sector intelligence: impact of covid-19

TRANSCRIPT

Sector Intelligence: Impact of COVID-19

LNG Industry

Updated: May 07, 2020

$9 trillion

Loss to global GDP 2020–21

Economic impact of 'great

lockdown’ (IMF)

$50+ billion

Reduction in CAPEX by oil &

gas majors, until March’20

~48%

Drop in average Brent price

(2020 vs 2019)

~9.1 MMT

Potential impact on LNG

demand in 2020 vs 2019 level

3.5%

(reduction in LNG demand from

2020 pre-COVID forecast)

(Scenario 1: Lockdown

extension until Q2’20)

$1.825/MMBTU

(Jun delivery)

New lows for JKM (on 28

Apr’20)

~60%

Drop in JKM price since early

2020

~$1.3/MMBTU

Lowest recorded tender price

(new low)

>110 MMT

Possible impact on FIDs in

2020

22+

Number of impacted

liquefaction projects

~87 MMT

Possible impact on supplies

(2020 vs 2030)

COVID-19: Potential Impact on LNG Industry

8%

(reduction in LNG demand from

2020 pre-COVID forecast)

(Scenario 2: Lockdown

extension until 2020-end)

COVID-19 could wipe off 13–30 MMT of LNG

demand in 2020. The industry is battling

depressed downstream demand, low prices,

high storage levels, and increased concerns

over the viability of projects and supply

cuts.

In the best-case scenario, Northeast Asia

will lead the demand recovery in H2’20, with

European storage space brimming with an

influx of cheaper LNG and piped gas.

3 © Evalueserve. All rights reserved.

Impact on LNG Demand

• Force majeure, DQT, and cargo deferment / cancellation requests

• Opportunistic buying and emergence of new buyers

• Demand recovery in China in H2’20

• Outline opportunistic versus strategic play frameworks for faster action

• Identify tier II and tier III players

• Develop China-focused strategy for expeditious Chinese player

Implication for Supply

• Threat to project viability amid low prices

• Cancellation of US cargoes and concerns over operability of US-based projects

• Depressed Asian demand and record storage levels in Europe

• Increased competition with dwindling demand

Outlook for Pricing

• Record fall in LNG pricing

• Tightened operational flexibility

• Eluding long-term contracts

Things to Watch Out For

• Market optimistic about Asia leading demand recovery in 2021

• Threats over projects financing and long-term commitment (s)

COVID-19: Implications and Way Ahead

The COVID-19 pandemic has led to demand destruction, record low pricing, and concerns over the viability of liquefaction projects. Global LNG trade is likely to register single digit or even negative growth in 2020 – compared with ~13% growth in 2019.

COVID-19: Evalueserve Recommendation

• Cut costs fast

• Consider LNG sourcing from other players

• Explore new sales horizon

• Review long-term capex plans in light of increased competition

• Optimize cross-basin sales

• Review shipping routes and storage space optimization

• Adopt innovative pricing mechanisms to secure greater term deals

• Engineer developments in markets for long-term plays

• Scout for activity in nascent markets and new buyers (including buyers

looking to switch from bunkering or coal fuels)

4 © Evalueserve. All rights reserved.

