short sales and foreclosures - home | rebacrebac.net/teach/foreclosure/2009/june/short sales and...

TRANSCRIPT

1. Homeowners in Jeopardy F

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

Student Manual

A program by the Real Estate Buyer’s Agent Council, Inc.

of the National Association of REALTORS®

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

2

Copyright © 2009 by the Real Estate Buyer’s Agent Council Note: The Real Estate Buyer’s Agent Council and National Association of REALTORS®, its faculty, agents and employees are not engaged in rendering legal, accounting, financial, tax, or other professional services through these course materials. If legal advice or other expert assistance is required, the student should seek competent professional advice. Real Estate Buyer’s Agent Council 430 North Michigan Avenue Chicago, Illinois 60611 Phone: 800‐648‐6224 [email protected] www.REBAC.net

i

1. Homeowners in Jeopardy

Table of Contents Acknowledgments iii About REBAC iii About This Course v 1. Homeowners in Jeopardy 1 Options for Distressed Homeowners 2 If Short Sale Is the Best Option: What Now? 8 2. The Short‐Sale Package 18 Components of an Effective Short‐Sale Package 18 Common Results from Short Sales 23 The Mortgage Forgiveness Debt Relief Act of 2007 24 3. Foreclosures 25 When All Alternatives Are Exhausted: Foreclosure 25 Forced Sale of Property 27 Redemption 28 When the Property Fails to Sell at Sheriff’s Auction: REO 29 4. How Consumers Can Prevent Foreclosure 36 Become Educated 36 Choosing the Right Loan 37 Staying Aware of Predatory Lending Practices 39 Responding to the Crisis 40 Appendix 42 Common Questions to Ask Lenders When Shopping for a Loan 42 Understanding Nontraditional Loan Products 43

ii

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

4

Acknowledgments

REBAC expresses gratitude and appreciation to the following individuals for their subject matter and industry expertise, input and feedback, and commitment to providing the best education for today’s real estate professionals: • Edward A. Bugos, ABR® • Lynn Madison, ABR®, ABRM, GRI, SRES® • Lori Cox, ABR®, GRI, SRES®, e‐PRO, CRB, CRS

About REBAC The Real Estate Buyer’s Agent Council, REBAC, of the National Association of REALTORS® promotes superior buyer representation skills and services. REBAC is the world’s largest organization of real estate professionals concentrating on buyer representation. Members who meet all course and professional experiential requirements are awarded the Accredited Buyer’s Representative (ABR®) and/or Accredited Buyer’s Representative Manager (ABRMSM) designation(s). Both are the only designations of their type recognized by NAR.

HOW TO BECOME AN ABR® 1. Successfully complete the two‐day ABR® Designation Course, including an

80% passing grade on the written exam. 2. Successfully complete an approved ABR® elective. Choose from the

following:

> e‐Buyer: Understanding Real Estate e‐Buyers and How to Market to Them > Innovative Marketing for Buyer’s Representatives > Short Sales and Foreclosures: What Buyer’s Representatives Need to

Know > Successful Buyer Representation in Relocation > Successful Buyer Representation in New‐Home Sales

> NEW! NAR’s Green Designation Core Course > Seniors Real Estate Specialist (SRES®) Designation Course > Introduction to Real Estate Auction (NAR) > International Real Estate for Local Markets (NAR) > Resort and Second‐Home Markets (NAR)

> Land 101: Fundamentals of Land Brokerage (RLI) > Harnessing the Power (WCR) > Effective Negotiating for Real Estate Professionals (WCR) > Creating Wealth through Residential Real Estate Investment (CRS) > e‐PRO (NAR)

iii

1. Homeowners in Jeopardy To learn about where classes are offered or to enroll in an online course, visit www.coursecalendar.com or www.realtor.org/RealtorUniversity. 3. Submit documentation, verifying five completed transactions in which you

served as the buyer’s representative. 4. Maintain membership in the National Association of REALTORS® and

REBAC. A free one‐year membership in REBAC is included with registration for the ABR® Designation Course. Thereafter, dues are $110 per year. Candidates have three years from successful completion of the ABR® Designation Course to fulfill the designation requirements. Candidates who do not complete the designation requirements within the three‐year time frame must start over.

BENEFITS OF BECOMING AN ABR® New designees receive a welcome packet that includes a letter of recognition, designation lapel pin, certificate, and press release for local media. Ongoing member benefits include: • Industry respect and recognition

> Listing in REBAC’s online membership directory at www.REBAC.net > National consumer awareness marketing campaign

• Information on buyer representation trends and influences

> Today’s Buyer’s Rep, REBAC’s award‐winning monthly newsletter > Weekly HotSheet e‐mail newsletter > The Real Estate Professional, a bi‐monthly trade magazine > Free Webinars on timely topics

• Tools to help you promote your business to consumers and other real estate

professionals

> ABR® logo for your business card and Web site > Customizable marketing materials, including brochures, flyers and

postcards > Home Buyer’s Toolkit, a 36‐page educational consumer booklet

• Networking opportunities

> REBAC Day at the annual NAR National Conference and Expo > Events at other industry conferences throughout the year

iv

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

6

About This Course The goal of this course is to educate buyer’s representatives about the processes of short sales and foreclosures. The course enables students to: 1. Differentiate between short sales and foreclosures.

2. Explain the process of a successful short‐sale transaction.

3. Identify the components of a short‐sale package.

4. Understand the processes and procedures of foreclosure.

5. Guide clients who want to purchase short‐sale or foreclosed properties.

6. Counsel buyers on how to prevent short sales and foreclosures.

MODULES AND OBJECTIVES Module 1: Homeowners in Jeopardy • Understand why so many homeowners are in default. • Define homeowner’s options when facing default. • List the concerns of real estate professionals when working with homeowners

in default. • Help guide buyers who want to purchase a short‐sale property. Module 2: The Short‐Sale Package • List the components of the short‐sale package. • Understand the tax exemptions for forgiven debt in real estate transactions. Module 3: Foreclosures • Differentiate judicial foreclosure from nonjudicial foreclosure. • Describe the foreclosure process. • Explain how to work with a listing agent on an REO property. • Help guide buyers who want to purchase a foreclosed property. Module 4: How Consumers Can Prevent Foreclosure • Explain how future foreclosures may be reduced by educating the buyer

public. • Recognize the signs of mortgage fraud and predatory lending. • Explain how mortgage fraud and predatory lending can impact home‐buying

decisions.

v

1. Homeowners in Jeopardy

1

1. Homeowners in Jeopardy In this module:

• Homeowner options

• Buyer considerations in short sales

In order to provide effective service to buyer clients involved in a potential short sale, foreclosure, or other distressed sale situation, it is imperative that agents understand the process and parties involved in the transaction. Knowing what is required and what transpires from the seller’s side of the transaction is critical in facilitating a successful buyer‐side transaction. Case Study #1: Upside‐Down Sellers You receive a call from Michael and Michelle, a couple to whom you sold a wonderful house a few years ago. They’d like to discuss selling the house with you. When you arrive at the home, Michael and Michelle explain that their option adjustable‐rate mortgage (ARM) payment adjusted upwards and they cannot handle the new mortgage payment. Your comparative market analysis (CMA) showed that the home values in their neighborhood have not increased, and Michael and Michelle are now “upside down”—they now owe more than the property is worth. They have only missed one mortgage payment, but they know they will not be able to make the next one since Michael was laid off of work a few months ago and they have depleted their savings. They have been using their credit cards for living expenses for quite some time. What are other reasons why homeowners today could be behind in their mortgage payments?

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

2

Pre ‐Foreclosure

Anytime homeowners are behind in their mortgage payments, they are considered in “pre‐foreclosure.” The length of what is considered pre‐foreclosure varies depending on state laws. During this time, the homeowner is initially notified of the mortgage payment default. This contact typically occurs within 30 days following the default on a payment. Before placing a lien on the property, the lender may follow up with letters and phone calls. It is still possible at this point for the homeowner to avoid foreclosure.

OPTIONS FOR DISTRESSED HOMEOWNERS While homeowners who are at risk of default or who have defaulted on their mortgage may feel that “walking away” is their only solution, there are options available to them. Real estate professionals can help outline the following foreclosure alternatives for clients and customers and direct them to seek legal and tax advice. Depending on the homeowner’s circumstances, some alternatives are more viable than others.

1. Refinance

Homeowners who are current with their mortgage payments may be able to take advantage of today’s mortgage rates and keep their homes by refinancing to a 30‐ or 15‐year fixed‐rate loan via Home Affordable Refinance, a component of the Making Home Affordable initiative launched in early 2009. For an overview of eligibility criteria, see Figure 1.

Figure 1: Eligibility Criteria Overview for Home Affordable Refinance

Home Owner occupied

Is a one‐ to four‐unit home

Existing Mortgage

Owned or backed by Fannie Mae or Freddie Mac

Loan‐to‐value (LTV) ratio is above 80% but not more than 105%

Borrower Current on existing mortgage payments

Has enough income to support new mortgage payments

For more information, visit www.MakingHomeAffordable.gov.

1. Homeowners in Jeopardy

3

2. Sell and Bring Cash to Closing

Although many homeowners today may not have the necessary cash to cure deficiencies at closing, they may have liquid assets, e.g., U.S. Treasury bonds, individual retirement accounts (IRAs), to do so. By curing deficiencies at closing, homeowners can avoid the credit damage that a short sale or foreclosure can cause. However, homeowners are strongly encouraged to consult with their tax professionals before bringing liquid assets to closing.

