slides on market structure

TRANSCRIPT

A primer on US equity market structure

Prepared for KAIST programWinter 2004

Agenda

The NYSE The Nasdaq Stock Market Inc. Regional Exchanges ATSs/ECNs Competition within and between markets

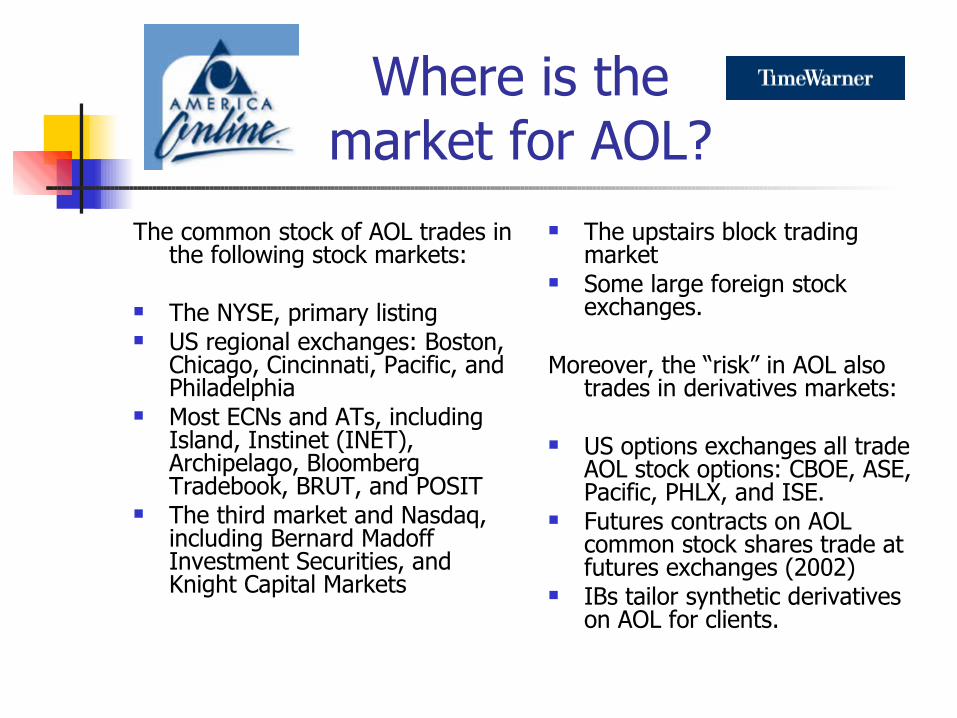

Where is the market for AOL?

The common stock of AOL trades in the following stock markets:

The NYSE, primary listing US regional exchanges: Boston,

Chicago, Cincinnati, Pacific, and Philadelphia

Most ECNs and ATs, including Island, Instinet (INET), Archipelago, Bloomberg Tradebook, BRUT, and POSIT

The third market and Nasdaq, including Bernard Madoff Investment Securities, and Knight Capital Markets

The upstairs block trading market

Some large foreign stock exchanges.

Moreover, the “risk” in AOL also trades in derivatives markets:

US options exchanges all trade AOL stock options: CBOE, ASE, Pacific, PHLX, and ISE.

Futures contracts on AOL common stock shares trade at futures exchanges (2002)

IBs tailor synthetic derivatives on AOL for clients.

