simon chapman - wbs entrepreneurship mentoring programme - final workshop

TRANSCRIPT

1www.burgisbullock.com

Valuations and the use of equity

WBS Entrepreneurship Mentoring Programme

Simon Chapman30 March 2012

2www.burgisbullock.com

Introduction to Burgis & Bullock

Midlands firm of accountants and business advisers.

Clients include entrepreneurs, owner-managed businesses, corporates, and private equity backed companies.

Specialist corporate finance practice.

Valuations for M&A deals, dispute resolution, tax purposes, and estate planning.

3www.burgisbullock.com

Speaker profile

Corporate finance partner at Burgis & Bullock.

17 years in M&A

Experience at Ernst & Young, Baker Tilly, and in industry

Valuations for M&A transactions, divorces, shareholder disputes, and fairness opinions

Panel of experts of the President ICAEW

4www.burgisbullock.com

How would you value……..

5www.burgisbullock.com

Key questions before you start a valuation

What am I valuing?

Why am I valuing it?

For whom am I doing this valuation?

As at what date is the valuation?

6www.burgisbullock.com

Reasons to carry out a valuation

Fiscal valuations

Dispute resolution

Commercial valuations

Financial reporting

7www.burgisbullock.com

Fiscal valuations

Share option schemes

Probate and inheritance tax purposes

Trust and estate planning

Group re-structurings

Capital Gains Tax

Employment Related Securities

8www.burgisbullock.com

Dispute resolution

Shareholder disputes and exits

Compulsory share transfers

Companies Act 2006

Divorce

Litigation

Share purchase agreements

9www.burgisbullock.com

Commercial valuations

Mergers and acquisitions

Disposals

MBOs and MBIs

IPOs

Capital reconstructions

Lender security assessments

Raising new finance

10www.burgisbullock.com

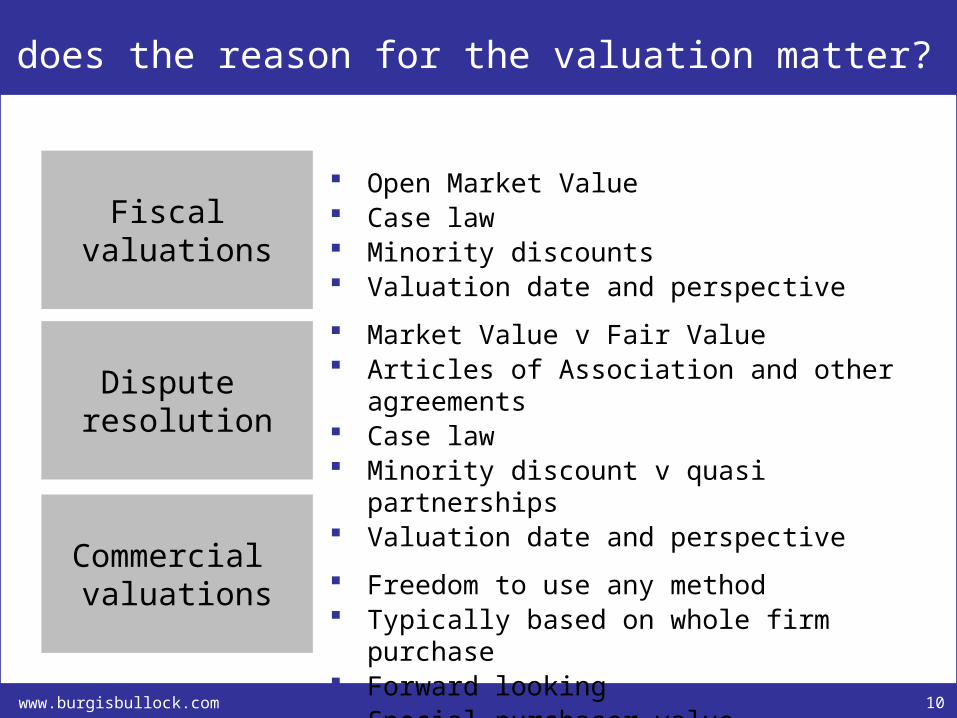

Why does the reason for the valuation matter?

Fiscal valuations

Dispute resolution

Commercial valuations

Open Market Value Case law Minority discounts Valuation date and perspective

Market Value v Fair Value Articles of Association and other agreements Case law Minority discount v quasi partnerships Valuation date and perspective

Freedom to use any method Typically based on whole firm purchase Forward looking Special purchaser value

