singapore property weekly issue 176

DESCRIPTION

In this issue:- Why I’ve Not Lost Money in 13 Years –Understanding the Time Value of Money and IRR- Singapore Property News This Week- Resale Property Transactions (September 17 – September 23)TRANSCRIPT

ContributeDo you have articles and insights and articles that you’d like to share with thousands of readers interested in the Singapore property market? Send them to us at [email protected], and if they’re good enough, we’ll publish them here, on our blog and even on Yahoo! News.

AdvertiseWant to get your brand, product, service or property listing out to thousands of Singapore property investors at a very reasonable cost? Head over to www.propwise.sg/advertise/ to find out more.

CONTENTS

p2 Why I’ve Not Lost Money in 13 Years –

Understanding the Time Value of

Money and IRR

p9 Singapore Property News This Week

p16 Resale Property Transactions

(September 17 – September 23 )

Welcome to the 176th edition of the Singapore Property Weekly.

Hope you like it!

Mr. Propwise

FROM THE

EDITOR

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 2Back to Contents

By Gerald Tay (guest contributor)

This post requires a basic understanding of

using a financial calculator. Explaining how to

use it is beyond the scope of this post as I

don‘t want to turn it into a bed-time lullaby if

you‘re one of those who has never touched a

financial (not scientific) calculator. It‘s

impossible to learn math by reading!

Rather, I‘ll try to explain in layman terms so

you can grasp the basics of what Internal

Rate of Return (IRR) and Time Value of

Money are, respectively, as well as why they

are essential for property investment.

Why I‘ve Not Lost Money in 13 Years –Understanding the

Time Value of Money and IRR

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 3Back to Contents

Tip: Cash flows are worth more today than

they are tomorrow.

One reason why I’ve not lost money in 13

years

The Internal Rate of Return (IRR) is arguably

the most holistic measure of an investment

property‘s return potential. That said, many

investors fail to utilize this key metric, or

underestimate its utility in measuring value.

But don‘t feel relatively uninformed if you

don‘t. I took courses in Financial Analysis and

Investment in the mid-2000s. The Time Value

of Money and Internal Rate of Return (IRR)

was one of the topics covered.

I flunked my Math!

I‘ve always been a B/C Math student in

school. I received a ‗C‘ grade for ‗Additional

Mathematics‘ for my ‗O‘ levels. At 17, I

dropped out of Engineering School because I

flunked each of my Engineering Math

subjects (I prefer to write and speak rather

than fix things up anyway).

My point is – you would have been a better

math student than me. You don‘t need to be a

Math genius to understand what I‘m going to

tell you. All you need is to understand basic

principles and how to input a few numbers

into a financial calculator - and voila!

Internal Rate of Return (IRR) is an extremely

powerful valuation metric for property

investment, and have been successfully

applying it for a while. But few of those who

use the Internal Rate of Return (IRR) in the

real estate industry know how to use it as a

powerful valuation tool. A property investor

can be a real estate professional but a real

estate professional may not be a real

investor.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 4Back to Contents

In this post I will address the following:

1. Internal Rate of Return (IRR)

2. Net Present Value (NPV)

3. Modified Internal Rate of Return (MIRR)

Internal Rate of Return (IRR)

The Internal Rate of Return is the interest

rate that brings the Net Present Value of all

future cash flow to zero.

Here‘s a hypothetical example:

For every $100 you lend to a friend, he‘ll

repay you $10 per year – forever and ever!

How much do you get every year in

percentage terms? $10 divided by$100

equals10%.

This 10% is called the Rate of Return.

But be careful; this is NOT yet the Internal

Rate of Return.

This 10% rate of return tells you how quickly

you get your money back in exactly 1 year –

compared to your original $100.

It was very easy to find the rate of return of

10%.

Now….

What if your friend pays you back a different

amount every year? In some years, he pays

$20, in other years he might pay only $5. And

in some years he doesn‘t pay! And what if it‘s

not forever? What if it‘s exactly 7 years?

The rate of return is now ‗hidden‘, and is

called the Internal Rate of Return (IRR)

In layman terms: The Internal Rate of Return

is a good way of judging an investment. The

bigger the better!

