seb facts and figures january september 2008

DESCRIPTION

TRANSCRIPT

1

www.sebgroup.com

Facts & FiguresJanuary – September 2008

2

PageSEB Group 3 – 30Asset quality 31 – 47Bond portfolios 48 – 57Divisions 58 – 64Merchant Banking 65 – 74Retail Banking 75 – 100Wealth Management 101 – 112Life 113 – 128Macro update 129 – 138

Contents

3

SEB has…an attractive platformhigh customer satisfactionstable profit growthseveral leading positions

...a strong customer base2,500 customers are large companies and financial institutions400,000 SME customers5 million private customers

3

SEB – the key to North-European markets

4

Business Support/Group StaffJan Erik Back / Ingrid Engström / Hans Larsson

Internal Audit

Agneta Brevenhag

Group Credits & Group Risk Control

Johan Andersson

President & CEO

Annika Falkengren

Merchant Banking

Magnus Carlsson

Retail Banking

Bo Magnusson

Life

Anders Mossberg

WealthManagementFredrik Boheman

SEB's organisation

5

Share of operating profitJan – Sep 2008

43%36%

8%13%

Retail Banking

Wealth Management

Life Merchant Banking

9%

9%6%

4%5%

5%

12%

50%

GermanySweden

Lithuania

Latvia

Estonia

Norway

Finland

Denmark

Geography - Adjusted for OtherDivisions - Adjusted for Other

6

Ratings of Skandinaviska Enskilda Banken ABRating target set by SEB Board at AA

Moody’s S&P Fitch DBRS

Bank Senior Rating

Short Term P-1 A-1 F-1 R-1 (middle)

Long Term Aa2 A+ A+ AA (low)

Outlook Negative Negative Stable Stable

Last Action Outlook change Outlook change Outlook change Unaffected rating

Date Dec-08 Oct-08 Jul-08 Jul-08

7

Key figuresSEB Group

Q3 Jan-Sep Q2 Q3 Jan-SepSEK m 2008 2008 2008 2007 2007

Operating income 8,705 27,910 -16% -8% -8%Operating expenses -5,970 -18,442 -7% 7% 7%Operating profit 2,010 7,927 -43% -46% -36%Net profit 1,514 6,171 -46% -51% -38%

Return on Equity, % 8.0 10.9 -7.2 -9.3 -8.1Cost / income ratio 0.69 0.66 0.07 0.10 0.09Credit loss level, % 0.27 0.19 0.10 0.19 0.09

Basel II Core capital ratio, % 8.1 8.1 -0.5 -0.2 -0.2Risk-weighted assets, SEK bn 937 937 66 140 140

Change

8

Profit and loss accountQ3 2008 vs. Q3 2007SEK m Q3 Q3 Change Excluding

2008 2007 % portfoliosNet interest income 4,553 3,917 16Net fee and commissions 3,754 4,101 -8Net financial income -269 163Net life insurance income 504 782 -36Net other income 163 530 -69

Total operating income 8,705 9,493 -8 -12%Staff costs -3,752 - 3,564 5Other expenses -1,820 - 1,691 8Depreciation of assets -398 - 325 22

Total operating expenses -5,970 - 5,580 7Gain/loss tangible/intangible assets 2 Net credit losses etc -725 - 189

Operating profit 2,010 3,726 -46 -48%Net profit 1,514 3,101 -51 -52%

9

Profit and loss accountQ3 2008 vs. Q2 2008SEK m Q3 Q2 Change Excluding

2008 2008 % portfoliosNet interest income 4,553 4,421 3Net fee and commissions 3,754 3,909 -4Net financial income -269 1,161 -123Net life insurance income 504 642 -21Net other income 163 270 -40

Total operating income 8,705 10,403 -16 -14%Staff costs -3,752 -3,993 -6Other expenses -1,820 -2,098 -13Depreciation of assets -398 -354 12

Total operating expenses -5,970 -6,445 -7Gain/loss tangible/intangible assets 1 Net credit losses etc -725 -452 60

Operating profit 2,010 3,507 -43 -34%Net profit 1,514 2,809 -46 -38%

10

Profit and loss accountJan – Sep 2008 vs. Jan – Sep 2007SEK m Jan – Sep Jan – Sep Change Excluding Jan – Dec

2008 2007 % portfolios 2007Net interest income 13,197 11,623 14 15,998Net fee and commissions 11,464 12,922 -11 17,051Net financial income 731 2,819 -74 3,239Net life insurance income 1,859 2,167 -14 2,933Net other income 659 874 -25 1,219Total operating income 27,910 30,405 -8 -6% 40,440Staff costs -11,644 -11,134 5 -14,921Other expenses -5,674 -5,137 10 -6,919Depreciations/amortisations -1,124 -995 13 -1,354Total operating expenses -18,442 -17,266 7 -23,194Gain/loss tangible/intangible assets 4 1 788Net credit losses etc -1,545 -703 120 -1,016Operating profit 7,927 12,437 -36 -30% 17,018Net Profit 6,171 9,885 -38 -32% 13,642

11

SEB GroupIncome, Expenses and Operating profit, SEK m

Operating profit

01 0002 0003 0004 0005 0006 000

Q1-04

Q2-04

Q3-04

Q4-04

Q1-05

Q2-05

Q3-05

Q4-05

Q1-06

Q2-06

Q3-06

Q4-06

Q1-07

Q2-07

Q3-07

Q4-07

Q1-08

Q2-08

Q3-08

*

* One-off charges of SEK 890m in Q4 2005 ** Including sales of Baltic properties in Q4 2007 of SEK 785m

**

0

2,000

4,000

6,000

8,000

10,000

12,000

Q1-04

Q2-04

Q3-04

Q4-04

Q1-05

Q2-05

Q3-05

Q4-05

Q1-06

Q2-06

Q3-06

Q4-06

Q1-07

Q2-07

Q3-07

Q4-07

Q1-08

Q2-08

Q3-08

Excluding portfolios Income Expenses

*

12

3,917

4,553-462

381

53996 82

Q3 2007 Lendingmargin

Lendingvolume

Depositmargin

Depositvolume

Funding &other

Q3 2008

Net interest income analysisSEB Group Q3 2008 vs. Q3 2007SEK m

13

4,4214,553-298

107

538

-6

-209

Q2 2008 Lendingmargin

Lendingvolume

Depositmargin

Depositvolume

Funding &other

Q3 2008

Net interest income analysisSEB Group Q3 2008 vs. Q2 2008SEK m

14

11,623

13,197

338311

670

870

-615

Jan – Sep2007

Lendingmargin

Lendingvolume

Depositmargin

Depositvolume

Funding &other

Jan – Sep2008

Net interest income analysisSEB Group Jan – Sep 2008 vs. Jan – Sep 2007SEK m

15

Net interest and Net fee and commission incomeSEB Group, SEK m

0

1,000

2,000

3,000

4,000

5,000

Q1-04

Q2-04

Q3-04

Q4-04

Q1-05

Q2-05

Q3-05

Q4-05

Q1-06

Q2-06

Q3-06

Q4-06

Q1-07

Q2-07

Q3-07

Q4-07

Q1-08

Q2-08

Q3-08

Net interest income Net fee and commissions

16

Fee and commission incomeGross quarterly development Q1 2004 – Q3 2008 SEB Group, SEK m

0

500

1,000

1,500

2,000

2,500

New issues &advisory

Secondarymarket &

derivatives

Custody &mutual funds

Payment, cards,structuredlending,

deposits,guarantees

Other

Deal driven

Securitiestransaction

driven

Value driven –performance

driven Non-capital market driven

Capital market driven

*

* Q2 2006 adjusted for gross commission on security lending, SEK 200m

17

-400

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

Net financial income Net life insurance income Net other income

Net financial, Life and Other insurance incomeQuarterly development Q1 2004 – Q3 2008 SEB Group, SEK m

18

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

Staff costs Other expenses Restructuring costs

Cost development per quarterQuarterly development Q1 2004 – Q3 2008* SEB Group, SEK m

* Include capitalisation of acquisition cost in Life from Q1 2005 – onwards** One-off charges of SEK 890m in Q4 2005

**

19

18,679

17,26618,442

736

1,217 129

-66982

-319

Jan-Sep2007

Inflation Organicgrowth +

Acq

Depreciation Variablesalaries

Cost beforeefficiency

gains

Efficiencygains

Redundancycost

Jan-Sep2008

19

Cost managementTotal expenses, Jan-Sep 2008 vs. Jan-Sep 2007

*

• Investments for operational excellence of SEK 668m included• Organic growth of SEK 378m• Acquisitions of KAM, Factorial of SEK 171m

