singtel investor day: mobile business overview · pdf fileforward looking statements -...

TRANSCRIPT

SingTel Investor Day:Mobile Business Overview

Michael Smith

Managing Director, Consumer

11 July 2011

2Forward looking statements - important note

The following presentation may contain forward looking statements by the management of SingTel Group relating

to financial trends for future periods, compared to the results for previous periods.

Some of the statements contained in this presentation that are not historical facts are statements of future expectations

with respect to the financial conditions, results of operations and businesses, and related plans and objectives. Forward

looking information is based on management's current views and assumptions including, but not limited to, prevailing

economic and market conditions. These statements involve known and unknown risks and uncertainties that could cause

actual results, performance or events to differ materially from those in the statements as originally made. Such

statements are not, and should not be construed as a representation as to future performance of SingTel Group.

In particular, such targets should not be regarded as a forecast or projection of future performance of SingTel Group.

It should be noted that the actual performance of SingTel Group may vary significantly from such targets.

3

1 Market overview

3 Future opportunities & strategy

2 FY11 performance

Today

4

1 Market overview

3 Future opportunities & strategy

2 FY11 performance

Today

5

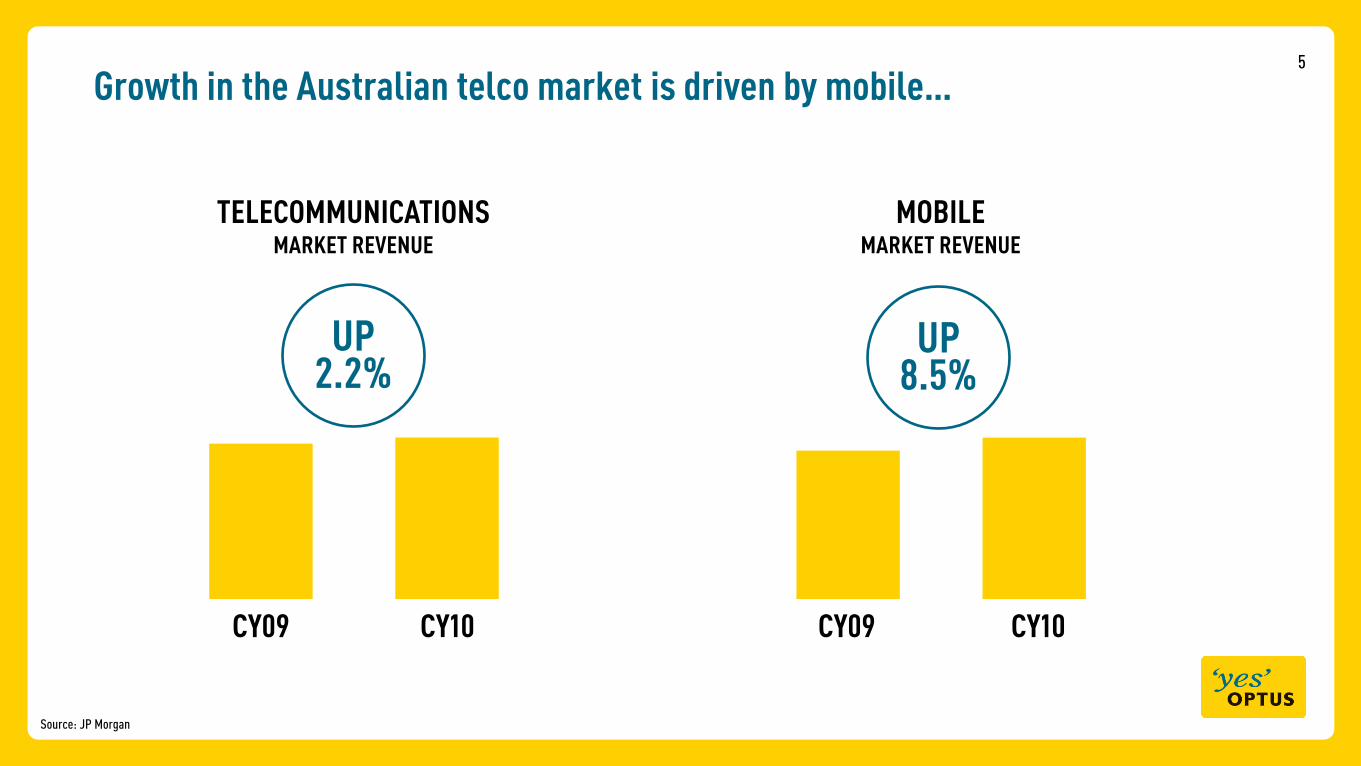

Source: JP Morgan

Growth in the Australian telco market is driven by mobile…

TELECOMMUNICATIONSMARKET REVENUE

MOBILEMARKET REVENUE

CY10CY09CY10CY09

UP2.2%

UP8.5%

6

Source: Merrill Lynch

YOY Mobile Subscriber Growth - CY10

2.7%

5.2%

9.8%

15.0% 15.0%

21.3%23.4%

27.9%

USAAustraliaGermanySpain Italy UK France Singapore

YOY Data Revenue Growth - CY10

-4.8%

0.5%

2.6%

4.4% 4.4%

6.0% 6.2%

9.8%

UK

USAFranceSpainItalyGermany AustraliaSingapore

…underpinned by leading subscriber and strong data revenue growth amongst world’s developed economies

