sez case studies

TRANSCRIPT

SEZ case studies7th Working Group Meeting on Investment Zones in Iraq

Anders Jönsson, Southeast Asia Division, GRSMike Pfister, Investment Division, DAFParis, France17 February 2015

Disclaimer

This presentation is not a result of OECD research and represents the insights and opinions of the presenters only.

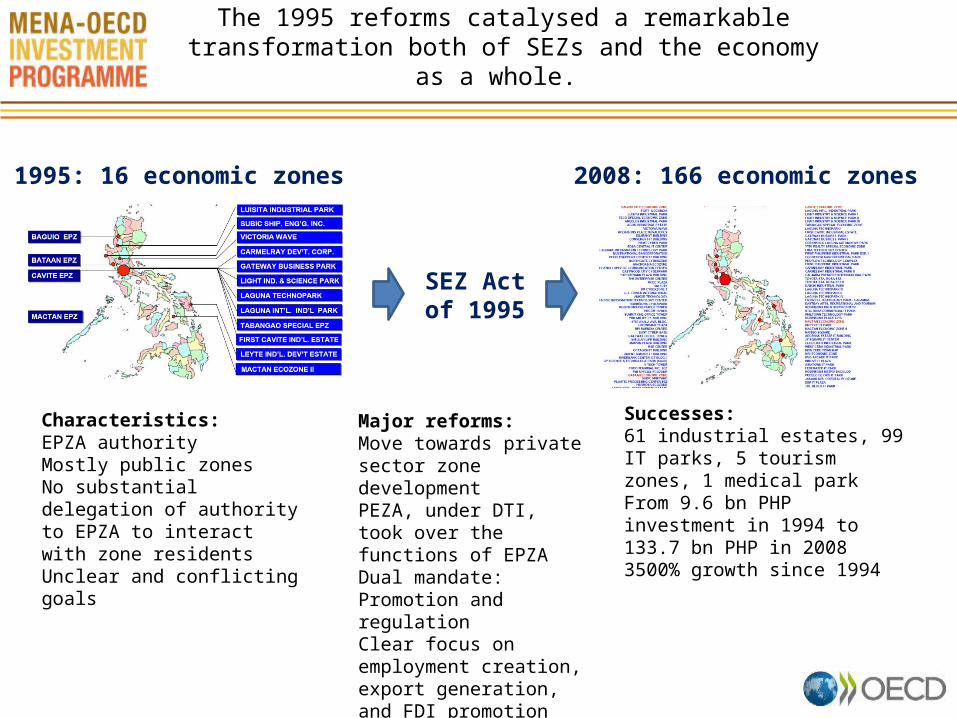

The 1995 reforms catalysed a remarkable transformation both of SEZs and the economy as a whole.

1995: 16 economic zones

Characteristics: EPZA authorityMostly public zonesNo substantial delegation of authority to EPZA to interact with zone residentsUnclear and conflicting goals

SEZ Act of 1995

Major reforms:Move towards private sector zone developmentPEZA, under DTI, took over the functions of EPZADual mandate: Promotion and regulationClear focus on employment creation, export generation, and FDI promotion

2008: 166 economic zones

Successes:61 industrial estates, 99 IT parks, 5 tourism zones, 1 medical parkFrom 9.6 bn PHP investment in 1994 to 133.7 bn PHP in 20083500% growth since 1994

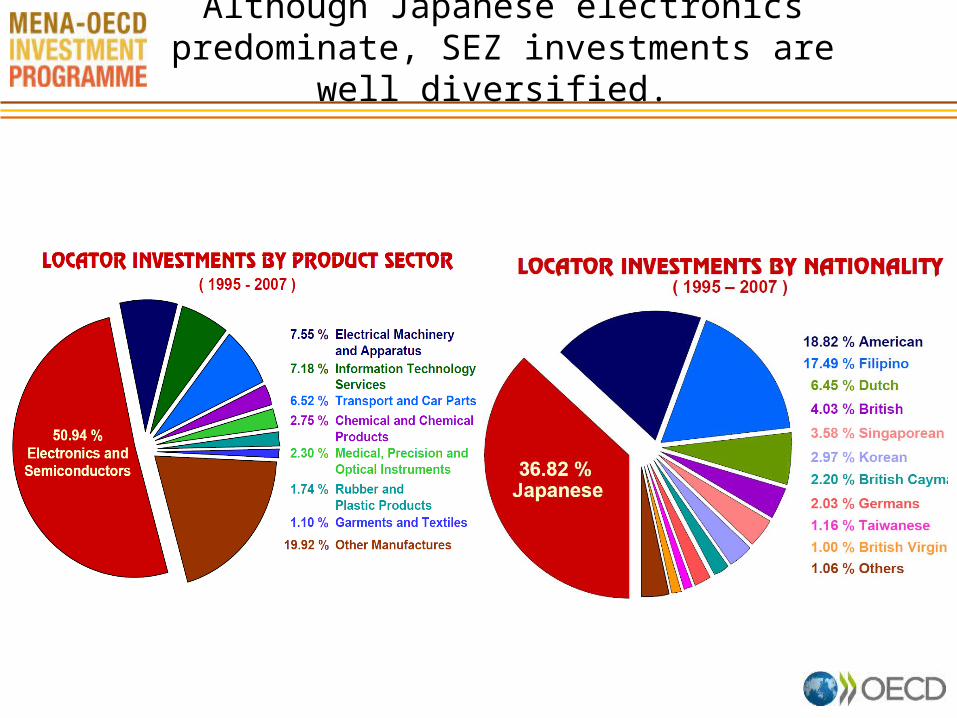

Although Japanese electronics predominate, SEZ investments are well diversified.

