shortening the securities and cash settlement cycle from ... · between cash and securities cycles...

TRANSCRIPT

Shortening the Securities and Cash Settlement Cycle from T+3 to T+2Bringing efficiency to the entire trade lifecycle is the key to decreasing risk. With increased cross border trade activities, the post trade process continues to be complex and challenging for investment firms due to lack of harmonization in market practices. Despite technology advances and business process improvements, there are inefficiencies in the settlement process leading to trade and settlement failure. The cost of stock borrowing to avert the risk of trade failure has increased because of the exponential increase in settlement failure. Many firms cite inaccurate settlement and account instruction (SI) data as the most significant reason for failure, followed by the deliberate failure to settle by counterparties and mismatches between cash and securities cycles. Both buy side and sell side firms are looking to mitigate counterparty and operational risks as well as reduce costs.

Recently, the European Commission (EC) mandated reducing the settlement cycle for securities to not later than T+2 - to be implemented by 2015. This mandate by EC is not only focused at driving market efficiency but also promises to act as an important enabler for the Target2Securities(T2S) implementation program. Countries such as India,

White Paper

2

Hong Kong, Taiwan and Germany that have transitioned to the T+2 settlement cycle have shown improvement in market efficiencies with decline in settlement failures and the associated risks.

Reducing the settlement cycle from T+3 to T+1 poses high risk and challenges to market participants due to the lack of key enablers, technology limitations and increased investments required for implementation. On the other hand, transitioning to T+2 requires lesser investment with fewer changes to the business processes by each participant. The most important change required for transition is to mandate market participants to affirm trades on the day the trade is executed, enabling timely and accurate settlement.

Firms must look beyond short-term goals and evaluate options to re-engineer business processes and enhance IT infrastructure of the impacted business areas before transitioning to a reduced settlement cycle. They must view this as an opportunity to invest in their technology infrastructure, to achieve the end objective of decreasing risk while enhancing business efficiency

3

About the Authors

Ganesh Padmanabhan

Ganesh has 7 years of experience in IT solutioning and consulting in the Capital Markets domain. He has worked with leading market infrastructure firms on the initiatives of Corporate actions and settlements.. Ganesh holds a master's degree in business administration from the S. P. Jain Center of Management, Singapore.

Ramakoteswara Rao T

Ramakoteswara Rao has over 15 years of experience working with manufacturing, retail, banking and capital market customers across the US, UK and Europe. His key areas of responsibility include large program management, wealth management and related industry initiatives. Rao holds a Master's degree in Mechanical Engineering from IIT, Madras.

4

Table of contents

1 Introduction 5

2 Shortening The Settlement Cycle 5

2.1. Current Scenario 5

2.2. Challenges In The Current Settlement Cycle 6

2.3. Why T+1 Is Not Possible 7

2.4. Changes Required For A Transition From T+3 Tot+2 Settlement Cycle 8

2.5. Benefits And Costs Associated With Reduced Settlement Periods 9

2.6. Areas And Measures Of Market Discipline To Be Followed For Moving T+2 Settlement Cycle 9

3 Experience From Other Geographies 10

4 Conclusion 11

1. Introduction

Over the years, the financial services industry has spent a substantial amount of money speeding up the trading process, but not a lot on the middle and back office for post-trade process. With recent changes to market structures, regulators have initiated important steps toward improving operational efficiencies and reducing risks (credit and liquidity) by shortening the equity trade settlement cycle. This initiative from the European Commission has spurred the United States and other Asian countries (except India, South Korea, Hong Kong and Taiwan) with divergent cycles to reconsider the adoption of T+2 as the standard equity settlement cycle. This initiative provides an opportunity to market participants to streamline processes in the middle-office to reduce operational risks and improve efficiencies through automation. However, there are concerns that reducing the settlement cycle will increase the risk of settlement failure particularly in the absence of a trade matching or confirmation process. This paper analyzes the potential impact of shortening the equities settlement cycle from T+3 to T+2.

