sbf national business survey 2014/2015

TRANSCRIPT

Slide 1 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

SBF NATIONAL BUSINESS

SURVEY

2014/2015 Supported by:

Slide 2 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

SURVEY OBJECTIVES

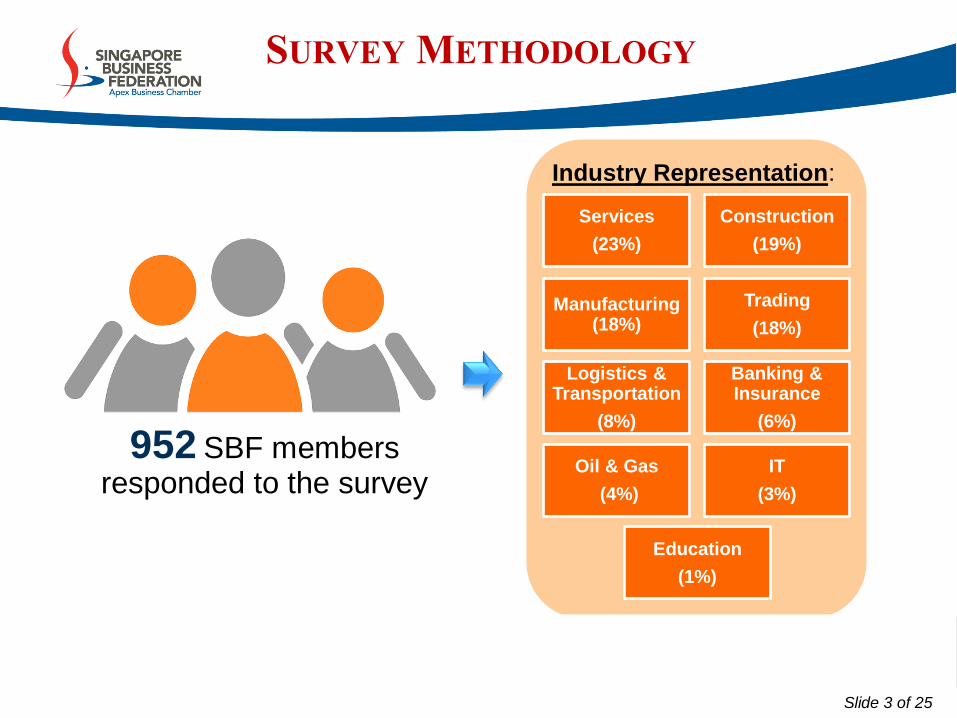

Slide 3 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

952 SBF members responded to the survey

Industry Representation:

Services

(23%)

Construction

(19%)

Manufacturing (18%)

Trading

(18%)

Logistics & Transportation

(8%)

Banking & Insurance

(6%)

Oil & Gas

(4%)

IT

(3%)

Education

(1%)

SURVEY METHODOLOGY

Slide 4 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

1 to 20 21 to 50 51 to 100 101 to 300 >300

2014 2013

More higher-headcount firms (>100) shared views this year

31% representation

Services (▲28%), IT (▲12%) & Oil & Gas (▲11%) registered higher increases

More in IT (▲15%) have fewer than 20 staff

CHARACTERISTIC #1: STAFF STRENGTH

Slide 5 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

More in IT (▲10%) and Services (▲4%) generating more than $100m

Contributed by stimulus from roll out of government schemes like the Enhanced PIC

Fewer Banking & Insurance companies with larger turnover, likely due to on-going regulatory changes

such as reduction of Quantitative Easing (QE)

Business Sector

Turnover

Up to

S$1m

> S$1m to

S$5m

> S$5m to

S$20m

> S$20m to

S$50m

> S$50m to

S$100m > S$100m

Banking & Insurance 17% 31% 19% 15% 7% 11%

Construction 12% 15% 36% 17% 12% 8%

Education* - 39% 15% 31% 15% -

IT 10% 29% 33% 6% 6% 16%

Logistics & Transportation 10% 23% 26% 17% 11% 13%

Manufacturing 4% 14% 37% 22% 6% 17%

Oil & Gas 5% 15% 10% 26% 18% 26%

Services 14% 18% 33% 14% 7% 14%

Trading 7% 22% 33% 17% 5% 16%

Overall 2014 10% 19% 31% 17% 9% 14%

2013 11% 20% 28% 15% 9% 17%

CHARACTERISTIC #2: TURNOVER

Slide 6 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

46% remained unclear of the impact from current global economy climate

More see optimism in the current global economic climate

IT register the highest increase (▲11%)

as more companies spend on productivity/

automation initiatives

Construction (▲4%) share the same

sentiments despite manpower constraints,

as level of public projects stays high

IMPACT OF GLOBAL ECONOMY CLIMATE

Slide 7 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Most continue to stay positive towards Singapore’s growth

