simplified cost options in european cohesion policy, yesterday and tomorrow louis vervloet, general...

TRANSCRIPT

Simplified Cost Options in European Cohesion policy, yesterday and tomorrow

Louis Vervloet, General director, ESF Agency Flanders

2

Purpose of the presentation

•Present the origin of “simplified cost options” (SCO’s) and their main features

•Present the SCO’s included in the Cohesion Regulations for 2014-2020

Name of your presentation

3Name of your presentation

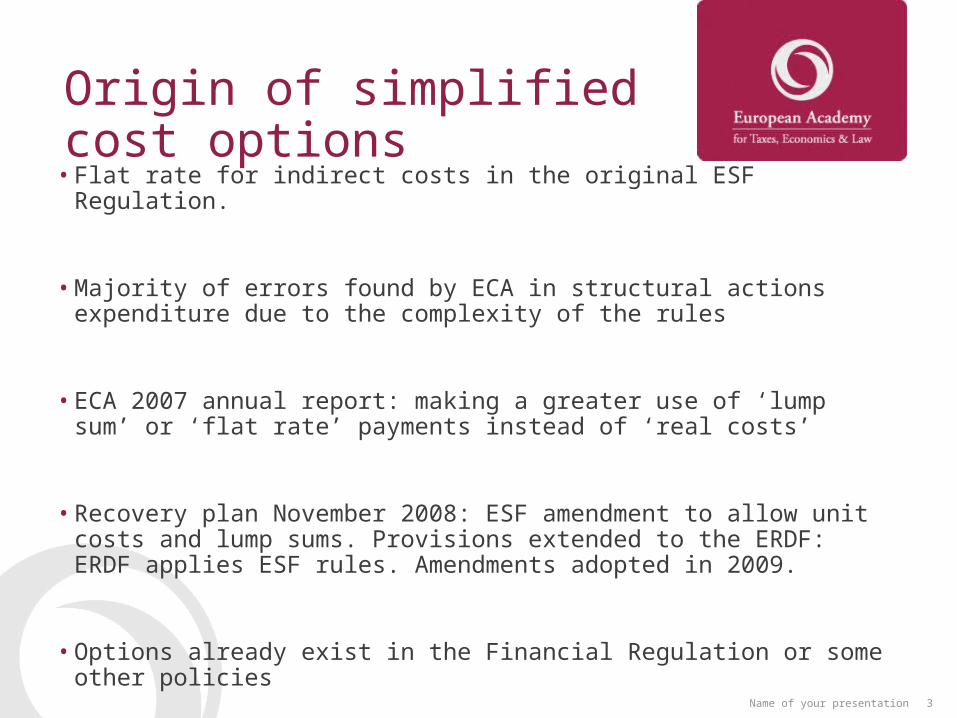

Origin of simplified cost options

• Flat rate for indirect costs in the original ESF Regulation.

• Majority of errors found by ECA in structural actions expenditure due to the complexity of the rules

• ECA 2007 annual report: making a greater use of ‘lump sum’ or ‘flat rate’ payments instead of ‘real costs’

• Recovery plan November 2008: ESF amendment to allow unit costs and lump sums. Provisions extended to the ERDF: ERDF applies ESF rules. Amendments adopted in 2009.

• Options already exist in the Financial Regulation or some other policies

4Name of your presentation

SCO’s in 2007-2013

1. Flat rate for indirect costs: indirect costs calculated as a % of direct costs (maximum 20%)

eligible cost = direct costs + (% of direct costs)

2. Standard scales of unit costs: reimbursement calculated on the basis of delivered quantities multiplied by a unit cost

