secretary brown's presentation

TRANSCRIPT

Virginia’s Budget Process, Fiscal Trends,

and Future Issues

Richard D. BrownSecretary of FinanceApril 10, 2010

2

Virginia’s Budget Process

Overview of Virginia’s Budget Process

Composition of Budget: Resources, Spending, and Budget Drivers

The Budget Shortfall and 2010 General Assembly Actions

Issues Affecting the Future – Looking Ahead

3

Overview of Virginia’s Budget

4

The Code of Virginia calls for the development of two budget documents: Executive Budget Document Budget Bill

Statute requires submission of these documents to the General Assembly by December 20

Both documents have operating and capital sections

The Budget Bill also specifically covers: Transfers General Provisions – These are conditions and

stipulations governing appropriations

Legal Requirements for the Virginia Budget

5

Each agency must have an appropriation from the General Assembly to spend money from the state treasury (State Constitution)

Individual agency heads may be held personally liable for (deficit) spending in excess of their appropriation (Appropriation Act)

The Governor must take all steps to see that spending is within revenue collections during the course of the biennium (two-year) budgetary period (State Constitution and Appropriation Act)

Legal Requirements for the Virginia Budget

6

Unique Features of the Virginia Budget

Two-year budget Year-by-year operating appropriations Movement between years

Deficits not allowed Governor’s responsibility in execution Personal liability of officials

Planning and evaluation Strategic planning initiatives Six-year capital outlay plan Consensus revenue forecasting Debt capacity model

7

Governor’s Role

As the chief planning and budget officer, the Governor prepares the biennial budget and executes it once the legislature completes its actions.

The Governor’s proposed budget bill is presented to a Joint Session of the House Appropriations and Senate Finance Committees in mid-December.

Governor gets the first “bite-at-the-apple” when allocating projected revenues. Also must propose reductions when deficits are projected.

8

Executive Agencies Involved in Budget Process

Department of Planning and Budget (DPB) analyzes agency budget requests and recommends resource needs.

Assist in developing funding strategies consistent with agency strategy plans and administration priorities.

Executes budget approved by the General Assembly.

Department of Taxation produces the revenue forecast on which the appropriations are based.

Department of Treasury develops and maintains the debt capacity model used to guide the use of debt for maintenance and construction projects.

Department of Accounts (State Comptroller) monitors spending against appropriation allotments.

9

Executive Branch Budget Development Late summer and fall, DPB issues instructions to

agencies regarding process and requirements. Secretaries meet with agencies to discuss budget

issues.

In the fall agencies generate and submit budget requests through their Secretary to DPB.

Revenue forecast is developed through fall. Governor meets with Finance and budget staff to

review requests and prioritize. Based on revenue forecast, requests are

recommended for funding. Budget is submitted to General Assembly by

December 20th each year.

Many Factors and Perspectives Influence Executive Budget Development

Agencies usually have requests that exceed available resources

• Changes in regulations and laws• Automation• Increase in number of clients• Demand for services• Increases/decreases in federal funds• Traditional practices• Public sentiment• Priorities of the Governor and General Assembly The Governor must view budget as zero-sum game

and balance competing demands• Increases/decreases in available revenues• Efficiency, effectiveness and economy• Continuing need for programs and agencies• Reconcile agency requests with Governor’s priorities

11

Governor’s Campaign Promises and Budget Issues

Robb - K-12 funding/teacher salaries

Baliles - Transportation

Wilder - Fiscal Crisis

Allen - Parole Abolition and Economic Development

Gilmore - Eliminating the Car Tax

Warner - Fiscal Crisis and Tax Reform

Kaine – Preschool, Virginia Tech, and Fiscal Crisis

McDonnell – Economic Development/Job Creation and Government Reform

Governors’ initiatives are generally tied to campaign promises, the state’s economic conditions, or unforeseen events.

12

General Assembly’s Role

Like the Governor, one of the primary responsibilities of the General Assembly is to craft a budget.

The House and Senate budgets are actually amendments to the Governor’s introduced budget.

The General Assembly adds, modifies, endorses or deletes items in the Governor’s proposed budget.

The General Assembly also increases or decreases proposed funding levels.

In even-numbered years, the General Assembly enacts a two-year or biennial budget. In odd years, the House and Senate tend to address unexpected increases or decreases.

13

Legislative Budget Process

The House Appropriations, House Finance and Senate Finance Committees comprise the General Assembly’s “money committees”

Through legislation and the budget process, these committees establish the Commonwealth’s fiscal policies

House of Delegates: Duties are split between the Finance Committee (tax policy) and the Appropriations Committee (spending decisions)

Senate: Duties are combined under the Finance Committee

14

House Appropriations and Senate Finance Committees

The House Appropriations and Senate Finance Committees have full-time legislative staff assigned to them.

These non-partisan staff provide the Committees:

Independent sources of information;

Professional expertise in various budget disciplines;

Recommendations on emerging funding issues; and

Guidance on spending and revenue trends.

15

Legislative Budget ProcessBudget Deliberation

House Appropriations and Senate Finance Committees begin budget deliberations in October and November

o Hold Committee “retreats” to examine fiscal outlook and issues driving budget decisions

After receiving Governor’s introduced budget, Committees hold 4-5 regional public hearings on budget in early January

Budget amendment requests by General Assembly members made to Committees usually by second full week of Session

Subcommittees review agency budgets and amendment requests.

Committees act on Subcommittee Reports

Committees send budget bill with amendments to the House and Senate Floors for adoption

16

Legislative Budget ProcessFinalizing the Budget Once each House adopts its version of the budget,

bills are sent to opposite house Committee of conference is appointed

Provides opportunities to correct mistakes and get additional input

Budget conferees resolve differences between House and Senate budgets

Conference committee report is sent back to House and Senate floors for final approval – up or down vote

Adopted budget sent to Governor for signature Governor’s amendments or vetoes considered during

Reconvened (Veto) Session

17

Virginia’s Budget ProcessTimeline of Important Dates

NovemberGovernor, DPB,Cabinet review

Develop revenue forecast

SeptemberAgencies

generate &submit requests

AugustDPB issues

instructions toagencies

DecemberGovernor submits

document &bill to GA

AprilGovernor signs/vetoes/

or returns items toGA with amendments

MarchConference Committeereports budget bill(s)/GA approves budget

FebruarySenate & Houseproduce separatebudget proposals

JanuaryBudget billsreferred to

money committees

Budget Development

Agency Budget Preparation Review & Recommendation

Budget Deliberation

Legislative Action Gov’s Review

18

State agencies

Legislative commissions

Legislators

Interest groups

Other studies/ events

Governor (Introduced

budget)

Conference Committee

(Final agreement)

House

Senate

Virginia’s Budget ProcessWhen and How to Influence the Process?

January

Testify at public hearings

on budget

Budget Development

Budget Deliberation

January - February

Attend committee hearings/request

budget amendments

Budget Decisions

April - December

Discuss issues and concerns/develop and communicate message

February - March

Make phone calls, send letters, and schedule

visits

Budget Demands

19

Conclusion: Budget Process

• Virginia’s budget process begins in the fall not in January

• Introduced budget is the starting point for discussion

• Based on its priorities, General Assembly makes any changes to the introduced budget in January and February (incremental process)

• Mandatory spending and short sessions tend to confine budgetary changes to the margin

20

Composition of Budget:Resources, Spending

& Budget Drivers

21

2008-2010 Budget:General Fund vs. Nongeneral Fund

Data from 2009 Appropriation Act (Chapter 780 )

General Fund

41.2%

Nongeneral Fund

58.8%

22

General Fund Revenues for 2008-2010

Economic trends are important because employment, wage gains, and consumer spending account for about 91 percent of all general fund revenues.

