shale gas plays: development, economics, and the future

TRANSCRIPT

Shale Gas Plays: Development, Economics, and the Future

University of Texas Center for Energy Economics

2010 Annual Meeting & Natural Gas Forum

December 1, 2010

Richard G. SmeadDirector, Navigant Consulting Inc.

Navigant Consulting Inc.30 South Wacker DriveSuite 3100Chicago, IL 60606(312) 583‐5700

www.navigantconsulting.com

909 Fannin StreetSuite 1900Houston, TX(713) 646‐5029

©2010 Navigant Consulting, Inc.

1©2010 Navigant Consulting, Inc. 1

Proved Reserves Plus Assessed Resources—Life of the Gas Resource

Yes, There Is a Lot of Gas Resource: The Recognition Started with the American Clean Skies Foundation

2008

82 years at

2006 Prod. Rate

88 years at

2007 Prod. Rate

118 years at

2007 Prod. Rate

-

U.S. Total Gas Supply (Tcf)

500

1,000

1,500

2,000

2,500

PGC 2006 MeanAssessment

Navigant Study PGC 2008 EstimateReleased June 2009

tcf

ShaleResource

All OtherTechnicallyRecoverableResource

• In 2006, the Potential Gas Committee (PGC) estimated 1,530 Tcf of total Recoverable Resource.

• In 2008, the American Clean Skies Foundation had Navigant perform the North AmericanNatural Gas Supply Assessment. This study found that shale and other unconventional supplieshad increased the resource to as much as 2,247 Tcf, including 842 Tcf of shale gas.. This would be118 years of production at 2007 levels.

• In June 2009, PGC issued its 2008 updated study—2,076 Tcf, including 616 Tcf of shale, also over100 years’worth.

U.S. Shale Gas Basins Align with the Nationwide Pipeline Grid

American Clean Skies Foundation

Sources: EIA, US Natural Gas Pipeline Nework

©2010 Navigant Consulting, Inc.

3©2010 Navigant Consulting, Inc.

‐

10.0

20.0

30.0

40.0

50.0

60.0

70.01990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Bcf per Day

Sources of U.S. Gas Supply, 1990 to 2010

Net LNG Imports

Net Pipeline Imports

Net Dry Gas Production

Total Gas Supply: For 15 years, Domestic Production was Flat, with Growing Imports—Then in 2005, the Ramp‐up Began

4©2010 Navigant Consulting, Inc.

45.0

50.0

55.0

60.0

65.0

70.0

2005 2006 2007 2008 2009 2010

Bcf per Day

The Rapid Change from 2005

Net LNG Imports

Net Pipeline Imports

Net Dry Gas Production

Total Consumption

The Last Five Years Have Been Very Different—Thanks to Domestic Growth, Supply Now Exceeds Demand, and Imports are Shrinking

©2010 Navigant Consulting, Inc. 5

40.0

42.0

44.0

46.0

48.0

50.0

52.0

54.0

56.0

58.0

60.0

Jan‐05

Jun‐05

Nov‐05

Apr‐06

Sep‐06

Feb‐07

Jul‐0

7

Dec‐07

May‐08

Oct‐08

Mar‐09

Aug‐09

Jan‐10

Jun‐10

Lower 48 Production, Total and Onshore, 2005‐2010Bcf p

er Day, D

ry

Average Total Pre‐Katrina

Gustav

and Ike

Katrina

and Rita

The Really Dramatic Story is Onshore, where Between 2005 and 2008, Enough Production Was Added to Replace Offshore

From 2005 to 2008, the

daily energy added from onshore sources

exceeds the thermal

content of all the oil we

import from Saudi Arabia.

6©2010 Navigant Consulting, Inc.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1990

1995

2000

2005

2010

2015

2020

2025

2030

EIA Projected Shale Production EstimatesBcf p

er Day, D

ry

Actuals to 2006

What about Shale Gas? EIA Developed a Robust Forecast in 2010

7©2010 Navigant Consulting, Inc.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1990

1995

2000

2005

2010

2015

2020

2025

2030

Shale Actual Production Through 2010Bcf p

er Day, D

ry

But Actual Production has Far Exceeded Even the Aggressive 2010 Forecast

©2010 Navigant Consulting, Inc. 8

Why? Didn’t drilling drop off a lot since 2008?

Yes, in total—but horizontal drilling is going strong. . .

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Source: Smith Bits

Gas‐Dire

cted

Drilling Rigs in

Service

9©2010 Navigant Consulting, Inc.

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

1990

1995

2000

2005

2010

2015

2020

2025

2030

Producer 2009 Composite ForecastBcf p

er Day, D

ry

Producers Expect the Trend to Continue if There’s a Demand for the Gas—2010 Actuals Exceeded Even the Producers’ 2009 Forecast

10©2010 Navigant Consulting, Inc.

50.0

55.0

60.0

65.0

70.0

75.0

80.0

85.0

90.0

95.0

100.0

1990

1995

2000

2005

2010

2015

2020

2025

2030

Total Supply per EIA and with Producer EstimateBcf p

er Day, D

ry

20 Bcf/Day

Based on that Producer Forecast, There Would Be Enough Additional Supply by 2020 to Displace Over Half of All U.S. Coal‐Fired Generation

11©2010 Navigant Consulting, Inc.