- Ex: eligible cost = nb of trainees x cost by trainee

5Name of your presentation

SCO’s in 2007-2013

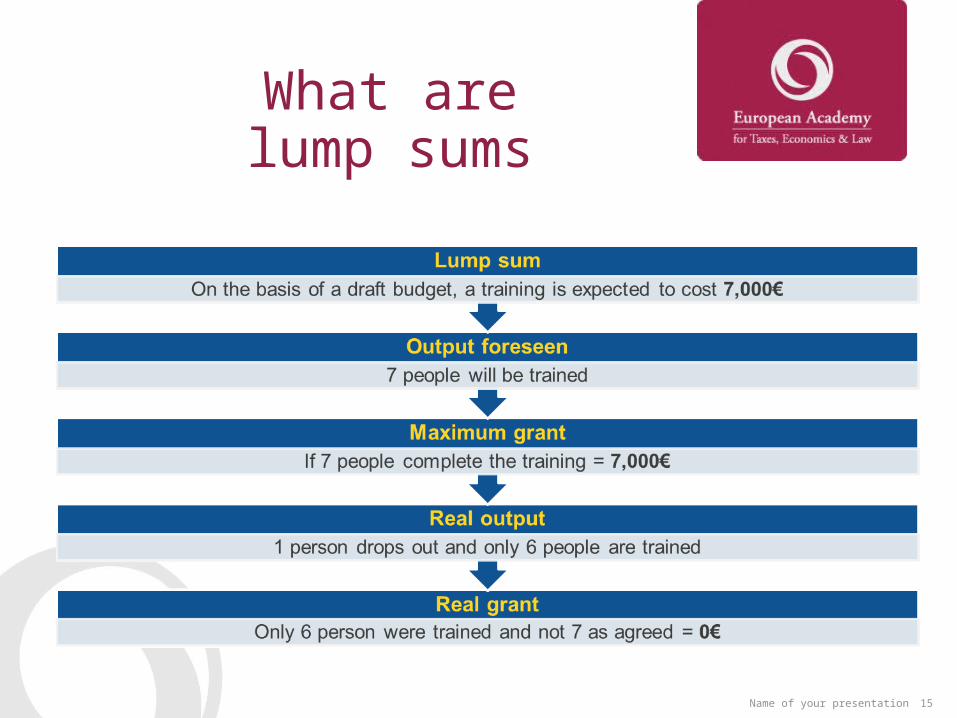

3. Lump sums (<50 kEUR): reimbursement when

pre-defined terms of agreement on activities and/or outputs are completed

- Eligible cost = lump sum amount (if completed) or 0.

6Name of your presentation

Key points of SCO’s in 2007-2013• Optional

• ESF and ERDF only

• Only for grants (no operations or projects subject to public procurement contracts)

