scotts investor deck

TRANSCRIPT

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 1/102

Annual Analyst Day

February 23, 2011

Boca Raton, Florida

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 2/102

2

Today’s Agenda

Jim Hagedorn, Chairman & Chief Executive OfficerOur vision to evolve into a more consumer-focused company continues

Barry Sanders, President

An update on Regionalization

An expanded and in-depth look at opportunities in our key categories

Dave Evans, CFO & EVP of Strategic Planning and Business Development

2011 outlook, financial goals and objectives

The evolving role of Business Development

Store visits

Lunch / Q&A

Season-to-date update

Highlights of store visits

Claude Lopez, President of Global Sales

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 3/102

3

Safe Harbor Disclosure

•Statement under the Private Securities Litigation Act of 1995: Certain of the

statements contained in this presentation, including, but not limited to,

information regarding the future economic performance and financial condition

of the company, the plans and objectives of the company’s management, and

the company’s assumptions regarding such performance and plans are forward-

looking in nature. Actual results could differ materially from the forward-lookinginformation in this presentation due to a variety of factors.

•

•The Scotts Miracle-Gro Company encourages investors to learn more about

these risk factors. A detailed explanation of these factors are available in the

company’s quarterly and annual reports filed with the Securities and ExchangeCommission.

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 4/102

Jim Hagedorn

Chairman and CEO

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 5/102

5

A year ago…We used this slide to outline the next phase in our journey, declaring

our success depended upon becoming the “Gardener’s Best Friend”

Assembleportfolio of

brands

Create a worldclass customerservice model

Explorenew

opportunities

Be thegardener’sbest friend

1995 2010

Outperform thecompetition in our

core business

The culture and mindsetthat succeeded in the

past

… Must change

dramatically aswe think ahead

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 6/102

6

We have changed …Over the past year, we have re-organized our business, focused

our portfolio and positioned SMG for continued success

2010: A year of progress

Record-setting innovation with EZ Seed

“Remaking of Marysville” marketing structure

Innovative people development efforts

Divestiture of Global Professional

New regional manufacturing capacity

Opening of Chicago and New York regional offices

Doubling of our quarterly dividend

Implementation of $500 million share repurchase plan

Record sales

Record profit Record free cash flow

A.G. Lafley

Gen. Stanley McChrystal

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 7/102

7

Regionalization

Compliance

Capital

Allocation

People Innovation

Sustainability

“Consumer First” MarketingEnterprise

Risk

Today: A broader vision …We have translated our “Gardener’s Best Friend” mission into

a new language that is resonating throughout our Company

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 8/102

8

Regionalization

Compliance

Capital

Allocation

People Innovation

Sustainability

“Consumer First” MarketingEnterprise

Risk

Today’s discussions …While our “Consumer First” efforts affect all parts of our

Company, today’s discussion will have a more limited focus

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 9/102

9

What you’ll hear today …We are well-positioned to maintain our momentum by leveraging

these key attributes in a way that drives shareholder value

What is Scotts Miracle-Gro today?

Focused

Well-positioned

Innovative Flexible

Strong

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 10/102

10

Clear focus …We have removed distractions from our portfolio and now

can devote 100% of our efforts to consumer lawn & garden

Global Professional: 10%

Scotts LawnService: 8%

Smith & Hawken: 7%

Global Consumer: 75%

Our previous portfolio Scotts Miracle-Gro today

Global Consumer: 92%

Scotts LawnService: 8%

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 11/102

11

The goal is clear …With half of consumers still absent, our investments in media, market

research, R&D and partnerships are focused on driving growth

83 million households participate in lawn

and gardening

31 million households have a vegetable

garden

More than 70% of homeowners desire to

have a nice looking lawn

While lawn & garden is the No. 1 outdoor

leisure activity, 50% of households are not

engaged in the category

Source: National Gardening Association, ScottsMiracle-Gro Research

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 12/102

12

Breakdown of Global Consumer

Lawn Care: 31%Gardens &

Landscape: 39%

Home Protection: 30%

Thinking like the consumer …We have re-organized our Global Consumer business to support more

internal collaboration that is focused around consumer activity

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 13/102

13

Leveraging our awareness …We will continue increasing investments in marketing and

innovation to leverage the trust consumers place in our brands

Strong Consumer Brand Awareness

93% 94%

82% 93%

Source: 2010 Millward Brown Brand Equity & In-Market Performance

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 14/102

14

Innovation to drive growth …The pipeline that has created groundbreaking new lawn & garden

products is poised to deliver even more growth in the years ahead

New in 2011

Products introduced over the past three years accounted for nearly 14% of sales in

2010. About one-third of sales were incremental and most were margin accretive

Note: Amount reflects U.S. consumer business and includes Roundup

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 15/102

15

Partners for growth …We have developed new partnerships, strengthened existing ones

and are exploring new ones in order to reach more consumers

Additional partnerships in discovery phase …

R&D partners on issues related to plant health

Supply partners to help mitigate commodity risks

NGO partners focused on the environment

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 16/102

16

Strong relationships …By leveraging our competitive advantages and partnerships we will

