sector study on tea - amazon simple storage …s3.amazonaws.com/zanran_storage/ · the sector study...

TRANSCRIPT

NEPAL

ADVISORY SERVICES ON EXPORT DEVELOPMENT OF PRIORITY SECTORS OF NEPAL

SECTOR STUDY ON TEA

June - September 2007

MAHINDA WARAKAULLE International Consultant on Tea

RAMESH MUNANKAMI

National Consultant

BASTIAAN BIJL Trade Consultant – Market Information, Market Analysis and Training

Project NEP/A1/01A A project financed by the EU and ITC under the Asia Trust Fund

Page ii

While efforts have been made to verify the information contained in this document, the International Trade Centre UNCTAD/WTO cannot accept responsibility for any errors that it may contain. The views expressed in this report can in no way be taken to reflect the official opinion of the European Union, the Trade and Export Promotion Centre and ITC. The usual disclaimers regarding responsibilities apply to this report.

Page iii

Preface This sector study is part of the Technical Cooperation Project “Advisory services on export development of priority sectors of Nepal” (NEP/A1/01A). The project is implemented by the International Trade Centre UNCTAD/WTO (ITC) and the Trade and Export Promotion Centre (TEPC), and co-funded by the European Union and ITC through the Asia Trust Fund (ATF). The project is intended to identify products that show good export potential, taking demand and supply side issues into account, and to formulate practical recommendations for the development of Nepal’s most promising exportable products, with a view to develop and diversify Nepal’s export potential. The project consists of two phases. The first phase of the project consisted of a comprehensive Export Potential Assessment, looking into the export potential of 14 non-traditional products. During the second phase the five most promising are studied in more detail, engaging international product specialists. The results of the Export Potential Assessment were presented to representatives of Nepal’s private sector, Government and donor community in February 2007. Following this meeting it was decided to study the following products in more detail during the second phase of the project: large cardamom, pulses, Chyangra cashmere and silk products, floriculture and tea. The present study must be seen in this context. The sector study on Tea was prepared by Mr. Mahinda Warakaulle (International Consultant on Tea), Mr. Ramesh Munankami (National Consultant), who conducted a number of interviews with enterprises concerned in Nepal, and Mr. Bastiaan Bijl (International Trade Data Analyst). The sector study builds on the results of a fact-finding and needs-assessment mission conducted in Nepal in June 2007 (see Annex I for mission programme). During this mission, the ITC Consultant entertained a number of meetings with individual companies, exporters, producers, traders, government officials, and business associations. The main findings and recommendations of the report were consequently presented to - and validated by - key sector stakeholders during a workshop in Kathmandu in August 2007. The authors would like to thank Mr. Koen Oosterom, Office for Asia-Pacific, Latin America & the Caribbean (OAPLAC), ITC, for his support. Lastly, the authors would like to thank all enterprises concerned who kindly answered the ITC questionnaire and key sector stakeholders who engaged in meaningful discussions with the team and volunteered their views and knowledge. For further details on the present study, please contact Mr. Koen Oosterom (email: [email protected]).

Page iv

Abbreviations and Acronyms Used ADBN Agriculture Development Bank of Nepal AEC Agro - Enterprise Center ATF Asia Trust Fund CoC Code of Conduct COP Cost of production CTC Cut, tear and curl DOA Department of Agriculture FCL Full container load FNCCI Federation of Nepalese Chamber of Commerce and Industry GL Green leaf HACCP Hazard Analysis and Critical Control Point HIMCOOP Himalayan Tea Producers Cooperative HOTPA Himalayan Orthodox Tea Producers Association ISO International Standards Organization ITC International Trade Centre MOA Ministry of Agriculture MOC Ministry of Commerce MOF Ministry of Finance MOI Ministry of Industries PAC Pakribas Agriculture Centre (Research) PE/PP Polyethylene/polypropylene MRL Maximum residue level NARC Nepal Agriculture Research Council NASAA National Association of Sustainable Agriculture of Australia NPC National Planning Commission NR Nepal rupee NTCDB Nepal Tea and Coffee Development Board NTDC Nepal Tea Development Corporation NTA Nepal Tea Association NTPA Nepal Tea Planters Association SAARC South Asian Association for Regional Cooperation SAFTA South Asian Free Trade Agreement TEPC Trade and Export Promotion Centre Terai Low level land mass SP Selling price

Page v

Table of Contents Preface .................................................................................................................................. iii Abbreviations and Acronyms Used ................................................................................... iv Table of Contents.................................................................................................................. v 1. General Context and Executive Summary........................................................ 7 1.1 Background and Objective ..................................................................................................7 1.2 Coverage of the Study ........................................................................................................8 1.3 Parties involved...................................................................................................................8 1.4 Key Findings: Obstacles and Short Comings .....................................................................8 1.5 Recommendations ............................................................................................................10 2. The tea Industry in Nepal ................................................................................. 16 2.1 The Sector in General .......................................................................................................16 2.2 The global tea market .......................................................................................................18 2.2.1 Overview of world production and trade ...........................................................................18 2.2.2 Trends in world consumption ............................................................................................24 2.3 Export of tea from Nepal ...................................................................................................24 2.3.1 Growth in national tea exports ..........................................................................................24 2.3.2 Export of tea to India .........................................................................................................25 2.3.3 Export of tea to countries other than India ........................................................................26 2.4 Tea production in Nepal ....................................................................................................27 2.4.1 Growth in tea cultivation and production...........................................................................28 2.4.2 Type of tea produced ........................................................................................................29 2.4.3 Yield and Cost of Production (COP) .................................................................................30 2.4.4 Geographical distribution of production ............................................................................31 2.4.5 Crop diversification............................................................................................................31 2.5 Tea development ..............................................................................................................32 2.6 Processing of Tea .............................................................................................................33 2.6.1 Basic household units .......................................................................................................33 2.6.2 CTC processing units:.......................................................................................................34 2.6.3 Orthodox tea factories:......................................................................................................34 2.7 Availability of raw material, price and quality ....................................................................35 2.8 Rules, regulations and standardization in the sector ........................................................38 2.9 Quality and international competitiveness ........................................................................38 2.10 Existing studies, strategies and policy papers in the sector .............................................39 2.11 Socio Economic Impact of the Sector ...............................................................................41 2.12 SWOT Analysis .................................................................................................................43 3. Bilateral, Regional and Multilateral Trade Agreements................................. 44 3.1 Bilateral agreements .........................................................................................................44 3.2 Transit Agreements...........................................................................................................44 3.3 Regional Trade Agreements .............................................................................................44 3.4 Pertinent provisions under the WTO agreements.............................................................45 3.5 Implications of these agreements for the sector in Nepal: ................................................46 4. Obstacles and shortcomings for exports....................................................... 48 4.1 At the Farmers and Company Level .................................................................................48 4.2 The enabling environment, both public and private ..........................................................48 5. Export Services in Nepal.................................................................................. 50

Page vi

5.1 The Government Institutional Supports ............................................................................50 5.2 The Private Agencies and NGOs......................................................................................51 6. Recommendations and Action Plan................................................................ 54 6.1 Recommendations for farmers, producers and exporters ................................................54 6.2 Recommendations for the business environment.............................................................57 6.3 Micro-level action plan ......................................................................................................58 6.4 Meso-level action plan ......................................................................................................59 6.5 Macro-level action plan .....................................................................................................60 6.6 Prioritization of action plan – If we have a million ….........................................................61 6.7 Conclusion.........................................................................................................................68 Annex I: Timetable of Meetings and Activities: .....................................................................................69 Annex II: geographical distribution of tea cultivation.............................................................................72 Annex IV: List of contacts in main two potential markets......................................................................75 Annex V: Flow chart ..............................................................................................................................77 Annex VI: Guidelines for good leaf standards and processing.............................................................78 Annex VII: Composition of a typical tea beverage ................................................................................79 Tables Table 2.1 - International trade in tea .....................................................................................................19 Table 2.2 - Production of Tea according by CTC/Orthodox in various countries, 2005 .......................19 Table 2.3 - Major Importers of black tea in bulk....................................................................................21 Table 2.4 - Major Importers of black tea in <3kg packages..................................................................22 Table 2.5 – Pakistan’s Imports of black tea- mainly CTC in bulk, 2003-2006 .....................................23 Table 2.6 - Major Importers of green tea in bulk...................................................................................23 Table 2.7 - Major Importers of green tea in <3kg packages .................................................................24 Table 2.8 - Growth in cultivation and trade of Nepalese tea.................................................................25 Table 2.9: Export and Import of Tea from/to Nepal to India (Q in Kg., Value in ‘000Rs.).....................25 Table 2.10 - Export of Nepal Black and Green to other countries except to India................................27 Table 2.11: Total Tea Production and Tea Plantation Area..................................................................29 Table 2.12 - Type of tea produced 2005/06..........................................................................................29 Table 2.13 - Geographical distribution of production ............................................................................31