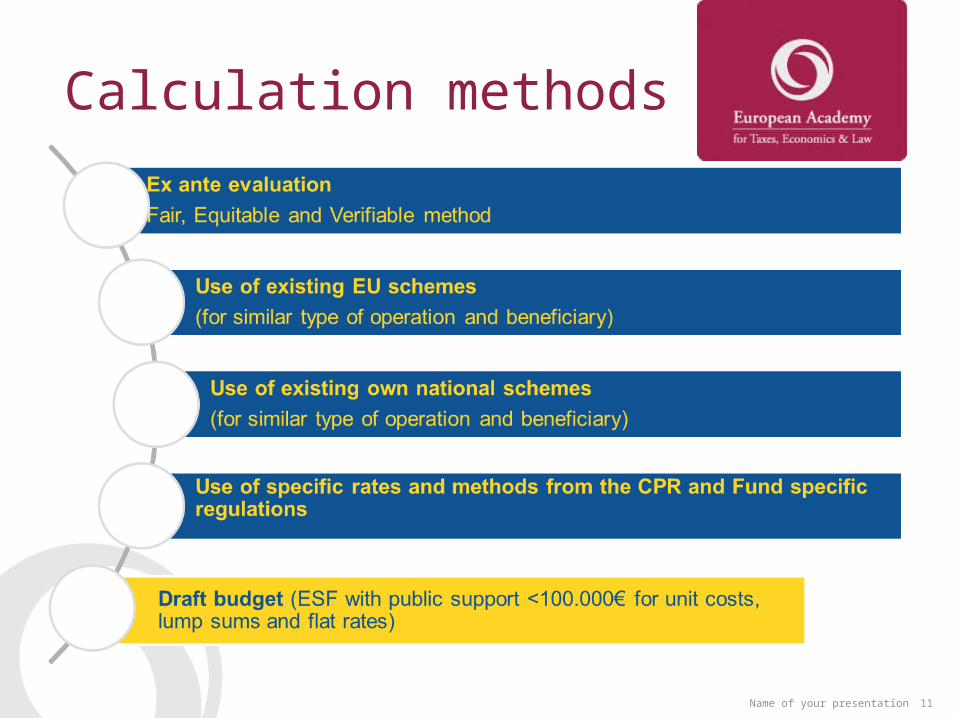

• SCOs shall be calculated ex ante on a fair, equitable and verifiable basis.

• Simplification! No audit of underlying financial documents. Amounts paid considered as paid expenditure if justified by direct costs (flat rate) or “quantities” (standard scales and lump sums)

7Name of your presentation

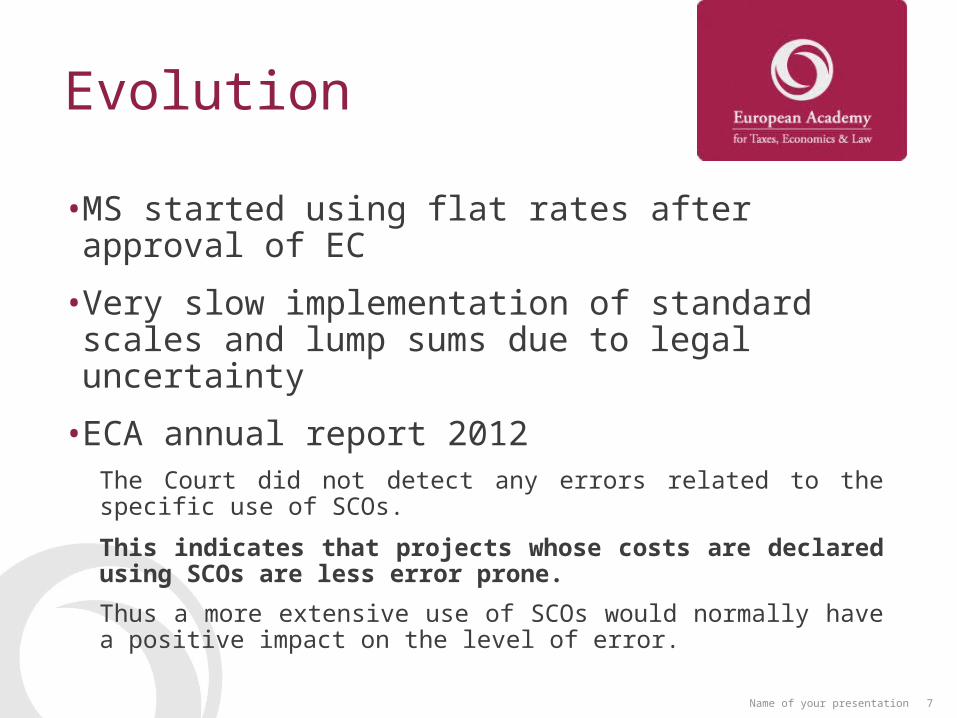

Evolution

• MS started using flat rates after approval of EC

• Very slow implementation of standard scales and lump sums due to legal uncertainty

• ECA annual report 2012The Court did not detect any errors related to the specific use of SCOs.

This indicates that projects whose costs are declared using SCOs are less error prone.

Thus a more extensive use of SCOs would normally have a positive impact on the level of error.