11www.burgisbullock.com

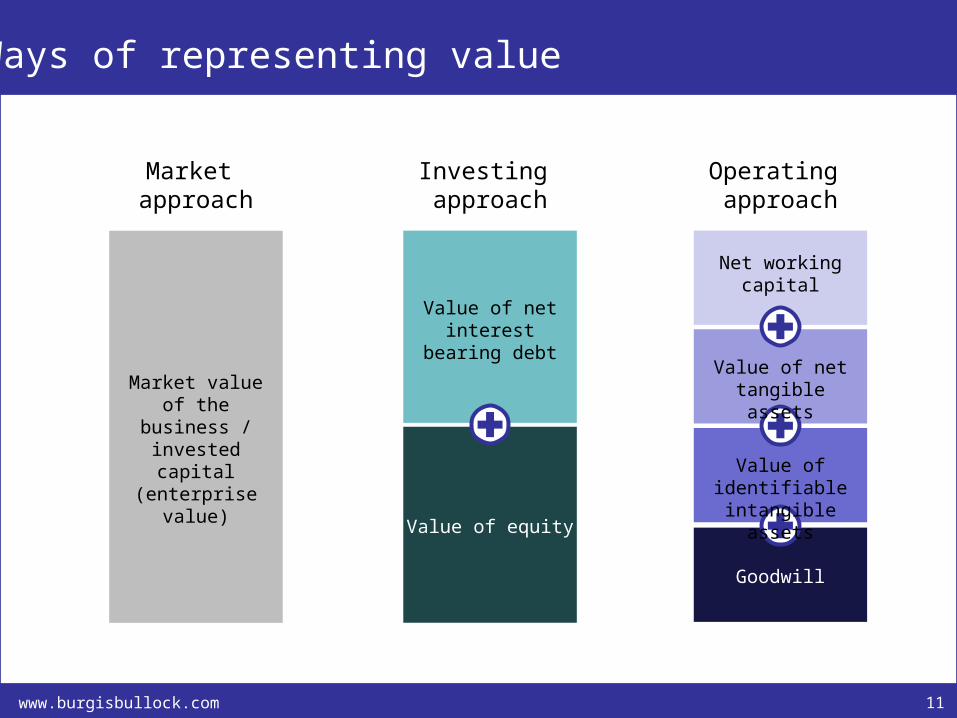

Ways of representing value

Market value of the business /

invested capital (enterprise

value)

Value of net interest bearing

debt

Value of equity

Net working capital

Value of net tangible assets

Value of identifiable intangible assets

Goodwill

Market approach

Investing approach

Operating approach

12www.burgisbullock.com

Theoretical underpinning of a valuation

Expected future earnings or cash flows

Risk of the earnings or cash flows

not materialising

Timing of the earnings

or cash flows

Fair or market value…What will someone pay

given these facts?

13www.burgisbullock.com

Main valuation methods

Asset value

Capitalisation of earnings

Mixed methods

Discounted cash flow

Industry “rules of thumb”