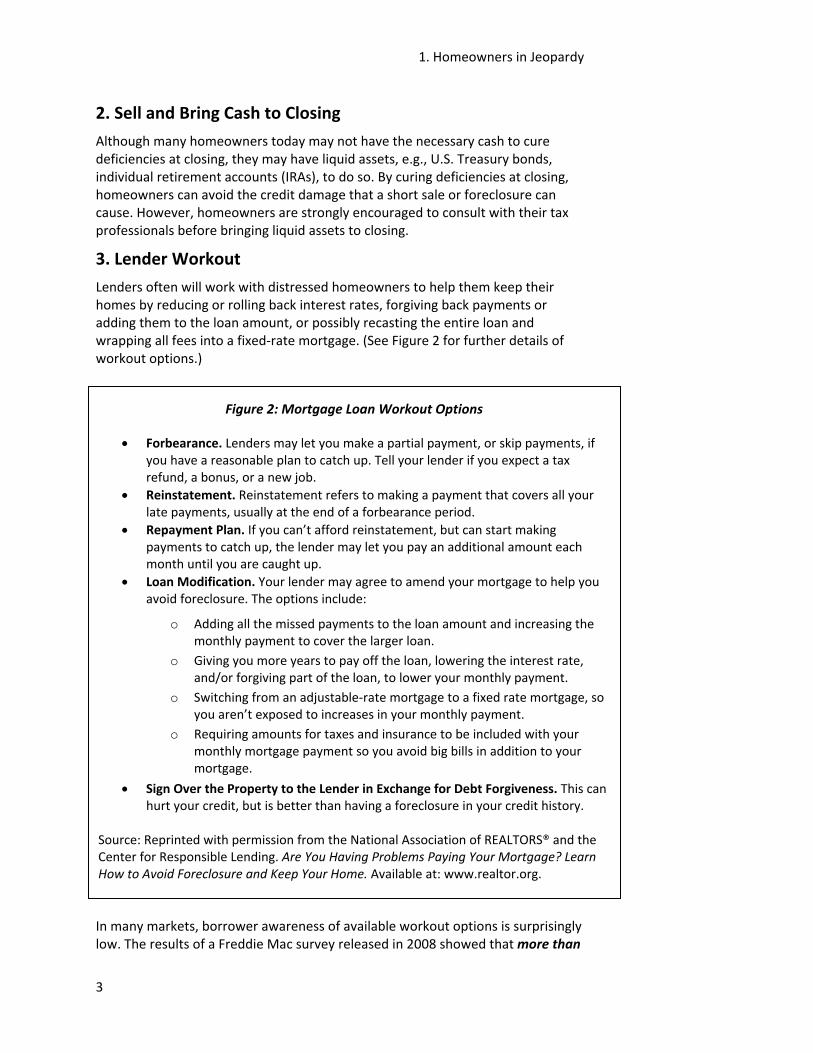

3. Lender Workout

Lenders often will work with distressed homeowners to help them keep their homes by reducing or rolling back interest rates, forgiving back payments or adding them to the loan amount, or possibly recasting the entire loan and wrapping all fees into a fixed‐rate mortgage. (See Figure 2 for further details of workout options.)

In many markets, borrower awareness of available workout options is surprisingly low. The results of a Freddie Mac survey released in 2008 showed that more than

Figure 2: Mortgage Loan Workout Options

• Forbearance. Lenders may let you make a partial payment, or skip payments, if you have a reasonable plan to catch up. Tell your lender if you expect a tax refund, a bonus, or a new job.

• Reinstatement. Reinstatement refers to making a payment that covers all your late payments, usually at the end of a forbearance period.

• Repayment Plan. If you can’t afford reinstatement, but can start making payments to catch up, the lender may let you pay an additional amount each month until you are caught up.

• Loan Modification. Your lender may agree to amend your mortgage to help you avoid foreclosure. The options include:

o Adding all the missed payments to the loan amount and increasing the monthly payment to cover the larger loan.

o Giving you more years to pay off the loan, lowering the interest rate, and/or forgiving part of the loan, to lower your monthly payment.

o Switching from an adjustable‐rate mortgage to a fixed rate mortgage, so you aren’t exposed to increases in your monthly payment.

o Requiring amounts for taxes and insurance to be included with your monthly mortgage payment so you avoid big bills in addition to your mortgage.

• Sign Over the Property to the Lender in Exchange for Debt Forgiveness. This can hurt your credit, but is better than having a foreclosure in your credit history.

Source: Reprinted with permission from the National Association of REALTORS® and the Center for Responsible Lending. Are You Having Problems Paying Your Mortgage? Learn How to Avoid Foreclosure and Keep Your Home. Available at: www.realtor.org.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

4

half of delinquent borrowers did not know that their lenders may have alternatives to help them avoid foreclosure. 1 For many lenders, however, loan modification is a suitable workout option since lender losses on foreclosures can run as high as $100,000 per property. According to HOPE NOW, a coalition of mortgage servicers and investors, loan modification as a percentage of workout options has more than doubled from Q1 2007 to Q1 2009. See Figure 3.

Figure 3: Loan Modifications as a Percentage of Workout Options: Q1 2007 – Q1 2009

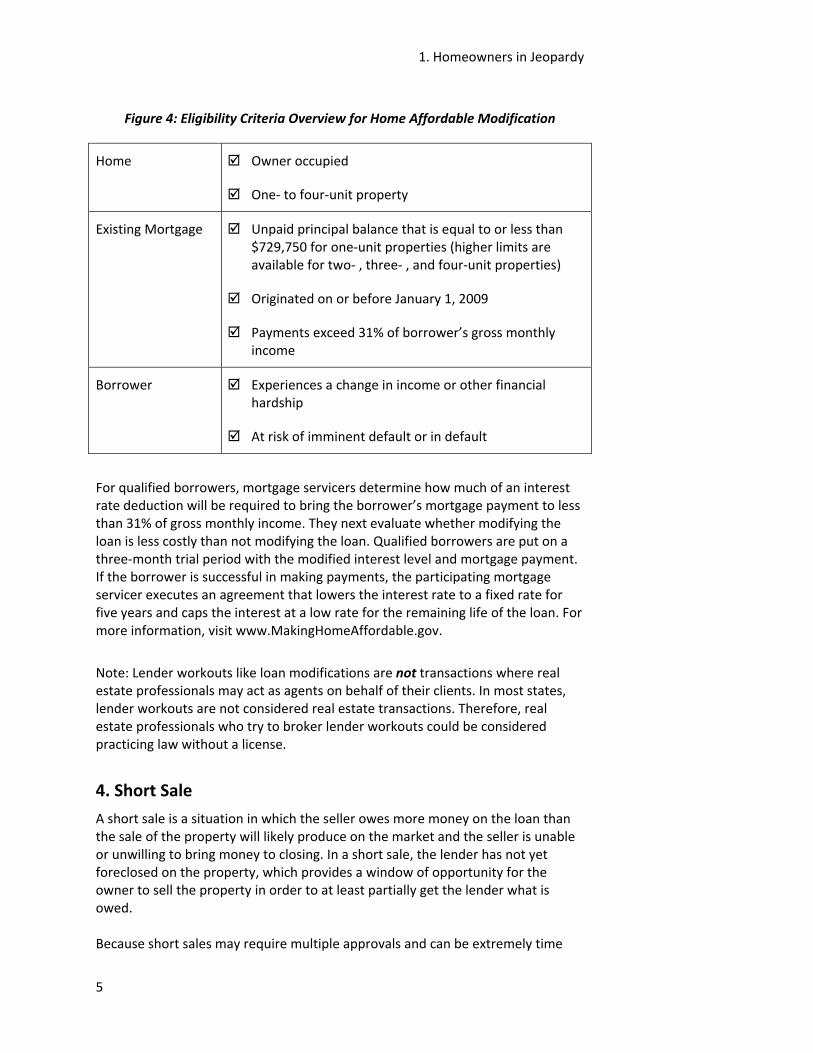

Source: HOPE NOW National Data July07 to March09. Available at: www.hopenow.com/industry_data.html. Homeowners struggling to stay current with mortgage payments who experience a change in income or other financial hardships may seek loan modification via Home Affordable Modification, a component of the Making Home Affordable Program. Home Affordable Modification is a voluntary program with participation from major mortgage servicers, including, but not limited to, Chase Financial, GMAC Mortgage, Countrywide, and Wells Fargo. Eligibility criteria are outlined in Figure 4.

1 Freddie Mac. Delinquent Borrowers: 57% Unaware of Workout Options, Says New Freddie Mac/Roper Survey. Available at: www.freddiemac.com.

1. Homeowners in Jeopardy

5

Figure 4: Eligibility Criteria Overview for Home Affordable Modification

Home Owner occupied

One‐ to four‐unit property

Existing Mortgage Unpaid principal balance that is equal to or less than $729,750 for one‐unit properties (higher limits are available for two‐ , three‐ , and four‐unit properties)

Originated on or before January 1, 2009

Payments exceed 31% of borrower’s gross monthly income

Borrower Experiences a change in income or other financial hardship

At risk of imminent default or in default

For qualified borrowers, mortgage servicers determine how much of an interest rate deduction will be required to bring the borrower’s mortgage payment to less than 31% of gross monthly income. They next evaluate whether modifying the loan is less costly than not modifying the loan. Qualified borrowers are put on a three‐month trial period with the modified interest level and mortgage payment. If the borrower is successful in making payments, the participating mortgage servicer executes an agreement that lowers the interest rate to a fixed rate for five years and caps the interest at a low rate for the remaining life of the loan. For more information, visit www.MakingHomeAffordable.gov.

Note: Lender workouts like loan modifications are not transactions where real estate professionals may act as agents on behalf of their clients. In most states, lender workouts are not considered real estate transactions. Therefore, real estate professionals who try to broker lender workouts could be considered practicing law without a license.

4. Short Sale

A short sale is a situation in which the seller owes more money on the loan than the sale of the property will likely produce on the market and the seller is unable or unwilling to bring money to closing. In a short sale, the lender has not yet foreclosed on the property, which provides a window of opportunity for the owner to sell the property in order to at least partially get the lender what is owed. Because short sales may require multiple approvals and can be extremely time

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

6

intensive, short sales are considered by many real estate practitioners to be complicated transactions. So what makes for a successful short sale? As a general rule, successful short sales reflect the following:

• The property is worth less than is owed.

• The seller has some hardship that makes it impossible or extremely impractical for the seller to keep the property.

• The seller is cooperative and willing to work with a real estate broker to package the short sale.

• The lender is contacted and expresses willingness to entertain a short sale.

• The property is listed, with appropriate caveats and protections for the seller, properly priced, and effectively marketed.

• The lender is presented with a contract, accepted, signed and dated by the seller, along with a completed short sale package and narrative explaining the necessity and desirability of the proposed short sale.

