sharing agents - changing character of insurance distribution · sharing agents - changing...

TRANSCRIPT

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Sharing agents - Changing character ofinsurance distribution

Josef Lilljegren∗

dpt. Geography and Economic History, Umea [email protected]

Abstract

Insurance agents were essential but problematic assets to Swedish property underwriters during theindustrialisation period. They enabled national firms’ growth in the provinces. Agents’ knowledge andthe trust they upheld were essential to the underwriters’ product distribution strategies. Their servicesalso came at financial, monitoring, and trust-related costs to the underwriters. Yet, from the 1880sthrough 1950, national firms kept relying on sophisticated agent-networks for their distribution. Thispaper looks into the changing functionality, development, and implementations of this strategy. Throughagent networks (19th century) and firm-relations through co-insurance (20th century), network analysis iscombined with an analysis of the contemporary agent-bulletins of the underwriters to cast new light uponthe changing market structure of Swedish property insurance during this formative period.

The history of Swedish underwriting hasbeen written in observance of both collu-

sive and competitive aspect of the marketdevelopment.1 Yet, little attention has beengiven to the distribution channels and the levelof contracting where the collusive and com-petitive aspects of the market actually playedout. From the dawn of commercial underwrit-ing by actuarial principals in the 19th century,2

insurance distribution was carried out by com-pany agents, whose responsibilities includedinformation gathering, actively seeking out po-tential customers, making risk-assessments onbehalf of the firm, and assessing and adminis-trating damages and payouts on behalf of theunderwriter. Knowledgable and trust-worthyagents was an essential resource to the under-writers. In many ways, it was the insuranceagents that carried out the competition for theirrespective firms. Agents were, however, oftennot exclusively hired by single underwriters.

They often worked on commission from multi-ple underwriters at the same time, giving riseto complicated relationships of loyalty whichhad implications for competition. The shar-ing of agents also intertwined with close col-laborative inter-firm relations maintained byhead-offices on the corporate level,3 particu-larly the industry’s extensive and long-livedcartel agreements.4

I. Insurance Agents and the

distribution problem

The American Agency System, placed a greatdeal of power over the control of informationcosts in the hands of the firms’ outsourcedagents who worked on commission in desig-nated geographical areas.5 Baranoff describeshow the late 19th century insurance agent pri-marily judged risk by the potential clients’ rep-utation.6 Inspections of the actual properties

∗PhD-candidate1Larsson and Lönnborg 2007, p. 89; Lönnborg and Larsson 2015, pp. 248-249,2The first joint-stock underwriter Skandia was launched in 1855.3Lilljegren (2018).4Lönnborg and Larsson 2015; Hallendorff 1923.5Bartley and Schneiberg 2002, p. 96.6Baranoff 2003, p. 124.

1

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

was secondary. The agent thereby functionedas a local and socially embedded extension ofthe underwriter. The implications for the un-derwriter were profound, since core decisionsin the risk-management were outsourced tothird-parties and based on their judgement ofthe trustworthiness of people. In Australia, theagent system made market entry easier, sinceit lowered the costs of establishement on a mar-ket with little or no regulation during the turnof the 19th century.7 The agent system shouldalso have worked as a stabalizing factor on thetariff agreements.

Intermediaries on the market, like insur-ance agents, provide some noticeable marketadvantages, but are simultaneously the sourceof an organizational dilemma for firms. Chan-dler touches on the importance of informationcosts in the example of organizational solutionsfor the distribution of sewing machines givenin Scale and Scope. Singer and McCormickmoved towards retail networks which wouldprotect producers from incompitent and in-effective intermediates, but still provide thefirm with an efficient market reach.8 The prob-lem was the technological threshold that theadvanced machineries could not be easily re-paired, explained, or even efficiently marketedby too under-qualified retailers. The dilema forinsurance firms vis à vis their agents is simi-lar. The complexity of the product demandsqualified distributors, and the agents missionexcedes the task of only selling the productas they also instruct and repair (as the case ofsewing machines) and perform other actuar-ial services for the firm (as was the case withSwedish insurance agents).

As mediators of underwriting services,Swedish insurance agents solved problems ofdistribution, trust, and matching, but also rep-resented an organisational challenge to the un-derwriters. In the early 20th century, the indus-try itself felt that efficient competition was hin-dered by the agents’ lacking ability to correctly

inform clients about significant differences inprice and policies.This in turn contributed tothe underwriters joining in collaborative effortsto standardise premiums and risk tariffs. Tariffstandardisation was indeed the outcome of sev-eral kinds of intense cooperation and variousforms of inter-firm networks between compet-ing underwriters in the first half of the 20th

century.

The distribution of insurance is very mucha market-matching problem as described intransaction cost economics.9 For a customer tobe able to buy insurance, which, already inthe 19th century were contracts of high com-plexity, they would have to gather informationabout market alternatives at the cost of theirinvested time. The looming uncertainty thatunderwriters would not honour their contractspost-hoc, would also constitute a barrier to in-vesting in insurance, and consequently thatbarrier would be lowest where the customer’suncertainty about the underwriter’s abilitiesand intentions would be the lowest.To the un-derwriter, on the other hand, uncertainty bar-riers include moral-hazard, - most of whichaccurate information about underwritten ob-jects help reduce uncertainty.

Social relations between buyer and sellermay operate as a a hurdle to keep oppor-tunistic behaviour at bay and stabilise trans-action costs by lowering uncertainty.10 Anothercrucial resource to underwriters is the qual-ity information about the very object they un-derwrite.Drawing from evidens in this article,Swedish underwriters seem to have organizedaccording to vastly different strategies of risk-reduction.11 They had a strategic choice be-tween developing social relations of deepertrust, or to reduce uncertainty about risk-levelsof its insured property. This strategic choicewas very much related to geographic proxim-ity to the market and the need (or not) to useagents for distributions.

7Keneley 2002, p. 58.8Chandler and Hikino 1990, pp. 66-67.9Jones 1997, p. 17.

10Williamson 1979, p. 240.11Adams et al. 2012.

