saudi ceramic company december 2013 - aljazira capital · saudi ceramics saudi ceramic company is...

TRANSCRIPT

1 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

Saudi Ceramics (2040)

• Saudi Ceramics leading producer of Ceramic and porcelain tiles – Saudi Ceramic Company is the leading manufacturer of ceramic tiles in Saudi Arabia. The company tiles product portfolio includes ceramic tiles, floor tiles, porcelain tiles. In line with its product line the company also produces sanitary ware, and ceramic road markers. The company also manufactures and sells electric water heaters.

• Strong product demand from the local market - Demand for construction material in Saudi Arabia is mainly led by Government projects in different sectors, as estimated value of awarded projects in the first 9 months of 2013 reached USD 67bn. Growth in the sector is supported by demographic, economic, and regulatory factors. A rising population, changing family structure and current age demographics are the main demographic factors that may have an effect on demand. Economic factors include a potential rise in household income, cost of borrowing and liquidity, and relative low home ownership. Implementation of the mortgage law, and the new structure decided by the ministry of housing to provide developed land along with a loan to build housing units are the main regulatory factors that might have an effect on demand.

• Diversified revenue source - The company’s major revenue source is its tiles business, whereas the road markers and sanitary ware business is an extension of its tiles production facilities. The company generates 78%-80% of its revenue from Sales of Ceramic & porcelain tiles and Sanitary ware business. The rest of its revenue is generated from the sales of Electric water heaters, which contributes around 20%-22% to the top line.

• New business lines to further dilute revenue - The company in 2012 announced that it is looking to enter the red brick business. For that matter the company in 2012 announced plans to establish a red brick factory with a capacity of 330,000tons per annum. The company is looking to enter plastics business, which will be first used internally and the rest will be sold to the market. This we believe will help the company in reducing its cost.

Company Snapshot (in SAR,000) 2011 2012 2013 e 2014 e 2015 e 2016 e

Net Sales 1,221 1,447 1,515 1,711 1,829 1,884 % Growth 13% 19% 5% 13% 7% 3%Net income 232 248 262 360 389 404 % Growth 5% 7% 6% 37% 8% 4%EBITDA Margins 30% 27% 27% 32% 32% 33%EBIT Margins 20% 18% 18% 22% 22% 22%Net Margins 19% 17% 17% 21% 21% 21%ROE 20% 19% 18% 21% 19% 17%ROA 10% 10% 9% 11% 11% 10%Dividend Yield 4% 3% 2% 2% 2% 2%PE (x) 10.67 11.40 15.87 11.56 10.70 10.29 PB (x) 2.16 2.16 2.81 2.38 2.03 1.76 EPS (diluted) 6 ٫19 6.60 7.00 9.60 10.38 10.78

Key financial indicators

Price Chart

T ASI Saud i C eram ic

70

80

9 0

100

110

120

130

6500 6700 69 00 7100 7300 7500 7700 79 00 8100 8300 8500

5-De

c-12

5-Ja

n-13

5-Fe

b-13

5-M

ar-1

3

5-Ap

r-13

5-M

ay-1

3

5-Ju

n-13

5-Ju

l-13

5-Au

g-13

5-Se

p-13

5-O

ct-1

3

5-N

ov-1

3

5-De

c-13

Source: TASI & Zawya

Recommendation ‘Overweight’

12-month price target; SAR 144.4

Current Price: SAR 111.0

Upside / (downside): 30.13%

Reuters code: 2040.SEBloomberg code: SCERCO:ABCountry: Saudi ArabiaSector: Bui ld ing & Construc t ionPrimary Listing: KSA exchangeM-Cap: SAR4,106mn52 Weeks H/L (SAR): 128.75/72.25

Key information

Analyst

Jassim Al-Jubran +966 12 6618602

Senior Analyst

Talha Nazar +966 12 6618603

• Valuation – We initiate our coverage on Saudi Ceramics Company with an “Overweight” recommendation We have used DCF for the company’s valuation, Our price target of SAR144.4 gives us a potential gain of 30.13% at current market price.

• Risk to our valuation – h Chinese Dumping: Saudi Ceramics is also facing competition from the Chinese imports, as according to the company the selling

price of Chinese products is even below the cost of production h Fuel Allocation: due to the on-going efforts by the government to curb fuel usage, the company is finding it hard to get allocation

for its new factories.

