seducing the runaway customer - banking … · consumer readiness one can better ... cross-channel...

TRANSCRIPT

SEDUCING THE RUNAWAY CUSTOMERStrategic insights for the digital age, from our survey of 5000

EU banking customers’ behaviours & expectations

2

06

03

28

0426

Co

ntents

Appendix

Introduction:research rationale and objectives

Outlook and final words

Executive summary

The road ahead for banksA strategy to shape the industry

Strong digital foundations

Advancing at high speed

Dare to be remarkable

8

9

10

12

14The customer perspectiveTrust is back

The un-differentiatied bank

Traditional banks are losing their appeal

Disruption is in the air

Innovation is key

The data opportunity

16

18

19

20

22

24

3

Executivesummary

In the face of changing customer demands, emerging competition, and global regulations, innovation is key for today’s banks to succeed. Whether it be by entering new markets, rebuilding their brand, introducing new services or initiating transformational process changes, innovation will be at the heart of any successful bank’s strategy today.

Because the user’s perspective is crucial in any innovation project, the European survey undertaken for this whitepaper focuses on the end consumer’s perception of banking, their expectations, and their openness towards alternative banking models.

At first glance, our survey painted a positive picture of banking.Customers do trust their banks, and overall they are satisfied with the services that they offer.

However, upon deeper inspection of the customers’ mindset we discover a sobering finding: customers are open to more, even though they might not know what it could be yet. As soon as someone – whether a bank or a non-bank – gets the formula right, customers will happily switch. It is therefore time for banks to take the necessary actions to offer customers new and exciting offers that they will naturally be drawn to.

Our study reveals key insights as to how to proceed in this regard.

Today’s banking customer is playing hard to get - and hard to keep

For example, a notable finding is that customers are in fact willing to share their personal data, as long as they get a clear benefit for doing so.

This finding strongly supports the idea that the bank of the future will make money by unlocking new ways of delivering value through data. More generally, technology combined with creative thinking is the way to gain loyalty and new customers. This of course requires strong digital foundations, as well as the capability to evolve at multiple speeds.

It is well time for banks to step out of their comfort zone and undertake the bold strategic moves that will shape the future of the industry – and seize the opportunity to be a leader in that change

4

One of the consequences of the digital world is that customers have changed. New technologies have empowered them. They are social and connected. They are more informed, pro-active, and they want to be in control. At the same time, industry barriers are fading: new business models are emerging and new entrants are threatening to seize the customer relationship – and the revenues from it.

As a result, banks have significantly sped up their digital transformation and increased their customer focus. But is it enough? And is it going in the right direction?

We wanted to measure the adequacy of banks’ digital strategies by getting insights directly from customers.

5000 customers surveyed in Western Europe

research rationale and objectives

Understanding customers’ expectations can guide innovation and business strategies

1The methodology used for the survey is detailed in the appendix.

How are banks perceived in terms of services and technology? Is there an interest for alternatives to banks?

With the support of research agency TNS Sofres, we surveyed 5000 customers in six EU countries: France, UK, Germany, Spain, Belgium, and the Netherlands. The population demographics were chosen to provide a representative survey in terms of gender, age, social class and regions.1

In this paper we discuss the major findings of the survey. In particular, we present the results from the entire survey (i.e., across age and countries) unless otherwise indicated. Country and demographics specifics are examined when significant differences arise.

Overall, the results are fairly similar across countries. The most notable differences come from Spain, which showed a more defiant attitude towards banks as well as an increased need for change and innovation. Differences between age groups exist, although not to the extent one might expect (see Appendix).

In this survey, we did not try to uncover what products or innovations customers want – which is a pointless exercise most of the time anyway. As Henry Ford famously said, “If I had asked people what they wanted, they would have said faster horses.”

Instead, we tried to determine customers’ technological appetite and to capture what is their attitude and state of mind. By testing hypotheses and understanding consumer readiness one can better identify innovation opportunities and devise business strategies

Introduction

5

If I had asked people what they

wanted,they would have said faster horses.

Henry Ford

6

THEROAD AHEADFOR BANKS

7

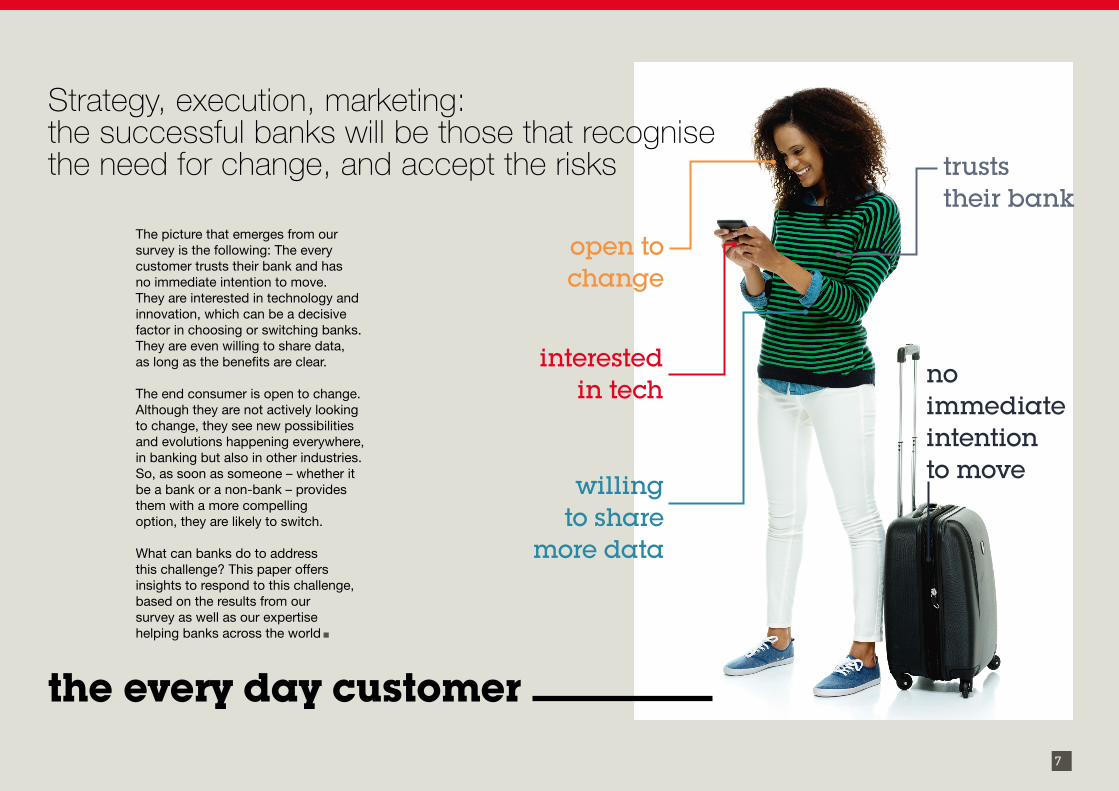

The picture that emerges from our survey is the following: The every customer trusts their bank and has no immediate intention to move. They are interested in technology and innovation, which can be a decisive factor in choosing or switching banks. They are even willing to share data, as long as the benefits are clear.

The end consumer is open to change. Although they are not actively looking to change, they see new possibilities and evolutions happening everywhere, in banking but also in other industries. So, as soon as someone – whether it be a bank or a non-bank – provides them with a more compelling option, they are likely to switch.

What can banks do to address this challenge? This paper offers insights to respond to this challenge, based on the results from our survey as well as our expertise helping banks across the world

truststheir bank

open to change

noimmediateintention to move

interestedin tech

willingto share

more data

the every day customer

Strategy, execution, marketing:the successful banks will be those that recognise the need for change, and accept the risks

8

Depending on the predictability of one’s industry and one’s power to change it, different types of strategies are to be applied.

The automotive or beverage industries, for instance, evolve in environments that are fairly predictable and are difficult for individual companies to significantly change their direction.For many years, this has also been the case for retail banking. The environment was predictable, and there weren’t many initiatives that banks could (or wanted to) launch to change things, partly because of technological limitations.

In this type of static environment, a classic strategic style has the best chances of success. A classical strategy rests upon familiar tools such as Porter’s five forces and growth-share matrix analyses. The company targets the most favourable market position by leveraging its strengths and capabilities and then tries to build and fortify that position through successive rounds of planning.

A strategy for shaping the industry

However, the digital age has significantly changed the rules of the game. Technology has increased the capacity of banks and financial services companies, traditional or not, to shape the industry.

When an industry is predictable and one indeed has the power to change it, a non-classical strategic style is in order. This situation calls for bold, visionary strategies - the kind entrepreneurs use to create entirely new markets, or corporate leaders use to revitalize a company – such as when Phillips moved into the healthcare business and became a world leader in state-of-the-art medical equipment.These are the ‘build-it-and-they-will-come’ strategies.

Interestingly the visionary style actually shares many principles with the classical approach. Because the chosen goal is clear, companies can take deliberate steps to reach their desired outcomes. In particular, it is important for players to take the time to plan thoroughly, mobilize resources, and to implement

The digital world calls for bold, visionary strategies

strategies correctly, so that the vision doesn’t fall victim to poor execution.

The winning banks will be those that launch the bold strategic moves to address the shortcomings of today’s dominant offerings. They will need the will to commit the necessary resources and the courage to follow their vision all the way. In other words, do it well or not at all

8

9

For a business transformation to be successful, it must be supported by a corresponding technology transformation. Banks need modern tools in order to implement new business models, co-operate with new players, and adapt to new customer expectations and behaviours.