7

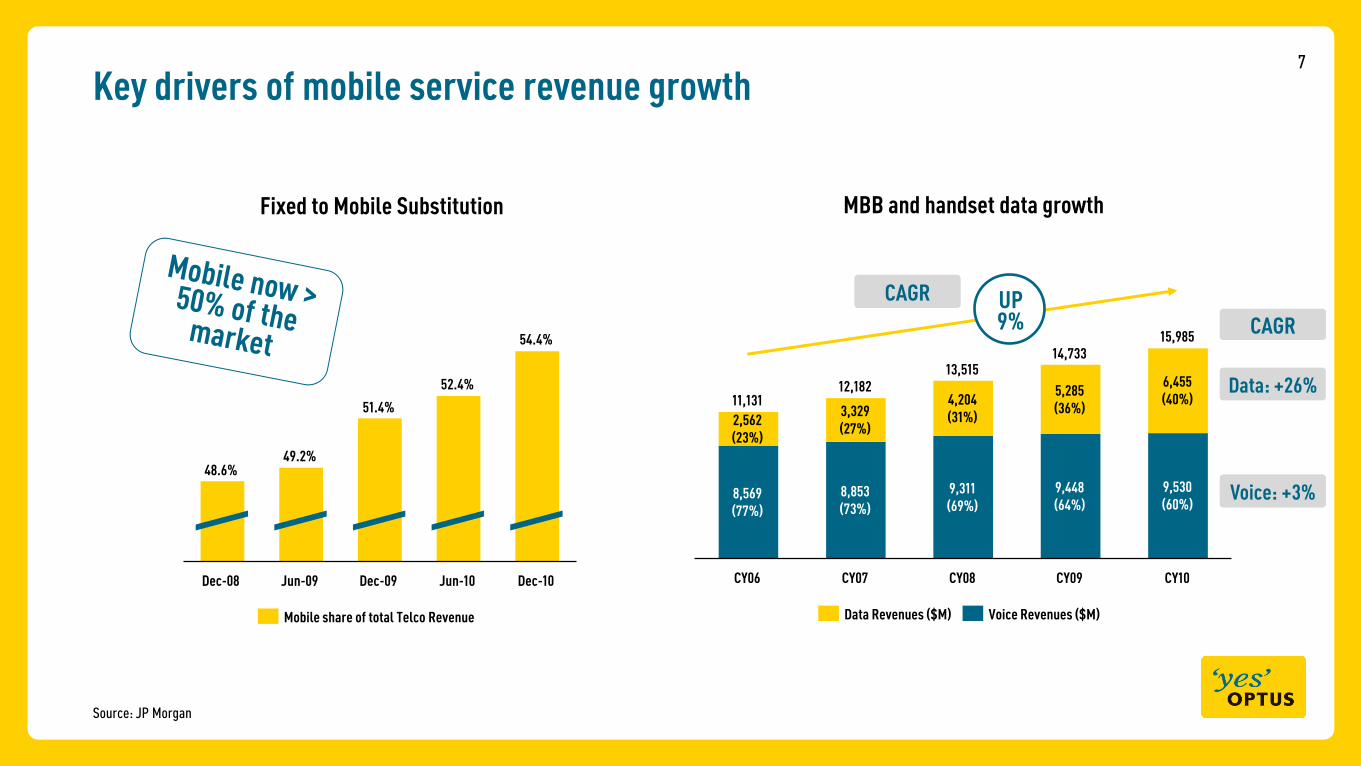

Key drivers of mobile service revenue growth

Source: JP Morgan

52.4%

Dec-10Dec-08

48.6%

Jun-09 Dec-09 Jun-10

54.4%

49.2%

51.4%

Mobile share of total Telco Revenue

Fixed to Mobile Substitution

CY10

15,985

9,530(60%)

6,455(40%)

CY09

14,733

9,448(64%)

5,285(36%)

CY08

13,515

9,311(69%)

4,204(31%)

CY07

12,182

8,853(73%)

3,329(27%)

CY06

11,131

8,569(77%)

2,562(23%)

Voice Revenues ($M)Data Revenues ($M)

