sgh ice momentum - equity trustees/media/equitytrustees/files/cts/... · 2015. 10. 27. · fy 2009...

TRANSCRIPT

1

SGH ICE – Momentum

* *** **

Callum Burns – Founder & Portfolio Manager

October 2015

SGH ICE

“Investing in more Certain Earnings growth”

3

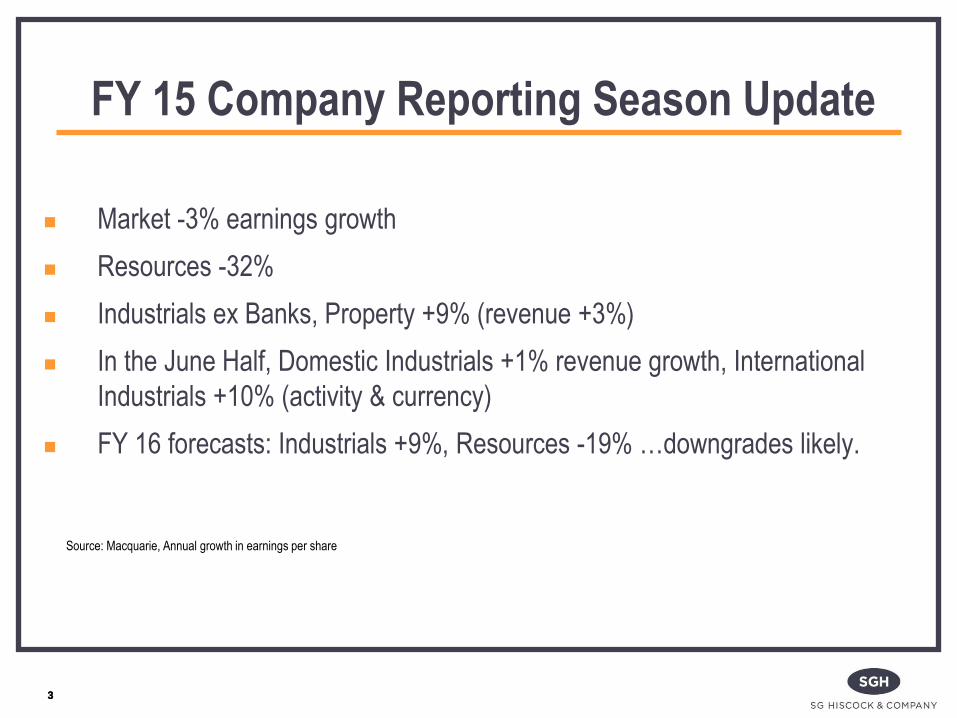

FY 15 Company Reporting Season Update

Market -3% earnings growth

Resources -32%

Industrials ex Banks, Property +9% (revenue +3%)

In the June Half, Domestic Industrials +1% revenue growth, International

Industrials +10% (activity & currency)

FY 16 forecasts: Industrials +9%, Resources -19% …downgrades likely.

3

Source: Macquarie, Annual growth in earnings per share

4 4

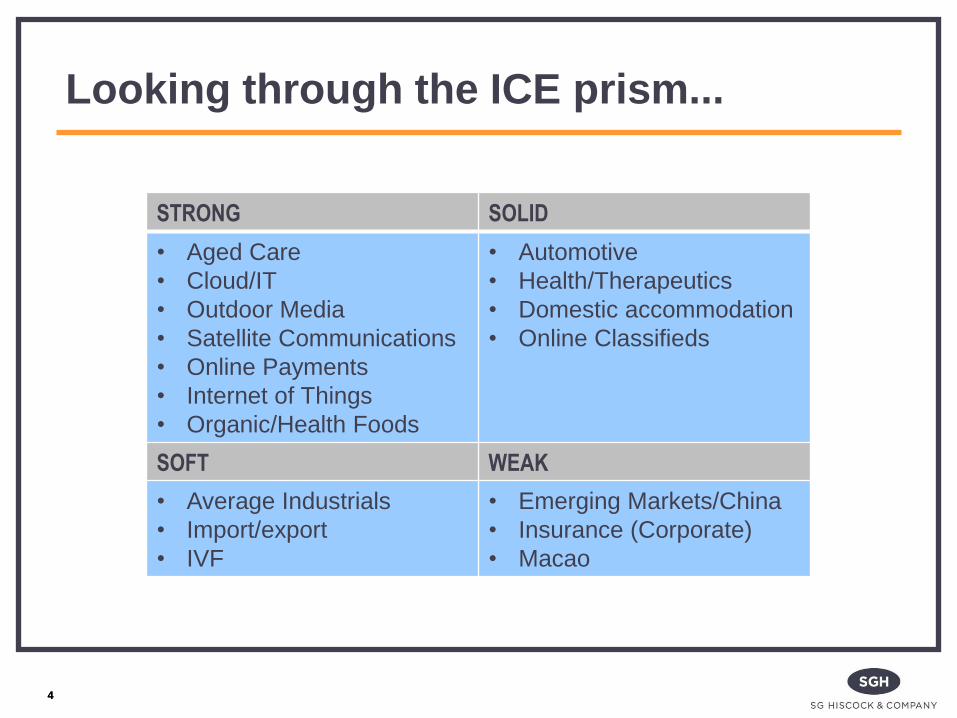

STRONG SOLID

• Aged Care

• Cloud/IT

• Outdoor Media

• Satellite Communications

• Online Payments

• Internet of Things

• Organic/Health Foods

• Automotive

• Health/Therapeutics

• Domestic accommodation

• Online Classifieds

SOFT WEAK

• Average Industrials

• Import/export

• IVF

• Emerging Markets/China

• Insurance (Corporate)

• Macao

Looking through the ICE prism...

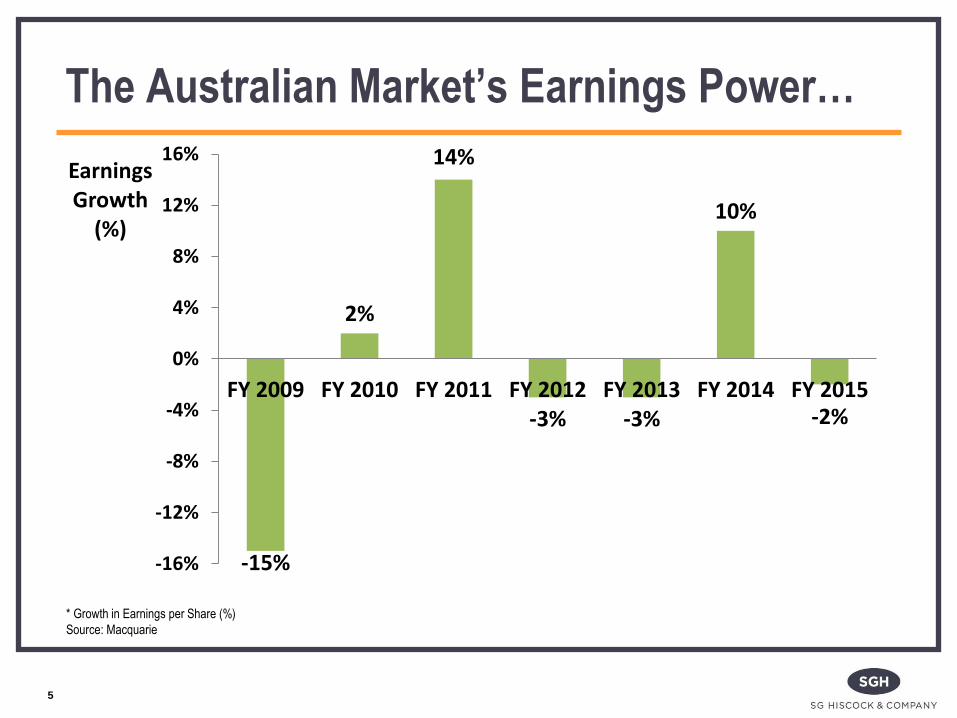

The Australian Market’s Earnings Power…

5

* Growth in Earnings per Share (%)

Source: Macquarie

-15%

2%

14%

-3% -3%

10%

-2%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

Earnings Growth

(%)

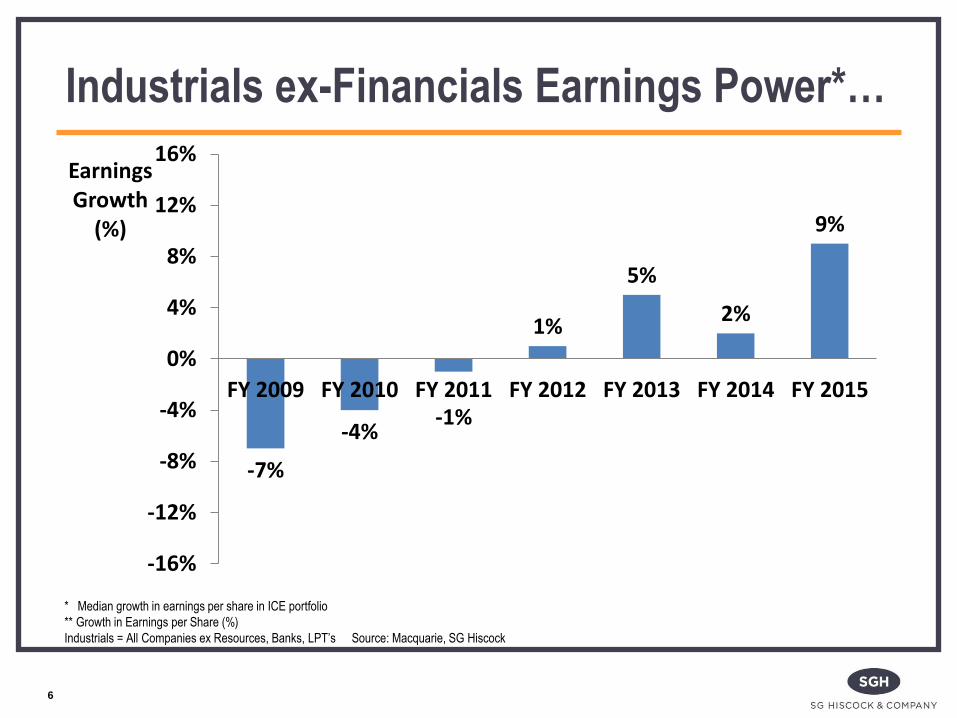

Industrials ex-Financials Earnings Power*…

6

* Median growth in earnings per share in ICE portfolio

** Growth in Earnings per Share (%)

Industrials = All Companies ex Resources, Banks, LPT’s Source: Macquarie, SG Hiscock

-7%

-4% -1%

1%

5%

2%

9%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

Earnings Growth

(%)