8Name of your presentation

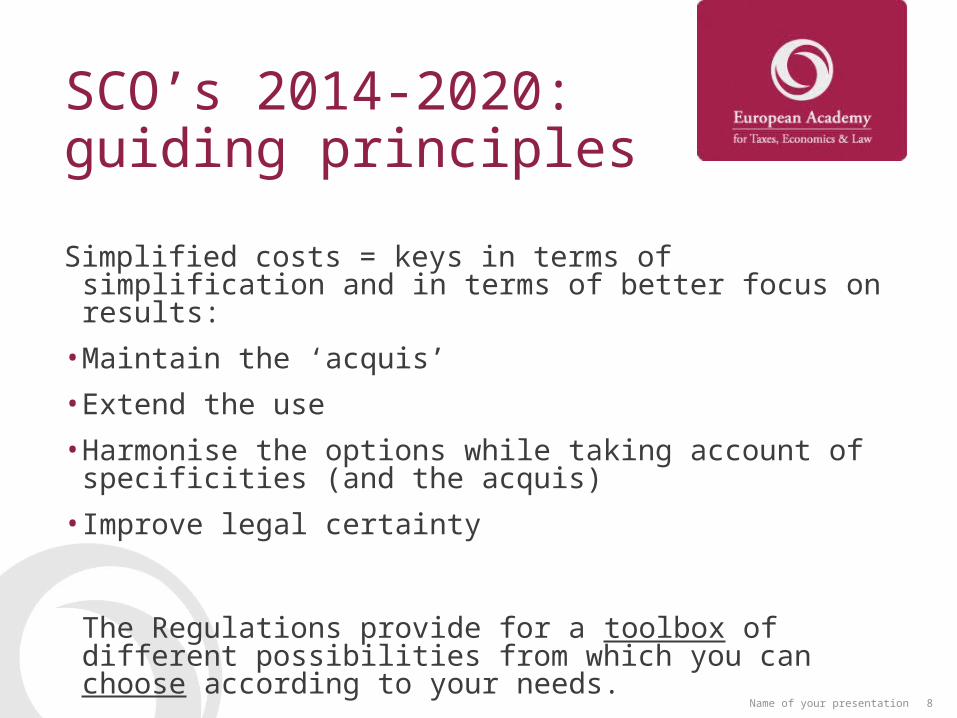

SCO’s 2014-2020: guiding principles

Simplified costs = keys in terms of simplification and in terms of better focus on results:

• Maintain the ‘acquis’

• Extend the use

• Harmonise the options while taking account of specificities (and the acquis)

• Improve legal certainty

The Regulations provide for a toolbox of different possibilities from which you can choose according to your needs.