2. Shortening the Settlement Cycle

2.1. Current Scenario

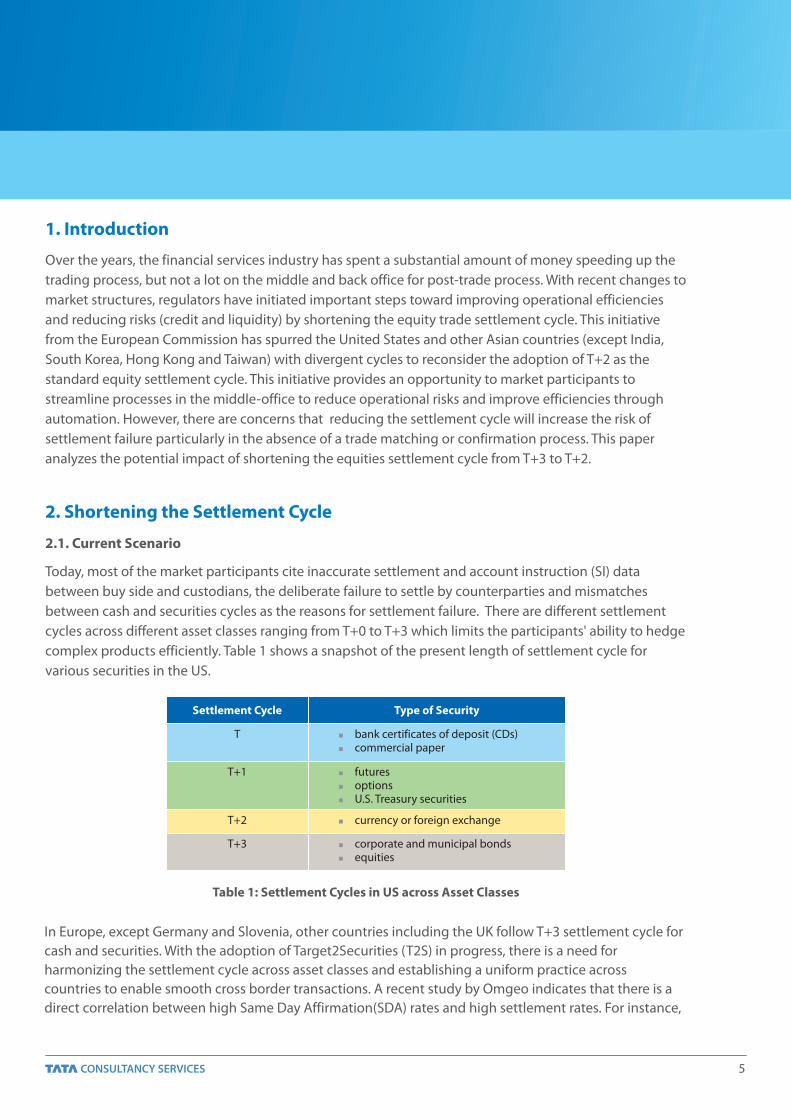

Today, most of the market participants cite inaccurate settlement and account instruction (SI) data between buy side and custodians, the deliberate failure to settle by counterparties and mismatches between cash and securities cycles as the reasons for settlement failure. There are different settlement cycles across different asset classes ranging from T+0 to T+3 which limits the participants' ability to hedge complex products efficiently. Table 1 shows a snapshot of the present length of settlement cycle for various securities in the US.

5

Settlement Cycle Type of Security

T bank certificates of deposit (CDs) commercial paper

T+1 futures options U.S. Treasury securities

T+2 currency or foreign exchange

T+3 corporate and municipal bonds equities

Table 1: Settlement Cycles in US across Asset Classes

In Europe, except Germany and Slovenia, other countries including the UK follow T+3 settlement cycle for cash and securities. With the adoption of Target2Securities (T2S) in progress, there is a need for harmonizing the settlement cycle across asset classes and establishing a uniform practice across countries to enable smooth cross border transactions. A recent study by Omgeo indicates that there is a direct correlation between high Same Day Affirmation(SDA) rates and high settlement rates. For instance,

