second annual nyse small-cap conference for non-u.s. companies new york, may 6 - 7, 2004

TRANSCRIPT

Second Annual NYSE Small-Cap Conferencefor Non-U.S. Companies

New York, May 6 - 7, 2004

Steel Sector

Gerdau S.A. Consolidated

Stock Market

2003 2002 Var. %

1 China 220.1 181.7 21.1%

2 Japan 110.5 107.7 2.6%

3 United States 91.4 92.2 -1.0%

4 Russia 61.3 58.6 4.7%

5 Korea 46.3 45.4 2.0%

6 Germany 44.8 45.0 -0.4%

7 Ukraine 36.7 34.1 7.8%

8 India 31.8 28.8 10.3%

9 Brazil 31.1 29.6 5.1%

10 I taly 26.7 26.0 3.0%

Other 244.4 236.7 3.3%

TOTAL 945.1 885.8 6.7%

World ProductionCrude Steel

In million tons

Sources: IISI and MEPS

In the 1Q 2004,

the world

produced

247.7 million

tons of crude

steel.

Brazil

contributed

with 3.2% of

this tonnage.

03

Largest ProducersCrude Steel 2002

Source: IISI

In million tonsProduction

1 Arcelor 44.0

2 LNM Group 34.8

3 Nippon Steel 29.8

4 POSCO 28.1

5 Shanghai Baosteel 19.1

6 Corus 16.8

7 Thyssen Krupp 16.4

8 NKK 15.2

Company

(LUX)

(ENG)

(JAP)

(KOR)

(CHI)

(ENG)

(GER)

(JAP)

9 Riva 15.0

10 US Steel 14.4

11 Kawasaki 13.7

12 Nucor 12.4

13 Sumitomo 11.8

14 Gerdau 11.5

15 SAIL 11.4

Company Production

(ITA)

(USA)

(JAP)

(USA)

(JAP)

(BRA)

(ENG)

04

OverviewBrazilian Steel Sector - 2003

Belgo (Arcelor) – 33.8%2,654 thousand tons

Gerdau Açominas – 49.6%3,894 thousand tons

Barra Mansa - 5%385 thousand tons

Aços Villares - 6%456 thousand tons

V&M do Brasil - 6%466 thousand tons

LONG STEEL PRODUCERS IN BRAZIL

Source: IBS

CRUDE STEEL PRODUCERS IN BRAZIL

In thousand tonsUsiminas/Cosipa

Gerdau Açominas

Belgo/CST/Acesita (Arcelor)

CSN

Aços Villares

V&M do Brasil

Barra Mansa

8,624

6,976

8,449

5,318

775

551

421

MWL Brasil 36

05

TOTAL 2003: 7,855 thousand tons

TOTAL 2003: 31,150 thousand tons

Exports of Long Steel ProductsBrazilian Steel Sector - 9M2003

Source: IBS

Exports Domestic SalesExports of long steel products

reached 2.2 million tons in 2003, an increase

of 78% YoY.

In million tons

Domestic SalesSep.2003/2001

- 11%

ExportsSep.2003/2001

+85%

2001 2002 2003

Monthly Average 517.2 thousand tons

100

200

300

400

500

600

700Monthly Average

528.2 thousand tonsMonthly Average

461.5 thousand tons

Monthly Average 84.4 thousand tons

Monthly Average 99.2 thousand tons

Monthly Average 156.3 thousand

tons

06

CompetitivenessBrazilian Steel Sector

Source: IBS

EBITDA MARGIN - 2002

Brazil Asia*

* Does not include Japan

Japan EU North America

Others (World)

In %

5

10

15

20

25

30

35

40

Despite increases in the prices of main inputs, Brazil has the highest operating margin in the world.

The mills operate with up-to-date technology due to a permanent investment program.