2008-2010 general fund revenues = $29.9 billion

Data does not include transfers or balances. Data from 2009 Appropriation Act

Individual income tax66.0%

Other taxes & revenue8.8%

Corporate income tax4.7%

Sales & use taxes20.5%

23

Nongeneral Fund Revenues for 2008-2010

Federal grants account for almost 40% of all nongeneral funds revenue

“Transportation” includes fuel tax, sales tax, motor vehicle sales tax, and motor vehicle licenses.Data does not include balances or bond proceeds. Data from Chapter 780, 2009 Appropriation Act.

2008-2010 nongeneral fund revenues = $41.4 billion

Transportation 10.3%Institutional revenue from higher education

tuition & fees and hospitals 21.7%

Other revenue 29.4%Federal grants

& contracts 38.6%

24

Where the Money Goes 2008-2010 (All Funds) = $74.9 Billion

Commerce and Trade2.7%

General Government

7.2%

Health and Human

Resources27.7%

Public Safety7.0%

Transporation12.1%

Other4.0%

Education39.4%

79.2% of the budget (all funds) goes to education, health and human resources, and transportation

“Other” includes legislative and judicial branches, technology, natural resources, independent agencies, and non-state agencies.

Source: Department of Planning and Budget April 2009. Data from 2009 Appropriation Act (Chapter 780) (operating only).

25

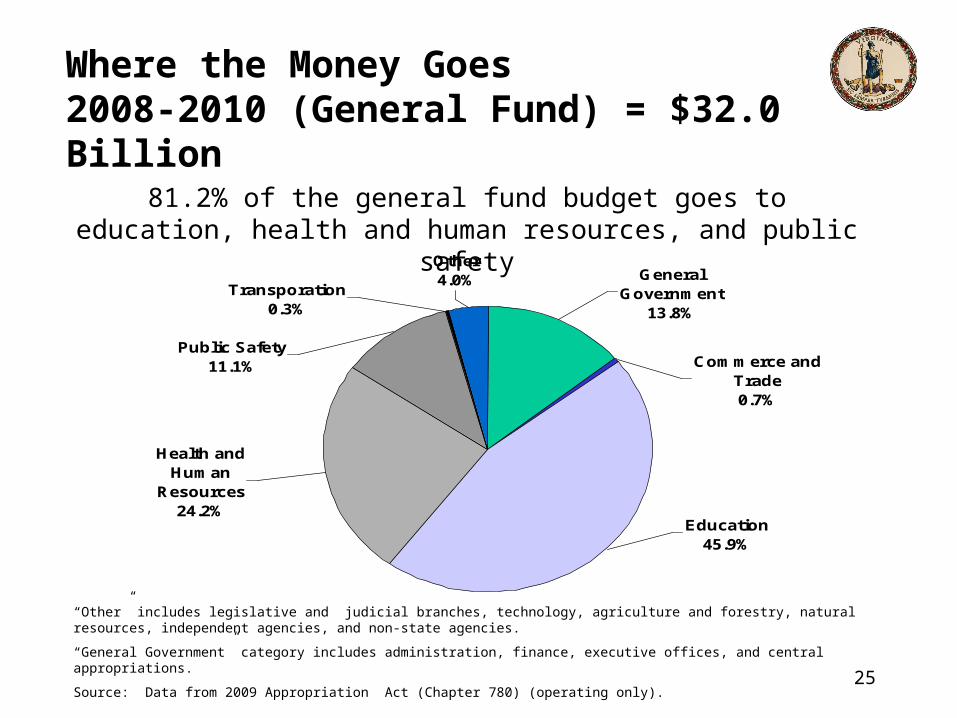

Where the Money Goes 2008-2010 (General Fund) = $32.0 Billion

Education45.9%

Other4.0%

Transporation0.3%

Public Safety11.1%

Health and Human

Resources24.2%

General Government

13.8%

Commerce and Trade0.7%

81.2% of the general fund budget goes to education, health and human resources, and public safety

“Other” includes legislative and judicial branches, technology, agriculture and forestry, natural resources, independent agencies, and non-state agencies.

“General Government” category includes administration, finance, executive offices, and central appropriations.

Source: Data from 2009 Appropriation Act (Chapter 780) (operating only).

26

Almost Half of the General FundOperating Budget Goes to Localities

Local Sheriffs$955.96.1%

Other Aid to Localities$1,964.312.5%

Car Tax$1,900.012.7%

Public Education$10,949.3

69.4%

State Programs$8,907.927.2%

Debt Service$957.32.9%

Aid to individuals$7,125.021.7%

Aid to Localities$15,769.6

48.1%

*Total GF Operating $32,759.7 million; HB1600 Introduced.

27

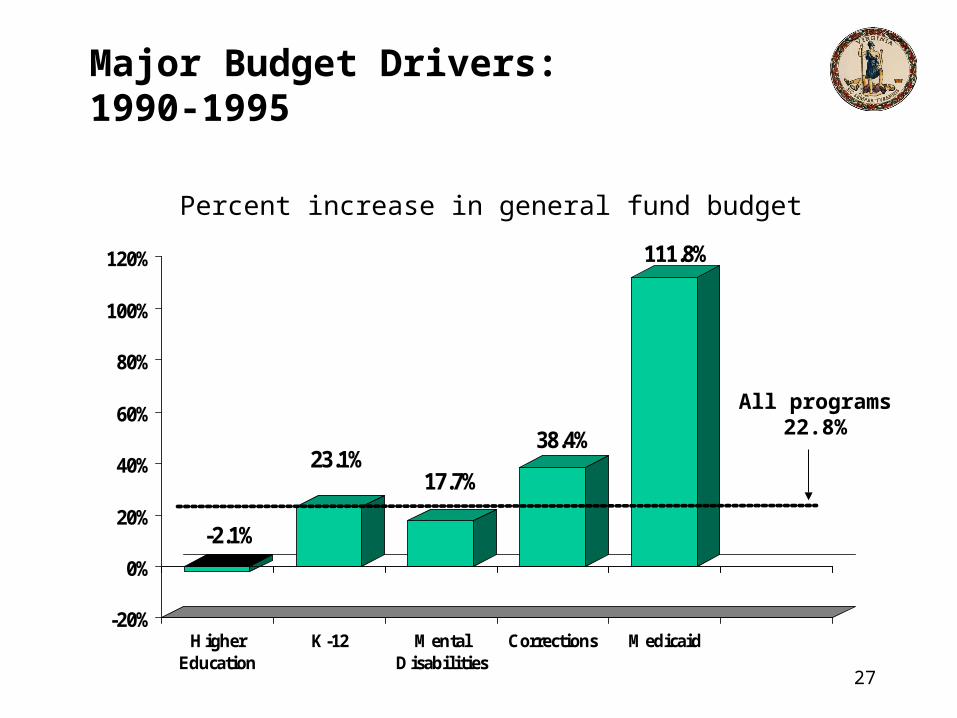

Major Budget Drivers: 1990-1995

-2.1%

23.1%17.7%

38.4%

111.8%

-20%

0%

20%

40%

60%

80%

100%

120%

HigherEducation

K-12 MentalDisabilities

Corrections Medicaid

All programs 22.8%

Percent increase in general fund budget

28

Major Budget Drivers: 1995-2000

54.9%

40.7% 40.1% 40.2%

27.7%

0%

10%

20%

30%

40%

50%

60%

HigherEducation

K-12 MentalDisabilities

Corrections Medicaid

All programs 50.8%

Percent increase in general fund budget

29

Major Budget Drivers: 2000-2005

-1.6%

28.7% 28.3%

20.1%

37.5%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

HigherEducation

K-12 MentalDisabilities

Corrections Medicaid

All programs 24.2%

Percent increase in general fund budget

30

Major Budget Drivers: 2005 - 2010

14.1%

38.4%

6.5%11.1%

22.1%

0%

5%

10%

15%

20%

25%

30%

35%

40%

HigherEducation

K-12 MentalDisabilities

Corrections Medicaid

All programs 15.0%

Percent increase in general fund budget

* For purposes of this slide, the FY 2010 appropriation base is CH 781, 2009 Acts of the Assembly.