Data: +26%

Voice: +3%

MBB and handset data growth

UP9% CAGR

CAGR

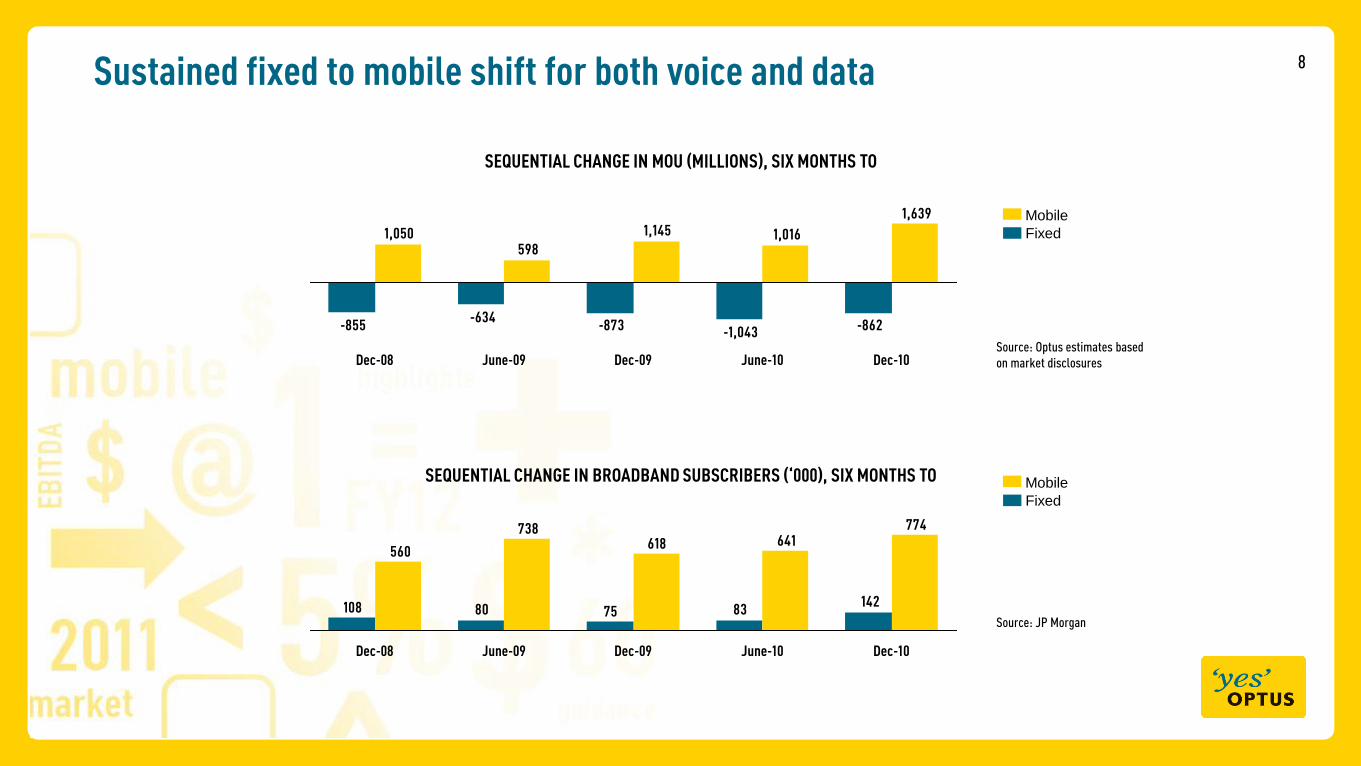

8

Source: Optus estimates based

on market disclosures

142837580108

774641618

738

560

Dec-10June-10Dec-09June-09Dec-08

SEQUENTIAL CHANGE IN MOU (MILLIONS), SIX MONTHS TO

SEQUENTIAL CHANGE IN BROADBAND SUBSCRIBERS (‘000), SIX MONTHS TO

Fixed

Mobile

Sustained fixed to mobile shift for both voice and data

Source: JP Morgan

-862-1,043-873-634

-855

1,639

1,0161,145

5981,050

Dec-10June-10Dec-09June-09Dec-08

Fixed

Mobile

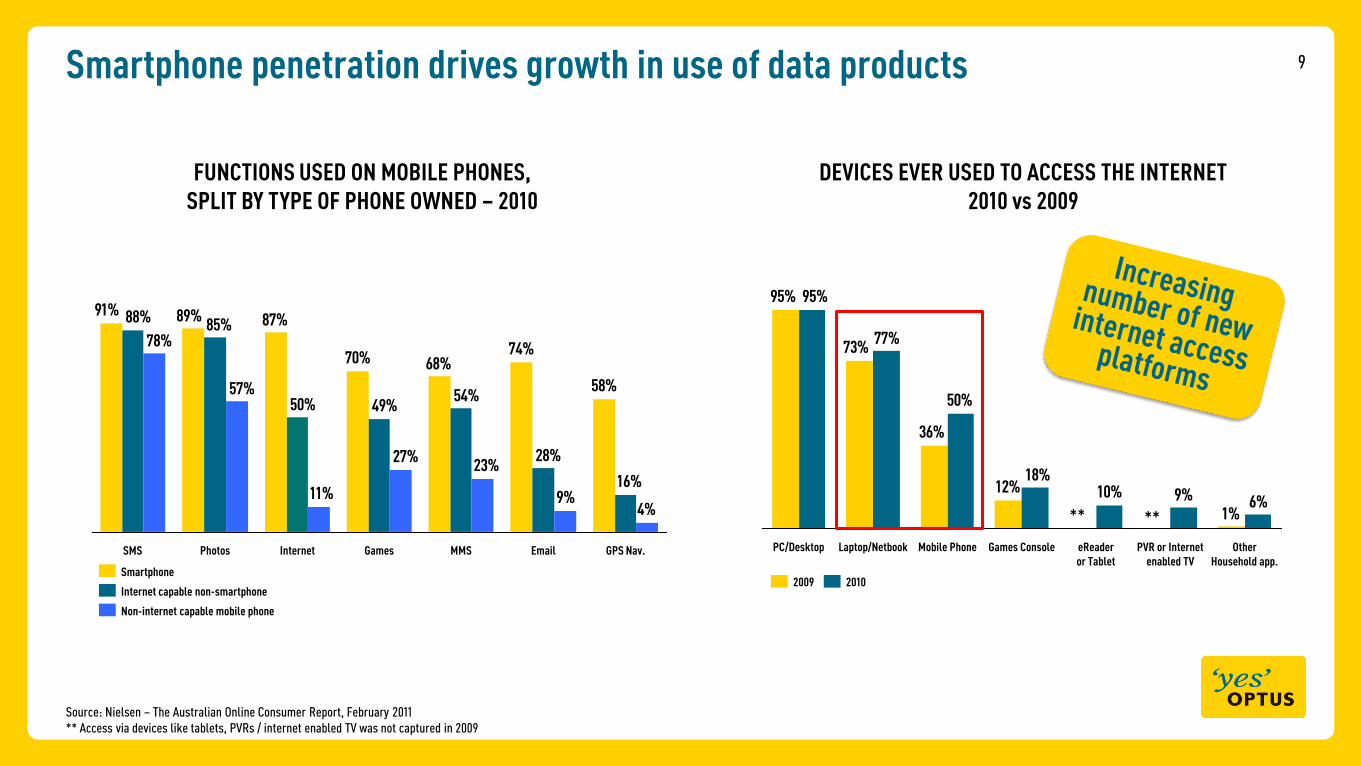

9Smartphone penetration drives growth in use of data products

58%

74%68%70%

87%89%91%

16%

28%

54%49%50%

85%88%

4%9%

23%27%

11%

57%

78%

InternetPhotosSMS GPS Nav.EmailMMSGames

Non-internet capable mobile phone

Internet capable non-smartphone

Smartphone

1%

12%

36%

73%

95%

6%9%10%18%

50%

77%

95%

Mobile Phone Games ConsoleLaptop/NetbookPC/Desktop Other Household app.

PVR or Internet enabled TV

eReader or Tablet

20102009

DEVICES EVER USED TO ACCESS THE INTERNET 2010 vs 2009

FUNCTIONS USED ON MOBILE PHONES, SPLIT BY TYPE OF PHONE OWNED – 2010

Source: Nielsen – The Australian Online Consumer Report, February 2011

** Access via devices like tablets, PVRs / internet enabled TV was not captured in 2009

****

10

Consumer Confidence

However various headwinds are emerging

CAGR: -3%

Dec-10Jun-10Dec-09Jun-09Dec-08

A$/Minute (Mob industry minutes / Pre+Post revenue, ex WBB)

* A$350, + unlimited on-net calls

Westpac Consumer Confidence Index - June 2011

364

555

10388

-18

74

Mar-11Dec-10

VHA

Optus

Telstra

Source: Company disclosures, Optus analysis

** VHA branded net adds

Mobile net adds for the quarter („000)

“Investment in the resources sector is picking up strongly… and the outlook remains very positive... In other areas, cautious behaviour by households … are having a noticeable dampening effect.”

Statement by Glenn Stevens, Governor RBA: Monetary Policy Decision (5 July 2011)

Pricing PressureCompetitive Aggression

**

**

Increase in plan inclusions

$25

0

$35

0 $45

0

Included value (A$)