9Name of your presentation

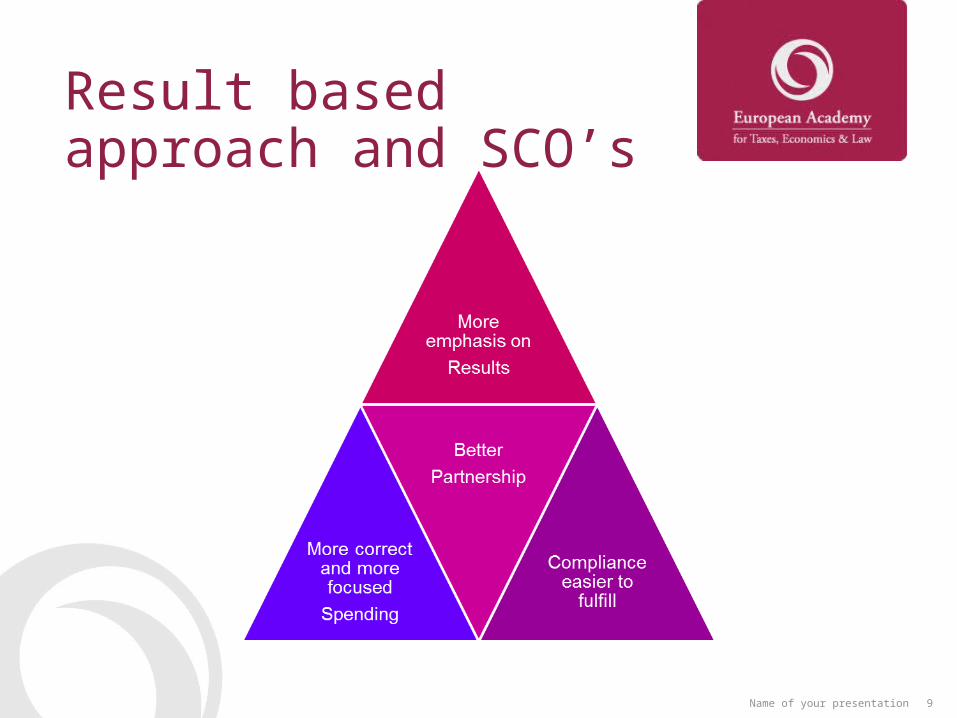

Result based approach and SCO’s

10Name of your presentation

SCO’s in 2014-2020 regulation

11Name of your presentation

Calculation methods

12Name of your presentation

What are standard scales of unit costs

13Name of your presentation

How to calculate standard scales of unit costs (1)

• STEP 1

–Define clearly the nature of the requested projects/operations in the call

= the cost drivers of your call for projects

• STEP 2Check the historical data (real costs) on similar

projects/operations

Look for possible benchmarks

PES, education system, other experiences

14Name of your presentation

How to calculate standard scales of unit costs (2)

• STEP 3

–Calculate the averages and define

• STEP 4

–Check and discuss with colleagues in MA-CA-AA

• STEP 5

–Decide Communicate and Implement

IMPORTANT : stay constructive – critical and be your own “devils advocate”

15Name of your presentation

What arelump sums

16Name of your presentation

How to calculate lump sums (1)

• STEP 1 - define the nature of the project/operation and the result wanted

the result is your cost driver• STEP 2 - define a detailed list of items/actions

that appear in a reasonable budget• STEP 3 - Check historical data or look for

benchmarks in public and private sector for the whole and for each item if possible

17Name of your presentation

How to calculate lump sums (2)

• STEP 3

–Calculate the averages and define

• STEP 4

–Check and discuss with colleagues in MA-CA-AA

• STEP 5

–Decide Communicate and Implement

IMPORTANT : stay constructive – critical and be your own “devils advocate”

18Name of your presentation

Limits of lump sums

•Only for projects with a max of 100.000 EUR public contribution

•Never use lump sums if you cannot define your result as a realistic and achievable

single unit

19Name of your presentation

What are flat rates

20Name of your presentation

How to calculateflat rates for indirect costs

21Name of your presentation

How to calculateflat rates for indirect costs

22Name of your presentation

How to calculatehourly staff costs (art 68,2 CPR)