31

Major Budget Drivers: 2010 - 2012

-14.0%

-2.1%

-29.5%-5.8%

64.3%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

HigherEducation

K-12 MentalDisabilities

Corrections Medicaid

All programs (1.4%)

Percent increase in general fund budget

* For purposes of this slide, the FY 2010 appropriation base is CH 781, 2009 Acts of the Assembly. The FY 2012 appropriation base is from HB/SB 30 as introduced.

32

Major Budget Drivers: 2005 - 2012

3.7%11.7%

-17.2%

14.0%

111.8%

129.9%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

HigherEducation

K-12 MentalDisabilities

Corrections Medicaid All Other

All programs 13.3%

Percent increase in general fund budget

33

Budget DriversFY 1985

K-12 $1,355,514,703

36.1%

All Other $1,078,603,451

28.7%

Medicaid $202,916,420

5.4%

Corrections $276,877,715

7.4%

HiED $627,012,547

16.7%Mental Disabilities $212,605,320

5.7%

Per CH 221

34

HiED $1,462,058,381

9.4%

K-12 $5,270,628,823

33.8%

All Other $3,676,731,092

23.5%

Medicaid $3,333,818,121

21.3%

Corrections $1,236,383,992

7.9%

Mental Disabilities $636,432,558

4.1%

Budget DriversFY 2012

Per HB 30 as introduced

35

Medicaid Enrollment & Expenditures, FY 2008

Children

Children

Adults

Adults

Blind & Disabled

Blind & Disabled

AgedAged

Recipients Expenditures

9%

20%

16%

55%

20%

47%

10%

23%

Budget Driver: Medicaid

Department of Planning and Budget, 2008.

36

The Budget Shortfalland

2010 General Assembly Actions

37

Total General Fund Revenue Collections Collapsed in the Second Half of Fiscal Year 2009

• Collections declined an unprecedented eleven consecutive months in fiscal year 2009.

• For the second half of fiscal year 2009:– Payroll withholding tax collections fell 1.0 percent;– Individual nonwithholding declined 24.8 percent;– Individual refunds increased 17.0 percent;– Sales tax collections declined 5.9 percent;– Corporate income tax receipts fell 19.0 percent, and;– Recordation taxes declined 16.8 percent.

Growth in Total General Fund Revenue CollectionsFY09 Monthly and Year-to-Date

2.9%

-4.2%-3.5% -3.7% -3.5%

-5.5%-6.8%

-8.6%-9.3% -9.2%

-6.1%

-1.9%

-24%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Monthly Year-to-Date

Forecast: -7.3%

Monthly Growth: 2.9% -6.6% -7.4% -1.0% -4.6% -2.6% -15.0% -13.6% -13.9% -19.7% -15.6% -8.0%

38

Fiscal Year 2009 Revenue and Transfer Collections Finished $299.2 Million - (2.0 Percent) Below Forecast

• The major driver of the fiscal year 2009 revenue shortfall was unexpected growth in individual refunds.

– Compared to fiscal year 2008, TAX issued 28.8 percent more refunds between April and June, with June’s total 110.2 percent above the prior year.

• Withholding and sales tax collections (83 percent of total revenues) finished a combined 0.6 percent below forecast.

• The three most volatile sources – individual nonwithholding, corporate income tax, and wills – finished 1.8 percent below the official forecast for the three sources.

Summary of Fiscal Year 2009 Revenue Collections(millions of dollars)

Major Source

Withholding $ 9,154.0 $ 9,138.1 $ (15.9) (0.2) % 2.3 %Nonwithholding 2,348.3 2,310.4 (37.9) (1.6) (19.2)Refunds (1,805.0) (1,967.4) (162.4) 9.0 17.1 Net Individual 9,697.3 9,481.1 (216.2) (2.2) (6.3)

Sales 2,960.9 2,903.4 (57.5) (1.9) (5.6)Corporate 685.0 648.0 (37.0) (5.4) (19.8)Wills (Recordation) 298.1 314.3 16.2 5.4 (31.1)Insurance 257.5 255.0 (2.5) (1.0) (35.7)All Other Revenue 715.1 713.2 (1.9) (0.3) (22.1)

Total Revenues $ 14,613.9 $ 14,315.1 $ (298.8) (2.0) % (9.2) %

ABC Profits 36.6 44.1 7.5 20.5 22.2Sales Tax (0.25%) 222.1 213.4 (8.7) (3.9) (5.8)Transfers 148.2 149.0 0.8 0.5 62.7

Total Transfers $ 406.9 $ 406.5 $ (0.4) (0.1) % (50.0) %

Total General Fund $ 15,020.8 $ 14,721.6 $ (299.2) (2.0) % (11.2) %

VarianceForecast Actual Dollars Percent Growth

Annual

39

The Governor Ordered the Secretary of Finance in Mid-June to Conduct a Reforecast of Revenues

• As part of the reestimation process, the Governor’s Advisory Board of Economists (GABE) met July 14th to discuss the economic outlook for fiscal year 2010 and the next biennium.– Recommendations from the Board, primarily downward adjustments to

employment and income growth over the next three fiscal years, were incorporated into the Global Insight June 2009 standard economic outlook.

• The June 2009 GABE economic forecast and associated revenue forecast were presented to the Governor’s Advisory Council on Revenue Estimates (GACRE) on August 5th.– The GACRE was more pessimistic than the baseline scenario. As a result,

the interim revenue forecast relied on a blend of the standard and pessimistic outlooks.

• However, over 80% of general fund revenues (withholding, sales, and corporate income tax) were based on the pessimistic alternative scenario.

• Governor Kaine released the interim revenue forecast on August 19, 2009, reducing revenues by $1.2 billion for fiscal year 2010.

40

Global Insight’s October Forecast for the National Economy Says – “Growth Is Back – Jobs Are Not”

• Global Insight expects a prolonged U-shaped recovery.

• Lackluster consumer demand prevents a V-shaped recovery.

• Employment is expected to bottom out in the first half of calendar year 2010.

Key U.S. Economic Indicators Interim and October Forecasts

Annual Percent Change

08 09 10 11 12Real GDP

Interim (Jun '09) 2.4 (1.7) (3.0) 1.0 2.9Oct Standard 2.2 (2.2) 0.4 2.3 3.5Oct Pessimistic (0.7) 0.3 2.6

Consumer SpendingInterim (Jun '09) 1.9 (1.3) (0.7) 0.8 0.5Oct Standard 1.5 (1.4) 0.7 2.2 2.4Oct Pessimistic 0.2 0.5 0.7

EmploymentInterim (Jun '09) 0.6 (2.3) (3.5) (0.6) 1.6Oct Standard (2.3) (2.9) 1.0 2.3Oct Pessimistic (3.3) (0.3) 1.5

Personal IncomeInterim (Jun '09) 5.3 1.6 (0.9) 1.3 4.4Oct Standard 4.5 (0.1) (0.2) 3.8 4.6Oct Pessimistic (0.8) 2.0 4.0

Fiscal Year

41

In the October Standard Economic Outlook for Virginia, the Economy Begins Recovery Earlier and Grows A Bit Faster Than in the Interim Forecast

• The U-shaped growth path for Virginia is slightly deeper with a mildly stronger recovery.

• Revenue model drivers – employment and income – are similar to interim estimates for FY 2010.