*

SEK 865m from the start

of 2007

20

Return on equitySEB Group, per cent

21.1

12.614.7

15.8

20.8

10.9

19.3

2004 2005 2006 2007 Jan – Sep 2008

Excluding portfolios Return on Equity

*

* 17.0 excluding one-off charges of SEK 890m in Q4 2005

21

Cost/income ratioSEB Group

0.65 0.650.58 0.57

0.66

0.550.63

2004 2005 2006 2007 Jan – Sep 2008

C/I ratio Excluding portfolio losses

*

* 0.62 excluding one-off charges of SEK 890m in Q4 2005

22

Basic earnings per shareSEB Group, SEK

21.83

10.3510.8312.58

18.72

9.00

19.97

2004 2005 2006 2007 Jan – Sep 2008

Excluding portfolios Earnings per share

*

* 13.54 excluding one-off charges of SEK 890m in Q4 2005

23

12 month rolling SEB Group*, SEK m

* Excluding restructuring costs and one-off charges of SEK 890m in Q4 2005

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Q1-04

Q2-04

Q3-04

Q4-04

Q1-05

Q2-05

Q3-05

Q4-05

Q1-06

Q2-06

Q3-06

Q4-06

Q1-07

Q2-07

Q3-07

Q4-07

Q1-08

Q2-08

Q3-08

Income

Expenses

Operatingprofit

24

Assets under managementSEB Group, SEK bn

Assets under management year-end 2007 1,370Inflow 222 (16%)Outflow -188 (-14%)Acquisition/disposal net 17Change in value -177 (-13%)

Assets under management Sep 2008 1,244 ** Of which:Retail Banking 75Wealth Management 1,181Life 382

25

SEB Group net inflow AuM Jan – Sep 2008, SEK bn

30.234.0

-11.1

2.5

11.11.3

Sweden Other Nordic Germany Baltic countries& Poland

Other & Elim Group

26

Balance sheet Sep 2008 Jun 2008 Sep 2007

Cash and balances with central banks 18,733 27,557 16,402Loans to credit institutions 221,403 219,111 242,706 Loans to the public 1,204,713 1,132,374 1,021,498Financial assets at fair value 633,099 597,723 661,314Available-for-sale financial assets 257,634 247,245 133,608Held-to-maturity investments 2,067 2,266 2,089Investment in associates 1,387 1,361 1,180Tangible and intangible assets 27,163 26,177 22,994Other assets 50,154 50,335 46,864

Total assets 2,416,353 2,304,149 2,148,655Deposits by credit institutions 399,940 397,601 360,609Deposits and borrowings from the public 794,266 757,904 706,623Liabilities to policyholders 206,473 211,938 217,516Debt securities 554,257 506,564 465,381 Financial liabilities at fair value 248,142 229,285 209,380Other liabilities 90,357 83,129 75,966 Provisions 1,378 1,265 1,590Subordinated liabilities 45,736 41,664 38,631Total equity 75,804 74,799 72,959

Total liabilities and equity 2,416,353 2,304,149 2,148,655

27

Relationship Deposits from and Lending to the public 2001 – 2008

30%

40%

50%

60%

70%

80%

90%

100%

2001 2002 2003 2004 2005 2006 2007 Q32008

Deposits to loans ratio

28

Deposits - Interbank

20%

Deposits - General Public

42%

CPs/CDs11%

Schuldscheins and Reg Bonds3%

Mortgage Covered Bonds Sweden10%

Mortgage Covered Bonds Germany2%Public Covered Bonds Germany7%

Senior debt2%

Subordinated debt3%

Funding structureSEB Group, Sep 2008SEK 1,702bn

* Over collateral within covered pools SEK 57bn

29

Net liquidity position across maturities30 Sep, SEK bn

More than 12 months matched funding, i.e. based on no access to capital markets, no refinancing of debt to credit institutions, issued bonds or subordinated capital; and moderate reduction of business activities.

0

50

100

150

200

250

300

1 week

2 weeks

4 weeks

2 months

3 months

4 months

5 months

6 months

9 months

12 months

Year-end 200730-Sep-08

SEB is match-funded approx.

one year

SEK bn

30

Capital adequacy SEB Group

7.9 8.0 7.8 7.5 8.2 8.6 8.1

10.5 10.2 10.3 10.8 11.5 11.010.4

Dec2002

Dec2003

Dec2004

Dec2005

Dec2006

Dec2007

Sep2008

Core capital ratio, % Total capital ratio, %

SEK bnCapital base 52.7 54.7 58.7 76.2 85.8 93.0 97.7Risk-w. Assets 503 535 570 704 741 842 937

Basel I 9,3%

Basel I 7,3%

Basel I 1.045

Basel II

31

Asset quality

32

Credit exposure On and off balance, SEK 1,805bn

14%

40%

14%

6%

26%

Property management

Public administration

BanksCorporate

Households

By sector

33

Credit exposure On and off balance, SEK bn

Sep 2008 (Dec 2007) Nordic German Baltic Total

Corporates 533 (416) 99 (72) 88 (83) 720 (571)

Property Management 119 (100) 98 (87) 28 (26) 245 (212)

Households 313 (292) 94 (87) 61 (55) 469 (434)

Public Administration 20 (18) 87 (66) 6 (3) 113 (88)

Total non-banks 986 (826) 377 (312) 183 (166) 1,547 (1,304)

Banks 204 (187) 52 (58) 2 (3) 258 (248)

Total 1,189 (1,013) 430 (369) 186 (169) 1,805 (1,552)

34

Dec -05 Dec -06 Dec -07 Jun -08 Sep -08Corporates 494 484 571 616 720

Property Management 192 192 212 229 245

Households 319 374 434 463 469

Public Administration 125 97 88 95 113

Total non-banks 1,130 1,146 1,304 1,403 1,547Banks 198 169 248 227 258

Total 1,328 1,315 1,552 1,631 1,805

Credit exposure On and off balance, SEK bn

35

240 269 330 35779

105104 111

Dec 2005 Dec 2006 Dec 2007 Sep 2008

Mortgage Other434

319 374469

Credit exposure – HouseholdsSEK bn

36

186219 227 235 235

55 67 68 70 7228 44 45 47 50

68

73 7679 78

27 20 20 21 22

1010 11 11 11

Dec'06

Dec'07

Mar'08

Jun'08

Sep'08

Dec'06

Dec'07

Mar'08

Jun'08

Sep'08

Dec'06

Dec'07

Mar'08

Jun'08

Sep'08

Mortgage Other

Nordic Germany Baltic

Households Credit PortfolioSEK bn

3737

Corporate credit exposure – by industrySEB Group, SEK bn

458 463

573

720

Dec2005

Dec2006

Dec2007

Sep2008

12%

11%

10%

18%3%

27%

19%

Finance and insurance Wholesale and retailTransportation Other service sectorsConstruction ManufacturingOther

38

40,5%

35,0%

3,3%

2,4%

6,3%

8,0%3,3%1,2%

Sweden Germany EstoniaLatvia Lithuania Other NordicOther European Other

Property management – by geography*SEB Group, SEK bn

101 111137 159

91 8175

86

Dec 2005 Dec 2006 Dec 2007 Sep 2008

Commercial Multi-family

192 192212

245

* By obligor’s domicile

39

0.6%

1.4%

0.2%

1.5%

0%

2%

Dec'03

Mar'04

Jun'04

Sep'04

Dec'04

Mar'05

Jun'05

Sep'05

Dec'05

Mar'06

Jun'06

Sep'06

Dec'06

Mar'07

Jun'07

Sep'07

Dec'07

Mar'08

Jun'08

Sep'08

SEB Group Germany Nordic Baltic

* Impaired loans gross* *Excluding Banks

Impaired Loan Volumes* % of Credit Exposure**

40

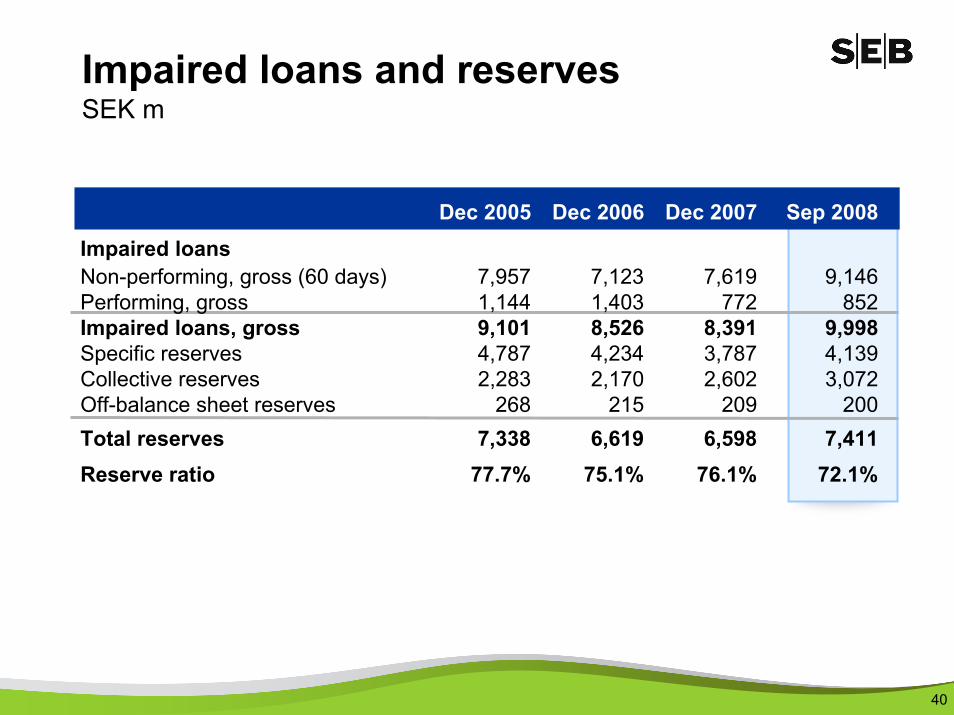

Impaired loans and reservesSEK m

Dec 2005 Dec 2006 Dec 2007 Sep 2008Impaired loansNon-performing, gross (60 days) 7,957 7,123 7,619 9,146Performing, gross 1,144 1,403 772 852Impaired loans, gross 9,101 8,526 8,391 9,998Specific reserves 4,787 4,234 3,787 4,139Collective reserves 2,283 2,170 2,602 3,072Off-balance sheet reserves 268 215 209 200Total reserves 7,338 6,619 6,598 7,411Reserve ratio 77.7% 75.1% 76.1% 72.1%

