sleeping giant or mirage? - viridis-iq.de giant or mirage? the potential of pv in and for saudi...

TRANSCRIPT

SLEEPING GIANT OR MIRAGE?The potential of PV in and for Saudi Arabia

Gold SponsorsPartner Silver Sponsors

3

THE POTENTIAL OF PV IN AND FOR SAUDI ARABIA

Summary

The Kingdom of Saudi Arabia plans to introduce a support scheme for renewable energy.

Details of the program are still under discussion but a decision is expected in the short term.

The Gross Domestic Product (GDP) in Saudi Arabia grew by 6.8% in 2012. The observed

economic growth goes hand in hand with an increasing electricity demand. As a result,

an increasing share of oil production is required for domestic electricity generation.

Due to the high solar irradiation PV is a cost competitive alternative in the Kingdom of

Saudi Arabia. Oil and gas powered plants can be utilized flexibly and therefore match the

volatile renewable generation patterns. Solar has a huge offsetting potential: Oil which is

currently used for domestic electricity generation can be sold on the world market instead.

The benefits of the deployment of the renewable program will not be limited to cost ef-

ficient power generation alone. Saudi Arabia will further ramp up a local PV manufactur-

ing industry: The closing of existing gaps in the c-Si PV value chain (i.e. the establishment

of a production for metallurgical silicon and solar cells) will lead to many benefits for the

involved partners. When choosing the right technology path, region-specific character-

istics could be taken into account to reveal attractive niche markets. Four cost categories

determine the viability and competitiveness of a distributed or co-located integrated PV

cluster: local procurement conditions, labor costs, depreciation on fixed assets and long-

term electricity prices which are amongst the lowest in KSA.

Besides creating direct and indirect jobs within the country, the social benefits will also be

increased by spill-over effects on adjacent industries. Long-term educational benefits are

likely to arise in academic fields as well that could help KSA to develop a unique know-

ledge basis and take the leading position within the region.

ةيالمستقبل تايمكاناإل :عوديةسال العربية المملكة في الضوئية أللواحا

االقتراحاتموجز/الاتخاذ ا متوقعكان انالبحث و وال تزال تفاصيل هذا البرنامج قيد برنامج دعم للطاقة المتجددةتخطط المملكة العربية السعودية لطرح

.في القريب العاجلبهذا الصدد قرار

هذا النمو ويقترن .2012في عام % 6.8بنسبة ا نمو قد شهد المحلي اإلجمالي في المملكة العربية السعودية الناتج وكان

إنتاج النفط لتوليد الطاقة من حصة الزيادة أصبح من الضروريونتيجة لذلك، االقتصادي الملحوظ بزيادة الطلب على الكهرباء.

الالزمة لألغراض المنزلية.

تحويليمكن إذ ، تعد األلواح الضوئية بديال منخفض التكلفةالتي تتمتع بها المملكة العربية السعودية الوفيرة شمسيةال لطاقةلونتيجة

صورمع هذه المصانع تتماشى س وبالتالي ،لتعمل بالطاقة الشمسية شديدة النفط والغاز بمرونة التي تستمد طاقتها من مصانعال

ا لتوليد الكهرباء الذي يستخدم حالي للنفط المتوازن دور البديل الطاقة الشمسية تلعبس ،بهذه الصورةو المتقلبة. توليد الطاقة المتجددة

.عوضا عن استخدامه في توليد الطاقةحيث يمكن بيع هذا النفط في السوق العالمية لألغراض المنزلية

بل تسعى المملكة العربية السعودية ، فحسبفضة التكلفة توليد طاقة منخ علىمزايا تفعيل برنامج الطاقة المتجددة ولن تقتصر

(أي c-SI PVأللواح الضوئية الحالية انتاج افي لسد العجز الموجود األلواح الضوئية محلي لتصنيعال االنتاجلتوسيع نطاق

لشركاء المعنيين. فعند اختيار المسار التقني ا على مما سيعود بالنفعوالخاليا الشمسية) المعدنيتأسيس خط إنتاج للسيليكون

. باستيعابها للمنتجتتسم متخصصة الصحيح، يمكن أخذ الخصائص المميزة لمنطقة محددة بعين االعتبار لكشف النقاب عن أسواق

ذات ه المجموعة هذسواء كانت -لواح الضوئية لأل المنتجةمجموعات الإحدى وقابلية تنافسية وتحدد أربع فئات من التكلفة مدى

شروط الشراء المحلية، وتكاليف العمل، واستهالك األصول الثابتة وأسعار واالزدهار: للنمو -واحد موقعمتمركزة في أو جد موزعاتو

تأتي ضمن األسعار األقل على اإلطالق في المملكة العربية السعودية.طويلة األجل التي الالكهرباء

ما ستحظى بهمن خالل رة وغير مباشرة داخل حدود الدولة، ستتزايد المنافع االجتماعيةفضال عن إيجاد فرص عمل مباشو

األمر الذي من شأنه ،. ومن المحتمل أيضا أن ترتفع المزايا التعليمية في المجاالت األكاديميةمن آثار جمة مجاورةالصناعات ال

المنطقة. فيمكانة رائدة وتبوؤمن نوعه مساعدة المملكة العربية السعودية في تطوير أساس معرفي فريد

ةيالمستقبل تايمكاناإل :عوديةسال العربية المملكة في الضوئية أللواحا

االقتراحاتموجز/الاتخاذ ا متوقعكان انالبحث و وال تزال تفاصيل هذا البرنامج قيد برنامج دعم للطاقة المتجددةتخطط المملكة العربية السعودية لطرح

.في القريب العاجلبهذا الصدد قرار

هذا النمو ويقترن .2012في عام % 6.8بنسبة ا نمو قد شهد المحلي اإلجمالي في المملكة العربية السعودية الناتج وكان

إنتاج النفط لتوليد الطاقة من حصة الزيادة أصبح من الضروريونتيجة لذلك، االقتصادي الملحوظ بزيادة الطلب على الكهرباء.

الالزمة لألغراض المنزلية.

تحويليمكن إذ ، تعد األلواح الضوئية بديال منخفض التكلفةالتي تتمتع بها المملكة العربية السعودية الوفيرة شمسيةال لطاقةلونتيجة

صورمع هذه المصانع تتماشى س وبالتالي ،لتعمل بالطاقة الشمسية شديدة النفط والغاز بمرونة التي تستمد طاقتها من مصانعال

ا لتوليد الكهرباء الذي يستخدم حالي للنفط المتوازن دور البديل الطاقة الشمسية تلعبس ،بهذه الصورةو المتقلبة. توليد الطاقة المتجددة

.عوضا عن استخدامه في توليد الطاقةحيث يمكن بيع هذا النفط في السوق العالمية لألغراض المنزلية

بل تسعى المملكة العربية السعودية ، فحسبفضة التكلفة توليد طاقة منخ علىمزايا تفعيل برنامج الطاقة المتجددة ولن تقتصر

(أي c-SI PVأللواح الضوئية الحالية انتاج افي لسد العجز الموجود األلواح الضوئية محلي لتصنيعال االنتاجلتوسيع نطاق

لشركاء المعنيين. فعند اختيار المسار التقني ا على مما سيعود بالنفعوالخاليا الشمسية) المعدنيتأسيس خط إنتاج للسيليكون

. باستيعابها للمنتجتتسم متخصصة الصحيح، يمكن أخذ الخصائص المميزة لمنطقة محددة بعين االعتبار لكشف النقاب عن أسواق

ذات ه المجموعة هذسواء كانت -لواح الضوئية لأل المنتجةمجموعات الإحدى وقابلية تنافسية وتحدد أربع فئات من التكلفة مدى

شروط الشراء المحلية، وتكاليف العمل، واستهالك األصول الثابتة وأسعار واالزدهار: للنمو -واحد موقعمتمركزة في أو جد موزعاتو

تأتي ضمن األسعار األقل على اإلطالق في المملكة العربية السعودية.طويلة األجل التي الالكهرباء

ما ستحظى بهمن خالل رة وغير مباشرة داخل حدود الدولة، ستتزايد المنافع االجتماعيةفضال عن إيجاد فرص عمل مباشو

األمر الذي من شأنه ،. ومن المحتمل أيضا أن ترتفع المزايا التعليمية في المجاالت األكاديميةمن آثار جمة مجاورةالصناعات ال

المنطقة. فيمكانة رائدة وتبوؤمن نوعه مساعدة المملكة العربية السعودية في تطوير أساس معرفي فريد