Key Virginia Economic Indicators Interim and October Forecasts

Annual Percent Change

08 09 10 11 12Employment

Interim (Jun '09) 0.6 (1.4) (2.1) (0.4) 0.9Oct Standard 0.5 (1.3) (2.3) 1.1 2.1Oct Pessimistic (2.6) (0.0) 1.2

Personal IncomeInterim (Jun '09) 4.5 2.6 0.5 1.4 4.0Oct Standard 4.5 1.1 1.6 3.0 3.7Oct Pessimistic 1.3 2.0 3.4

Wages & SalariesInterim (Jun '09) 4.4 2.8 1.0 1.5 3.4Oct Standard 3.9 0.7 0.4 3.0 3.7Oct Pessimistic 0.1 2.0 2.9

Average WageInterim (Jun '09) 3.8 4.3 3.2 1.9 2.5Oct Standard 3.4 2.0 2.7 1.9 1.6Oct Pessimistic 2.8 2.0 1.6

Fiscal Year

42

Pending Home Sales

Seasonally-adjusted 2-quarter moving average

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

99q1 99q3 00q1 00q3 01q1 01q3 02q1 02q3 03q1 03q3 04q1 04q3 05q1 05q3 06q1 06q3 07q1 07q3 08q1 08q3 09q1 09q3

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Northern Virginia Hampton Roads Richmond38% 21% 11%

Northern Virginia

Hampton Roads

Richmond

(% share of total home sales in Virginia)

Average Sale Price2008 Q4 2009 Q4 % Growth

Northern Virginia $340,757 $381,908 12%Hampton Roads 258,227 240,680 -7%Richmond 251,586 230,064 -9%

43

Payroll Withholding andEmployment Growth

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 'Jan-01 'Jan-02 'Jan-03 'Jan-04 'Jan-05 'Jan-06 'Jan-07 'Jan-08 'Jan-09 'Jan-10-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Withholding (L) Original Revised

3-month Moving Average

44

Sales Tax and Employment Growth

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

20.0

Jan-92 Jan-93 Jan-94 Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 'Jan-01 'Jan-02 'Jan-03 'Jan-04 'Jan-05 'Jan-06 'Jan-07 'Jan-08 'Jan-09 'Jan-10-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

Sales Tax (L) Original Revised

3-month Moving Average

45

Economists and Business Leaders Were Mixed on the Most Probable Path for the Economy and General Fund Revenues

• The Governor’s Advisory Board of Economists (GABE) met October 14th to review Global Insight’s standard and pessimistic alternative forecasts.– The members were about evenly split, with five choosing the Global

Insight standard, five choosing the pessimistic alternative scenario, and one choosing an economic path somewhere in between the two.

• The Governor’s Advisory Council on Revenue Estimates (GACRE) met November 23rd to review revenue projections based on the standard and pessimistic alternative forecasts.– The business leaders were split on the forecasts, with six supporting

the October standard forecast, three supporting the pessimistic alternative scenario, and four choosing “standard minus.”

– Members of the General Assembly who attended the meeting expressed pessimism; however, most supported projections from their respective staffs which were consistent with the standard forecast presented to the GACRE.

46

The December General Fund Revenue Forecast Reflects the Sentiment of the Advisory Boards

• The standard forecast presented to the GACRE included downward adjustments from the August interim forecast totaling $229.8 million for fiscal year 2010.– The reduction included downward revision to withholding and

increased projections for individual refunds, consistent with the revised economic forecast and year-to-date collections.

• Based on members’ comments and near-term pessimism, the outlook for fiscal year 2010 was reduced further to a level consistent with the pessimistic alternative forecast.– In addition to reductions to withholding and increased projections for

individual refunds, the December forecast includes a reduction in nonwithholding.

• The total general fund revenue reduction for fiscal year 2010 is $340.0 million.

• The outlook for the 2010-12 biennium is based on the standard economic outlook.

47

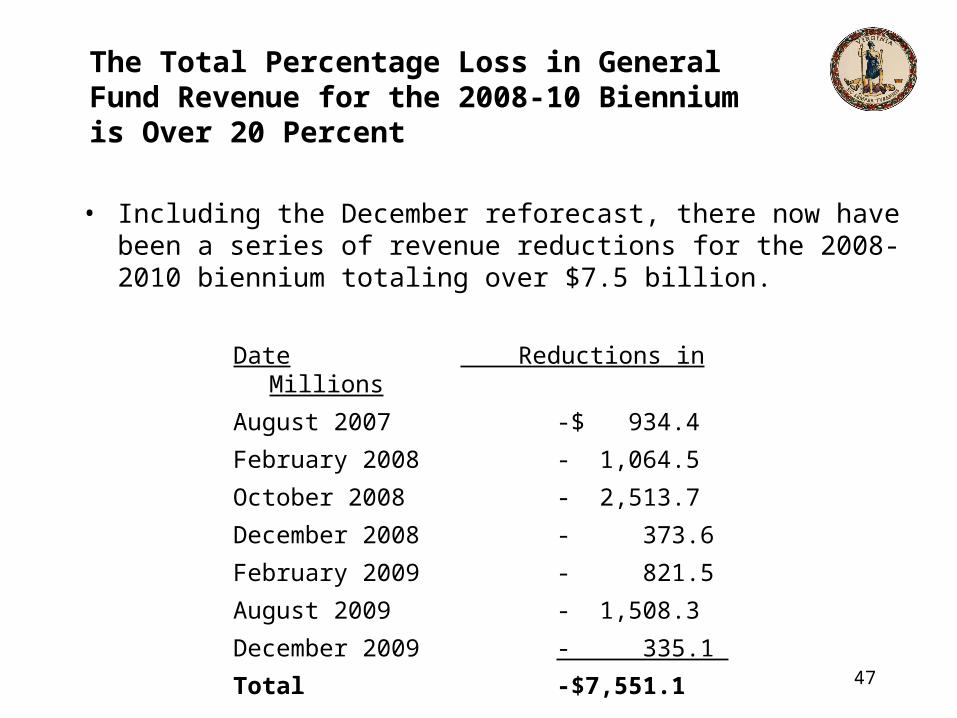

The Total Percentage Loss in General Fund Revenue for the 2008-10 Biennium is Over 20 Percent

• Including the December reforecast, there now have been a series of revenue reductions for the 2008-2010 biennium totaling over $7.5 billion.

Date Reductions in Millions

August 2007 -$ 934.4

February 2008 - 1,064.5

October 2008 - 2,513.7

December 2008 - 373.6

February 2009 - 821.5

August 2009 - 1,508.3

December 2009 - 335.1

Total -$7,551.1

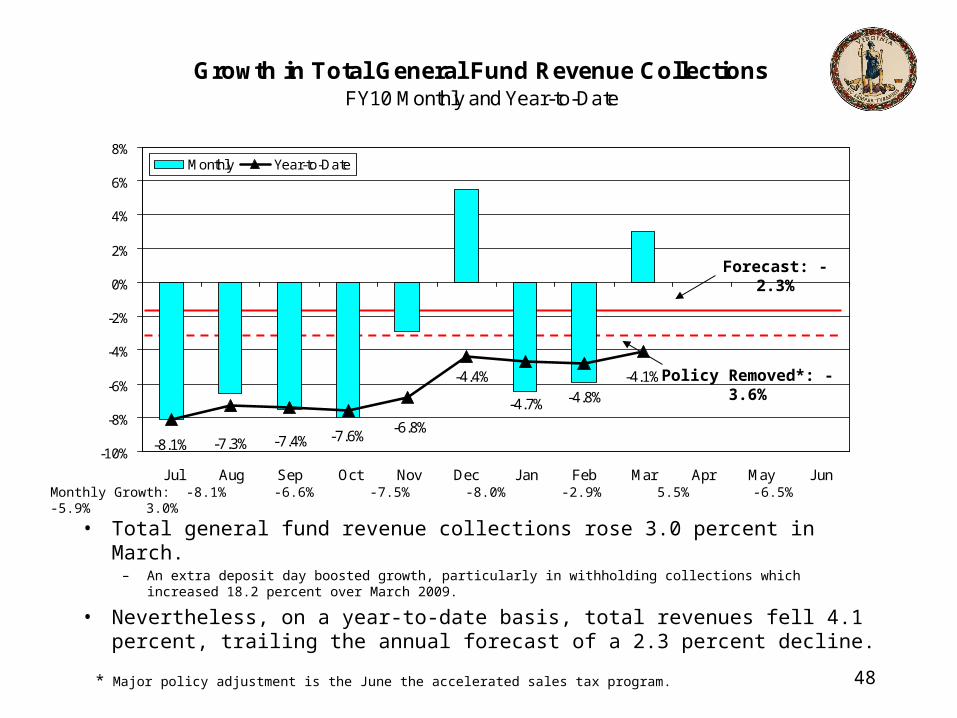

• Total general fund revenue collections rose 3.0 percent in March.