Consumer

7.81

7.44

7.678.12

OCTOBER 2009

A$49

Mar-10

A$49

Mar-10A$49

Mar-11

A$45

Mar-11

Unl

imit

ed c

alls

, tex

ts &

soci

al n

etw

ork

*

11

1 Market overview

3 Future opportunities & strategy

2 FY11 performance

Today

12

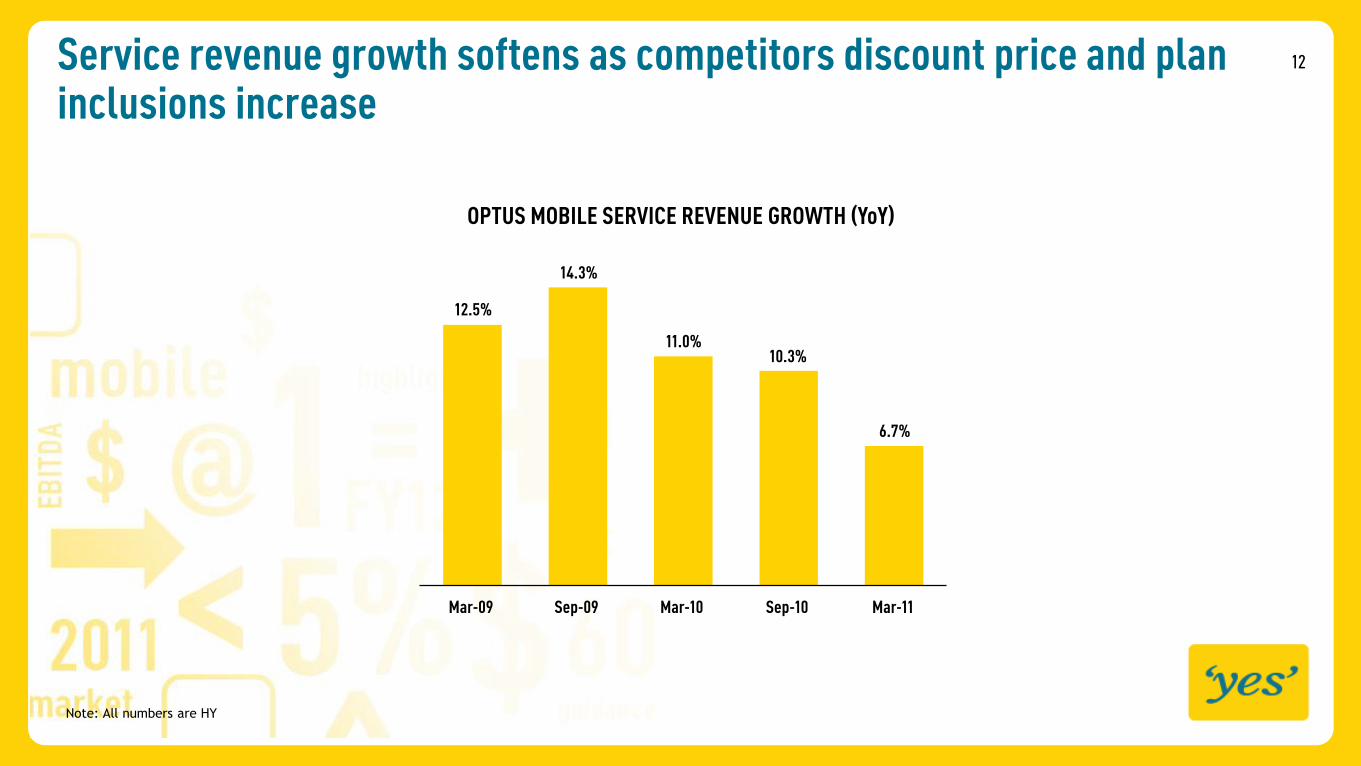

12.5%

14.3%

11.0%10.3%

6.7%

Mar-11Sep-10Mar-10Sep-09Mar-09

OPTUS MOBILE SERVICE REVENUE GROWTH (YoY)

Service revenue growth softens as competitors discount price and plan inclusions increase

Note: All numbers are HY

13

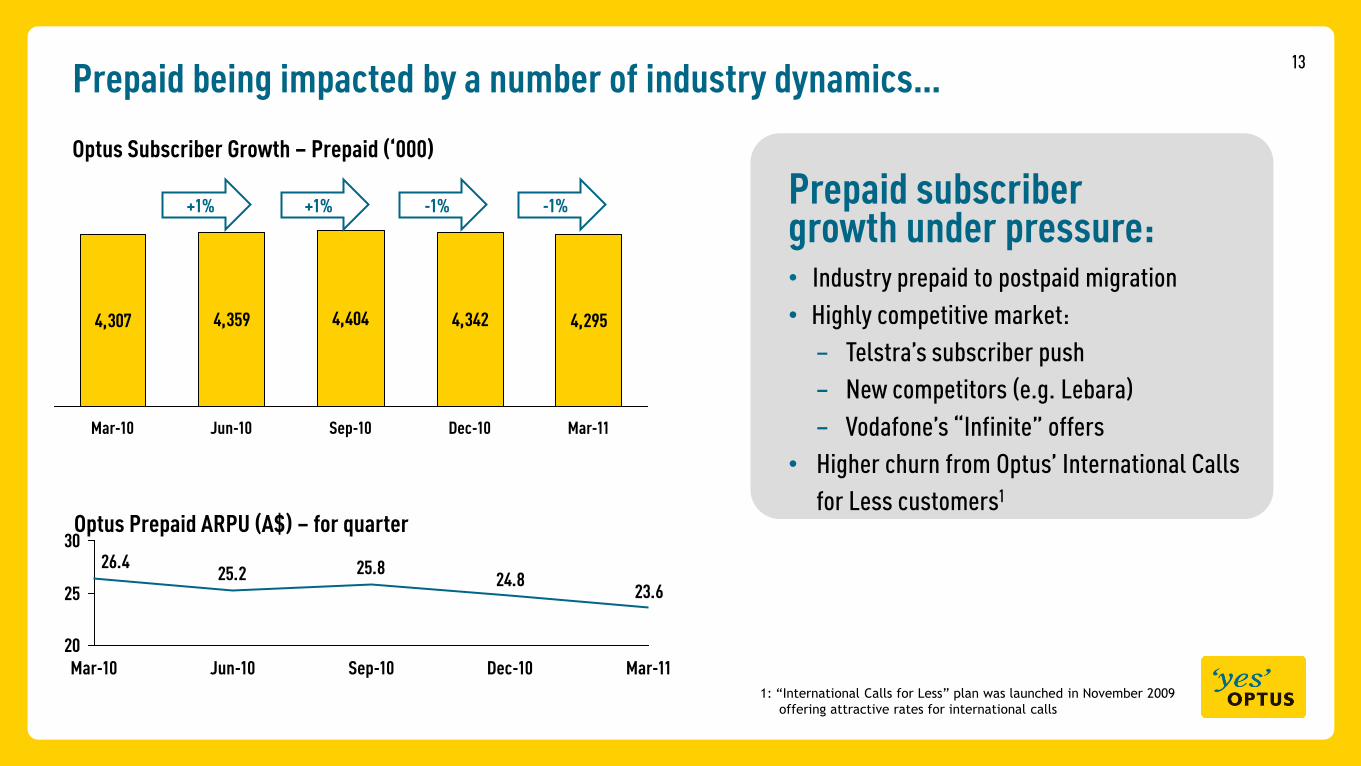

Prepaid being impacted by a number of industry dynamics…

4,307 4,359 4,404 4,342 4,295

Mar-10 Sep-10Jun-10 Mar-11Dec-10

Optus Subscriber Growth – Prepaid (‘000)