Page 7

1. General Context and Executive Summary 1.1 Background and Objective Nepal is a landlocked country with a highly literate population of 28 million, with land area of 147,181 sq km that stretches 885 km from east to west. It enjoys diverse weather and climatic conditions where the topography ranges from 305 m to 8848 m altitude, about 70% hilly areas having ideal conditions for agriculture development and crop diversification. Administratively, the country is demarcated into 5 development regions, 14 zones and 75 districts whilst ecologically it can be divided into the mountain, hill and lower or Terai regions. Over the years the importance of some agricultural crops such as paddy and jute have declined sharply due to loss of export markets and farmers changing to other cash crop and to tea cultivation which seem to be more remunerative and eco friendly. Currently, Nepal depends heavily on exports of hand woven carpets and ready made garments which bring in nearly 60% of their annual export earnings. With the phasing out of the Multi Fibre Agreement from 1st January 2005 and the decline in export demand for the carpets, the significance of these two major items, which dominated the export sector, is declining and facing increased threats. India is the main trading partner of Nepal and the official figures indicate that 68% of export and 67% of import trade of Nepal is with India. If the unofficial figures are added on, these percentages will be above 80. This dependence makes the economy of Nepal vulnerable. The decline in their rice and jute exports, dependent mainly on this one market caused these two items to lose their importance as a sustainable agriculture commodity bringing in earnings to the rural farmers. Against this background, the Government of Nepal requested the support of the Asia Trust Fund to identify products that show good export potential, taking demand and supply side issues into account, and to formulate practical recommendations for the development of Nepal’s most promising exportable products, with a view to developing and diversifying export business. This study is in the spirit of a quest to diversify and lift Nepal’s exports away from its overdependence on Carpet and Clothing exports. A comprehensive Export Potential Assessment looked into 14 non-traditional product sectors and five sectors were identified as having high potential for further export development. Further in-depth studies were conducted on the five product sectors that included large cardamom, lentils, tea, Pashmina and silk based products, and floriculture products. This document covers the study on Tea. An immediate purpose of the study is to assess the export promotion potential of tea products and to present the findings, conclusions and recommendations at a roundtable meeting of stakeholders that will validate the main findings and endorse a future course of action. The objectives of this study are to identify the priorities for export policies, determine the strategies, recommend practical action programmes and provide guidance to the government, the private sector and the donor agencies for the export development and promotion of tea from Nepal.

Page 8

1.2 Coverage of the Study The study on tea focuses on supply side issues, backward and forward linkages, buyer requirements, trade data, obstacles and shortcomings for export, export support services, implications of regional and multilateral agreements and the recommendations with action plan. The coverage of the study includes:

- Overview of the sector and opportunities - Key obstacles and shortcomings for export - Consequences of multilateral, regional and bilateral trade agreements on the

sector - Export Services in Nepal of interest to the sector - Action Plan for further development of the sector. - Wise spending on recommendations for future projects – “If we had a

million....”

1.3 Parties involved The major parties involved in the study are the Government of Nepal, the European Union, the International Trade Centre UNCTAD/WTO, and the Trade and Export Promotion Centre (TEPC). The other responsible supporting agencies for the programme or project implementation are the Ministry of Industries, Commerce and Supplies, Ministry of Agriculture and Cooperative, Department of Agriculture, Nepal Agriculture Research Council, Nepal Tea and Coffee Board (NTCDB), Agro-Enterprise Centre of Federation of Nepalese Chambers of Commerce and Industries (FNCCI), Local Chamber of Commerce and Industry, Bilateral and Multilateral Donor Agencies, Himalayan Orthodox Tea Producers Association (HOTPA), the Nepal Tea Planters Association (NTPA), the Nepal Tea Association (NTA), Himalayan Tea Producers Cooperative (HIMCOOP). 1.4 Key Findings: Obstacles and Short Comings This report highlights the current obstacles and shortcomings in production, processing and marketing, focusing on the areas that need be improved so that Nepal tea can gain a firm foothold in the international tea market both for quality and supplies. Shortcomings for Exports: Shortcomings or gaps for export are the factors missing – and which could facilitate existing and potential export.

a) The past efforts of all stakeholders have helped increase the production of green leaf at small farmers, cooperatives and tea estates. But the processing capacity has not developed to cope with the increased production of green leaf. As a result, Nepal’s tea sector is selling raw materials to Indian factory instead of value adding in the country and exporting the finished tea. Additional processing facilities will thus help increase Nepal’s tea export. On the other hand, the recent restriction imposed by India in the imports of green leaf from Nepal has raised a serious fear among the farmers, specially the small farmers, which may be detrimental to this sector.

Page 9

b) Certifications and test reports on the products from accredited laboratories/ authorities are not available.

c) Accredited and equipped laboratory not available to test and analysis of samples for exports. Many buyers and countries require test reports on residue level, heavy metal, radiation clearances with each consignment. Orders are held up for long periods till the results are released from laboratories overseas.

d) Insufficient product diversification to interest buyers of speciality range of teas into niche markets.

e) No brand image still built to make global buyers aware of Nepal tea and their quality.

f) Only small parcels of lots are available to be offered out. No blending or mixing facilities available to cater to the demands of buyers who require bigger consignments. Inconsistent quality and non-uniformity of products with no supportive certificates causing difficulties to make good blend mixes.

g) No central marketing facility, such as an auction market to attract sellers and buyers to one location.

h) Lack of human resources and professionally qualified and experienced personnel to promote tea sector. And there is no institutional setup that generates such human resources in the country.

i) No market information system available to give guidance to exporters on current trends, price movements in other auction centres, changes in consumption habits, etc

j) Facilities to add value to the basic product are not available. This has been due to the overdependence on Indian exporters and marketers performing this function using blend mixes of both origins with Nepal tea “lost” in their identity.

k) No research facilities of tea including for promotional and marketing linked with research, which will help in developing new products suitable for changing market demand.

Obstacles for Exports Obstacles or bottlenecks to export are the existing factors reducing or delaying or otherwise disturbing existing and potential export.

a) Cost of inputs and mainly electricity with interruptions to supply, affect quality, increase the cost of processing and the exportable item becomes too pricey. The State’s supply of electricity to essential business houses such as tea factories should be made available on an uninterrupted and continues basis. The machine downtime and effect to quality of product can be at high cost.

b) Bank loans are difficult to obtain and interest rates are high. Export prices can be higher by 1-2 USCts per kg, which is sometimes the difference between a contract or refusal mainly to the bottom level of tea.

c) Packing material such as plywood chests/paper sacks, all imported, and used for packing tea for export to India and other destinations are not eligible to a duty rebate. This duty of 10—15%, if waived, will make the product more competitive.

d) Export trade is not supported by the Government. Exporters are levied a VAT payment of 13% which although refundable is very difficult to get back. Thus

Page 10

finances are scarce and export cost pricing calculations has to include such costs

e) Exporters unable to deliver as per standard accepted by buyers resulting in loss of credibility of Nepal trade.

f) Although bilateral and multilateral trade agreements have been entered into with various Governments, no real benefits have still accrued to Nepal except with Pakistan.

g) Delays and hold ups at Indian seaport and in transit effecting delivery times.

h) Route via India to the Bangladesh seaport of Chittagong should be developed to overcome delays, and facilitate shipments to Pakistan, Poland and elsewhere.

i) Policies in India affecting consignments to some buyer countries.

j) Tea policy and NTCDB are conceptually well established but are ineffective. These should either be abolished or made seriously effective. The government’s commitment should be clear and transparent.

k) Little Government support for active participation in international trade fairs to showcase Nepal tea.