2

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

II. Method and source data

The analytical contribution of this paper isbased on two separate datasets of network rela-tions between property underwriters. The firstconsists of 19th century insurance agents andtheir affiliations, and the second of 20th cen-tury co-insurance relationships. A systematicscrutiny has also been made by the availableproperty underwriters’ agent-bulletins. Thesewere publications issued by insurance compa-nies directed to its agents around the country.These include Hanseaten which was issuedby Hansa (1913-59),12 Malmogia was issued byMalmö (1929-1943), and Kontakten served allthree of the underwriters Fylgia (1911-1929),Valkyrian (1916-1929), and Land och Sjö (1918-1929). Trafik-bladet for Trafik (1930-1965)12

as well as the respective bulletins by Nornan(1918-1943) and Skandia with its subsidiaryFreja (1906-1919). The different bulletins servelargely the same purpose. To maintain con-tacts and information channels with agents.13

The bulk of all content consists of 1) informa-tion about new tariffs and insurance rules, 2)company performance over the past years, 3)encouragement to agents to sell more, workmore, and generally act to the pleasing of themain-office. Several bulletins have competi-tions for their agents where biggest sellersare published. Particularly the aggressivelygrowing Trafik makes a big deal about agent-performance in its bulletins Trafikbladet. Issuesare 4-6 pages, but sometimes up to 10. Kontak-ten, which is Fylgia’s bulletin, is often longerand carries a different and more well-writtenliterary tone. While all companies bulletinsnag about the shortcomings of agents and urgethem to work harder or more meticulously,only Kontakten do it in the shape of a two-pagefirst-person semi-fiction drama featuring its au-thor and how he is being asked by the directorof Fylgia to share in writing the company’sview on its conflicts with its agents.14 Skandia’s

buletine is on the contrary very dry, and mostlyfilled with statistics and reports of agents earn-ings and firm performances. The analysis alsodraws on a literary review of contemporaryinsurance journals and secondary sources ofpreviously conducted company monographsof 25 contemporary property underwriters.

The data of the network of insuranceagents was printed in the insurance journalFörsäkringsföreningens tidskrift 1885-86, and ina separate, and unique, publication from 1889that list all major underwriters with affiliatedactive agents per-city.15 This source constitutesan inherently bipartite network data, and canbe formalized as such to treat the data as a net-work graph. In such a network, agents can belisted in a vector V = {a1, a2, a3, ...} of agentsai ∈ V, and all companies in another vector likeF = {x1, x2, x3, ...} where (xj ∈ F). Considerthat agents are tied to firms in connectionsdenoted eij, and that connections must be di-rected so that directed ties are formed runningfrom agents to firms (ai → xj). A list of suchconnections can be expressed as a third vector,E, where eij ∈ E : i ∈ V : j ∈ F. The ensembleof firms, agents, and their connections makeout a bipartite network, commonly denoted asa graph G(V, F, E).16

The 20th century co-insurance source-material has been collected from the insur-ance periodical Gjallarhornet (1810-1940), wherelarger fires-events have been coded from in-magazine news articles. Every fire is listedalong with all participating directly underwrit-ing firms. This fire-event database has beenused in Lilljegren and Andersson 2014 to deter-mine market-segments in fire insurance. Hereinstead, the data is re-coded as a networkG(D, F, E) where D is a vector of fire-events, Fis a vector of firms (as above), and E is a vectorof ties, eij, running from firms to fire-eventswhere eij ∈ E : i ∈ D : j ∈ F.

Each data source suffers from limitationsin terms of missing firms or imprecise data.

12Only issues up until 1940 have been thoroughly investigated here.13Nornan (1918) No. 1; Malmogia (1929) 1:1; Kontakten (1918) No. 2 and 614Kontakten Jubileumsnummer (1921) p. 22-23.15Assurans-Tidning 1889.16Brandes and Erlebach 2005, pp. 7-8.

3

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

It is still possible to draw several conclusionsabout the firms bargaining with its agents andchanging strategies of distribution and market-matching. Precious little has been writtenabout Scandinavian insurance agents, and nooverwhelming attention was given the some-times complicated firm-agent relationship incontemporary literature of the era. Withoutbeing able to paint a complete picture, thisstudy hopes to add to the understanding ofthe market dynamics and development of thisimportant industry.

III. Market structure

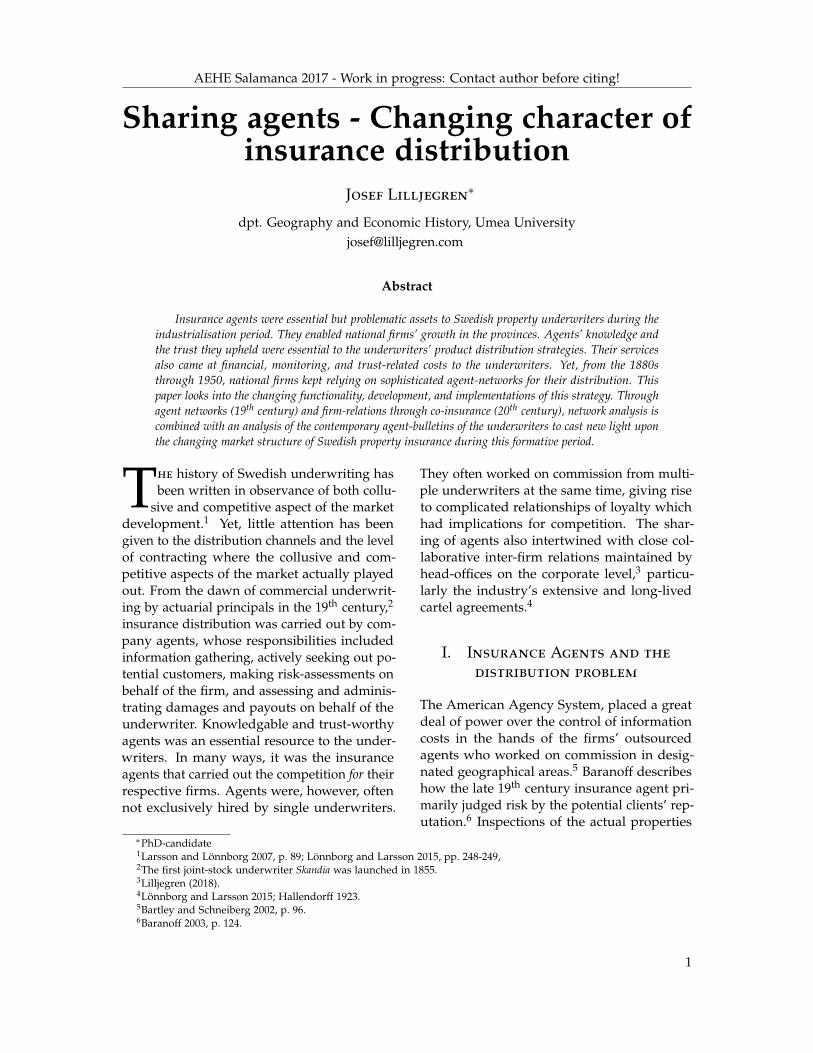

The market of Swedish property underwriterswas dominated during the entirety of this pe-riod by national big firms. The 19th centuryfirst movers of Skandia, Skåne, Svea, each themajor underwriter in Stockholm, Malmö, andGothenburg respectively, maintained strongmarket positions well into the 20th century, andstill exist today in the shape of newly mutual-ized Skandia. During the the 19th century, othermajor players were marine underwriters Ocean,and SÅAF, and, during the first half of the 20th

century, fire insurers Städernas Allmänna andFylgia.17 The market share of the top four na-tional underwriters (as measured by premiumincomes and shown in figure ??) never fellbelow one quarter of the national premiumincomes.17.