2 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

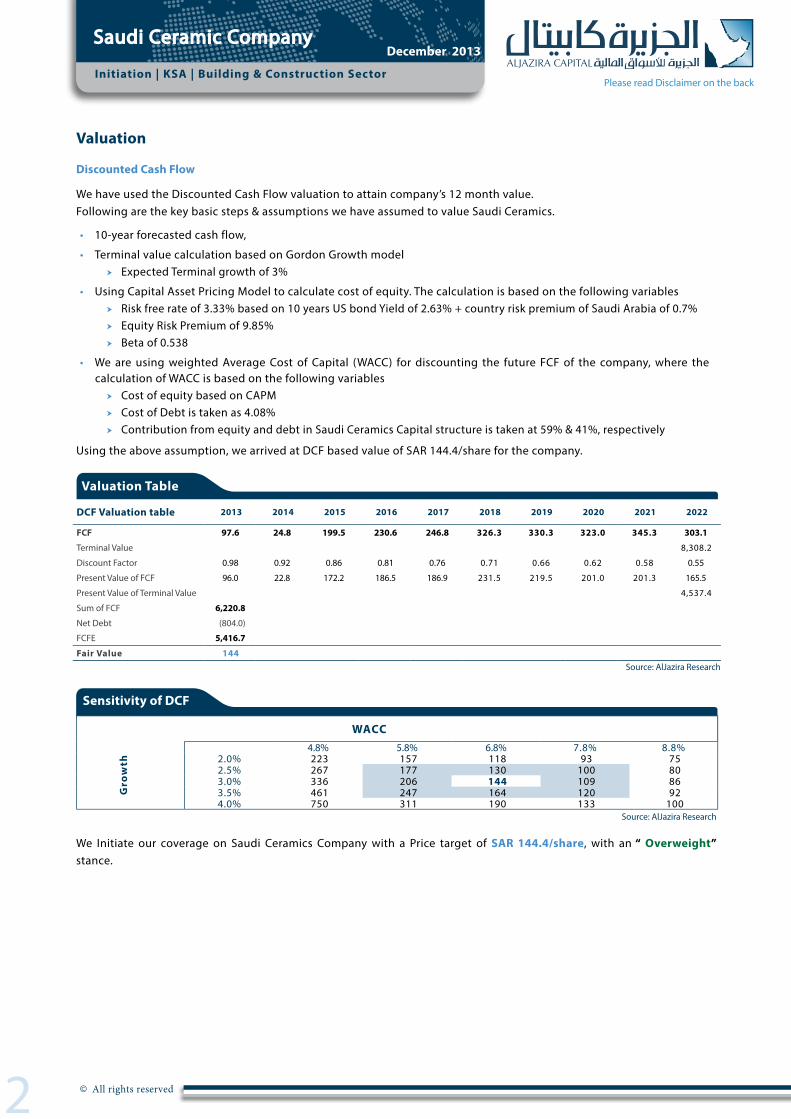

Valuation

DCF Valuation table 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

FCF 97.6 24.8 199.5 230.6 246.8 326.3 330.3 323.0 345.3 303.1

Terminal Value 8,308.2

Discount Factor 0.98 0.92 0.86 0.81 0.76 0.71 0.66 0.62 0.58 0.55

Present Value of FCF 96.0 22.8 172.2 186.5 186.9 231.5 219.5 201.0 201.3 165.5

Present Value of Terminal Value 4,537.4

Sum of FCF 6,220.8

Net Debt (804.0)

FCFE 5,416.7

Fair Value 144 Source: AlJazira Research

Valuation Table

Sensitivity of DCF

WACC

Gro

wth

4.8% 5.8% 6.8% 7.8% 8.8%2.0% 223 157 118 93 75 2.5% 267 177 130 100 80 3.0% 336 206 144 109 86 3.5% 461 247 164 120 92 4.0% 750 311 190 133 100

Source: AlJazira Research

Discounted Cash Flow

We have used the Discounted Cash Flow valuation to attain company’s 12 month value.Following are the key basic steps & assumptions we have assumed to value Saudi Ceramics.

• 10-year forecasted cash flow,

• Terminal value calculation based on Gordon Growth model h Expected Terminal growth of 3%

• Using Capital Asset Pricing Model to calculate cost of equity. The calculation is based on the following variables h Risk free rate of 3.33% based on 10 years US bond Yield of 2.63% + country risk premium of Saudi Arabia of 0.7% h Equity Risk Premium of 9.85% h Beta of 0.538

• We are using weighted Average Cost of Capital (WACC) for discounting the future FCF of the company, where the calculation of WACC is based on the following variables

h Cost of equity based on CAPM h Cost of Debt is taken as 4.08% h Contribution from equity and debt in Saudi Ceramics Capital structure is taken at 59% & 41%, respectively

Using the above assumption, we arrived at DCF based value of SAR 144.4/share for the company.