6

countries with short settlement cycles such as India, Hong Kong and Taiwan which adopted T+2 early have better settlement efficiency than countries like the US, UK and other European countries. Today, a majority of the Central Securities Depositories (CSD) have a penalty scheme in place for late settlement, although the type of fee levied varies across markets (recycling fee vs. penalty fee, with some CSDs charging both). These penalty fees form a part of CSD revenue and apply to a broad set of transfer instructions, both for settlement failures due to lack of securities or lack of cash. In order to support settlement efficiency and reduce the incidence of settlement failure, CSDs are offering securities lending and borrowing services ranging from providing technical facilities to enable matching of lenders and borrowers to acting as principals in a securities lending and borrowing transaction. In the current scenario, a few of the major European CSDs report that nearly 20 – 50% of the transactions are settled in less than T+3 and, 45% to 65% in T+3 while a very small proportion have a longer settlement period.2.2. Challenges with the current settlement cycle

2.2. Challenges with the current settlement cycle

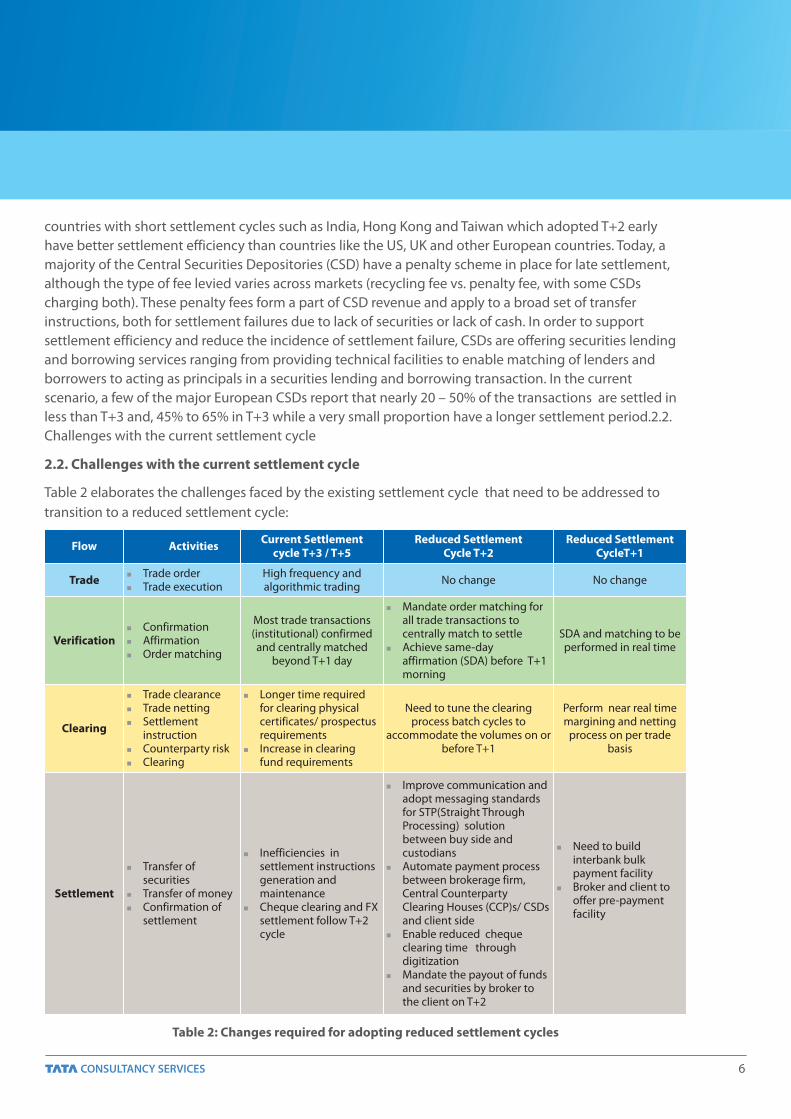

Table 2 elaborates the challenges faced by the existing settlement cycle that need to be addressed to transition to a reduced settlement cycle:

Flow ActivitiesCurrent Settlement

cycle T+3 / T+5Reduced Settlement

Cycle T+2Reduced Settlement

CycleT+1

Trade Trade order Trade execution

High frequency and algorithmic trading

No change No change

Verification Confirmation Affirmation Order matching

Most trade transactions (institutional) confirmed and centrally matched

beyond T+1 day

Mandate order matching for all trade transactions to centrally match to settle

Achieve same-day affirmation (SDA) before T+1 morning

SDA and matching to be performed in real time

Clearing

Trade clearance Trade netting Settlement

instruction Counterparty risk Clearing

Longer time required for clearing physical certificates/ prospectus requirements

Increase in clearing fund requirements

Need to tune the clearing process batch cycles to

accommodate the volumes on or before T+1

Perform near real time margining and netting

process on per trade basis

Settlement

Transfer of securities

Transfer of money Confirmation of

settlement

Inefficiencies in settlement instructions generation and maintenance

Cheque clearing and FX settlement follow T+2 cycle

Improve communication and adopt messaging standards for STP(Straight Through Processing) solution between buy side and custodians

Automate payment process between brokerage firm, Central Counterparty Clearing Houses (CCP)s/ CSDs and client side

Enable reduced cheque clearing time through digitization

Mandate the payout of funds and securities by broker to the client on T+2

Need to build interbank bulk payment facility

Broker and client to offer pre-payment facility

Table 2: Changes required for adopting reduced settlement cycles

7

2.3. Why T+1 is not possible

Limitation in existing market infrastructure – To successfully adopt the T+1 settlement cycle, CSDs have to rationalize the settlement batch process accordingly. The settlement process will need to be advanced and start in the evening of the given trade (T) day rather than at night. As a result, pre-settlement activities such as CCP netting activities as well as the entire process of initiating, transmitting, matching and funding settlement instructions will need to be advanced and completed before the start of the settlement process. This will significantly impact operational efficiencies.

Pressure on back office function of buy side - The biggest challenge in shortening settlement cycle is to reduce the time given to the back-offices of buy and sell side firms to perform all the pre-settlement activities. Many firms currently use obsolete modes of communication and transaction processing. In addition, the adoption rate of messaging standards is low for most of the broker dealers and investment management firms. Following non-standard communication methods and outdated technology lead to higher cost and problems in reconciliation of trade details which impact reclaimed transactions on settlement day.

Payment system and client funding bottlenecks – Reducing the settlement cycle will impact payment systems which support and act as an enabler for markets. Broker dealers have to transition their clients to make payments before the transaction or use Automated Clearing House debits. The current cheque clearing time will need to be reduced and real-time clearing will have to be enabled through digitization.

Foreign exchange (FX) transaction for cross border trades – Cross border trading and securities transactions result in spot foreign exchange (FX) transactions which follow the T+2 settlement cycle. Under T+1, investors will need to tap 'Tomorrow's Market(TOM)Next' for the FX market or borrow the currencies involved in the trade.

Technological limitations – To adopt T+1 settlement cycle, firms have to revamp their back-office operations and technology architecture, as well as basic business practices which call for fundamental changes.

The back office system should be capable of real-time, concurrent multi-stage trade-data enrichment for executing, allocating and settling trades. This requires parallel processing which involves significant investments in hardware and middleware.

The order-management or portfolio-accounting systems have to be re-designed to rule based processing / complex event processing (CEP) platforms similar to FX platforms. Buy side firms will struggle to support the changes due to the presence of multiple platforms.

Firms will need to improve their data infrastructure due to reduced time available for reconciliation and correction of data. Adopting an appropriate data infrastructure to manage and process data to cater to the changes and demands will require significant investments.

Firms will need to implement high-availability systems such as real-time data and application backups and have disaster recovery mechanisms in place to switch to a standby system without losing any transactions.

8

Buy side firms will need to enable real-time monitoring of trade status and implement an operational risk management system for continuous monitoring of operations, processes and infrastructure systems.