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 5Back to Contents

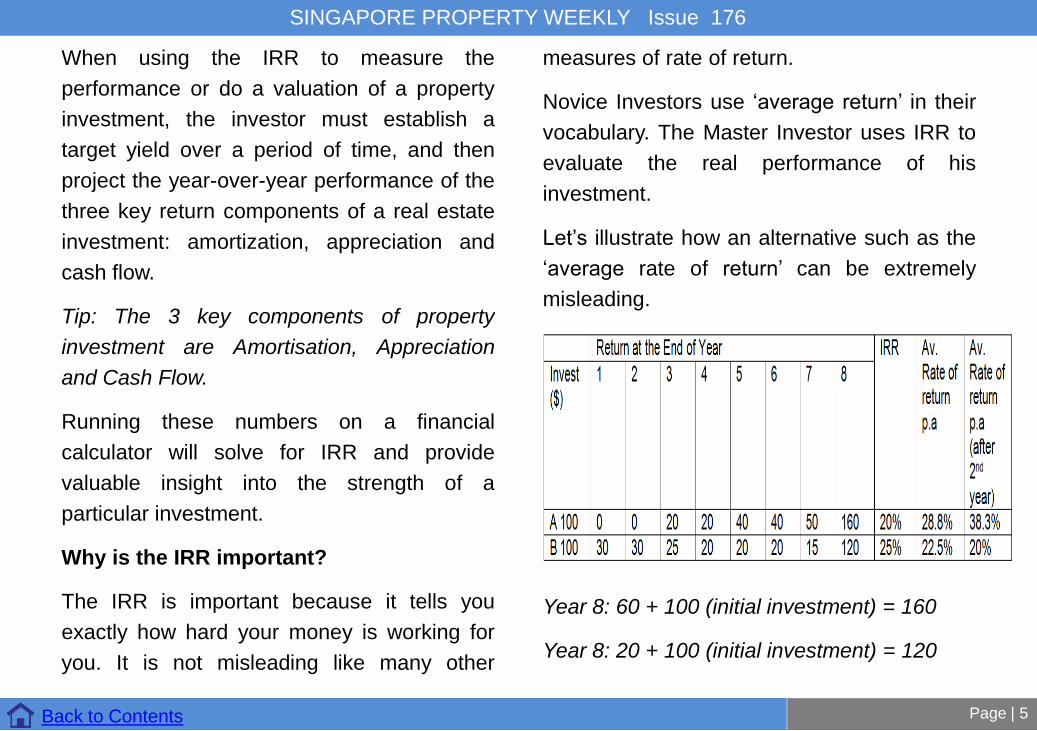

When using the IRR to measure the

performance or do a valuation of a property

investment, the investor must establish a

target yield over a period of time, and then

project the year-over-year performance of the

three key return components of a real estate

investment: amortization, appreciation and

cash flow.

Tip: The 3 key components of property

investment are Amortisation, Appreciation

and Cash Flow.

Running these numbers on a financial

calculator will solve for IRR and provide

valuable insight into the strength of a

particular investment.

Why is the IRR important?

The IRR is important because it tells you

exactly how hard your money is working for

you. It is not misleading like many other

measures of rate of return.

Novice Investors use ‗average return‘ in their

vocabulary. The Master Investor uses IRR to

evaluate the real performance of his

investment.

Let‘s illustrate how an alternative such as the

‗average rate of return‘ can be extremely

misleading.

Year 8: 60 + 100 (initial investment) = 160

Year 8: 20 + 100 (initial investment) = 120

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 6Back to Contents

In Investment A, the average rate of return

p.a. over the investment period is 28.8% i.e.

(0+0+20+20+40 +40+50+60)/8.

But in Investment B, it is only 22.5%. Yet, the

Internal Rate of Return (IRR) is higher in

investment B than in A (25% versus 20%).

Funds invested are working harder in

investment B. The reason is that the bulk of

returns are received earlier.

Even more misleading is when sales

prospectuses report an average rate of return

for only part of an investment‘s life. In

investment A, some prospectuses might state

the average rate of return p.a. after the

second year is 38.3%

(20+20+40+40+50+60)/6)! This is a way of

excluding the zero cash flows from years 1

and 2 in an attempt to improve the

appearance of returns.

In an extreme example, the rate of return in

some timber plantation investments is very

high in year 25 when trees are harvested. But

there is no income in the first 24 years! An

IRR is essential to get a real perspective on

the rate of return.

Tip: In real estate investment, returns in the

early years are more important than returns in

the later years.

Be wary of published rates of returns

So, beware of investments which show high

rates of return in the later years and publish

these figures (and not IRRs) in sales

prospectuses. Always use the IRR for the

most accurate indication of returns.