1.5 Recommendations Recommendations for farmers, producers and exporters

a) Infrastructure: Green leaf farmers are located in areas, which have poor infrastructure. Although they are able to produce the leaf in quantities, transport is affected by using methods, which are unsatisfactory such as on animal back, bicycles, causing damage to the leaf in transit. The bags used for plucking are also not the current recommended types which have now been designed to keep the leaf intact as well as allowing it to “breathe’ without causing fermentation before it arrives at the factory premises. Access to the farmer’s premises quickly and in vehicles that are suitable should be made available to the providers of ancillary services. Recommend the import of commercial vehicles suitable to the industry on duty free basis.

b) In opening of new land, good agricultural practices must be strictly followed

to ensure minimum damage to soil and environment. Thus soil erosion and leaching can be minimized whilst organic population can be preserved. The physical properties of soil such as density, porosity, and moisture retention must be well addressed to minimize adverse effects of weather.

c) In order to tap into new markets, it is important to look into product

diversification, taking into account the trends in volume of imports by target countries and their preferences in taste and tea grades.

d) Tools and Implements: As the NTCDB has in their program a scheme to

supply tools and implements at subsidized costs the new type of plucking bag should be imported free of duty and made available at reduced cost so that the leaf quality can be preserved.

e) Quality Controls: Whilst the farmers should ensure that their pluckers are

following the practice of selective plucking, the factories should be very strict

Page 11

in their controls of leaf intake to reject all unsuitable and damaged leaf at factory door.

f) Political Interference: Government should support the factories to run their

business in the best practical manner to achieve quality products without allowing labour or outside influences to dictate terms to factory staff on good management practices.

g) Agricultural Inputs: Tea extension staff and the individual farmers must be

more vigilant regarding the indiscriminate use of chemicals and pesticides. Although it is a difficult task, the state machinery should be used effectively to patrol the borders so that import of inferior quality inputs not only to the tea industry but agricultural crops in totality is protected by not allowing substandard and banned cheap products.

h) Health Hazards: Some factories and packaging plants are unsuitable for tea

processing and are a health hazard. A scheme must be evolved by the NTCDB to register all tea farmers, processors, however small their operation. Regular inspections of their premises should be undertaken so that inferior, substandard and polluted products are not put out into either export or domestic market.

i) Certifications: As far as possible most medium and large export oriented

factories should be encouraged and assisted to obtain the ISO/HACCP certifications as a strategy for future marketing.

j) Packaging Material: All packaging material is imported either from India or

Sri Lanka through Indian traders. The industry is at present too small for any commercially viable enterprises to produce the needs of the industry only. Hence there will have to be continuation of imports for export packaging for the time being. With bilateral trade agreements, such as with Sri Lanka and multilateral agreement with SAFTA under SAARC countries already in force, opportunities should be created to import packaging items directly on a duty free basis .eg multi-wall and rigid type aluminium foil lined kraft paper sacks from Sri Lanka.

k) The traditional plywood chests, which were discarded from use some time

ago, are still being used for exports into India. These items are imported and re-exported. Duty concessions should be available for such transactions. As it is not an environmentally friendly form of packaging material, its use should be discouraged and the use of rigid paper sack should be promoted.

l) The made tea is packed into PE/PP bags and are stored till they are ready for

use. This form of packaging, particularly in the Terai areas where temperatures and humidity can be very high will speed up the deterioration of the product. In such instances dispatch of the made, packed and ready product to more suitable storage facilities should be done without delays.

m) The same applies to the export cargo, which is held up in covered trucks for

many days in transit to Kolkata port in open storage areas. Whilst some instances can be beyond the control of Nepal, it is always prudent to develop an efficient system for clearance of cargo with minimum delays being incurred. Improvement and minimizing documentation requirements is one method of reducing down time.

Page 12

n) Quality of Product: Above recommendations, if carried out, should ensure a product of better quality than what is presently available which would be the ultimate goal of the producer and processor and the tea industry as a whole. Further enhancement to quality can be achieved if the manufacturing practices are adjusted to different times of the season to make optimum use of the leaf quality and their inherent characters to bring out the maximum natural flavour, aroma and strength.

o) Test Reports: There are no laboratories or survey companies capable of

conducting tests and analyses on residue levels, heavy metal presence, fungal infestation and issuing reports that are required by the larger section of international trade today. This is a big disadvantage, as samples of teas awaiting export have to be sent to laboratories in India and Germany for such tests to be performed. There have been many instances where such samples have been found to be contaminated and thus orders having to be cancelled. Once the consignment is rejected, there is no “home” for it. Therefore the need to have a well equipped laboratory in Nepal. However there are limitations in setting up a laboratory by a private enterprise as well as any international survey company due to the volume of business being commercially unattractive. The alternative would be to strengthen the existing Government Food Testing Laboratory with a mandate to do commercial testing of export samples of all agricultural products to become a profit center whilst at the same time to devote a part of the time to conducting research and development.

p) Information System: There seem to be a total lack of information gathering

in the industry with little or no active attempt to collect, analyse and distribute the information to the stakeholders. The Agro Enterprise Center of FNCCI puts out some information but this is insufficient when market information and current developments are the essential information that an exporter requires. A website is to be developed by the NTCDB which is an excellent concept and all stakeholders should be involved in it’s design as the information required by each different sector is different and it takes time to get an information system designed with a professional planner. This must include as much as possible, information on world markets, speciality market segments, demand patterns, new concepts in tea consumption and a whole array of inter-related subjects from which the interested visitor can drawn on. The trade attachés in all the embassies overseas must be used as a constant source of information gathering and updating. A full list of buyers of all types of tea in every consuming country must be incorporated into the database so that they can be accessed. Furthermore the information of the individual export companies in Nepal with the types of tea they can offer showing the leaf appearance and cup quality in the form of photographs can be included in the website, for an annual fee, so that the exercise becomes a viable proposition for the NTCDB.

q) Export Marketing: The tea industry in Nepal is small. The volume exported

currently is around 0.23% and production is 0.32%, out of the total global output. (ITC statistics). With this small quantity entering the world market, it is difficult to build up a brand image unless with personal contacts and constant interaction. Furthermore any promotional and advertising would be at a prohibitive cost. Therefore it is more prudent to work with marketing and distributing companies who are experienced in handling food items and specifically beverages and tea. As the orthodox tea is considered a special product, it would also be more beneficial to work with the Speciality Tea

Page 13

Associations and such bodies established in a number of countries. HOTPA/HIMCOP are already working closely with the American Speciality Tea Association and are developing the product within the parameters set down by them to facilitate entry to their market segments. In every country, there are tea buyers who supply the cafes that serve special blends and varieties of beverages including tea and these buyers must be contacted by participating in trade fairs where special teas are exhibited and their business solicited. Negotiate with international brand owners and get into JV partnerships with them to supply and ensure Nepal teas are included in these branded products.

r) Two marketing entities have been formed in the orthodox and CTC sectors to

do the marketing function under the names of PLANTEA and HIMCOOP. Merging them to form one marketing company or association with a board representative of stakeholders in both sectors for the improvement of market share in the global market for Nepal tea in totality needs to be seriously considered.This company to undertake the promotional and market intelligence work, market planning forecasts, future trends, market information and international statistics. It should be the driving force to establish the Nepal Tea logo and brand in the global market. The company must monitor the quality available for export through the respective associations. This private company composed of senior and experienced persons should direct the affairs but also ensure that the interests of all parties are met fairly.

s) It is also necessary that the seedling and clones developed in Nepal be

protected. Nepal must strive and develop Geographical Indicators, mainly for the orthodox tea areas, similar to Darjeerling in India and Dimbula/Nuwara Eliya in Sri Lanka so that branding and marketing such produce can be done. The production and processing and the quality of the final product in such clearly defined and identified areas has to be closely studied and special features associated with them classified to use them as a marketing tool.

t) Research and Training: Like all other areas of the industry this too lags

behind. Research has been generally neglected. Due to the vicinity of India and easy access, progress at field level and development of new plant varieties, usage of inputs, and technology have all been directly or indirectly brought into Nepal. All the machinery is of Indian origin except those in the older factories some of which are from UK. Therefore the tea produced/processed bear a very close similarity to the Indian Darjeerlings and CTC’s.

