012 Analysis by partner of intercompany provisions must equal account total at closing

PA44-014 Analysis by partner of intercompany provisions must equal account total at opening

PA44-016 Analysis by partner of intercompany provisions must equal account total in movement flows

PA44-018 The gross value of loans and cash advances, current must be > or = impairment by partner at opening

PA44-020 The gross value of loans and cash advances, current must be > or = impairment by partner at closing

PA44-022 The gross value of other receivables must be > or = allowance for bad and doubtful debts by partner at opening

PA44-024 The gross value of other receivables must be > or = allowance for bad and doubtful debts by partner at closing

PA44-026 The gross value of trade receivables must be > or = allowance for bad and doubtful debts by partner at opening

PA44-028 The gross value of trade receivables must be > or = allowance for bad and doubtful debts by partner at closing

Package Controls

18

CODE DESCRIPTION (PACKAGE CONTROLS)

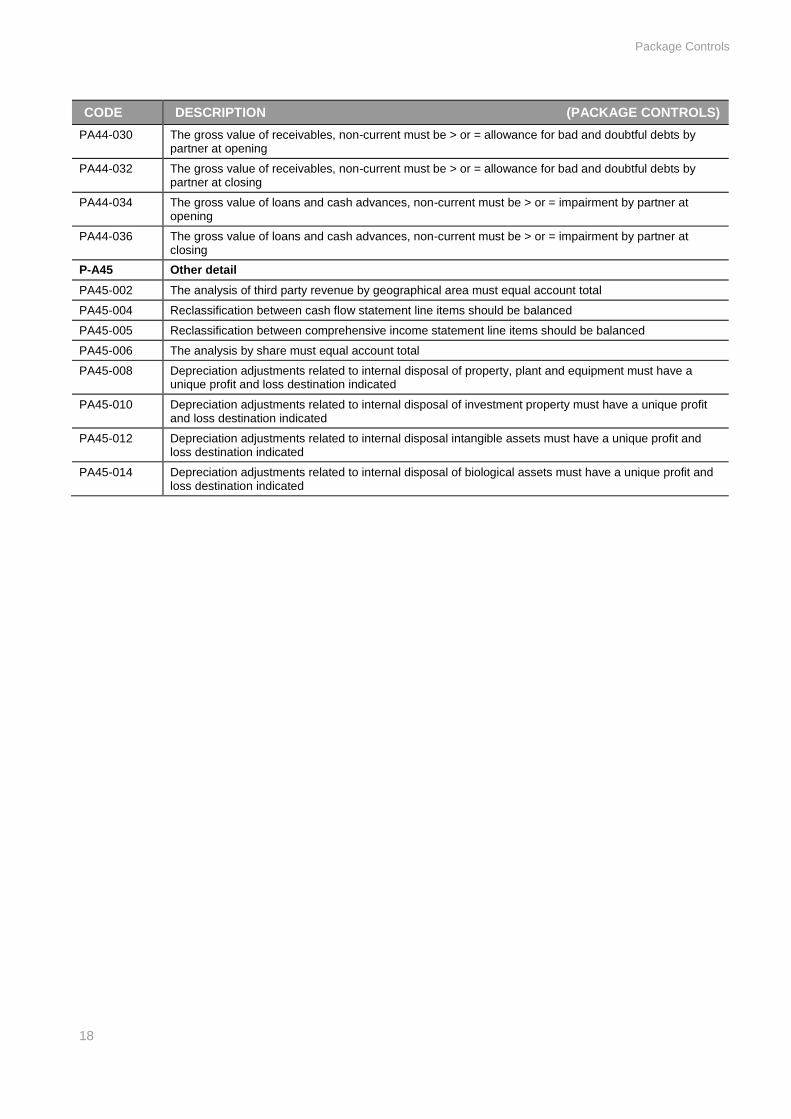

PA44-030 The gross value of receivables, non-current must be > or = allowance for bad and doubtful debts by partner at opening

PA44-032 The gross value of receivables, non-current must be > or = allowance for bad and doubtful debts by partner at closing

PA44-034 The gross value of loans and cash advances, non-current must be > or = impairment by partner at opening

PA44-036 The gross value of loans and cash advances, non-current must be > or = impairment by partner at closing

P-A45 Other detail

PA45-002 The analysis of third party revenue by geographical area must equal account total

PA45-004 Reclassification between cash flow statement line items should be balanced

PA45-005 Reclassification between comprehensive income statement line items should be balanced

PA45-006 The analysis by share must equal account total

PA45-008 Depreciation adjustments related to internal disposal of property, plant and equipment must have a unique profit and loss destination indicated

PA45-010 Depreciation adjustments related to internal disposal of investment property must have a unique profit and loss destination indicated

PA45-012 Depreciation adjustments related to internal disposal intangible assets must have a unique profit and loss destination indicated

PA45-014 Depreciation adjustments related to internal disposal of biological assets must have a unique profit and loss destination indicated

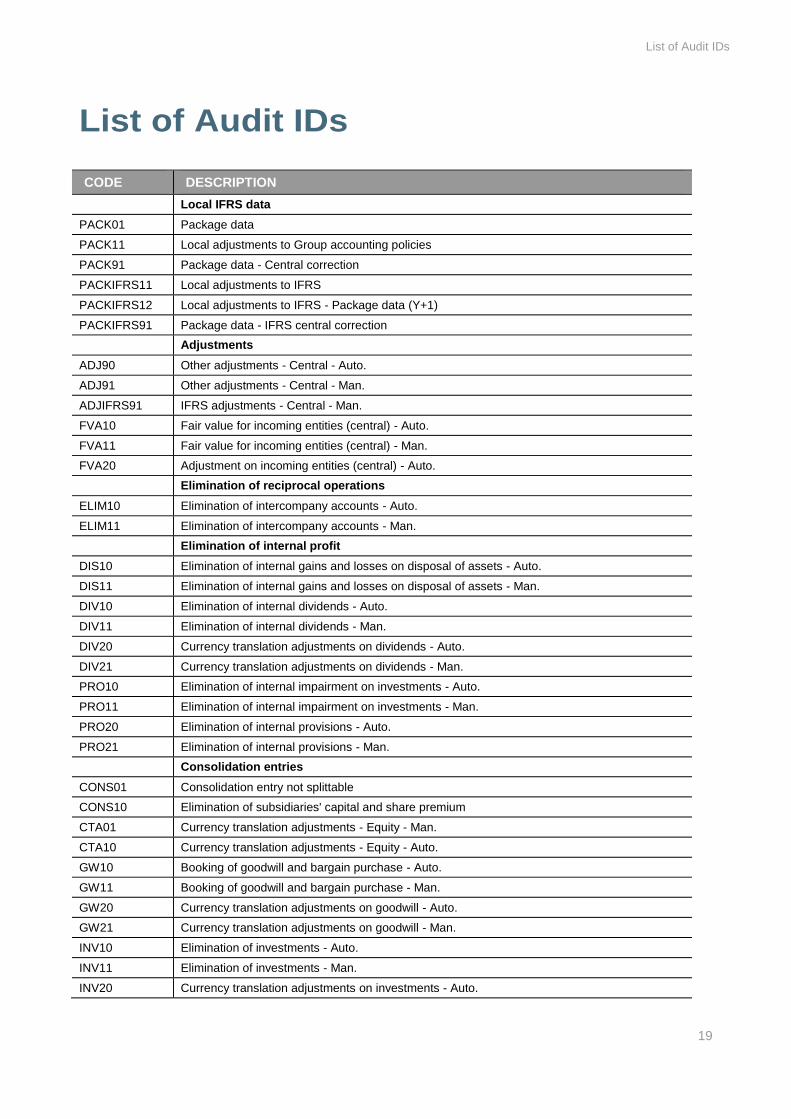

List of Audit IDs

19

List of Audit IDs

CODE DESCRIPTION

Local IFRS data

PACK01 Package data

PACK11 Local adjustments to Group accounting policies

PACK91 Package data - Central correction

PACKIFRS11 Local adjustments to IFRS

PACKIFRS12 Local adjustments to IFRS - Package data (Y+1)

PACKIFRS91 Package data - IFRS central correction

Adjustments

ADJ90 Other adjustments - Central - Auto.

ADJ91 Other adjustments - Central - Man.

ADJIFRS91 IFRS adjustments - Central - Man.

FVA10 Fair value for incoming entities (central) - Auto.

FVA11 Fair value for incoming entities (central) - Man.

FVA20 Adjustment on incoming entities (central) - Auto.