5

TABLE OF CONTENT

THE POTENTIAL OF PV IN AND FOR SAUDI ARABIA ..............................................3

Summary ...........................................................................................................................3

ENERGY SCENARIOS FOR KSA – NEED FOR RENEWABLE ENERGIES ......................6

Dependency on oil and gas jeopardize economic growth ...................................................6

Solar resources in KSA .......................................................................................................6

PV INSTALLATIONS IN KSA ..................................................................................7

In KSA solar is a cost competitive alternative ......................................................................7

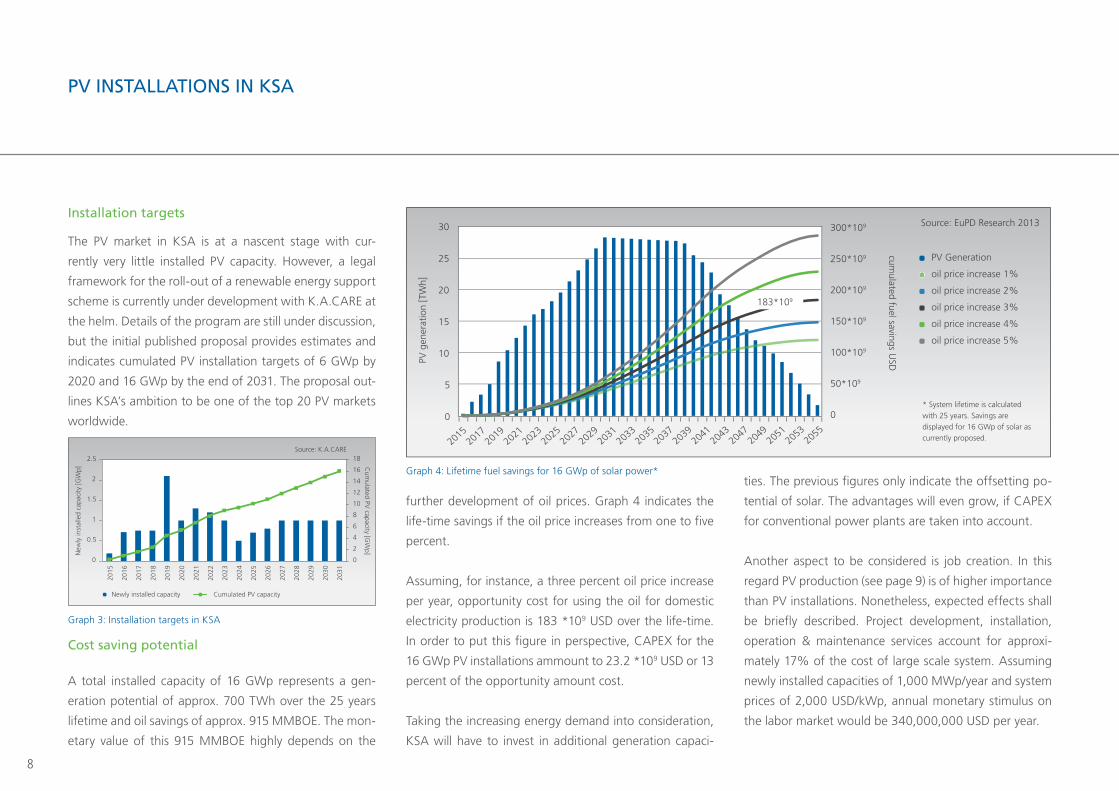

Installation targets .............................................................................................................8

Cost saving potential .........................................................................................................8

LEARNING FROM OTHER MARKETS .....................................................................9

Feed-in-tariffs are a phase out model .................................................................................9

PV in KSA: Different market drivers ....................................................................................9

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE .........................10

Motivation factors for local manufacturing .........................................................................10

Social benefits from the establishment of a c-Si PV manufacturing cluster ..........................11

Spill-over effects from local manufacturing.........................................................................12

Social impacts resulting from a c-Si PV manufacturing cluster .............................................13

Manufacturing along the PV value chain – Developing the Saudi solar industry ..................14

Current trend to local manufacturing .................................................................................16

PV Solar technology roadmap: Adapting to the region .......................................................17

Best practice: Developing a PV industry step by step ...........................................................18

Cost categories for PV manufacturing ................................................................................19

Ecological impacts ..............................................................................................................20

KSA – GREEN LIGHTHOUSE PROJECT FOR THE ENTIRE REGION ............................21

KSA – Technology and production hub in the MENA region ...............................................21

ABOUT THE AUTHORS .........................................................................................22

EuPD Research ...................................................................................................................22

Viridis.iQ GmbH .................................................................................................................22

COOPERATION PARTNER ......................................................................................23

Saudi Arabia Solar Industry Association (SASIA) ..................................................................23

MEYER BURGER TECHNOLOGY LTD .....................................................................25

SMA SOLAR TECHNOLOGY AG ...........................................................................26

SIC PROCESSING (DEUTSCHLAND) GMBH ...........................................................28

SINGULUS TECHNOLOGIES .................................................................................29

AIR LIQUIDE ........................................................................................................30

IMPRINT ...............................................................................................................32

6

ENERGY SCENARIOS FOR KSA – NEED FOR RENEWABLE ENERGIES

Dependency on oil and gas jeopardize economic

growth

With a surface of 2,149,690 sq.km1, the Kingdom of Sau-

di Arabia is the 13th largest country in the world. Accord-

ing to 2013 estimates, the population of the country is ap-

proximately 27,000,0002 and growing at a rate of 1.51%

per year. Since the year 2000, the country has shown a

steady growth in gross domestic product (GDP) figures –

barring a one-time dip in 2009. In 2012, the GDP grew at

the rate of 6.8%. Saudi Arabia is an oil-based economy

with the petroleum industry accounting for 45% of the

GDP.

1 CIA Factbook: https://www.cia.gov/library/publications/the-world-fact-book/geos/sa.html

2 CIA Factbook: https://www.cia.gov/library/publications/the-world-fact-book/geos/sa.html

An increasing energy demand has accompanied the King-

dom’s economic growth and the generation capacities

have been extended. Generation capacities grew by 13%

per year between 1971 and 2009 and 6.2% during the

years from 1999 to 2009. Applying a similar compound

annual growth rate (6.2%) for the upcoming years, 300

TWh would be reached in 2015.3 The peak power de-

mand is expected to nearly triple in the next 20 years.

In 2000, 24% of the country’s oil and gas production

was used to cover domestic needs. In 2010, this share

increased to 35% and estimates suggest that more than

40% of the oil and gas production will be required in

order to cover the domestic demand by 2020. Further-

more, domestic oil consumption is expected to exceed oil

exports by the year 2025. This trend towards domestic

consumption of oil jeopardizes economic growth.

In order to counter this trend, Saudi Arabia’s Alternative

Energy Program aims to:

• CONTRIBUTE to a sustainable future for Saudi Arabia

• PRESERVE non-renewable fossil fuel resources

• SAFEGUARD KSA‘s international energy leadership

• ENSURE long-term global energy market stability

• TRANSFORM KSA into the Kingdom of Sustainable Energy

3 KSA does not import or export electricity to a significant amount and therefore electricity generation almost equals to electricity consumption

Solar resources in KSA

Different generation technologies do have specific (dis)

advantages, such as external cost or base load capabil-

ity. These (dis)advantages

are to be taken into ac-

count when replacing one

technology with another.

However, in order to gain

clarity of this aspect, an

important question to ask

is: How much PV energy

would be required in order

to cover the entire electri-

cal demand in KSA?

Depending on the precise location a ground mounted one

MWp PV power plant will produce an average of 1,800

MWh/year. Thus, in order to produce 300 TWh/year,

167 GWp of installed PV capacity would be required. On

average, such a one MWp system requires 0.014 sq.km

of land area and therefore the installation of 167 GWp

would require an area of 2,300 sq.km or 0.11% of the

Kingdom’s territory.

Figure 1: Solar potential in KSA

Graph 1: Electricity generation capacities in Saudi Arabia

Source: IEA

0

50

100

150

200

250

300

[TWh]

13%

6.2%

Year

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

e

2012

e

2014

e

Required PV area in order to porduce 300,000 GWh / year

Saudi Arabia

Source: EuPD Research 2013

7

PV INSTALLATIONS IN KSA

Graph 2: LCOE of PV depending on PV system price for three different irradiation levels in KSA

In KSA solar is a cost competitive alternative

Since 2006 several European countries have introduced

feed-in-tariffs (FiT) in order to stimulate PV demand. FiTs

used to be significantly higher than electricity prices. The

intersection point between electricity prices and the cost

per kWh of solar generated electricity was considered as

benchmark for competitiveness. Due to falling system

prices this intersection point – so called grid parity – has

been reached in several of the European markets but this

did not lead to a booming demand.