drive more consumer traffic into all the retail channels we serve

Strong Retail Partnerships

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 17/102

17

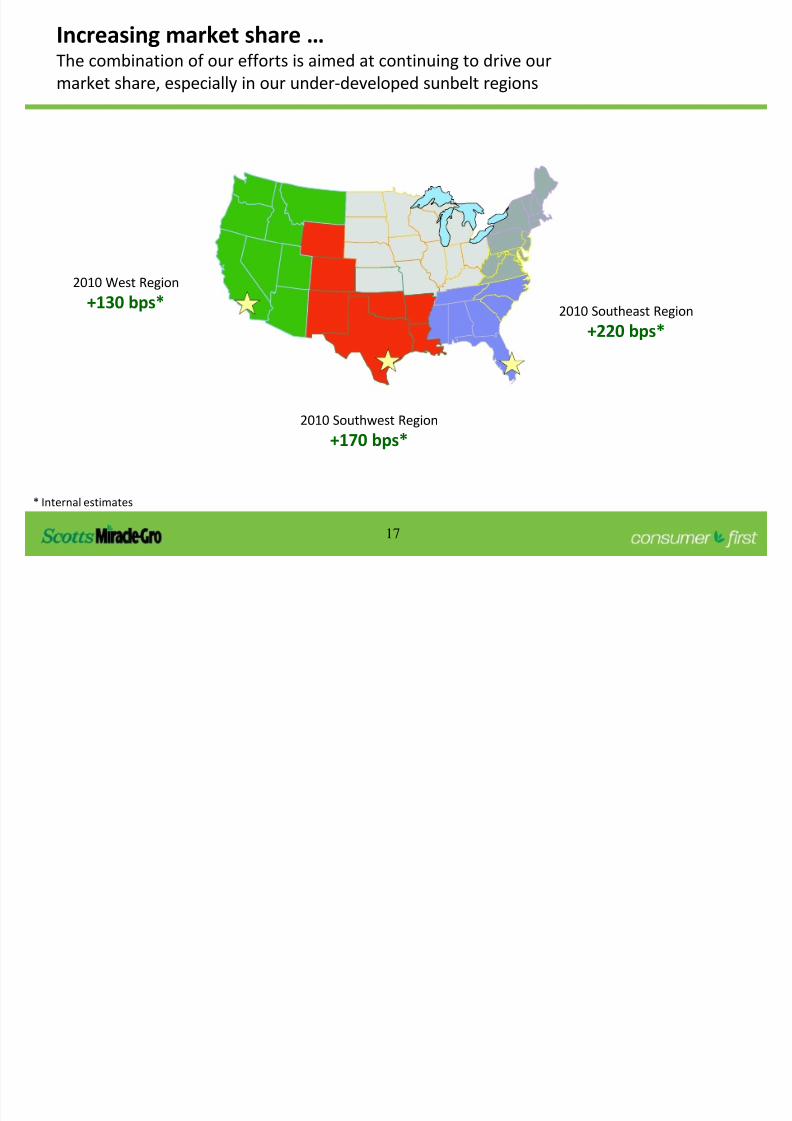

Increasing market share …The combination of our efforts is aimed at continuing to drive our

market share, especially in our under-developed sunbelt regions

2010 Southwest Region

+170 bps*

2010 Southeast Region

+220 bps*

2010 West Region

+130 bps*

* Internal estimates

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 18/102

18

Strength that benefits shareholders …With leverage ratios near the lowest levels since 1995, we can fund

investments that drive growth and take shareholder friendly actions

Maintenance

Cap-Ex

Investment

Cap-ex

Dividend

Remaining

Available

Projected operating cash flow of nearly $1.7 billion over 5 year period

Note: Estimates assume leverage ratio declines over planning period to ~1.4x in Fiscal 2015

Uses of Operating Cash Flow: 2011 - 2015

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 19/102

19

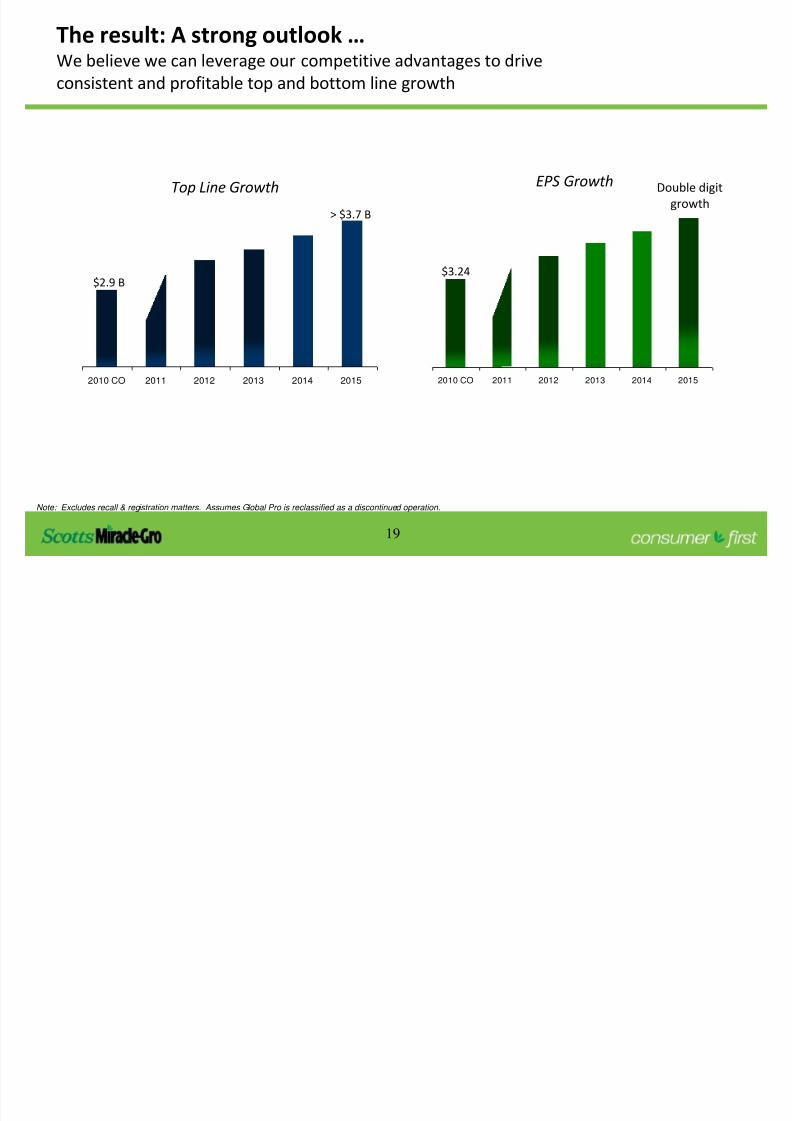

The result: A strong outlook …We believe we can leverage our competitive advantages to drive

consistent and profitable top and bottom line growth

2010 CO 2011 2012 2013 2014 2015

Note: Excludes recall & registration matters. Assumes Global Pro is reclassified as a discontinued operation.

Top Line Growth EPS Growth

$2.9 B

> $3.7 B

2010 CO 2011 2012 2013 2014 2015

$3.24

Double digit

growth

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 20/102

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 21/102

21

A strong and experienced team …Members of our “Office of the Chairman” are aligned, committed and

focused on delivering strong shareholder returns

Barry Sanders Dave Evans Claude Lopez

Denise Stump Vince Brockman

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 22/102

Barry Sanders

President

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 23/102

23

Marketing

– Category overviews

– Consumer learnings and opportunities

Consumer First …Today, we will discuss how Regionalization, Marketing, and

Innovation will sustain our growth for the future

Regionalization

Mass market to local market focus

Balance and alignment

Running the day-to-day business

Innovation

Consumer relevant innovation

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 24/102

24

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

2008 2009 2010 2011

Net Sales EBITA

Bringing it to life in 2011 …

Continued consumer and retailer support should drive 4% to 6% top line growth

and strong improvements in operating income for 2011 and beyond

2008 - 2010

Net Sales

CAGR = 7.8%

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 25/102

25

Top growth themes:

Global consumer innovation

Increased knowledge of local consumers

Improved category knowledge

Clear focus on local competitors

Improved productivity from our sales force

Strong retailer relationships and support

World-class customer service

Focus on sustainability

Category

Growth

55%

Market Share

Gains

45%

Sources of growth …Our 2011 – 2015 Strategic Plans call for our growth to be fairly balanced

between market share gains and category growth

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 26/102

26

Our evolution continues …We have moved day-to-day operations to the regions,

allowing Marysville to focus on strategy & category growth

Marysville HQ

“Define the Strategy”