Risk/reward models

Other methods, e.g. options

14www.burgisbullock.com

Asset value

Valuation of individual asset components

Book value v adjusted book value

Liquidation value

Entry cost

Bank security

Net realisable value

Low risk / underpins other valuation methods

15www.burgisbullock.com

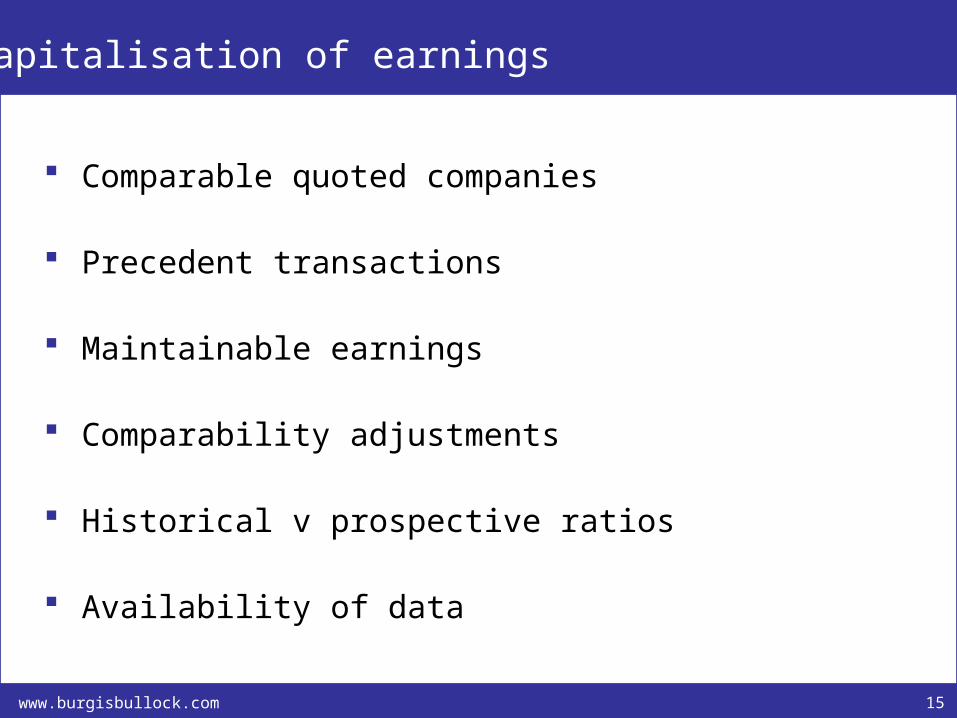

Capitalisation of earnings

Comparable quoted companies

Precedent transactions

Maintainable earnings

Comparability adjustments

Historical v prospective ratios

Availability of data

16www.burgisbullock.com

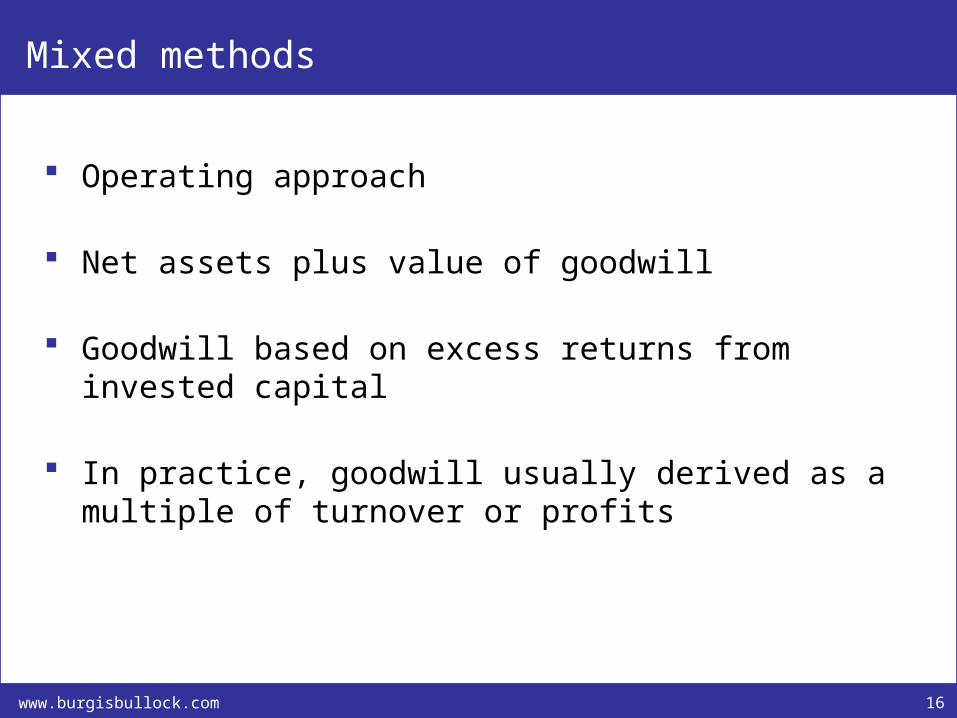

Mixed methods

Operating approach

Net assets plus value of goodwill

Goodwill based on excess returns from invested capital

In practice, goodwill usually derived as a multiple of turnover or profits

17www.burgisbullock.com

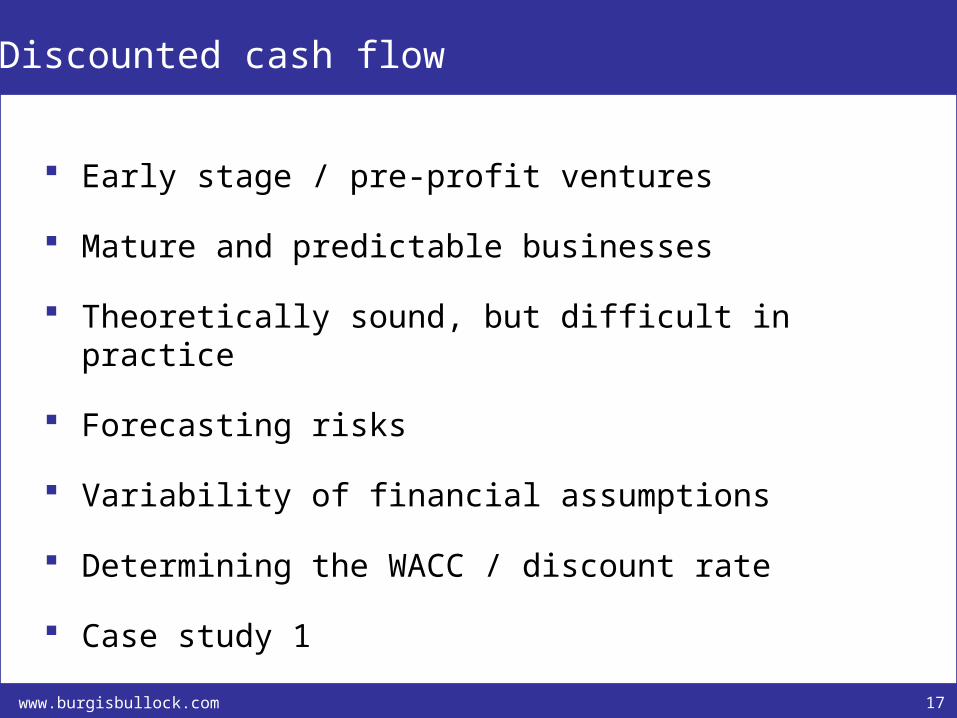

Discounted cash flow

Early stage / pre-profit ventures

Mature and predictable businesses

Theoretically sound, but difficult in practice

Forecasting risks

Variability of financial assumptions

Determining the WACC / discount rate

Case study 1

18www.burgisbullock.com

Industry “rules of thumb”

Very common in practice

Ultimately derived from DCF and comparables – but are the base assumptions still valid?

Per unit basis, e.g. nursing homes

Turnover multiples, e.g. accountancy practices

Per user basis, e.g. internet businesses

19www.burgisbullock.com

Risk/reward models

Investor’s target return

Forecasting risk

Exit risk/assumptions

Impact of gearing

Impact of share structuring and different share rights

20www.burgisbullock.com

Key methods preferred by investors

Capitalisation of earnings – based on precedent transactions

Risk/reward models

Asset basis and “rules of thumb” may be used as secondary methods to underpin core methods

Discounted cash flow rarely used in practice

21www.burgisbullock.com

Quoted company comparables

Selecting the peer group

Liquidity and marketability discounts

Control premia and minority discounts

Differential size and growth characteristics

22www.burgisbullock.com

Quoted company comparables

Case study 2

Privately owned specialist nuclear engineering business

Turnover of £14m and EBIT of £1.8m

Forecast profit growth of 15% per annum over next 3 years

Approached by listed company

How would you value based on listed comparators?