In order to assess the true competitiveness of solar the

benchmark must not be the electricity price, but the gen-

eration cost of other power plants. In order to analyze the

cost competitiveness of PV, the levelized cost of electricity

(LCOE) of PV shall be compared to the fuel cost (rated at

market price of 107 USD) which is required in order to

produce one kWh of electricity from oil. Capital equip-

ment costs of a conventional power plant are not consid-

ered in the calculation.

On average 1.3 barrels of oil are required to generate

one MWh of electricity – 1.3 barrels worth 139 USD that

cannot be sold on the world market. Thus, the opportu-

nity cost for the usage of oil for electricity production is

139 USD per MWh, respectively 0.139 USD per kWh. As

mentioned, this cost does not consider any CAPEX for the

power plant but just fuel costs rated at market price.

Graph 2 compares LCOE4 of PV for three different loca-

tions in KSA with the 0.139 USD fuel cost. In high yield

regions PV is a competitive source if a system price below

2,475 USD/kWp is achieved. At average irradiation levels

a system price as low as 1,750 USD/kWp is required. From

today’s point of view 1,750 USD/kWp is ambitious in a

non-mature market like KSA and some learning curve ef-

fects are required in order to achieve this price. Against

the background of system prices below 1,300 USD in

more mature PV markets the benchmark is definitely

achievable. It should be considered that this calculation

does not include external cost which are much lower

in the case of PV compared to conventional generation

sources.

4 Discount rate = 8% | degradation = 0,25% | OPEX = 1% of initial invest-ment | Inflation = 1.5% | system runtime = 25 years

Source: EuPD Research 2013

1,0

00

1,1

00

1,2

00

1,3

00

1,4

00

1,5

00

1,6

00

1,7

00

1,8

00

1,9

00

2,0

00

2,1

00

2,2

00

2,3

00

2,4

00

2,5

00

LCO

E / f

uel c

ost [

USD

/kW

h]

PV System Price [USD/kWp]

PV yield LCOE low irradiation (1250 kWh/kWp)

PV yield LCOE average (1550 kWh/kWp)

PV yield LCOE high irradiation(2200 kWh/kWp)

Fuel cost for electricity generation per kWh

< 1200 1600 2000 2400 2800 > kWh/m²

0

0.05

0.10

0.15

0.20

0.25

0.30

© 2010-2013 GeoModel Solar

Project Cost +

LCOE =

-

Initial KWh X (1 - System Degradation rate)n

(1 + DR)n

n=1∑N

n=1∑N

RV

(1 + DR)n

AO

(1 + DR)n

1,7501,400 2,475

8

PV INSTALLATIONS IN KSA

Installation targets

The PV market in KSA is at a nascent stage with cur-

rently very little installed PV capacity. However, a legal

framework for the roll-out of a renewable energy support

scheme is currently under development with K.A.CARE at

the helm. Details of the program are still under discussion,

but the initial published proposal provides estimates and

indicates cumulated PV installation targets of 6 GWp by

2020 and 16 GWp by the end of 2031. The proposal out-

lines KSA’s ambition to be one of the top 20 PV markets

worldwide.

Cost saving potential

A total installed capacity of 16 GWp represents a gen-

eration potential of approx. 700 TWh over the 25 years

lifetime and oil savings of approx. 915 MMBOE. The mon-

etary value of this 915 MMBOE highly depends on the

further development of oil prices. Graph 4 indicates the

life-time savings if the oil price increases from one to five

percent.

Assuming, for instance, a three percent oil price increase

per year, opportunity cost for using the oil for domestic

electricity production is 183 *109 USD over the life-time.

In order to put this figure in perspective, CAPEX for the

16 GWp PV installations ammount to 23.2 *109 USD or 13

percent of the opportunity amount cost.

Taking the increasing energy demand into consideration,

KSA will have to invest in additional generation capaci-

ties. The previous figures only indicate the offsetting po-

tential of solar. The advantages will even grow, if CAPEX

for conventional power plants are taken into account.

Another aspect to be considered is job creation. In this

regard PV production (see page 9) is of higher importance

than PV installations. Nonetheless, expected effects shall

be briefly described. Project development, installation,

operation & maintenance services account for approxi-

mately 17% of the cost of large scale system. Assuming

newly installed capacities of 1,000 MWp/year and system

prices of 2,000 USD/kWp, annual monetary stimulus on

the labor market would be 340,000,000 USD per year.

Source: K.A.CARE

Newly installed capacity

0

0.5

1

1.5

2

2.5

0

2

4

6

8

10

12

14

16

18

New

ly in

stal

led

capa

city

[GW

p]

Cum

ulated PV capacity [G

Wp]

Cumulated PV capacity

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

Source: EuPD Research 2013

PV Generation

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2047

2049

2051

2053

2055

0

5

10

15

20

25

30cum

ulated fuel savings USDPV

gen

erat

ion

[TW

h]

* System lifetime is calculated with 25 years. Savings are displayed for 16 GWp of solar as currently proposed.

oil price increase 1%

oil price increase 2%

oil price increase 3%

oil price increase 4%

oil price increase 5%

0

50*109

100*109

150*109

200*109

250*109

300*109

183*109

Graph 3: Installation targets in KSA

Graph 4: Lifetime fuel savings for 16 GWp of solar power*

9

LEARNING FROM OTHER MARKETS

Feed-in-tariffs are a phase out model

Until now global PV markets have been majorly driven

by feed-in-tariffs (FiTs). In 2012, Europe contributed to

57% of the global PV market. Major countries in Europe

such as Germany, Italy, France, etc. led the overall growth

of the PV market and some countries, for instance Spain

and Czech Republic underwent a boom and bust cycle.

The installed capacities in Spain and Czech Republic sky-

rocketed due to the lucrative FiTs which led to handsome

return on investment. However, due to the faster than

envisioned growth the incentive schemes were scrapped

leading to a total collapse of PV in these markets.

Furthermore, the consistent strong year-on-year growth

in major PV markets such as Germany and Italy has also

led to an overall reduction of the generous feed-in-tariffs

resulting in a slowdown in newly installed capacities in

these markets.

When FiTs were first introduced, it was the right measure

to stimulate the market and necessary in order to real-

ize cost reductions, however, new models now need to

replace the FiT mechanism to continue with sustainable

development. There is no doubt that FiT schemes are a

phase-out model and (former) FiT markets will have to

develop alternative long-term models in order to keep the

markets alive.

PV in KSA: Different market drivers

For KSA market drivers are different compared to Eu-

ropean marketes and these drivers will also work in the

long-run:

• Whereas most European markets target to replace ex-

isting conventional power plants by renewables, ener-

gy demand in KSA is increasing and there is a demand

for new generation facilities.

• The Kingdom will not be a feed-in-tariff market but an

offsetting market.

• In most European countries electricity generation is

determined by nuclear and coal and thus non-flexible

generation facilities. Oil and gas powered plants can be

utilized flexibly and therefore match the volatile renew-

able generation patterns.

Due to the different market drivers, the development of

the Saudi Arabian market is expected to be different. It is

rather unlikely that the market unfolds the full potential

within a short time. In KSA we will see a slower but steady

growth with an almost unlimited long-term potential.

Source: EuPD Research 2013

[MWp]

Germany Italy Spain CzechRepublic

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2006 2007 2008 2009 2010 2011 2012 2013e

Graph 5: Newly installed capacities in selected markets

10

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Motivation factors for local manufacturing

As PV is about to become the cheapest form of energy

generation in the foreseeable future, KSA – like many oth-

er regions in the world - has started to explore opportuni-

ties and risks associated with industrial PV manufactur-

ing. Apart from shareholder-value oriented targets, many

projects have secondary objectives that follow from direct

or indirect government involvement. The most important

consideration within the set of secondary objectives is

usually the benefit for people or communities located

near the sites, where production facilities will eventually

be situated. These objectives are usually defined by the

project owner in collaboration with government agencies

and if required with the support of external PV experts.

Figure 2 shows potential goals that may play a role in the

decision to pursue an industrial PV project.

