section 2: risk management for institutional investors financial risk management uc berkeley prof....

TRANSCRIPT

Section 2: Risk Management for Institutional Investors

Financial Risk Management

UC Berkeley

Prof. Jeff (YuQing) Shen

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley2

The BIG Picture

• Theory

•Efficient Frontier

•Asset/Liability Framework

•Alpha/Beta risk budgeting

• Practice

•Pension Crisis

•GM Pension Plan

•Yale Endowment

• Theory

•VaR

•Stochastic behavior of asset

returns

•Worst case scenario

• Practice

•Investment bank VaR

•Bear Stearns

• The Theory

•Active Portfolio Management

•Quantitative equity models

•Hedge fund investment

• The Practice

•Hedge fund industry

•Aug 2007 crisis for quant

Investment BankInstitutional Investor Hedge Fund

Institutional investors in the US

3

Asset allocation trend

4

Significant turnover of managers

5

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley6

Institutional investor risk management

US corporate defined benefit plans

Endowment and foundation

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley7

The liability is the present value of benefit cash flows

Present value (discounted at 7.0%)

= $2.56 billion liability

Year Benefit payments2003 150,000,000$

2004 151,500,000$

2005 153,166,500$

2006 155,019,815$

2007 157,083,128$

2008 159,382,982$

2009 161,949,861$

2010 164,818,902$

2011 168,030,756$

2012 171,632,645$

2013 175,679,653$

2014 180,236,330$

2015 185,378,683$

2016 191,196,660$

2017 197,797,288$

2018 205,308,636$

2019 213,105,228$

2020 221,197,896$

… ……….

… ……….

… ……….

Annual benefit payment cash flows ($mm)

$-

$50

$100

$150

$200

$250

$300

20032006

20092012

20152018

20212024

20272030

20332036

2039

($ m

illio

ns

)

Year

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Duration estimation in a pension plan

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley9

The liability risk is sensitive to discount rate changes

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2 3 4 5 6 7 8 9 10 11 12

Discount Rate

Pre

sen

t V

alu

e o

f L

iab

iliti

es (

$ m

illio

ns)

$3.5 billion @ 7%

•Duration measures the sensitivity of a liability’s value to changes in interest rates.

Bottom Line: Rates = Liabilities and Rates = Liabilities

•A duration of 14 means that the liability value will increase (decrease) by 14% given a 1% decrease (increase) in rates. Longer duration = greater sensitivityof liability value to rate changes.

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley10

ABO and PBO

ABO (Accumulated Benefit Obligation) is the value of all benefits earned to date. It includes nonvested as well as vested benefits. It may approximate the value of benefits payable on a plan termination and is the basis of a potential balance sheet liability.

PBO (Projected Benefit Obligation) is a measure of the liability for accumulated service, but reflects future salary increases. “Projected” refers to the projection of salaries.

The key difference is that PBO reflects future salary growth, which can be driven by at least two important factors:– Inflation– Productivity growth

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley11

Funded ratio is a key risk measure for managing pension plan

Funded RatioA ssets

L iab ility_

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley12

Case study: Pension Crisis of 2002

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Pension Crisis of 2002

1. Institutional context

2. Funded status

3. Assets

4. Liability

5. Contribution

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Significant assets in corporate DB plans

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Industry distribution of DB plans

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Pension Crisis of 2002

1. Institutional context

2. Funded status

3. Assets

4. Liability

5. Contribution

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley17

Funded ratios were at an all-time low in 2002

PBO funded ratio — Top 200 corporate plansFive-year intervals since 1987

Top 20% Median Bottom 20%

1987 150% 119% 82%

1992 142% 107% 79%

1997 147% 112% 90%

Source: S&P Compustat

2002 2002 113%113% 80%80% 60%60%

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley18

A volatile history with a dramatic drop

80% Funded

145% Funded

Assumes beginning Funded ratio of 100% in 1975, 10 duration, 6% benefit payouts, 3.5% Service cost. Asset returns reflect a hypothetical portfolio of 60% S&P 500/40% Lehman Aggregate Bonds. Discount rate is the AA Corp. Bond Yield. Assumes zero contributions.

60%

80%

100%

120%

140%

160%

19751977

19791981

19831985

19871989

19911993

19951997

19992001

2003

Fu

nd

ed

ra

tio

Funded ratio of a hypothetical DB plan

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Funded ratio status

19

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Underfunding crisis

20

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

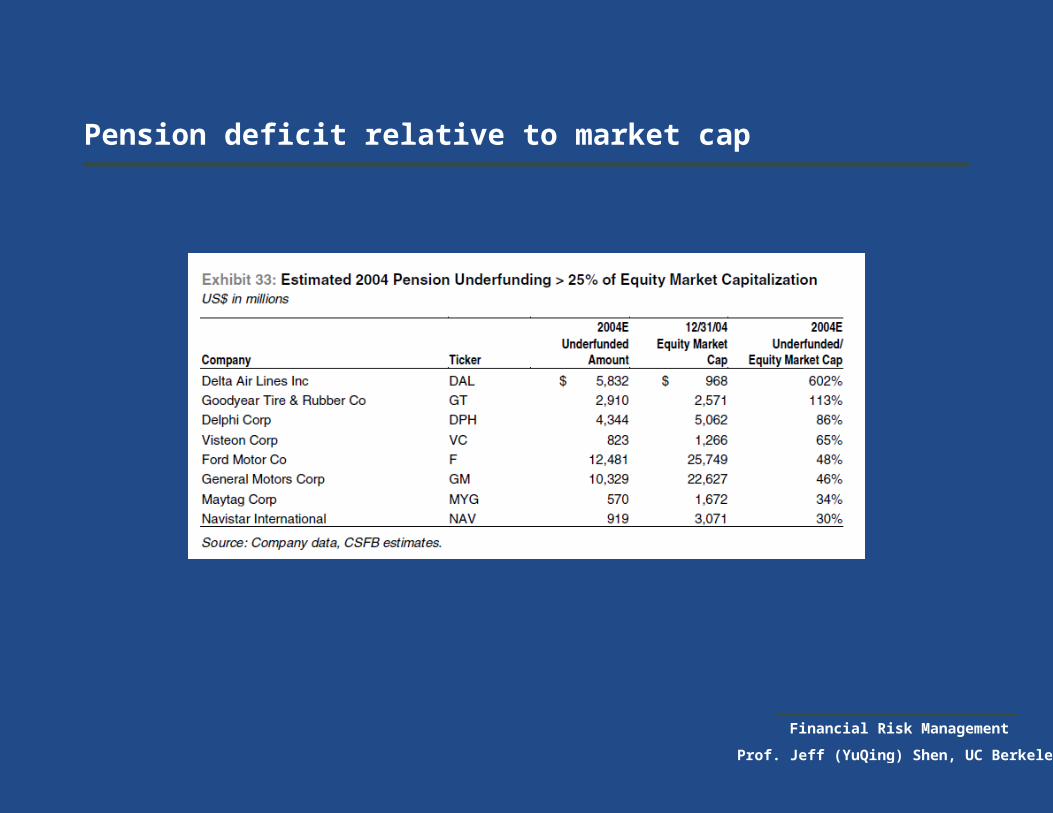

Pension deficit relative to market cap

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Pension Crisis of 2002

1. Institutional context

2. Funded status

3. Assets

4. Liability

5. Contribution

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Asset allocation

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Equity and fixed income allocations

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Asset allocation over time

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Different views of the world

26

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

What are the pros and cons of owning the company stock in the pension plan?