Japan

South Korea

India

ChinaSpain

Turkey

Italy

France

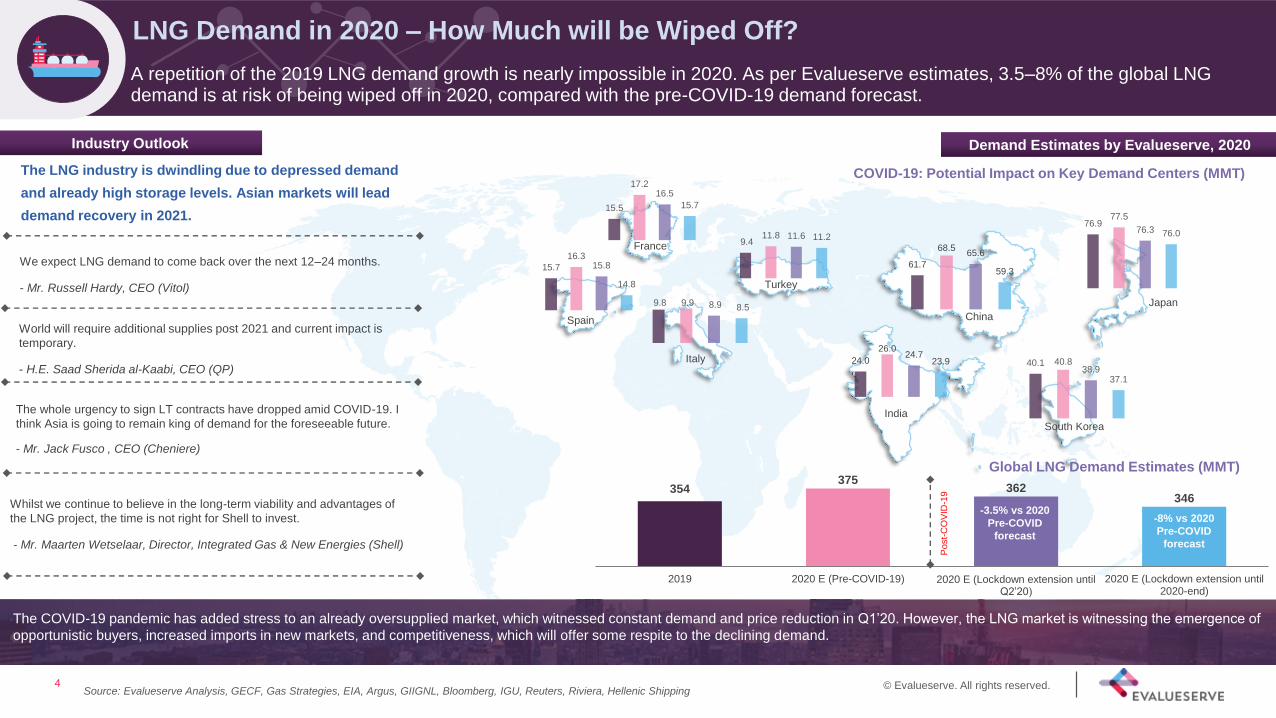

Industry Outlook

The LNG industry is dwindling due to depressed demand

and already high storage levels. Asian markets will lead

demand recovery in 2021.

Global LNG Demand Estimates (MMT)

We expect LNG demand to come back over the next 12–24 months.

- Mr. Russell Hardy, CEO (Vitol)

World will require additional supplies post 2021 and current impact is

temporary.

- H.E. Saad Sherida al-Kaabi, CEO (QP)

The whole urgency to sign LT contracts have dropped amid COVID-19. I

think Asia is going to remain king of demand for the foreseeable future.

- Mr. Jack Fusco , CEO (Cheniere)

Whilst we continue to believe in the long-term viability and advantages of

the LNG project, the time is not right for Shell to invest.

- Mr. Maarten Wetselaar, Director, Integrated Gas & New Energies (Shell)

354375

362346

2019 2020 E (Pre-COVID-19) 2020 E (Lockdown extension until Q2’20)

2020 E (Lockdown extension until2020-end)

COVID-19: Potential Impact on Key Demand Centers (MMT)

Demand Estimates by Evalueserve, 2020

Post-

CO

VID

-19

76.9 77.5

76.3 76.0

40.1 40.8 38.9

37.1

61.7

68.5 65.6

59.3

24.0

26.0 24.7

23.9

9.4 11.8 11.6 11.2

15.5

17.2 16.5

15.7

9.8 9.9 8.9 8.5

15.7

16.3 15.8

14.8

Source: Evalueserve Analysis, GECF, Gas Strategies, EIA, Argus, GIIGNL, Bloomberg, IGU, Reuters, Riviera, Hellenic Shipping

The COVID-19 pandemic has added stress to an already oversupplied market, which witnessed constant demand and price reduction in Q1’20. However, the LNG market is witnessing the emergence of

opportunistic buyers, increased imports in new markets, and competitiveness, which will offer some respite to the declining demand.

-3.5% vs 2020

Pre-COVID

forecast

-8% vs 2020

Pre-COVID

forecast

LNG Demand in 2020 – How Much will be Wiped Off?