Diversificationand broadening

of nationalindustrial profilesegmentation

Jobcreation and

skill-setbuildingEnergy

security andbroadening

of generationprofile

Conservation ofnatural resources,

e.g. depletinghydro-carbon

in KSA

Compliancewith

internationalCO2 emission

targets

Leverageof regionalresources

Development of a regional PV excellence

cluster

Regionaltechnology

leaderpotential

Competitiveadvantages,

e.g. lowelectricity price

Increase in depth ofvertical integrationand value creation

incl. entrepreneurialbusiness opportunities

for domesticsuppliers

Source: Viridis.iQ GmbH 2013

Figure 2: Potential goals when setting-up a local PV manufacturing industry

11

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Social benefits from the establishment of a c-Si

PV manufacturing cluster

Social benefits from the establishment of an integrated

c-Si PV cluster can be differentiated in direct and indirect

or short- and medium-term effects. Furthermore, with the

location of an mg-Si smelter and a c-Si cell-plant on the

grounds of the Arabian Peninsula, KSA would close exist-

ing gaps in its c-Si manufacturing project portfolio. Ad-

vantages from integration are discussed on page 12/13.

Direct social benefits will be realized in the communities

adjacent to the eventual sites or single agglomerations.

Even though labor intensity is lower in the capital intensive

silicon part of the value chain, the impact on regional job

quotas should not be underestimated, especially if spill-

over effects to supplier and service segments are taken

into consideration. For example, in the case that suitable

quartz reserves are available for silicon production, a sus-

tainable explorative mining industry could be established

for the region. Additional political objectives relating to

industrial diversification, trade, environmental and social

aspects could be tackled by an intelligent, prudent and

sensible site selection. Taking multiple and interrelated

economic objectives on a national level into consideration

increases project complexity significantly, while the list of

involved stakeholders expands.

Source: Viridis.iQ GmbH 2013

MetallurgicalSilicon

Polysilicon Ingot/Wafer Cell Module

Prod

uctio

n la

bor

per

GW

of p

rodu

ctio

n ca

paci

ty

0

200

400

600

800

1000

1200

spread

Graph 6: Needed production labor per GW of production capacity

12

Spill-over effects from local manufacturing

Longer-term educational benefits are likely to arise in

the academic fields of mechanical engineering, chemical

engineering, semiconductor physics and manufacturing

operations. Furthermore, an increase in demand for tech-

nically skilled operators will most probably have positive

and lasting effects on the statistics of highly skilled labor

in KSA. Figure 3 illustrates the relationship between short-

term direct effects and medium-term indirect spill-over

effects: As outlined above, effects from the settlement of

a fully integrated, industrial silicon-solar cluster can be dif-

ferentiated in direct and indirect effects as well as short-

to medium-term consequences. The first wave of visible

effects will be felt within the local communities where the

parts of or the complete cluster will eventually be located.

Apart from the creation of construction jobs, infrastruc-

tural projects are likely to have a positive impact on other

segments of the economy, which do not necessarily stand

in a direct relation to the industrial project itself.

In addition, medium- to longer-term effects on the

growth rate for the economy are likely to result from an

increase in the relative amount of skilled labor within the

workforce of the respective community but also within

the overall skill-set composition of the labor force in the

overall economy. Further, possible collaborations with lo-

cal universities could help to create a globally renowned

cluster for industrial scale c-Si based PV production in

KSA.

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Source: Viridis.iQ GmbH 2013

Community benefits, per capitaincome increase

Utilization of localquartz

reservoirs

Lower dependencyon imports

Integratedc-Si PVcluster

Opportunisticprocurement

strategy

Educationalbenefits

(academics, skilled labor)

Cluster benefits:

e.g. process gases

Academic knowledge

cluster

Higher taxes

Spill-over on

adjacent industries

...

Figure 3: Spill-over effects from a domestic PV manufacturing cluster

13

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Social impacts resulting from a c-Si PV manufac-

turing cluster

If potential sites are chosen in accordance to pre-deter-

mined selection criteria that also take other economic de-

velopment targets into account, multiple goals could be

served by a large industrial PV development program. For

example, some regions might lack infrastructural connec-

tions which put them into a disadvantage to better de-

veloped communities. If all other factors are comparable

to an alternative site that is situated in a region with a

more advanced infrastructure, it might be advantageous

to consider the site with the mediocre infrastructure in

order to set impulses for growth.

Another set of direct benefits might result from an in-

crease in the average per capita income, sustainable re-

ductions in unemployment rates, increases in community

and state taxes as well as consumption levels.

Secondary effects might arise from spill-over effects on

other areas of the local economy (local trade, craftsmen,

service providers, etc.) and the targeted development of

adjacent fields, e.g. from increasing the proportion of

supplies sourced from local companies. Another advan-

tage comes from the possibility to tap existing industrial

gas supply of the petro-chemical industry. Further sec-

ondary economic benefits could be realized through the

exploitation of possible local quartz reserves.

Short-term Medium-term

Direct

• Creation of jobs related to PV production

• Know-how transfer on silicon processing and semiconductor physics

• Creation of construction jobs with industrial scope

• Creation of construction jobs for civil engi-neering (infrastructure, utility connection)

• Creation of a global center of competency for c-Si based production in collaboration with universities

• Increase in the ratio of skilled- to unskilled labor within the national labor force

• Increase in per capita income with increased consumption

• Increase in local- and state taxes

Indirect

• Short-term indirect effects will depend on the timing of parallel initiatives (e.g. potential development of explorative industries)

• Increase of local service providers within respective communities

• Example: mg-Si know-how can easily be leveraged to access basic chemical and alu-minum industry

• Increase in mobility and educational levels likely to have positive impacts in non-related fields of the economy

• Increase of local supply of materials with lasting effects on adjacent industries

• Increased usage of solar energy frees-up fossil resources for export

Table 1: Social impact matrix

14

Manufacturing along the PV value chain – Devel-

oping the Saudi solar industry

The announcement by Polysilicon Technology Co., Ltd. in

February of 2011 to build a 3,000mt production facility

made clear that KSA plans to supply the PV power plants

set forth in the ambitious K.A.CARE targets with locally

manufactured products. This became even more evident

after Green Gulf released plans to erect a 750MW wafer

and 200MW module plant in June 2013. A major stra-

tegic motivation for the establishment of an integrated

silicon-based production infrastructure within the realm

of KSA could be to close the gap between existing natural

resources in the form of quartz minerals (SiO2) and mod-

ule production. If implemented, the KSA would achieve

a depth of integration within the c-Si based value chain

that is hardly matched by any single other region, globally.

One obvious advantage from a fully integrated c-Si manu-

facturing approach is the reduction of uncertainty result-

ing from long-term sourcing decisions, e.g. the relative

extent of feedstock sourced through long-term contracts

versus the proportion sourced in spot markets. Although,

each individual investment within the integrated cluster

should earn an adequate risk-adjusted return on capital

over the project lifetime, temporal pricing induced market

imbalances can better be absorbed over a fully integrated

manufacturing cluster, as currently witnessed in the pho-

tovoltaic market. The figure on the next page gives an

indication as to the relative resistance of integrated vs.

specialized business models in the PV downstream.

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Polysilicon Technology

Company (PTC)

IDEA

Saudi Arabia’s position in the PV value chain

characteristics

Notpresent

Mg Silicon Poly Si Ingot Wafer Cell Module

similar to steel industry

chemical factory like, petrochemical

environment; large electricity

needs

Green Gulf

Polysilicon Technology Company (PTC)

Notpresent

Green Gulf

Desert Technologies

thermal and mechanical processing; energy- and labor intensive

semiconductor manufacturing like;

technology important

for solar module power output

glass processing like; large number of operators required

Source: Viridis.iQ GmbH 2013

Figure 4: Photovoltaic value chain: KSA´s position and characteristics

15

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

This strategic position over the complete value chain gives

integrated manufacturers a superior position to follow an

opportunistic sourcing approach in times of severe mar-

ket imbalances on different steps of the value chain. This

means if a certain intermediate product is priced below

the marginal costs, a temporal halt of production and ex-

ternal sourcing approach could give an integrated manu-

facturer a competitive advantage. In addition, in times

where prices for photovoltaic products exhibit a high vol-

atility a more stabilized pricing policy over the complete

value chain of an integrated manufacturer can alleviate

temporal uncertainties that otherwise could arise and dis-

tract the organization.