The Losing Investor will say, ―I‘m still making

money in investment A even though the IRR

is lower. So why should I care about IRR?‖

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 7Back to Contents

That‘s why the Losing Investor makes

‗mediocre‘ returns, while The Master Investor

makes ‗extraordinary‘ returns. The difference

here is about first having the right ‗mentality‘

to make money, and not the other way round!

This is one reason why I repeatedly

mentioned how buying off-plan properties as

investments (uncompleted/new launch) can

be an expensive gamble. The first 3 to 4

years have zero cash flows. After construction

is completed, the performance of the property

is highly questionable as too many optimistic

assumptions from the time of purchase

seldom materialise eventually.

If we measure our IRR from buying a re-sale

property instead, we‘ll easily find that our

returns are a better (or safer) bet than that of

a new property.

Tip: The IRR will tell you exactly how hard

your money is working for you, irrespective of

the pattern of income distribution over time.

No other measure of return will do this.

Concluding Comments

The IRR has been a popular metric for

evaluating investments for many years —

primarily due to the simplicity with which it

can be interpreted. However, the IRR suffers

from a couple of flaws.

The most important flaw is that it implicitly

assumes that the cash flows will be

reinvested for the life of the investment at a

rate that equals the IRR. A good project may

have an IRR that is considerably greater than

any reasonable reinvestment assumption.

Therefore, the IRR can be misleading at

times.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 8Back to Contents

The Modified Rate of Return (MIRR) and Net

Present Value (NPV)solves this problem by

using an explicit reinvestment rate (i.e. bank

deposits). We will cover these in a future

article.

By guest contributor Gerald Tay, who is the

founder and coach at CREI Academy Group

Pte Ltd, an organization dedicated to

empowering retail property investors with

smarter investing philosophy and strategies.

He is a full-time investor with over 13 years of

solid experience in building his wealth

through Property Investment and is financially

wealthy today.

SINGAPORE PROPERTY WEEKLY Issue 176

Singapore Property This Week

Page | 9Back to Contents

Residential

400 applications made for Woodlands EC

Bellewoods, which is the first executive

condominium launched this year has drew

400 applications. The condominium which is

located in Woodlands comprises of 561 units

and is expected to be sold for between $750

and $820 per square foot. Buyers would not

need to pay HDB resale levy when they

purchase a unit at Bellewoods as it is one of

the last executive condominiums in the

northern area of Singapore to be privatised.

Since January 2013, developers are required

to put their executive condominium projects

up for sale after only 15 months from the date

of award of the site. This has

moderateddevelopers‘ bids for executive

condominium sites in the Government Land

Sales programme.

(Source: Business Times)

Private residential market and HDB resale

market softens in Q3

Market experts believe that the weak holding

power of private home owners and

developers has pushed prices of private

homes and HDB resale flats down in Q3

2014. Flash estimates by the Urban

Redevelopment Authority (URA) showed that

the overall Private Residential Property Price

Index (PRPPI) has fell 0.6 per cent in Q3 this

year. This follows a 1 per cent fall in the

PRPPI in Q2 this year.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 10Back to Contents

Over the last four quarters, prices of private

homes have fallen by 3.8 per cent. On the

other hand, resale HDB prices have also

fallen due to the implementation of the

mortgage servicing ratio. Not only so, the

increase in supply of build-to-order flats has

reduced demand for resale flats. Flash

estimates from HDB showed that resale price

index has slipped by 1.6 per cent in Q3, while

resale prices have dropped by 6.8 per cent in

Q3 2014 from Q3 2013. Ong Teck Hui from

JLL does not expect the private home market

to rebound soon. URA flash estimates also

showed that prices of landed properties have

fallen 1.7 per cent in Q3. Ong believes this is

because the total debt servicing ratio has

reduced the demand for landed properties.

Eugene Lim from ERA Realty also added that

the gradual fall in prices is an effect of the

government‘s cooling measures.

(Source: Business Times)

Condo prices in August remains flat

According to flash estimates by the National

University of Singapore, resale prices of

completed private apartments and condos

have been flat in August. From July to August,

prices for the overall market and the central

region, including the financial district and

Sentosa Cove, have remained unchanged.

Yet, small apartments in the non- central

regions have increased by 0.1 per cent in

August. LumSau Kim said that the low

turnover is likely to be due to fewer

successful transactions. This is because

sellers have not adjusted their asking prices

to meet buyers‘ expectations.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 11Back to Contents

Not only so, only 318 condo units were

transacted in August. This is a fall from the

376 units that changed hands in July.