With competition from a growing num-ber of property underwriters during the peak-years of the Swedish industrialization in the1880s, the market underwent several notewor-thy structural transformations. The rise of rela-tively big national firms organized as mutualfirms competed against the joint stock compa-nies in a spirit of mutual animosity described

as the controversy of principals.18 By 1903, contro-versy was resolved, and the first national insur-ance regulation was put in place witch harmo-nized conditions for underwriters. In the firstdecades of the 20th century, mutual firms be-gan mimicking joint-stock business models oflarger reserves, steady ex-ante premium-flows,and line-diversification.They also increasinglyjoined the national (and numerous) cartel or-ganizations where premium rates and (increas-ingly) actuarial risk categories were agreedupon between member firms. The first car-tel was the fire-cartel launched in 1873,19 andremained active through 1963. The first halfof the 20th saw an increasing number of sub-market cartels, where by the 1920s, virtuallyevery line of property insurance, from bicycleto water-pipe insurance, was regulated withinper-line cartel collaborations.20

A relatively small but numerous foreignfirms never enjoyed large market-shares in theSwedish property market during the period.21

Domestic firms also acted to push foreign firmsout of the market as they made for unrulycollaboration-partners and unwelcome under-bidders of the domestic firms cartelised pre-miums. Some foreign firms nevertheless didcome participate in the cartel collaborations.22

While property insurance originally con-sisted mainly of fire and marine insurance, themarket segments of other lines grew consid-erably during the early decades of the 20th

century.21 Fire and marine insurance had com-fortably made up over 75% of all property in-surance until the 1910s, but then sank to hoveraround 40% and 20% respectively from the1920s onward. A wide range of new smallerlines gained momentum in the early decadesof the 20th century, and the market share oftraffic insurance in particular grew rapidly and

17Market concentration and dominating actors based on ranking of premium incomes from property underwrit-ing (all lines) of all listed Swedish insurance companies per year: Försäkringsväsendet i riket (1889, 1899); EnskildaFörsäkringsanstalter (1916,1930,1950).

18Bergander 1967, pp. 334-335; Boksjö and Lönnborg 1994, pp. 141-14219Hallendorff 1923.20Lönnborg and Larsson 2015.21Försäkringsföreningens Tidskrift (1878), and public statistics: Försäkringsväsendet i riket (1889, 1899, 1910); Enskilda

Försäkringsanstalter (1916,1930,1950).22SFT (1920, 1930, 1940, 1950).

4

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Figure 1: Market concentration (RC4) by premium incomes in property insurance 1880-1940.

.2

.3

.4

.5

.6

Mar

ket c

once

ntra

tion

(CR

4)

1875 1900 1925 1950Year

was a major branch of property the total prop-erty insurance market by the 1930s. Accidentinsurance (grouped into the Swedish firms’ def-inition of property insurance as all non-life andnon-health insurance) was also a major marketsegment with double digit percentages of alldomestic property insurance premiums frombefore the turn of the 20th century and through-out the period.

A parallel, and for this paper, importantsub-market division existed in the division be-tween national and local underwriters. In thelines of fire, livestock, and sometimes marineinsurance, very local micro-insurer also com-peted for insurance customers. They were,much smaller than their national counterparts,sometimes with few more than hundred mem-bers, but were much more numerous.23 Theseorganizational forms have been found to con-centrate on different market segments,24 and tocompete with different advantages.25 Smallermutual underwriters concentrated more ho-mogenous non-industrial risks. Rural under-

writers also relied heavily on the closeness totheir market, where they could keep checks onmoral-hazard and face capital deficiency prob-lems by trust-based ex-post premium systemswithin smaller groups of arms-length insuranceclubs.

IV. Local firms without agents

Smaller firms of micro-insurers had no out-of-town agents. A rather different model wasemployed which nevertheless was driven bythe same reliance of social trust. The boardsof smaller mutual firms were often directly in-volved in 19th century underwriting decisions.Their company structure had emerged directlyfrom the institutionalized form of insuranceof brandstod, where local clubs were obligedby law to help victims of disastrous fires. Themandatory brandstods were abolished in 1853.When these clubs were made voluntary, mem-bership, often formalised in resemblance of thebrandstod, as ex-post premiums, remained a

23Larsson and Lönnborg 2007, p. 87; Bergander 1967.24Lilljegren and Andersson 2014.25Adams et al. 2012.

5

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

strictly local affair. In the surrounding decades,hundreds of brandstod-associations were formedin this manner. The socially forged trust andinformation transparency of arms-length un-derwriting engagements proved to be a sus-tainable organizational solution well into the20th century (judging by the number of prevail-ing micro-insurers). Their size, however, wasstrictly confined to the reach of their competi-tive information and trust advantage which inturn relied a sociogeographic cohesion.

In somewhat larger local mutual under-writers, boardmembers played the agents’ rolein over-bridging problems of information andtrust. Both enjoying the mandate. These firmstypically had larger boards (which is tellingfor the direct overlapping with operational ac-tivities that the board had). The directoratesof smaller local firms like Västernorrlands länsbrandstodsbolag were directly involved in theestablishment of contracts and the decisionof payouts.26 It was to the the board, person-ally, that customers turned to pay premiumsor claim damages. Even the comparativelylarge (10’914 owners in 1875, and 18’489 own-ers in 1939)27 mutual local underwriter Wil-lands, Gärds och Albo Brandförsäkringsbolag rantheir offices from the private home of the com-pany secretary cantor M. Cederholm in his villain rural Köpinge.28 Local insurance men, likeM. Cederholm, had local knowledge and con-nections, were nevertheless steadily membersof a local socioeconomic elite. The c.e.o. ofthe regional company Östergötlands nya brand-stodsbolag would literally inspect the risks ofupcoming contracts or recent fires himself.29

To these local companies, a common asset oftheir in-the-field directors, was their knowl-edge and submersion into local structures oftrust and reputation. This helped them makeactuarial demissions that were both based inlocal socially structures which simultaneously

upheld the tenability of those decisions. It isarguably harder for an insurance customer toact recklessly with his insured property, if theunderwriters chairmen (and fire inspector) isalso his neighbour - or indeed any person oflocal significance and reputation.