– An extra deposit day boosted growth, particularly in withholding collections which increased 18.2 percent over March 2009.

• Nevertheless, on a year-to-date basis, total revenues fell 4.1 percent, trailing the annual forecast of a 2.3 percent decline.

Growth in Total General Fund Revenue CollectionsFY10 Monthly and Year-to-Date

-8.1%-7.6%

-4.1%

-4.7%

-6.8%

-4.4%

-7.4%

-4.8%

-7.3%-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun

Monthly Year-to-Date

Forecast: -2.3%

Monthly Growth: -8.1% -6.6% -7.5% -8.0% -2.9% 5.5% -6.5% -5.9% 3.0%

Policy Removed*: -3.6%

* Major policy adjustment is the June the accelerated sales tax program. 48

49

Growth in Total General Fund Revenues

Fiscal Year 1961 - Fiscal Year 2012

(Nominal - Actual Dollars)

FY Total Revenues Growth FY Total Revenues Growth

61 230,998,887 - 87 4,590,434,000 11.1%

62 242,144,567 4.8% 88 5,054,382,000 10.1%

63 286,304,265 18.2% 89 5,478,912,000 8.4%

64 298,033,919 4.1% 90 5,494,884,000 0.3%

65 323,213,412 8.4% 91 5,471,879,000 -0.4%

66 365,129,776 13.0% 92 5,623,213,000 2.8%

67 414,755,644 13.6% 93 6,133,637,000 9.1%

68 533,597,744 28.7% 94 6,503,368,000 6.0%

69 706,254,374 32.4% 95 6,881,145,000 5.8%

70 743,721,322 5.3% 96 7,356,110,000 6.9%

71 807,954,651 8.6% 97 7,949,327,000 8.1%

72 922,653,686 14.2% 98 8,773,520,000 10.4%

73 1,054,469,443 14.3% 99 9,702,747,000 10.6%

74 1,168,562,871 10.8% 00 10,788,482,000 11.2%

75 1,303,178,893 11.5% 01 11,105,275,000 2.9%

76 1,428,421,157 9.6% 02 10,678,954,000 -3.8%

77 1,636,301,819 14.6% 03 10,867,149,000 1.8%

78 1,923,085,084 17.5% 04 11,917,867,000 9.7%

79 2,115,211,522 10.0% 05 13,687,252,000 14.8%

80 2,344,928,934 10.9% 06 14,834,298,000 8.4%

81 2,579,663,941 10.0% 07 15,565,827,000 4.9%

82 2,796,458,741 8.4% 08 15,766,951,000 1.3%

83 2,975,687,935 6.4% 09 14,315,060,000 -9.2%

84 3,397,710,261 14.2% 10* 13,987,600,000 -2.3%

85 3,790,816,000 11.6% 11* 14,582,300,000 4.3%

86 4,131,778,000 9.0% 12* 15,313,300,000 5.0%

* March 14, 2010 Post-GA Forecast (Excludes Transfers)

50

• When new spending requirements are added, the total general fund shortfall increases to $1.8 billion in FY 2010 and to $4.5 billion in the 2010-2012 biennium

*Amounts shown in millions

FY 2010 FY 2011 FY 2012GF Resource base per CH 781 15,755.4$ 15,755.4$ 15,755.4$ Adjust - August Interim Forecast (1,209.1) (809.4) (30.7) Adjust - December Forecast (335.1) (278.6) (308.1) Available GF Resources 14,211.2 14,667.4 15,416.6

Less:Spending Base per CH 781 (15,844.0) (15,845.4) (15,845.4) New Spending - Operating (154.9) (989.2) (1,850.2) New Spending - Capital - (39.2) - GF Spending Requirements (15,998.9) (16,873.8) (17,695.6)

Net Shortfall (1,787.7)$ (2,206.4)$ (2,279.0)$

Budget Shortfall 2010-2012 Biennium

51

Medicaid and Public Education Continue to Dominate the Majority of New GF Spending Requirements in the 2010-2012 Biennium

*Amounts shown in millions

Description of Action

Backfill Medicaid program due to loss of federal stimulus matching funds $ 1,191.49

Fund Medicaid utilization and inflation 777.7

Fund debt service requirements 165.7

Rebenchmark Standards of Quality (SOQ) costs (includes enrollment update) 143.8

Eliminate aid to locality reductions 100.0

Adjust support for Virginia Retirement System payments 89.5

Provide funding for the state employee health insurance program 84.6 Reserve funding for an anticipated mandatory deposit to the Revenue Stabilization Fund in FY 2013 40.0

Delay the update of the composite index for direct aid programs until FY 2012 39.0

Adjust funding for the Health Care Fund 32.6 Provide additional funding for state mental health and mental retardation facility Medicaid costs 31.9

Fund medical assistance services for low-income children utilization and inflation 26.6 2,723.0 94.6%

Other General Fund Spending 151.3 5.3%

Base and technical spending 5.0 0.2%

Total of All General Fund Spending $ 2,879.3

Biennial Spending

52

• 83 Percent of the Additional GF Savings Actions Recommended in the 2010-2012 Biennium Appear in the Top Ten Strategies

*Amounts shown in millions

Description of Action

Eliminate reimbursements for personal property tax relief $ 1,900.0

Fund health care costs in Standards of Quality based on actual plan participation 269.2

Implement policy changes to the Standards of Quality model 174.2

Utilize State Fiscal Stabilization Funds for general fund supported programs in K-12 126.4

Reduce HB599 funding 88.4

Withhold inflation adjustments from hospital operating rates 76.0

Eliminate state support for retirement and life insurance premiums to constitutional offices 61.6

Require state employees to pay a portion of retirement contributions 55.7

Reduce income limits for optional 300 percent Supplemental Security Income eligibility group 53.3

Postpone mandated increase in annual Mental Retardation and Developmental Disability waiver slots 39.2 2,844.0 82.9%

All Other Reduction Strategies 587.6 17.1%

Total of Additional Savings Actions Since September $ 3,431.6

Biennial Savings

Introduced Budget Bill

Savings Items in Enrolled Budget Bill

53

Item DescriptionGeneral Fund

FY 2011 FY 2012 Total132 Misc. K-12 Savings - See Below for Breakout ($249,585,541) ($230,501,503) ($480,087,044)132 #19c K-12 VRS Rates - Note 1 ($188,992,393) ($156,822,961) ($345,815,354)

297 Medicaid Reductions ($60,475,451) ($163,362,724) ($223,838,175)473.10 #1c Aid to locality reversion clearing account ($60,000,000) ($60,000,000) ($120,000,000)

