selling guide - november13, 2012 - fannie mae

TRANSCRIPT

Selling GuideFannie Mae Single Family

November 13, 2012

Selling Guide: Fannie Mae Single FamilyPublished November 13, 2012

November 13, 2012

Fannie Mae Copyright Notice

(1) © 2012 Fannie Mae. No part of this Selling Guide may be reproduced in any form or byany means without Fannie Mae’s prior written permission, except as may be provided hereinor unless otherwise permitted by law. Limited permission to download and/or print a copy ofthe PDF version of this Selling Guide from Fannie Mae-controlled websites is granted solelyfor internal business purposes, which permission Fannie Mae may revoke in its sole discretion.Limited permission to reproduce this Selling Guide in print in whole or in part and limitedpermission to distribute electronically parts of this Selling Guide are granted to Fannie Mae-approved lenders strictly for their own use in originating mortgages and selling mortgages toFannie Mae. Fannie Mae may revoke these limited permissions by written notice to any or allFannie Mae-approved lenders.

Trademarks are the property of their respective owners.

A full version of the Selling Guide is also available for viewing on the AllRegs website ofMortgage Resource Center, Inc., (“MRC”), which posts the Selling Guide under license fromand with the express permission of Fannie Mae. If there should ever be a difference between theSelling Guide as it appears on the AllRegs website and this version, the difference is an error. Insuch event, this version shall be deemed the correct authoritative version. Material discrepanciesbetween the two versions, identified by Fannie Mae or otherwise brought to our attention, maybe addressed by Announcement.

(2) Disclaimer: You acknowledge and agree (individually and on behalf of the entity for whichyou are accessing the Selling Guide) that you (and the entity for which you are accessing theSelling Guide) may not make any claim against Fannie Mae for any errors, and Fannie Mae shallnot be liable to you (or the entity for which you accessing the Selling Guide) for any losses ordamages whatsoever resulting directly or indirectly from any errors.

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. i

Table of ContentsPreface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . xxPart A, Doing Business with Fannie Mae . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Subpart A1, Approval Qualification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3A1-1, Application and Approval of Lender . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

A1-1-01, Application and Approval of Lender (06/26/2012) . . . . . . . . . . . . . . . 4Subpart A2, Lender Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

A2-1, Contractual Obligations for Fannie Mae–Approved Lenders . . . . . . . . . . . . . 10A2-1-01, Contractual Obligations for Lenders (04/01/2009) . . . . . . . . . . . . . . 10A2-1-02, Nature of Mortgage Transaction (04/01/2009) . . . . . . . . . . . . . . . . . . 13A2-1-03, Indemnification for Losses (09/27/2011) . . . . . . . . . . . . . . . . . . . . . . 14

A2-2, Contractual Representations and Warranties . . . . . . . . . . . . . . . . . . . . . . . . . . 16A2-2-01, Contractual Representations and Warranties (04/01/2009) . . . . . . . . . 16A2-2.1, Additional Selling Representations and Warranties . . . . . . . . . . . . . . . 18

A2-2.1-01, Selling Representations and Warranties Overview(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18A2-2.1-02, Delivery Information and Delivery-Option SpecificRepresentations and Warranties (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . 18A2-2.1-03, Document Warranties (07/26/2011) . . . . . . . . . . . . . . . . . . . . . 20A2-2.1-04, Limited Waiver of Contractual Warranties for MortgagesSubmitted to DU (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24A2-2.1-05, Invalidation of Limited Waiver of Representation andWarranties (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

A2-3, Lender Breach of Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29A2-3.1, Lender Breach of Contract . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

A2-3.1-01, Lender Breach of Contract (04/01/2009) . . . . . . . . . . . . . . . . 30A2-3.1-02, Sanctions, Suspensions, and Terminations (04/01/2009) . . . . . 32

A2-3.2, Loan Repurchases Requested by Fannie Mae . . . . . . . . . . . . . . . . . . . 35A2-3.2-01, Loan Repurchases Requested by Fannie Mae (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35A2-3.2-02, Repurchases Resulting From Warranty Violations(11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39A2-3.2-03, No Repurchase of Performing Mortgages for Breach ofContractual Selling Warranties (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . 40

A2-3.3, Compensatory Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43A2-3.3-01, Compensatory Fees (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . 43

A2-4, Master Agreement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46A2-4-01, Master Agreement Overview (06/28/2011) . . . . . . . . . . . . . . . . . . . . 46A2-4-02, Terms of a Master Agreement (04/01/2009) . . . . . . . . . . . . . . . . . . . 48A2-4-03, Variances and Special Provisions (06/26/2012) . . . . . . . . . . . . . . . . . 49

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. ii

A2-4-04, Breaches of a Master Agreement (04/01/2009) . . . . . . . . . . . . . . . . . 50A2-5, Mortgage Files and Records . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

A2-5.1, Establishment and Maintenance of Mortgage Files and Records . . . . . 52A2-5.1-01, Overview of Mortgage Files and Records (04/01/2009) . . . . . 52A2-5.1-02, Individual Mortgage Loan Files (11/13/2012) . . . . . . . . . . . . . 53A2-5.1-03, Electronic Records, Signature, and Transactions(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55A2-5.1-04, Lender’s or Document Custodian’s Electronic TransactionsWith Third Parties (07/26/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

A2-5.2, Ownership, Retention, and Examination of Mortgage Files andRecords . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

A2-5.2-01, Ownership of Mortgage Loan Files and Records(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62A2-5.2-02, Access to Records (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . 63A2-5.2-03, Retention and Storage of Mortgage File Records(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

A2-6, Fannie Mae Trade Name and Trademarks . . . . . . . . . . . . . . . . . . . . . . . . . . . 67A2-6-01, Fannie Mae Trade Name and Trademarks (04/01/2009) . . . . . . . . . . 67

Subpart A3, Getting Started With Fannie Mae . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71A3-1, Fannie Mae’s Technology Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

A3-1-01, Fannie Mae’s Technology Products (04/01/2009) . . . . . . . . . . . . . . . 72A3-2, Compliance With Requirements and Laws . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

A3-2-01, Compliance With Laws (12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . 74A3-2-02, Responsible Lending Practices (05/15/2012) . . . . . . . . . . . . . . . . . . . 76

A3-3, Third-Party Lending Functions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82A3-3-01, Outsourcing of Mortgage Processing and Third-Party Originations(07/26/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83A3-3-02, Concurrent Servicing Transfers (09/27/2011) . . . . . . . . . . . . . . . . . . 86A3-3-03, Subservicing (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90A3-3-04, Document Custodians (11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . 91A3-3-05, Custody of Mortgage Documents (09/27/2011) . . . . . . . . . . . . . . . . . 98A3-3-06, Fannie Mae's Designated Document Custodian (06/28/2011) . . . . . 101A3-3.1, Other Document Custodians . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

A3-3.1-01, Operational Requirements for all Document Custodians(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103A3-3.1-02, Document Custodian Reporting Requirements: Active andInactive Status (10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

A3-3.2, Document Custodian Electronic Transactions . . . . . . . . . . . . . . . . . . 110A3-3.2-01, Document Custodian Electronic Transactions (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 110

A3-4, Lending Practices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. iii

A3-4-01, Confidentiality of Information/Conflict of Interest Parameters(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112A3-4-02, Data Quality and Integrity (06/26/2012) . . . . . . . . . . . . . . . . . . . . . 113A3-4-03, Preventing, Detecting, and Reporting Mortgage Fraud (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

A3-5, Fidelity Bond and Errors and Omissions Coverage . . . . . . . . . . . . . . . . . . . 120A3-5-01, Fidelity Bond and Errors and Omissions Coverage Provisions(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 120A3-5-02, Fidelity Bond Policy Requirements (04/01/2009) . . . . . . . . . . . . . . 122A3-5-03, Errors and Omissions Policy Requirements (03/02/2010) . . . . . . . . 123A3-5-04, Reporting Fidelity Bond and Errors and Omissions Events(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

Subpart A4, Maintaining Lender Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 126A4-1, Maintaining Lender Eligibility: Overview . . . . . . . . . . . . . . . . . . . . . . . . . . 127

A4-1-01, Maintaining Lender Eligibility (10/02/2012) . . . . . . . . . . . . . . . . . . 127A4-2, Submission of Operational and Financial Information . . . . . . . . . . . . . . . . . 130

A4-2-01, Net Worth and Liquidity Requirements (01/27/2011) . . . . . . . . . . . 130A4-2-02, Financial Statements and Reports (04/01/2009) . . . . . . . . . . . . . . . . 134A4-2-03, Lender Record Information (Form 582) (04/01/2009) . . . . . . . . . . . 137

A4-3, Changes in the Lender’s Organization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 139A4-3-01, Report of Changes in the Lender’s Organization (04/01/2009) . . . . 139

Part B, Origination Through Closing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141Subpart B1, Loan Application Package . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

B1-1, Application Package Documentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144B1-1-01, Contents of the Application Package (09/20/2010) . . . . . . . . . . . . . 144B1-1-02, Blanket Authorization Form (04/01/2009) . . . . . . . . . . . . . . . . . . . . 146B1-1-03, Allowable Age of Credit Documents (10/30/2009) . . . . . . . . . . . . . 147

Subpart B2, Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148B2-1, Mortgage Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 149

B2-1.1, LTV, CLTV, HCLTV, and Subordinate Financing . . . . . . . . . . . . . . . 150B2-1.1-01, Loan-to-Value (LTV) Ratios (03/31/2011) . . . . . . . . . . . . . . 150B2-1.1-02, Combined Loan-to-Value (CLTV) Ratios (03/31/2011) . . . . . 152B2-1.1-03, Home Equity Combined Loan-to-Value (HCLTV) Ratios(10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154B2-1.1-04, Subordinate Financing (08/21/2012) . . . . . . . . . . . . . . . . . . . 156

B2-1.2, Loan Purpose . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 161B2-1.2-01, Purchase Transactions (12/20/2011) . . . . . . . . . . . . . . . . . . . 161B2-1.2-02, Limited Cash-Out Refinance Transactions (11/13/2012) . . . . 164B2-1.2-03, Cash-Out Refinance Transactions (11/13/2012) . . . . . . . . . . 168B2-1.2-04, Continuity of Obligation (06/28/2011) . . . . . . . . . . . . . . . . . 172B2-1.2-05, Prohibited Refinancing Practices (11/13/2012) . . . . . . . . . . . 174

