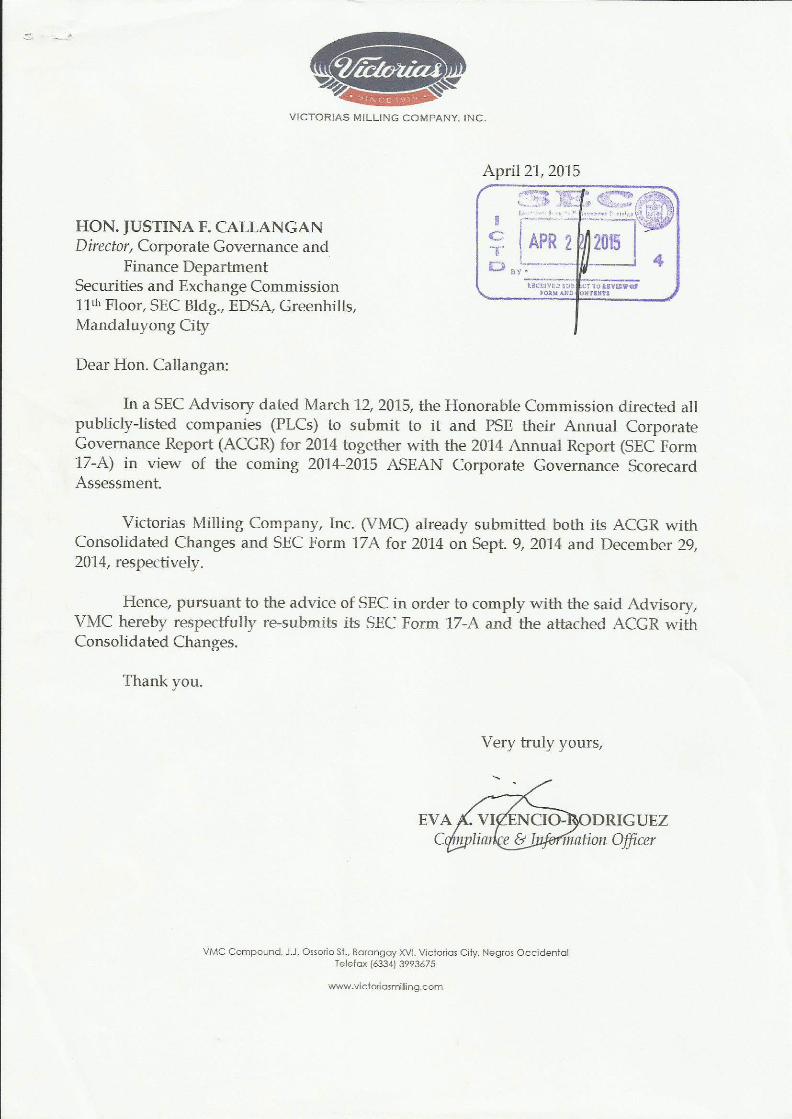

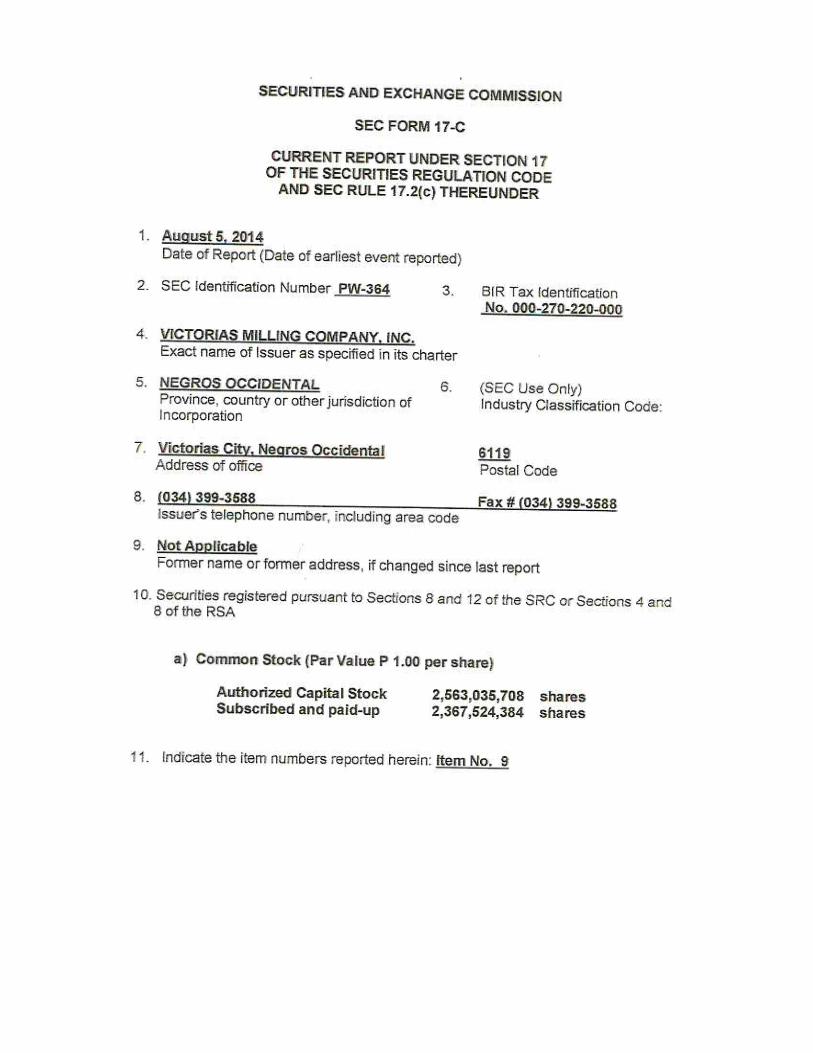

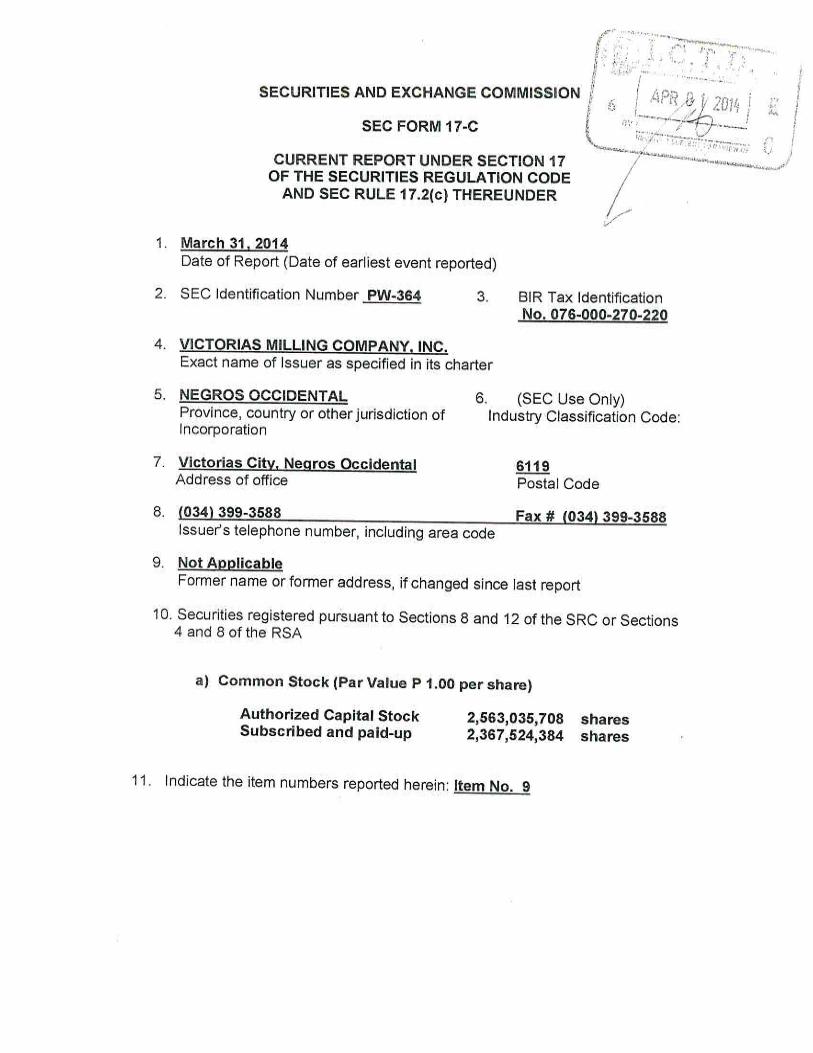

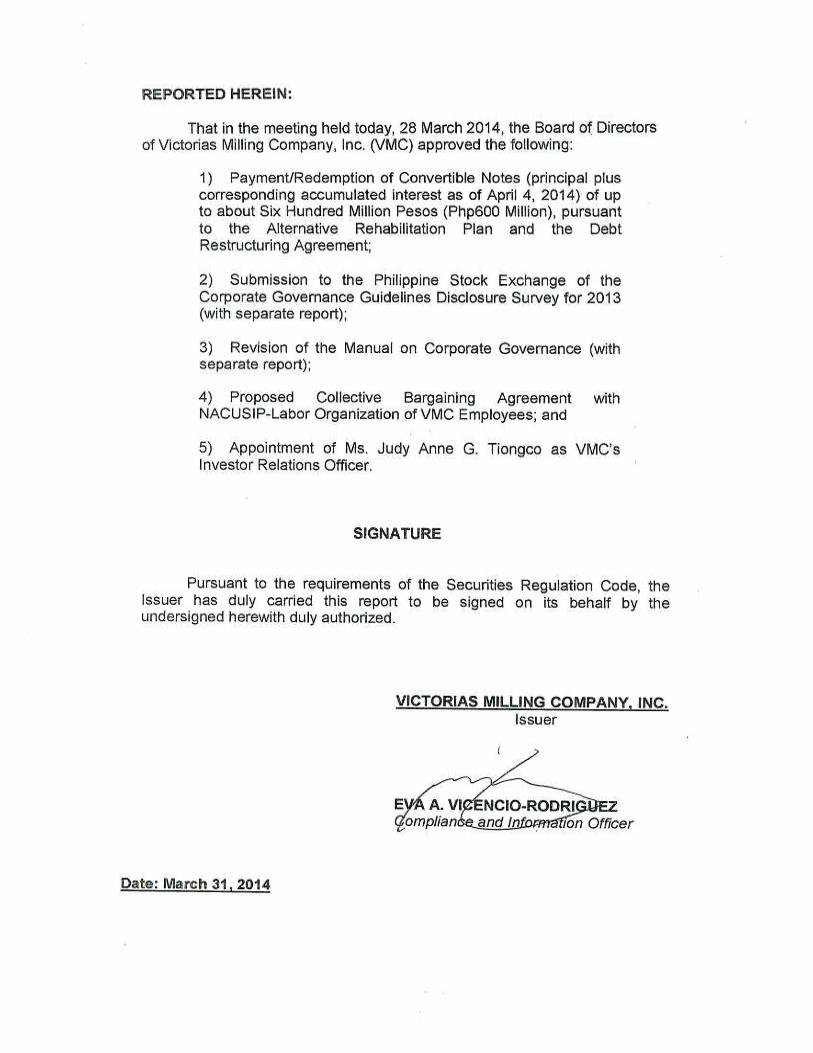

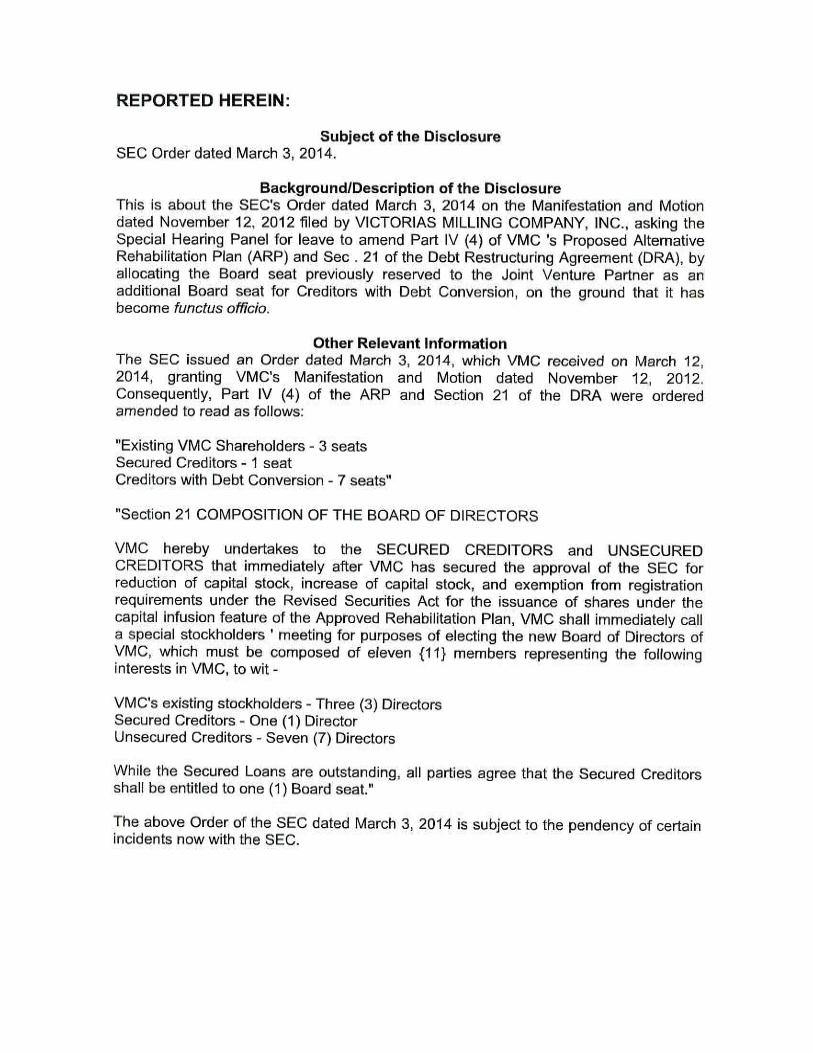

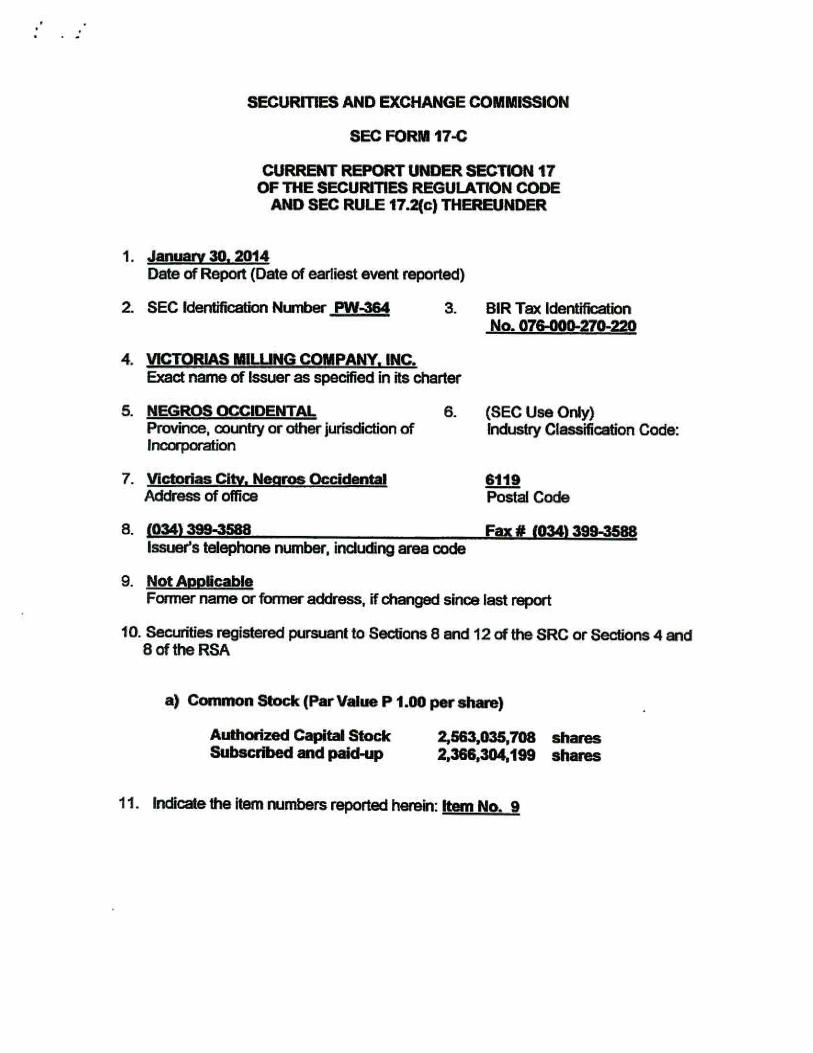

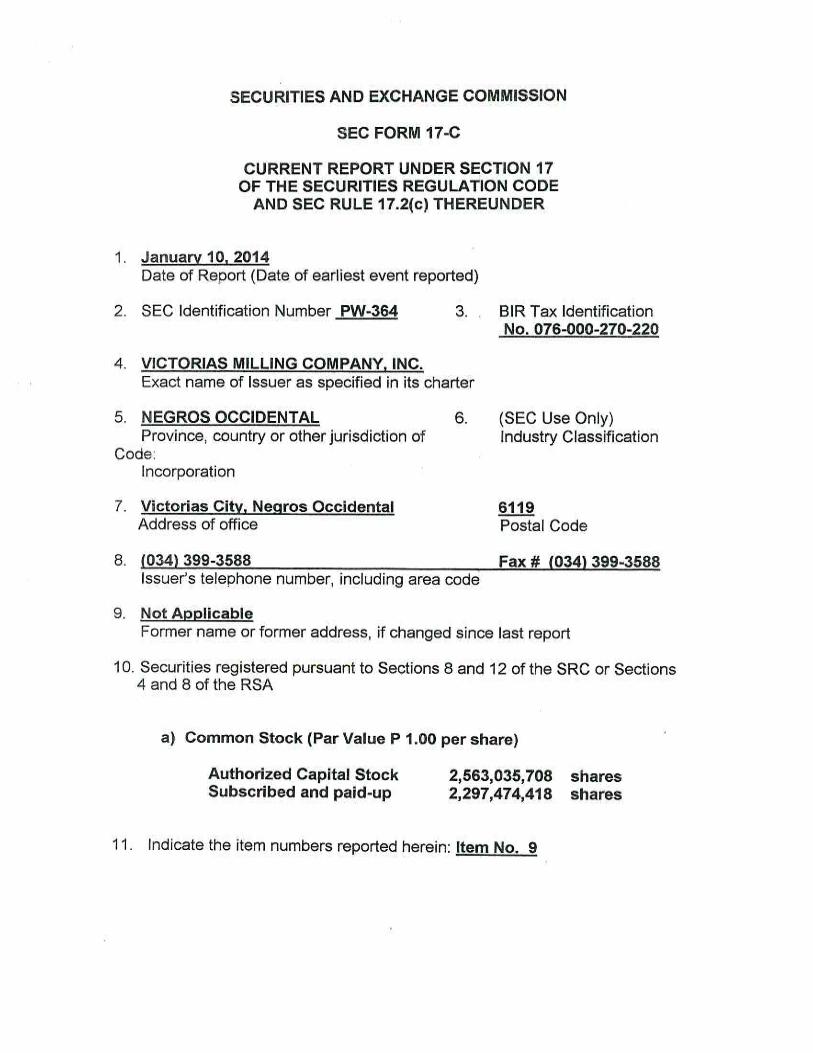

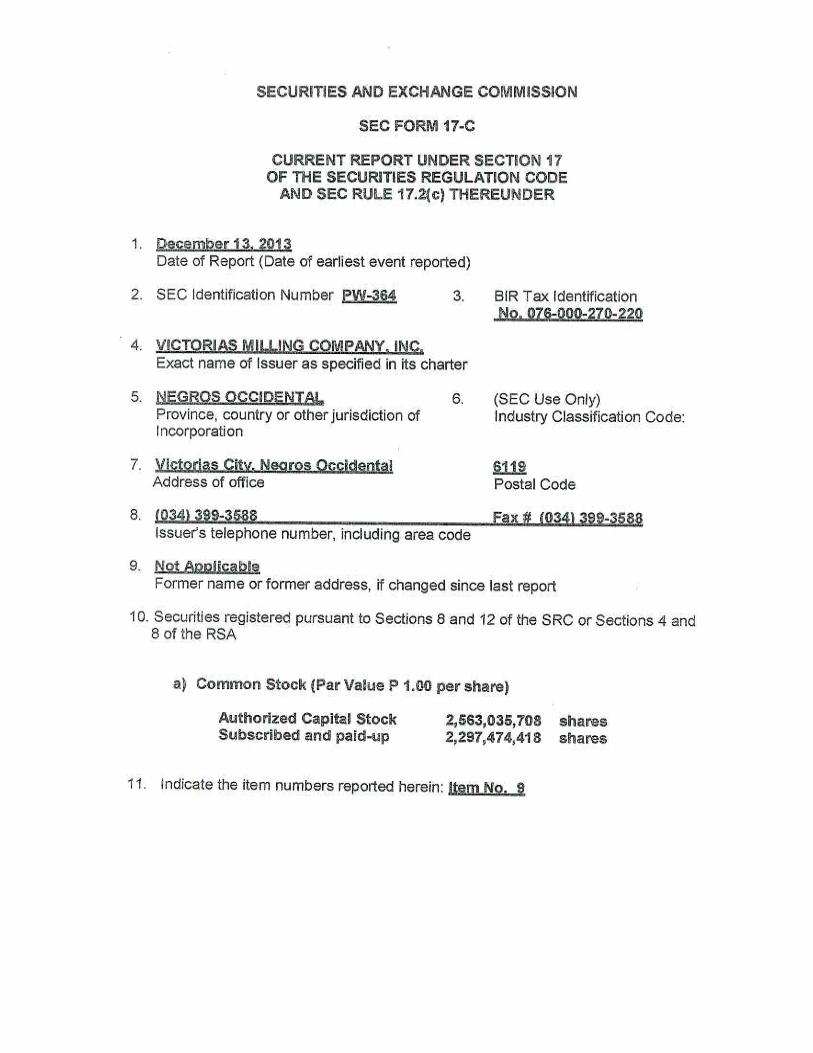

securities and exchange commission - victorias milling · securities and exchange commission sec...

TRANSCRIPT

1

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-A

ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141

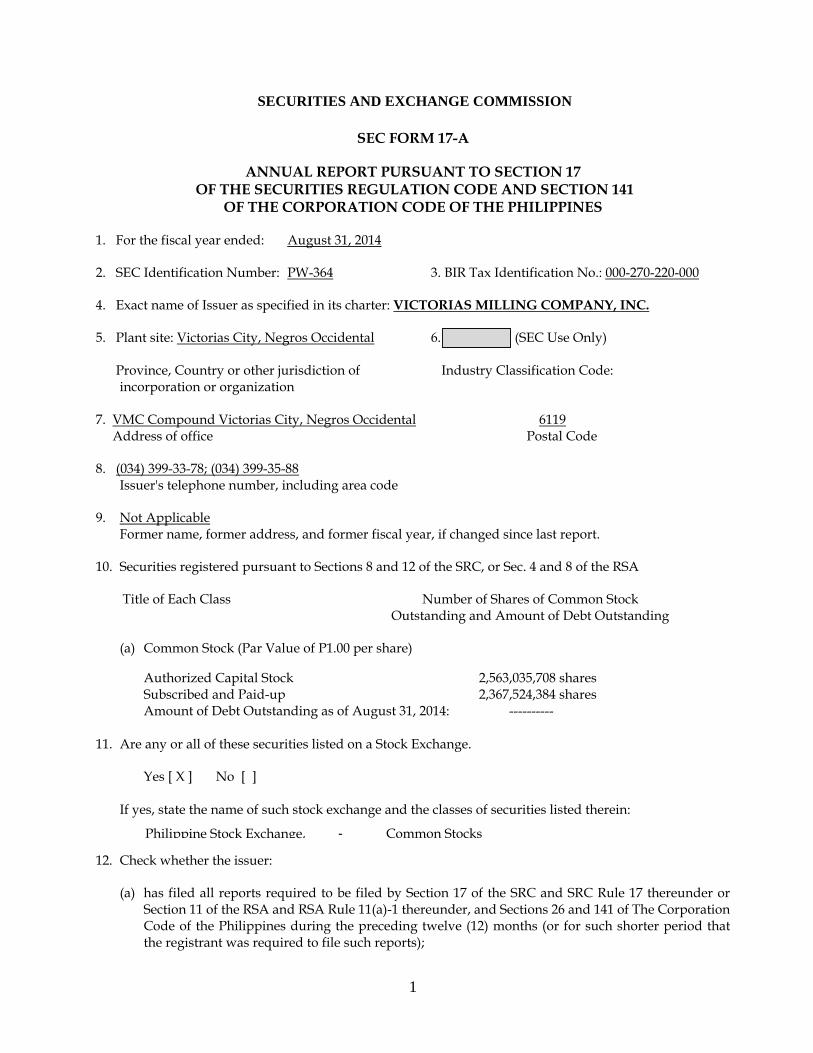

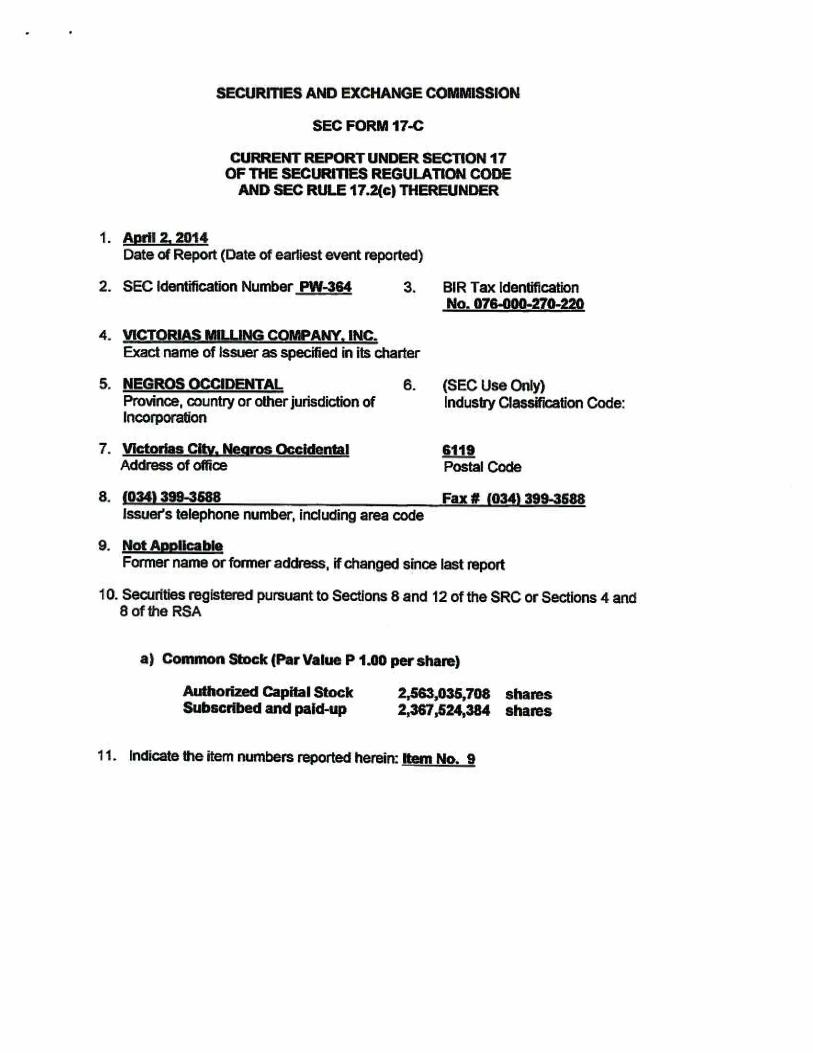

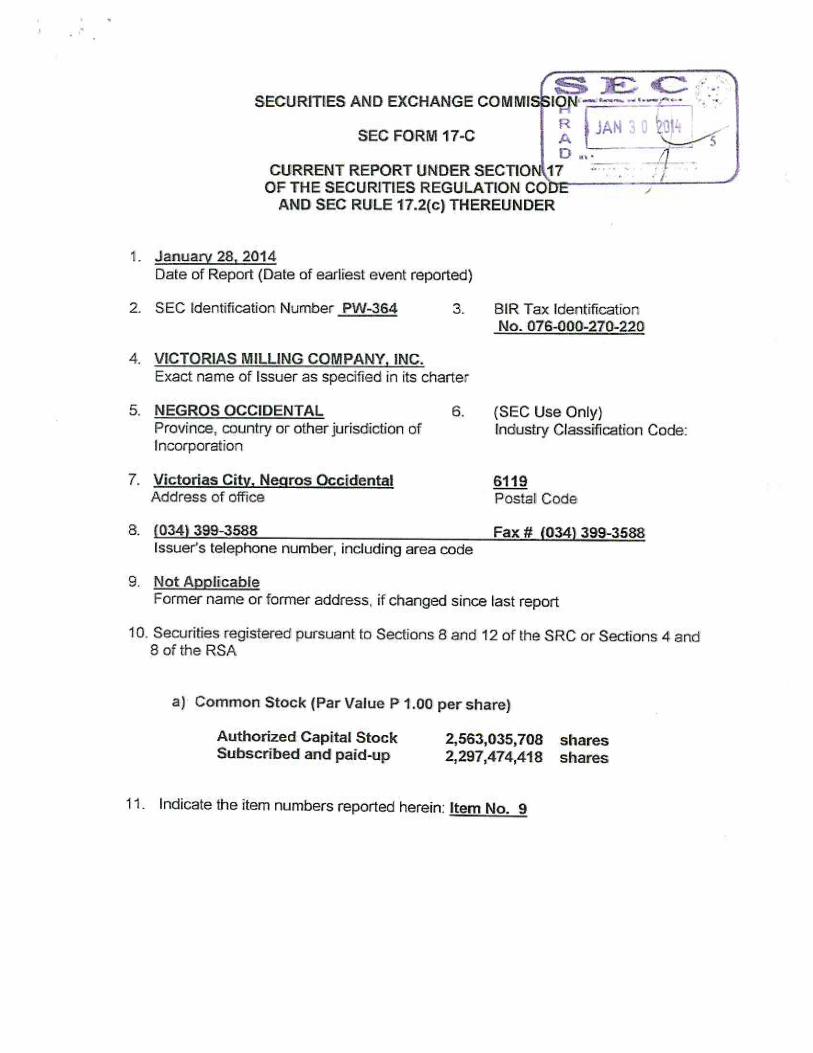

OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended: August 31, 2014 2. SEC Identification Number: PW-364 3. BIR Tax Identification No.: 000-270-220-000 4. Exact name of Issuer as specified in its charter: VICTORIAS MILLING COMPANY, INC. 5. Plant site: Victorias City, Negros Occidental 6. (SEC Use Only)

7. VMC Compound Victorias City, Negros Occidental 6119 Address of office Postal Code 8. (034) 399-33-78; (034) 399-35-88 Issuer's telephone number, including area code 9. Not Applicable Former name, former address, and former fiscal year, if changed since last report. 10. Securities registered pursuant to Sections 8 and 12 of the SRC, or Sec. 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock

Outstanding and Amount of Debt Outstanding

(a) Common Stock (Par Value of P1.00 per share)

Authorized Capital Stock 2,563,035,708 shares Subscribed and Paid-up 2,367,524,384 shares Amount of Debt Outstanding as of August 31, 2014: ---------- 11. Are any or all of these securities listed on a Stock Exchange. Yes [ X ] No [ ] If yes, state the name of such stock exchange and the classes of securities listed therein: 12. Check whether the issuer:

(a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports);

Province, Country or other jurisdiction of incorporation or organization

Industry Classification Code:

Philippine Stock Exchange, - Common Stocks

2

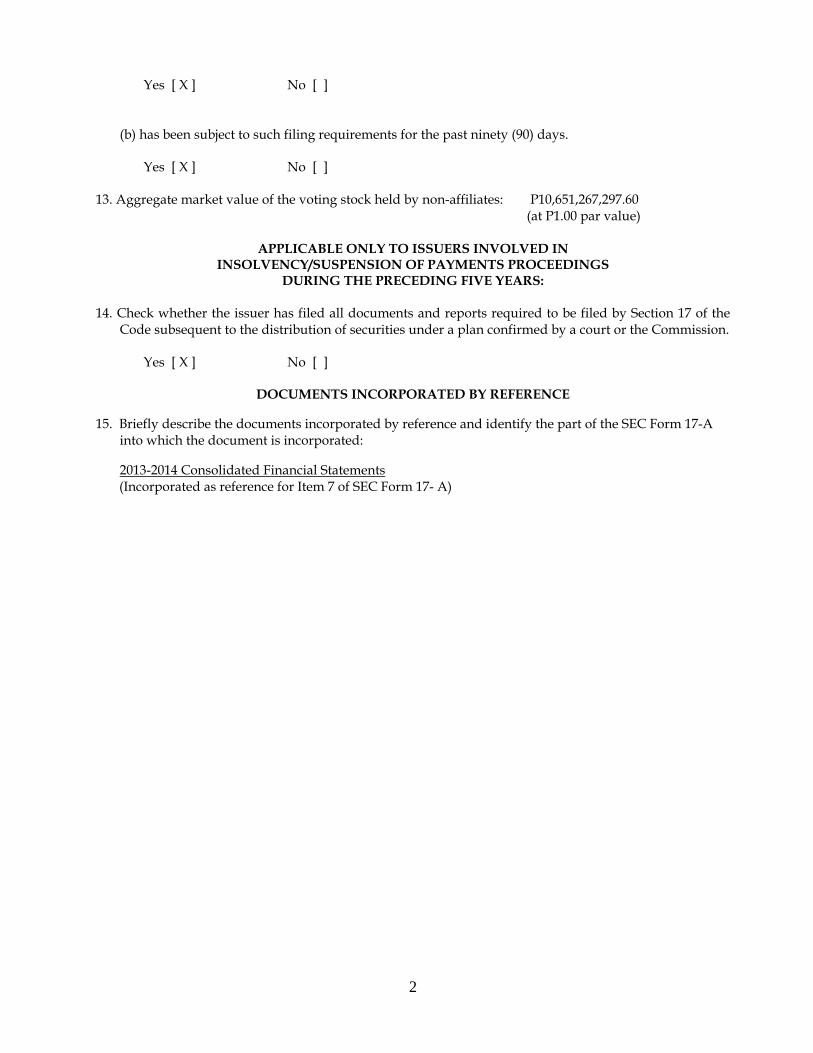

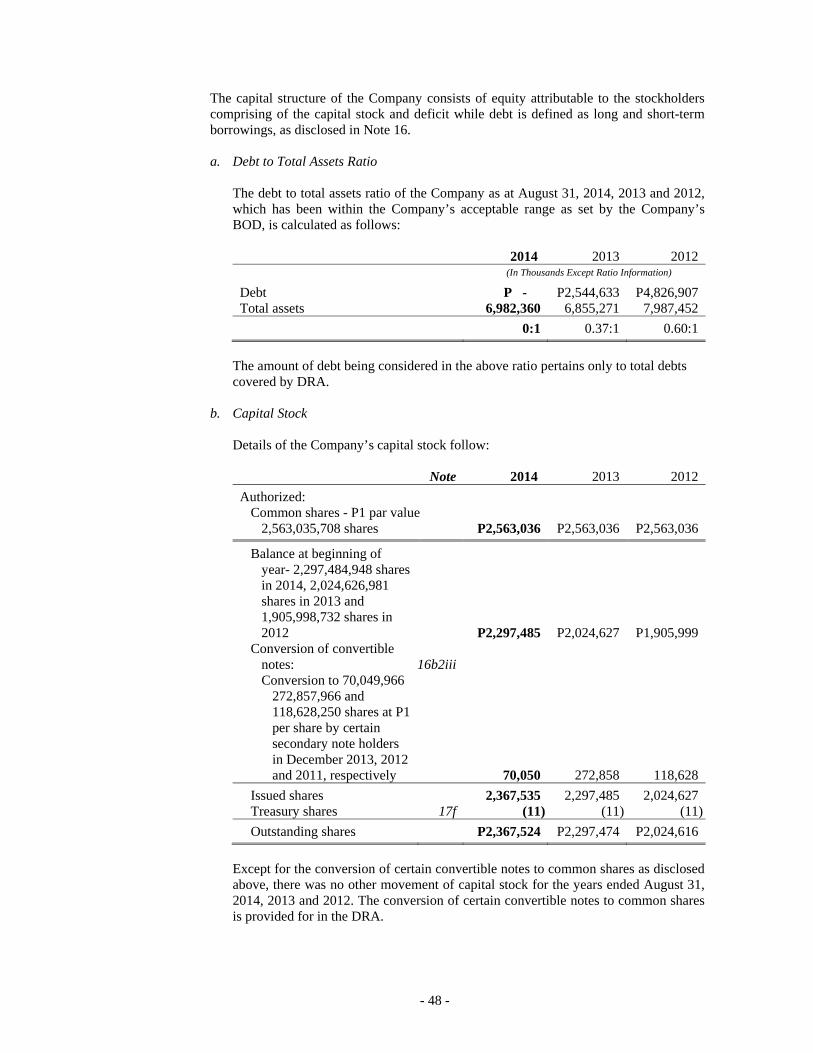

Yes [ X ] No [ ] (b) has been subject to such filing requirements for the past ninety (90) days. Yes [ X ] No [ ] 13. Aggregate market value of the voting stock held by non-affiliates: P10,651,267,297.60

(at P1.00 par value)

APPLICABLE ONLY TO ISSUERS INVOLVED IN INSOLVENCY/SUSPENSION OF PAYMENTS PROCEEDINGS

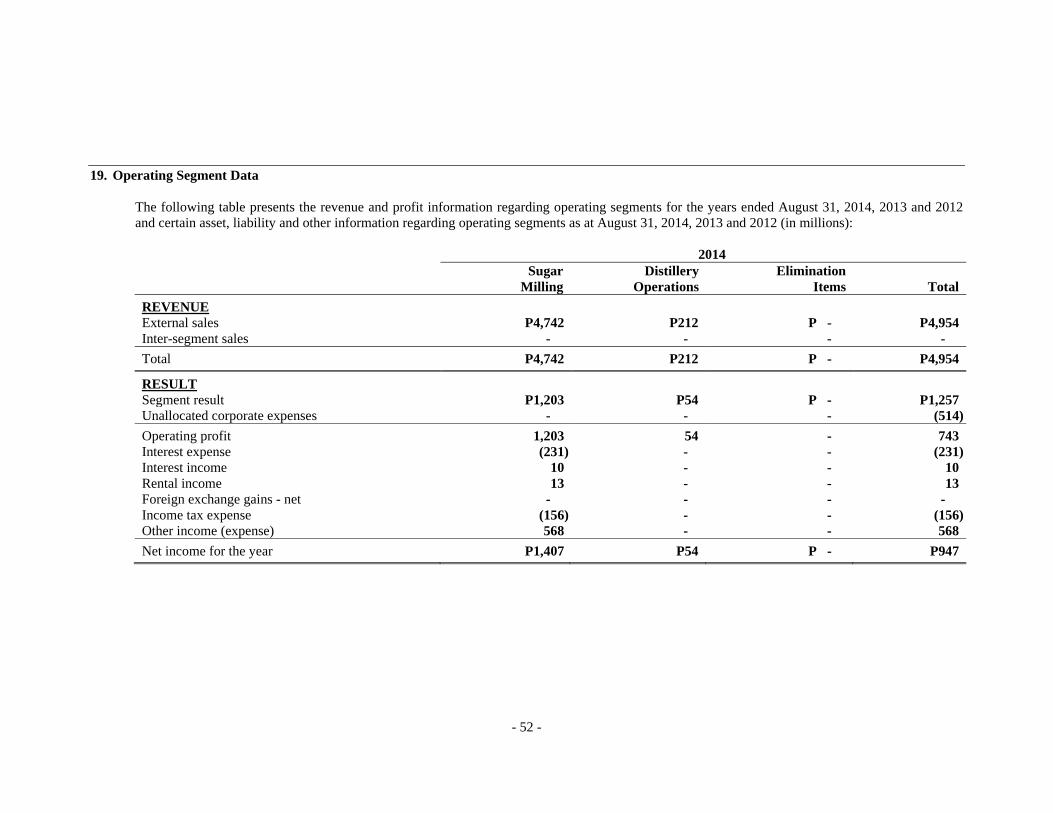

DURING THE PRECEDING FIVE YEARS:

14. Check whether the issuer has filed all documents and reports required to be filed by Section 17 of the Code subsequent to the distribution of securities under a plan confirmed by a court or the Commission.

Yes [ X ] No [ ]

DOCUMENTS INCORPORATED BY REFERENCE 15. Briefly describe the documents incorporated by reference and identify the part of the SEC Form 17-A

into which the document is incorporated: 2013-2014 Consolidated Financial Statements (Incorporated as reference for Item 7 of SEC Form 17- A)

3

TABLE OF CONTENTS PART I - BUSINESS AND GENERAL INFORMATION Page Item 1. Business 4 Item 2. Property 12 Item 3. Legal Proceedings 13 Item 4. Submission of Matters to a Vote of Security Holders 14 PART II - OPERATIONAL AND FINANCIAL INFORMATION Item 5. Market for Issuer’s Common Equity and Related

Stockholder Matters 14

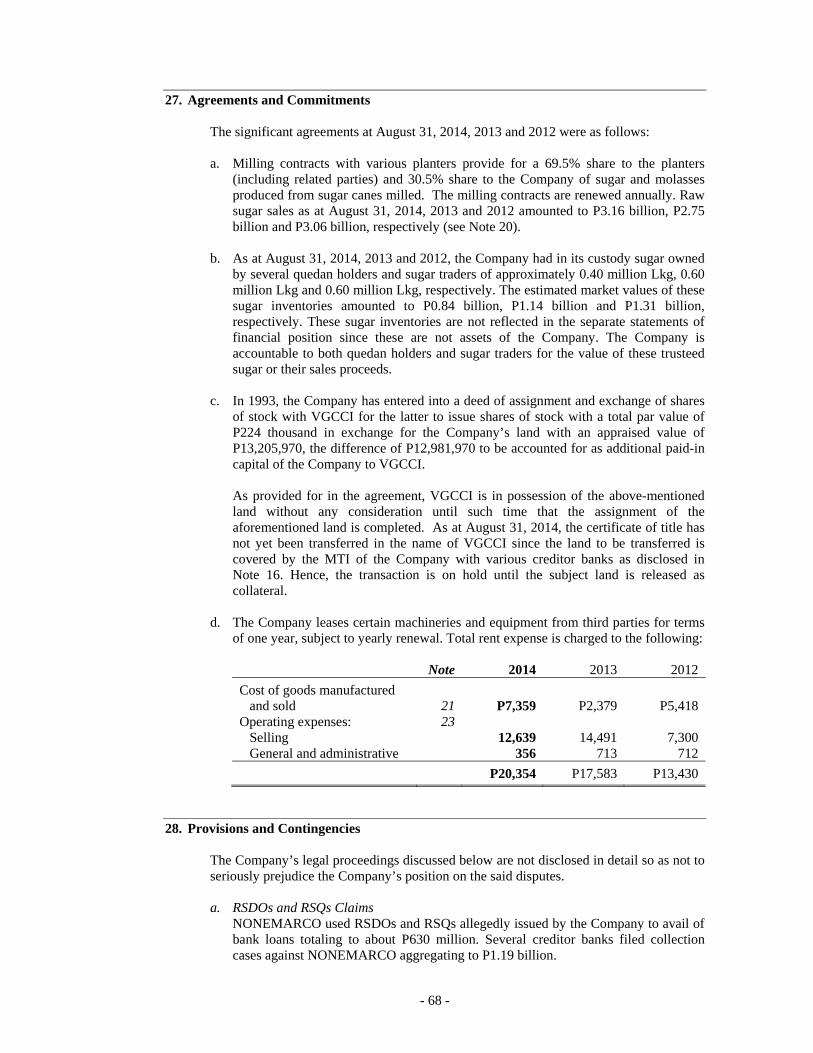

Item 6. Management's Discussion and Analysis or Plan of Operation.

14

Item 7. Financial Statements 22 Item 8. Changes in and Disagreements With Accountants on

Accounting and Financial Disclosure 22

PART III - CONTROL AND COMPENSATION INFORMATION Item 9. Directors and Executive Officers of the Issuer 23 Item 10. Executive Compensation 26 Item 11. Security Ownership of Certain Beneficial Owners and

Management 27

Item 12. Certain Relationships and Related Transactions 27

PART IV – CORPORATE GOVERNANCE Item 13. Corporate Governance 27 PART V- EXHIBITS AND SCHEDULES

28 (a) Exhibits (b) Reports on SEC Form 17-C 28

4

PART I- BUSINESS AND GENERAL INFORMATION

ITEM 1 - BUSINESS DESCRIPTION OF BUSINESS Victorias Milling Company, Inc. (VMC) is a domestic corporation located in Victorias City, Negros Occidental. Since its incorporation on May 7, 1919, VMC has been engaged in integrated raw and refined sugar manufacturing. It also operates engineering services and has the following subsidiaries:

DATE OF REGISTRATION

% Ownership

Description of Business

Victorias Foods Corporation (VFC)

February 24, 1993 100% produces and sells canned sardines, hot bangus, mackerel, luncheon meat, lechon paksiw, ham, bacon and other meat products

Canetown Development Corporation (CDC)

February 9, 1979 88% develops and sells real estate properties; develops, operates and sells memorial lots

Victorias Golf and Country Club, Inc. (VGCCI)

May 5, 1994 81% operates a golf club

Victorias Agricultural Land Corporation (VALCO)

June 30, 1987 100% acquires and owns agricultural lands and properties

BUSINESS DEVELOPMENT DURING THE PAST THREE (3) YEARS

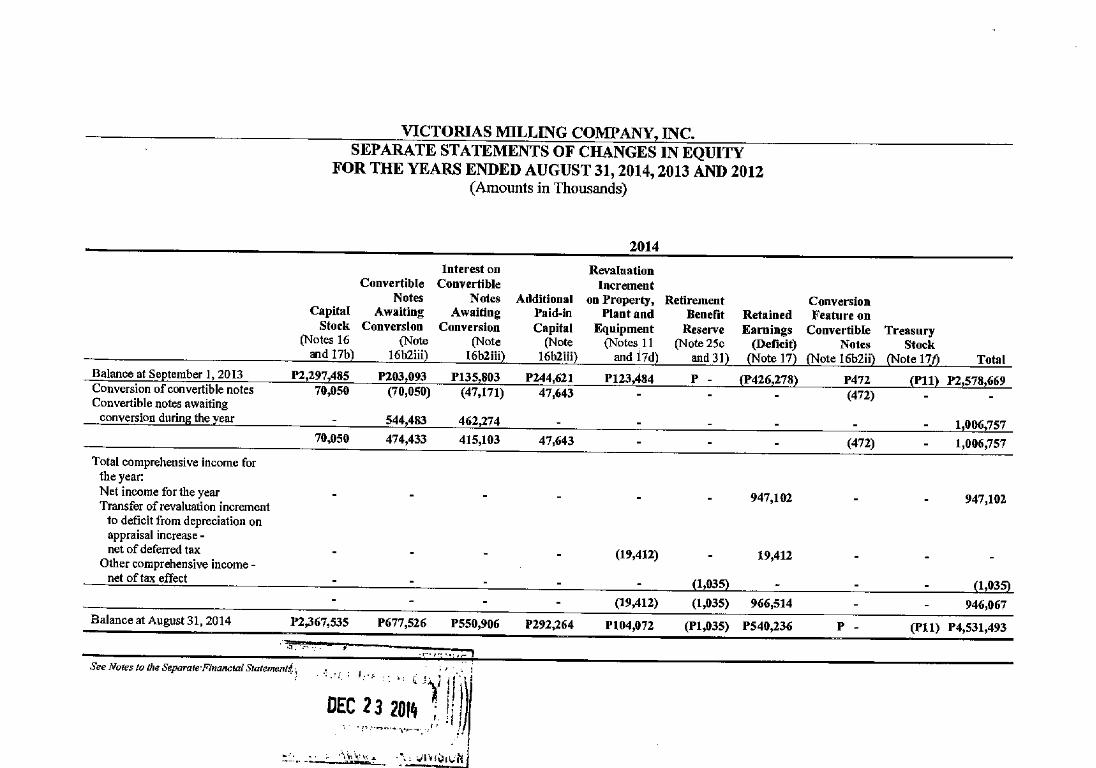

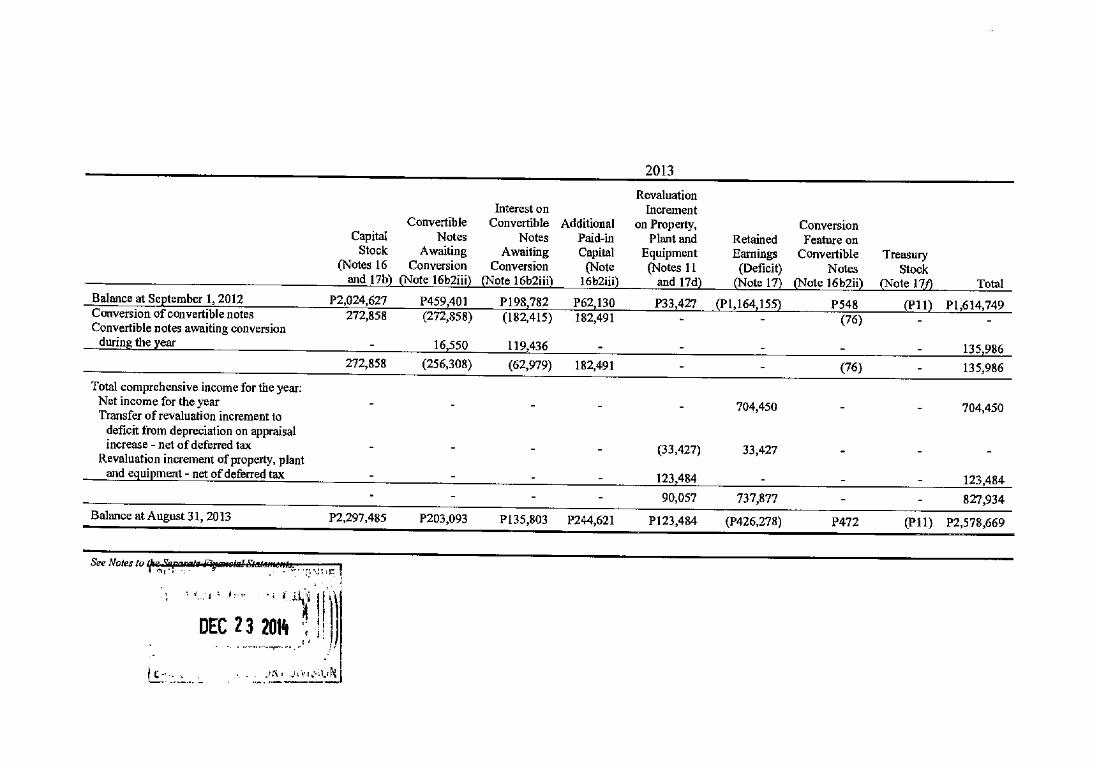

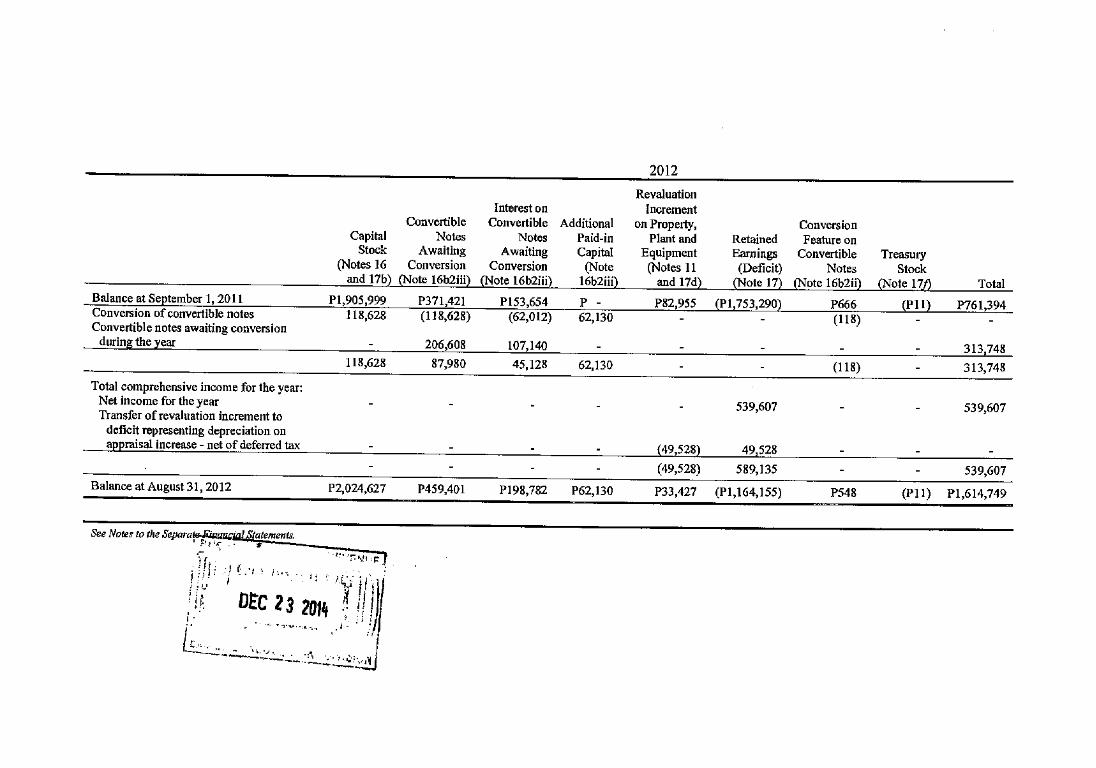

VMC is serious in its efforts to further improve its efficiency as well as product quality and the same are manifested in different major expansion programs for the past three (3) years. The unprecedented expansion programs resulted to high milling efficiency rates for Crop Years 2009-2010 and 2010-2011 by milling 2,552,299 MT and 3,115,914 MT, respectively. For Crop Year 2011-2012, VMC milled 3,100,509 tonnes cane, producing 6,400,064 Lkg. raw sugar, slightly lower by 15,405 tonnes cane from last crop year’s 3,115,914 tonnes cane, lower by 99,491 tonnes cane or three (3%) percent from the projection of 3.2 million tonnes cane. Although this production is lower than the previous crop year, VMC has retained its leadership when it comes to tons cane milled in the province with 25.82% share. CURRENT STATUS OF REHABILITATION PROGRAM In 1997, VMC filed with the Securities and Exchange Commission (SEC) a Petition for the Declaration of Suspension of Payments, and for the Approval of a Rehabilitation Plan. VMC’s total principal obligations and interest at that time stood at P7.9 Billion. Part of the rehabilitation plan was the restructuring of P4.4 Billion of debt over a period of fifteen (15) years beginning on 1 September 2003. Over the years, VMC has continued to pay its creditors in accordance with the scheduled amortization payments of its restructured debts. In fiscal year 2013-2014, VMC paid in full the remaining restructured loans to its secured and unsecured creditors. Another component of the rehabilitation plan was the conversion of P2.4 Billion of debt into convertible notes (CNs) and the conversion of the CNs into equity in accordance with the conversion schedules as provided for in the Debt Restructuring Agreement (DRA). As of FY 2013-2014, VMC has converted a total of P702 Million convertible notes into common shares at the ratio of P1 convertible note to 1 common share. P273 Million worth of debts were converted in 2013, while P429 Million convertible notes were converted in previous years.

5

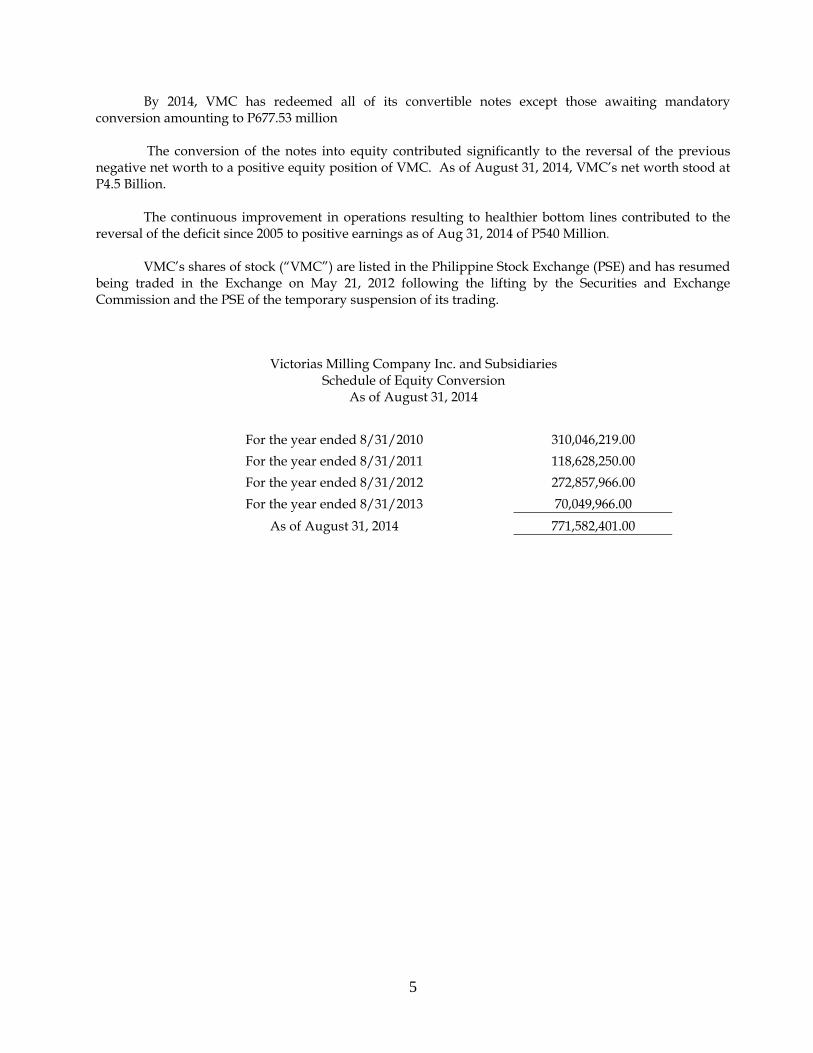

By 2014, VMC has redeemed all of its convertible notes except those awaiting mandatory conversion amounting to P677.53 million The conversion of the notes into equity contributed significantly to the reversal of the previous negative net worth to a positive equity position of VMC. As of August 31, 2014, VMC’s net worth stood at P4.5 Billion. The continuous improvement in operations resulting to healthier bottom lines contributed to the reversal of the deficit since 2005 to positive earnings as of Aug 31, 2014 of P540 Million. VMC’s shares of stock (“VMC”) are listed in the Philippine Stock Exchange (PSE) and has resumed being traded in the Exchange on May 21, 2012 following the lifting by the Securities and Exchange Commission and the PSE of the temporary suspension of its trading.

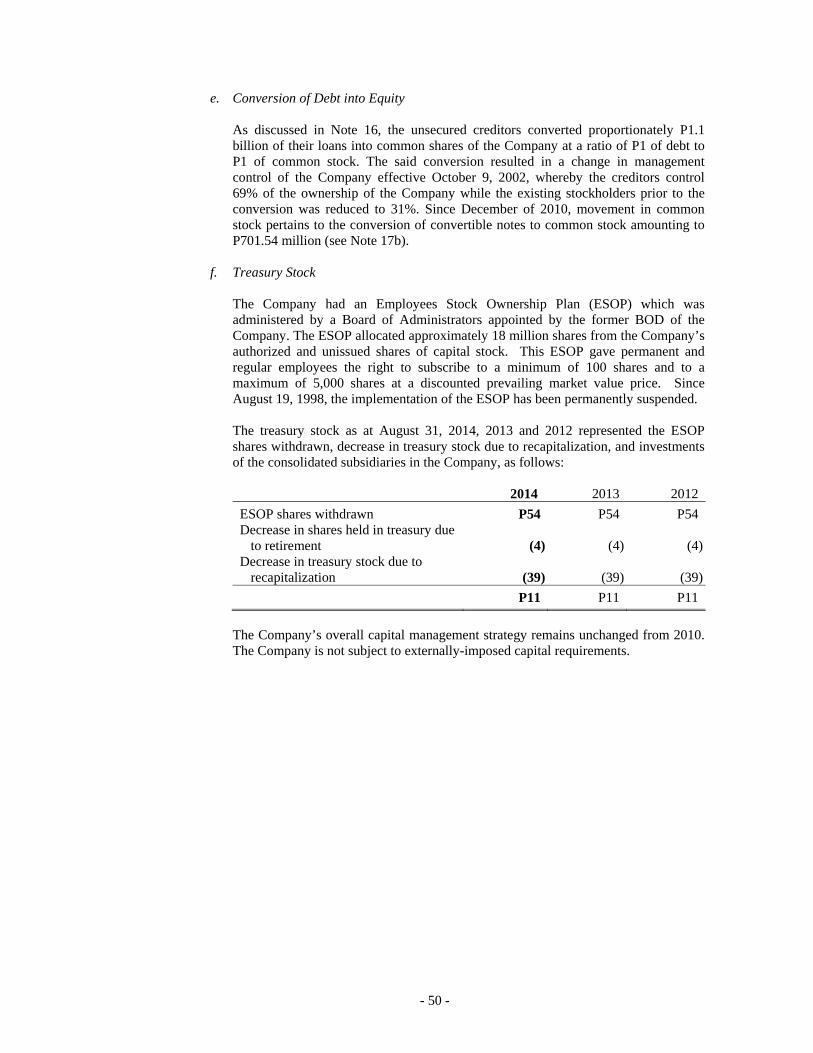

Victorias Milling Company Inc. and Subsidiaries Schedule of Equity Conversion

As of August 31, 2014

For the year ended 8/31/2010 310,046,219.00 For the year ended 8/31/2011 118,628,250.00 For the year ended 8/31/2012 272,857,966.00 For the year ended 8/31/2013 70,049,966.00

As of August 31, 2014 771,582,401.00

6

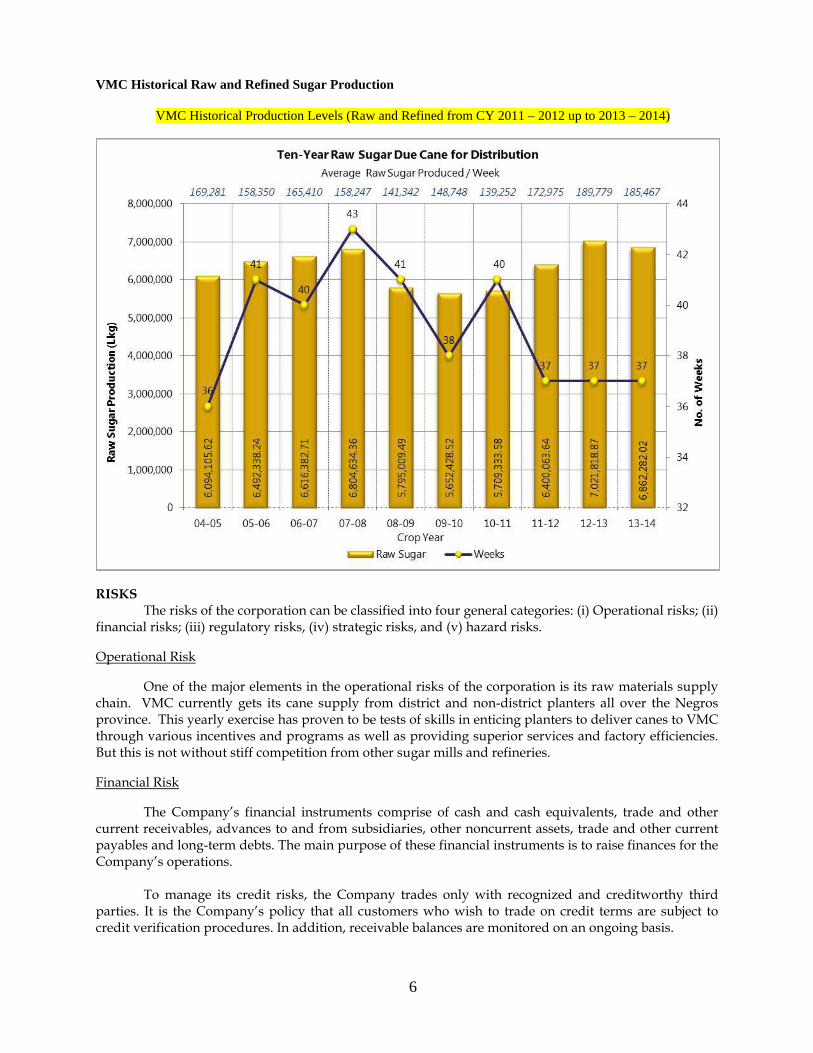

VMC Historical Raw and Refined Sugar Production

VMC Historical Production Levels (Raw and Refined from CY 2011 – 2012 up to 2013 – 2014)

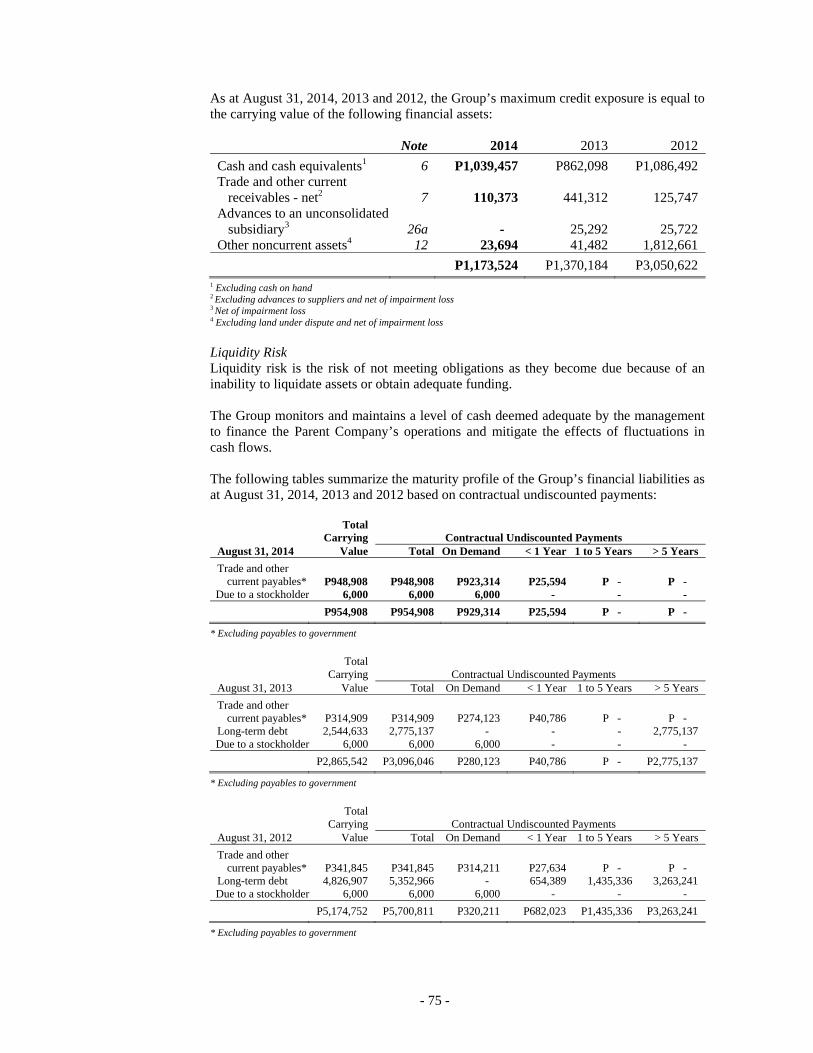

RISKS The risks of the corporation can be classified into four general categories: (i) Operational risks; (ii) financial risks; (iii) regulatory risks, (iv) strategic risks, and (v) hazard risks. Operational Risk One of the major elements in the operational risks of the corporation is its raw materials supply chain. VMC currently gets its cane supply from district and non-district planters all over the Negros province. This yearly exercise has proven to be tests of skills in enticing planters to deliver canes to VMC through various incentives and programs as well as providing superior services and factory efficiencies. But this is not without stiff competition from other sugar mills and refineries. Financial Risk The Company’s financial instruments comprise of cash and cash equivalents, trade and other current receivables, advances to and from subsidiaries, other noncurrent assets, trade and other current payables and long-term debts. The main purpose of these financial instruments is to raise finances for the Company’s operations. To manage its credit risks, the Company trades only with recognized and creditworthy third parties. It is the Company’s policy that all customers who wish to trade on credit terms are subject to credit verification procedures. In addition, receivable balances are monitored on an ongoing basis.

