schorn speaks at cowen & company energy & natural

TRANSCRIPT

Patrick SchornExecutive Vice President, New Ventures

Cowen & Company

7th Annual Energy & Natural Resources Conference

New York, December 4, 2017

This presentation contains “forward-looking statements” within the meaning of the federal securities laws — that is,statements about the future, not about past events. Such statements often contain words such as “expect,” “may,”“believe,” “plan,” “estimate,” “intend,” “anticipate,” “should,” “could,” “will,” “see,” “likely,” and other similar words.Forward-looking statements address matters that are, to varying degrees, uncertain, such as statements about ourfinancial and performance targets and other forecasts or expectations regarding business outlook; growth forSchlumberger as a whole and for each of its segments (and for specified products or geographic areas within eachsegment); oil and natural gas demand and production growth; oil and natural gas prices; improvements in operatingprocedures and technology, including our transformation program; capital expenditures by Schlumberger and the oil andgas industry; the business strategies of Schlumberger’s customers; the success of Schlumberger’s SPM projects, jointventures and alliances; future global economic conditions; and future results of operations. These statements aresubject to risks and uncertainties, including, but not limited to, global economic conditions; changes in exploration andproduction spending by Schlumberger’s customers and changes in the level of oil and natural gas exploration anddevelopment; general economic, political and business conditions in key regions of the world; foreign currency risk;pricing pressure; weather and seasonal factors; operational modifications, delays or cancellations; production declines;changes in government regulations and regulatory requirements, including those related to offshore oil and gasexploration, radioactive sources, explosives, chemicals, hydraulic fracturing services and climate-related initiatives; theinability of technology to meet new challenges in exploration; the inability to retain key employees; and other risks anduncertainties detailed in our most recent Forms 10-K, 10-Q, and 8-K filed with or furnished to the U.S. Securities andExchange Commission. If one or more of these or other risks or uncertainties materialize (or the consequences of sucha development changes), or should underlying assumptions prove incorrect, actual outcomes may vary materially fromthose reflected in our forward-looking statements. The forward-looking statements speak only as of the date of thispresentation, and Schlumberger disclaims any intention or obligation to update publicly or revise such statements,whether as a result of new information, future events or otherwise.