The last strategic aspect that should be considered is that

the increased depth of knowledge and control over the

full value chain within a PV cluster can shorten innova-

tion cycles. For example, by aligning engineered and op-

timized silicon feedstock with tighter specifications on

predetermined key parameters an optimization of inter-

mediate or final products, e.g. higher efficiency cells with

lower standard deviation, can be achieved.

The benefits of co-located production integration along

the supply chain can be distinguished in the categories

displayed in table 2.

InfrastructureShared facilities (power, water, etc.), roads, substations, buildings, construction costs, administration costs, etc.

LogisticsLower cost packaging requirements, shorter distances, less breakage, opportunities for bulk transit, less fees to brokers, insurances, transportation costs, etc.

Process OptimizationCustomization of one step in the supply chain specifically to the next one (at the co-located factory), consolidated quality control, alignment of process steps, in-ter-process communication, shorter innovation cycles, etc.

Financial and Economic Lower working capital, streamlined process flows, faster time-to-market, etc.

Recycling and byproduct synergies

Reuse and optimization of by-products between process steps, synergies in common on site production requirements (gases, acids, etc.), etc.

Q2

´05

Q4

´05

-20%

-10%

0%

10%

20%

30%

40%

Q2

´06

Q4

´06

Q2

´07

Q4

´07

Q2

´08

Q4

´08

Q2

´09

Q4

´09

Q2

´10

Q4

´10

Q2

´11

Q4

´11

Q2

´12

Q4

´12

Integrated wafer-to-module

capa

city

wei

ghte

d gr

oss

mar

gin

Specialized / cell

Source: Viridis.iQ GmbH 2013

Table 2: Agglomeration benefitsGraph 7: Downstream gross margin of specialized & integrated manufacturers

16

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Current trend to local manufacturing

In the last couple of months many announcements were

made regarding set-up of production sites in not yet es-

tablished PV production markets. The reasons are mani-

fold:

• Production (of modules, sometimes also of cells) in

close proximity to installation markets due to relative

increase of transportation cost and low price of com-

modity product.

• Chinese cost advantages decrease with increasing la-

bor cost in China.

• Depending on the PV value chain step benefitting from

ideal local conditions and competitive advantages.

• Government-driven industry settlement with establish-

ment of local supply chain.

• Established producers diversify to fully tap market po-

tential.

• Strategies to avoid trade barriers.

• Adaptation to local conditions (“desert module”, “salt-

water module”).

Examples:

• In July 2013 Samsung Renewable Energy reached a

partnership agreement with Canadian Solar to open a

new module manufacturing facility in Ontario.

• The president of the local energy agency announced

at the beginning of 2013 that the Argentinan province

of San Juan plans a fully-integrated PV production with

70MW equipped by German turnkey provider Schmid

to be finalized by the end of 2014.

• CSUN started their cell and module production in Tur-

key in 2013 (100 resp. 150MW). It was announced that

parts of the module production equipment would be

transfered from Shanghai to Turkey.

• Two months ago Comtec Solar started construction of

a 1GW N-type mono wafer plant in Malaysia that is

suppost to be completed by the end of 2013.

Source: Viridis.iQ GmbH 2013

Indu

stria

l Ele

ctric

ity P

rices

(US$

/MW

h)

KSA

Uni

ted

Stat

es

Braz

il

Fra

nce

Kiz

ad

Can

ada

Aus

tral

ia

Spai

n

Om

an

Thai

land

Chi

na

Sout

h A

fric

a

Ger

man

y

Nor

way

80

20

30

40

50

60

70

Graph 8: KSA‘s competitive edge: electricity price

17

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

PV Solar technology roadmap: Adapting to the

region

• The vast majority of solar panels installed utilize c-Si

multi- & mono-wafers.

• The proportion of “standard” c-Si based technologies

increased even further throughout the current market

correction phase (2011-2013).

• The technology selection can also reveal attractive

niches. However, from a risk-reward perspective, a

balance must be found between advantages of main-

stream (established supply chain, economy of scale,

low risk) and an innovative path opting for USP, but

taking higher risk.

• The specific needs of the Arabian peninsula with re-

spect to extreme temperatures and sand storms re-

quire the adaption of the solar module designs. The

hereof resulting emerging domestic market provides

promising perspectives for local PV producers.

Source: Viridis.iQ GmbH 2013

a-Si/uc-Si5-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Prod

uctio

n vo

lum

e 20

12

CIGS + CdTe10-13%

c-Si mono/multi13-17%

High-Efficiency-Segment17-21%

total area efficiency

3%7%

86%

3%

One reasonable strategy: Establish leadingposition within the high volume-segmentof “standard“ c-Si module producers, while leaving enough headroom for further developments, e.g. passivated rearside, long-lifetime-modules adapted tothe region.The technology roadmap needs to be defined with tight eye side on Cost of Ownership (CoO).

Graph 9: Global technology segmentation

18

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Best practice: Developing a PV industry step by

step

The previous pages have demonstrated that the complex-

ity of an integrated PV project is a consequence of the

diverse nature of involved industries that reaches from

heavy metallurgy, to chemical refining, from material

processing to high-tech high-volume material processing

and assembling under clean room environment. Further

complexity can be added by different stakeholders with

varying objectives and scopes. As such, a rigorous plan-

ning, monitoring and managing process by an experi-

enced interdisciplinary team of industry experts becomes

a necessary side-condition for a successful project imple-

mentation over the various project planning, realization

and operation stages. Table 3 provides an overview on

general project steps which are typically performed.

Project White Paper A conceptual overview of the project at the highest level with a description of the motivation of the project. This can be used to motivate govern-ments and policy makers to understand the project and its importance.

Feasibility Study

A technical, economic, commercial and strategic factor review for the project. Includes technology overviews, supply chain details, cost modeling, site requirements review, mass flows, and other technical information. Additionally, it includes detailed market information, forecasts, fundamentals, critical requirements for market entry and other strategic concepts and plans. The outcome of the study is not decided before the study is complete and the report should be a critical analysis of the project that can withstand investor scrutiny.

Pre-engineering Process descriptions, basic equipment, estimated space requirements, shift schedules, output estimates, process and mass flows, etc.

Basic Engineering Building and equipment requirements, bill of materials, facilities and utilities matrix, block layouts, staff requirements, recycling potential, process design, quality control plan, FMEA, production risk assessment, safety, etc.

Permitting Site, environmental, personnel, etc.

Logistics and Supply Audits Logistics planning, supplier qualification/audits, raw material specification designs, procurement strategy.

Environmental Study Waste stream and off gas effects, disposal and landfill planning, establishment of limits, monitoring, etc.

Investor Acquisition Business case, cost models, financial models, project evaluation, etc.

Project Planning Organization of equipment, utilities, site requirements, earthworks, infrastructure and buildings, installation and construction coordination and management, usually requires an experienced EPC contractor.

Project Execution Training, scheduling, cost controlling, claims, move in planning, coordination, document management, reporting, etc.

Commissioning and Start Up Equipment commissioning, start-up sequences, acceptance process, process optimization, etc.

Market Entry Marketing plan, strategic roadmap, technology planning, R&D, etc.

Table 3: Description of industrial project realization stages

19

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Cost categories for PV manufacturing

The economic viability and competitiveness of a distribut-

ed or co-located integrated PV cluster is ultimately deter-

mined by four broad cost categories: local procurement

conditions, long-term electricity prices, labor costs and

depreciation on fixed assets. A rigorous benchmarking of

capital requirements to international PV plants in combi-

nation with local labor and electricity rates can already

lead to a reasonable estimate of production costs before

a costly procurement study is initiated, e.g. at an early

planning stage.

The capital intensity of the individual production facilities

of an integrated manufacturing cluster for c-Si based PV

modules declines from the up- to the downstream, mean-

ing that poly-Si sites typically have the highest-, while

module assembling sites exhibit the lowest investment

need expressed in units of output.

A major reason for this is the extended engineering and

project management complexity associated with the ma-

terial purification and crystal formation steps of the c-Si

PV value chain. In turn, engineering costs are influenced

to a great extent from numerous location specific factors,

such as experience and availability of local construction

firms. In the poly-Si segment the relative proportion of

unit investment costs attributable to EPC and technology

transfer typically ranges between 40-60%, an invest-

ment coefficient of 110 US$/kg is in accordance with the

average capital intensity deduced from an industry peer

group of new entrants to this segment.

The EPC related portion decreases in the downstream as

building and infrastructure related complexities decline.

The relation of infrastructure, facility & building induced

spending to total invest for the structural complex in-

cluding equipment are 20-30% for the ingot & wafer-,

15-25% for the cell- and 30-40% for the module plant.