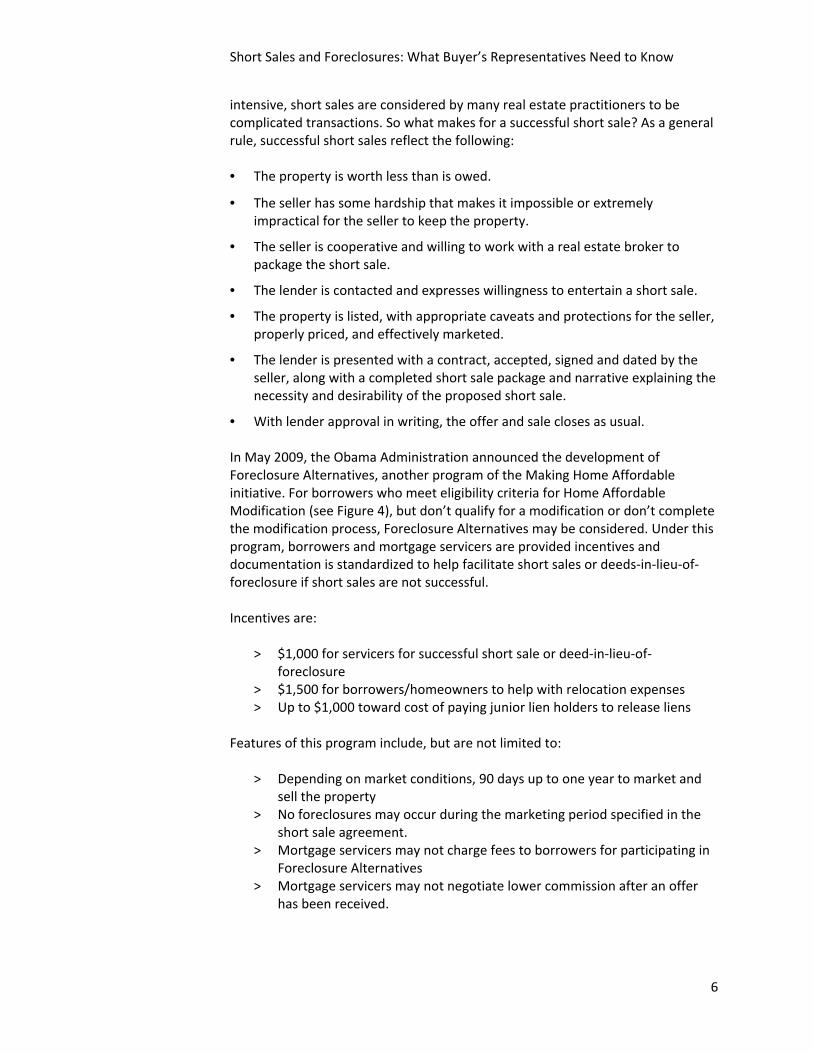

• With lender approval in writing, the offer and sale closes as usual. In May 2009, the Obama Administration announced the development of Foreclosure Alternatives, another program of the Making Home Affordable initiative. For borrowers who meet eligibility criteria for Home Affordable Modification (see Figure 4), but don’t qualify for a modification or don’t complete the modification process, Foreclosure Alternatives may be considered. Under this program, borrowers and mortgage servicers are provided incentives and documentation is standardized to help facilitate short sales or deeds‐in‐lieu‐of‐foreclosure if short sales are not successful. Incentives are:

> $1,000 for servicers for successful short sale or deed‐in‐lieu‐of‐foreclosure

> $1,500 for borrowers/homeowners to help with relocation expenses > Up to $1,000 toward cost of paying junior lien holders to release liens

Features of this program include, but are not limited to:

> Depending on market conditions, 90 days up to one year to market and sell the property

> No foreclosures may occur during the marketing period specified in the short sale agreement.

> Mortgage servicers may not charge fees to borrowers for participating in Foreclosure Alternatives

> Mortgage servicers may not negotiate lower commission after an offer has been received.

1. Homeowners in Jeopardy

7

5. Deed in Lieu of Foreclosure

A deed in lieu of foreclosure occurs when the borrower agrees to trade the property to the lender in exchange for the cancellation of the note. This foreclosure alternative is more likely to work in states where there is a long foreclosure timeline. The lender will be able to get the property much sooner than going through the foreclosure process, which lessens the probability of the property being in disrepair as well as eliminates the lender’s costs to foreclose. Like the mortgage workout, sellers who are interested in a deed in lieu of foreclosure should consult their attorney or contact the lender directly. Market conditions as well as state‐specific laws will influence whether and how a lender accepts a deed in lieu of foreclosure. Typically, lenders are less willing to consider a deed in lieu of foreclosure in declining markets. However, in appreciating markets, lenders may accept properties in lieu of foreclosure. Note: when accepting deeds in lieu of foreclosure, the lender assumes all outstanding liens on the property as well.

6. Foreclosure

If the homeowner is only weeks away from the foreclosure taking place, the homeowner may not be able to pursue any of the previous options, including a short sale. If contacted by the homeowner at a late date, you should instruct the homeowner to contact the lender immediately, and see if there is any way to explore foreclosure alternatives. Also, in some situations, foreclosure may even be in the best interest of distressed homeowners, although doing so will wreak the most damage to their credit. If the lender will not explore foreclosure alternatives, real estate professionals should instruct their clients and customers to contact their attorney for advice.

7. Do Nothing or Walk Away

If homeowners are simply unhappy that the value of the property is less than what they paid or owe, they need to contact an attorney for advice. Walking away from the loan or asking the lender to proceed with a short sale simply because the value went down may not be a viable option and if it is, there will often be additional financial consequences.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

8

Don’t Practice Law Without a License

NAR Code of Ethics Article 13 states: REALTORS® shall not engage in activities that constitute the unauthorized practice of law and shall recommend that legal counsel be obtained when the interest of any party to the transaction requires it.

Alert Homeowners to Rescue Scams

Warn homeowners to watch out for unethical investors who will try to convince an owner facing foreclosure to sign a quitclaim deed for the property, and then lease the property. In such cases, the former owners will still be liable for the mortgage payments, even though they no longer own the house.

IF SHORT SALE IS THE BEST OPTION: WHAT NOW?

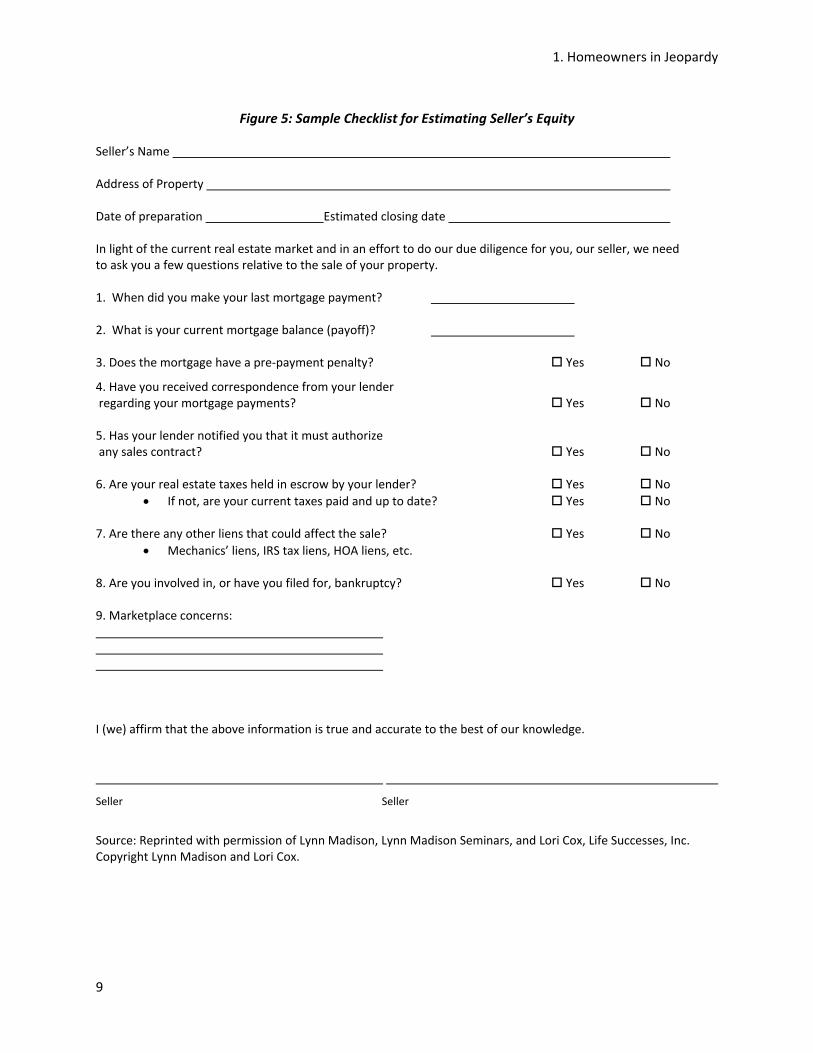

Estimate the Seller’s Equity

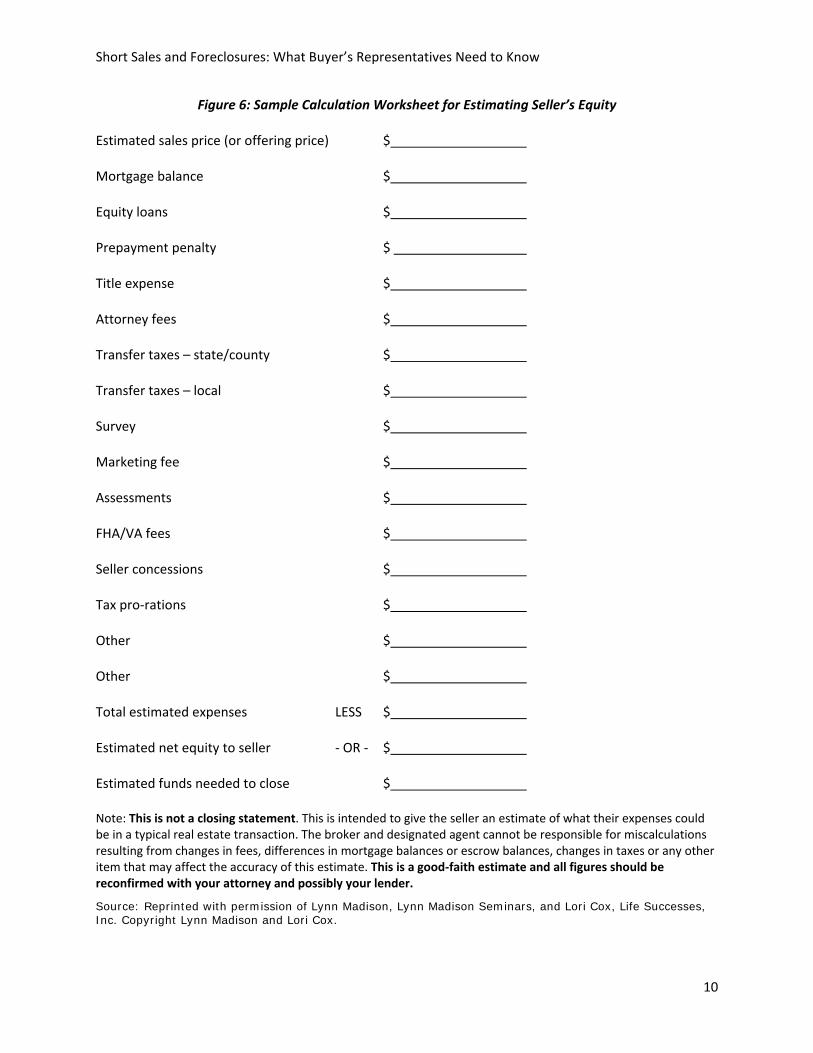

It is critical for real estate professionals to provide a careful and thorough estimate of the seller’s equity. With any short sale or possible short sale, it is imperative that real estate professionals carefully estimate the seller’s net equity because once the listing is placed in the MLS and an offer of compensation is made to cooperating brokers, the listing broker is responsible for paying that compensation even if the seller doesn’t pay the listing broker. A sample checklist and worksheet for estimating net equity are provided in Figures 5 and 6.