Elimination of reciprocal operations

ELIM10 Elimination of intercompany accounts - Auto.

ELIM11 Elimination of intercompany accounts - Man.

Elimination of internal profit

DIS10 Elimination of internal gains and losses on disposal of assets - Auto.

DIS11 Elimination of internal gains and losses on disposal of assets - Man.

DIV10 Elimination of internal dividends - Auto.

DIV11 Elimination of internal dividends - Man.

DIV20 Currency translation adjustments on dividends - Auto.

DIV21 Currency translation adjustments on dividends - Man.

PRO10 Elimination of internal impairment on investments - Auto.

PRO11 Elimination of internal impairment on investments - Man.

PRO20 Elimination of internal provisions - Auto.

PRO21 Elimination of internal provisions - Man.

Consolidation entries

CONS01 Consolidation entry not splittable

CONS10 Elimination of subsidiaries' capital and share premium

CTA01 Currency translation adjustments - Equity - Man.

CTA10 Currency translation adjustments - Equity - Auto.

GW10 Booking of goodwill and bargain purchase - Auto.

GW11 Booking of goodwill and bargain purchase - Man.

GW20 Currency translation adjustments on goodwill - Auto.

GW21 Currency translation adjustments on goodwill - Man.

INV10 Elimination of investments - Auto.

INV11 Elimination of investments - Man.

INV20 Currency translation adjustments on investments - Auto.

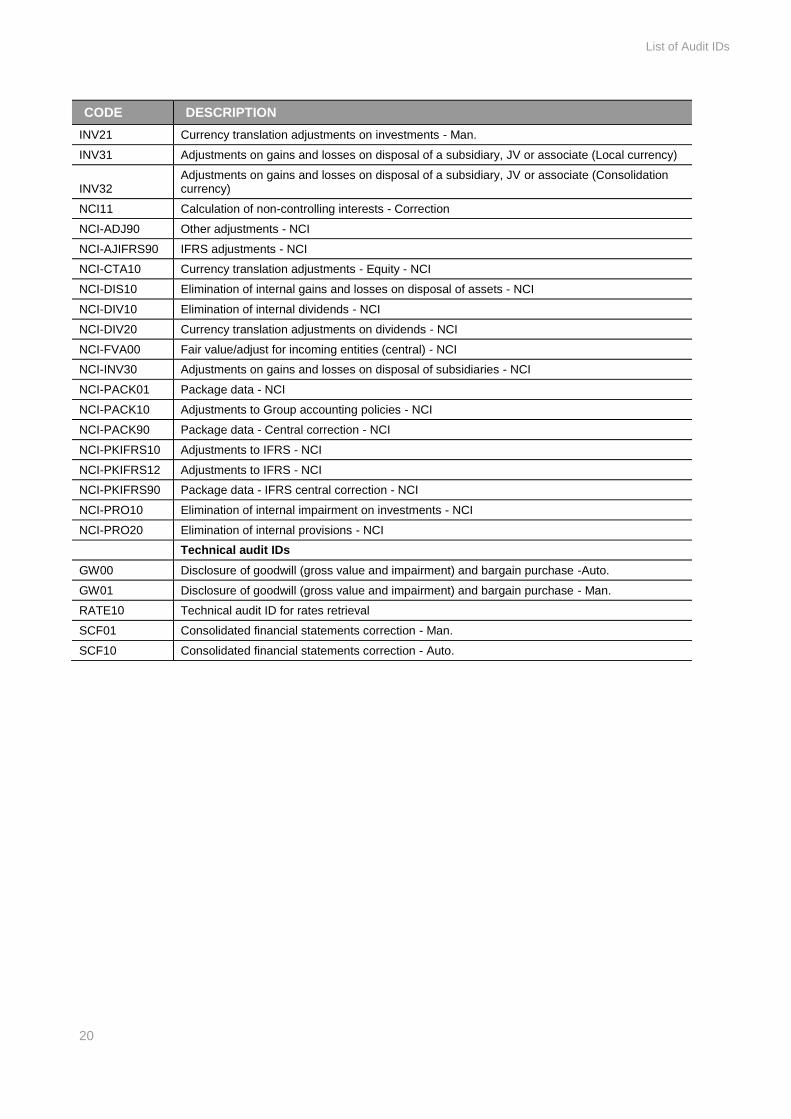

List of Audit IDs

20

CODE DESCRIPTION

INV21 Currency translation adjustments on investments - Man.

INV31 Adjustments on gains and losses on disposal of a subsidiary, JV or associate (Local currency)

INV32 Adjustments on gains and losses on disposal of a subsidiary, JV or associate (Consolidation currency)

NCI11 Calculation of non-controlling interests - Correction

NCI-ADJ90 Other adjustments - NCI

NCI-AJIFRS90 IFRS adjustments - NCI

NCI-CTA10 Currency translation adjustments - Equity - NCI

NCI-DIS10 Elimination of internal gains and losses on disposal of assets - NCI

NCI-DIV10 Elimination of internal dividends - NCI

NCI-DIV20 Currency translation adjustments on dividends - NCI

NCI-FVA00 Fair value/adjust for incoming entities (central) - NCI

NCI-INV30 Adjustments on gains and losses on disposal of subsidiaries - NCI

NCI-PACK01 Package data - NCI

NCI-PACK10 Adjustments to Group accounting policies - NCI

NCI-PACK90 Package data - Central correction - NCI

NCI-PKIFRS10 Adjustments to IFRS - NCI

NCI-PKIFRS12 Adjustments to IFRS - NCI

NCI-PKIFRS90 Package data - IFRS central correction - NCI

NCI-PRO10 Elimination of internal impairment on investments - NCI

NCI-PRO20 Elimination of internal provisions - NCI

Technical audit IDs

GW00 Disclosure of goodwill (gross value and impairment) and bargain purchase -Auto.

GW01 Disclosure of goodwill (gross value and impairment) and bargain purchase - Man.

RATE10 Technical audit ID for rates retrieval

SCF01 Consolidated financial statements correction - Man.

SCF10 Consolidated financial statements correction - Auto.

Consolidation Journal Entries

21

Consolidation Journal Entries

Form 1 – Elimination of Intra-group Transactions

Form 2 – Elimination of Internal Provisions

Form 3 – Elimination of Internal Dividends

Form 4 – Elimination of Internal Capital Gains or Losses

Form 5 – Non-controlling Interests

Form 6 – Elimination of Investments

Form 7 – Currency Translation Adjustment

Form 8 – Goodwill and Bargain Purchase

Consolidation Journal Entries

22

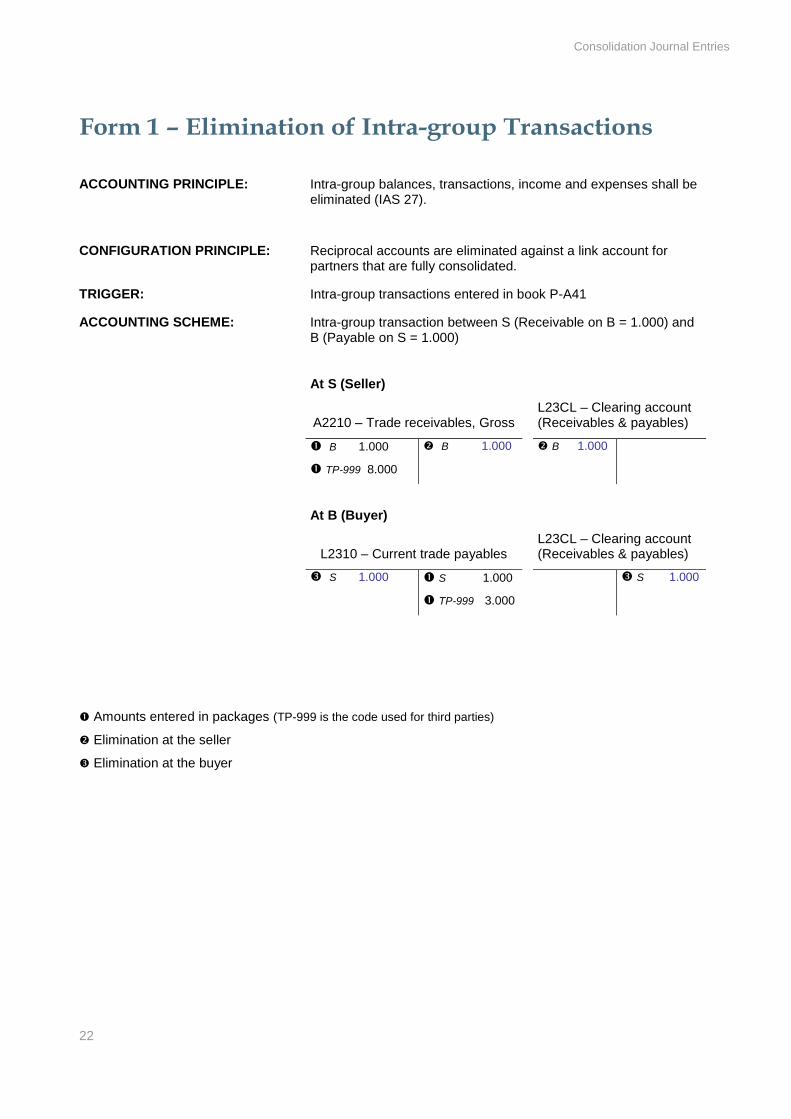

Form 1 – Elimination of Intra-group Transactions

ACCOUNTING PRINCIPLE: Intra-group balances, transactions, income and expenses shall be eliminated (IAS 27).