35%

07

InvestmentsBrazilian Steel Sector

Source: IBS

INVESTMENT SCHEDULE

In US$ million

30 31 29

33 33 34 34 35

40 40

3028 302826 25 25 26 26 25

28 27

31

2423222119181918161617

151313

0

10

20

30

40

50

20071994 95 96 97 98 99 00 01 02 03 04 05 06

In million tons

Apparent Consumption

Installed Capacity

Crude Steel Production

INSTALLED CAPACITY X PRODUCTION X APPARENT CONSUMPTION

08

2003 2004 2005 2006 2007 TOTAL

FLAT STEEL 613.4 694.0 854.4 351.5 117.9 2,631.2

LONG STEEL 290.3 276.2 281.2 185.9 180.1 1,213.7

SPECIALTY STEEL 72.8 58.5 50.4 38.1 32.3 252.1

TOTAL 976.5 1,028.8 1,186.0 575.4 330.4 4,097.0

Steel Sector

Gerdau S.A. Consolidated

Stock Market

Main Products

BILLETS, BLOOMS& SLABS MERCHANT BARS REBARS FABRICATED STEEL

HEAVYSTRUCTURAL SHAPES WIRE-ROD WIRES NAILS

10

Billets, merchant bars, rebars, wire

rod, drawn products, welded

meshes, nails, downstream

products and fabricated steel

products.

Billets, slabs, blooms, merchant bars,

rebars, wire rod, drawn products,

welded wire meshes, structurals,

nails, downstream products, fab.

steel products and specialty steel.

Billets, merchant bars, rebars

and wire rod.

CRUDE STEEL

SLABS, BLOOMS

& BILLETS

In thousand tons

Gerdau Açominas

SouthAmerica

NorthAmerica

7,575

510

6,568

2,610

TOTAL 14,653 2,610

COMMON ROLLED PRODUCTS

4,640

634

6,186

11,460

-

-

PRODUCTS

Installed Capacity

11

12.3 million

9.0 million

AzaChile1992

MRMCanada1995

Part. Açominas

1997AmeriSteel

USA1999

CearenseGuaíra1982

LaisaUruguay

1981

Hime1985

Barão de Cocais1988

CourticeCanada1989

Usiba1989

Piratini1992

Pains1994

Sipsa Argentina

1997

Açominas(control)

2002

Co-Steel2002

20031980 1984 199619921988 2000

Part. Sipar

Argentina1998

Output EvolutionAVERAGE GROWTH RATE

1980 - 2003Crude Steel 10.2% per year

Rolled Products 9.2% per year

14th largest world steel producer according to the IISI. Largest long steel producer in the Americas.