7

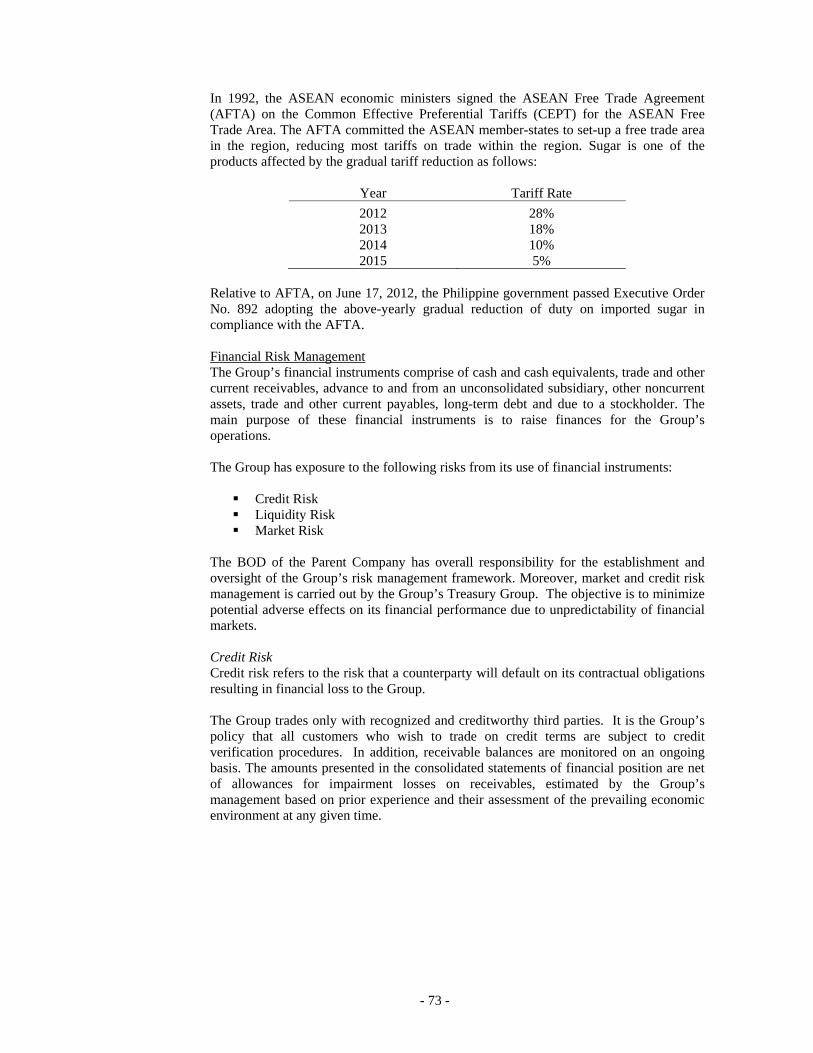

Regulatory risk The Company is subject to laws and regulations in the Philippines in which it operates. The Company has established policies and procedures in compliance with local and other laws. Management performs regular reviews to identify compliance risks and to ensure that the systems in place are adequate to manage those risks. One key element is its compliance to environmental regulatory requirements. One of the longest running environmental issues is the Cease and Desist order issued to VMC in 1989 due to air pollution concerns. This was exacerbated with VMC being under rehabilitation, having financial constraints to invest on anti-pollution equipment. To date however, VMC has installed eight (8) scrubbers on its smoke stacks and expects to be fully compliant with the air emission standards of the DENR. Another imminent risk is the gradual tariff reduction on imported sugar, which, by 2015, will go down to only 5%. This exposes the sugar industry as a whole to global competition that if not prepared for, will drastically change the financial viability of the corporation, in particular. Strategic Risk Competition and industry changes form part of strategic risks to which VMC is exposed. The sugar industry has been threatened by the ethanol industry, which also uses sugarcane as raw material. Fortunately, the ethanol business has yet to stabilize as a new industry under threats from world oil prices. Change in customer demand is something that VMC should also be concerned of to ensure that its product specifications suit the dynamics of its customers. VMC is also fully exposed to the risks of the extreme weather conditions. The recent typhoon Yolanda is expected to cause damage to cane crops and thereby reduce tonnage. Since its business is agriculturally-based, weather is a very critical factor for a successful crop year. Low farm inputs from planters will translate to low production that will trigger stiff cane competition among sugar millers in the region and will affect the price following supply and demand forces. The numerous legal cases are likewise a source of risk for the Corporation. Collection cases versus the Corporation are currently under suspension, with VMC being under corporate rehabilitation. The potential impact of these cases on the corporation once the suspension is lifted is continually being assessed. GOVERNMENT LICENSES REQUIRED

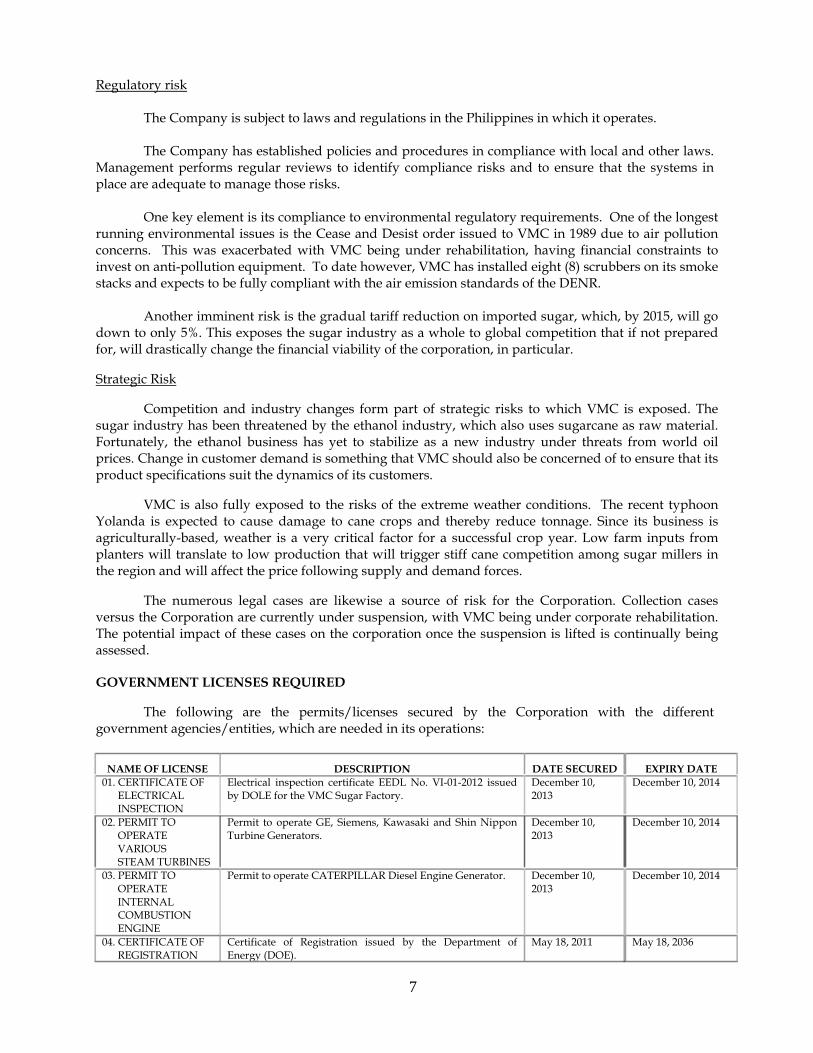

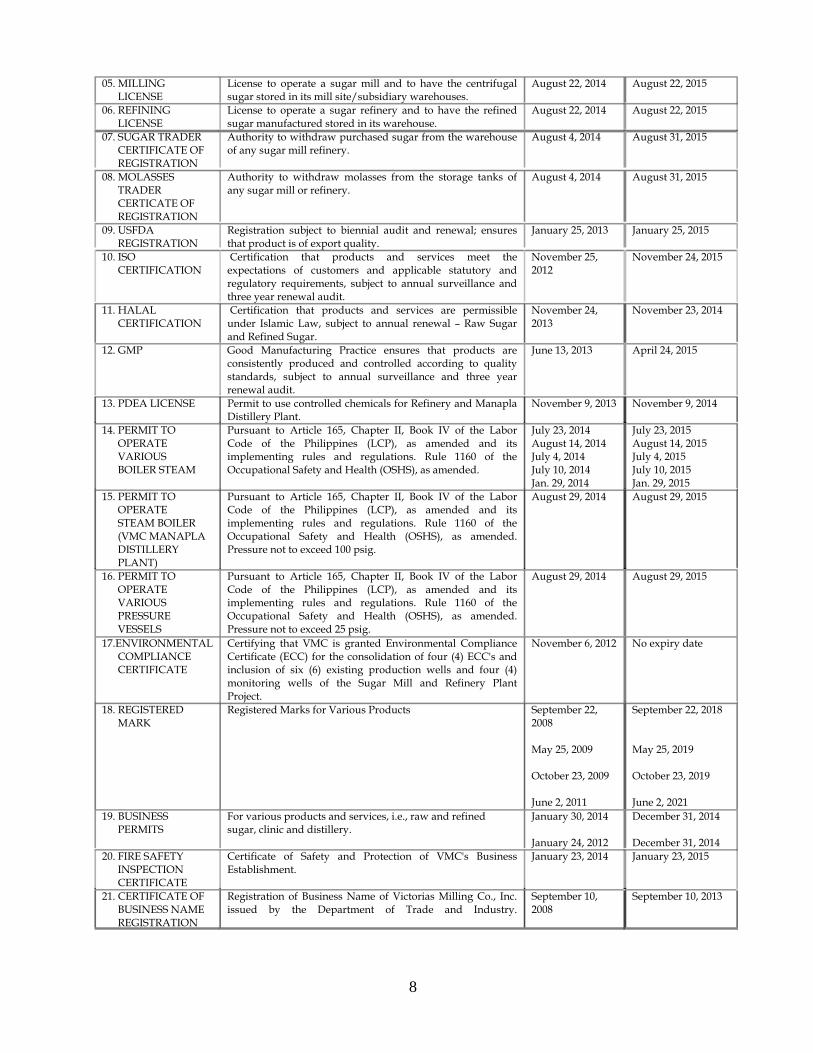

The following are the permits/licenses secured by the Corporation with the different government agencies/entities, which are needed in its operations:

NAME OF LICENSE DESCRIPTION DATE SECURED EXPIRY DATE 01. CERTIFICATE OF ELECTRICAL INSPECTION

Electrical inspection certificate EEDL No. VI-01-2012 issued by DOLE for the VMC Sugar Factory.

December 10, 2013

December 10, 2014

02. PERMIT TO OPERATE VARIOUS STEAM TURBINES

Permit to operate GE, Siemens, Kawasaki and Shin Nippon Turbine Generators.

December 10, 2013

December 10, 2014

03. PERMIT TO OPERATE INTERNAL COMBUSTION ENGINE

Permit to operate CATERPILLAR Diesel Engine Generator. December 10, 2013

December 10, 2014

04. CERTIFICATE OF REGISTRATION

Certificate of Registration issued by the Department of Energy (DOE).

May 18, 2011 May 18, 2036

8

05. MILLING LICENSE

License to operate a sugar mill and to have the centrifugal sugar stored in its mill site/subsidiary warehouses.

August 22, 2014 August 22, 2015

06. REFINING LICENSE

License to operate a sugar refinery and to have the refined sugar manufactured stored in its warehouse.

August 22, 2014 August 22, 2015

07. SUGAR TRADER CERTIFICATE OF REGISTRATION

Authority to withdraw purchased sugar from the warehouse of any sugar mill refinery.

August 4, 2014 August 31, 2015

08. MOLASSES TRADER CERTICATE OF REGISTRATION

Authority to withdraw molasses from the storage tanks of any sugar mill or refinery.

August 4, 2014 August 31, 2015

09. USFDA REGISTRATION

Registration subject to biennial audit and renewal; ensures that product is of export quality.

January 25, 2013 January 25, 2015

10. ISO CERTIFICATION

Certification that products and services meet the expectations of customers and applicable statutory and regulatory requirements, subject to annual surveillance and three year renewal audit.

November 25, 2012

November 24, 2015

11. HALAL CERTIFICATION

Certification that products and services are permissible under Islamic Law, subject to annual renewal – Raw Sugar and Refined Sugar.

November 24, 2013

November 23, 2014

12. GMP Good Manufacturing Practice ensures that products are consistently produced and controlled according to quality standards, subject to annual surveillance and three year renewal audit.

June 13, 2013 April 24, 2015

13. PDEA LICENSE Permit to use controlled chemicals for Refinery and Manapla Distillery Plant.

November 9, 2013 November 9, 2014

14. PERMIT TO OPERATE VARIOUS BOILER STEAM

Pursuant to Article 165, Chapter II, Book IV of the Labor Code of the Philippines (LCP), as amended and its implementing rules and regulations. Rule 1160 of the Occupational Safety and Health (OSHS), as amended.

July 23, 2014 August 14, 2014 July 4, 2014 July 10, 2014 Jan. 29, 2014

July 23, 2015 August 14, 2015 July 4, 2015 July 10, 2015 Jan. 29, 2015

15. PERMIT TO OPERATE STEAM BOILER (VMC MANAPLA DISTILLERY PLANT)

Pursuant to Article 165, Chapter II, Book IV of the Labor Code of the Philippines (LCP), as amended and its implementing rules and regulations. Rule 1160 of the Occupational Safety and Health (OSHS), as amended. Pressure not to exceed 100 psig.

August 29, 2014 August 29, 2015

16. PERMIT TO OPERATE VARIOUS PRESSURE VESSELS

Pursuant to Article 165, Chapter II, Book IV of the Labor Code of the Philippines (LCP), as amended and its implementing rules and regulations. Rule 1160 of the Occupational Safety and Health (OSHS), as amended. Pressure not to exceed 25 psig.

August 29, 2014 August 29, 2015

17.ENVIRONMENTAL COMPLIANCE CERTIFICATE

Certifying that VMC is granted Environmental Compliance Certificate (ECC) for the consolidation of four (4) ECC's and inclusion of six (6) existing production wells and four (4) monitoring wells of the Sugar Mill and Refinery Plant Project.

November 6, 2012 No expiry date

18. REGISTERED MARK

Registered Marks for Various Products September 22, 2008 May 25, 2009 October 23, 2009 June 2, 2011

September 22, 2018 May 25, 2019 October 23, 2019 June 2, 2021

19. BUSINESS PERMITS

For various products and services, i.e., raw and refined sugar, clinic and distillery.

January 30, 2014 January 24, 2012

December 31, 2014 December 31, 2014

20. FIRE SAFETY INSPECTION CERTIFICATE

Certificate of Safety and Protection of VMC's Business Establishment.

January 23, 2014 January 23, 2015

21. CERTIFICATE OF BUSINESS NAME REGISTRATION

Registration of Business Name of Victorias Milling Co., Inc. issued by the Department of Trade and Industry.

September 10, 2008

September 10, 2013

9

22. LICENSE TO OPERATE

License to Operate as a Food Manufacturer of Sugar issued by the Department of Health Bureau of Food and Drugs Pursuant to Section 4(e) Chapter III of Republic Act No. 3720, otherwise known as the Foods, Drugs and Devices and Cosmetics Act.

March 21, 2012 April 24, 2015

23. CERTIFICATE OF ELIGIBILITY

Certificate of Eligibility issued by the Department of Agriculture certifying that VMC is an agriculture enterprise corporation engaged in Sugarcane Milling and therefore eligible for tariff-exempt importation of agricultural inputs, machinery and equipment.

October 9, 2014 October 9, 2015

24. BIR IMPORTER CLEARANCE CERTIFICATE

Certificate of Accreditation as Importer issued by the Bureau of Internal Revenue.

September 12, 2014

Provisional for 6-months period

25. ICARE CERTIFICATE OF ACCREDITATION

Certificate of Accreditation as Importer issued by the Bureau of Customs

September 12, 2014

Provisional for 6-months period

26. CERTIFICATE OF REGISTRATION

Certificate of Registration issued by the Bureau of Customs (BOC).

September 12, 2014

Provisional for 6-months period

27. NATIONAL WATER RESOURCES BOARD (NWRB) PERMIT

Permit to use water from various water sources. May 2012 Conditional permit until September 18, 2013

28. ENERGY REGULATORY COMMISSION CERTIFICATE OF COMPLIANCE

VMC is entitled to all the rights and privileges subject Section 38 of Republic Act No. 9136 (RA 9136).

January 21, 2014 January 21, 2019

All obligations of VMC pertinent to the abovementioned licenses and permits are religiously

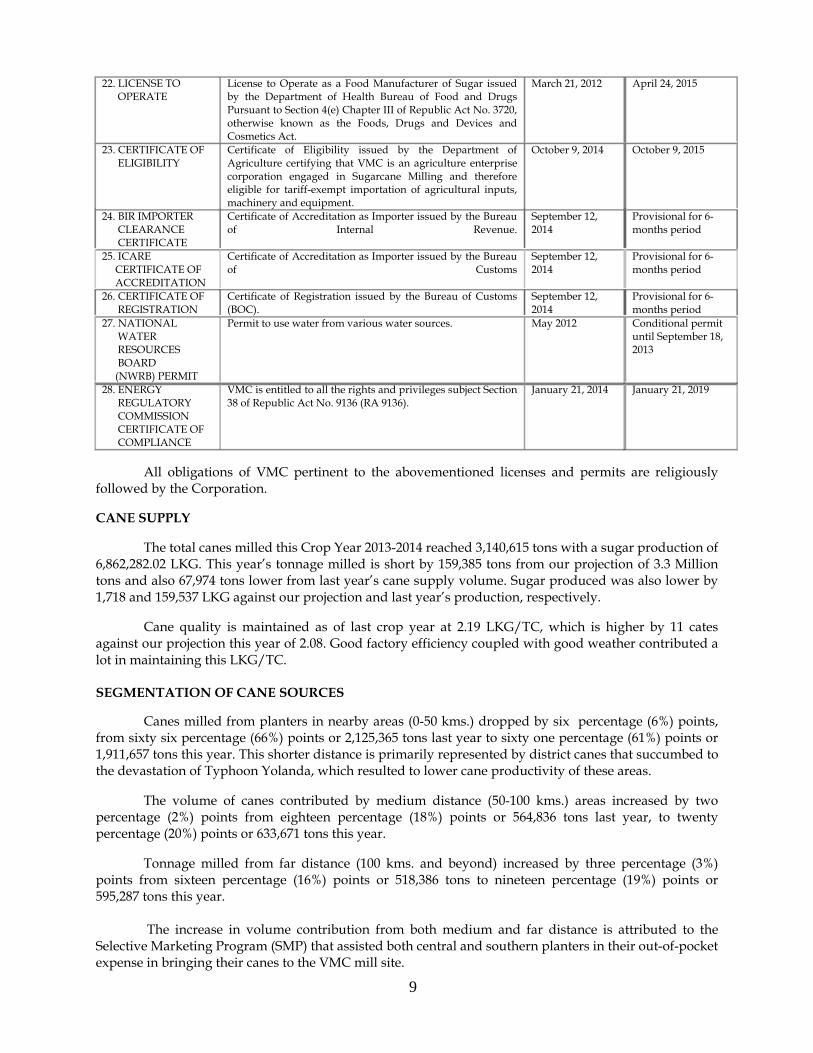

followed by the Corporation. CANE SUPPLY

The total canes milled this Crop Year 2013-2014 reached 3,140,615 tons with a sugar production of 6,862,282.02 LKG. This year’s tonnage milled is short by 159,385 tons from our projection of 3.3 Million tons and also 67,974 tons lower from last year’s cane supply volume. Sugar produced was also lower by 1,718 and 159,537 LKG against our projection and last year’s production, respectively. Cane quality is maintained as of last crop year at 2.19 LKG/TC, which is higher by 11 cates against our projection this year of 2.08. Good factory efficiency coupled with good weather contributed a lot in maintaining this LKG/TC. SEGMENTATION OF CANE SOURCES

Canes milled from planters in nearby areas (0-50 kms.) dropped by six percentage (6%) points, from sixty six percentage (66%) points or 2,125,365 tons last year to sixty one percentage (61%) points or 1,911,657 tons this year. This shorter distance is primarily represented by district canes that succumbed to the devastation of Typhoon Yolanda, which resulted to lower cane productivity of these areas. The volume of canes contributed by medium distance (50-100 kms.) areas increased by two percentage (2%) points from eighteen percentage (18%) points or 564,836 tons last year, to twenty percentage (20%) points or 633,671 tons this year.

Tonnage milled from far distance (100 kms. and beyond) increased by three percentage (3%) points from sixteen percentage (16%) points or 518,386 tons to nineteen percentage (19%) points or 595,287 tons this year.

The increase in volume contribution from both medium and far distance is attributed to the

Selective Marketing Program (SMP) that assisted both central and southern planters in their out-of-pocket expense in bringing their canes to the VMC mill site.

10

Relating to the province, VMC shared 23.73% on total cane of 13,232,469 million tonnes, a decrease of 1.99% points from 25.72% points of the previous year. The decrease of VMC’s share in the province is attributed to the delay in start-up and the devastating effect of the strong typhoon that hit Northern Negros especially the district area. SERVICES TO PLANTERS

Cane supply is VMC’s major contributor for success. Hence for many years, the Corporation has considered its services to planters to be as important as maintaining the high efficiency of its operations. Incentive Programs are launched every now and then and the farm road repairs activities are on-going.

OVER-ALL CANE SUPPLY TREND AND COMPETITION BASED ON SUGAR REGULATORY ADMINISTRATION RECORDS FOR CY 2011-2012 to CY 2013-2014

Cane supply for the last three years (C. Y. 2011-2012 to 2013-2014) was maintained above the 3

million mark. This was due to our maintained factory efficiency that is being sought for by more planters and also due to favorable weather that brought in higher cane productivity in the province. Moreover, better sugar prices gave sugarcane planters the opportunity to put in the necessary farm inputs to attain higher farm productivity.

Other mills have also implemented improvements in their factory especially on their capacity and

efficiency. Some have ventured into power generation. Because of this, competition of the sugar mills is getting stiffer in so far as their quest for bigger slice of the province’s cane supply is concerned.

2012-2013ACTUAL PROJECTION ACTUAL TCM PERCENT TCM PERCENT

I. VICT. MPLA, CADIZ AREAS

TCM 1,156,519.08 1,262,600 1,254,285.17 (106,081) -8% (97,766) -8%

LKG SUGAR 2,532,776.79 2,626,208 2,741,894.49 (93,431) -4% (209,118) -8%

LKG/TC 2.19 2.08 2.19 0.11 5% - 0%

II. OTHER AREAS

TCM 1,984,095.81 2,037,400 1,954,303.37 (53,304) -3% 29,792 2%

LKG SUGAR 4,329,505.23 4,237,792 4,279,924.38 91,713 2% 49,581 1%

LKG/TC 2.18 2.08 2.19 0.10 5% (0.01) 0%

III. GRAND TOTAL

TCM 3,140,614.89 3,300,000 3,208,588.54 (159,385) -5% (67,974) -2%

LKG SUGAR 6,862,282.02 6,864,000 7,021,818.87 (1,718) 0% (159,537) -2%

LKG/TC 2.19 2.08 2.19 0.11 5% (0.00) 0%

2013-2014 PROJ C. Y. 2012-2013INCREASE / (DECREASE)

CANE & SUGAR PRODUCTION COMPARATIVECrop Year 2013-2014 vs. Projection and Crop Year 2012-2013

CROP YEAR2013-2014

11

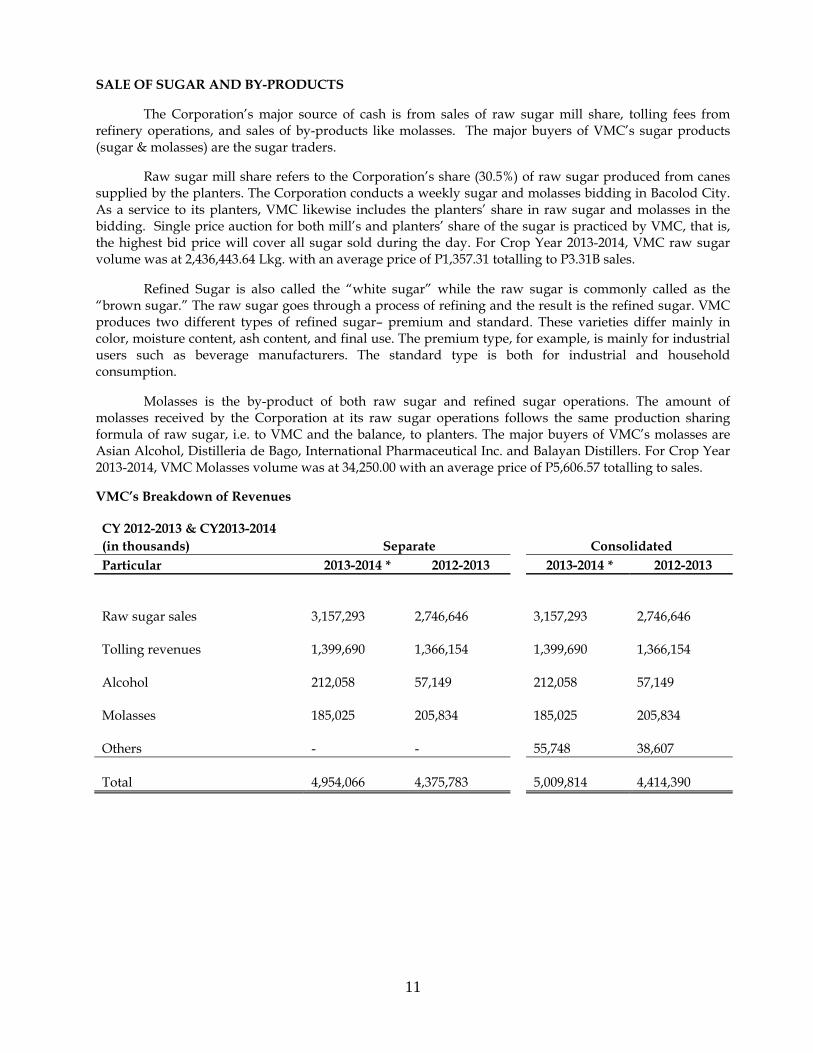

SALE OF SUGAR AND BY-PRODUCTS The Corporation’s major source of cash is from sales of raw sugar mill share, tolling fees from refinery operations, and sales of by-products like molasses. The major buyers of VMC’s sugar products (sugar & molasses) are the sugar traders.

Raw sugar mill share refers to the Corporation’s share (30.5%) of raw sugar produced from canes supplied by the planters. The Corporation conducts a weekly sugar and molasses bidding in Bacolod City. As a service to its planters, VMC likewise includes the planters’ share in raw sugar and molasses in the bidding. Single price auction for both mill’s and planters’ share of the sugar is practiced by VMC, that is, the highest bid price will cover all sugar sold during the day. For Crop Year 2013-2014, VMC raw sugar volume was at 2,436,443.64 Lkg. with an average price of P1,357.31 totalling to P3.31B sales.

Refined Sugar is also called the “white sugar” while the raw sugar is commonly called as the “brown sugar.” The raw sugar goes through a process of refining and the result is the refined sugar. VMC produces two different types of refined sugar– premium and standard. These varieties differ mainly in color, moisture content, ash content, and final use. The premium type, for example, is mainly for industrial users such as beverage manufacturers. The standard type is both for industrial and household consumption.