41

0.000.100.200.300.400.500.600.700.800.90

2003 2004 2005 2006 2007 Q12008*

Q1-Q22008*

Q1-Q32008*

Germany Baltics Nordics SEB Group

Level of Net Credit Losses, %

* Annualised

Estonia 1.31Latvia 0.96Lithuania 0.43Baltics 0.85

42

Credit losses and build up of reserves SEK m

Sum Average/ Jan – Sep Jan – Sep Change8 quarters quarter 2007 2008

Net credit losses, quarterly 2006 – 2008ProvisionsNet collective provisions -597 -75 -405 -419 -14Specific provisions -2,038 -255 -422 -930 -508Reversals of specificprovisions no longer required 772 97 242 194 -48Net provisions for contingent liabilities -2 0 32 -20 -52Net provisions (build-up of reserve) -1,865 -233 -553 -1,175 -622Write-offsTotal write-offs -2,803 -350 -833 -964 -131Reversal of specific provisionsutilized for write-offs 1,421 178 469 489 20Write-offs not previously provided for -1,382 -173 -364 -475 -111Recovered from previous write-offs 477 60 208 122 -86Net write-offs -905 -113 -156 -353 -197

Net credit losses -2,770 -346 -709 -1,528 -819Change in value of seized assets -13 -2 6 -17 -23Net credit losses incl change in value -2,783 -348 -703 -1,545 -842

43

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3Net credit losses, quarterly 2006 2006 2007 2007 2007 2007 2008 2008 2008

ProvisionsNet collective provisions -89 212 -114 -220 -71 15 -112 11 -318Specific provisions -124 -455 -245 -77 -100 -231 -190 -409 -331Reversals of specific provisions no longer required 133 173 75 87 80 163 44 79 71Net provisions for contingent liabilities 1 10 31 -7 8 -24 1 2 -23

Net provisions (build-up of reserve) -80 -60 -253 -217 -83 -77 -257 -317 -601

Write-offsTotal write-offs -334 -444 -243 -240 -350 -562 -332 -367 -265Reversal of specific provisionsutilized for write-offs 196 221 124 131 214 242 201 217 71Write-offs not previously provided for -138 -223 -119 -109 -136 -320 -131 -150 -194Recovered from previous write-offs 81 62 135 43 30 85 24 19 79

Net write-offs -57 -161 16 -66 -106 -235 -107 -131 -115

Net credit losses -137 -221 -237 -283 -189 -312 -364 -448 -716

Change in value of seized assets 1 -1 3 3 - -1 -4 -4 -9

Net credit losses incl change in value -136 -222 -234 -280 -189 -313 -368 -452 -725

Credit losses and build up of reserves quarterly developmentSEK m

44

17 22 22 18 21 2234 39 458 8 8

4 5 6

813

15

1419 20

1014 14

13

2226

564441

34

525041

89

76

Dec'06

Dec'07

Sep '08 Dec'06

Dec'07

Sep '08 Dec'06

Dec'07

Sep '08

Total

Banks

PublicAdministrationHouseholds

PropertyManagementCorporate

SEB Estonia SEB Latvia SEB Lithuania

Growth rates in local currency+38% +17% +40% +18% +47% +30%

2006 2007 2006 2007 2006 2007

+1%

2008 YTD

+4% +13% 2008 YTD 2008 YTD

Baltic countries – Credit exposure On and of balance, SEK bn

45

Baltic countries - Asset Quality

0

50

100

150

200

250

Estonia Latvia Lithuania

Net credit losses Q1 2007 - Q3 2008, SEK m

Impaired loans Q4 Q1 Q2 Q3% 2007 2008 2008 2008

Estonia 0.4 0.7 1.6 2.0Corporate 0.2 0.5 2.0 2.2Private 0.7 1.1 1.3 1.8

Latvia 0.5 0.8 1.1 1.6Corporate 0.3 0.3 0.6 1.0Private 1.0 1.5 2.0 2.8

Lithuania 0.8 0.9 1.0 1.2Corporate 0.8 0.8 0.9 1.1Private 0.8 1.2 1.4 1.6

* Corporate including Property Mangement

46

SEB Estonia

SEB Latvia

SEB Lithuania

Total Baltic

Impaired loans, gross

1,019 694 1,037 2,750

Specific reserves 294 80 401 775Collective 482 384 311 1,177Off balance reserves

0 0 0 0

Total reserves 776 464 713 1,952

Reserve ratio 76.1% 66.8% 68.8% 71.0%

Baltic countries Impaired Loans and ReservesSeptember 2008, SEK m

Impaired loans Q4 Q1 Q2 Q3SEK m 2007 2008 2008 2008

Estonia 186 334 819 1 019Corporate 47 132 570 657Private 138 202 249 362

Latvia 218 301 444 694Corporate 84 86 152 285Private 134 216 292 410

Lithuania 573 682 819 1 037Corporate 398 416 492 633Private 176 266 327 404

47

Estonia Latvia Lithuania Total

Net Write-offs & Actual Losses 3 -11 -1 -9

Net New Specific Provisions -273 -58 -69 -400

Net New Collective Provisions -158 -187 -117 -462

Change in Value of Seized Assets -1 -1 -5 -7

Net Credit Losses -429 -257 -192 -878

Baltic countries – Net Credit Losses Jan – Sep 2008, SEK m

48

Bond portfolios

49

Trading and Treasury etc

Held for trading (MTM over income) Available for sale (MTM over equity)

Mark-to-market losses over income of SEK 3,055m

Mark-to-market loss over equity of SEK 4,518m

The losses are expected to be recovered over time

Further volatility from the mark-to-market of these securities is expected; however with limited impact on income since 87 per cent of the SEK 130bn portfolio is classified as Available-for-sale at 30 September 2008

Investments (MB Credit and PortfolioManagement)

Fixed-income securities portfolio 30 September 2008, SEK 358bn

114

16

227 130

*Net of short and fully matched positions; excluding holdings in the insurance business

Impact on SEB’s portfolio values from credit turbulence since summer 2007

50

*Net of short and fully matched positions; excluding holdings in the insurance business

Structured credits18%

Financials24%

Covered bonds19%

Cover pool25%

Corp, Gov't etc

14%

Merchant Banking 207Group Treasury 143

Other divisions 8

Total 358

SEB Bond Portfolio*30 September, 2008, SEK bn

51

Capital Markets and other

30%

47%

9%

14%

Corporate bonds Financial institutionsGov't Covered bonds

Credit & Portfolio Management

49%42%

9%Structured credits Financial institutionsCovered bonds etc

Trading Investments

Merchant Banking Bond Portfolios30 September, 2008

Volume SEK 77bn Volume SEK 130bn

52

Structured creditsReduced volume: SEK 63bn (71)AAA-rating: 96.8% (99.3)MTM losses highly dependent on seniority, underlying assets and vintage

Financial institutions Unchanged volume: SEK 55bn (55)Rapid credit spread wideningMTM losses on all financial holdings, not only investment banks

Bond investment portfolio – status30 September, 2008 (31 December, 2007)

Covered bonds etc. SEK 12bn (5)

2007 Q1 08 Q2 08 Q3 08-872 -348

-2,134

-2,482

-1,630-1,769

-2,502

-66-56

-122

MTM (SEK m) Equity -698 -4,518

-2,467

AccP/L -3,055

-7,573

53

Structured credits Financial institutions2007 Q1 08 Q2 08 Q3 08

-41 -400

-1,107-1,507

-15-56

P/L

Equity

Acc-794-1,056

-626 -990 -2,738-1,682

-2,291

-1,784 -5,029

2007 Q1 08 Q2 08 Q3 08-26 51

-687-637

-52-78

P/LEquity

Acc-78-563

-72 -438 -1,249-635

-616

-515 -1,864

+ Covered bonds etc accumulated -680

Bond investment portfolio – financial effects30 September, 2008, SEK m

2007 Q1 08 Q2 08 Q3 08-872 -348

-2,134

-2,482-1,630

-1,769

-2,502

-66-56

-122

MTM (SEK m) Equity -698 -4,518

-2,467

AccP/L -3,055

-7,573

54

Limit P/L volatility by increasing AFS portfolios and reducing HFT portfolios Reduce subprime holdings, primarily in the HFT portfolioReduce the credit spread risk through partial hedging (ITRAXX)

30 29

0

26

41

5

ABS Financialinstitutions

Coveredbonds etc.