CONFIGURATION PRINCIPLE: Reciprocal accounts are eliminated against a link account for partners that are fully consolidated.

TRIGGER: Intra-group transactions entered in book P-A41

ACCOUNTING SCHEME: Intra-group transaction between S (Receivable on B = 1.000) and B (Payable on S = 1.000)

At S (Seller)

A2210 – Trade receivables, Gross

L23CL – Clearing account (Receivables & payables)

B 1.000

TP-999 8.000

B 1.000 B 1.000

At B (Buyer)

L2310 – Current trade payables

L23CL – Clearing account (Receivables & payables)

S 1.000 S 1.000

TP-999 3.000

S 1.000

Amounts entered in packages (TP-999 is the code used for third parties)

Elimination at the seller

Elimination at the buyer

Consolidation Journal Entries

23

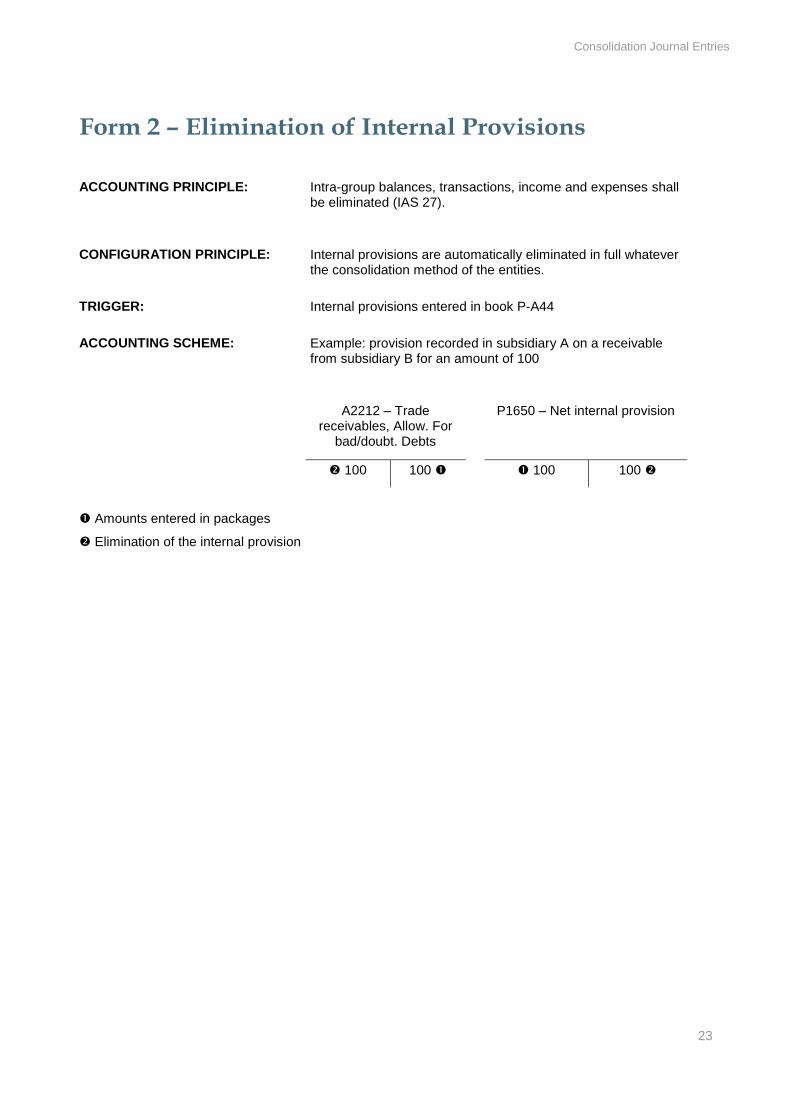

Form 2 – Elimination of Internal Provisions

ACCOUNTING PRINCIPLE: Intra-group balances, transactions, income and expenses shall be eliminated (IAS 27).

CONFIGURATION PRINCIPLE: Internal provisions are automatically eliminated in full whatever the consolidation method of the entities.

TRIGGER: Internal provisions entered in book P-A44

ACCOUNTING SCHEME: Example: provision recorded in subsidiary A on a receivable from subsidiary B for an amount of 100

A2212 – Trade receivables, Allow. For

bad/doubt. Debts

P1650 – Net internal provision

100 100 100 100

Amounts entered in packages

Elimination of the internal provision

Consolidation Journal Entries

24

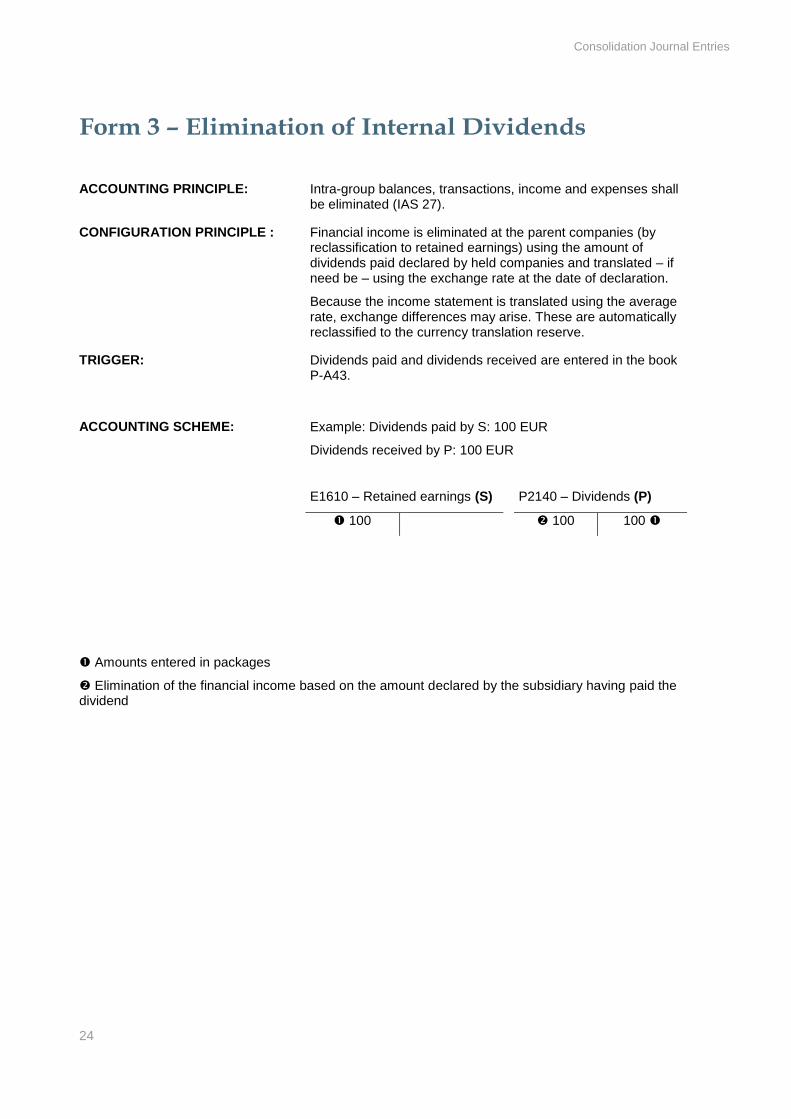

Form 3 – Elimination of Internal Dividends

ACCOUNTING PRINCIPLE: Intra-group balances, transactions, income and expenses shall be eliminated (IAS 27).