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Pension Crisis of 2002

1. Institutional context

2. Funded status

3. Assets

4. Liability

5. Contribution

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Discount rate

29

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Discount rate

30

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Discount rate distribution

31

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Pension Crisis of 2002

1. Institutional context

2. Funded status

3. Assets

4. Liability

5. Contribution

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

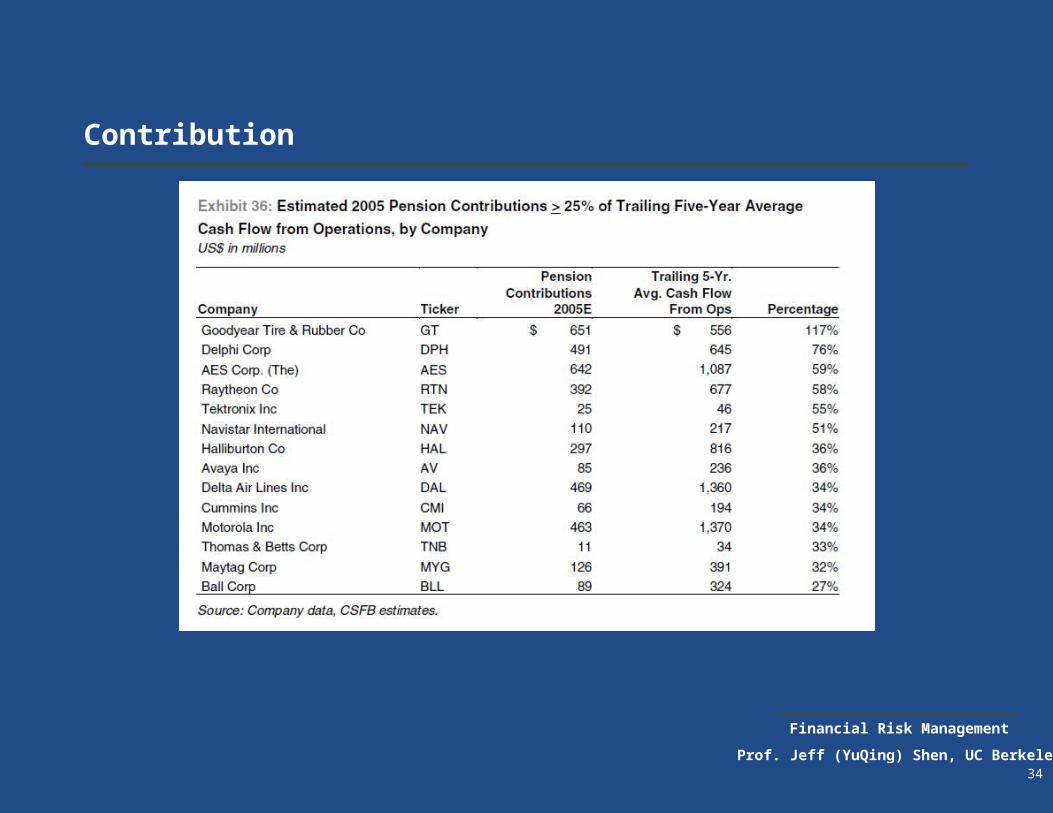

Contribution

33

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Contribution

34

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Pension income/expenses

35

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley36

What happened?

1. Interest rate

2. Asset return

3. Corporate finance implication

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley37

Liabilities “outperformed” assets

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1996 1997 1998 1999 2000 2001 2002 2003

Ann

ual a

sset

or

liabi

lity

grow

th

Asset growth (60/40)

Liability growthFor illustrative purposes only. Assumes 10-duration liability, 3.5% Service cost. Asset returns reflect a hypothetical portfolio of 60% S&P 500/40% Lehman Aggregate Bonds. Discount rate derived by the Lehman AA Long Corp. Bond and Moody’s AA Long Corp. Bond Yields. Assumes zero contributions. Benefit payouts are not reflected in individual years’ annual growth. Assumes rates dropped 135bp, from 7.85% at end of 1999 to 6.50% as of end of Aug 2003, as follows: 2000: -50bp; 2001: -60bp; 2002: -25bp; 2003: 0bp. Without rate drops over the last 4 years, liabilities would have outperformed assets by 46.5%.

Annual asset returns and liability growth

(hypothetical plan, before benefit payouts)

Assets outperform Liabilities outperform

12%17%16%

-9%-4%

-1%

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley38

Declining discount rate => increase in liability

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

End of Year

Dis

co

un

t R

ate

Discount Rate

Long AA Corp Bond Yield

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Corporate finance risk implications

39

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley40

Lower reported income (GAAP)Lower reported income (GAAP)

Decrease in book value

Decrease in book value

Rating agency pressure

Rating agency pressure

– Cash contribution required after extended funding holiday

– Large negative effect on earnings resulting from pension expense

– Writedown of book equity due to critical under-funding

– Shareholder aversion to earnings volatility created by pension income

Quality of earningsQuality of earnings

Liquidity requirements

Liquidity requirements

– Overhang of increasing net pension liability

Large bottom-line impacts

6

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Shareholder exposure

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley42

Accounting and corporate finance implications of pensions are asymmetric - the risks are weighted to the downside

There is greater downside to the corporation when the plan does poorly than upside when the plan does well

There is greater downside to the corporation when the plan does poorly than upside when the plan does well

Downside associated with poor performance

Downside associated with poor performance

Upside associated with strong performance

Upside associated with strong performance

Diversion of cash from core operations to cure deficits and meet statutory contribution minimums

Equity write-downs from ABO underfunding can threaten debt covenants

Attracts rating agency attention and may contribute to downgrade

Poor plan performance is often correlated with weak operating environment for core business

Severely underfunded plans must give notice to employees describing pension condition

May add to non-cash earnings– However, excise taxes prevent company

from realizing a cash benefit

May reduce or avoid the need to make ongoing contributions– Risk levels required to generate high returns

can lead directly to the harsh consequences of pension deficits

7

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley43

Financial economics and corporate pensions risk management

The shareholder’s perspective

If shareholders want equity leverage they can obtain it directly themselves

Companies should prefer to borrow in the capital markets or buy-back stock if they want to increase leverage – not mis-match pension liabilities

Pension investment decisions should be justified relative to other uses of corporate capital

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

What are the lessons learned?

Did we manage pension risk well?

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Did we really learn the lessons?

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

2008 Pension crisis

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

What happened in 2008 for the pension plans?

What happened to

Equity return?

Interest rate?

Contribution?

47

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Funded ratio

48

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Asset liability performance

49

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

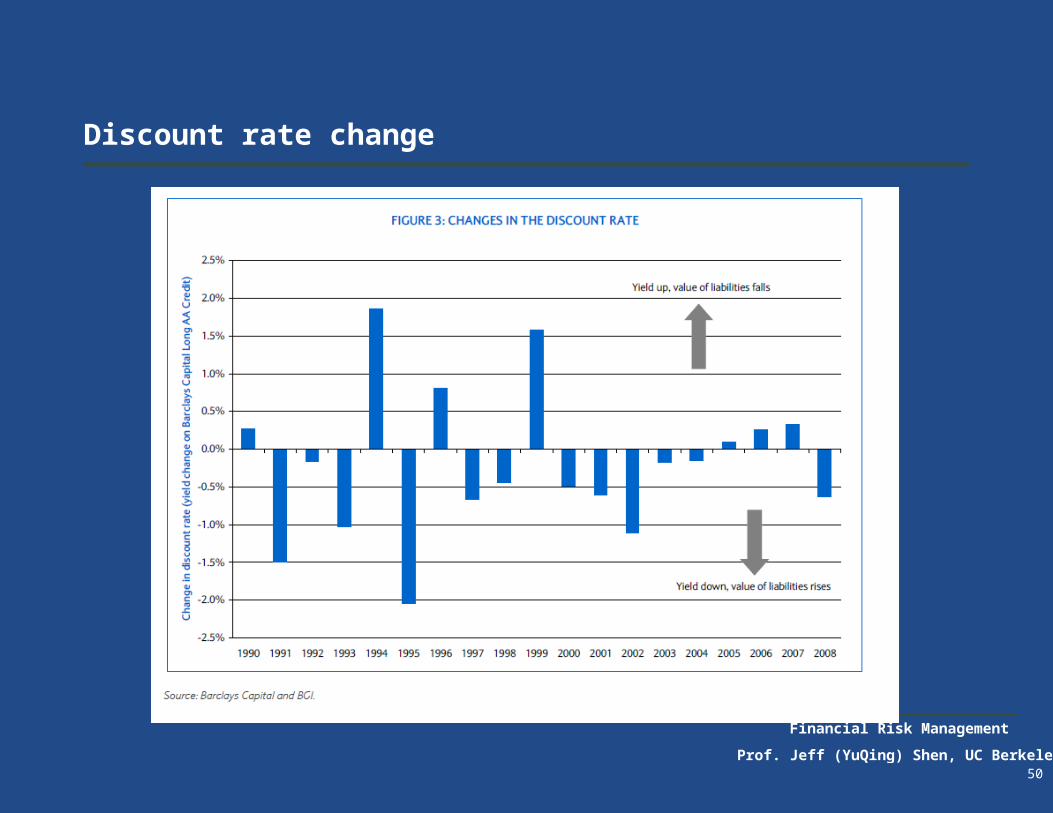

Discount rate change

50

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Risk free rate and credit spread

51

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Inflation

52

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Credit spread

53

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

What are the lessons learned?

Did we manage pension risk well?

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley55

The BIG Picture

• Theory

•Efficient Frontier

•Asset/Liability Framework

•Alpha/Beta risk budgeting

• Practice

•Pension Crisis

•GM Pension Plan

•Yale Endowment

• Theory

•VaR

•Stochastic behavior of asset

returns

•Worst case scenario

• Practice

•Investment bank VaR

•Bear Stearns

• The Theory

•Active Portfolio Management

•Quantitative equity models

•Hedge fund investment

• The Practice

•Hedge fund industry

•Aug 2007 crisis for quant

Investment BankInstitutional Investor Hedge Fund

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Efficient frontier theory

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley57

Short-term (one period) analysis

Two assets:Risk free asset Rf,t+1 and risky asset Rt+1

The risky asset has expected return of EtRt+1 and expected variance t2.