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. iv

B2-1.2-06, Payoff of Installment Land Contract Requirements(11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176

B2-1.3, Loan Amortization Types . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 178B2-1.3-01, Fully Amortizing Fixed-Rate Mortgages (12/30/2009) . . . . . 178B2-1.3-02, Adjustable-Rate Mortgages (ARMs) (08/21/2012) . . . . . . . . 180B2-1.3-03, Convertible ARMs (07/26/2011) . . . . . . . . . . . . . . . . . . . . . . 193B2-1.3-04, Refinanced Balloon Mortgages (06/26/2012) . . . . . . . . . . . . 198B2-1.3-05, Growing-Equity Mortgage (GEM) Loans (04/01/2009) . . . . 201B2-1.3-06, Temporary Interest Rate Buydowns (08/21/2012) . . . . . . . . . 202

B2-1.4, Other Loan Attributes and Related Policies . . . . . . . . . . . . . . . . . . . . 207B2-1.4-01, Mortgage Loan Limits (03/31/2011) . . . . . . . . . . . . . . . . . . . 207B2-1.4-02, Mortgage Loan Eligibility (06/26/2012) . . . . . . . . . . . . . . . . 209B2-1.4-03, Legal Requirements (07/26/2011) . . . . . . . . . . . . . . . . . . . . . 220B2-1.4-04, Escrow Accounts (11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . 223

B2-2, Borrower Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 226B2-2-01, General Borrower Eligibility Requirements (06/26/2012) . . . . . . . . 226B2-2-02, Non–U.S. Citizen Borrower Eligibility Requirements (03/02/2010). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 229B2-2-03, Multiple Financed Properties for the Same Borrower (11/13/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230B2-2-04, Guarantors, Co-Signers, or Non-Occupant Co-Borrowers(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237B2-2-05, Inter Vivos Revocable Trusts (04/01/2009) . . . . . . . . . . . . . . . . . . . 239B2-2-06, Home-buyer Education and Counseling (03/31/2011) . . . . . . . . . . . 242

B2-3, Occupancy and Property Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 246B2-3-01, Occupancy Type Requirements (08/30/2011) . . . . . . . . . . . . . . . . . . 246B2-3-02, One- to Four-Unit Properties (10/30/2009) . . . . . . . . . . . . . . . . . . . 249B2-3-03, Co-op Properties (05/15/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 252B2-3-04, Leasehold Estates (05/15/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 257B2-3-05, Factory-Built Housing (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . 261

Subpart B3, Underwriting Borrowers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 263B3-1, Manual Underwriting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 265

B3-1-01, Comprehensive Risk Assessment (08/21/2012) . . . . . . . . . . . . . . . . 265B3-2, Desktop Underwriter (DU) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 268

B3-2-01, General Information on DU (08/21/2012) . . . . . . . . . . . . . . . . . . . . 269B3-2-02, Risk Factors Evaluated by DU (08/21/2012) . . . . . . . . . . . . . . . . . . 274B3-2-03, DU Documentation Requirements (06/26/2012) . . . . . . . . . . . . . . . 279B3-2-04, Approve/Eligible, EA-I/Eligible, EA-II/Eligible, and EA-III/Eligible Recommendations (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 280B3-2-05, Approve/Ineligible, EA-I/Ineligible, EA-II/Ineligible, and EA-III/Ineligible Recommendations (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . 282

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. v

B3-2-06, Refer with Caution and Refer with Caution/IV Recommendations(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 283B3-2-07, Out of Scope Recommendations (04/01/2009) . . . . . . . . . . . . . . . . . 285B3-2-08, Erroneous Credit Report Data (08/21/2012) . . . . . . . . . . . . . . . . . . 285B3-2-09, Accuracy of DU Data, DU Tolerances, and Errors in the CreditReport (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 287B3-2-10, DU Underwriting Findings Report (08/21/2012) . . . . . . . . . . . . . . . 291

B3-3, Income Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 294B3-3.1, Employment and Other Sources of Income . . . . . . . . . . . . . . . . . . . . 295

B3-3.1-01, General Income Information (06/26/2012) . . . . . . . . . . . . . . 295B3-3.1-02, Standards for Employment Documentation (05/15/2012) . . . 301B3-3.1-03, Base Pay (Salary or Hourly), Bonus, and Overtime Income(05/15/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 303B3-3.1-04, Commission Income (05/15/2012) . . . . . . . . . . . . . . . . . . . . 306B3-3.1-05, Secondary Employment Income (Second Job and MultipleJobs) and Seasonal Income (05/15/2012) . . . . . . . . . . . . . . . . . . . . . . . . 308B3-3.1-06, Requirements and Uses of IRS Form 4506-T (05/15/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 310B3-3.1-07, Verbal Verification of Employment (05/15/2012) . . . . . . . . . 312B3-3.1-08, Rental Income (05/15/2012) . . . . . . . . . . . . . . . . . . . . . . . . . 316B3-3.1-09, Other Sources of Income (11/13/2012) . . . . . . . . . . . . . . . . . 323

B3-3.2, Self-Employment Income . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 341B3-3.2-01, Underwriting Factors and Documentation for a Self-Employed Borrower (09/20/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 341B3-3.2-02, Business Structures (03/02/2010) . . . . . . . . . . . . . . . . . . . . . 344B3-3.2-03, IRS Forms Quick Reference (04/01/2009) . . . . . . . . . . . . . . 349B3-3.2.1, Documentation Requirements for an Individual . . . . . . . . . . . 351B3-3.2.2, Documentation Requirements for a Business . . . . . . . . . . . . . 362

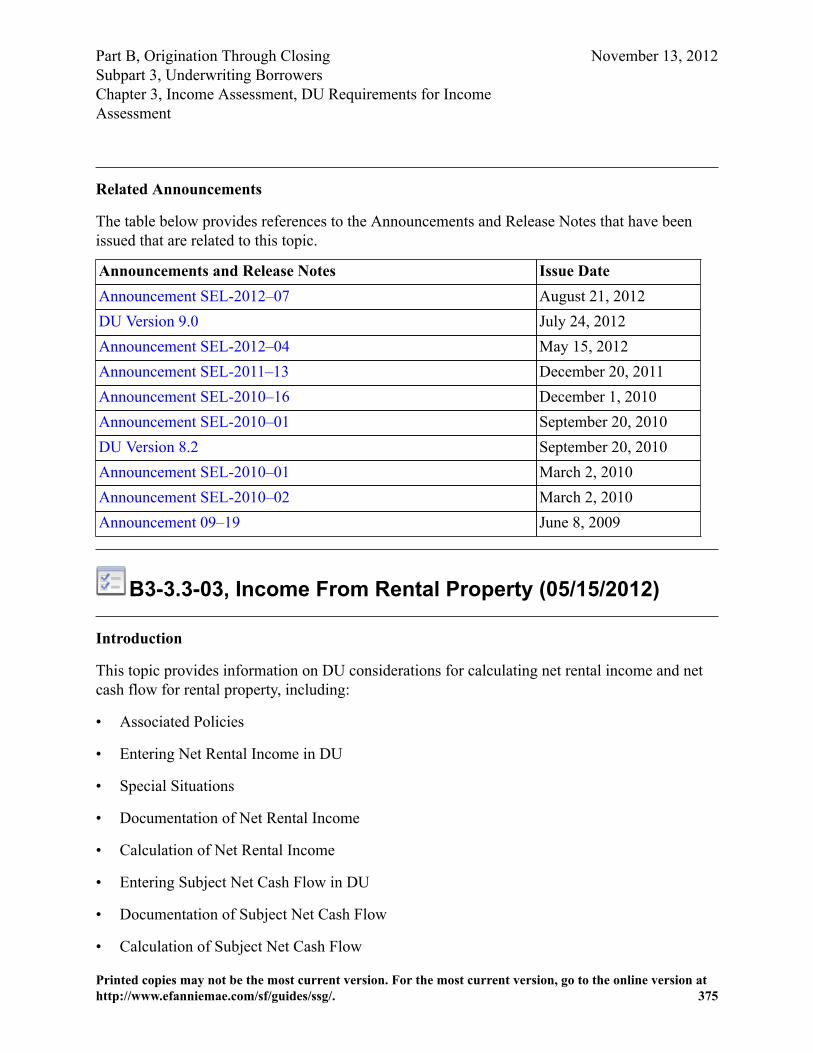

B3-3.3, DU Requirements for Income Assessment . . . . . . . . . . . . . . . . . . . . . 368B3-3.3-01, Documents Used for DU Income Assessment (08/21/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 368B3-3.3-02, Income and Employment Documentation for DU(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 370B3-3.3-03, Income From Rental Property (05/15/2012) . . . . . . . . . . . . . 375

B3-4, Asset Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 380B3-4.1, General Asset Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 381

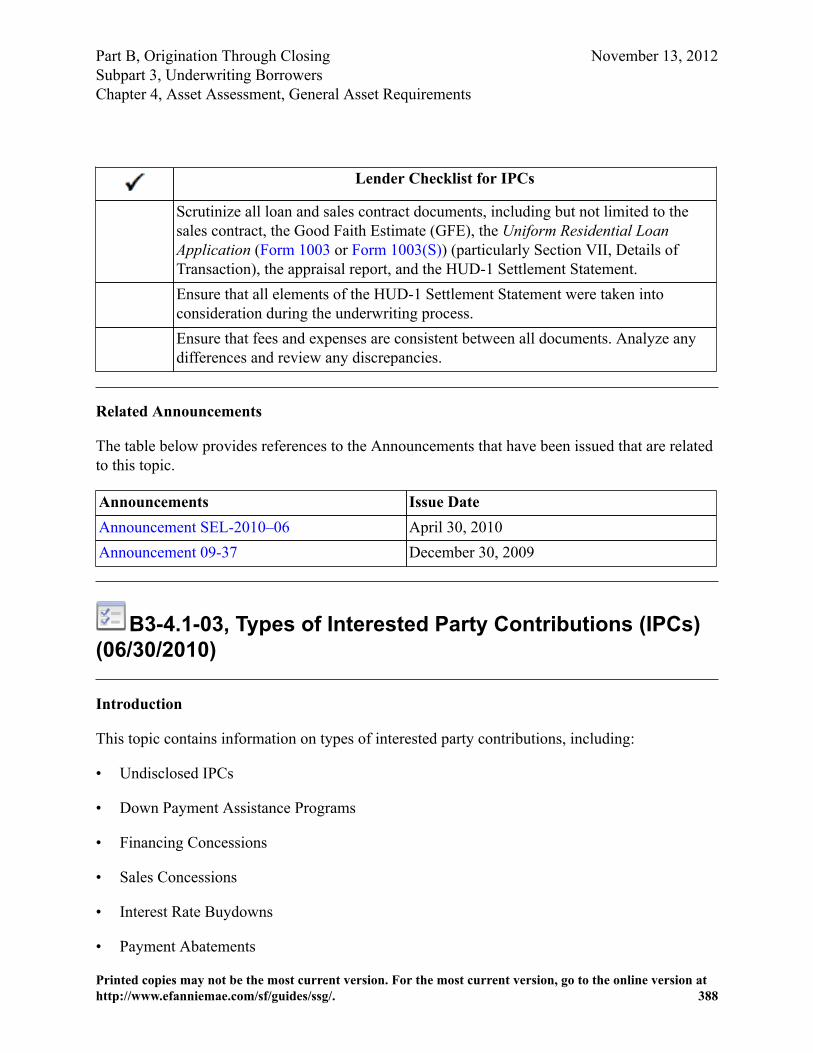

B3-4.1-01, Minimum Reserve Requirements (08/21/2012) . . . . . . . . . . . 381B3-4.1-02, Interested Party Contributions (IPCs) (04/30/2010) . . . . . . . 386B3-4.1-03, Types of Interested Party Contributions (IPCs) (06/30/2010). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 388