Crude Steel Rolled Products

12

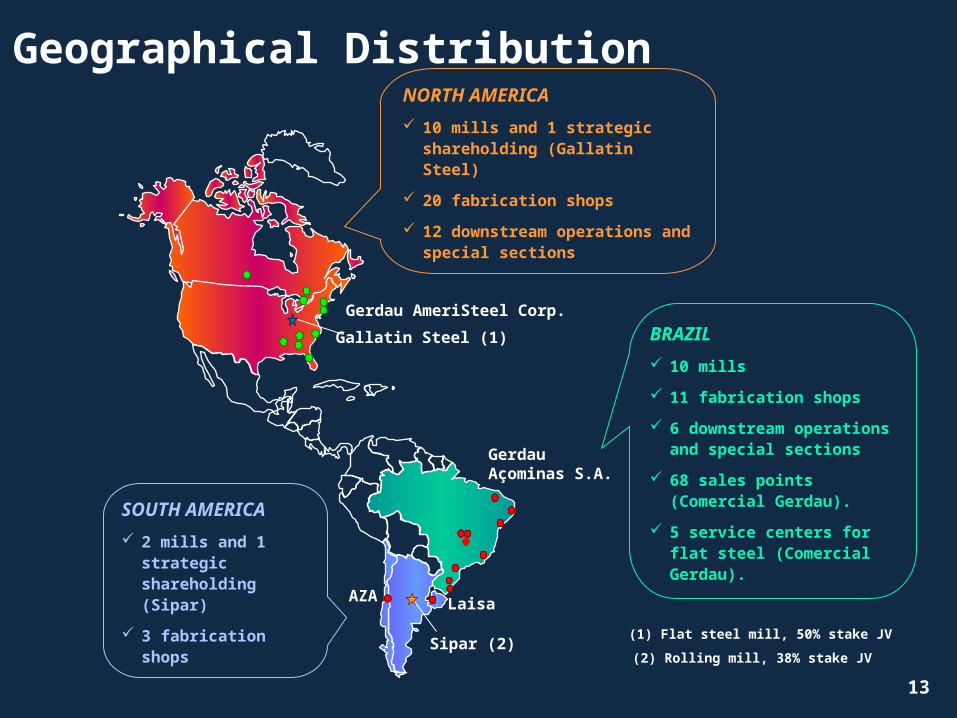

Geographical Distribution

(2) Rolling mill, 38% stake JV

(1) Flat steel mill, 50% stake JV

SOUTH AMERICA

2 mills and 1 strategic shareholding (Sipar)

3 fabrication shops

BRAZIL

10 mills

11 fabrication shops

6 downstream operations and special sections

68 sales points (Comercial Gerdau).

5 service centers for flat steel (Comercial Gerdau).

NORTH AMERICA

10 mills and 1 strategic shareholding (Gallatin Steel)

20 fabrication shops

12 downstream operations and special sections

Gerdau AmeriSteel Corp.

Sipar (2)

Laisa

GerdauAçominas S.A.

AZA

Gallatin Steel (1)

13

Competitive Edge

Focus on long steel products manufacturing and distribution

Market mill approach

Up-to-date technology

Competitive production costs

Diversified production processes

Multiple raw materials sourcing

Vertical and horizontal integration

Relevant market share in every country in which the Company has operations

Financial soundness and access to international capital markets

Confirmed experience in turning around distressed operations

14

Results 1Q20041Q2004 4Q2003 1Q2003

GROSS SALES 4,973 4,169 3,925

Net Sales 4,173 3,516 3,327

Cost of Sales (3,156) (2,648) (2,495)

Gross Profit 1,017 869 832

SG&A (306) (364) (280)

Net Financial Expenses (154) (156) (109)

Other Operating Revenues 18 16 -

Equity Pick Up 17 (14) (89)

Operational Income 593 350 353

Non Operating Revenues/ Expenses (10) 6 (1)

Income Tax & Social Contribution (148) (117) (60)

Statutory Participation (8) (13) (5)

Net Income 427 460 287

Controlling Shareholders 382 458 246

Minority Shareholders 45 2 41 15

NORTH SOUTH TOTAL TOTALBRAZIL AMERICA AMERICA 1Q04 2003

In R$ millionNet Sales 1,988 2,028 157 4,173 13,367 Gross Profit 759 195 63 1,017 3,290 EBITDA 620 204 59 883 2,683 Net Income 324 62 41 427 1,255

In R$/ TonNet Sales 1,221 1,460 1,300 1,330 2,029 Gross Profit 466 140 522 324 499 EBITDA 381 147 489 281 407 Net Income 199 45 339 136 191

In %Gross Margin 38% 10% 40% 24% 25%EBITDA Margin 31% 10% 38% 21% 20%Net Margin 16% 3% 26% 10% 9%

Results by Regions1Q2004

16

Brazil(domestic sales)

Brazil(exports)

NorthAmerica

SouthAmerica

436416

352

376

5,180

3,476

3,400

5,140

3,211

3,376

3,034

1,891

3,874

2,294

1,068

3,656

351

2,264

1,052

3,546

285

927

730

3,152

260505208

2,837208

240499

2,711

1997 1998 1999 2000 2001 2002 2003 1Q04Annualized

3,658 3,811 5,094 7,213 7,394 9,151 12,144 12,492 TOTAL TONS

Sales Track Record

In thousand tons

17

Indebtedness

In R$ million

GROSS DEBT

Short Term

Local Currency

Foreign Currency

Companies Abroad

Long Term

Local Currency

Foreign Currency

Companies Abroad

Cash & Equivalents

Local Currency

Companies Abroad

NET DEBT

6,378 100% 6,263 100%

2,230 35% 2,417 39%

187 3% 281 4%

1,540 24% 1,343 21%

504 8% 794 13%

4,148 65% 3,845 61%

714 11% 717 11%

1,243 19% 1,031 16%

2,191 34% 2,097 33%

1,151 100% 1,017 100%

421 37% 430 42%

730 63% 587 58%

5,228 5,246

DEZ. 03MAR. 04

HEDGE

Total Debt 100%

In US$ (Brazil) 44%

In R$ (Brazil) 14%

Companies Abroad 42%

In R$ million

Debt in US$ (Brazil) 2,783

Swap Operations 1,030

Cash & Equiv. In US$ 730

Total Hedge 1,760

Coverage 0,63X

COST OF DEBT

In % p.a.