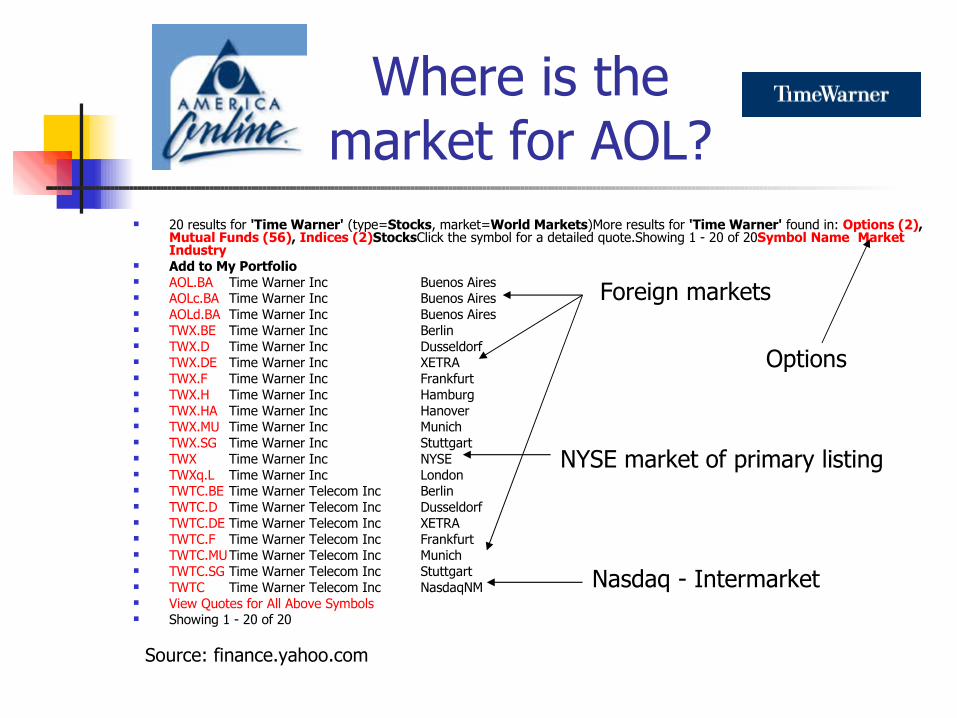

Where is the market for AOL?

20 results for 'Time Warner' (type=Stocks, market=World Markets)More results for 'Time Warner' found in: Options (2), Mutual Funds (56), Indices (2)StocksClick the symbol for a detailed quote.Showing 1 - 20 of 20Symbol Name Market Industry

Add to My Portfolio AOL.BA Time Warner Inc Buenos Aires AOLc.BA Time Warner Inc Buenos Aires AOLd.BA Time Warner Inc Buenos Aires TWX.BE Time Warner Inc Berlin TWX.D Time Warner Inc Dusseldorf TWX.DE Time Warner Inc XETRA TWX.F Time Warner Inc Frankfurt TWX.H Time Warner Inc Hamburg TWX.HA Time Warner Inc Hanover TWX.MU Time Warner Inc Munich TWX.SG Time Warner Inc Stuttgart TWX Time Warner Inc NYSE TWXq.L Time Warner Inc London TWTC.BE Time Warner Telecom Inc Berlin TWTC.D Time Warner Telecom Inc Dusseldorf TWTC.DE Time Warner Telecom Inc XETRA TWTC.F Time Warner Telecom Inc Frankfurt TWTC.MUTime Warner Telecom Inc Munich TWTC.SG Time Warner Telecom Inc Stuttgart TWTC Time Warner Telecom Inc NasdaqNM View Quotes for All Above Symbols Showing 1 - 20 of 20

NYSE market of primary listing

Foreign markets

Nasdaq - Intermarket

Options

Source: finance.yahoo.com

The New York Stock Exchange

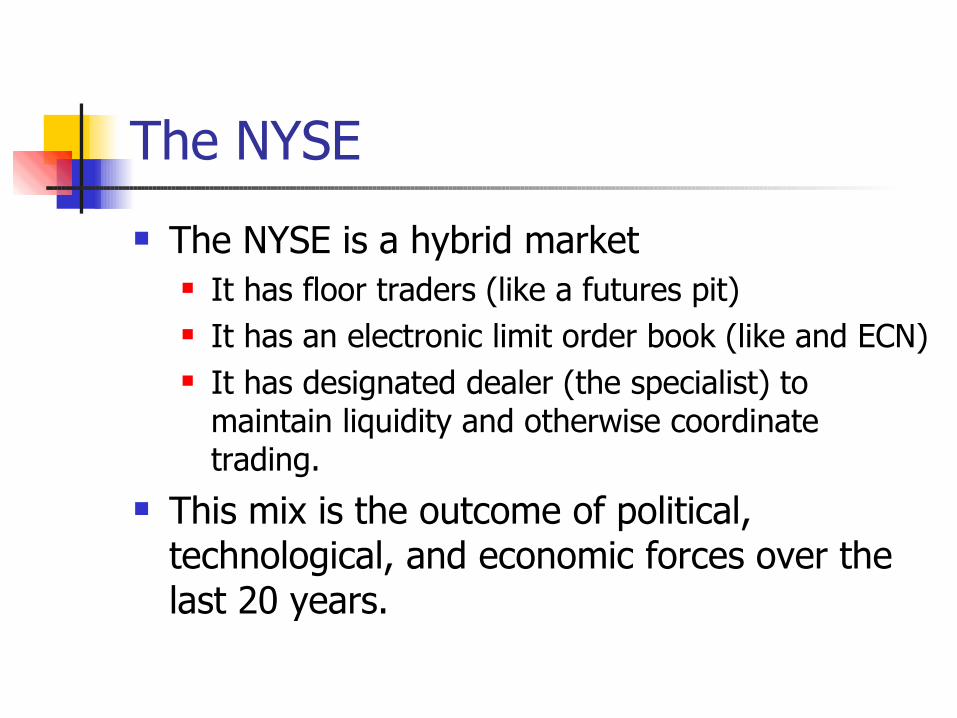

The NYSE

The NYSE is a hybrid market It has floor traders (like a futures pit) It has an electronic limit order book (like and ECN) It has designated dealer (the specialist) to

maintain liquidity and otherwise coordinate trading.