We Initiate our coverage on Saudi Ceramics Company with a Price target of SAR 144.4/share, with an “ Overweight” stance.

3 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

Saudi Arabia- Construction Demand

Demand for construction material in Saudi Arabia is mainly led by government projects in different sectors, as estimated value of awarded projects in the first 9 months of 2013 reached USD 67bn1. The Saudi Government’s 2013 budget is currently funding construction-intensive, multibillion-riyal projects ranging from ports and roads to rail networks and communications facilities. This large influx of construction project is bound to raise demand for construction material and sustain growth in the short to medium term.

The residential building sector, is expected to expand at a CAGR of 8–10% in the long term. The development in the residential housing sector is primarily led by the projects awarded by the Saudi Ministry of Housing (MOH). Contracts worth SAR 4 Billion were approved in 2013 by the Ministry of Housing providing 60,000 units of housing across different provinces, these contracts are part of the ministry’s long term plan to provide 500,000 units in the long term2. Real estate service company Jones Lang LaSalle estimates annual demand for housing to be between 150,000 and 200,000 units per year.

Growth in the sector is supported by demographic, economic, and regulatory factors. A rising population, changing family structure and current age demographics are the main demographic factors that may have an effect on demand. Economic factors include a potential rise in household income, cost of borrowing and liquidity, and relative low home ownership. Implementation of the mortgage law, and the new structure decided by the ministry of housing to provide developed land along with a loan to build housing units are the main regulatory factors that might have an effect on demand.

Demand is expected to remain healthy in the long term. Long term support by the government fueling direct and indirect demand for construction material is bound to keep demand at high levels at least till the end of 2014.

1 Zawya2 Colliers International

Population of Saudi Arabia

Source: CDSI

Source: Delliote, Business Monitor; Note: “e”: estimate; “f”: forecast

1. 8% 1. 8% 1. 9 % 1. 9 % 2. 0% 2. 0% 2. 1% 2. 1% 2. 2% 2. 2% 2. 3% 2. 3%

0

5

10

15

20

25

30

35

2012 2013 2014 2015 2016 2017

Mn

T o tal Po p ulatio n Saud i Po p ulatio n G ro w th R ate ( Saud i)

C o nstructio n ind ustry value, U SD b n C o nstructio n ind ustry , % o f G D P

0

1. 0

2. 0

3. 0

4. 0

5. 0

6. 0

0

10. 0

20. 0

30. 0

40. 0

50. 0

2014f2013f2012e2011 2015f 2016f

% of G

DP

US

$ bn

Estimated Construction Growth-KSA

4 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

Saudi Ceramics

Saudi Ceramic Company is the leading manufacturer of ceramic tiles in Saudi Arabia. The company tiles product portfolio includes ceramic tiles, floor tiles, porcelain tiles. In line line with its product line the company also produces sanitary ware, and ceramic road markers. The company also manufactures and sells electric water heaters.

The company offers its producrs through an existing 32 showrooms across the Kingdom, as well as through a local network of distributors and international markets. The company operates through 11 factories in Saudi Arabia, distributing more than 68mn pieces of different types of products.

Revenue mix

The company’s major revenue source is its tiles business, whereas the road markers and sanitary ware business is an extension of its tiles production facilities. The company generates 78%-80% of its revenue from sales of ceramic & porcelain tiles and sanitary ware business. The rest of its revenue is generated from the sales of electric water heaters, which contributes around 20%-22% to the top line.

The company also stated that more than 50% of its sales goes towards the distributors,10% is exported and the rest of sales in generated through direct sales to projects and sales from the company’s 32 showrooms.

Sales Channels Revenue Distribution

Source: Saudi CeramicsSource: Saudi Ceramics

Product Classification Variety Capacity

Ceramics and Porcelain Tiles

The company produces ceramic tiles according to international standards

wall tiles, floor tiles and decoration tiles, featuring innovative textures and varnishes, decoration tiles, skirting tiles and tile accessories of different sizes and designs.

52 mn sqm per year of ceramics and porcelain tiles,including 12mn sqm of floor tiles per year

Sanitary Ware The company produces bathroom and toilet Sanitary.