1. Homeowners in Jeopardy

9

Figure 5: Sample Checklist for Estimating Seller’s Equity

Seller’s Name Address of Property Date of preparation Estimated closing date In light of the current real estate market and in an effort to do our due diligence for you, our seller, we need to ask you a few questions relative to the sale of your property. 1. When did you make your last mortgage payment? 2. What is your current mortgage balance (payoff)? 3. Does the mortgage have a pre‐payment penalty? Yes No

4. Have you received correspondence from your lender regarding your mortgage payments? Yes No 5. Has your lender notified you that it must authorize any sales contract? Yes No 6. Are your real estate taxes held in escrow by your lender? Yes No

• If not, are your current taxes paid and up to date? Yes No

7. Are there any other liens that could affect the sale? Yes No • Mechanics’ liens, IRS tax liens, HOA liens, etc.

8. Are you involved in, or have you filed for, bankruptcy? Yes No 9. Marketplace concerns: I (we) affirm that the above information is true and accurate to the best of our knowledge.

Seller Seller

Source: Reprinted with permission of Lynn Madison, Lynn Madison Seminars, and Lori Cox, Life Successes, Inc. Copyright Lynn Madison and Lori Cox.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

10

Figure 6: Sample Calculation Worksheet for Estimating Seller’s Equity

Estimated sales price (or offering price) $ Mortgage balance $

Equity loans $

Prepayment penalty $

Title expense $

Attorney fees $

Transfer taxes – state/county $

Transfer taxes – local $

Survey $

Marketing fee $

Assessments $

FHA/VA fees $

Seller concessions $

Tax pro‐rations $

Other $

Other $ Total estimated expenses LESS $ Estimated net equity to seller ‐ OR ‐ $ Estimated funds needed to close $ Note: This is not a closing statement. This is intended to give the seller an estimate of what their expenses could be in a typical real estate transaction. The broker and designated agent cannot be responsible for miscalculations resulting from changes in fees, differences in mortgage balances or escrow balances, changes in taxes or any other item that may affect the accuracy of this estimate. This is a good‐faith estimate and all figures should be reconfirmed with your attorney and possibly your lender.

Source: Reprinted with permission of Lynn Madison, Lynn Madison Seminars, and Lori Cox, Life Successes, Inc. Copyright Lynn Madison and Lori Cox.

1. Homeowners in Jeopardy

11

It is also vital for real estate professionals to determine if there are any liens (mechanics’ liens, IRS tax liens, home owners’ association (HOA) liens) that could affect the sale. If the seller has a first and second mortgage or a home equity line of credit, it is highly likely that all lenders will need to approve a short sale. In addition, approval may be required from the entity holding the pool of loans if the mortgage has been securitized. In some instances the primary lien holder will contact the other lien holders. In others, you—or the seller’s attorney—will be making the contacts. Check with the primary lender on its protocol and processes. When real estate professionals have determined that the seller owes more than the property is worth, they should advise the seller in writing to obtain separate legal, credit, and tax advice.

Contact the Loss Mitigation Department

The lender’s loss mitigation department, not the collection or customer service department, is responsible for approving short sales. Finding the decision maker is often one of the biggest initial challenges in short sales. There are varying opinions on when to contact the lender. Some practitioners recommend contacting the lender as soon as they know a short sale is probable. Other practitioners suggest waiting until a buyer has accepted the contract terms, subject to the lender’s approval. Consider talking with colleagues who have worked on short sales to get a better understanding of what lenders require. A large number of lenders will respond more favorably if the real estate professional has an accepted contract and an entire submission package to present. Other lenders will not even consider a short sale, in which case real estate professionals should help the homeowner consider other alternatives.

Obtain the Borrower’s Authorization to Contact the Lender

Real estate professionals must have a signed borrower authorization to release information in order to contact the lender. See Figure 7 for a sample authorization form.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

12

Figure 7: Sample Authorization to Release Information Date: Loan #: Lien Holder Property Address Seller consents that Lien Holder and its representatives may supply and communicate any loan, financial or other information of Seller, confidential or otherwise, with any of the following involved in the transaction and their representatives: Seller’s attorney or representative (names) Seller’s Broker and Agent (names)

Listing Potential Short‐Sale Properties to Prospective Buyers

When listing properties where a potential short sale is an issue, two things need to be considered: 1. No confidential information should be disclosed without written permission

of the client—the seller. 2. All rules and regulations of the local multiple‐listing service (MLS) need to

be followed. Real estate professionals need to check with their local MLS to determine when, how, and where to disclose the fact that the seller is involved in a potential short‐sale situation.

The NAR has approved language for disclosing lender approval listings in the MLS, which amends the policies of NAR’s 2008 Handbook on Multiple Listing Policy. See Figure 8.

1. Homeowners in Jeopardy

13

Figure 8: NAR‐Approved Language for Disclosing Short Sales in Multiple Listing Services (MLSs)

Multiple Listing Services must give participants the ability to disclose to other participants any potential for a short sale. As used in these rules, short sales are defined as a transaction where title transfers; where the sale price is insufficient to pay the total of all liens and costs of sale; and where the seller does not bring sufficient liquid assets to the closing to cure all deficiencies. Multiple Listing Services may, as a matter of local discretion, require participants to disclose potential short sales when participants know a transaction is a potential short sale. In any instance where a participant discloses a potential short sale, they must also be permitted to communicate to other participants how any reduction in the gross commission established in the listing contract required by the lender as a condition of approving the sale will be apportioned between listing and cooperating participants. All confidential disclosures and confidential information related to short sales must be communicated through dedicated fields or confidential “remarks” available only to participants and subscribers. Multiple Listing Services that permit, but do not require participants to disclose potential short sales should adopt the following rule: Section 5.0.1: Participants may, but are not required to, disclose potential short sales to other participants and subscribers. When disclosed, participants may, at their discretion, advise other participants whether and how any reduction in the gross commission established in the listing contract, required by the lender as a condition of approving the sale, will be apportioned between listing and cooperating participants. Alternatively, Multiple Listing Services that require participants to disclose potential short sales should adopt the following rule: Section 5.0.1: Participants must disclose potential short sales when reasonably known to the listing participants. When disclosed, participants may, at their discretion, advise other participants whether and how any reduction in the gross commission established in the listing agreement, required by the lender as a condition of approving the sale, will be apportioned between listing and cooperating participants. Source: National Association of REALTORS® Short Sales Issues Working Group. The Short Sale Workflow. Available at: www.realtor.org.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

14

Counseling Buyers on Short Sales Considering the exponential growth in short sales and foreclosures and the potential for “bargain deals,” many buyers today are interested in purchasing short‐sale and foreclosure properties, which may be reflected by the growing popularity of repo or foreclosure bus tours in some markets. When buyers are considering the purchase of a short sale, buyer’s representatives should perform an initial needs assessment. Needs assessment includes addressing the following questions: • Are the buyers in a position where they can wait for the lender’s approval?

• Do the buyers have a home to sell before they can purchase the short sale?

• Will the buyers follow through on your counsel regarding, among other things, market value and contract contingencies?

• Do the buyers understand that the lender will be making the final call on price and terms?

• Are the buyers interested in “flipping” the property? If yes, additional due diligence will need to be performed.

• How willing are the buyers to consult an attorney regarding home inspections, earnest money, and the contingency period for third‐party approval?

• Is the buyer willing to enter into an exclusive buyer representation agreement and be responsible for compensation should it not be paid by the seller’s side?

1. Homeowners in Jeopardy

15

Showing Short‐Sale Listings

Most MLSs require that a listing broker report within a specified period of time (typically within 24, 48, or 72 hours) that their listing has gone under contract. These will appear in the MLS in a variety of ways, but almost always under the “Active‐Contingent” field.

Case Study #2: Buyers and a Potential Short‐Sale Property Buyers Zach and Tammy, whose son plays on your sons’ little league team, have contacted you about a property for sale. As it turns out, it is Michael and Michelle’s home (Case Study #1) , and Michael and Michelle have listed it with another broker. In the MLS it is noted that this property is a potential short sale. 1. Can you disclose to the Zach and Tammy confidential information about Michael and Michelle that you may know because of your prior meeting with them? Why or why not? 2. The buyers are interested in purchasing the property. You explain what a short sale is. They have you write an offer. The offer is presented to the sellers, signed by Michael and Michelle, with a counteroffer asking the buyers for $2,000 at closing, which will not be part of the contract. The listing broker says this is a short‐sale fee or it is to pay for personal property the seller is leaving. Is this okay? Why or why not?

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

16

If the buyer’s representative has a buyer client who wishes to see potential short‐sale properties, these properties should be included in the list of available properties. It would be the buyer’s request not to see properties that had an accepted contract, not the agent’s choice. Remember, in this situation, subsequent offers may have an equal chance of being approved by the lender if the lender has not provided the listing agent/broker a written approval of the contract.

Buyer Issues in Short‐Sale Transactions Short‐sale transactions can be an excellent purchase for the buyer, however, they can also be challenging for buyer's representatives for the following reasons: • As noted earlier, there may be multiple lien holders—first, second, and third

mortgages; IRS liens; and state tax liens. PMI companies also may be involved, therefore, making the third‐party approval process even more challenging and adding time to the approval process.

• The fact that a seller accepts the offer contingent on bank approval does not guarantee bank approval and therefore does not guarantee your buyer will actually be able to purchase the property.

• Documentation requirements from each lender may vary considerably. • Continuing investigation of the property—CMA updates while property is

pending lender approval.