Regions

“Run the Business”

Define category strategies

Develop global innovations

Provide smart shared services

Define local sales &

marketing plans; execute

with excellence

Gain local consumer insights

Manage the P&L

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 27/102

27

Our evolution continues …We have moved day-to-day operations to the regions,

allowing Marysville to focus on strategy & category growth

Marysville HQ

“Define the Strategy”

Regions

“Run the Business”

Define category strategies

Develop global innovations

Provide smart shared services

Define local sales &

marketing plans; execute

with excellence

Gain local consumer insights

Manage the P&L

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 28/102

28

The Regional operating model …With the consumer as our “north star” we are

strengthening our capabilities in key areas

Key Regional Responsibilities

Provide world-class store service & sales

Advertise effectively

Address competitive insights

Understand local consumer needsManage Regional accounts for growth

Key Centralized Responsibilities

Define global category strategies

Build our brandsDeliver breakthrough innovation

Develop go-to-market capability

Leverage scale

Develop people

MW SE SW WE INTL

Regions

C e n t r a l i z e d

S u p p

o r t

Marketing

R&D

Supply Chain

Finance

HR

NE

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 29/102

29

48%

52%

56%

39%42%

42%

We continue to fine-tune…With five regional offices and a DMA-level focus, we have identified

the necessary operating model refinements to drive our success

To fully leverage the opportunity

requires us to understand consumer

needs on a truly “local” level

Establishing a “regional” presence

allowed us to better understand the

competitive marketplace…

Step 2Step 1

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 30/102

30

2010 wins: Southeast…Regionally targeted products drove high consumer

engagement and the strongest share gains in the U.S.

Total 2010 Share Gain +220 bps*

Created regional-specific

consumer programs:

Summer Essentials Winter Snowbirds

* Internal estimates

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 31/102

31

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Dallas Houston Denver San

Antonio

Austin

Plan

Revised

Total 2010 Share Gain +170 bps*

Optimized Lawn Fertilizer

Media Plan: +20% Bonus S POS increase in

Houston through morebalanced media planning

across DMA’s

Previous Media Plan vs. Revised Media Plan

2010 wins: Southwest…Improved media buys led to strong growth in

fertilizer consumption and solid share gains

* Internal estimates

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 32/102

32

2010 wins: West Coast …Spanish language advertising, improved media timing and

more relevant messaging led to strong share gains

Total 2010 Share Gain +130 bps*

Developed program targeting

Hispanic consumers. Spanish language Ortho

commercial

Targeted stores with Spanish POP

* Internal estimates

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 33/102

33

2011 Efforts: Southeast …Continued migration to local messaging led to strong fall lawn

care results and will be used throughout the season

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 34/102

34

Fall

Winter

Spring

Outdoor advertising on

major highways

Garden Essentials

aimed at 55+

Direct mail as snowbirds

prepare to leave

2011 Efforts: Southeast …Our marketing efforts will continue to focus on talking to

“snowbirds” at the various phases of their migration

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 35/102

35

RegionalIn-Store Support

Regional

Cross-Merchandising

2011 Efforts: West …EZ Seed Winter Lawn Mix in the desert Southwest

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 36/102

36

2011 Efforts: Southwest …In the Southwest, we are leveraging the local lawn &

garden knowledge pipeline to influence consumers

ConsumersRadio

Personalities

Universities and

Extension Agents

ff

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 37/102

37

2011 Efforts: West …Partnering with Chivas USA is allowing us to interact

and build higher awareness with Hispanic consumers

Our outreach extends: On the web

Sweepstakes

In store

In local communities

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 38/102

38

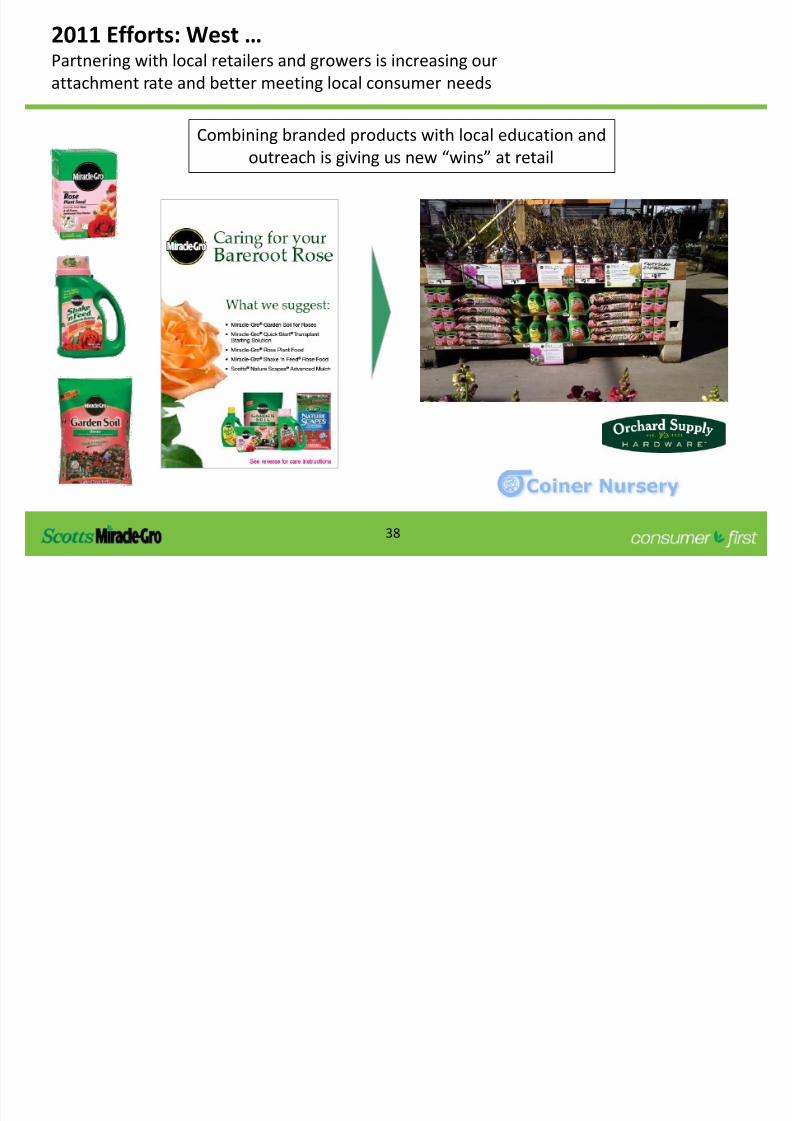

2011 Efforts: West …Partnering with local retailers and growers is increasing our

attachment rate and better meeting local consumer needs

Combining branded products with local education andoutreach is giving us new “wins” at retail