This mix is the outcome of political, technological, and economic forces over the last 20 years.

What does the NYSE do? Trading and trading services

The NYSE charges (directly and indirectly) for trades that occur and for software supplied to its members.

Listing To be listed on the NYSE, a corporation must meet/maintain certain

financial standards and pay listing fees. An NYSE listing is a certification that enhances a firm’s credibility.

Information The NYSE is (indirectly) an information vendor.

Regulation The NYSE monitors and regulates the trading activity of its

members. Through the listing relationship and the listing standards, it can

affect corporate governance behavior.

NYSE sources of revenue

Organization and governance The NYSE is a “mutual” organization, a not-for-profit

corporation owned by its members. A membership is a “seat” = trading privileges + ownership

rights. There are 1,366 seats. Last sale price (2/25/2004) was $1.5

million. The bid is $1.45m and the offer $1.8m.

The NYSE recently considered de-mutualization (conversion to for-profit form with shareholders), but decided against it.

Governed by a board of directors and various committees, which generally have public representation.

In practice, the NYSE represents a balance of diverse powerful constituencies.

Richard A. Grasso In 2003, there was a scandal involving the compensation

package of the Chairman of the NYSE, Richard A. Grasso. His total pay package of some $140 million dollars was leaked to

the media and the membership. Grasso was eventually forced to resign from his post

(9/17/2003), and an interim chairman, Mr. John Reed, was appointed. He was paid $1.00 per year!!!

Earlier in January, Mr. John Thain, formerly of Goldman Sachs, was recruited to take over the chairmanship of the NYSE.

Governance changes have been implemented to reduce potential conflicts of interest.

Physical layout of the floor

Trading in a particular stock takes place at a particular post.

Posts are arranged around horse-hoe shaped trading booths.

Booths are arranged around the trading floor. Broker booths are arranged around the

perimeter of the floor. A broker (e.g., Merrill) will have one or more

broker booths.

At the post

The “crowd”: one or more floor brokers

Specialist work station*Specialist’s clerk

Specialists

*In January, 2002, theExchange released NYSEOpenBookTM.

The hybrid structure of trading

The specialist work station contains the limit order book. Most orders are delivered electronically to the work station. It looks roughly like the screen of an ECN, and has similar

functionality. The crowd comprises floor brokers representing

customer orders and (less often) their own orders. The crowd is similar to the crowd in a futures pit.

One broker has a unique role – the specialist The specialist’s key function is to provide liquidity when no

one else is willing to do so. In this respect, the specialist is acting as a dealer.

How do orders execute?

At the NYSE, even marketable orders do not automatically execute. The specialist or the clerk must hit a key to

complete the trade. Automatic executions are available for:

Odd lot orders (< 100 shares) Market orders designated as “NYSE Direct.” NYSE Direct and odd-lot orders are executed

immediately against the specialist’s account. Order size is max 1,099 shares, but this size limit is

about the be increased very soon…

What do floor brokers do?

Floor brokers are members (seat holders). Floor broker may work for a large brokerage firm

(e.g., Merrill), or they may be independent. Floor brokers manually handle large almost

exclusively institutional orders. They trade these orders manually by representing

them in the crowd. They may also delegate the execution to the

specialist. Floor brokers also gather information, and help bring

out latent liquidity.

What does the specialist do?

The specialist is the designated dealer. There is one per stock, but a single specialist may be the

designated dealer for as many as a dozen stocks. The specialist is physically present at the stock’s

post. The specialist is responsible for “maintaining an

orderly market.” Specialist posts bid and ask quotes, and sizes. Specialist affirmative obligations

Narrow spreads, price continuity, act as agent. Specialist negative obligations

Yield to public customers, discouraged from trading.