Presenting Offers: NAR Code of Ethics Standards of Practice

Standard of Practice 1‐6 REALTORS® shall submit offers and counter‐offers objectively and as quickly as possible. (Adopted 1/93, Amended 1/95)

Standard of Practice 1‐7 When acting as listing brokers, REALTORS® shall continue to submit to the seller/landlord all offers and counter‐offers until closing or execution of a lease unless the seller/landlord has waived this obligation in writing. REALTORS® shall not be obligated to continue to market the property after an offer has been accepted by the seller/landlord. REALTORS® shall recommend that sellers/landlords obtain the advice of legal counsel prior to acceptance of a subsequent offer except where the acceptance is contingent on the termination of the pre‐existing purchase contract or lease. (Amended 1/93) Standard of Practice 3‐6 REALTORS® shall disclose the existence of accepted offers, including offers with unresolved contingencies, to any broker seeking cooperation.

1. Homeowners in Jeopardy

17

• Many lenders take weeks to review submitted offers, but provide only days, sometimes as few as five, for buyers to close, which does not give most buyers sufficient time to order a property inspection.

• Unless the contract stipulates that the deposit of earnest money, mortgage application, home inspection and attorney review (if applicable) will not take effect until after approval of the lender, all of these will take effect upon signature of the seller.

• The buyer is under contract, and unless there is a way for the buyer to cancel the contract while lender approval is pending he or she is committed to the transaction.

• If the buyer chooses to purchase another home during this time he or she will need to do it “subject to release of prior contract.”

Succeeding as a buyer's agent in short sales requires education, diligence, and exceptional follow through.

While waiting for a response from the lender, the buyer’s representative should continue analyzing the property value and showing properties to the buyer.

Don’t Practice Law Without a License

The ability for buyers to nullify the original contract if they find another property or realize the value has decreased and choose to withdraw will be entirely based on how the original contract was written. This is one of the many situations in which legal counsel should be consulted.

Once the seller signs your buyer’s offer it becomes an accepted contract, which triggers the deposit of earnest money according to your state statutes.

Discussion Questions

How would you counsel your buyer client on the following issues of purchasing a short‐sale property?

• Home inspection

• Earnest money

• Property condition

• Additional lien holders

• Mortgage application

• Other?

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

18

2. The Short‐Sale Package In this module: • Components of an effective short‐sale package • Common results from a short sale • Mortgage Forgiveness Debt Relief Act of 2007

COMPONENTS OF AN EFFECTIVE SHORT‐SALE PACKAGE The contents of an effective short‐sale package include: • Short‐sale proposal letter (cover letter) • Borrower’s signed short‐sale payoff application, if available • Seller’s hardship letter • Seller’s financial information • Supporting financial information • Supporting hardship information • Repair estimate for the property, if repairs are required • CMA with supporting sales history • Marketing history, showings, and feedback • Purchase contract signed by both the buyer and seller • Written proof of the buyer’s ability to purchase the property (completed loan

application, lender’s preapproval, or bank statement if the buyer is purchasing with cash)

• Copy of certified escrow instructions, if applicable • HUD‐1 settlement statement • Preliminary title report, if applicable Remember, there can be multiple loans and you will need to repeat this process for each lien holder. If there is more than one lien holder, they will generally want payoff information from each other. In terms of the amount of paperwork required by short sales, one expert notes: “It takes more documentation to get out of their mortgage than it took them to get it in the first place.”

Proposal Letter

The proposal letter should be clear and concise giving the needed information to the bank. It should include an overview of the homeowner’s situation, what they owe on the property, what it is really worth and mention the amount of the needed repairs and what the offer to the bank is. See Figure 9 for a sample letter.

2. The Short‐Sale Package

19

Figure 9: Sample Proposal Letter TO: The Loss Mitigation Department of ABC Lenders ATTN: Janice Johnson, Loss Mitigation Specialist FROM: Alice Agent RE: Short Sale Proposal for 123 Main Street, Anytown, USA

Dear Ms. Johnson,

We have a signed real estate purchase contract with your borrower Daniel and Sandy Smith, the owners of 123 Main Street, Anytown, USA. The Smiths have agreed to sell their property to Lee and Sandra Jones for a purchase price of $375,000.

The current loan balance for loan #456781239 is $450,000. The Smiths are five payments behind in the amount of $9,000. Since their real estate taxes were not escrowed, the current taxes in the amount of $8,000 are also due. Daniel has lost his job as a manager of a large home improvement company and Sandy is a stay‐at‐home mom with their four children.

Please review the enclosed information. Our market analysis of the property and overview of the market as well as the situation of the seller indicate that it is in the best interest of both you as the lender and the Smiths to accept this buyer’s offer.

We look forward to doing business with you.

Sincerely,

Alice Agent

Short‐Sale Payoff Application

This application is provided by the lender. The real estate professional may have obtained this in advance of putting together the short‐sale submission package. If that is the case, the borrower/owner should fill it out and the real estate professional should make it a part of the package. Note: some lenders provide this only after receiving the submission package.

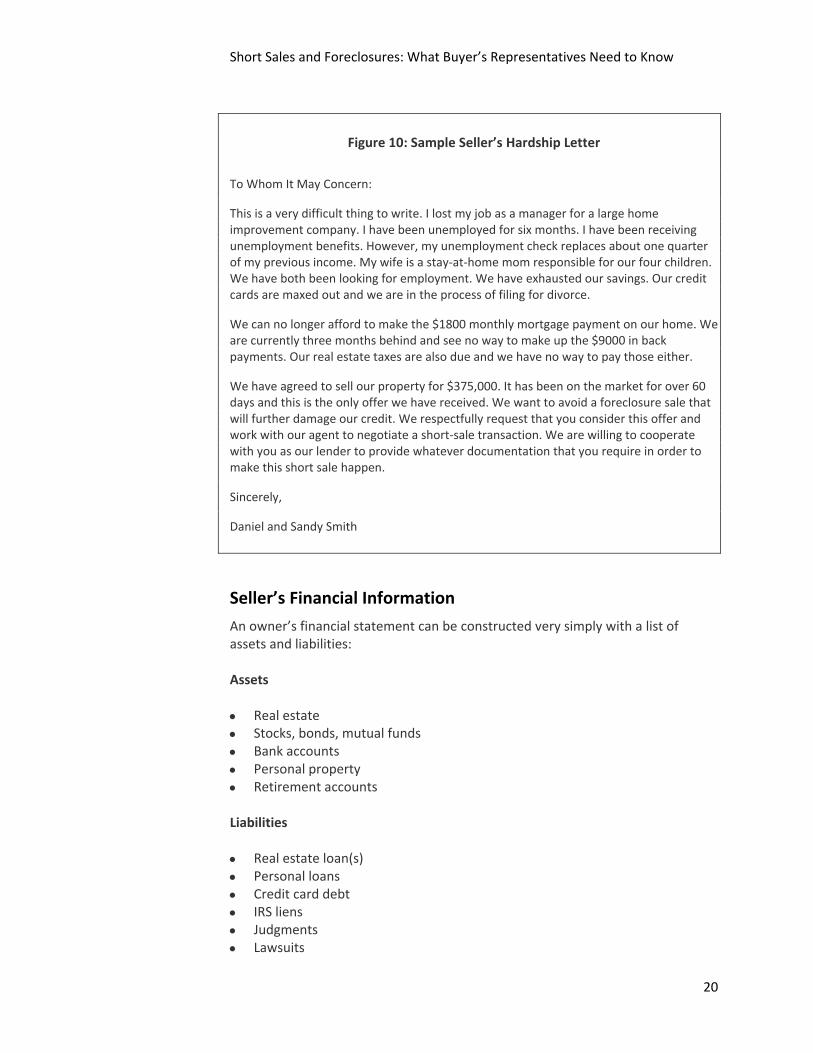

Seller’s Hardship Letter

The goal of the hardship letter is to simply have the homeowner explain their situation to the bank. This will include key items such as job loss, medical issues, divorce, health issues, damage to the property not covered by insurance, etc. See Figure 10 for a sample hardship letter.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

20

Figure 10: Sample Seller’s Hardship Letter

To Whom It May Concern:

This is a very difficult thing to write. I lost my job as a manager for a large home improvement company. I have been unemployed for six months. I have been receiving unemployment benefits. However, my unemployment check replaces about one quarter of my previous income. My wife is a stay‐at‐home mom responsible for our four children. We have both been looking for employment. We have exhausted our savings. Our credit cards are maxed out and we are in the process of filing for divorce.

We can no longer afford to make the $1800 monthly mortgage payment on our home. We are currently three months behind and see no way to make up the $9000 in back payments. Our real estate taxes are also due and we have no way to pay those either.

We have agreed to sell our property for $375,000. It has been on the market for over 60 days and this is the only offer we have received. We want to avoid a foreclosure sale that will further damage our credit. We respectfully request that you consider this offer and work with our agent to negotiate a short‐sale transaction. We are willing to cooperate with you as our lender to provide whatever documentation that you require in order to make this short sale happen.

Sincerely,

Daniel and Sandy Smith

Seller’s Financial Information

An owner’s financial statement can be constructed very simply with a list of assets and liabilities: Assets • Real estate • Stocks, bonds, mutual funds • Bank accounts • Personal property • Retirement accounts Liabilities • Real estate loan(s) • Personal loans • Credit card debt • IRS liens • Judgments • Lawsuits

2. The Short‐Sale Package

21

Some lenders want you to include the amount of all the monthly expenses in addition to the assets and liabilities. These would include:

• Credit card bills • Utility bills • Car payments • Insurance costs • Food and clothing • Medical bills • Child support • Tuition expenses

Supporting Financial Information

These items are typically the same required by a borrower when applying for a loan: • Pay stubs. Pay stubs allow the lender to see if the monthly take‐home pay

would cover the loan payments plus all the other monthly expenses. If the owner is unemployed, there will be no pay stubs to include.

• W‐2s and/or tax returns. The lender is trying to get a complete picture of the owner’s financial situation. Is the income going up? Is the income going down? Will the borrower be able to make payments if the lender agrees to a repayment program?

• Bank statements and credit reports. Again, the lender wants to be sure the borrower is truly unable to make the payments and these support that. The bank will order a credit report on the borrower but if they have one available attaching it is a benefit.

Skill Builder Tip: Fraud Alert Any explanation of the seller’s financial status that differs from what they put on their original loan application to get the mortgage could become a problem for the seller. If the lender sees an unexplained difference between what was stated on the application to get the loan and what is now being used to get out of the loan it could raise the question of loan fraud. If the seller is concerned or has questions they should consult with their attorney. Source: National Association of REALTORS® Short Sales Issues Working Group. The Short Sale Workflow. Available at: www.realtor.org.