297 #5c Reduce GF Share of Medicare Part D "Clawback" Payment ($85,736,111) $0 ($85,736,111)469 #7c Eliminate Funding for Second Year Health Insurance Premiums $0 ($37,231,433) ($37,231,433)297 #13c Adjust Funding for Virginia Health Care Fund (Tobacco Taxes) ($9,000,000) ($9,000,000) ($18,000,000)C-84 #1c Maintenance Reserve ($15,000,000) $0 ($15,000,000)271 #1c Treasury Board OS Fee ($7,221,523) ($7,221,523) ($14,443,046)297 #7c FMAP-Indigent Care Funding at State Teaching Hospitals ($7,100,000) ($7,100,000) ($14,200,000)379 #4c Potential Correctional Facility Closure ($1,307,733) ($10,954,446) ($12,262,179)137 #2c Reduction to the Tuition Assistance Grant (TAG) Program ($5,000,000) ($5,000,000) ($10,000,000)351 #3c Reduce Funding for Agricultural Best Management Practices ($5,000,000) ($5,000,000) ($10,000,000)

473.10 #2c Higher Education Reversion Clearing Account $0 ($10,000,000) ($10,000,000)271 #2c Higher Education Equipment Trust Fund Debt $0 ($8,334,167) ($8,334,167)

SUBTOTAL - TOP 15 GENERAL FUND SAVINGS (87% of total savings) ($694,418,752) ($710,528,757) ($1,404,947,509)

ALL OTHER - GENERAL FUND SAVINGS ($99,470,986) ($112,770,114) ($212,241,100)

TOTAL - GENERAL FUND SAVINGS (Less Comp Board related net zero) ($793,889,738) ($823,298,871) ($1,617,188,609)

Note 1 Does not include $504M in NGF Revenues (State Employee Retirement and other VRS administered savings) over the biennium.

K-12 Savings include the following:

Item DescriptionGeneral Fund

FY 2011 FY 2012 Total132 #20c K-12: Lottery ($87,256,683) ($77,514,188) ($164,770,871)132 #12c K-12: Include Zero Values for Non-personnal & Transportation for LWA in Support Costs ($39,197,951) ($39,525,220) ($78,723,171)132 #3c K-12: Technical - Use Fiscal & Contractual Div ADM for combined divisions ($24,458,371) ($24,712,726) ($49,171,097)132 #14c K-12: Eliminate Leases, Rental & Facility Costs ($20,221,733) ($20,206,203) ($40,427,936)132 #21c K-12: Textbooks ($15,572,268) ($18,487,237) ($34,059,505)132 #10c K-12: Modify Federal Deduct for Percent Funded Support Costs ($16,980,132) ($17,028,693) ($34,008,825)132 #13c K-12: Eliminate Staff Travel Costs ($14,439,393) ($14,617,019) ($29,056,412)132 #17c K-12: Update School Bus Replacement ($9,758,835) ($9,619,372) ($19,378,207)132 #1c K-12: Technical - Correct SOQ Model for Regional Centers ($8,700,175) ($8,790,845) ($17,491,020)132 #11c K-12: Program Additional Literary Funds for VRS Payments ($13,000,000) $0 ($13,000,000)

TOTAL K-12 SAVINGS $ (249,585,541) $ (230,501,503) $ (480,087,044)

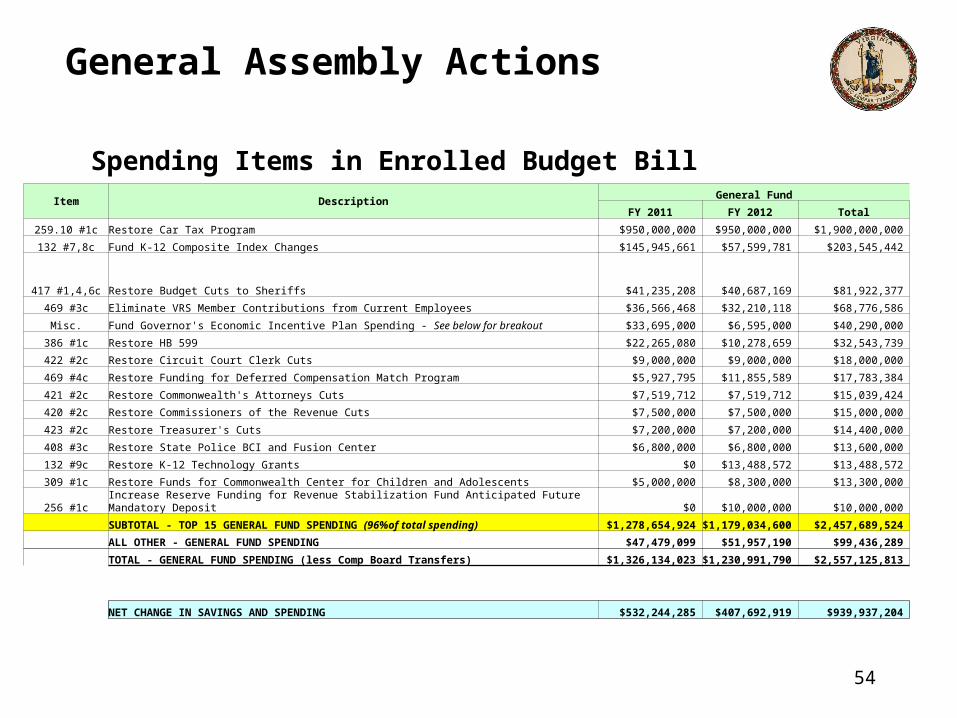

General Assembly Actions

Spending Items in Enrolled Budget Bill

54

Item DescriptionGeneral Fund

FY 2011 FY 2012 Total

259.10 #1c Restore Car Tax Program $950,000,000 $950,000,000 $1,900,000,000

132 #7,8c Fund K-12 Composite Index Changes $145,945,661 $57,599,781 $203,545,442

417 #1,4,6c Restore Budget Cuts to Sheriffs $41,235,208 $40,687,169 $81,922,377

469 #3c Eliminate VRS Member Contributions from Current Employees $36,566,468 $32,210,118 $68,776,586

Misc. Fund Governor's Economic Incentive Plan Spending - See below for breakout $33,695,000 $6,595,000 $40,290,000

386 #1c Restore HB 599 $22,265,080 $10,278,659 $32,543,739

422 #2c Restore Circuit Court Clerk Cuts $9,000,000 $9,000,000 $18,000,000

469 #4c Restore Funding for Deferred Compensation Match Program $5,927,795 $11,855,589 $17,783,384

421 #2c Restore Commonwealth's Attorneys Cuts $7,519,712 $7,519,712 $15,039,424

420 #2c Restore Commissioners of the Revenue Cuts $7,500,000 $7,500,000 $15,000,000

423 #2c Restore Treasurer's Cuts $7,200,000 $7,200,000 $14,400,000

408 #3c Restore State Police BCI and Fusion Center $6,800,000 $6,800,000 $13,600,000

132 #9c Restore K-12 Technology Grants $0 $13,488,572 $13,488,572

309 #1c Restore Funds for Commonwealth Center for Children and Adolescents $5,000,000 $8,300,000 $13,300,000

256 #1c Increase Reserve Funding for Revenue Stabilization Fund Anticipated Future Mandatory Deposit $0 $10,000,000 $10,000,000

SUBTOTAL - TOP 15 GENERAL FUND SPENDING (96%of total spending) $1,278,654,924 $1,179,034,600 $2,457,689,524

ALL OTHER - GENERAL FUND SPENDING $47,479,099 $51,957,190 $99,436,289

TOTAL - GENERAL FUND SPENDING (less Comp Board Transfers) $1,326,134,023 $1,230,991,790 $2,557,125,813

NET CHANGE IN SAVINGS AND SPENDING $532,244,285 $407,692,919 $939,937,204

General Assembly Actions

55

Issues Affecting the Future

Looking Ahead

Application of Federal Medical Assistance Percentage (FMAP)

• The Medicaid Program is a state/federal health insurance program for the indigent

• Costs are shared based on FMAP• The normal split for Virginia is 50% state, 50% federal• The Federal Stimulus Program raised the federal percentage for all

states for the period October 1, 2008 to December 31, 2010 (Virginia’s matching rate is now 39% state, 61% federal)

• Different pieces of legislation, passed by US House/US Senate have proposed extending the more generous FMAP federal rate for another 6 months (through June 30, 2011)

• States are now budgeting for this change even though no single bill has passed both US House/US Senate.