Any potential research instincts have been suppressed to the extent that innovation in the industry or changes in the style of manufacture, or applying subtle changes to the methods of manufacture, have not been introduced. It is very necessary to establish a Research station, which is specific to tea with all the relevant divisions of an agricultural based commodity in place to look into agronomy, physiology, pathology, bio-chemistry, manufacture, extension, training, information and now the important aspect of marketing to look into new product developments with global consumers in mind.

There is a need to establish a tea training centre or tea school to develop human resources required for the tea sector.

Page 14

Recommendations for the business environment

a) Business Environment and Export Services: With the privatization of the tea industry, the Government controls were gradually removed in the operations of the large tea gardens and factories, which they controlled. However, contributions in certain areas, which are essential in giving directions to the industry, have also lost their significance, which is detrimental. The NTCDB, which still remains under Government control and is responsible for giving direction and guidance is lacking in performing their duties. On paper the program is well thought out looking into all aspects to solve the shortcomings. However the main positions on the Board must be with the now important private sector, who’s task is to drive the industry forward. The composition of the present Board is not fully and really representative of all stakeholders. Hence there is lack of purpose and direction and almost all the programs, which are outlined on paper for the betterment of the industry, still remain largely unattended. Financial constraints seem to affect even the extension and training programs which have been severely hampered and farmers are left to seek advise from their Indian counterparts for almost all their inputs both advisory, technologically and guidance on application of agri-inputs. Immediate revamping of the direction in which the NTCDB should focus and methods to obtain financial assistance from the Government must be treated as priority. The industry must be willing to contribute their share to the common cause, as it has been handed over to them to develop the industry. Therefore it is essential that their attitude towards the Government authorities and statutory bodies change and work in a combined manner in a cohesive way so that all stakeholders become willing partners to get moving forward. It is also essential that a scheme should be drawn to bring in finances by way of a Cess payment, membership payment, contribution towards advertising and promotion etc from the now private industry to swell the coffers of the NTCDB for their use in extension, expansion, research, training, information and marketing which can be developed to benefit all.

The environment is also not conducive to conduct business in a smooth way due to political interference and disruptions to normal work at field, factory and city levels, interruptions to supply of essentials, high costs, tax levies, import duty on necessary inputs which need to addressed by the Government and some changes introduced if the industry is to move forward. Export services at present are lacking and this aspect too has to be drastically improved not only on the state side but also with the private sector’s participation.

b) Export Financing: There is only one international bank, the State Bank of

India, operating in Nepal. There are a few Banks with foreign collaboration established such as Standard Chartered Bank, Himalayan Bank, Nepal Bangladesh Bank, Nabil Bank, Nepal Investment Bank. Many local banks are operating, some specific to one sector like the Agriculture Development Bank, whilst others such as Nepal Bank Limited, Rastriya Banjiya bank, Machhapuchera Bank, Kumari Bank, Lakshmi Bank, Everest Bank, NIC Bank, Bank of Kathmandu, Nepal Commercial and Credit Bank. Although these banks are able to handle export financing and documentation, they do not have the network of correspondents overseas to facilitate transaction, which hinders the smooth transactions in banking matters. There are no financial facilities available to exporters at favourable rates. There are no incentive schemes for the development of exports, such as pre-shipment finance. There is also no

Page 15

Export Credit Insurance scheme available to safeguard exporters in the event of default from overseas buyers which is now a grim reality. Factoring opportunities are not available. The Government has to look at opening up opportunities for more foreign participation not only in the fields of finance and banking but also joint venture partnerships and land ownership by foreigners.

c) Route via India to the Bangladesh seaport of Chittagong should be developed

to overcome delays, and facilitate shipments to Pakistan and Poland.

Page 16

2. The tea Industry in Nepal 2.1 The Sector in General The tea industry began in 1863 in the Himalayan area with the first factory for processing built in the district of Ilam in 1878. Although tea was known as a commercially viable crop, it was not until 1982 that it’s significance as an export earner was identified by the government with the designation of eastern districts (Jhapa, Ilam, Panchthar, Terhathum and Dhankuta) of Nepal as tea zones. From then onwards, the Government provided assistance to the tea growers and processor in a modest way for its development. The industry began to be more organized and recognized as a potentially significant sector with the government promoting the establishment of the Nepal Tea and Coffee Development Board Act in 1993 and setting up of the Tea Board. A National Tea Policy was introduced in year 2000 to support the growth of the sector. The Government divested their holdings so that the private sector would become the engine of growth for the industry envisaging that tea would be one of the major crops for poverty reduction in the rural and Hill areas and become a significant export earner. Against this background, there has been a significant increase of export in quantity and value of tea over the past years. Nonetheless, tea constitutes only 0.5% to the total export earnings of Nepal commodities at present. Due to the varied weather conditions and soil composition, tea is grown in two areas, under significantly different agro-climatic regions, in the Terai and the hills. It is a seasonal crop with no harvesting in the cold period. The first flush leaf comes out in May/June and followed by the second flush. The rainy period starts in July and more weathery teas are processed at this time, which are lower in quality. Again in August/September, the leaf improves with good sunshine and dry winds to give the Autumnal teas with better quality. This quality differences are more pronounced in the orthodox teas. Nepalese tea plantations, benefiting from diverse agro-climatic conditions, have comparatively young bushes with 29% of smallholder farmers owning bushes less than 5 years old. The bushes are grown both from clones and seed stock varieties and should enable the producers to capitalize on these natural conditions to increase, diversify product range, and improve on quality with proper application of new developments using modern technology. However, because of individual or separate interests and insufficient willingness to work together in a cohesive manner to achieve a common goal, these aspects have not been addressed by the vast array of authorities, organizations, associations and local bodies involved in the tea business. There appears to be a lack of committed focus and outlook for the betterment of the industry as a whole. A large number of small holder farmers are engaged in growing tea in both areas and they now account for 26.5% whilst the bigger estates produce 73.5% of CTC tea. Over 30,000 people are directly involved in the industry with a large percentage being rural women. Therefore this industry has the potential to empower rural women through poverty alleviation and has become the focus of attention of many international organizations and many NGO’s. The tea produced in the Terai region originates predominantly from clone bushes, which are very similar to those of the Indian Siliguri region, and producing similar

Page 17

CTC type of tea. They reportedly produce around 12 m kgs per annum in 23 factories, using Indian lines of machinery. Although data available in general, seem to be inaccurate, a guesstimate is that around 20m kgs of green leaf goes to Indian factories across the border. Orthodox tea grown in the hill regions mainly from seedling varieties is very close to the Indian Darjeerling type, the processing too, being similar. With tea growing areas very close to each other, across the borders of the two countries, the plant material used come from the same mother bushes and clones. As the machinery used for processing being the same supplied by Indian manufacturers, the final product range of Orthodox tea is same/similar. Over 90% of the produce is exported to India officially/unofficially whilst the small balance find their way to international speciality tea markets in small parcels at attractive prices. A guesstimate, based on available data indicates that approximately 17- 20 m kgs of green leaf from the hill areas find it’s way to Indian factories in the Darjeerling area. Reliability of data It should be noted that accurate data is not available, in-spite of there being many authorities, institutions, associations, cooperative units, farmer groups, NGO’s and INGO’s working in the sector. There seem to be a lack of a cohesive working environment being followed and implemented so that a united national development effort is lacking. There is a large volume of trade in many countries across the borders, a fairly high percentage of which is done unofficially or smuggled. Tea is one item, which is traded heavily in this manner. These porous borders are a haven for unofficial business in tea. Large quantities of tea, produced in countries such as China, India, Bangladesh, Iran, Turkey, Nepal and many other countries remain therefore unaccounted for. Most of this trade goes unchecked and cannot be quantified, although most governments in these countries accept it and even encourage it. It must be noted that the per capita consumption in the Asia producer region, which is normally high, particularly in China, India, Vietnam and their neighbouring countries cannot be correctly calculated and even guesstimates may not be accurate. This is due to the rapid expansion in land area and increased production, a high amount at cottage level, all of which are not monitored and recorded. Most of produce in border areas enters neighbouring countries via unofficial channels. Therefore customs data in these countries are inaccurate. This situation is spread even to the CIS states, Afghanistan, Pakistan, Iran, as cross border trade and smuggling is common. As no one source is able to provide a comprehensive picture, different data sources are used in this report to present production and export figures, i.e. National Tea and Coffee Development Board, TEPC, Department of Customs and ITC databases. Differences in methods of measuring and recording data (official and unofficial), assumptions used, classifications, etc. lead to some pertinent discrepancies. These figures must therefore be treated with care. However, the data is not contradictory in supporting the main message of the report, the main findings, obstacles and recommendations for future action.