Q4 07 Q3 08

Held for trading (MTM over income)

Available for sale (MTM over equity)

SEK bn

Bond investment portfolio – strategy

51 51

114

12

1

ABS Financialinstitutions

Coveredbonds etc.

51 49

114

10

1

ABS Financialinstitutions

Coveredbonds etc.

Q2 08

55

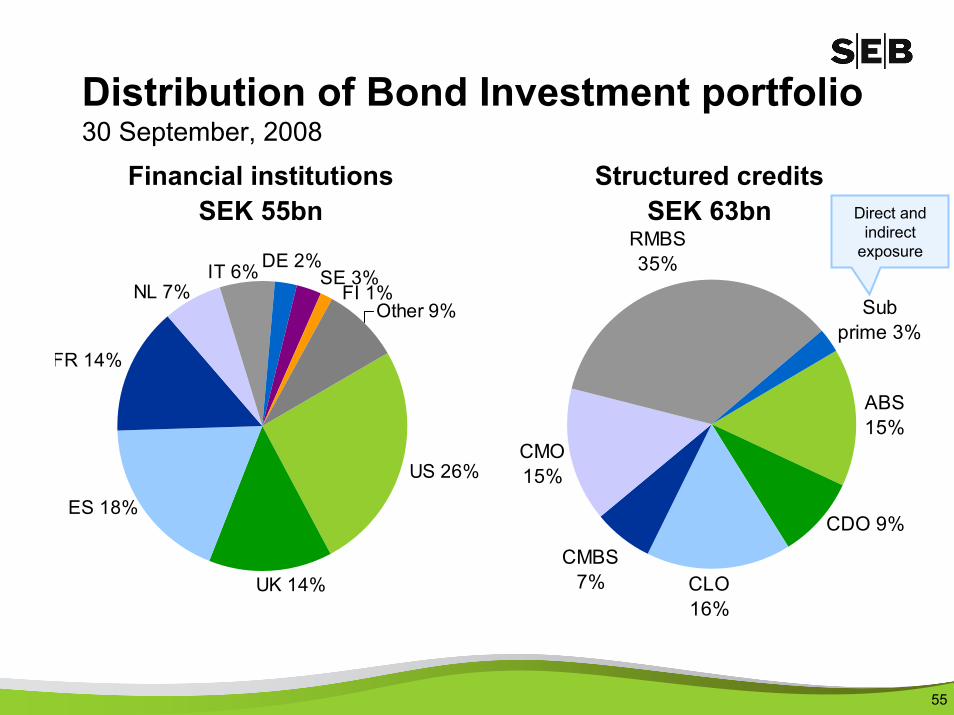

CMBS 7%

CMO 15%

RMBS 35%

Sub prime 3%

CLO 16%

CDO 9%

ABS 15%

Direct and indirect

exposure

Distribution of Bond Investment portfolio30 September, 2008

Financial institutionsSEK 55bn

Structured creditsSEK 63bn

FR 14%

IT 6%NL 7%

Other 9%FI 1%

SE 3%DE 2%

US 26%

UK 14%

ES 18%

56

A high quality investment portfolio initiated 1998 with fixed income securities eligible as central bank collateral

Total volume SEK 63bn – 684 positions

96.8% of the portfolio is rated Aaa/AAA, only 0.2% below investment grade– 9 positions have been downgraded from Aaa/AAA during Q3 by Moody’s

and Standard & Poor’s. Since the summer 2007, 34 positions have been downgraded

– Well diversified across products, asset classes and geographies– Cash-flow based – only one synthetic transaction (USD 10.5m)

Mark-to-market prices applied to all 684 positions– No level 3 assets

Current average remaining maturity ~4 years

Current annual amortisation rate is SEK ~10bn

Main characteristics of structured credits portfolio 30 September, 2008

57

Structured credits portfolio – ratingRating Composition (S&P, Moody’s and Fitch)Outstanding volumes , 30 September, 2008

0.02%0.18%0.07%2.98%

96.75%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

AAA AA/A BBB BB/B CCC

Q4-07 Q1-08 Q2-08 Q3-08

58

Divisions

Please note:A restatement of the divisional financial reporting has been carried out in conjunction with the Q1 2008 report as previously announced.Please consult www.sebgroup.com for more information.

59

Operating profit per divisionJan – Sep 2008 vs. Jan – Sep 2007SEK m

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000

Life

WealthManagement

Retail Banking

MerchantBanking

Jan-Sep 2008

Jan-Sep 2007

Changevs. Jan-Sep 2007

-21% (-11%)

-19%

-31%

-36%

ROEJan-Sep 2008

15.6% (20.2%)

14.5%

19.8%

13.3%

Excl. portfolio losses

Sweden: 3%Germany: -41%Estonia: -67%Latvia: -58%Lithuania: -11%Cards: -7%

60

Q1 Q2 Q3 Q4 Q1 Q2 Q32007 2007 2007 2007 2008 2008 2008

MB 465 492 459 483 526 531 589Retail Banking 468 483 493 513 518 545 561RB Sweden 256 264 271 279 286 303 307RB Estonia 37 39 40 42 42 43 44RB Latvia 31 35 34 36 35 36 37RB Lithuania 46 50 54 59 60 64 69RB Germany 85 81 80 81 81 82 87RB Cards 13 14 14 14 14 17 17Wealth Management 30 31 33 32 31 29 28Life - - - - - - -Other/Elim 54 42 36 39 24 27 27SEB Group 1,017 1,048 1,021 1,067 1,099 1,132 1,205

VolumesPublic lendingSEK bn

61

VolumesPublic depositSEK bn

Q1 Q2 Q3 Q4 Q1 Q2 Q32007 2007 2007 2007 2008 2008 2008

MB 371 384 364 389 409 392 426Retail Banking 231 249 249 262 257 264 269RB Sweden 130 139 139 145 145 149 151RB Estonia 18 20 20 22 20 22 22RB Latvia 16 17 17 18 17 18 17RB Lithuania 25 26 26 30 28 28 30RB Germany 43 46 46 48 47 47 49RB Cards - - - - - - -Wealth Management 47 54 51 53 54 56 52Life - - - - - - -Other/Elim 20 28 43 46 45 46 47SEB Group 670 715 707 750 765 758 794

62

FTEs, end of quarter

Q1 Q2 Q3 Q4 Q1 Q2 Q32007 2007 2007 2007 2008 2008 2008

MB 2,540 2,568 2,550 2,672 2,742 2,760 2,719Retail Banking 8,655 8,912 8,807 8,925 8,995 9,325 9,139RB Sweden 2,742 2,812 2,660 2,736 2,733 2,875 2,738RB Estonia 1,011 1,095 1,061 1,061 1,048 1,084 1,046RB Latvia 1,052 1,089 1,117 1,118 1,108 1,122 1,093RB Lithuania 1,333 1,387 1,428 1,492 1,520 1,579 1,652RB Germany 1,668 1,699 1,728 1,733 1,802 1,830 1,794RB Cards 849 830 813 785 784 835 816Wealth Management 1,099 1,050 1,064 1,073 1,160 1,143 1,123Life 1,194 1,203 1,199 1,218 1,222 1,235 1,250Other/Elim 5,842 5,886 5,820 5,906 7,091 7,182 7,197SEB Group 19,330 19,619 19,440 19,794 21,210* 21,645 21,428

* Whereof 1,039 encompasses the consolidated acquisitions of Factorial bank in Ukraine and Key Asset Management.

