shares - bowleven plc oil and gas company

TRANSCRIPT

Private & Confidential 2

Important Notice

Nothing in this presentation or in any accompanying management discussion of this presentation (the "Presentation") constitutes, nor is it

intended to constitute: (i) an invitation or inducement to engage in any investment activity, whether in the United Kingdom or in any other

jurisdiction; (ii) any recommendation or advice in respect of the ordinary shares (the "Shares") in Bowleven plc (the "Company"); or (iii) any

offer for the sale, purchase or subscription of any Shares.

The Shares are not registered under the US Securities Act of 1933 (as amended) (the "Securities Act") and may not be offered, sold or

transferred except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and in

compliance with any other applicable state securities laws.

The Presentation may include statements that are, or may be deemed to be "forward-looking statements". These forward-looking statements

can be identified by the use of forward-looking terminology, including the terms "believes", "estimates", "anticipates", "projects", "expects",

"intends", "may", "will", "seeks" or "should" or, in each case, their negative or other variations or comparable terminology, or by discussions of

strategy, plans, objectives, goals, future events or intentions. These forward-looking statements include all matters that are not historical facts.

They include statements regarding the Company's intentions, beliefs or current expectations concerning, amongst other things, the results of

operations, financial conditions, liquidity, prospects, growth and strategies of the Company and its direct and indirect subsidiaries (the “Group”)

and the industry in which the Group operates. By their nature, forward-looking statements involve risks and uncertainties because they relate to

events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not guarantees of future

performance. The Group’s actual results of operations, financial conditions and liquidity, and the development of the industry in which the

Group operates, may differ materially from those suggested by the forward-looking statements contained in the Presentation. In addition, even

if the Group’s results of operations, financial conditions and liquidity, and the development of the industry in which the Group operates, are

consistent with the forward-looking statements contained in the Presentation, those results or developments may not be indicative of results or

developments in subsequent periods. In light of those risks, uncertainties and assumptions, the events described in the forward-looking

statements in the Presentation may not occur. Other than in accordance with the Company's obligations under the AIM Rules for Companies,

the Company undertakes no obligation to update or revise publicly any forward-looking statement, whether as a result of new information, future

events or otherwise. All written and oral forward-looking statements attributable to the Company or to persons acting on the Company's behalf

are expressly qualified in their entirety by the cautionary statements referred to above and contained elsewhere in the Presentation.

‘Bowleven’, ‘EurOil’ and the Bowleven logo are trade marks of Bowleven plc and copyright in the content of this document is owned by

Bowleven plc. They should not be used without permission.

Disclaimer

Private & Confidential 3

Overview – focused on Cameroon in Africa

• Deliver value to all our shareholders by

developing and growing our resource base in

our Cameroon assets whilst maintaining

rigorous attention to costs and value

• Right sized our organisation commensurate

with the needs of our current portfolio

• Convert portfolio resources to reserves and

monetise the gas and condensate

• Focus attention on monetising the existing

exploration assets ahead of deploying capital

on new exploration

• Seek and optimise value-adding partnerships

Strategic framework:

Creating shareholder value

“We are dedicated to realising

material shareholder value from our

assets in Cameroon whilst maintaining

capital discipline and employing a

rigorous approach to other value-

enhancing opportunities”

Private & Confidential 4

Delivering value for all our shareholders

New leadership

• Chris Ashworth was appointed Chairman

and Eli Chahin was CEO in March.

• The Board was subsequently expanded

with two new non-executive Directors. Joe

Darby was appointed in April and Matt

McDonald was appointed in August

Fresh approach

• Refocussed strategy away from exploration

to maximising value from our existing asset

portfolio

• Right sized organisation and moved to

London

• Enhanced capital discipline

• Aligned cost based with strategy

Average G&A costs reduced to less than

$350k per month

Executive Board costs reduced

significantly

Private & Confidential 5

Financial results

• Strong balance sheet with over $84m cash at

30 November 2017

• No debt and no outstanding work programme

commitments

• Etinde farm-out transaction:

o Access to $40 million (net) carry; covers

share of drilling/testing of two Etinde

appraisal wells2

o $25 million at Etinde FID

• G&A reduced to less than $0.35m net per

month on average

• Bomono asset fully impaired at an impairment

charge of $46m

• 7.8m shares purchased under share buyback

programme at total consideration of $2.6m1

B – current budget for calendar year 2017

Administrative expenses net of costs recovered against the asset base and includes UK and overseas costs1 Sterling gross consideration converted to USD at 1.26952 Cash alternative in 2020 available