Molasses is the by-product of both raw sugar and refined sugar operations. The amount of

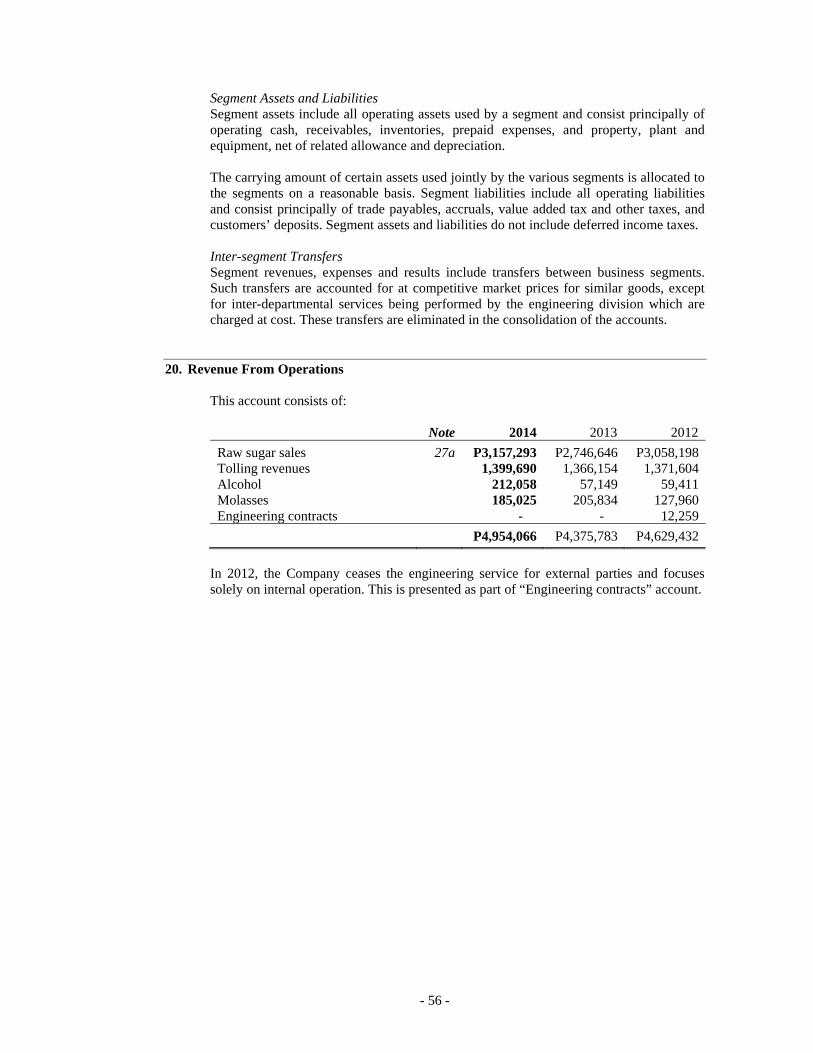

molasses received by the Corporation at its raw sugar operations follows the same production sharing formula of raw sugar, i.e. to VMC and the balance, to planters. The major buyers of VMC’s molasses are Asian Alcohol, Distilleria de Bago, International Pharmaceutical Inc. and Balayan Distillers. For Crop Year 2013-2014, VMC Molasses volume was at 34,250.00 with an average price of P5,606.57 totalling to sales. VMC’s Breakdown of Revenues CY 2012-2013 & CY2013-2014 (in thousands) Separate Consolidated Particular 2013-2014 * 2012-2013 2013-2014 * 2012-2013

Raw sugar sales 3,157,293

2,746,646

3,157,293

2,746,646

Tolling revenues 1,399,690

1,366,154

1,399,690

1,366,154

Alcohol 212,058

57,149

212,058

57,149

Molasses 185,025

205,834

185,025

205,834

Others -

-

55,748

38,607

Total 4,954,066

4,375,783

5,009,814

4,414,390

12

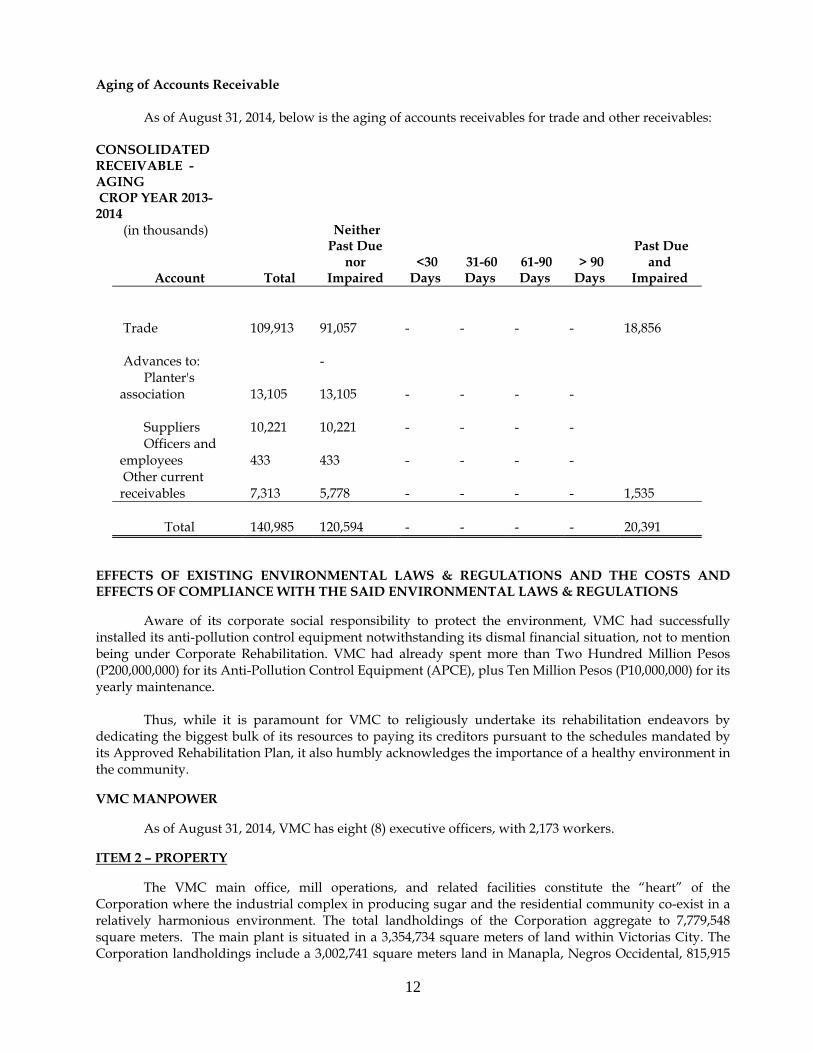

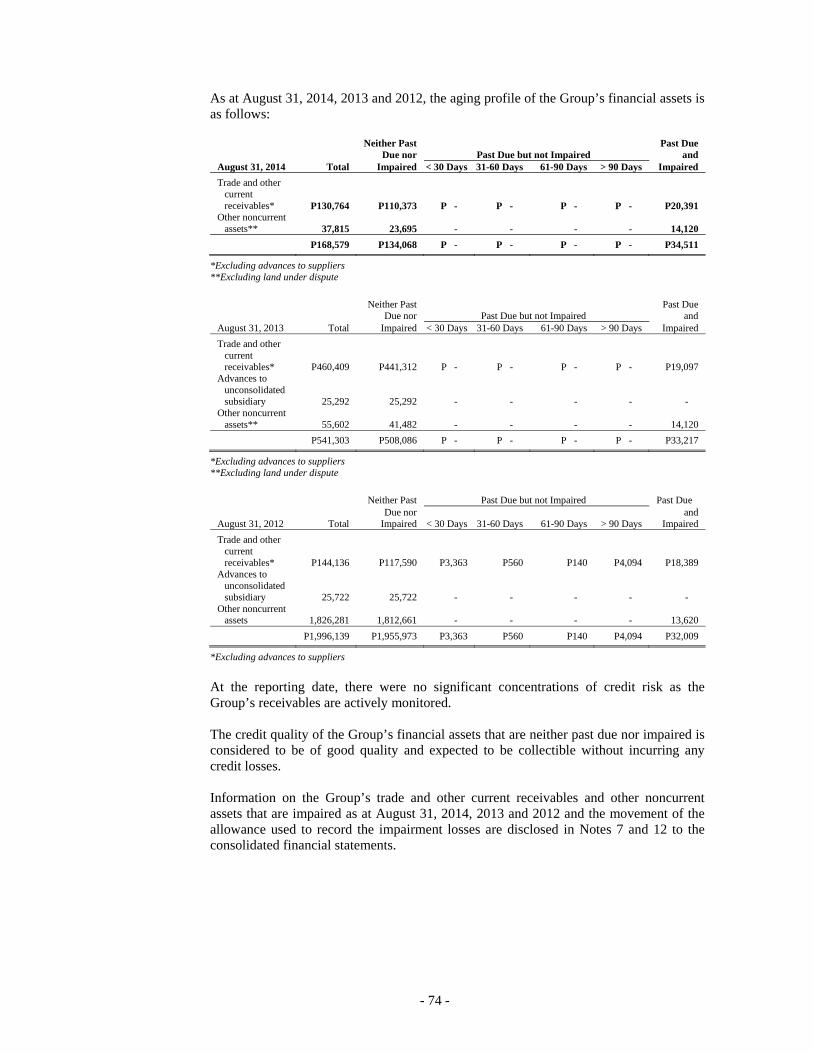

Aging of Accounts Receivable

As of August 31, 2014, below is the aging of accounts receivables for trade and other receivables: CONSOLIDATED RECEIVABLE - AGING CROP YEAR 2013-2014 (in thousands)

Account Total

Neither Past Due

nor Impaired

<30 Days

31-60 Days

61-90 Days

> 90 Days

Past Due and

Impaired

Trade 109,913

91,057

-

-

-

-

18,856

Advances to: -

Planter's

association 13,105

13,105

-

-

-

-

Suppliers 10,221

10,221

-

-

-

-

Officers and

employees 433

433

-

-

-

-

Other current receivables

7,313

5,778

-

-

-

-

1,535

Total 140,985

120,594

-

-

-

-

20,391

EFFECTS OF EXISTING ENVIRONMENTAL LAWS & REGULATIONS AND THE COSTS AND EFFECTS OF COMPLIANCE WITH THE SAID ENVIRONMENTAL LAWS & REGULATIONS

Aware of its corporate social responsibility to protect the environment, VMC had successfully installed its anti-pollution control equipment notwithstanding its dismal financial situation, not to mention being under Corporate Rehabilitation. VMC had already spent more than Two Hundred Million Pesos (P200,000,000) for its Anti-Pollution Control Equipment (APCE), plus Ten Million Pesos (P10,000,000) for its yearly maintenance.

Thus, while it is paramount for VMC to religiously undertake its rehabilitation endeavors by dedicating the biggest bulk of its resources to paying its creditors pursuant to the schedules mandated by its Approved Rehabilitation Plan, it also humbly acknowledges the importance of a healthy environment in the community. VMC MANPOWER

As of August 31, 2014, VMC has eight (8) executive officers, with 2,173 workers.

ITEM 2 – PROPERTY

The VMC main office, mill operations, and related facilities constitute the “heart” of the Corporation where the industrial complex in producing sugar and the residential community co-exist in a relatively harmonious environment. The total landholdings of the Corporation aggregate to 7,779,548 square meters. The main plant is situated in a 3,354,734 square meters of land within Victorias City. The Corporation landholdings include a 3,002,741 square meters land in Manapla, Negros Occidental, 815,915

13

square meters in Cadiz City, 1,000 square meters in Bacolod City, 159 square meters in Talisay City, 4,089 square meters in Iloilo and 13,013 square meters property in Antipolo, Rizal.

However, practically all of the land holdings, including some plant and equipment of the Corporation, are under a Mortgage Trust Indenture (MTI) with a fair market value of almost P2.0 billion, as collateral to VMC loans in the past.

The following are the major operational machineries and equipment owned by VMC and located within its compound in Victorias City, Negros Occidental: a) A & C Mills; b) Various Boilers; c) Boiling House Equipment; d) Refinery; e) Powerhouse; f) other engineering equipment and machineries; g) Manapla Distillery.

These properties were mortgaged to VMC’s creditor banks. They are fully owned by VMC.

The following are the VMC Subsidiaries’ respective principal properties, machineries and equipment: 1) VICTORIAS GOLF & COUNTRY CLUB, INC. (VGCCI) - Clubhouse, 18-hole Golf Course, Office Room, Locker & Shower Room, Canteen & Kitchen, Pavilion, Basement, Green Mowers 22”, Five Gang Fairway Mower. 2) VICTORIAS FOODS CORPORATION (VFC) - Cold Storage 2 compressor 9 cooling PL-EVAP with motor, Steamer Vacuum Automatic Shin-1 for can size 211 x 300, Fish Processing Plant Building, Coldroom/Cold Storage, Blast Freezer, Refrigeration Equipment System, Boiler House, Tank & equipment, Waste Water Treatment Plant. 3) CANETOWN DEVELOPMENT CORPORATION (CDC) - Subdivision lots at Manapla and Victorias, Memorial Garden, Agricultural Land, VMC Engineering Complex Land Area. 4) VICTORIAS AGRICULTURAL LAND CORPORATION (VALCO) - Total of 3,058,178 square meters landholdings. Other VMC Properties:

1. 202.02 hectares of cane field located in Manapla and Cadiz City, Negros Occidental.

2. 113.5015 hectares of cane field located in Victorias City, Negros Occidental.

3. A parcel of land located at Bacolod City, Negros Occidental covered by TCT No. 183131 (Lot No. 26-B) and TCT No. 183132 (Lot No. 26-A).

4. 3.537 hectares of land located in Manapla, Negros Occidental is being utilized by VMC for its

distillery.

5. A part of a parcel of land located at Brgy. XVIII, Hda. Florencia, VMC Compound, Victorias City, Negros Occidental covered by TCT No. RT-105-75.

ITEM 3 – LEGAL PROCEEDINGS

Cases filed for and against VMC are being handled by the Corporation’s In-house Counsels and by its External Counsels.

The External Counsels are Hilado Hagad & Hilado Law Offices, Gabionza De Santos & Partners, Mirano Mirano Mirano & Mirano Law Offices, Hechanova Bugay & Vilchez, Quiason Makalintal Barot Torres Ibarra & Sison, Zambrano & Gruba Law Offices, Manuel Lao Ong & Linus Abaquin Law Firm, Torres & Sy Law Office and Puyat Jacinto & Santos Law Firm, Puno & Puno Law Offices, Roxas De Los

14

Reyes Laurel Rosario & Leagogo Law Offices, Adarlo Caoile & Associates Law Offices, and Paner Hosaka & Ypil Attorneys-At-Law. ITEM 4 – SUBMISSION OF MATTER TO A VOTE OF SECURITY HOLDERS

Except for the matters taken up during the Annual Stockholders’ Meeting, there was no other matter submitted to a vote of security holders during the period covered by this report.

PART II – OPERATION AND FINANCIAL INFORMATION

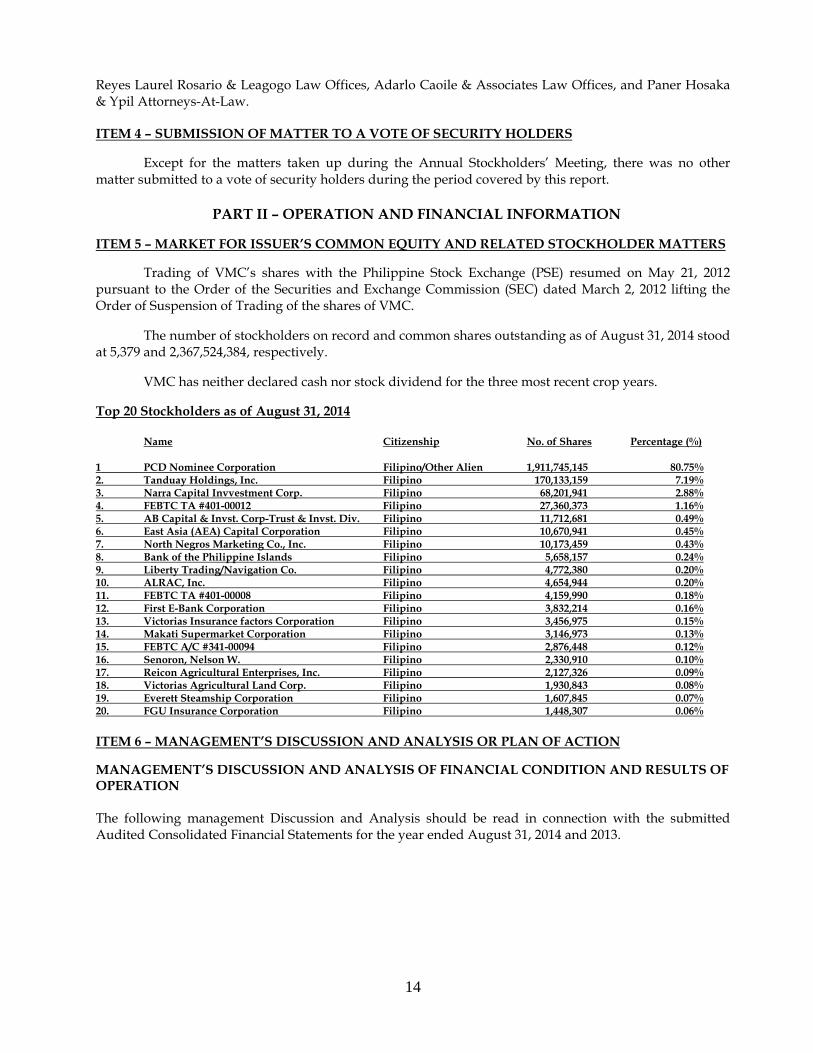

ITEM 5 – MARKET FOR ISSUER’S COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Trading of VMC’s shares with the Philippine Stock Exchange (PSE) resumed on May 21, 2012 pursuant to the Order of the Securities and Exchange Commission (SEC) dated March 2, 2012 lifting the Order of Suspension of Trading of the shares of VMC.

The number of stockholders on record and common shares outstanding as of August 31, 2014 stood at 5,379 and 2,367,524,384, respectively.

VMC has neither declared cash nor stock dividend for the three most recent crop years. Top 20 Stockholders as of August 31, 2014

Name Citizenship No. of Shares Percentage (%) 1 PCD Nominee Corporation Filipino/Other Alien 1,911,745,145 80.75% 2. Tanduay Holdings, Inc. Filipino 170,133,159 7.19% 3. Narra Capital Invvestment Corp. Filipino 68,201,941 2.88% 4. FEBTC TA #401-00012 Filipino 27,360,373 1.16% 5. AB Capital & Invst. Corp-Trust & Invst. Div. Filipino 11,712,681 0.49% 6. East Asia (AEA) Capital Corporation Filipino 10,670,941 0.45% 7. North Negros Marketing Co., Inc. Filipino 10,173,459 0.43% 8. Bank of the Philippine Islands Filipino 5,658,157 0.24% 9. Liberty Trading/Navigation Co. Filipino 4,772,380 0.20% 10. ALRAC, Inc. Filipino 4,654,944 0.20% 11. FEBTC TA #401-00008 Filipino 4,159,990 0.18% 12. First E-Bank Corporation Filipino 3,832,214 0.16% 13. Victorias Insurance factors Corporation Filipino 3,456,975 0.15% 14. Makati Supermarket Corporation Filipino 3,146,973 0.13% 15. FEBTC A/C #341-00094 Filipino 2,876,448 0.12% 16. Senoron, Nelson W. Filipino 2,330,910 0.10% 17. Reicon Agricultural Enterprises, Inc. Filipino 2,127,326 0.09% 18. Victorias Agricultural Land Corp. Filipino 1,930,843 0.08% 19. Everett Steamship Corporation Filipino 1,607,845 0.07% 20. FGU Insurance Corporation Filipino 1,448,307 0.06% ITEM 6 – MANAGEMENT’S DISCUSSION AND ANALYSIS OR PLAN OF ACTION

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION The following management Discussion and Analysis should be read in connection with the submitted Audited Consolidated Financial Statements for the year ended August 31, 2014 and 2013.

15

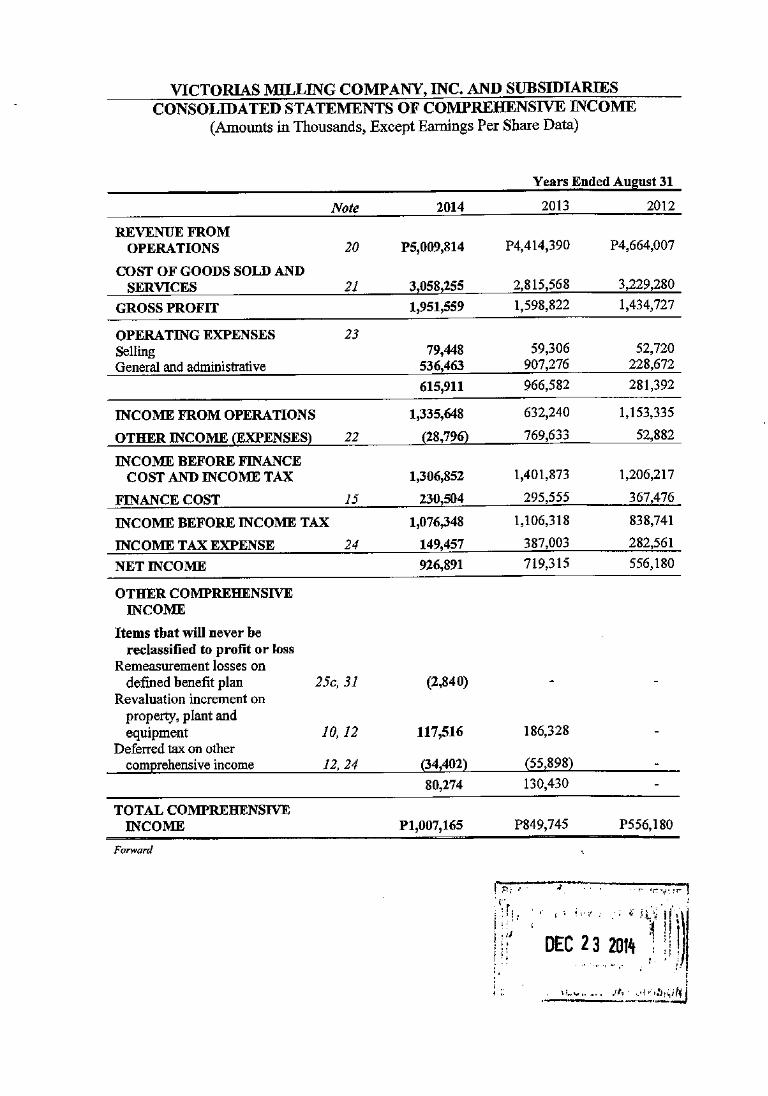

Amounts in Php Thousands 2014 2013 Amount PctParent Revenue 4,954,066 4,375,783 578,283 13%Raw sugar revenue 3,157,293 2,746,646 410,647 15%Tolling revenues 1,399,690 1,366,154 33,536 2%Molasses revenue 185,025 205,834 (20,809) -10%Alcohol revenue 212,058 57,149 154,909 271%Subsidiaries Revenue 55,748 38,607 17,141 44%Total Revenue 5,009,814 4,414,390 595,424 13%

Periods Ended August 31 Change

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013Cost of hauling 898,856 902,449 (3,593) 0% 18% 20%Repairs and maintenance 541,538 658,830 (117,292) -18% 11% 15%Materials and supplies 422,878 343,328 79,550 23% 8% 8%Depreciation 256,203 261,204 (5,001) -2% 5% 6%Professional fees and contracted services 240,267 309,555 (69,288) -22% 5% 7%Fuel and transportation 210,431 173,195 37,236 21% 4% 4%Direct Labor 81,884 6,658 75,226 1130% 2% 0.2%Input tax allocable to exempt sales 81,520 60,508 21,012 35% 2% 1%Light and water 72,700 63,464 9,236 15% 1% 1%Taxes and licenses 48,774 50,269 (1,495) -3% 1% 1%Rental 7,359 2,379 4,980 209% 0.1% 0%Others 34,271 46,371 (12,100) -26% 1% 1%Total cost of goods manufactured 2,896,681 2,878,210 18,471 1% 58% 65%Decrease (increase) in inventories 161,574 (62,642) 224,216 -358% 3% -1%Cost of Goods Sold and Services 3,058,255 2,815,568 242,687 9% 61% 64%

Periods Ended August 31 Change Pct to Rev

Results of Operations Revenues

The Parent company’s revenue accounted for 99% of the Group’s consolidated revenue for the year-to-date (YTD) August 31. It includes sales from raw sugar, refining service, molasses and distillery operations, which grew by13% in the YTD August 31 compared to same period in 2013.

Revenues from raw sugar increased by 15% for the year compared to 2013 due primarily to increase in volume sold by 8%.

Tolling fees from refining services also increased by 2% for the year compared to 2013 due mainly to increase of refined volume collected by 3%.

Revenues from distillery operations significantly increased by 271% due to increase in volume sold and selling price by 263% and 2%, respectively.

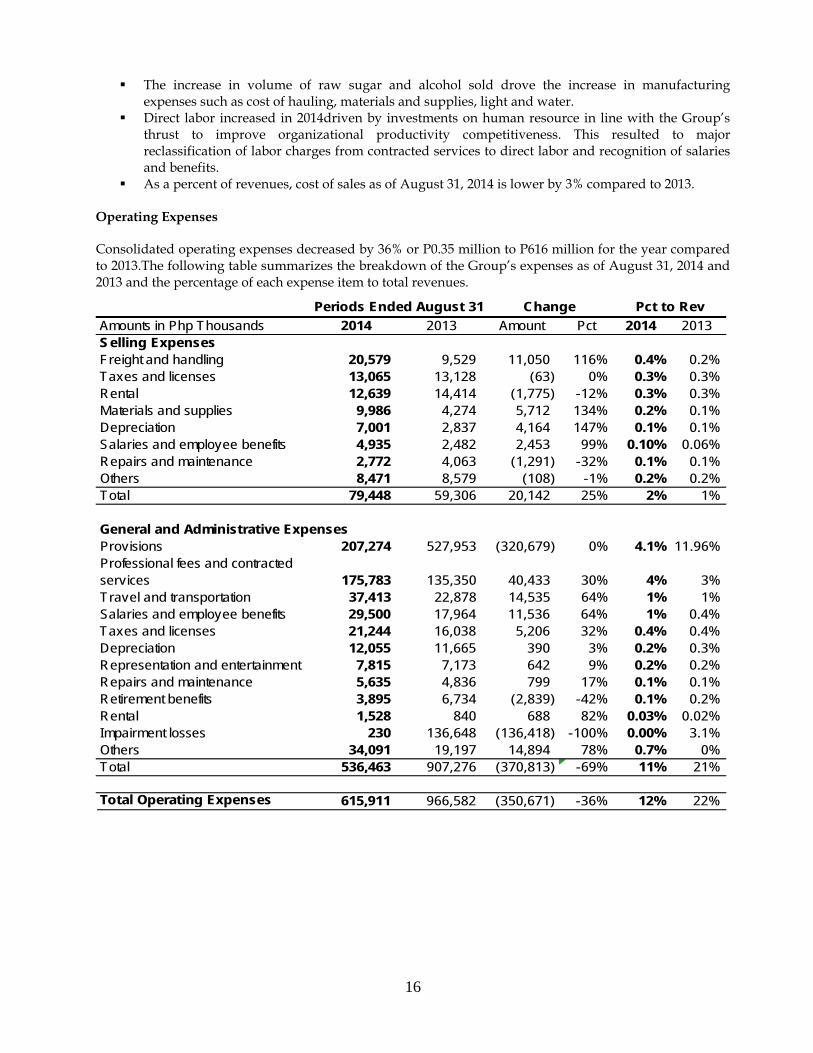

Cost of Goods Sold and Services Consolidated cost of goods sold and services increased by 9% or P0.24 million to P3 billion for the year compared to 2013. The following table summarizes the breakdown of the Group’s cost of sales as of August 31, 2014 and 2013 and the percentage of each cost item to total revenues.

16

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013Selling ExpensesFreight and handling 20,579 9,529 11,050 116% 0.4% 0.2%Taxes and licenses 13,065 13,128 (63) 0% 0.3% 0.3%Rental 12,639 14,414 (1,775) -12% 0.3% 0.3%Materials and supplies 9,986 4,274 5,712 134% 0.2% 0.1%Depreciation 7,001 2,837 4,164 147% 0.1% 0.1%Salaries and employee benefits 4,935 2,482 2,453 99% 0.10% 0.06%Repairs and maintenance 2,772 4,063 (1,291) -32% 0.1% 0.1%Others 8,471 8,579 (108) -1% 0.2% 0.2%Total 79,448 59,306 20,142 25% 2% 1%

Provisions 207,274 527,953 (320,679) 0% 4.1% 11.96%Professional fees and contracted services 175,783 135,350 40,433 30% 4% 3%Travel and transportation 37,413 22,878 14,535 64% 1% 1%Salaries and employee benefits 29,500 17,964 11,536 64% 1% 0.4%Taxes and licenses 21,244 16,038 5,206 32% 0.4% 0.4%Depreciation 12,055 11,665 390 3% 0.2% 0.3%Representation and entertainment 7,815 7,173 642 9% 0.2% 0.2%Repairs and maintenance 5,635 4,836 799 17% 0.1% 0.1%Retirement benefits 3,895 6,734 (2,839) -42% 0.1% 0.2%Rental 1,528 840 688 82% 0.03% 0.02%Impairment losses 230 136,648 (136,418) -100% 0.00% 3.1%Others 34,091 19,197 14,894 78% 0.7% 0%Total 536,463 907,276 (370,813) -69% 11% 21%

Total Operating Expenses 615,911 966,582 (350,671) -36% 12% 22%

General and Administrative Expenses

Periods Ended August 31 Change Pct to Rev

The increase in volume of raw sugar and alcohol sold drove the increase in manufacturing expenses such as cost of hauling, materials and supplies, light and water.

Direct labor increased in 2014driven by investments on human resource in line with the Group’s thrust to improve organizational productivity competitiveness. This resulted to major reclassification of labor charges from contracted services to direct labor and recognition of salaries and benefits.

As a percent of revenues, cost of sales as of August 31, 2014 is lower by 3% compared to 2013.

Operating Expenses Consolidated operating expenses decreased by 36% or P0.35 million to P616 million for the year compared to 2013.The following table summarizes the breakdown of the Group’s expenses as of August 31, 2014 and 2013 and the percentage of each expense item to total revenues.

17

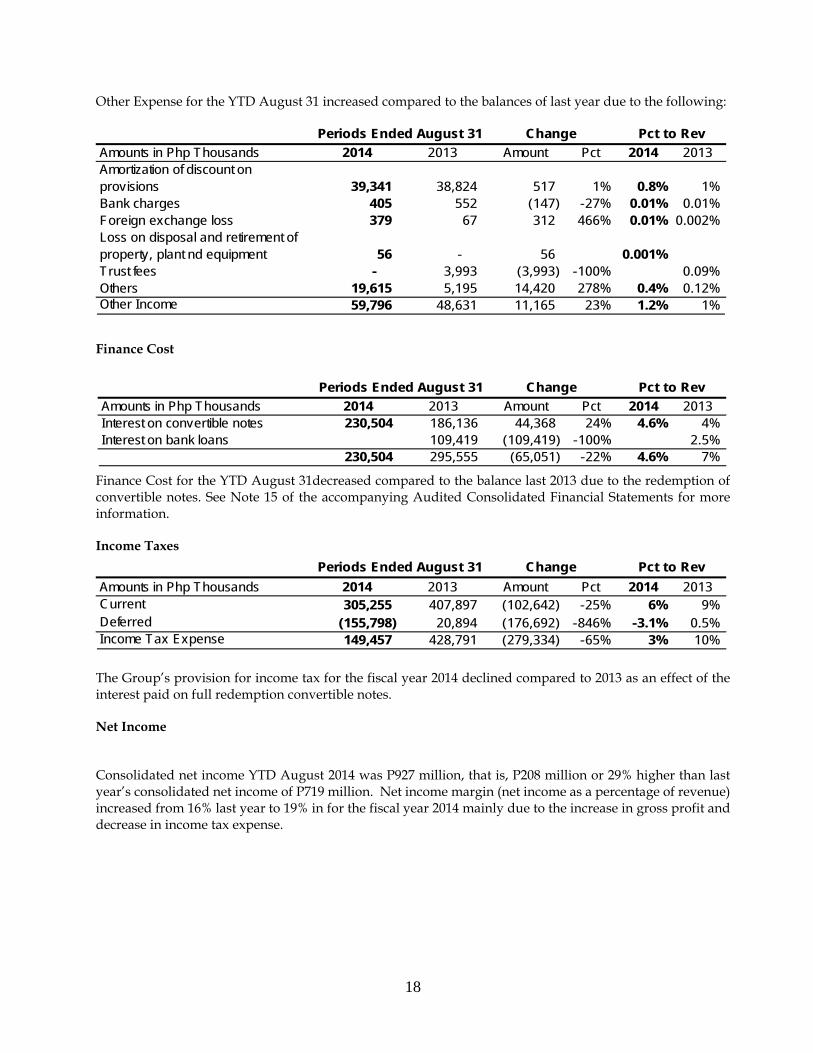

Amounts in Php Thousands 2014 2013 Amount PctRental income 13,256 14,879 (1,623) -11%Interest income 11,041 38,546 (27,505) -71%Others 5,578 1,230 4,348 353%Gain on sale of property, plant and equipment 624 268 356 133%Gain on sale of inventory 434 - 434 Gain on extinguishment of liability 67 280,143 (280,076) -100%Foreign exchange gain - 8,334 (8,334) -100%Fair value gain on investment properties - 455,133 (455,133) -100%Curtailment gain - 19,731 (19,731) -100%Other Income 31,000 818,264 (787,264) -96%

Periods Ended August 31 Change

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013

Other Income 31,000 818,264 (787,264) -96% 0.6% 19%

Periods Ended August 31 Change Pct to Rev

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013

Other Expenses 59,796 48,631 11,165 23% 1.2% 1%

Periods Ended August 31 Change Pct to Rev

The increase in volume of raw sugar and alcohol sold drove the increase in selling expenses such as freight and handling and contracted services.

The increase in depreciation was due to VMC’s Raw House Upgrading and Modernization program, which aims for higher efficiency and competitiveness.

Salaries and employees benefits increased in 2014 driven by investments on human resource in line with the Group’s thrust to improve organizational productivity and competitiveness.

Additional provision was accrued to cover various legal claims. See Note 14 of the accompanying Consolidated Financial Statements for more information.

Operating Income Taking into account the factors discussed above, operating income for the year ended August 31, 2014 is higher by 111% or P703 million to P1.3 billion compared to same period in 2013. Other Income

Other Income in YTD August 31 decreased compared to the balance as of the same period last year due to the following:

Decrease in interest earned was due to the decline in cash resources after paying off the convertible notes and drop in money market placement rates.