63

Summary per division Jan – Sep 2008

Merchant Banking

RetailBanking

WealthManagement Life Other Group

Operating profit, SEK m 4,397 3,603 1,360 852 -2,285 7,927

Business equity, SEK bn 27 25.3 ** 6.6 7.5 75.2 *

Return on equity, % 15.6 14.5 19.8 13.3 10.9

Cost / income ratio 0.55 0.61 0.59 0.66 0.66

RWA, SEK bn, Basel II 473 378 37 49 937

RWA, SEK bn, Basel I 541 426 23 55 1,045

Tax Rate 28% 24% 28% 12%

* Average shareholders' equity

** Where of Sweden 7.4bn Estonia 3.3bn, Latvia 3.1bn, Lithuania 4.4bn, Germany 4.5bn and Cards 2.6bn.

64

01020304050

MerchantBanking

Retail Banking WealthManagement

Life* Group

Jan - Sep 2007 Jan - Sep 2008Cost/income ratio per division

Return on Equity per division, per cent

* Based on operating profit

0.000.200.400.600.801.00

MerchantBanking

Retail Banking WealthManagement

Life Group

Jan- Sep 2007 Jan- Sep 2008

RoE and Cost/Income ratio per division

65

Magnus CarlssonHead of Merchant Banking

Merchant BankingHighlights

Continued strong earnings, despite market dislocations and summer effects

Underlying income in line with Q3 last year

Cost decline 17% from Q2

Operating profit reduced by MTM valuation effects and provisions for exposure on Lehman Brothers

Ranked No. 1 globally for customer satisfaction in cash management (Euromoney)

SEK m Jan – Sep 2008 Δ 2007

Total income 10,381 -11%Interest, net 4,801 17%Commission, net 4,085 -11%Financial, net 1,296 -45%

Total expenses -5,677 -3%Credit losses, net -311 21%Operating profit 4,397 -21%

RoE, % 15.6 20.3C/I 0.55 0.50

66

Merchant Banking SEK m

0

500

1,000

1,500

2,000

2,500

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Operating profit Excluding portfolios

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Excluding portfolios Income Expenses

67

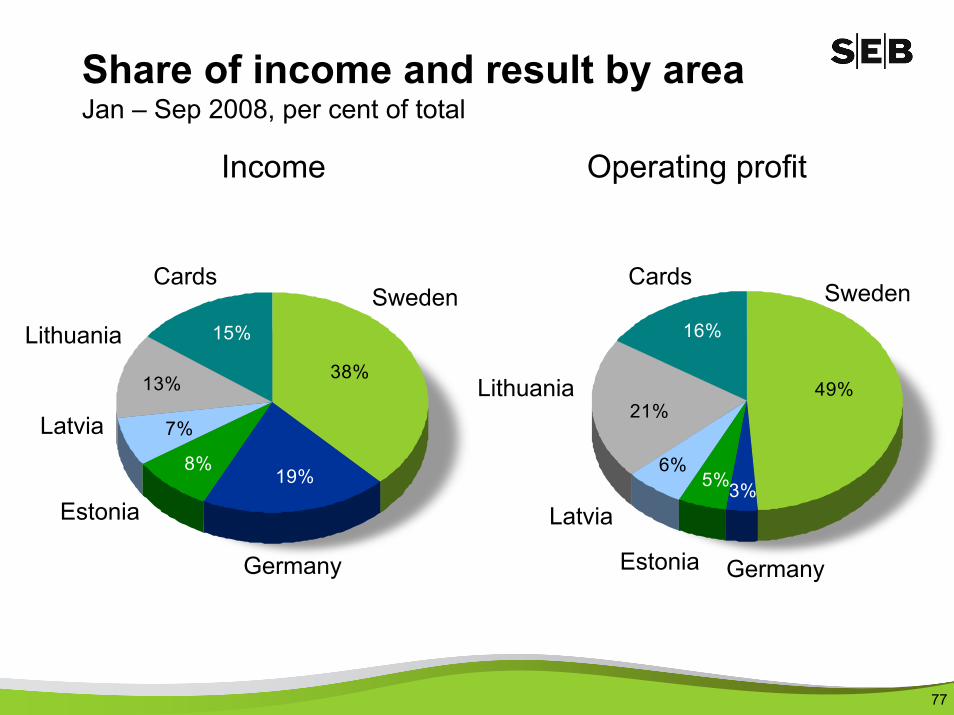

40%

37%

23%

Share of income and result by areaJan – Sep 2008, per cent of total

Income Operating profit

34%

41%

25%

Trading and Capital Markets

Global transaction services

CorporateBanking

Trading and Capital Markets

Global transaction services

CorporateBanking

68

Trading and Capital MarketsSEK m

0

300

600

900

1,200

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Operating profit Excluding portfolios

0

500

1,000

1,500

2,000

2,500

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Excluding portfolios Income Expenses

69

Trading and Capital Markets– focus on client driven activities

45%36%26% 28% 33% 38% 41%

45%49%

44% 46% 64% 46%49%

8%8%22% 15% 11%3%

6% 1%

7%11%8% 5%

4%

Q1 -07

Q2 Q3 Q4 Q1 -08

Q2 Q3

Trading and Capital Markets income by main product cluster, excl. investment portfolios

FX

Structured Derivatives and other TCM

Equities

Capital Markets

●Focus on customer flows ensures continued strong revenues

●Positive profitability trend in FX areas

●Strong revenues and increased market shares in Equities

● Lower profits in fixed income related units due to ongoing uncertainty in credit markets

70

Operating profit

0200400

600800

1,000

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0200400600800

1,0001,2001,4001,600

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

Corporate banking SEK m

2007 and 2008 including Baltics

71

Operating profit

0

100

200

300

400

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0100200300400500600700800900

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

Global Transaction Services SEK m

2007 and 2008 including Baltics

72

Custody volume development

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2004 2005 2006 2007 20080

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000Assets under custody, SEK bn No of transactions/day

73

Market Shares Nordic Stock Exchanges *Jan – Sep 2008

*Source: The Nordic Stock exchanges**Rank based on announced deals. All Nordic involvement. Source: Thomson Financial

4.6%

5.3%

5.4%

5.4%

9.2%

Carnegie

SHB

MorganStanley

Glitnir

SEB

Nordic M&A**

Jan – Sep 2008 (EUR m)

Merchant BankingInvestment banking rankings

9,137

12,163

12,786

15,582

18,127

SEB

UBS

MorganStanley

DeutscheBank

JP Morgan

10 Deals

14 Deals

14 Deals

17 Deals

29 Deals

74

Merchant Banking– Recent rankingsOctober 2008 No. 1 Globally for Overall Customer Satisfaction regarding Cash Management

Best for Real Estate Commercial Banking in the Nordic and Baltic region

Trade and Forfaiting Review July 2008 Best Trade Bank in Northern Europe & Scandinavia

Euromoney July 2008Best for Cash Management in Nordic & Baltic regionBest Equities House in Nordic & Baltic regionBest M&A House in the Nordic & Baltic region

Risk Magazine July 2008 Best derivatives dealer in Sweden

Thomson Rueters Extel June 2008 Best research house in the Nordic countries

Global FinanceApril 2008

World’s Best Developed Market Banks 2008, no. 1 in SwedenWorld’s Best Emerging Market Banks 2008 Central and Eastern Europe, no. 1 in Latvia and Lithuania

Söderberg & Partners February 2008 Best Arranger Structured Products, Sweden

Euroweek February 2008 Best Arranger Nordic Loans, Syndicated Loans and Leveraged Finance Awards 2007

Prospera January 2008 No.1 stockbroker in the Nordic region

FX Week January 2008 Best bank for international currency forecasts in 2007

Global Custodian November 2007October 2007

Top rated in Central and Eastern Europe (2007 Emerging Markets Agent Bank Review)Top rated in all four Nordic markets (2007 Major Market Agent Bank Review )

Global FinanceJanuary 2008

Best Bank for Cash, Liquidity and Risk Management, Nordic RegionBest Trade Finance bank, Nordic Region, Sweden and LithuaniaBest Foreign Exchange Bank and Provider in the Nordic countries and Lithuania

TMI January 2008 Best bank for Cash Management, Nordic RegionBest Bank for supply Chain Finance, Nordic Region

75

Retail Banking

SEK m Jan – Sep 2008 Δ 2007

Total income 12,547 3%Interest, net 7,899 10%Commission, net 4,233 -8%

Total expenses -7,677 6%Credit losses, net -1,267 195%Operating profit 3,603 -19%

RoE, % 14.5 18.6C/I 0.61 0.60

HighlightsBo MagnussonHead of Retail Banking Continued strong income

– NII +10% vs. 2007 offsets low security related fees

– Income growth Q3 +1% vs. Q2

Cost growth in Baltics due to inflation, real estate sale and 2007 sales expansion; higher pension cost in Sweden– Cost Q3 -2% vs. Q2

Profit before credit losses stable

Decrease in operating profit mainly driven by increased provisions in Estonia, Latvia and Lithuania

76

Retail BankingSEK m

Operating profit

0

500

1,000

1,500

2,000

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

77

Share of income and result by areaJan – Sep 2008, per cent of total

38%

19%8%

7%

13%

15%

Germany

Latvia

Estonia

SwedenLithuania

Cards

Income

16%

21%

6%5%3%

49%

Germany

Latvia

Sweden

Lithuania

Cards

Estonia

Operating profit

78

Business volume development by areaSEK bn Q3 2008 change vs. Q3 2007 (local currency)

53

27

29

23

70

16

11

15

64

237

Lithuania

Latvia

Estonia

Germany

Sweden 10%

0%

8%

8%

37%

10%

2%

4%

4%

19%

Mortgages Other lending

30

17

22

49

151

Deposits

8%

2%

1%

-2%

8%

Note: Figures for Estonia, Latvia and Lithuania include SEB:s large corporate business volumesSwedish Other lending growth adjusted for transfered leasing volumes

79

41%13%25%21%

Transaction account privateTransaction account corporate & publicSavings account privateSavings account corporate & public

