second bounce of the ball - what's going on in tech?

TRANSCRIPT

Industrial Revolution 2.0 3.0 4.0& The Next Bounce of the Ball

YC NgPartner @ Potential VC

Agenda

What’s going on in the tech market - a VC perspective

What industries are being disrupted?

How does it affect Deloitte?

YC Ng Partner @ Potential.vc

Previously: Barclays, Debt Syndicate Startup stuff: Scarlett of Soho (acquired) Investor/Advisor @ hackajob, Inkpact, CaseHub, Papier, Mindmate, leaf.fm, Rentecarlo Mentor @ Techstars, Ignite, Entrepreneur First, Accelerate Cambridge

In God we trust, all others must bring data.

With more money (and new non-VC entrants), venture financings have been on the rise - 2015 was an enormous year

0

25

50

75

100

0

2,500

5,000

7,500

10,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

# OF ROUNDS CLOSED CAPITAL INVESTED ($BN)

Source: Pitchbook 2015 Annual US Venture Industry Report; Upfront VC

Pre-recession levels of LP contributions to the VC industry - 2016 seems likely to keep growing

US FINANCING ACTIVITY

0

15

30

45

60

0

75

150

225

300

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: DowJones Venture Source; Upfront VC

The opportunity cost to “play” has fallen

# OF VC/GROWTH FUNDS RAISED BY SIZE (M) (2013 - Q42014)

0

25

50

75

100

$1 - $50 $101 - $150 $201 - $250 $301 - $350 $401 - $450 $501+

2013 FUNDS RAISED 2014 FUNDS RAISED

Source: CBInsights

Source: Source: Pitchbook 2015 Annual US Venture Industry Report; Upfront VC

Dollars into later-stage deals have been largely driven by non-traditional VCs (up 50% in the last 3 yrs)

NON-VC PARTICIPATION IN $20M-PLUS ROUNDS

0%

15%

30%

45%

60%

2012 2013 2014 2015

55%47%47%

37%

Source: Pitchbook 2015 Annual US Venture Industry Report; Upfront VC

Corporate VC is the new “cool thing”

