sarah ritchie- principal financial group keith hoffman- nfp

TRANSCRIPT

Sarah Ritchie- Principal Financial GroupKeith Hoffman- NFP

INTERNAL USE ONLY. Not for public distribution.

If you don’t help your clients with income protection, you’re not doing your due diligence. And you’re giving recurring revenue away to your competitors. May is Disability Insurance Awareness Month — a perfect opportunity to talk about the importance of disability

insurance (DI).

Why You Should Offer Income Protection

Individual Disability Insurance

Sarah Ritchie, Sr. Relationship Manager – IDI Sales

4

Creating a solid financial foundation

Are your clients protected in the

event of a disabling injury or

illness?

5

Top 5 Reasons to Sell Individual Disability Insurance

1 It’s a great door opener.

2Upon a disability, it helps your clients pay daily living expenses and bills, including premiums on other insurance products they have with you.

3 It helps you diversify your portfolio offering and provides attractive compensation.

4 It’s part of your due diligence.

5 Solutions are available in sought-after markets – business owners and higher-income individuals.

6

The DI conversation

• It’s up to you to talk about income protection… – Ask clients about their current coverage. Their answers may

surprise you. – Ask for the sale.

• If you don’t, someone else will.

Compensation potential

Producers who take a comprehensive approach with clients earn 30% more than those who do not.2

1- Social Security Administration, Fact Sheet, March 20112 - 2010 Principal Life Insurance Company retail sales data

Marketpotential

67% of the private sector workforce has no long-term disability insurance.1

7

DI Affordability

• Premiums typically cost 1% to 3% of gross income for a benefit that could pay out millions of dollars in the event of a disability

Compare the cost of disability coverage to a daily

cup of premium store-bought coffee.

$3.56/day = $3,000 monthly paycheck*

Compare the cost of disability coverage to a daily

cup of premium store-bought coffee.

$3.56/day = $3,000 monthly paycheck*

1Not available in states for single life cases, optional in most states for multi-life cases, always required in California, not available in Vermont)2Assumptions: Male, Colorado resident, $50,000 annual income, To Age 65 Benefit Period and Your Occupation Period, nonsmoker, $2,925 Maximum Monthly Benefit, 90-day elimination period, 3A occupation class. DI insurance can not be purchased for a daily premium; illustration of concept only.

• Showcase available discounts:– 20% Multi-Life Discount– 10% Select Occupation Discount – Up to 10% MNSA1 Discount– 10% Association Discount

8

Offer DI to employers

•Get recognized for your benefits expertise.•Build stronger client relationships and increase sales.•Help improve group coverage persistency •See increased compensation potential

Help your clients enhance their employee benefits and reward and retain their key employees.