7

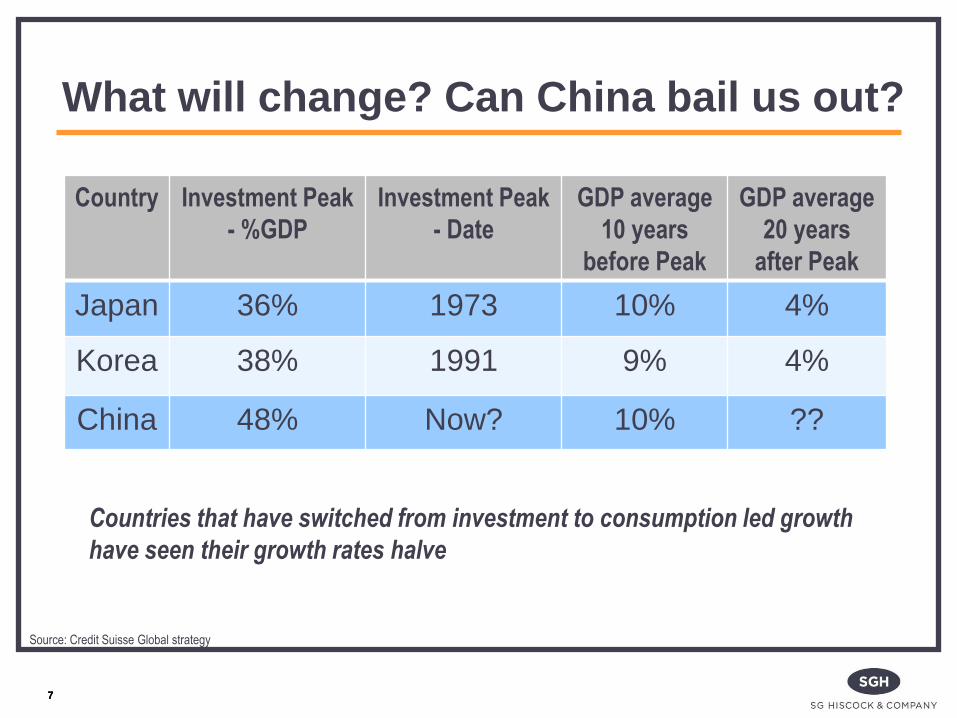

What will change? Can China bail us out?

7

Country Investment Peak

- %GDP

Investment Peak

- Date

GDP average

10 years

before Peak

GDP average

20 years

after Peak

Japan 36% 1973 10% 4%

Korea 38% 1991 9% 4%

China 48% Now? 10% ??

Countries that have switched from investment to consumption led growth

have seen their growth rates halve

Source: Credit Suisse Global strategy

8

Can China bail us out? No-one knows…

8

No-one knows…it may but

is it wise to rely on it?

9

So has earnings growth disappeared?

There is very limited growth in revenue in the Big Caps

Need to go outside the top 100 to get growth

The days of index plus investing are gone

Investors want the growth but are concerned about volatility

A difficult dilemma for advisors

Anti depressant pill – remember the charts relate to the overall market,

dominated by a relatively small number of big caps

We only need to find 40 (out of 1500) good companies at the right price

9

10

SGH ICE

Invests in ASX Industrial Franchises – Established & Emerging

Predominantly Mid to Small Cap Industrials = SAFE END OF SMALL CAPS

Typically 40 stocks, current max position 3% = normal

Size $240 million

10

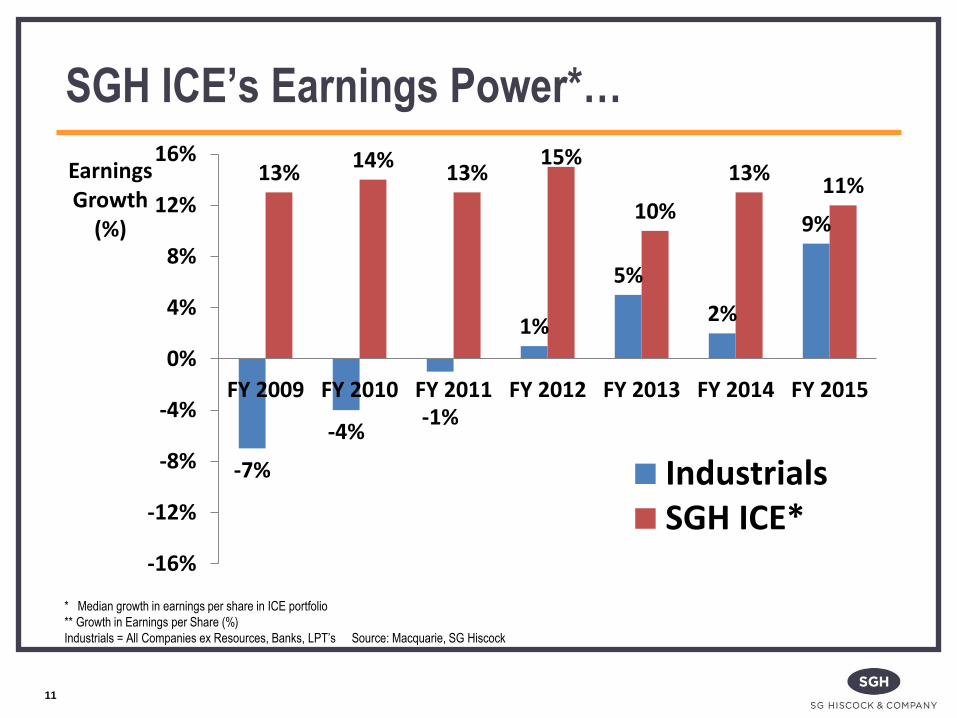

SGH ICE’s Earnings Power*…

11

* Median growth in earnings per share in ICE portfolio

** Growth in Earnings per Share (%)

Industrials = All Companies ex Resources, Banks, LPT’s Source: Macquarie, SG Hiscock

-7%

-4% -1%

1%

5%

2%

9%

13% 14%

13% 15%

10%

13% 11%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

16%

FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015

Earnings Growth

(%)

IndustrialsSGH ICE*

=EARNINGS POWER

12

SGH ICE Business Franchise

What is a mature Franchise?

FEATURES

A QUALITY business with SUSTAINABLE GROWTH

Possesses a sustainable competitive advantage

Barriers to entry for competitors

Typically owns/uses assets that are difficult to replicate

Hard for clients to change = an entrenched market position

Often has pricing power

Has a moat around the business

BENEFITS

More certain earnings growth

Superior shareholder returns

13

“Investing in more Certain Earnings growth”

14

Examples of franchises

14

Investment Decision Process

16

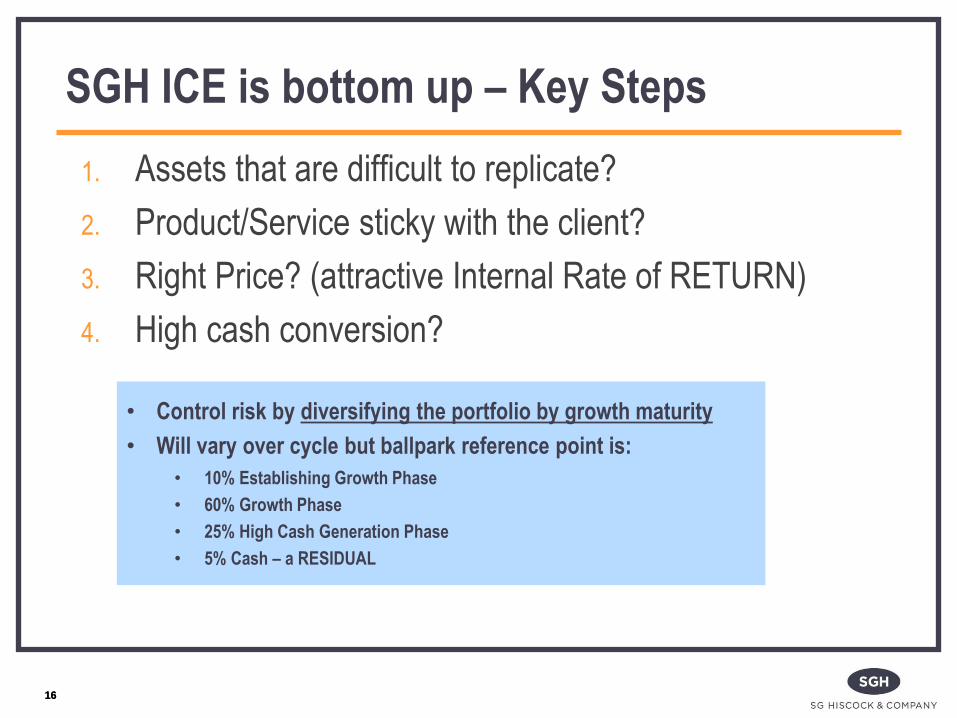

SGH ICE is bottom up – Key Steps

1. Assets that are difficult to replicate?

2. Product/Service sticky with the client?

3. Right Price? (attractive Internal Rate of RETURN)

4. High cash conversion?

• Control risk by diversifying the portfolio by growth maturity

• Will vary over cycle but ballpark reference point is:

• 10% Establishing Growth Phase

• 60% Growth Phase

• 25% High Cash Generation Phase

• 5% Cash – a RESIDUAL

16

17

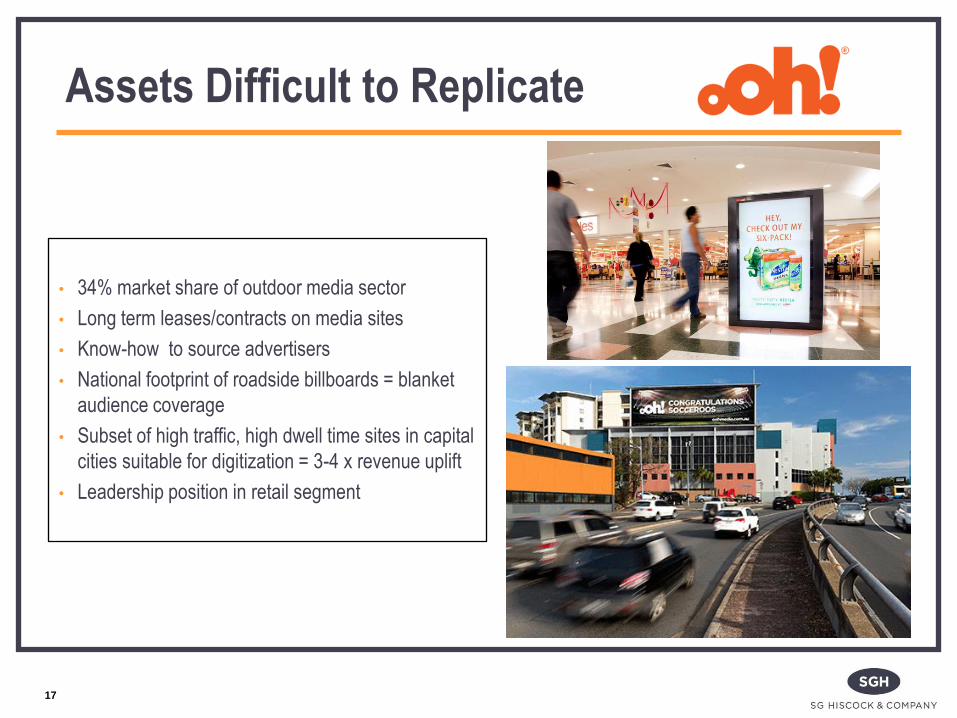

• 34% market share of outdoor media sector

• Long term leases/contracts on media sites

• Know-how to source advertisers

• National footprint of roadside billboards = blanket

audience coverage

• Subset of high traffic, high dwell time sites in capital

cities suitable for digitization = 3-4 x revenue uplift

• Leadership position in retail segment

Assets Difficult to Replicate

• Outdoor now one of the only categories of media

with broad/national audience reach

• Digitisation of outdoor allows the advertiser to more

effectively reach its audience

• If you want that location you have to deal withOoh

* As at 28 September 2015

18

Sticky Customers

• IRR Valuation = 11 -14%

• Digital conversions offer 3-4x revenue uplifts,

rents not kept pace yet.

19

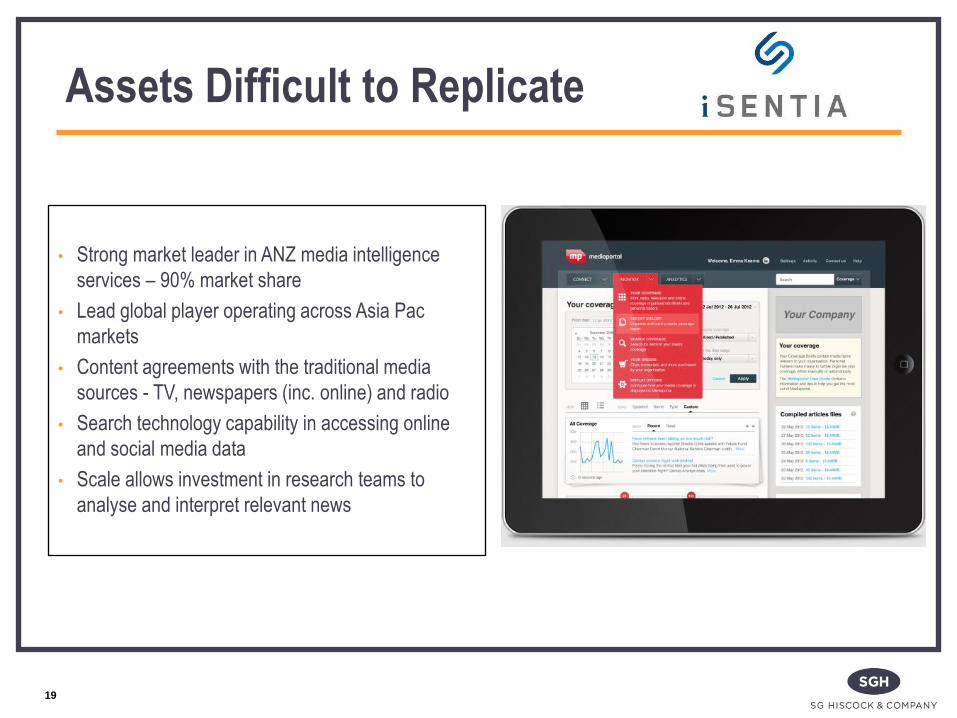

• Strong market leader in ANZ media intelligence

services – 90% market share

• Lead global player operating across Asia Pac

markets

• Content agreements with the traditional media

sources - TV, newspapers (inc. online) and radio

• Search technology capability in accessing online

and social media data

• Scale allows investment in research teams to

analyse and interpret relevant news

Assets Difficult to Replicate

• Keep the corporate client across ‘trending’ news far

more efficiently than the corporate could achieve in

house

• In Australia no real alternative

• Potential entrants would need to invest in content

deals and technology well ahead of signing customers

• Mediaportal adds additional layer of stickiness once

client converted to the platform…

• …client habit = hard to change

• IRR Valuation = 10 -13%

• Asia and ‘Value Added Services’ a growth opportunity

* As at 28 September 2015

20

Sticky Customers

21

• Leading aged care industry consolidator

• Quality of care – evidenced by leading proportion of

facilities with single rooms

• Locations are key:

• Residents tend to move from within a 5km

radius of their home

• Government licenses in local areas

• Access to land/sites

• Scale drives efficiency and expertise

Assets Difficult to Replicate

• Residents choose an operator based on location

and quality of care

• Aged care facilities run at high occupancy rates –

once moved in, residents stay for their full tenure

* As at 28 September 2015

22

Sticky Customers

• IRR Valuation = 12 -15%

• Bonding scheme a source of strong cash flow for

investment in growth (including acquisitions)

23

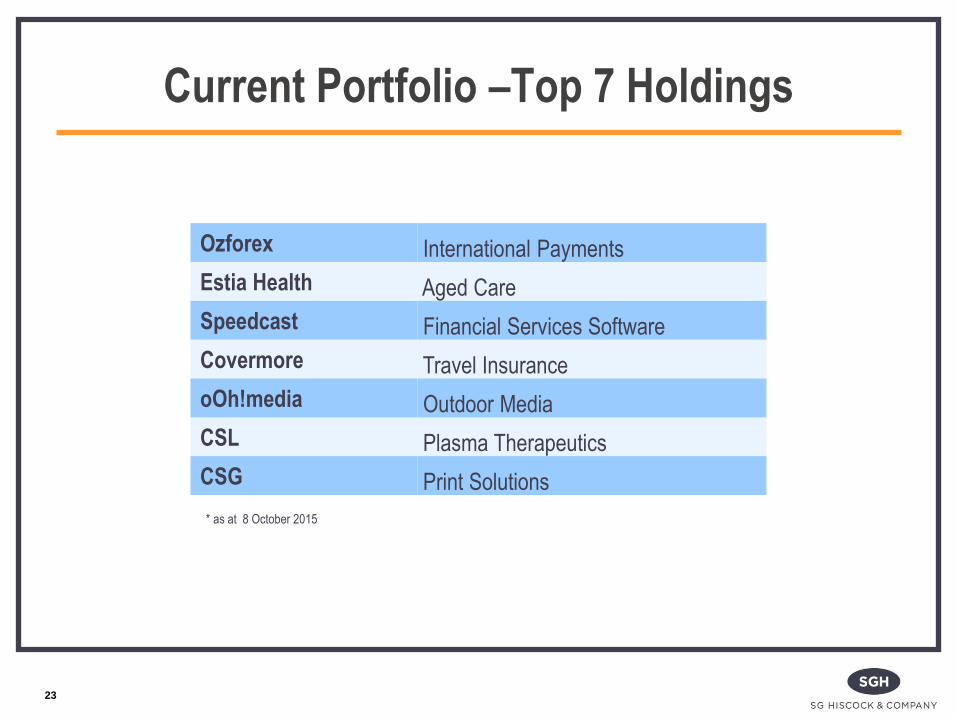

Current Portfolio –Top 7 Holdings

Ozforex International Payments

Estia Health Aged Care

Speedcast Financial Services Software

Covermore Travel Insurance

oOh!media Outdoor Media

CSL Plasma Therapeutics

CSG Print Solutions

* as at 8 October 2015

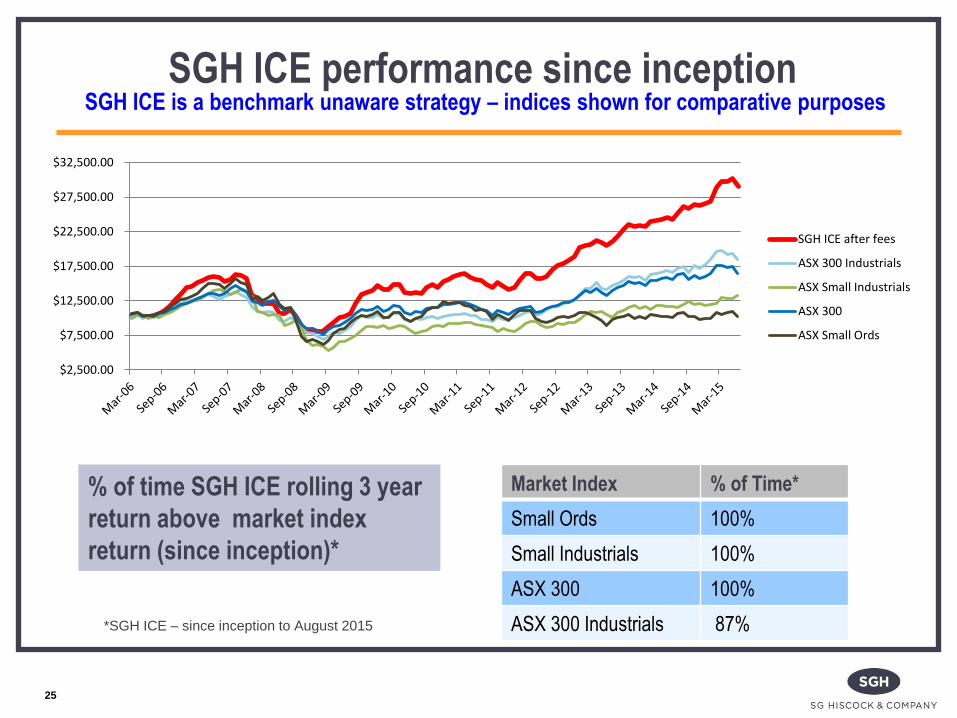

Performance

SGH ICE performance since inception SGH ICE is a benchmark unaware strategy – indices shown for comparative purposes