Nicholas Mak from SLP International believes

that the Hungry Ghost month has slowed

sales in August. Mak added that there were

no launched private residential projects in

August, and as such, condo sales have been

flat.

(Source: Business Times)

Sembawang EC site sold for $353 psfppr

A Sembawang executive condominium site

has been sold for $353 per square feet per

plot ratio, which is marginally higher than the

$350 psfppr that an adjacent site had fetched

in January this year. The bid was won by

Qingjian Realty. Despite the high price, the

tender had only attracted two bids. The low

participation in the tender reflects the

developers‘ sentiments in the executive

condominium market. Ong Kah Seng from

R‘ST Research believes that Qingjian Realty

may have offered a high bid price as it

believes that the government will soon lift

cooling measures on the executive

condominium market. Currently, executive

condominiums can only be released 15

months from the date of award of the site.

Also, there is a mortgage service ratio cap

that impacted residential property demand.

Nicholas Mak from SLP International predicts

that Qingjian Realty‘s breakeven cost is as

high as $740 per square foot.

(Source: Business Times)

Marina One to be launched on Oct 11 2014

M+S Pte Ltd will only be launching 150 to 200

units at the expected launch of Marina One

Residences.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 12Back to Contents

The released units are part of the first

residential block. The second residential

block, which has about 521 units, will be

released after the project‘s temporary

occupation permit has been issued. Market

experts believe this will help moderate the

supply of residential units. The mixed-used

project, which comprises 1,042 units in total,

is expected to be released on October 11.

Prices of the residential units will range from

$1,960 to $3,100 per square foot. One-

bedroom units start from 700 square feet and

are priced at $1.4 million while a two-

bedroom unit is about 1,001 square feet and

is selling for about $2 million. On the other

hand, a three-bedder is going for $3.46

million. Since the project does not come

under the qualifying certificate rules, the

developer will not be required to sell all its

units within two years of its completion.

Kemmy Tan from M+S expects the property

to fetch a rental yield of 2 to 3 per cent due to

its prime location.

(Source: Business Times)

Lake Life launches before 15-month sale-

launch rule is up

To moderate the market, developers can only

launch their executive condominium projects

15 months after the date of award of the site,

or after the completion of foundation works,

whichever is earlier. The Lake Life executive

condominium is likely to be the first executive

condominium that will be launched before the

stipulated 15 months as it is slated to be

released for sale on October 4. Vincent Ong

from Evia Real Estate said that developers

have been able to complete foundation works

within the first eight months. The Lake Life

executive condominium consists of two-

bedroom units of about 969 square feet,

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 13Back to Contents

three-bedroom units from 1,033 square feet

and four-bedroom units from 1,195 square

feet. The units are expected to be priced

between $880 and $890 per square foot.

Commercial

Havelock II well received among buyers

Since its soft launch in July, about 70 per cent

of the 50 units at Havelock II have been sold

by Guthrie GTS. The 50 units sold in

Havelock II made up half of the 100 office and

retail units released by Guthrie to revamp HR

buildings acquired earlier in March 2013. Of

the 245 units in that project, 151 are retail

units and the remaining are office spaces.

Michael Leong from Guthrie said that the total

debt servicing ratio framework has slowed

sales. Office units, ranging from 312 square

feet to 2,357 square feet have been sold for

an average price of $2,228 per square feet.

On the other hand, retail units from 150

square feet to 1,335 square feet have been

sold for an average of $4,657 per square feet.

All retail units are provided with water points

and discharge outlets. Selected units will also

be provided with independent air-conditioning

systems. Last year, Guthrie had paid $282.88

million to acquire the eight-storey building.

(Source: Business Times)

DTZ: 1m sqft office space to be available

in 2015

According to DTZ, about one million square

feet of office space will be available in 2015

when current tenants move out of existing

buildings to new offices. Not only so, there

will be another 133,000 square feet of

shadow spaces released next year. This will

add on to the current 550,000 square feet of

shadow office space.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 14Back to Contents

These spaces are made available for

subletting or reassignment by tenants. Thus,

there will be a net increase of 159,000 square

feet in office supply in 2015, said DTZ. While

office rents have been projected to grow by

15 per cent by the end of this year, Lee Lay

Keng from DTZ believes that rental growth in

the CBD area will increase by a slower rate in

2015. The average gross monthly rental for

offices in Raffles Place has increased 2.7 per

cent to $10.55 per square foot from Q2 to Q3

this year. Not only so, DTZ said that

occupancy rates were higher in Q3 across the

island. This is because no new office space

was released in that quarter. Occupancy rates

have rose by 0.8 percent to 95.8 percent in

Q3 2014.