The portfolio return is:

The portfolio expected return is

The portfolio expected risk is

1,11, )1( tfttttp RwRwR

1,11,1, tfttttftpt RREwRRE

222, tttp w

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley58

Mean-variance optimization: quadratic utility function

This can be rewritten as:

The solution is

MAXwt E tRp,t1 k

2 p,t

2

MAXwt R f ,t1 wt E tRt1 R f ,t1 k2

wt2 t

2

2

1,1

t

tfttt k

RREw

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley59

What does this mean?

2

1,1

t

tfttt k

RREw

Risk Aversion Parameter

The higher the risk aversion, the less

investment in the risky asset class

Risk of portfolio

The higher the risk or variance of return,

the less investment in the risky asset class

Return Premium of Risky Asset Class

The higher the return premium,

the more investment in the risky asset class

Allocation to

Risky Asset

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley60

Return and risk assumptions are crucial for efficient frontier construction

Optimal Portfolio

Expected Returns

Volatility Mean VarianceOptimisation

Correlation

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

5.0% 7.0% 9.0% 11.0% 13.0% 15.0% 17.0%

Standard Deviation

Ex

pe

cte

d R

etu

rn

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley61

Market cap can help to set constraints

Source: Bloomberg.*

ASSET CLASS Constraints

Cash

US Core Fixed

High Yield Max 5%, <=10% US Fixed

US Large Cap

US Small Cap <=20% US Large Cap

Int'l Devpd Equity <=40% US Equity

Em.Mkts.Equity <=20% Int'l Devpd Equity

Private Equity PE Max 5%

REITS Alternatives (PE+REIT+RE+HF)

Direct Real Estate <={10%, 15%, 20%}

Hedge Funds Each Alternative Max 10%

These constraints were applied for illustrative purposes and do not represent the client’s specific risk or asset exposure tolerances. We recommend that a full asset-liability and investment policy analysis be conducted to determine an appropriate allocation for a given plan.

The constraints imposed can be informed by a consideration of global market capitalizations as well as risk tolerance, market views, liquidity needs, and other factors

SAMPLE CONSTRAINTS

Fixed Income: 48% Equity: 52%

Relative weights

US High Yield/US Inv.Grade 5%

US Small Cap/US Large Cap 7%

Em.Mkts./Int'l Devpd.Equity 11%

Int'l Equity/US Equity 60%

Global Market Weights

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Mar-99

Jun-99S

ep-99D

ec-99M

ar-00Jun-00S

ep-00D

ec-00M

ar-01Jun-01S

ep-01D

ec-01M

ar-02Jun-02S

ep-02D

ec-02M

ar-03

Int'l Devpd Fixed Income $6,200B (21%)

US High Yield FI $355B (1%)

US Investment Grade FI $7,600B (26%)

Emerging Markets Equity $532B (2%)

Int'l Developed Equity $5,275B (18%)

US Small Cap $625B (2%)

US Large Cap $8,700B (30%)

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Long term return forecasting

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley63

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

How would you calculate the expected return of a condo in the bay area?

What’s the rent income return?

What’s the rent income growth potential?

What’s the potential for valuation upside/downside?

64

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Long term risk forecasting

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley66

US large cap equity volatility

Note: US large cap here is defined as S&P 500 index

Monthly standard deviation of US large cap 4.14%, which can be annualised to be 14.3%.

(20.00)

(15.00)

(10.00)

(5.00)

-

5.00

10.00

15.00

S&P 500 Monthly return

Postive 1 STD

Negative 1 STD

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley67

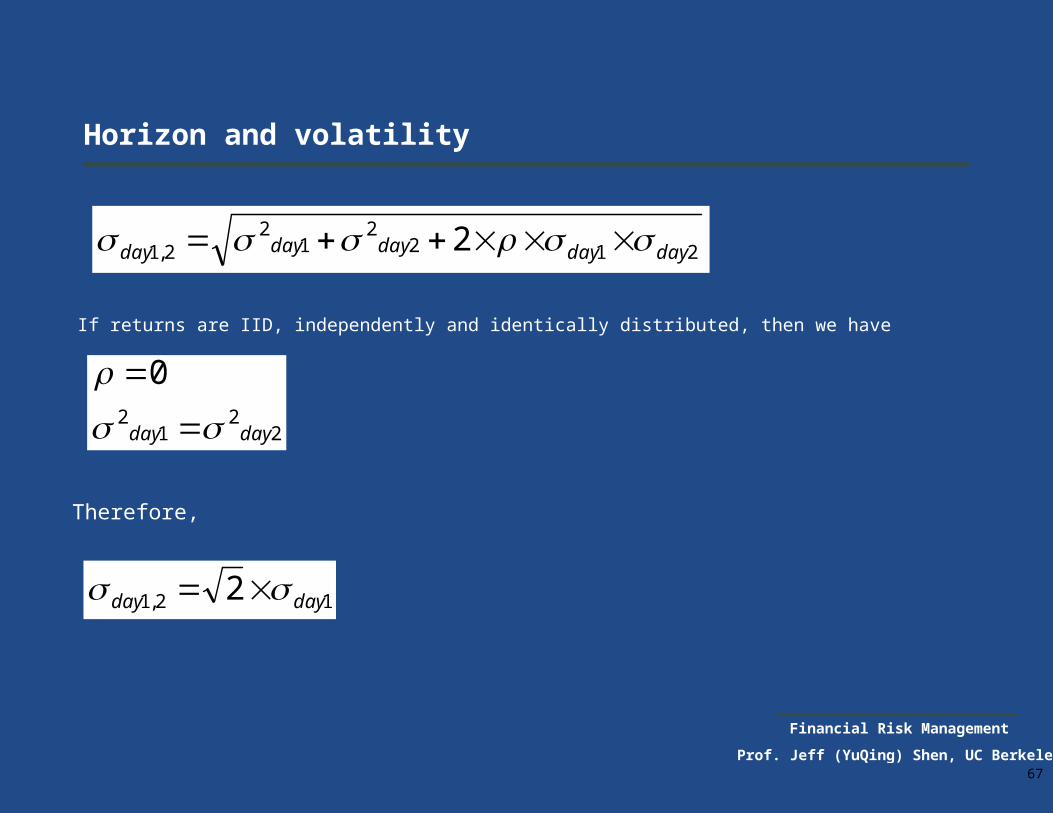

Horizon and volatility

If returns are IID, independently and identically distributed, then we have

2122

12

2,1 2 daydaydaydayday

22

12

0

dayday

Therefore,

12,1 2 dayday

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley68

Squared root of time

Volatility calculation

Monthly Quarterly Semiannualy Annualy1.0% 1.7% 2.4% 3.5%2.0% 3.5% 4.9% 6.9%3.0% 5.2% 7.3% 10.4%4.0% 6.9% 9.8% 13.9%5.0% 8.7% 12.2% 17.3%6.0% 10.4% 14.7% 20.8%7.0% 12.1% 17.1% 24.2%8.0% 13.9% 19.6% 27.7%9.0% 15.6% 22.0% 31.2%

10.0% 17.3% 24.5% 34.6%

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley69

Portfolio volatility calculation

22112

222

11 2 wwwwportfolio

33113,1

33223,2

22112,1

233

222

211

2

2

2

ww

ww

ww

www

portfolio

Two Assets

Three Assets

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley70

Portfolio volatility calculation

)''()( wwportfolio

n Assets

nnnn

n

n

n

nwwww

where

,2,1,

,22,21,2

,12,11,1

21

21

...

............

...

...

,...,

,...,

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley71

The BIG Picture

• Theory

•Efficient Frontier

•Asset/Liability Framework

•Alpha/Beta risk budgeting

• Practice

•Pension Crisis

•GM Pension Plan

•Yale Endowment

• Theory

•VaR

•Stochastic behavior of asset

returns

•Worst case scenario

• Practice

•Investment bank VaR

•Bear Stearns

• The Theory

•Active Portfolio Management

•Quantitative equity models

•Hedge fund investment

• The Practice

•Hedge fund industry

•Aug 2007 crisis for quant

Investment BankInstitutional Investor Hedge Fund

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley72

Asset only framework

US Equities SC

Emerging markets

Long Bonds

Cash

US Equities LC

Japanese EquitiesEuropean Equities

Increasing volatility

Incr

easi

ng r

etur

n

Aggressive Plans

Conservative Plans

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley73

ABO and PBO

ABO (Accumulated Benefit Obligation) is the value of all benefits earned to date. It includes nonvested as well as vested benefits. It may approximate the value of benefits payable on a plan termination and is the basis of a potential balance sheet liability.