*SGH ICE – since inception to August 2015

25

$2,500.00

$7,500.00

$12,500.00

$17,500.00

$22,500.00

$27,500.00

$32,500.00

SGH ICE after fees

ASX 300 Industrials

ASX Small Industrials

ASX 300

ASX Small Ords

% of time SGH ICE rolling 3 year

return above market index

return (since inception)*

Market Index % of Time*

Small Ords 100%

Small Industrials 100%

ASX 300 100%

ASX 300 Industrials 87%

26

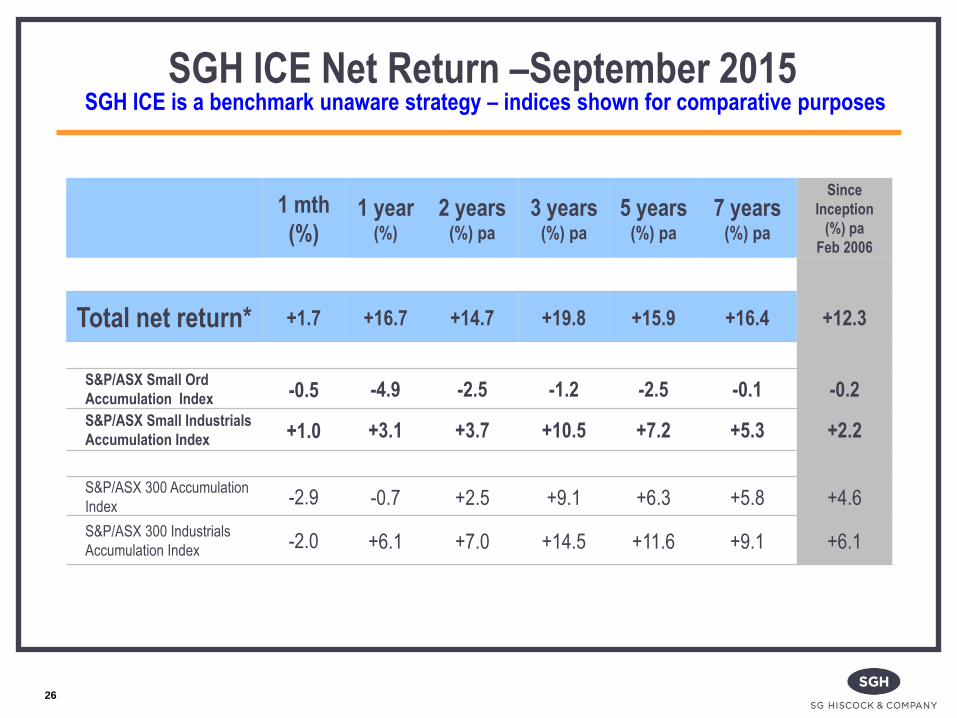

1 mth

(%) 1 year

(%)

2 years (%) pa

3 years (%) pa

5 years (%) pa

7 years (%) pa

Since

Inception

(%) pa

Feb 2006

Total net return* +1.7 +16.7 +14.7 +19.8 +15.9 +16.4 +12.3

S&P/ASX Small Ord

Accumulation Index -0.5 -4.9 -2.5 -1.2 -2.5 -0.1 -0.2

S&P/ASX Small Industrials

Accumulation Index +1.0 +3.1 +3.7 +10.5 +7.2 +5.3 +2.2

S&P/ASX 300 Accumulation

Index -2.9 -0.7 +2.5 +9.1 +6.3 +5.8 +4.6

S&P/ASX 300 Industrials

Accumulation Index -2.0 +6.1 +7.0 +14.5 +11.6 +9.1 +6.1

SGH ICE Net Return –September 2015 SGH ICE is a benchmark unaware strategy – indices shown for comparative purposes

Relative

Performance* vs

1 mth (%)

1 year (%)

2 years (%) pa

3 years (%) pa

5 years (%) pa

7 years (%) pa

Since Inception

(%) pa

Feb 2006

S&P/ASX Small Ord

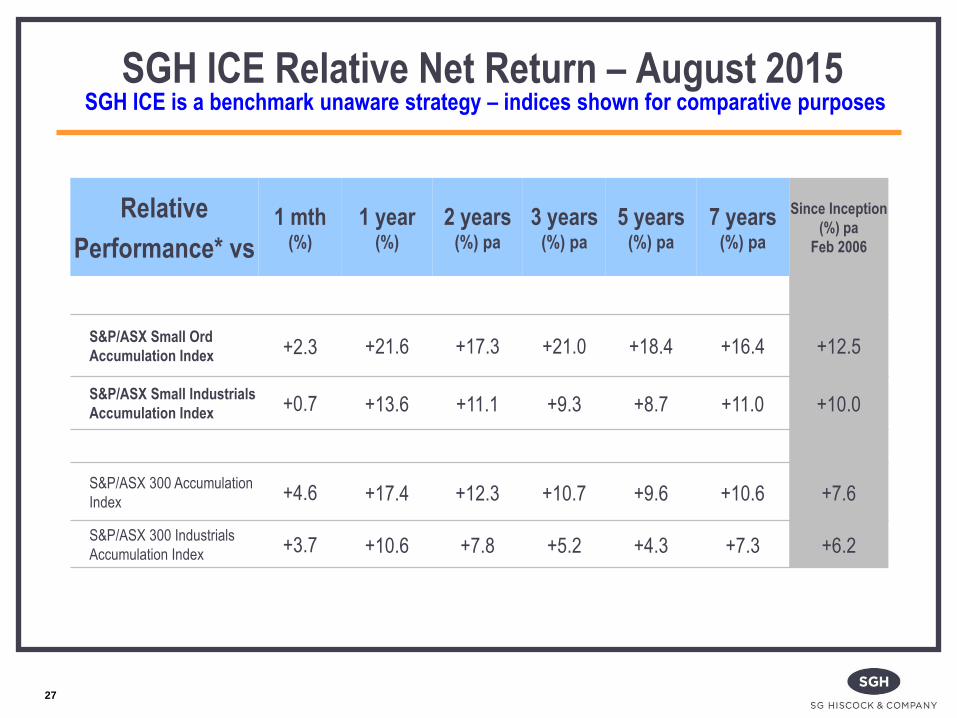

Accumulation Index +2.3 +21.6 +17.3 +21.0 +18.4 +16.4 +12.5

S&P/ASX Small Industrials

Accumulation Index +0.7 +13.6 +11.1 +9.3 +8.7 +11.0 +10.0

S&P/ASX 300 Accumulation

Index +4.6 +17.4 +12.3 +10.7 +9.6 +10.6 +7.6

S&P/ASX 300 Industrials

Accumulation Index +3.7 +10.6 +7.8 +5.2 +4.3 +7.3 +6.2

27

SGH ICE Relative Net Return – August 2015 SGH ICE is a benchmark unaware strategy – indices shown for comparative purposes

28

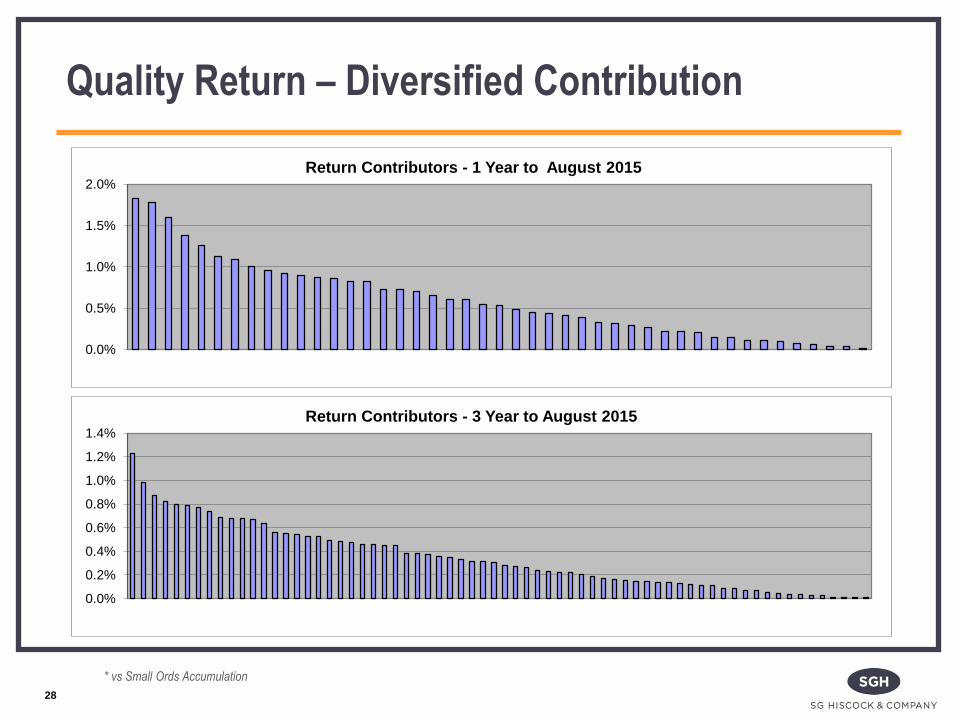

Quality Return – Diversified Contribution

* vs Small Ords Accumulation

0.0%

0.5%

1.0%

1.5%

2.0%

Return Contributors - 1 Year to August 2015

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

Return Contributors - 3 Year to August 2015

Source: Morningstar Direct, updated August 2015

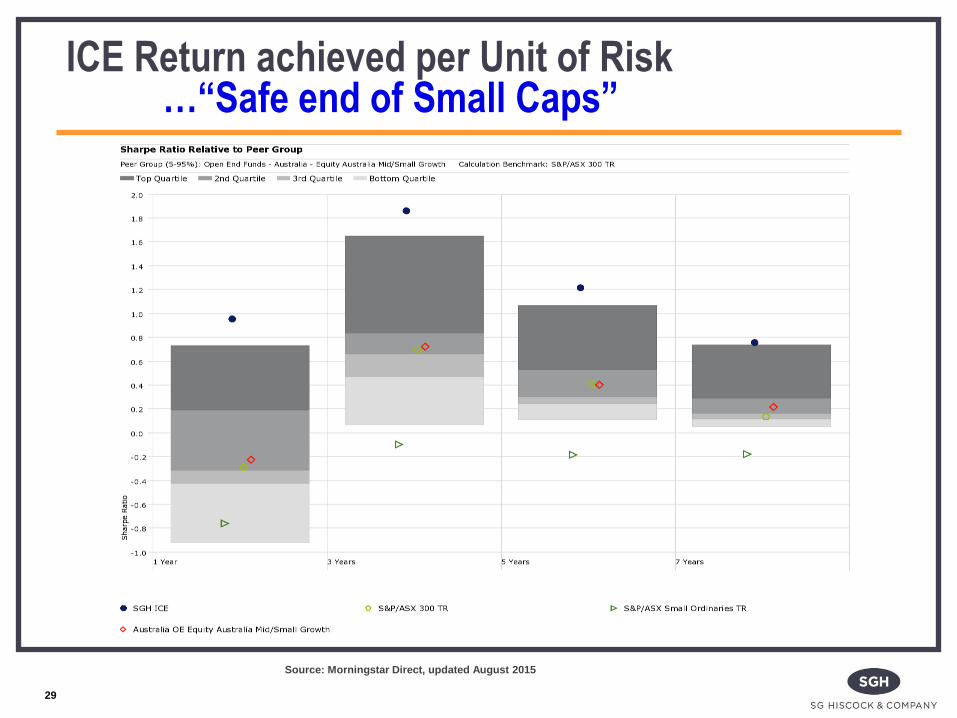

ICE Return achieved per Unit of Risk …“Safe end of Small Caps”