A consistent, cross-channel customer experience is also a requirement for success. Similarly, a convincing marketing and CRM platform, based on advanced analytics, leveraging existing and newly available customer data for real time risk management and assessment, is a must.

Open platforms and APIs are also required to participate in an extended ecosystem, in order to deliver offerings and services beyond traditional financial products. Examples include a digital wallet management platform, in which banks can integrate services from third-parties, such as receipt management or in-store promotions

Strong digital foundationsFully leveraging digital potential requires a platform designed for the digital age

that are dynamically triggered by a consumer’s geographical position, their loyalty profile and their purchase history. These services can in turn be managed and activated by customers when and how they see fit, allowing them to use the services that best suit their needs. Through a digital wallet not only does a bank provide additional value to its customers, but they also get to keep the customer relationship and the revenues generated around it.

However, the only way to fully leverage digital potential and digital capabilities is by having everything underpinned by a platform designed for the digital age. A digital platform is designed for data distribution in a global network. Investment prioritisation should therefore be around a robust technical foundation for digitalisation, including customer communication solutions, cybersecurity, collaboration tools, storage technologies, analytics, modern core systems, and risk management

9

10

There is an increasing gap between ‘fast-moving’ banks and the slower ‘others.’ If a bank can’t muster the budgets and the will for change, it will become one of a group of “low-speed” banks — and fall behind its peers.

This need for speed results not only from enhanced competition, but also from regulatory initiatives.As an example, the upcoming Payment Service Directive 2 (PSD2) will give third-party providers access to bank accounts for payment initiations.In parallel, the Euro Retail Payments Board has mandated the payments industry to design a scheme for instant payments in euros, with the first results expected in November 2015.

Advancing at multiple speeds

In effect, instant payments and the PSD2 will jointly drive innovation in the European payment space. This is why, despite a questionable financial business case, several banks in the UK have launched the “Faster Payments” scheme, which has become the backbone for a number of innovative payment solutions, such as Pingit, Paym and Zapp. Such evolutions not only require an acceleration of business practices, but also an underlying technological modernisation.

Many businesses may find it hard to move to a digital business, especially if it means investing in areas that may initially offer lower or limited returns. This is why a differentiated, multiple-speed approach is required when transforming a business’s technological and organisational foundations.

You can’t afford to be a low-speed bank in an industry that is reinventing itself

There is an urgent need to develop new use cases and revenue streams.Not only does this demand speed, but it also requires a venture capital mindset. Venture capital firms recognise that only one out of ten companies in which they invest will actually be successful. However, the one company that is successful will more than compensate for the demise of the others.Similarly, innovation projects should be rapidly prototyped and tested in order to determine which ones are viable and to refrain from investing unnecessarily in the unsuccessful ones as soon as possible. The successful innovations can then be integrated rapidly and efficiently into the standard offering.

10

11

In conjunction, customer facing applications and services need to be constantly evolving, both in terms of design and features. Like mobile apps, updates and incremental improvements must occur at a rapid pace, say, on a weekly or even daily basis in order to keep up with consumer expectations.

In parallel, core banking and payment systems must be able to support these new developments, all whilst remaining scalable, reliable and cost-efficient. They must therefore be modernised to support the need for speed and agility of customer-facing activities.

Such modernisation is typically done at a more moderate pace, especially given the need to ensure a stable, flawless transition.Modern systems that are truly componentised provide a reliable way to effect these modernisation

efforts at a custom pace.Another option is to outsource part of the activities in a cloud environment.

In short, success depends on advancing business and innovation at a high speed, supported by a pace-layer approach for the underlying technological evolution. Banks that miss this opportunity will find it hard to win, serve, and retain customers. You simply can’t afford to be a low-speed bank in an industry that is reinventing itself to cope with the challenges of digital disruption

11

12

Our survey reveals that most customers see banking as a commodity.Yet, given the opportunities that digital is unlocking, banks could be much more than that. It is therefore imperative to make banks and banking interesting, compelling, and remarkable.

As a first step, banking products must become simpler, more modular and transparent. Such changes are imperative because today’s e-enabled customer is looking for products that they understand, that they can buy without worrying about the small print, and which they can easily change (and without penalty) as their personal situation evolves.New value-added services such as wallet solutions or peer advisory can then uplift these products, enabling strong differentiation from competitors.

Differentiation, however, is not enough – at least in the way that we approach differentiation in today’s world, i.e. as a series of reasons why someone should buy one thing over another based on proven features and benefits.

Dare to be remarkable

Indeed, customers don’t all share the same obsessed knowledge of features and benefits. Today the opportunity lies in creating something that actually interests consumers and that they want to talk about - regardless of what the competition is doing.The opportunity lies in standing out and offering solutions that are remarkable.

In the following sections of this paper examples of banks creating value for their customers with non-conventional products and initiatives, from music streaming to educational games, tailored couponing, and even

Banking is not only becoming a commodity,

it is becoming a boring commodity. Customers are ready and waiting for more

Playing it safe is the riskiest strategy of all

car buying intermediaries based on social networks shall be presented. The successes in these examples attest that, rather than such broader offerings diminishing a bank’s brand, such approaches in fact instil loyalty and recognition. These banks dare to be different and bring new values, and customers respond positively to that.

Playing it safe is the riskiest strategy of all. As marketer Seth Godin aptly put it: “In a crowded marketplace, fitting in is a failure. In a busy marketplace, not standing out is the same as being invisible.”

12

1313

14

THECUSTOMERPERSPECTIVE

1515

16

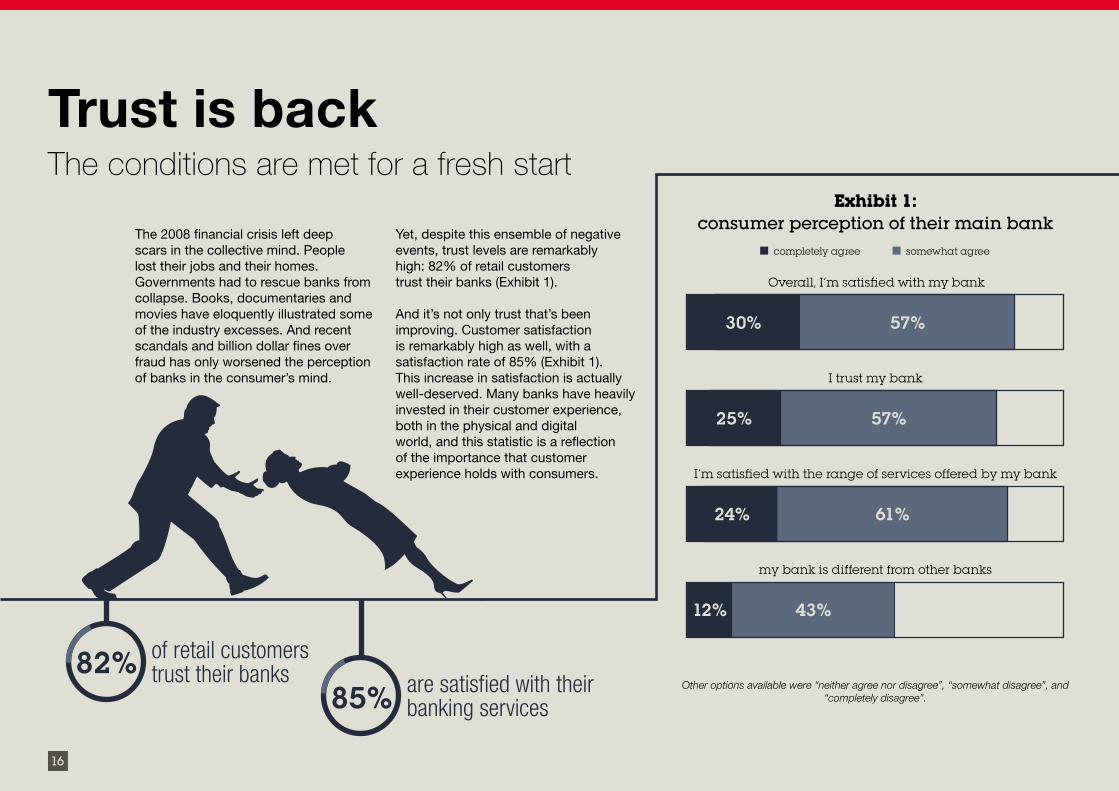

Trust is back

The 2008 financial crisis left deep scars in the collective mind. People lost their jobs and their homes.Governments had to rescue banks from collapse. Books, documentaries and movies have eloquently illustrated some of the industry excesses. And recent scandals and billion dollar fines over fraud has only worsened the perception of banks in the consumer’s mind.

.82%

Yet, despite this ensemble of negative events, trust levels are remarkably high: 82% of retail customers trust their banks (Exhibit 1).

And it’s not only trust that’s been improving. Customer satisfaction is remarkably high as well, with a satisfaction rate of 85% (Exhibit 1). This increase in satisfaction is actually well-deserved. Many banks have heavily invested in their customer experience, both in the physical and digital world, and this statistic is a reflection of the importance that customer experience holds with consumers.

85%

of retail customerstrust their banks are satisfied with their

banking services

The conditions are met for a fresh start

Overall, I’m satisfied with my bank

completely agree somewhat agree

I trust my bank

I’m satisfied with the range of services offered by my bank

my bank is different from other banks

30%

25%

24%

12%

57%

57%

61%

43%

Other options available were “neither agree nor disagree”, “somewhat disagree”, and “completely disagree”.

