slg economics packets market study presentation for postal and delivery economics conference

TRANSCRIPT

Center for Research in Regulated Industries19th Conference on Postal and Delivery Economics

Stephen Gibson and Nancy RaceJune 2011

St Helier, Jerseywww.SLG-Economics.co.uk

Market Study on Parcels and Packets Services (PPS)

2

OutlineBackground and evidenceMarket definitionMarket power Regulatory proposals

A market study

Why? Good regulatory practice: Ofcom, OFT, ORR and Ofwat use market

studies to support their regulatory proposals Allows us to assess the need for regulatory intervention It gives stakeholders more information about how we view the

postal market and how this has informed policy proposals To facilitate quicker investigations in future Hooper Review recommended a market study

Objective To define a set of relevant postal markets; and To determine whether Royal Mail has market power in those

marketsApproach

Using the hypothetical monopolist (SSNIP) approach, taking the evidence in the round.

However the market study is not an end in itself Part of the evidence to develop a new regulatory framework for Royal Mail

4

PPS Market studyEvidence base Structural interviews of over 90 customer and 19 operators. Detailed questionnaires to main operators. Discussion paper published (2009); Stakeholder workshops and company visits Consultation published (May 2010) Stakeholder consultation workshops and written responses from 20

Stakeholders. Considerable RM input: Bi-weekly meetings, position paper and

response to consultation including undertaking it own survey. Reports from: Accent Rand, Oxera, Royal Mail, Frontier Economics,

ONS, Triangle, Investec, Mintel, Verdict, Postwatch, Datamonitor, IMRG and ECORYS

Decision published (November 2010)

5

Market definitionProduct dimensions

Price

Speed of

delivery

Customer type

Contract

Volume

Weight

Value added

Format

6

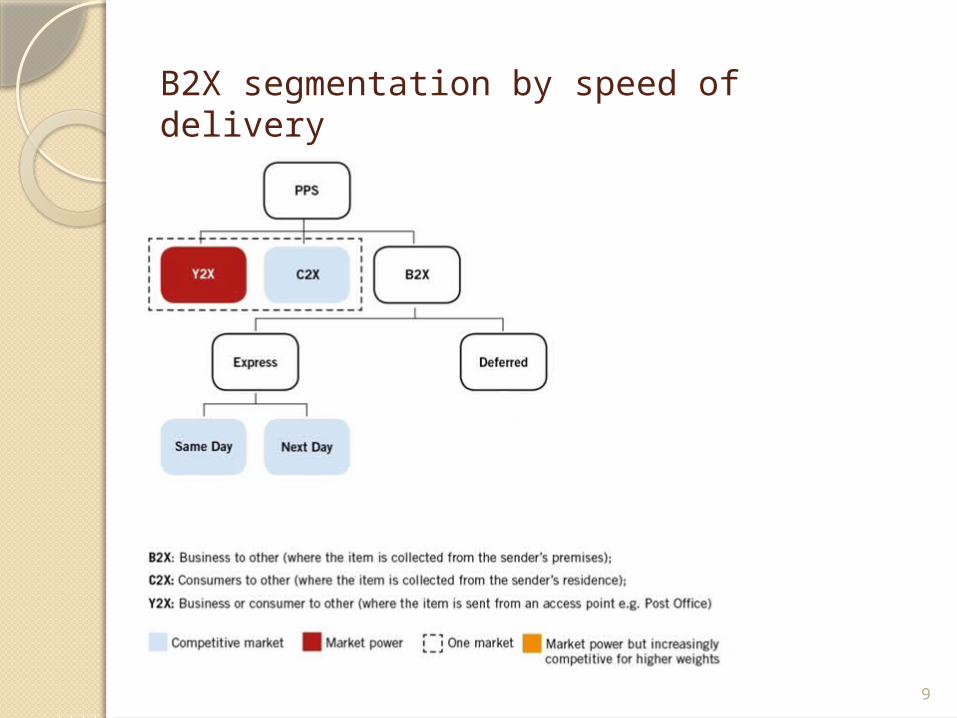

Customer segmentationPPS market split into:

C2X: Items sent by customers from their premises Very small (but growing), no Royal Mail presence Likely to be in the same market as Y2X (demand-side

substitution)

Y2X: Items sent by customers and small businesses from collection points (Post Offices, pillar boxes, retail outlets) Royal Mail has market power

B2X: Items sent from business premises B2C and B2B distinction increasingly blurred as operators

able to serve both types of customers Further segmentation required to assess the competitive

conditions

Customer segmentation

7

8

B2X Segmentation by speed of delivery

Express (time-guaranteed) and Deferred services form separate markets◦ Operational models are different and switching is difficult.

◦ Customers do not tend to switch between deferred and express services because of SSNIP. Large price differentials and quality differences .

◦ Express market very competitive with many operators.

Express can be sub-divided into Same day and Next day.◦ Network differences (point to point vs hub and spoke)

◦ Same day is highly contestable (taxis and one man operations).

◦ We have left this open

B2X segmentation by speed of delivery

9

10

Competitive choice a function of weight and volume

Weight is important.◦ RM currently price by weight steps and believes it to be an important

dimension for determining how the market functions.◦ Customers actively manage their choice of operator by weight of consignment.◦ Competition increases with weight.◦ For low weights the competitive conditions are different.

Contract volume is also important

Increasing

competitionV

olum

e

Weight

– Contract volume influences the degree of competitive choice (depending on weight).

– Higher volume customers have more incentive to shop around and are able to multi-source.

11

Breakpoints Above 2kg end-to-end operators and Royal Mail have

similar cost structures . There was broad agreement that the market was competitive above 2kg.

Up to 2kg evidence suggested greater competition for heavier weights and volumes,

The evidence did not allow us to conclude on one unique weight or volume break point at which the conditions of competition changed significantly.

Defined one broad market up to 2kg, and considered the different levels of competition in our market power assessment.

12

The Packets and Parcels (PPS) Market Study Conclusions

The economics of different delivery models

Foot based network

Van based network

Cost

Weight

2kg500g

Foot Van

Van (high volume)

Van (low volume)

1kg

Foot/ Van

Foot

Market Power in the deferred B2X <2kg market

The ability of end-to-end operators to compete depends on their cost structure and whether the service can be bundled with more expensive services.

Collection costs determine the extent to which operators can compete for low volume contracts.

Delivery costs determine the extent to which operators can compete for low weight items.

The greater the volume of higher weight items sent with an operator the lower the price offered for light weight services.

14

15

Market power assessment

16

Regulatory Proposals

• C7 Requirement for advance notification and publication of tariff changes

• C7- Requirement for notification of tariff changes (more limited publication)

• C11 Promotion of effective competition

• C15 Accounting separation

• C21 Price Control

17

Market study publications

May 2010 Consultation: Packets and Parcels Services (PPS) Wholesale Letters and Large Letters

markets Retail Letters and Large Letters supply-side

Nov 2010 Decision: Packets and Parcels Services (PPS) Wholesale Letters and Large Letters

markets Retail Letters and Large Letters supply-side

Feb 2011 Consultation: Retail Letters and Large Letters markets

May 2011 Consultation: International Outbound markets

Available at www.psc.gov.uk

Questions?