29

Source: Morningstar Direct, updated August 2015

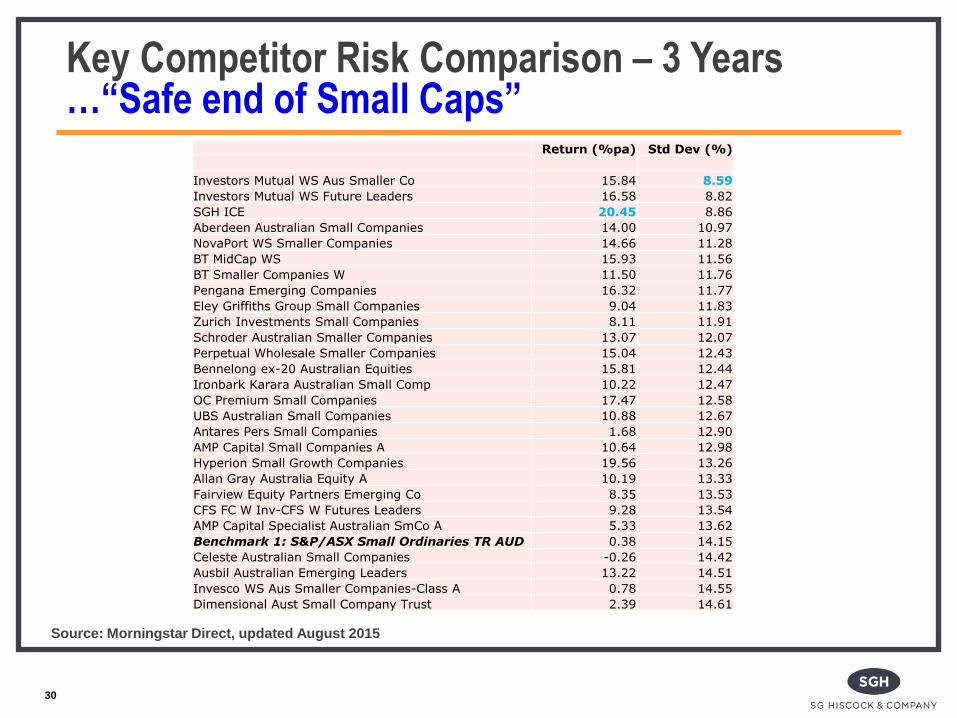

Key Competitor Risk Comparison – 3 Years …“Safe end of Small Caps” Return (%pa) Std Dev (%)

Investors Mutual WS Aus Smaller Co 15.84 8.59

Investors Mutual WS Future Leaders 16.58 8.82

SGH ICE 20.45 8.86

Aberdeen Australian Small Companies 14.00 10.97

NovaPort WS Smaller Companies 14.66 11.28

BT MidCap WS 15.93 11.56

BT Smaller Companies W 11.50 11.76

Pengana Emerging Companies 16.32 11.77

Eley Griffiths Group Small Companies 9.04 11.83

Zurich Investments Small Companies 8.11 11.91

Schroder Australian Smaller Companies 13.07 12.07

Perpetual Wholesale Smaller Companies 15.04 12.43

Bennelong ex-20 Australian Equities 15.81 12.44

Ironbark Karara Australian Small Comp 10.22 12.47

OC Premium Small Companies 17.47 12.58

UBS Australian Small Companies 10.88 12.67

Antares Pers Small Companies 1.68 12.90

AMP Capital Small Companies A 10.64 12.98

Hyperion Small Growth Companies 19.56 13.26

Allan Gray Australia Equity A 10.19 13.33

Fairview Equity Partners Emerging Co 8.35 13.53

CFS FC W Inv-CFS W Futures Leaders 9.28 13.54

AMP Capital Specialist Australian SmCo A 5.33 13.62

Benchmark 1: S&P/ASX Small Ordinaries TR AUD 0.38 14.15

Celeste Australian Small Companies -0.26 14.42

Ausbil Australian Emerging Leaders 13.22 14.51

Invesco WS Aus Smaller Companies-Class A 0.78 14.55

Dimensional Aust Small Company Trust 2.39 14.61

30

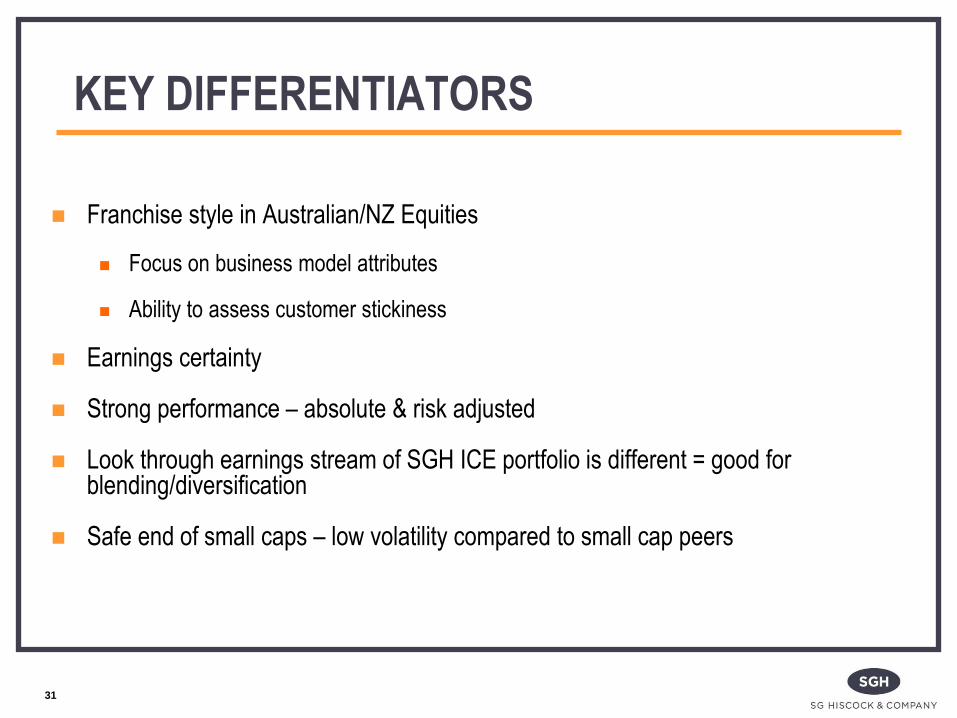

KEY DIFFERENTIATORS

Franchise style in Australian/NZ Equities

Focus on business model attributes

Ability to assess customer stickiness

Earnings certainty

Strong performance – absolute & risk adjusted

Look through earnings stream of SGH ICE portfolio is different = good for blending/diversification