CONFIGURATION PRINCIPLE : Financial income is eliminated at the parent companies (by reclassification to retained earnings) using the amount of dividends paid declared by held companies and translated – if need be – using the exchange rate at the date of declaration.

Because the income statement is translated using the average rate, exchange differences may arise. These are automatically reclassified to the currency translation reserve.

TRIGGER: Dividends paid and dividends received are entered in the book P-A43.

ACCOUNTING SCHEME: Example: Dividends paid by S: 100 EUR

Dividends received by P: 100 EUR

E1610 – Retained earnings (S) P2140 – Dividends (P)

100 100 100

Amounts entered in packages

Elimination of the financial income based on the amount declared by the subsidiary having paid the dividend

Consolidation Journal Entries

25

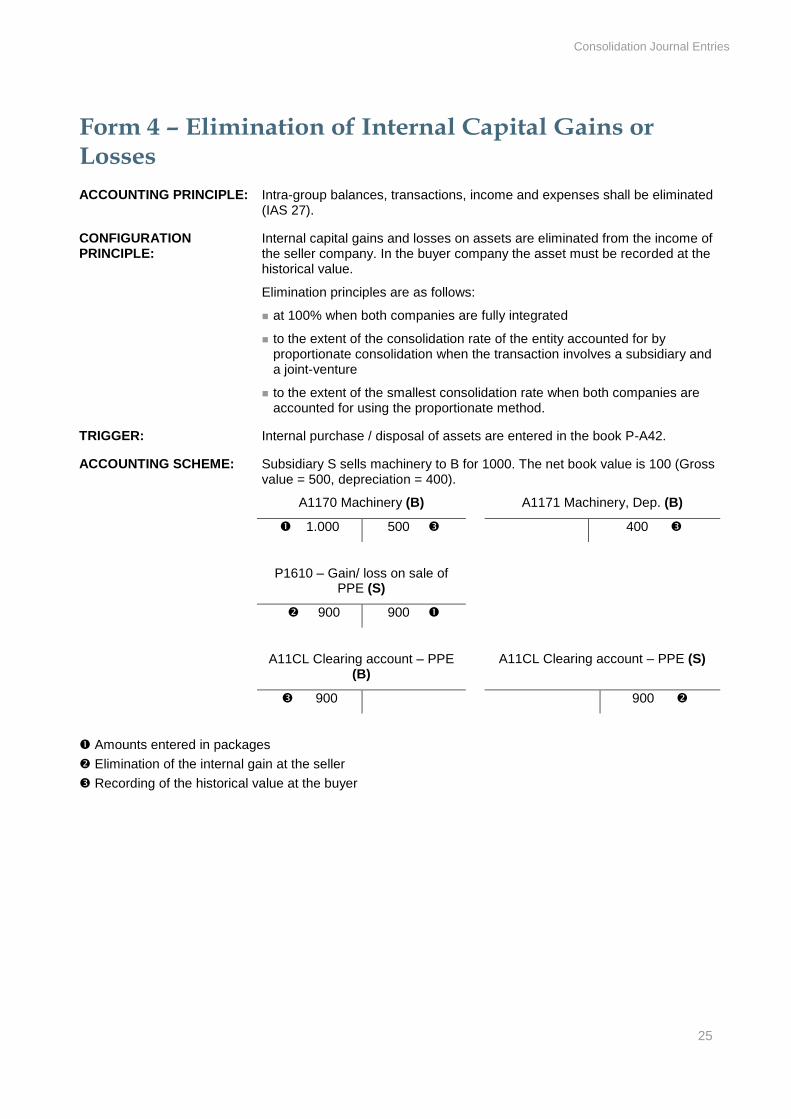

Form 4 – Elimination of Internal Capital Gains or Losses

ACCOUNTING PRINCIPLE: Intra-group balances, transactions, income and expenses shall be eliminated (IAS 27).

CONFIGURATION PRINCIPLE:

Internal capital gains and losses on assets are eliminated from the income of the seller company. In the buyer company the asset must be recorded at the historical value.

Elimination principles are as follows:

at 100% when both companies are fully integrated

to the extent of the consolidation rate of the entity accounted for by proportionate consolidation when the transaction involves a subsidiary and a joint-venture

to the extent of the smallest consolidation rate when both companies are accounted for using the proportionate method.

TRIGGER: Internal purchase / disposal of assets are entered in the book P-A42.

ACCOUNTING SCHEME: Subsidiary S sells machinery to B for 1000. The net book value is 100 (Gross value = 500, depreciation = 400).

A1170 Machinery (B) A1171 Machinery, Dep. (B)

1.000 500 400

P1610 – Gain/ loss on sale of PPE (S)

900 900

A11CL Clearing account – PPE (B)

A11CL Clearing account – PPE (S)

900 900

Amounts entered in packages

Elimination of the internal gain at the seller

Recording of the historical value at the buyer

Consolidation Journal Entries

26

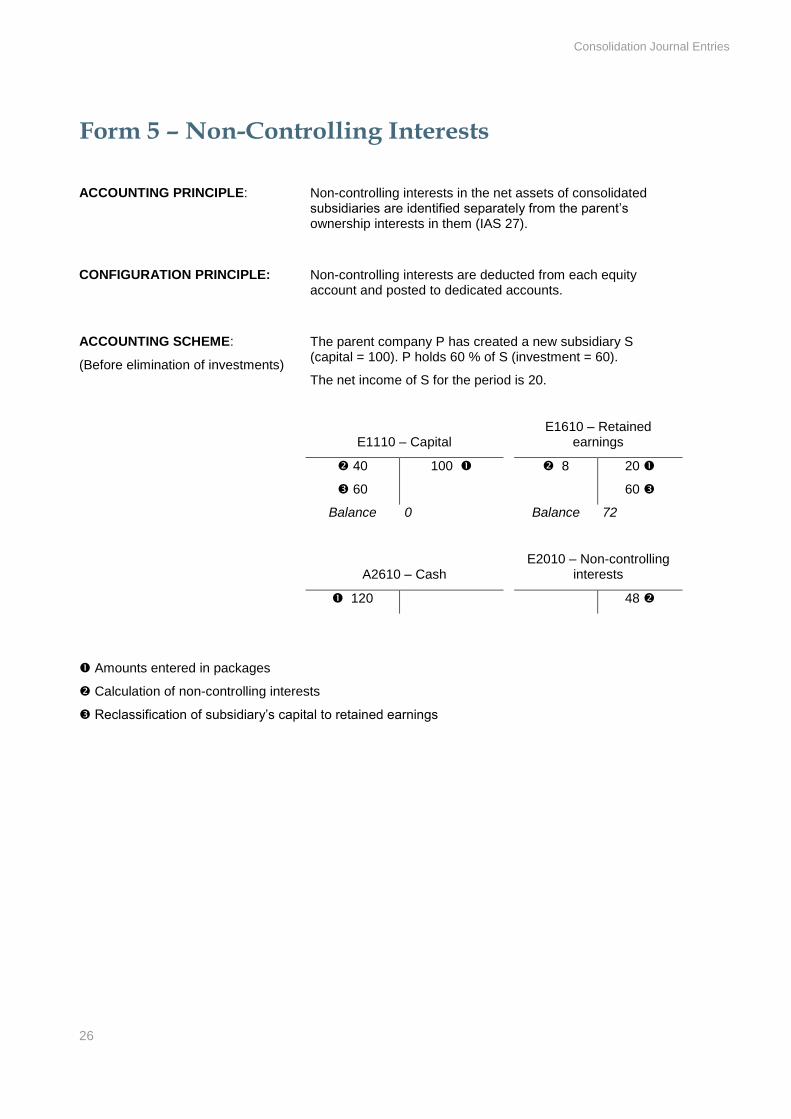

Form 5 – Non-Controlling Interests

ACCOUNTING PRINCIPLE: Non-controlling interests in the net assets of consolidated subsidiaries are identified separately from the parent’s ownership interests in them (IAS 27).

CONFIGURATION PRINCIPLE: Non-controlling interests are deducted from each equity account and posted to dedicated accounts.

ACCOUNTING SCHEME:

(Before elimination of investments)

The parent company P has created a new subsidiary S (capital = 100). P holds 60 % of S (investment = 60).

The net income of S for the period is 20.