(Source: Business Times)

Tuas and Tampines industrial site on sale

Two sites at Tuas South and one at Tampines

North have been put on sale. All three sites

have been zoned for Business-2

development. The site at Tampines is 2.7 ha.

It is the largest site that has been launched in

H2 2014, under the industrial government

land sales confirmed list. It has a gross plot

ratio of 2.5 and has a lease of 30 years.

Nicholas Mak from SLP International predicts

that there will be four to seven bids for the

Tampines site. Also, he expects the top bid to

be around $70 to $82 per square foot per plot

ratio. On the other hand, Ong Kah Seng from

R‘ST Research said that the winning bid

would be around $90 to $105 per square foot

per plot ratio. Market experts expect the Tuas

site to attract lower bid prices.

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 15Back to Contents

The site at Tuas South Street 9, which has a

20 year 8 month lease and a gross plot ratio

of 1.0, is expected to draw bids as high as

$65 per square foot per plot ratio, said Mak.

The other site at Tuas South Street 6 will be

released under the reserved list. It also has a

gross plot ratio of 1.0. However it has a 20

year and 4 month lease. Analysts believe that

that site will be sold for about $60 to $75 per

square foot per plot ratio.

(Source: Business Times)

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 16Back to Contents

Non-Landed Residential Resale Property Transactions for the Week of Sep 17 – Sep 23