Private & Confidential 6

Near-term Business Objectives

Maximise the value of Etinde

• Ensure appraisal drilling is carried out in 2018

• Work towards prompt development alignment

• FID to be achieved quickly thereafter

De risk Bomono

• Relinquish operator status

• Complete farm-out with VOG on agreeable terms

• Further appraisal/exploration activities may follow

Selective capital deployment

• Assess value enhancing opportunities across

Etinde value chain

• Seek to cover G&A with proactive cash

management

G&A containment

• Continuous G&A scrutiny whilst retaining execution

capacity

Private & Confidential 7

Ghana To

go

Be

nin

Nigeria

Gabon Congo

E.Guinea

20km

Cameroon

Douala

Bomono

20km

In a strong financial position with $40M carry for

the 2018 appraisal wells

Asset overview

Etinde

Bomono

Equity Interest NewAge (operator) – 37.5 %

LUKOIL – 37.5 %

Bowleven – 25 %

SNH – 0%

P50 contingent

resources

290 mmboe

Equity Interest Bowleven (operator) –

100%*

* Victoria Oil and Gas plc have farmed-in for 80 % interest, but this is subject to

completion

Has exploration licence extended to December

2018 and PEA submitted to authorities. Farm-out

with VOG pending

Private & Confidential 8

2018 Etinde Appraisal drilling (1)

• Outline agreement to proceed with two

appraisal wells in 2018

• JV partners closely aligned re well

location

• Final decision in Q1 2018 following

shallow level drilling hazard assessment

and sea bottom survey

• Initial well designs completed

• Tender process for drilling contractor and

other major suppliers under way

• Well testing programme under evaluation

• Drilling vessel expected to mobilise on

site in Q2 2018

• IM-6 well spud planned for Q2 2018

• Two well drilling programmes expected to

conclude in Q4 2018

Work Programme and timeline Isongo

Marine

Discovery

ID/IE

Discovery

Intra

Isongo

Dicovery

Private & Confidential 9

2018 Etinde Appraisal drilling (2)

IM-5ZR well discovery

• Drilled to the SE of the earlier IM-3 well with

approximately 0.47 tcf of wet gas resource)

• Tested >10,800 boepd from 29m net pay

(37mmscfd & 4,664 bcpd)

Primary target

RMS Amplitude map showing the proposed IM-6 location due south of the IM-5Zr well (source: New Age)

IM-6 appraisal well

• Southward extension of the 410 intra-Isongo

sandstone horizon gas condensate discovery

from the IN-5ZR

• 200 to 280m potential column height targeted

• Well designed with the ability to convert to a

production well at a later date

• If well proves to be below the gas/water

contact, then data collected should be

sufficient to allow an up-dip side track

• In a success case, the well targets 0.87 tcf of

wet gas resource at P50 in the 410

sandstone horizon

Private & Confidential 10

2018 Etinde Appraisal drilling (3)

IM-6 well

• The IM-6 well located to explore two additional

potential reservoir formations above and below the

410 resource

• Shallower depth “510/Grinder” sandstone formation

• Deeper depth “310/Yankee” sandstone formation

• On a success case basis, the larger 510 sandstone

has up to 1.1 tcf (at P50 confidence) of wet gas

within the RMS amplitude defined structure

• The deeper 310 sandstone package may contain up

to 0.2 tcf of gas in place (P50)

IM-7 Appraisal well

• The IM-7 proposed well location is designed to

identify the likely size of the 510 sandstone

formation

Appraisal well success outcome

Both wells have the potential to increase total gas

condensate resource in place from c1 tcf to 3 tcf at the

P50 confidence level (total field basis)

Secondary target

Appraisal Success

GIIP (Bcf)

P90 P50 P10 Mean

Discovered

volumes

776 1.003 1,301 1,025

510 803 1,120 1,495 1,137

410

(remaining)