Prepaid subscriber growth under pressure:• Industry prepaid to postpaid migration

• Highly competitive market:

– Telstra‟s subscriber push

– New competitors (e.g. Lebara)

– Vodafone‟s “Infinite” offers

• Higher churn from Optus‟ International Calls

for Less customers1

+1% +1% -1% -1%

24.825.825.2

26.4

23.6

20

25

30

Dec-10 Mar-11Sep-10Jun-10Mar-10

Optus Prepaid ARPU (A$) – for quarter

1: “International Calls for Less” plan was launched in November 2009

offering attractive rates for international calls

14

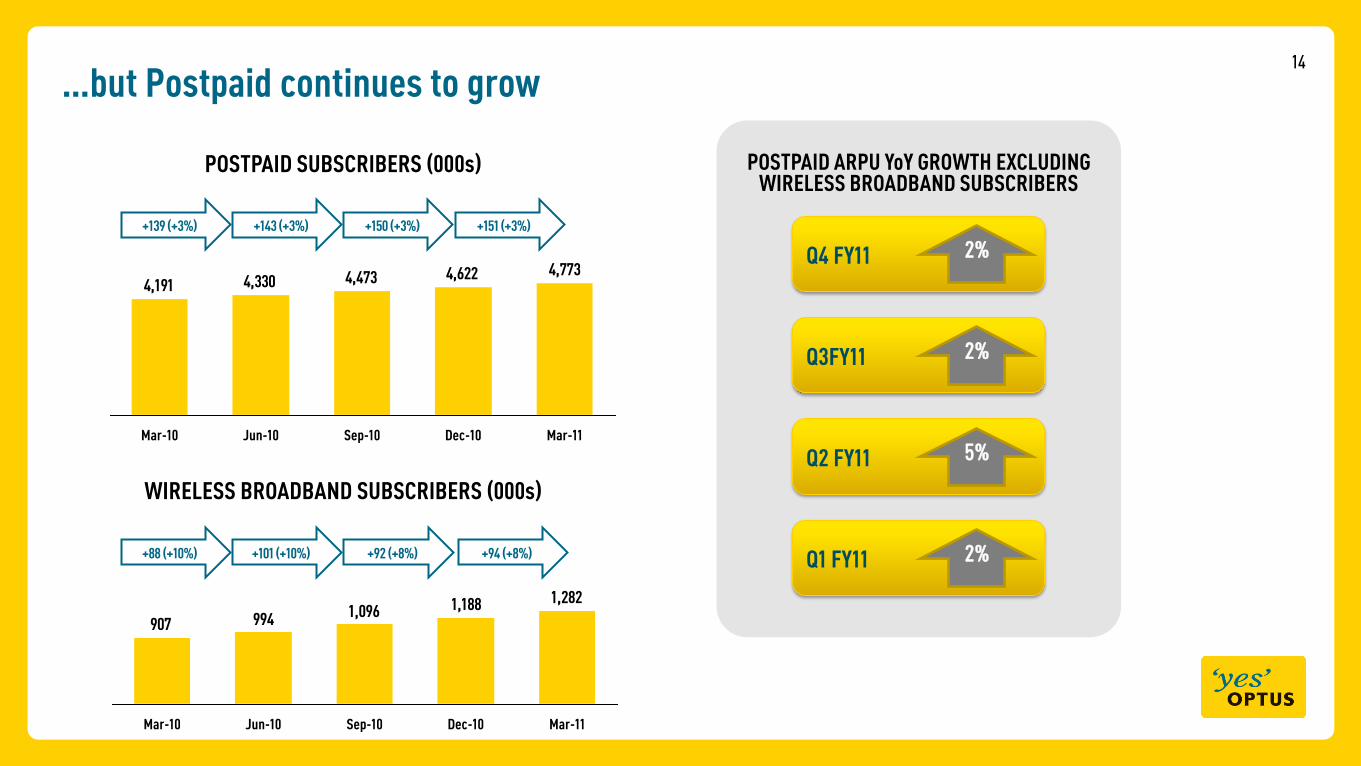

…but Postpaid continues to grow

POSTPAID SUBSCRIBERS (000s)

+139 (+3%) +143 (+3%) +150 (+3%) +151 (+3%)

WIRELESS BROADBAND SUBSCRIBERS (000s)

4,7734,6224,4734,3304,191

Mar-11Dec-10Sep-10Jun-10Mar-10

+88 (+10%) +101 (+10%) +92 (+8%) +94 (+8%)