A repetition of the 2019 LNG demand growth is nearly impossible in 2020. As per Evalueserve estimates, 3.5–8% of the global LNG demand is at risk of being wiped off in 2020, compared with the pre-COVID-19 demand forecast.

5 © Evalueserve. All rights reserved.

Macroeconomic Industrial Gas Market

Power Demand LNG Activities

1 2 1 2

Scenario 1: Lockdown extension until Q2’20

Scenario 2: Lockdown extension until 2020-end

1

2Low impact on LNG Demand

Medium impact on LNG Demand

Significant impact on LNG Demand

No

rth

east

Asia

No

rth

east

Asia

Eu

rop

e

Eu

rop

e

1 2 1 2

Ind

ian

Su

b

co

nti

nen

t

Scenario 1: Rapid recovery of power

demand from C&I sectors

Scenario 1 & 2: CCGTs to become

competitive to coal

Europe’s recovery to be the slowest in

both cases

India to become fastest growing major

economy in Scenario-1

China’s GDP growth rate may fall to 1%

in Scenario-2

Scenario 1: Best for economic revival

Modest recovery in both scenarios

Scenario 1: High productivity after

lockdown

Industrial production very less

Scenario 1 & 2: Power generation to

remain abundant with high share of

nuclear & renewables

Scenario 2: Delay in LNG-to-Power

projects

Scenario 2: Prolonged high storage

levels

Scenario 1: Rise in Tender activity (vs

Mar’20) with increased LNG viability

Caribbean and Brazil to offer some

respite

Scenario 1: Rapid recovery of power

demand from C&I sectorsScenario 1: Jump in industrial production

index

Scenario 2: Loss of industrial productivity Scenario 2: Coal-to-gas switching to be

delayed to sustain economy

Current Impact

on Demand,

by Region

No

rth

east

Asia

Ind

ian

Su

bco

nti

nen

tR

OW

RO

W

Demand Recovery Outlook

1 2

Lockdown until Q2’20 Lockdown until

2020-end

No

rth

east

Asia

No

rth

east

Asia

Eu

rop

e

Eu

rop

eIn

dia

n

Su

bco

nti

nen

t

Source: Evalueserve Analysis, IMF, Bloomberg, IEA, EIA, Argus, GIIGNL, GECF, IGU, Reuters, Riviera, Natural Gas Intel, Hellenic Shipping

The shaded portion indicates a

possible positive impact on demand

recovery.

Ind

ian

Su

bco

nti

nen

tR

OW

Eu

rop

eN

ort

heast

Asia

LNG Demand Recovery in 2020 - A Myth or Possibility?

LNG demand recovery in 2020 remains unlikely, unless normalcy returns by the end of Q2’20. Northeast Asian countries will likely absorb most of the excess LNG this year and the market will start rebalancing in 2021.

Scenario-1 (China) – Emergence of

new buyers with greater regas access

Opportunistic buying in both cases.

Cargoes deferral to Singapore/Thailand

6 © Evalueserve. All rights reserved.

These threats will add to the bearishness of European

gas prices, thereby offering cross-basin supply

opportunities for LNG suppliers

Threat from Piped Gas

Higher piped gas supply

may further pose risk to

LNG imports in 2020

Threats from Nuclear &

Renewables

Several European nations

may prefer to reduce gas-

based power output to

maintain grid balance

Near-full Storage Levels

(~96% in Aug’20)

LNG imports could be

lower than the earlier

estimate of 100 MMT in

2020

Declining Gas Demand

4–10% of Europe’s gas

demand may be impacted in

H1’20

Scenario #1: Lockdown extension until Q2’20

Scenario #2: Lockdown extension until 2020-end

THREATS TO EUROPEAN BACKSTOPS

European Storage Levels (Between Jan-Apr)

• 5-year average = 42.4%

• 2020 = 64.9%

European Gas Storage Levels vs Utilisation Forecast

Will Europe Continue to be the Preferred Backstop?

With record storage levels already achieved in Q1’20, the outlook for Europe absorbing excess LNG in 2020 remains ‘bleak’. However, opportunistic buying in Turkey and underutilized storage facilities in Ukraine may offer some respite.