Exhibit 1:consumer perception of their main bank

17

none of the above

I will switch to a different bank

I will get some information about other

banks, but want to stay with the same bank

I will stay with the same bank without

seeking any information about other banks

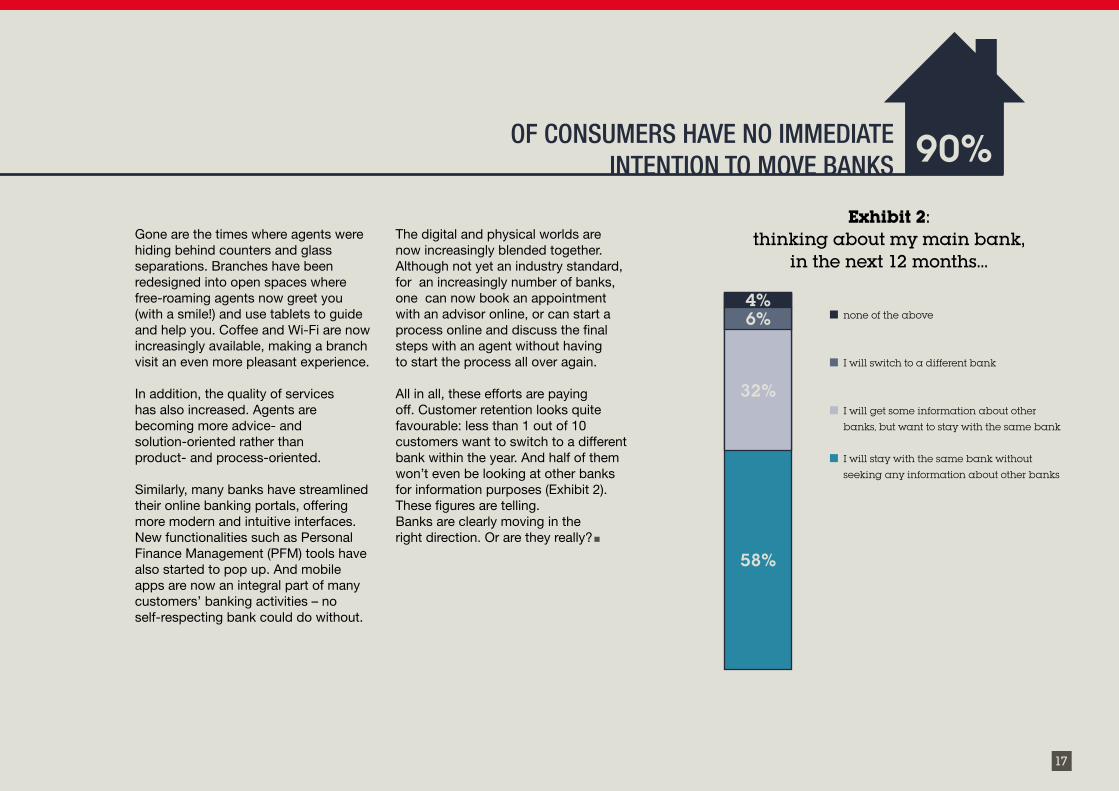

90%OF CONSUMERS HAVE NO IMMEDIATEINTENTION TO MOVE BANKS

Gone are the times where agents were hiding behind counters and glass separations. Branches have been redesigned into open spaces where free-roaming agents now greet you (with a smile!) and use tablets to guide and help you. Coffee and Wi-Fi are now increasingly available, making a branch visit an even more pleasant experience.

In addition, the quality of services has also increased. Agents are becoming more advice- and solution-oriented rather than product- and process-oriented.

Similarly, many banks have streamlined their online banking portals, offering more modern and intuitive interfaces. New functionalities such as Personal Finance Management (PFM) tools have also started to pop up. And mobile apps are now an integral part of many customers’ banking activities – no self-respecting bank could do without.

The digital and physical worlds are now increasingly blended together. Although not yet an industry standard, for an increasingly number of banks, one can now book an appointment with an advisor online, or can start a process online and discuss the final steps with an agent without having to start the process all over again.

All in all, these efforts are paying off. Customer retention looks quite favourable: less than 1 out of 10 customers want to switch to a different bank within the year. And half of them won’t even be looking at other banks for information purposes (Exhibit 2).These figures are telling.Banks are clearly moving in the right direction. Or are they really?

Exhibit 2: thinking about my main bank,

in the next 12 months…

4%6%

32%

58%

18

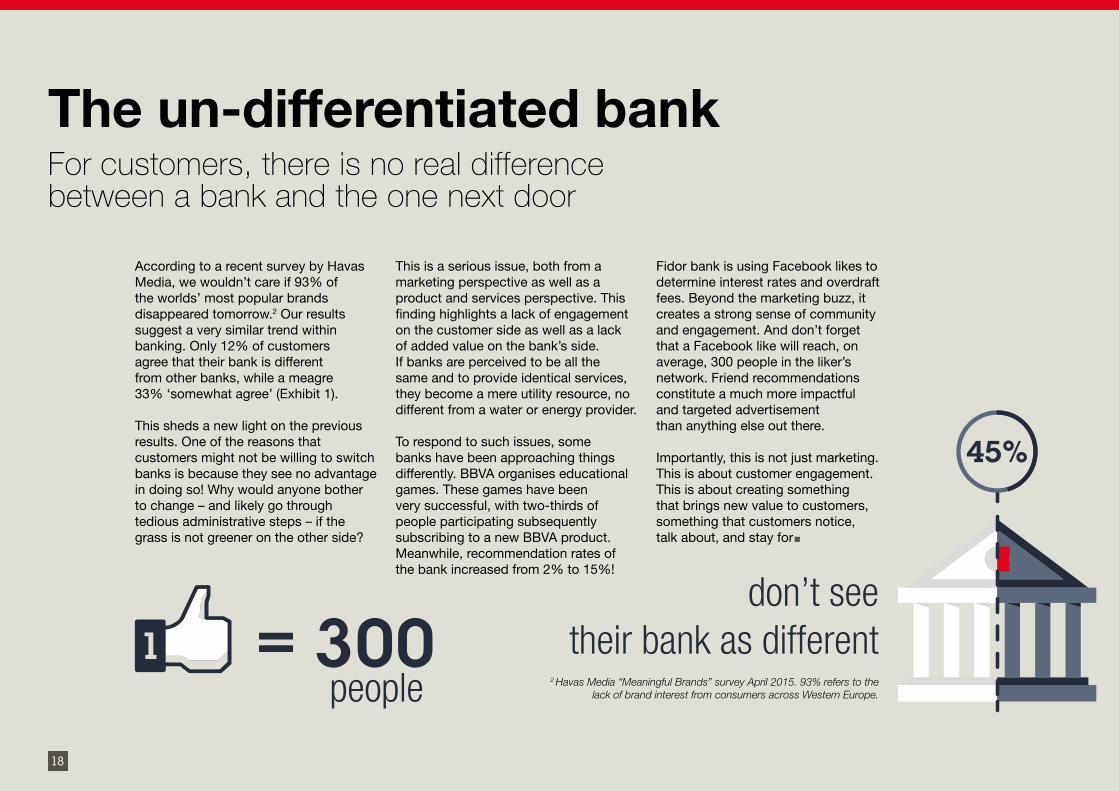

The un-differentiated bank

According to a recent survey by Havas Media, we wouldn’t care if 93% of the worlds’ most popular brands disappeared tomorrow.2 Our results suggest a very similar trend within banking. Only 12% of customers agree that their bank is different from other banks, while a meagre 33% ‘somewhat agree’ (Exhibit 1).

This sheds a new light on the previous results. One of the reasons that customers might not be willing to switch banks is because they see no advantage in doing so! Why would anyone bother to change – and likely go through tedious administrative steps – if the grass is not greener on the other side?

This is a serious issue, both from a marketing perspective as well as a product and services perspective. This finding highlights a lack of engagement on the customer side as well as a lack of added value on the bank’s side.If banks are perceived to be all the same and to provide identical services, they become a mere utility resource, no different from a water or energy provider.

To respond to such issues, some banks have been approaching things differently. BBVA organises educational games. These games have been very successful, with two-thirds of people participating subsequently subscribing to a new BBVA product. Meanwhile, recommendation rates of the bank increased from 2% to 15%!

2 Havas Media “Meaningful Brands” survey April 2015. 93% refers to the lack of brand interest from consumers across Western Europe.

don’t see their bank as different

For customers, there is no real difference between a bank and the one next door

Fidor bank is using Facebook likes to determine interest rates and overdraft fees. Beyond the marketing buzz, it creates a strong sense of community and engagement. And don’t forget that a Facebook like will reach, on average, 300 people in the liker’s network. Friend recommendations constitute a much more impactful and targeted advertisement than anything else out there.