B3-4.2, Verification of Depository Assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . 392

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. vi

B3-4.2-01, Verification of Deposits and Assets (11/13/2012) . . . . . . . . . 392B3-4.2-02, Depository Accounts (11/13/2012) . . . . . . . . . . . . . . . . . . . . 394B3-4.2-03, Individual Development Accounts (12/01/2010) . . . . . . . . . . 395B3-4.2-04, Pooled Savings (Community Savings Funds) (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 398B3-4.2-05, Verification of Assets for Non-U.S. Citizen Borrowers(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 398

B3-4.3, Verification of Non-Depository Assets . . . . . . . . . . . . . . . . . . . . . . . . 400B3-4.3-01, Stocks, Stock Options, Bonds, and Mutual Funds(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 400B3-4.3-02, Trust Accounts (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . 401B3-4.3-03, Retirement Accounts (11/13/2012) . . . . . . . . . . . . . . . . . . . . 402B3-4.3-04, Personal Gifts (09/20/2010) . . . . . . . . . . . . . . . . . . . . . . . . . 403B3-4.3-05, Gifts of Equity (11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . 406B3-4.3-06, Donations From Entities (09/20/2010) . . . . . . . . . . . . . . . . . 407B3-4.3-07, Disaster Relief Grants or Loans (04/01/2009) . . . . . . . . . . . . 409B3-4.3-08, Employer Assistance (09/20/2010) . . . . . . . . . . . . . . . . . . . . 410B3-4.3-09, Earnest Money Deposit (08/21/2012) . . . . . . . . . . . . . . . . . . 412B3-4.3-10, Anticipated Sales Proceeds (04/01/2009) . . . . . . . . . . . . . . . 414B3-4.3-11, Trade Equity (12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . 415B3-4.3-12, Rent Credit for Option to Purchase (04/01/2009) . . . . . . . . . 417B3-4.3-13, Sweat Equity (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . 417B3-4.3-14, Bridge/Swing Loans (04/01/2009) . . . . . . . . . . . . . . . . . . . . 418B3-4.3-15, Borrowed Funds Secured by an Asset (10/30/2009) . . . . . . . 419B3-4.3-16, Credit Card Financing (10/30/2009) . . . . . . . . . . . . . . . . . . . 420B3-4.3-17, Personal Unsecured Loans (09/20/2010) . . . . . . . . . . . . . . . . 421B3-4.3-18, Sale of Personal Assets (04/01/2009) . . . . . . . . . . . . . . . . . . 422B3-4.3-19, Cash Value of Life Insurance (04/01/2009) . . . . . . . . . . . . . . 423B3-4.3-20, Anticipated Savings and Cash-on-Hand (04/01/2009) . . . . . . 424

B3-4.4, DU Requirements for Asset Assessment . . . . . . . . . . . . . . . . . . . . . . 425B3-4.4-01, Asset Verification (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . 425B3-4.4-02, Documentation Requirements (09/20/2010) . . . . . . . . . . . . . 428

B3-5, Credit Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 433B3-5.1, Credit Scores . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 434

B3-5.1-01, General Requirements for Credit Scores (11/13/2012) . . . . . 434B3-5.1-02, Determining the Representative Credit Score for a MortgageLoan (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 438

B3-5.2, Credit Reports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 441B3-5.2-01, Requirements for Credit Reports (10/30/2009) . . . . . . . . . . . 441B3-5.2-02, Types of Credit Reports (09/20/2010) . . . . . . . . . . . . . . . . . . 445

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. vii

B3-5.2-03, Accuracy of Credit Information in a Credit Report(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 448

B3-5.3, Traditional Credit History . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 450B3-5.3-01, Number and Age of Accounts (04/01/2009) . . . . . . . . . . . . . 450B3-5.3-02, Payment History (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . 450B3-5.3-03, Previous Mortgage Payment History (04/01/2009) . . . . . . . . 451B3-5.3-04, Inquiries: Recent Attempts to Obtain New Credit(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 453B3-5.3-05, Credit Utilization (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . 453B3-5.3-06, Authorized Users of Credit(10/30/2009) . . . . . . . . . . . . . . . . 454B3-5.3-07, Significant Derogatory Credit Events — Waiting Periodsand Re-establishing Credit (05/15/2012) . . . . . . . . . . . . . . . . . . . . . . . . . 456B3-5.3-08, Extenuating Circumstances for Derogatory Credit(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 461B3-5.3-09, DU Credit Report Analysis (11/13/2012) . . . . . . . . . . . . . . . 462

B3-5.4, Nontraditional Credit History . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 471B3-5.4-01, Nontraditional Mortgage Credit Reports (08/21/2012) . . . . . 471B3-5.4-02, Types of Credit (Tiers I, II, and III) (10/30/2009) . . . . . . . . . 474B3-5.4-03, Verification and Documentation of Alternative Credit(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 476

B3-6, Liability Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 479B3-6-01, General Information on Liabilities (09/20/2010) . . . . . . . . . . . . . . . 479B3-6-02, Debt-to-Income Ratios (10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . 481B3-6-03, Monthly Housing Expense (08/21/2012) . . . . . . . . . . . . . . . . . . . . . 485B3-6-04, Qualifying Payment Requirements (08/21/2012) . . . . . . . . . . . . . . . 486B3-6-05, Monthly Debt Obligations (05/24/2011) . . . . . . . . . . . . . . . . . . . . . 489B3-6-06, Qualifying Impact of Other Real Estate Owned (11/13/2012) . . . . . 494B3-6-07, Debts Paid Off At/Prior to Closing (11/13/2012) . . . . . . . . . . . . . . . 498B3-6-08, DU: Requirements of Liability Assessment (12/01/2010) . . . . . . . . 500

Subpart B4, Underwriting Property . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 503B4-1, Appraisal Guidelines . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 504

B4-1.1, General Appraisal Requirements . . . . . . . . . . . . . . . . . . . . . . . . . . . . 505B4-1.1-01, General Information on Appraisal Requirements(07/26/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 505B4-1.1-02, Lender Disclosure of Information to Appraisers(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 509B4-1.1-03, Appraiser Selection (12/01/2010) . . . . . . . . . . . . . . . . . . . . . 511B4-1.1-04, Use of Supervisory or Review Appraisers (10/30/2009) . . . . 514B4-1.1-05, Field Reviews (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . 516

B4-1.2, Appraisal Document Standards, Report, and Property Inspections . . . 518

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. viii

B4-1.2-01, Age of Appraisal or Age of Property Inspection(07/26/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 518B4-1.2-02, Objective and Unbiased Appraisals (04/01/2009) . . . . . . . . . 520B4-1.2-03, Definition of Market Value (04/01/2009) . . . . . . . . . . . . . . . 521B4-1.2-04, Requirements for Postponed Improvements (07/26/2011) . . . 522B4-1.2-05, Requirements for the Appraisal Report (10/25/2011) . . . . . . 526B4-1.2-06, Appraisal Forms and Report Exhibits (06/26/2012) . . . . . . . 529B4-1.2-07, Certifications and Statements of Assumptions and LimitingConditions (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 535

B4-1.3, Special Appraisal Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . 537B4-1.3-01, Special Appraisal Considerations for Properties Affected byEnvironmental Hazards (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . 537B4-1.3-02, Special Appraisal Considerations for Factory-Built Housing(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 539B4-1.3-03, Special Appraisal Considerations for Modular,Prefabricated, Panelized, or Sectional Housing (04/01/2009) . . . . . . . . . 540B4-1.3-04, Special Appraisal Considerations for Mixed-Use Properties(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 541B4-1.3-05, Special Appraisal Considerations for Properties in SpecialAssessment Districts (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 542B4-1.3-06, Special Appraisal Considerations for Properties Subject toLeasehold Interests (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 545B4-1.3-07, Special Appraisal Considerations for Units in Co-op Projects(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 546B4-1.3-08, Special DU Property Fieldwork Requirements forForeclosure and REO Properties (10/30/2009) . . . . . . . . . . . . . . . . . . . . 549