23www.burgisbullock.com

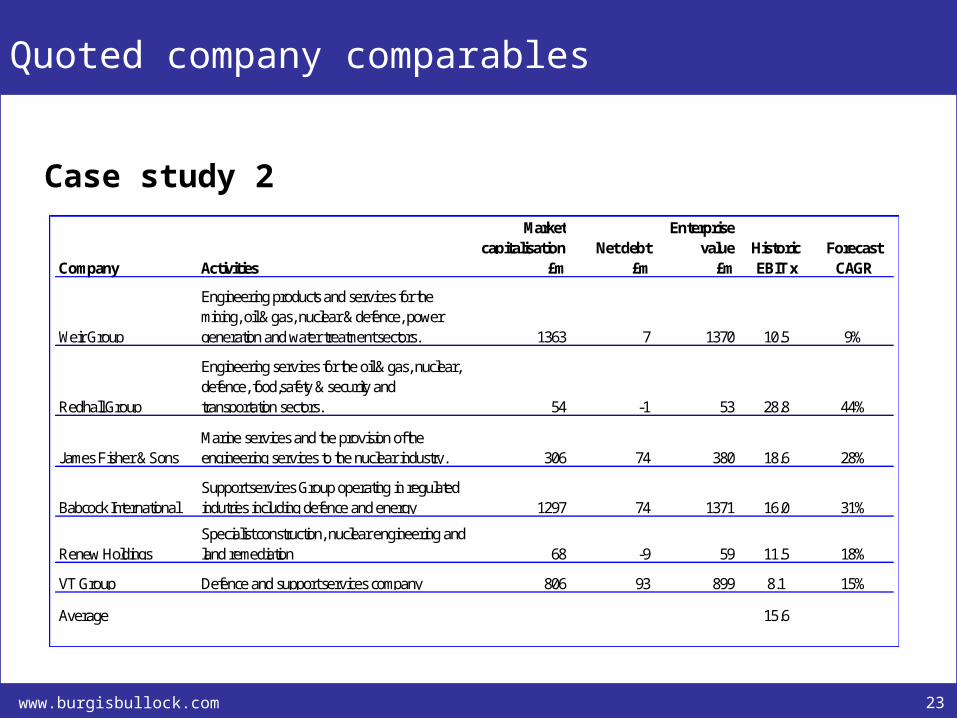

Quoted company comparables

Case study 2Market

capitalisation Net debtEnterprise

value Historic ForecastCompany Activities £m £m £m EBIT x CAGR

Weir Group

Engineering products and services for the mining, oil & gas, nuclear & defence, power generation and water treatment sectors. 1363 7 1370 10.5 9%

Redhall Group

Engineering services for the oil & gas, nuclear, defence, food,safety & security and transportation sectors. 54 -1 53 28.8 44%

James Fisher & SonsMarine services and the provision of the engineering services to the nuclear industry. 306 74 380 18.6 28%

Babcock InternationalSupport services Group operating in regulated indutries including defence and energy 1297 74 1371 16.0 31%

Renew HoldingsSpecialist construction, nuclear engineering and land remediation 68 -9 59 11.5 18%

VT Group Defence and support services company 806 93 899 8.1 15%

Average 15.6

24www.burgisbullock.com

Quoted company comparables

y = 50.523x + 2.5518R² = 0.8986

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

0% 10% 20% 30% 40% 50% 60%

EV

/EB

IT

EBIT CAGR

Case study 2

Implied valuation of £18m

Negotiations with trade buyer terminated

MBO at £16m completed

25www.burgisbullock.com

Precedent transactions

Key method used in commercial transactions including fund raisings and MBOs

Determining the earnings / profit figure

Population of comparable deals

Assessing the final valuation figure or range

26www.burgisbullock.com

Precedent transactions

Reported profit – EBITDA, EBITA, EBIT, PBT etc?

Historical, current or prospective – ensure consistency

Maintainable/normalised profits:

Exceptional items

Shareholder remuneration

Non-business costs

27www.burgisbullock.com

Precedent transactions

Large and general population of comparables

Small and focused comparator group

Accessing the deal information

Reported v true deal statistics – using databases

Earn-outs, deferred consideration and partial exits

28www.burgisbullock.com

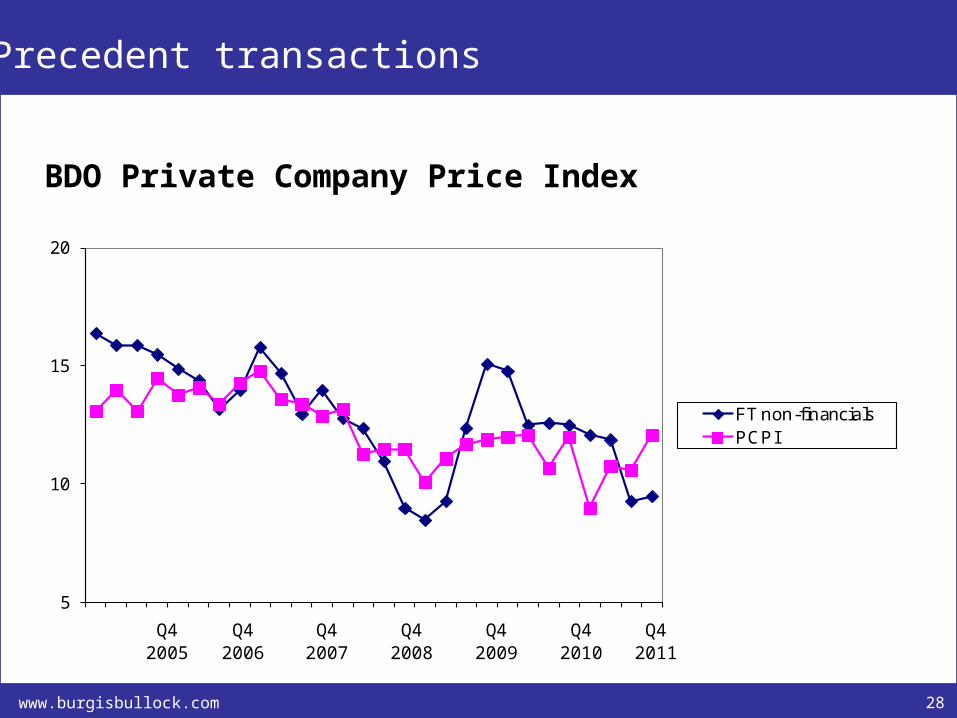

Precedent transactions

BDO Private Company Price Index

5

10

15

20

Q1 2005

Q4 2005

Q3 2006

Q2 2007

Q1 2008

Q4 2008

Q3 2009

Q2 2010

Q1 2011

Q4 2011

FT non-financialsPCPI

Q4 Q4 Q4 Q4 Q4 Q4 Q42005 2006 2007 2008 2009 2010 2011

29www.burgisbullock.com

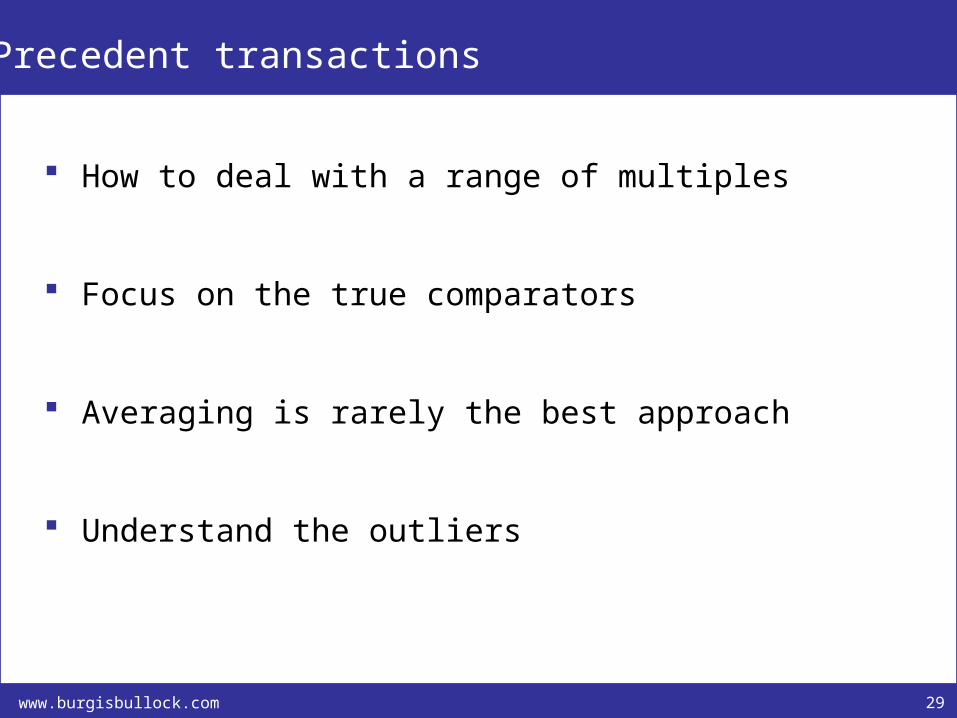

Precedent transactions

How to deal with a range of multiples

Focus on the true comparators

Averaging is rarely the best approach

Understand the outliers

30www.burgisbullock.com

Risk/reward models

Is it a valuation method?

Variant of a DCF model

Based on target investor returns

Reliant on company forecasts – subjectivity areas

Capital gain drives the return – impact of assumed exit multiples

31www.burgisbullock.com

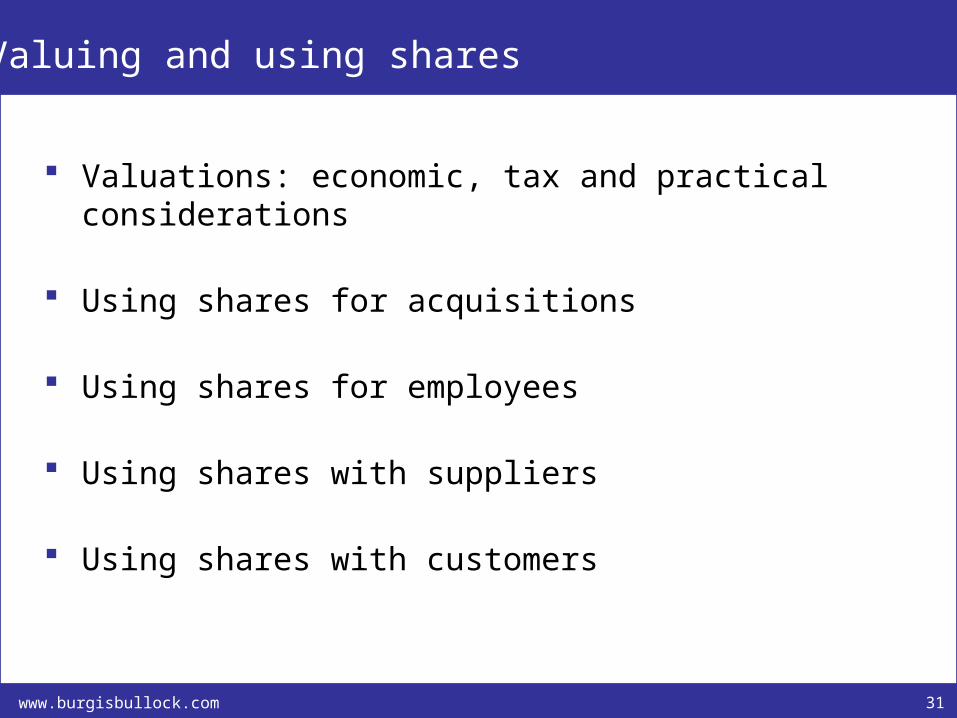

Valuing and using shares

Valuations: economic, tax and practical considerations

Using shares for acquisitions

Using shares for employees

Using shares with suppliers

Using shares with customers

32www.burgisbullock.com

Valuing your shares

Market value

Minority discounts

Restricted shares

Will the recipients attach the same value as you to shares?

