sin tax reform in the philippines - imf tax reform in the philippines juvy c. danofrata ... for...

TRANSCRIPT

SIN TAX REFORM IN THE PHILIPPINES

JUVY C. DANOFRATADirector, Department of Finance

Republic of the Philippines

Outline I. Reasons for reform

B k d I f ia. Background Information –tobacco use in the country

b. Weaknesses of the old structureII Impact of the ReformII. Impact of the Reform III. Key elements for a successful ylegislative reform

lIV. Conclusion

BACKGROUND INFORMATION1. Cigarette prices in the Philippines are among the

lowest in the ASEAN region, while tax rates are among the lowest in the world

2. The Philippines is among the top smoking countries in Southeast Asia, with the poorest being the largest consumer.

3. “Strongest tobacco lobby in Asia”;4. Economic cost of of the top four non-communicable

di l d ki i i d U$3disease related to smoking is estimated at U$3 to U$6 billion (Sta. Ana and Latuja, 2011)

Weaknesses of the old structureCharacteristics RA No. 9334 RA No. 10351Characteristics RA No. 9334 RA No. 10351

Price/brand classification freeze

For purposes of ascertaining the tax rate, the law pegged the classification of brands based on their net retail price. This kept the

i l ifi i f ld i b d

Removal of tax advantages of legacy brands. The tax classification of sin products will b d i dprice classification of old cigarette brands

fixed based on the brands’ net retail price as of October 1996.

be determined every two years.

M lti ti d t S ifi t t ith h b d b i Shift d t t ti d tMulti-tiered tax system

Specific tax rates with cheaper brands being taxed less than the more expensive brands.

Shifted to a two-tiered tax structure based on the brands’prices until year 2017 when the law provides for a uniform tax.

Lack of price indexation

Inadequate adjustment of specific tax rates to inflation even with the yearly increases which ended in 2011.

Prescribed annual increases in cigarette prices from 2013 to 2018 and an annual increase of excise tax rates by 4% effective January 1, 2018.

Non-compliant with WTO rules (distilled spirits)

Differential tax treatment between old brands and new/imported brands resulted to WTO findings of discrimination against

Removal of the classification.

spirits) to WTO findings of discrimination against imported spirits in violation of the GATT.

Source: Health Justice Philippines (Sta. Ana and Latuja, 2011; Philippine legislations

Philippine Tobacco Tax Reform Path at a GlanceIn Philippine Peso

25.00

30.00

35.00Premium Tier 1 Unitary

10.00

15.00

20.00

Medium

High

Tier 2

0.00

5.00

10.00

2012 2013 2014 2015 2016 2017

Low 341%

2012 2013 2014 2015 2016 2017

Key Features Removal of price classification freeze/tax

advantages of legacy brands.

2013 2014 2015 2016 2017

Projected Incremental Revenue (Tobacco) 23.4 29.6 33.5 37.1 40.9g g y

Unitary tax structure by 2017. Tax rates indexed to inflation starting 2017. Bulk of incremental revenues earmarked

for UHC

Revenue (Tobacco)

Projected Incremental Revenue (Alcohol) 10.6 13.3 17.1 19.8 23.3

P j t d I t lfor UHC. Safety nets for tobacco farmers/others.

Projected Incremental Revenue (Total) 34.0 42.9 50.6 56.9 64.2

Estimated Earmark for Health 30.5 38.4 45.6 51.3 58.0

Prior to reform, excise tax collection were almost stagnantFISCAL IMPACT OF THE REFORM, g

Cigarettes

Weighted Effective Tax Rates for Cigarettes

20.0

25.0

15.0Before Sin Tax Reform

5 0

10.0AfterSin Tax Reform

0.0

5.0

Cigarettes

There is a significant spike in the share of tobacco and alcohol i ll i G i h fexcise collections to GDP since the reform.

b & l h l i ll i

1.1%1.1%

1.2%

Tobacco & Alcohol Excise Collection

0.9%

0.8% 0.8% 0.8% 0.8%

0.9% 0.9%

0.8%

0.9%

1.0%

0.7% 0.7% 0.7%

0.6% 0.6% 0.6% 0.6%

0.5% 0.5%0.6%

0.7%

0.4%

0.5%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: BIR and NSCB

Tobacco & Alcohol Excise Collection

Share of tobacco excise tax collections to GDP

0.8%0.8%

Tobacco Excise Tax Collection

0.6% 0.6%0.6%

0.7%

0.5%0.5% 0.5%

0.5%0.4% 0.5%

0.4% 0.4%

0.3% 0.4% 0.4%0.4%

0.5%

0.3%0.3%

0.3%

0.2%

0.3%

1999 2000 2001 2002 2003 2004 200 2006 200 2008 2009 2010 2011 2012 2013 2014 2011999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Tobacco Excise Tax Collection

