slide 0 - deutsche bank

TRANSCRIPT

Research Deutsche Bank

Deutsche Bank Research The House View: Common Sense Prevails October 18 2013

DISCLOSURES AND ANALYST CERTIFICATIONS ARE LOCATED IN APPENDIX 1. MICA(P) 054/04/2013.

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

2 Special report – Japan: The Great Escape

1 The House View – Common Sense Prevails

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

The House View – October 18 2013: Common Sense Prevails

The much-awaited reopening of the US government and suspension of the debt ceiling marks an end,

albeit temporarily, to the political spectacle in Washington. While we were never in doubt that the US

would avoid default, the episode highlights that political brinkmanship and short-term fixes are

phenomena not unique to Europe. However, the resolution of this episode has inflicted deep wounds

on the Republican party and Congress. As a result, chances for meaningful progress in the upcoming

budget negotiations have improved. Another government shutdown and debt ceiling showdown next

year seem less likely

We expect the economic impact of the shutdown and political impasse to be relatively muted.

Somewhat perversely, the deadlock in Washington helped underpin risk appetite, as the elevated state

of uncertainty raised expectations that Fed tapering will be delayed, thus containing the recent rise in

borrowing costs

Although we remain constructive on equities, the majority of this year’s rally has been driven by

multiples normalising from depressed levels rather than higher earnings. As a result, Q3 reporting will

provide crucial insights as to whether the earnings inflection required to propel the rally is materialising

An exception to this trend is Japan, where multiples remain little changed despite earnings growth of

>60% this year. In a special report, we outline our conviction in Abenomics and why we think Japanese

equities could double over the coming years

David Folkerts-Landau, Group Chief Economist

The views in this publication are informed by Deutsche Bank’s Global Strategy Group, which advises management and clients on broad market risks and

global economic and financial developments. The views and forecasts of the group, which consists of senior research staff, may occasionally differ from

those disseminated by their research colleagues

Editors: Raj Hindocha, Marcos Arana,

Wolf von Rotberg, Sahil

Mahtani, Erin Urquhart

3

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

Expect global growth to pick-up led by the US and Europe. See minimal impact from the US budget standoff

Fed: QE tapering to start by March-14 and QE to end in

2014, exact timing data dependent. No hikes until 2015

then Fed to surprise with faster hiking cycle than

currently priced by the market

ECB on hold with easing bias. Additional liquidity for

banks (LTROs) possible but not imminent

BoJ on hold but stands ready to ease further if needed

BoE on hold, using forward guidance on rate rises

PBoC on hold given inflation risk contained

EM mostly on hold with some countries (e.g., Brazil,

India) tightening to to counter inflation / outflow risk

Monetary policy shock: path to normal monetary policy

surprises markets, leads to volatility, hurts growth

Euro crisis reignites: politics lead to crisis escalation,

recovery stalls

Corporate earnings disappoint, fail to accelerate

EM growth slowdown: amid lack of reform and capital

outflows, or if export traction fails to materialise

US fiscal accident: around debt ceiling / budget

negotiations

Global growth of 2.8% in 2013, 3.7% in 2014

US growth of 1.8% in 2013, 3.2% in 2014. Recovery

remains intact, converging to 3% growth in 2014.

Strengthening labour market, housing sector recovery

and reduced fiscal drag to support economy

Eurozone growth at -0.2% in 2013 and 1.2% in 2014.

Growth to be supported by domestic demand, export

traction and slower pace of fiscal tightening

EM growth of 4.5% in 2013 and 5.4% in 2014. US /

Europe demand to support export-driven recovery

US fiscal negotiations: short-term deal is a mild positive that buys time for a more comprehensive solution, which should be easier to achieve next time around

Fed policy normalisation: tapering to begin by March, with Yellen taking over as chair (pending confirmation). Earlier taper possible if data strengthens materially and a real fiscal resolution is reached by December

Euro politics: expect Merkel-led Grand Coalition with SPD in Germany to be announced by mid-/ late-Nov, no change to crisis response approach. No escalation in Italy in next 18-24 months, political map improved

Economic outlook Central bank watch

Note: H / M / L indicates estimated probability of risk (High, Medium, Low)

Views on key themes Key risks to our view

4

M

L

M

M

L

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

Downside risks

— Monetary policy shock: path to normal monetary policy

surprises markets, leads to volatility, hurts growth

— Crisis returns to Europe: return to recession; political

breakdown raises tensions, e.g., snap election in Italy,

weak government coalition in Germany

— Corporate earnings disappoint, fail to accelerate

— EM growth slowdown: export traction fails to materialise;

lack of structural reform limits growth potential

— US fiscal accident: unexpected slowdown in data; fiscal

uncertainty dents growth

— Geopolitical tensions escalate and push up oil prices or

slow economic activity, e.g., escalation of Syria conflict

Upside risks

— Global growth upside surprise: limited fiscal drag in the US,

sharper-than-expected recovery in Europe, reforms and

stronger growth in EM, effective policy stimulus in Japan

1

2

3

4

5

7

Lower Probability

Imp

act o

n o

ur

ba

se

ca

se

Higher

Lo

we

r H

igh

er

Higher risk

Lower risk

The House View - Risk Matrix

* Moves represent change in risk outlook over previous month

Major risks have receded as policy uncertainty fades and tapering is delayed

5

5

6

2

1 1

5

2

4 4

6

3

7

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

41%

26% 23% 22%

20% 16% 16% 15%

6% 5% 0%

-8%

4% 1% 1%

-2%

5%

-2% -2% -4%

3% 2% 1% 0%

-4%

-10% -11% -12% -14%

1% 0%

-23% (25)%

(20)%

(15)%

(10)%

(5)%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Japan N

ikkei

Spain

IB

EX

35

US

S&

P 5

00

Italy

Mila

n

Fre

nchC

AC

40

Euro

pe S

toxx 6

00

Germ

an D

AX

30

UK

FT

SE

100

Hang S

eng

India

Nifty

MS

CI E

M

Bra

zil

Bovespa

US

Hig

h Y

ield

EU

IG

EU

IG

Fin

US

IG

Italy

Germ

any

US

UK

EU

R

RM

B

Dolla

r In

dex

MX

N

MY

R

TR

Y

INR

JP

Y

ZA

R

Com

modity Index

Bre

nt O

il

Gold

YTD 2013 Since October 1 shutdown

* October 1 is the first trading day after Fed postponed potential tapering

Note: Total return accounts for both income (interest or dividends) and capital appreciation.

Source: Bloomberg Finance LP, Deutsche Bank Research. Prices as of 16 Oct 2013, COB

Total returns YTD 2013, change since 1 October (start of shutdown)

Risk appetite has remained healthy despite the US government shutdown and debt ceiling impasse

6

Equities Corporate

credit

Sovereign

debt

Commodities FX

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

0

3

6

9

12

15

18

1940 1950 1960 1970 1980 1990 2000 2010

Statutory debt limit

The deal: US debt ceiling suspended until 7-Feb. Treasury can fund

the government through May thanks to its extraordinary measures

USD tn

January 2012: +USD1.2tn

August 2011: +USD0.9tn

Source: US Treasury, Haver Analytics, Deutsche Bank Research

Debt Ceiling suspended until 7 Feb 2014

The US government went into partial shutdown at

the start of the new fiscal year on 1-October after

Congress failed to pass a budget for FY 2014, or a

continuing resolution (temporary budget extension)

to keep the government funded

Late on 16-October, Congress compromised on a

bill which included

− Continuing resolution though 15-Jan-2014, to

end the 3rd longest shutdown in US history

− Suspension of debt ceiling through 7-Feb-2014,

although Treasury retains extraordinary

measures that will enable it to borrow until mid-

May

Furthermore, agreement was reached between

House and Senate leaders to appoint negotiators to

reach a budget agreement by 13-Dec-2013

− A report must be issued by then – though

agreement is not necessary

10 12

8 8

18

11

2 1 3 3 2 1 1 1

5 5

21

16

0

5

10

15

20

25

US government shutdowns: 2013 was the third longest shutdown in

history

Number of days

Source: Deutsche Bank Research

7

Late on 16-Oct, US Congress agreed to suspend the debt ceiling and pass a continuing resolution to keep the government funded