Safe end of small caps – low volatility compared to small cap peers

31

Appendix

32

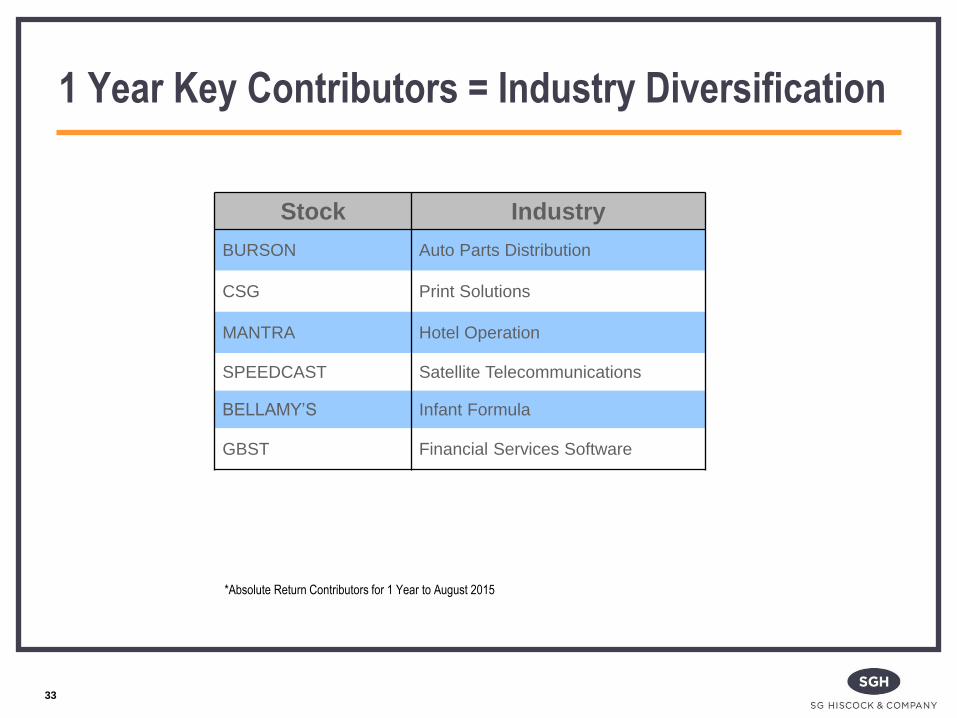

1 Year Key Contributors = Industry Diversification

33

Stock Industry

BURSON Auto Parts Distribution

CSG Print Solutions

MANTRA Hotel Operation

SPEEDCAST Satellite Telecommunications

BELLAMY’S Infant Formula

GBST Financial Services Software

*Absolute Return Contributors for 1 Year to August 2015

34

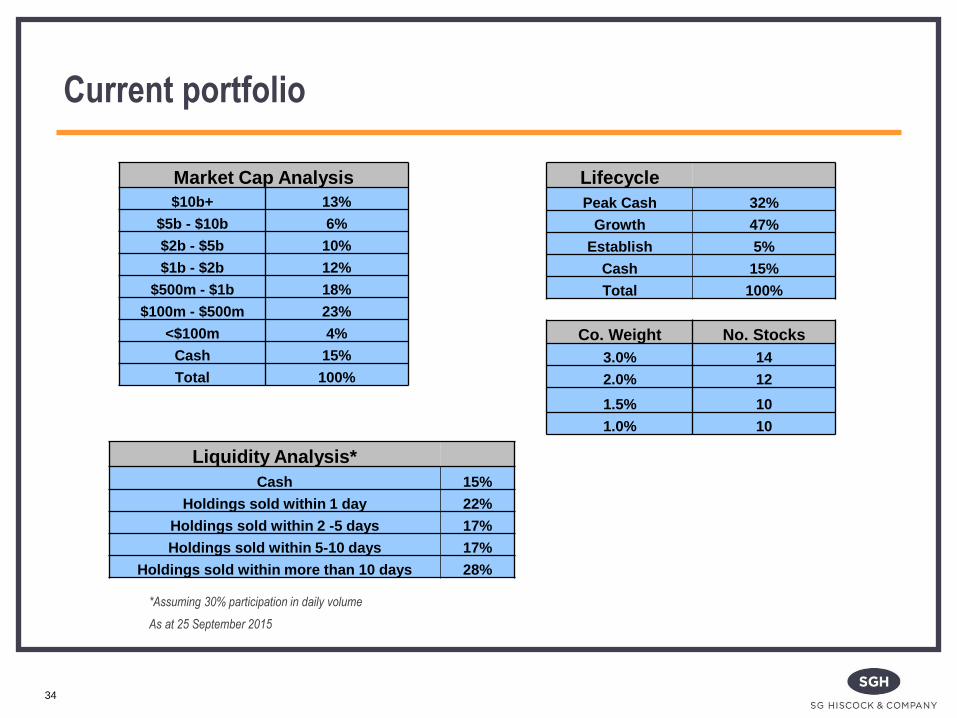

Current portfolio

*Assuming 30% participation in daily volume

As at 25 September 2015

Market Cap Analysis

$10b+ 13%

$5b - $10b 6%

$2b - $5b 10%

$1b - $2b 12%

$500m - $1b 18%

$100m - $500m 23%

<$100m 4%

Cash 15%

Total 100%

Liquidity Analysis*

Cash 15%

Holdings sold within 1 day 22%

Holdings sold within 2 -5 days 17%

Holdings sold within 5-10 days 17%

Holdings sold within more than 10 days 28%

Lifecycle

Peak Cash 32%

Growth 47%

Establish 5%

Cash 15%

Total 100%

Co. Weight No. Stocks

3.0% 14

2.0% 12

1.5% 10

1.0% 10

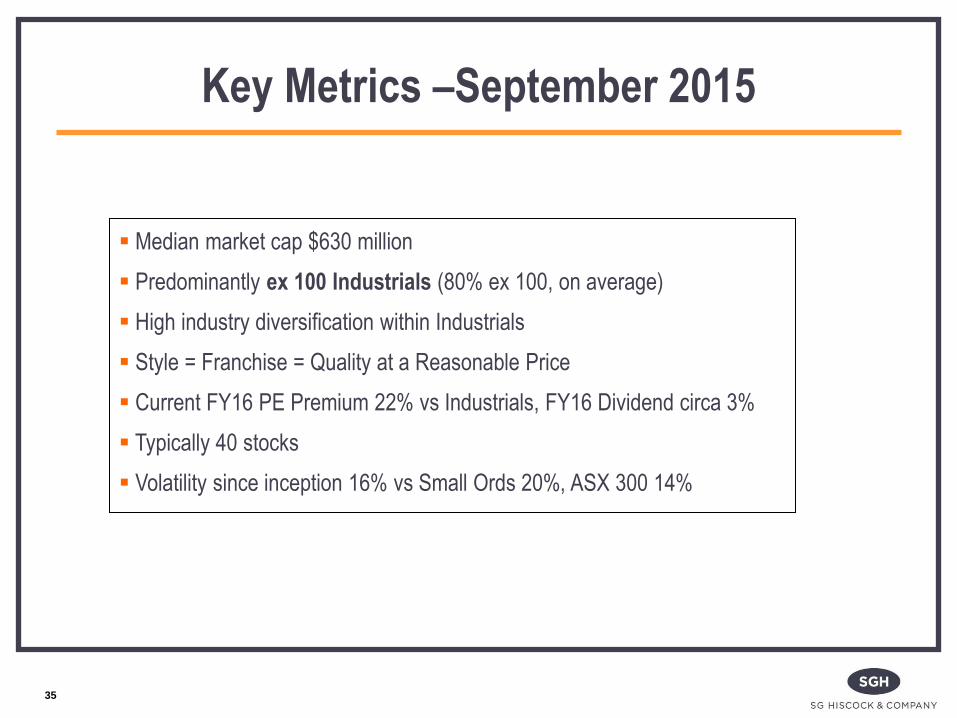

Median market cap $630 million

Predominantly ex 100 Industrials (80% ex 100, on average)

High industry diversification within Industrials

Style = Franchise = Quality at a Reasonable Price

Current FY16 PE Premium 22% vs Industrials, FY16 Dividend circa 3%

Typically 40 stocks

Volatility since inception 16% vs Small Ords 20%, ASX 300 14%

35

Key Metrics –September 2015

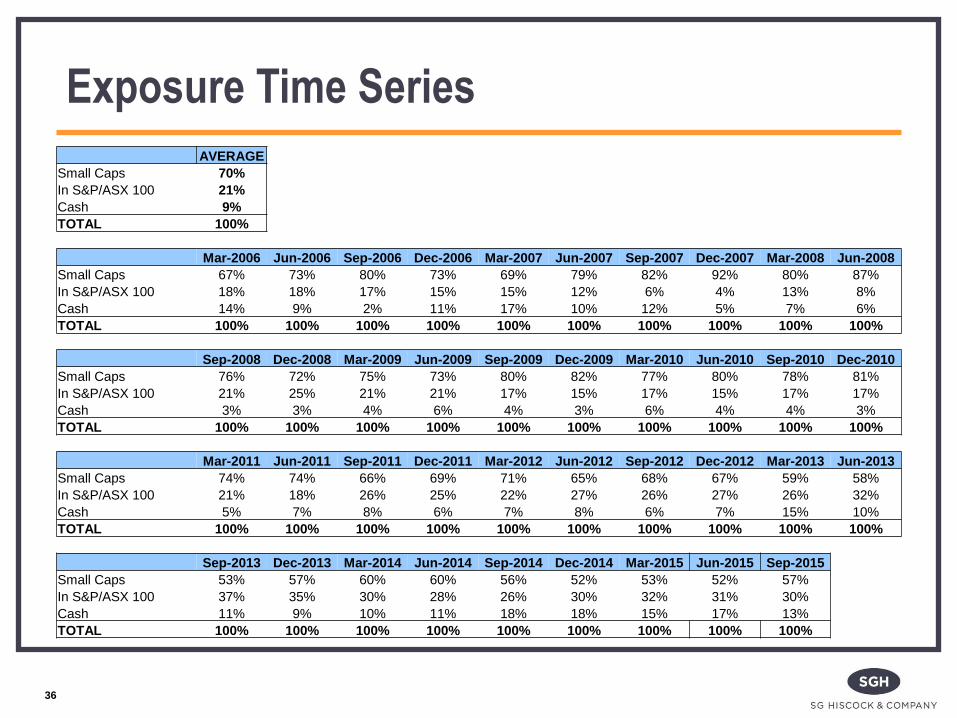

Exposure Time Series

AVERAGE

Small Caps 70%

In S&P/ASX 100 21%

Cash 9%

TOTAL 100%

Mar-2006 Jun-2006 Sep-2006 Dec-2006 Mar-2007 Jun-2007 Sep-2007 Dec-2007 Mar-2008 Jun-2008

Small Caps 67% 73% 80% 73% 69% 79% 82% 92% 80% 87%

In S&P/ASX 100 18% 18% 17% 15% 15% 12% 6% 4% 13% 8%

Cash 14% 9% 2% 11% 17% 10% 12% 5% 7% 6%

TOTAL 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Sep-2008 Dec-2008 Mar-2009 Jun-2009 Sep-2009 Dec-2009 Mar-2010 Jun-2010 Sep-2010 Dec-2010

Small Caps 76% 72% 75% 73% 80% 82% 77% 80% 78% 81%

In S&P/ASX 100 21% 25% 21% 21% 17% 15% 17% 15% 17% 17%

Cash 3% 3% 4% 6% 4% 3% 6% 4% 4% 3%

TOTAL 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Mar-2011 Jun-2011 Sep-2011 Dec-2011 Mar-2012 Jun-2012 Sep-2012 Dec-2012 Mar-2013 Jun-2013