Supporting Hardship Information

In order to provide the lender with a complete picture of the homeowner’s hardship, it can help to provide additional documents:

• HOA liens

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

22

• Medical bills • Disability statements • Unemployment benefits or status • Divorce decree Medical hardships and unemployment, to a certain extent, are easy for a lender to understand and they will agree to a short sale in just about every medical hardship situation. The seller should not try to “fake” medical hardship. The lender will verify this information.

Comparative Market Analysis

The real estate professional should create a comparative market analysis (CMA) using the most current comparable sales. The lender will order one or two broker price opinions (BPOs) after they receive the short‐sale submission package. Real estate professionals should not mislead the lender as to the fair market value. If the CMA is too far below the BPOs, the lender may view the entire short‐sale package in a negative light.

Marketing History

Lenders should be presented with a complete history of showings, feedback, and advertising—in short, all the marketing efforts made to provide the lender an offer. Real estate professionals need to show lenders that they’ve done a thorough job of attempting to get the best price possible. Real estate professionals will need to write a short narrative about the market and market trends in the immediate area of the property being sold. Highlight such data as: • Average time on market • Number of short sale and REO listings in the area • Price trends • Market absorption rate/months of inventory • Recent economic data

Skill Builder Tip: Understanding BPOs The acronym BPO is short for broker price opinion. Where permitted by law, lenders will hire brokers to do a BPO when they are considering a short sale. Customarily more than one BPO will be ordered and the lender will factor those prices into their decision making. Buyer’s representatives should be aware of and communicate to their buyers the knowledge the lender has regarding property value.

2. The Short‐Sale Package

23

The decision maker(s) are most likely in another state and will not necessarily understand what is happening in your market.

Repair Estimate for the Property

Providing the lender with a detailed repair estimate from a reputable (licensed) contractor will assist greatly in getting the short sale accepted. The lender doesn’t want to own property—and especially not property that needs a complete overhaul. Some lenders have been known to make some repairs. However, they would much rather sell “as is” and have the buyer make the needed repairs. Two offers netting the lender the same bottom line—one where the buyer will do their own repairs (buying “as is”) and one where the lender is asked to do them—usually results in the “as is” buyer being successful. Including pictures of the property showing the lender its current condition will aid in its decision making process.

Contract and the HUD‐1 Settlement Statement

The real estate professional should provide the lender with a copy of the purchase contract. The contract or purchase agreement should be as free of home‐sale contingencies as possible. Preferably, the buyer agrees to purchase “as is.” All supporting documents, including the HUD‐1 settlement statement and buyer’s preapproval letter, should be attached. Earnest money should be appropriate. Note: Many lenders will reference the HUD‐1 settlement statement in their acceptance, e.g., “Lender will accept net proceeds of no less than $327, 500 no later than [specified date].”

COMMON RESULTS FROM SHORT SALES There are a number of outcomes when lenders consider short‐sale packages: 1. Lien is released; seller is forced to carry remaining debt on a payment plan. 2. Lien is released; seller is forced to liquidate other assets to pay remaining

balance. 3. Lien is released; lender sues for deficiency. 4. Lien is released; lender reports the loss as a “charge off” or “collection” to

credit bureau, thereby causing seller’s credit to be negatively affected (similar to a foreclosure or a bankruptcy).

5. Lien is released; lender forgives remaining indebtedness. 6. The lender ignores the contract. 7. The lender refuses to approve the contract as written and agreed to by buyer

and seller. With this rejection, the lender may indicate the net proceeds it requires for approval of the short sale.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

24

In many cases, sellers think that a short sale will solve all of their problems and get them out of trouble. This is not always the case. The terms of the mortgage will have a significant impact on the results. For example, if the seller has a non‐recourse loan the lien holder has no ability to seek compensation for the amount forgiven in the short sale. If the seller has a recourse loan, the lien holder has the ability to force the seller to repay the debt. Note: In the event of default and foreclosure in a non‐recourse loan the lienholder still has the ability to seek relief.

THE MORTGAGE FORGIVENESS DEBT RELIEF ACT OF 2007 Prior to the Mortgage Forgiveness Debt Relief Act of 2007, forgiven debt (the portion of the mortgage debt canceled by the lender in a short sale) was considered taxable income, which placed considerable strain on distressed sellers. Under this law, which was passed in December 2007, up to $2 million of qualifying mortgage debt forgiven on the taxpayer’s principal residence in 2007, 2008 or 2009 will not be treated as income for the taxpayer. The limit is $1 million for a married person filing a separate return. Mortgage debt reduced (forgiven) through restructuring, such as a workout or a short sale, as well as mortgage debt forgiven in connection with a foreclosure, all qualify for the tax exclusion. The act applies only to principal residences, not vacation homes or investment property. Also, the exclusion applies only to “acquisition indebtedness,” which is generally defined as debt used to originally build, purchase, or improve a property; therefore, home equity funds used to improve the primary residence also qualify. Although short sales tend to minimize the difference between what is owed and the proceeds turned over to the lender, thereby minimizing the taxable income potentially accruing to the seller, the possibility remains. Sellers should be advised to consult with tax or legal counsel regarding the impact of the new law and other tax rules on their circumstances.

3. Foreclosures

25

3. Foreclosures In this module: • Judicial foreclosure vs. nonjudicial foreclosure • Buyer counseling on REOs

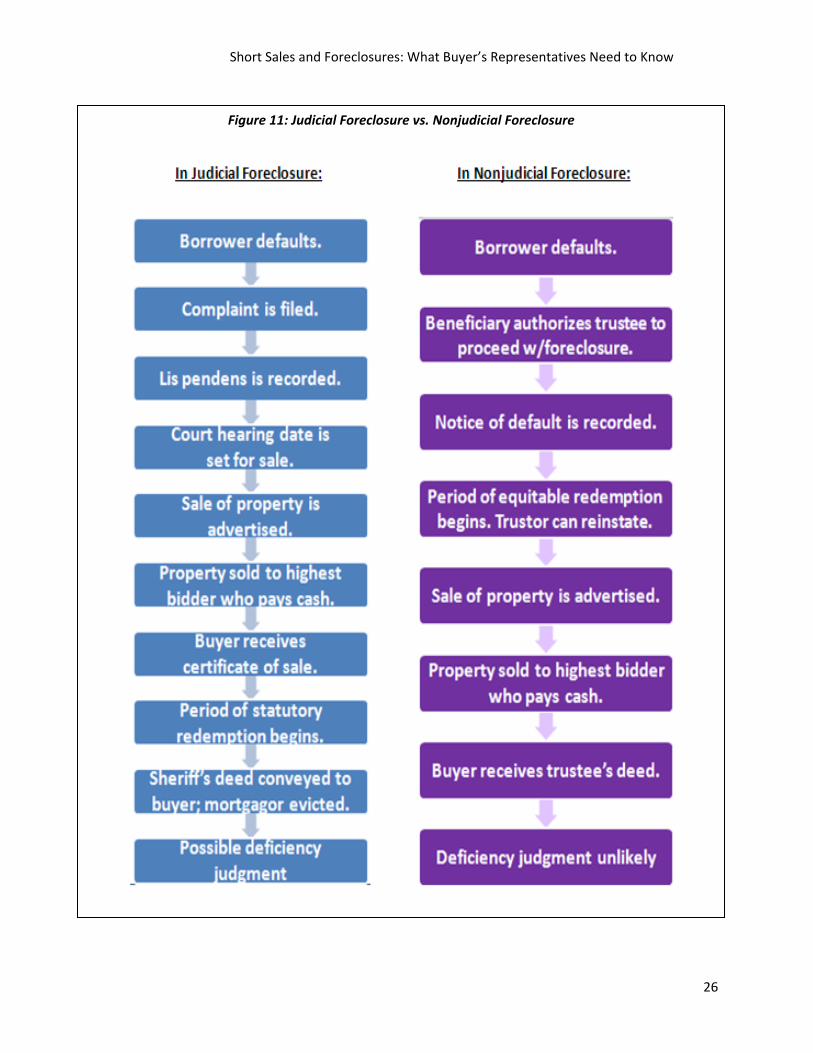

WHEN ALL ALTERNATIVES ARE EXHAUSTED: FORECLOSURE When refinancing, short sales, and/or loan modifications don’t work, the distressed homeowner is left with only one solution: foreclosure, which results in eviction of the homeowner and a forced sale of the property. How the proceedings will take place, the length of time to complete proceedings, and the outcome are largely are guided based on how property is held: mortgage or deed of trust. If the instrument is a mortgage, a judicial foreclosure or court‐ordered action is typically used to execute the foreclosure proceedings. In a judicial foreclosure, the lender obtains the right to foreclose by filing and winning a lawsuit. Note: The key is “winning” because a judicial foreclosure can turn into a nightmare for a lender when the mortgagor’s attorney plays on the heart strings of the court. To circumvent a full‐blown courtroom trial, most states allow summary judgment, which is a brief overview of the facts followed by a decision. If the instrument is a deed of trust, a nonjudicial foreclosure is typically used to execute the foreclosure proceedings. Nonjudicial foreclosures generally take less time to complete than judicial foreclosures. This is because the borrower pre‐authorizes the sale of the home in the loan document, which is usually in the form of a trust deed. The power‐of‐sale clause orders foreclosure upon default. This is similar to a power of attorney in that it grants the specified person, typically a trustee, the right to sell the borrower’s property if the lender notifies the trustee that the loan is in default.

Web Sites to Visit To determine if your state uses judicial and/or nonjudicial foreclosures, please visit: > www.foreclosurelaws.org > www.realtytrac.com

For a simplified overview of judicial and nonjudicial foreclosure processes, please see Figure 11.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

26

Figure 11: Judicial Foreclosure vs. Nonjudicial Foreclosure

3. Foreclosures

27

FORCED SALE OF PROPERTY If homeowners are unable to explore foreclosure alternatives, foreclosure proceedings require a forced sale of the property. A sheriff’s sale entails sale of a property, commonly through a sheriff’s auction, under authority of a court judgment in order to satisfy an unpaid obligation. In some states, this forced sale is done through a trustee sale. Recently, the term “foreclosure sale” has been used inappropriately by many real estate professionals as well as by consumers. The actual foreclosure sale is the sheriff’s auction/sale. Once the property is foreclosed it becomes an REO and should no longer be referred to as a “foreclosure sale.”