Note: The debt ceiling is a limit on the amount that the US government can borrow for public spending

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

8

Market distortions in the US Treasury market have normalised, while equity markets remain close to all-time highs

The equity market shrugged off the shutdown and

default fears

− S&P 500 up +2.4% over the course of the

shutdown

Risk appetite was supported as the elevated state

of uncertainty raised expectations that tapering will

be delayed into Q1

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

19/09 26/09 03/10 10/10 17/10

US 1M yield

US 12M yield

US Treasuries market: 1M yields rose above 1Y yields amid concern

that near-term payments could be disrupted

%

Source: Bloomberg Finance LP, Deutsche Bank Research

1,550

1,600

1,650

1,700

1,750

Jun-13 Jul-13 Aug-13 Sep-13 Oct-13

S&P500 closing prices: Equity market response was fairly benign

during the shutdown

Source: Bloomberg Finance LP, Deutsche Bank Research

All time closing high

The yield curve inverted as 1M yields surged above

1Y yields

− At height of the crisis, US 1M yields spiked to

45bp intraday (vs. 0bp a month ago)

− Investors were concerned about payment issues

with maturing short-term debt, rather than over

widespread fears of a default

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

9

We expect the economic impact of the shutdown and political impasse to be relatively muted

Macro impact on the US economy will be small, as

in the August 2011 debt ceiling episode –

annualised rate of real GDP growth down by a few

tenths of 1% in Q4

Only a subset of federal government employees

initially classified as non-essential were affected by

the shutdown – and even for those, Congress

agreed early on to grant retroactive pay, so the

effect on consumer spending should be limited

While sentiment and confidence indicators declined

in the past few weeks levels still remained above

those seen in August 2011. We expect these

indicators to reverse sharply now a deal is in place

Equities remains relatively resilient, thus avoiding

any negative wealth effects for consumers

3.2mn 2.4mn

800k 350k

450k

0

1

2

3

4

Federal Gov Employees

Essential Initial "Furloughed" -

off work

Reclassified as 'essential'

Off work

US federal government: after initial shutdown of ~800k non-essential

employees, 350k DOD staff were reclassified as essential

Source: Deutsche Bank Research

Congress deal means workers

Will receive retroactive pay

-70

-60

-50

-40

-30

-20

-10

0

2008 2009 2010 2011 2012 2013

US Economic Confidence: shutdown and gridlock caused sharp

drop, but confidence remained above Aug-2011 levels

3d moving avg.

Source: Gallup, Deutsche Bank Research

Oct-15 shows

rebound as hopes

of a deal rose

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

0

10

20

30

40

50

60

70

80

2007 2008 2009 2010 2011 2012 2013

VIX Volatility has diminished in response to recurring systemic threatss

VIX Index

Mar-11 Japan

earthquake

Italian elections

and Cyprus Bailout

Sep/Oct-08:

Financial Crisis:

Lehman, AIG,

TARP

Aug-11 US

downgrade and

debt ceiling crisis Nov-11 Euro

crisis spreads

to Italy / Spain,

2nd Greek

bailout

Greek elections

Apr/May-10 Euro crisis /

1st Greek bailout

US shutdown /

debt ceiling

debate

US Fiscal Cliff Tapering

10

Markets have become less volatile around systemic threats, as investors anticipate an official response to contain tail risks

Source: Bloomberg Finance LP, Deutsche Bank Research

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

4.0 4.9

5.5 6.2

3.1

4.6

6.2

7.6

8.3

10.0

7.5

7.2

2.2

1.3 3.4

4.5

17.6

20.8

22.6

25.5

0

5

10

15

20

25

30

2000 2013 2025 2035

Net Interest Discretionary (including defense)

Medicare + Medicaid Social Security

US government spending is forecast to increase by approximately 5% of GDP by 2035

% of

GDP

Source: CBO, Deutsche Bank Research

Net Interest

3.5x

Change

since 2013

Discretionary

0.7x

Medicare +

Medicaid

1.7x

Social Security

1.3x

US government has a long-

term fiscal problem that

translates into recurring

fiscal deficits

On the spending side, the

Congressional Budget

Office estimates that

Government spending will

rise to over 25% of GDP by

2035, up from ~20% today

Discretionary spending

(including defense) will

come down, but will be

more than offset by

increases in health

(Medicare + Medicaid),

Social Security and cost of

debt

11

The US fiscal deal resolved the immediate issues (shutdown, debt ceiling), but long-term budget concerns remain unaddressed

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

The US continues to follow the European approach to crisis resolution: brinkmanship followed by short-term fixes

12

“Governments and central banks have to take out the catastrophic

risk from markets, they have to definitively remove the threat of

…cascading defaults”

Tim Geithner, US Treasury Secretary, September 2011

"The sooner [leaders] act, the more decisive and concrete their

actions, the sooner people and markets will regain some

confidence, the cheaper the costs of cleanup will be down the

road.”

President Obama, June 2012

At the height of the euro crisis in 2011-2012, US

authorities urged their European counterparts to

make the necessary decisions to end uncertainty

− Europe’s ‘muddle through’ incremental

approach was criticised

US has taken a similar approach with its fiscal

negotiations, with successive deals only buying

time, multiplying deadlines and showdowns

Current deal is yet another example, with the

next installments on 13-Dec and 14-Jan

This episode was the third time since 2011 that US political paralysis over fiscal issues has dominated global markets

3-May-2011: Geithner: "Debt ceiling to be

breached by 2-Aug"

May -Jul 2011: “Grand Bargain” negotiations to reduce deficit by USD4tn

in 10 Y

1-Aug-2011: Debt ceiling lifted, introduction of

budget sequester and bipartisan Supercom-

mittee on LT fiscal reform

‘Do as I say, not as I do’ – comments on the euro crisis

5-Aug-2011: S&P strips US off AAA rating

21-Nov-2011: Super-committee fails to agree

on long-term fiscal reform, automatic

sequester cuts to kick-in in Jan-2013

Kicking the can down the road

Nov-Dec-2012: Fiscal cliff negotiations. Failure to reach agreement by

31-Dec, fiscal cliff kicks-in on 1-Jan

1-Jan-2013: 11th hour deal undoes fiscal cliff,

suspends sequester to 1-Mar

4-Feb-2013: Debt ceiling suspended until 18-May-

2013

19-May-2013: Debt ceiling reinstated, revised projection puts deadline

in Oct-2013

Through Sep: Budget / debt ceiling negotiations

25-Sep-2013: Lew*: "Debt ceiling to be

breached by 17-Oct"

1-Oct-2013: Failure to reach agreement on budget / debt ceiling

Government shuts down

17-Oct-2013: 11th hour deal. CR extended for 3

months, debt ceiling suspended to 7-Feb Government reopens

Note: (*) Current US Treasury Secretary Jack Lew

Episode 1: 2011 debt ceiling Episode 2: 2013 fiscal cliff Episode 3: 2013 budget and debt ceiling

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

13

However this episode inflicted deep political wounds thus raising chances for meaningful progress in upcoming negotiations

“I guess that we could get lower in the polls. We’re down to

blood relatives and paid staffers now.”

Sen. John McCain (Republican, Arizona), Oct 13

“We fought the good fight; we just didn’t win.”