In R$ (Brazil) 14.0%

In US$ (Brazil) + FX 5.4%

In Us$ (Abroad) 6.3%

19

FX rate US$ R$ 2.9086 R$ 2.8892

Investments2003

Gerdau AçominasUS$ 230 mm

South AmericaUS$ 7 mm

North AmericaUS$ 59 mm

NEW WIRE-ROD MILL

Installed capacity:

550 thousand tons/year

Total investment:

US$ 66 mm

TOTAL IN 2003: US$ 295 MMFORECAST FOR 2004: US$ 350

MM 20

Operational Integration Combination of strengths of both companies: greater competitiveness

Project developed in partnership between Gerdau and CEA (Employee Investment Club)

Headquarters in Ouro Branco - MG

Gerdau Açominas S.A.Gerdau S.A. Aço Minas Gerais S.A.Açominas

NEW CORPORATE GOVERNANCE

Met. Gerdau S.A.

Gerdau Açominas S.A.

Brazil NorthAmerica

SouthAmerica

Gerdau Ameristeel

Gerdau AZA

Gerdau Laisa

Sipar

Gerdau S.A.

21

Stronger demand in Brazil (domestic market);

Lower interest rates in Brazil expected for the end of the year;

Economic stability in Brazil and uncertainty in the political scenario;

International prices trend: stable to upwards;

North American operations pursuing better results;

US economy recovering;

South American operations in very good shape and improving.

Outlook

22

Steel Sector

Gerdau S.A. Consolidated

Stock Market

Shareholders Structure

Metalúrgica Gerdau S.A.

Other Gerdau Companies 25%

Brazilian Inst. Investors 24%

Foreign Inst. Investors

15%

Other Shareholders

36%

Gerdau S.A.

Met. Gerdau and otherGerdau companies

52%

Brazilian Inst.

Investors 10%

Foreign Inst. Investors

22%

Other Shareholders

16%

Gerdau Açominas S.A.

GerdauGroup

92%

CEA Clube / Fund. Aços 4%

Other Shareholders 4%

24

Adjusted Net Income Dividends paid

Payout of 30% of the Adjusted Net Income.

Dividend payments are being made on a quarterly basis since March 2003.

Dividend Policy

* Met. Gerdau paid a higher amount due to a one-time supplementary dividend payment in 2001. 25