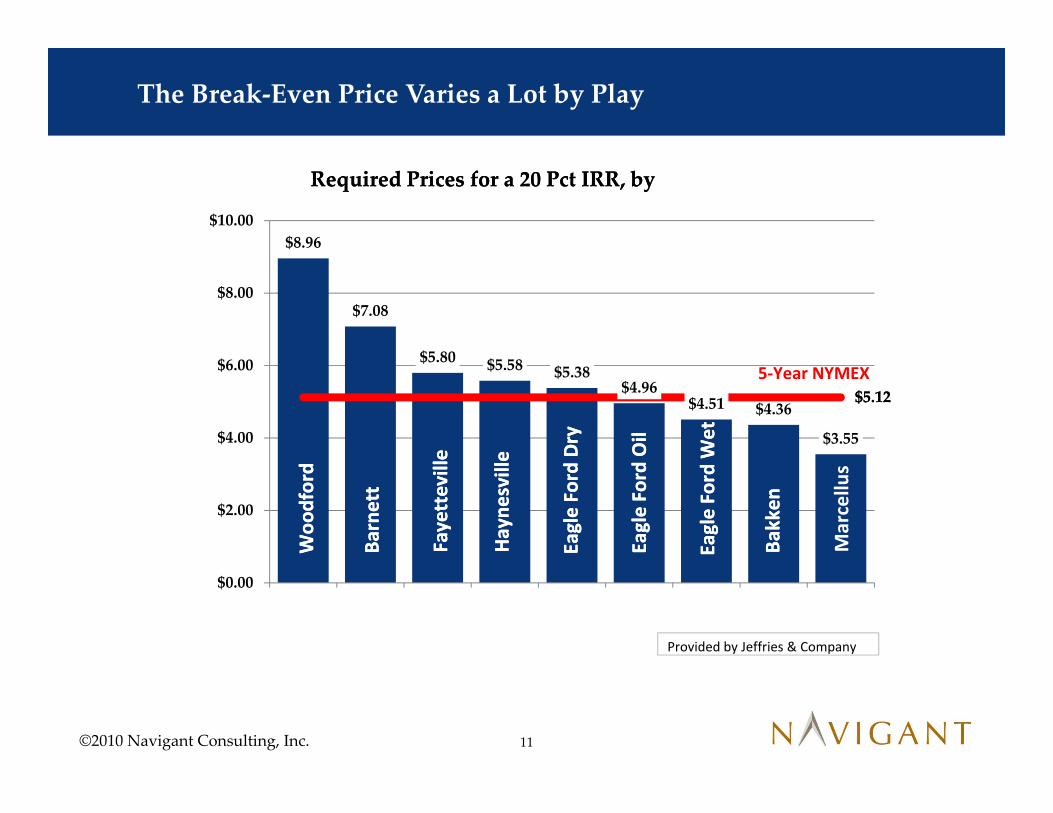

The Break‐Even Price Varies a Lot by Play

$8.96

$7.08

$5.80 $5.58 $5.38$4.96

$4.51 $4.36

$3.55

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

1 2 3 4 5 6 7 8 9

Woo

dford

Barnett

Fayetteville

Hayne

sville

Eagle Ford Dry

Eagle Ford Oil

Eagle Ford W

et

Bakken

$5.12

Required Prices for a 20 Pct IRR, by

5‐Year NYMEX

Woo

dford

Barnett

Fayetteville

Hayne

sville

Eagle Ford Dry

Eagle Ford Oil

Eagle Ford W

et

Bakken

$5.12

Required Prices for a 20 Pct IRR, by

Provided by Jeffries & Company

Marcellu

s

12©2010 Navigant Consulting, Inc.

Schlumberger Sees a Steady Decline in Break‐Even Costs Because of Technological Advances

13©2010 Navigant Consulting, Inc.

Not the Result of Big Tech Breakthroughs—Just Getting Very Good at Using the Existing Tools

14©2010 Navigant Consulting, Inc.

What Has All this Meant for the Competitive Position of Gas?

Delivered Eastern Coal vs. Appalachian Gas

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

Dominion, South Point Central Appalachian Coal

Delivered Price per M

MBtu

15©2010 Navigant Consulting, Inc.

44.0%

45.0%

46.0%

47.0%

48.0%

49.0%

19.0%

20.0%

21.0%

22.0%

23.0%

24.0%

Dec 08

Jan 09

Feb 09

Mar 09

Apr 09

May 09

June 09

July 09

Aug 09

Sept 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Apr 10

May 10

June 10

July 10

Gas and Coal Generation Market ShareRolling 12‐Month Totals 2008 ‐ 2010

Gas M

arket S

hare

Coal M

arket S

hare

Gas Has Gained Market Share vs. Coal, A Little Over 2 Percent

Market and Development Impact• The Market is oversupplied—So prices have been in the $3 to $4 range, when

most think it takes $6 for full development—We need more demand.— Until now, lease retention, NGL production, and being in the “Sweet Spots”

has kept development going at a high pace.— But without a stronger market, the industry will redirect toward oil, slowing

the pace of development .

• The added supply, on top of EIA’s highest estimates, is enough to replace half of all coal use by 2020! This is a huge opportunity, but it is also a huge amount of supply to find a home for.

• Meanwhile, land impact, water questions around hydraulic fracturing, and road impacts are causing opposition to development.

• Of all those issues, hydraulic fracturing has been the most controversial—water supply and produced‐water handling are the biggest environmental issues faced by the industry.

©2010 Navigant Consulting, Inc. 16

Challenges Faced in the United States

KeyC O N T A C T S

17©2010 Navigant Consulting, Inc. Confidential and proprietary. Do not distribute or copy. E N E R G Y

Rick Smead | [email protected] direct

Gordon Pickering \ [email protected] direct