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 39/102

39

2011 Efforts: Europe …Success of EZ Seed will used to grow sales in France,

Central Europe, Belgium and Southern Europe

Key to success:

Local brands and local messages that meet a local need

North Americal l di l

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 40/102

40

North America

For 2011, Regional media represents 66% of our total spend

A local dialogue …A higher percentage of local advertising and marketing spend

provides more flexibility and better results on a local basis

0%

10%

20%

30%

40%50%

60%

70%

2009 2010 2011

National Regional Interactive

Note: Sports marketing illustrated as “regional” spend. Previous SMG illustrations showed sports marketing as “national” spend

North America

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 41/102

41

Advertising and Promotions…Improved efforts and outreach in regional and digital marketing

will drive a double-digit increase in investments

Growing Media MLB

Increased investment inhigh growth categories

Increased support

Local Partnerships

NY Yankees in FY11

Digital

Web site improvements

Focus on social media

Email reminder service support

Regions

More regionally initiatedmedia

Creating region specific plans

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 42/102

42

Building better Regions: Marketing …Our focus in the Regions will concentrate more heavily on

marketing as the role of Marysville continues to evolve

Key Changes

Increased senior-level marketing oversightAnnual marketing plans now developed regionally

Channel marketing managed regionally

Regional input critical to innovation pipeline

Regional Marketing Structure

Regional

Marketing Lead

NE MW SE SW WE Channel Int’l

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 43/102

43

Building better Regions: Sales …Our sales force of the future will create a more variable and flexible

workforce by shifting more resources to consumer engagement

Miami –Ft.

Lauderdale,FL

WPB –

Ft.Pierce,

FLFt.Meyers – Naples,

FL

Tampa –

St.Petersburg(Sarasota), FL

Orlando –

DaytonaBeach-

Melbourne, FL

Gainesville,

FL

Tallahassee, FL –

Thomasville,GAJacksonville,

FL

Savannah,GA

Albany,GA

Macon,GA

Augusta,GA Charleston,

SC

Columbia,SC

Panama City,

FL

Dothan,

AL

Columbus,

GA(Opelika,

AL)

Mobile,AL –

Pensacola(Ft.WaltonBeach,FL)

Montgomery-

Selma,AL

Meridian,MS

Jackson,MS

Monroe,LA –ElDorado,AR

Greenwood –

Greenville,MS

Columbus –

Tupelo –

West Point,MS

Memphis,TN

Jackson,TN

Nashville,TN

Huntsville – Decatur(Florence),AL

Birmingham(Anniston&Tuscaloosa),

AL

Atlanta,GA

Chattanooga,TN

Knoxville,

TN

Greenville –

Spartanburg,SC –

Asheville NC –

Anderson,SC

Tri-Cities,TN -V A

Charlotte,

NC

Florence(MyrtleBeach),

SC

Wilmington,NC

Greenville –

New Bern –Washington,

NC

Raleigh –

Durham(Fayetteville),

NC

Greensboro –

HighPoint –

WinstonSalem,NC

SE Region – Current State

2 Zones, 8 DistrictsPresident

VP Sales

Zone Directors

District Managers

Sales Managers

Merchandisers / Counselors (all part time)

President

Leaders

Middle

Merchandisers & Counselors

-

Miami –Ft. Lauderdale,

FL

WPB –

Ft. Pierce,FL

Ft. Meyers –Naples,FL

Tampa – St.Petersburg

(Sarasota), FL

Orlando –Dayt onaBeach-

Melbourne,FL

Gainesville,FL

Tallahassee,FL –Thomasville,GA

Jacksonville, FL

Savannah,GA

Albany,GA

Macon,GA

Augusta,GACharleston,

SC

Columbia,SC

PanamaCity,FL

Dothan,

AL

Columbus,GA

(Opelika,AL)

Mobile,AL –Pensacola (Ft.

WaltonBeach,FL)

Montgomery-Selma,AL

Meridian,MS

Jackson,MS

Monroe,LA – ElDorado,AR

Greenwood –Greenville, MS

Columbus –Tupelo – West

Point, MS

Memphis,TN

Jackson,TN

Nashville,TN

Huntsville –Decatur(Florence),AL

Birmingham

(Anniston&Tuscaloosa),AL

Atlanta,GA

Chattanooga,TN

Knoxville,TN

Greenville –Spartanburg,SC

– Asheville NC –Anderson,SC

Tri-Cities,TN-VA

Charlotte,NC

Florence

(MyrtleBeach), SC

Wilmington,NC

Greenville – New

Bern –Washington,NC

Raleigh –Durham

(Fayetteville),NC

Greensboro – HighPoint – WinstonSalem,

NC

Current

Future

More variable and

flexible workforce

Organizationmatches agronomic

zones

Highly-skilled front

line

Gets us closer to

consumers byeliminating layers

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 44/102

44

Improves field sales ROI

Increases efficiency – Administrative time down 33%

Improves store service and

retailer compliance

Improves talent

A stronger, smarter sales force…Key enablers like technology and improved local training will result in less

administration time, faster decisions in the field, and more “selling” time,

Benefits

O l ti ti

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 45/102

45

Our evolution continues …We have successfully moved day-to-day operations to the regions,

allowing Marysville to focus on strategy & category growth

Marysville HQ

“Define the Strategy”

Regions

“Run the Business”

• Define category strategies

• Develop global innovations

• Provide smart shared services

• Define local sales &

marketing plans; execute

with excellence

• Gain local consumer insights

• Manage the P&L

M k ti

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 46/102

46

Marketing…Our new business model provides an excellent

opportunity to transform Global Consumer Marketing

Historical

Customer-focused

North America only

Incremental product ideas

Annual marketing plans

Current year execution

Traditional media

Product focused

Current

Consumer-focused

Global

Breakthrough innovation

Global category strategies

2 – 4 year planning horizon

1:1 relationship with consumer

Brand / Category focused

LAWN CAREGARDEN &

LANDSCAPE

HOME

PROTECTION

Major progress

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 47/102

47

Major progress …With a more strategic focus, our global marketing teams

are now aligned based on consumer activity, not by brand

Lawn Care

31%

Garden &

Landscape

39%

Home

Protection

30%

$886M

$928M

$1,140M

Fiscal Year 2010 net sales by category for Global Consumer business, including Roundup sales

What is Lawn Care?