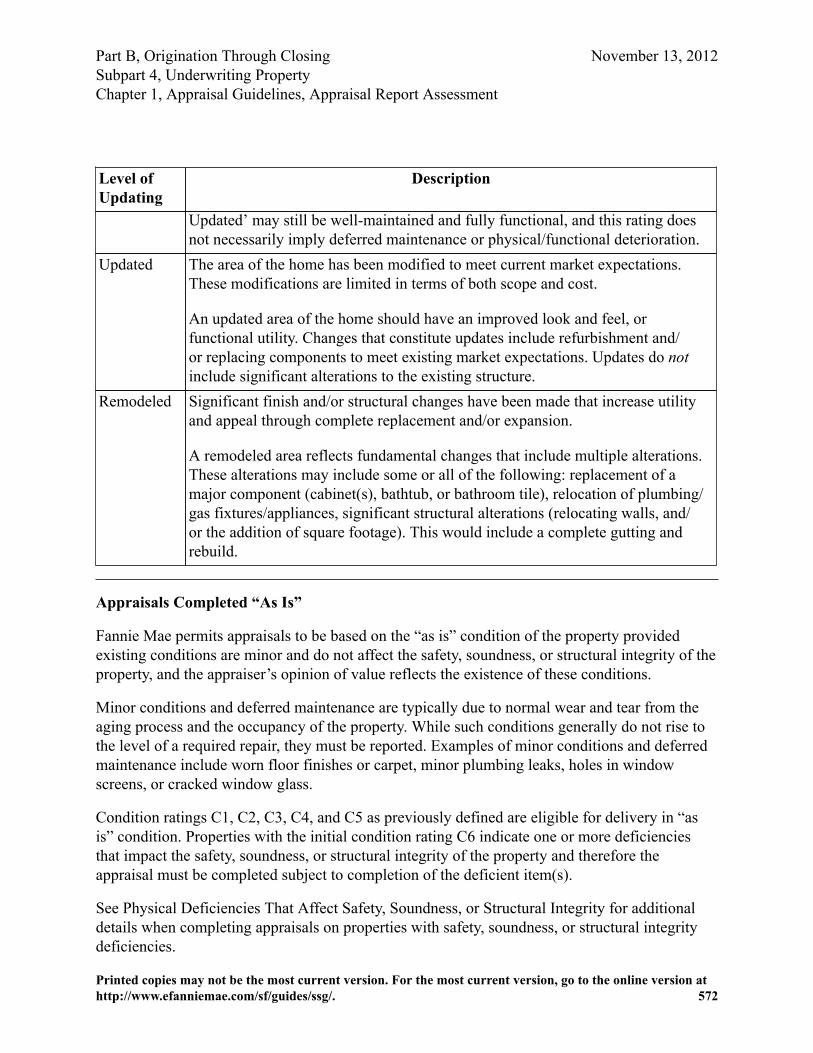

B4-1.4, Appraisal Report Assessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 551B4-1.4-01, Reviewing the Appraisal Report (04/01/2009) . . . . . . . . . . . 551B4-1.4-02, Appraisal Report Review: Urban Properties (04/01/2009) . . 552B4-1.4-03, Appraisal Report Review: Property Location (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 553B4-1.4-04, Appraisal Report Review: Trend of Neighborhood PropertyValues, Demand/Supply, and Marketing Time (10/30/2009) . . . . . . . . . . 555B4-1.4-05, Appraisal Report Review: Site Analysis Parameters(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 556B4-1.4-06, Appraisal Report Review: Subject Property Zoning(12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 558B4-1.4-07, Appraisal Report Review: Site Utilities (04/01/2009) . . . . . . 560B4-1.4-08, Appraisal Report Review: Off-Site Improvements(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 561

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. ix

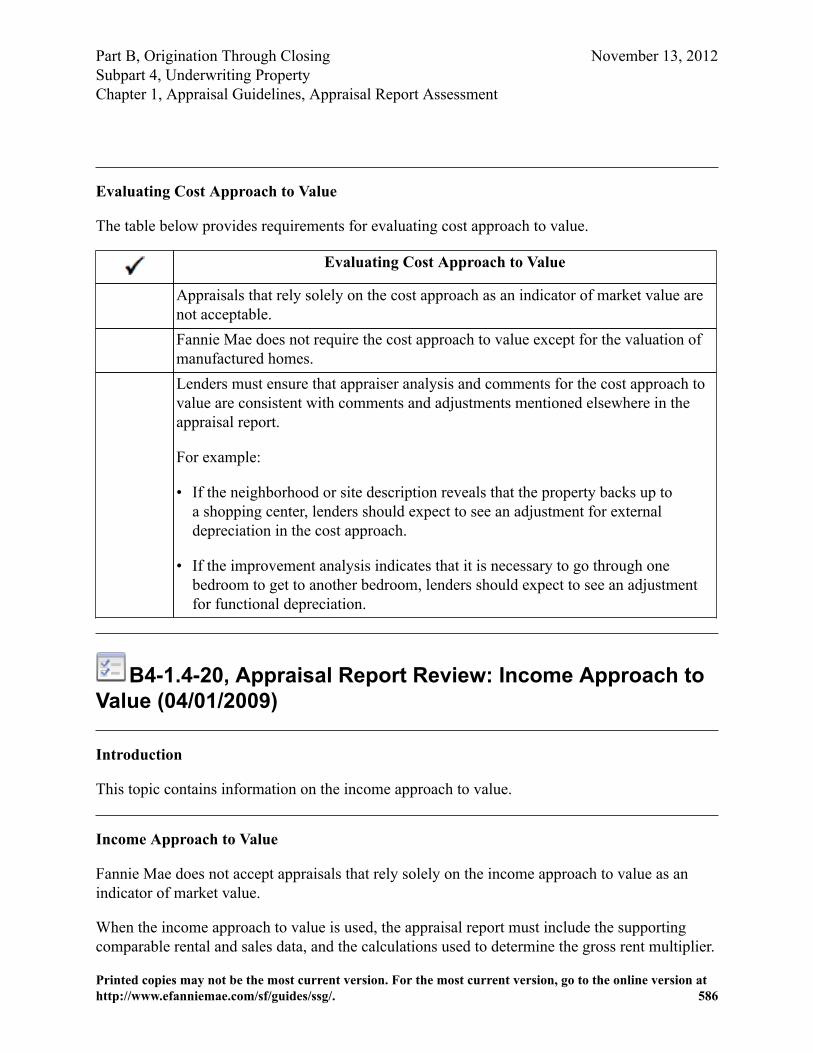

B4-1.4-09, Appraisal Report Review: Special Flood Hazard Area(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 562B4-1.4-10, Appraisal Report Review: Improvements Analysis Overview(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563B4-1.4-11, Appraisal Report Review: Conformity of Improvements toNeighborhood (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 564B4-1.4-12, Appraisal Report Review: Actual and Effective Ages of theImprovements (10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 564B4-1.4-13, Appraisal Report Review: Insulation and Energy Efficiencyof the Improvements (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 565B4-1.4-14, Appraisal Report Review: Layout, Floor Plans, and GrossBuilding and Living Areas (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . 566B4-1.4-15, Appraisal Report Review: Property Condition and Quality ofConstruction (07/26/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 568B4-1.4-16, Appraisal Report Review: Sales Comparison Approach(06/30/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 576B4-1.4-17, Appraisal Report Review: Adjustments to Comparable Sales(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 581B4-1.4-18, Appraisal Report Review: Lender Review of the AdjustmentGrid (10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 582B4-1.4-19, Appraisal Report Review: Cost Approach to Value(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 585B4-1.4-20, Appraisal Report Review: Income Approach to Value(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 586B4-1.4-21, Appraisal Report Review: Valuation Analysis and FinalReconciliation (06/30/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 587

B4-2, Project Standards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 590B4-2.1, General Project Standards and Environmental Hazards . . . . . . . . . . 591

B4-2.1-01, General Information on Project Standards (07/26/2011) . . . . 591B4-2.1-02, Ineligible Projects (12/01/2010) . . . . . . . . . . . . . . . . . . . . . . 594B4-2.1-03, Projects with Special Considerations and Project EligibilityWaivers (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 598B4-2.1-04, Project Identification and Document Retention (06/26/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 599B4-2.1-05, Project Insurance Requirements (04/01/2009) . . . . . . . . . . . . 600B4-2.1-06, Priority of Common Expense Assessments (08/21/2012) . . . 601B4-2.1-07, Project Standards: Environmental Hazard Assessments(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 602B4-2.1-08, Unacceptable Environmental Conditions (04/01/2009) . . . . . 605B4-2.1-09, Remedial Actions for Environmental Assessments BelowStandards (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 607