QUARTERLY CORPORATE VC PARTICIPATION Q3’12 - Q4’14

0

25

50

75

100

Q3'12 Q4'12 Q1'13 Q2'13 Q3'13 Q4'13 Q1'14 Q2'14 Q3'14 Q4'14

969392

83

73

666668

6064

Source: CBInsights

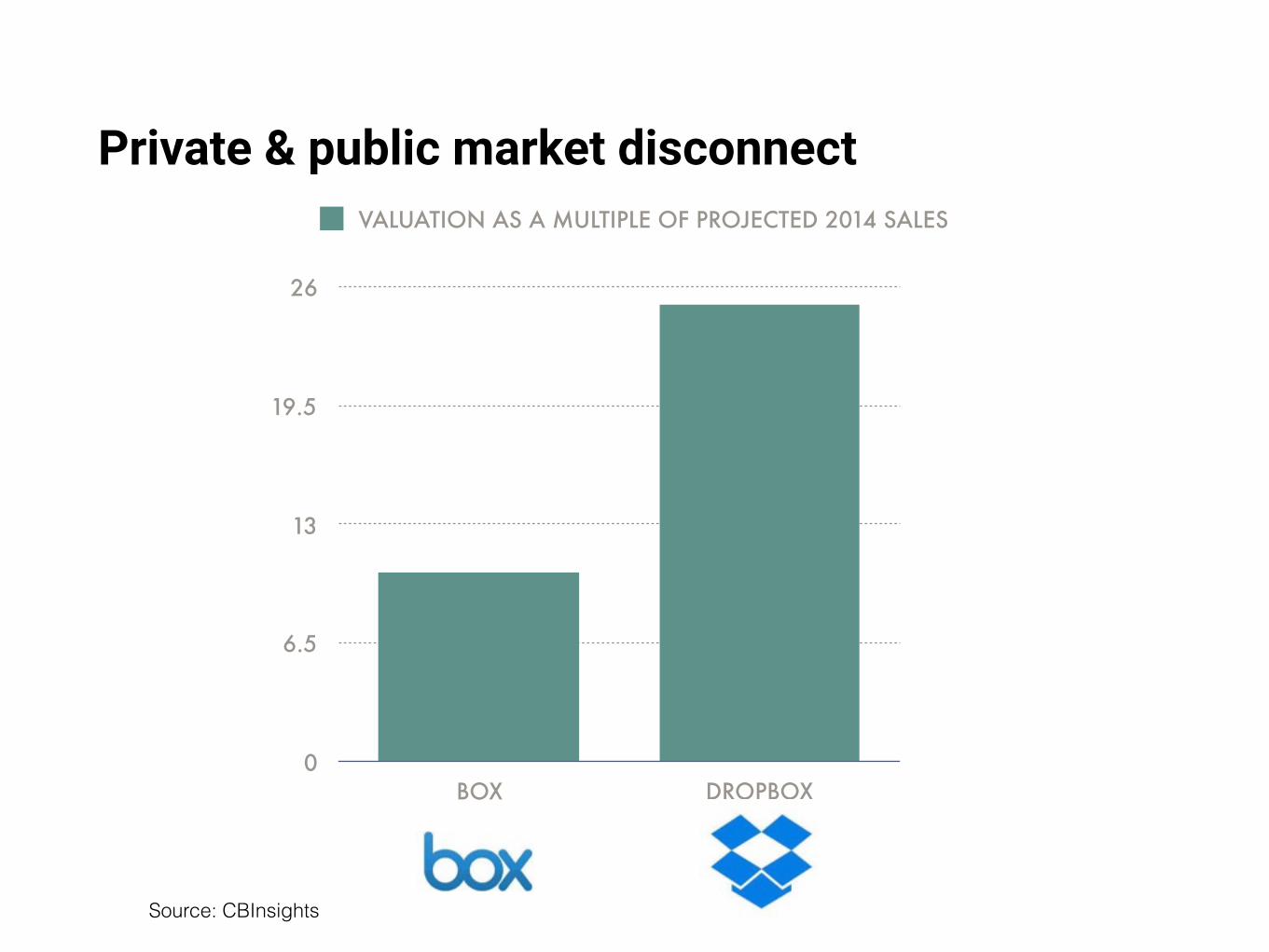

Private & public market disconnect

0

6.5

13

19.5

26

BOX DROPBOX

VALUATION AS A MULTIPLE OF PROJECTED 2014 SALES

Source: CBInsights

A very visible re-calibration of valuations of pre-IPO mutual fund cohort at places like Fidelity

FIDELITY’S HOLDINGS: % PRICE CHANGES SINCE PURCHASE

BLUE BOTTLE

MONGODB SERIES F

TABOOLA SERIES E

TURN INC.

ZENEFITS SERIES C

DATAMINR SERIES D

DROPBOX SERIES C

SNAPCHAT SERIES F

-70% -52.5% -35% -17.5% 0%

-15%

-29%

-35%

-44%

-45%

-47%

-54%

-61%

% CHANGE

Source: Upfront VC

More than 90% of respondents in the Upfront VC Survey expected valuations to go down in 2016 with a full 1/3 of investors expecting significant price corrections

INCREASE

ABOUT THE SAME

MARGINALLY DOWN

SIGNIFICANTLY DOWN

0% 17.5% 35% 52.5% 70%

30%

61%

8%

1%

5%

61%

28%

6%

Q4'15 1H'16 (EST)Source: Upfront VC

More than 90% of respondents in the Upfront VC Survey expected valuations to go down in 2016 with a full 1/3 of investors expecting significant price corrections

INCREASE

ABOUT THE SAME

MARGINALLY DOWN

SIGNIFICANTLY DOWN

0% 17.5% 35% 52.5% 70%

30%

61%

8%

1%

5%

61%

28%

6%

Q4'15 1H'16 (EST)Source: Upfront VC

But a full 82% of LPs are likely to maintain their existing investment pace

HOW WOULD YOU DESCRIBE YOUR LIKELY INVESTMENT PACE IN VENTURE

OVER THE NEXT 3 YEARS?

10%

82%

8%

WE'RE LIKELY TO INCREASE OUR INVESTMENT PACEWE'RE LIKELY TO KEEP THE SAME INVESTMENT PACEWE'RE LIKELY TO SLOW DOWN OUR INVESTMENT PACE

Source: Upfront VC

Areas being disrupted

How does this affect

Changing loyalties

Defensive Strategy• Helping the current FTSE companies respond to

threats & disruption

Proactive Strategy• Identifying and helping the next-generation of FTSE

companies

What role should you play?

3.5%“Unicorns” as a % of Nasdaq total market cap