Local firms did feel the tension of competi-tion with national firms due to the differencesbetween the actuarial and the trust-based mod-els.30 Many local firms had applied minimaldifferentiation of risk classes, partly becauseof the wide homogeneity of their rural risk-objects.The increased diversity of fire-hazardsdue to technical change (electrification, ad-vancements in building techniques, new ma-terials, security regulations etc.), local under-writers’ advantage from homogenous risk de-creased. Another important reason for the localfirms lack of tariff systems was that they longoperated in a spirit of social equality and char-ity.31 It was not the wish that one poor farmershould have to pay more for his insurance thananother poor farmer, merely because they hap-pened to have differently designed chimneyswhich caused one of the farmers to be at muchhigher risk. Consequently, many local firmsresisted tariff differentiation for its membersas long as possible. In 1890, local underwriterÖstergötlands moves to differentiate tariffs as aresult of too high losses in industrial risks32 Atthe same time, national firms were pushing forstrategies of increased actuarial sophisticationas a means of competition, and as a way toovercome their uncomfortable reliance on theirlocal agents and their knowledge.

V. National Firms

Agent-relations

The insurance agents of national firms filled asimilar function. The 19th century Swedish un-derwriters appreciated the agents’ “knowledge

26Silén 1944, p. 81.27Fredrikson 1937, pp. 80-82.28Fredrikson 1937, p. 62.29Petersson 1941, p. 27.30Petersson 1941, p. 83.31Petersson 1941, p. 83.32Petersson 1941, p. 28.

6

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

of people and circumstances at their location”.33

National underwriters, on the other hand,could not approach the local markets with thesame ease. Where local firms relied on so-cial arms-length connections, national firmsbalanced the social trust confined in theirinsurance-agents with geographic reach, het-erogenous risk-pools, and actuarial principals.Underwriters regulated the risks they wantedto underwrite by thorough instructions toagents. The 19th century instructions, how-ever, emphasise the social cognisance of agents,and sometimes seem vague on actuarial de-scriptions of fire hazards. Categories such assawmills, warehouses, theatres, etc. are listedas particularly hazadrous by Svea, and the firmadvices its agents to pursue the underwritingthereof with caution.34

The larger firms have a complex trust rela-tion. In many ways, the national underwriterswere unhappy with the efficiency and relia-bility of their agents, while at the same timebeing crucially dependent on them. They de-pended on agents for their local trust, con-tacts, and knowledge, but they are venerableto their incompetence and dishonesty. Swedishlife insurers also suffered from lacking edu-cation in agents, which they pinpointed as aproblem for distribution in the 1800s.35 In itsagent-instructions from 1887, Svea threatens theagents with responsibility for error in hazard-reporting in the events following a fire. Theyalso admit their responsibility to uphold thecompany’s trust as a firm that stands to itscommitments in spite of incompetent agents.They then urge agents to come clear to the firmabout any “the agent at the establishement of theinsurance contract ” so that he may be warnedby the board, but thereby also ensure his futuretrust by the firm. The firm explicitly says that

such openness will be regarded as a reassur-ance against similar mishandling reoccurringin the future.36

Agents were expected to represent the com-pany’s interest immediately after fires. Theyurged their agents to physically go to ensurethat all necessary efforts were being made toprotect the firm from further liabilities andfrom moral-hazard in the salvage of undam-aged assets and movables. SVEA[56] Theyshould also encourage speedy execution of apolice-interegation (where the agent shouldseek to be present) in which the cause of thefire can hopefully be established. 37 To thisregard, the distribution system of agents andthe agents’ responsibilities remained strikinglysimilar into the 1940s.38

The map in figure 2 shows the geograph-ical location of major property underwriters’agents. Large concentrations of agents occurin the larger industrial and port cities. Thecapital of Stockholm had 86 operating in 1889,several of which acted as agents for multiplecompanies. The geographical distribution ofagent is telling for the national reach of themajor underwriters, and also largely mimicsthe patterns of populated and industrial centaof the country.

An alternative organization would havebeen to establish branch-offices. To large na-tional firms, however, the establishment of re-gional in-house branch offices was too costlyand never really considered.39 The thresholdcost per branch office was too high, and sowas the number of offices needed to create thedesired geographic reach. As with Chandlersexample of the Singer sewing machines men-tioned in the introduction, underwriters facedtheir own dilemma with the agents.

33Svea 1887: In Swedish: “kännedom om personer och förhållanden inom sin ort”.34Svea 1887, pp. 22-23.35Boksjö and Lönnborg 1994, p. 143.36Svea 1887, p. 53: (In Swedish) “borgen för att dylika [misstag] derefter skola unvikas”.37Svea 1887, p. 60 (§84).38SOU 1949:25 p. 1839In insurance company monographs (published as company historiographies, often to commemorate firm anniversaries)

no mentioning of considerations of a system of branch offices for distribution has been found after scrutinising thecompany histories of 25 Swedish property underwriters with available publications.

7

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Figure 2: Geographic distribution of agents

0 100 200 300 km

Gothenburg

Helsingborg

Malmö

Stockholm

N

1

10

100

A diffusion system of agents offered de-creased tangible costs for opening branch of-fices. They also reduced a much less tangibletransaction and information cost for the under-writer. Agents could 1) decrease risks of moralhazard through their geographic presence, 2)overcome information-problems through localknowledge, 3) actively seek out customers inorder to underwrite their risk ahead of com-petitors, and 4) be the vessel of the trust neededbetween underwriters and customers in orderto establish underwriting contracts. On theother hand, agents also created a trust-problemfor underwriters. When delegating the market-matching to third-parties, firms could not beentirely sure that their interests were being

well represented. That risk applied to the mainfunctions of the agent, namely the carrying outactuarial due-diligence, information gatheringand reporting to head-offices, the correct assess-ments of damages, and upholding of the firm’slocal reputation were important functions. Yet,the tradeoff between the loss of market controland the costs for alternative strategies of dis-tribution seem to have remained clear for thenational firms.