Practical issues

33www.burgisbullock.com

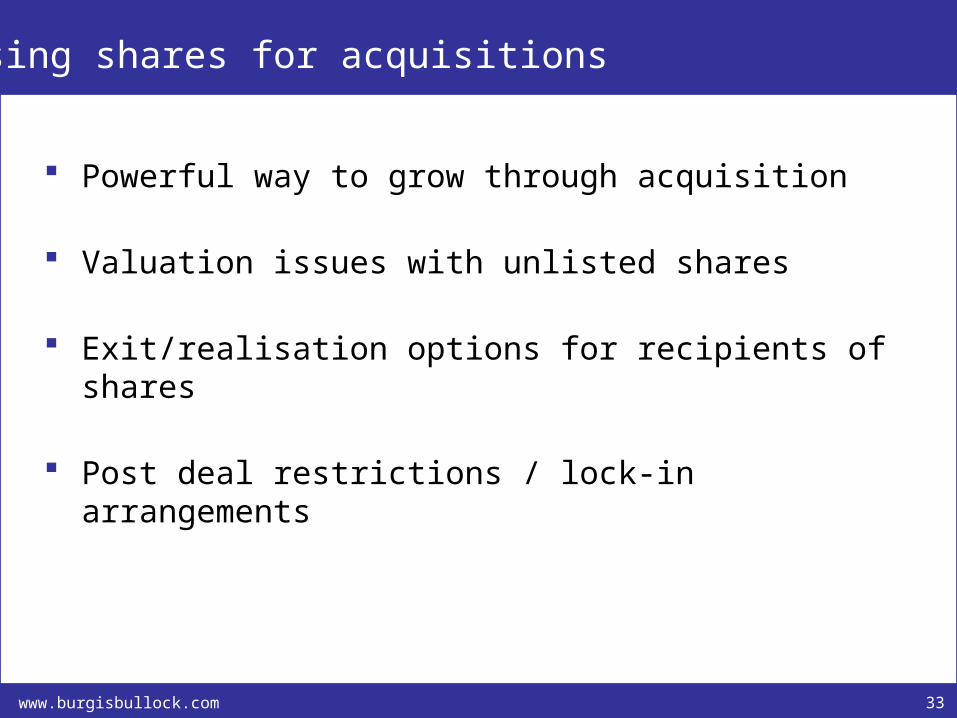

Using shares for acquisitions

Powerful way to grow through acquisition

Valuation issues with unlisted shares

Exit/realisation options for recipients of shares

Post deal restrictions / lock-in arrangements

34www.burgisbullock.com

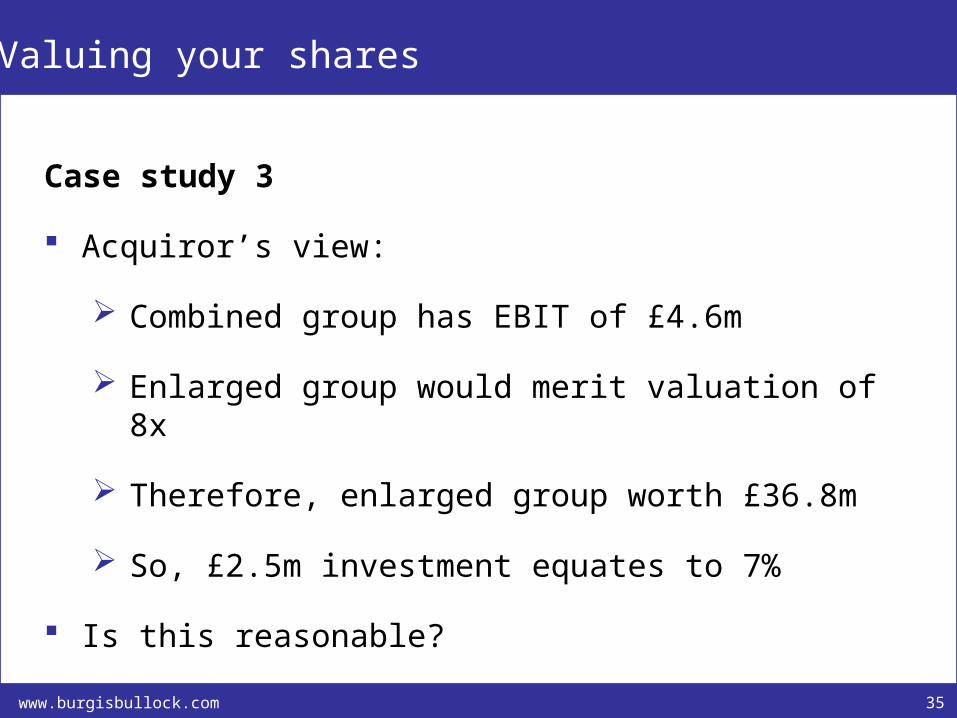

Valuing your shares

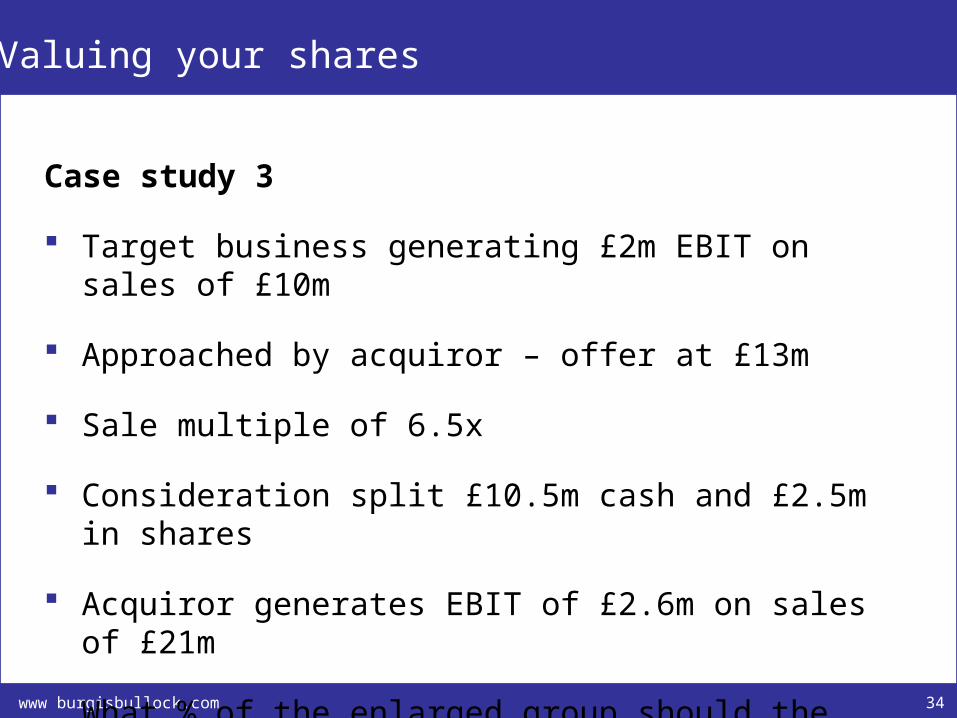

Case study 3

Target business generating £2m EBIT on sales of £10m

Approached by acquiror – offer at £13m

Sale multiple of 6.5x

Consideration split £10.5m cash and £2.5m in shares

Acquiror generates EBIT of £2.6m on sales of £21m

What % of the enlarged group should the vendor shareholders have?