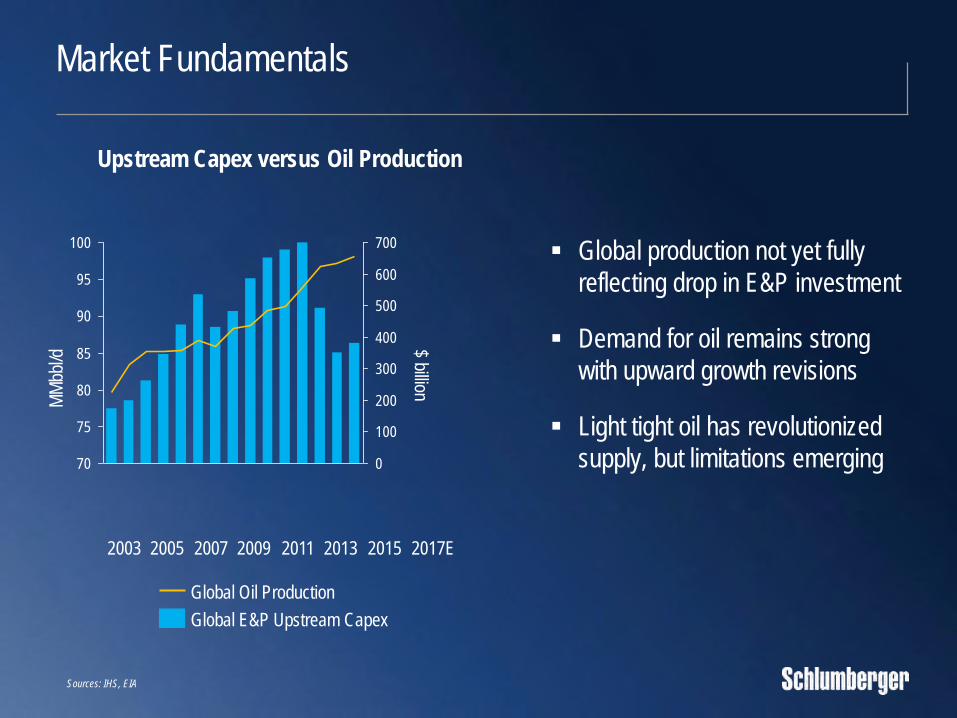

Market Fundamentals

Sources: IHS, EIA

0

100

200

300

400

500

600

700

70

75

80

85

90

95

100

$ billion

MM

bbl/d

2017E20152009 20112003 2007 20132005

Global E&P Upstream Capex

Global Oil Production

Upstream Capex versus Oil Production

▪ Global production not yet fully

reflecting drop in E&P investment

▪ Demand for oil remains strong

with upward growth revisions

▪ Light tight oil has revolutionized

supply, but limitations emerging

Light Tight Oil Revolutionized Supply—But Limits Emerge

Sources: IHS, EIA ; * Nov 2017 EIA

2008-2017 Global E&P Capex ($ trillion)