The actual relative capital distribution within the fixed as-

set basis will depend on nameplate capacities, selected

technologies, state of development of available sites,

civil-engineering & environmental regulations as well as

industrial focus of locally available engineering and con-

struction partners.

A benchmarking process of actual project announce-

ments reveals that the correlation between manufactur-

ing capacity and unit investment costs for the individual

production steps is not particularly high. This indicates

that most of the fixed capital investments depends on

technology choice, supplier selection, negotiation efforts

(that -to a great extent- are a function of the design &

facilitation of bids) as well as the market environment and

location specific factors. An exception constitutes the ca-

pacity expansions derived through process optimizations,

e.g. debottlenecking carried out by established poly-Si

manufacturers. Here we see a strong correlation between

capital spend and capacity.

A technology selection pre-determines the short-list of

globally available equipment manufacturers. Hence, tech-

nology selection is a critical path as it narrows down the

capital equipment supplier choice, confines the technol-

ogy roadmap and thereby ultimately impacts the selec-

tion of addressable markets for the end-product, e.g. the

c-Si module. Last but not least this decision will have a

tremendous impact on the unit production costs, as capi-

tal related expenses in the form of depreciation charges

contribute up to 20% to total unit costs.

mg-Si 5.2-7.2 US$/kg

poly-Si 79-153.8 US$/kg

ingot-wafering 0.30-0.47 US$/Wp

cell 0.16-0.30 US$/Wp

module 0.09-0.16 US$/Wp

Table 4: Bandwidth of relative capital investment needs

20

DOMESTIC PV MANUFACTURING – GENERATING LOCAL VALUE

Ecological impacts

The technology selection also determines the list of criti-

cal or hazardous materials that need to be treated with

specific care and disposed of in accordance to local and

international hazardous waste treatment regulations.

The list of chemicals dealt within a PV facility is to be con-

sidered in conjunction with the technology choice. The

goal is usually to increase the recycling quota in order to

minimize or even eliminate the effective emissions. Haz-

ardous chemicals that need to be considered in an envi-

ronmental analysis are for example:

• TCS - Trichlorsilane

• STC - Tetrachlorosilane

• HCl - Hydrogen-chloride (tt forms hydrochloric acid

which can easily be neutralized by using lime.)

• HF - Hydrofluoric acids (can be turned into harmless

fluorspar by lime treatment.)

• Coal – if it is used in the metallurgical plant as reduc-

tion source (Carbon)

• Silane gases and other exhausts (they are discarded

through a scrubber/burner turning them into harmless

compounds.)

All substances are well known and if applying state-of-

the-art handling they do not cause health issues. No carci-

nogenic substance will be used. For example in the met-

allurgical silicon step, the off gas from the mgSi plant will

be cleaned and treated in the baghouse system where it

is in principle possible to burn the CO (carbon monoxide)

and generate energy for local consumption. In addition,

particle emission from the furnace can be used in the

concrete manufacturing. Similar recycling and byproduct

strategies must be developed based on location specific

environmental regulations.

Ultimately, waste products that cannot be fed back into

the process flow need to be disposed of at a hazardous

waste dump. Potential sites need to be earmarked by the

awarding authority.

Additional considerations that need to be taken into ac-

count are:

• Control and protection of fresh water resources

• Conservation of identified production sites

• Air emissions and gas treatment

• Generation of a systematic process of solid waste man-

agement

• Development of a Green Concept for the local and re-

gional communities

• Energy generation by gas and biomass

• Conservation of ecosystem (biodiversity)

21

KSA – GREEN LIGHTHOUSE PROJECT FOR THE ENTIRE REGION

KSA – Technology and production hub in the

MENA region

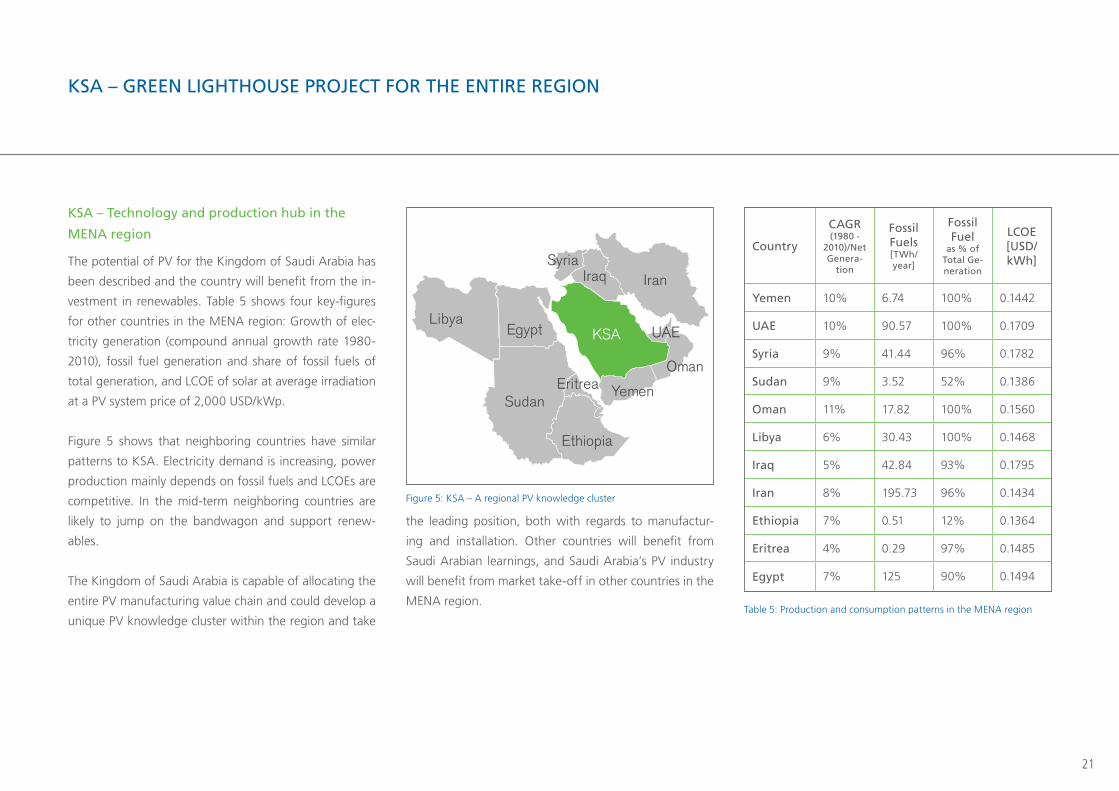

The potential of PV for the Kingdom of Saudi Arabia has

been described and the country will benefit from the in-

vestment in renewables. Table 5 shows four key-figures

for other countries in the MENA region: Growth of elec-

tricity generation (compound annual growth rate 1980-

2010), fossil fuel generation and share of fossil fuels of

total generation, and LCOE of solar at average irradiation

at a PV system price of 2,000 USD/kWp.

Figure 5 shows that neighboring countries have similar

patterns to KSA. Electricity demand is increasing, power

production mainly depends on fossil fuels and LCOEs are

competitive. In the mid-term neighboring countries are

likely to jump on the bandwagon and support renew-

ables.

The Kingdom of Saudi Arabia is capable of allocating the

entire PV manufacturing value chain and could develop a

unique PV knowledge cluster within the region and take

the leading position, both with regards to manufactur-

ing and installation. Other countries will benefit from

Saudi Arabian learnings, and Saudi Arabia’s PV industry

will benefit from market take-off in other countries in the

MENA region.

Iran

Oman

Yemen

UAEKSA

IraqSyria

Egypt

Sudan

Ethiopia

Eritrea

Libya

Country

CAGR (1980 -

2010)/Net Genera-

tion

Fossil Fuels [TWh/ year]

Fossil Fuel

as % of Total Ge-neration

LCOE [USD/kWh]

Yemen 10% 6.74 100% 0.1442

UAE 10% 90.57 100% 0.1709

Syria 9% 41.44 96% 0.1782

Sudan 9% 3.52 52% 0.1386

Oman 11% 17.82 100% 0.1560

Libya 6% 30.43 100% 0.1468

Iraq 5% 42.84 93% 0.1795

Iran 8% 195.73 96% 0.1434

Ethiopia 7% 0.51 12% 0.1364

Eritrea 4% 0.29 97% 0.1485

Egypt 7% 125 90% 0.1494

Figure 5: KSA – A regional PV knowledge cluster

Table 5: Production and consumption patterns in the MENA region

22

ABOUT THE AUTHORS

EuPD Research pursues a strategy that values providing customers with integrated solu-

tions based on first-rate market intelligence, consulting know-how, communications ex-

cellence and implemented go-to market strategies. We have completed more than 2,000

exclusive projects for multinationals, global associations and governments. Our global

reach allows us to serve customers in their target markets and deliver solutions custom-

ized to what they need and where they are.