Source: Evalueserve Analysis, GIE, EIA, Argus, GIIGNL, GECF, IGU, OIES Analysis, Naftogaz, Riviera, Natural Gas Intel, Hellenic Shipping

Note: Assuming storage injection average of 10 BCM/month. 1 BCM = 10.46 TWh

10

20

30

40

50

60

70

80

90

100

0

20

40

60

80

100

120

140

160

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

in %BCM

Average Storage Levels (2018) Average Storage Levels (2019)

Average Storage Levels (2020) % Full (5-year average) (RHS)

% Full (2020) (RHS) % Full Storage Levels Forecast (Scenario 1) (RHS)

% Full Storage Levels Forecast (Scenario 2) (RHS)

7 © Evalueserve. All rights reserved.

Exporting nations (particularly dependent on petroleum exports) are facing tightened

finances with lower oil & gas prices

Double blow on economy

EXPORTING COUNTRIESIMPORTING COUNTRIES

Low LNG prices have raised concerns over the viability of multiple LNG projects

(both operational and proposed)

Supplies cuts and greenfield project deferrals / cancellation

Suppliers across the globe are facing competition and are looking to expand

beyond their traditional markets. NOCs need to market their cancelled cargoes in

the spot market

Increased competition for supplies

Most of the term deliveries across Asian countries are signed at a high Brent

slope. A fall in Brent prices could result in ~50% reduction in DES cost for

deliveries in H2’20.

Reduction in import bill

A drop in spot / term prices could significantly reduce the cost of electricity

generation using LNG across key demand centres such as India.

LNG becoming cost-competitive with other fuels

Lower LNG prices could mean that it is becoming increasingly viable as

feedstock across industries and for CGD use.

Greater LNG downstream demand

-

20

40

60

80

Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021 Q2 2021

$/BBL Brent Price Outlook

Note: Term contracts prices calculated based on 3-months average Brent prices

Source: Evalueserve Analysis, Bloomberg, Argus, GIIGNL, GECF, IGU, Reuters, Natural Gas Intel, Hellenic Shipping

0

5

10

15

Jan Mar May July Sep Nov Jan Mar May July Sep Nov Jan Mar May July Sep Nov Jan Mar May July Sep Nov

2018 2019 2020 2021

$/MMBTU Term vs Spot Price Forecast

14.5% Brent Slope (Term) JKM

What Does a Fall in LNG Prices Mean for the Market?

Lower LNG prices will increase LNG’s competitiveness to ‘coal’ and boost its relevance as ‘feedstock’. However, suppliers will need to undertake production curbs as well as defer planned projects, to ensure business continuity and initiate market re-balance.

8 © Evalueserve. All rights reserved.Source: Bloomberg, OilPrice, EIA, OIES Analysis, GIIGNL, Rystad, IGU, Reuters, CME Group, GECF

200

300

400

500

600

700

800

900

1000

2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

MMT

Pre-COVID-19 Liquefaction Capacity Post-COVID-19 Liquefaction Capacity

Impact of COVID-19 & low oil price

~87 MMT lower liquefaction capacity

addition by 2030

Rising Concerns about:

Deferral / Cancellation of 2nd Wave of

US LNG projects

Viability of backfill Australian projects

New Greenfield investments

Bearish oil & gas indicators in 2020 (post COVID-19) have not only raised concerns

over the viability of operational projects but will also delay / defer most of the FIDs

in 2020

Covid-19: Potential Impact on LNG Supplies vs Capacity Additions

QatarDetermined to maintain its ‘Leader’ status

Set to achieve FID of ‘NFE’ project by early 2021

Russia

Strong government support

Government targeting greater LNG integration, will

support FIDs/operability of major LNG projects

Asia

Major threat to Brownfield expansion

Low oil prices to defer / delay most of the backfill LNG

projects (particularly across Australia)

US

Threat to Second Wave Projects

Lack in investor confidence and commitments, rising

concerns over viability of operational and planned

projects

Ne

t C

ost

of

LN

G o

f O

pera

tio

na

l P

roje

cts

Low

High

Category 1 Category 2

Category 1 Category 2

Category 1 Category 2

Category 1 Category 2

Net CLNG Range - GlobalNet CLNG Range - Region

Can Suppliers Maintain Liquefaction Capacity Growth?