Small Caps 74% 74% 66% 69% 71% 65% 68% 67% 59% 58%

In S&P/ASX 100 21% 18% 26% 25% 22% 27% 26% 27% 26% 32%

Cash 5% 7% 8% 6% 7% 8% 6% 7% 15% 10%

TOTAL 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

Sep-2013 Dec-2013 Mar-2014 Jun-2014 Sep-2014 Dec-2014 Mar-2015 Jun-2015 Sep-2015

Small Caps 53% 57% 60% 60% 56% 52% 53% 52% 57%

In S&P/ASX 100 37% 35% 30% 28% 26% 30% 32% 31% 30%

Cash 11% 9% 10% 11% 18% 18% 15% 17% 13%

TOTAL 100% 100% 100% 100% 100% 100% 100% 100% 100%

36

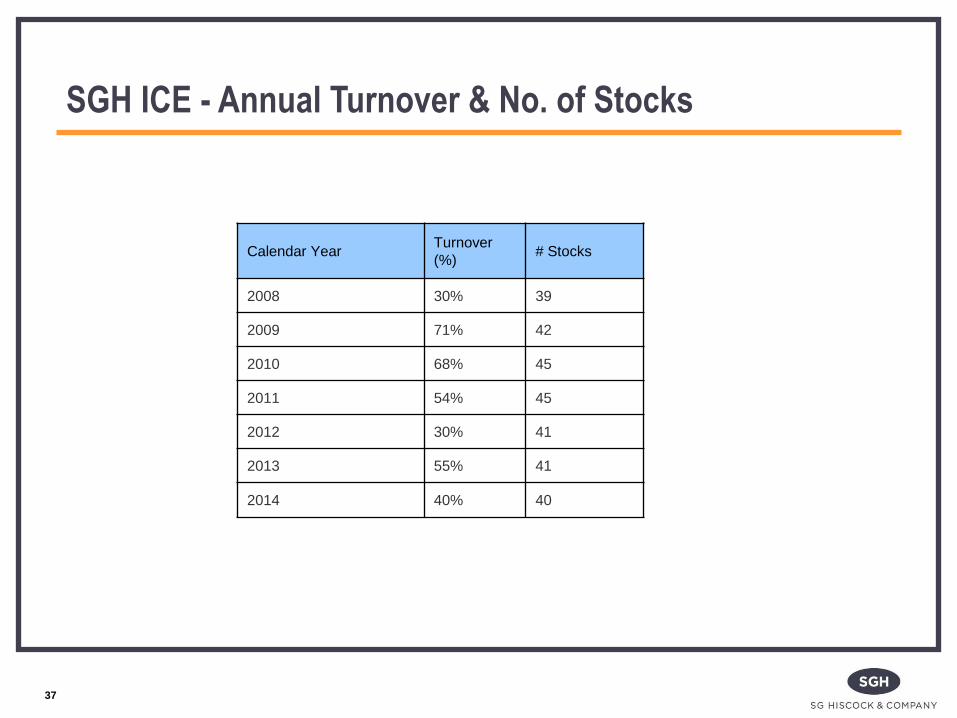

SGH ICE - Annual Turnover & No. of Stocks

Calendar Year Turnover

(%) # Stocks

2008 30% 39

2009 71% 42

2010 68% 45

2011 54% 45

2012 30% 41

2013 55% 41

2014 40% 40

37

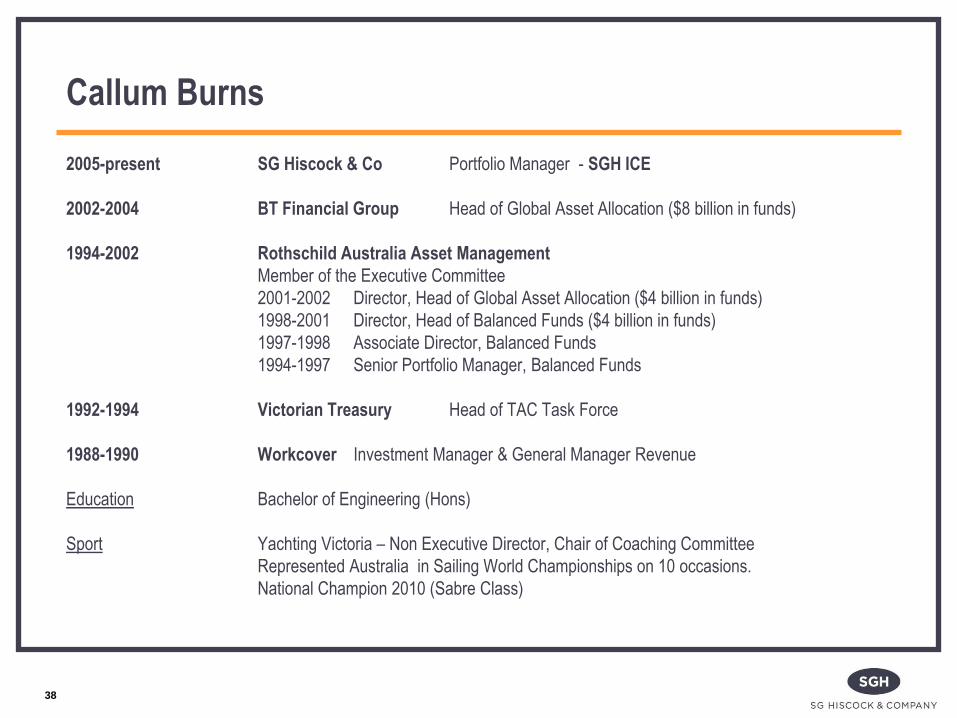

Callum Burns

2005-present SG Hiscock & Co Portfolio Manager - SGH ICE

2002-2004 BT Financial Group Head of Global Asset Allocation ($8 billion in funds)

1994-2002 Rothschild Australia Asset Management

Member of the Executive Committee

2001-2002 Director, Head of Global Asset Allocation ($4 billion in funds)

1998-2001 Director, Head of Balanced Funds ($4 billion in funds)

1997-1998 Associate Director, Balanced Funds

1994-1997 Senior Portfolio Manager, Balanced Funds

1992-1994 Victorian Treasury Head of TAC Task Force

1988-1990 Workcover Investment Manager & General Manager Revenue

Education Bachelor of Engineering (Hons)

Sport Yachting Victoria – Non Executive Director, Chair of Coaching Committee

Represented Australia in Sailing World Championships on 10 occasions.

National Champion 2010 (Sabre Class)

38

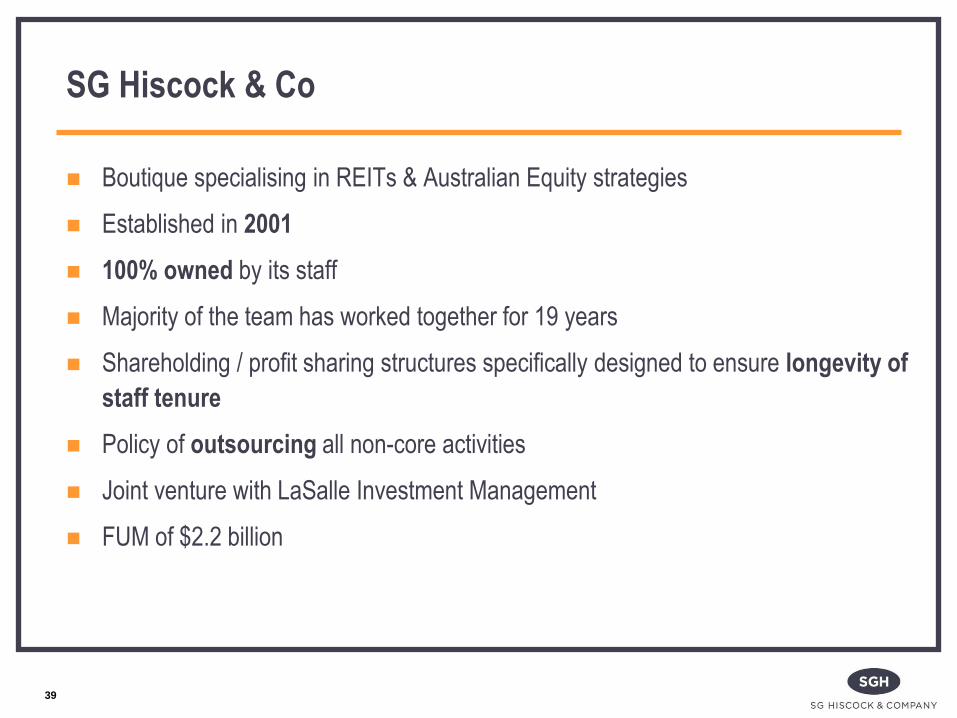

SG Hiscock & Co

Boutique specialising in REITs & Australian Equity strategies

Established in 2001

100% owned by its staff

Majority of the team has worked together for 19 years

Shareholding / profit sharing structures specifically designed to ensure longevity of

staff tenure

Policy of outsourcing all non-core activities

Joint venture with LaSalle Investment Management

FUM of $2.2 billion

39

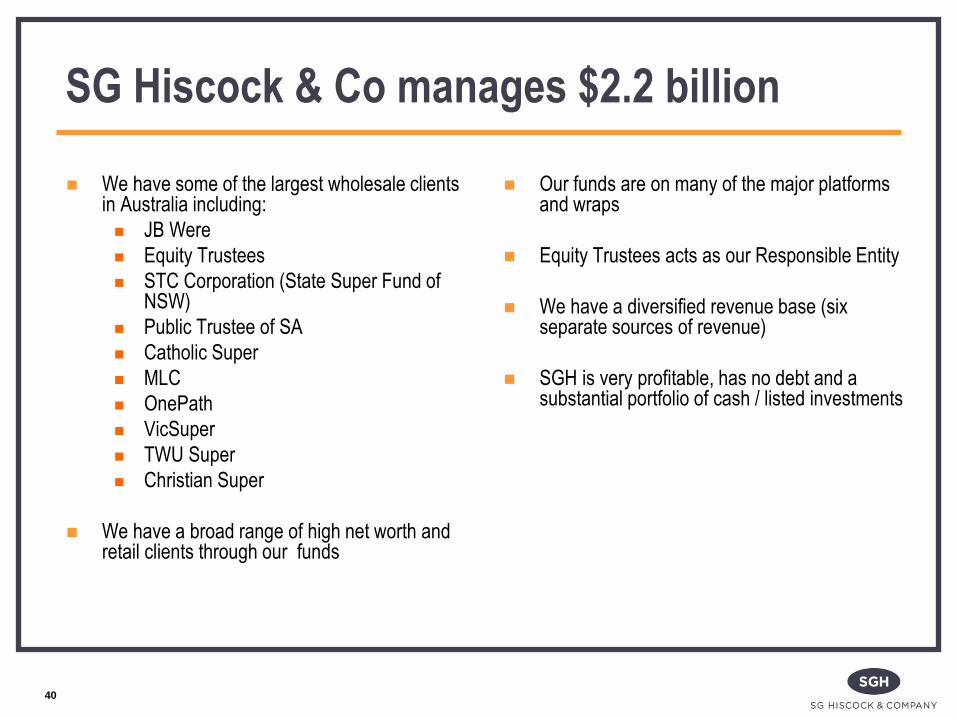

We have some of the largest wholesale clients in Australia including:

JB Were

Equity Trustees

STC Corporation (State Super Fund of NSW)

Public Trustee of SA

Catholic Super

MLC

OnePath

VicSuper

TWU Super

Christian Super

We have a broad range of high net worth and retail clients through our funds

Our funds are on many of the major platforms and wraps

Equity Trustees acts as our Responsible Entity

We have a diversified revenue base (six separate sources of revenue)

SGH is very profitable, has no debt and a substantial portfolio of cash / listed investments