E1110 – Capital E1610 – Retained

earnings

40

60

100

8 20

60

Balance 0 Balance 72

A2610 – Cash E2010 – Non-controlling

interests

120 48

Amounts entered in packages

Calculation of non-controlling interests

Reclassification of subsidiary’s capital to retained earnings

Consolidation Journal Entries

27

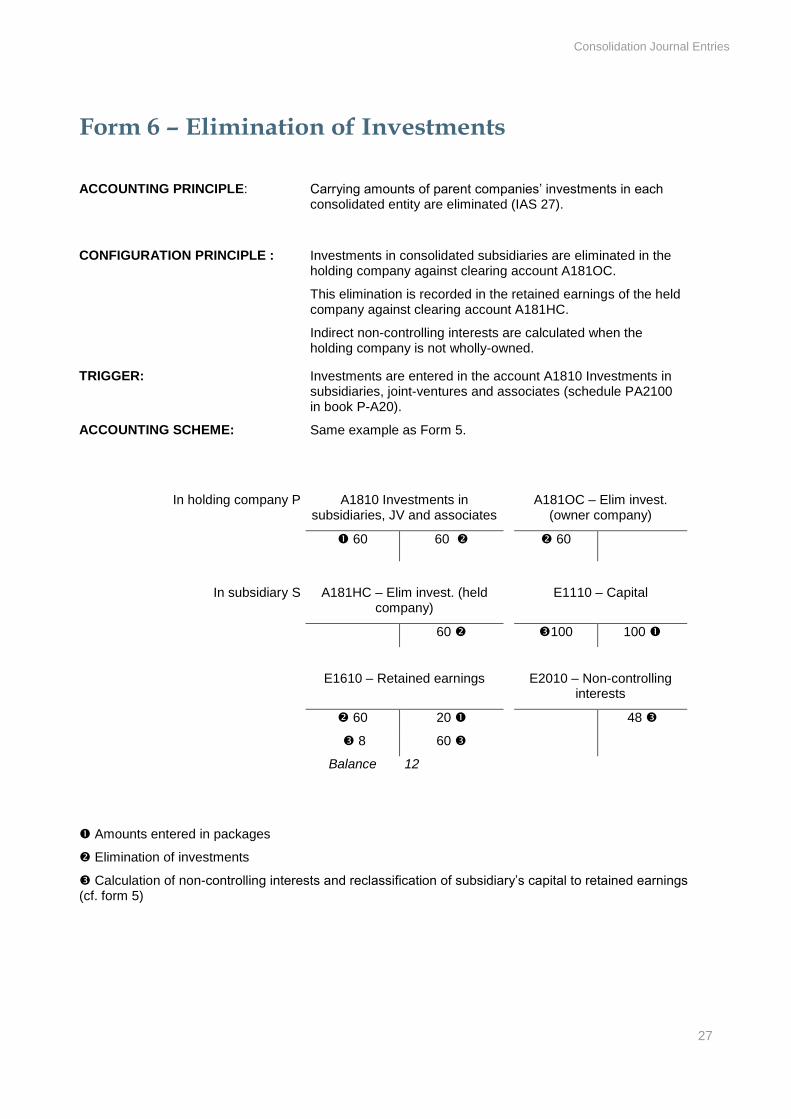

Form 6 – Elimination of Investments

ACCOUNTING PRINCIPLE: Carrying amounts of parent companies’ investments in each consolidated entity are eliminated (IAS 27).

CONFIGURATION PRINCIPLE :

Investments in consolidated subsidiaries are eliminated in the holding company against clearing account A181OC.

This elimination is recorded in the retained earnings of the held company against clearing account A181HC.

Indirect non-controlling interests are calculated when the holding company is not wholly-owned.

TRIGGER: Investments are entered in the account A1810 Investments in subsidiaries, joint-ventures and associates (schedule PA2100 in book P-A20).

ACCOUNTING SCHEME: Same example as Form 5.

In holding company P A1810 Investments in subsidiaries, JV and associates

A181OC – Elim invest. (owner company)

60 60

60

In subsidiary S A181HC – Elim invest. (held company)

E1110 – Capital

60 100 100

E1610 – Retained earnings

E2010 – Non-controlling interests

60 20 48

8 60

Balance 12

Amounts entered in packages

Elimination of investments

Calculation of non-controlling interests and reclassification of subsidiary’s capital to retained earnings (cf. form 5)

Consolidation Journal Entries

28

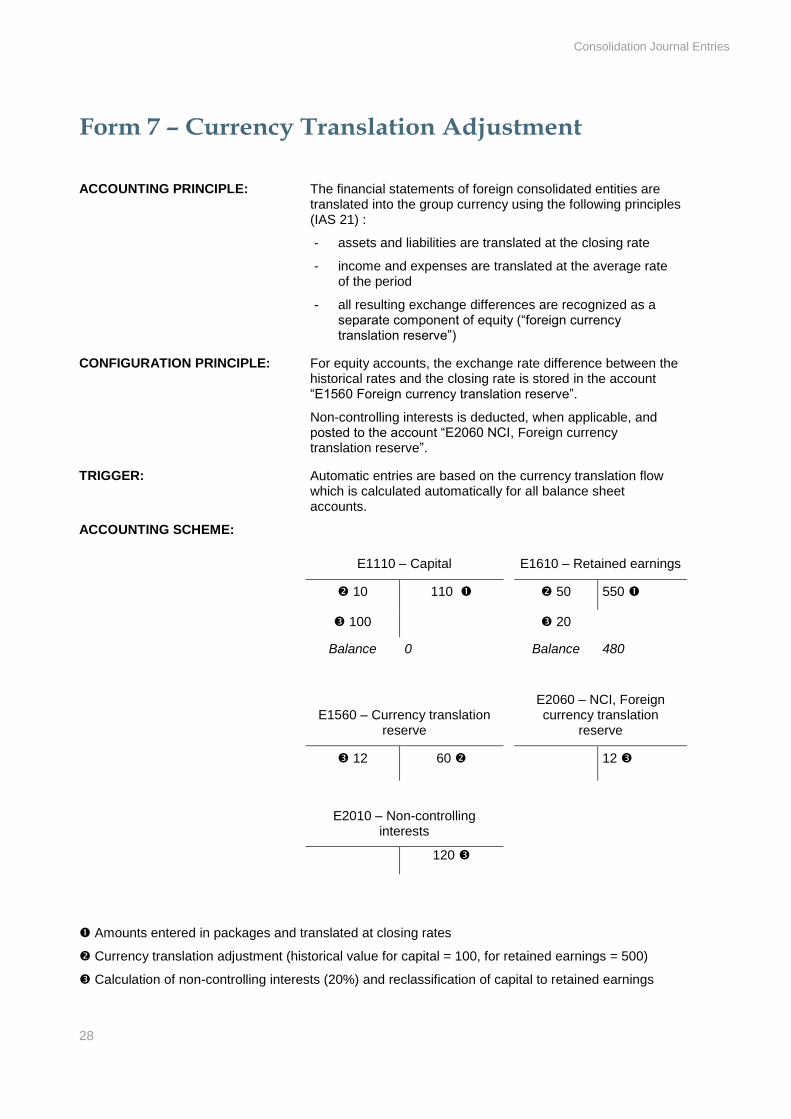

Form 7 – Currency Translation Adjustment

ACCOUNTING PRINCIPLE: The financial statements of foreign consolidated entities are translated into the group currency using the following principles (IAS 21) :

- assets and liabilities are translated at the closing rate

- income and expenses are translated at the average rate of the period

- all resulting exchange differences are recognized as a separate component of equity (“foreign currency translation reserve”)

CONFIGURATION PRINCIPLE: For equity accounts, the exchange rate difference between the historical rates and the closing rate is stored in the account “E1560 Foreign currency translation reserve”.

Non-controlling interests is deducted, when applicable, and posted to the account “E2060 NCI, Foreign currency translation reserve”.

TRIGGER: Automatic entries are based on the currency translation flow which is calculated automatically for all balance sheet accounts.