Larger companies (i.e. MNC,

GLC/TLC & Local Large) are

comparably more positive

Slight muted outlook is partially

contributed by tight foreign labour

curbs and restructuring cost

CONFIDENCE LEVEL IN LOCAL

ECONOMIC GROWTH

Slide 8 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Manpower costs continue to trouble SMEs the most

4 in 5 affected by the high labour costs

(▲10%)

Uneven global economic performance

across US, China & Europe keeps 56%

guessing as to the overall direction of

economic environment in 2015

CHALLENGES: NEXT 6 TO 12 MONTHS

Slide 9 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Competition and Growth potential remained as top 2 concerns

62% affected by the strong

competition, supported by an open

market policy in Singapore

3rd highest is Reduction in Gross

Margin due to cost structure in

Singapore

Payments delay expected to

trouble more companies (▲5%)

* Option not available in previous questionnaire

CHALLENGES: SALES-RELATED

Slide 10 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Managing labour-related costs remains vital in sustaining profits

91% (▲3%) viewed wage cost

contributes the most to their profitability

More affected by high labour costs

(86%), a result of tightening workforce &

foreign labour quota

Rental also affecting more SBF members

this year

97% foresee higher operational

expenditure in 2015

CHALLENGES: COST COMPETITIVENESS

Slide 11 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Investing to Stay Productive and Cost Efficient (71%) – Remains the Key Business Strategy Moving Forward

With manpower issues looming,

42% are looking at Staff Retention/

Fill Existing Positions

24% are relooking their current

business model

* Option not available in previous questionnaire

KEY BUSINESS STRATEGIES

Slide 12 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

* Option not available in previous questionnaire

Increasing workers’ efficiency as a key measure in combating high labour costs

54% (▲10%) are looking to

expanding workers’ capabilities

More (▲4%) intend to invest in

machinery & equipment to further

improve productivity

13% will invest in R&D

More turning to Business Consultants

(12%)

2015 INVESTMENTS PLANS

Slide 13 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Members’ overseas presence increased in 2014

Larger MNC and Local Large enterprises

engaged more business in overseas

All sectors are seen having an increase in

overseas presence, except for Oil & Gas

Asia tops the highest overseas presence

among members

72% (▲10%) are exploring for more

business opportunities overseas, with

51% generating up to 50% in

overseas revenue

Overseas Presence by Region 2014 2013 2012

Asia 97% 96% 94%

Europe 18% 22% 22%

Middle East 17% 18% 21%

Oceania 12% 12% 14%

Americas 12% 20% 21%

Africa 9% 9% 10%

OVERSEAS PRESENCE

Slide 14 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

More have interest in developing countries

Malaysia sees continued strong

interest

Indonesia (53%) replaced China as

the second highest destination

Political stability and labour relation

continues to rank high as seen in

lower interest towards Thailand

(▼4%) and Vietnam (▼2%)

Top 5 Asian Countries

OVERSEAS PRESENCE

Slide 15 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Asian countries are gaining attention from members

Europe dropped out of the top 10, due to its patchy economic performance

Emerging markets like Myanmar (36%) and Cambodia (24%) see increased interests

Post election political stability in Indonesia helped renew interest

Top 3 Countries Venturing Into

OVERSEAS PRESENCE

Slide 16 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Rank

No. Key Obstacles Faced Overseas 2014 2013 2012

1 Competition From Companies Already Established in the Country 50% 55% 56%

2 Unclear Rules & Regulations 33% 32% 31%

Lack of Overseas Business Knowledge & Information 33% 25% 26%

3 Manpower Issues 28% 30% 28%

4 Compliance Issues 25% 24% 20%

5 Lack of Business Contact 21% 21% 24%

Customs Related Issues 21% 21% 18%

6 Funding 17% 11% 13%

Strong In-Country competition and lack of knowledge remains the top key challenges for our SBF members

New entrants to overseas markets need help with overseas business knowledge (▲8%)