Other Expenses

18

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013Amortization of discount on provisions 39,341 38,824 517 1% 0.8% 1%Bank charges 405 552 (147) -27% 0.01% 0.01%Foreign exchange loss 379 67 312 466% 0.01% 0.002%Loss on disposal and retirement of property, plant nd equipment 56 - 56 0.001%Trust fees - 3,993 (3,993) -100% 0.09%Others 19,615 5,195 14,420 278% 0.4% 0.12%Other Income 59,796 48,631 11,165 23% 1.2% 1%

Pct to RevPeriods Ended August 31 Change

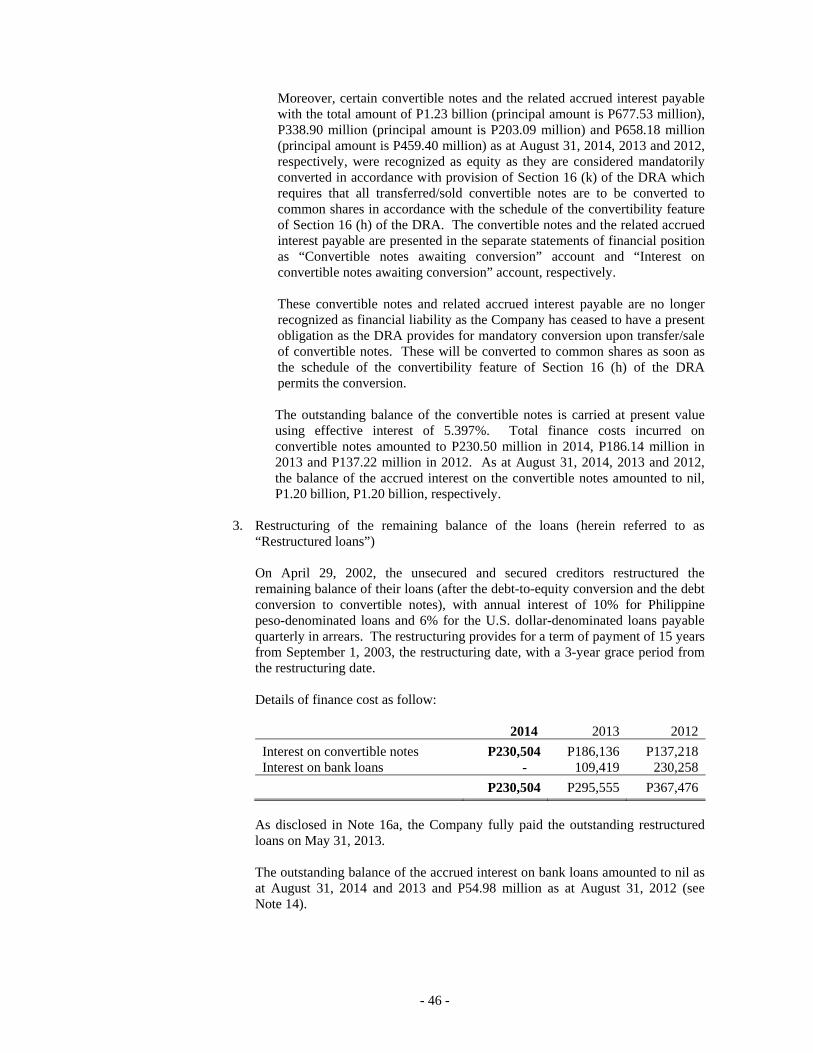

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013Interest on convertible notes 230,504 186,136 44,368 24% 4.6% 4%Interest on bank loans 109,419 (109,419) -100% 2.5%

230,504 295,555 (65,051) -22% 4.6% 7%

Periods Ended August 31 Change Pct to Rev

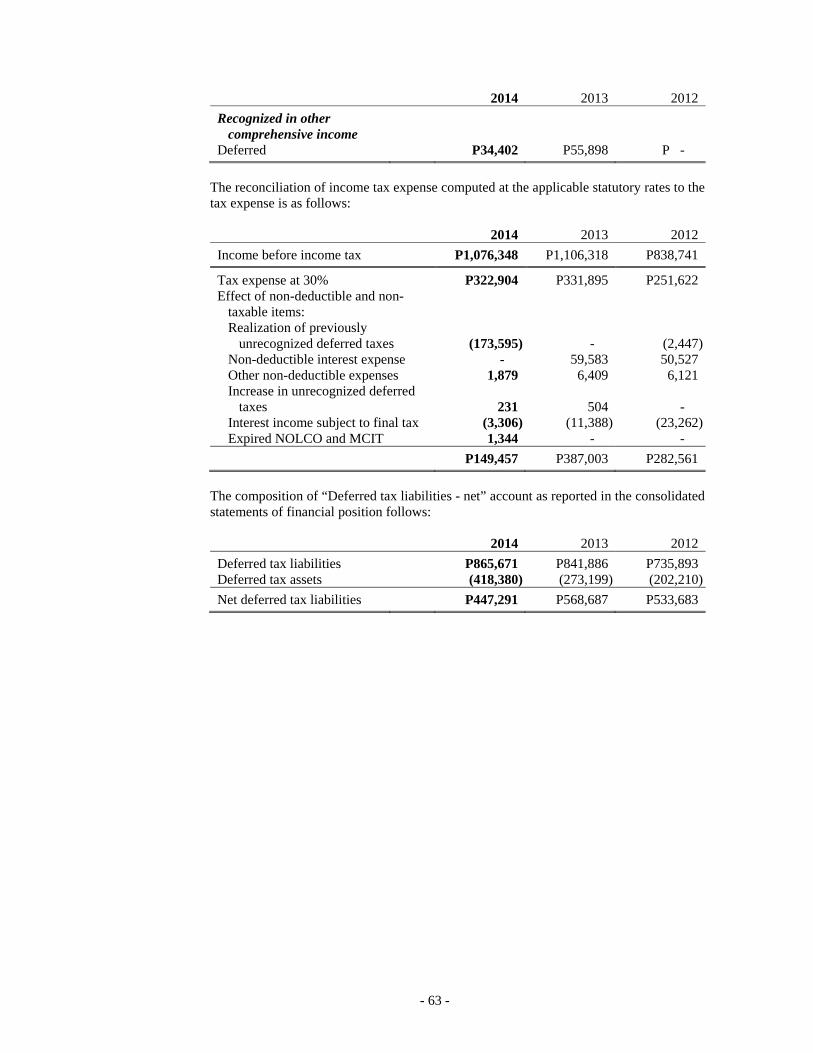

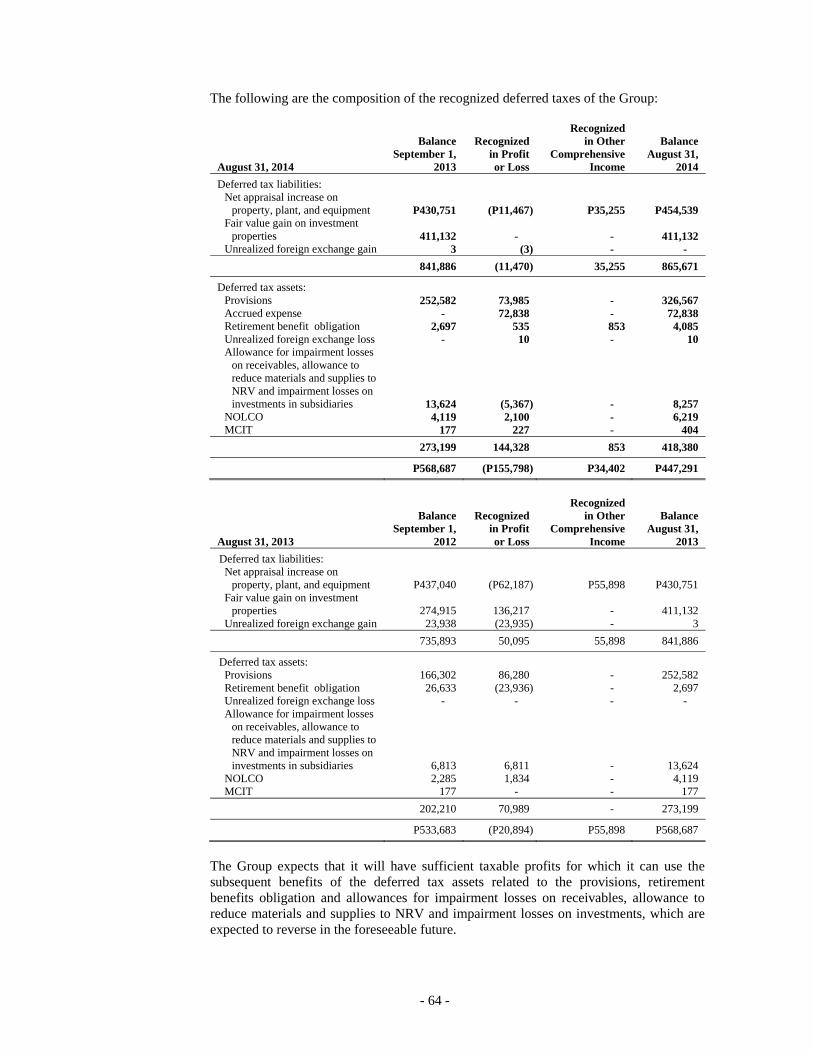

Amounts in Php Thousands 2014 2013 Amount Pct 2014 2013Current 305,255 407,897 (102,642) -25% 6% 9%Deferred (155,798) 20,894 (176,692) -846% -3.1% 0.5%Income Tax Expense 149,457 428,791 (279,334) -65% 3% 10%

Periods Ended August 31 Change Pct to Rev

Other Expense for the YTD August 31 increased compared to the balances of last year due to the following:

Finance Cost

Finance Cost for the YTD August 31decreased compared to the balance last 2013 due to the redemption of convertible notes. See Note 15 of the accompanying Audited Consolidated Financial Statements for more information. Income Taxes

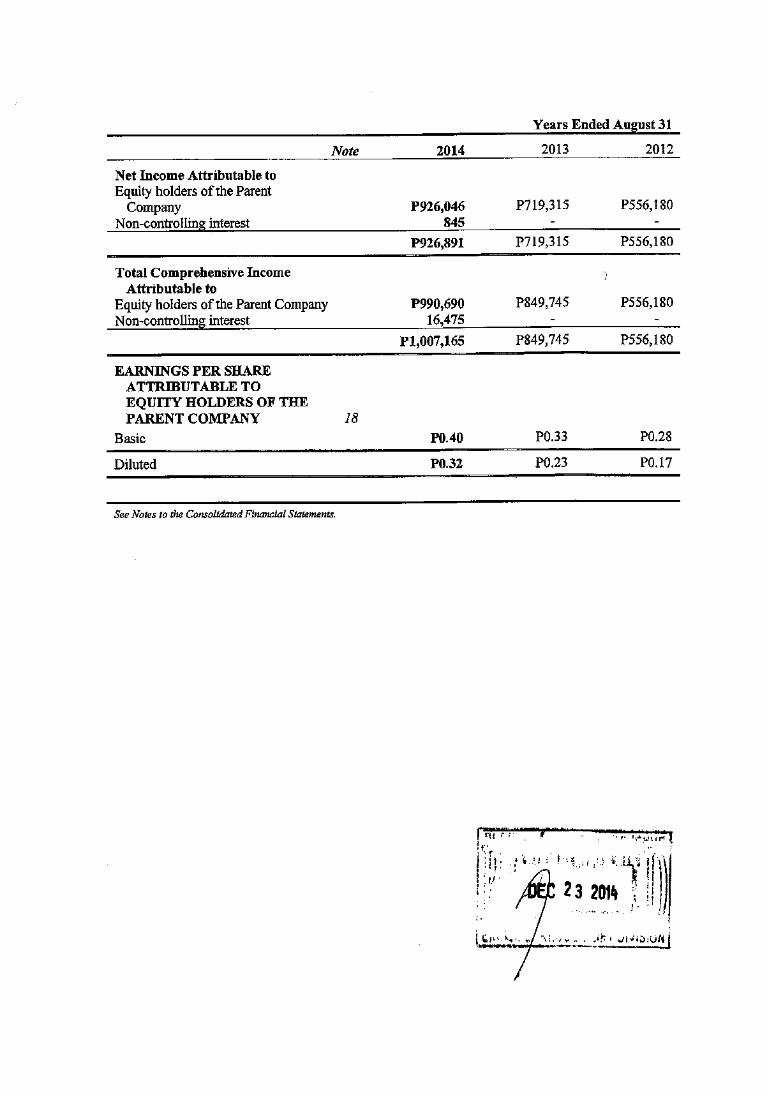

The Group’s provision for income tax for the fiscal year 2014 declined compared to 2013 as an effect of the interest paid on full redemption convertible notes. Net Income Consolidated net income YTD August 2014 was P927 million, that is, P208 million or 29% higher than last year’s consolidated net income of P719 million. Net income margin (net income as a percentage of revenue) increased from 16% last year to 19% in for the fiscal year 2014 mainly due to the increase in gross profit and decrease in income tax expense.

19

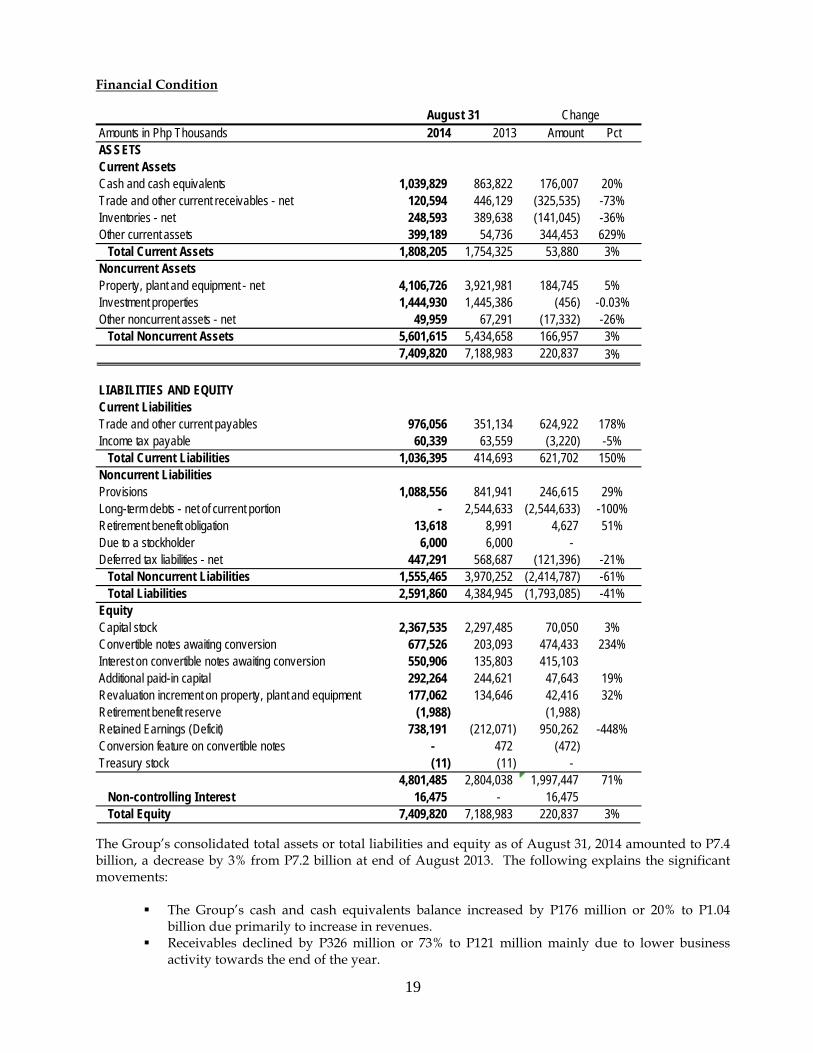

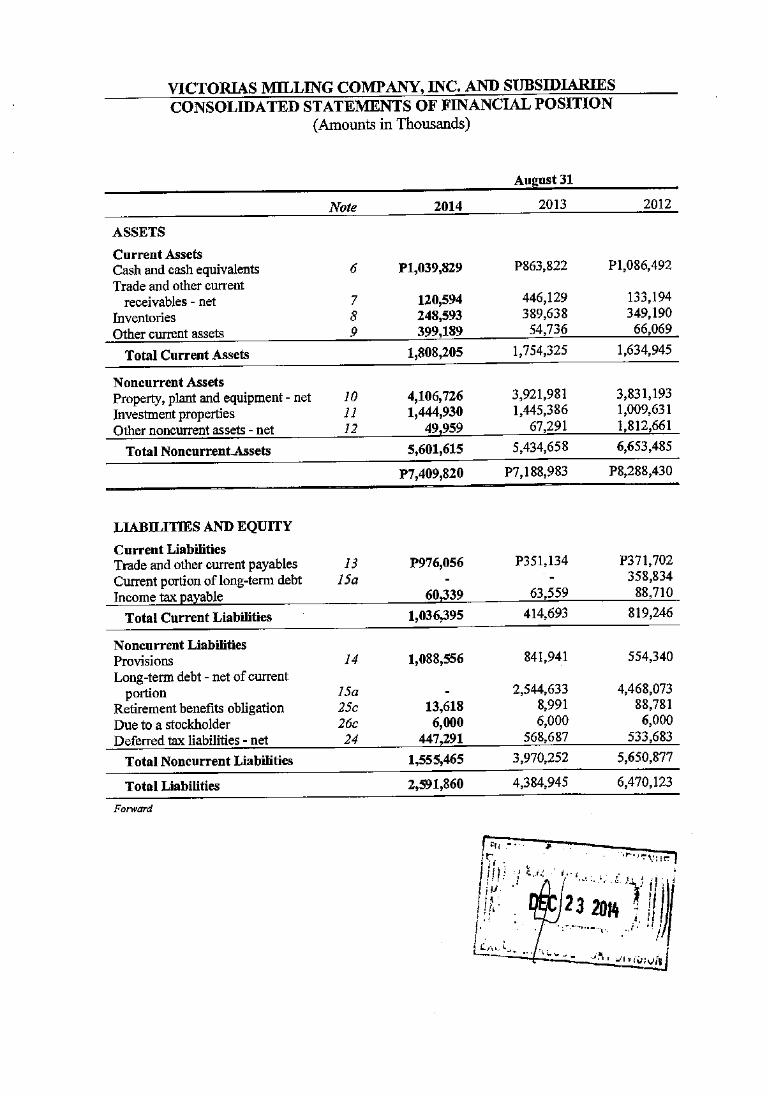

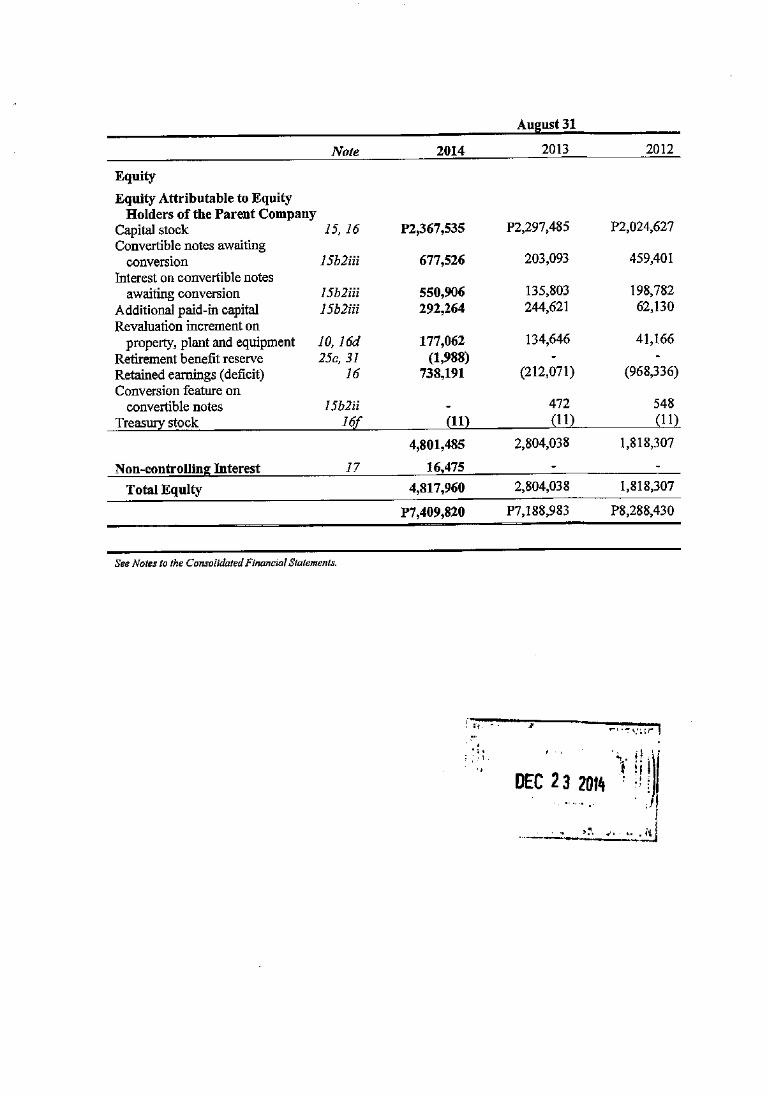

Amounts in Php Thousands 2014 2013 Amount PctASSETSCurrent AssetsCash and cash equivalents 1,039,829 863,822 176,007 20%Trade and other current receivables - net 120,594 446,129 (325,535) -73%Inventories - net 248,593 389,638 (141,045) -36%Other current assets 399,189 54,736 344,453 629%

Total Current Assets 1,808,205 1,754,325 53,880 3%Noncurrent AssetsProperty, plant and equipment - net 4,106,726 3,921,981 184,745 5%Investment properties 1,444,930 1,445,386 (456) -0.03%Other noncurrent assets - net 49,959 67,291 (17,332) -26%

Total Noncurrent Assets 5,601,615 5,434,658 166,957 3% 7,409,820 7,188,983 220,837 3%

LIABILITIES AND EQUITYCurrent LiabilitiesTrade and other current payables 976,056 351,134 624,922 178%Income tax payable 60,339 63,559 (3,220) -5%

Total Current Liabilities 1,036,395 414,693 621,702 150%Noncurrent LiabilitiesProvisions 1,088,556 841,941 246,615 29%Long-term debts - net of current portion - 2,544,633 (2,544,633) -100%Retirement benefit obligation 13,618 8,991 4,627 51%Due to a stockholder 6,000 6,000 - Deferred tax liabilities - net 447,291 568,687 (121,396) -21%

Total Noncurrent Liabilities 1,555,465 3,970,252 (2,414,787) -61%Total Liabilities 2,591,860 4,384,945 (1,793,085) -41%

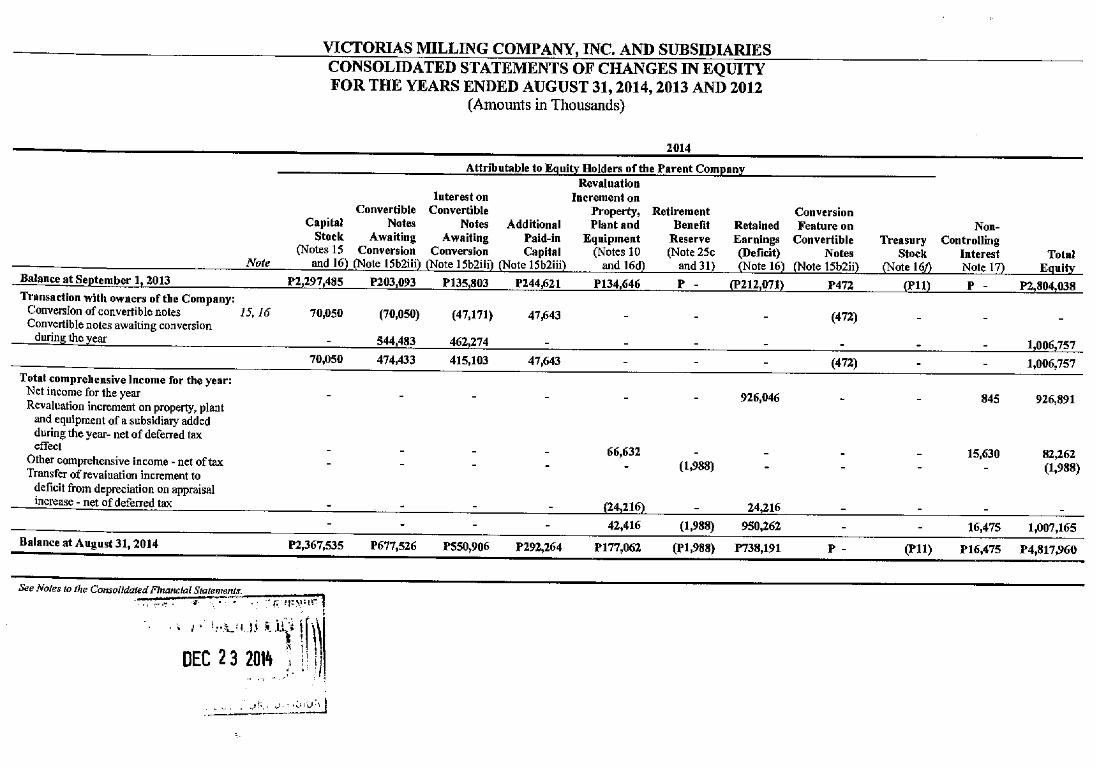

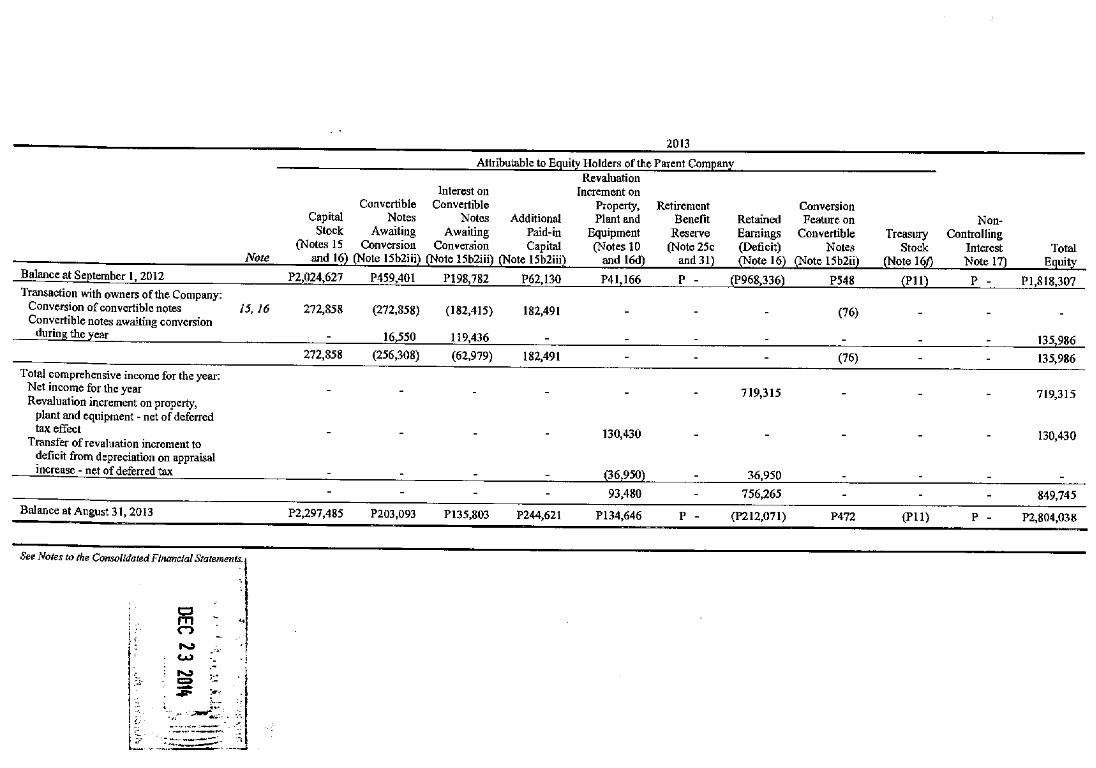

EquityCapital stock 2,367,535 2,297,485 70,050 3%Convertible notes awaiting conversion 677,526 203,093 474,433 234%Interest on convertible notes awaiting conversion 550,906 135,803 415,103 Additional paid-in capital 292,264 244,621 47,643 19%Revaluation increment on property, plant and equipment 177,062 134,646 42,416 32%Retirement benefit reserve (1,988) (1,988)Retained Earnings (Deficit) 738,191 (212,071) 950,262 -448%Conversion feature on convertible notes - 472 (472)Treasury stock (11) (11) -

4,801,485 2,804,038 1,997,447 71%Non-controlling Interest 16,475 - 16,475 Total Equity 7,409,820 7,188,983 220,837 3%

ChangeAugust 31

Financial Condition

The Group’s consolidated total assets or total liabilities and equity as of August 31, 2014 amounted to P7.4 billion, a decrease by 3% from P7.2 billion at end of August 2013. The following explains the significant movements:

The Group’s cash and cash equivalents balance increased by P176 million or 20% to P1.04 billion due primarily to increase in revenues.

Receivables declined by P326 million or 73% to P121 million mainly due to lower business activity towards the end of the year.

20

The decrease in inventories by P141 million or 36% to P249 million is chiefly driven by the increase in volume of raw sugar sold.

Trade and other current liabilities increased by P625 million or 178% to P976 million largely due to set up of liability for check payable to a CN holder and recognition of accrued expenses. See Note 13 of the accompanying Audited Consolidated Financial Statements for more information.

Income tax payable decreased by P3 million or 5% to P60 million. Taxable income was significantly reduced by payment of interest of convertible notes.

Provisions increased by P247 million or 29% to P1 billion to cover probable liability on various legal claims. See Note 14 of the accompanying Audited Consolidated Financial Statements for more information.

The redemption of convertible notes wiped out the remaining balance of Long-term Debts as of August 31, 2014.

The increase in Retirement benefit obligation by P5 million mainly refers to re-measurement losses on defined benefit plan with reference to the actuarial valuation made as of August 31, 2014.

Net deferred tax liabilities decreased by P121 million or 21% to P447 million, due to the increase of recognized deferred tax asset on additional provision for various legal claims and accrued expenses.

The increase in Capital stock by 3% or P70 million to P2.4 billion refers to actual conversion of certain convertible notes. See Note 16b of the accompanying Audited Consolidated Financial Statements for more information.

Convertible notes awaiting conversion increased by P890 million or 262% to P1.2 billion due to transfer/sale of certain convertible notes by primary/original note holders. As such, these transactions were booked as equity in accordance with the DRA. See Note 15b2 of the accompanying Audited Consolidated Financial Statements for more information.

Additional paid in capital likewise increased by P47 million or 19% to P292 million due to recognition as equity of accrued interest on convertible notes which were converted to common shares. Interest is not convertible to shares.

The increase in Revaluation increment on property, plant and equipment by P43 million refers to recognition of revaluation adjustments.

Retained earnings turned positive to P734 million from deficit of P212 million, with the net income attributable to equity holders for the YTD August 2014 of P950 million.

Liquidity and Capital Resources

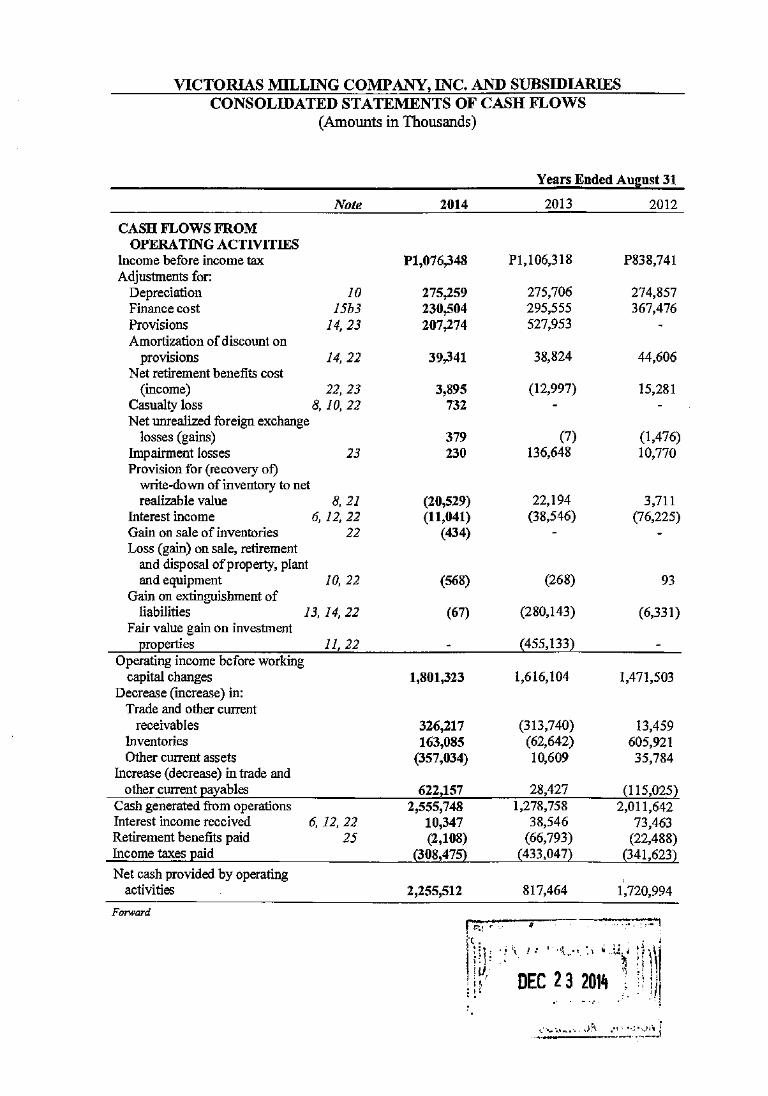

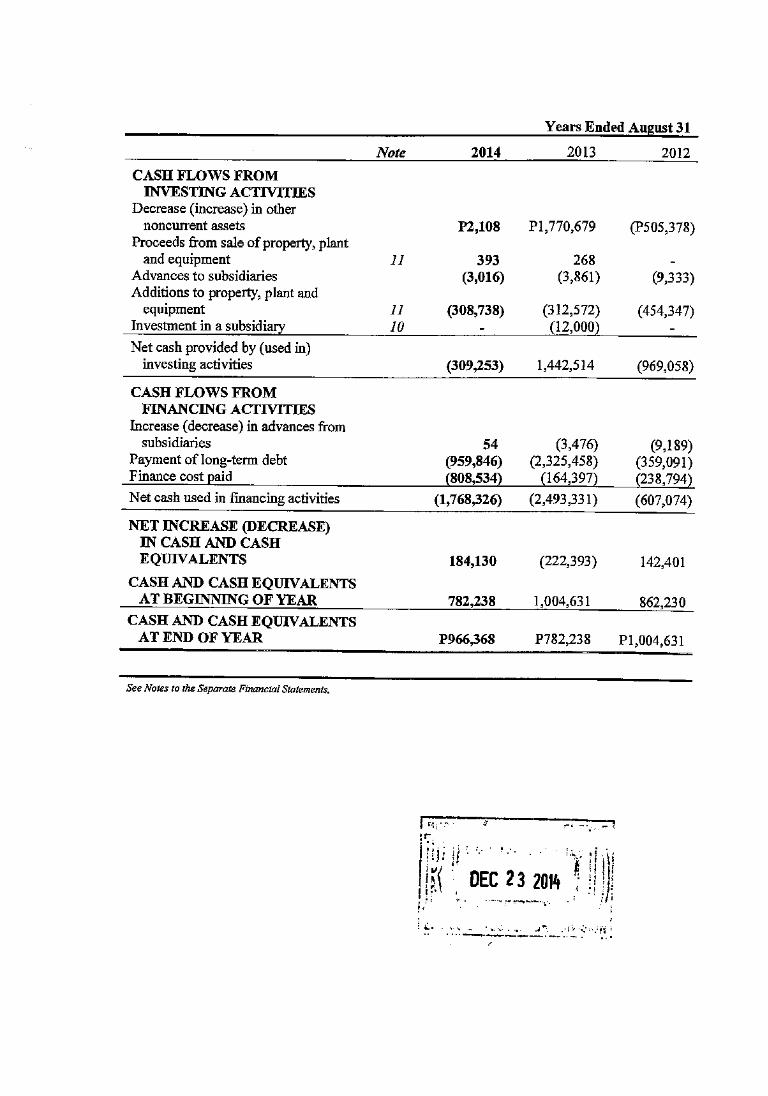

Net cash provided by operating activities as of August 31, 2014 was P2.3 billion, 176% or P1.4billion higher compared to the net cash provided by operating activities of the same period in 2013 amounting to P0.82 million which was mainly contributed by stronger operating results.