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 48/102

48

ControlsFeeding Seeding

What is Lawn Care? …Consumers use all of these tools – and more – to

maintain the lawn that they want

Seeding

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 49/102

49

Seeding

Seeding …Innovation has led to an improved consumer experience that

has driven growth and continues to provide opportunities

Category Facts

Size: $500M

HHP: 40%

SMG $ Share*: 50%

Key Learnings:

1. EZ Seed has transformed the category, the consumer

experience, and our business

2. Significant opportunity to drive seeding projects

3. Hot, dry 2010 summer ravaged lawns in MW & NE

*Estimated

(1)

1 US Only

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 50/102

50

Controls

Controls …Keeping unwanted weeds and insects out of lawns

Lawn Insect

Size: $650M

HHP: 41%

SMG $ Share*: 20%

Selective Weed

Size: $200M

HHP: 42%

SMG $ Share*: 54%

Two Largest Segments

Key Learnings:

1. Consumer awareness of lawn weed control is still low

2. Fire Ant & Grub regional strategies are working

3. Spot weed control represents opportunity

* Estimated

(1)

1 US Only

Feeding

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 51/102

51

Feeding

Feeding …Innovation and improved marketing can drive growth in this

business, which is the largest in the lawn care category

Category Facts

Size: $1+B

HHP: 46%

SMG Share*: 61%

Key Learnings & Opportunities:1. Decline in frequency (not HH’s) is driving category decline

2. 33% of HH’s are “in & out” of category

3. Under 35 year old as likely to fertilize lawn as 50 year old

4. Top 2 reasons why consumers don’t apply:

lack of perceived need (looks okay, no problems)

financial (less income, price)

* Estimated

(1)

1 US Only

Lawn Fertilizer Myth Busters

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 52/102

52

1. “Lawns are Less Relevant ”

2. <35 Year Olds Don’t Fertilize due

to environmental concerns

3. More consumers have beenexiting the category

64% Of Consumers Want a “Nice”/ “Best”Lawn, 71% if < 35yrs old

52% Of < 35yrs Old Homeowners Fertilize,

Similar for 35-50yrs.

Lack of Knowledge Key Barrier

HH Penetration Is Essentially Flat 1/3 Consumers Are “In/Out” Behavior

50% Reduce Apps / 50% Skip A Year

4. Consumers are primarily do-

it-yourself OR do-it-for-me

10% do-to-for-me exclusively

50% do-it-yourself exclusively

14% do-to-for-me and DIY in same year

5. Price elasticity is the primary

driver of lower unit volume

Top 2 Reasons for Less Frequency

52% Lawn OK / No Problems

51% Financials (↓ income, ↑cost)

Source: Nov 2010 Lawns “Sanity” Segmentation Research; Copernicus

Lawn Fertilizer Myth Busters …Our largest research project ever debunked key myths and

provided insights that could drive strong future growth

Younger homeowners

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 53/102

53

Q8: Which one of the following statements best describes how you would like your lawn to be?Q9: And which of the following statements best describes the current state of your lawn?

Q10: Which of the following statements best describes the immediate neighborhood you live in?

One of Nicer

Average

Best

Below Average

Source: Nov 2010 Lawns “Sanity” Segmentation Research; Copernicus

Younger homeowners …This group is actually more interested in wanting the “best” lawn

but don’t understand how to achieve the result

Simpler message needed:

WHY to Feed Delivered in Interactive

Forums

HOW To Feed with Confidence /

Knowledge, Safety, Time Savings

Changing our message

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 54/102

54

TRADITION APPROACH NEW APPROACH

Cosmetic Focus: Thick, Green

Problem-Solution Based w/Pesticides

Reactive

Based on Agricultural Practices

Complex

Healthy grass = Sustainable

Nutrition/Feeding Focused

Proactive Routine

Driven by typical behaviors

Simple advice

Strategic promotions

Changing our message …The goal of future communications will be to keep “lapsed” users

engaged and to increase usage by 1 application annually

Simple is a solution

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 55/102

55

Regional Expansion

2011 launches: Atlanta, Chicago, Austin,

Salt Lake City

+2010 initial launch of 3 Existing DMA’s

Non-Traditional Channels

Simple is a solution …Key learnings from our initial test give us continued

optimism about the potential of Scotts Snap

Science is a solution

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 56/102

56

Simple

Weatherproof - Apply Anytime!

Before After

SafeReplaces 2,4D and Atrazine

EffectiveDual ActionEliminates weeds for 4 - 6 months

Science is a solution …Beginning in 2012, improved and proprietary active

ingredients will provide better results and be easier to use

Convenient is a solution

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 57/102

57

Convenient is a solution …Helping consumers understand the benefits of “spot” weed

control will save them time and money

Less than 50% of Lawn Fertilizer users have ever used liquid Lawn Weed Control

Cross Merchandising

22 million households are prime candidates for Spot Weed Control

Lawn Fertilizer opportunity …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 58/102

58

Costs Time

Confusion?Concerns

LooksO.K.

Lawn Fertilizer opportunity …Better understanding core consumer issues is allowing us to

create new strategies to drive growth

What is Garden & Landscape? …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 59/102

59

Plant Food Growing Media &Mulch

What is Garden & Landscape? …Our largest category provides continued growth opportunities