But why did small local firms not get agentsin other cities? There were several reasons.Firstly, they operated in a club-like spirit ofcharity, to which growth outside arms-lengthwas seen as an unnecessary risk. Smaller firmshad a not so developed tariff-system, and dur-ing the 19th century, many of them operatedon flat-rate premiums. The maticulous divisi-son into adequate premiums corresponding tothe underwriting risk allowed national firmsto economize on underwriting costs to financeagents, but was also part of the few monitoringand control tools that national underwritershad on agents. This tool would have been lack-ing for smaller underwriters. Even regionalmutuals pushing 20000 customers could main-tain competitive advantages from local socialembeddedness and . That was a firm orga-nization that was ill-adapted to the scale ofcoordination needed to administrate a networkof agents. General trends of the adoptationof smaller mutual firms cause them to differ-entiate their tariffs and enlarge their opera-tive boards as they grow, but only a few re-gional mutuals switch direction and transforminto companies of national reach. One suchcompany was Göta. Göta struck a deal withanother property underwriter, Tor in 1907 inorder to get access to reinsurance.40 Reinsur-ance access required previous steps away fromthe micro-insurance trust-based organizationalmodel since a precisely defined tariffs (prefer-ably along lines of the cartel organization) wasneeded.41

40Linn 1966, pp. 44-45.41Petersson 1941, p. 83.

8

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

VI. A network of agents

Agents were the national firms’ replacementfor the resource of local arms-length relationsto customers which they could not achieve attheir levels of operational scale and geographicscope. Gustav Dahlgren was the agent of threefirms in 1889, even though the firms listed himas their agent in the two separate localities ofBosäter (for Ägir) and Hemsjö (for Sverige, andFylgia). It is rare that the agents act in differentlocalities. The few cases encountered in thedatabase, are, like Bosäter and Hemsjö, loca-tions within a few hours bike-ride of distance.Even though the distance is not negligible, it isstill quite possible for the persons to maintaintheir local affiliation and reputation in bothplaces simultaneously.

Looking at figure 1, the extent of co-usageof agents in 1889 reveals some interesting cir-cumstances. All larger firms had shared agents.The portion of each firm’s agents which wasshared with other firms varied between 28%and 60%. A significant number of every reg-istered firm.42 It also seems like the numberof agents used does not correspond linearlyto the size of each firm. Though Skandia wasbigger than Fylgia at this time (in terms of do-mestic premium incomes), the latter firm hadalmost twice as many agents. This was due tothe placement of agents in more, and smallerlocations around the country rather than theuse of several agents for the same cities, eventhough most companies also had several agentscovering the larger cities.

Table 1: Agents of firms in 1889

Company AgentsShared agents

Total Percentage

Fylgia 272 133 49 %Gauthiod 15 9 60 %Ocean 38 12 32 %Skandia 149 53 36 %Skåne 151 43 28 %Sthlm. Sjö 33 13 39 %Svea 144 48 33 %Sverige 134 69 51 %Sv. Allm. 22 12 55 %Sv. Häst 133 54 41 %Ägir 84 36 43 %

.Source: Assurans-Tidning 1889; SFT 1885-1887.

A different social dimension can be seenin the agent network in that members of thesame families show up as agents for firms inlocations of close proximity. The Schmidts inthe Malmö area. Major C. J. Schmidt was theagent of Skåne in Malmö, and shopkeepr H. J. A.Schmidt in neighbouring Landskrona. It couldalso be due to the overrepresentation of socioe-conomic elites in prestigious positions of re-sponsibility (as which insurance agents clearlyqualified at this time).43 The noble family vonSydow for example had family members asagents in both the cities of Jönköping andLund.44 Interestingly, the majority of agentswith noble names in this dataset were simulta-neous agents for more than one underwriter,while the average number of firms per agentin the whole dataset was .

The maintenance of the agent network,through which every individual insurance con-tract flowed to the main offices, required a highlevel of systematization and efficiency in thefirm-agent communication. The 19th century

42In this working paper, all data for 1889 has not been processed. There is public statistics for more firms whencombining data for 1886. It is highly likely that the share of shared agents per firm would rise with the addition of newfirms since the number of agents |Va| of firm a would not be affected by the number of agents |Vb| of firm b even though itis likely (given the current descriptives) that |Va

⋂Vb| > 0.

43Rothstein 1998.44Svea 1887.45Svea 1887, p. 75 (§117).46Svea 1887, p. 55.

9

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Firm

Shape by institution

Colour by agent out-degree:

Individual

Underwriter1 firms2 firms3 firms4 firms5 firms

Figure 3: Property underwriters and their agents 1889

costs of communication forced national firmsto advice agents to limit the use of efficienttelegraphs.45 The use of such information tech-nology was costly, and Svea instructed theiragents not to telegraph head office to informabout fires in their vicinity unless really neces-sary.46

In the 20th century, the communicationtechnology enhanced dramatically with the in-troduction of phones and new storage andfiling systems for contracts and actuarialdata.Modern writing and calculation machinewas described as essential to the central officeof Fylgia in the early 1910s.47 These inovationshelped to speed up the information flow, al-lowed national firms who could offord to investin them to act quickly against insurance fraud.In spite of telegraphs, central fire-inspectorsfrom Stockholm, could take days to arrive atthe scene of an insured fire in the provinces.The increased accessibility to provincial townthrough the railway network which expanded

rapidly during the final decades of the 19th

century also shrank the time- and cost- thresh-olds for companies to send out central fire-inspectors to verify agents’ reports and fire-damage assessments before approving payouts.In the 20th century, still, however, the largernational firms kept relying on agent structuresfor damage assessments of all smaller fires.

The sharing of agents could also have hada stabalizing effect on cartels. Stigler statesthat the assigning of one single seller for goodsof many companies undermines the possibil-ities for firms to violate cartel-agreements byunderbidding their fellow price-fixers.48 In ad-dition, the harmonization of tariffs were mea-sures taken by firms in order to decrease thefriction of having to rely on agents.

Firms profited from co-agents in other waystoo. The established customer channels of oneagent were an important resource, and whenfirms shared agents, they could use that con-tact to sell non-competing insurances to other

47Kontakten (1911) No. 448Stigler 1964, p. 47.

10

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

firms customers. Nornan, a firm specializedin a wide range of smaller lines of insurancehas numerous agents that worked principallyas fire-insurance agents for Svea in the 1910sand 1920s. While Svea’s clients were alreadyinsured against fire, water-pipes, burglary orglass-window insurance (which Nornan pro-vided) were not part of Svea’s contracts. Con-sequently Nornan urged its shared agents touse their double agency to sell Nornan’s insur-ance to Svea’s customers.49 This led to agentsplaying an active role in another important risk-sharing strategy of the national underwriters,namely co-insurance.