We pride ourselves on compiling data specific to your requirements, applying rigorous

methodologies and critical thinking as well as deep and diverse industry insight to deliver

products that add measureable value to your bottom line, and, embody the principles of

sustainability.

Founded in 2000 and part of the Hoehner Research and Consulting Group, our interna-

tional presence enables us to analyze markets, industries and stakeholders closely and

accurately as well as providing proximity to our customers.

Our customers come from a multitude of backgrounds including CleanTech with particu-

lar focus on renewable and smart energy as well as enterprises and public institutions that

strive for sustainable excellence and practice sustainable management.

Our commitment and dedication to securing the role of renewable energies in the energy

mix of the future has shown us that success goes beyond the generation of green profit.

Investing in the well-being of employees and promoting sustainable business practices

sees the transfer of the strategies we implement to better our environment to the way we

run companies and conduct business.

Viridis.iQ GmbH is an independent German technology and engineering consulting firm

with unique technical expertise on every step of the PV value chain (from metallurgical

silicon to systems) that is grounded in hands-on industrial experience with a focus on inte-

gration value and innovative technologies. Our interdisciplinary specialists have extensive

experience in providing feasibility and detailed technical studies on all industrial phases of

PV manufacturing along with a strong foundation in financial and economic modeling,

costs of ownership, environmental impact, market entry advice, competitive strategies and

industrial development planning.

• Strategic: roadmapping, critical path analysis, market entry, competitive advantage and

process intelligence, value-oriented business management, project owner representation.

• Technical: process flows, mass balance, material specifications, equipment, technol-

ogy, layouts, benchmarking analysis and value stream mapping.

• Market: risks and opportunities, player analysis, consolidation effects and tier dynamics.

• Academy: Lean Six Sigma and technical trainings, education, know-how transfer,

games and dynamics applied for business.

• Financial: project evaluation, scenario-driven multi-layer sensitivity analysis, ROI, IRR,

business planning, costs of ownership, TCO and other economic modeling.

• Logistics/ trade: import/export, trade, supply chain analysis, cost simulations and sup-

pliers evaluation.

• Environmental: waste streams, treatment/ handling, recycling options, local laws and

regulation analysis.

• Human resources: skills, labor requirements, organizational structure and O&M evaluation.

EuPD Research Viridis.iQ GmbH

23

COOPERATION PARTNER

The Saudi Arabia Solar Industry Association (SASIA) is a non profit, non governmental as-

sociation which aims to promote solar power in the Saudi Arabia and across the Middle

East. The organization aims to: Facilitate business opportunities for its members through

face to face meetings, workshops and lectures; Expand the use of all solar technologies at

national and regional level; Offer assistance to international solar companies establishing

or contemplating the establishment; Publish white papers and research reports that aim to

assist policy-makers on matters related to solar policies, standards, and product certifica-

tions.

Saudi Arabia Solar Industry Association (SASIA)

24

PASSIONATE ABOUT PV

COMMITTED TO SYSTEMS AND PROCESSESProcesses and systems from the Meyer Burger Group play a vital role in increasing overall performance and effi ciency throughout the photovoltaic value chain. We enhance the crucial key factors for all manufacturing processes - for optimum yield, lowest possible costs and maximum availability.

Meyer Burger Technology Ltdwww.meyerburger.com

25

Passionate about PV

We are a comprehensive system supplier in photovoltaics,

in the semiconductor and optoelectronics industries, as well

as in other industrial sectors utilising semiconductor materi-

als. In our core business of photovoltaics, we are among

the pioneers of the industry. We use our expert know-how

to constantly advance the industrialisation of trendsetting,

cost-effective production processes. In the field of building

technology, we set global standards for building-integrated

solar systems for the efficient and environmentally-friendly

production of electricity from sunlight.

Core expertise along the entire PV value chain

Our spectrum of systems, production equipment and ser-

vices along the photovoltaic value chain encompasses wa-

fering, solar cell, solar module and solar system processes.

Thanks to a focus on the entire value chain, we create clear

added value for customers and set ourselves apart from our

competitors. In addition, our Group is a leader in systems

designed to monitor and support the entire production pro-

cess.

Atacama Slate – the technology designed for hot

desert climates

Our innovative solar module “Atacama Slate” is a cost-ef-

fective solution for producing electricity in regions with high

solar irradiance, sand storms and high temperatures. Ataca-

ma Slate is based on a robust combination of high efficiency

technologies and an innovative module design adapted to

the specific requirements of delicate desert regions.

Atacama Slate consists of a bi-facial, frameless, glass/glass

module design combining the high efficiency heterojunc-

tion and SmartWire connection technologies. This leading

technology combination meets the challenge presented by

desert regions in order to achieve optimum energy yield

under delicate climatic conditions while lowering the total

cost of ownership and module maintenance. High solar ir-

radiance, high environmental temperatures, sand storms as

well as a different light spectrum need to be considered in

the design and technology of solar modules for these chal-

lenging regions.

Our Atacama Slate module is the solution for reach-

ing maximum energy yield by combining high effi-

ciency technologies with a dedicated module design

adapted to desert regions like Saudi Arabia.

Atacama Slate relies on the high performance combination

of heterojunction cells connected with SmartWire connec-

tion technology. Heterojunction cells have a low tempera-

ture coefficient of approx. 0.20% and are designed for high

irradiance conditions. The cost effective SmartWire connec-

tion technology electrically connects solar cells using thin

copper wires on both sides of the cell instead of bus bars

and is capable of achieving up to 5% higher power output

compared to best-in-class bus bar technology., The inno-

vative bi-facial Atacama Slate also enables vertical module

installation while its frameless design effectively counters

sand and dust retention. A robust glass/glass construction

ensures long module endurance. The Atacama Slate com-

bines leading high efficiency technologies with a dedicated

module design to tackle tough desert climatic conditions

and deliver a cost-effective solution for producing electricity.

MEYER BURGER TECHNOLOGY LTD

Schorenstrasse 39

CH-3645 Gwatt (Thun)

Switzerland

www.meyerburger.com

MEYER BURGER TECHNOLOGY LTD

26

READY FOR SAUDI ARABIA

The SMA Group is the world market leader for solar invert-

ers, a key component of all PV plants, and as an energy

management group, offers innovative key technologies for

future power supply structures. SMA offers first-class prod-

ucts, system solutions and worldwide servicing for every

PV system. The company generated sales of € 1.5 billion in

2012 and is headquartered in Niestetal, Germany. It is rep-

resented internationally in 21 countries, employs more than

5,000 people and maintains 90 service stations worldwide.

LEADING SOLUTIONS AND EXPERTISE FOR UTILITY-

SCALE PV POWER PLANTS

More than 30 years of experience and PV power plant proj-

ects in the multi megawatt range in more than 30 countries

show the outstanding competence of the company. Invert-

ers are the intelligent central component at the heart of

every PV system and their quality and reliability determine

the performance of the entire PV power plant. As a pioneer

in grid integration, SMA furthermore offers worldwide tai-

lor-made solutions that fulfill the complex requirements for

PV power plants in the local markets. SMA’s experts work

together with various bodies and committees to establish

the necessary regulations worldwide. SMA central invert-

ers have been meeting the requirements of country-specific

connection conditions for years in a number of countries,

including Germany, Japan, and the US.

CHALLENGING ENVIRONMENTAL CONDITIONS IN

SUNBELT COUNTRIES

The world’s sunbelt regions with countries such as Saudi

Arabia are extremely attractive for large-scale PV projects.

Countries with rising populations, booming economies and

increasing demand for energy supply not only profit from

vaster possibilities of energy production but also from the

creation of jobs through new technologies. Saudi Arabia

has favorable irradiation conditions for the deployment of

PV energy generation and therefore the chance to save oil

and thus extent the nominal lifetime of this fossil energy

resource. When it comes to water desalination PV power

is indispensable in countries with dry and hot environmen-

tal conditions. The implementation of PV technologies also

represents a great opportunity in value chain development.