PBO (Projected Benefit Obligation) is a measure of the liability for accumulated service, but reflects future salary increases. “Projected” refers to the projection of salaries.

The key difference is that PBO reflects future salary growth, which can be driven by at least two important factors:– Inflation– Productivity growth

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley74

Asset Liability Framework

US Equities SC

Emerging markets

Long Bonds

US Equities LC

Japanese EquitiesEuropean Equities

Increasing variability of fund surplus

Incr

easi

ng r

etur

n

Aggressive Plans

Conservative Plans

Note: This surplus optimization was performed including liabilities as a “negative asset,” highly negatively correlated with interest rates.

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley75

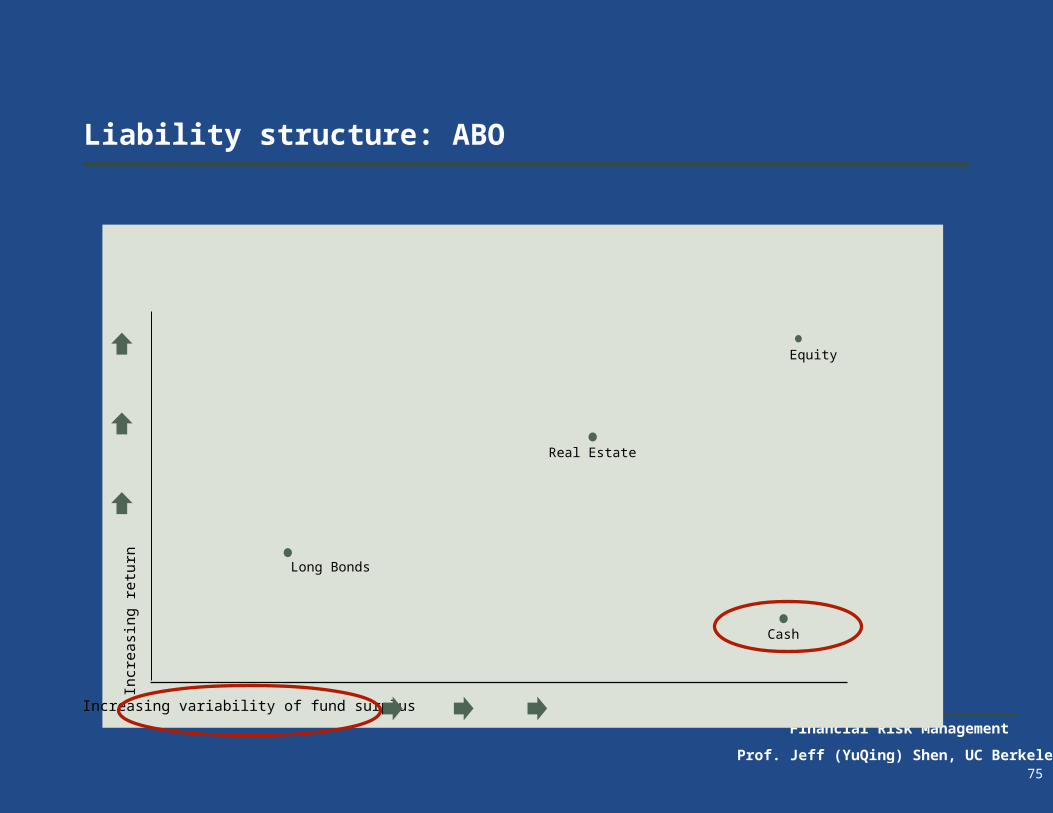

Liability structure: ABO

Equity

Long Bonds

Real Estate

Increasing variability of fund surplus

Incr

easi

ng r

etur

n

Cash

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley76

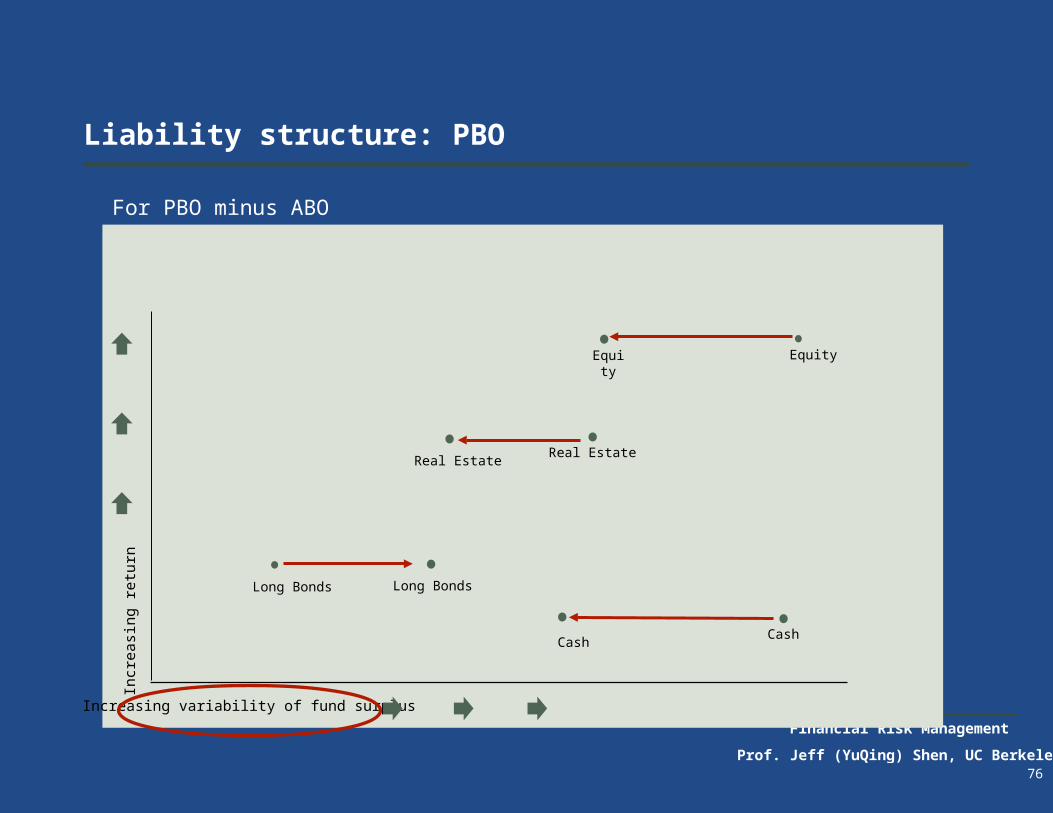

Liability structure: PBO

For PBO minus ABO

Equity

Long Bonds

Real Estate

Increasing variability of fund surplus

Incr

easi

ng r

etur

n

CashCash

Long Bonds

Real Estate

Equity

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley77

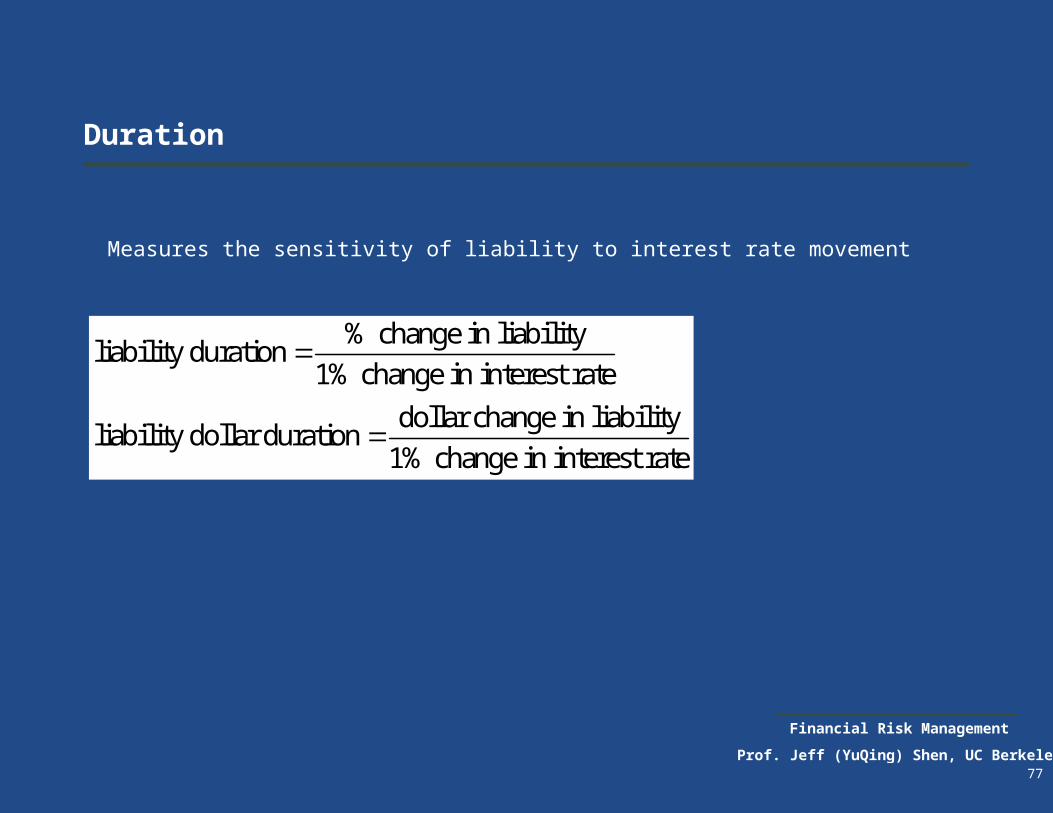

Duration

Measures the sensitivity of liability to interest rate movement

% change in liabilityliability duration

1% change in interest rate

dollar change in liabilityliability dollar duration

1% change in interest rate

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley78

Immunization

Immunization = Asset/liability duration matching

= Asset Liability Net Duration Close to Zero

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Liability driven investment

79

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley80

The BIG Picture

• Theory

•Efficient Frontier

•Asset/Liability Framework

•Alpha/Beta risk budgeting

• Practice

•Pension Crisis

•GM Pension Plan

•Yale Endowment

• Theory

•VaR

•Stochastic behavior of asset

returns

•Worst case scenario

• Practice

•Investment bank VaR