VII. Risk management and

Co-insurance

Co-insurance is the practice in which severalunderwriters are direct insurers of the samerisk. It is different from re-insurance in which adirect insurer underwrites risk, fractures it intosmaller portions and seeds parts of risks to re-insurers. Swedish reinsurance practices of thelate 19th and early 20th centuries built on sev-eral standardised but sophisticated contractualstandards of splitting up and passing on risk toreinsurers.50Mostly stock companies used re-insurance as a risk management strategy in the19th century, and domestic re-insurers emergedas Swedish underwriters sought alternativesto seeking re-insurance on the continent. Inthe late 19th century, a developed, global in-ternational reinsurance market was dominatedby German and Swiss multinational actors.51

This global market initially enabled underwrit-ing of large risk-objects in late industrializerslike the Scandinavian countries.52.In Spain, thereinsurance-market at this time was charac-terised by a need for risk-spreading pushedby capital-constraints on a domestic market

and a consequently strong presence of foreignreinsurance companies.53 In Sweden, however,domestic reinsurance companies emerged asalternatives to reinsurance on the continent al-ready in the last quarter of the 19th century,often launched as subsidiaries to the largestmarket players. With the subsidiary solutions,companies, like Skandia could maintain in con-trol also of the reinsuring firm, and reinsur-ance became a risk-spreading strategy whichwas entangled with the ownership structuresof the underwriting firms themselves.54 Thisorganizational solution also helped dodge thepotential cost for risk-spreading through re-insurance since reinsurance premiums werecollected by subsidiary firms which payed div-idends to their mother-companies.

The aim of better risk management thoughsmaller bulks of risk at big numbers remainsimilar in the co-insurance practice. While co-insurance does away with the additional pre-mium with which the underwriter pays thereinsurer for the service of spreading its risks,co-insurance was affiliated with other costs re-lated to 1) matching and 2) trust. In order toestablish a co-insurance contract, several directunderwriters would have to be able to simulta-neously establish a contract of underwriting arisk which they all agree on. Theoretically, allsimultaneous direct underwriters must haveevaluated the risk in question is tannable. Thiswas already a task which national underwritershad sublet to the insurance agents, and there-fore agents played a crucial role in resolvingthe matching problems of underwriting carriedout as co-insurance.

During this period. Co-insurance seems tohave occurred through two main practices. Thefirst emerged dynamically through peu-a-peuinsurance 55. A factory might first have had itsmachines insured by firm A, and its factory-

49Nornan (1921:5).50Holmgren and Lindbohm 1939.51pearson_development_1995.52Bergander 1967.53Gutiérrez González and Pons Pons 2017.54Skandia (1906) October, p. 6.55Kontakten (1919) No. 10 p. 4.56Gjallarhornet (1929):When the mansion of the pulp factory Rottneros (still an active company today) burned on

11

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Table 2: Co-insurance in fire-insurance 1917-1940

Period Large fires Avg. damages†Direct underwriters per fire

Total Percentage

1917-1924 27 0.93 18.77 211925-1928 52 0.2 6.85 51929-1931 40 0.74 8.27 61932-1934 36 1.53 5.63 51935-1947 63 2.28 5.79 61938-1940 47 2.57 9.31 7

.† Average damages per large fire in million Swedish crowns at 1913 prices deflated by consumer price index.

buildings insured at a later time by firm B.Both direct insurers would have to honour theircontracts in the event of a disastrous fire.56 Thesecond emerged as multiple firms were able toshare direct insurance through agents whichwere able and encouraged to split larger risksbetween multiple firms at the moment of un-derwriting.57 In spite of the largest compa-nies financial muscles, they much preferred tounderwrite smaller stakes in industrial risks,and encouraged their agents to arrange suchconstellations.57 Such co-insurance contractswere drawn up with participating firms statingthe shares in total losses according to whichthe damages would be distributed amongstco-insurers.58

The co-insurance practice demanded themutual trust and agreements of the underwrit-ing boards. In 1907, Göta struck a deal withTor to share co-insurance contracts in a colab-oration deal that enabled both firms to growand take on more risk in spite of financial con-straints.59 The deal was indirectly a result ofthe social contacts with Stockholmian firmslike Tor that the formally regionally based firm

of Göta had acquired when recruiting a c. e. o.from the capital that year.

VIII. The use of co-insurance

From the biggest fires in Sweden between 1917and 1940, only 52 (or 16.3%) were insured bya single direct underwriter. 60 The rest hadmore then one underwriter that co-insured therisk, agreeing to assume a partial risk, and toshare the remainder with “competitors”. Thisdata stems from a total of 287 major fires thatwere reported in news items in the insurancejournal of Gjallarhornet. The reports often con-tained detailed actuarial information, such asinsurance sums and details of underwriters lia-bilities. It is important, however, to rememberthat the largest fires, with the largest losses,make out an extreme segment of the under-writing risk.

Some descriptives of the co-insurance infire-insurance are summarized in table 2. Thelarge fires are distributed in key periods withan uneven average number of fires per yearbeing as the frequency of large fires varied,

December 13th 1929, national stock-company Svea was the sole underwriter of the damaged inventory. The house, however,had been co-insured between Svea and a mutual firm: Allm. Brandförsäkringsverket. .

57Skandia (1920), september58Lönnborg and Larsson 2015.59Linn 1966, pp. 44-45.60Gjallarhornet (1910-1940): Note that the minimum, mean, and maximum numbers of directly co-insuring firms were 1,

5.05, and 31 respectively, and that a tail of only 30 fires had 10 direct co-underwriters or more.61The source, Gjallarhornet, states that it prints news items on larger fires with damages above a certain threshold value,

but their accuracy has not been controlled or triangulated. Single fires of the database can be traced and confirmed invarious ad-hoc secondary sources, but the information about insuring companies is often missing there. Fires overlookedby Gjallarhornet would be missing from the database without any satisfactory way of investigating any possible biases in

12

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Figure 4: Co-insurance networks in larger fires

(a) 1925 (b) 1931 (c) 1940

National mutual firm National investor owned firm Local or regional small firm

but also due to some inherent inconsistenciesin the source.61 The damages (in fixed prices)of the larger fires generally rise during thetwo recorded decades from below one millionSwedish crowns in the 1910s and 20s, to abovetwo million in the late 1930s. Some exceptionalfires in the 1910s had a huge numbers of simul-taneous direct insurers. The median number ofco-insuring firms per fire, however, remainedbetween 5 and 7 for most of the 1920s and 30s.Conclusively, large fires were generally insuredby several direct insurers as once.