Specialist-SEC settlement 2004

On February 19, 2004, five major specialist firms (there are only 9!!!) reached a settlement with the SEC for at total of $240million. LaBranche & Co. Van Der Moolen Holdings. Fleet Specialists Bear Wagner Specialists Spear, Leeds & Kellogg

The charges against the firms were that they had engaged in quote-matching. They essentially traded ahead of public limit orders by

improving the price by one penny.

The Nasdaq Stock Market Inc.

Better for companiesBetter for investors

The Nasdaq Stock Market Inc.

The Nasdaq Stock Market is NOT (yet) an Exchange. Nasdaq has applied to become recognized as an exchange,

but even though the application has been pending for almost 4 years, it has not yet been approved.

The Nasdaq Stock Market is a dealer market. Each stock has multiple market makers posting best bids

and offers, and sizes, for a particular stock. The market is decentralized, and all order routing

and trade execution is done electronically. The market for trading Nasdaq-listed stocks is highly

contested.

Nasdaq players Market makers have maximum access to Nasdaq trading

facilities. They alone are allowed to post bid and offer quotes.

Any Nasdaq member may execute a trade. A market maker must satisfy capital rules and maintain a market

presence. Order entry firms collect customer orders.

They route orders to market makers (but don’t make markets themselves).

ECN’s (electronic communication networks), e.g., Island. In principle, and ECN can function independently (standalone) The ECN’s rely on Nasdaq systems to display their quotes, report

their trades, and access other market participants. The integration of ECN’s into Nasdaq is frequently awkward and

contentious.

What does Nasdaq do? Trading and trading services

Nasdaq charges (directly and indirectly) for trades that occur and for software supplied to its members.

Listing To be listed on the Nasdaq, a corporation must meet/maintain

certain financial standards and pay listing fees. A Nasdaq listing is a certification that enhances a firm’s credibility.

Information The Nasdaq is (indirectly) an information vendor.

Regulation The Nasdaq monitors and regulates the trading activity of its

members. Regulation is outsourced to NASD-R. Through the listing relationship and the listing standards, it can

affect corporate governance behavior.

Nasdaq’s trading platform Nasdaq’s trading platform is called SuperMontage. It is an extremely fast, all computerized, trading system where

all marketable orders are executed automatically. Each registered market maker has to submit their top of file to

the system. This can be either the dealer’s own bid and ask quotes, the best

limit buy order and the best limit sell order, or a combination of both.

Market makers can submit their interest at multiple price levels. Market makers can preference, and internalize trades through the

system. The system allows anonymous orders, as well as orders with

“hidden” size. Order-entry firms may also enter their orders to the system. The SuperMontage system is NOT a central limit order book.