A Closer Look at Sheriff’s Sales

Sheriff’s sales are usually listed among the legal/judicial notices in the local newspaper. The scheduled sale of a particular property is published for a specific number of weeks prior to the sheriff’s auction/sale. The public notice usually includes the property address, mortgagee, mortgagor, appraised value, amount in default, property description, and date of the actual sale. Other information sources are the local legal news, county recorder’s office, or county Web sites. Even though the sheriff’s auction/sale of a specific property may be advertised and scheduled, often properties are not actually auctioned that day because the property owner has either sold it or reached an agreement with the lender (workout option) that takes the property “off the sheriff’s auction block.” Sheriff’s auctions/sales pose unique considerations for real estate buyers: • The opportunity to conduct property inspections can be negligible or

extremely limited. Real estate professionals should not expect to schedule a property inspection before the sheriff’s auction/sale. Potential buyers usually have limited or no access to properties offered at a sheriff’s sale because they are often still occupied by the owners or tenants.

Skill Builder Tip: Sheriff’s Auction vs. Private Auction There is a difference between the sherriff’s auction and a private auction. Any seller can use auction as a marketing tool to dispose of property. The sheriff’s auction is the forced sale of the property due to delinquency on the part of the borrower. • Buyers may be responsible for evicting occupants. After completion of the

sale and approval by the courts, if required by state law, it may be necessary for the buyer to initiate legal action to evict the occupants.

• Buyers may be responsible for paying outstanding liens.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

28

• Buyers may not receive clear title. For example, if a special warranty deed is issued, clear title is not guaranteed.

• Buyers may be impacted in states that offer borrowers the right of redemption.

Skill Builder Tip: Getting to Know Sheriff’s Auctions Buyers may want to attend the sheriff’s auction and attempt to purchase the property there. If you are going to accompany your buyer to a sheriff’s auction you both should attend at least 2 or 3 sheriff’s auctions to observe the protocol. Real estate professionals should consider recommending that buyers have a limited lien search done prior to the sheriff’s auction. Note: Most buyer’s representatives who accompany buyer clients to sheriff’s auctions, private auctions, etc., do so only with a written buyer representation agreement.

Sheriff’s Sale Reality Check: Why the Lender Gets the House

The minimum bid the lender will consider at a sheriff’s auction is, typically, more than what a purchaser is willing to pay. Just the mortgage alone is often more than the property is worth, and when you consider the extra costs incurred by the lender as well as delinquent property taxes, legal fees, etc., the property is not a bargain. In an area of declining property values, savvy investor buyers will not pay what is owed since that would be more than the market value of the property. Additionally, most investor buyers who attend sheriff’s sales are looking for a bargain. Consequently, the property goes back to the lender. Additionally, the pool of well‐financed investors has diminished in many markets. These issues, plus those mentioned previously, are why, in most cases, the sheriff’s auction process does not bring viable buyers for the property and the lender takes the property back.

REDEMPTION The right of the borrower to recover a property after foreclosure is known as a redemption period. This period varies widely from state to state; some states allow no redemption period, others allow up to a year or longer. If the borrower makes good on the past due payments during the redemption period, title to the property can be recovered. Some states allow the borrower to redeem the property by paying only the missed payments along with any accrued late charges and penalties; however, many states require the borrower to pay the loan balance in full.

3. Foreclosures

29

WHEN THE PROPERTY FAILS TO SELL AT SHERIFF’S AUCTION: REO When foreclosed properties don’t attract bidders at the sheriff’s auction, the property is considered real estate owned, or REO for short. REO means that the property or asset is owned by the lender. Lenders are motivated to recover the current balance of the asset and minimize the future loss. Some lenders handle asset management in‐house; others will outsource this responsibility. The asset manager is the person assigned to oversee the REO property from the listing through sale to close. They will work with the listing broker once the property has been assigned. All communication about the listing will go through the asset manager who may handle 200 to 300 listings at a time and oversee a multi‐state territory.

Counseling Buyers on REOs

As a general rule, buyers who are good candidates to purchase REO properties have the following characteristics: • Are experienced investors

• Understand that most REO properties are sold “as is”

• Have resources to repair and rehab the property if necessary

Buyer‐clients who are not good candidates are:

• “Wanna‐be” investors

• Those who have contingencies, such as those who need to sell another residence before they can buy

Preparing Buyer‐Clients on What to Expect

Buyers should be prepared as to what to expect before viewing properties. Most REO properties are sold “as‐is” and often need considerable repair. Some examples of property problems include:

• “Gutted” properties, missing appliances, cabinets, wiring, siding, plumbing

• Electricity disconnected

• Structural damage

• Missing or broken fixtures

Note: Most banks will not give seller concessions.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

30

Buying REOs

The lender’s internal cost to foreclose can be significant, considering items such as accrued interest, legal fees, condo fees/assessments, property taxes, water/sewer and the like. Costs accumulate and as the lender continues to incur costs over time, it improves the buyer client’s negotiating position. The buyer’s representative should understand that REO properties are different from the typical listings with which they are accustomed to working. REO transactions are investment driven; therefore, there are no emotional ties to the properties other than asset managers achieving their monthly goals. The buyer’s representative must be able to counsel the buyer on procedures and keep the end result in mind.

Showing REOs

If possible and appropriate, previewing properties on behalf of your buyer client should be considered as one of the value‐added benefits you provide as a buyer’s agent and also a practical approach so that you can prepare your buyer clients for what they are about to see.

Discussion Question

What other issues would need to be discussed when counseling and preparing

buyers on REOs?

3. Foreclosures

31

Skill Builder Tip: Don’t Allow the Client Unsupervised Access

A serious error made by many agents is to give a buyer client the access code or lock combination to enter these properties without the licensee being present. In many states this would be considered a violation of license law and/or MLS rules. Given their busy schedules, some licensees may think that this practice offers a transaction shortcut and saves time. However, allowing clients unsupervised access to an REO property is dangerous and should be avoided.

Issues of safety cannot be overlooked when showing vacant properties. In all cases the buyer representatives should know who their buyers are prior to showing and should not be meeting buyers at the property for the first time. Additionally, many of these properties have no electricity and showing them at night, and sometimes even during the day, can be hazardous. Real estate professionals should always take a flashlight with them and be mindful at all times of the potential for less than admirable condition of the premises.

Writing Offers on REO Properties

Typically the initial offer is written on the contract form customarily used by the buyer’s representative. The chances of your buyer’s offer being accepted are greater when: • The buyer makes an offer based upon market value. • The buyer has been pre‐approved for financing and includes this

information from the buyer’s lender with the contract. If buyer does not have a lender, sometimes having the existing lender doing the new buyer financing may make the transaction worthwhile for the lender.

• The buyer asks for a closing date that is sooner rather than later…possibly closing before month’s end so that the lender does not have to continue to carry the property on their books.

• The buyer agrees upfront to an “as‐is” transaction. • The buyer does not have any home sale or home close contingencies.

The buyer’s representative should call the listing agent for instructions on presentation of an offer. The listing agent then submits the offer to the asset

Skill Builder Tip 6: Home Inspections Buying in “as‐is” condition does NOT eliminate the right to an inspection period. Be certain your buyer asks for a home inspection in their offer and has a licensed inspector do a thorough inspection of the property.

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

32

manager, which can be accomplished in a variety of ways. In some instances, a Web site may be provided to help negotiate the offer with communication exchanged through the Web site until an offer is accepted. A counteroffer is handled through an addendum, which is sent to the listing agent from the asset manager, who forwards it to the buyer’s representative via fax or e‐mail. It is imperative that the buyer understands fully the contents of the addendum and it is advisable that the buyer seeks legal counsel. When the offer is accepted, the listing agent contacts the buyer’s representative and advises the acceptance of the offer. It is helpful to determine who the decision maker is when negotiating price or other considerations in an REO transaction. Even though the offer may have been accepted by the asset manager, it is common for the acceptance to be subject to senior management approval. Also, if possible, try to determine the parameters that an asset manager has been given for a particular property. Real estate professionals may find that they are only a few dollars away from the asset manager being able to make a decision; this can avoid the necessity for taking the decision to a higher organizational level for an approval. The asset manager’s focus is on the NET proceeds as a result of working with the buyer’s offer. It’s all about the bottom line. Buyer’s representatives should listen carefully to listing agents because they are an extension of the asset manager who deals with the decision maker/seller (remember, the bank or lender is the seller) and the asset manager is an extension of the seller and acts according to the sellers (bank/lender) directions. Any information you can gather from the listing agent will help your buyer‐client make an informed decision.

Don’t Practice Law Without a License

The review of lender addendums on an REO is another example of the NAR Code of Ethics Article 13 reference to recommending experts when the transaction warrants and agents should not be practicing law.

Limited Property Disclosures

Keep in mind that there may be limited property disclosures when it comes to REO properties. In some states, sellers of REO properties have no duty to disclose defects. Even though REO properties are generally bought “as is,” a home inspection offers some protection. If the client refuses to schedule a property inspection, the buyer’s representative should ask the client to sign an acknowledgment of the waiver of inspection. If a seller agrees to make

3. Foreclosures

33

concessions to the buyer for repairs, make sure it is included in the contract to make this a reality. As a good rule of thumb, ask the listing agent if this will be a possibility.

Managing the Funds

Earnest money deposits on REO transactions are handled in the same way as any other transaction. Customarily, in most states, earnest money is not deposited until there is a signed contract. The issue of who holds the earnest money may vary, but the timing of the deposit does not. If the lender holds off on signing the contract until the buyer signs any addendums the lender requires, earnest money should not be deposited until there is a fully executed contract. What is different is that in most REO transactions the lender will require that the earnest money be certified funds.

City Point of Sale (POS) Inspection

Some cities require a point of sale (POS) inspection. The purpose of this inspection is to assess the safety, soundness, and security of the property. The POS inspection may include both internal and external aspects, such as landscaping, sewer, and the like. An occupancy permit will not be issued until POS criteria are met. Customarily, the buyer assumes responsibility for correcting violations unless the seller fixes the violations. Lenders interested in a quick sale may be willing to discuss concessions regarding the repair of violations. Many cities require an escrow fund to cover costs of such repairs; for example, the municipality may require an amount equivalent to 1.5 times the bid be placed in escrow to assure correction of violations. Other cities have been known to block the closing until the repairs are made. It is imperative that you know what the requirements and rules are in the cities in which you are selling.