It sell complete sets and single pieces like wash basins, water closets, etc. 2.5mn sanitary ware per year

Electric Water HeatersThe Company manufactures Electrical water heaters in different shapes and sizes. The heater comes with different water storage capacity.

Vertical, horizontal, slim, square, central. 1.5mn electric water heaters per year

Ceramic Road Markers The company produces high visibility ceramic road markers

The makers come in two colors white and yellow 1.8mn ceramic road makers per year

Bathroom Accessories The company also produces a wide variety of bathroom accessories

mirrors, mixers, bathtubs, toilet seat covers, flushing systems, as well as grout and tile adhesive materials and other various materials for the fixing of tiles.

6 million bathroom tile accessories per year

Source: Saudi Ceramics, Zawya

Product Portfolio

D istrib uto rs 5 5 %

E x p o rts 10% O th ers ( Pro j ect & D irect Sales

3 5 % C eram ic T iles and Sanitary W are 7 8%

W ater H eaters 2 2 %

5 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

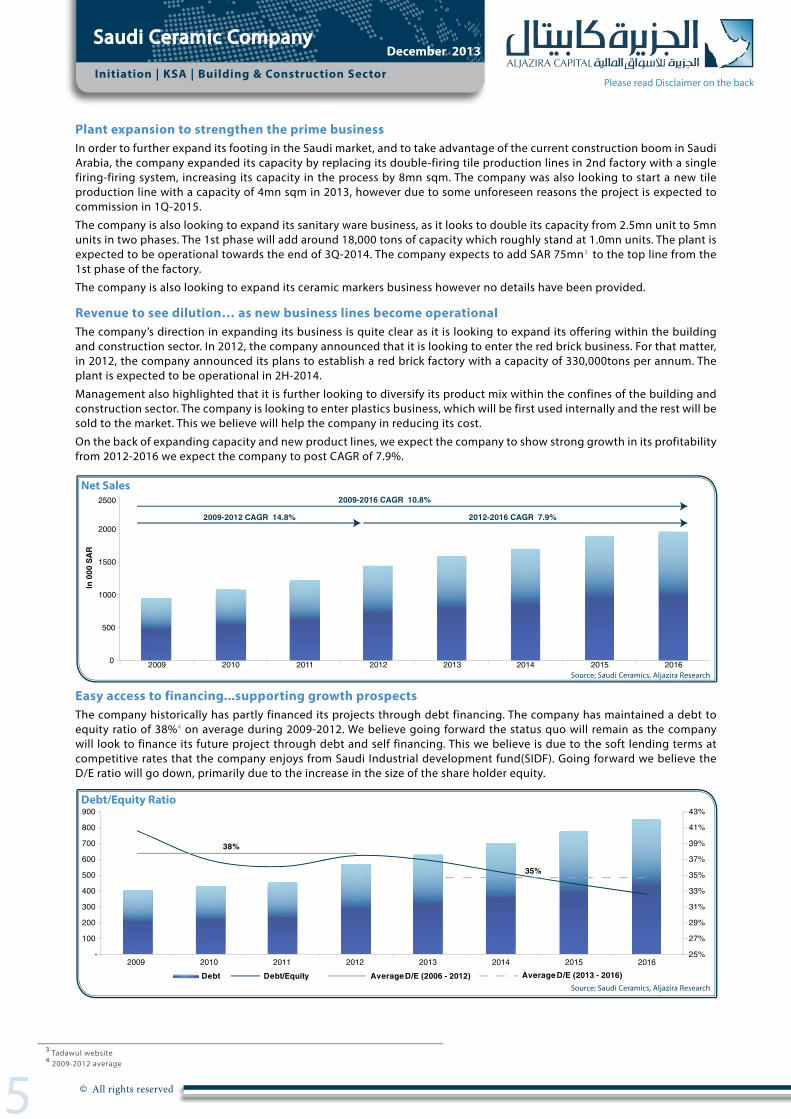

Plant expansion to strengthen the prime businessIn order to further expand its footing in the Saudi market, and to take advantage of the current construction boom in Saudi Arabia, the company expanded its capacity by replacing its double-firing tile production lines in 2nd factory with a single firing-firing system, increasing its capacity in the process by 8mn sqm. The company was also looking to start a new tile production line with a capacity of 4mn sqm in 2013, however due to some unforeseen reasons the project is expected to commission in 1Q-2015.