2.4. Changes required for a transition from T+3 toT+2 settlement cycle

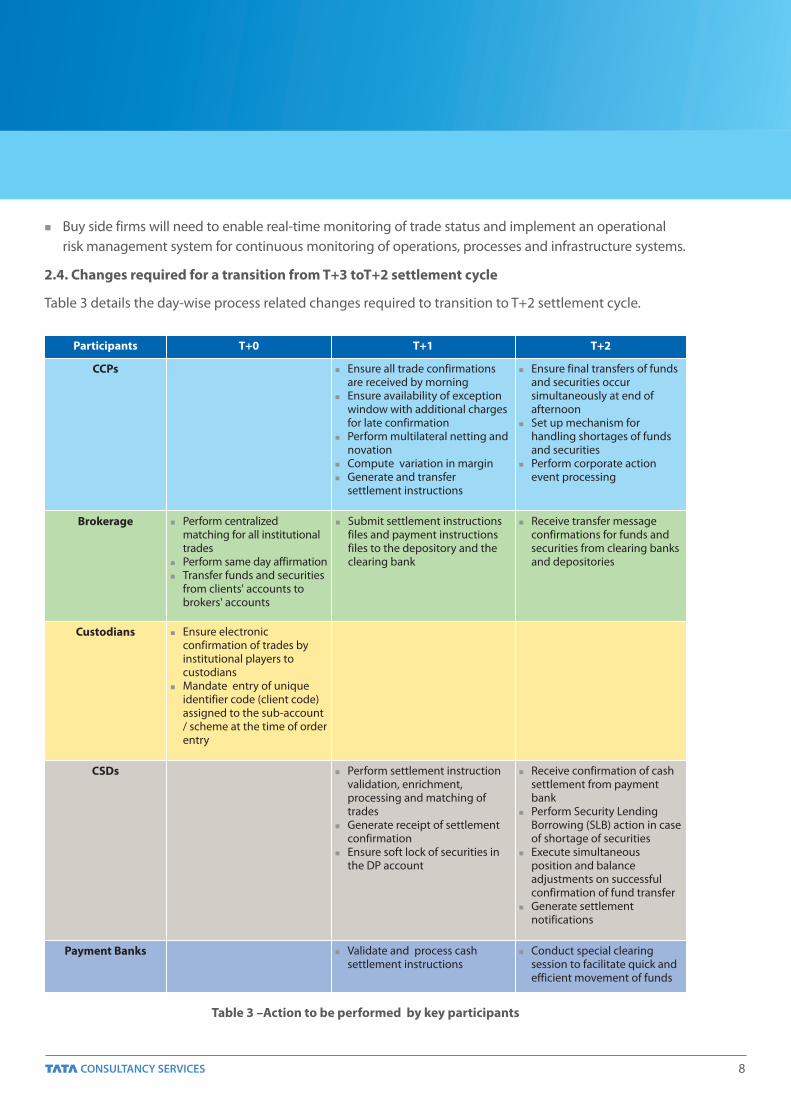

Table 3 details the day-wise process related changes required to transition to T+2 settlement cycle.

Participants T+0 T+1 T+2

CCPs Ensure all trade confirmations are received by morning

Ensure availability of exception window with additional charges for late confirmation

Perform multilateral netting and novation

Compute variation in margin Generate and transfer

settlement instructions

Ensure final transfers of funds and securities occur simultaneously at end of afternoon

Set up mechanism for handling shortages of funds and securities

Perform corporate action event processing

Brokerage Perform centralized matching for all institutional trades

Perform same day affirmation Transfer funds and securities

from clients' accounts to brokers' accounts

Submit settlement instructions files and payment instructions files to the depository and the clearing bank

Receive transfer message confirmations for funds and securities from clearing banks and depositories

Custodians Ensure electronic confirmation of trades by institutional players to custodians

Mandate entry of unique identifier code (client code) assigned to the sub-account / scheme at the time of order entry

CSDs Perform settlement instruction validation, enrichment, processing and matching of trades

Generate receipt of settlement confirmation

Ensure soft lock of securities in the DP account

Receive confirmation of cash settlement from payment bank

Perform Security Lending Borrowing (SLB) action in case of shortage of securities

Execute simultaneous position and balance adjustments on successful confirmation of fund transfer

Generate settlement notifications

Payment Banks Validate and process cash settlement instructions

Conduct special clearing session to facilitate quick and efficient movement of funds