Page 18

Box 1: Comparison of Orthodox and CTC Tea

Orthodox Tea CTC (Cut, Tear and Curl) Tea Leaf Mainly leaf from seedling plants, China JAT (type) is preferred.

Leaf from VP plants. Assam JAT is preferred

Seedling leaf has less moisture, more leathery appearance and has more concentration of flavour compounds (amino acids) which can be enhanced with environmental conditions.

More moisture or juicy, less leathery and environment does not assist in enhancing the concentrates.

In the withering process of green leaf, , the moisture content has to be reduced to 40-45% by using hot air for 12-16 hrs

Withering is done to reduce moisture to 65-70% using normal air for a shorter period of time.

Processing Processing broken up to 4 main stages of withering, rolling in 4-5 rolls, fermentation and drying (firing). The leaf is rolled to process whole leaf, semi leaf size and a lesser percentage of small leaf. There are about 10-12 grades based on leaf size.

The process is continuous. The leaf is broken into small particle sizes using a rotovane (similar mincing machine), and sent though the CTC machine to make the small sized leaf shotty. It then goes through the fermenting bed and into the drier. There are no big leaf grades in this method of processing. Only 3 grades.

Liquor properties Leaf black in appearance. Has more flavour, aroma and quality, less bright infusion, not very strong and coloury but brisk and bright in cup.

Leaf brown in appearance. Very strong liquor, with darker colour and bright infusion. Less quality, flavour and aroma.

Suitable for traditional brewing but small leaf grades are used in the quality conscious and high end teabag markets

Suitable for teabags but also used in the traditional manner of brewing in certain countries which prefer a very strong liquors.

Marketed as loose tea in packets, tins as well as the now developing pyramid bags.

Mainly marketed as the single or double chambered 2g teabags servicing the middle segment of the global market

Popular in the Middle East and high end developed markets

Quick brewing convenience item very popular in the developed markets.

2.2 The global tea market 2.2.1 Overview of world production and trade In the year 2005 International Tea Committee bulletin, published the following figures, expressed in thousand metric tons, extracted from available data collected.

Page 19

Table 2.1 - International trade in tea Year Production in

35 countries Retention at

Origin Imports Global

Consumption 2005 3,420 1,869 1,446 3,315 Source: International Tea Committee Statistics Yearbook It must be noted that above figures, usually obtained from official channels do not present the correct picture as data available from China, Vietnam and a few other countries of origin do not reflect the actual situation. From above data, the origin countries retain nearly 100m kgs additional, from their increased production, for growing domestic consumption annually. Calculated figures based on per capita consumption, indicates an annual increase of around 1.5%, which is about 21,000 MT. However it must be noted that in the Middle East, and Near East, tea consumption is very high and increasing at 3.5% or higher whilst in the highly populated Asia it would similar. The production figures indicate a rate of expansion and growth at 3.29% per annum, which will reflect an official increase of 110,000 MT. The increased quantity retained in all producer countries is calculated at 94,000 MT annually thus indicating a figure of 5,000MT shortfall from the calculated 21,000 MT to supply the world non-producing consumer markets only. It can be safely assumed that there would be an annual shortfall in production to meet the demand much more than the data indicates of 5,000MT. The current world export is 1,563,199 million kgs (incl. re-exports) produced in 12 Asian, 13 East African, 4 South American countries together with some smaller producers (COMTRADE). From a global perspective Nepal is still one of the smallest players representing two tenths of a percent of global production. Also as a producer of orthodox tea Nepal is a small player. Table 2.2 shows world tea producers broken down into CTC and orthodox teas. As can be seen from the table, orthodox production is in smaller volume, especially in Africa, but the opposite in the case of producers like Turkey, Indonesia, Sri Lanka and Vietnam. Table 2.2 - Production of Tea according by CTC/Orthodox in various countries, 2005 CTC Orthodox India 833 88 Bangladesh 57 2 Sri Lanka 16 298 Indonesia 12 113 China - 48 Taiwan - 1 Iran - 25 Malaysia - 3 Myanmar - 18 Nepal 7 1 Turkey - 135 Vietnam 8 62 Africa 475 16 CIS countries - 17 S.America - 83 PNG 7 - Total 1,415 910

*Includes Estimates, excludes other teas Source: International Tea Committee Statistics Yearbook

Page 20

The production quantities in each major producing country is closely monitored by international buyers, particularly now due to the very advanced communications systems. Decline in quantity or damage to crop, political upheavals, change in import and export regulations that may disrupt normal supplies can cause price fluctuations.. Although it would be difficult to list all big buyers in most consuming countries there are some like Unilever/Lipton who have become worldwide marketers of tea with others like Lyons-Tetley, Nestle, Douwe Egberts and a few other brands which are also marketed worldwide although not as widely. The bigger international buyers usually wish to base their purchases on “just in time” deliveries at their doorstep to reduce financial costs and also buy large consignments. Nepal tea industry does not have the facilities to offer such large consignment as a central warehousing and blending complex is not available. On both counts Nepal is at a distinct disadvantage. Annex V presents a typical flowchart that described the consecutive steps involved in growing, processing and exporting of tea. Table 2.3, 2.4, show the main world importers of black tea in bulk (mostly CTC), black tea in <3kg packs (orthodox and CTC tea) pre-packed and retail packed, and green tea respectively. As orthodox tea is of higher value, it can be assumed that the countries showing highest unit value imports in table 2.4 have a preference for orthodox teas. Norway and Finland especially stand out in this context and to lesser but not insignificant extent, Italy and Canada. Germany is an important buyer of Nepalese orthodox tea, and paid an average CIF value of 19,000 US$/ton in for its imports from Nepal. The German market is also showing steady growth, averaging 12% in value over the last 5 years and paying increasing prices as growth in value exceeds growth in quantity over this period. Pakistan is an important buyer of CTC tea from Nepal and is in fact the world’s second largest buyer of bulk packed black tea. As table 2.5 shows, Pakistan’s imports in 2006 were up from 2003 and mainly in value. Pakistan buys most of its tea from Kenya/other East African producers meeting 61% of it’s import requirements in 2006. In 2005 Pakistan’s imports peaked significantly higher than other years, East African producers, mainly Kenya met this supply requirement with 72% market share in the same year. Pakistan is clearly an attractive market for Nepalese CTC exports and Nepal also enjoys a 10% tariff advantage under SAPTA over Kenya. Strong growth in imports of black tea in bulk is occurring in Middle East, in countries such as Iran, Saudi Arabia, Syria, UAE, Egypt and Jordan (likely to be importing on Iraq’s behalf) and CIS countries like Ukraine and Kazakhstan.

Page 21

Table 2.3 - Major Importers of black tea in bulk

Importers

Imported Value US$ thousand

Imported Quantity

(MT) Unit value (US$/unit)

Av. Growth

Value p.a. 2001-2005

(%)

Av. Growth

p.a. Quantity

2001-2005 (%)

World estimation 1,809,369 1,022,965 1,769 4 1

UK 243,439 144,551 1,684 -2 -2

Pakistan 227,800 137,600 1,656

Russian Federation 166,151 128,684 1,291 13 8

USA 124,967 75,350 1,658 1 -1

Japan 98,271 31,430 3,127 -4 -4

UAE * 94,920 39,962 2,375 5 2

Iran 87,423 33,914 2,578 92

Germany * 78,467 28,775 2,727 2 -2

Saudi Arabia 57,534 16,916 3,401 31 27

Kenya * 43,002 51,962 828 11 15

Syria * 41,507 19,241 2,157 0 0

Ukraine 37,884 15,896 2,383 40 15

Kazakhstan * 36,161 20,147 1,795 23 19

Sudan 35,145 17,684 1,987 4 -14

Netherlands* 34,852 23,193 1,503 7 5

Poland * 34,556 25,649 1,347 2 -2

South Africa 22,742 19,307 1,178 10 5

Chile 20,521 17,636 1,164 2

India 19,828 15,223 1,303 18 16

Canada 19,485 8,606 2,264 5 1

Jordan 18,262 4,632 3,943 153 114

Ireland 16,796 8,454 1,987 -3 -3

Iraq 16,701 7,916 2,110 -18 -25

Hong Kong 16,640 7,429 2,240 -7 -5

Malaysia 14,648 12,882 1,137 20 10 Source: ITC calculations based on COMTRADE * Re-export figures included