POSTPAID ARPU YoY GROWTH EXCLUDING WIRELESS BROADBAND SUBSCRIBERS

Q1 FY11 2%

Q2 FY11 5%

Q3FY11 2%

Q4 FY11 2%

1,2821,1881,096994907

Mar-11Dec-10Sep-10Jun-10Mar-10

15Smartphone penetration and innovative data services driving data growth

OPTUS DATA SHARE OF SERVICE REVENUE

3%

5%

9% 13%18%

2011

40%

23%

2010

36%

23%

2009

33%

24%

2008

28%

23%

2007

24%

20%

SMS % of Service Rev

Non SMS Data % of Service Rev

Note: All numbers are FY end

389,000 live streams of the 2010 FIFA World Cup matches

79% increase in Australian Open Tennis live streaming

Google Apps Partnership

Helping SMBs manage

their communications

Unlimited mobile access, within Australia, to these sites

16

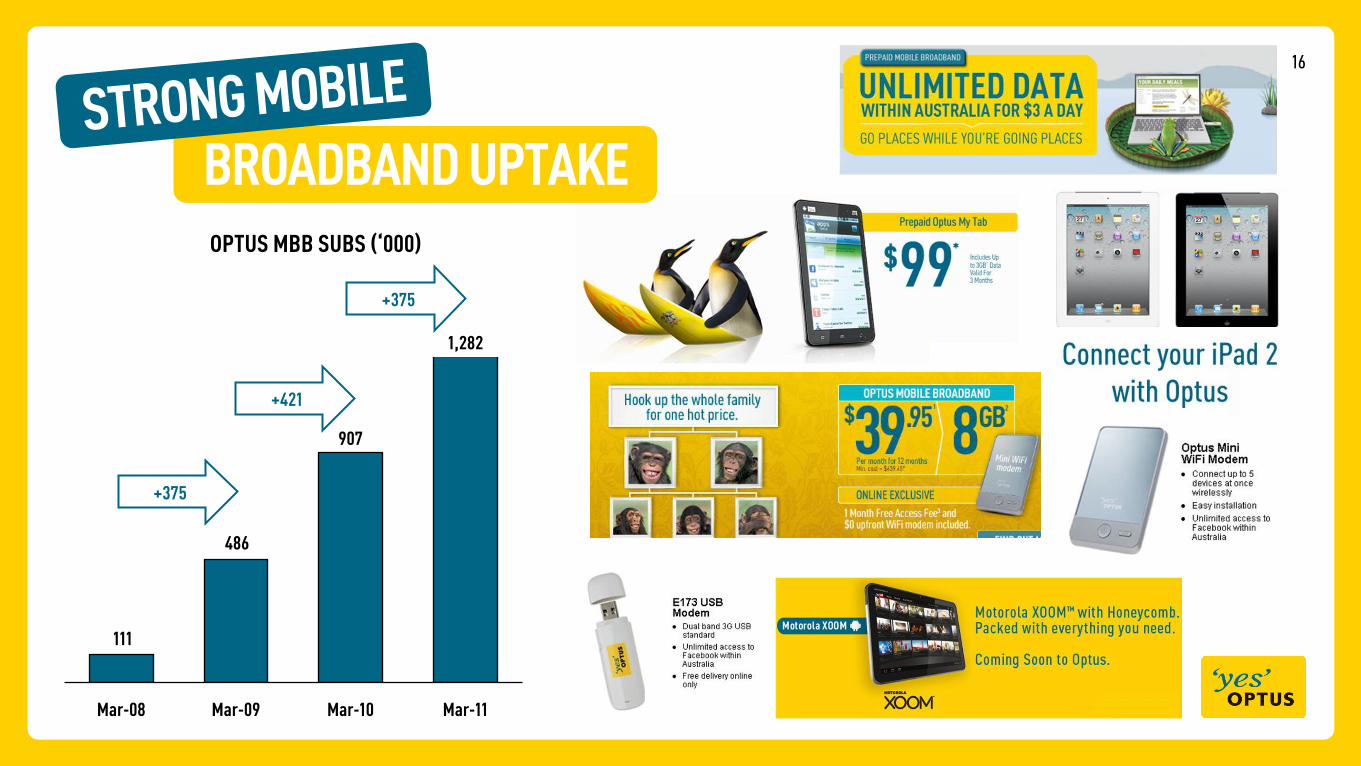

OPTUS MBB SUBS (‘000)

111

486

907

1,282

Mar-11Mar-10Mar-09Mar-08

+375

+421

+375

BROADBAND UPTAKE

17

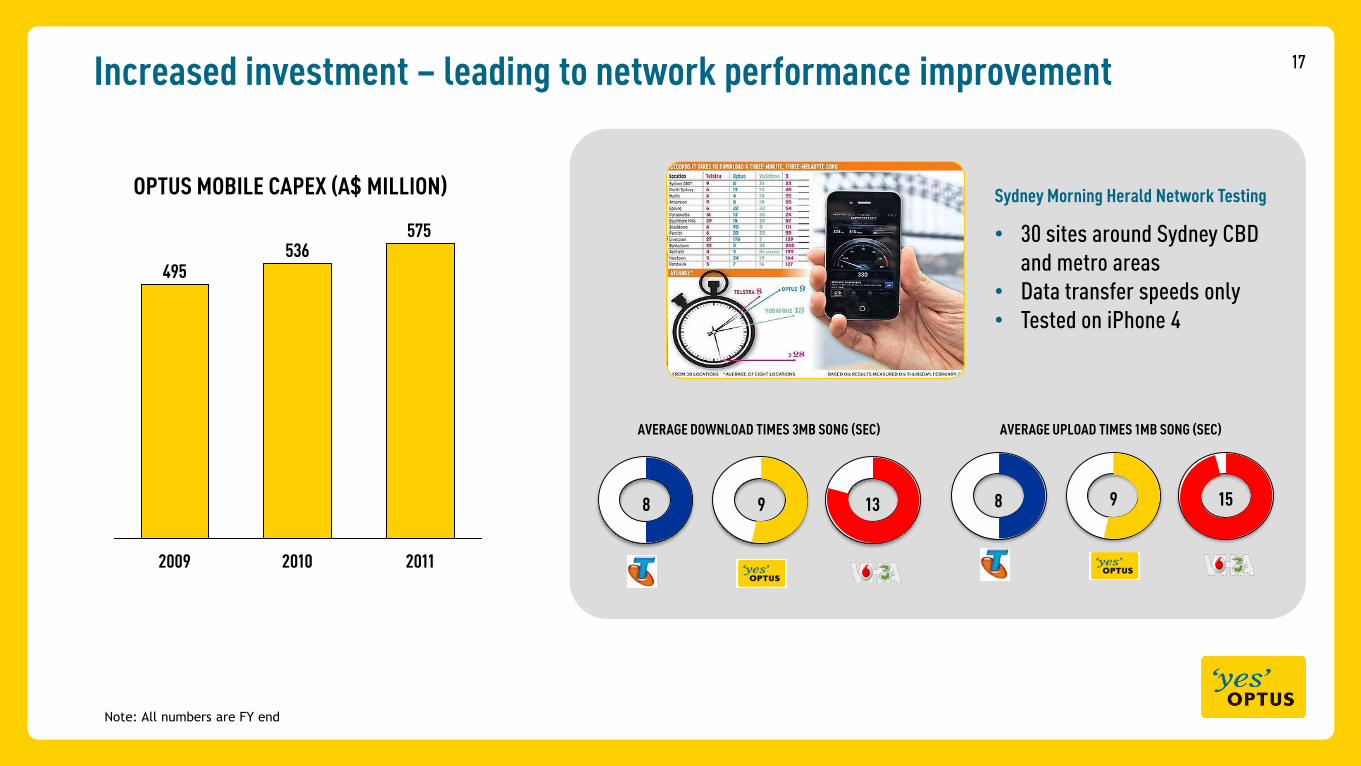

8 9 13

AVERAGE DOWNLOAD TIMES 3MB SONG (SEC)

OPTUS MOBILE CAPEX (A$ MILLION)

575536

495

201120102009

Note: All numbers are FY end

8 9 15

AVERAGE UPLOAD TIMES 1MB SONG (SEC)