Table 3 –Action to be performed by key participants

9

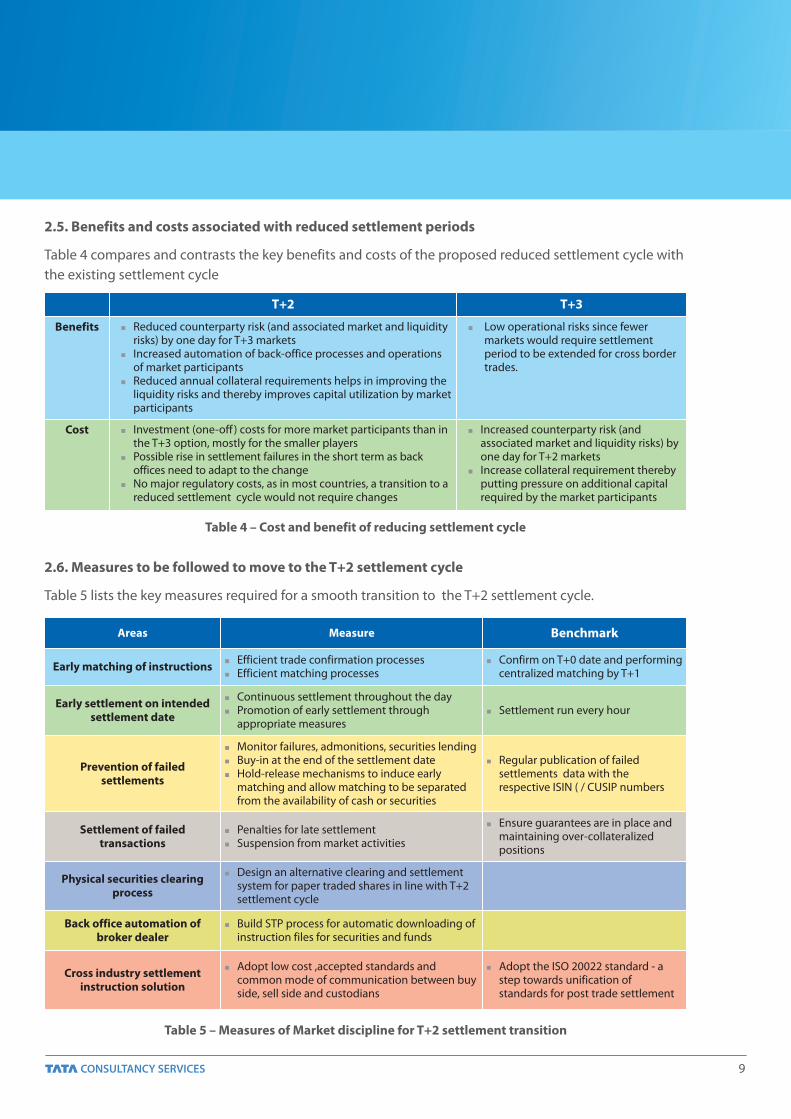

2.6. Measures to be followed to move to the T+2 settlement cycle

Table 5 lists the key measures required for a smooth transition to the T+2 settlement cycle.

2.5. Benefits and costs associated with reduced settlement periods

Table 4 compares and contrasts the key benefits and costs of the proposed reduced settlement cycle with the existing settlement cycle

T+2 T+3

Benefits Reduced counterparty risk (and associated market and liquidity risks) by one day for T+3 markets

Increased automation of back-office processes and operations of market participants

Reduced annual collateral requirements helps in improving the liquidity risks and thereby improves capital utilization by market participants

Low operational risks since fewer markets would require settlement period to be extended for cross border trades.