The company is also looking to expand its sanitary ware business, as it looks to double its capacity from 2.5mn unit to 5mn units in two phases. The 1st phase will add around 18,000 tons of capacity which roughly stand at 1.0mn units. The plant is expected to be operational towards the end of 3Q-2014. The company expects to add SAR 75mn3 to the top line from the 1st phase of the factory.

The company is also looking to expand its ceramic markers business however no details have been provided.

Revenue to see dilution… as new business lines become operationalThe company’s direction in expanding its business is quite clear as it is looking to expand its offering within the building and construction sector. In 2012, the company announced that it is looking to enter the red brick business. For that matter, in 2012, the company announced its plans to establish a red brick factory with a capacity of 330,000tons per annum. The plant is expected to be operational in 2H-2014.

Management also highlighted that it is further looking to diversify its product mix within the confines of the building and construction sector. The company is looking to enter plastics business, which will be first used internally and the rest will be sold to the market. This we believe will help the company in reducing its cost.

On the back of expanding capacity and new product lines, we expect the company to show strong growth in its profitability from 2012-2016 we expect the company to post CAGR of 7.9%.

Easy access to financing...supporting growth prospectsThe company historically has partly financed its projects through debt financing. The company has maintained a debt to equity ratio of 38%4 on average during 2009-2012. We believe going forward the status quo will remain as the company will look to finance its future project through debt and self financing. This we believe is due to the soft lending terms at competitive rates that the company enjoys from Saudi Industrial development fund(SIDF). Going forward we believe the D/E ratio will go down, primarily due to the increase in the size of the share holder equity.

Net Sales

Debt/Equity Ratio

Source; Saudi Ceramics, Aljazira Research

Source; Saudi Ceramics, Aljazira Research

0

500

1000

1500

2000

2500

2009 2010 2011 2012 2013 2014 2015 2016

In 0

00 S

AR

2 009 - 2 016 C AG R 10. 8%

2 012 - 2 016 C AG R 7 . 9 %2 009 - 2 012 C AG R 14 . 8%

3 8%

3 5 %

25%

27%

29 %

31%

33%

35%

37%

39 %

41%

43%

-

100

200

300

400

500

600

700

800

9 00

2009 2010 2011 2012 2013 2014 2015 2016D eb t D eb t/ E q uity Average D / E ( 2 006 - 2 012 ) Average D / E ( 2 013 - 2 016)

3 Tadawul website4 2009-2012 average

6 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

Source: Bloomberg

Fuel Allocation to new plants

The company receives fuel at a subsidized rates. All the company’s factories are run on subsidized fuel. However due to the on-going efforts by the government to curb fuel usage, the company is finding it hard to get allocation for its new factories. We believe, in-line with the governments initiative to provide affordable housing for the masses, it will be a conflict of interest for the government to stop fuel allocation for the building and construction sector.

Chinese Dumping a threat

Ceramic tiles from China has been treated as a threat from multiple countries as they are selling below the manufacturing cost. Countries like Brazil, Argentina, India and countries from the European Union has put an anti-dumping duty, on Chinese ceramic products in order to control irrational pricing.

Saudi Ceramics is also facing competition from the Chinese imports, as according to the company the selling price of Chinese products is even below the cost of production, the company is pushing hard for an anti-dumping duty on Chinese products in-order to level the playing field.

Electric Water Heater margins- a function of steel price

The company water heater business margins are inversely related to steel prices, due to which the profitability of the division swings with the change in steel prices. Going forward we believe without the absence of any hedging the margins will fluctuate with the changes in the steel prices.

618

601

480

530

580

630

680

730

Mar - 12 May - 12 Jul - 12 Sep - 12 Nov - 12 Mar - 13 May - 13 Jul - 13 Sep - 13 Nov - 13

Steel Price Annual Average Prices

Jan - 12 Jan - 13

Chinese Hot Roll Steel Prices

7 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

Amount in SARmn, unless otherwise specified 2011 2012 2013 e 2014 e 2015 e 2016 e