House Speaker Boehner (Republican), Oct 16

63%

70%

74%

56%

61% 61%

50% 51% 53%

Sept. 25-29 Oct. 2-6 Oct. 9-13

(Dis)approval ratings: political brinkmanship has cost all players,

although Republicans have suffered most

Republicans in Congress

Democrats in Congress

Barack Obama

Source: Washington Post-ABC News, Deutsche Bank Research

% disapproving of the way …is handling

negotiations over the federal budget

Despite repeated episodes of political deadlock,

public opinion was overwhelmingly negative this

time

− Approval ratings fell throughout the shutdown,

with Republicans hit the hardest

Chances for meaningful progress on upcoming

budget negotiations have improved significantly

− The difference between the two parties on

spending levels narrowed substantially during

the CR and debt ceiling negotiations

− Popular patience with intransigence in

Washington is wearing thin

− In an election year the cost of displeasing voters

is higher (mid-term elections Nov 2014)

Another government shutdown and debt ceiling

showdown next year seem less likely “The debt ceiling is a political weapon of mass destruction

and the threat of it is huge just like a nuclear weapon would

be a huge threat. (…) Don't use something that can destroy

a 237 year old asset of the United States.”

Warren Buffet, Oct 16

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

14

In this context, the Fed should begin tapering by March 2014

US Economics Daily Note - 10th Oct 2013

0

1

2

3

4

5

6

7

8

132

134

136

138

140

142

144

146

148

2000 2002 2004 2006 2008 2010 2012

Civilian employment (lhs)

Civilians unemployed >6 months (rhs)

Some drivers behind unemployment are still weak, e.g., total

employment and number of unemployed for over 6 months

Source: BLS, Haver Analytics, Deutsche Bank Research

Million Million

FOMC Taper? Comment

Oct 29-30 Fed not more comfortable now than in Sep

Dec 17-18 ?

Possible, but “burden of proof” for data

high, e.g., payrolls above +200k

Chances of real long-term fiscal resolution

by December have risen

Jan 28-29 ? Possible; data will be stronger, political

uncertainty likely reduced

Last meeting under Bernanke

Mar 18-19

Market

pricing*

Fed publishes new forecasts, Chair holds

press conference – making it easy to

explain / justify taper

Note: (*) Based on US 10Y real curve

In September, the Fed’s decision not to taper was a

close call, and many FOMC members expected to

taper by year-end

As of now, the Fed’s reading of the recovery is no

clearer than in September

− Key data delayed due to shutdown (e.g.,

payrolls, inflation)

− Some data softness, including initial claims

− Uncertainty as to extent of shutdown impact

Yellen likely to remain concerned that some drivers

behind unemployment are still weak

− Labour participation at lowest since 1978, total #

of people employed still below pre-crisis

− Workers unemployed for over 6m still high

Fed will most likely begin tapering by March 2014,

barring negative shocks

− A December or January taper will require

significant data strength (labour market /

housing) and good progress on fiscal matters

− We expect QE to end in H2 2014

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

Global economy continues to gain traction

− Global PMI points to global GDP growth of 4%

qoq saar in Q3 vs. +3.3% in Q2 – which was

already the best growth since the start of 2012

− PMIs for all major economies in expansion

US recovery remains robust, with both hard and

soft data generally pointing to faster growth

− Some mixed data (e.g., consumer confidence,

vehicle sales) but not a major cause for concern

Europe: signals of gradual recovery remain

− PMIs accelerated in September, with recovery

evident in both the core and periphery

− On the negative side, high employment and

subdued credit growth offer reasons for caution

EM, especially export oriented economies, to

benefit strongly from acceleration of global growth

and delay of Fed tapering

15

We expect global growth will continue to accelerate, led by the US and Europe

-8

-6

-4

-2

0

2

4

6

8

30

35

40

45

50

55

60

2001 2003 2005 2007 2009 2011 2013

Global Mfg PMI

Global GDP (qoq% saar, rhs)

Global manufacturing PMI points to annualised GDP growth of 4% in

Q3 2013

Source: IHS Global Insights, Deutsche Bank Research

Accelerating

PMIs suggest

stronger GDP

45

50

55

60

Jan-12 May-12 Sep-12 Jan-13 May-13 Sep-13

Rising composite PMIs (3mma) show that growth momentum is

strong, with major economies in expansion territory

Source: Haver Analytics, Deutsche Bank Research

US

Global

Eurozone

China

Expansion

Contraction

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

Some data points have disappointed recently, but

we do not see a major cause for concern, e.g.,

− Services ISM -4.2pt mom in September, but level

remains consistent with above consensus growth

− Consumer, business confidence down in October

– but only marginally

Impact of the budget / debt ceiling debate on the

economy to be immaterial

The reduction in the pace of fiscal austerity in 2014

will further support growth – especially if part of the

sequester* is reduced during upcoming budget

negotiations

The consumer sector continues to contribute to the

recovery as deleveraging approaches completion

In housing, underlying drivers of the recovery are

robust enough to withstand rise in mortgage rates

16

In the US, mixed data and uncertainty surrounding the fiscal debate have raised concerns, but underlying strength is intact

Note: (*) Automatic spending cuts that came into force on 1-Jan-2013 as part of the fiscal cliff negotiations

-0.3

-2.1

-3.0

-0.2

1.0 1.1

2.3

0.7 0.4

-4

-3

-2

-1

0

1

2

3

2007 2008 2009 2010 2011 2012 2013 2014 2015

US fiscal stance (change in cyclically adjusted primary balance)

Fiscal tightening will continue in 2014, but at a much reduced pace

% of GDP

Source: IMF, Deutsche Bank Research

Positive = fiscal tightening

Negative = fiscal easing

Austerity will continue in

2014, but the incremental

tightening will be 1.6pp of

GDP less than in 2013

48

50

52

54

56

58

60

2010 2011 2012 2013

Manufacturing

Services

US ISM: data continues to point to robust growth. Decline in

Services ISM not a concern, September reading still very strong

Index

Source: Haver Analytics, Deutsche Bank Research

<50: contraction

>50: expansion

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

The European recovery continues

− Euro-area composite PMI improved to 52.2 in

September, the highest since Jun-2011

− Recovery broad-based, with strength in both

core and periphery

− The four largest countries of the eurozone are

all expected to post positive growth in H2 –

ending recession in Italy and Spain

There are four main drivers of the recovery

− Global growth: export PMIs >50 in four largest

eurozone economies – 1st time since Sep-2011

− Slower austerity: fiscal stance of +0.3% in 2014,

vs. +0.8% in 2013 – i.e., austerity continues, but

incremental tightening less than in 2013

− Less scope for crisis escalation: threat of ECB

intervention (OMT) keeps yields in check

− Uptick in credit impulse: credit supply to be

consistent with 2% GDP growth in 2014, well

above our own and consensus forecasts

17

Europe continues to recover from its longest recession on record, on rising exports and slowing austerity

Focus Europe - The bank/sovereign nexus 11 Oct 2013

30

35

40

45

50

55

60

65

2006 2007 2008 2009 2010 2011 2012 2013

Germany+France Italy+Spain+Ireland

Euro Composite PMIs point to a broad based recovery across both

the core and the periphery

Index

Source: Haver Analytics, Deutsche Bank Research

<50: contraction

>50: expansion

0.8

0.3

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2001 2003 2005 2007 2009 2011 2013 2015 Source: Deutsche Bank Research

Slower austerity will support the recovery and enable stronger

growth in 2014

Fiscal Stance

(change in structural primary budget balance)

% of GDP

Forecast Positive = fiscal tightening

Negative = fiscal easing

Austerity will continue in

2014, but the incremental

tightening will be 0.5pp of

GDP less than in 2013

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

18

While political concerns remain, they have become more manageable in recent months, especially in Spain and Italy

Greece: Pressured to stay on course

New PSI unlikely

Discussions on OSI* and additional

funding will not occur until mid 2014

when Greece has a primary surplus

IMF wants OSI but EU is resisting.