2017 Estimated Oil Supply (MMbbl/d)

$4.2T

$1.1T

All other E&P

Land unconventional

93 MMbbl/d

5

US tight oil

All other oil supply

▪ Forecast rates of production growth

slowing in the medium term

▪ Pursuit of growth now balanced by

stronger focus on financial performance

▪ Investment in light tight oil has reached

one-fifth of total E&P investment

▪ Well spacing and completion volumes

may be reaching technology limit

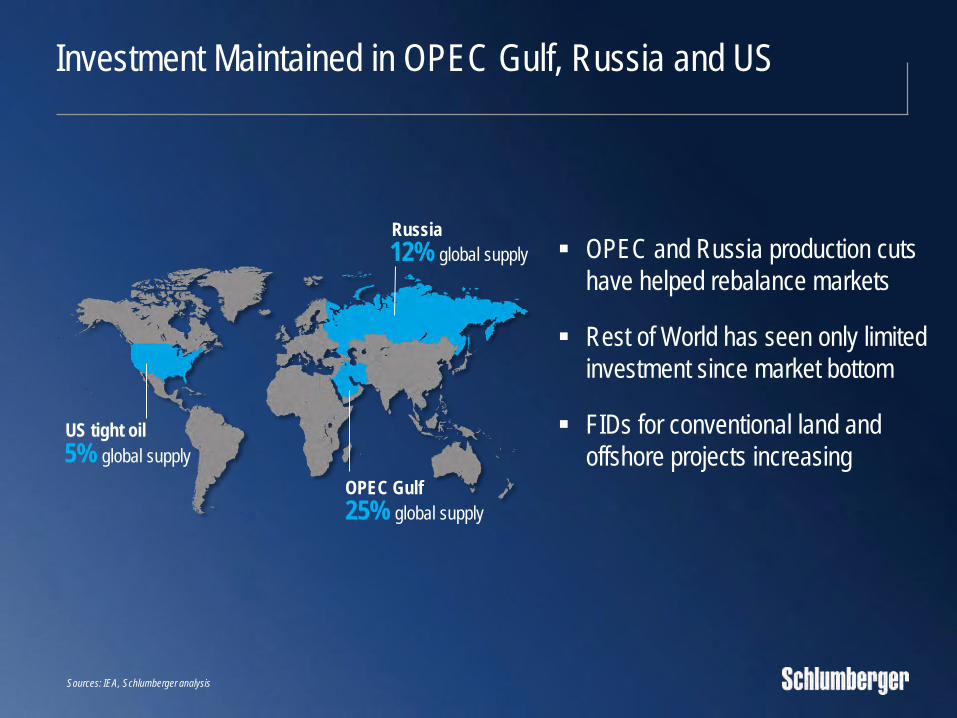

Investment Maintained in OPEC Gulf, Russia and US

Sources: IEA, Schlumberger analysis

Russia

12% global supply

US tight oil

5% global supply

OPEC Gulf

25% global supply

▪ OPEC and Russia production cuts

have helped rebalance markets

▪ Rest of World has seen only limited

investment since market bottom

▪ FIDs for conventional land and

offshore projects increasing

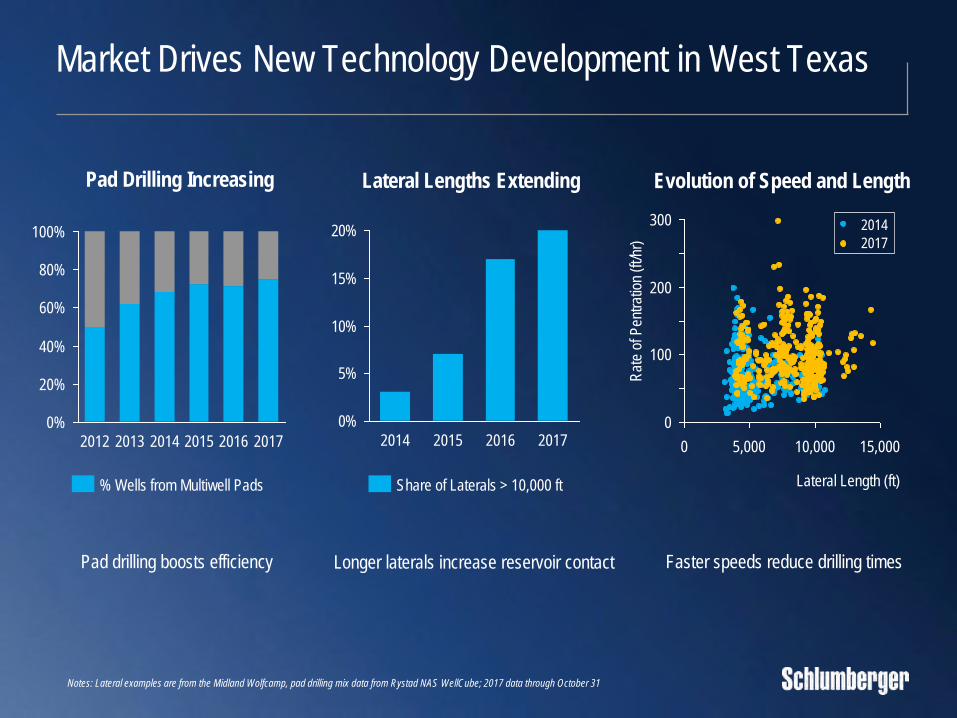

Notes: Lateral examples are from the Midland Wolfcamp, pad drilling mix data from Rystad NAS WellCube; 2017 data through October 31

Market Drives New Technology Development in West Texas

Lateral Lengths ExtendingPad Drilling Increasing

Pad drilling boosts efficiency Longer laterals increase reservoir contact Faster speeds reduce drilling times

0%

80%

20%

100%

60%

40%

2013 201720152012 2014 2016

0%

5%

10%

15%

20%

2017201620152014

Share of Laterals > 10,000 ft% Wells from Multiwell Pads

Evolution of Speed and Length

0

300

15,0000 5,000

200

100

10,000

Lateral Length (ft)

Rat

e of

Pen

trat

ion

(ft/h

r) 2017

2014

Note: Cost of ownership includes compensation, maintenance and capex per job; 2017 data through October 31

Transformation Improves Internal Efficiency in US Land

Asset Utilization Improving Remote Operations Expanding

Cost of Ownership Decreasing Tool Reliability Increasing

0

20

40

60

80

100

-32%

xBolt

%

TelePacer

500

1,500

2,500

0

xBoltTelePacer

+17%

Hrs

/Fai

lure

0

2

4

6

8

20172015

Tool

s/Jo

b

-49%

2016

0

10

20

30

40

2017

+149%

2014 2016

%

2015

PowerDrive RSS Technology Drives Performance in US Land

7-Well Campaign for

Eclipse Resources in Ohio

Average Lateral Footage Per Well

Average Days Per Well

Cost Per Lateral

80-Well Campaign for

Parsley Energy in West Texas

5,000

10,000

15,000

20,000

25,000

30,000

0 2 4 6 8 10 12

Mea

sure

d D

epth

(ft)

Drilling Time (days)