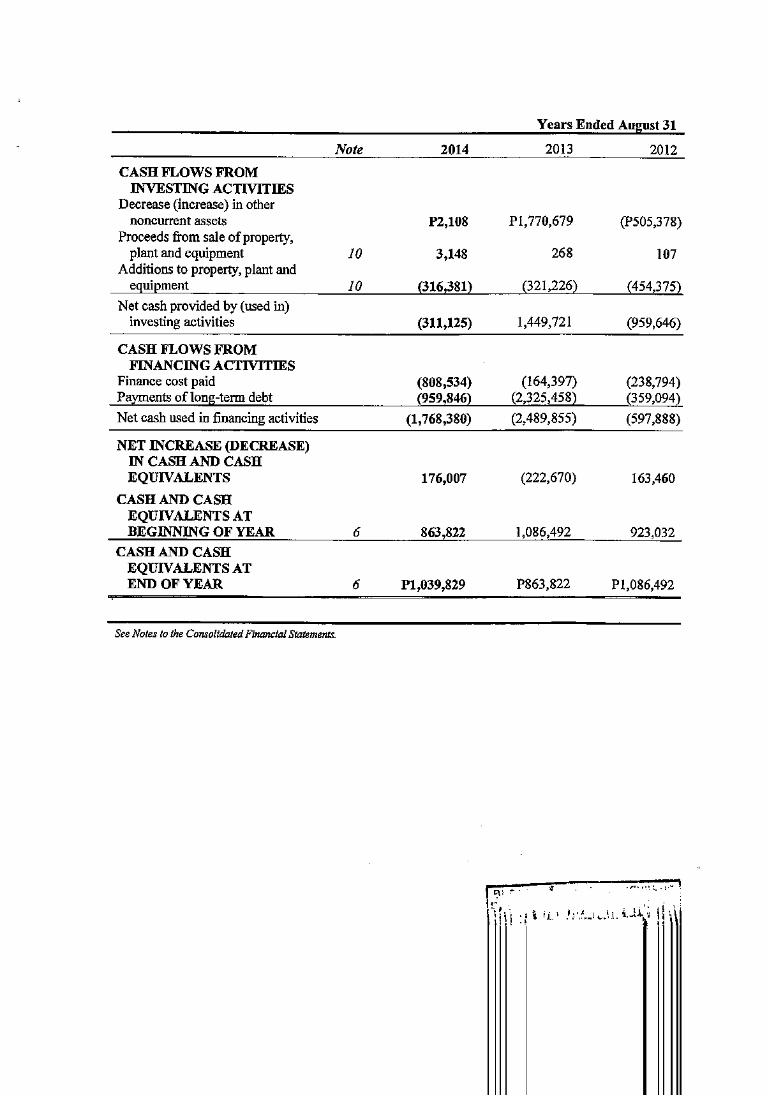

Net cash used in investing activities was P311 million as of August 31, 2014, which pertains to capital expenditures spending for factory machinery upgrades.

Net cash used in financing activities amounted to P1.8 billion as of August 31, 2014 due to

redemption of convertible notes and payments of the related accrued interest. Generally, there is a net increase in cash and cash equivalents by P176 million as of August 31, 2014.

Discussion and Analysis of Material Events and Uncertainties

1. There were no events or commitments that will result to material liquidity problem to the Group.

2. There were no material off-balance sheet transactions, arrangements or obligations entered to during the period.

21

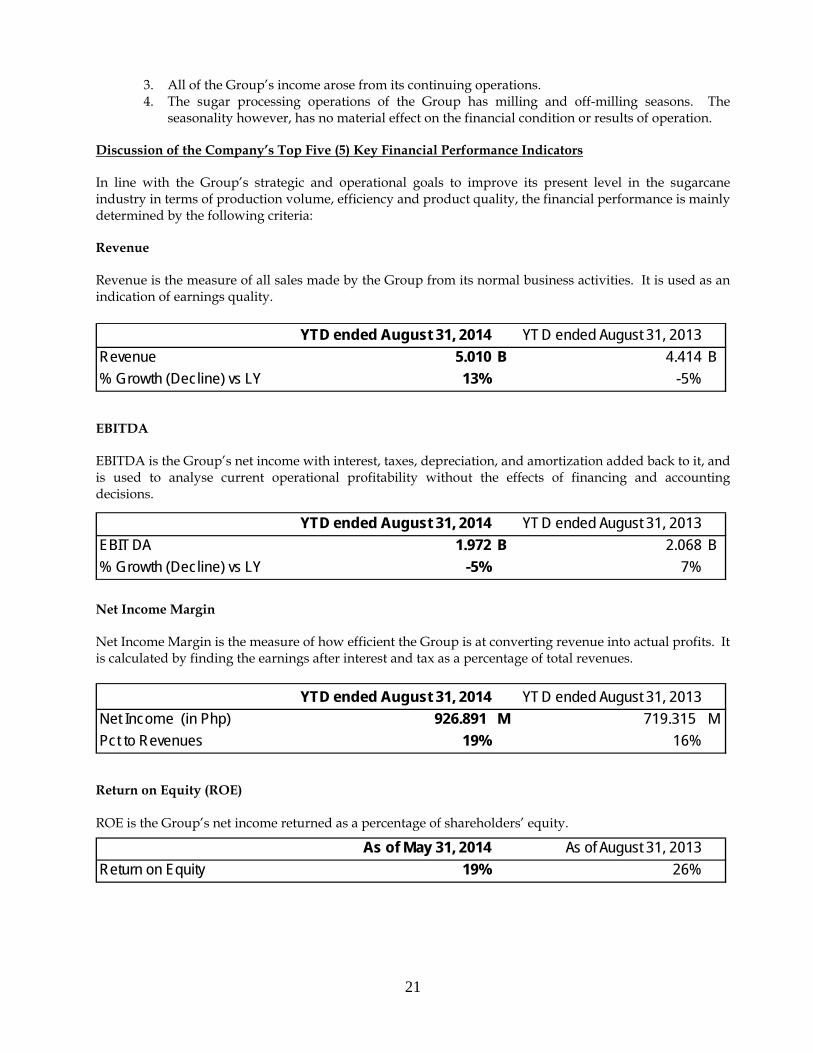

YTD ended August 31, 2014 YTD ended August 31, 2013Revenue 5.010 B 4.414 B% Growth (Decline) vs LY 13% -5%

YTD ended August 31, 2014 YTD ended August 31, 2013EBITDA 1.972 B 2.068 B% Growth (Decline) vs LY -5% 7%

YTD ended August 31, 2014 YTD ended August 31, 2013Net Income (in Php) 926.891 M 719.315 MPct to Revenues 19% 16%

As of May 31, 2014 As of August 31, 2013Return on Equity 19% 26%

3. All of the Group’s income arose from its continuing operations. 4. The sugar processing operations of the Group has milling and off-milling seasons. The

seasonality however, has no material effect on the financial condition or results of operation.

Discussion of the Company’s Top Five (5) Key Financial Performance Indicators

In line with the Group’s strategic and operational goals to improve its present level in the sugarcane industry in terms of production volume, efficiency and product quality, the financial performance is mainly determined by the following criteria: Revenue Revenue is the measure of all sales made by the Group from its normal business activities. It is used as an indication of earnings quality.

EBITDA EBITDA is the Group’s net income with interest, taxes, depreciation, and amortization added back to it, and is used to analyse current operational profitability without the effects of financing and accounting decisions.

Net Income Margin Net Income Margin is the measure of how efficient the Group is at converting revenue into actual profits. It is calculated by finding the earnings after interest and tax as a percentage of total revenues.

Return on Equity (ROE) ROE is the Group’s net income returned as a percentage of shareholders’ equity.

22

YTD ended August 31, 2014 YTD ended August 31, 2013Earnings per share (in Php) 0.40 0.33

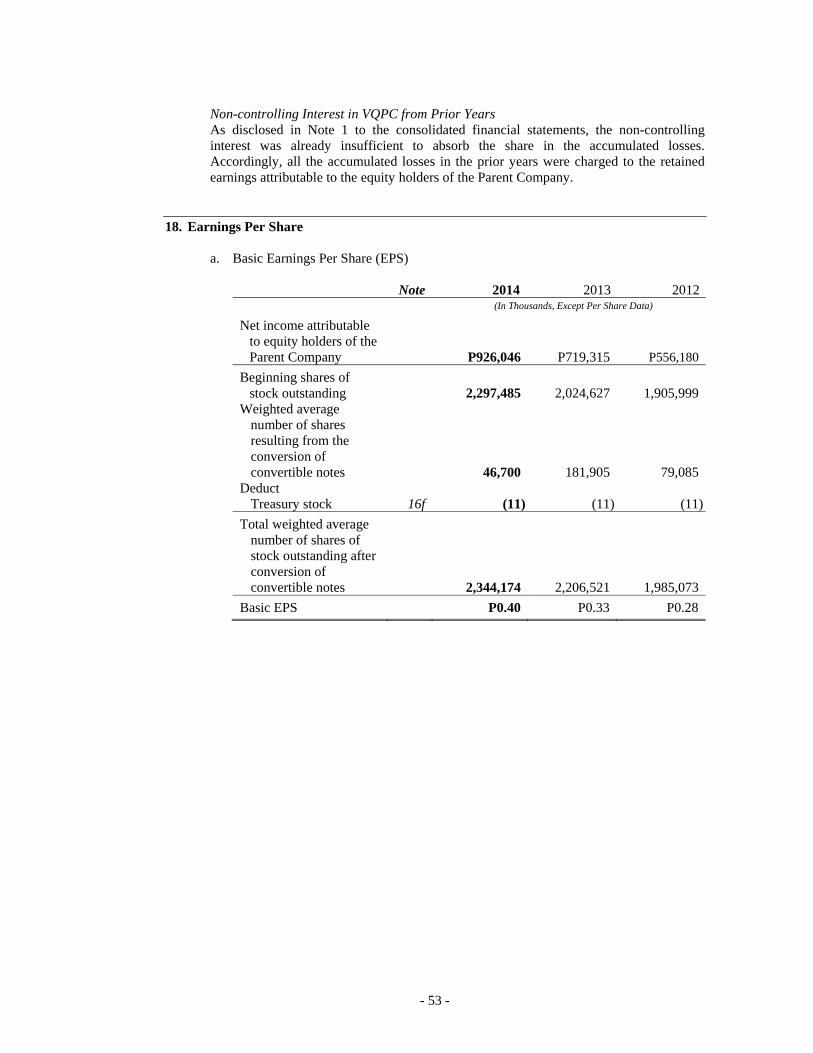

Basic Earnings per share (EPS) Basic EPS is used as a barometer to gauge the Group’s profitability per unit of shareholder ownership. It is calculated by dividing net income earned in a given reporting period by the weighted average number of shares outstanding during the same term.

ITEM 7 – FINANCIAL STATEMENTS

(Please see attached duly signed Corporation’s Consolidated Financial Statements as of August 31, 2014, together with the notarized Statement of Management’s Responsibility, which was prepared by R.G. Manabat & Co. (KPMG), the Corporation’s external auditor for crop year 2013-2014, as Exhibit “A“. ITEM 8 – CHANGES IN & DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

There has been no disagreement with the external auditor on accounting, financial concerns, and

disclosures in the Financial Statements, which is attached hereto as Exhibit “A”. INFORMATION ON INDEPENDENT ACCOUNTANT

For Crop Year 2013-2014, the services of the accounting firm R.G. Manabat & Co. (KPMG), with office address at 9th Floor, KPMG Center, 6787 Ayala Avenue, Makati City, 1226, Metro Manila, Philippines, was engaged to be the Corporation’s External Auditors, in compliance with the Corporation’s Code of Corporate Governance that provides that the Corporation’s External Auditor shall be rotated or the handling partner shall be changed every five (5) years or earlier. EXTERNAL AUDIT FEES Audit and Audit-Related Fees

The aggregate fees billed for each of the last two (2) fiscal years for professional services rendered by the external auditor for the audit of the Corporation’s annual financial statements or services that are normally provided by the external auditor in connection with statutory and regulatory filings or engagement for those fiscal years were: CY 12-13 – P2,840,000.00 – net of VAT CY 13-14 – P 1,481,200.00 - net of VAT Tax Fees

There has been no fee billed for the last two (2) fiscal years for professional services rendered by the external auditor for tax accounting, compliance, advice, planning and any other form of tax services. Audit Committee’s Approval Policies and Procedures for the Above Services

The Audit Committee’s approval policies and procedures for the above services are as follows: 1. The Audit committee invites bidders for the external audit engagement for preliminary evaluation. 2. The Committee then presents to the bidders, the corporate profiles of the companies to be covered

by the audit.

23

3. The Committee likewise presents its expectations on the deadline for the completion of the Audit and filing of the audited financial statement.

4. The bidders are required to make its corporate profiles, list of experiences, and proposed audit engagement fee.

5. The Committee evaluates the proposals and makes a choice. 6. The choice is announced during the Stockholder’s meeting.

PART III – CONTROL AND COMPENSATION INFORMATION

ITEM 9 – DIRECTORS AND EXECUTIVE OFFICERS OF THE ISSUER

VMC BOARD OF DIRECTORS

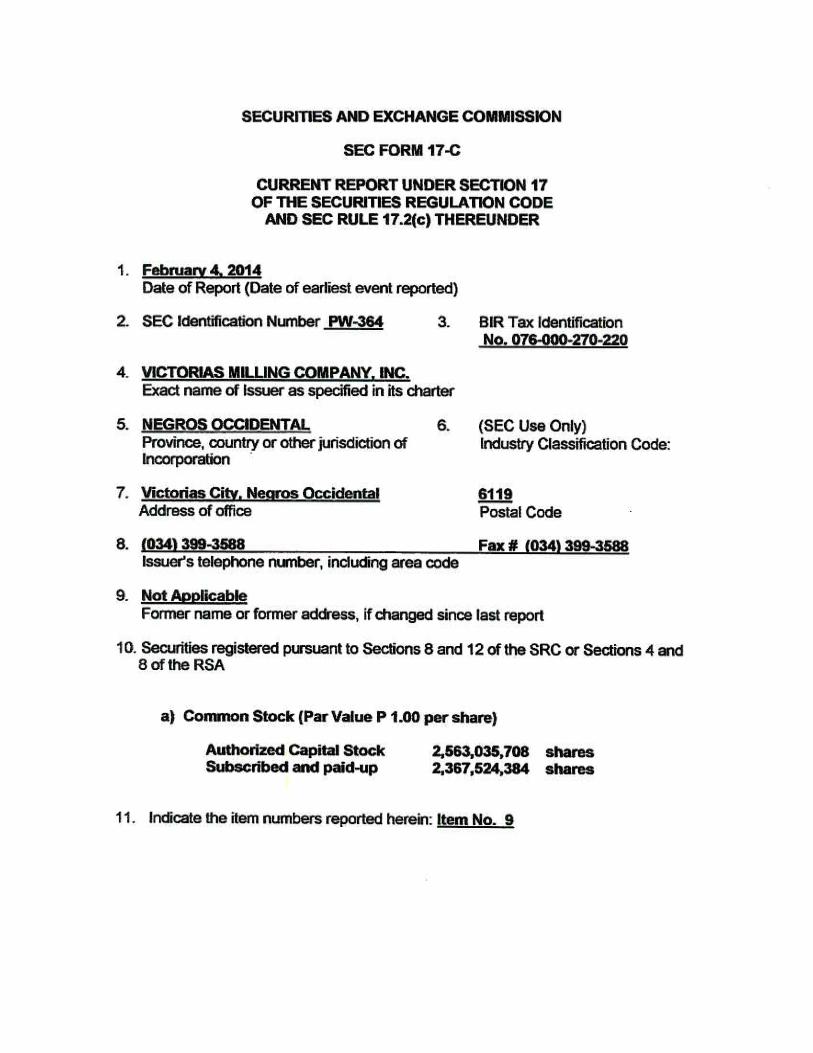

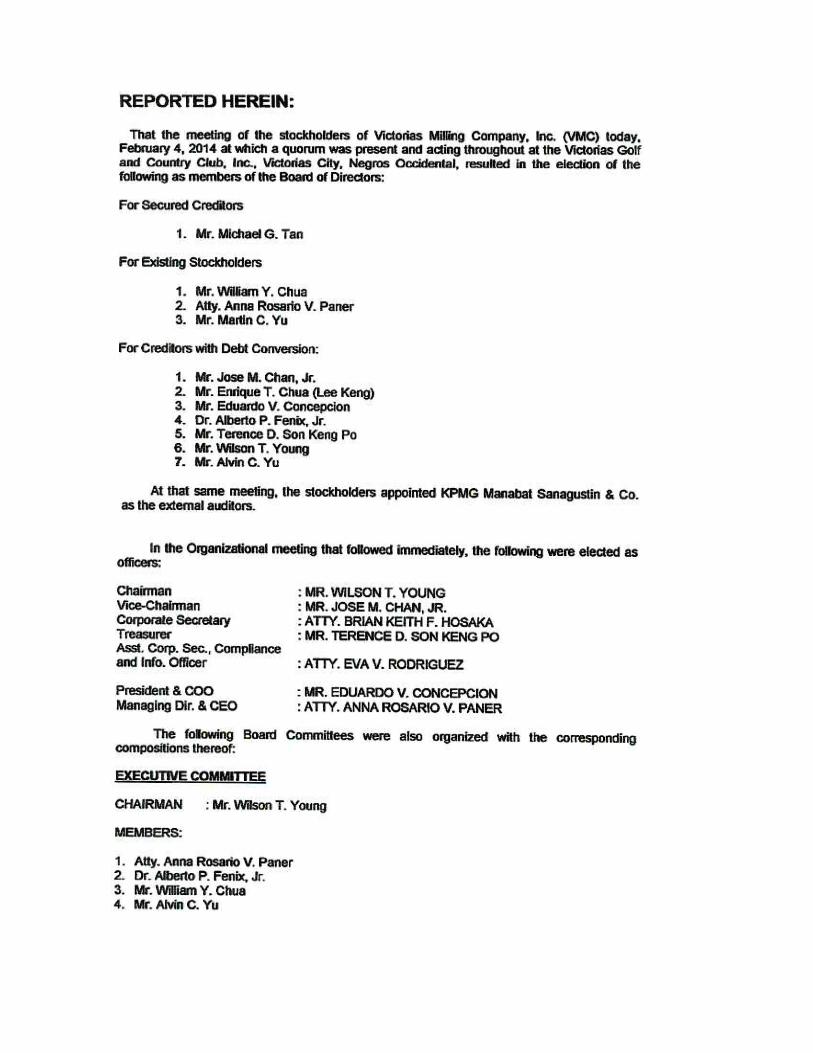

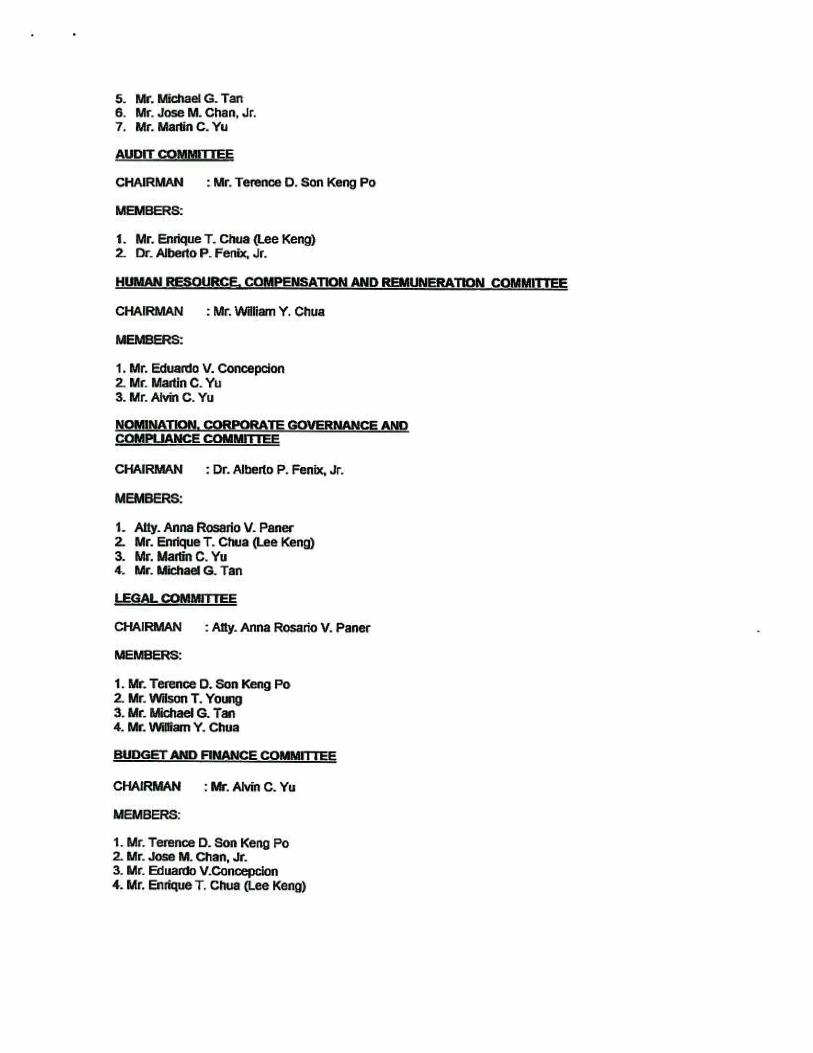

During VMC’s Annual Stockholder’s Meeting held on February 4, 2014, the following were elected as members of the VMC Board of Directors to serve as such from February 4, 2014 and until their successors shall have been duly elected and qualified:

1. Wilson T. Young, age 58, Filipino, current Chairman of Victorias Milling Company, Inc.’s Board. Director of BK Titans, Inc., Perf Restaurants, Inc. (franchisee of Burger King in the Philippines). He is also a member of the Board of Trustees of the University of the East and Vice-Chairman of the University of the East Ramon Magsaysay Memorial Medical Center, Inc., member of the International Board of Advisers of the Philippine School of Prosthetics and Orthotics, as well as member of the Board of the following foundations: Mithing Pangarap Foundation, Inc., Norfil Foundation, Inc., and the National Defense College of the Philippines Educational and Development Foundation, Inc. He also serves as member of the Board of Admissions of the National Defense College of the Philippines and Chairman of Total Credit Cooperative. He was formerly an instructor of Taxation and Accounting at Assumption College, San Lorenzo Makati and Financial Accounting at the Ateneo de Manila Loyola. A Certified Public Accountant and holds a Masters Degree in National Security Administration. Likewise he is a Director and/or Officer of various family-owned and controlled corporation and was a former Director and Officer of certain companies of the LT Group, Inc.

2. Anna Rosario V. Paner, age 43, Filipino, is VMC's Managing Director, Chief-Executive Officer

and Chair of the Legal Committee. She has been a private law practitioner since 1996 and is one of the founding partners of Paner Hosaka & Ypil Attorneys-at-Law. She currently chairs Victorias Foods Corporation and, for the past five (5) years, she has been connected with Philippine Opportunities for Growth, Income (SPV-AMC), Inc., Techbox International Inc. and Nota Bene as their director.

3. Eduardo V. Concepcion, age 61, is currently the President and Chief Operating Officer of

VMC. He graduated with Honors at the De la Salle University with a degree of Bachelor of Science in Chemical Engineering. He is a licensed Chemical Engineer and took his Master in Business Administration (without thesis) at University of San Agustin-Iloilo. He has served Central Azucarera de La Carlota, Inc. as Vice President/Resident Manager. Morever, he has rendered service to Ma-ao Sugar Central and Passi (Iloilo) Sugar Central, Inc. He has been working with the sugar industry for more than 39 years.

4. William Y. Chua, age 50, Filipino, is the President of Agro Bulk Marine Corporation, Wilch

Realty Corporation and MC Metroplex Holding Corp. He is also the Vice President of Oro Allado Commodities, Inc., Negros Ship-owners Association and Federation of Sugar Traders of the Phils.

5. Brian Keith F. Hosaka, age 43, Filipino, is the Corporate Secretary and Director of VMC. He is one of the founding partners of Paner Hosaka & Ypil Attorneys-at-Law. He graduated from the Ateneo de Manila University in 1993, and thereafter obtained a Juris Doctor degree from the Ateneo De Manila Law School in 1998. He was admitted to the Philippine BAR in 1999. He previously worked for the Supreme Court of the Philippines, and also served as Deputy General Counsel of the Integrated Bar of the Philippines (National Office) from 2006 to 2007.

24

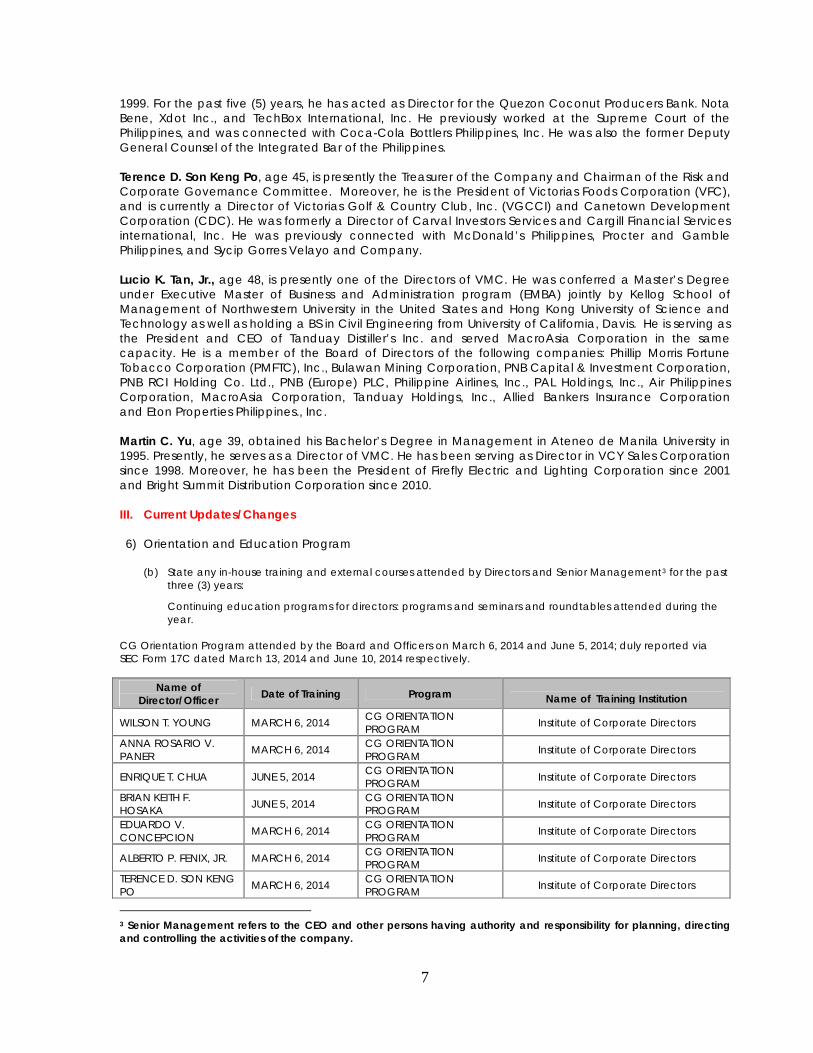

6. Lucio K. Tan, Jr., age 48, is presently one of the Directors of VMC. He was conferred a Master’s Degree under Executive Master of Business and Administration Program (EMBA) jointly by Kellogg School of Management of Northwestern University in the United States and Hong Kong University of Science and Technology was well as holding a BS in Civil Engineering from University of California, Davis. He is serving as the President and CEO of Tanduay Distiller’s Inc. and served MacroAsia Corporation in the same capacity. He is a member of the Board of Directors of the following companies: Phillip Morris Fortune Tobacco Corporation (PMFTC), Inc., Bulawan Mining Corporation, PNB Capital & Investment Corporation, PNB RCI Holding Co., Ltd., PNB (Eirope) PLC, Philippine Airlines, Inc., Air Philippines Corporation, MacroAsia Corporation, Tanduay Holdings, Inc., Allied Bankers Insurance Corporatiion and Eton Properties Philippines, Inc.

7. Michael G. Tan, age 48, Filipino, is presently the Chief Operating Officer of Asia Brewery, Inc.

and the President and Chief Operating Officer of LT Group, Inc. (formerly Tanduay Holdings Inc.). For the past five (5) years, he served as a director of the following corporations: Abacus Distribution Systems Philippines, Inc., Allied Banking Corporation, Eton Properties, Inc., Philippine National Bank and PMFTC.

8. Terence D. Son Keng Po, age 46, Filipino, is presently the Treasurer of the corporation.

Moreover he is the President of Victorias Foods Corporation (“VFC”). He is currently a Director of Victorias Golf & Country Club, Inc. (“VGCCI”) and Canetown Development Corporation (“CDC”). He served as a Director of Carval Investors Services and Cargill Financial Services International, Inc. (both subsidiaries of Cargill, Inc.).

9. Alberto P. Fenix, Jr., age 70, Filipino, is currently the Chairman of VMC’s Audit Committee.

He is also the Chairman and President of Fenix Management and Capital, Inc., Chairman of Newtech Pulp, Inc., President of Ivoclar Vivadent, Inc., and Executive Director of SPC Power Corporation, a publicly listed corporation. He also serves as an Officer and Director in the subsidiaries and affiliates of the above companies. He graduated from the Ateneo de Manila University with a bachelor’s degree in Mathematics, and holds Masters and Doctorate degrees in Industrial Management from the Sloan School of Management of the Massachusetts Institute of Technology. He was the 1998 and 1999 President of the Philippine Chamber of Commerce and Industry (PCCI), and up to the present, its Honorary President.

10. Alvin C. Yu, age 41, Filipino, is the President of Narra Capital Investment Corporation,

Bacolod DN Triumph Steel Corporation and Bacolod Twinstar Shipping Corporation. He is the Vice President of VCY Sales Corporation and the Manager of Bacolod Triumph Hardware. He graduated from the Ateneo de Manila University with a Management Engineering degree.

11. Martin C. Yu, age 39, is the President of Firefly Electric & Lighting Corporation from 2001 until

the present years. He is likewise a Director of VCY Sales Corporation since 1998. He took up Business Management in the Ateneo de Manila University.

In the subsequent organizational meeting of the Board of Directors, the following corporate officers were appointed –

1. Wilson T. Young, Chairman of the Board of Directors

2. Anna Rosario V. Paner, Vice Chairman of the Board of Directors

3. Eduardo V. Concepcion, President & Chief Operating Officer

4. Terence D. Son Keng Po, Treasurer

25

5. Brian Keith F. Hosaka, Corporate Secretary

6. Eva A. Vicencio-Rodriguez, Assistant Corporate Secretary, and Compliance and Information Officer.

Executive Officers of VMC

1. Atty. Anna Rosario V. Paner, age 43, Filipino, a Bachelor of Laws degree holder and presently the Managing Director and CEO of the corporation.

2. Eduardo V. Concepcion, age 61, Filipino, a Bachelor of Science in Chemical Engineering

graduate and a Masters in Business Administration degree holder. He is presently the President and Chief Operating Officer of VMC.

3. Linley A. Retirado, age 53, Filipino, is currently occupying the position of the Chief Manufacturing Officer. He is a licensed Mechanical Engineer and presently the Chairman of the Board of the Philippine Sugar & Technologist Association, Inc. (PHILSUTECH). 4. Teresita V. Ilagan, age 55, Filipino, is the Chief Finance Officer of VMC She is concurrently Director and Treasurer of various VMC subsidiaries, particularly Canetown Development Corporation (CDC) and Victorias Agricultural Land Corporation (VALCO), Victorias Food Corporation (VFC) and Victorias Golf & Country Club Inc. (VGCCI). She is the Assistant Treasurer and the Liquidator of Victorias Quality Packaging Company, Inc. (VQPC). She is a Certified Public Accountant and a Masters in Business Administration degree holder.

5. Eva A. Vicencio-Rodriguez, age 46, Filipino, is the Acting Chief Administrative Officer of VMC. A BS Psychology and Bachelor of Laws graduate and is a degree holder of Masters in Business Administration. She is also the Assistant Corporate Secretary and Compliance Information Officer of the Corporation. She is likewise the Head of VMC’s Legal & Compliance Division and the Corporate Secretary of the following VMC subsidiaries: Victorias Foods Corporation (VFC), Victorias Golf & Country Club, Inc., Victorias Quality Packaging Company, Inc. (VQPC) and Canetown Development Corporation (CDC) where she likewise serves as a Director. She is also the Director of Victorias Agricultural Land Corporation (VALCO). To the knowledge and/or information of the Corporation, the above elected members of the Board of Directors, are not, presently or during the last (5) years, involved or have been involved in any legal proceedings affecting/involving themselves and/or their property before any court of law or administrative body in the Philippines or elsewhere and have not been convicted by final judgment of any offense, except as follows:

a. Vivian T. Tiongkiao vs. MERALCO, Paner, Hosaka, & Ypil Offices (PHY Law); ERC Case No. 2010-059CC. Complainant filed a complaint against MERALCO and PHY Law to ensure continued service of electricity by MERALCO to a condominium unit owned by PHY Law but occupied by Complainant. The case has been submitted for resolution;

b. Ernie V. Atanez et. al. vs. Firefly Electric & Lighting Corporation (FELCO), Martin Yu and Sherwin Yu, NLRC NCR Case No. 02-01885-14, and Rafael G. Escarda et. al. vs. Firefly Electric & Lighting Corporation (FELCO), Martin Yu and Sherwin Yu, NLRC NCR Case No. 03-0324040-14 (Consolidated Cases). Agency personnel filed an illegal dismissal case with monetary claims against FELCO before the Labor Arbiter’s Office. Martin Yu was impleaded in his capacity as President of FELCO. Immediately prior to the filing of the case, the agency personnel were employed with Total Staff Skills Corporation (TSSC), a registered job contractor. TSSC is now impleaded as a party respondent. The case is still pending mediation/conciliation.