23Name of your presentation

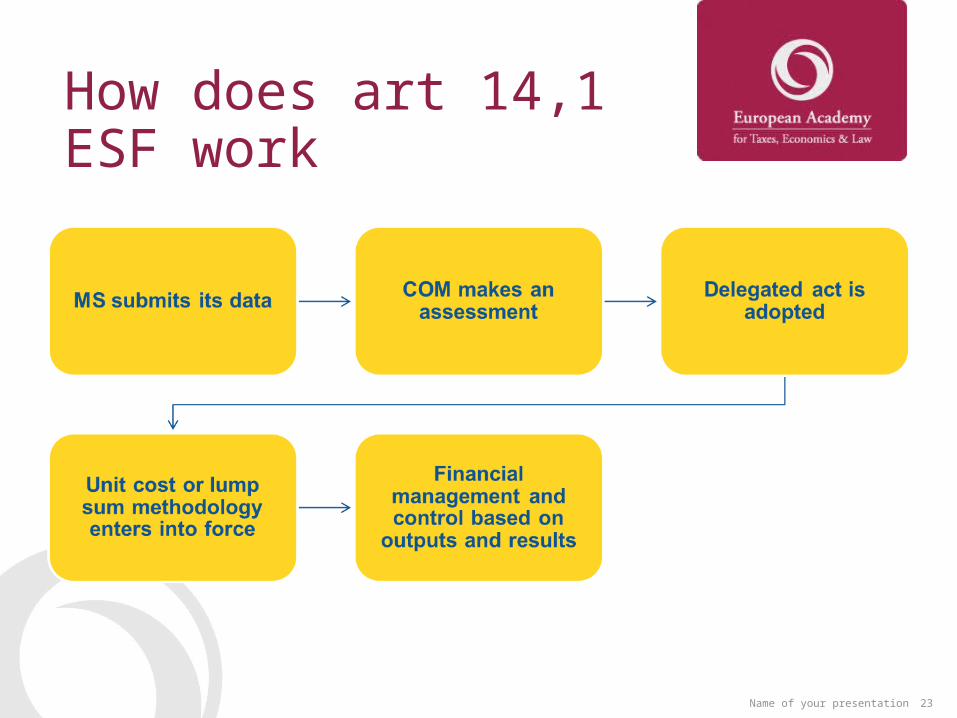

How does art 14,1 ESF work

24

Project

MA/CA

agreed UC/LS1 people = 100€

Eligible expenditure

10 people justified x 100€ = 1000€

Project = outcome

10 people

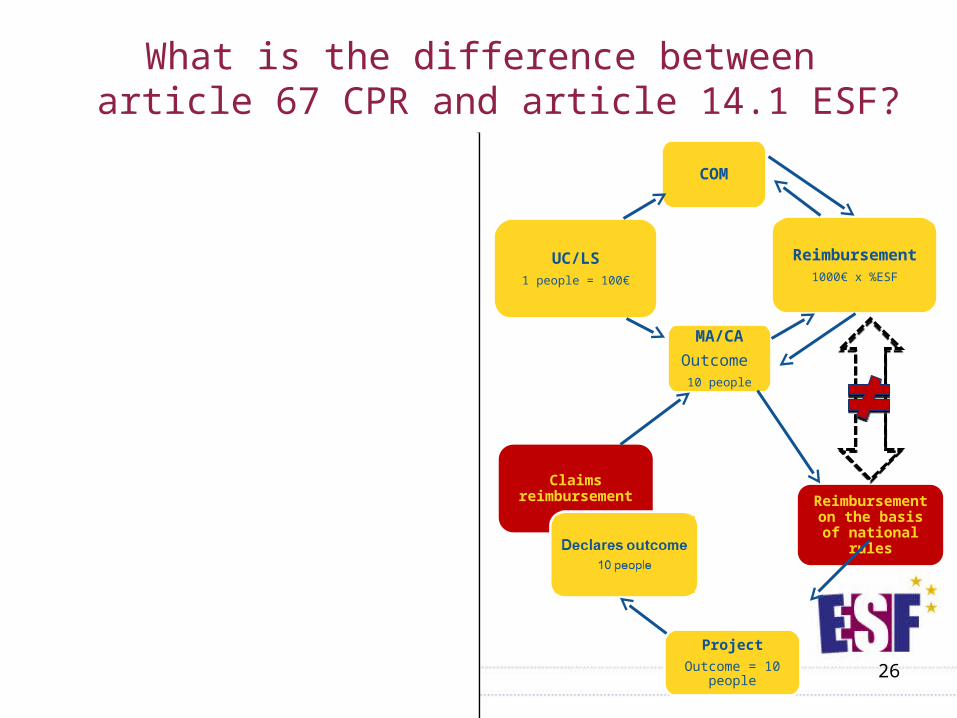

What is the difference between article 67 CPR and article 14.1 ESF?

Claims reimbursement

10 x 100€ = 1000€

Reimbursement1000€ x %ESF

25Project

MA/CA

agreed UC/LS1 people = 100€

Eligible expenditure

10 people justified x 100€ = 1000€

Project = outcome

10 people

MA/CA

COM

UC/LS1 people = 100€

MA/CA

Outcome 10 people

What is the difference between article 67 CPR and article 14.1 ESF?