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. x

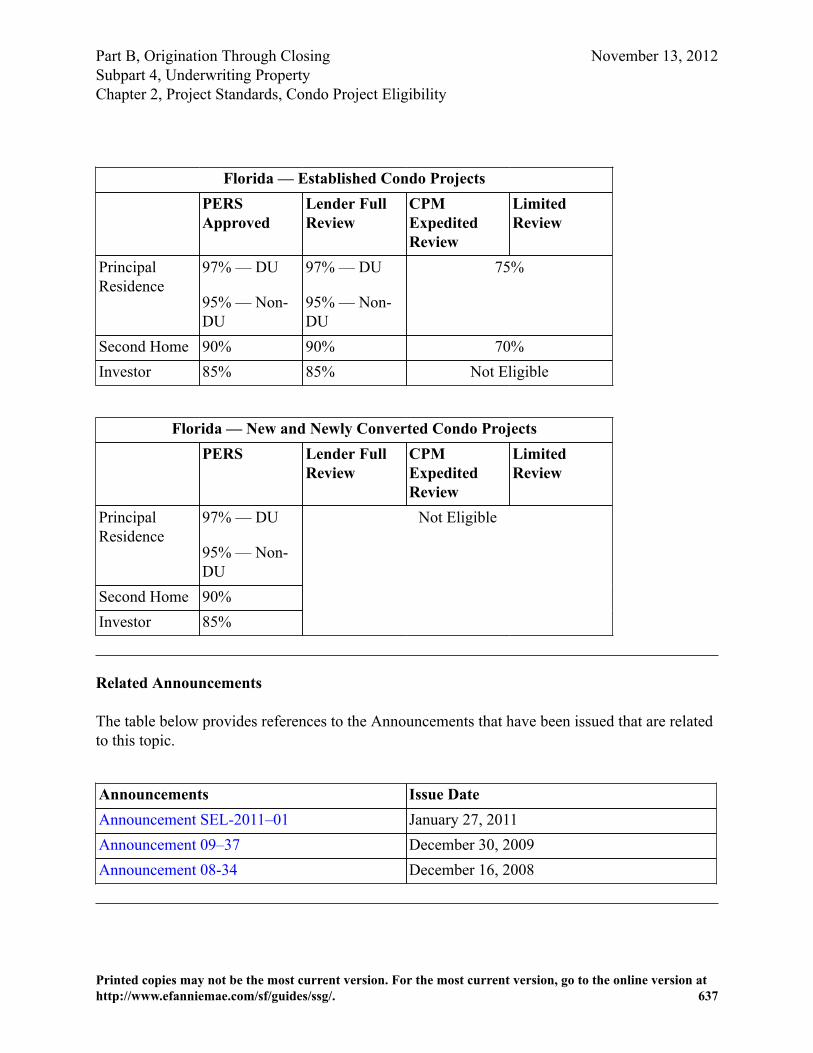

B4-2.2, Condo Project Eligibility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 609B4-2.2-01, Condo Project Eligibility (06/28/2011) . . . . . . . . . . . . . . . . . 609B4-2.2-02, Limited Review Process for Attached Condo Units(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 611B4-2.2-03, Limited Review Process for Detached Condo Units(06/28/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 613B4-2.2-04, Lender Full Review: General Eligibility Requirements forAll Condo Projects (12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 615B4-2.2-05, Lender Full Review: Additional Eligibility Requirementsfor New Condo Projects and Newly Converted Attached CondoProjects(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 618B4-2.2-06, Lender Full Review: Additional Eligibility Requirements forEstablished Condo Projects(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . 622B4-2.2-07, Owner-Occupancy Ratio Requirements and FinancialInstitution-Owned REO Units (10/30/2009) . . . . . . . . . . . . . . . . . . . . . . 625B4-2.2-08, Project Eligibility Review Service (PERS) (06/26/2012) . . . 626B4-2.2-09, Condo Project Manager (CPM) Expedited Review for Newand Established Condo Projects(06/26/2012) . . . . . . . . . . . . . . . . . . . . . 630B4-2.2-10, FHA-Approved Condo Review Eligibility (06/26/2012) . . . . 633B4-2.2-11, Fannie Mae Review of Condo Projects Comprised ofManufactured Homes (06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 634B4-2.2-12, Geographic-Specific Condo Project Considerations(01/27/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 636B4-2.2-13, Condo Project Review and Legal Document Requirements(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 638

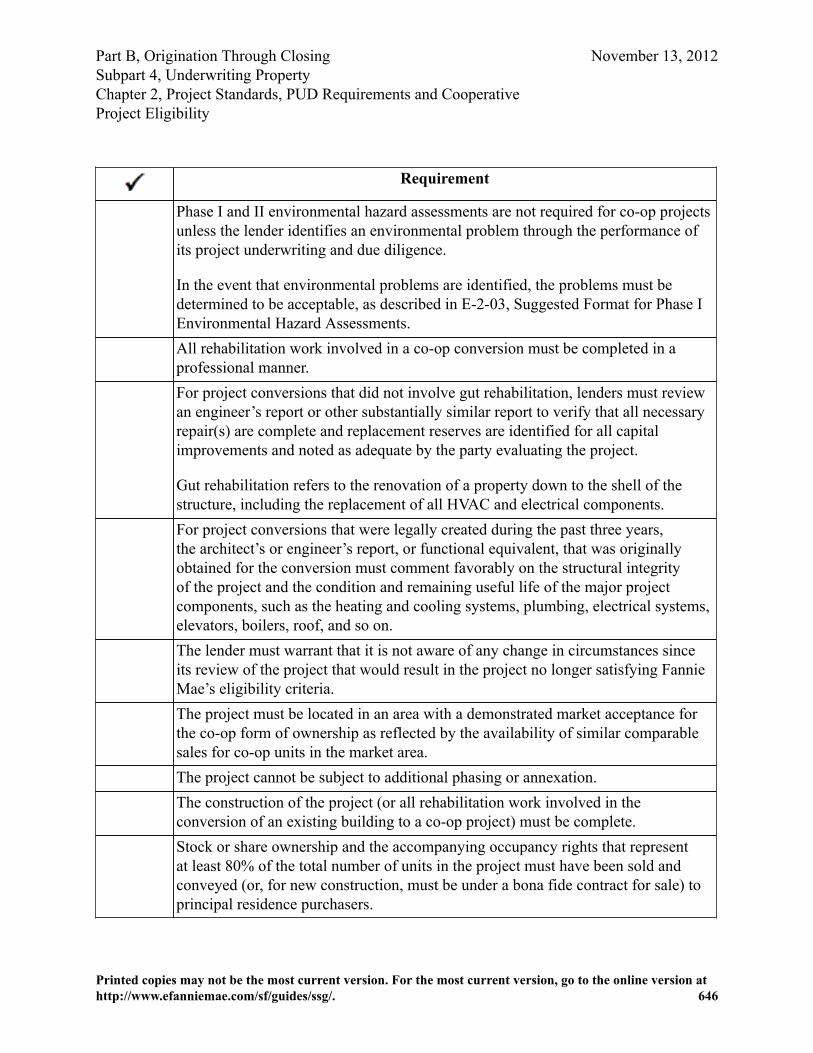

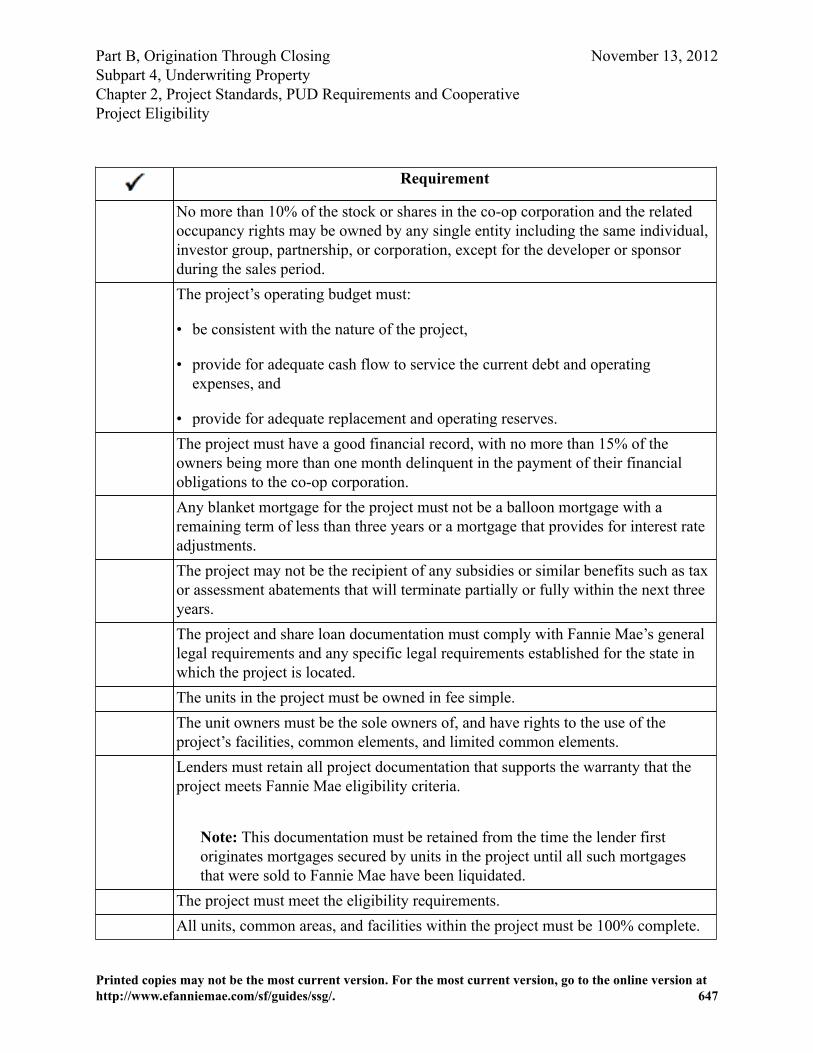

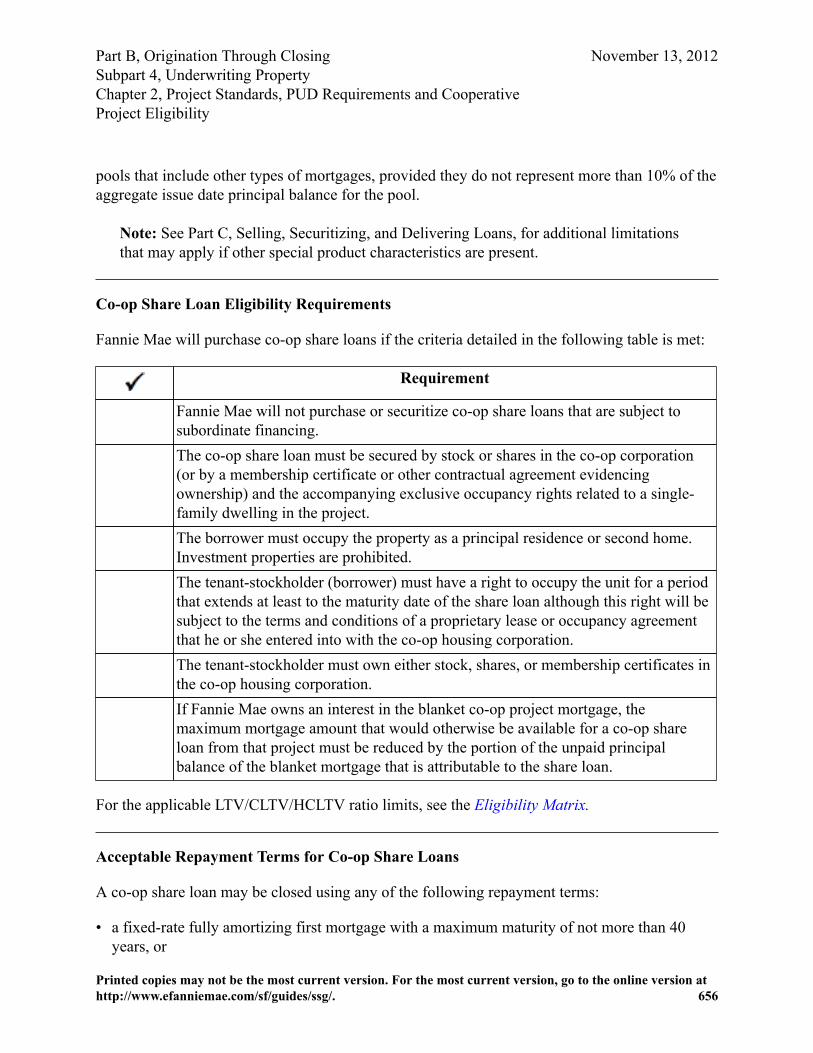

B4-2.3, PUD Requirements and Cooperative Project Eligibility . . . . . . . . . . . 642B4-2.3-01, PUD: Lender Full Review Requirements (06/28/2011) . . . . . 642B4-2.3-02, Cooperative Project Eligibility (06/28/2011) . . . . . . . . . . . . . 643B4-2.3-03, Legal Requirements for Co-op Projects (04/01/2009) . . . . . . 649B4-2.3-04, Loan Eligibility for Co-op Share Loans (03/31/2011) . . . . . . 654