Page 22

Table 2.4 - Major Importers of black tea in <3kg packages

Importers

Imported Value US$ thousand

Imported Quantity

(MT) Unit value (US$/unit)

Av. Growth

Value p.a. 2001-2005

(%)

Av. Growth

p.a. Quantity

2001-2005 (%)

World estimation 1,021,863 243,180 4,202 5 -4 Russian Federation 122349 38,206 3,202 7 -10

Saudi Arabia 70228 8,713 8,060 -7 -8

Canada 68588 6,309 10,871 9 -6

UAE * 63,028 26,670 2,363 4 6

USA 56663 10,565 5,363 19 19

France 56,661 5,719 9,908 8 -5

Australia 56552 10,231 5,528 16 14

Japan 42919 4,744 9,047 0 4

Italy 29,084 2,658 10,942 9 6

Sweden 25,210 2,747 9,177 8 -1

Syria * 23,369 8,526 2,741 12 7

United Kingdom 21,588 6,371 3,388 8 -3

Poland 20,872 3,765 5,544 9 2

Libya 20,614 10,643 1,937 -22 1

Ukraine 17,494 3,694 4,736 -11 -26

Iraq 17,269 11,234 1,537 12 9

Netherlands 16,723 4,088 4,091 7 -6

Kenya 16,225 13,437 1,207 -2 -7

New Zealand 13793 2,767 4,985 11 13

Germany 13,539 3,797 3,566 12 11

Belarus 12927 2,544 5,081 42 26

Belgium 12,729 1,854 6,866 6 8

Norway 11,659 868 13,432 7 2

Denmark 11,269 1,181 9,542 7 6

Finland 11,070 846 13,085 3 -5 Source: ITC calculations based on COMTRADE * Re-export figures included

Page 23

Table 2.5 – Pakistan’s Imports of black tea- mainly CTC in bulk, 2003-2006

Value 2006 US$

thousand

Quantity 2006 (MT)

Value 2005 US$

thousand

Quantity 2005 (MT)

Value 2004 US$

thousand

Quantity 2004 (MT)

Value 2003 US$

thousand

Quantity 2003 (MT)

World 221,008 115,419 227,800 137,600 200,843 118,634 190,567 114,576

Kenya 138,431 65,458 164,442 91,497 139,565 75,862 134,277 72,646

India 18,211 13,191 9,365 8,487 4,050 3,977 6,687 6,276

Indonesia 14,704 8,941 12,645 9,199 12,322 9,435 10,612 8,578

Sri Lanka 8,136 3,504 7,035 3,261 6,177 2,813 6,182 2,941

Rwanda 7,991 4,050 6,227 3,469 5,042 2,672 831 462

Viet Nam 5,315 4,067 1,727 1,476 3,207 2,710 3,283 3,265

Bangladesh 5,207 3,748 9,118 6,777 11,952 9,337 12,257 9,570

Burundi 5,163 2,484 2,559 1,721 3,568 2,178 822 445

Tanzania 4,071 1,957 2,897 1,910 5,451 3,086 5,485 3,077

Uganda 3,446 1,743 3,302 2,101 1,222 767 40 23

Malawi 2,663 1,467 1,542 1,081 1,441 991 1,492 1,117

Nepal 1,398 806 1,013 685 728 631 969 819Source: COMTRADE Table 2.6 and 2.7 show the world’s major importers of green tea. Traditional markets are in North Africa and France’s North African population, but the importance of United States, Canada, Russian Federation and West Africa cannot be ignored. Growth and upward pressure on prices can be seen in both bulk and non-bulk global imports. Very rapid growth in Ghana cannot go unnoticed. Table 2.6 - Major Importers of green tea in bulk

Importers

Imported Value US$

thousand

Imported Quantity

(MT)

Unit value

(US$/unit)

Av. Growth Value p.a.

2001-05 (%)

Av. Growth

p.a. Quantity 2001-05

(%)

% of World

Imports World estimation 263,241 141,232 1,864 10 3 100 USA 41728 11,325 3,685 27 8 16

Japan 36987 14,136 2,617 -1 -2 14

Germany 26,886 9,460 2,842 20 19 10

Morocco 12,355 9,392 1,315 -5 -7 5

France 10,918 2,134 5,116 20 9 4

Russian Federation 9,518 7,901 1,205 34 28 4

Mauritania 8,316 3,767 2,208 22 4 3

Uzbekistan 7,092 12,283 577 0 -7 3

Senegal 6,372 5,900 1,080 -8 3 2

Algeria 6,287 3,238 1,942 7 0 2 Source: ITC calculations based on COMTRADE

Page 24

Table 2.7 - Major Importers of green tea in <3kg packages

Importers

Imported Value US$ thousand

Imported Quantity

(MT) Unit value (US$/unit)

Av. Growth Value p.a.

2001-05 (%)

Av. Growth

p.a. Quantity 2001-05

(%)

% of World

Imports

World estimation 318,770 120,427 2,647 21 11 100 Morocco 70,821 40,394 1,753 18 8 22

France 29,296 5,402 5,423 15 1 9

Ghana 23,018 11,326 2,032 134 120 7

USA 20,217 2,822 7,164 19 14 6

Canada 19,536 3,196 6,113 41 9 6

Russian Federation 15,057 4,786 3,146 54 23 5

Algeria 14,833 8,163 1,817 19 13 5

Mauritania 9,836 4,848 2,029 70 60 3

Libya 8,245 5,884 1,401 33 3

Belgium 7,345 1,705 4,308 12 38 2 Source: ITC calculations based on COMTRADE 2.2.2 Trends in world consumption The world market has developed 3 distinct preferences in which to enjoy the favourite cup of tea.

a) Teabags mainly in the developed countries and for convenience. b) Orthodox tea sometimes whole and semi leaf tea which gives a light brew c) Green tea which has a completely different taste

There are subtle changes from the above 3 main types where consumers with special preference and fancies look for their requirements1. The tea market fluctuates according to the demand of these three main types, being distinctly seasonal in temperate countries. There is also a shift in the manner in which tea is consumed with these seasonal changes with a move from it being a hot beverage to iced tea or cold beverage. Weather plays an important role in the production as the quality of the made tea is considered to be lower during the rainy seasons and buyers who seek a distinct quality in the blends operate to a lesser degree during these “rush” periods. An interesting development is the increased demand for speciality, bio-organic and herbal teas. Capitalizing on tea being increasingly recognized as a health beverage following recent scientific and medical findings, there is more demand now being created with emphasis more on bio-organically grown varieties. 2.3 Export of tea from Nepal 2.3.1 Growth in national tea exports

1 Annex VII presents a composition of a typical tea beverage

Page 25

Due to a strategy of expansion, the total area for tea cultivation has increased with some 450 % over the last 10 years. As the following table shows, growth of tea exports from Nepal has even been more impressive, and reached some 650% over the last decade. Table 2.8 - Growth in cultivation and trade of Nepalese tea 1996/7 2005/6 percentage

increase/decrease Area 3,500 ha 15,700 ha 450% Imports 6.2 million kgs 0.5 million kgs (800%) Exports 0.77 million kgs 5.0 million kgs 650% The exporters have grown to 20 whilst the importers have decreased. An increase of 61% is recorded in export volume of unit packs below 3 kgs whilst bulk exports have risen by 35% over the last one year. The total recorded export earnings in 2005/6 amounts to US$ 982,000. 2.3.2 Export of tea to India Nepal tea industry is very vulnerable due to their dependency on one major market – India, for over 90% of their orthodox and nearly 40% for the CTC teas. Therefore any changes outlined above which will affect this one outlet will cause severe price fluctuations. Table 2.9: Export and Import of Tea from/to Nepal to India (Q in Kg., Value in ‘000Rs.)