Income StatementNet Sales 1,221 1,447 1,515 1,711 1,829 1,884 % Growth 13% 19% 5% 13% 7% 3%Cost of Sales (775) (973) (1,019) (1,086) (1,160) (1,195)Gross Income 446 474 496 624 669 690 Selling and marketing expenses (137) (157) (161) (180) (187) (188)General and Administrative expenses (65) (60) (62) (71) (75) (78)Income from main operations 244 258 273 374 407 423 % Growth 10% 6% 6% 37% 9% 4%Financing cost (17) (16) (17) (20) (24) (24)Other revenues and expenses , net 13 15 15 18 19 19 Net income before Zakat 239 256 271 373 403 418 Zakat provision (7) (9) (9) (12) (13) (14)Net income 232 248 262 360 389 404 % Growth 5% 7% 6% 37% 8% 4%Balance Sheet Assets Current Assets Cash and equivalent 64 57 100 145 366 608 Account Receivable, net 136 132 173 159 204 206 Inventories,net 535 598 627 712 762 785 Prepayments and other assets 57 106 82 97 105 114 Total current assets 793 893 981 1,113 1,437 1,713 Non-current assets Investments and financial assets 61 81 81 81 81 81 Project under construction 277 284 284 284 284 284 Property, Plant and Equipment,net 1,138 1,288 1,439 1,682 1,812 1,957 Loan to associate company - - - - - - Total non-current assets 1,476 1,653 1,803 2,047 2,177 2,322 TOTAL ASSETS 2,269 2,546 2,784 3,160 3,614 4,035 Liabilities and Shareholders Equity Current Liabilities Short term loans 160 120 126 142 152 156 Accounts payable 175 201 230 224 262 262 Notes payables due within a year 12 11 11 11 11 11 Accruals and other liability 78 73 - - - - Current Portion of Short term loans 195 213 255 277 310 335 Total current liabilities 620 618 622 654 735 764 Non-current liabilities Notes payables Long term loans 454 570 632 704 776 853 Employees end of service benefits 48 52 52 52 52 52 Total non-current liabilities 502 622 683 756 828 904 Total Liabilities 1,122 1,240 1,305 1,410 1,563 1,669 Shareholders Equity Share capital 250 375 375 375 375 375 Statutory reserve 125 150 150 150 150 150 Retained earnings 769 778 952 1,223 1,523 1,839 Unrealized gain from avaliable-for-sale securities 2 3 3 3 3 3 Total Shareholders' Equity 1,147 1,306 1,479 1,750 2,051 2,366 TOTAL LIABILITIES & SHAREHOLDERS' EQUITY 2,269 2,546 2,784 3,160 3,614 4,035 Cash Flow Cash Flow from:Operating Activities 350 297 390 435 514 576 Investing Activities (285) (310) (293) (410) (314) (346)Financing Activities (40) 6 (55) 20 22 12 Changes in Cash 25 (7) 42 45 221 242 Cash Opening Balance 39 64 57 100 145 366 Cash Ending Balance 64 57 100 145 366 608