The extensive co-insurance over the era areshown in a collection of network-graphs (figure4 of co-insurance leading up to the years 1925,1931, and 1940 respectively. The connectionswere so numerous that most firms had somekind of co-insurance arrangement with mostother firms. Future network analysis, like cor-relating network statistics with company prop-erty, or modelling the network structures withexponential random graph models (ERGM:s),could give further insight into the underlyingdeterminants of the network structures shownin the figures 4. By only analyzing the descrip-tives, however, a most striking difference in op-erational strategies between firm-types standsout. On a sliding scale, local micro-insurers,national mutuals, investor owned stock com-panies, and foreign firms seemed to premiere

different types of risk-distributions and choos-ing risk-objects by different means.

Figure 5 shows histograms of the directunderwriters’ share in total damages in all reg-istered larger fires 1917-1940. Few of these fireswere insured in only one company, and con-sequently, each company’s responsibility wasoften less than 100% of total damages. Thesubdivision by company type reveals differentstructures of risk-taking in firms of differentorganizational forms. Investor-owned firms(figure 5), has a higher relative frequency ofsmaller shares of direct co-insured risk thanmutual firms (figure ??). Literature drawingon ??? has predicted that mutual firms, dueto agency implications, are more likely to in-sure heterogenous risk. They would rely onlocal knowledge and social trust to dodge in-formation asymmetries and the risks associ-ated with moral hazard. As a consequence,they would be relatively more inclined to takelarger chunks of risk and forego the law ofbig numbers as their access to accurate localinformation would be better than that of stock-companies. Stock companies on the other hand,who lack the access to local information of mu-tual firms, would have to rely on the law of bignumbers and actuarial principals to a largerextent relative their mutual counterparts. Theywould thereby be more inclined to seek smaller

the source publication.

13

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Figure 5: Distribution of risk-shares in coinsurance (by firm-type)

0

20

40

60

Freq

uenc

y

0 .2 .4 .6 .8 1Firm's share of total damages

(a) National mutual firms

0

50

100

150

200

Freq

uenc

y

0 .2 .4 .6 .8 1Firm's share of total damages

(b) Investor owned firms

0

50

100

150

Freq

uenc

y

0 .2 .4 .6 .8 1Firm's share of total damages

(c) Foreign firms

0

5

10

15

Freq

uenc

y.2 .4 .6 .8 1

Firm's share of total damages

(d) Local and regional firms

direct shares in co-insurance contracts, whichseems supported by the steeper slope in figure??.Stock companies preferred smaller shares oftotal damages.

On the other two extremes are foreign firmsand local an regional micro-insurers. The lat-ter company type often held large stakes inthe biggest fire-damage payouts. In spite oftheir small size, and lesser ability to dodgeexceptionally large claims, their risk was verybulky. Foreign firms, on the other hand, oper-ated with very small co-insurance shares in thelargest fires (see figure ??). There are severallikely explanations for this.

Firstly, the operational strategy for diffu-sion and use of agents probably payed a cru-cial role. Smaller firms, which operated onqualitative, socially acquired information aboutrisk objects, naturally had a smaller reach, anddid not rely on an agent-network for contract-matching. National firms, who relied on agentsfor a wide geographic reach, operated the un-derwriting business on actuarial principals for

which the micro-insurers did not have the tech-nological and informational capacity. Armedwith fire-statistics and the law of big numbers,national firms would prefer to keep a largenumber of (preferably smaller) underwritingengagements to spread risk. They could alsoincrease their risk appetite by increased ad-hocknowledge about risk objects through contactswith insured industries, collaboration withfactory-owners over security enhancements,62

and arms-length trust and obligations betweeninsured and insurer63. These were closenessesthat local underwriters would have had inabundance, but which were harder to estab-lish for foreign firms, in spite of local agents.Being as co-insurance of the second type cameabout though the sharing of insurance agents,and that insurance agents were the large na-tional firms’ solution to a distribution problem,local and regional firms had a weaker presencein the co-insurance contracts.

The risk distribution may also have implica-tions for the understanding of the usage of re-

62Götherström 1941.63En massa referenser till mikro-insurer monografier

14

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

insurance. Co-insurance seems to have madeup an alternative to re-insurance in terms ofactuarial risk management.This study has got-ten no insight into wether co-insurance andre-insurance was regularly combined by under-writers, or mutually excluding. Either way, theneed for re-insurance to receive smaller blocksof direct risk must have been diluted by co-insurance practices - at least in the subsectionof large-risk fire-insurance where co-insurancewas common. Stock-underwriters have pre-viously been found to use re-insurance to alarger degree than mutual firms.Given thatthey also prefer smaller direct stakes in co-insurance schemes, stock company underwrit-ers come out as even more driven by the wishfor smaller risk-objects and risk-managementalong actuarial principles.

IX. Conclusion

This paper has looked into the role of insur-ance agents to the operation of Swedish prop-erty insurance firms during industrialization.The use of agents related closely to the opera-tional model and distribution strategies of un-derwriters. Several underwriters could sharethe same agent, both as a compromise by un-derwriters which desired to be present at acertain geographic location at a cost, but alsosymptomatic of a collaborative spirit of trustbetween the underwriters. Shared agents fa-cilitated co-insurance, in which direct insurers

could share a single policy proportionally withother direct underwriters resulting in lowertransaction costs (by avoiding commissions forreinsurance) and smaller direct risk-objects foreach underwriter. Agent networks thereby hadgeographic, actuarial, and collaborative impli-cations to underwriters.

On a scale between underwriting based insocial trust and local knowledge on one hand,and actuarial principles and the law of bignumbers on the other, stock companies po-sition themselves further out than their mu-tually owned counterparts. Even further out,more estranged to allowing local knowledge ofrisk-objects and trust-like relations with theirowners prop up the underwriting contractsare the foreign firms. Their shares of dam-ages in the larger fires were even smaller thanthe domestic stock companies. The risk-sharesseem to relate to the operational peculiarity ofmicro-insurers,64 in that they are the most re-liant on locally embedded and socially drivencontrol mechanisms for risk management. Theoperational strategy for diffusion and use ofagents probably payed a crucial role. Smallerfirms, which operated on qualitative, sociallyacquired information about risk objects, natu-rally had a smaller reach, and did not rely onan agent-network for contract-matching. Na-tional firms, who relied on agents for a widegeographic reach, operated the underwritingbusiness on actuarial principals for which themicro-insurers did not have the technologicaland informational capacity.