Without a major crisis, OSI-lite is

more likely, with maturity extensions

rather than writedowns

Germany: Merkel-led grand coalition with

SPD to be announced by mid-/late-November

Expect a CDU/SPD grand coalition, with

talks likely to last until mid-/late- November

Compromise to include the introduction of a

minimum wage (SPD demand) and no rise

in income tax (CDU demand)

Constitutional court ruling on OMT unlikely

to deliver a materially negative outcome

Spain: Political situation is manageable

following a turbulent summer

Questions over Rajoy’s involvement in a

funding scandal have weakened him, but…

…he still controls the majority in parliament

…near-term election unlikely as major

parties would lose out to fringe parties

Portugal: Weaker government, funding

uncertainty to linger

Austerity eroding support for adjustment

Constitutional court ruling on austerity

measures could impact exit negotiations /

government stability

Sovereign fully funded through year-end,

but future funding uncertainty will linger

Expect no PSI beyond voluntary rollover

of domestically held sovereign debt

Under Troika programme

Pursuing adjustment programme

Italy: Scope for material crisis escalation in the next

18-24 months has receded

Berlusconi losing control of PDL but will remain

an important right-wing figure

Unlikely to see progress on economic reforms

Economy to benefit from payment of state arrears

in 2014

Note: (*) Haircuts on debt held by official sector i.e., EFSF loans

Ireland: Crisis success story, but

potential uncertainty in 2014

Exit bailout programme in Dec-2013

and roll onto precautionary support

Having injected 40% of GDP in

banks, mid-2014 EBA stress test is

next significant challenge

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

25

30

35

40

45

50

55

60

65

70

-30

-20

-10

0

10

20

30

40

50

2003 2005 2007 2009 2011 2013

EM

US,EU orders (rhs)

Source: Deutsche Bank Research

US & EU orders vs. EM exports: US and EU growth should help lift

EM exports

% yoy, 3mma 3mma,

6M lead

The Fed’s decision not to taper asset purchases in

September was a welcome respite for EMs

− EM currencies have stabilised against the USD

after the “taper shock”

− The hope is that when tapering does begin, EMs

will be on a firmer footing and better able to

withstand the pain of higher interest rates

EMs will also benefit from import demand from DMs

− From Q1 2009 to Q2 2013, exports were a net

drain on growth for most EMs

− Most growth in EM economies in this period was

due to public and private spending

− However, the recovery in the US and EU

suggests higher export growth is coming to EMs

in the next few months

− This will help export oriented economies, and

countries like China ease the transition to a

more consumption-led economy

19

EM are enjoying some respite after a turbulent summer. Export traction from the US and Europe recovery should support growth

-20

-10

0

10

20

30

40

50

BRA IND RUS* CHN**

Pr.cons. Pub.cons. Invest. Next exp. GDP

* Q2-2009

**Q4-2008/ Q4-2012/ breakdown of private/ public consumption not available

Source: National statistical offices, Haver Analytics, Deutsche Bank Research

Exports were a drag on BRIC GDP growth between Q1-2009 and

Q2-2013

% pts

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

We expect more differentiation among EM

economies going forward

− Not all countries suffered from the summer

“taper shock” – e.g., some EMFX are up since

May 1, reflecting more positive investor

sentiment

− Broadly, countries with high current account

imbalances and inflation have fared worse

− Further tightening of liquidity would put more

pressure on these countries ( e.g., India,

Indonesia, Turkey, South Africa and Brazil)

− We expect Mexico, Philippines, South Korea

and some Central Europe countries to perform

better

Overall, we do not expect significant divestment

from EM assets, just more differentiation

20

EM will continue to benefit from inflows but going forward more differentiation is expected

Indonesia

India Turkey

Brazil

South Africa

Mexico

Philippines Korea

Taiwan

Poland

Hungary

-8

-4

0

4

8

12

0 1 2 3 4 5 6 7 8

Source: Deutsche Bank Research

Some countries are more vulnerable than others on balance of

payments and inflation indicators

CA, % GDP

Consumer prices (% avg, 2013F)

Better positioned

More vulnerable

3.9% 3.1% 2.8% 2.7%

0.9% 0.3%

-0.3% -1.1%

-3.1% -3.9%

-4.6% -4.9% -5.1%

-7.3%

-8.7% -9.3%

-11.0%

-12.5% -14% -12% -10%

-8% -6% -4% -2% 0% 2% 4% 6%

Since May 1st

Several EM currencies have depreciated significantly against USD

*As of Oct 16, COB

Source: Bloomberg Finance LP, Deutsche Bank Research

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

-10

-5 -2 0

6 9

25

63

12 14

11 13

11

30

21

9

-20

-10

0

10

20

30

40

50

60

70

DA

X

CA

C

UK

SX

6E

S&

P

MIB

IBE

X

TO

PIX

2013F

2014F

Earnings growth is expected to accelerate in most countries in 2014

YTD and index gains/loss rounded off and are based on 16 Oct close prices

Source: IBES, DataStream, Deutsche Bank Research

%

Consensus expectations for 2013 earnings growth

is weak across most DMs, except Spain and Japan

− Negative earnings growth expected in Germany,

France, UK; modest growth in the US and Italy

2014 earnings growth, though, expected to be

positive across the major DM markets

The rally in most indices is down to multiples

normalising from depressed post-crisis levels rather

than higher earnings

− Higher multiple accounts for all gains in France,

Germany and UK and most gains in the US

With valuations normalising and limited scope for

further multiple expansion, an earnings inflection is

required to propel the rally further over the medium-

term

Exceptions are Japan (positive response to

Abenomics) and Spain (strong recovery in the

corporate sector) where the rally has been driven

entirely by earnings

21

The strong YTD equity rally has mostly been driven by multiple expansion; further advances will require an uptick in earnings

% of index gain/loss

by PE: 26% 21% 13% 13% 15% 10% -5% -15%

by EPS: -10% -5% -1% 0% 6% 8% 26% 54%

YTD gain: 16% 17% 11% 13% 21% 18% 21% 39%

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

-30

-10

10

30

50

70 S&P 500 S&P 500 non-Financials Financials

* 3Q13 based on actual for reported and estimate for others

Source: First Call, IBES, Deutsche Bank

S&P 500 EPS growth y/y has been driven by Financials

Expect S&P 500 Q3

earnings growth to

pick up to ~5%

For greater evidence of an earnings inflection, we

would need to see a pickup in non-financial

earnings growth with decent sales growth in Q3

− Non-financials earnings growth has averaged

only 1.5% over the past 4 quarters

− Stronger earnings growth is needed to offset

some of the deceleration in Financials

Q3 earnings have started slowly, although only 42

S&P 500 companies have reported (19 Financials)

− Non-financial earnings running at 2.6%; expect

a pick up to 5%+

− Financials are underperforming, largely due to

JP Morgan’s miss on large litigation charges

We maintain our S&P 2013 year-end target of

1,750

− 1,800 S&P target for mid-Q1 sensitive to any

fiscal showdown

− 1,850 end-2014 target sensitive to unresolved

fiscal issues left after the midterm elections

22

In US Q3 reporting, non-financial earnings growth of 5%+ would support our view of an earnings inflection to propel the rally

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

23

We expect the recent outperformance of European equities over their US counterparts will be short lived