Funding challenges also affecting more companies

CHALLENGES FACED OVERSEAS

Slide 17 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

More than half (60%) are aware of AEC

70% believes AEC will present business opportunities

More of the Local Large Enterprises are optimistic about AEC

More knowledge sharing needs to be done on the full details of AEC with those that find it a

threat (3%)

ASEAN ECONOMIC COMMUNITY 2015

Slide 18 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

1 in 3 has difficulties keeping up the pace of the restructuring

Manpower constraints and high costs limit ability

in Construction (40%) & Manufacturing (35%) to

keep pace

GLC/ TLC (40%) not immune to restructuring

pains

32% of SME members find the pace too fast

23% of Local Large Enterprises find the pace too

slow

Company Category Pace of Economic Restructuring

Total Too fast Just nice Too slow

SME 32% 58% 10% 100%

MNC 24% 68% 8% 100%

GLC / TLC 40% 50% 10% 100%

Local Large Enterprise 24% 53% 23% 100%

Overall 31% 59% 10% 100%

ECONOMIC RESTRUCTURING

Slide 19 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

4 in 5 have plans to cope with the restructuring

More in Local Large Enterprises (91%), Education (92%) and Manufacturing (88%) have taken

measures to cope

Investing in staff productivity and streamlining operations stay as the key measures to address

restructuring challenges

Of concern, 12% have no counter measures

IMPACT OF ECONOMIC RESTRUCTURING

Slide 20 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

More local staff to be hired in the near term

Net balance increase of 33% for

Full-time, and 17% for Part-time

More from Oil & Gas (54%), IT

(45%) and Services (41%) are

expecting to hire more Local Full-

time staff to address short-fall in

foreign workforce

IMPACT ON STAFF HEADCOUNT

Slide 21 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

More have gained from initiatives introduced in 2013 budget

82% have gain from PIC

Bonus

▲31% benefited from

Corporate Tax rebate

▲28% benefitted WCS

1 in 10 failed to gain from

WCS (12%)

2013/ 2014 BUDGET SCHEMES

Slide 22 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

New Initiatives or Enhancements

Awareness of Schemes in Budget 2014

Not aware Aware Not

applicable

Not

Answered

Extension & Enhancement to PIC Scheme 4% 88% 8% 2%

Extension of Tax Deduction on Qualifying R&D Expenditure 11% 43% 46% 9%

Extension of Writing Down Allowance for Cost of Acquiring IP

Rights 18% 28% 54% 9%

Extension of Land Intensification Allowance Scheme 23% 20% 57% 9%

Top-up to Lifelong Learning Endowment Fund 32% 26% 42% 9%

ICT for Productivity & Growth Programme 25% 39% 36% 9%

Overall 1%* 96%** 2%*** 1%****

* answered not aware of all schemes ** answered aware for at least 1 scheme

*** answered not applicable for all schemes **** did not answer this question

Enhanced budget schemes have benefited more firms 88% are aware of the enhanced PIC Scheme, and 67% of this find the scheme effective

Tax Deduction on Qualifying R&D expenditure and ICT for Productivity & Growth Programme are

equally popular

More interest and awareness needed for Top-Up to Lifelong Learning Endowment Fund & Enhancement to Global Company Partnership Programme

2014 BUDGET SCHEMES

Slide 23 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Enhanced Budget measures have brought more assistance to SBF members

▲14% felt that the measures are

useful this year

More in Construction (59%) &

Services (59%) sees benefits from

2014 measures as focus shifted

towards productivity adoption

measures

USEFULNESS OF BUDGET SCHEMES

Slide 24 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Help with reducing business costs stays as top concern (62%)

34% hope to see a more granular foreign

worker policies; especially within

Construction, Manufacturing, IT & Services

18% hope for better incentives for

capability building

17% of SMEs looking for assistance with

overseas business expansion

Concept of portable employee medical

benefits also gaining traction with members

(13%)

To help enlarge workforce, more are

hoping to tap on polys & ITE students and

attract economically inactive

* Option not available in previous questionnaire

WISHLIST FOR BUDGET 2015

Slide 25 of 25

© DP Information Network Pte Ltd. All rights reserved.

Commercial Confidential

Training and retaining workers the key drive to improve overall productivity

1 in 2 chose Training & Skills

Development to improve productivity

More from Banking & Insurance (79%)

hope for more training funds

Difficulties in finding the right talent due to

manpower constraint has led to more in

Construction and IT (58%; 58%) seeing the

importance of retaining workers

WISHLIST FOR BUDGET 2015