Multi-Life program discount starting at 20%

9

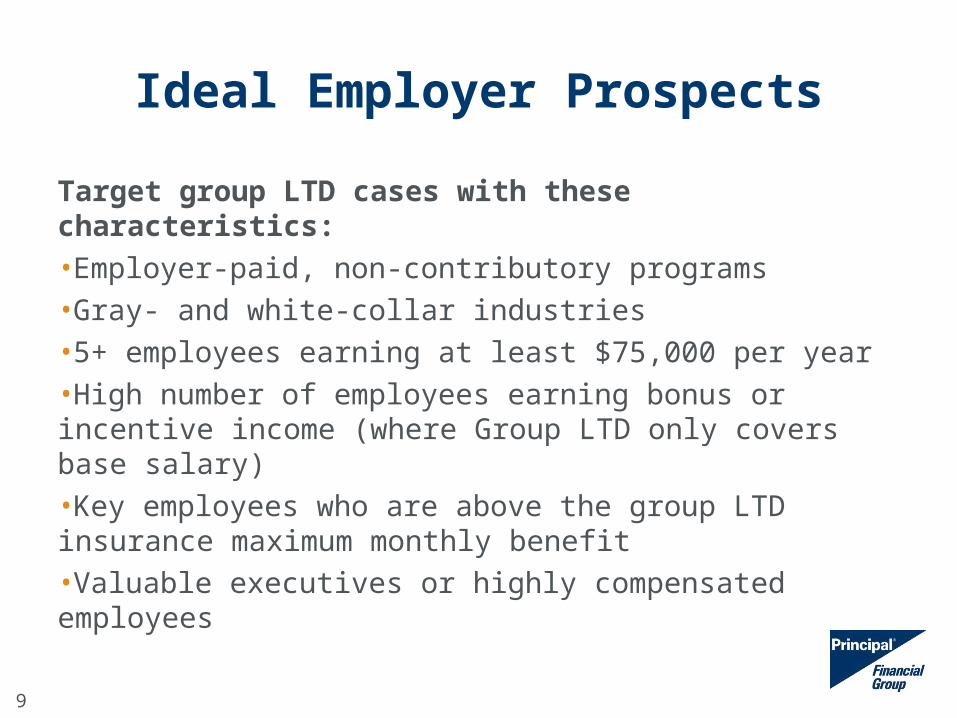

Ideal Employer Prospects

Target group LTD cases with these characteristics:•Employer-paid, non-contributory programs•Gray- and white-collar industries•5+ employees earning at least $75,000 per year•High number of employees earning bonus or incentive income (where Group LTD only covers base salary)•Key employees who are above the group LTD insurance maximum monthly benefit•Valuable executives or highly compensated employees

10

Reverse Discrimination

Structuring Group LTD and DI for affordability•Lower the group LTD maximum monthly benefit cap•Change the group LTD definition of disability•Vary the maximum monthly benefit by employee class

11

Disability Insurance Awareness Month

• DIAM materials: principal.com/incomeprotection

• NEW Sales openers: Scripts and sales ideas

– Marketing document (DI8583)

– Brainshark coming soon

• Producer Satisfaction Survey

Questions?

For Producer Information Only – Not for Client Presentation

Please remember to abide by the company's policy on disclosure of compensation. You can obtain more information, as well as a sample disclosure form, at www.principal.com.

No part of this presentation may be reproduced or used in any form or by any means, electronic or mechanical, including photocopying or recording, or by any information storage and retrieval system,

without prior written permission from the Principal Financial Group®.

Copyright ©2011 Principal Financial Services, Inc.

Insurance issued by Principal Life Insurance Company, a member of the Principal Financial Group, Des Moines, IA 50392.

DI 2760 | 4/2011

INTERNAL USE ONLY. Not for public distribution.

NFP DI Business Center

- Multi Life DI Sales Center- Customizable Marketing Material- Request for Proposal System- Claims Expertise- Underwriting Advocacy- Point of Sale Assistance- Income Analysis Tools - Carrier and Product Information- Training & Education

School of Excellence: May 6 -9th Austin, TX Learn how to overcome objections from clients when they say they don’t need to protect their

incomes in the event of disability. A good advisor will mention the need for DI, but a great advisor is able to handle any objections that may arise. (CE credits)

Disability Insurance Call Series Selling DI to the Individual Client- May 2, 2012 at 1:00pm CT

Learn how to talk to your clients about DI and hear how one of our producers is successfully selling DI to his clients and winning the business of new clients because he is discussing DI.

Selling DI to the Corporate Client – May 3, 2012 at 10:15 am CT Branden Pierson, national sales director for Executive Benefits with Unum, explains effective

ways to sell DI to corporate clients, including customer characteristics and packaging concepts that you need to know. DI helps clients protect their most valuable asset: their ability to earn an income. It gives you an opportunity to offer more than your competition. If you’re doing business in the corporate marketplace but not doing DI, you will after this call!

Microsite

INTERNAL USE ONLY. Not for public distribution.

NFP DI Resources

Kat Freeman, Manager DI Support512-697-6151

Keith Hoffman, Vice President, Disability512-697-6155