European equities have outperformed US equities

by 8% since July, following a record 15 straight

weeks of inflows into European equities – improving

European data, US fiscal concerns

Expect this trend to reverse and US equities to

resume their long-run outperformance

− Weaker European earnings explain Europe’s

45% underperformance since 2010

− Relative valuations show European equities

near top of their trading range since the early

2000s – European valuations reflect above

consensus earnings growth

− Stronger US growth outlook relative to more

balanced European picture

Long US over Europe for stocks with global growth

exposure via Tech, Staples, Materials, Industrials

− Valuations in Europe relatively high as investors

favoured less-EU sectors during the crisis

Long Europe over US for stocks with domestic

exposure Financials, Discretionary, Telco, Utilities

− Sectors still trade at a notable discount vs. US

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

Oct-12 Jan-13 Apr-13 Jul-13

Weekly flows as a % of NAV 10-week average flows as a % of NAV

Western Europe equities have seen inflows for 15 straight weeks

60 70 80 90

100 110 120 130

2005 2007 2009 2011 2013

Relative price performance

Relative earnings

EMU vs. US price and earnings (Dec 2002 = 100)

Relative price performance has very closely tracked earnings

Europe underperformed US by 45% since

2010, driven by weaker earnings

Since July, EMU

equities outperformed

US by 8%

-4.0

-3.0

-2.0

-1.0

2005 2007 2009 2011 2013

EMU minus US NTM PE Average

Source: EPFR, IBES, Deutsche Bank Research

EMU relative to US 12m forward P/E

Relative valuations* show European equities near top of their trading range since the early 2000s

Europe: More Expensive Than It Looks 1 Oct 2013

Note: (*) Based on US 10Y real curve

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

Asset price views

Asset Class View Rationale

Equities

US: bullish Bullish view on the back of improving macro backdrop, EPS, DPS and P/E expansion

Delay in tapering and low rates provide further support for equities

Q3 earnings showing growth (esp. in non-financials) will increase comfort in our targets

Europe: bullish Recovering growth and stronger global economy to translate into upward earnings revisions

Japan: bullish Abenomics could lead to a doubling of Japanese equities on a weaker JPY, higher

operational leverage and improving domestic economy

EM: least preferred vs. US

and Europe Relative to DM, EM to continue multi-year derating amid structural weakness, poor cash flow

generation and unwinding of central bank induced inflows – but delay in tapering is positive

Rates Neutral rates in short-term,

but fundamentally bearish

Fundamentally, as data strength continues, as we expect, on the back of favourable fiscal

and credit dynamics, the Fed will proceed with its exit strategy and rates will rise

Tapering delay will keep treasuries supported

FX Long USD

Entering a multi-year uptrend as a result of US growth resurgence, China economic

rebalancing, higher real yields and change in USD / risk correlation (to positive correl.)

Market substantially short USD

Sustained dollar strength will be dependent on US data

Credit Tapering delay favours

asset class

Asset class has repriced, currently trading at levels seen pre- signalling of tapering (22-May)

Stronger data will be positive for credit in long-term (fewer default rates)

In short-term, we expect further tightening as US fiscal deal brings renewed appetite for

carry trades – especially in higher beta; USD to outperform EUR credit

Tapering should see a widening of spreads as liquidity gets withdrawn

EM Long EM IG sovereign

credit

EM should benefit from returning risk appetite and ongoing respite from delayed QE tapering

EM IG sovereign credit has most value and is most likely to benefit from a return in fund

inflows. Favour high quality credits (Mexico, Philippines, Russia, Colombia)

Commodities Bearish crude oil Easing geopolitical risk and fading of supply disruptions negative for oil

24

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

2 Special report – Japan: The Great Escape

1 The House View – Reason Prevails

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

26

Japan has endured nearly two lost decades of growth

400

800

1200

1600

2000

2400

2800

3200

1981 1986 1991 1996 2001 2006 2011

Japanese equities remain significantly below their all-time peak as well as 2007 high

Source: Haver Analytics, Deutsche Bank Research

Topix Index

28

82 85 86 89 90 103

117 124 127

157

238

0

50

100

150

200

250 General Govt debt % of GDP (2012)

The lost decades have left Japan with the highest gross public debt among OECD countries

Source: IMF, Deutsche Bank Research

-10 -8 -6 -4 -2 0 2 4 6 8

10

88 90 92 94 96 98 00 02 04 06 08

GDP %YoY

Japan GDP growth was broadly range-bound between 1992 and 2008 after its epic asset bubble burst

Source: Haver Analytics, Deutsche Bank Research

-5

0

5

10

15

20

25

30

35

40

1996 2000 2004 2008 2012

Japan US

UK Germany

France

Japan has had the lowest cumulative GDP growth since 1996 of major developed economies

Source: Haver Analytics, Deutsche Bank Research

%

Japan +11%

US +39%

UK +33%

Fra +26%

Ger +22%

~60% below

all-time peak

~30% below

2007high

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

-1

0

1

2

3

4

5

6

90 93 96 99 02 05 08 11

Real GDP 5Y trend

Real interest rate (10Y JGB - CPI) 5Y trend

In Japan, real rates exceeded real GDP growth, encouraging saving, discouraging spending and investment, underpinning deflation

Source: Haver Analytics, Deutsche Bank Research

Japan’s economy has not grown in nominal terms

since 1997

− Nominal GDP in 2012 was 10% lower than in

1997

Policy errors in response to the bursting of the

stock and land price bubble in the 1990s, caused

persistent deflation

− Policymakers kept real borrowing costs high

instead of using monetary policy to boost growth

− Banks were not recapitalised quickly enough,

impeding lending

− Fiscal tightening was premature (esp. in 1997)

As prices fell, the economy steadily contracted

− Falling prices are problematic because

consumers, expecting prices to fall, spend less

− Firms become reluctant to borrow and invest

− This creates a vicious circle of sagging demand

leading to more deflation leading to less demand

27

The Japanese economy has not grown in nominal terms since 1997 due to deflation

90

92

94

96

98

100

102

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

CPI: All Items excluding Food and Energy (SA, 11/97=100)

Deflation has seen core CPI trending downward since late ‘97

Source: Haver Analytics, Deutsche Bank Research

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

PM Abe was elected in 2012 on a platform to end

deflation and revive Japan. This was spurred by:

− Impact of earthquake and tensions with China

encouraged a shift to a more activist policy

− Success of Fed and ECB crisis intervention

prompted a rethink of BoJ policy

− Decline in corporate profitability (i.e. Sony,

Sharp) raised concerns across Japan Inc.

Abenomics has three arrows:

− Monetary easing, to lower real interest rates and

approach a new BoJ inflation target of 2%

− Fiscal stimulus, to boost consumption

− Growth initiatives, to boost potential output

By increasing investment and consumption, the BoJ

aims to jump-start the economy

To reduce the debt burden, real GDP growth must

exceed real interest rates for a sustained period

i.e., if real GDP is 1% and real borrowing costs are

0%, debt/GDP falls over time

28

Abenomics is a policy to end deflation using a combination of monetary easing, fiscal stimulus and growth initiatives

Japan is entering a new steady state of positive inflation

Expected Steady

State

1998-2012

CPI, Overall (% yoy) 1.0% -0.22%

Nominal GDP (% yoy) 2.0% -0.6%

10-year JGB yield (%) 1.0% 1.4%

Note: Excluding the effect of the one-time consumption tax hike for new steady state