Source: Aljazira Research

Key financial data

8 © All rights reserved

Please read Disclaimer on the back

Saudi Ceramic Company

Initiation | KSA | Building & Construction Sector

December 2013

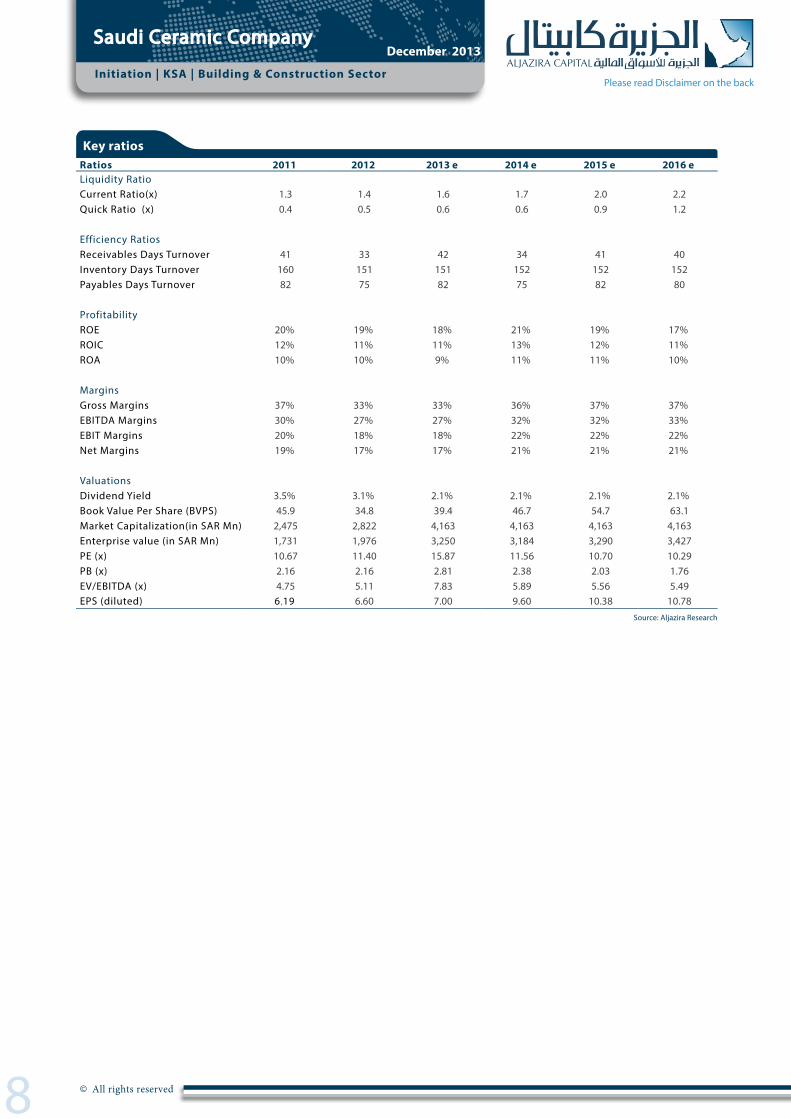

Key ratiosRatios 2011 2012 2013 e 2014 e 2015 e 2016 eLiquidity RatioCurrent Ratio(x) 1.3 1.4 1.6 1.7 2.0 2.2 Quick Ratio (x) 0.4 0.5 0.6 0.6 0.9 1.2

Efficiency Ratios Receivables Days Turnover 41 33 42 34 41 40 Inventory Days Turnover 160 151 151 152 152 152 Payables Days Turnover 82 75 82 75 82 80

Profitability ROE 20% 19% 18% 21% 19% 17%ROIC 12% 11% 11% 13% 12% 11%ROA 10% 10% 9% 11% 11% 10%

MarginsGross Margins 37% 33% 33% 36% 37% 37%EBITDA Margins 30% 27% 27% 32% 32% 33%EBIT Margins 20% 18% 18% 22% 22% 22%Net Margins 19% 17% 17% 21% 21% 21%

Valuations Dividend Yield 3.5% 3.1% 2.1% 2.1% 2.1% 2.1%Book Value Per Share (BVPS) 45.9 34.8 39.4 46.7 54.7 63.1 Market Capitalization(in SAR Mn) 2,475 2,822 4,163 4,163 4,163 4,163 Enterprise value (in SAR Mn) 1,731 1,976 3,250 3,184 3,290 3,427 PE (x) 10.67 11.40 15.87 11.56 10.70 10.29 PB (x) 2.16 2.16 2.81 2.38 2.03 1.76 EV/EBITDA (x) 4.75 5.11 7.83 5.89 5.56 5.49 EPS (diluted) 6 ٫19 6.60 7.00 9.60 10.38 10.78

Source: Aljazira Research

RESE

ARC

H D

IVIS

ION

RESE

ARC

H

DIV

ISIO

NRA

TIN

GTE

RMIN

OLO

GY

BRO

KERA

GE A

ND IN

VEST

MEN

T CE

NTER

S DI

VISI

ON

Disclaimer

AlJazira Capital, the investment arm of Bank AlJazira, is a Shariaa Compliant Saudi Closed Joint Stock company and operating under the regulatory supervision of the Capital Market Authority. AlJazira Capital is licensed to conduct securities business in all securities business as authorized by CMA, including dealing, managing, arranging, advisory, and custody. AlJazira Capital is the continuation of a long success story in the Saudi Tadawul market, having occupied the market leadership position for several years. With an objective to maintain its market leadership position, AlJazira Capital is expanding its brokerage capabilities to o�er further value-added services, brokerage across MENA and International markets, as well as o�ering a full suite of securities business.

1. Overweight: This rating implies that the stock is currently trading at a discount to its 12 months price target. Stocks rated “Overweight” will typically provide an upside potential of over 10% from the current price levels over next twelve months.

2. Underweight: This rating implies that the stock is currently trading at a premium to its 12 months price target. Stocks rated “Underweight” would typically decline by over 10% from the current price levels over next twelve months.

3. Neutral: The rating implies that the stock is trading in the proximate range of its 12 months price target. Stocks rated “Neutral” is expected to stagnate within +/- 10% range from the current price levels over next twelve months.