513 743 1,011 756

310 184 233 293 236

Total 2,276 3,099 4,100 3,154

Private & Confidential 11

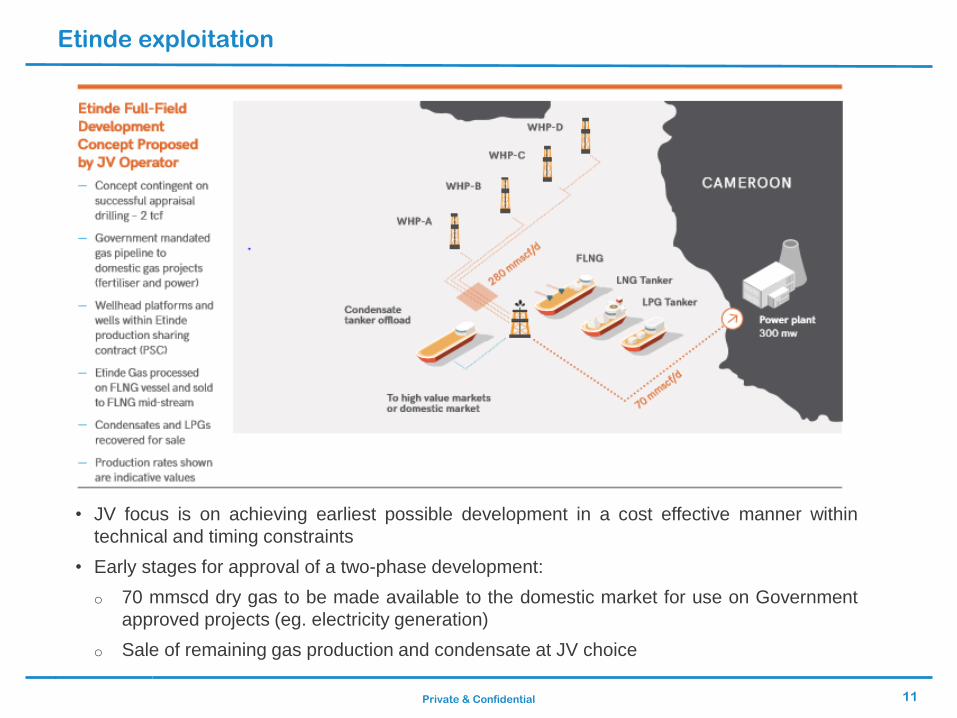

Etinde exploitation

• JV focus is on achieving earliest possible development in a cost effective manner within

technical and timing constraints

• Early stages for approval of a two-phase development:

o 70 mmscd dry gas to be made available to the domestic market for use on Government

approved projects (eg. electricity generation)

o Sale of remaining gas production and condensate at JV choice

Private & Confidential 12

Gulf of Guinea – Floating LNG proving ground?

• Perenco, Gazprom marketing and trading and

SNH signed an 8 year deal with Golar LNG

• Golar provide a Floating LNG vessel (the “Hilli

Episeyo”) to process 500 bcf of gas from

Perenco/SNH’s Sanga Sud and Ebome fields off

Cameroon

• Hilli Episeyo arrived in Cameroon waters in late

November 2017

• Ophir Energy pursuing a FLNG solution for

Fortuna JV in Equatorial Guinea waters to

the SW of Etinde

• FID expected early 2018

• OneLNG (JV) to operate the FLNG facility

• Subsea Integration Alliance (JV) awarded in

October 2017 upstream construction

contract

• Targeting first gas with a planned 440

mmscf/d gas production in 2020

Schematic development design for Fortuna LNG JV (source: Fortuna presentation)

The Hilli Episeyo en route to Cameroon

Private & Confidential 13

Bomono

Monetising the asset is dependent of finalising the agreement with VOG

• Victoria Oil & Gas plc (“VOG”) represent an ideal partner to develop Bomono

• Farm-out transaction for 80 % stake signed with VOG in March 2017 subject to conditions precedent

• VOG, with our agreement, have rolled the long-stop date for the contract to 31 December 2017

• Should the farm-out arrangement not complete, we will not be in a position to generate an alternative

development plan before the existing exploration authorisation terminates in December 2018

• We consider a likely risk that the Government will not approve a further extension to the exploration

authorisation without attaching additional exploration work commitments

Given the ongoing discussion and fundamental uncertainty, the carrying value of the Bomono

intangible asset has been fully impaired, with a charge of $46 million being made in the year

Private & Confidential 14

Conclusion – creating shareholder value

• Deliver value to all our shareholders by developing our resource base in our Cameroon

assets

• Right sized our organisation commensurate with the needs of our current portfolio

• Convert portfolio resources to reserves and monetise the gas and condensate in Etinde

• Disciplined capital deployment conducive with the set near term objectives

• Seek and optimise value-adding partnerships across the Etinde value chain where

appropriate and commensurate with the risk/return proposition

Private & Confidential 15

Q & A