EXPORT IMPORT Green Tea Black Tea Total Total Year

Quantity Value Quantity Value Quantity Value Quantity Value 2005-06 80,449 7,246 4,279,524 375,579 4,359,973 382,825 195,093 18,196

2004-05 704,196 98,825 3,608,681 347,512 4,312,877 446,337 330,327 31,157

2003-04 2,983,176 264,549 1,024,500 113,749 4,007,676 378,298 323,966 31,297

2002-03 28,714 6,006 2,839,350 219,697 2,868,064 225,703 291,946 28,640

2001-02 482,158 2,455 1,613,994 262,469 2,096,152 264,924 408,946 44,421

2000-01 360,800 25,496 39,518 7,874 400,318 33,370 757,890 82,055

1999-00 410,207 58,195 NA NA 410,207 58,195 736,533 74,854 Source: Department of Customs. As the above table shows, the dependency on India as a trading partner for tea has increased tremendously in the past 5 years, which further illustrates Nepal’s vulnerability. It is therefore imperative that their agricultural produce as well as expansion of their international markets be diversified. Nepal has a very large border trade going on primarily with India although there is also some border trade with Tibet. There appears to be about 10-12% of the green leaf from the CTC areas and over 200% of green leaf from the orthodox areas going across the border to India. They may be sold locally in the mountain areas out of small householders’ domestic production units. This is based on the land area in the orthodox region of 6,700 ha calculated even at a low yield of 750 kgs made tea per ha from available data. The published figure of processed orthodox tea is only 1.6 m kgs. The imposition of strict control at the border and stopping of imports of orthodox made tea as well as green leaf by India caused a complete stoppage to the otherwise

Page 26

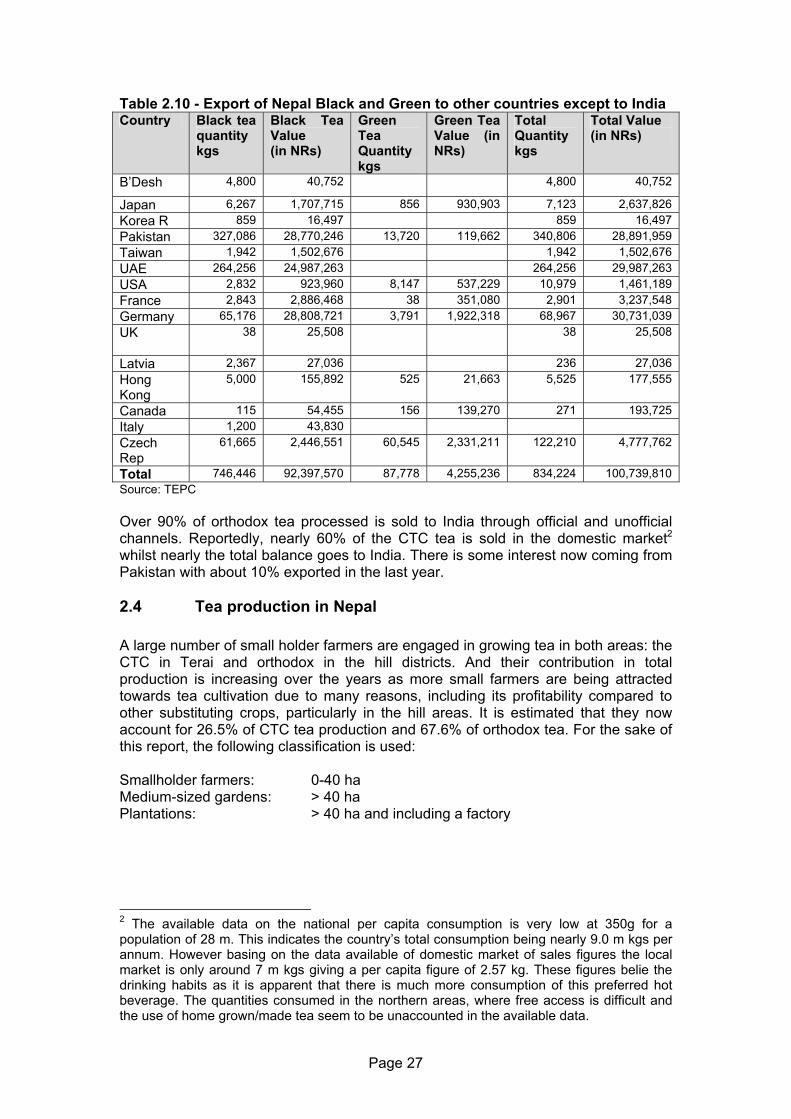

free flow of export and sharp price declines occurred, whilst green leaf became un-saleable and unusable. Similarly, the work stoppages caused due to political unrest in India, which is now taking it’s toll on the Darjeerling tea with both quality and quantity declining will open the possibilities for Nepal orthodox tea for price gains and entry into new markets. Indian authorities are getting more concerned by the decline in the volume produced of their own Darjeerling tea, and potential threat posed to their special tea image and brand built over many years. Many discerning overseas tea buyers/packers and consumers are aware of this situation in the planting areas and there is a danger of the value of the Geographical Indicator (GI) of Darjeeling Tea eroding. Therefore Indian border patrols have been intensified this year to stop the flow of green leaf and made orthodox tea from Nepal, which has caused many hardships to the farmers. This situation has become a problem of concern to the Nepal Government. Unless, urgent action is taken to rectify the shortcomings mainly in the orthodox tea sector, it is likely that Nepal orthodox tea would face the same fate as their rice and jute industries. Herein lie the problems the tea industry confronts as the giant neighbour with unlimited porous borders can/will use the produce of Nepal origin to sell into, both their insatiable domestic market and lucrative export markets either passing them off as Indian tea or unfortunately using the Nepal tea as low priced blend mixes or “fillers” and “price reducers” in their export blends. In this way, Indian traders have created a psychological myth that Nepal tea is lower in quality and does not command as high a price in the open market or through auction system. Another reason for the price to be beaten down is that once Nepal teas enter the Indian territory it becomes a terminal market for it’s disposal and unscrupulous traders capitalize in such situations. This position is further compounded by the indiscriminate use of pesticides and insecticides by the Nepali farmers who have therefore brought upon themselves a dubious reputation of being producers of tea that has higher than accepted pesticide residue levels rejected by most buyers in the EU, North America, Japan, Australia and New Zealand. 2.3.3 Export of tea to countries other than India The following table presents the recorded exports of black and green tea to countries other than India.

Page 27

Table 2.10 - Export of Nepal Black and Green to other countries except to India Country Black tea

quantity kgs

Black Tea Value (in NRs)

Green Tea Quantity kgs

Green Tea Value (in NRs)

Total Quantity kgs

Total Value (in NRs)

B’Desh 4,800 40,752 4,800 40,752

Japan 6,267 1,707,715 856 930,903 7,123 2,637,826 Korea R 859 16,497 859 16,497 Pakistan 327,086 28,770,246 13,720 119,662 340,806 28,891,959 Taiwan 1,942 1,502,676 1,942 1,502,676 UAE 264,256 24,987,263 264,256 29,987,263 USA 2,832 923,960 8,147 537,229 10,979 1,461,189 France 2,843 2,886,468 38 351,080 2,901 3,237,548 Germany 65,176 28,808,721 3,791 1,922,318 68,967 30,731,039 UK

38 25,508 38 25,508

Latvia 2,367 27,036 236 27,036 Hong Kong

5,000 155,892 525 21,663 5,525 177,555

Canada 115 54,455 156 139,270 271 193,725 Italy 1,200 43,830 Czech Rep

61,665 2,446,551 60,545 2,331,211 122,210 4,777,762

Total 746,446 92,397,570 87,778 4,255,236 834,224 100,739,810 Source: TEPC Over 90% of orthodox tea processed is sold to India through official and unofficial channels. Reportedly, nearly 60% of the CTC tea is sold in the domestic market2 whilst nearly the total balance goes to India. There is some interest now coming from Pakistan with about 10% exported in the last year. 2.4 Tea production in Nepal A large number of small holder farmers are engaged in growing tea in both areas: the CTC in Terai and orthodox in the hill districts. And their contribution in total production is increasing over the years as more small farmers are being attracted towards tea cultivation due to many reasons, including its profitability compared to other substituting crops, particularly in the hill areas. It is estimated that they now account for 26.5% of CTC tea production and 67.6% of orthodox tea. For the sake of this report, the following classification is used: Smallholder farmers: 0-40 ha Medium-sized gardens: > 40 ha Plantations: > 40 ha and including a factory

2 The available data on the national per capita consumption is very low at 350g for a population of 28 m. This indicates the country’s total consumption being nearly 9.0 m kgs per annum. However basing on the data available of domestic market of sales figures the local market is only around 7 m kgs giving a per capita figure of 2.57 kg. These figures belie the drinking habits as it is apparent that there is much more consumption of this preferred hot beverage. The quantities consumed in the northern areas, where free access is difficult and the use of home grown/made tea seem to be unaccounted in the available data.