4. Suspension of rating or rating on hold (SR/RH): This basically implies suspension of a rating pending further analysis of a material change in the fundamentals of the company.

The purpose of producing this report is to present a general view on the company/economic sector/economic subject under research, and not to recommend a buy/sell/hold for any security or any other assets. Based on that, this report does not take into consideration the specific financial position of every investor and/or his/her risk appetite in relation to investing in the security or any other assets, and hence, may not be suitable for all clients depending on their financial position and their ability and willingness to undertake risks. It is advised that every potential investor seek professional advice from several sources concerning investment decision and should study the impact of such decisions on his/her financial/legal/tax position and other concerns before getting into such investments or liquidate them partially or fully. The market of stocks, bonds, macroeconomic or microeconomic variables are of a volatile nature and could witness sudden changes without any prior warning, therefore, the investor in securities or other assets might face some unexpected risks and fluctuations. All the information, views and expectations and fair values or target prices contained in this report have been compiled or arrived at by Aljazira Capital from sources believed to be reliable, but Aljazira Capital has not independently verified the contents obtained from these sources and such information may be condensed or incomplete. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this report. Aljazira Capital shall not be liable for any loss as that may arise from the use of this report or its contents or otherwise arising in connection therewith. The past performance of any investment is not an indicator of future performance. Any financial projections, fair value estimates or price targets and statements regarding future prospects contained in this document may not be realized. The value of the security or any other assets or the return from them might increase or decrease. Any change in currency rates may have a positive or negative impact on the value/return on the stock or securities mentioned in the report. The investor might get an amount less than the amount invested in some cases. Some stocks or securities maybe, by nature, of low volume/trades or may become like that unexpectedly in special circumstances and this might increase the risk on the investor. Some fees might be levied on some investments in securities. This report has been written by professional employees in Aljazira Capital, and they undertake that neither them, nor their wives or children hold positions directly in any listed shares or securities contained in this report during the time of publication of this report, however, The authors and/or their wives/children of this document may own securities in funds open to the public that invest in the securities mentioned in this document as part of a diversified portfolio over which they have no discretion. This report has been produced independently and separately by the Research Division at Aljazira Capital and no party (in-house or outside) who might have interest whether direct or indirect have seen the contents of this report before its publishing, except for those whom corporate positions allow them to do so, and/or third-party persons/institutions who signed a non-disclosure agreement with Aljazira Capital. Funds managed by Aljazira Capital and its subsidiaries for third parties may own the securities that are the subject of this document. Aljazira Capital or its subsidiaries may own securities in one or more of the aforementioned companies, and/or indirectly through funds managed by third parties. The Investment Banking division of Aljazira Capital maybe in the process of soliciting or executing fee earning mandates for companies that is either the subject of this document or is mentioned in this document. One or more of Aljazira Capital board members or executive managers could be also a board member or member of the executive management at the company or companies mentioned in this report, or their associated companies. No part of this report may be reproduced whether inside or outside the Kingdom of Saudi Arabia without the written permission of Aljazira Capital. Persons who receive this report should make themselves aware, of and adhere to, any such restrictions. By accepting this report, the recipient agrees to be bound by the foregoing limitations.

Asset Management Brokerage Corporate Finance Custody Advisory

Head Office: Madinah Road, Mosadia، P.O. Box: 6277, Jeddah 21442, Saudi Arabia، Tel: 02 6692669 - Fax: 02 669 7761

Aljazira Capital is a Saudi Investment Company licensed by the Capital Market Authority (CMA), license No. 07076-37

AGM - Head of ResearchAbdullah Alawi+966 12 [email protected]

Senior Analyst Syed Taimure Akhtar +966 12 6618271 [email protected]

Senior Analyst

Talha Nazar +966 12 [email protected]

Analyst

Saleh Al-Quati+966 12 [email protected]

Analyst

Jassim Al-Jubran +966 12 [email protected]

General Manager - Brokerage DivisionAla’a Al-Yousef+966 11 [email protected]

AGM-Head of international

and institutional brokerageLuay Jawad Al-Motawa +966 11 [email protected]

Regional Manager - West and South Regions

Abdullah Al-Misbahi+966 12 [email protected]

Sales And Investment Centers Central Region

Manger

Sultan Ibrahim AL-Mutawa +966 11 [email protected]

Area Manager - Qassim & Eastern Province

Abdullah Al-Rahit+966 16 [email protected]

AGM - Head of Institutional Brokerage

Samer Al- Joauni +966 1 225 6352 [email protected]