Deposit breakdownPercent of total deposits

45%

24%

21%

10%

Retail Total

Estonia

Sweden Germany

Latvia Lithuania

53%

9%

21%

17%

42%

3%

3%

52%

22%

18%

39%

21%

29%

15%

36%

20%

35%

10%

31%

24%

80

Development of lending market shares – Baltics Per cent, Jan 2005 – Sep 2008

Estonia* Latvia Lithuania

* Sampo as per Q1 2008Swedbank as per Q2 2008

0%

10%

20%

30%

40%

50%

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q30%

10%

20%

30%

40%

50%

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q30%

10%

20%

30%

40%

50%

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

SEBSwedbankDnB NordParex BankaSampo/Danske bankNordea

81

Retail SwedenHighlightsSEK m Jan – Sep 2008 Δ 2007

Total income 4,749 4%Interest, net 3,453 14%Commission, net 1,106 -14%

Total expenses -2,899 5%Credit losses, net -86 29%Operating profit 1,764 3%

RoE, % 22.9 22.9 C/I 0.61 0.61

Total lending* 306,600 13%Total deposits 150,600 8%

Continued strong net income growth supported by volume and margin development

Decreased commission income due to brokerage and structured products

Strong SME growth: 5,300 new SME customers (2,800 same period 2007)

Cost affected by higher pension costs

* Adjusted for moved leasing volumes, lending increased with 10%

82

Business volume developmentRetail Sweden, SEK bn

Mortgages

0

50

100

150

200

250

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

CorporatePrivate

Other lending*

0

50

100

150

200

250

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Deposits

0

50

100

150

200

250

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

* Excluding leasing

83

Market share development Sweden, per cent Corporate

Private

Note: Other lending and deposits=SEB Parent Bank Sweden, i.e. not only Retail Sweden

Mortgages*

0

5

10

15

20

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q308

Other lending

0

5

10

15

20

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

Deposits

0

5

10

15

20

25

30

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

* New measurement method from Q4 2007. Lowers the volume market share with approximately 0.2 percentage points

84

Mortgages private marketRetail SwedenMarket share, per cent

02468

101214161820

Q105

Q2 Q3 Q4 Q106

Q2 Q3 Q4 Q107

Q2 Q3 Q4 Q108

Q2 Q3

Sales Volume

* New measurement method from Q4 2007. Lowers the volume market share with approximately 0.2 percentage points

*

85

Mortgages private marketTotal SwedenVolumes and margins

0

50

100

150

200

250

Q12005

Q2 Q3 Q4 Q12006

Q2 Q3 Q4 Q12007

Q2 Q3 Q4 Q12008

Q2 Q30.00%

0.25%

0.50%

0.75%

1.00%

1.25%Outstanding volume, SEK bn Average margin

86

Mortgages private marketSwedenCustomers’ choice of fixed / floating interest rates

0%

20%

40%

60%

80%

100%

Q12005

Q2 Q3 Q4 Q12006

Q2 Q3 Q4 Q12007

Q2 Q3 Q4 Q12008

Q2 Q3

FixedFloating

87

Retail GermanyHighlightsSEK m Jan – Sep 2008 Δ 2007

Total income 2,434 -4%Interest, net 1,449 3%Commission, net 960 -11%

Total expenses -2,247 -1%Credit losses, net -67 14%Operating profit 120 -41%

RoE, % 2.8 5.1C/I 0.92 0.90

Total lending 87,000 8%Total deposits 49,200 6%

Reduced profitability due to lower customer activity within securities-related-areas

Higher sales of insurance (+13%) and mortgages (+31%) vs. same period 2007

Stable cost level

88

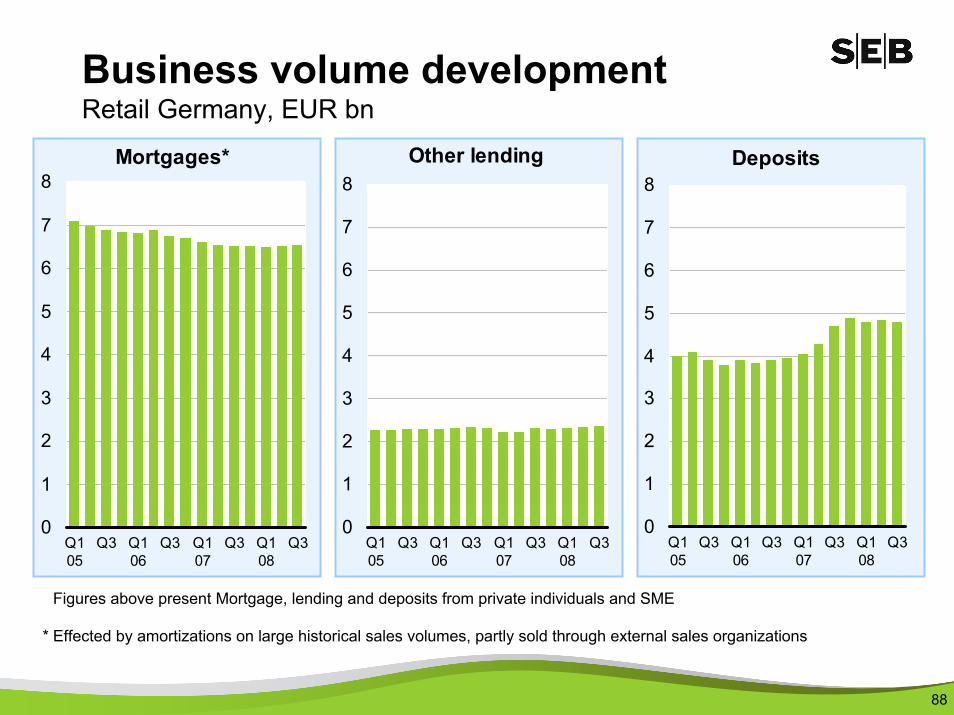

Business volume developmentRetail Germany, EUR bn

Mortgages*

0

1

2

3

4

5

6

7

8

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Other lending

0

1

2

3

4

5

6

7

8

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Deposits

0

1

2

3

4

5

6

7

8

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Figures above present Mortgage, lending and deposits from private individuals and SME

* Effected by amortizations on large historical sales volumes, partly sold through external sales organizations

89

New mortgage*

0

50

100

150

200

250

300

350

400

450

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Customer appointments*

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Insurance

0

20

40

60

80

100

120

140

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

* by Call centre

EUR m EUR m

* incl. prolongation

Sales developmentRetail Germany

90

Retail Estonia

Highlights

Strong focus on credit quality, including increase of loans overdueIncreased credit provisioning reflecting weakened macro economic outlookReduced lending market shareIncreased savings focus - new mutual funds launched Package solution for private customers’ daily needs attracted more than 30,000 customers, whereof half new to the bankLower cost in Q3 than Q2

SEK m Jan – Sep 2008 Δ 2007

Total income 1,032 8%Interest, net 685 6%Commission, net 255 -2%

Total expenses -426 23%Credit losses, net -428 598%Operating profit 178 -67%

RoE, % 6.1 17.7C/I 0.41 0.36

Total lending 44,500 +12%Total deposits 21,900 +7%

91

Business volume developmentRetail Estonia, EUR bn Corporate

Private

Mortgages

0

1

2

3

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Other lending

0

1

2

3

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Deposits

0

1

2

3

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Mortgages defined as home loans to private individualsNote: Figures include SEB:s large corporate business volumes

92

Market share developmentRetail Estonia, per cent Corporate

Private

Mortgages

0

5

10

15

20

25

30

35

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

Deposits

0

5

10

15

20

25

30

35

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

Mortgage market share for home loans to private individuals

93

Retail Latvia

HighlightsHighlightsSEK m Jan – Sep 2008 Δ 2007

Total income 926 -6%Interest, net 754 4%Commission, net 141 -43%

Total expenses -462 19%Credit losses, net -244 268%Operating profit 220 -58%

RoE, % 8.1 18.6C/I 0.50 0.40

Total lending 37,500 11%Total deposits 17,000 3%

Strong focus on credit quality, including increase of loans overdue

Increased credit provisioning reflecting weakened macro economic outlook

Reduced lending market share

Increased savings focus - new mutual funds launched

Lower cost in Q3 than Q2

94

CorporatePrivate

Business volume developmentRetail Latvia, EUR bn

Mortgages

0

1

2

3

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Other lending

0

1

2

3

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Deposits

0

1

2

3

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Mortgages defined as home loans to private individuals