Sydney Morning Herald Network Testing

• 30 sites around Sydney CBD

and metro areas

• Data transfer speeds only

• Tested on iPhone 4

Increased investment – leading to network performance improvement

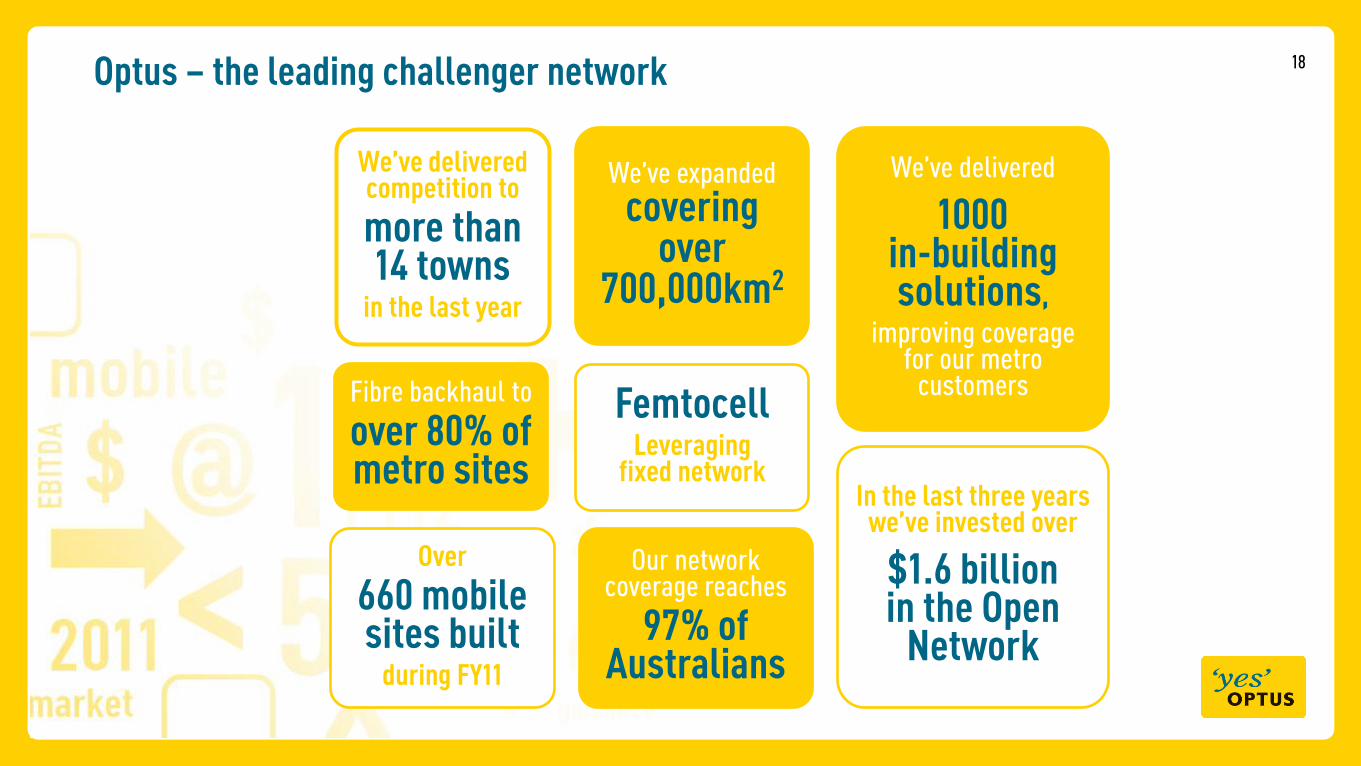

18

We’ve delivered competition to

more than 14 towns

in the last year

Our network coverage reaches

97% of Australians

We‟ve expanded

covering over

700,000km2

Fibre backhaul to

over 80% of metro sites

We‟ve delivered

1000 in-building solutions,

improving coverage for our metro

customers

Over

660 mobile sites built

during FY11

In the last three years we’ve invested over

$1.6 billion in the Open

Network

FemtocellLeveraging

fixed network

Optus – the leading challenger network

19The Customer Experience program continues to deliver improvements for our Mobile Customers

Reduction in number

of technical enquiries

− through a simplified activation

process in Mobile Billing and

General enquiries

Faster delivery of online

orders for mobile handsets 50%

Reduction in early tenure

churn in Post Paid Mobile

30%

25%

Outperforming our major competitor in key CE metrics

+5%

+4%

+7%

Activation

Billing

Customer Service

20

1 Market overview

3

2 FY11 performance

Today

Future opportunities & strategy

21

Driving a breakthrough in Customer Experience

Driving a Customer-centric attitude

Fix vital service experience

Design for Lifetime ValueProduct is the Network

Understand the CustomerLink Customer

Experience to ValueClosed Loop Feedback

We are resolving the key

Customer pain points.

We will continue to invest

in systems and our people to

exceed customer expectations.

We will continue to invest in our network

and will work to close our customers‟

perception gap of our performance.

We will empower our people to drive continuous

improvement by ensuring Customer

feedback is achieved on a timely basis.

We will drive loyalty through our

acquisition, retention and

rewarding of our Customers

We will link Customer

Experience to performance.

We will breakout in customer experience

22Device leadership across handsets, tablets and other devices

Number of Applications (‘000)