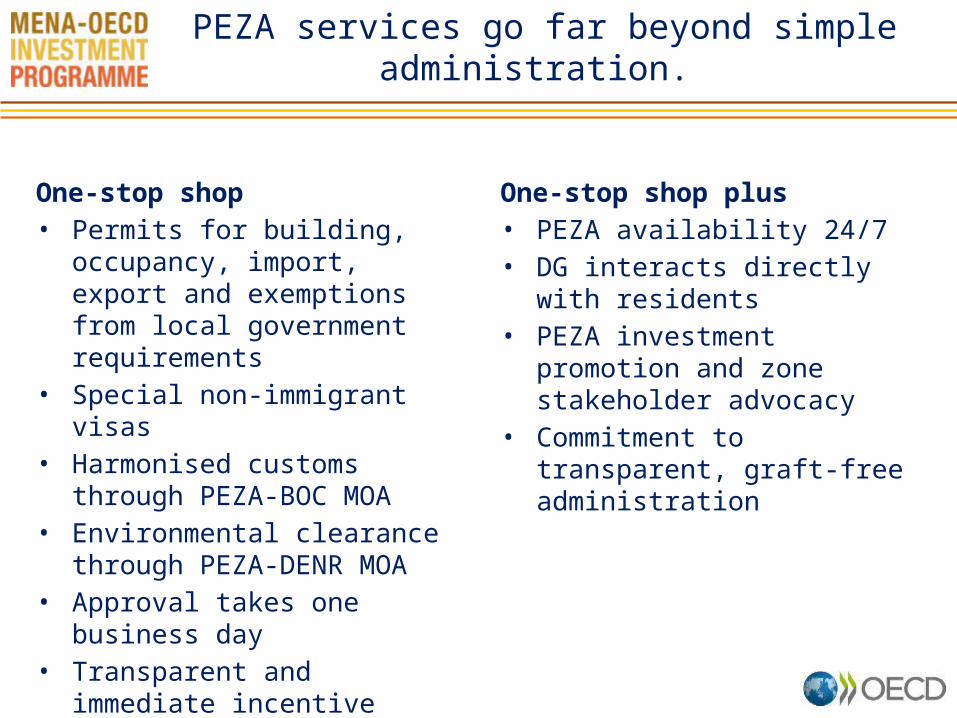

One-stop shop• Permits for building, occupancy,

import, export and exemptions from local government requirements

• Special non-immigrant visas• Harmonised customs through

PEZA-BOC MOA• Environmental clearance through

PEZA-DENR MOA• Approval takes one business day• Transparent and immediate

incentive allocation

One-stop shop plus• PEZA availability 24/7• DG interacts directly with residents• PEZA investment promotion and

zone stakeholder advocacy• Commitment to transparent, graft-

free administration

PEZA services go far beyond simple administration.