Cost Investment (one-off ) costs for more market participants than in the T+3 option, mostly for the smaller players

Possible rise in settlement failures in the short term as back offices need to adapt to the change

No major regulatory costs, as in most countries, a transition to a reduced settlement cycle would not require changes

Increased counterparty risk (and associated market and liquidity risks) by one day for T+2 markets

Increase collateral requirement thereby putting pressure on additional capital required by the market participants

Table 4 – Cost and benefit of reducing settlement cycle

Areas Measure Benchmark

Early matching of instructions Efficient trade confirmation processes Efficient matching processes

Confirm on T+0 date and performing centralized matching by T+1

Early settlement on intended settlement date

Continuous settlement throughout the day Promotion of early settlement through

appropriate measures Settlement run every hour

Prevention of failed settlements

Monitor failures, admonitions, securities lending Buy-in at the end of the settlement date Hold-release mechanisms to induce early

matching and allow matching to be separated from the availability of cash or securities

Regular publication of failed settlements data with the respective ISIN ( / CUSIP numbers

Settlement of failed transactions

Penalties for late settlement Suspension from market activities

Ensure guarantees are in place and maintaining over-collateralized positions

Physical securities clearing process

Design an alternative clearing and settlement system for paper traded shares in line with T+2 settlement cycle

Back office automation of broker dealer

Build STP process for automatic downloading of instruction files for securities and funds

Cross industry settlement instruction solution

Adopt low cost ,accepted standards and common mode of communication between buy side, sell side and custodians

Adopt the ISO 20022 standard - a step towards unification of standards for post trade settlement

Table 5 – Measures of Market discipline for T+2 settlement transition

10

3. Experience across different geographies

Case 1 - India moved to the T+2 settlement cycle in 2003 though the online fund settlement system was at a nascent stage. Despite the movement of funds under the Real-Time Gross Settlement (RTGS) system not being smooth, the regulator mandated confirmation of institutional trades by custodians latest by 11.00 a.m. on T+1.

Case 2 -Taiwan moved to the T+2 settlement cycle and made changes to the implementation process, similar to India. The changes included introducing a pre-settlement mechanism, in which custodian banks need to confirm pre-settlement for the executed DVP trades by T+1 afternoon, and trade affirmation between investors and broker on T+1. Further, local sub- custodians are required to send trade affirmation to the execution brokers on T+1 to facilitate trade settlement on T+2.

Case 3 - Hong Kong has recently moved to the T+2 settlement cycle with a prepayment option on exchange trades settled in the Central Clearing and Settlement System (CCASS), operated by HKEx's wholly-owned subsidiary, Hong Kong Securities Clearing Company (HKSCC). However, for non-pre-payment option, the settlement mechanism follows the T+3 cycle for securities and money settlement. For the T+2 settlement cycle, the payment obligation is fulfilled using overnight interbank bulk settlement processes by the Hong Kong Interbank Clearing Limited (HKICL). With this settlement arrangement, Hong Kong has bridged the gaps and adopted international best practices by finalizing securities transactions including money settlement on the same day.

From the above cases, it is clear that one of the critical success factors for shortening the settlement cycle is the confirmation of trades between direct market participants as soon as possible after trade execution, but no later than the trade date (T+0).

Where confirmation of trades by indirect market participants (such as institutional investors) is required, it should occur as soon as possible after trade execution, preferably on T+0, but no later than T+1.

Pre-payment options can be leveraged to eliminate funding bottlenecks and act as an enabler for the market participants to adopt the change faster. Mandating same day affirmation helps in improving settlement efficiencies.

Case - Canada mandated that 90% of the institutional trades be matched by noon one day after the trade is executed through a regulatory rule NI 24-101 in 2007. Due to this regulation, many of the Canadian investment management firms focused on improving the process efficiency of post-trade operations.

Three years after enforcing the regulation, the domestic Canadian market is increasingly automated. While 93% of investment managers use electronic trade matching solutions for equity trades, 80% use it for fixed income trades. For cross-border transactions, 80% are using trade matching for equities and 74% use it for fixed income.

As a result of this regulation and investment in back office systems, Canadian investment firms and custodians are confident of adapting to changes in trade settlement cycles in North America and Europe.

11

4. Conclusion

Over the years, significant developments in front office systems and low latency trading capabilities which threaten the stability and integrity of the markets have been a cause of concern for regulatory and other salutatory bodies.

Currently, the European Commission is undertaking several initiatives to rationalize the settlement process. By standardizing the settlement cycle, the European commission can aim for smoother adoption of its Target2Securities program and then look at opportunities to harmonize corporation actions cycles.