Subpart B5, Unique Eligibility and Underwriting Considerations . . . . . . . . . . . . . . . . . 658B5-1, High-Balance Mortgage Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 659

B5-1.1, High-Balance Mortgage Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 660B5-1.1-01, High-Balance Mortgage Loan Eligibility and Underwriting(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 660B5-1.1-02, High-Balance Pricing, Mortgage Insurance, Special FeatureCodes, and Delivery Limitations (06/26/2012) . . . . . . . . . . . . . . . . . . . . 662

B5-2, DU-Only Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 665B5-2.1, Interest-Only Mortgages . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 666

B5-2.1-01, Mortgages with an Interest-Only Feature (08/21/2012) . . . . . 666

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xi

B5-2.1-02, Interest-Only Pricing, Mortgage Insurance and SpecialFeature Codes (12/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 669

B5-2.2, Manufactured Housing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 671B5-2.2-01, Manufactured Housing (04/01/2009) . . . . . . . . . . . . . . . . . . . 671B5-2.2-02, Manufactured Housing Loan Eligibility (07/26/2011) . . . . . . 673B5-2.2-03, Manufactured Housing Underwriting Requirements(07/26/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 677B5-2.2-04, Manufactured Housing Appraisal Requirements(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 683B5-2.2-05, Manufactured Housing Pricing, Mortgage Insurance, andSpecial Feature Code Requirements (12/30/2009) . . . . . . . . . . . . . . . . . 688B5-2.2-06, Manufactured Housing Legal Considerations (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 690

B5-3, Construction and Energy Financing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 698B5-3.1, Conversion of Construction-to-Permanent Financing . . . . . . . . . . . . . 699

B5-3.1-01, Conversion of Construction-to-Permanent Financing:Overview (01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 699B5-3.1-02, Conversion of Construction-to-Permanent Financing:Single-Closing Transactions (01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . 700B5-3.1-03, Conversion of Construction-to-Permanent Financing: Two-Closing Transactions (01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 704

B5-3.2, Homestyle Renovation Mortgage . . . . . . . . . . . . . . . . . . . . . . . . . . . . 706B5-3.2-01, HomeStyle Renovation Mortgage: Lender Eligibility(12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 706B5-3.2-02, HomeStyle Renovation Mortgages: Borrower Eligibility(12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 708B5-3.2-03, HomeStyle Renovation Mortgages: Underwriting andCollateral Considerations (03/31/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . 711B5-3.2-04, HomeStyle Renovation Mortgages: Costs and EscrowAccounts (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 714B5-3.2-05, HomeStyle Renovation Mortgages: Completion(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 716B5-3.2-06, HomeStyle Construction Contract, Construction LoanAgreement, and Lien Waiver (12/30/2009) . . . . . . . . . . . . . . . . . . . . . . . 717

B5-3.3, Mortgage Loans with Energy Improvement Features on ExistingProperties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 721

B5-3.3-01, Mortgage Loans with Energy Improvement Features onExisting Properties (03/31/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 721

B5-3.4, Property Assessed Clean Energy Loans . . . . . . . . . . . . . . . . . . . . . . . 726B5-3.4-01, Property Assessed Clean Energy Loans (12/01/2010) . . . . . . 726

B5-4, Geographic-Specific Products . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 729

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xii

B5-4-01, Texas Section 50(a)(6) Mortgages (03/29/2010) . . . . . . . . . . . . . . . 729B5-4-02, Texas Section 50(a)(6) Mortgage Eligibility (03/29/2010) . . . . . . . . 732B5-4-03, Texas Section 50(a)(6) Underwriting and Collateral Considerations(03/29/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 736B5-4-04, Texas Section 50(a)(6) Mortgage Delivery Considerations(03/29/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 738B5-4-05, Texas Section 50(a)(6) Mortgage Legal Considerations(03/29/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 739B5-4-06, Native American Conventional Lending Initiative (NACLI)(06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 741B5-4-07, Disaster-Related Limited Cash-Out Refinance Flexibilities(06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 742

B5-5, Community Seconds, Community Land Trusts, DU Refi Plus™ and RefiPlus™, and Loans with Resale Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 746

B5-5.1, Community Seconds and Community Land Trusts . . . . . . . . . . . . . . 747B5-5.1-01, Community Seconds Mortgages (10/30/2009) . . . . . . . . . . . 747B5-5.1-02, Community Seconds Loan Eligibility (08/21/2012) . . . . . . . 749B5-5.1-03, Community Seconds Delivery Considerations (06/26/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 756B5-5.1-04, Community Land Trusts (06/26/2012) . . . . . . . . . . . . . . . . . 758

B5-5.2, DU Refi Plus and Refi Plus Mortgage Loans . . . . . . . . . . . . . . . . . . . 766B5-5.2-01, DU Refi Plus and Refi Plus Eligibility (11/13/2012) . . . . . . . 766B5-5.2-02, DU Refi Plus and Refi Plus Underwriting Considerations(10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 784B5-5.2-03, DU Refi Plus and Refi Plus Property Valuation and ProjectStandards (10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 801B5-5.2-04, DU Refi Plus and Refi Plus Closing, Pricing, and Delivery(10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 807

B5-5.3, Loans with Resale Restrictions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 810B5-5.3-01, Loans With Resale Restrictions: Lender Eligibility(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 810B5-5.3-02, Loans with Resale Restrictions: Loan and BorrowerEligibility (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 812B5-5.3-03, Loans with Resale Restrictions: Underwriting and CollateralConsiderations (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 813B5-5.3-04, Loans with Resale Restrictions: Legal Considerations(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 816B5-5.3-05, Loans with Resale Restrictions: Delivery Considerations(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 817B5-5.3-06, Loans with Resale Restrictions: Pricing, Mortgage Insuranceand Special Feature Codes (06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . 818

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xiii

B5-5.3-07, Massachusetts Resale Restriction Loan EligibilityRequirements (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 819

B5-6, MyCommunityMortgage (MCM) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 821B5-6-01, MyCommunityMortgage (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . 821B5-6-02, MyCommunityMortgage Loan and Borrower Eligibility(08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 823B5-6-03, MyCommunityMortgage Underwriting Methods and Requirements(11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 828B5-6-04, MyCommunityMortgage: Additional Eligibility and UnderwritingRequirements for Community Solutions and Community HomeChoice(11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 834B5-6-05, MyCommunityMortgage Pricing, Mortgage Insurance, and SpecialFeature Codes (12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 840

Subpart B6, Government Programs Eligibility and Underwriting Requirements . . . . . . 842B6-1, Government Insured and Guaranteed Mortgages . . . . . . . . . . . . . . . . . . . . . 843

B6-1-01, General Government Mortgage Requirements (06/26/2012) . . . . . . 844B6-1-02, Eligible FHA-Insured Mortgage Loans (06/28/2011) . . . . . . . . . . . . 847B6-1-03, Eligible VA-Guaranteed Mortgages (10/30/2009) . . . . . . . . . . . . . . 849B6-1-04, Eligible HUD-Guaranteed Section 184 Mortgages (06/26/2012) . . . 850B6-1-05, Eligible RD-Guaranteed Mortgages (06/26/2012) . . . . . . . . . . . . . . 852B6-1-06, Government Mortgage Loan Guaranty or Insurance (04/01/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 853

Subpart B7, Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 854B7-1, Mortgage Insurance/Loan Guaranty . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 855

B7-1-01, Provision of Mortgage Insurance (06/26/2012) . . . . . . . . . . . . . . . . 855B7-1-02, Mortgage Insurance Coverage Requirements (06/26/2012) . . . . . . . 859B7-1-03, Lender-Purchased Mortgage Insurance (05/27/2010) . . . . . . . . . . . . 861B7-1-04, Financed Borrower-Purchased Mortgage Insurance (06/26/2012) . . 862B7-1-05, Government Mortgage Loan Guaranty or Insurance (06/26/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 866

B7-2, Title Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 869B7-2-01, Provision of Title Insurance (04/01/2009) . . . . . . . . . . . . . . . . . . . . 869B7-2-02, Title Insurer Requirements (10/02/2012) . . . . . . . . . . . . . . . . . . . . . 870B7-2-03, General Title Insurance Coverage (05/24/2011) . . . . . . . . . . . . . . . . 872B7-2-04, Special Title Insurance Coverage Considerations (06/26/2012) . . . . 874B7-2-05, Title Exceptions and Impediments(08/12/2010) . . . . . . . . . . . . . . . . 879

B7-3, Hazard and Flood Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 883B7-3-01, Hazard Insurance Policy Requirements (12/20/2011) . . . . . . . . . . . 883B7-3-02, General Hazard Insurance Coverage (06/28/2011) . . . . . . . . . . . . . . 887B7-3-03, Determining the Amount of Required Hazard Insurance Coverage(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 889

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xiv

B7-3-04, Hazard Coverage for Units in Project Developments (01/31/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 890B7-3-05, Additional Insurance Coverage (04/01/2009) . . . . . . . . . . . . . . . . . . 897B7-3-06, Evidence of Hazard Insurance (12/20/2011) . . . . . . . . . . . . . . . . . . 900B7-3-07, Flood Insurance Coverage Requirements (08/21/2012) . . . . . . . . . . 903B7-3-08, Mortgagee Clause for Hazard and Flood Insurance (05/24/2011) . . 908

B7-4, Additional Project Insurance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 911B7-4-01, Liability Insurance (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . 911B7-4-02, Fidelity Insurance (10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 912B7-4-03, Rent Loss Insurance for Co-op Projects (04/01/2009) . . . . . . . . . . . 914

Subpart B8, Closing: Legal Documents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 915B8-1, General Information on Legal Documents . . . . . . . . . . . . . . . . . . . . . . . . . . 916

B8-1-01, Publication of Legal Documents (06/28/2011) . . . . . . . . . . . . . . . . . 916B8-2, Security Instruments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 919

B8-2-01, Security Instruments for Conventional Mortgages (04/30/2010) . . . 919B8-2-02, Special-Purpose Security Instruments (04/30/2010) . . . . . . . . . . . . . 922B8-2-03, Signature Requirements for Security Instruments (04/01/2009) . . . . 926