40

SG Hiscock & Co manages $2.2 billion

41

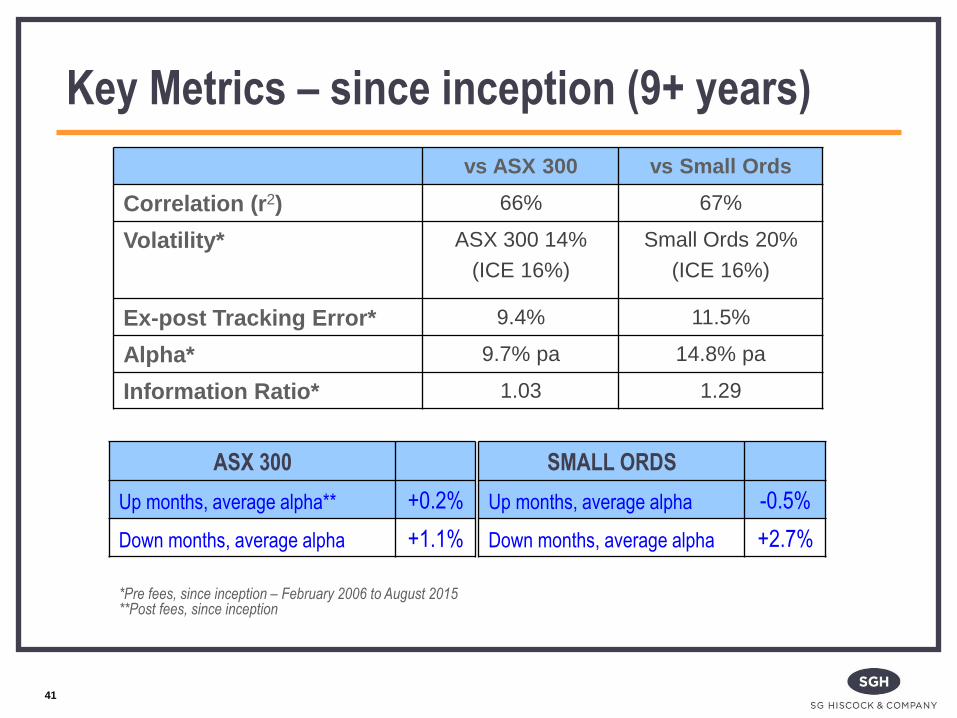

Key Metrics – since inception (9+ years)

vs ASX 300 vs Small Ords

Correlation (r2) 66% 67%

Volatility* ASX 300 14%

(ICE 16%)

Small Ords 20%

(ICE 16%)

Ex-post Tracking Error* 9.4% 11.5%

Alpha* 9.7% pa 14.8% pa

Information Ratio* 1.03 1.29

*Pre fees, since inception – February 2006 to August 2015 **Post fees, since inception

SMALL ORDS

Up months, average alpha -0.5%

Down months, average alpha +2.7%

ASX 300

Up months, average alpha** +0.2%

Down months, average alpha +1.1%

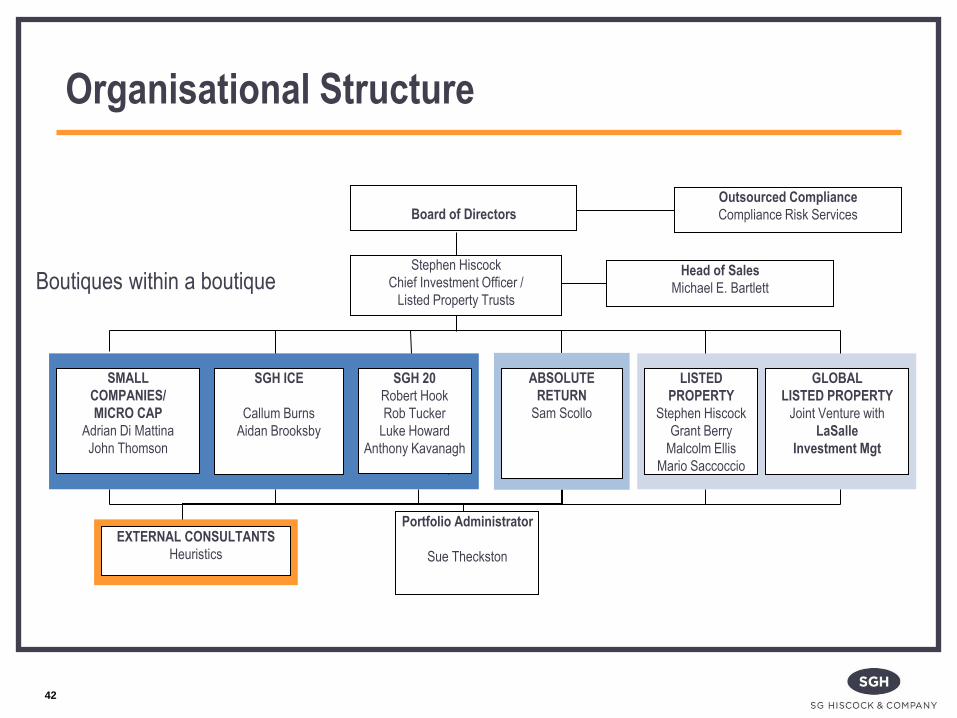

Organisational Structure

EXTERNAL CONSULTANTS

Heuristics

Board of Directors

SMALL

COMPANIES/

MICRO CAP

Adrian Di Mattina

John Thomson

LISTED

PROPERTY

Stephen Hiscock

Grant Berry

Malcolm Ellis

Mario Saccoccio

SGH 20

Robert Hook

Rob Tucker

Luke Howard

Anthony Kavanagh

GLOBAL

LISTED PROPERTY

Joint Venture with

LaSalle

Investment Mgt

Portfolio Administrator

Sue Theckston

Outsourced Compliance

Compliance Risk Services

SGH ICE

Callum Burns

Aidan Brooksby

Stephen Hiscock

Chief Investment Officer /

Listed Property Trusts

ABSOLUTE

RETURN

Sam Scollo

Head of Sales

Michael E. Bartlett

Boutiques within a boutique

42

43

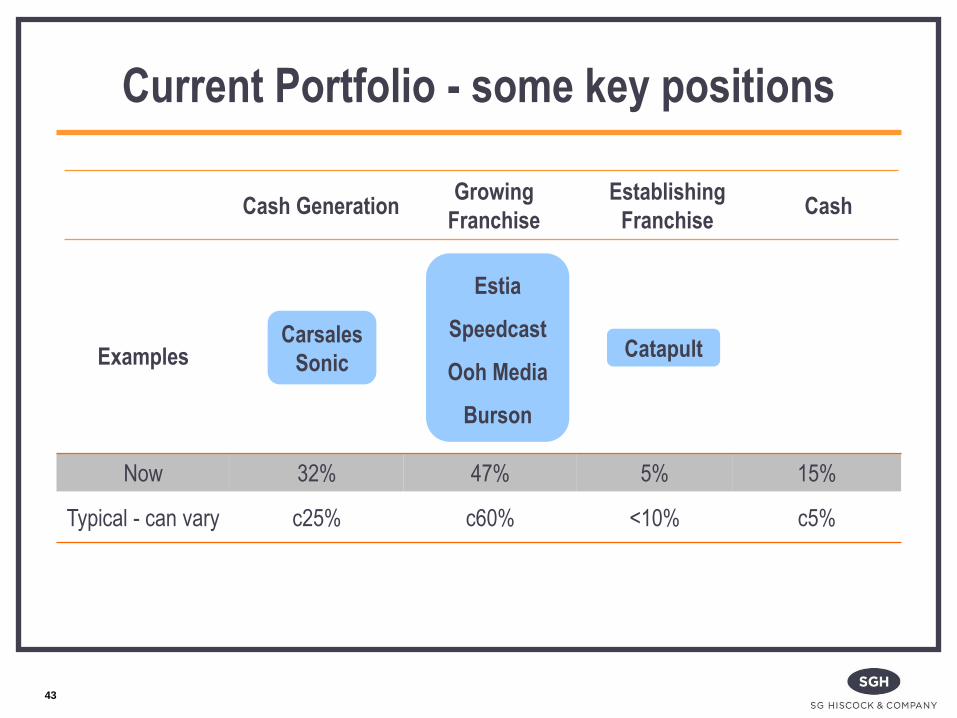

Current Portfolio - some key positions

Carsales

Sonic

Catapult

Estia

Speedcast

Ooh Media

Burson

Examples

Now 32% 47% 5% 15%

Typical - can vary c25% c60% <10% c5%

Cash Generation Growing

Franchise

Establishing

Franchise Cash

44

Further information

For further information contact Equity Trustees

distribution partner for SG Hiscock & Company

T: 1300 555 511

W: www.eqt.com.au

45

*The Lonsec Rating (assigned February 2015) presented in this document is published by Lonsec Research Pty Ltd ABN 11 151 658 561 AFSL 421445. The Rating is a

“class service” (as defined in the Financial Advisers Act 2008 (NZ)) or is limited to “General Advice” (as defined in the Corporations Act 2001 (Cth)) and based solely on

consideration of the investment merits of the financial product(s). In New Zealand it must only be provided to “wholesale clients” (as defined in the Financial Advisers Act

2008 (NZ)). Past performance information is for illustrative purposes only and is not indicative of future performance. It is not a recommendation to purchase, sell or hold SG

Hiscock & Company product(s), and you should seek independent financial advice before investing in this product(s). The Rating is subject to change without notice and

Lonsec assumes no obligation to update the relevant document(s) following publication. Lonsec receives a fee from the Fund Manager for researching the product(s) using

comprehensive and objective criteria.

For further information regarding Lonsec’s Ratings methodology, please refer to our website at: http://www.beyond.lonsec.com.au/intelligence/lonsec-ratings

**Morningstar – © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be

accurate, complete or timely nor will they have any liability for its use or distribution. Any general advice or 'class service' have been prepared by Morningstar Australasia Pty

Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or

needs. Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if

applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest. Our

publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily

indicate a financial product's future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is copyright and published

under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

**Morningstar Awards 2014(c). Morningstar, Inc. All Rights Reserved. Awarded to SGH ICE for Fund Manager of the Year 2014 - Undiscovered Manager Category, Australia.

**Morningstar Awards 2015(c). Morningstar, Inc. All Rights Reserved. Awarded to SGH ICE for Fund Manager of the Year 2015 - Small Companies Category, Australia.

***The Zenith Investment Partners (“Zenith”) Australian Financial Services License No. 226872 rating (assigned June 2015) referred to in this document is limited to “General

Advice” (as defined by the Corporations Act 2001) for Wholesale clients only. This advice has been prepared without taking into account the objectives, financial situation or

needs of any individual. It is not a specific recommendation to purchase, sell or hold the relevant product(s). Investors should seek independent financial advice before

making an investment decision and should consider the appropriateness of this advice in light of their own objectives, financial situation and needs. Investors should obtain a

copy of, and consider the PDS or offer document before making any decision and refer to the full Zenith Product Assessment available on the Zenith website. Zenith usually

charges the product issuer, fund manager or a related party to conduct Product Assessments. Full details regarding Zenith’s methodology, ratings definitions and regulatory

compliance are available on our Product Assessment’s and at http://www.zenithpartners.com.au/RegulatoryGuidelines.

September 2015

45

Disclaimers

Important Information:

This presentation has been prepared by SG Hiscock & Company

Limited (ABN 51 097 263 628, AFSL 240679) which are responsible

for its contents. Neither SG Hiscock & Company Limited nor its related

entities, directors or officers guarantees the performance of, or the

repayment of capital or income invested in the funds. Applications for

investment in the Fund may only be made on the application form

attached to the current fund’s PDS available from Equity Trustees.

You should consider the PDS when deciding whether to acquire or to

continue to hold units in the funds.

46