26

What is the difference between article 67 CPR and article 14.1 ESF?

Project

MA/CA

agreed UC/LS1 people = 100€

Eligible expenditure

10 people justified x 100€ = 1000€

Project = outcome

10 people

MA/CA

COM

UC/LS1 people = 100€

Reimbursement1000€ x %ESF

MA/CA

Outcome 10 people

Claims reimbursement

1000€

COM

Reimbursement 1000€ x %ESF

Project

Outcome = 10 people

Claims reimbursement

Reimbursement on the basis of national rules

27Name of your presentation

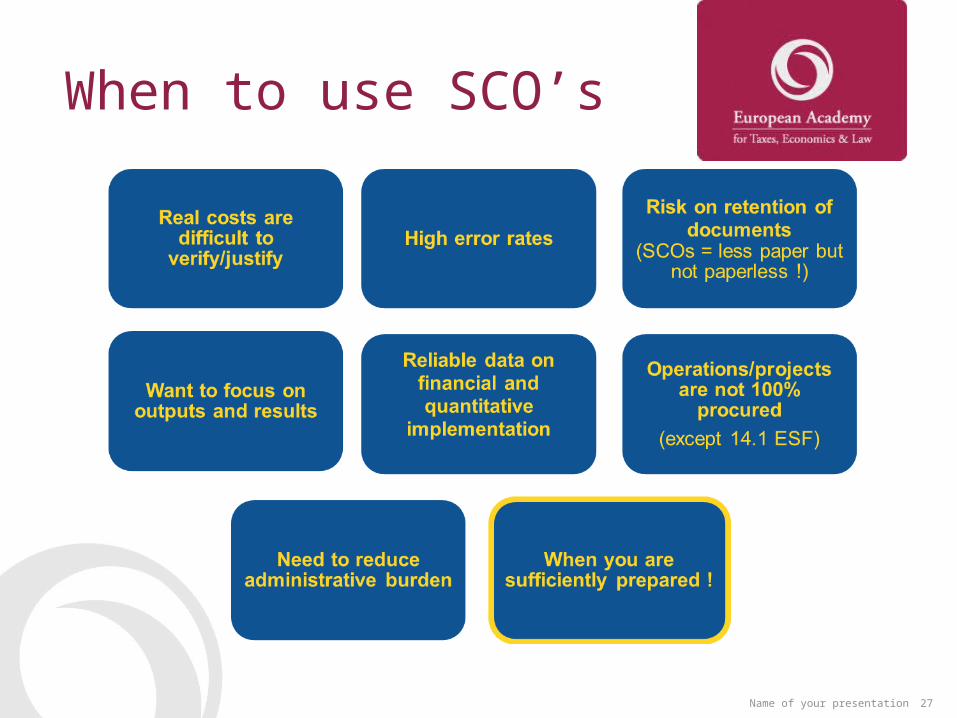

When to use SCO’s

28Name of your presentation

Flat-rate financing (1)General (Art 67,1 d): examples

• Reminder: Never compare rates directly! Compare also the categories of costs calculated with the rate, and the categories of costs to which the rate is applied.

29Name of your presentation

Flat rate financing (2)calculate indirect costs (Art 68 CPR)

• * ESF, for grants < EUR 100.000

30Name of your presentation

Comparison current / future

- flat rate to calculate indirect costs -> flat rate to calculate any type of costs

- increase of lump sum threshold

- more calculation methods

- lump sums / unit costs compulsory for small ESF grants

• But everything that is used now is usable in the future!