ACCOUNTING SCHEME:

E1110 – Capital E1610 – Retained earnings

10 110 50 550

100 20

Balance 0 Balance 480

E1560 – Currency translation reserve

E2060 – NCI, Foreign currency translation

reserve

12 60

12

E2010 – Non-controlling interests

120

Amounts entered in packages and translated at closing rates

Currency translation adjustment (historical value for capital = 100, for retained earnings = 500)

Calculation of non-controlling interests (20%) and reclassification of capital to retained earnings

List of Retrieval Schedules

29

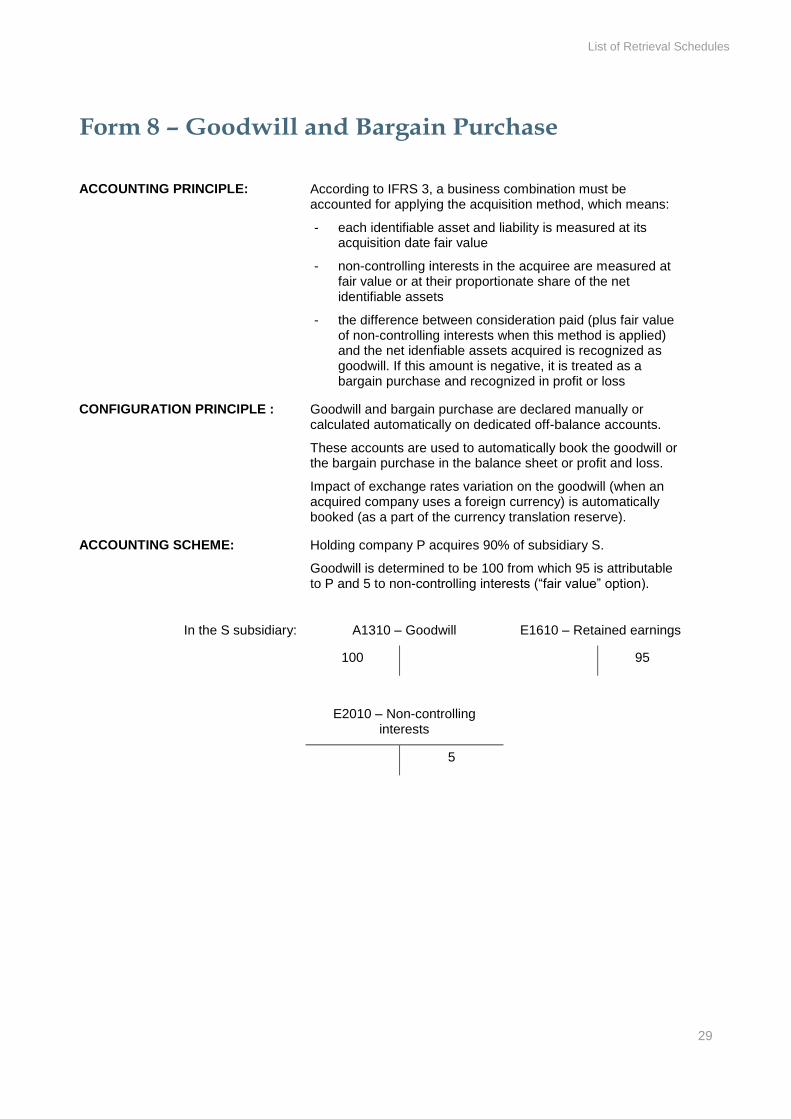

Form 8 – Goodwill and Bargain Purchase

ACCOUNTING PRINCIPLE: According to IFRS 3, a business combination must be accounted for applying the acquisition method, which means:

- each identifiable asset and liability is measured at its acquisition date fair value

- non-controlling interests in the acquiree are measured at fair value or at their proportionate share of the net identifiable assets

- the difference between consideration paid (plus fair value of non-controlling interests when this method is applied) and the net idenfiable assets acquired is recognized as goodwill. If this amount is negative, it is treated as a bargain purchase and recognized in profit or loss

CONFIGURATION PRINCIPLE : Goodwill and bargain purchase are declared manually or calculated automatically on dedicated off-balance accounts.

These accounts are used to automatically book the goodwill or the bargain purchase in the balance sheet or profit and loss.

Impact of exchange rates variation on the goodwill (when an acquired company uses a foreign currency) is automatically booked (as a part of the currency translation reserve).

ACCOUNTING SCHEME: Holding company P acquires 90% of subsidiary S.

Goodwill is determined to be 100 from which 95 is attributable to P and 5 to non-controlling interests (“fair value” option).