26

c. Richard T. Divinagracia and Clinton Cayao vs. Victorias Milling Company, Inc./Francis Ferraris, Dept. Head/Eduardo V. Concepcion, President, RAB VI Case No. 10-10978-14, and Rene Sobremisana vs. Victorias Milling Company, Inc. vs. Eduardo V. Concepcion, President and COO, RAB VI Case No. 10-10944-14. For illegal dismissal, and money claims.

The said persons mentioned above are not related to each other in any way. There is no person who is not a corporate officer of the Corporation who is expected to make a significant contribution to the business. The Corporation, however, engages the services of consultants. As of August 31, 2014, the Corporation has 8 consultants and none under special contract. There were no transactions during the last two years or any proposed transactions, to which the Corporation was or is to be a party, in which any director or officers, any nominee for election as a director, any security holder or any member of the immediate family of any of the person mentioned had or is to have a direct or indirect material interest. ITEM 10 – EXECUTIVE COMPENSATION

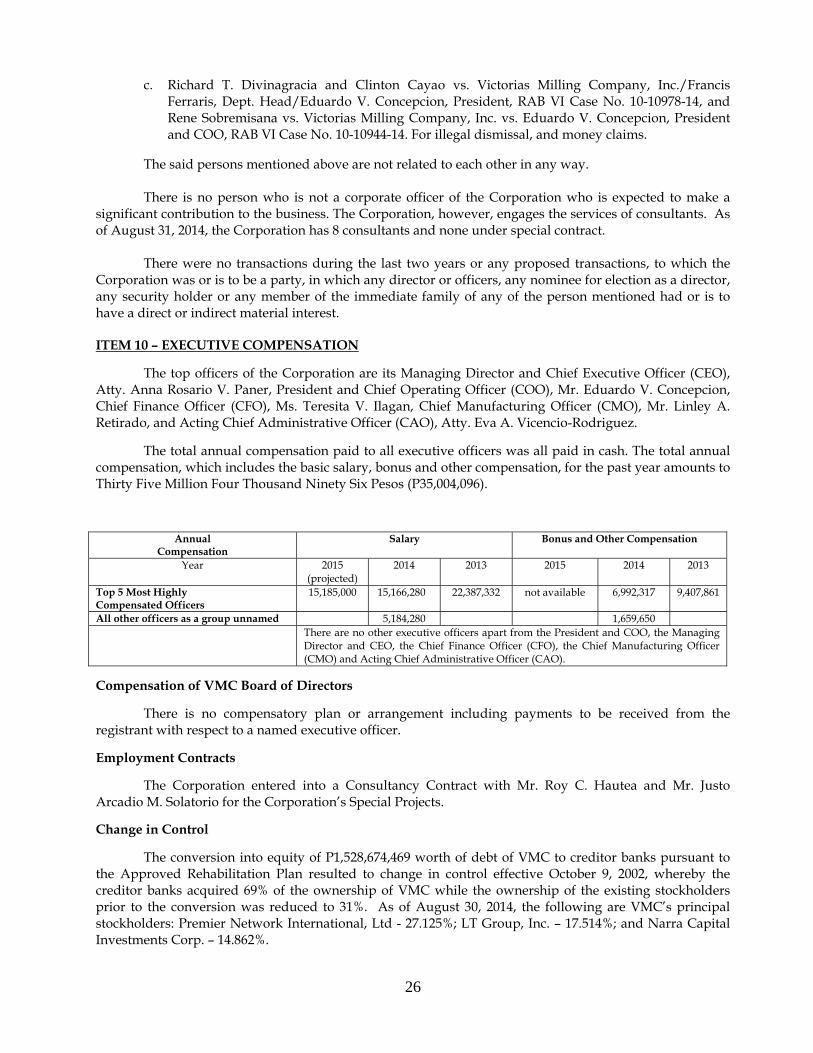

The top officers of the Corporation are its Managing Director and Chief Executive Officer (CEO), Atty. Anna Rosario V. Paner, President and Chief Operating Officer (COO), Mr. Eduardo V. Concepcion, Chief Finance Officer (CFO), Ms. Teresita V. Ilagan, Chief Manufacturing Officer (CMO), Mr. Linley A. Retirado, and Acting Chief Administrative Officer (CAO), Atty. Eva A. Vicencio-Rodriguez.

The total annual compensation paid to all executive officers was all paid in cash. The total annual compensation, which includes the basic salary, bonus and other compensation, for the past year amounts to Thirty Five Million Four Thousand Ninety Six Pesos (P35,004,096).

Annual Compensation

Salary Bonus and Other Compensation

Year 2015 (projected)

2014 2013 2015

2014 2013

Top 5 Most Highly Compensated Officers

15,185,000 15,166,280 22,387,332 not available 6,992,317 9,407,861

All other officers as a group unnamed 5,184,280 1,659,650 There are no other executive officers apart from the President and COO, the Managing

Director and CEO, the Chief Finance Officer (CFO), the Chief Manufacturing Officer (CMO) and Acting Chief Administrative Officer (CAO).

Compensation of VMC Board of Directors

There is no compensatory plan or arrangement including payments to be received from the registrant with respect to a named executive officer. Employment Contracts

The Corporation entered into a Consultancy Contract with Mr. Roy C. Hautea and Mr. Justo Arcadio M. Solatorio for the Corporation’s Special Projects. Change in Control

The conversion into equity of P1,528,674,469 worth of debt of VMC to creditor banks pursuant to the Approved Rehabilitation Plan resulted to change in control effective October 9, 2002, whereby the creditor banks acquired 69% of the ownership of VMC while the ownership of the existing stockholders prior to the conversion was reduced to 31%. As of August 30, 2014, the following are VMC’s principal stockholders: Premier Network International, Ltd - 27.125%; LT Group, Inc. – 17.514%; and Narra Capital Investments Corp. – 14.862%.

27

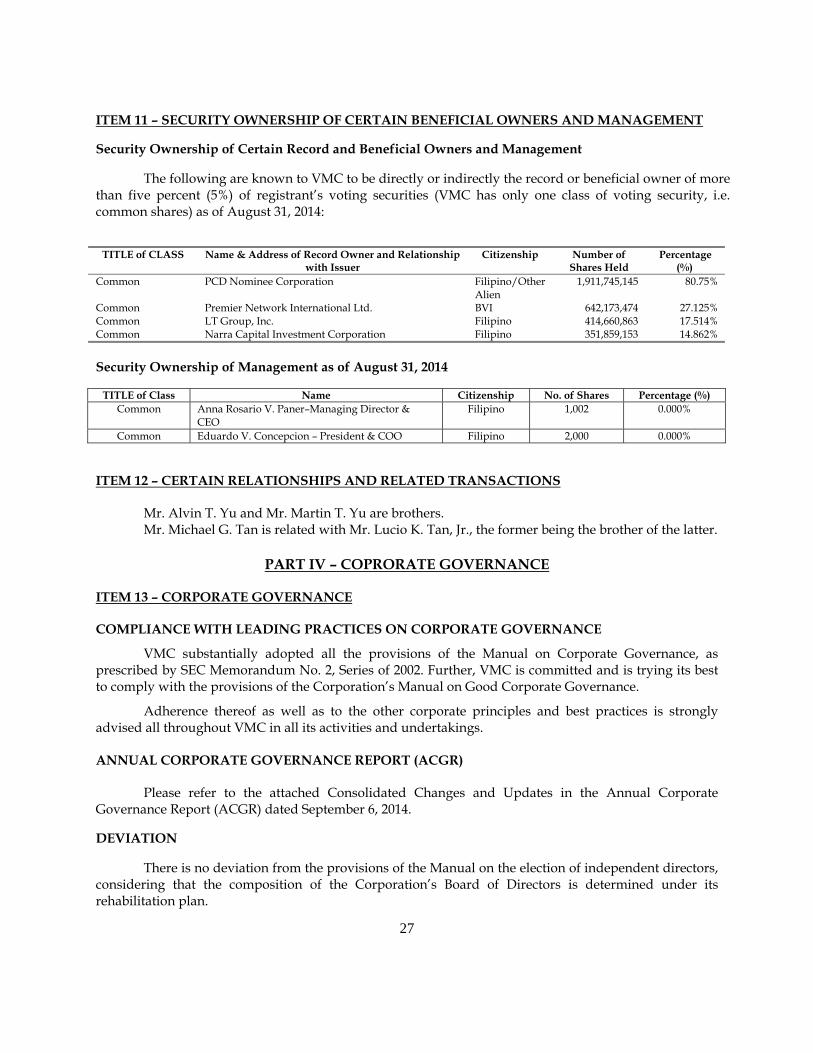

ITEM 11 – SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT Security Ownership of Certain Record and Beneficial Owners and Management

The following are known to VMC to be directly or indirectly the record or beneficial owner of more

than five percent (5%) of registrant’s voting securities (VMC has only one class of voting security, i.e. common shares) as of August 31, 2014:

TITLE of CLASS Name & Address of Record Owner and Relationship with Issuer

Citizenship Number of Shares Held

Percentage (%)

Common PCD Nominee Corporation Filipino/Other Alien

1,911,745,145 80.75%

Common Premier Network International Ltd. BVI 642,173,474 27.125% Common LT Group, Inc. Filipino 414,660,863 17.514% Common Narra Capital Investment Corporation Filipino 351,859,153 14.862% Security Ownership of Management as of August 31, 2014

TITLE of Class Name Citizenship No. of Shares Percentage (%)

Common Anna Rosario V. Paner–Managing Director & CEO

Filipino 1,002 0.000%

Common Eduardo V. Concepcion – President & COO Filipino 2,000 0.000% ITEM 12 – CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS Mr. Alvin T. Yu and Mr. Martin T. Yu are brothers.

Mr. Michael G. Tan is related with Mr. Lucio K. Tan, Jr., the former being the brother of the latter.

PART IV – COPRORATE GOVERNANCE

ITEM 13 – CORPORATE GOVERNANCE COMPLIANCE WITH LEADING PRACTICES ON CORPORATE GOVERNANCE

VMC substantially adopted all the provisions of the Manual on Corporate Governance, as prescribed by SEC Memorandum No. 2, Series of 2002. Further, VMC is committed and is trying its best to comply with the provisions of the Corporation’s Manual on Good Corporate Governance.

Adherence thereof as well as to the other corporate principles and best practices is strongly advised all throughout VMC in all its activities and undertakings. ANNUAL CORPORATE GOVERNANCE REPORT (ACGR) Please refer to the attached Consolidated Changes and Updates in the Annual Corporate Governance Report (ACGR) dated September 6, 2014. DEVIATION There is no deviation from the provisions of the Manual on the election of independent directors, considering that the composition of the Corporation’s Board of Directors is determined under its rehabilitation plan.

28

PART V- EXHIBITS AND SCHEDULES

A. EXHIBITS AND SCHEDULES

1. EXHIBIT “A” – Consolidated Audited Financial Statement as of August 31, 20142. EXHIBIT “B” – Reports on SEC Form 17-C3. EXHIBIT “C” – Consolidated Changes & Updates in the Annual Corporate Governance Report

B. REPORTS ON SEC FORM 17-C (EXHIBIT”B”)

1. Reported on August 5, 2014, election of Atty. Anna Rosario V. Paner as Vice-Chairman of the Board, to fill the vacancy caused by the resignation of Mr. Jose M. Chan, Jr. as Director of VMC, who was also the Vice-Chairman of the Board.

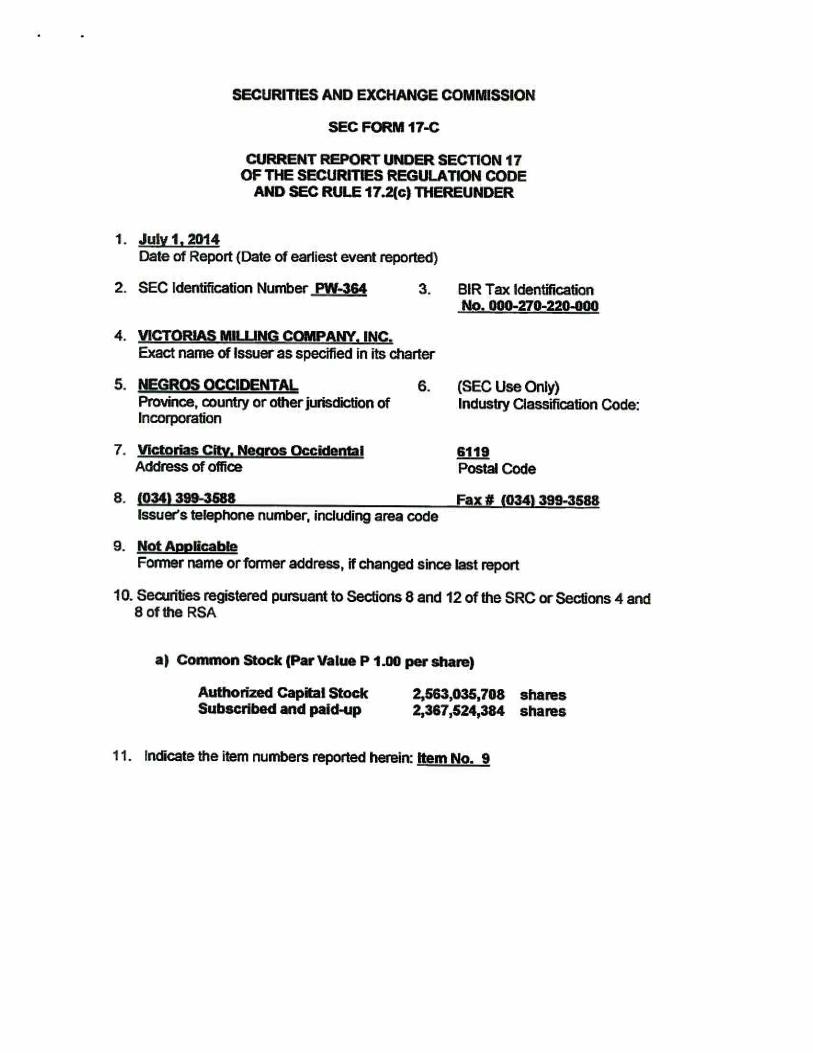

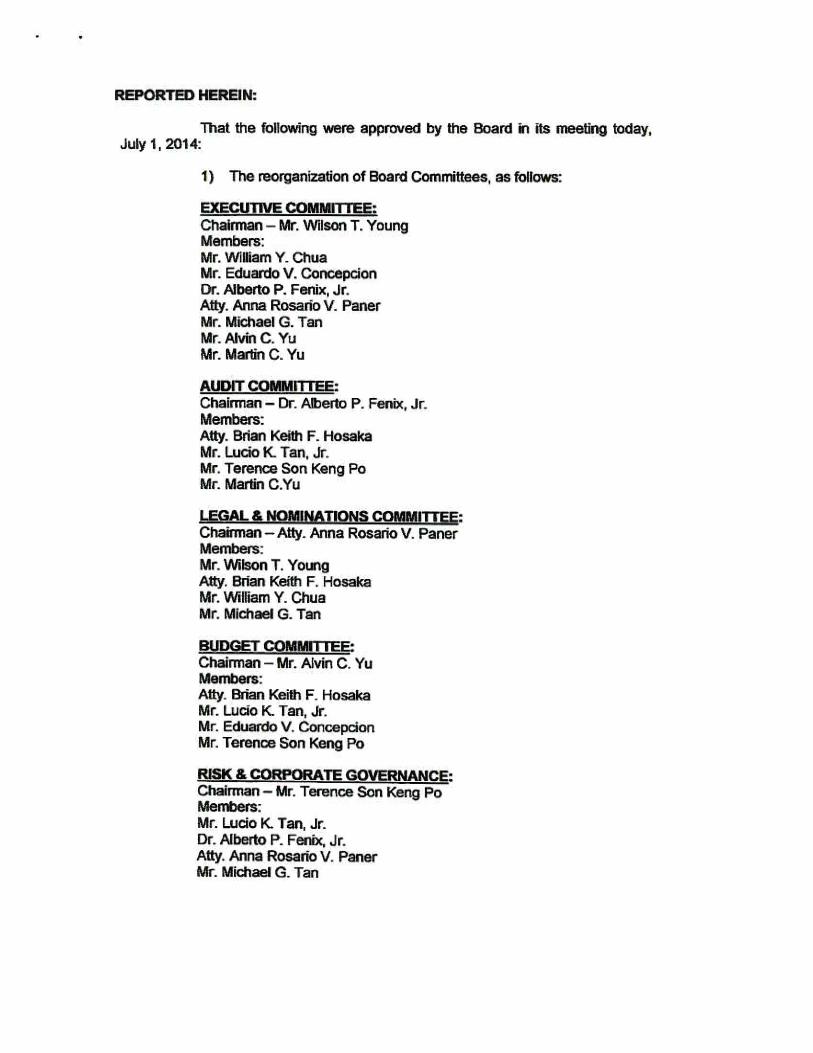

2. Reported on July 1, 2014, the reorganization of the Board Committees and the appointment of Atty. Eva A. Vicencio-Rodriguez as Acting Chief Administrative Officer.

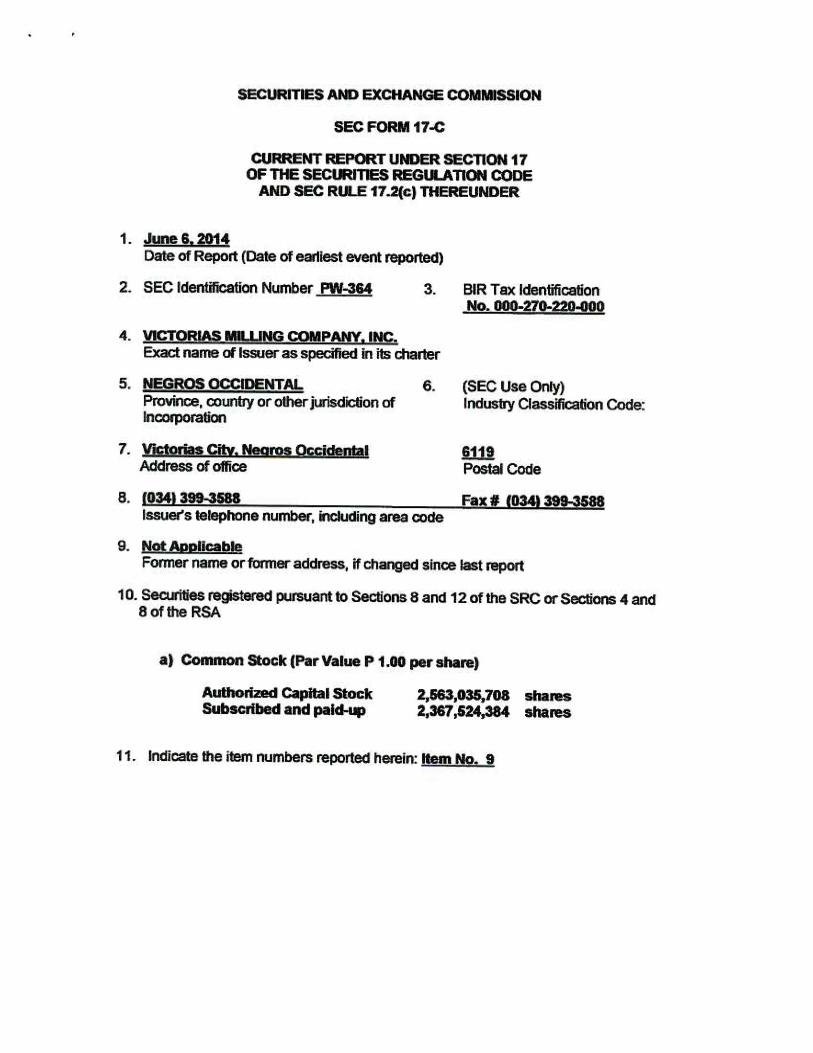

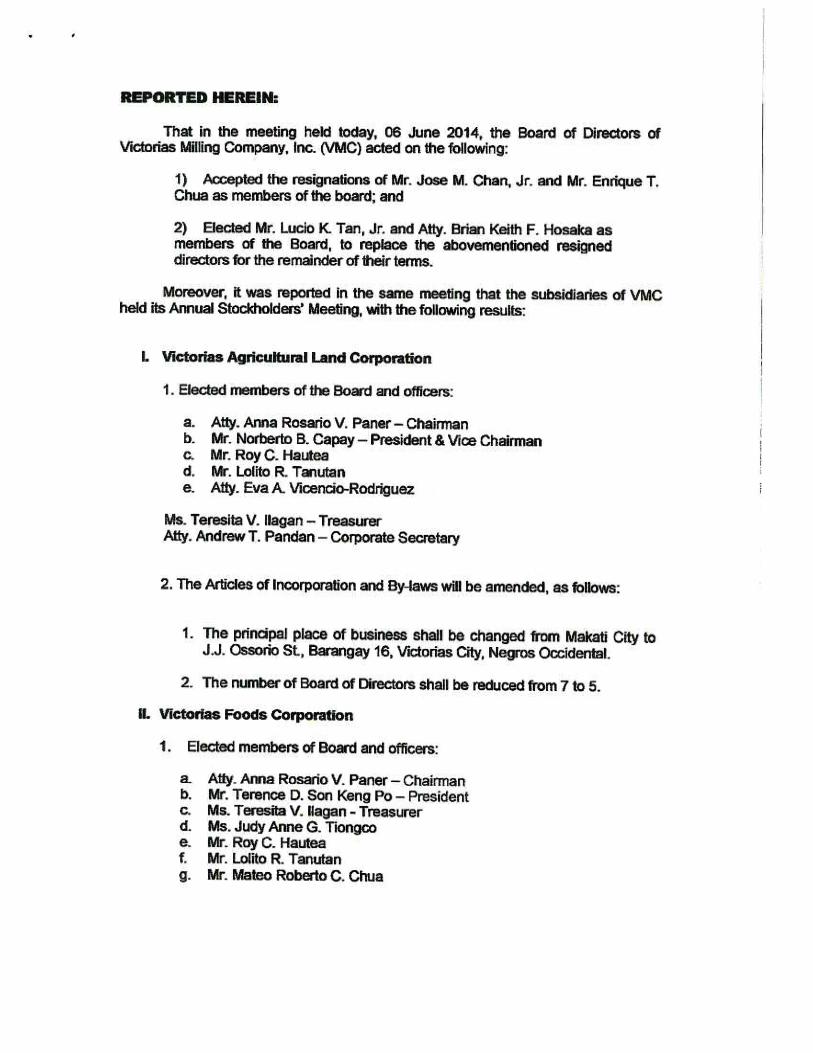

3. Reported on June 6, 2014, the resignation of Mr. Jose M. Chan, Jr., and Mr. Enrique T. Chua as members of the Board of Directors. Elected Mr. Lucio K. Tan, Jr. and Atty. Brian Keith F. Hosaka to replace the directors for the remainder of their terms. Disclosed also the stockholders’ meeting of VMC’s subsidiaries, Victorias Agricultural Land Corp. (VALCO) and Victorias Foods Corp. (VFC) with its newly elected directors and officers. Amended its principal office and numbers of the Board of Directors on the Articles of Inc. and By Laws.

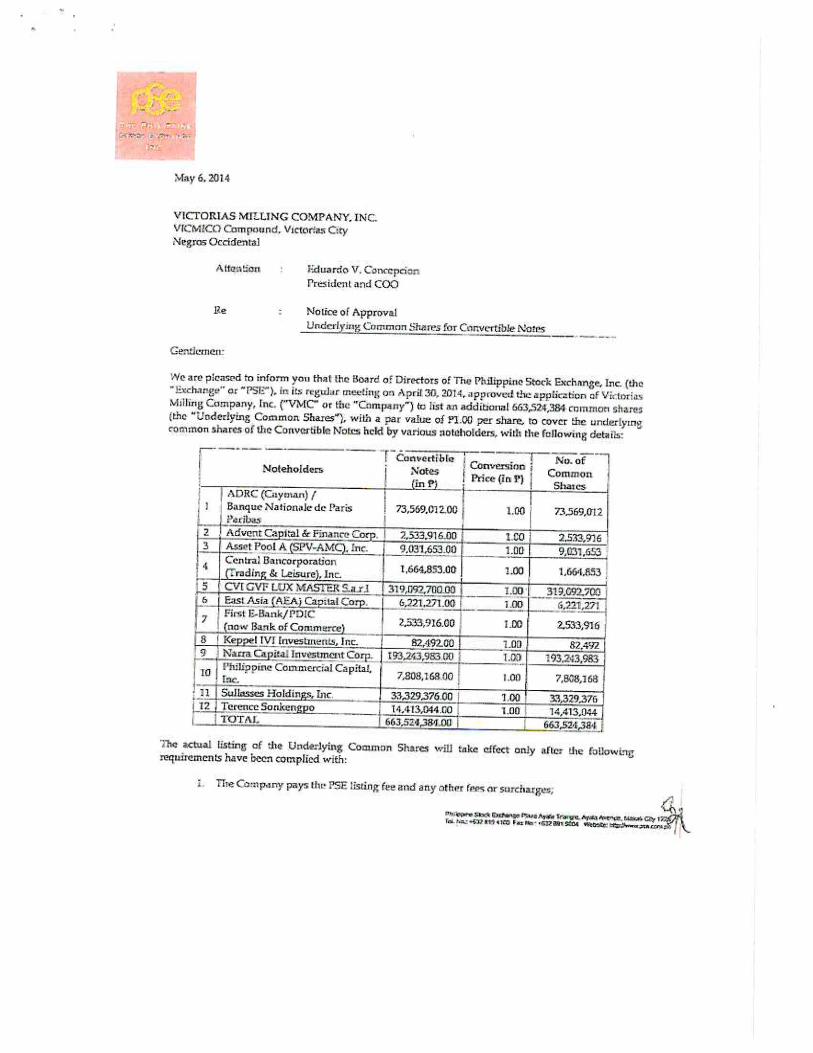

4. Reported on May 9, 2014, the approval of VMC’s listing application with the Philippine Stock Exchange, which was received by VMC on May 8, 2014.

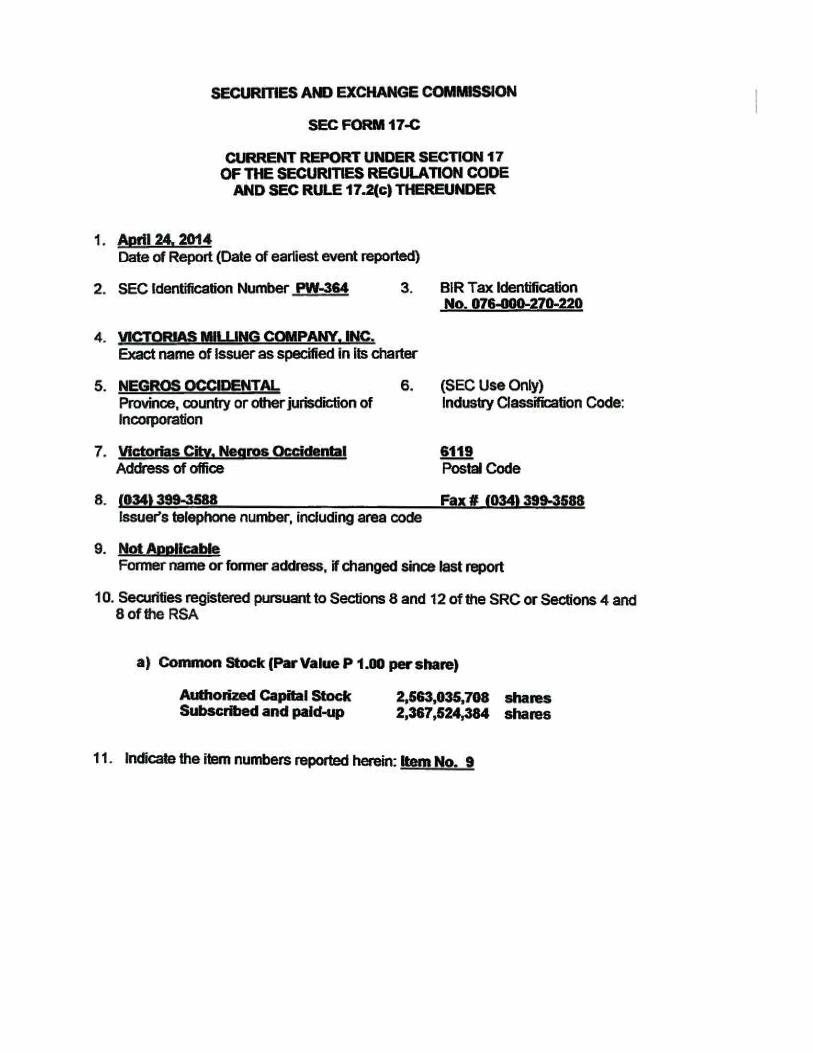

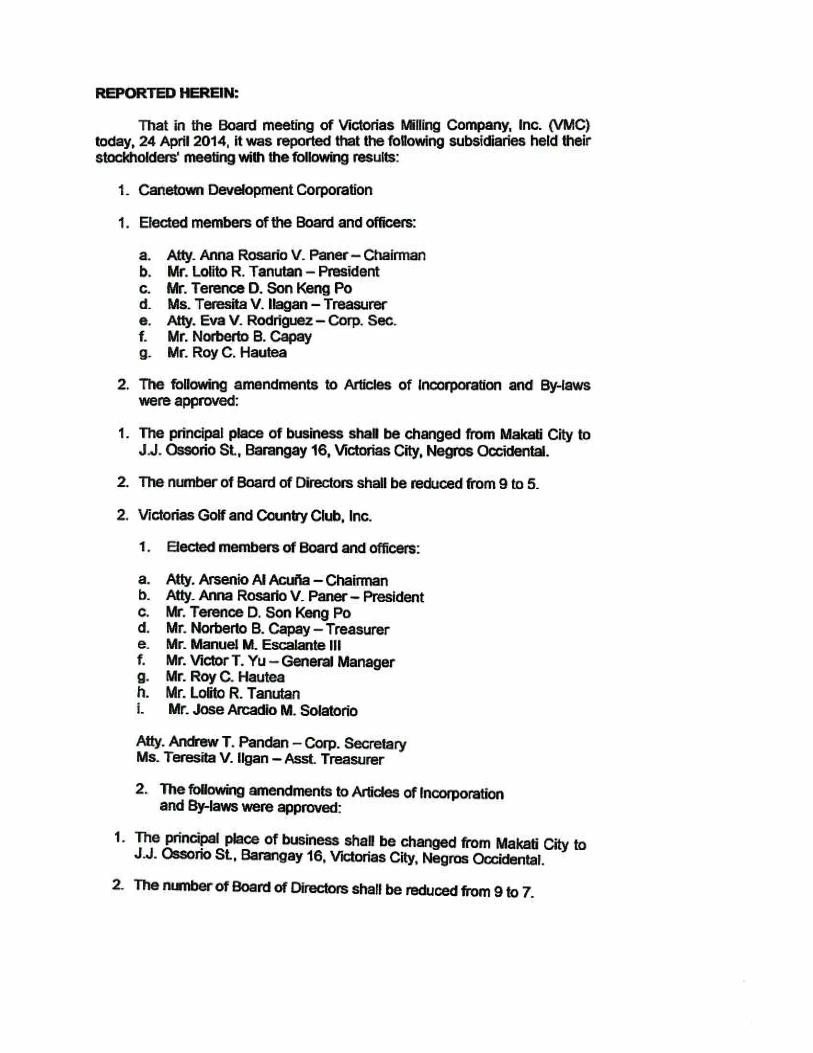

5. Reported on April 24, 2014, the stockholders meeting of the subsidiaries of VMC, the Canetown Development Corp (CDC) and Victorias Golf & Country Club, Inc. (VGCCI), with its newly elected directors and officers. Amended its principal office and numbers of the Board of Directors on the Articles of Incorporation and By Laws of the corporation.

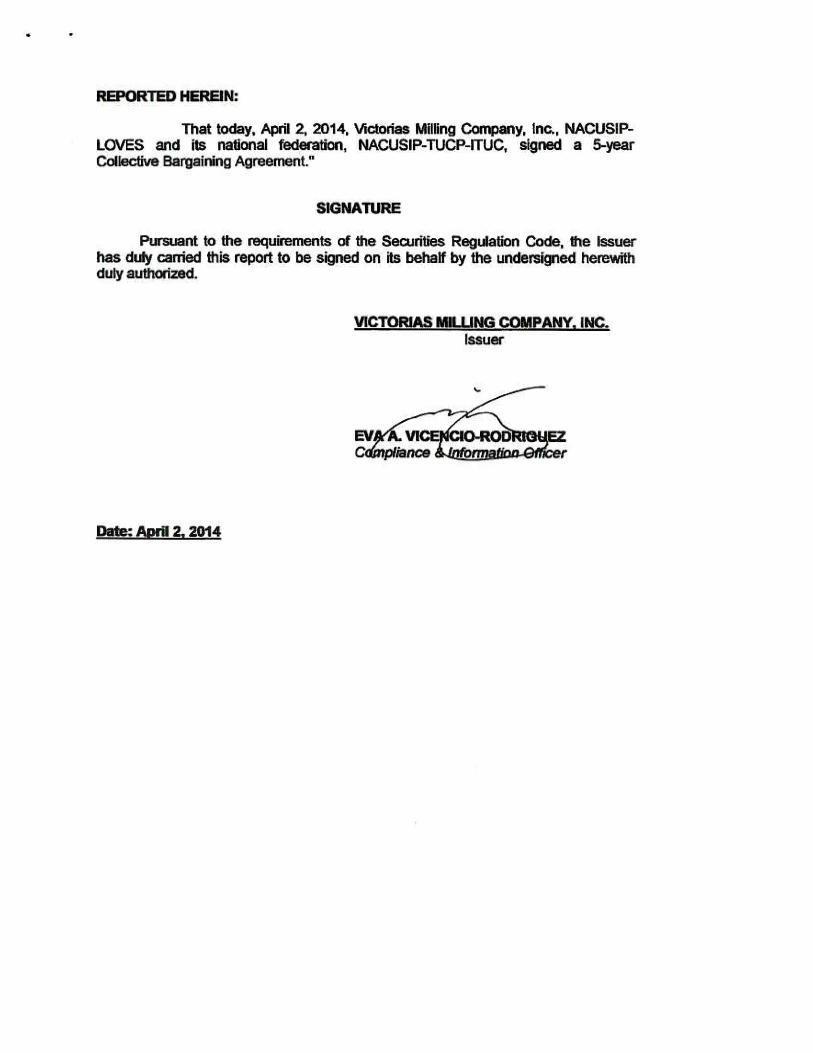

6. Reported on April 2, 2014, VMC, NACUSIP-LOVES and its national federation, NACUSIP-TUCP-ITUC, signed a five (5) year Collective Bargaining Agreement.