Note: Figures include SEB:s large corporate business volumes

95

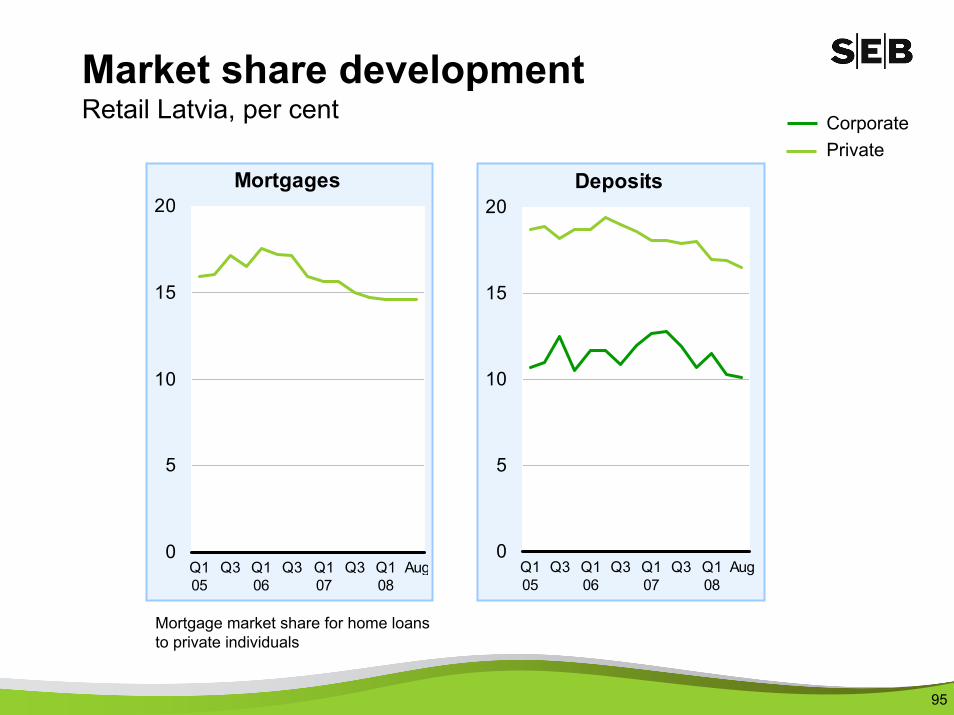

Market share developmentRetail Latvia, per cent

Mortgage market share for home loans to private individuals

CorporatePrivate

Mortgages

0

5

10

15

20

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

Deposits

0

5

10

15

20

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

96

Retail LithuaniaSEK m Jan – Sep 2008 Δ 2007

Total income 1,575 8%Interest, net 1,193 10%Commission, net 311 1%

Total expenses -642 22%Credit losses, net -186 103%Operating profit 747 -11%

RoE, % 19.2 21.1C/I 0.41 0.36

Total lending 68,700 28%Total deposits 30,100 15%

Highlights

Controlled credit growth

Increased credit provisioning reflecting macro economic outlook

Reduced lending market share

SEB awarded best consumer Internet bank in Lithuania for the third consecutive year by Global Finance

97

Business volume developmentRetail Lithuania, EUR bn Corporate

Private

Mortgages

0

1

2

3

4

5

6

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Other lending

0

1

2

3

4

5

6

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Deposits

0

1

2

3

4

5

6

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Q3

Mortgages defined as home loans to private individualsNote: Figures include SEB:s large corporate business volumes

98

Market share developmentRetail Lithuania, per cent

Mortgage market share for home loans to private individuals

CorporatePrivate

Mortgages

0

5

10

15

20

25

30

35

40

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

Deposits

0

5

10

15

20

25

30

35

40

Q105

Q3 Q106

Q3 Q107

Q3 Q108

Aug

99

CardsSEK m Jan – Sep 2008 Δ 2007

Total income 1,834 10%Interest, net 364 45%Commission, net 1,445 4%

Total expenses -1,004 3%Credit losses, net -257 204%Operating profit 573 -7%

RoE, % 21.2 28.1C/I 0.55 0.58

Highlights

Continued underlying business growth, turnover +7%

Continued strong cost discipline

Increased losses due to consumer finance transfer and higher fraud

Several new customer offerings launched, e.g. Eurocard Platinum

100

Cards

Turnover cards

203040506070

Q12003

Q2 Q3 Q4 Q12004

Q2 Q3 Q4 Q12005

Q2 Q3 Q4 Q12006

Q2 Q3 Q4 Q12007

Q2 Q3 Q4 Q12008

Q2 Q3

SEKbn

Number of cards

2.62.83.03.23.4

Q12005

Q2 Q3 Q4 Q12006

Q2 Q3 Q4 Q12007

Q2 Q3 Q4 Q12008

Q2 Q3

Millions

101

Fredrik BohemanHead of Wealth Management

Wealth ManagementHighlights

Revenues stable compared to Q2. Strong net interest, weak performance fees. Cost lower than Q2. Profit slightly up compared to Q2

Strong net sales in Q3 for both PB and IC

Assets under management. SEK 1,181bn, -8% since year end

SEB kept capturing volumes on a continued weak net sales market for Swedish mutual funds, SEK +5,9bn vs. total market of SEK -31bn.

SEKm Jan – Sept 2008 Δ 2007

Total income 3,320 -12%Interest, net 678 13%Commission, net 2,562 -17%

Total expenses -1,958 10%

Operating profit 1,360 -31%

RoE, % 19.8 34.5C/I 0.59 0.47

102

Share of income and result by areaJan – Sep 2008, per cent of total

67%

33%

Private Banking

Institutional Clients

Income

25%

75%

Private Banking

Institutional Clients

Operating profit

103

Operating profit

0

200

400

600

800

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0200400600800

1,0001,2001,400

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

Wealth ManagementSEK m

104

Institutional ClientsSEK m

Operating profit

0

200

400

600

800

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0100200300400500600700800900

1,000

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

105105

Private BankingSEK m

Operating profit

050

100150200250

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0

100

200

300

400

500

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

106

1,285

1,181-156

19

33

Dec 2007 Value Fx Net sales Q3 2008

Assets under managementWealth Management, SEK bn

107

Q1-06 Q2-06 Q3-06 Q4-06 Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Institutional portf incl Stiftelser & Ftg (excl MF) Mutual Funds Private Clients

48%

1,107 1,0791,147 1,192

1,266 1,320 1,300 1,285 1,256

48% 47% 47% 46% 46% 45% 45% 45% 44%

13% 14% 15%15%

15%15% 15% 15% 15% 15%

39% 38% 38% 39% 39% 40% 40% 40% 41%40%

1,217

46%

40%

14%

1,181

Assets under managementper product typeWealth Management, SEK bn

107

108

Total net sales per quarterSEK bn

19,7

9,413,6

7,6

16,4 15,5

6,32,0

8,2 9,0

3,0

2,31,0

0,8

4,1

2,92,6

3,5

5,8

4,9 5,3

10,9

0

5

10

15

20

25

Q12006

Q2 Q3 Q4 Q12007

Q2 Q3 Q4 Q12008

Q2 Q3

IC PB

The figures are not eliminated.

109

Mutual funds per product type Wealth Management, Sep 2008 (Jun 2008)

32.0%

29.1%

12.5%

26.4%

Equity funds 32.0% (35.5 %)

Fixed income funds 26.4% (25.0 %)

Balanced funds 12.5% (12.0 %)

Alternative funds 29.1% (27.5 %)

Total amount SEK 475bn (SEK 496bn)

Note: Key Asset Mgmt is included from Q1-08

110

Swedish Mutual Funds MarketNet sales and SEB market share

-30

-10

10

30

50

70

90

110

2001 2002 2003 2004 2005 2006 2007 Q32008 0

10

20

30

40

50

60

70

Total Net Sales, SEKbn SEB share, %

%N/A

Source: Svensk Fondstatistik

SEK -31bn

SEBSEK +5,9bn

111

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Jan-05

Maj Sep Jan-06

May Sep Jan-07

May Sep Jan-08

May Sep

SEBSHBRoburNordea

Mutual Funds Net Sales SwedenCumulative Jan 2005 – Sep 2008, including PPMSEKm

Distribution per type of fundJan – Sep 2008

-80%-60%-40%-20%

0%20%40%60%80%

SEB Total

Equity funds Mixed fundsShort bond funds Long bond fundsFund in fund Alternative funds

Activity level – Wealth

Source: Svensk Fondstatistik

112

Performance vs. benchmark 2008

6149

30

79

54

34

0

20

40

60

80

100

2006 2007 Q3 20080

20

40

60

80

100

AuMexceeding benchmark

No. of portfoliosexceeding benchmark

113

LifeAnders MossbergHead of Life

* Based on business result

SEK m Jan – Sep 2008 Δ 2007

Total income 2,525 -13%Total expenses -1,673 6%

Operating profit 852 -36%Change in surplusvalues, net 609 -28%

Business result 1,461 -33%

ROE, %* 22.9 33.9C/I ratio 0.66 0.54

Highlights

Positive sales development – up 11%, despite increasingly competitive markets and financial unrest

Lower operating profit due to adverse equity and interest rate development

Increased costs owing to investments in new markets and higher sales

Provision made to cover potential future guarantees in Nya Liv

114

LifeSEK m

Operating profit

0100200300400500

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

0

200

400

600

800

1,000

1,200

Q1-07 Q2-07 Q3-07 Q4-07 Q1-08 Q2-08 Q3-08

Income Expenses

115

Share of income and profit by areaLife, Jan – Sep 2008 – per cent of total

63%28%

9%

Sweden

Denmark

International

Income Operating profit

65%

30%

5%

Sweden

Denmark

International

Sweden including central functions etc

116

Results – LifeSEK m

Jan – Sep Jan – Sep Change2008 2007 %

Income unit-linked 1,444 1,589 -9Income other insurance 741 886 -16Other income 340 431 -21Total income 2,525 2,906 -13