In the S subsidiary: A1310 – Goodwill E1610 – Retained earnings

100 95

E2010 – Non-controlling interests

5

List of Retrieval Schedules

30

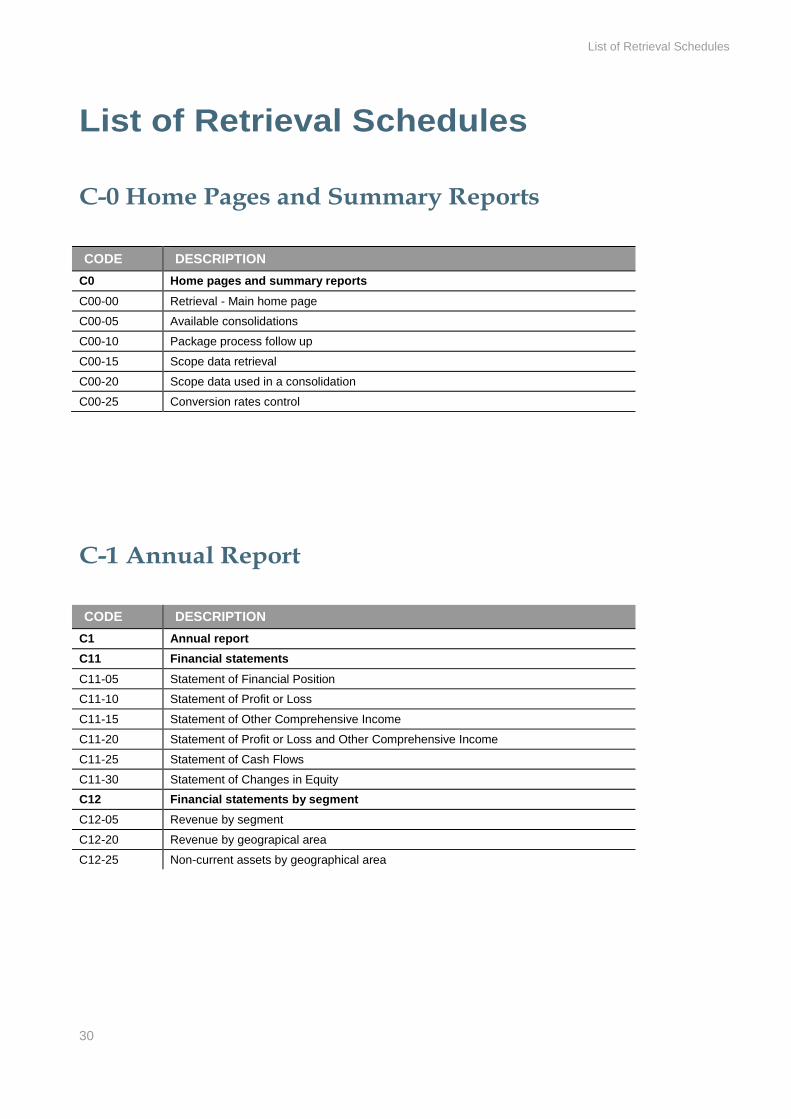

List of Retrieval Schedules

C-0 Home Pages and Summary Reports

CODE DESCRIPTION

C0 Home pages and summary reports

C00-00 Retrieval - Main home page

C00-05 Available consolidations

C00-10 Package process follow up

C00-15 Scope data retrieval

C00-20 Scope data used in a consolidation

C00-25 Conversion rates control

C-1 Annual Report

CODE DESCRIPTION

C1 Annual report

C11 Financial statements

C11-05 Statement of Financial Position

C11-10 Statement of Profit or Loss

C11-15 Statement of Other Comprehensive Income

C11-20 Statement of Profit or Loss and Other Comprehensive Income

C11-25 Statement of Cash Flows

C11-30 Statement of Changes in Equity

C12 Financial statements by segment

C12-05 Revenue by segment

C12-20 Revenue by geograpical area

C12-25 Non-current assets by geographical area

List of Retrieval Schedules

31

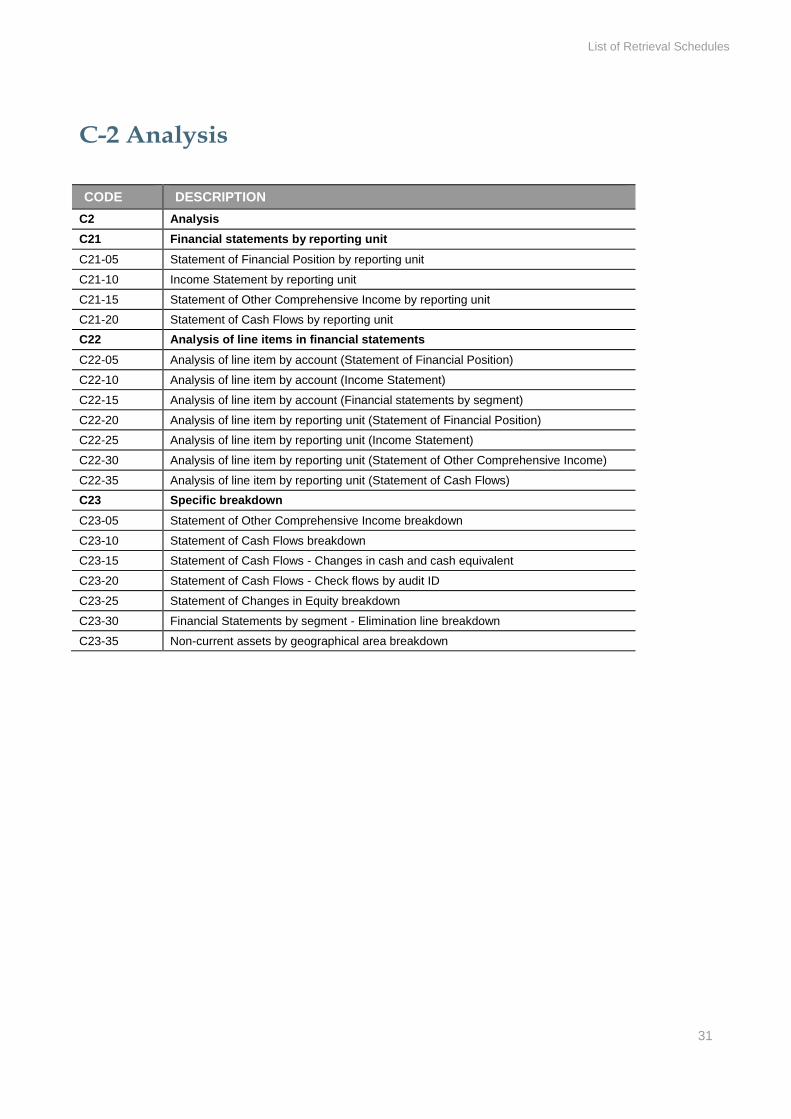

C-2 Analysis

CODE DESCRIPTION

C2 Analysis

C21 Financial statements by reporting unit

C21-05 Statement of Financial Position by reporting unit

C21-10 Income Statement by reporting unit

C21-15 Statement of Other Comprehensive Income by reporting unit

C21-20 Statement of Cash Flows by reporting unit

C22 Analysis of line items in financial statements

C22-05 Analysis of line item by account (Statement of Financial Position)

C22-10 Analysis of line item by account (Income Statement)

C22-15 Analysis of line item by account (Financial statements by segment)

C22-20 Analysis of line item by reporting unit (Statement of Financial Position)

C22-25 Analysis of line item by reporting unit (Income Statement)

C22-30 Analysis of line item by reporting unit (Statement of Other Comprehensive Income)

C22-35 Analysis of line item by reporting unit (Statement of Cash Flows)

C23 Specific breakdown

C23-05 Statement of Other Comprehensive Income breakdown

C23-10 Statement of Cash Flows breakdown

C23-15 Statement of Cash Flows - Changes in cash and cash equivalent

C23-20 Statement of Cash Flows - Check flows by audit ID

C23-25 Statement of Changes in Equity breakdown

C23-30 Financial Statements by segment - Elimination line breakdown

C23-35 Non-current assets by geographical area breakdown

List of Retrieval Schedules

32

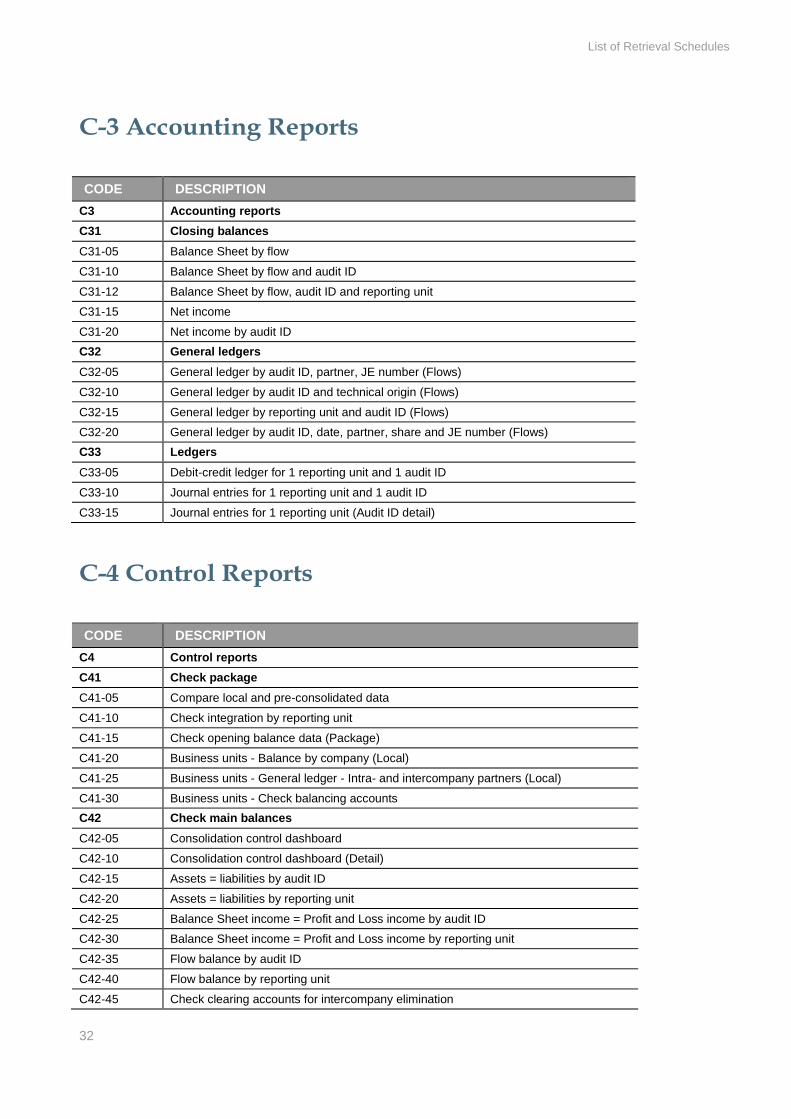

C-3 Accounting Reports

CODE DESCRIPTION

C3 Accounting reports

C31 Closing balances

C31-05 Balance Sheet by flow

C31-10 Balance Sheet by flow and audit ID

C31-12 Balance Sheet by flow, audit ID and reporting unit

C31-15 Net income

C31-20 Net income by audit ID

C32 General ledgers

C32-05 General ledger by audit ID, partner, JE number (Flows)

C32-10 General ledger by audit ID and technical origin (Flows)

C32-15 General ledger by reporting unit and audit ID (Flows)

C32-20 General ledger by audit ID, date, partner, share and JE number (Flows)

C33 Ledgers

C33-05 Debit-credit ledger for 1 reporting unit and 1 audit ID

C33-10 Journal entries for 1 reporting unit and 1 audit ID

C33-15 Journal entries for 1 reporting unit (Audit ID detail)

C-4 Control Reports

CODE DESCRIPTION

C4 Control reports

C41 Check package

C41-05 Compare local and pre-consolidated data

C41-10 Check integration by reporting unit

C41-15 Check opening balance data (Package)

C41-20 Business units - Balance by company (Local)

C41-25 Business units - General ledger - Intra- and intercompany partners (Local)

C41-30 Business units - Check balancing accounts

C42 Check main balances

C42-05 Consolidation control dashboard

C42-10 Consolidation control dashboard (Detail)