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

3 HARVEST MANSIONS 947 1,250,000 1,320 99

3 TANGLIN VIEW 1,141 1,450,000 1,271 99

4 THE AZURE 2,271 4,030,000 1,774 99

4 THE INTERLACE 1,001 1,330,000 1,329 99

5 THE PARC CONDOMINIUM 1,421 1,880,000 1,323 FH

5 VARSITY PARK CONDOMINIUM 1,453 1,720,000 1,184 99

5 DOVER PARKVIEW 1,249 1,430,000 1,145 99

5 DOVER PARKVIEW 1,249 1,325,000 1,061 99

5 VARSITY PARK CONDOMINIUM 1,636 1,680,000 1,027 99

5 WEST BAY CONDOMINIUM 1,216 1,100,000 904 99

5 VARSITY PARK CONDOMINIUM 2,250 2,025,000 900 99

7 BURLINGTON SQUARE 1,302 1,460,000 1,121 99

8 CITY SQUARE RESIDENCES 1,195 1,650,000 1,381 FH

9 RIVERSIDE 48 904 1,990,000 2,201 FH

9 RESIDENCES AT EMERALD HILL 2,282 4,950,000 2,169 FH

9 VIDA 883 1,725,000 1,954 FH

9 SKYLINE 360 @ SAINT THOMAS WALK 22,238 35,000,000 1,574 FH

10 ARDMORE PARK 2,885 7,840,000 2,718 FH

10 BELMOND GREEN 1,281 2,241,750 1,750 FH

10 VALLEY PARK 1,808 2,712,000 1,500 999

10 SOMMERVILLE PARK 1,948 2,750,000 1,411 FH

10 DORMER PARK 2,540 3,400,000 1,338 FH

10 SIGNATURE AT LEWIS 6,534 7,000,000 1,071 FH

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

11 NEWTON 18 614 1,050,000 1,711 FH

11 PARK INFINIA AT WEE NAM 3,315 4,500,000 1,357 FH

11 LA MAISON 1,292 1,720,000 1,332 FH

12 THE MEZZO 840 1,270,000 1,513 FH

14 LE CRESCENDO 947 1,080,000 1,140 FH

15 DE CENTURION 775 1,120,000 1,445 FH

15 PRESTIGE LOFT 388 545,000 1,406 FH

15 THE ESTA 1,313 1,755,000 1,336 FH

15 FINLAND GARDENS 1,324 1,600,000 1,208 FH

15 AMBER RESIDENCES 2,217 2,600,000 1,173 FH

15 DUNMAN PLACE 1,442 1,680,000 1,165 FH

15 PARK EAST 1,345 1,535,000 1,141 FH

15 CHAPEL COURT 807 770,000 954 FH

15 BLU CORAL 1,948 1,530,000 785 FH

16 BAYSHORE PARK 936 968,000 1,034 99

16 SUNHAVEN 2,099 1,538,000 733 FH

17 EDELWEISS PARK CONDOMINIUM 1,281 1,180,000 921 FH

19 AMARANDA GARDENS 1,464 1,868,000 1,276 FH

19 KOVAN RESIDENCES 1,270 1,410,000 1,110 99

19 CHUAN PARK 1,173 1,145,000 976 99

19 RIO VISTA 1,378 1,235,000 896 99

19 RIO VISTA 1,249 1,100,000 881 99

19 CHUAN PARK 1,528 1,280,000 837 99

SINGAPORE PROPERTY WEEKLY Issue 176

Page | 17Back to Contents

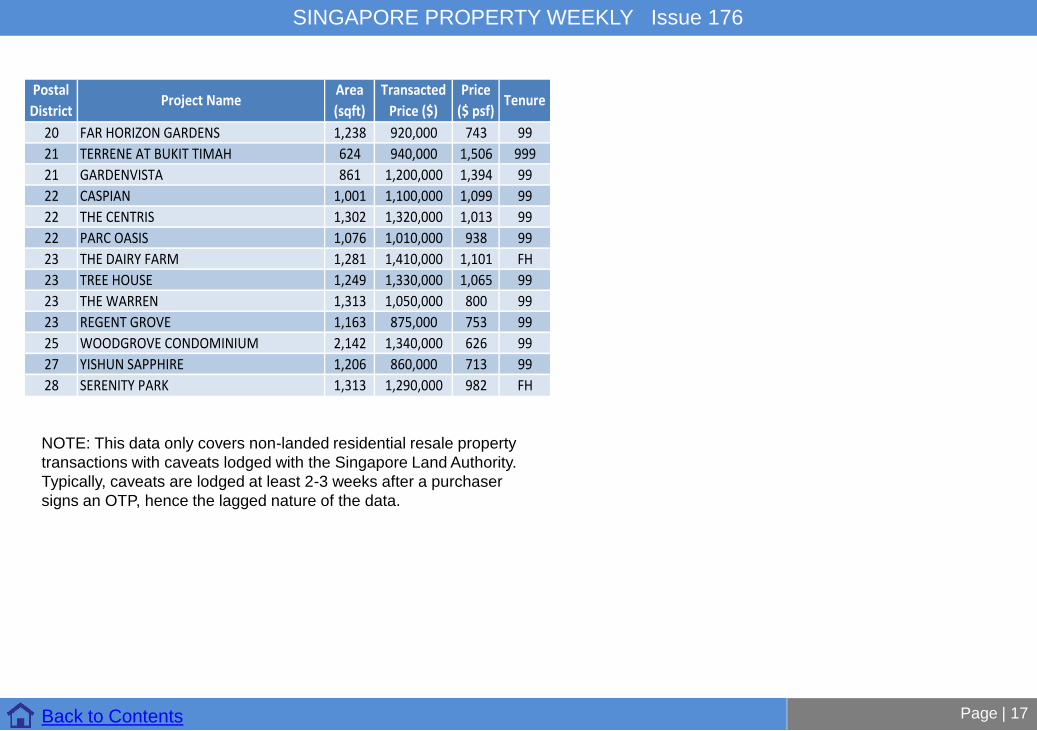

NOTE: This data only covers non-landed residential resale property

transactions with caveats lodged with the Singapore Land Authority.

Typically, caveats are lodged at least 2-3 weeks after a purchaser

signs an OTP, hence the lagged nature of the data.

Postal

DistrictProject Name

Area

(sqft)

Transacted

Price ($)

Price

($ psf)Tenure

20 FAR HORIZON GARDENS 1,238 920,000 743 99

21 TERRENE AT BUKIT TIMAH 624 940,000 1,506 999

21 GARDENVISTA 861 1,200,000 1,394 99

22 CASPIAN 1,001 1,100,000 1,099 99

22 THE CENTRIS 1,302 1,320,000 1,013 99

22 PARC OASIS 1,076 1,010,000 938 99

23 THE DAIRY FARM 1,281 1,410,000 1,101 FH

23 TREE HOUSE 1,249 1,330,000 1,065 99

23 THE WARREN 1,313 1,050,000 800 99

23 REGENT GROVE 1,163 875,000 753 99

25 WOODGROVE CONDOMINIUM 2,142 1,340,000 626 99

27 YISHUN SAPPHIRE 1,206 860,000 713 99

28 SERENITY PARK 1,313 1,290,000 982 FH