Operating expenses -1,838 - 1,683 9Other expenses -23 - 19 20Change in deferred acquisition costs 188 123 53Total expenses -1,673 - 1,579 6

Operating profit 852 1,327 -36Change in surplus values, net 609 842 -28Business result 1,461 2,169 -33Financial effects due to market fluctuations -2,912 374 -Change in assumptions 12 - -Total result -1,439 2,543 -157

117

852

-263 -177 -121 -47

1817316

570

968

1,520

1,802

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 Jan-Sep

2008

Operating profit developmentLife, SEK m

118

Strong market position in all marketsMarket shares, gross premium income, unit-linked insurance (%, 2008)

1

2

2

3

2

SEBRank

Skandia (15)

Hansa (37)

Sampo (35)

Hansa (30)

Main competitor

Danica (41)

* Sweden new sales** Denmark full year 2007

26

18

33

10

24

0% 20% 40% 60% 80% 100%

Lithuania

Latvia

Estonia

Denmark**

Sweden*

SEB Market share Competitors

119

Market shares, Sweden Unit-linked new business,12 months to September 2008 (2007)

Övriga 0,2% (0,2)

Moderna9,9% (13,5%)

AMF 3,0% (3,1%)

Folksam 8,0% (8,0%)

Danica 3,3% (4,1%)

SHB 4,5% (4,7%)

Swedbank 10,7% (10,5%)

LF 10,4% (10,1%)

Skandia13,9% (13,6%)

SEB Trygg Liv 23,8% (23,6%)

Nordea 7,7% (4,8%)

SPP 4,5% (3,7%)

120

Note: SPE = Single premiums plus regular premiums times ten

Sales (SPE) Life, SEK m

Jan – Sep 2008 Jan – Sep 2007 Change

Unit linked 27,343 25,911 6%

Traditional andSickness/health 8,541 6,410 33%

35,884 32,321 11%

121

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 Jan-Sep

2008

Traditional andsickness/health

Unit Linked

Note: SPE = Single premiums plus regular premiums times ten

Sales SPE – traditional vs. unit-linkedLife including SEB Pension from 2005 and the Baltics from 2006

122

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007 Jan-Sep

2008

Individual

Corporate

Note: SPE = Single premiums plus regular premiums times ten

Sales SPE – individual vs. corporateLife including SEB Pension from 2005 and the Baltics from 2006

123

Unit-linked insurance sales growthSwedish* sales volumes weighted, SEK bn

27.1

34.931.6

26.722.8

2004 2005 2006 2007 Jan-Sep2008

Market ShareSweden, % 34.6 32.4 29.1 22.1 24.4**

*Including Swedish customers of the Irish subsidiary.

** 12 months to Q2 2008.

124

New business profitLife (2005-2006 only Swedish market), SEK m

Oct 2007- Full year Full year Full yearSep 2008 2007 2006 2005

New sales (single/10+regular) 3,845 3,689 3,345 3,678

Net present value 1,592 1,775 1,788 1,924Acquisition cost -850 -901 -970 -1,116

New business profit 742 874 818 808

Margin*, % 19.3 23.7 24.5 22.0Swedish market 20.5 22.9

* Rolling 12-months comparison

125

Sep Dec Dec Dec2008 2007 2006 2005

Equity * 8,421 8,836 8,450 7,696

Surplus value ** 12,160 14,496 12,872 10,765

* Dividend paid; 2008 SEK -1,275 2007: SEK -1,150 2006: SEK -400m.

** Value of in-force business; Net of DAC, including SEB Link (Denmark) from 2005

Embedded valueLife Holding group, SEK m

126

Life, assets under management(net assets)SEK bn

215

311

368395 408

364

0

100

200

300

400

500

2003 2004 2005 2006 2007 2008 Q3

Traditional and Risk Unit-linked

127

Life, premium income grossSEK bn

13

17

31 31

26

21

0

5

10

15

20

25

30

35

2003 2004 2005 2006 2007 2008 Q3

Traditional and Risk Unit-linked

128

-16,000

-12,000

-8,000

-4,000

0

4,000

8,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20Year

Income/Costs& CF, SEK

Cost Income Accum cash flow

Net present value after sales costs is 11,000 SEK

Acc op result -592 -540 977* SEK 35,000

Profits generated over timeExample: Occupational pension – regular premium*Total duration of 20 years and premium duration of 15 years

129

Macro Update

130

Overall assessment

Asset erosion and financial stress are seriously jeopardising global growth

Inflation risks are fading while deflation is knocking on the door

Downside risks to our previous below consensus forecasts are now materialising

We still welcome further central bank actions, but conclude that fiscal policy must become more proactive to support growth

131

Sweden: Lengthy cyclical slowdown

Exports continuing to lose momentum

Falling asset prices will squeeze consumption

Inflation has peaked

Further interest rate cuts next year

Expansive fiscal policy and budget deficits

GDP and Economic tendency indicator

0

1

2

3

4

5

6

7

97 98 99 00 01 02 03 04 05 06 07 080

20

40

60

80

100

120

140

GDP (LHS) Economic tendency indicator (RHS)

Sources: Statistics Sweden, SEB

Index

Year-on-year percentage change

132

Mainland GDP and Employment

-3

-2

-1

0

1

2

3

4

5

6

03 04 05 06 07 08

GDP Employment

Weaker global demand slows export growth

Buying spree fading –construction falling

Unemployment has bottomed out

Rate cuts

Year-on-year percentage change

Source: Statistics Norway

Norway: Clear deceleration from a high level

133

Finland: Weak growth next year

Sharp decline in leading indicators

Capital spending and exports will decelerate

Private consumption will slow down

Unemployment will start to climb this autumn

High inflation this year, lower next

Index

Source: Reuters EcoWin

Leading indicators

-60

-40

-20

0

20

40

60

80

99 00 01 02 03 04 05 06 07 08

Manufacturing Service Construction

134

Denmark: Close to stagnation

Continued house market correction

Unemployment turns upwards in the second half of 2008

Continued weak private consumption

Exports being squeezed from several directions

Expansive fiscal policy despite inflation upturn

GDP and Economic sentiment indicator

-2

-1

0

1

2

3

4

5

95 96 97 98 99 00 01 02 03 04 05 06 07 080

20

40

60

80

100

120

140

GDP (LHS) Economic sentiment indicator (RHS)

Sources: DG ECFIN, Statistics Denmark

Year-on-year percentage change Index

135

German IFO Index

60

70

80

90

100

110

120

99 00 01 02 03 04 05 06 07 08

Main index Current conditions Expectations

Index

Euro zone: Recession on its way

Sources: Eurostat, SEB

Negative GDP growth in Q2, and probably also in Q3, Q4No private consumption upturn in sightLabour market conditions are beginning to softenInflation will peak in late 2008ECB will cut refi rate to 2.00 per cent next year

136

Baltics: Lengthy adjustment Lengthy recession in Estonia and Latvia; negative growth both in 2008 and 2009Weak growth in less overheated Lithuanian economyDomestic demand remains depressedIncreased exchange rate risk in Estonia and LatviaLarge imbalances will dampen:– Wage inflation declines sharply – Large current account deficits will

shrink, but still high 2010

Year-on-year percentage change

Source: Reuters EcoWin

Retail sales

-15-10

-505

101520253035

01 02 03 04 05 06 07 08

Estonia Latvia Lithuania

137

GDP growth forecasts

2007 2008 2009 2010

United States 2.0 1.3 -1.5 0.8

Euro zone 2.6 1.0 -1.3 0.5

United Kingdom 3.0 0.8 -2.0 0.5

Nordic countries 3.0 1.4 -1.0 0.7

OECD 2.6 1.0 -1.2 0.6

World 5.0 3.4 0.9 2.3

138

SEB Forecasts GDP (%) Inflation (%)2007 2008 2009 2010 2007 2008 2009 2010

Denmark* 1.8 0.2 -1.5 0.0 1.7 3.6 1.8 1.8Finland* 4.4 2.4 -0.3 0.6 1.6 4.0 2.2 1.7Norway 3.7 1.9 0.1 1.8 0.8 3.8 2.1 2.1Sweden 2.9 0.8 -1.3 0.6 2.2 3.6 1.2 0.9Germany* 2.5 1.3 -1.2 0.6 2.3 2.8 1.0 1.2Euro zone* 2.6 1.0 -1.3 0.5 2.1 3.3 0.9 1.0Estonia* 7.1 -2.0 -4.0 -1.0 6.6 10.5 3.9 1.9Latvia* 10.3 -1.5 -5.0 -1.0 10.1 15.5 5.0 3.0Lithuania* 8.8 5.5 -2.0 -2.0 5.8 11.5 8.0 7.0Russia 8.1 6.5 1.0 3.0 9.0 14.0 9.8 8.5Ukraine 7.3 5.0 -5.0 2.0 12.8 24.5 15.0 10.0

Specific GDP growth forecasts

Sources: National statistical agencies, SEB Nordic Outlook October 2008* Harmonised consumer price index