• Virginia has a $417 million contingent appropriation to distribute additional FMAP savings, if enacted. The contingent appropriation would seem to play it safe.

• But,

56

Federal Health Care Reform• The Federal Health Care Reform Program contains a permanent

“Maintenance of Eligibility (MOE)” provision for basic Medicaid services and the Children’s Health Insurance Program (CHIP).

• Because of budget reductions, Virginia will only meet the MOE if the FMAP extension is enacted. (The contingent appropriation will restore enough to satisfy the requirements of the MOE if FMAP is extended).

• Without the FMAP extension, Virginia has a hole of $165.3 million in the recently enacted budget now before the Governor.

• The news on the FMAP extension is that there will be no action by Congress until late April or early May.

• A very uncertain situation for the near future with potential consequences after Virginia’s budget is enacted.

57

Restorations Contingent on FMAP Extension and Required for Health Care Reform

58

Restorations or Spending Items (Introduced Budget Items Shaded) FY 2011 FY 2012 FY 2011 FY 2012Freeze enrollment in Medicaid community-based waivers in CY 2011 $3,745,802 $0 $3,745,802 $0Reduce income limits for SSI from 300 to 275% of SSI $16,870,746 $0 $16,870,746 $0Implement a provider tax on ICF-MR facilities $4,168,066 $0 $0 $0Adjust for Impact of Introduced Budget Reductions on GF $14,452,315 $0 $0 $0Adjust for Impact of Conference Amendments on GF $6,522,348 $0 $0 $0FAMIS eligibility restored to 200 percent of poverty (296#2c) $0 $19,295,228 $0 $19,295,228Inflation increase of medically needy income limits (297#4c) $0 $563,081 $0 $0Environmental Modifications / Assistive Technology Limits (297#6c) $276,385 $0 $0 $0Indigent care funding for teaching hospitals (297#7c) $7,100,000 $7,100,000 $0 $0Long-stay hospital rates (297#11c) $449,298 $522,102 $0 $0Podiatry services (297#12c) $0 $487,500 $0 $0Out-of-state inpatient hospital reimbursement (297#14c) $2,253,621 $0 $0 $0Inpatient hospital reduction (297#18c) $14,609,580 $24,164,264 $0 $0Outpatient hospital reduction (297#19c) $6,928,731 $10,802,339 $0 $0Nursing facility operating and capital rates (297#20c) $12,935,953 $16,334,061 $0 $0Physician rates (297#21c) $8,777,395 $14,714,275 $0 $0Dental rates (297#22c) $1,473,404 $2,334,840 $0 $0Pharmacy dispensing fee (279#23c) $0 $523,579 $0 $0Eligibility reduction for Aged, Blind and Disabled (297#24c) $0 $36,167,138 $0 $36,167,138Auxiliary grant rate - Medicaid impact (297#26c) $0 $623,520 $0 $623,520Eligibility reduction of SSI Group from 300 to 250% (297#26c) $0 $72,881,622 $0 $72,881,622Medicaid waiver rates, freeze and limit on respite care (297#27c) * $23,349,291 $52,510,241 $0 $13,310,010Pharmacy reimbursement (297#28c) $819,468 $927,000 $0 $0Optometry services (297#29c) $344,954 $418,500 $0 $0Residential psychiatric treatment services (297#30c) $1,321,092 $0 $0 $0Add 250 new Intellectual Disability wavier slots (297#31c) $5,407,821 $7,779,375 $0 $0Hospital capital rates (297#32c) $1,609,968 $2,649,535 $0 $0School revenue maximization (297#33c) $0 $592,869 $0 $0Mental health therapeutic day treatment rates (297#35c) $1,494,140 $0 $0 $0Community mental health services for children (304#4c) $2,100,000 $2,100,000 $0 $0Centers for Independent Living (320#2c) $469,454 $0 $0 $0Local departments of social services (328#1c) $1,641,894 $4,642,133 $0 $0Auxiliary grant reduction (330#1c) $0 $2,413,152 $0 $2,413,152Child Welfare Services (331#3c) $3,000,000 $0 $0 $0Chore and companion services (330#2c and 331#2c) $1,000,000 $0 $0 $0

Other purchased services for local departments of social services (330#3c) $1,000,000 $0 $0 $0General relief (332#1c) $2,400,000 $2,400,000 $0 $0Healthy Families (333#1c) $1,368,195 $0 $0 $0

Total $147,889,921 $282,946,354 $20,616,548 $144,690,670

Biennial Total $430,836,275 $165,307,218

FMAP Resources Potentially Available DMAS FMAP 2 Qtr. Extension $ 376,817,847 DMAS FMAP 2 Qtr. Extension - Part D $ 20,400,000 Medicaid Match for DBHDS State Facilities $ 13,075,011 Medicaid Match for CSA $ 3,773,039 FMAP Available to IV-E Foster Care $ 3,000,000

$ 417,065,897

Remaining FMAP Available / (Overspent) (13,770,378)

* Details of Medicaid Waiver Item: Reduced limit on hours for respite care $5,195,132 $21,238,946 $0 $0Waiver freeze $0 $13,310,010 $0 $13,310,010Waiver rates $18,154,159 $17,961,285 $0 $0Subtotal $23,349,291 $52,510,241 $0 $13,310,010

59

The Projected Balance in the Revenue Stabilization Fund Will Be $361.2 Million After the Proposed FY 2010 Withdrawal of $292.9 Million and the Proposed $50 Million Deposit in FY 2012

Revenue Stabilization Fund -- June 30 BalanceFY 1995-09 Actual and FY 2010-2012 Forecast

(millions of dollars)

$0

$200

$400

$600

$800

$1,000

$1,200

$80.1 $85.0

$156.6

$224.3

$361.5

$574.6

$715.6

$472.4

$247.5

$340.1

$482.3

$1,064.7

$1,189.8

$1,014.9

$575.1

$293.8 $300.9$361.2

Mil

lio

ns

60

VRS Funded Status: State Employees

78.0% 81

.7% 89.3%

95.3%

105.5

%10

6.8%

104.1

%

100.4

%

94.6%

85.8%

83.3% 85

.1% 88.0%

84.0%

78.5%

72.9%

65.7%

61.7%

0%

20%

40%

60%

80%

100%

120%

1994 1998 2000 2002 2004 2006 2008 2010 2012

Assumptions: • FY 2009 investment return is -21.1%.• All projected years investment return is 7.5% and 2.5% inflation rate.• Employer contribution rates for fiscal year 2009 is fixed at 6.23% and for 2010 at 6.26% for state employees.• Actual value of assets subject to 5-year smoothing with no corridor.

61

VRS Funded Status: Teachers

0%

20%

40%

60%

80%

100%

120%

1994 1998 2000 2002 2004 2006 2008 2010 2012

Assumptions: • FY 2009 investment return is -21.1%•All projected years investment return is 7.5% and 2.5% inflation rate with 20-year amortization period.•Employer contribution rates for FY 2009 and FY 2010 are fixed at 8.81%•Actual value of assets subject to 5-year smoothing with no corridor.