that are linked to improving the consumer experience

Wild Bird

Plant Food …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 60/102

60

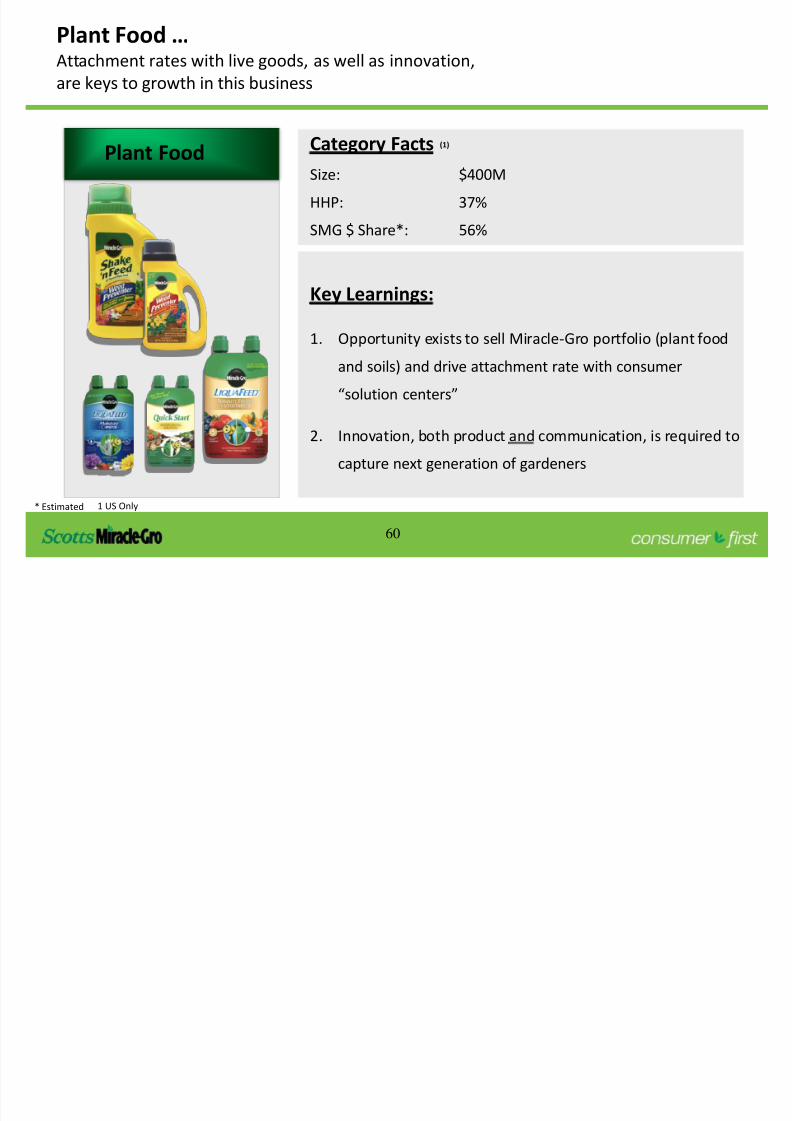

Plant Food

Plant Food …Attachment rates with live goods, as well as innovation,

are keys to growth in this business

Category Facts

Size: $400M

HHP: 37%

SMG $ Share*: 56%

Key Learnings:

1. Opportunity exists to sell Miracle-Gro portfolio (plant food

and soils) and drive attachment rate with consumer

“solution centers”

2. Innovation, both product and communication, is required to

capture next generation of gardeners

* Estimated

(1)

1 US Only

Growing Media …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 61/102

61

Growing Media

Growing Media …A $1+ billion business with continued growth opportunity

based on innovation and improved communication

Category FactsSize: $1050M

HHP: 50%

SMG $ Share*: 75%

Key Learnings:

1. Our pricing study validates Miracle-Gro pricing model

2. Improving live good attachment requires consumer change

3. Watering confusion…is a universal insight/need to both

Potting and Garden Soil

4. Innovation, both product and communication, required to

capture next generation of gardeners

* Estimated

(1)

1 US Only

A better soil solution …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 62/102

62

Holds 50% More Water than Ordinary Potting Mix.

#1 consumer perceived reason for success/failure.

Improves Native Soil - 90% more air space.

Consumers concerned with quality of native soil.

Feeds for up to 6 months!

Consumers want big, beautiful plants.

Miracle-Gro Expand ‘n Gro is one of our most exciting gardening

innovations ever and makes success easier to achieve

Mulch …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 63/102

63

Mulch

Mulch …This has been a fast growing business for SMG with

significant upside potential still available

Category FactsSize: $750M

Non-traditional: $2+B

HHP: 35%

SMG $ Share*: 34%

Key Learnings:

1. Mulch is largest single lawn & garden category

2. Consumer price sensitivity is very high – leads to competitive

retails and high switching

3. SMG represents all category growth for mulch $

* Estimated

(1)

1 US Only

Wild Bird Food …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 64/102

64

Category FactsSize: $900M

HHP: 24%

SMG $ Share*: 11%

Key Learnings:

1. Due to the economy in 2010, category declined by $100M

and 1 million consumers exited

2. Business is highly-concentrated with a few large customers

3. Two-thirds of category volume is “commodity” – provingopportunity for trade-up to branded product

4. 75% of unit volume in category sells below $8 price point

Wild Bird

d d oodA large category with passionate consumers; strategic pricing

and innovation will be keys to growth

* Estimated

(1)

1 US Only

What is Home Protection?

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 65/102

65

Non-Selective Weed

Control

Indoor & Perimeter

Pest Control

What is Home Protection? …Helping consumers control unwanted bugs and weeds

Indoor and Perimeter Pest Control …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 66/102

66

Indoor & Perimeter

Pest Control

Home Defense has driven growth in recent years;

share gain opportunities remain significant

Category FactsSize: $1.3B

HHP: 66%

SMG $ Share*: 19%

Key Learnings:

1. Aerosols are the most popular consumer form and we

are launching a Home Defense range of aerosols

2. Consumers have a heightened awareness of Bed Bug

infestations and we are responding by educating

consumers and providing them with product solutions

3. We are leveraging our regional operating model to

improve our Hispanic marketing

* Estimated

(1)

1 US Only

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 67/102

Pulling it all together …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 68/102

68

Marketing – Thinking like the consumer

– Insights show continued opportunities

– Increased household penetration is key

g gThree key pillars will define our success on a day-to-day basis

and as we drive for long-term growth

Regionalization Continued strong progress

Intensified marketing efforts on the way

Sales force enhanced for productivity

Innovation Consumer-focused insights = success

Leveraging investment for global growth

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 69/102

Pulling it all together

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 70/102

70

Pulling it all together …What you should take away from this morning

Our financial strategy has been focused and consistent

We are ahead of plan

Our outlook projects sustained double-digit shareholder returns

Strong, consistent cash flow provides ability for meaningful returns to

shareholders while still investing for growth

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 71/102

71

Our financial strategy has been focused and consistent …

Focus portfolio to leverage unique capabilities

Improve operating metrics

Execute long-term capital structure strategy

Provide enhanced cash return to shareholders

f li l i bili i

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 72/102

72

Focus portfolio to leverage unique capabilities

Disposed of Smith & Hawken retail and catalog operation in 2010

Will complete divestiture of Global Pro business in 2011

Evaluating options to exit non-European Professional Seed business

Leverage unique capabilities and brands to generate

incremental growth from within and around the core

Looking Forward:

I O i M i

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 73/102

73

Improve Operating Metrics

36.6%

34.0%

35.0%

36.0%

37.0%

2007 2010

13.1%

10.5%

11.5%

12.5%

13.5%

2007 2010

$213

$150

$175

$200

$225

2007 2010

$3.41

$2.10

$2.60

$3.10

$3.60

2007 2010

Note: Reflects adjusted earnings which exclude impairments, recall & registration matters. Also, results are prior to reclassification of Global Pro as a discontinued operation.

Gross Margin Rate Operating Margin Rate

Free Cash Flow EPS

$ in millions (except EPS)

E l i l

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 74/102

74

0.0

1.0

2.0

3.0

4.0

2007 2008 2009 2010

Ideal L/T Range

Execute long-term capital structure strategy

Future State Financing Maturity*

Traditional bank facility 2016

Bond tranche #1 2018

Bond tranche #2 2020

* Current or anticipated

Average Debt to EBITDA – September 30

P id h d h t t h h ld

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 75/102

75

$ in millions

Provide enhanced cash return to shareholders

$0

$100

$200

$300

$400

$500

$600

2007 2008 2009 2010 2011 est.

Dividend Share Repurchase

Cash Return

Five year return estimated to exceed $1.3 Billion

Recent Actions

Doubled dividend to annual

rate of $1/share in September

2010

Anticipate maintaining 2.0 to

2.5% yield

Launched 4 year, $500 million

share repurchase program in

September 2010

Note: Fiscal 2011 estimated share repurchases include $190

million from proceeds of Global Pro divestiture.