Source: MIC, Cabinet Office, BoJ, Deutsche Bank Research

Abenomics: Japan has successfully deployed monetary and fiscal

stimulus and is beginning to deliver on growth initiatives

Massive expansion of money base

Purchase of long-maturity JGBs

2% inflation target implemented

Supplementary budget for FY 2012

Tax incentives for labour, R&D

Corporate tax cuts

Free trade agreements

Labour, agriculture, health and

energy market deregulation

~

The 3 arrows

Fiscal Stimulus

Monetary Easing

Growth Initiatives

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

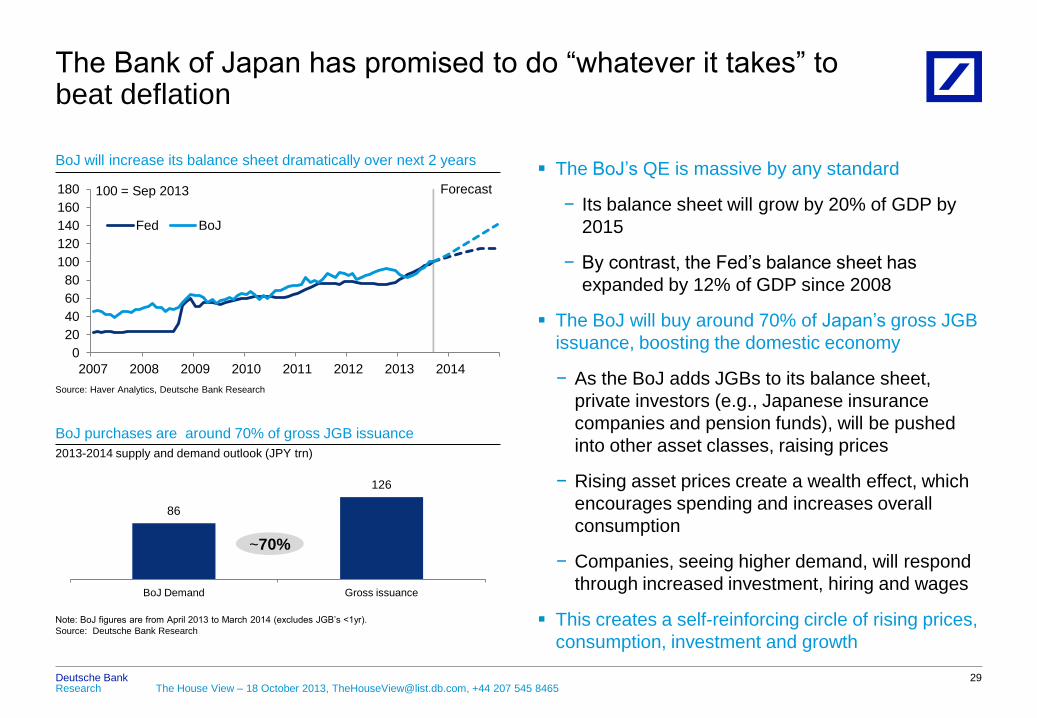

The BoJ’s QE is massive by any standard

− Its balance sheet will grow by 20% of GDP by

2015

− By contrast, the Fed’s balance sheet has

expanded by 12% of GDP since 2008

The BoJ will buy around 70% of Japan’s gross JGB

issuance, boosting the domestic economy

− As the BoJ adds JGBs to its balance sheet,

private investors (e.g., Japanese insurance

companies and pension funds), will be pushed

into other asset classes, raising prices

− Rising asset prices create a wealth effect, which

encourages spending and increases overall

consumption

− Companies, seeing higher demand, will respond

through increased investment, hiring and wages

This creates a self-reinforcing circle of rising prices,

consumption, investment and growth

29

The Bank of Japan has promised to do “whatever it takes” to beat deflation

0

20

40

60

80

100

120

140

160

180

2007 2008 2009 2010 2011 2012 2013 2014

Fed BoJ

BoJ will increase its balance sheet dramatically over next 2 years

Forecast 100 = Sep 2013

Source: Haver Analytics, Deutsche Bank Research

~70%

86

126

BoJ Demand Gross issuance

BoJ purchases are around 70% of gross JGB issuance

2013-2014 supply and demand outlook (JPY trn)

Note: BoJ figures are from April 2013 to March 2014 (excludes JGB’s <1yr).

Source: Deutsche Bank Research

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

30

Abenomics is slowly working - initially in financial markets, but now more convincingly in the domestic economy

65

70

75

80

85

90

95

100

105

110

200

250

300

350

400

450

500

550

1980 1985 1990 1995 2000 2005 2010 2015

Nominal GDP

CPI excl. food and energy (rhs)

Source: Cabinet Office, MIC, Deutsche Bank Research

Now, nominal GDP and prices are set to recover into 2014

JPY trn, saar Index, 2010 = 100

F’cast

96

106

116

126

136

146

156

Jan-13 Apr-13 Jul-13 Oct-13

Japanese equities have risen 40% YTD on expectations that Abenomics will succeed

Japan

Europe

MSCI Indices; 100= Jan 2013

Source: Bloomberg Finance LP, Deutsche Bank Research

US

Abenomics appears to be working, initially in

financial markets

− Equities are up 65% over the past 12 months

− Yen has weakened by 25% since Abe’s election

− Inflation expectations have risen by 100bp since

early 2012

Abenomics has triggered a domestic recovery

− After nearly 20 years of falling nominal GDP,

prices are set to recover in 2013

− Investment/GDP has risen for 3 quarters due to

falling long-term rates and higher asset prices

− Wages began to rise in Q3 2012, though via

bonuses (regular wages are still falling)

− However, we expect 2% nominal wage growth in

the years ahead, a significant change for Japan

− The recovery has been driven by domestic

activity rather than the typical export-led growth

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

A common worry is that investors will dump JGBs if

real returns fall

− If JGBs sold off, interest rates would rise,

increasing Japan’s debt-service costs and

risking a sovereign debt crisis

But most of the debt is domestically funded in

contrast to many OECD countries

− The arrangement is stable, has substantial

inertia due to regulation and domestic bias, thus

preventing a sustained sell-off

− Capital flight is unlikely in large, developed,

socially stable economies

Furthermore, the BoJ is committed to stabilising

bond market volatility through asset purchases

− BoJ holdings as a percentage of total JGBs will

expand to 20% by end-2014 from the 16%

projected for end-2013

31

Slightly higher inflation is unlikely to prompt a sovereign debt crisis via domestic capital flight

727

140

Held by financial market

Held by BOJ

The Bank of Japan’s purchases of JGBs adds another major buyer

to the JGB market

Source: Deutsche Bank Research

December 2013 December 2014

747

190

60 58

32 30

5

0 10 20 30 40 50 60 70

Most Japanese debt is held by domestic financial institutions

Source: Haver Analytics, Deutsche Bank Research

% of Govt. Bonds held overseas Share of JGB holding (Q2 2013)

79%

5%

1%

2% 12% Financial Institutions (inc BoJ)

Overseas

Corporates

Households

Others

JPY tn

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

0

50

100

150

200

250

300

350

71 74 77 80 83 86 89 92 95 98 01 04 07 10 13

TOPIX (in JPY)

TPX & long USDJPY*

Jan 2001=100

Even if a currency hedged Topix index* doubles, the index would

still be below 2007 levels

Source: Bloomberg Finance LP, Deutsche Bank Research

32

Japanese equities could double and the USD/JPY could reach 120 by 2015

If Abenomics continues to be successful, we

expect the Topix could double in the next few years

− Operational leverage is highest in Japan. For

every 1% revenue growth, earnings go up by

3% (vs. 1% in Europe and the US)

− Further JPY weakness will continue to be a

positive driver for Japanese profits

− Stocks remain cheap. More than 60% of

companies trade on a 'real' Price/Book of less

than 1x

The Yen will continue to remain under pressure

− BoJ easing exerts a powerful downward force

− Japan’s current account surplus has vanished

due to higher fuel imports after the nuclear

shutdown

− Expect USD/JPY at 120 by 2015 from 100 today

70

80

90

100

110

120

130

140

150

160 -1.0

-0.5

0.0

0.5

1.0

1.5

2.0

90 92 94 96 98 00 02 04 06 08 10 12

Narrow basic balance

USDJPY, inverted (rhs)

JPY tn

Source: Haver Analytics, DBResearch. Narrow basic balance is current account balance + FDI flows