Smooth implementation by market participants, however, requires adopting a methodological approach. Transitioning directly to a T+1 settlement cycle is challenged by technology limitations and key business risks impacting the overall implementation. Hence moving to T+2 can be the first step with key enablers such as building stronger payment and foreign exchange infrastructure. With this in place, adoption of T+1 adoption can be reevaluated and subsequently executed.

Moving from the existing T+3 to T+2 settlement cycle is considered less risky given the current scenario. However, it will require some business process re-engineering efforts in pre-settlement activities by the buy side, custodians and sell side. Market infrastructure firms will have to fine tune their clearing and settlement functions and align with changes to the business process.

Reducing the settlement cycle to T+2 will bring benefits in the form of reduced capital requirement through reduction of counterparty and liquidity risk, reduced collateral requirements for settlements and improved market efficiency through STP, achieved by enhancing the efficiency of middle and back office processes through automation. For the successful adoption of T+2 settlements the following need to be in place-

Mandating market participants to affirm trades on the day the trade is executed, enabling both timely and accurate settlement

Pre-payment options eliminating the funding bottlenecks and also acting as an enabler for market participants to adopt the change faster

Early matching of instructions and promotion of early settlement by CSDs

Prevention of failed settlements through continuous monitoring and measures improving the settlement efficiencies

Promoting Regulations in bringing efficiency in the post trade operations.

Investment management firms, asset management firms and custodians should not consider shortening settlement cycles a regulatory burden. They should look at it as an opportunity to improve their systems and processes thereby reducing trade lifecycle risks.

12

References[1] Hong Kong Exchanges and Clearing Limited, Consultation Paper on Introduction of T+2 Finality Arrangement for CCASS Money Settlement, November 2009 [2] SEBI, Implementation of T+2 Rolling Settlement, April 2003[3] ESCB, CESR Recommendation for Securities Settlement Systems in European Union, May 2009[4] ECSDA, Market Discipline Regimes in Europe, September 2009[5] ECB, Settlement Fails : Report on Securities Settlement Systems Measures to Ensure Timely Settlement, April 2011[6] European Commission, Impact assessment on improving securities settlement in the European Union and on Central Securities Depositories (CSDs) and amending Directive 98/26/EC, March 2012[7] Boston Consulting Group Commissioned by The Depository Trust and Clearing Corporation, Cost benefit analysis of shortening the settlement cycle, December 2012[8] Harmonization of Settlement cycles Working Group, Reasons why T+1 was not considered as a valid option, October 2010[9] Omgeo, Mitigating Operational Risk and Increasing Settlement Efficiency through Same Day Affirmation, October 2010[10] Victoria Lynn Messman, Securities Processing : The Effects of a T+3 system on Security Prices, May 2011

All content / information present here is the exclusive property of Tata Consultancy Services Limited (TCS). The content / information contained here is correct at the time of publishing. No material from here may be copied, modified, reproduced, republished, uploaded, transmitted, posted or distributed in any form without prior written permission from TCS. Unauthorized use of the content / information appearing here may violate copyright, trademark and

other applicable laws, and could result in criminal or civil penalties. Copyright © 2013Tata Consultancy Services Limited TCS

Des

ign

Serv

ices

M

07

13

II

I

IT ServicesBusiness SolutionsConsulting

Subscribe to TCS White PapersTCS.com RSS: http://www.tcs.com/rss_feeds/Pages/feed.aspx?f=wFeedburner: http://feeds2.feedburner.com/tcswhitepapers

ContactFor more information about TCS’ consulting services, contact [email protected]

About Tata Consultancy Services (TCS)Tata Consultancy Services is an IT services, consulting and business solutions organization that delivers real results to global business, ensuring a level of certainty no other firm can match.TCS offers a consulting-led, integrated portfolio of IT and IT-enabled infrastructure, engineering

TMand assurance services. This is delivered through its unique Global Network Delivery Model , recognized as the benchmark of excellence in software development. A part of the Tata Group, India’s largest industrial conglomerate, TCS has a global footprint and is listed on the National Stock Exchange and Bombay Stock Exchange in India.

For more information, visit us at www.tcs.com