Source: BIR and NSCB

Actual revenues continue to exceed targetProjected vs. Actual Incremental Revenue from RA 10351

(In Billion Pesos)Projected Annual

64.2

73.1Projected Annual

42.9

50.6

56.951.2 50.2

$ 1.61 B

$ 1 29 B

$ 1.46 B

34.0

$ 0.80 B $ 0.97 B

$ 1.21 B$ 1.13 B

$ 1.11 B$ 1.29 B

2013 2014 2015 2016 2017

From 2013 to 2015, the average actual excess in collection i P15 66 billi f 0 46% f GDPis P15.66 billion pesos or an average of 0.46% of GDP.

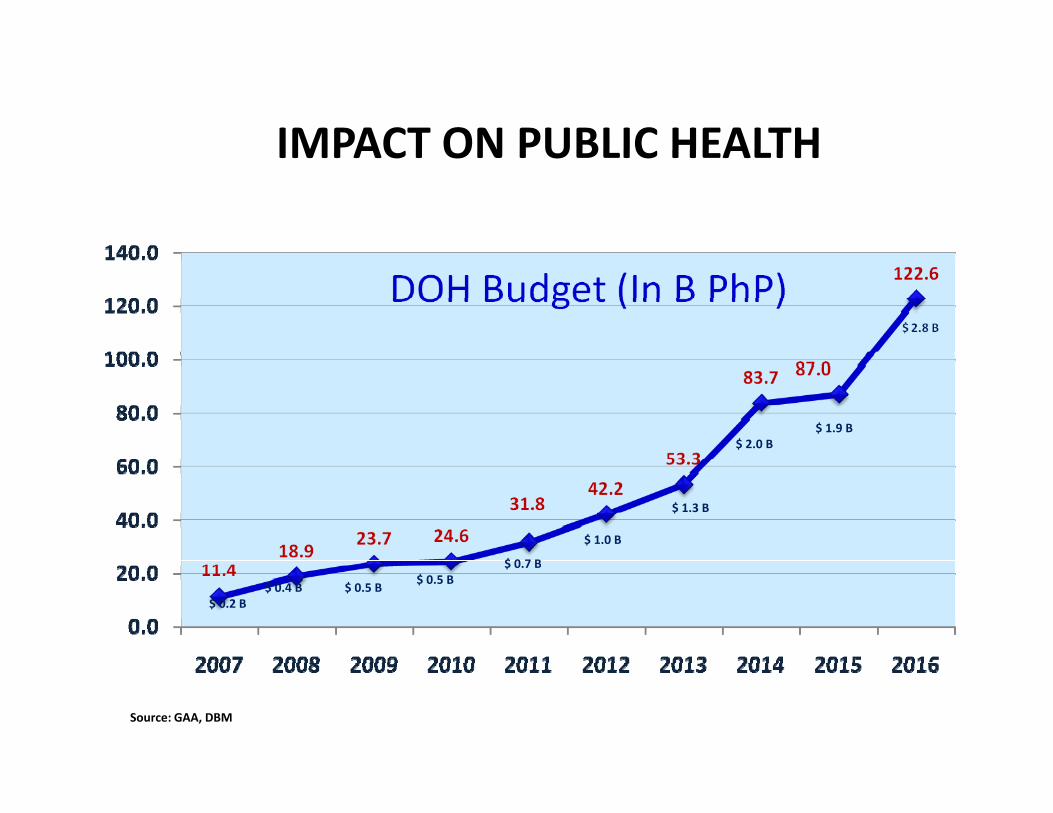

IMPACT ON PUBLIC HEALTHIMPACT ON PUBLIC HEALTH

$ 1.9 B $ 2.0 B

$ 1.3 B

$ 1.0 B

$ 0 7 B$ 0.7 B$ 0.5 B$ 0.5 B$ 0.4 B

$ 0.2 B

Source: GAA, DBM

National Government Allocation for

50.0

Health Insurance Premiums for the Poor.924 US$

(Billion)