Seventh well 5 days

First well 10 days

+9%-17% -30%

2015

2016

Note: Cost of ownership includes compensation, maintenance and capex per job

▪ Drill time halved between first and seventh wells

▪ Two record-breaking laterals >20k feet drilled in October

▪ All seven wells drilled fully in geological window

▪ Drilling cost per lateral reduced by 30%

▪ Total lateral footage drilled per well extended by 9%

▪ 7,128-ft lateral drilled in 1.7 days

Transforming Completions and Production—OneStim

Improving Asset Utilization and Reducing Unit Cost—OneStim

Operations Planning

Global Traceability

▪ Sand volume doubled since 2014

▪ Asset utilization increased by 30%

▪ Unit cost reduced by 56%

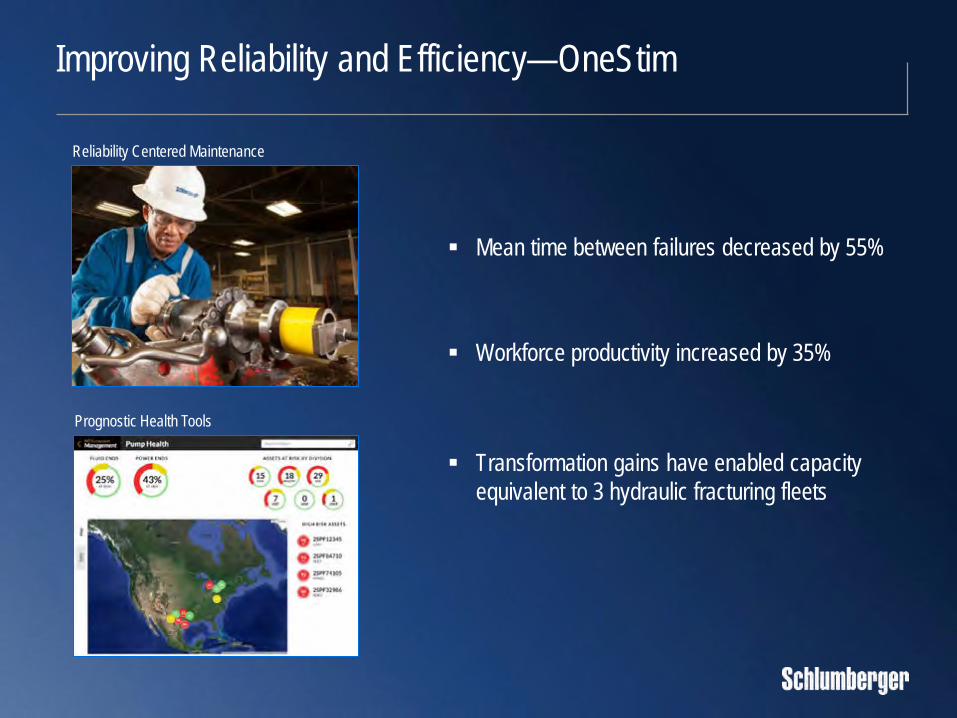

Improving Reliability and Efficiency—OneStim

Reliability Centered Maintenance

Prognostic Health Tools

▪ Mean time between failures decreased by 55%

▪ Workforce productivity increased by 35%

▪ Transformation gains have enabled capacity

equivalent to 3 hydraulic fracturing fleets

New Generation Hydraulic Fracturing Equipment—OneStim

Activity since introduction in 2017

Stages completed: 3,732

Wells completed: 128

Operating time: 26,143 hours

Connecting E&P Workflows with Digital Enablement

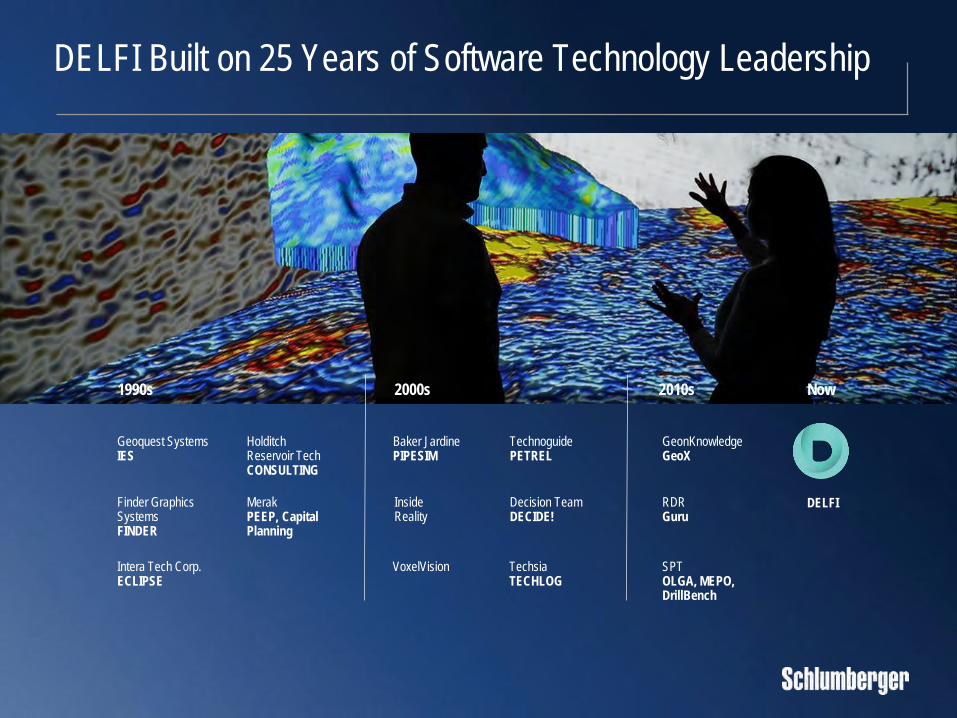

DELFI Built on 25 Years of Software Technology Leadership

1990s

Geoquest SystemsIES

HolditchReservoir TechCONSULTING

Finder Graphics SystemsFINDER

Intera Tech Corp.ECLIPSE

MerakPEEP, Capital Planning

TechnoguidePETREL

Baker JardinePIPESIM

InsideReality

VoxelVision

Decision TeamDECIDE!