Importantly, this is not just marketing. This is about customer engagement. This is about creating something that brings new value to customers, something that customers notice, talk about, and stay for

45%

= 3001people

19

would choose anon-traditional bank

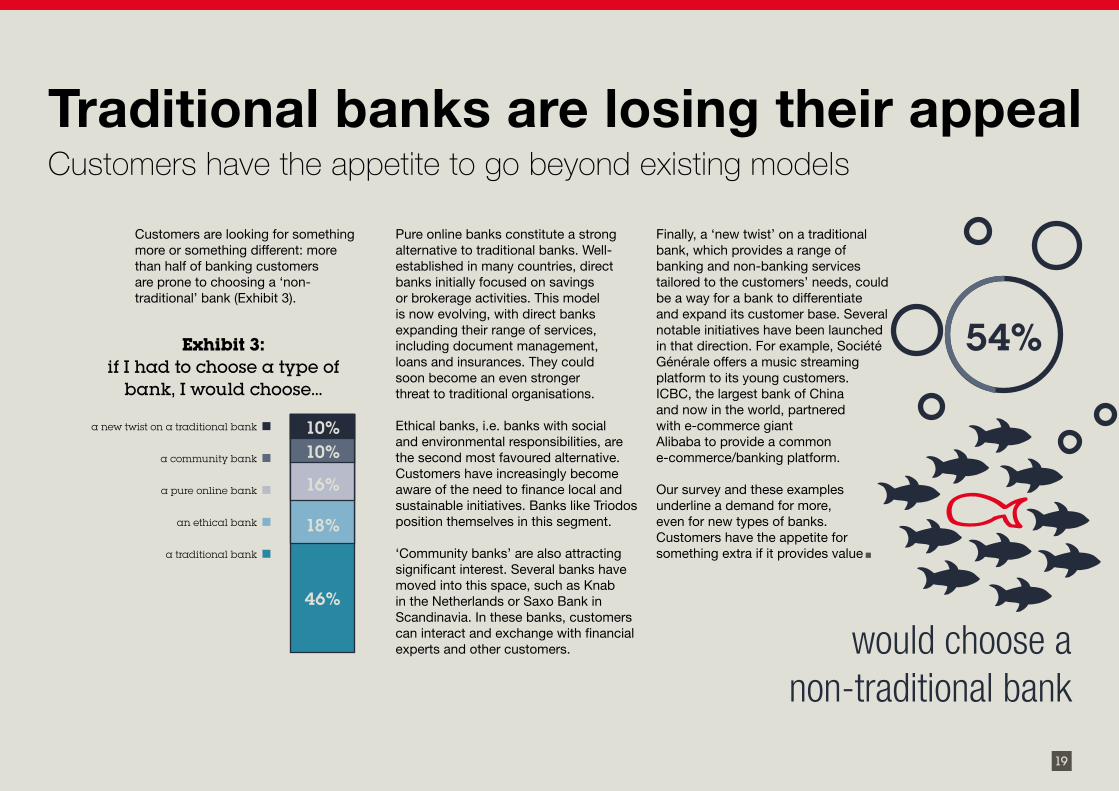

Traditional banks are losing their appeal

Customers are looking for something more or something different: more than half of banking customers are prone to choosing a ‘non-traditional’ bank (Exhibit 3).

Pure online banks constitute a strong alternative to traditional banks. Well-established in many countries, direct banks initially focused on savings or brokerage activities. This model is now evolving, with direct banks expanding their range of services, including document management, loans and insurances. They could soon become an even stronger threat to traditional organisations.

Ethical banks, i.e. banks with social and environmental responsibilities, are the second most favoured alternative. Customers have increasingly become aware of the need to finance local and sustainable initiatives. Banks like Triodos position themselves in this segment.

‘Community banks’ are also attracting significant interest. Several banks have moved into this space, such as Knab in the Netherlands or Saxo Bank in Scandinavia. In these banks, customers can interact and exchange with financial experts and other customers.

Customers have the appetite to go beyond existing models

54%

Finally, a ‘new twist’ on a traditional bank, which provides a range of banking and non-banking services tailored to the customers’ needs, could be a way for a bank to differentiate and expand its customer base. Several notable initiatives have been launched in that direction. For example, Société Générale offers a music streaming platform to its young customers.ICBC, the largest bank of China and now in the world, partnered with e-commerce giant Alibaba to provide a common e-commerce/banking platform.

Our survey and these examples underline a demand for more, even for new types of banks. Customers have the appetite for something extra if it provides value

a new twist on a traditional bank

a community bank

a pure online bank

an ethical bank

a traditional bank

10%10%

16%

18%

46%

Exhibit 3:if I had to choose a type of

bank, I would choose…

20

Disruption is in the air

Putting a twist on banking might, however, not be enough. The tech giants as well as e-commerce, social networks, retailers and telco companies now all constitute a credible alternative: 57% of customers would be ready to bank with at least one of the companies presented in the panel (Exhibit 4).

As a result, non-banks are increasingly trying to capture their fair share of the financial industry. This is especially visible in the world of payments,

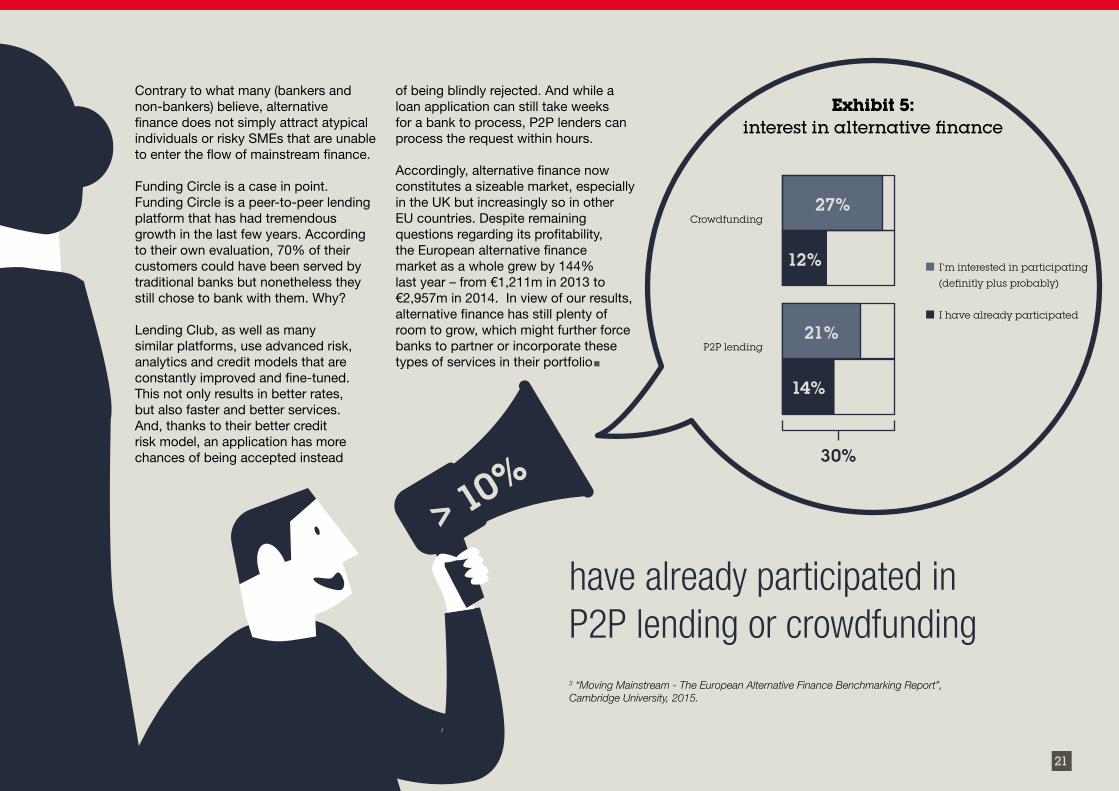

The rise of alternative finance is another sign that customers are looking for more. Alternative finance, which comprises activities such as donation-, reward- and equity-based crowdfunding, peer-to-peer consumer and business lending, invoice trading and debt-based securities, is burgeoning in Europe.

The interest of customers in peer-to-peer (P2P) lending and crowdfunding is significant, with 21% and 27%, respectively stating their interest (Exhibit 5). What’s more, over 10% of customers have already participated in either one of these activities.

ready to bankwith a non-bank

Non-banks are now seen ascredible banking services providers

57%where the battle for the customer context and relationships are the real prizes. It is no coincidence that all major tech companies – such as Apple, Samsung or Microsoft - have all launched their wallet solutions.

But this goes beyond payments. Amazon and Paypal, for instance, now offer lending to SMEs.Every banking activity, from remittance to lending and foreign exchange, is now challenged by new entrants.

Exhibit 4: I would be interested if the following companies offered banking services:Other options available were “probably not” and “definitely not”. Multiple responses accepted. 57% of respondents selected at least one option where they were willing to bank with a non-bankFacebook Apple Mobile network

provider

Amazon Google Major

supermarket

Paypal

4% 4%5% 5% 5%13%

6%11%

15% 16% 19% 19% 23%

33%50%

definitely

probably

21

have already participated in P2P lending or crowdfunding3 “Moving Mainstream - The European Alternative Finance Benchmarking Report”,Cambridge University, 2015.

Contrary to what many (bankers and non-bankers) believe, alternative finance does not simply attract atypical individuals or risky SMEs that are unable to enter the flow of mainstream finance.

Funding Circle is a case in point. Funding Circle is a peer-to-peer lending platform that has had tremendous growth in the last few years. According to their own evaluation, 70% of their customers could have been served by traditional banks but nonetheless they still chose to bank with them. Why?