35.237.1

43.9

35 0

40.0

45.0

50.0(Billion) Pesos

.793

.815

25.0

30.0

35.0

5 0 5 0

12.512.6

10.0

15.0

20.0

057 076 .101 .105 .111 .081

.297.296

0.5 0.5 0.5 0.5 0.82.9 3.5 4.5 5.0 5.0 3.5

0.0

5.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

.009.010 .010 .009 .015.057 .076

Source: PhilHealth, DOH, GAA

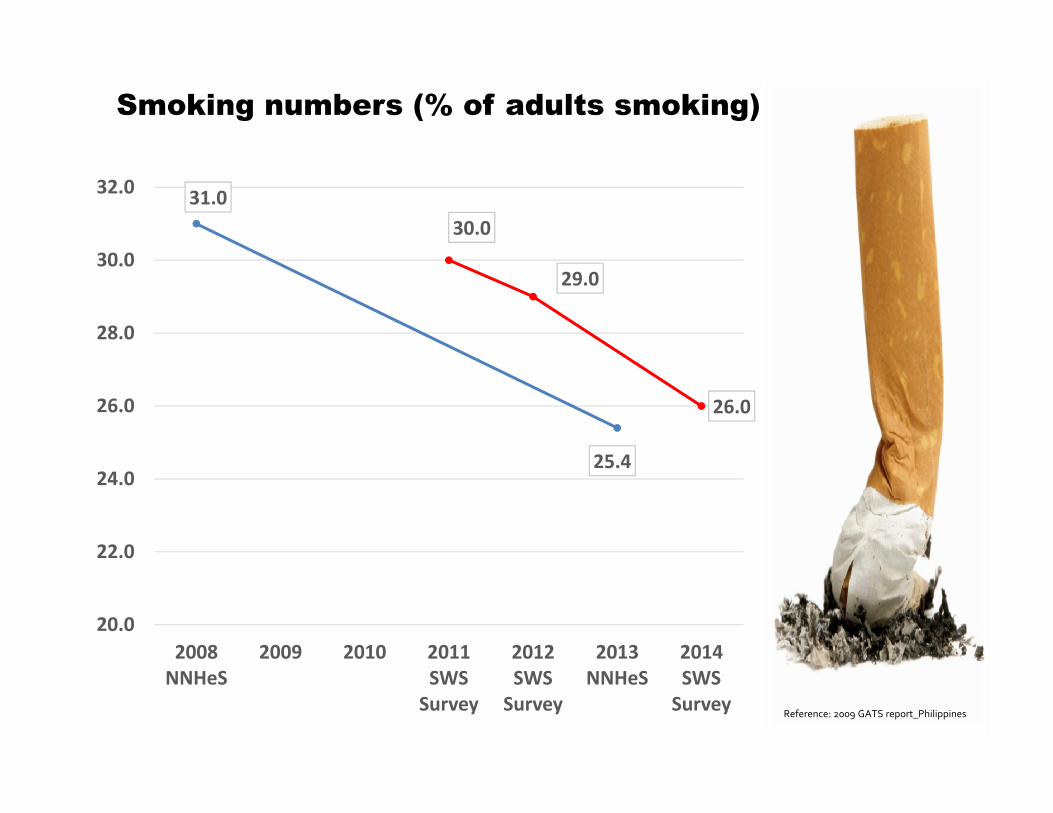

Smoking numbers (% of adults smoking)

31.030.0

30 0

32.0

29.0

28.0

30.0

25 4

26.026.0

25.4

22.0

24.0

20.02008 2009 2010 2011 2012 2013 2014

Reference: 2009 GATS report_Philippines

NNHeS SWS Survey

SWS Survey

NNHeS SWS Survey

Key elements for a successful legislative reform

Framing the advocacy focus on Framing the advocacy – focus on health Political support at the highest levels C t ti t ith Constructive engagement with

stakeholdersstakeholders Analytical support Strategic communications

CONCLUSION Philippine Sin Tax Reform generated US$2.3 billion

additional revenues in its first two years ofadditional revenues in its first two years of implementation. About 80% of this increase is accounted for by tobacco taxes.

While the country reap significant benefits from the reform, several facts remain to be addressed, such as cigarette prices in the country that remain to becigarette prices in the country that remain to be cheapest in ASEAN, next to Cambodia, that may counter the health objective of the law.

This situation coupled with increases in the consumer’s income can be a trigger towards another round of reform that can ultimately bring in not just additionalreform that can ultimately bring in not just additional fiscal space but greater health benefits.

THANK YOUTHANK YOU