•Bear Stearns

• The Theory

•Active Portfolio Management

•Quantitative equity models

•Hedge fund investment

• The Practice

•Hedge fund industry

•Aug 2007 crisis for quant

Investment BankInstitutional Investor Hedge Fund

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley81

Alpha/Beta Framework

Issues

Solution 1: Diversify Beta

Solution 2: Diversify Alpha

Solution 3: Alpha/Beta Framework

Case Study

– Yale endowment approach

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley82

No free lunch: higher return requires higher risk

Strategically overweight high return assets: return the easy way

Tactically take more active risk: smart, but difficult

Exp

ecte

d R

etur

n

Risk

Easy but risky

CashGov’ts

CreditHigh Yield

EquitiesEmerging markets

Smart but harder

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley83

What are Beta and Alpha risks?

Beta returns are derived from asset class returns.

Characteristics of Beta return:

Limited in number

Economic fundamentals driven

Relatively low Sharpe ratio

Reliable over the long run

Easy but risky

Alpha returns are active managers’ value-added.

Characteristics of Alpha return:

Abundant in number

Manager skills driven

Zero-to-negative-sum game

Not necessarily reliable

Smart but harder

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley84

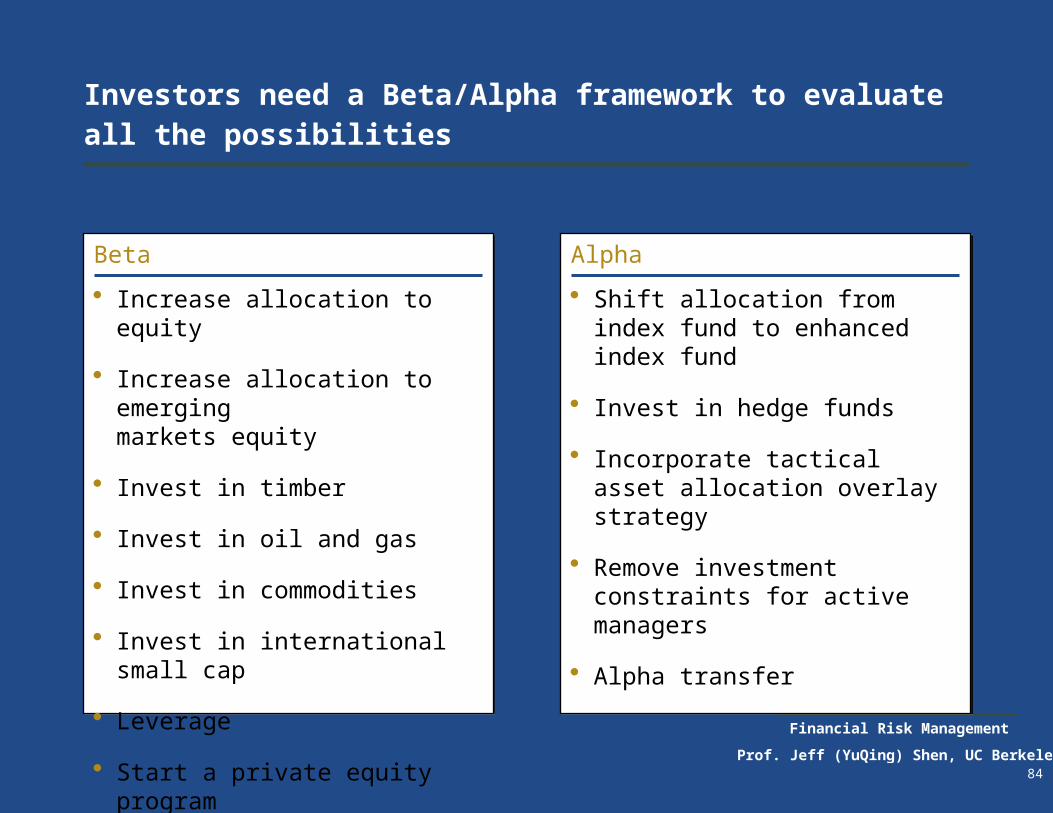

Investors need a Beta/Alpha framework to evaluate all the possibilities

Beta

Increase allocation to equity

Increase allocation to emergingmarkets equity

Invest in timber

Invest in oil and gas

Invest in commodities

Invest in international small cap

Leverage

Start a private equity program

Alpha

Shift allocation from index fund to enhanced index fund

Invest in hedge funds

Incorporate tactical asset allocation overlay strategy

Remove investment constraints for active managers

Alpha transfer

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley85

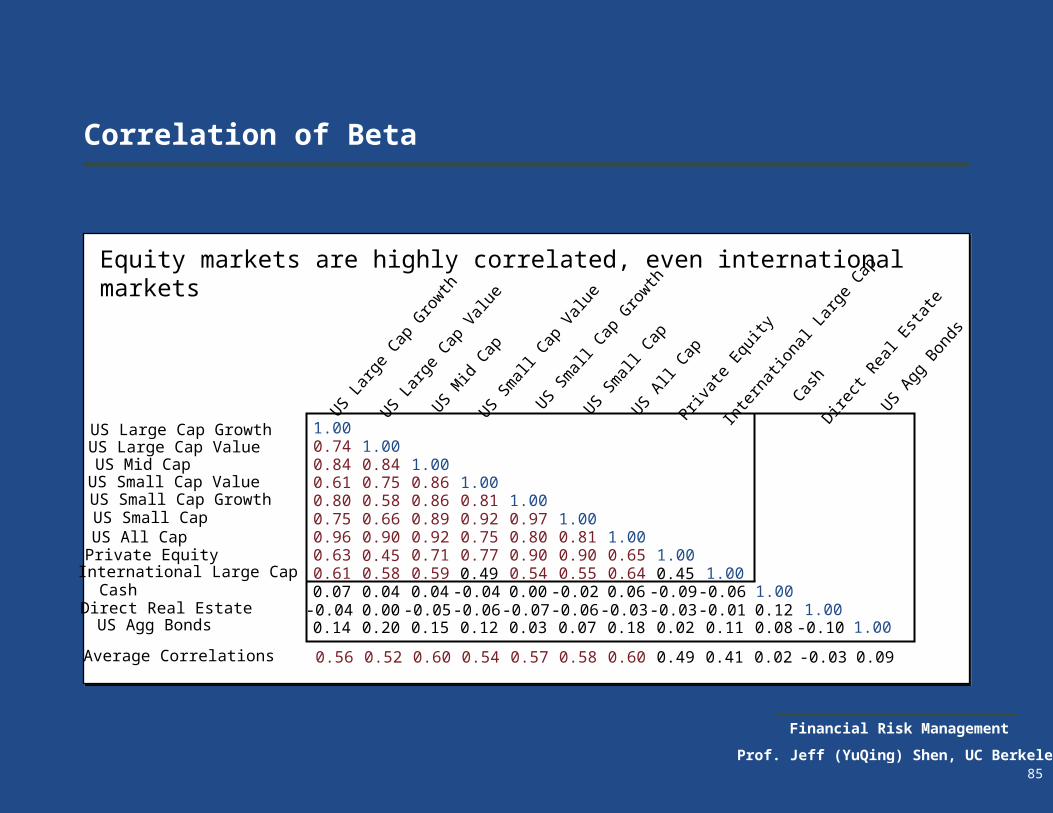

Correlation of Beta

Equity markets are highly correlated, even international markets

US Large Cap GrowthUS Large Cap ValueUS Mid CapUS Small Cap ValueUS Small Cap GrowthUS Small CapUS All Cap