Lending Club, as well as many similar platforms, use advanced risk, analytics and credit models that are constantly improved and fine-tuned. This not only results in better rates, but also faster and better services. And, thanks to their better credit risk model, an application has more chances of being accepted instead

of being blindly rejected. And while a loan application can still take weeks for a bank to process, P2P lenders can process the request within hours.

Accordingly, alternative finance now constitutes a sizeable market, especially in the UK but increasingly so in other EU countries. Despite remaining questions regarding its profitability, the European alternative finance market as a whole grew by 144% last year – from €1,211m in 2013 to €2,957m in 2014. In view of our results, alternative finance has still plenty of room to grow, which might further force banks to partner or incorporate these types of services in their portfolio

Crowdfunding

P2P lending

I’m interested in participating

(definitly plus probably)

I have already participated

Exhibit 5: interest in alternative finance

27%

12%

21%

14%

30%

> 10%

22

Innovation is key

Entrants from other industries bring new practices and different ways of thinking. Have banks been able to keep up? Although 62% of consumers surveyed find that their bank is ‘somewhat innovative’, only 12% fully agree that their bank is innovative.

Not surprisingly, 69% of customers say it is important to have an innovative bank. In addition, technology can be a driver for a customer to change banks: 33% are ready to switch banks for the latest technologies.

ready to switch banks in exchange for33%

This figure varies somewhat by country (see Appendix). In particular, Spanish customers are more demanding: 78% consider it to be important to have an innovative bank and 58% are ready to switch to a bank providing the latest technologies! These figures are all the most surprising as Spanish banks are amongst the most advanced banks in terms of digitalisation and innovation. Perhaps, once you open Pandora’s box of innovation you cannot close it.

Customers see the world evolving rapidly around them – and they expect the same to happen in banking

23

In any case, innovation and technology play an important role in customer acquisition and retention.Innovation, however, requires new competencies as well as a change of culture and mindset. It can also be hindered by technological legacy. There are ways to circumvent these difficulties and to kickstart an innovation program, using existing tool boxes or ‘internal start-ups’, but even these are not without pitfalls.

However, innovation doesn’t have to be a big exercise for a bank, or rely on new flashy technologies.Innovation can be small, yet meaningful. Inventor Edwin Land once remarked that “people who seem to have had a new idea have often simply stopped having an old idea.” A simple example is interest rates on savings accounts. Instead of giving them once a year, why not offer them to your customers every month? Or even every day?There are countless other ideas that can be implemented easily and that, when combined with each other, result in a

fully agree that their bank is innovative

truly enhanced customer experience.Combining fresh ideas with digital technology creates a perfect mix for the customer. However, regulations often serve as an excuse not to innovate. When in doubt, one can talk to regulators and convince them that one’s innovation plan is sound.

This is what Michael Harte, when at Commonwealth Bank of Australia, did. He went to convince his Executive Team to put their entire infrastructure into the Cloud. The Executive Team refused, arguing that the regulator would not allow it. So Michael went to the regulator and explained how cloud would work for the bank, the cost savings it would achieve and the flexibility it would bring to respond to customer needs for real-time mobile. After several exchanges, the regulator realised that the proposal was robust and would work.

12%

It therefore signed off on the project. So by talking things through with the regulator, rather than automatically assuming that they will shoot new ideas down, meaningful innovation can be put in place. More generally speaking, the world is changing, and banks need to play an active part in changing it too - even if it might mean disrupting themselves.Case in point, why weren’t Paypal – or Bitcoin – invented by banks?

24

The data opportunity

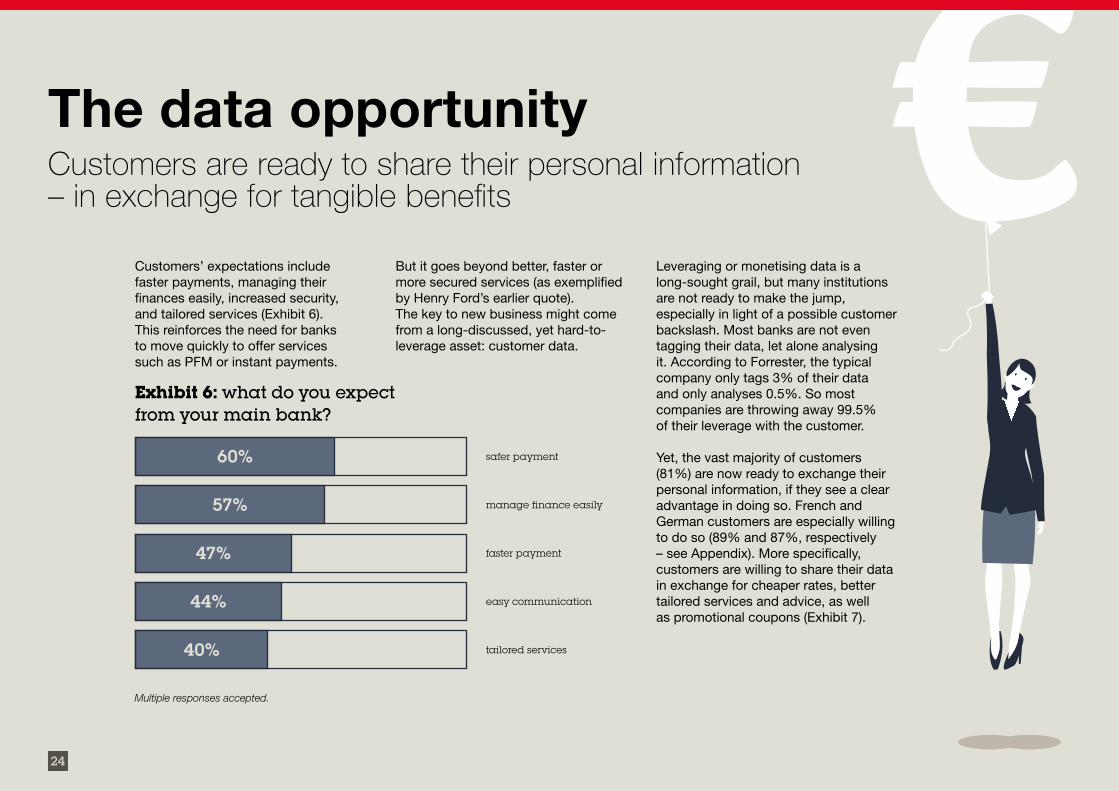

Customers’ expectations include faster payments, managing their finances easily, increased security, and tailored services (Exhibit 6). This reinforces the need for banks to move quickly to offer services such as PFM or instant payments.

Customers are ready to share their personal information – in exchange for tangible benefits

But it goes beyond better, faster or more secured services (as exemplified by Henry Ford’s earlier quote).The key to new business might come from a long-discussed, yet hard-to-leverage asset: customer data.

Leveraging or monetising data is a long-sought grail, but many institutions are not ready to make the jump, especially in light of a possible customer backslash. Most banks are not even tagging their data, let alone analysing it. According to Forrester, the typical company only tags 3% of their data and only analyses 0.5%. So most companies are throwing away 99.5% of their leverage with the customer.

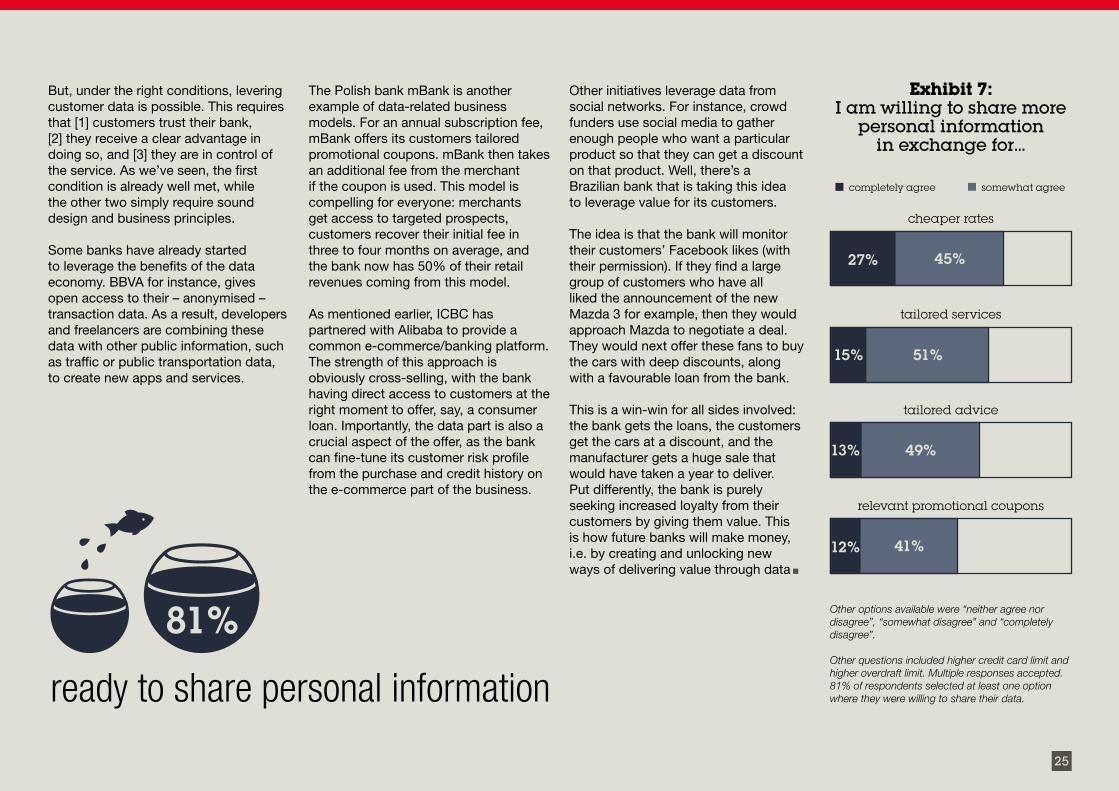

Yet, the vast majority of customers (81%) are now ready to exchange their personal information, if they see a clear advantage in doing so. French and German customers are especially willing to do so (89% and 87%, respectively – see Appendix). More specifically, customers are willing to share their data in exchange for cheaper rates, better tailored services and advice, as well as promotional coupons (Exhibit 7).