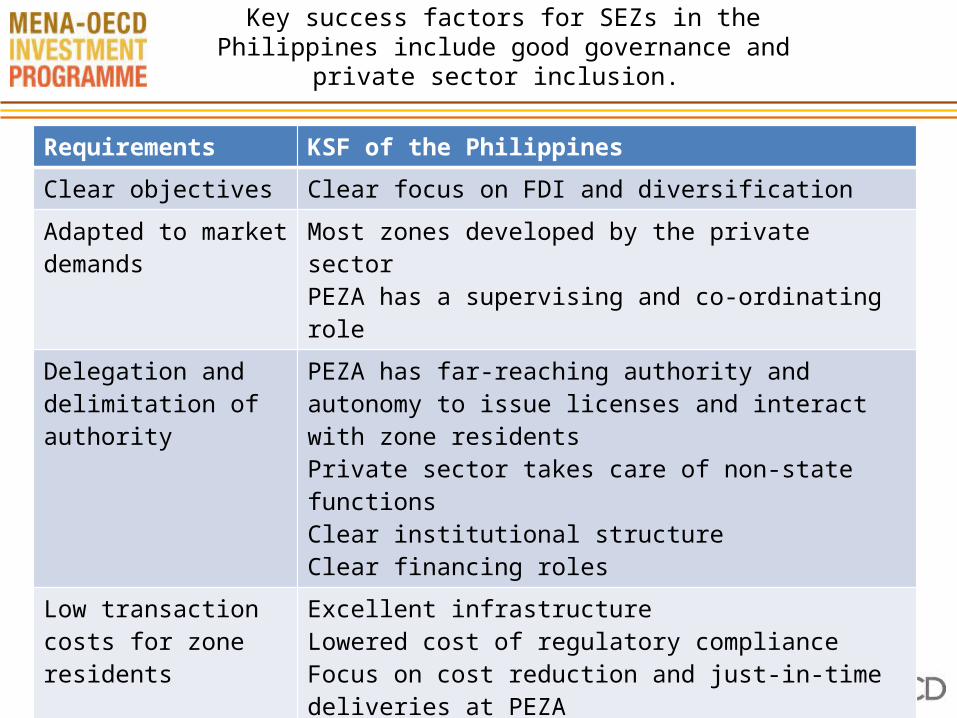

Key success factors for SEZs in the Philippines include good governance and private sector inclusion.

Requirements KSF of the Philippines

Clear objectives Clear focus on FDI and diversification

Adapted to market demands

Most zones developed by the private sectorPEZA has a supervising and co-ordinating role

Delegation and delimitation of authority

PEZA has far-reaching authority and autonomy to issue licenses and interact with zone residentsPrivate sector takes care of non-state functionsClear institutional structureClear financing roles

Low transaction costs for zone residents

Excellent infrastructureLowered cost of regulatory complianceFocus on cost reduction and just-in-time deliveries at PEZA

Access to labour Availability of skilled labourStaff training support through PEZA

Efficient promotion PEZA promotes zones overall, and private operators promote specific opportunities

Strong political support SEZs have a strong role in all national economic planning instruments.

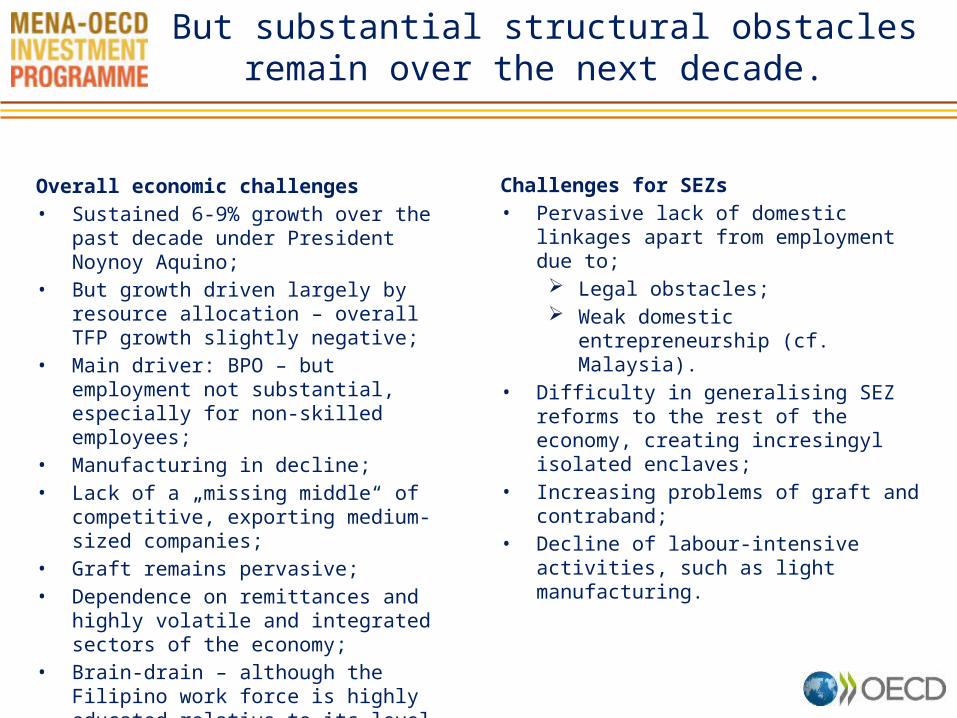

Overall economic challenges• Sustained 6-9% growth over the past decade

under President Noynoy Aquino; • But growth driven largely by resource

allocation – overall TFP growth slightly negative;

• Main driver: BPO – but employment not substantial, especially for non-skilled employees;

• Manufacturing in decline; • Lack of a „missing middle“ of competitive,

exporting medium-sized companies; • Graft remains pervasive; • Dependence on remittances and highly volatile

and integrated sectors of the economy; • Brain-drain – although the Filipino work force

is highly educated relative to its level of economic development, many opt to seek employment abroad.

Challenges for SEZs• Pervasive lack of domestic linkages apart from

employment due to; Legal obstacles; Weak domestic entrepreneurship (cf.

Malaysia).• Difficulty in generalising SEZ reforms to the rest

of the economy, creating incresingyl isolated enclaves;

• Increasing problems of graft and contraband; • Decline of labour-intensive activities, such as

light manufacturing.

But substantial structural obstacles remain over the next decade.