B8-3, Notes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 927B8-3-01, Notes for Conventional Mortgages (06/26/2012) . . . . . . . . . . . . . . . 927B8-3-02, Special Note Provisions and Language Requirements (03/02/2010). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 929B8-3-03, Signature Requirements for Notes (04/01/2009) . . . . . . . . . . . . . . . 931B8-3-04, Note Endorsement (12/20/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 932

B8-4, Riders and Addenda . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 935B8-4-01, Riders and Addenda (05/27/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . 935

B8-5, Special-Purpose Legal Documents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 939B8-5-01, General Information on Special-Purpose Legal Documents(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 939B8-5-02, Inter Vivos Revocable Trusts (04/01/2009) . . . . . . . . . . . . . . . . . . . 940B8-5-03, Texas Section 50(a)(6) Mortgage Documentation (03/29/2010) . . . . 943B8-5-04, HomeStyle Mortgage Documentation Requirements (12/30/2009). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 944B8-5-05, Sample Legal Documents (01/27/2011) . . . . . . . . . . . . . . . . . . . . . . 945

B8-6, Mortgage Assignments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 948B8-6-01, General Information (04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . 948B8-6-02, Mortgage Assignment to Fannie Mae (04/01/2009) . . . . . . . . . . . . . 949B8-6-03, Authorized Use of Intervening and Blanket Assignments(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 951

B8-7, Mortgage Electronic Registration System (MERS) . . . . . . . . . . . . . . . . . . . . 954B8-7-01, Mortgage Electronic Registration Systems (MERS) (06/26/2012). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 954

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xv

Part C, Selling, Securitizing, and Delivering Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 958Subpart C1, General Information on Execution Options and Loan Delivery . . . . . . . . . 960

C1-1, Execution Options Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 961C1-1-01, Execution Options (11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . 961

C1-2, Loan Delivery Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 967C1-2-01, General Information on Delivering Loan Data and Documents(10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 968C1-2-02, Loan Data and Documentation Delivery Requirements(06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 970C1-2-03, Ownership of Mortgage Loans Prior to Purchase or Securitizationand Third-Party Security Interests (11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . 973C1-2-04, Bailee Letters (06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 975

C1-3, Loan Remittance Types Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 980C1-3-01, General Information on Remittance Types (12/30/2009) . . . . . . . . . 980

Subpart C2, Whole Loan Transactions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 983C2-1, Mandatory and Best Efforts Commitments to Sell Whole Loans . . . . . . . . . 984

C2-1.1, Mandatory Commitments to Sell Whole Loans . . . . . . . . . . . . . . . . . 985C2-1.1-01, Mandatory Commitment Process (10/30/2009) . . . . . . . . . . . 985C2-1.1-02, Pricing, Fees, and Pricing Adjustments (04/01/2009) . . . . . . 986C2-1.1-03, Mandatory Commitment Terms, Amounts, Periods andOther Requirements (06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 989C2-1.1-04, Mandatory Commitment Extensions and Pair-Offs(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 992C2-1.1-05, Servicing Fees (10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . 994C2-1.1-06, Accrued Interest Payments for Regularly AmortizingMortgages (06/28/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 995C2-1.1-07, Standard ARM and Converted ARM Resale Commitments(04/09/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 996

C2-1.2, Best Efforts Commitments to Sell Whole Loans . . . . . . . . . . . . . . . . 999C2-1.2-01, Best Efforts Commitment Process (10/25/2011) . . . . . . . . . . 999C2-1.2-02, Best Efforts Commitment Pricing, Periods, and Fees(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1000C2-1.2-03, Best Efforts Commitment Terms, Amounts, and OtherRequirements (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1002C2-1.2-04, Servicing Execution Tool in eCommitONE (10/25/2011) . . 1005

C2-2, Whole Loan Deliveries to and Purchasing by Fannie Mae . . . . . . . . . . . . . 1008C2-2-01, General Requirements for Good Delivery of Whole Loans(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1009C2-2-02, Documentation Requirements for Whole Loan Deliveries(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1012

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xvi

C2-2-03, General Information on Whole Loan Purchasing Policies(11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1014C2-2-04, Timing of Distribution of Whole Loan Purchase Proceeds(06/28/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1016C2-2-05, Whole Loan Purchasing Process (11/13/2012) . . . . . . . . . . . . . . . . 1017C2-2-06, Authorization to Transfer Funds (04/01/2009) . . . . . . . . . . . . . . . . 1020C2-2-07, Purchase Payee Codes (06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . 1022C2-2-08, Triparty Wiring Instructions (04/01/2009) . . . . . . . . . . . . . . . . . . . 1024

Subpart C3, Mortgage-Backed Securities (MBS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1027C3-1, MBS Program Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1028

C3-1-01, General Information About Fannie Mae’s MBS Program(06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1029C3-1-02, Preparing to Pool Loans into MBS (10/30/2009) . . . . . . . . . . . . . . 1033

C3-2, Entering Into an MBS Pool Purchase Contract . . . . . . . . . . . . . . . . . . . . . 1035C3-2-01, Determining Eligibility for Loans Pooled into MBS (10/25/2011). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1035C3-2-02, Establishing the Contract Amount (12/30/2009) . . . . . . . . . . . . . . 1039C3-2-03, Selecting a Servicing Option (04/01/2009) . . . . . . . . . . . . . . . . . . 1040C3-2-04, MBS Remittance Type and Selecting a Remittance Cycle(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1041C3-2-05, Obtaining a Pool Purchase Contract (11/13/2012) . . . . . . . . . . . . . 1042

C3-3, MBS Guaranty Fees and Guaranty Fee Buyups and Buydowns . . . . . . . . . 1046C3-3-01, Determining and Remitting Guaranty Fees (10/25/2011) . . . . . . . . 1046C3-3-02, Accessing Buyup and Buydown Ratios and Calculating Paymentsor Charges (11/13/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1048C3-3-03, Buying Up and Buying Down the Guaranty Fee for MBS(10/02/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1051

C3-4, Pooling Loans into Fixed-Rate MBS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1053C3-4-01, Term-Related Fixed-Rate Mortgage Pooling Parameters(10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1053C3-4-02, Commingling Fixed-Rate Mortgages in MBS (03/02/2010) . . . . . 1056

C3-5, Pooling Loans into ARM MBS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1059C3-5-01, Creating Stated-Structure ARM MBS (08/30/2011) . . . . . . . . . . . . 1060C3-5-02, Stated-Structure ARM MBS Pooling Process (04/01/2009) . . . . . . 1062C3-5-03, Creating Weighted-Average ARM MBS (04/01/2009) . . . . . . . . . . 1067C3-5-04, Calculating the Weighted-Average Pool Accrual Rates for ARMFlex Pools Using a Fixed MBS Margin (04/01/2009) . . . . . . . . . . . . . . . . . . 1068C3-5-05, Calculating the Weighted-Average Pool Accrual Rates for ARMFlex Pools Using a Weighted-Average MBS Margin (04/01/2009) . . . . . . . . 1071C3-5-06, Pooling ARMs with a Conversion Option (04/01/2009) . . . . . . . . 1074C3-5-07, Uniform Hybrid ARM MBS (04/01/2009) . . . . . . . . . . . . . . . . . . . 1076

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xvii

C3-5-08, Commingling ARMs in MBS (04/01/2009) . . . . . . . . . . . . . . . . . . 1078C3-6, Pooling Loans into Fannie Majors . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1079

C3-6-01, Parameters for Pooling Loans Into Fannie Majors (06/26/2012) . . 1079C3-7, Delivering and Trading MBS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1083

C3-7-01, Establishing an MBS Trading Account (10/25/2011) . . . . . . . . . . . 1084C3-7-02, Initiating an MBS Sale (10/25/2011) . . . . . . . . . . . . . . . . . . . . . . . 1090C3-7-03, Making Good Delivery (10/30/2009) . . . . . . . . . . . . . . . . . . . . . . . 1093C3-7-04, Delivering Data and Documents (11/13/2012) . . . . . . . . . . . . . . . . 1096C3-7-05, Confirming Presettlement Information (04/01/2009) . . . . . . . . . . . 1102C3-7-06, Settling the Trade (03/31/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . 1104C3-7-07, Sale of Fannie Mae Securities to Third Parties (04/01/2009) . . . . . 1108

Part D, Ensuring Quality Control (QC) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1112Subpart D1, Lender QC Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1113

D1-1, Lender QC Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1114D1-1-01, General Information on Lender QC Process (01/31/2012) . . . . . . . 1114D1-1-02, Lender QC Process (01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . 1116D1-1-03, Lender QC Staff and Outsourcing of the QC Process (03/29/2010). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1120

D1-2, Lender Prefunding QC Mortgage Review . . . . . . . . . . . . . . . . . . . . . . . . . . 1123D1-2-01, General Information on Lender Prefunding QC Review Process(03/29/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1123

D1-3, Lender Post-Closing QC Mortgage Review . . . . . . . . . . . . . . . . . . . . . . . . 1127D1-3-01, General Information on Lender Post-Closing QC Review Process(03/29/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1127D1-3-02, Lender Mortgage Selection Process for Post-Closing QC MortgageReviews (01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1128D1-3-03, Lender Post-Closing QC Review of Underwriting Decisions andDocumentation (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1131D1-3-04, Lender Post-Closing QC Review of Data Integrity (01/31/2012) . . 1135D1-3-05, Lender Post-Closing QC Review of Appraisers and Appraisals(12/01/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1137D1-3-06, Lender Post-Closing QC Review of Closing Documents(01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1139D1-3-07, Lender Post-QC Review Reporting, Record Retention, and Audit(01/31/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1143

Subpart D2, Fannie Mae QC Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1146D2-1, General Information on Fannie Mae QC Process . . . . . . . . . . . . . . . . . . . . 1147

D2-1-01, General Information on Fannie Mae QC Reviews (04/01/2009) . . 1147D2-1-02, Fannie Mae QC File Request and Submission Requirements(03/29/2010) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1148D2-1-03, Fannie Mae QC Report of Findings (04/01/2009) . . . . . . . . . . . . . 1149

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xviii

D2-1-04, Rebuttal of Fannie Mae QC Review Decisions (04/01/2009) . . . . 1150Part E, Quick Reference Materials . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1151