St Fi l 2010 lt t h d f l

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 76/102

76

Strong Fiscal 2010 results put us ahead of plan …

Feb '10 Actual

Conference Results

Sales growth +3 - 5% +5.3%

Gross margin rate +30 bps +70 bps

Net income +18 - 22% +33%

EPS $3.00 - $3.10 $3.41

Free cash flow $193 million $213 million

Fiscal 2010

Note: Reflects adjusted earnings which exclude impairments, recall & registration matters. Also, results are prior to reclassification of Global Pro as a discontinued operation.

What to expect in 2011 …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 77/102

77

Top line growth exceeding GDP

Continued margin improvement

Stable capital structure

What to expect in 2011 …Our outlook projects sustained double-digit shareholder returns

Strong shareholder returns

Resetting our model …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 78/102

78

Note: Reflects adjusted earnings which exclude impairments, recall & registration matters. Continuing Ops reflects results after Global Pro is reclassified as a discontinued

operation.

Resetting our model …Breaking down the impact of Global Pro as a discontinued operation

Fiscal 2010

Pro Forma*

* Pro Forma reflects share count as if $190 million of proceeds from Global Pro sale were used to repurchase shares at the beginning of the Fiscal 2010.

Actual Continuing

Results Operations Change

Net sales $3,140 $2,898 ($242)

Gross margin rate 36.6% 37.2% + 60 bps

SG&A $747 $695 ($52)

Operating margin % 13.1% 13.5% + 40 bps

Interest $47 $43 ($4)

Share count 67.6 67.6 0.0 64.3

EPS $3.41 $3.24 ($0.17) $3.40

$ in millions (except EPS)

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 79/102

79

Top line growth exceeding GDP …

$ in millions

Global Consumer

2010 base: $2,650

2011 expectations:

Total Company +4 - 6%

low high

Category 2% 3%

Share (sales impact) 1% 2%

Pricing 1% 1%

Total 4% 6%

Scotts LawnService

2010 base: $224

2011 expectations:

low high

Customer count 4% 6%

Mix 1% 1%

Pricing - -

Total 5% 7%

C ti d i t i t

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 80/102

80

Continued gross margin rate improvement …

2010 Global ProDiscontinued

Operation

2010 ContinuingOperations

2011 estimate

36.6%

37.2%

+ 70 to100 bps

+ Productivity

+ Innovation

+ Pricing, net of

commodity inflation

+ Year-over-year comp

on H1 FY2010 costs

- ICL supply agreement

+ 60 bps

C i t t S l Ch i t d ti it

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 81/102

81

$ in millions

Consistent Supply Chain cost productivity …

$0

$2

$4

$6

$8

$10

$12

$14

$16

2007 2008 2009 2010 2011

Estimate

Annual Savings 2007 – 2010 Initiatives

1. Leverage growing media’s

low-cost distribution model

2. Invest in regional production

capacity

3. Rationalize logistics footprint

Key Themes for Future

Continue regionalization

Globalization

Value chain optimization

Reformulations / new

technology

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 82/102

Commodities in the long-run …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 83/102

83

Consumer driven innovation

Supply chain cost productivity

Dynamic pricing program for commodity Wild Bird Food

Proactive hedging program on all other commodities

Increased pricing as appropriate

gInflationary pressures and volatility will be mitigated through multiple vehicles

Focused SG&A …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 84/102

84

Investing in competitive capabilities while managing portfolio of spend

Revenue

Enhancing

~60%

2010 SG&A from Continuing Operations

Key Investments in Growth

Consumer insights

Innovation

Consumer communication

Business developmentAll Other

Managing the portfolio of spend

Standardized global processes

Robust decision support

Transactional efficiency

2011 increase of 4 - 5%

Operating margin improvement

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 85/102

85

Operating margin improvement …

2010 2011 Estimate

13.5%

13.1%

> 14%

Impact of Global Pro

as discontinued

operation

Key Drivers

• Top line growth

• Gross margin rate

improvement

Interest expense …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 86/102

86

Rates resume to market based levels as 2007 bank facility is replaced

Bank

Facility Fixed Bonds

Fixed

Bank Facility

Floating

Capital StructureFiscal 2011

Pro Forma 2011 reflects full year rate impact of bonds issued in December 2010

and anticipated increased spread on bank facility to be renewed in Q3 Fiscal 2011

2010 Estimate Pro Forma

Total average debt ~$ 1.0 B <$ 1.0 B <$ 1.0 B

Interest rate 4.68% 5.98% 6.65%

Interest expense $ 43 $ 57 $ 63

Note: Interest rate is a weighted average.

$ in millions (unless otherwise noted)

Share repurchases …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 87/102

87

Beginning shares* 67.6

Share repurchases:

Current year (2.4)

Prior year (0.3)

Shares issued (options) 1.4Other 0.3

Ending shares* (est.) 66.6

Fiscal 2011

Q1 Q2 Q3 Q4 Ful l Year

Share repurchases 0.5 1.4 2.2 2.0 6.1

Weighting 87.5% 62.5% 37.5% 12.5%

Impact on 2011 shares* 0.4 0.9 0.8 0.3 2.4

Carry over impact in 2012 3.7* Weighted average

2011 repurchases will further reduce weighted average shares in 2012

Shares in millions

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 88/102

Summarized Fiscal 2011 Financial Guidance

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 89/102

89

Fiscal 2010

Summarized Fiscal 2011 Financial Guidance

Fiscal 2011Continuing

Operations Guidance

Net sales $2,898 + 4 - 6%

Gross margin rate 37.2% + 70 - 100 bps

SG&A $695 + 4 - 5%

Operating margin % 13.5% > 14%

Interest $43 $57

Share count 67.6 66.6

EPS $3.24 $3.60 - $3.70

Free cash flow na $200

Note: Reflects adjusted earnings which exclude impairments, recall & registration matters. Continuing Ops reflects results after Global Pro is reclassified as a discontinued

operation.