Over 110 MMT of planned FIDs in 2020 are expected to be affected by the global pandemic. With gas prices facing headwinds, the viability of production from several US-based and a few Asian projects remains a concern.

9 © Evalueserve. All rights reserved.

Least Impacted Least Impacted

Threat - High net cost of LNG,

strategically focused on oil market,

and greater greenfield investments

Highest Impact Least ImpactHigh Impact Moderate Impact

Traders

Portfolio

PlayersLNG

Marketers NOCs

Strategy / Guidance

• Optimize finances & portfolio

management

• Manage LNG portfolio risk

• Optimize shipping and storage

space, cargo reshuffle

• Proceed only with marquee

projects while delay others

Strategy / Guidance

• Undertake ‘Production cuts’

• Be open to procuring LNG than to

producing themselves

• Target nearby markets

• Manage and restructure debt

Threat – Cargo cancellations (most

US players), greater dependence on

spot, and delay in term deals

Threat – ‘Tank-top’ or Force Majeure

requests

Threat – Low arbitrage

opportunities amid price drop, and

limited storage capabilities

Strategy / Guidance

• Explore new market while pushing

greater LNG to Europe

• Leverage the low cost of LNG to

market deferred cargoes on spot

basis

• Defer maintenance and maintain

high productivity

• Continue brownfield projects

Strategy / Guidance

• Optimize cross-basin sales

• Leverage trading prowess

• Explore alternative opportunities

such as storage space trading

Source: Bloomberg, IEA, EIA, Argus, GIIGNL, GECF, IGU, Reuters, Riviera, Natural Gas Intel, Hellenic Shipping

Note: Strategy / Guidance represents Evalueserve’s views on the steps that the value-chain players could take to sustain top line.

With LNG price markers continually recording new lows, LNG production cuts look eminent. High exposure to the oil market, coupled with greater net LNG costs, are putting portfolio players at the risk of giving up early to the dwindling LNG demand.

Impact on LNG Suppliers – Who will Blink First?

10 © Evalueserve. All rights reserved.Source: Evalueserve Analysis, IEA, Gas Strategies, Evalueserve Insights, GasMalaysia, IGU, LNG World News, Petroleum Economist, HC Processing, GIIGNL

Key Lookouts For LNG Suppliers That May Support Demand Growth

Emergence of non-NOC

players in China

Addition of new

geographies

LNG-to-Power

developments

Pipeline Connectivity in

Asian nations

Direct Procurement by

downstream LNG users

Snowball effect in

Bunkering

Asia Europe & Middle East

AmericasAfrica

POTENTIAL MARKET FOR EXPANSION / INCREASED LNG SUPPLY

Senegal Benin

Ghana Cote d’Ivoire

South Africa Mauritius

El Salvador Nicaragua

Ecuador Cote d’Ivoire

Puerto Rico Brazil

Philippines Vietnam

Singapore Thailand

Cambodia Bangladesh

Cyprus Bahrain

Hungary Bulgaria

Ukraine Slovenia

Emergence of Potential LNG Buyers

Northeast Asian Buyers Others

Third-party Access (China)

• Sanhe Penghao Gas Co., Ltd.

• Zhenhua Oil

• Shengli Oilfield Tianyuan

• Longkou Shenton Energy

• Shandong Zhongnuo

Others

• Zhejiang Energy

• Guangdong Yudean

• Gas Malaysia Energy

• ENN

• SBEE

• Ghana National Petroleum Company

• New Fortress Energy

Our Take:

Evalueserve has identified multiple other

gas value chain players that may secure

spot volumes in the short term and may

even sign term deals in the long run. The

cumulative objective is to promote cleaner

fuel use at competitive pricing.

In the long run, with increased availability and competitiveness of LNG with other fuels, new markets and new buyers are set to join the LNG game. COVID-19 provides the much-needed time for suppliers to re-strategize and gain an ‘early bird’ advantage to increase sales.

Is There Any Silver Lining?

11 © Evalueserve. All rights reserved.

Author (s)

Yashika Vats

Group Manager, Oil & Gas

Contact Yashika: [email protected]

Pritam Singh

Senior Analyst, Oil & Gas

Contact Pritam: [email protected]