Bibliography

Adams, Michael et al. (2012). “Competing Models of Organizational Form: Risk ManagementStrategies and Underwriting Profitability in the Swedish Fire Insurance Market Between1903 and 1939.” In: Journal of Economic History 72.4, pp. 990–1014. issn: 00220507. url: http://search.ebscohost.com/login.aspx?direct=true&db=buh&AN=84342408&site=ehost-live&scope=site.Assurans-Tidning, Svensk (1889). Matrikel Öfver de Svenska Försäkrings-Bolagens Hrr Agenter :Utg. i December 1889. Stockholm.

64Adams et al. 2012.

15

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Baranoff, D. (2003). “A Policy of Cooperation: The Cartelisation of American Fire Insurance,1873-1906”. In: Financial History Review 10.2, pp. 119–136+113. issn: 09685650 (ISSN). url:http://www.scopus.com/inward/record.url?eid=2-s2.0-0348222462&partnerID=40&md5=9997efaaf42fe8771204c4e3da26238f.Bartley, Tim and Marc Schneiberg (2002). “Rationality and Institutional Contingency : The Vary-ing Politics of Economic Regulation in the Fire Insurance Industry”. In: Sociological Perspectives45.1, pp. 47–79. issn: 0731-1214.Bergander, Bengt (1967). Försäkringsväsendet i Sverige 1814-1914. Stockholm: [Försäkringsinspek-tionen] ;Boksjö, Alexander and Mikael Lönnborg (1994). “Collusive and Competitive Institutions in theSwedish Insurance Market”. In: Nordisk Försäkringstidskrift 2, pp. 139–159. issn: 0348-6516.Brandes, Ulrik and Thomas Erlebach (2005). “Fundamentals”. In: Network Analysis. Ed. byUlrik Brandes and Thomas Erlebach. Berlin: Springer, pp. 7–15. isbn: 3-540-24979-6.Chandler, Alfred D. and Takashi Hikino (1990). Scale and Scope : The Dynamics of IndustrialCapitalism. Cambridge, Mass.: Belknap Press. isbn: 0-674-78994-6.Fredrikson, L. (1937). Willands, Gärds Och Albo Brandförsäkringsbolag 1837-1937 : Minnesskrift : PåUppdrag Av Brandstodsnämnden Utarb. Kristianstad: Kristianstads Läns Tidning.Götherström, R. (1941). Handledning i Industriellt Brandskydd : På Uppdrag Av Sveriges Industriför-bund. In collab. with R. Sundfeldt and Y. Nordensten. Stockholm: Sveriges industriförb.Gutiérrez González, Pablo and Jeròna Pons Pons (2017). “Risk Management and ReinsuranceStrategies in the Spanish Insurance Market (1880–1940)”. In: Business History 59.2, pp. 292–310.issn: 0007-6791. doi: 10.1080/00076791.2016.1187136. url: http://www-tandfonline-com.proxy.ub.umu.se/doi/abs/10.1080/00076791.2016.1187136 (visited on 06/05/2017).Hallendorff, Carl (1923). Svenska Brandtariff-Föreningen 1873-1923 : Minnesskrift Vid FöreningensFemtio-Årsjubileum. Stockholm: Sv. brandtariff-fören.Holmgren, Gunnar and Einar Lindbohm (1939). Om Brandförsäkring. Svenska försäkrings-föreningens studiehandböcker ; 7. Stockholm.Jones, S. R. H. (1997). “Transaction Costs and the Theory of the Firm: The Scope and Limitationsof the New Institutional Approach”. In: Business History 39.4, pp. 9–25. issn: 0007-6791. doi:10.1080/00076799700000143. url: http://dx.doi.org/10.1080/00076799700000143(visited on 05/22/2016).Keneley, Monica (2002). “The Origins of Formal Collusion in Australian Fire Insurance1870–1920.” In: Australian Economic History Review 42.1, p. 54. issn: 00048992. doi: Article.url: http://search.ebscohost.com/login.aspx?direct=true&db=buh&AN=6296812&site=ehost-live&scope=site.Larsson, Mats and Mikael Lönnborg (2007). “Ömsesidig Försäkringsverksamhet i Den SvenskaFörsäkringsmodellen”. In: Nordisk Försäkringstidskrift, pp. 85–100. issn: 0348-6516.Lilljegren, Josef and Lars Fredrik Andersson (2014). “Variation in Organizational Form acrossLines of Property Insurance: Sweden, 1913–1939”. In: Financial History Review 21 (01), pp. 77–101.doi: 10.1017/S0968565014000031.Linn, Gustaf (1966). Från Provinsbolag till Riksföretag: En Krönika Om Vegetebolagen. Lund: Rahmsboktryckeri.Lönnborg, Mikael and Mats Larsson (2015). “Regulating Competition of the Swedish InsuranceBusiness - The Role of the Insurance Cartel Registry”. In: Regulating Competition: Cartel Registersin the Twentieth Century World. Ed. by Susanna Fellman and Martin Shanahan, pp. 248–267.isbn: 978-1-138-02164-8.Petersson, Viktor (1941). Östergötlands Läns Brandstodsbolag 1841-1941. Linköping: ÖstgötaCorrespondentens.

16

AEHE Salamanca 2017 - Work in progress: Contact author before citing!

Rothstein, Bo (1998). “State Building and Capitalism: The Rise of the Swedish Bureaucracy”.In: Scandinavian Political Studies 21.4, pp. 287–306. issn: 1467-9477. doi: 10.1111/j.1467-9477.1998.tb00016.x. url: http://onlinelibrary.wiley.com/doi/10.1111/j.1467-9477.1998.tb00016.x/abstract (visited on 06/28/2016).Silén, Sven (1944). Västernorrlands Läns Brandstodsbolag 1844-1944 : Minnesskrift. Uppsala:Almqvist & Wiksell.Stigler, George J. (1964). “A Theory of Oligopoly”. In: Journal of Political Economy 72.1, pp. 44–61.issn: 0022-3808. JSTOR: 1828791.Svea (1887). Brand- Och Lifförsäkrings-Aktiebolaget Svea : Instruktion För Agenter : Brandförsäkringsrörelsen.Göteborg.Williamson, Oliver E. (1979). “Transaction-Cost Economics: The Governance of ContractualRelations”. In: Journal of Law and Economics 22.2, pp. 233–261. issn: 00222186. doi: 10.2307/725118. JSTOR: 725118.

17