Components of General Fund Revenues

In FY09, individual nonwithholding, corporate income, and recordation tax payments accounted for $3.3 billion of GF revenues, up from FY02’s $2.0 billion, but down significantly from FY08’s $4.1 billion (-21%).

In FY09, 84% of GF revenues were from ongoing economic activity via withholding and sales tax collections, similar to the FY02 recession rate of 83%, but up significantly from the 75% average share over the four previous fiscal years. Sales

23%Withholding

60%

Corporate3%

Nonwithholding14%

Recordation2%

Note: The percentages below each source reflect the percent share of total general fund revenues. The sum of the components exceeds 100 due to the exclusion of individual refunds and other revenue sources.

Sales20%

Withholding64%

Corporate5%

Nonwithholding16%

Recordation2%

Withholding Sales Nonwithholding Corporate Recordation

FY 2009

FY 2002

62

63

Growth in Total General Fund Revenues

Fiscal Year 1961 - Fiscal Year 2012

(Nominal - Actual Dollars)

FY Total Revenues Growth FY Total Revenues Growth

61 230,998,887 - 87 4,590,434,000 11.1%

62 242,144,567 4.8% 88 5,054,382,000 10.1%

63 286,304,265 18.2% 89 5,478,912,000 8.4%

64 298,033,919 4.1% 90 5,494,884,000 0.3%

65 323,213,412 8.4% 91 5,471,879,000 -0.4%

66 365,129,776 13.0% 92 5,623,213,000 2.8%

67 414,755,644 13.6% 93 6,133,637,000 9.1%

68 533,597,744 28.7% 94 6,503,368,000 6.0%

69 706,254,374 32.4% 95 6,881,145,000 5.8%

70 743,721,322 5.3% 96 7,356,110,000 6.9%

71 807,954,651 8.6% 97 7,949,327,000 8.1%

72 922,653,686 14.2% 98 8,773,520,000 10.4%

73 1,054,469,443 14.3% 99 9,702,747,000 10.6%

74 1,168,562,871 10.8% 00 10,788,482,000 11.2%

75 1,303,178,893 11.5% 01 11,105,275,000 2.9%

76 1,428,421,157 9.6% 02 10,678,954,000 -3.8%

77 1,636,301,819 14.6% 03 10,867,149,000 1.8%

78 1,923,085,084 17.5% 04 11,917,867,000 9.7%

79 2,115,211,522 10.0% 05 13,687,252,000 14.8%

80 2,344,928,934 10.9% 06 14,834,298,000 8.4%

81 2,579,663,941 10.0% 07 15,565,827,000 4.9%

82 2,796,458,741 8.4% 08 15,766,951,000 1.3%

83 2,975,687,935 6.4% 09 14,315,060,000 -9.2%

84 3,397,710,261 14.2% 10* 13,987,600,000 -2.3%

85 3,790,816,000 11.6% 11* 14,582,300,000 4.3%

86 4,131,778,000 9.0% 12* 15,313,300,000 5.0%

* March 14, 2010 Post-GA Forecast (Excludes Transfers)

• In 2007, the top 0.1% paid 20%.

• In 2007, the top 1% of filers paid 40% of total revenues

– Up from 25% in 1991

• The top 5% paid 60%

• The top 10% paid 71%

Top 0.1%

Top 0.1%Top 0.1%

Top 1% Top 1%

Top 1%

Top 5%Top 5%

Top 5%Top 10%

Top 10%Top 10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

1997 2002 2007

High-End Filers Determine Personal Income Tax Revenues

Source: IRS data and Tax Foundation

65

Trends in Withholding Compared to Individual Nonwithholding

Percent Growth Over the Prior Year

-40

-30

-20

-10

0

10

20

30

40

50

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09'10*'11*'12*

Percent Change

Withholding Nonwithholding* Forecast

66

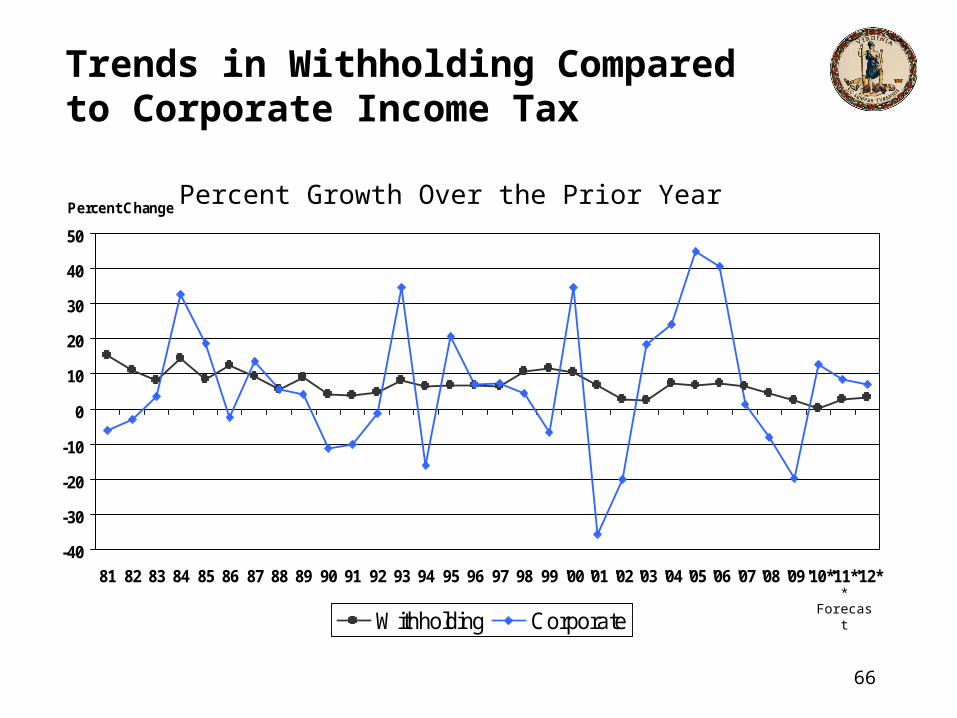

Trends in Withholding Compared to Corporate Income Tax

Percent Growth Over the Prior Year

-40

-30

-20

-10

0

10

20

30

40

50

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09'10*'11*'12*

Percent Change

Withholding Corporate* Forecast

67

Trends in Withholding Compared to Recordation Tax

Percent Growth Over the Prior Year

-40

-30

-20

-10

0

10

20

30

40

50

81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09'10*'11*'12*

Percent Change

Withholding Wills (Recordation)* Forecast

Note: Recordation growth rate is adjusted to remove the rate increase and for transfers per HB 3202.

Growth in Total General Fund Revenues FY 1962 - FY 2012

-15

-10

-5

0

5

10

15

20

25

30

35

62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 '00 '02 '04 '06 '08 10* 12*

Annual Percent Change

Fiscal Year * March 14, 2010 Post-GA Forecast

68

69

General Fund Revenue Growth% Increase Year-Over-Year

-15

-10

-5

0

5

10

15

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Percent Change

Fiscal Year

FY10-12 = Conference, FY13-16 = December Introduced

70

Looking Ahead: Slower Revenue Growth

Average Annual Growth

5 years (FY03 to FY08) +7.6%10 years (FY98 to FY08) +6.0%15 years (FY93 to FY08) +6.5%20 years (FY88 to FY08) +5.9%25 years (FY83 to FY08) +6.9%30 years (FY78 to FY08) +7.3%35 years (FY73 to FY08) +8.0%40 years (FY68 to FY08) +7.8%

• How have general fund revenues grown?

• The forecast of general fund revenues projects much slower growth in the future.

Average Annual Growth

FY2010 -2.3%FY2011 +4.3%FY2012 +5.0%