E-1, Selling Guide Resources . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1152E-1-01, References to eFannieMae.com (08/21/2012) . . . . . . . . . . . . . . . . . . . . . 1152E-1-02, Acronyms and Abbreviations (08/21/2012) . . . . . . . . . . . . . . . . . . . . . . . 1154E-1-03, List of Contacts (02/28/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1157E-1-04, List of Lender Contracts (06/26/2012) . . . . . . . . . . . . . . . . . . . . . . . . . . . 1162

E-2, Exhibits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1165E-2-01, Borrower’s Authorization for Counseling (04/01/2009) . . . . . . . . . . . . . . 1165E-2-02, Document Submission Packages for All Mortgages (12/20/2011) . . . . . . 1166E-2-03, Suggested Format for Phase I Environmental Hazard Assessments(06/28/2011) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1169E-2-04, Master Agreement Terms and Conditions (08/21/2012) . . . . . . . . . . . . . . 1178E-2-05, Revocable Trust Rider (Sample Language) (04/01/2009) . . . . . . . . . . . . 1184E-2-06, Signature Requirements for Mortgages to Inter Vivos Revocable Trusts(04/01/2009) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1186E-2-07, Post-Closing Mortgage Loan File Documentation (11/13/2012) . . . . . . . 1188

E-3, Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1192E-3-01, Glossary of Fannie Mae Terms: A (01/31/2012) . . . . . . . . . . . . . . . . . . . 1193E-3-02, Glossary of Fannie Mae Terms: B (12/30/2009) . . . . . . . . . . . . . . . . . . . 1196E-3-03, Glossary of Fannie Mae Terms: C (03/31/2011) . . . . . . . . . . . . . . . . . . . 1199E-3-04, Glossary of Fannie Mae Terms: D (01/31/2012) . . . . . . . . . . . . . . . . . . . 1205E-3-05, Glossary of Fannie Mae Terms: E (06/28/2011) . . . . . . . . . . . . . . . . . . . 1208E-3-06, Glossary of Fannie Mae Terms: F (08/21/2012) . . . . . . . . . . . . . . . . . . . 1211E-3-07, Glossary of Fannie Mae Terms: G (04/01/2009) . . . . . . . . . . . . . . . . . . . 1216E-3-08, Glossary of Fannie Mae Terms: H (06/28/2011) . . . . . . . . . . . . . . . . . . . 1217E-3-09, Glossary of Fannie Mae Terms: I (04/01/2009) . . . . . . . . . . . . . . . . . . . . 1219E-3-10, Glossary of Fannie Mae Terms: J (04/01/2009) . . . . . . . . . . . . . . . . . . . . 1222E-3-11, Glossary of Fannie Mae Terms: K (10/02/2012) . . . . . . . . . . . . . . . . . . . 1222E-3-12, Glossary of Fannie Mae Terms: L (10/02/2012) . . . . . . . . . . . . . . . . . . . 1223E-3-13, Glossary of Fannie Mae Terms: M (06/26/2012) . . . . . . . . . . . . . . . . . . . 1225E-3-14, Glossary of Fannie Mae Terms: N (06/28/2011) . . . . . . . . . . . . . . . . . . . 1233E-3-15, Glossary of Fannie Mae Terms: O (08/21/2012) . . . . . . . . . . . . . . . . . . . 1234E-3-16, Glossary of Fannie Mae Terms: P (12/01/2010) . . . . . . . . . . . . . . . . . . . 1235E-3-17, Glossary of Fannie Mae Terms: Q (04/01/2009) . . . . . . . . . . . . . . . . . . . 1239E-3-18, Glossary of Fannie Mae Terms: R (06/28/2011) . . . . . . . . . . . . . . . . . . . 1240E-3-19, Glossary of Fannie Mae Terms: S (01/27/2011) . . . . . . . . . . . . . . . . . . . . 1244E-3-20, Glossary of Fannie Mae Terms: T (10/25/2011) . . . . . . . . . . . . . . . . . . . 1249E-3-21, Glossary of Fannie Mae Terms: U (04/01/2009) . . . . . . . . . . . . . . . . . . . 1251E-3-22, Glossary of Fannie Mae Terms: V (04/01/2009) . . . . . . . . . . . . . . . . . . . 1251E-3-23, Glossary of Fannie Mae Terms: W (12/20/2011) . . . . . . . . . . . . . . . . . . . 1252

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xix

E-3-24, Glossary of Fannie Mae Terms: X (04/01/2009) . . . . . . . . . . . . . . . . . . . 1252E-3-25, Glossary of Fannie Mae Terms: Y (04/01/2009) . . . . . . . . . . . . . . . . . . . 1253E-3-26, Glossary of Fannie Mae Terms: Z (04/01/2009) . . . . . . . . . . . . . . . . . . . 1253

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xx

PrefaceContent Organization

The Selling Guide is organized into parts that reflect how lenders generally categorize variousaspects of their business relationship with Fannie Mae:

Part A, Doing Business with Fannie Mae Subpart 1: Approval Qualification Subpart 2: Lender Contract Subpart 3: Getting Started With Fannie Mae Subpart 4: Maintaining Lender Eligibility

Part B, Originating through Closing Subpart 1: Loan Application Package Subpart 2: Eligibility Subpart 3: Underwriting Borrowers Subpart 4: Underwriting Property Subpart 5: Unique Eligibility and Underwriting Considerations Subpart 6: Government Programs Eligibility and Underwriting Requirements Subpart 7: Insurance Subpart 8: Closing: Legal Documents

Part C, Selling, Securitizing, and Delivering Loans Subpart 1: General Information on Execution Options and Loan Delivery Subpart 2: Whole Loan Transactions Subpart 3: Mortgage-Backed Securities (MBS)

Part D, Ensuring Quality Control Subpart 1: Lender QC Process Subpart 2: Fannie Mae QC Process

Part E, Quick Reference Materials

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xxi

Chapter 1: Selling Guide Resources Chapter 2: Exhibits Chapter 3: Glossary

Part A through Part D are structured hierarchically—by subpart, chapter, section, and topic—tostate Fannie Mae requirements logically and with increasing levels of detail, so that readers canquickly locate a subject of interest and find desired content. Part E includes a variety of supportcomponents—including Selling Guide Resources, Exhibits, and Glossary.

The Table of Contents provides additional details on the content. To learn more about the contentincluded in a particular part and how content in that part is organized, see the Introductionprovided at the beginning of the part.

Use of the Numbering System to Identify Levels of Content

The numbering system used to identify the levels of detail of the content contained within thisSelling Guide can help you to navigate the Guide more easily and to recognize where a particulartopic is contained within the content hierarchy.

Consider the numbering system identifier for the topic “Personal Gifts”:

B2-5.3.2-01 Personal Gifts

If you know that each:

Part has a corresponding Letter (uppercase beginning with A)Subpart has a corresponding Numeral (one-digit beginning with 1)Chapter has a corresponding Numeral (one-digit beginning with 1)

Section Level has a corresponding Numeral (one-digit beginning with 1)Topic has a corresponding Numeral (two-digit beginning with 01)

Then you can use the numbering system identifier (“B2-5.3.2-01”) to map the location and levelof content detail of this topic within the Selling Guide.

For example, here is how the numbering system identifier for this topic maps to the contentlevels:

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xxii

As shown above, the part and subpart are combined as B2-. The chapter, section, and level arecombined as 5.3.2-. And the topic is added as 01.

Keep in mind that not all parts have subparts, not all chapters have sections, and not all sectionshave topics. For example, the topic “Obtaining a Master Agreement” has the numbering systemidentifier “A2-7-04” (which does not include sections or levels):

Note: As topics are added, updated and deleted with each publication of the SellingGuide, the chapters, sections and topic identifiers will change accordingly (For example,B2-5.3.2-01 Personal Gifts).

Use of Icons to Identify Types of Content

The online and PDF versions of this Selling Guide use various icons to help you quickly identifythe type of content:

Icon DescriptionOverview topics provide the logic behind the arrangement of a part, subpart, orchapter.

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xxiii

Icon DescriptionPolicy topics instruct you about what must or must not be done (for example, lawsand rules).

Process and Procedure topics present actions that must be followed over time or thatmust be performed in a particular instance.

Supporting Information topics present concepts, facts, structures, or backgroundinformation that corroborate or expand upon a topic.

Glossary topics present key terms and their definitions.

Terms and General Conventions

Lenders may contract to sell mortgages to Fannie Mae using either of the two following deliverymethods. (Fannie Mae acquires title to the mortgages in both types of transactions.)

• As whole mortgage loans — when the lender contracts to sell mortgages to Fannie Mae aswhole mortgages (to hold in our portfolio or to include later in MBS pools that we form). Weremit cash proceeds to the lender in payment of the purchase price for these mortgages.

• As MBS mortgage loans — when the lender contracts to sell mortgages to us that we conveyto an MBS trust under the terms of our MBS program, and we deliver to the lender (or itsdesignee) mortgage pass-through certificates representing interests in the mortgages. Thesepass-through certificates are in payment of the purchase price for the mortgages.

The term “delivery” is used in this Selling Guide to refer to whole mortgage loans and to MBSpools. In cases where specific requirements apply to one type of transaction, we specify thedelivery method.

Also, for the sake of brevity, the term “loan” is used to mean “mortgage loan” unless specifiedotherwise.

The glossary provides definitions of all terms used in connection with Fannie Mae requirements.

Amendments to the Guide

Fannie Mae may at any time alter or waive any of the requirements of this Selling Guide, imposeother additional requirements, or rescind or amend any and all material set forth in this SellingGuide. The lender must make sure that its staff is thoroughly familiar with the content andrequirements of this Selling Guide, as it now exists and as it may be changed from time to time.

November 13, 2012

Printed copies may not be the most current version. For the most current version, go to the online version athttp://www.efanniemae.com/sf/guides/ssg/. xxiv

Notification of Changes and Updates

Fannie Mae notifies lenders of changes and updates to our Selling Guide policies and procedures—as communicated in Announcements, Notices and Lender Letters—in two ways:

• By posting the documents on eFannieMae.com and the AllRegs website.

• By email notification of these postings to lenders that subscribe to Fannie Mae’s emailsubscription service and select the option “Selling News.”

Fannie Mae does not mail printed copies of Selling Guide updates, announcements, noticesor lender letters. Lenders that want printed copies may download and print PDF files of thedocuments posted on eFannieMae.com.

Contents of the Selling Guide