International Large CapCashDirect Real EstateUS Agg Bonds

Private Equity

1.000.74 1.000.84 0.84 1.000.61 0.75 0.86 1.000.80 0.58 0.86 0.81 1.000.75 0.66 0.89 0.92 0.97 1.000.96 0.90 0.92 0.75 0.80 0.81 1.000.63 0.45 0.71 0.77 0.90 0.90 0.65 1.000.61 0.58 0.59 0.49 0.54 0.55 0.64 0.45 1.000.07 0.04 0.04 -0.04 0.00 -0.02 0.06 -0.09 -0.06 1.00

-0.04 0.00 -0.05 -0.06 -0.07 -0.06 -0.03 -0.03 -0.01 0.12 1.000.14 0.20 0.15 0.12 0.03 0.07 0.18 0.02 0.11 0.08 -0.10 1.00

Average Correlations 0.56 0.52 0.60 0.54 0.57 0.58 0.60 0.49 0.41 0.02 -0.03 0.09

US Lar

ge C

ap G

rowth

US Lar

ge C

ap V

alue

US Mid

Cap

US Sm

all C

ap V

alue

US Sm

all C

ap G

rowth

US Sm

all C

apUS A

ll Cap

Inte

rnat

iona

l Lar

ge C

ap

Cash

Direct

Rea

l Est

ate

US Agg

Bon

ds

Privat

e Equ

ity

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley86

First problem: portfolio risk is concentrated in Beta risk taking...

Description Allocation Risk contribution

Alpha Large Cap Managers 22%Small and Mid Cap Managers 26%International Managers 22%Alternative Investments 7%Fixed Income and Cash Managers 19%Real Assets 4%

Total Alpha Risk Contribution 100%

Beta U.S. Equities 48%International Equities 22%Fixed Income and Cash (incl Alt. Inv.) 26%Real Assets 4%

Total Beta Risk Contribution 100%

Total Risk

0.27%0.37%

-0.12%0.38%0.03%0.00%

0.93%

7.16%3.23%0.12%0.00%

10.51%

11.44%

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley87

The only Bloomberg Screen that matters

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley88

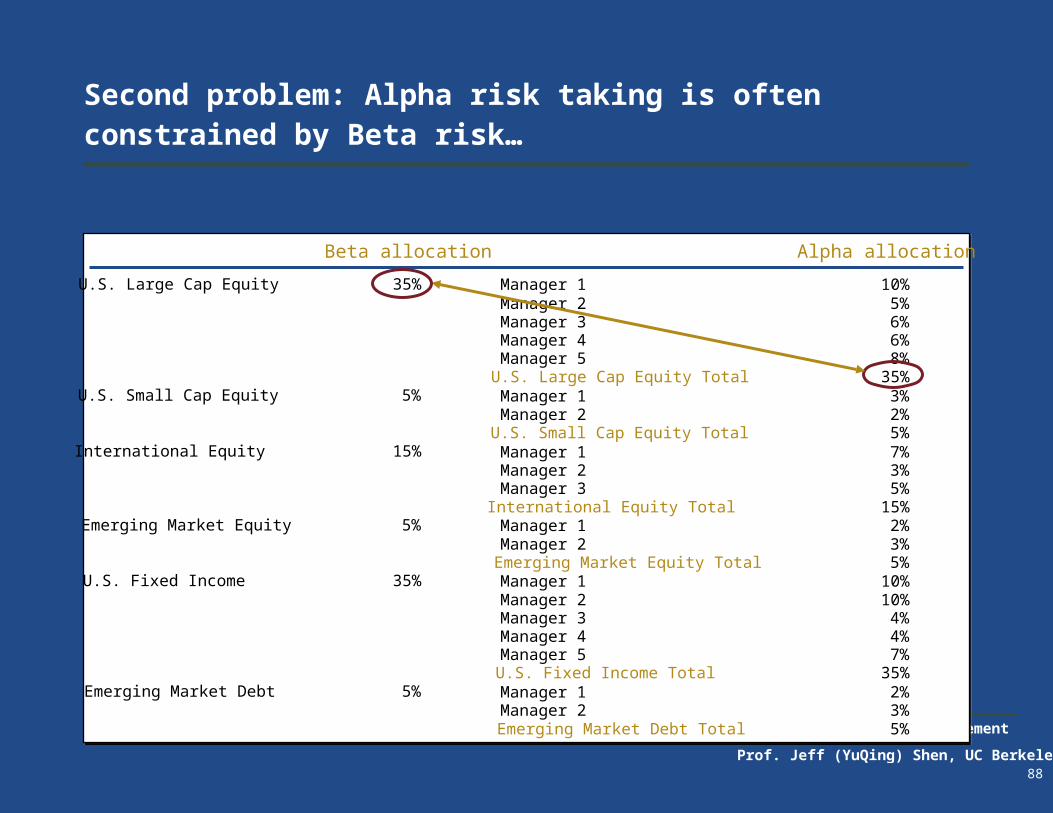

Second problem: Alpha risk taking is often constrained by Beta risk…

Beta allocation Alpha allocation

Manager 2 5%Manager 3 6%Manager 4 6%Manager 5 8%

U.S. Small Cap Equity 5% Manager 1 3%Manager 2 2%

U.S. Small Cap Equity Total 5%International Equity 15% Manager 1 7%

Manager 2 3%Manager 3 5%

International Equity Total 15%Emerging Market Equity 5% Manager 1 2%

Manager 2 3%Emerging Market Equity Total 5%

U.S. Fixed Income 35% Manager 1 10%Manager 2 10%Manager 3 4%Manager 4 4%Manager 5 7%

U.S. Fixed Income Total 35%Emerging Market Debt 5% Manager 1 2%

Manager 2 3%Emerging Market Debt Total 5%

U.S. Large Cap Equity 35% Manager 1 10%

U.S. Large Cap Equity Total 35%

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley89

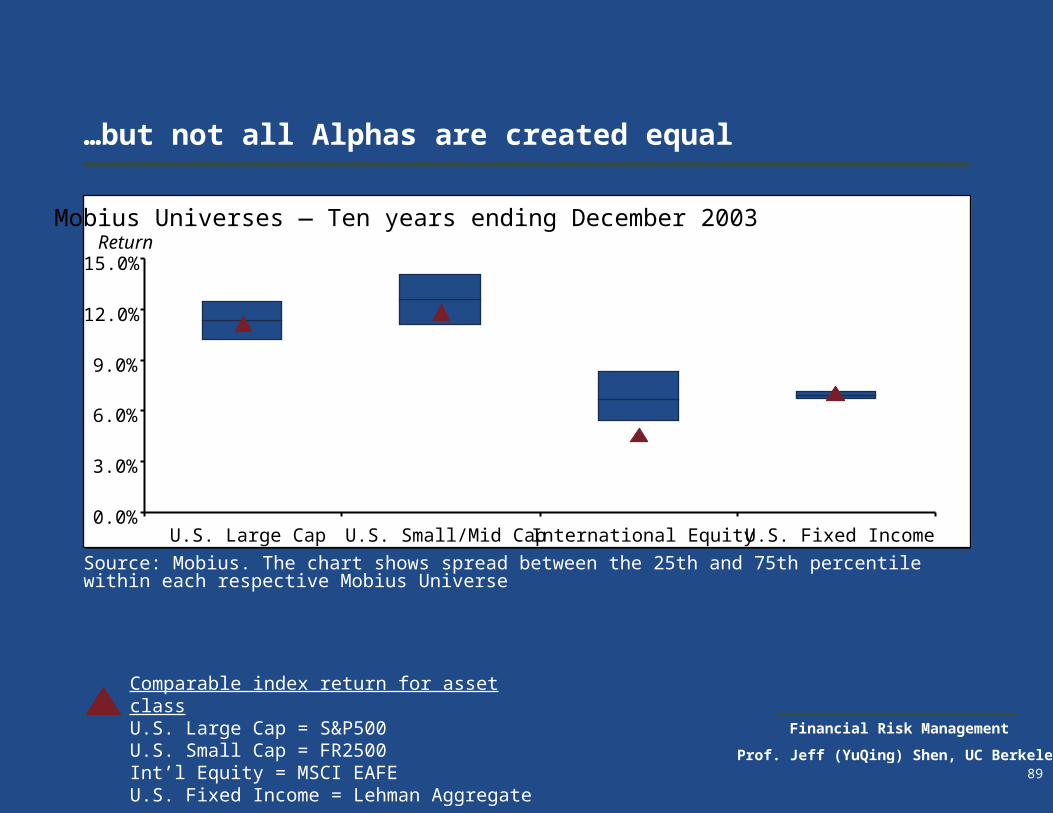

…but not all Alphas are created equal

Comparable index return for asset classU.S. Large Cap = S&P500U.S. Small Cap = FR2500Int’l Equity = MSCI EAFEU.S. Fixed Income = Lehman Aggregate