In addition to high efficiency and low energy self-consump-

tion, SMA central inverters are designed for extreme con-

ditions such as extreme heat or sandstorms. Only invert-

ers with excellent technical properties will guarantee the

long-term benefits of PV projects in climatically challenging

regions.

FLAGSHIP PROJECTS IN THE GULF REGION

SMA is the local market leader in Saudi Arabia and has al-

ready installed a base of 16 MW in Saudi Arabia specifi-

cally and more than 65 MW in the Gulf Region – continuing

to rise. Flagship projects are the solar parc KAPSARC (King

Abdullah Petroleum Studies and Research Center) equipped

with SMA Sunny Central 720 CP inverters and the world’s

largest parking lot to be covered with PV panels in Khobar

with 10.5 MW PV power utilizing 18 Sunny Central inverters.

These are only two examples of recent PV power plant proj-

ects in the kingdom which expects its energy consumption

tripling until 2032. SMA shows local presence with a ser-

vice company in Dammam, provides local on-site service,

local trainings and education as well as sales and technical

support from its presence in Dubai and Abu Dhabi. SMA

is optimally positioned in the market and preparing for an

even stronger engagement in Saudi Arabia according to the

local requirements.

SMA SOLAR TECHNOLOGY AG

Sonnenallee 1

34266 Niestetal Germany

www.SMA.de

SMA SOLAR TECHNOLOGY AG

27

28

SIC PROCESSING (DEUTSCHLAND) GMBH

SiC Processing (Deutschland) GmbH

YOUR PARTNER TO REDUCE WAFER COSTS.

The SiC Processing (Deutschland) GmbH is a leading, worldwide operating service partner for processing

of used sawing suspension (slurry) with outstanding market position and product quality. Improved process

performance, lower consumption of virgin resources, significant waste reduction and finally lower total

wafer costs are the motivation for our customers using our slurry management capabilities.

Photovoltaic and semiconductor industry are using slurry to produce wafers out of mono- or multi-crys-

talline silicon blocks on wire saws. The suspension consists of a fine-grained, sharp edged abrasive (most

silicon carbide) and a viscose carrier liquid (most glycol) which acts as a transportation- and cooling medium.

During the wire sawing process the slurry is collecting the removed fine silicon (kerf) and other impurities

(Fe, H2O), the cutting efficiency is decreasing and the used slurry has to be replaced.

Our multi-step technology separates solid and liquid components, eliminates all residues and recovers SiC-

abrasive and liquid with customized characteristics.Recovery rates of 80 to 95 % are possible for the com-

ponents. We can provide the recycled materials separately or the ready to use slurry according to customer

process specifications. For almost all residues applications are available to ensure waste avoidance.

Also for other materials our processing concept can be modified. Separation, classification and cleaning of

fine solid powders as well as filtration, purification and distillation of technical liquids are part of our busi-

ness. In our plants in Bautzen/ Germany it is possible to process up to 40,000 tons per year. R&D projects,

lab analyses and logistics are additional services.

For further information please contact: SiC Processing (Deutschland) GmbH

Neuteichnitzer Straße 46 , 02625 Bautzen , Germany

Phone: +49 3591 529330 , [email protected] , www.sic-processing-bautzen.de

• Worldwide operating service partner for sawing suspension

(slurry)

• 12 year experience and technical know-how improvement

• Complete slurry management (recycling, virgin compo-

nents, logistics, plant construction)

• Supply of specified components or ready to use slurry

• Own R&D center; highly qualified laboratory; own TCO

models

• Separation, classification and purification of other solid

materials/ powders/ liquids

29

Optical Disc >

Solar >

Semiconductor >

Mastering

Molding

Replication

Crystalline Photovoltaic

Thin FilmPhotovoltaic

MRAMThin Film HeadsSensor

SINGULUS TECHNOLOGIESInnovative Technology for Photovoltaic

Optical DiscSolarSemiconductor

anzeige_Indien_2013:Layout 1 31.07.13 12:10 Seite 1

SINGULUS TECHNOLOGIES

DEVELOPER, ENABLER AND SUPPLIER FOR THE PV MARKET

SINGULUS TECHNOLOGIES is a supplier of manufacturing solutions and production equipment for the Mar-

kets Optical Disc, Semiconductor and Solar. With new machine concepts and manufacturing processes in

the crystalline and thin-film solar technology SINGULUS TECHNOLOGIES establishes itself as development

partner and equipment supplier for investments in new high-performance solar cell concepts. SINGULUS

TECHNOLOGIES continues to expand its activities in the Solar segment. and cooperates with cell manufac-

turers worldwide and develop processes, which improve the efficiency of solar cells and at the same time

reduce production costs. In addition, SINGULUS TECHNOLOGIES has set up development partnerships with

universities, institutes and leading solar companies to establish a proprietary technology as standard for the

development of the new cell concepts.

Evolutionary improvement in cell concepts like PERC (PERL/PERT), n-type material, IBC – back con-

tacted cell or Heterojunction cells will drive the future of crystalline solar cells.

SINGULUS is the market leader for the application of CIS/CIGS processes. New plant concepts expand the

value-added chain of the company in the area of thin-film solar technology.

SINGULUS offers modern production systems such as Selenisation furnace for an optimized CIGS absorber

formation, Sputtering & Evaporation machines as well as Wet-chemical systems.

SINGULUS TECHNOLOGIES AG

Hanauer Landstrasse 103 , 63796 Kahl am Main , Germany

Tel.: +49 [0] 61 88 - 4 40 - 0 , E-mail: [email protected]

30

Air Liquide, world leader in gases for industry, health and the environment

Gases and Precursors for the Solar PV Industry

Air Liquide serves >50% of PV Manufacturing Worldwide

AIR LIQUIDE

AIR LIQUIDE IS THE WORLD LEADER IN GASES FOR INDUSTRY, HEALTH AND THE ENVIRONMENT, AND IS PRESENT IN OVER 80 COUNTRIES WITH NEARLY 50,000 EMPLOYEES.

Oxygen, nitrogen, hydrogen and rare gases have been at the core of Air Liquide’s activities since its creation

in 1902. Using these molecules, Air Liquide continuously reinvents its business, anticipating the needs of

current and future markets. The Group innovates to enable progress, to achieve dynamic growth and a

consistent performance.

Air Liquide explores the best that air can offer to preserve life, staying true to its sustainable development

approach. In 2012, the Group’s revenues amounted to €15.33 billion, of which almost 80% were generat-

ed outside France. With over 1400 employees in the Middle East and North Africa Air Liquide is present in

Morocco, Tunisia, Algeria, Egypt, Lebanon, Kuwait, Oman, Qatar, Saudi Arabia, Syria and the United Arab

Emirates, where the Group has its Middle East and North Africa headquarters.

Its Electronics business line supplies advanced materials and services to over 50% of Photovoltaic manufac-

turers globally in an effort to advance the industry and help achieve grid parity.

Air Liquide has decided around one billion dollars investments over the 2002-2012 period in the MENA

region.

A partner for the long term, Air Liquide relies on employee commitment, customer trust and shareholder

support to pursue its vision of sustainable, competitive growth.

Air Liquide is listed on the Paris Euronext stock exchange (compartment A) and is a member of the CAC 40

and Dow Jones Euro Stoxx 50 indexes.

31

32

Editor

EuPD Research

Adenauerallee 134

53113 Bonn

Germany

Tel +49 (0) 228 – 971 43 - 0

Fax +49 (0) 228 – 971 43 -11

www.eupd-research.com

Authors

Martin Ammon

Markus Lohr

Picture Index

Cover

fotolia.de | industry robotic © industrieblick

fotolia.de | Solar enegery © Mark Smith

fotolia.de | solar panel with desert house © xiaoliangge

fotolia.de | Hi Tech factory inside © industrieblick

fotolia.de | High Tech industrie factory © industrieblick

IMPRINT

Editor

Viridis.iQ GmbH

Reichenaustr. 21

78467 Konstanz

Germany

Telefon (+49) 7531 3610 4953

Telefax (+49) 7531 3610 4882

www.viridis-iq.de

Authors

Magdalena Ulmer

Matthias Grossmann

Dr. Wolfgang Herbst

Art Direction

360|Concept

www.360concept.de

Stefanie Becker

Rebecca Ohagen

© EuPD Research 09/2013

EuPD Research® is a trade of

HOEHNER RESEARCH & CONSULTING GROUP GmbH.

www.eupd-research.com | www.viridis-iq.de