60%

57%

47%

44%

40%

safer payment

manage finance easily

faster payment

easy communication

tailored services

Exhibit 6: what do you expect from your main bank?

Multiple responses accepted.

25

ready to share personal information

But, under the right conditions, levering customer data is possible. This requires that [1] customers trust their bank, [2] they receive a clear advantage in doing so, and [3] they are in control of the service. As we’ve seen, the first condition is already well met, while the other two simply require sound design and business principles.

Some banks have already started to leverage the benefits of the data economy. BBVA for instance, gives open access to their – anonymised – transaction data. As a result, developers and freelancers are combining these data with other public information, such as traffic or public transportation data, to create new apps and services.

The Polish bank mBank is another example of data-related business models. For an annual subscription fee, mBank offers its customers tailored promotional coupons. mBank then takes an additional fee from the merchant if the coupon is used. This model is compelling for everyone: merchants get access to targeted prospects, customers recover their initial fee in three to four months on average, and the bank now has 50% of their retail revenues coming from this model.

As mentioned earlier, ICBC has partnered with Alibaba to provide a common e-commerce/banking platform. The strength of this approach is obviously cross-selling, with the bank having direct access to customers at the right moment to offer, say, a consumer loan. Importantly, the data part is also a crucial aspect of the offer, as the bank can fine-tune its customer risk profile from the purchase and credit history on the e-commerce part of the business.

Other initiatives leverage data from social networks. For instance, crowd funders use social media to gather enough people who want a particular product so that they can get a discount on that product. Well, there’s a Brazilian bank that is taking this idea to leverage value for its customers.

The idea is that the bank will monitor their customers’ Facebook likes (with their permission). If they find a large group of customers who have all liked the announcement of the new Mazda 3 for example, then they would approach Mazda to negotiate a deal. They would next offer these fans to buy the cars with deep discounts, along with a favourable loan from the bank.

This is a win-win for all sides involved: the bank gets the loans, the customers get the cars at a discount, and the manufacturer gets a huge sale that would have taken a year to deliver.Put differently, the bank is purely seeking increased loyalty from their customers by giving them value. This is how future banks will make money, i.e. by creating and unlocking new ways of delivering value through data

81%

completely agree somewhat agree

Exhibit 7:I am willing to share more

personal information in exchange for…

cheaper rates

tailored services

tailored advice

relevant promotional coupons

27%

15% 51%

49%

41%

13%

12%

45%

Other options available were “neither agree nor disagree”, “somewhat disagree” and “completely disagree”.

Other questions included higher credit card limit and higher overdraft limit. Multiple responses accepted. 81% of respondents selected at least one option where they were willing to share their data.

26

Outlook and final words

Customers are ready for more. Their awareness of the current banking shortcomings is creating the possibility of new markets.

These new markets will likely emerge from the same technological advances that are challenging the status-quo. We can already imagine multiple scenarios that could deeply affect the way banking is conducted.

For example, blockchain technologies like Bitcoin or Ripple provide the foundations for a network where value can be exchanged without the need for trusted intermediaries.This is possible thanks to a distributed ledger combined with game theory and cryptographic techniques. The first applications are of course transactional – including remittances, securities issuance and servicing etc. Activities such as trade finance or syndicated lending and collateral management can also benefit from the technology.

Other applications are being envisioned as well. Smart contracts are programmes that can automatically execute the terms of a contract.With smart contracts, one can cut the mortgage rate, update a will more easily, or ensure that a friend would never be able to back down from paying up on a bet. Smart contracts therefore hold the potential to build more affordable and more efficient legal and financial systems.Conceivably, they could even replace notaries, lawyers and banks in the handling of certain common financial transactions.

In reality, smart contracts are but just another, albeit vital, element of a larger, emerging ‘programmable economy’, where value is exchanged without central authority and where markets can be created on demand, including markets in resources that are not directly monetary.Blockchain technologies for example have the potential to revolutionise banking practices over the next decade.

In the future, competition could take on a very different form than it is today

27

Another industry defining event could be the development and adoption of cognitive technologies. Apple’s Siri, Microsoft’s Cortana and now Facebook’s M - these personal assistants are just the first manifestations of their newfound capabilities. Other notable initiatives include IBM Watson, which provides insights into activities as diverse as cooking, trading, or cancer research, or Amelia from IP Soft, a cognitive agent that interacts with and learns from humans.

These developments have now reached the point where they can be deployed in real business environments. In fact, solutions such as Watson and Amelia are already used by top financial institutions. For instance, DBS Bank uses Watson to identify the needs of wealth management customers, offer better advice and determine customers’ best financial options. Also, one of the biggest US banks uses Amelia to manage trading platforms and call centres.

As the technology matures and gains further adoption, it is conceivable that customers delegate their personal finance management to cognitive agents. Banks will need to start designing their offerings for these smart advisors instead of the customers themselves. Or the banks will have to provide these agents to their customers, in which case the winning banks will be those with the best models and machine training capabilities.

Yet another market development is the rise of banking marketplaces.In a marketplace, instead of having the customer visiting multiple providers, the providers themselves come to the customers with their offers.

If you are a visitor to such a marketplace, instead of visiting multiple banks, you simply provide your needs and profile before receiving offers from all the banks interested in your business. You then pick the offer that best suits you. Easy, fast, and efficient.

In practice, we can imagine a process in which the conditions offered are non-negotiable, but we can also imagine a competitive bidding process to get the best offer for each client at any point in time. In a fully networked, marketplace world, it is the brands that can instantly match fickle customer demand that will be the last ones standing.

Combining these different trends and advances, we can now envision a very different financial world, one where customers sell their data, banks bid in real-time for their business, with all decisions augmented by cognitive agents, and where many banking activities or even markets are set up by the customers themselves (or their smart agents) and enforced and executed by smart contracts. In such a world, competition will take on a very different form than what we currently see today.

These scenarios – and others – are still potential futures at this stage, although a transition point might be closer than one might expect. We will report on these fascinating and defining issues in forthcoming publications.

In any case, the biggest risk is not to act at all. As for much digital evolution these days, banks need to start addressing these developments as a matter of urgency, because an evolution like this requires acquiring and mastering new tools, skills and competencies, developing robust technical foundations, and devising new, bold strategies for business growth. Banks must proactively invent the future of banking – before others step in to make that decision for them

David Andrieux, PhD

28

APPENDIX

29

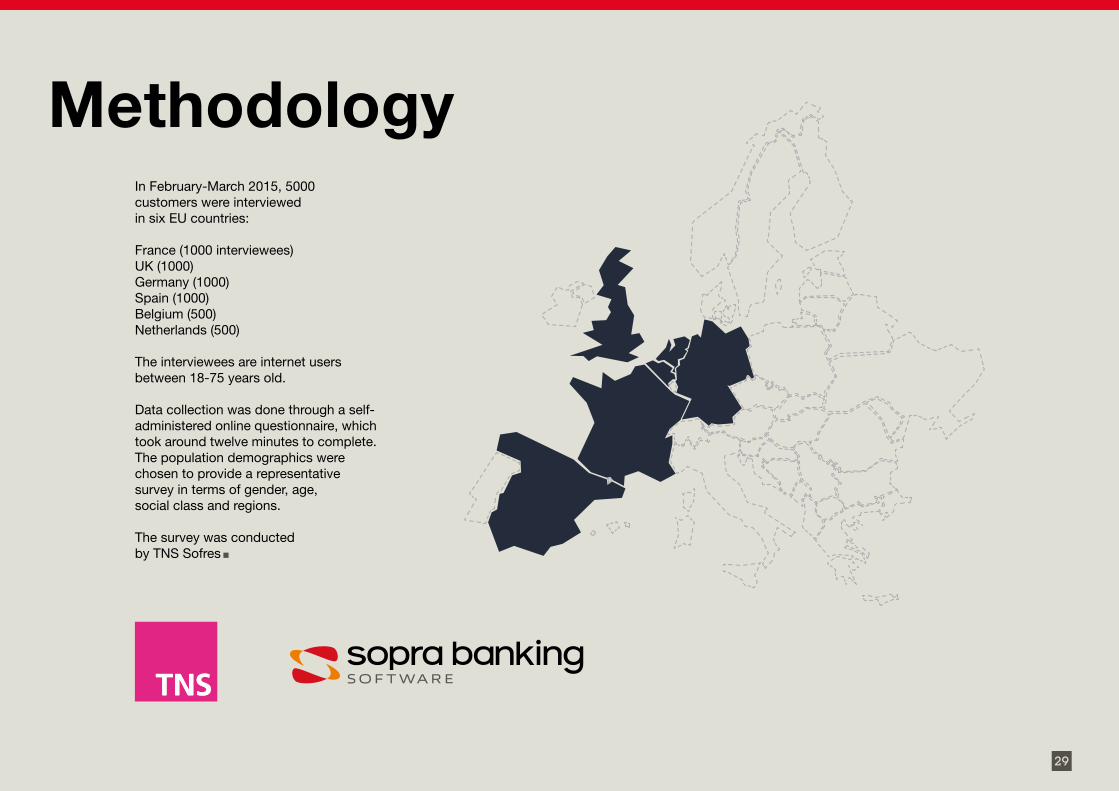

MethodologyIn February-March 2015, 5000 customers were interviewed in six EU countries:

France (1000 interviewees)UK (1000)Germany (1000)Spain (1000) Belgium (500) Netherlands (500)

The interviewees are internet users between 18-75 years old.