Page 28

2.4.1 Growth in tea cultivation and production Both the total area and production of tea in Nepal have increased tremendously over the years and have significantly increasing trend as is clear from Figure 1 below.

Figure 1 Area and Production of Tea: NEPAL

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1992

/3

1993

/4

1994

/5

1995

/6

1996

/7

1997

/8

1998

/9

1999

/00

2000

/1

2001

/2

2002

/3

2003

/4

2004

/5

2005

/6

Year

Qua

ntity Area Ha.

Production Mt.

As the following table shows, tea production and cultivation of tea by both smallholder farmers and larger gardens/plantations has grown considerably in recent years. The NTDC was privatised and accordingly the area and production under it are reported into the private sector category. Accordingly, a sudden jump in area and production under private category is noticed in the year 2000/01.

Page 29

Table 2.11: Total Tea Production and Tea Plantation Area

Tea Plantation area in hectares Tea production in Kg's

Financial Year Small holders

Private NTDC3

No. of small-farmers

Plantation area Total Private NTDC

Small holders Total

1992/3 75,400 860,000 1614000

1993/4 1,191 493 687,000 982,000 75000 1744000

1994/5 1,788 644 837,000 1,009,403 10,000 1946403

1995/6 2,243 828 1,500,000 1,112,329 125000 2737329

1996/7 1,685 938 2,390 879 3,501 1,800,000 925,942 18,000 2905942

1997/8 2,192 938 2,591 1,385 4,515 194,655 603,136 468980 3018571

1998/9 6,073 938 4,915 3,239 10,250 3,577,857 496,881 418242 4492980

1999/00 6,073 938 4,915 3,239 10,250 3,577,857 496,881 1010499 5085237

2000/1 8,179 5,310 3,818 11,997 5,089,579 1548503 6638082

2001/2 8,179 5,575 4,186 12,346 5,864,720 1653855 7518575

2002/3 8,321 5,760 4,314 12,643 6,478,000 1720000 8198000

2003/4 8,869 6,252 6,143 15,012 7714669 3956535 11651204

2004/5 8312 6,845 6,989 15,900 7789893 4816188 12606081

2005/6 8,912 7,154 7,100 16,012 8,443,907 5,244,320 13,688,237 Source: National Tea and Coffee Development Board Although the government’s plan was to have 28,000 ha under tea cultivation by year 2010 and further projected to 62,000 ha by 2020, the expansion has been much lower and estimates have been revised to have 18,000 ha under tea cultivation by 2010. Nonetheless, growth has been impressive. 2.4.2 Type of tea produced There are reportedly a total of 12,2004 smallholder plots, 134 medium sized gardens and 38 large plantations. Combined, these produce a total 13.6 million kgs of made tea of which 1.6 million kgs is orthodox type. Table 2.12 - Type of tea produced 2005/06

Particulars

Orthodox

CTC Total

Area in ha Production in kg. Area in ha

Production in kg. Area in ha5

Production in kg.

1 Garden 2,805 542,090 6,107 7,901,817 8,912 8,443,907 2 Small Holder 4,231 1,113,060 2,869 4,131,270 7,100 5,244,330 Total 7,036 1,655,150 8,976 12,033,087 16,012 13,688,237 Source: National Tea and Coffee Development Board 3 The Nepal Tea Development Corporation (NTDC) was established in 1966 by the Nepalese Government. The Government divested their holdings so that the private sector would become the engine of growth for the industry 4 Table 2.1 indicates a total of 7,100 smallholder farmers. However, data collected from associations/chambers/and INGO/NGO's suggests that a total of 12,200 smallholder farmers are active in areas concerned. 5 Please note that other data sources suggest a total of 15,700 ha in 2005/2006

Page 30

According to this table, smallholder farmers account for 67 and 34 percent of the production of orthodox and CTC tea respectively. These data should be taken with care though, as more than 11 plantations and 45 gardens (mostly non-small farmers) have not yet been registered with NTCDB. Also, other data suggests that smallholder farmers account for 26.5 % of the CTC produce. 2.4.3 Yield and Cost of Production (COP) According to NTCDB field representatives and Farmers in the CTC area, the average yield per plant is 1.55 kg pa and the density of plants is 14,000 per ha. Farmers in the CTC areas are able to get a fair price for their leaf, almost double their cost of production (COP), during better times whereas the orthodox tea farmer suffers very often obtaining a price about 10-15% lower than their COP. In the orthodox areas, however, the yields are significantly low, nearly 25% lower than India and 30% below Sri Lanka. In the CTC areas the yields are lower than in Kenya. As the international tea market is very competitive, relative low yield is a cause of concern. At the factory level, there seem to be no fixed method of calculation to arrive at the green leaf price. Farmers have to accept price levels indicated by the factories. In the CTC areas, the Siliguri auction prices are used as a guideline and is reviewed every week whereas in the orthodox regions they are completely at the mercy of the factory. The farmers sometimes get paid almost after six months from date of direct delivery to the factories. They prefer to sell to middlemen or tea dealers as most often money is paid immediately on delivery. However they are beaten down on the price by about 10-20 %. Those who follow the Code of Conduct are able to get a premium of nearly 20 % for their green leaf. The farmers are unable to get an accurate calculation of their COP and very often the financial costs are not taken into account. Even fertilizer and pest control inputs seem to be inaccurately compiled. This is due to lack of knowledge of simple costing methods. Smallholder farmers Smallholder farms are generally well maintained with plant population being adequate, although in some instance overcrowding was observed.

In Jhapa and Morang the farmers indicated that their yields are in the region of 18,500 kgs going to 22,000 kgs in some instances. These are high indications but seem to be acceptable, as the quality of plucking is not kept at the ideal 2 or 3 leaves and bud. In the hilly areas of Ilam and Fikkel the plant population in the plots observed were less and more scanty. The incidence of pests, insects and fungi was more as this region is damp and is more conducive for them to thrive.

Their COP is around 0.093 to 0.125 US$ per kg. The selling price is around US$ 1.50 to 1.60 from the factories. The COP and corresponding selling prices are lower in the CTC areas. However, this money is delayed sometimes up to 6 months in both areas, causing financial strain. There are Green Leaf Tea Dealers who pay spot cash, about US$ 0.03 kg less. Farmers fall into difficulty and find it hard to obtain loans at the Government’s stated low interest rates and as farmers are also at the

Page 31

mercy of the middlemen, habitually they are not amenable to accepting technical advice and change their methods

Medium sized gardens and big plantations These are tea gardens in excess of 40 ha and with many having their own processing factories. The larger estates average lower yields/ha than the smallholder farmers. Their yields are lower being around 14,500 to 16,000 per ha. Here again the same scenario of coarse plucking and haphazard use of chemicals were evident. The estate workforce tea plucker earns US$ 1.50 per day for delivering 26 kgs of leaf with an incentive payment of 0.018 US$ per each additional kg. There are instances of pluckers delivering up to 35 and even 50 kgs, consisting of mixed leaf - good and coarse, which affects quality whilst processing. However due to political pressure on labour matters the factories are forced to accept all leaf delivered. 2.4.4 Geographical distribution of production In 1982, the Government declared the five districts i.e. Jhapa, Ilam, Panchthar, Terhathum and Dhankuta of the eastern development region as 'Tea Zone'. In these five districts the main production of tea is concentrated, as also highlighted in map included as annex II. The bulk of the tea, however, is grown in Jhapa (only CTC grown there), which is situated in the far southeastern Terai part of Nepal. According to NTCDB data, presented in table 2.13 below, this district alone accounts for approximately 88 % of the tea production of Nepal. Table 2.13 - Geographical distribution of production

S. No District Gardens Small Farmers Total

Area Production Kg

Area ha

Production Kg

Farmers No.

Area ha

Production Kg