Final Walkthrough

It is not uncommon to see an addendum to the contract that reads “buyer to have walkthrough immediately before title transfer to ascertain property is in same condition as when purchase agreement was written.” It might be best for the walkthrough to occur a few days prior to the closing, if possible, to ensure there is time to work out any issues that may arise. Even though the buyer knows he or she is buying the property “as is,” the walkthrough assures the same “as is” condition as when the offer was presented. Keep in mind that the listing agent and seller usually have photos of the property condition at the time it was listed to ensure the buyer does not request unneeded repairs at closing. It is a good idea for a buyer’s

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

34

representative to take photos for the buyer at the time of purchase contract as a precaution in the event the property is not in the same condition at time of closing.

Closing Dates and Per Diems

In order to meet monthly revenue goals, asset managers prefer closings to take place at the end of the month rather than the beginning of the next month. A buyer’s representative should explain to their buyer that the closing date must be adhered to because, if not, it could cost the buyer extra dollars above and beyond the contract purchase price. Most sellers charge a daily penalty for every day the buyer is late in meeting the contract closing date. This fee is charged regardless of who caused the delay on the buyer’s side of the transaction, whether it is the buyer who is slow to deliver documents or the buyer’s lender who has no sense of urgency or a combination of both.

3. Foreclosures

35

Discussion Question: What are the possible benefits and disadvantages of buyers purchasing property at each of the following?

Possible Benefits

Short Sale Sheriff’s Sale REO

Possible Disadvantages

Short Sale Sheriff’s Sale REO

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

36

4. How Consumers Can Prevent Foreclosure In this module: • Become educated • Choosing the right loan

BECOME EDUCATED Education is a consumer’s strongest self‐defense in avoiding foreclosure. Real estate professionals who work with buyers—especially first‐time home buyers—should encourage them to take advantage of free pre‐purchase counseling offered by agencies and/or organizations approved or certified by the U.S. Department of Housing and Urban Development (HUD) and/or NeighborWorks® Center for Homeownership Education and Counseling (NCHEC). Education topics include: When homeownership is the right decision

Credit

How to qualify for a loan

Loans and financing options

Recourse or non‐recourse loan

Understanding what constitutes mortgage fraud

Finding the right house

What to expect at the loan closing

How to budget and make mortgage payments on time

Home insurance

Home maintenance and other post‐purchase considerations

The NAR, in partnership with the Center for Responsible Lending and NeighborWorks® America, has developed two brochures for consumers: • Shopping for a Mortgage? Do Your Homework First. Avoid Predatory Lending

• Are You Having Problems Paying Your Mortgage? Learn How to Avoid Foreclosure and Keep Your Home (available in English and Spanish)

Members of the NAR can downloaded these brochures for free at www.realtor.org/RightTools.

4. How Consumers Can Prevent Foreclosure

37

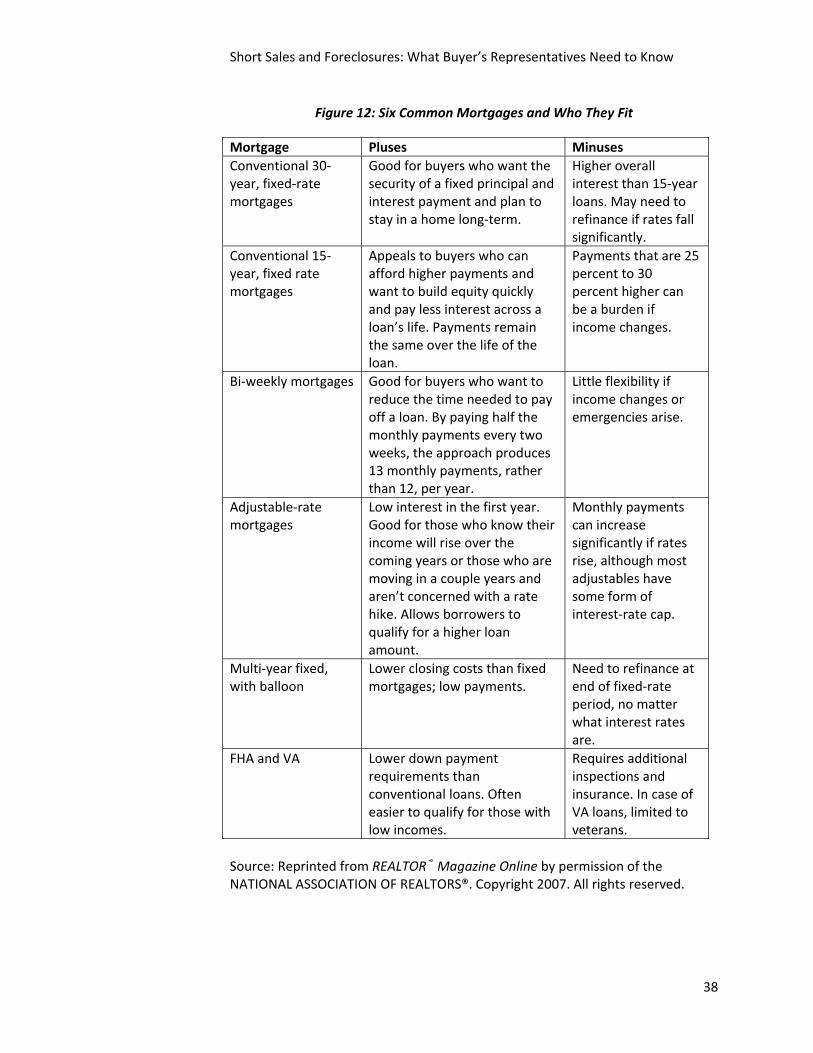

CHOOSING THE RIGHT LOAN Put simply, the best way for a buyer client to prevent foreclosure is choosing the right loan. Buyers must know their credit score, and they need to learn about the implications of credit scoring as it relates to mortgage rate availability. A lender may quote rates without ever looking at a credit score, but this will not give the buyer a true picture of an available rate for their mortgage loan. It is ONLY with credit scores that a buyer will actually learn about the accurate rate and terms that are available to them. Real estate professionals are encouraged to provide buyers with lender recommendations. Knowing the terms of one’s loan and having legal advice when reviewing the loan documents prior to signing are important as well. See the appendix for Common Questions to Ask Lenders when Shopping for a Loan. For a comparison of common mortgage products, see Figure 12. The primary determining factors in selecting a loan are chiefly the length of time the borrower plans to stay in the house and the amount of monthly payment that is affordable. If the borrower plans to stay in the house for less than five to seven years, it may be reasonable to consider an adjustable rate, balloon, or two‐step mortgage. For example, ARMs traditionally offer lower interest rates than fixed‐rate loans during the early years of the loan, a two‐step mortgage offers a lower interest rate than a 30‐year mortgage for the first five to seven years, and a balloon mortgage offers lower interest rates for shorter term financing, usually five or seven years. Low interest rates make it is easier to qualify for these types of mortgages. However, borrowers should not accept an ARM unless they can afford the maximum possible monthly payment (or will be able to when the payment increases).

Short Sales and Foreclosures: What Buyer’s Representatives Need to Know

38

Figure 12: Six Common Mortgages and Who They Fit

Mortgage Pluses Minuses Conventional 30‐year, fixed‐rate mortgages

Good for buyers who want the security of a fixed principal and interest payment and plan to stay in a home long‐term.

Higher overall interest than 15‐year loans. May need to refinance if rates fall significantly.

Conventional 15‐year, fixed rate mortgages

Appeals to buyers who can afford higher payments and want to build equity quickly and pay less interest across a loan’s life. Payments remain the same over the life of the loan.

Payments that are 25 percent to 30 percent higher can be a burden if income changes.

Bi‐weekly mortgages Good for buyers who want to reduce the time needed to pay off a loan. By paying half the monthly payments every two weeks, the approach produces 13 monthly payments, rather than 12, per year.

Little flexibility if income changes or emergencies arise.

Adjustable‐rate mortgages

Low interest in the first year. Good for those who know their income will rise over the coming years or those who are moving in a couple years and aren’t concerned with a rate hike. Allows borrowers to qualify for a higher loan amount.

Monthly payments can increase significantly if rates rise, although most adjustables have some form of interest‐rate cap.

Multi‐year fixed, with balloon

Lower closing costs than fixed mortgages; low payments.

Need to refinance at end of fixed‐rate period, no matter what interest rates are.

FHA and VA Lower down payment requirements than conventional loans. Often easier to qualify for those with low incomes.

Requires additional inspections and insurance. In case of VA loans, limited to veterans.

Source: Reprinted from REALTOR® Magazine Online by permission of the NATIONAL ASSOCIATION OF REALTORS®. Copyright 2007. All rights reserved.

4. How Consumers Can Prevent Foreclosure

39

STAYING AWARE OF PREDATORY LENDING PRACTICES It is also important to stay vigilant for illegal or abusive practices, such as bait‐and‐switch, stated‐income loans and the consumer’s liability, subprime loans, and traps of second mortgages.

Predatory Lending

Predatory lending can be characterized as lending practices that are harmful or abusive to borrowers. While the definition of predatory lending varies from state to state, there are many common practices. For a list of possible warning signs, see Figure 13.

Figure 13: Possible Warning Signs of a Predatory Loan • Sounds too easy. “Guaranteed approval” or “no income verification” regardless

of borrower’s current employment, credit history, and assets. These claims indicate the lender doesn’t care about whether you can afford to make the payments over the long haul.

• Excessive fees. Higher lender and/or mortgage broker fees than are typical in your market. Because these costs can be financed as part of the loan, they are easy to disguise or downplay. On competitive loans, fees are negotiable. It is common for home buyers to pay only one percent of the loan amount for prime loans. By contrast, a typical predatory loan may cost five percent or more.

• Large future costs. High‐risk adjustable‐rate mortgages where the payment rises a lot after a short introductory period are seldom appropriate for families who already have had problems repaying other loans. Home buyers also should avoid a large single “balloon” payment (a lump sum due at the end of the loan’s term).

• Closing delays. The lender deliberately delays closing so the commitment on a reasonably‐priced loan expires.

• Over‐valued property. Inflated appraisals that allow excessive fees to be included in the loan and result in the borrower owing more to the bank than the home is worth.

• Barriers to refinancing. Prepayment penalties that make it hard for a borrower to refinance in order to pay off a high‐cost loan by taking advantage of a low‐cost loan.

• No down payment loans. These loans may be split into two mortgages, with one having a much higher cost. Home buyers should be sure they can afford the payments.

• Unethical document management. An ethical lender or broker will always require you to sign key loan papers, and they will never ask you to sign a document dated before the date you sign it.