Source: Mobius. The chart shows spread between the 25th and 75th percentile within each respective Mobius Universe

Mobius Universes — Ten years ending December 2003Return

0.0%

3.0%

6.0%

9.0%

12.0%

15.0%

U.S. Large Cap U.S. Small/Mid Cap International Equity U.S. Fixed Income

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley90

…and dispersion is significant in alternative asset classes

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

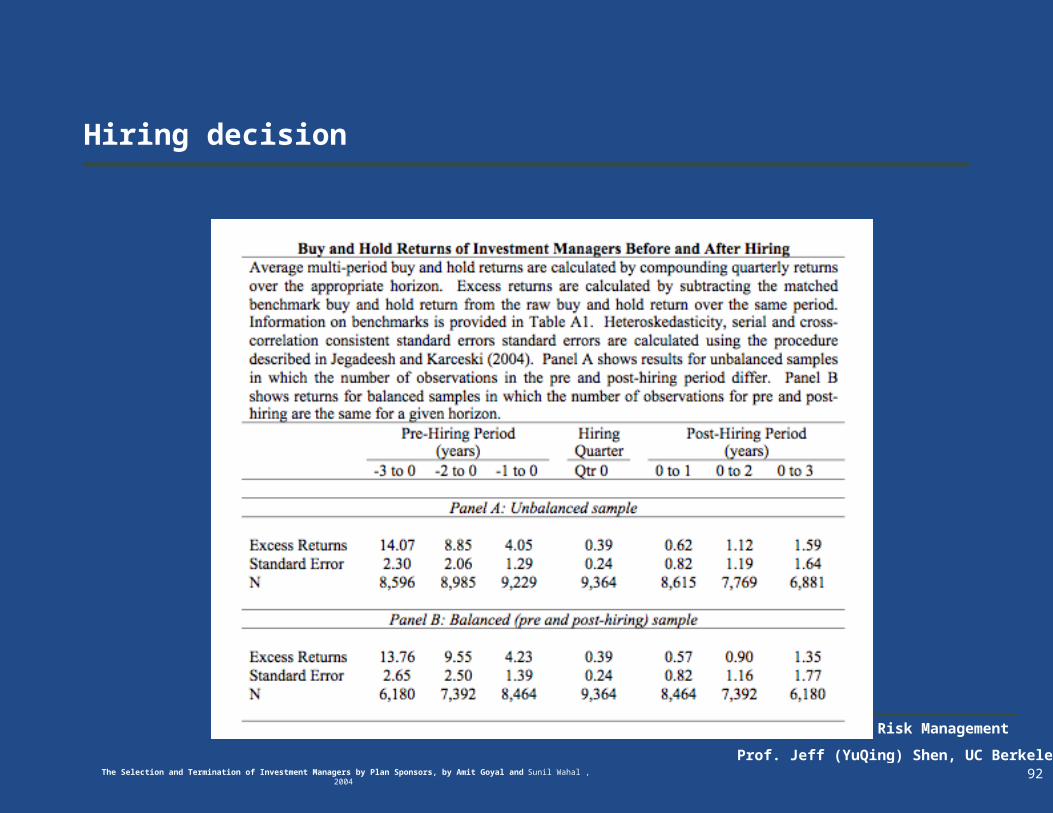

Persistence

We examine the selection and termination of investment managers by plan sponsors, representing public and corporate pension plans, unions, foundations, and endowments. We build a unique dataset that comprises hiring and firing decisions by approximately 3,700 plan sponsors over a 10-year period from 1994 to 2003. Our data represent the allocation of over $730 billion in mandates to hired investment managers and the withdrawal of $110 billion from fired investment managers. We find that plan sponsors hire investment managers after these managers earn large positive excess returns up to three years prior to hiring. However, despite general persistence in investment manager returns, this return chasing behavior does not deliver positive excess returns thereafter; post-hiring excess returns are indistinguishable from zero. Plan sponsors terminate investment managers after underperformance but the excess returns of these managers after being fired are frequently positive. Finally, using a matched sample of firing and hiring decisions, we find that if plan sponsors had stayed with fired investment managers, their excess returns would be larger than those actually delivered by newly hired managers.

91

The Selection and Termination of Investment Managers by Plan Sponsors, by Amit Goyal and Sunil Wahal , 2004

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Hiring decision

92The Selection and Termination of Investment Managers by Plan Sponsors, by Amit Goyal and Sunil Wahal , 2004

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Firing decision

93The Selection and Termination of Investment Managers by Plan Sponsors, by Amit Goyal and Sunil Wahal , 2004

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Comparison of hiring and firing

94

The Selection and Termination

of Investment Managers by

Plan Sponsors, by Amit Goyal

and Sunil Wahal , 2004

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley95

% a

lloca

tion

35%

5%

15%

5%

35%

5%

15%

10%

25%

20%

10%

20%

0%

5%

10%

15%

20%

25%

30%

35%

40%

U.S. Large

Cap Equity

U.S. Small

Cap Equity

International

Equity

Emerging

Market

Equity

U.S. Fixed

Income

Emerging

Market Debt

Beta allocationAlpha allocation

Liberate Alpha from Beta

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley96

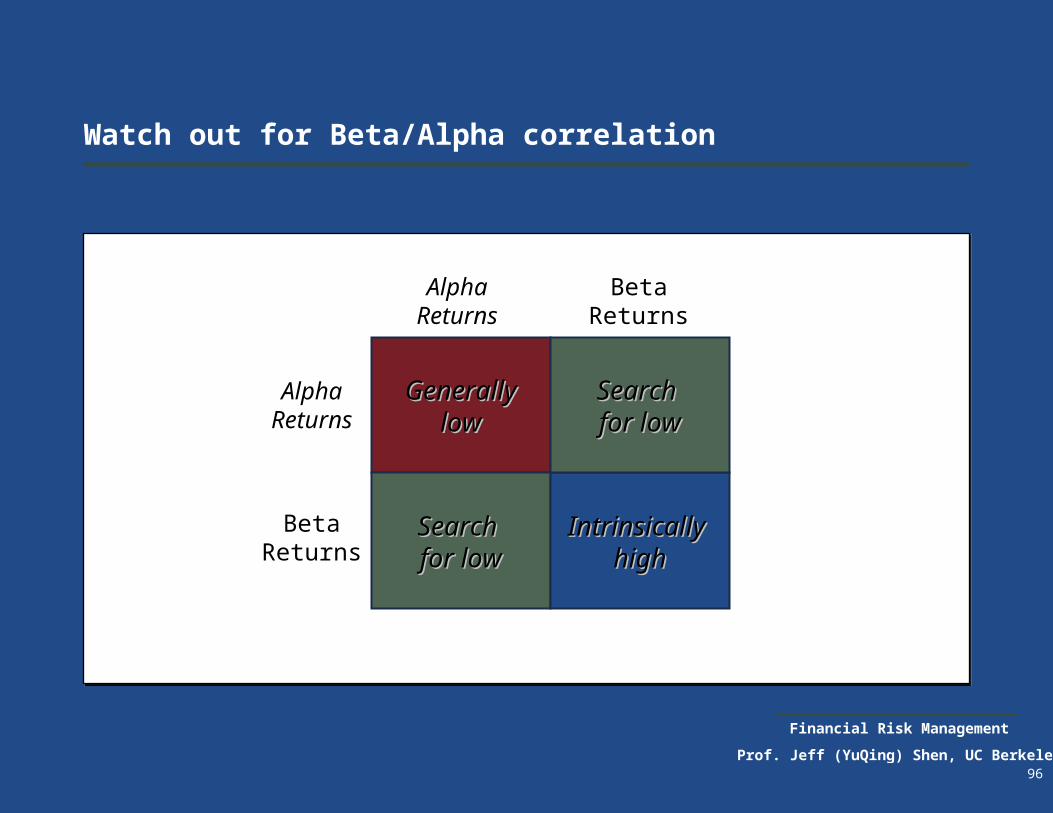

Watch out for Beta/Alpha correlation

GenerallyGenerallylowlow

Search Search for lowfor low

Intrinsically Intrinsically highhigh

Search Search for lowfor low

Alpha Returns

Beta Returns

Alpha Returns

Beta Returns

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley97

BetaBeta AlphaAlphaPortfolioReturn

Beta vs. Alpha framework

Diversify Beta risk

Liberate Alpha from Beta

…potential for more consistent portfolio return

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley98

The BIG Picture

• Theory

•Efficient Frontier

•Asset/Liability Framework

•Alpha/Beta risk budgeting

• Practice

•Pension Crisis

•GM Pension Plan

•Yale Endowment

• Theory

•VaR

•Stochastic behavior of asset

returns

•Worst case scenario

• Practice

•Investment bank VaR

•Bear Stearns

• The Theory

•Active Portfolio Management

•Quantitative equity models

•Hedge fund investment

• The Practice

•Hedge fund industry

•Aug 2007 crisis for quant

Investment BankInstitutional Investor Hedge Fund

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley99

Institutional investor risk management

US corporate defined benefit plans

Endowment and foundation

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley100

University of Illinois Endowment Investment Policy

The investment policy recognizes the long term nature of endowment funds and seeks to balance present and future support.