31Name of your presentation

Key points for implementation (1)

• Consider, consult and involve all stakeholders in the development and implementation of SCO’s

• Keep It Simple and Clear

• Timely and transparent communication prevent frustrations and misunderstanding

•

32Name of your presentation

Key points for implementation (2)

• Change the mindset:

• First SCO’s – only if proven impossible – real costs are allowed

• SCO’s are averages, some will gain but some will lose

• Simplification is key for better results

33Name of your presentation

Key points for implementation (3)

• Always keep in mind the simplification purpose.

• Compare the options and decide before the start of the programme!

• type of operations,

• data availability,

• legal certainty or flexibility,

• Define where your national rules block you

34Name of your presentation

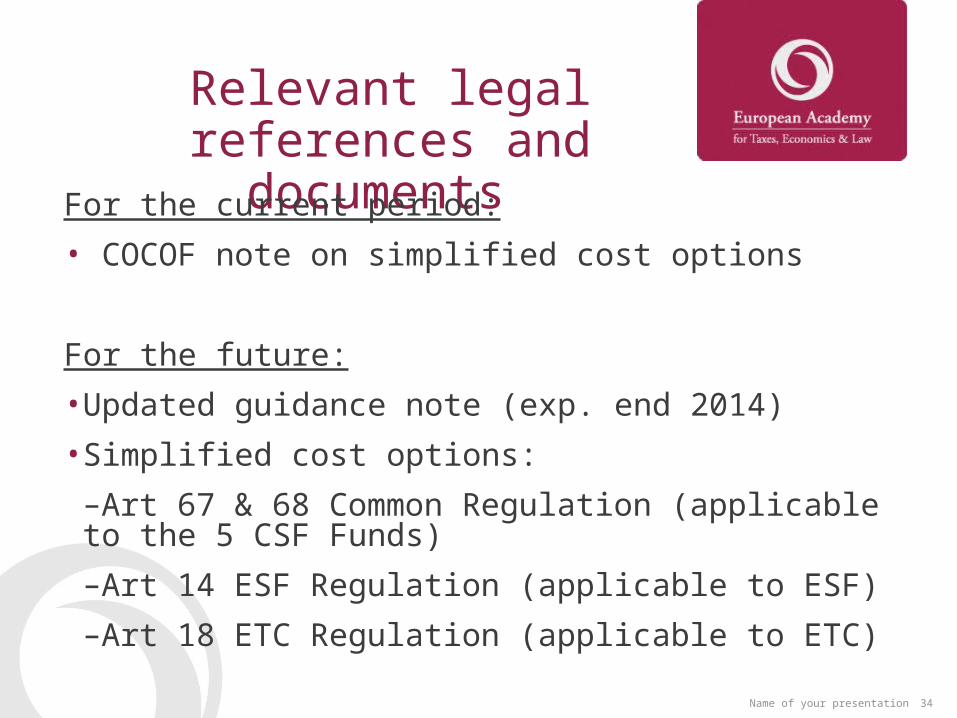

Relevant legal references and documents

For the current period:

• COCOF note on simplified cost options

For the future:

•Updated guidance note (exp. end 2014)

•Simplified cost options:

–Art 67 & 68 Common Regulation (applicable to the 5 CSF Funds)

–Art 14 ESF Regulation (applicable to ESF)

–Art 18 ETC Regulation (applicable to ETC)

35

References

Louis Vervloet

General director

ESF-Agency Flanders

Gasthuisstraat 35 5th floor

1000 BRUSSELS

[email protected] of your presentation

36Name of your presentation

Subheadline

• Content

26

What is the difference between article 67 CPR and article 14.1 ESF?

Project

MA/CA

agreed UC/LS1 people = 100€

Eligible expenditure

10 people justified x 100€ = 1000€

Project = outcome

10 people

MA/CA

COM

UC/LS1 people = 100€

Reimbursement1000€ x %ESF

MA/CA

Outcome 10 people

Claims reimbursement

1000€

COM

Reimbursement 1000€ x %ESF

Project

Outcome = 10 people

Claims reimbursement

Reimbursement on the basis of national rules

38Name of your presentation

Subheadline

• Content