7. Reported on March 31, 2014, the VMC Board of Directors approved the payment/redemption of convertible notes of up to about P600 Million Pesos, pursuant to the Alternative Rehabilitation Plan and the Debt Restructuring Agreement; submission to the PSE of the Corporate Governance Disclosure Survey for 2013; Revision of the Manual on Corporate Governance; proposed Collective Bargaining Agreement with NACUSIP-Labor Organization of VMC Employees (LOVES); and appointment of Ms. Judy Anne G. Tiongco as VMC’s Investor Relations Officer.

8. Reported on March 12, 2014, SEC Order dated March 3, 2014 on the Manifestation and Motion dated November 12, 2012 filed by VMC to amend Part IV of the ARP and Section 21 of the DRA were ordered amended.

9. Reported on February 21, 2014, the appointment of AB Stock Transfers Corporation as the Corporation’s new stock transfer agent effective April 1, 2014. Disclosed the payment/redemption of Convertible Notes (principal plus corresponding accumulated interest as of February 28, 2014) up to One Billion Four Hundred Twenty Million Pesos (Php1.420 Billion), pursuant to the Debt Restructuring Agreement. The appointment of Mr. Victor T. Yu as Acting Chief Administrative Officer.

29

10. Reported on February 4, 2014, the result of the election of the members of the Board of Directors, Officers and the Board Committees with its corresponding composition. Appointed R.G. Manabat & Co. (KPMG) as the external auditors.

11. Disclosed on February 3, 2014 wherein the Board approved the recommendation of the Corporation’s Nomination Corporate Governance & Compliance Committee for the nomination of Mr. Michael G. Tan by Philippine National Bank, to the seat allocated for the Secured Creditors in the Board of VMC, in compliance with the Order of the Securities & Exchange Commission dated January 27, 2014 to elect its Board of Directors in accordance with the Approved Rehabilitation Plan and Debt Restructuring Agreement.

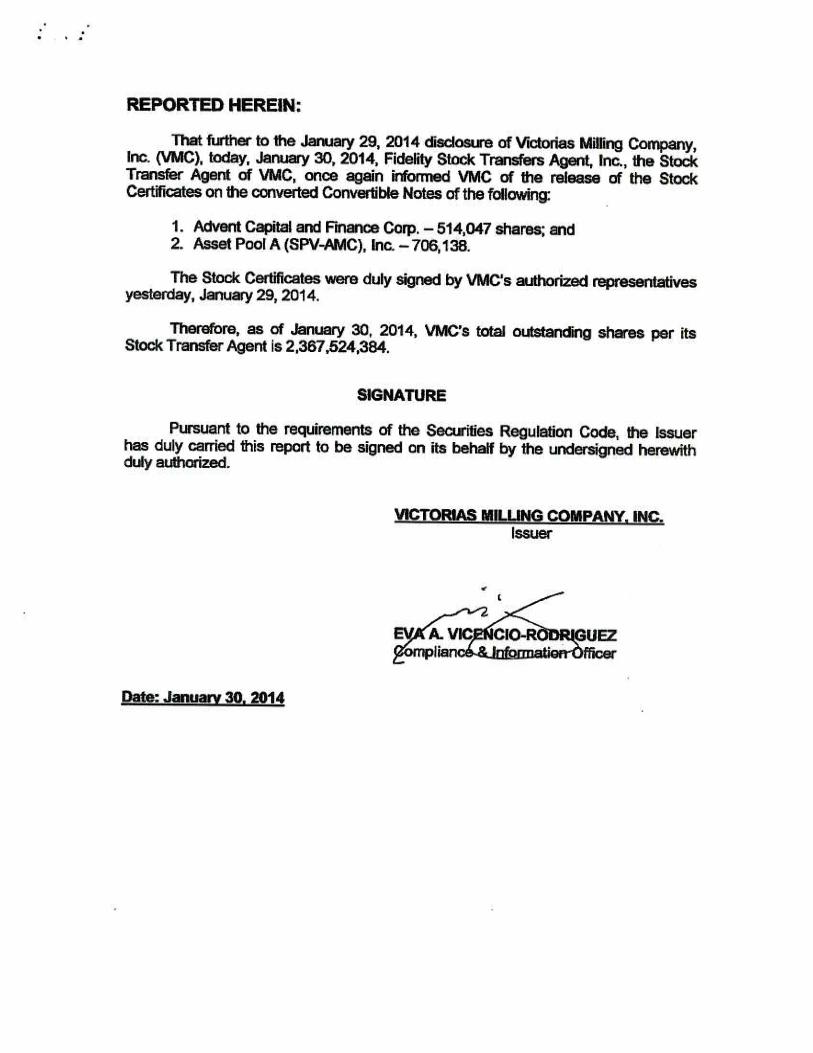

12. Reported on January 30, 2014, once again the release of the Stock Certificates on the converted Convertible Notes. Total Outstanding Shares per stock transfer agent is 2,367,524,384.

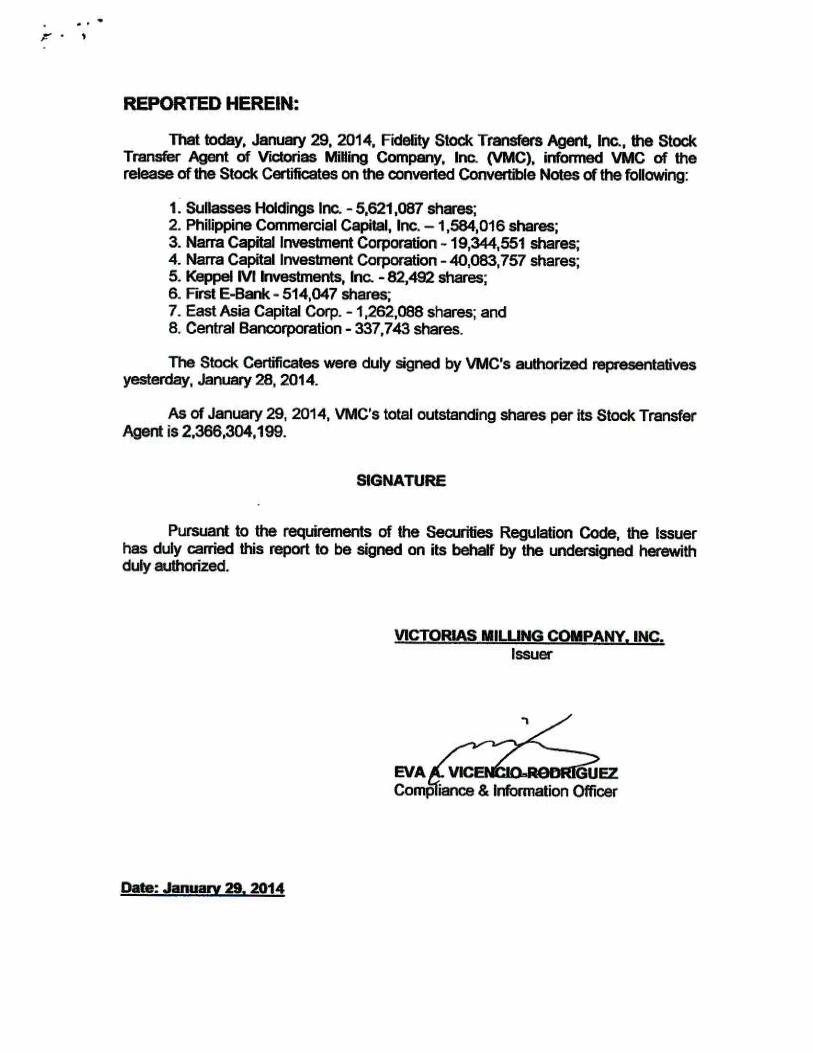

13. Reported on January 29, 2014, wherein Fidelity Stock Transfers, Inc. informed VMC of the release of the Stock Certificates on the converted Convertible Notes. Total outstanding shares per stock transfer agent is 2,366,304,199.

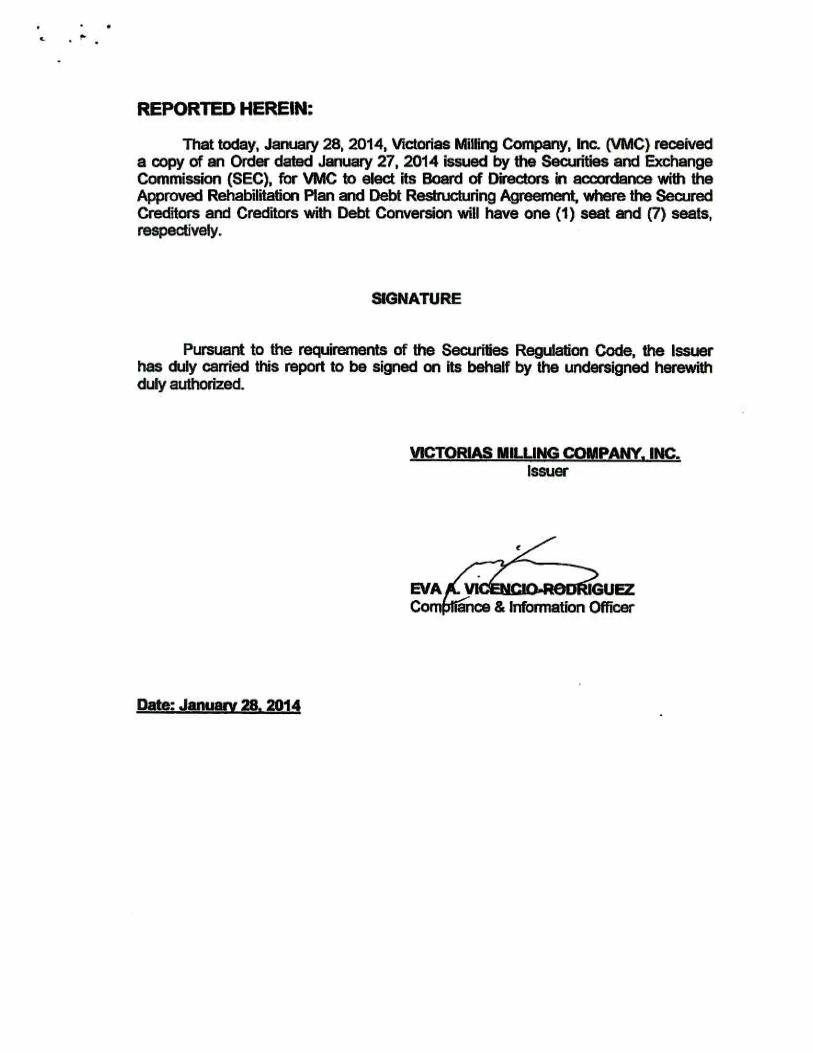

14. Reported on January 28, 2014, pursuant to an Order issued by the Securities and Exchange Commission of January 27, 2014 to elect its Board of Directors in accordance with the Approved Rehabilitation Plan and Debt Restructuring Agreement, where the Secured Creditors and Creditors with Debt Conversion will have one (1) seat and seven (7) seats respectively.

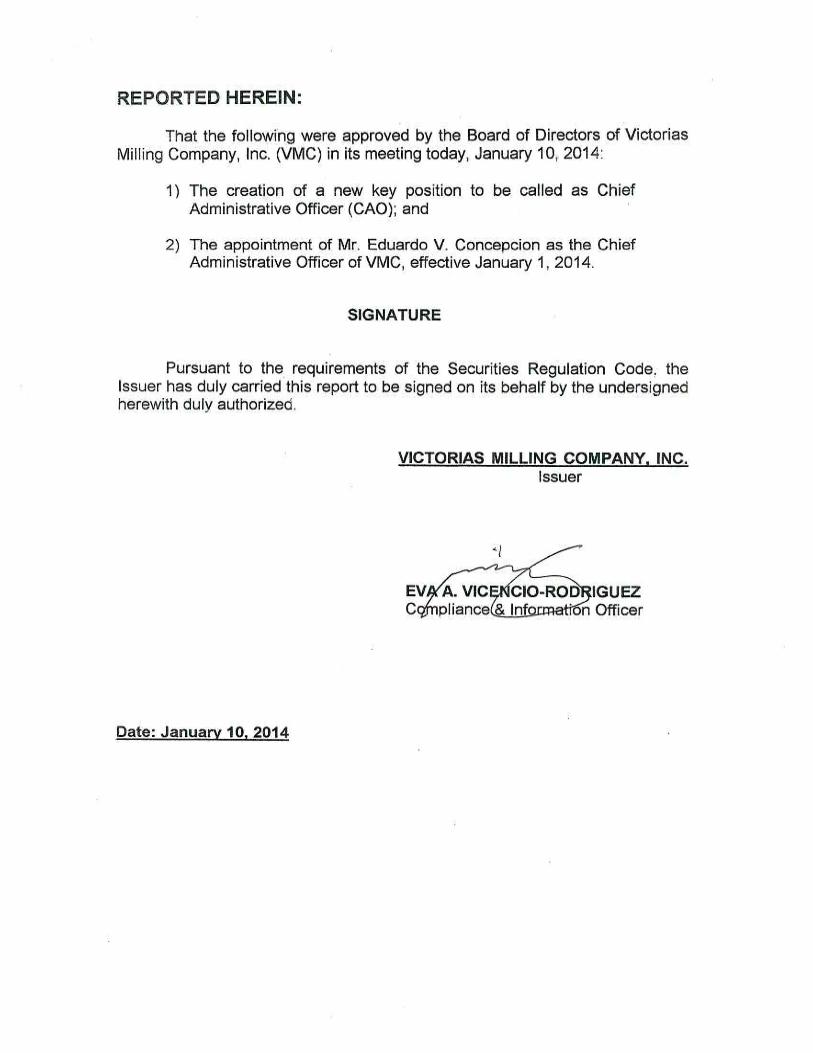

15. Reported on January 10, 2014, the creation of a new key position called Chief Administrative Officer, and the appointment of Mr. Eduardo V. Concepcion as the Chief Administrative Officer.

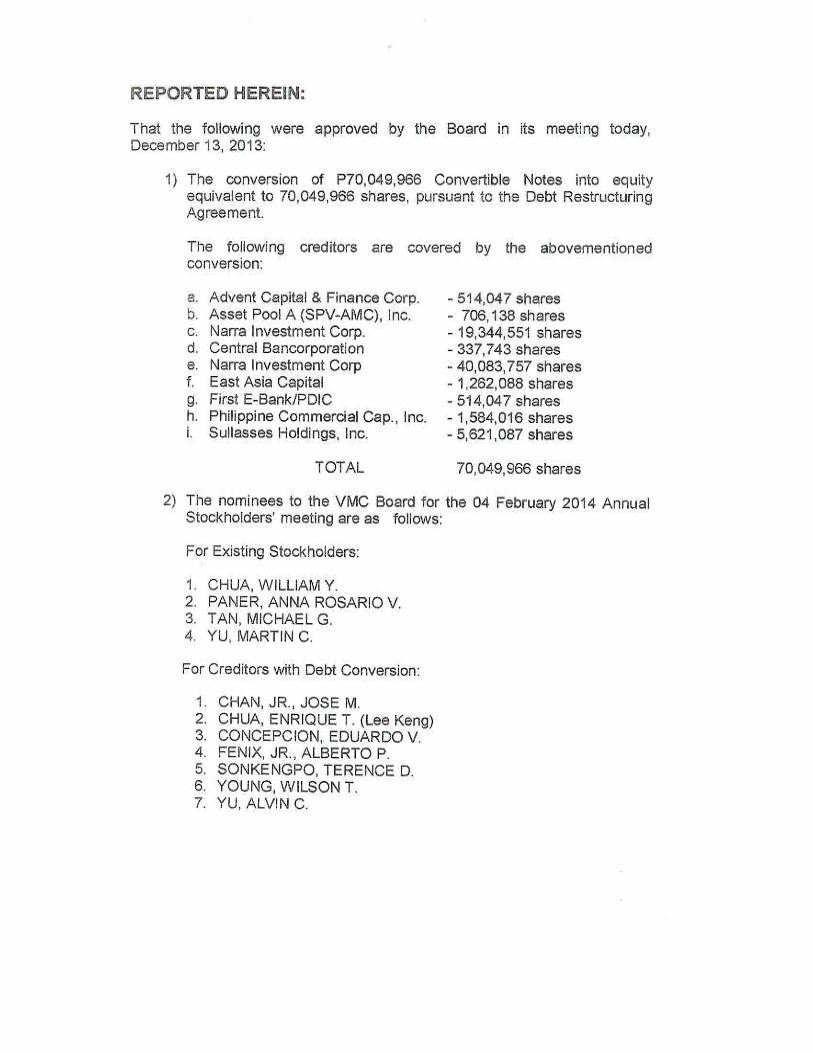

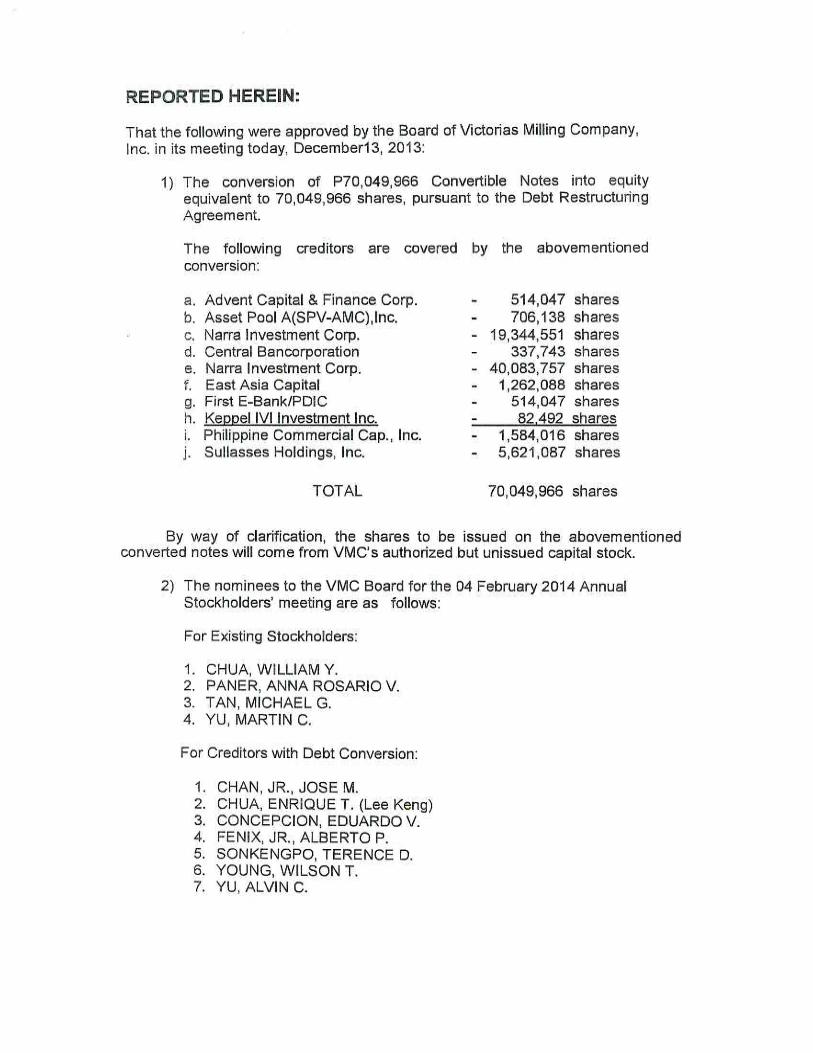

16. Reported on December 13, 2013, the conversion of P70, 049,966 Convertible Notes into equity equivalent to 70,049,966 shares, pursuant to the Debt Restructuring Agreement and the nominees to the VMC Board for the February 04, 2014 Annual Stockholders’ Meeting.

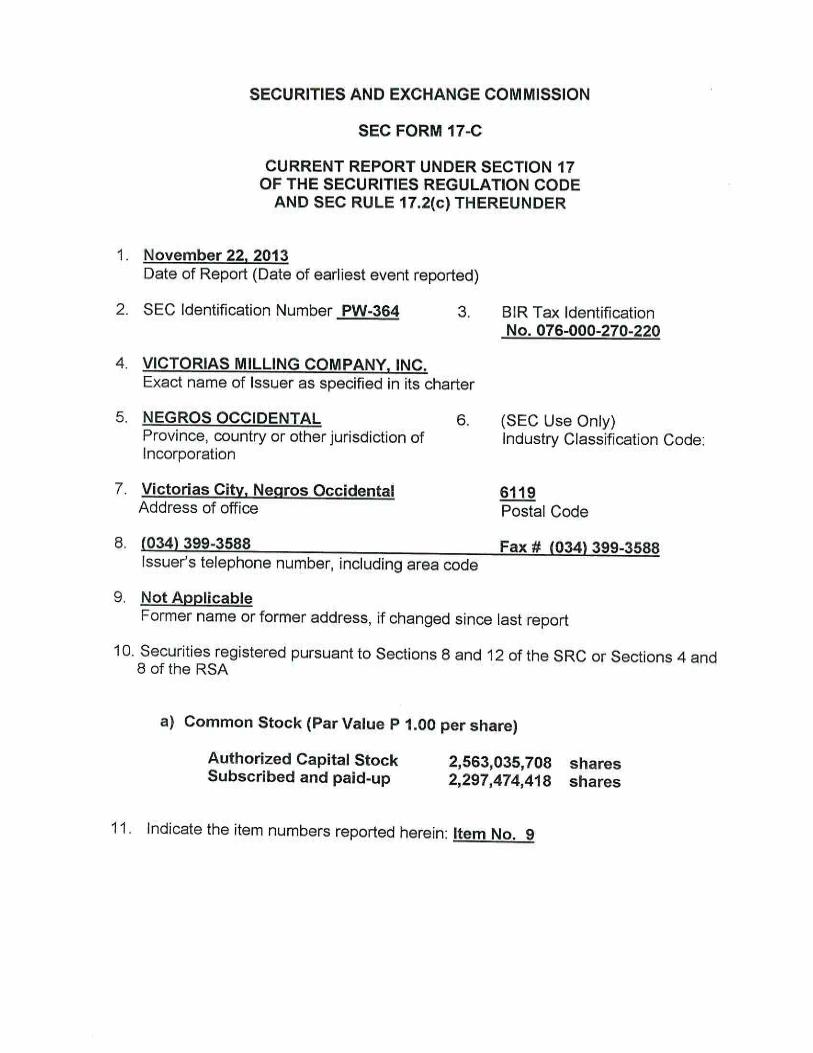

17. Reported on November 22, 2013, Board Actions as to the convening of the Annual Stockholders’ Meeting on February 4, 2014; Stockholders of record at the close of business on December 31, 2014, will be entitled to notice and to attend the meeting; Board seats for consideration at the Annual Stockholder’s Meeting shall be allocated as follows: four (4) for the Existing Stockholders and seven (7) for Creditors with Debt Conversion.

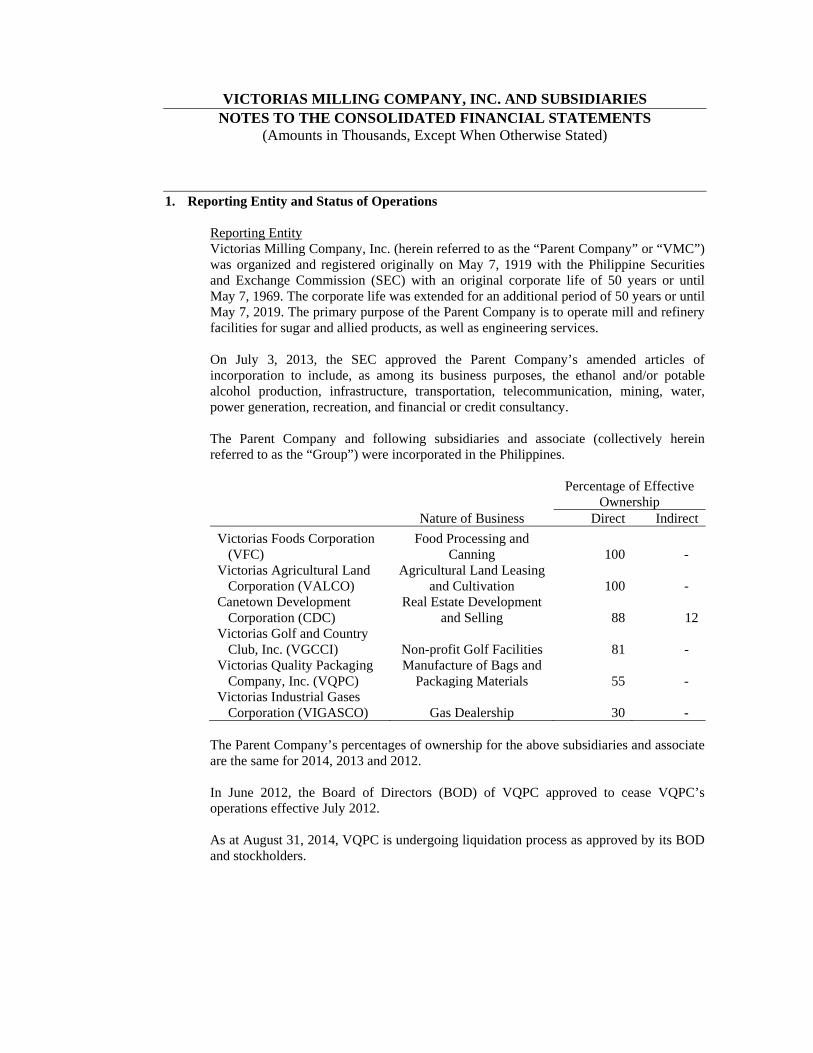

VICTORIAS MILLING COMPANY, INC. AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

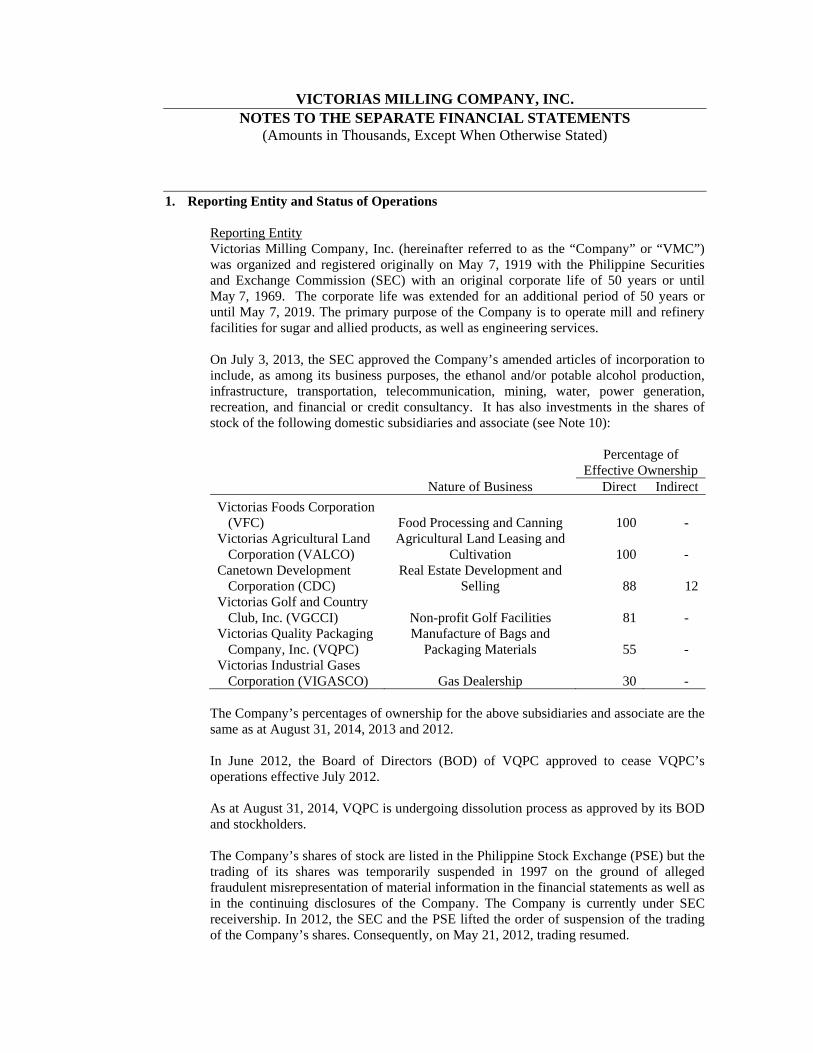

(Amounts in Thousands, Except When Otherwise Stated) 1. Reporting Entity and Status of Operations

Reporting Entity Victorias Milling Company, Inc. (herein referred to as the “Parent Company” or “VMC”) was organized and registered originally on May 7, 1919 with the Philippine Securities and Exchange Commission (SEC) with an original corporate life of 50 years or until May 7, 1969. The corporate life was extended for an additional period of 50 years or until May 7, 2019. The primary purpose of the Parent Company is to operate mill and refinery facilities for sugar and allied products, as well as engineering services. On July 3, 2013, the SEC approved the Parent Company’s amended articles of incorporation to include, as among its business purposes, the ethanol and/or potable alcohol production, infrastructure, transportation, telecommunication, mining, water, power generation, recreation, and financial or credit consultancy. The Parent Company and following subsidiaries and associate (collectively herein referred to as the “Group”) were incorporated in the Philippines.

Percentage of Effective

Ownership Nature of Business Direct Indirect

Victorias Foods Corporation (VFC)

Food Processing and Canning 100 -

Victorias Agricultural Land Corporation (VALCO)

Agricultural Land Leasing and Cultivation 100 -

Canetown Development Corporation (CDC)

Real Estate Development and Selling 88 12

Victorias Golf and Country Club, Inc. (VGCCI) Non-profit Golf Facilities 81 -

Victorias Quality Packaging Company, Inc. (VQPC)

Manufacture of Bags and Packaging Materials 55 -

Victorias Industrial Gases Corporation (VIGASCO) Gas Dealership 30 -

The Parent Company’s percentages of ownership for the above subsidiaries and associate are the same for 2014, 2013 and 2012. In June 2012, the Board of Directors (BOD) of VQPC approved to cease VQPC’s operations effective July 2012. As at August 31, 2014, VQPC is undergoing liquidation process as approved by its BOD and stockholders.

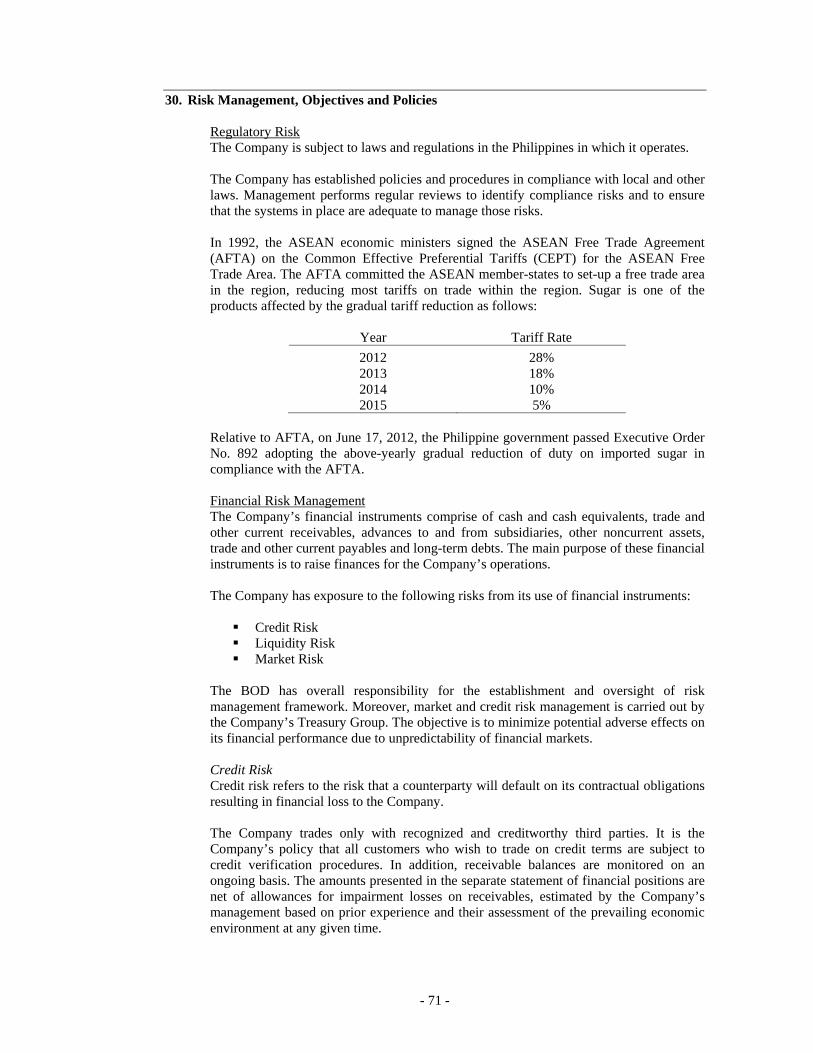

- 2 -