The investment objective is to preserve the real value, or purchasing power, of the endowment pool assets and the annual support provided by these assets for an infinite period. The endowment pool investment policy embraces the total return concept.

Total InvestmentReturn

Rate of PurchasingPower Loss

Spending Rate Real Asset GrowthRate

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley101

University of Illinois Endowment Investment Policy

The purpose of the spending rate formula is to provide a stable income stream that keeps pace with inflation and does not degrade the real value of the corpus of the endowment over time. Typically 5% in in the industry.

The rate of purchasing power loss is inflation. The primary inflation measure used to determine purchasing power is the Consumer Price Index.

The universe of comparison is the EK&A Endowment Fund Universe, which consists of the returns of approximately 274 endowments.

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley102

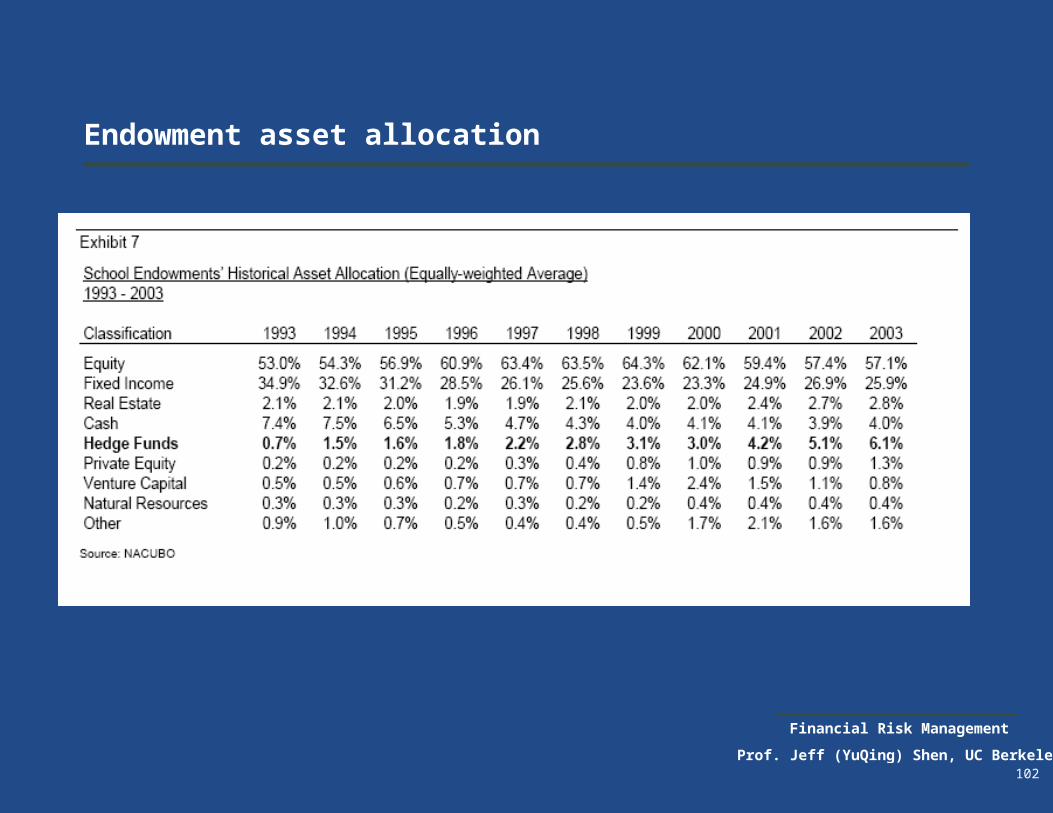

Endowment asset allocation

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley103

Case Study: Yale Endowment

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley104

Performance

*Source: Yale Endowment Annual Report 2008

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Endowment highlights

105

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Operating budget contribution

106

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Spending rate

107

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Peer comparison

108

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley109

Peer comparison

*Source: Yale Endowment Annual Report 2008

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley110

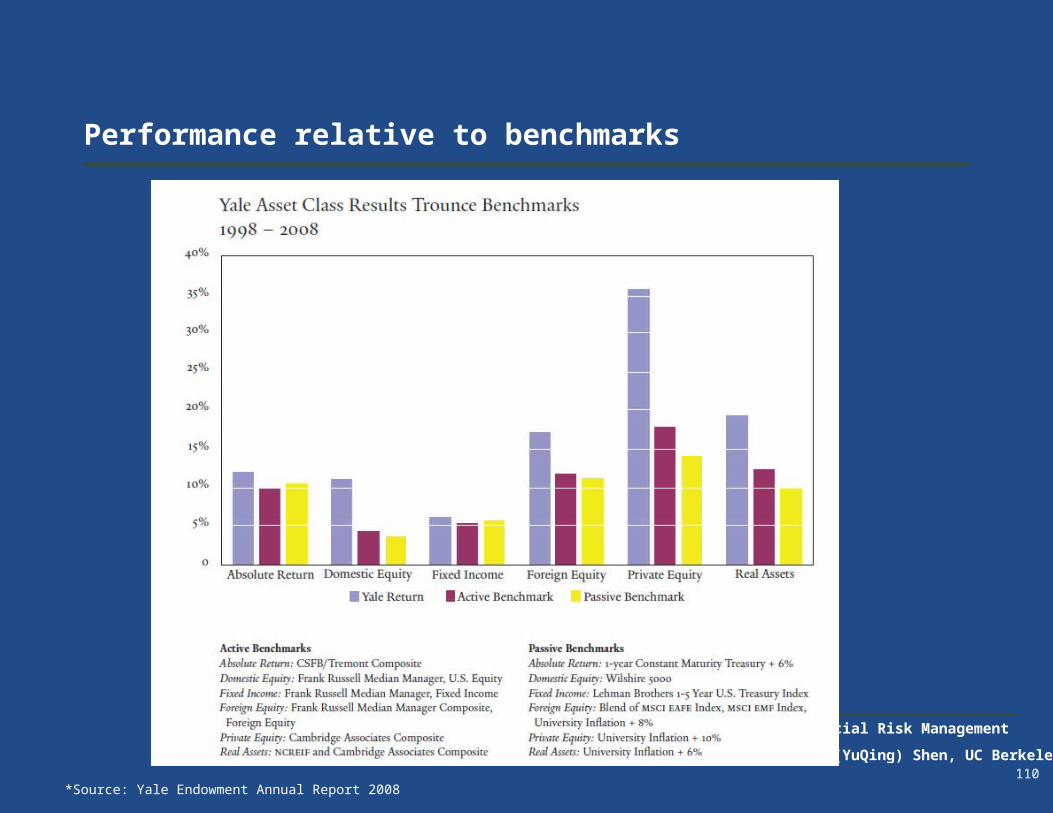

Performance relative to benchmarks

*Source: Yale Endowment Annual Report 2008

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Dispersion of active returns

111

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Dispersion of active returns

112

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley113

Historical asset allocation trends

*Source: Yale Endowment Annual Report 2005

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley114

Liquidity profile

*Source: Yale Endowment Annual Report 2005

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Yale Endowment Case Study Questions

What are the pros and cons of Yale Endowment investment style?

What are the key risk factors in Yale’s investment?

How does Yale manage its investment risk?

115

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley

Financial Risk Management

Prof. Jeff (YuQing) Shen, UC Berkeley117

The BIG Picture

• Theory

•Efficient Frontier

•Asset/Liability Framework

•Alpha/Beta risk budgeting

• Practice

•Pension Crisis

•GM Pension Plan

•Yale Endowment

• Theory

•VaR

•Stochastic behavior of asset

returns

•Worst case scenario

• Practice

•Investment bank VaR

•Bear Stearns

• The Theory

•Active Portfolio Management

•Quantitative equity models

•Hedge fund investment

• The Practice

•Hedge fund industry

•Aug 2007 crisis for quant

Investment BankInstitutional Investor Hedge Fund