TechsiaTECHLOG

SPTOLGA, MEPO, DrillBench

GeonKnowledgeGeoX

RDRGuru

DELFI

2000s 2010s Now

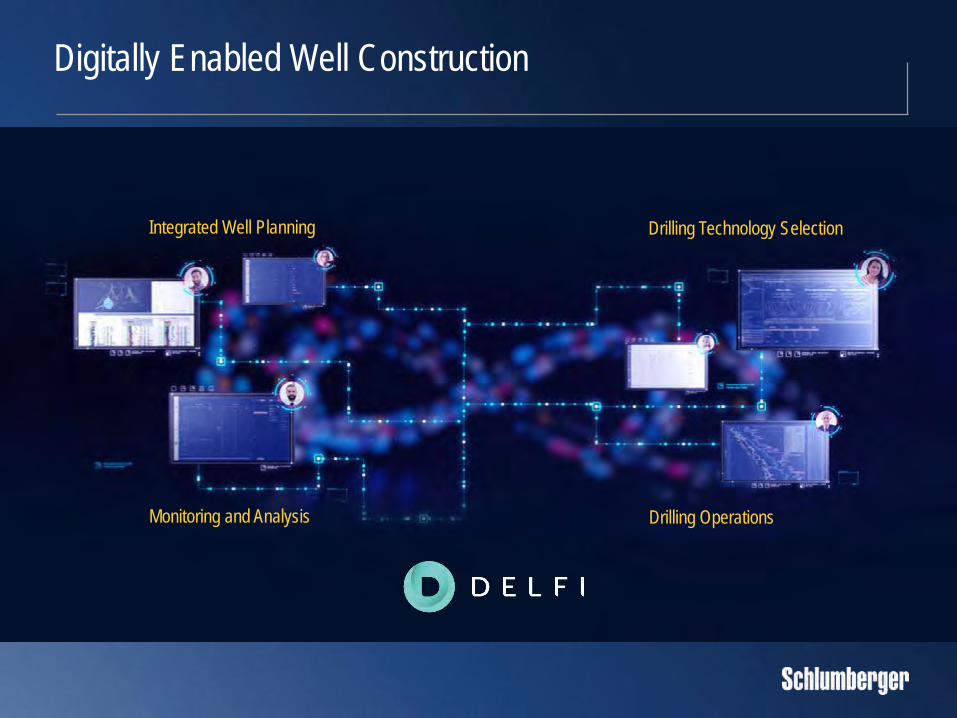

Digitally Enabled Well Construction

Integrated Well Planning Drilling Technology Selection

Monitoring and Analysis Drilling Operations

Fourth-Quarter Sequential Outlook

Reservoir Characterization Group – Lower▪ Northern hemisphere seasonal reductions across several product

lines and muted year-end multiclient and software sales

Drilling Group – Flat ▪ Higher drilling in North America land offset by seasonal decline in the

Northern Hemisphere following Q3 strong summer drilling campaigns

Production Group – Higher

▪ Continued growth in North America land with full quarter benefit from

capacity redeployment although moderated by seasonality

Cameron Group – Modestly Higher

▪ Surface and V&M higher on robust North America activity partially

offset by slowing decline in OneSubsea and Drilling Systems

▪ NAM land growth continues—moderated by holiday season

and rig count flattening

▪ Modest growth in Latin America and Middle East,

Europe/Africa/Central Asia lower on winter seasonality

▪ Year-end product sales muted

Summary

▪ The narrowing gap between oil supply and demand is leading commodity prices

higher. We are increasingly positive on the outlook for our global business

▪ We continue to invest in our business, and our technology leadership coupled with

increasing digital enablement provides a foundation to leverage market recovery

▪ Our multiyear transformation program continues to contribute to performance while

innovative technology development meets evolving market needs

▪ We are confident that our financial strength, geographical footprint and technology

portfolio position us as the oilfield services leader as the market moves to recovery