An unfavourable external balance is set to drive JPY sharply lower

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

33

Japan’s outbound M&A activity has increased substantially and will continue to rise on Abenomics

0

5000

10000

15000

20000

25000

30000

1995 1998 2001 2004 2007 2010 2013

Japanese outbound M&A has risen substantially in recent years

Source: Dealogic, Deutsche Bank Research

Deal value

(USD mn)

M&A picked up after the earthquake in 2011, but

much of it was defensive

− Purchase of energy assets overseas after

shutdown of nuclear supply

− To diversify supply chain away from Japan

Since the introduction of Abenomics, M&A activity

has been much more broad-based

− Purchase of Sprint Nextel by Softbank for USD

36bn; Japan’s largest outbound M&A deal

− Purchase of Thai bank Ayudhya by Mitsubishi

UFJ for USD 6bn

Inbound M&A is also occurring: Applied Materials

Inc. is completing a purchase of Tokyo Electron Ltd.

for USD 9.4bn

Expect M&A activity will continue to rise on

Abenomics

− Japanese firms can borrow much more cheaply

than corporates in other countries (as much as

3-4X lower)

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

34

Five common objections to Abenomics can be countered

Objection Arguments in response

1. Japan’s demographics will curb

potential growth

Empirical evidence finds little correlation between demographics and economic

growth in developed economies

In some ways, Japan is returning to its historical norm with a dependency ratio that

prevailed during the mid-20th century

In general, demographic arguments can be too deterministic.

2. As inflation rises, investors will

flee the bond market, triggering a

sovereign debt crisis

Capital flight is unlikely in large and socially stable economies

95% of JGBs are owned by domestic institutions.

The BoJ has signaled its willingness to adjust asset purchases to cap JGB volatility

and curb an excessive rise in yields as long as the government delivers credible

fiscal consolidation

In fact, reflation is the key to debt stabilisation as higher growth leads to higher

government revenues. Yields will eventually rise, but along with growth, as in a

conventional recovery

3. Inflation without wage growth will

cripple household finances

Old people with fixed assets do not gain significantly from Abenomics and may even

lose. However, Japanese households have USD 16tn in assets (half of which is in

deposits and cash) to cushion them through the transition

Presently, deflationary expectations, not income, is the major constraint on spending

4. Structural reforms will not be

pursued with enough vigour to

boost growth

Reforms have failed to boost growth in the past due to a lack of aggregate demand

Conventional macro policy mistakes have been bigger drags on growth than

excessive regulation

5. Sales tax hikes in 2014* will

cause premature fiscal drag (as in

1997)

The 1997 fiscal drag was broader and coincided with the Asian financial crisis and

resurgent domestic financial instability. It was also implement at a time of much

weaker domestic growth than today

* Note: Planned sales tax increase of 3% in 2014

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

DB forecasts

35

GDP growth (%)

2012 2013F 2014F 2015F

Global 3.0 2.8 3.7 3.9

US 2.8 1.8 3.2 3.5

Eurozone -0.6 -0.2 1.2 1.4

Germany 0.7 0.5 1.5 1.4

Japan 2.0 1.8 1.0 1.2

UK 0.2 1.5 2.5 2.0

China 7.8 7.8 8.6 8.2

India 4.1 3.7 5.3 6.0

EM (Asia) 5.9 5.9 6.9 6.7

EM (Lat Am) 2.8 2.5 2.9 3.2

EM (CEEMEA) 2.7 2.4 3.4 3.8

EM 4.7 4.5 5.4 5.5

DM 1.4 1.2 2.2 2.4

* CPI (%) forecasts are period averages

CEEMEA: Czech Rep., Hungary, Poland, Russia, Turkey, South Africa, Israel, Romania, Kazakhstan,

Ukraine, Egypt, Saudi Arabia and UAE

LATAM: Argentina, Brazil, Chile, Colombia, Mexico, Venezuela

ASIA: China, Hong Kong, India, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan, Thailand

DM: US, Japan, Euro area, UK, Denmark, Norway, Sweden, Canada, Australia, New Zealand, Switzerland

Key market metrics

Current Q4-13 Q1-14 Q3-14

US 10Y yield (%) 2.59 2.50 2.75 3.00

EUR 10Y yield (%) 1.87 2.20 2.30 2.50

EUR/USD 1.367 1.25 1.23 1.18

USD/JPY 97.9 110 111 115

S&P 500 1,733 1,750 - 1,850#

Stoxx 600 316 315* - 345#

Gold (USD/oz) 1,320 1,350 1,350 1,325

Oil WTI (USD/bbl) 100.7 105 105 95

Oil Brent (USD/bbl) 109.0 110 110 105 #end 2014. * reached in September

Current prices as 22.00GMT, 17 October

CPI inflation, YoY* (%)

2012 2013F 2014F 2015F

US 2.1 1.7 2.6 2.3

Eurozone 2.5 1.5 1.4 1.5

Japan 0.0 0.2 2.7 1.5

UK 2.8 2.7 2.2 2.0

China 2.6 2.5 3.5 3.0

India 7.5 5.9 5.4 6.5

Central Bank policy rate (%)

Current Q4-13 Q1-14 Q3-14

US 0-0.25 0-0.25 0-0.25 0-0.25

Eurozone 0.50 0.50 0.50 0.50

Japan 0-0.1 0-0.1 0-0.1 0-0.1

UK 0.50 0.50 0.50 0.50

China 3.00 3.00 3.00 3.25

India 7.50 7.50 7.25 6.75

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

Appendix 1 Important Disclosures Additional Information Available upon Request

Analyst Certification

This report covers more than one security and was contributed to by more than one analyst. The views expressed in this report accurately reflect the

views of each contributor to this compendium report. In addition, each contributor has not and will not receive any compensation for providing a specific

recommendation or view in this compendium report. Raj Hindocha/Marcos Arana

Attribution

The Author of this report wishes to acknowledge the contributions made by Shakun Guleria, Pravin Kumar and Varun Narang, employees of Infosys

Technologies Ltd., a third party provider to Deutsche bank offshore research support services.

For disclosures pertaining to recommendations or estimates made on a security mentioned in this report, please see the most recently

published company report or visit our global disclosure look-up page on our website at

http://gm.db.com/ger/disclosure/DisclosureDirectory.eqsr.

36

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

37

Regulatory Disclosures

1. Important Additional Conflict Disclosures

Aside from within this report, important conflict disclosures can also be found at https://gm.db.com/equities under the “Disc losures Lookup” and “Legal” tabs. Investors are strongly

encouraged to review this information before investing.

2. Short-Term Trade Ideas Deutsche Bank equity research analysts sometimes have shorter-term trade ideas (known as SOLAR ideas) that are consistent or inconsistent with Deutsche Bank’s existing longer term

ratings. These trade ideas can be found at the SOLAR link at http://gm.db.com.

3. Country-Specific Disclosures

Australia and New Zealand: This research, and any access to it, is intended only for "wholesale clients" within the meaning of the Australian Corporations Act and New Zealand Financial

Advisors Act respectively.

Brazil: The views expressed above accurately reflect personal views of the authors about the subject company(ies) and its(their) securities, including in relation to Deutsche Bank. The

compensation of the equity research analyst(s) is indirectly affected by revenues deriving from the business and financial transactions of Deutsche Bank. In cases where at least one Brazil

based analyst (identified by a phone number starting with +55 country code) has taken part in the preparation of this research report, the Brazil based analyst whose name appears first

assumes primary responsibility for its content from a Brazilian regulatory perspective and for its compliance with CVM Instruction # 483

EU countries: Disclosures relating to our obligations under MiFiD can be found at http://www.globalmarkets.db.com/riskdisclosures.