Source: Samsung Securities – April 2011

10

20

50

275

350iOS

Windows

Blackberry

Android

Symbian

23Deliver relevant and personalised digital services to our customers

Lead in online digital experience with products and VAS of

RELEVANCE

Optus Smart Safe

• secured data

• accessible on any device

• easily shared with friends and family

Google Apps Partnership

• helping small medium businesses manage their communications

• range of integrated business tools

• accessible via a single web portal on a range of devices

• dedicated IT helpdesk offering up to 24/7 support

Optus Smart Safe Optus Call BuddyOptus Now

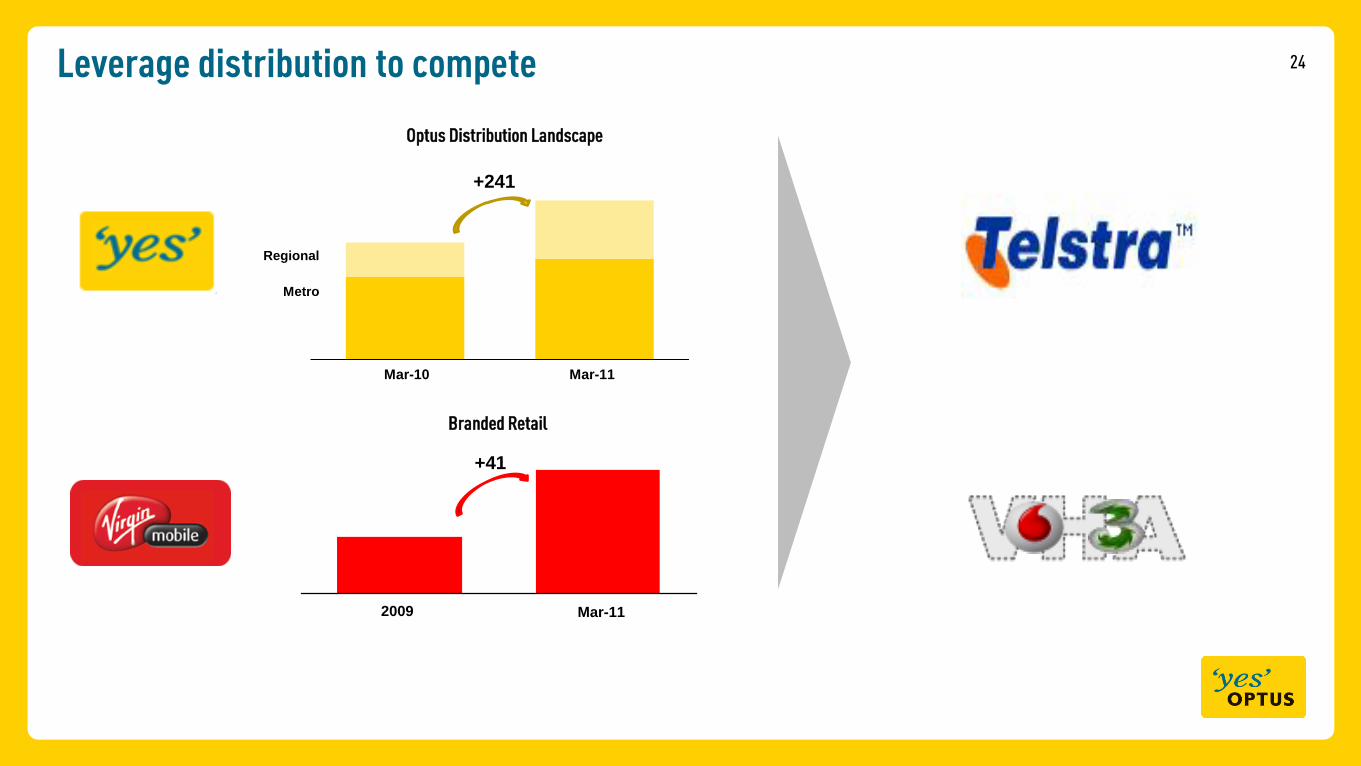

24Leverage distribution to compete

Mar-112009

Branded Retail

Consumer

7.81

7.44

7.678.12

OCTOBER 2009

Metro

Regional

Mar-11Mar-10

+241

Optus Distribution Landscape

+41

25

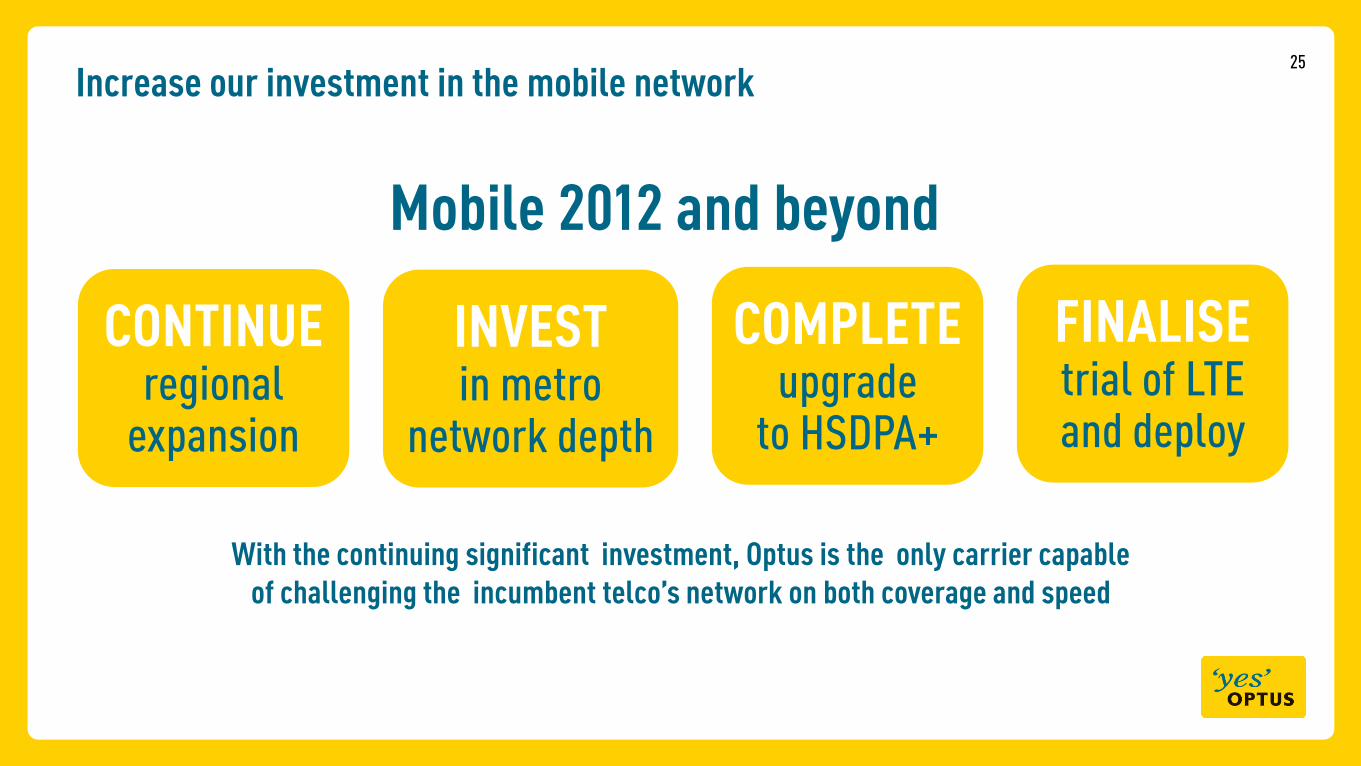

FINALISEtrial of LTE and deploy

COMPLETEupgrade

to HSDPA+

CONTINUEregional

expansion

INVESTin metro

network depth

Mobile 2012 and beyond

Increase our investment in the mobile network

With the continuing significant investment, Optus is the only carrier capable of challenging the incumbent telco’s network on both coverage and speed

26

Video: Network

SingTel Investor Day:Mobile Business Overview

Michael Smith

Managing Director, Consumer

11 July 2011