Data collection was done through a self-administered online questionnaire, which took around twelve minutes to complete.The population demographics were chosen to provide a representative survey in terms of gender, age, social class and regions.

The survey was conducted by TNS Sofres

30

Four generations under one bank

The Spanish attitude

While results of the survey were fairly similar between the different countries surveyed, Spain showed significant differences(see Appendix for more details).

Possibly because of the aftermath of the 2008 financial crisis, Spanish customers have a lower opinion of their banks. They are also less satisfied with their banks and the services they provide.

Different generations live differently and have different expectations. That said, our results show the generation gap might not be so large after all.Or at least not the one you’d expect.

People across generations tend to have a similarly good opinion of their bank. Not surprisingly, the older generations tend to favour more traditional banking institutions over alternatives.They are also less sensitive to innovation and technological advances in banking.

Technology and innovation is important not just for the youngest generation (18-24), but also for the whole 18-44 age range. Similarly, interest for banking with non-banks is more pronounced in the 18-44 age range, with a marked interest for alternative finance such as crowdfunding and P2P lending.

Consumers are open to share their personal information in exchange for clearly identified benefits.Remarkably, this finding holds across generations, i.e. in the whole 18-75 age range.

They are particularly interested in innovative services and new ways to communicate, even more so than other countries.Consumers are also more open to new entrants and to alternative finance such as crowdfunding and peer-to-peer lending.

These findings are somewhat unexpected as Spanish banks are amongst the most innovative banks in Europe. Perhaps, once people get a taste of the possibilities enabled by modern thinking and technologies, they can’t get enough?

31

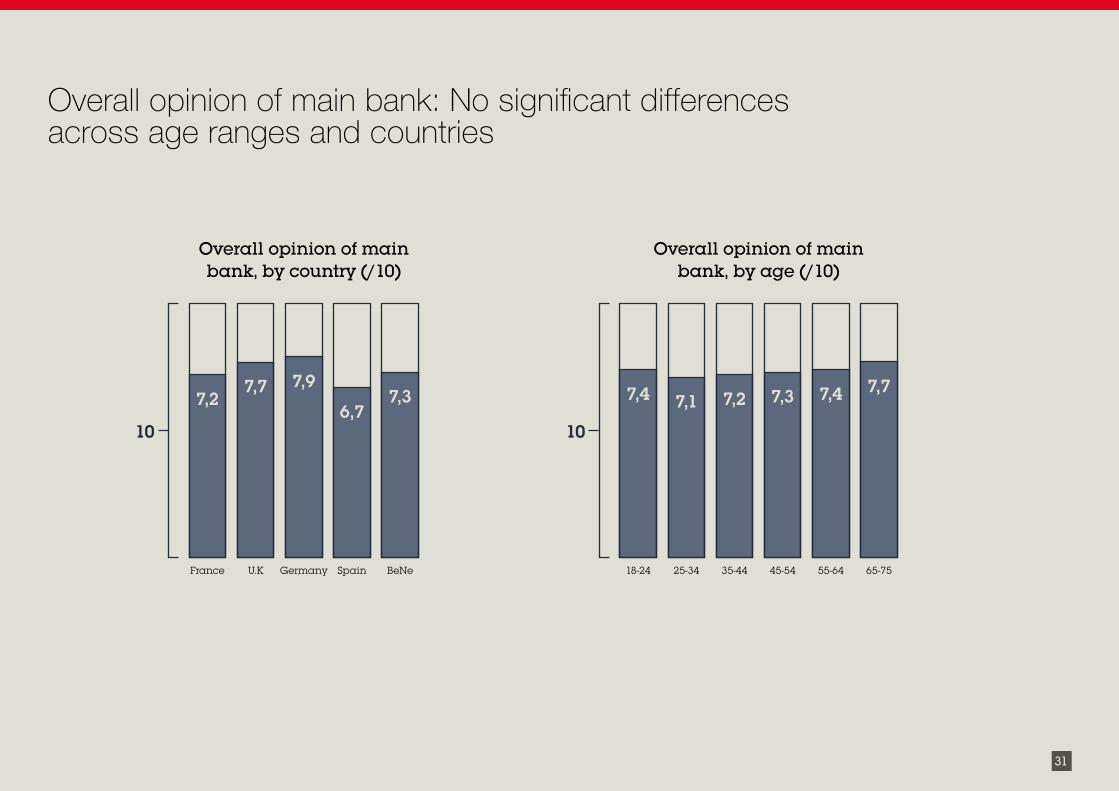

Overall opinion of main bank: No significant differences across age ranges and countries

France U.K Germany Spain BeNe

7,27,7 7,9

6,77,3

10

18-24 25-34 35-44 45-54 55-64 65-75

7,4 7,1 7,2 7,3 7,4 7,7

10

Overall opinion of main bank, by country (/10)

Overall opinion of main bank, by age (/10)

32

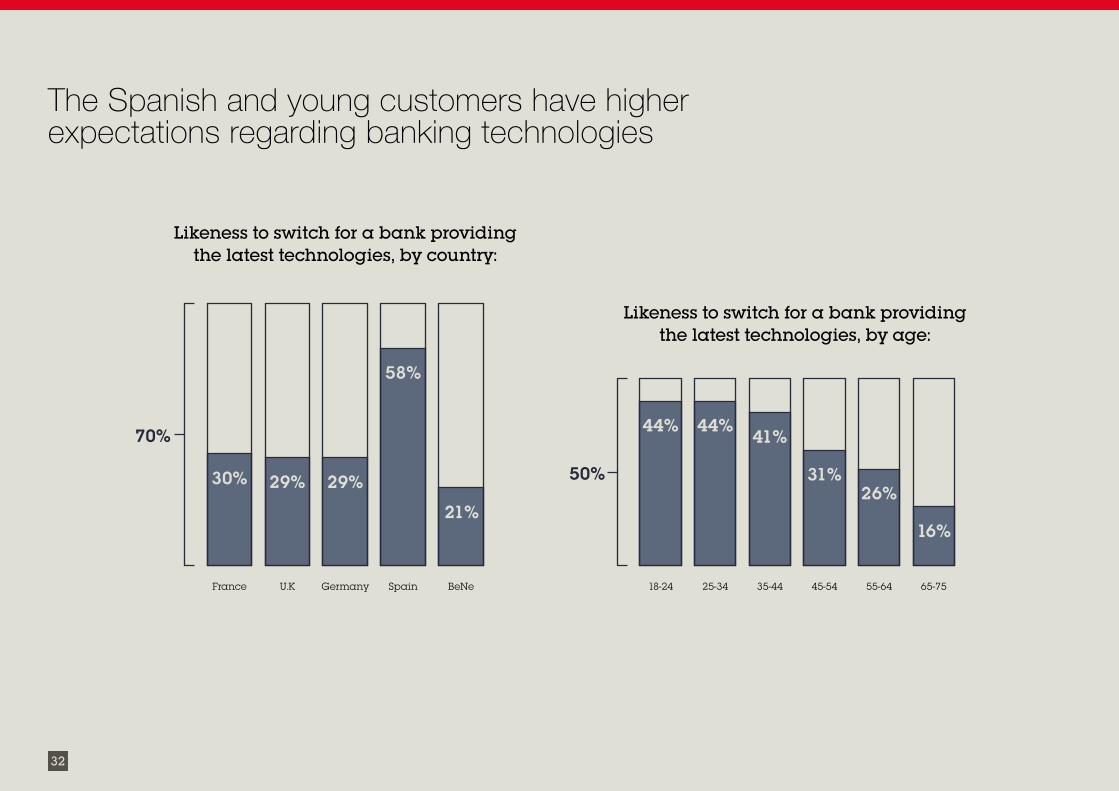

The Spanish and young customers have higher expectations regarding banking technologies

France U.K Germany Spain BeNe

30% 29%

70%

18-24 25-34 35-44 45-54 55-64 65-75

44% 44%41%

31%26%

16%

50%

Likeness to switch for a bank providing the latest technologies, by country:

Likeness to switch for a bank providing the latest technologies, by age:

58%

21%29%

29%

33

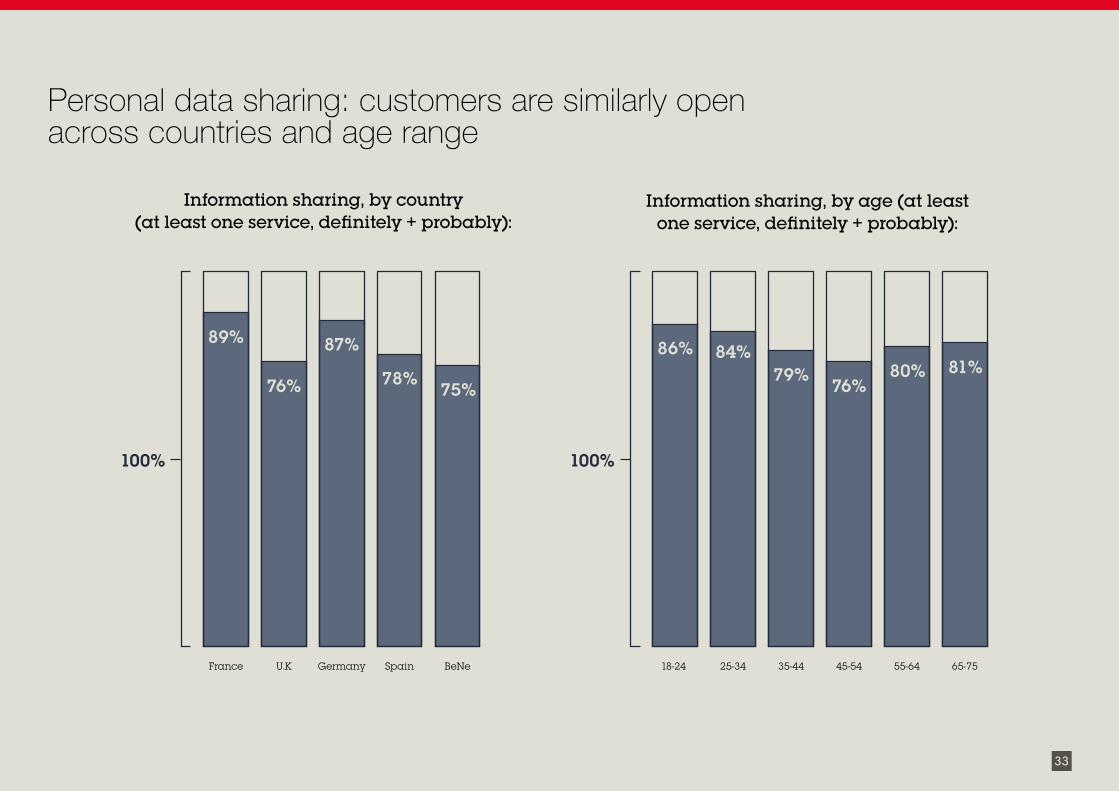

Personal data sharing: customers are similarly open across countries and age range

Information sharing, by country(at least one service, definitely + probably):

Information sharing, by age (at least one service, definitely + probably):

France U.K Germany Spain BeNe

89%

76%

100%

78%75%

29%

87%

18-24 25-34 35-44 45-54 55-64 65-75

86% 84%

100%

76%80% 81%

29%

79%

34

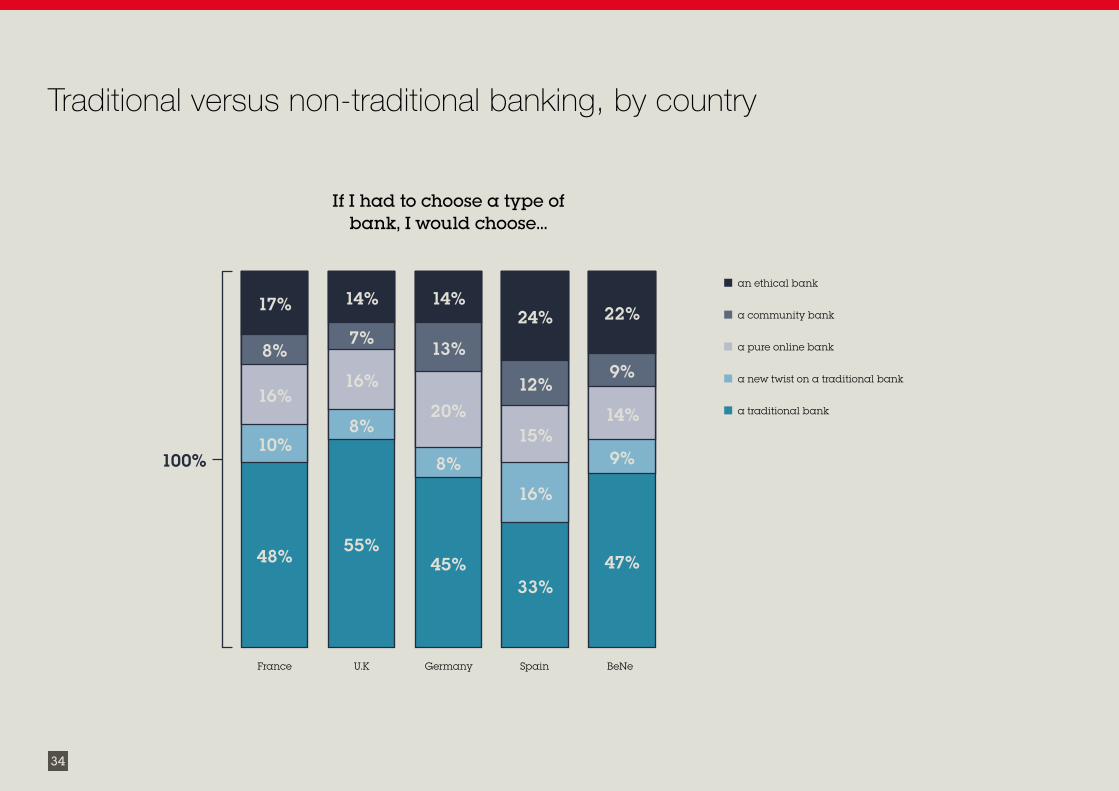

Traditional versus non-traditional banking, by country

France U.K Germany Spain BeNe

100%

If I had to choose a type of bank, I would choose…

a new twist on a traditional bank

a community bank

a pure online bank

an ethical bank

a traditional bank

17% 14% 14%24% 22%

8%7%

13%

12%9%

16%16%

20%15%

14%

10%8%

8%

16%

9%

48%55%

45%33%

47%

35

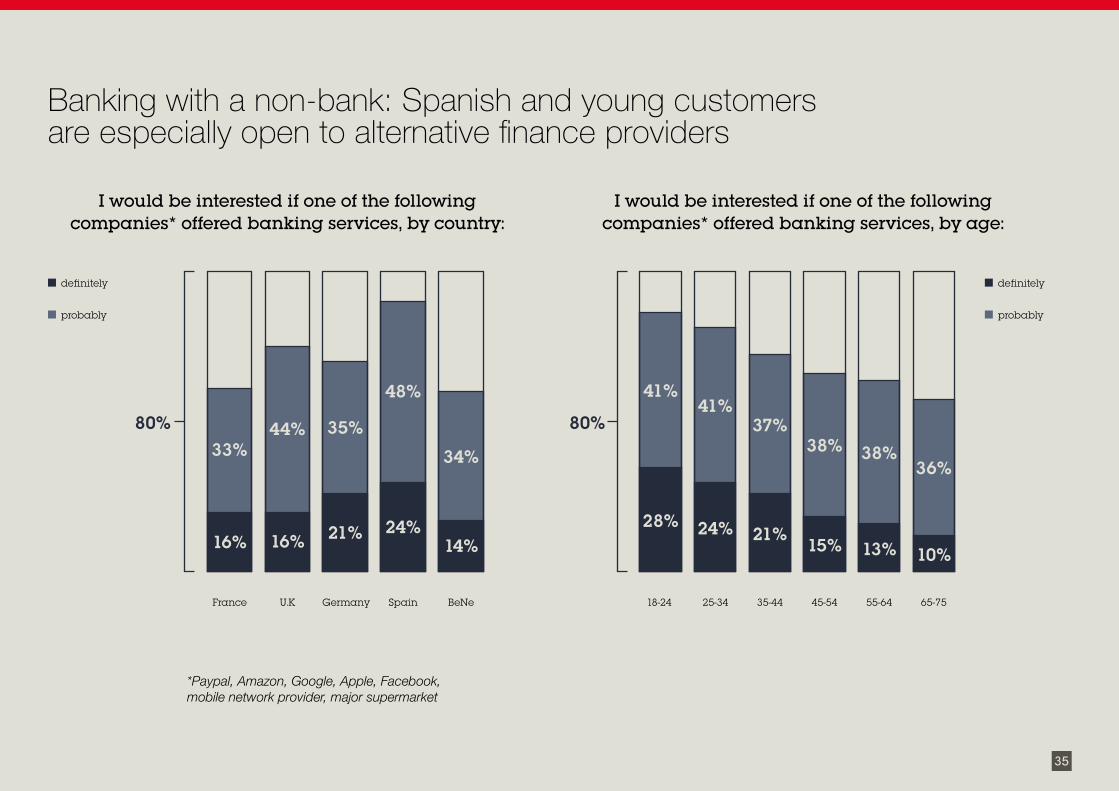

Banking with a non-bank: Spanish and young customers are especially open to alternative finance providers

France 18-24 25-34 35-44 45-54 55-64 65-75U.K Germany Spain BeNe

16%

33%

41%

28%

41%

24%

37%

21%

38%

15%

38%

13%

36%

10%16%

44% 80% 80%

I would be interested if one of the following companies* offered banking services, by country:

I would be interested if one of the following companies* offered banking services, by age:

24%

48%

14%

34%

29% 21%

35%

*Paypal, Amazon, Google, Apple, Facebook,mobile network provider, major supermarket

definitely definitely

probably probably

www.soprabanking.com