35www.burgisbullock.com

Valuing your shares

Case study 3

Acquiror’s view:

Combined group has EBIT of £4.6m

Enlarged group would merit valuation of 8x

Therefore, enlarged group worth £36.8m

So, £2.5m investment equates to 7%

Is this reasonable?

36www.burgisbullock.com

Valuing your shares

Case study 3

Seller’s view:

Acquiror should be rated at 6.5x – the same as target

Therefore, acquiror worth £16.9m pre deal

Post deal value of £19.4m

So, share investment of £2.5m equates to 13%

What happened?

37www.burgisbullock.com

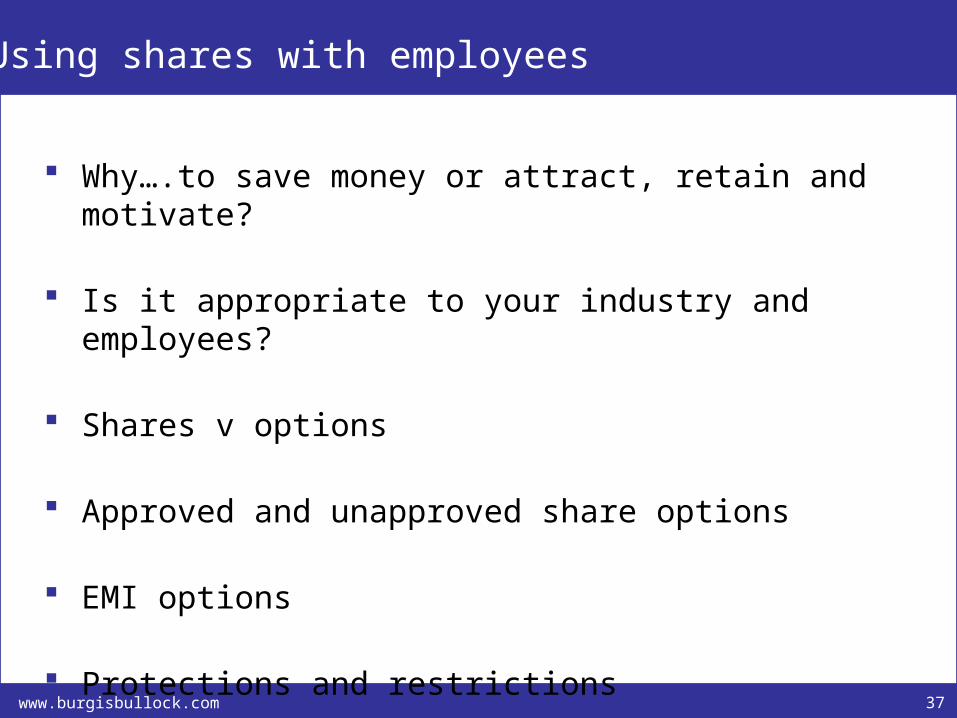

Using shares with employees

Why….to save money or attract, retain and motivate?