C42-15 Assets = liabilities by audit ID

C42-20 Assets = liabilities by reporting unit

C42-25 Balance Sheet income = Profit and Loss income by audit ID

C42-30 Balance Sheet income = Profit and Loss income by reporting unit

C42-35 Flow balance by audit ID

C42-40 Flow balance by reporting unit

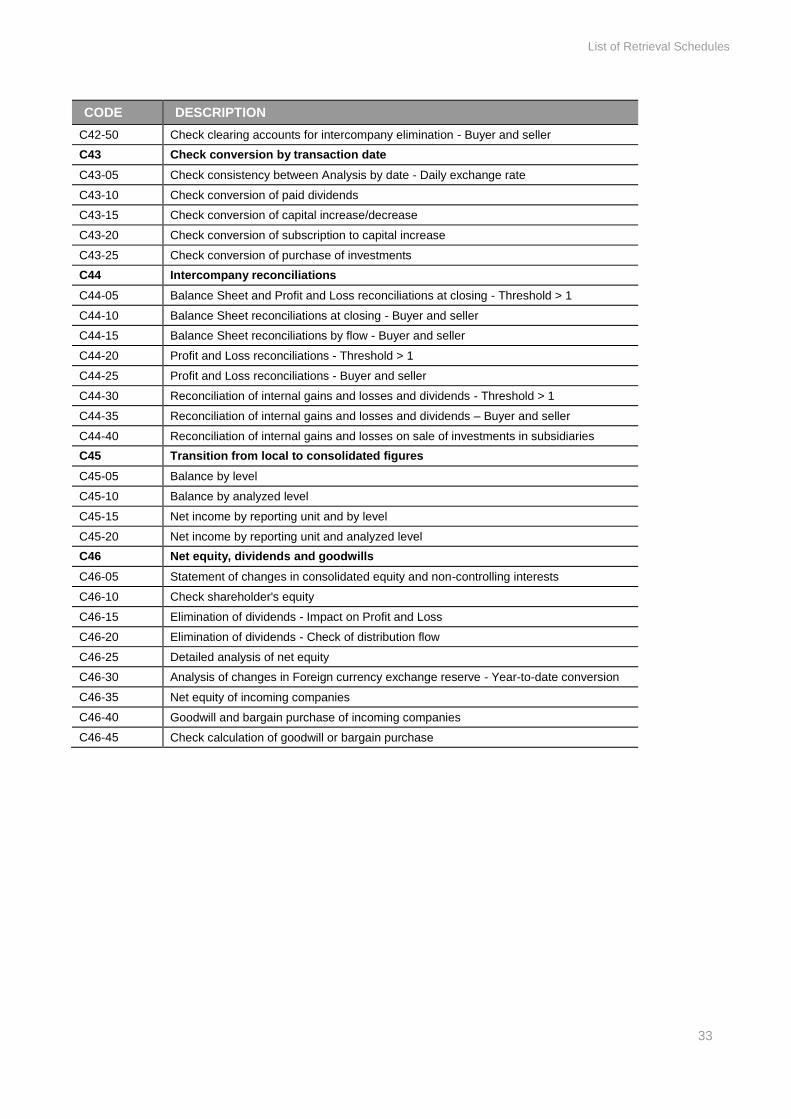

C42-45 Check clearing accounts for intercompany elimination

List of Retrieval Schedules

33

CODE DESCRIPTION

C42-50 Check clearing accounts for intercompany elimination - Buyer and seller

C43 Check conversion by transaction date

C43-05 Check consistency between Analysis by date - Daily exchange rate

C43-10 Check conversion of paid dividends

C43-15 Check conversion of capital increase/decrease

C43-20 Check conversion of subscription to capital increase

C43-25 Check conversion of purchase of investments

C44 Intercompany reconciliations

C44-05 Balance Sheet and Profit and Loss reconciliations at closing - Threshold > 1

C44-10 Balance Sheet reconciliations at closing - Buyer and seller

C44-15 Balance Sheet reconciliations by flow - Buyer and seller

C44-20 Profit and Loss reconciliations - Threshold > 1

C44-25 Profit and Loss reconciliations - Buyer and seller

C44-30 Reconciliation of internal gains and losses and dividends - Threshold > 1

C44-35 Reconciliation of internal gains and losses and dividends – Buyer and seller

C44-40 Reconciliation of internal gains and losses on sale of investments in subsidiaries

C45 Transition from local to consolidated figures

C45-05 Balance by level

C45-10 Balance by analyzed level

C45-15 Net income by reporting unit and by level

C45-20 Net income by reporting unit and analyzed level

C46 Net equity, dividends and goodwills

C46-05 Statement of changes in consolidated equity and non-controlling interests

C46-10 Check shareholder's equity

C46-15 Elimination of dividends - Impact on Profit and Loss

C46-20 Elimination of dividends - Check of distribution flow

C46-25 Detailed analysis of net equity

C46-30 Analysis of changes in Foreign currency exchange reserve - Year-to-date conversion

C46-35 Net equity of incoming companies

C46-40 Goodwill and bargain purchase of incoming companies

C46-45 Check calculation of goodwill or bargain purchase

List of Retrieval Schedules

34

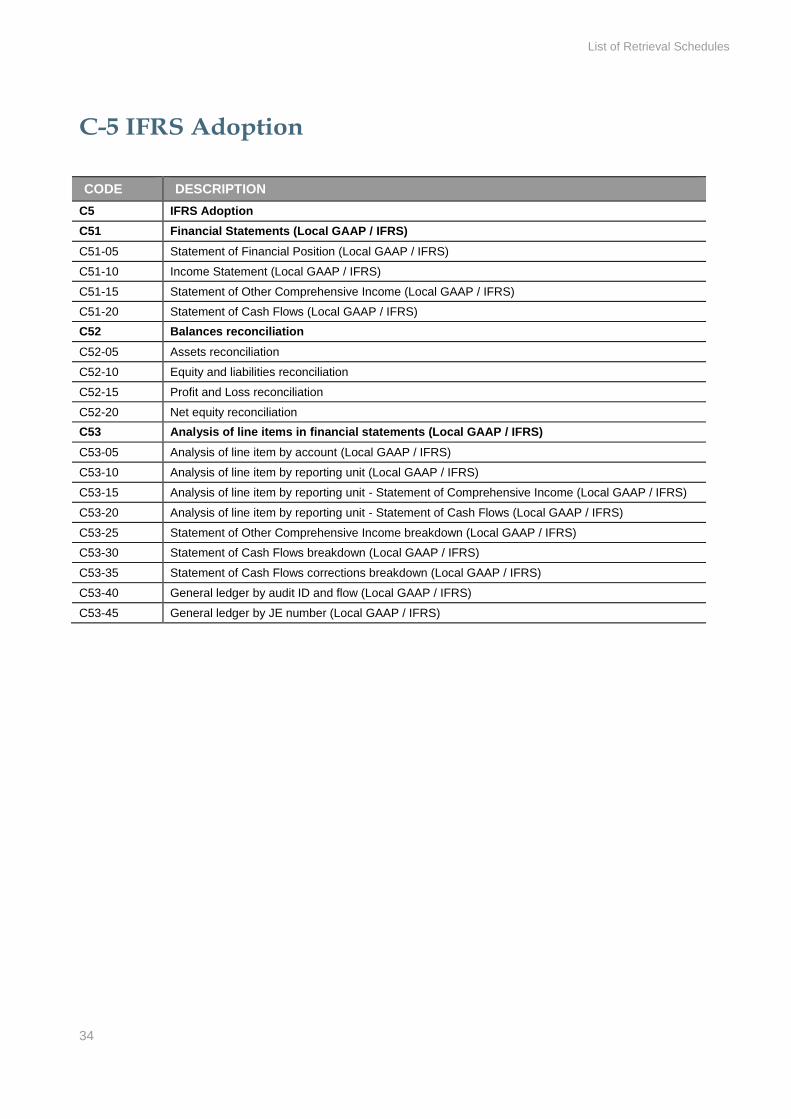

C-5 IFRS Adoption

CODE DESCRIPTION

C5 IFRS Adoption

C51 Financial Statements (Local GAAP / IFRS)

C51-05 Statement of Financial Position (Local GAAP / IFRS)

C51-10 Income Statement (Local GAAP / IFRS)

C51-15 Statement of Other Comprehensive Income (Local GAAP / IFRS)

C51-20 Statement of Cash Flows (Local GAAP / IFRS)

C52 Balances reconciliation

C52-05 Assets reconciliation

C52-10 Equity and liabilities reconciliation

C52-15 Profit and Loss reconciliation

C52-20 Net equity reconciliation

C53 Analysis of line items in financial statements (Local GAAP / IFRS)

C53-05 Analysis of line item by account (Local GAAP / IFRS)

C53-10 Analysis of line item by reporting unit (Local GAAP / IFRS)

C53-15 Analysis of line item by reporting unit - Statement of Comprehensive Income (Local GAAP / IFRS)

C53-20 Analysis of line item by reporting unit - Statement of Cash Flows (Local GAAP / IFRS)

C53-25 Statement of Other Comprehensive Income breakdown (Local GAAP / IFRS)

C53-30 Statement of Cash Flows breakdown (Local GAAP / IFRS)

C53-35 Statement of Cash Flows corrections breakdown (Local GAAP / IFRS)

C53-40 General ledger by audit ID and flow (Local GAAP / IFRS)

C53-45 General ledger by JE number (Local GAAP / IFRS)