1.080

33.0% 32.6% 52.5% 34.2% PAY OUT

YIELD6.0% 7.9% 17.0% 12.4 %

32.2% 32.8% 35.7% 34.7% 32.5%

3.6% 6.1% 6.8% 7.1 % 3.9%

31.5%

6.2 %

METALÚRGICA GERDAU S.A.In R$ million

234

123

163

54

174

57

413141

546

172

20001999 2001* 2002 2003

763

265

462

165381

125306

98

351

200120001999 2002 2003

GERDAU S.A.In R$ million

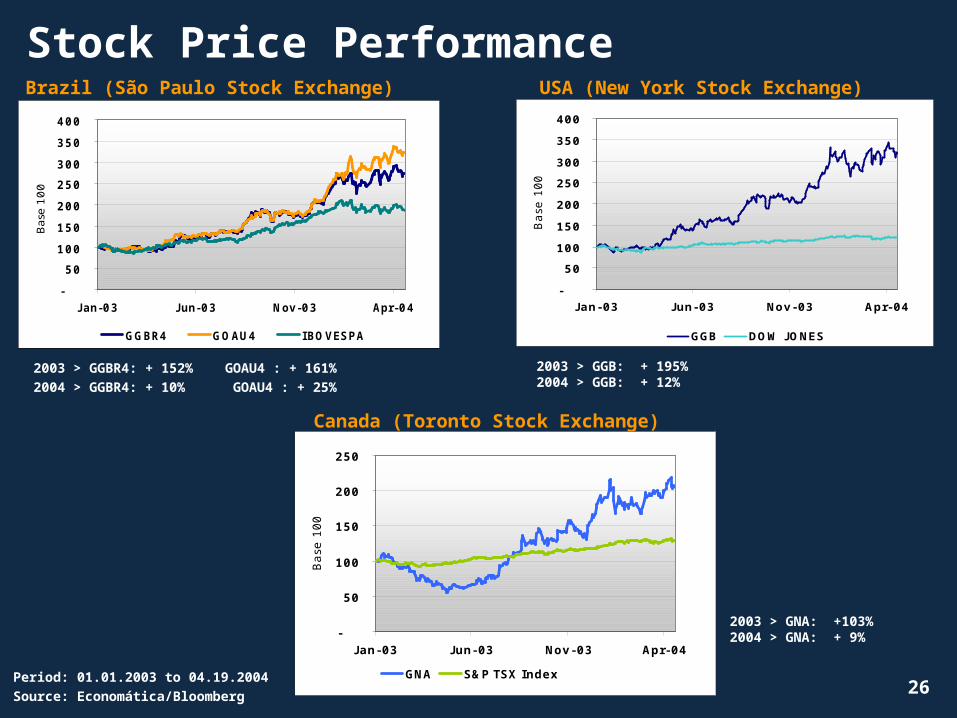

Stock Price Performance

Period: 01.01.2003 to 04.19.2004Source: Economática/Bloomberg

USA (New York Stock Exchange)

Canada (Toronto Stock Exchange)

26

2003 > GGBR4: + 152% GOAU4 : + 161%2004 > GGBR4: + 10% GOAU4 : + 25%

2003 > GGB: + 195%2004 > GGB: + 12%

2003 > GNA: +103%2004 > GNA: + 9%

-

50

100

150

200

250

300

350

400

J an-03 J un-03 Nov-03 Apr-04

Bas

e 1

00

GGBR4 GOAU4 IBOVESPA

-

50

100

150

200

250

300

350

400

Jan-03 Jun-03 Nov-03 Apr-04

Base

100

GGB DOW JONES

-

50

100

150

200

250

Jan-03 Jun-03 Nov-03 Apr-04

Base

100

GNA S&P TSX Index

Brazil (São Paulo Stock Exchange)

1 year 3 years 5 years

Appreciation ChartIn US$

Source: EconomáticaBase: 04.19.2004Dividend-adjusted

USA (NYSE)

GGB+171%

GGB+246%

GGB+304%

DOW+25% DOW

-2.4%DOW0%

1 year 3 years 5 years

BRAZIL (Bovespa)

GGBR4+180%

GGBR4+468%

GGBR4+319%GOAU4

+199%

GOAU+720%

GOAU4+458%

IBOV+82%

IBOV+11%IBOV

13%

Gerdau S.A.

Metalúrgica Gerdau S.A.

Ibovespa

Gerdau - ADR

Dow Jones

27

Comparative ChartGERDAU BELGO CSN USIMINAS NUCOR

STEEL DYNAMICS

TICKER SYMBOL GGBR BELG CSN USIM NUE STLD

Market Capitalization04.19.2004 (US$ mm)

3,367 1,834 4,267 2,581 5,088 1,307

Enterprise Value - EV (US$ mm)

5,183 1,971 5,966 4,920 5,642 1,849

EBITDA annualized(US$ mm)

929 402 1,039 1,063 469 113

EV/ EBITDA annual.(X)

5.6 4.9 5.7 4.6 12.0 16.4

Price04.19.2004 (US$)

22.68 261.16 59.45 11.99 65.09 27.49

Net Income(US$ mm)

434 271 357 452 63 47

P/ E - Price/ Earningsper share (X)

7.7 6.8 11.9 6.0 81.0 27.8

Market Cap/ EBITDA annual.(X)

3.6 4.6 4.1 2.4 10.8 11.6

Source: Economática and company websites28