Japan: Disclosures under the Financial Instruments and Exchange Law: Company name - Deutsche Securities Inc. Registration number - Registered as a financial instruments dealer by the

Head of the Kanto Local Finance Bureau (Kinsho) No. 117. Member of associations: JSDA, Type II Financial Instruments Firms Association, The Financial Futures Association of Japan,

Japan Securities Investment Advisers Association. This report is not meant to solicit the purchase of specific financial instruments or related services. We may charge commissions and fees

for certain categories of investment advice, products and services. Recommended investment strategies, products and services carry the risk of losses to principal and other losses as a

result of changes in market and/or economic trends, and/or fluctuations in market value. Before deciding on the purchase of financial products and/or services, customers should carefully

read the relevant disclosures, prospectuses and other documentation. "Moody's", "Standard & Poor's", and "Fitch" mentioned in this report are not registered credit rating agencies in Japan

unless “Japan” or "Nippon" is specifically designated in the name of the entity.

Malaysia: Deutsche Bank AG and/or its affiliate(s) may maintain positions in the securities referred to herein and may from t ime to time offer those securities for purchase or may have an

interest to purchase such securities. Deutsche Bank may engage in transactions in a manner inconsistent with the views discussed herein.

Russia: This information, interpretation and opinions submitted herein are not in the context of, and do not constitute, any appraisal or evaluation activity requiring a license in the Russian

Federation.

Risks to Fixed Income Positions Macroeconomic fluctuations often account for most of the risks associated with exposures to instruments that promise to pay f ixed or variable interest rates. For an investor that is long fixed

rate instruments (thus receiving these cash flows), increases in interest rates naturally lift the discount factors applied to the expected cash flows and thus cause a loss. The longer the

maturity of a certain cash flow and the higher the move in the discount factor, the higher will be the loss. Upside surprises in inflation, fiscal funding needs, and FX depreciation rates are

among the most common adverse macroeconomic shocks to receivers. But counterparty exposure, issuer creditworthiness, client segmentation, regulation (including changes in assets

holding limits for different types of investors), changes in tax policies, currency convertibility (which may constrain currency conversion, repatriation of profits and/or the liquidation of

positions), and settlement issues related to local clearing houses are also important risk factors to be considered. The sensitivity of fixed income instruments to macroeconomic shocks may

be mitigated by indexing the contracted cash flows to inflation, to FX depreciation, or to specified interest rates – these are common in emerging markets. It is important to note that the index

fixings may -- by construction -- lag or mis-measure the actual move in the underlying variables they are intended to track. The choice of the proper fixing (or metric) is particularly important

in swaps markets, where floating coupon rates (i.e., coupons indexed to a typically short-dated interest rate reference index) are exchanged for fixed coupons. It is also important to

acknowledge that funding in a currency that differs from the currency in which the coupons to be received are denominated carries FX risk. Naturally, options on swaps (swaptions) also bear

the risks typical to options in addition to the risks related to rates movements.

Deutsche Bank Research The House View – 18 October 2013, [email protected], +44 207 545 8465

38

Global Disclaimer The information and opinions in this report were prepared by Deutsche Bank AG or one of its affiliates (collectively "Deutsche Bank"). The information herein is believed to be reliable and has been obtained from public sources believed to be reliable.

Deutsche Bank makes no representation as to the accuracy or completeness of such information.

Deutsche Bank may engage in securities transactions, on a proprietary basis or otherwise, in a manner inconsistent with the view taken in this research report. In addition, others within Deutsche Bank, including strategists and sales staff, may take a view

that is inconsistent with that taken in this research report.

Opinions, estimates and projections in this report constitute the current judgment of the author as of the date of this report. They do not necessarily reflect the opinions of Deutsche Bank and are subject to change without notice. Deutsche Bank has no

obligation to update, modify or amend this report or to otherwise notify a recipient thereof in the event that any opinion, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. Prices and availability of financial instruments are

subject to change without notice. This report is provided for informational purposes only. It is not an offer or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. Target prices are inherently

imprecise and a product of the analyst judgment.

As a result of Deutsche Bank’s March 2010 acquisition of BHF-Bank AG, a security may be covered by more than one analyst within the Deutsche Bank group. Each of these analysts may use differing methodologies to value the security; as a result, the

recommendations may differ and the price targets and estimates of each may vary widely.

In August 2009, Deutsche Bank instituted a new policy whereby analysts may choose not to set or maintain a target price of certain issuers under coverage with a Hold rating. In particular, this will typically occur for "Hold" rated stocks having a market cap

smaller than most other companies in its sector or region. We believe that such policy will allow us to make best use of our resources. Please visit our website at http://gm.db.com to determine the target price of any stock.

The financial instruments discussed in this report may not be suitable for all investors and investors must make their own informed investment decisions. Stock transactions can lead to losses as a result of price fluctuations and other factors. If a financial

instrument is denominated in a currency other than an investor's currency, a change in exchange rates may adversely affect the investment. Past performance is not necessarily indicative of future results. Deutsche Bank may with respect to securities

covered by this report, sell to or buy from customers on a principal basis, and consider this report in deciding to trade on a proprietary basis.

Derivative transactions involve numerous risks including, among others, market, counterparty default and illiquidity risk. The appropriateness or otherwise of these products for use by investors is dependent on the investors' own circumstances including their

tax position, their regulatory environment and the nature of their other assets and liabilities and as such investors should take expert legal and financial advice before entering into any transaction similar to or inspired by the contents of this publication.

Trading in options involves risk and is not suitable for all investors. Prior to buying or selling an option investors must review the "Characteristics and Risks of Standardized Options," at http://www.theocc.com/components/docs/riskstoc.pdf . If you are unable

to access the website please contact Deutsche Bank AG at +1 (212) 250-7994, for a copy of this important document.

The risk of loss in futures trading and options, foreign or domestic, can be substantial. As a result of the high degree of leverage obtainable in futures and options trading losses may be incurred that are greater than the amount of funds initially deposited

Unless governing law provides otherwise, all transactions should be executed through the Deutsche Bank entity in the investor's home jurisdiction. In the U.S. this report is approved and/or distributed by Deutsche Bank Securities Inc., a member of the

NYSE, the NASD, NFA and SIPC. In Germany this report is approved and/or communicated by Deutsche Bank AG Frankfurt authorized by the BaFin. In the United Kingdom this report is approved and/or communicated by Deutsche Bank AG London, a

member of the London Stock Exchange and regulated by the Financial Conduct Authority for the conduct of investment business in the UK and authorized by the BaFin. This report is distributed in Hong Kong by Deutsche Bank AG, Hong Kong Branch, in

Korea by Deutsche Securities Korea Co. This report is distributed in Singapore by Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch, and recipients in Singapore of this report are to contact Deutsche Bank AG,

Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch in respect of any matters arising from, or in connection with, this report. Where this report is issued or promulgated in Singapore to a person who is not an accredited investor, expert

investor or institutional investor (as defined in the applicable Singapore laws and regulations), Deutsche Bank AG, Singapore Branch or Deutsche Securities Asia Limited, Singapore Branch accepts legal responsibility to such person for the contents of this

report. In Japan this report is approved and/or distributed by Deutsche Securities Inc. The information contained in this report does not constitute the provision of investment advice. In Australia, retail clients should obtain a copy of a Product Disclosure

Statement (PDS) relating to any financial product referred to in this report and consider the PDS before making any decision about whether to acquire the product. Deutsche Bank AG Johannesburg is incorporated in the Federal Republic of Germany

(Branch Register Number in South Africa: 1998/003298/10). Additional information relative to securities, other financial products or issuers discussed in this report is available upon request. This report may not be reproduced, distributed or published by any

person for any purpose without Deutsche Bank's prior written consent. Please cite source when quoting.

Copyright © 2013 Deutsche Bank Securities Inc.