$ in millions (except EPS)

A few words on why my responsibilities are evolving …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 90/102

90

We have followed a disciplined path over the past 5 years

Decision to focus business in Fiscal 2006 around core; launched multi-year

share repurchase program with excess cash

Opportunistically accessed credit market in early 2007 to accelerate and

increase shareholder returns

Focused organic capital on domestic CPG business; increased consumer

orientation to sustain future growth

Divested Smith & Hawken and Global Professional businesses

Drove improved returns in Int’l Consumer and Scotts LawnService

Directed free cash flow from 2007 - 2010 to reduce leverage

This path has led to a unique and enviable position

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 91/102

91

This path has led to a unique and enviable position …

Maintenance

Cap-Ex

Investment

Cap-ex

Dividend

RemainingAvailable

Projected operating cash flow of nearly $1.7 billion over 5 year period

Note: Estimates assume leverage ratio declines over planning period to ~1.4x in Fiscal 2015

Uses of Operating Cash Flow: 2011 - 2015

Expanded responsibility …

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 92/102

92

Disciplined approach to sustain and accelerate growth over the next 5 years

Ensure we size and align resources around key initiatives and capabilities

within the core businesses to realize growth potential

With a critical eye, more actively explore new growth opportunities

(including alliances) which leverage our unique strengths and assets while

increasing L/T shareholder return

Enhance our capability to explore and, as appropriate, execute initiatives

emanating from the strategy with the formation of a dedicated Business

Development team

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 93/102

Claude Lopez

President, Global Sales

2011 off to a solid start …Consumer activity remains strong entering the start of the season in

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 94/102

94

What we’re seeing so far:

Consumer purchases up 11% YTD through mid-February

Season break report (since Jan. 1)

Florida +32%,

California +27%

Retail inventory levels are in line with expectations

Consumer activity remains strong entering the start of the season in

sunbelt markets and shipments are increasing company-wide

Retailer support of the lawn and garden category –

as wellas our brands – remains strong as the season breaks

Store walks: What to look for …Our core competitive strengths – as well as our longer-term growth

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 95/102

95

Three key things to keep in mind: The size and prominence of lawn & garden (retail commitment)

The support needed in the space (Scotts Miracle-Gro commitment)

Opportunities for growth (attachment rates, mulch, controls, etc.)

Our core competitive strengths as well as our longer term growth

opportunities – will be on display

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 96/102

Today’s presenters

Jim HagedornCh i Chi f E ti Offi

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 97/102

97

Chairman, Chief Executive Officer

Jim was named chief executive officer of ScottsMiracle-Gro in 2001 and

Chairman of the Board of Directors in 2003.

After the merger of Scotts and Miracle-Go in 1995, Jim was named senior vice

president, Consumer Gardens Group. At Miracle-Gro, Jim had served as

executive vice president and was a major architect of Miracle-Gro's success

both in the U.S. and in the UK. Following the merger, he was instrumental in

the effective integration of the two businesses and served as head of the

Company’s North America business.

Jim is a graduate of The Harvard Business School Advanced Management

Program and holds a degree in aeronautical science from Embry Riddle

Aeronautical University, where he is now a member of the Board of Trustees.

Jim is co-chairman of the National Fund for the U.S. Botanic Garden in Washington, D.C., an associate trustee of the

North Shore Hospital in Manhasset, N.Y. and Chairman of the Board for the Farms for City Kids Foundation, Inc. in

Reading, Vt. He is also a board member for the Centers for Disease Control and Prevention (CDC) Foundation, serves

on Intrepid Foundation Board of Trustees, is a member of the Council on Competitiveness Executive Committee and

is on the Board of Directors for the Nurse-Family Partnership in Denver, Colo.

Additionally, he served in the United States Air Force for seven years, where he was a captain and an accomplished F-

16 fighter pilot.

Dave EvansChief Financial Officer Executive Vice President Strategic

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 98/102

98

Chief Financial Officer, Executive Vice President Strategic

Planning and Business Development

Dave was named executive vice president and chief financial officer in

September 2006. In that capacity, he has responsibility for corporate financial

functions, which include accounting, financial planning and analysis, treasury,

tax, risk management, audit, financial compliance and investor relations.

In 2010, his role was expanded to include Strategic Planning and Business

Development. This expanded role is focused on exploring new growth areas and

focusing on a broad array of initiatives that are focused on driving growth and

economic value.

Dave previously was senior vice president, Global Service Center and Finance.

He joined the Company in 1993 as finance director, Operations, and was

promoted to vice president of Finance for the Consumer Lawns business in

1998. In 2000, he was named vice president of Finance, North America Sales,

before being named Finance lead for the North America business unit in 2003.

A certified public accountant, Dave attended the Kellogg Management Instituteat Northwestern University. He holds a bachelor of science degree in accounting

from The Ohio State University, where he serves as a member of Fisher College

of Business Accounting Advisory Board.

Barry SandersP id t

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 99/102

99

President

Barry was named president in 2010, with responsibility for day-to-dayoversight of all business operations. Previously, he was executive vice

president of the Company’s Global Consumer segment, which comprises

more than 90 percent of annual revenue.

Barry joined ScottsMiracle-Gro in 2001 as senior vice president in charge

of Global Business Improvement. He later held leadership positions in

sales and supply chain for the North America consumer and professional

businesses and was head of the Smith & Hawken retail business. He also

served as executive vice president of Global Technologies & Operations,

which included worldwide supply chain, research and development and

information technology.

Prior to ScottsMiracle-Gro, Barry was with the former Ernst & Young

consulting organization for 10 years, specializing in operations

management.

He has a bachelor’s degree in business from Bowling Green University

and an MBA degree from the University of Dayton.

Claude Lopez

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 100/102

100

President, Global Sales

Claude was named President of Global Sales in 2010, with oversight foreach of the Company’s Regional Offices worldwide as well as its Business

Development teams. In 2007, he was named executive vice president of

the International business, responsible for the Company’s consumer lawn

and garden business outside of North America and the Global Professional

business.

Claude joined ScottsMiracle-Gro in 2001 as general manager of theCompany’s French business. He was named senior vice president of the

International business in December 2004.

Before joining ScottsMiracle-Gro, Claude was with Reckitt Benckiser, where

he was a European category director for disinfectants, before becoming

general manager of its Belgium operations. Prior to Reckitt Benckiser,

Claude had several leadership assignments at Cadbury Schweppes.

He completed his MBA degree at the Ecole des Hautes Etudes

Commerciales in France and earned a master’s degree in law from Paris

University.

Jim King

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 101/102

101

Senior Vice President, Investor Relations & Corporate Affairs

Jim is senior vice president, responsible for leading the Company’sinvestor relations, internal communications, public affairs and

community relations activities, a position he has held since June 2008.

He began his career at ScottsMiracle-Gro in 2001 as director, Investor

Relations and Corporate Communications.

Prior to joining ScottsMiracle-Gro, Jim was vice president, Investor

Relations, with the consulting firm of Edward Howard & Co., inCleveland; manager of Investor and Media Relations, at American

Greetings Corp., Cleveland; and a business journalist in Phoenix, Atlanta

and Cleveland.

Jim is a member of the National Investor Relations Institute and the

Arthur Page Society. He also serves on the Board of Directors of Keep

America Beautiful and the Board of Advisors of the School of Journalismand Mass Communications at Kent State University, where he received

both his bachelor's degree in journalism and an MBA degree.

8/6/2019 Scotts Investor Deck

http://slidepdf.com/reader/full/scotts-investor-deck 102/102

Annual Analyst Day

February 23, 2011

Boca Raton, Florida