Is it appropriate to your industry and employees?

Shares v options

Approved and unapproved share options

EMI options

Protections and restrictions

38www.burgisbullock.com

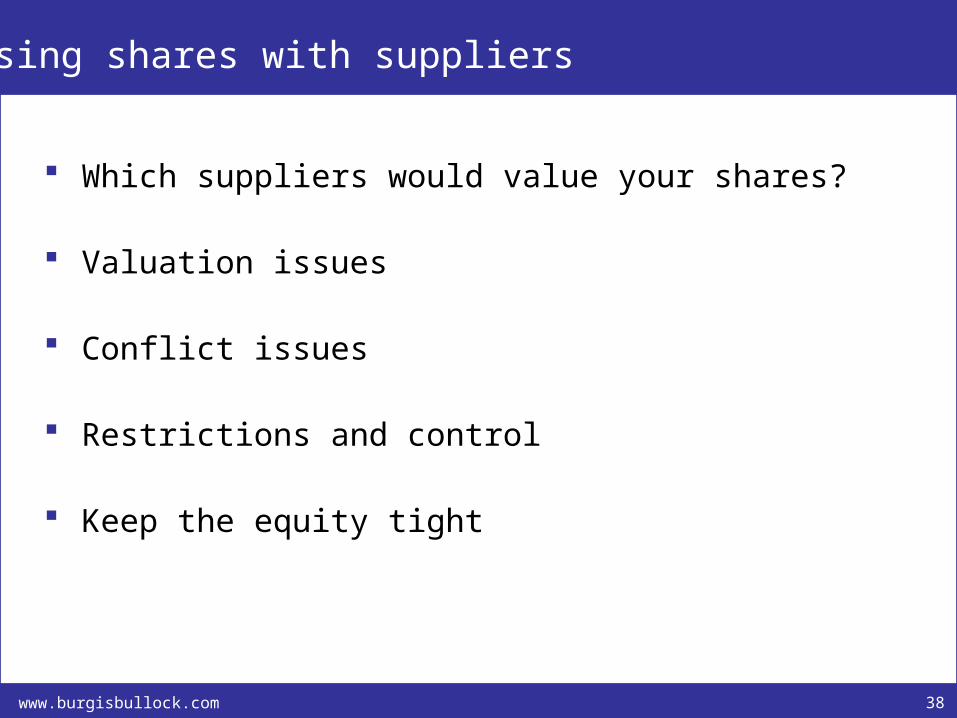

Using shares with suppliers

Which suppliers would value your shares?

Valuation issues

Conflict issues

Restrictions and control

Keep the equity tight

39www.burgisbullock.com

Using shares with customers

Recruitment and loyalty tool

Will your customers value them?

Shared equity schemes

Case study 4: Unichem

Regulatory issues

40www.burgisbullock.com

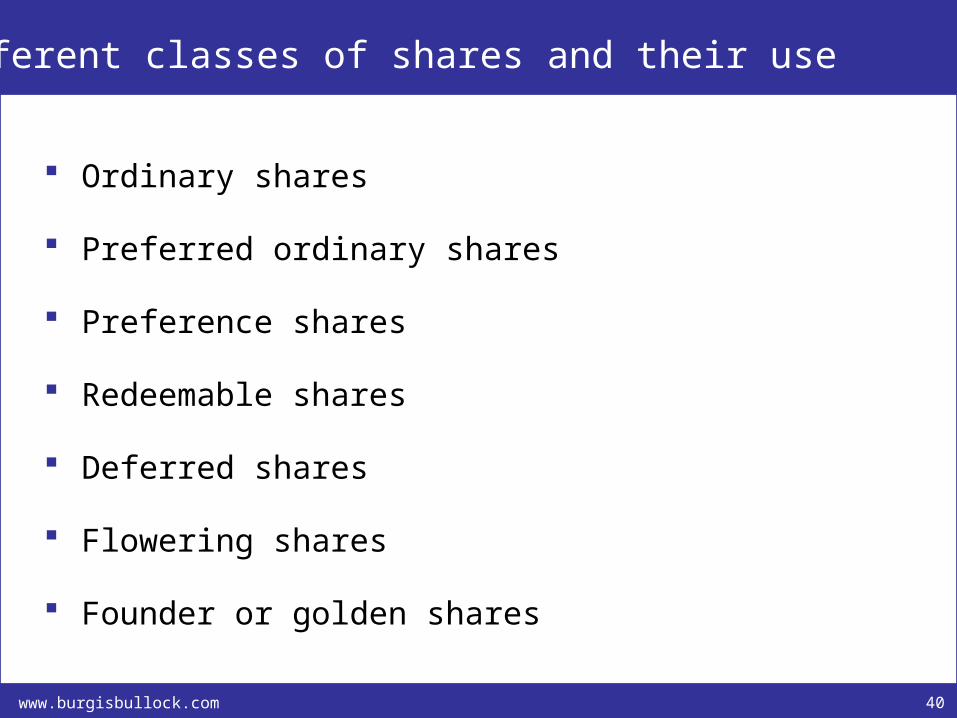

Different classes of shares and their use

Ordinary shares

Preferred ordinary shares

Preference shares

Redeemable shares

Deferred shares

Flowering shares

Founder or golden shares

41www.burgisbullock.com

Conclusion

Triangulate your valuations using several methods

Thorough analysis of inconsistent benchmarks

Beware of simplistic methodologies

Don’t rely on mathematical models – use judgement and knowledge of key value drivers

Equity is your most valuable asset