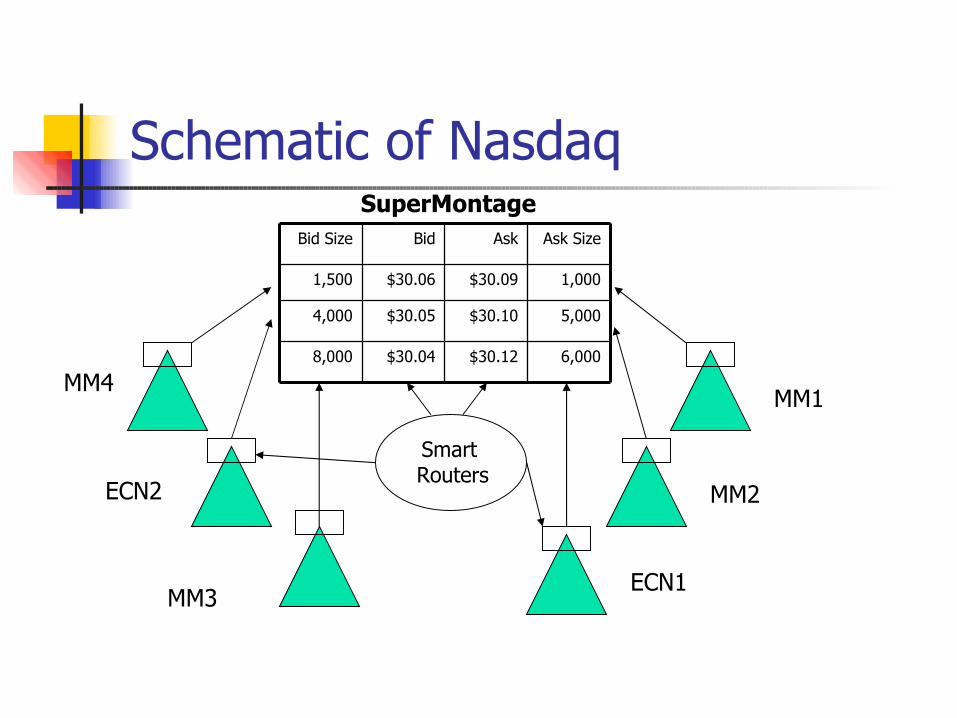

Schematic of Nasdaq

6,000$30.12$30.048,000

5,000$30.10$30.054,000

1,000$30.09$30.061,500

Ask SizeAskBidBid Size

SuperMontage

MM1

MM2

ECN1MM3

ECN2

MM4

Smart Routers

The Nasdaq trading networkNASDAQ’s inclusive structure includes market maker firms, ECNs and regional stock exchanges. There are over 400 market making firms, linked electronically from all over the globe, that provide capital support to the trading of NASDAQ securities.

Competing Market Makers

• Facilitators of Orderly Market• Independent Dealers Competing for

Orders• Proactive Trading• Research Analysis / Corporate Finance • Institutional Sales / Retail Sales• No Limit to the Number of Participants• Display continuous two-sided firm

quotes

ECNs

Provide order anonymity Provide institutional access Create added competition Bring competitively priced orders into

the marketplace Enhance liquidity

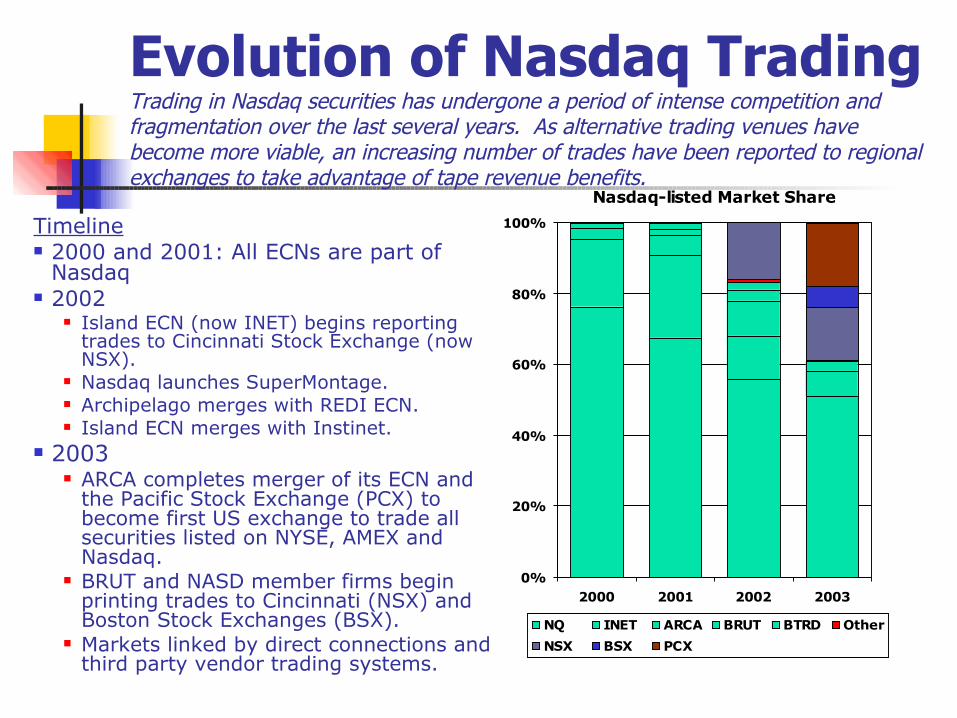

Evolution of Nasdaq TradingTrading in Nasdaq securities has undergone a period of intense competition and fragmentation over the last several years. As alternative trading venues have become more viable, an increasing number of trades have been reported to regional exchanges to take advantage of tape revenue benefits.

Timeline 2000 and 2001: All ECNs are part of

Nasdaq 2002

Island ECN (now INET) begins reporting trades to Cincinnati Stock Exchange (now NSX).

Nasdaq launches SuperMontage. Archipelago merges with REDI ECN. Island ECN merges with Instinet.

2003 ARCA completes merger of its ECN and

the Pacific Stock Exchange (PCX) to become first US exchange to trade all securities listed on NYSE, AMEX and Nasdaq.

BRUT and NASD member firms begin printing trades to Cincinnati (NSX) and Boston Stock Exchanges (BSX).

Markets linked by direct connections and third party vendor trading systems.

Nasdaq-listed Market Share

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003

NQ INET ARCA BRUT BTRD Other

NSX BSX PCX

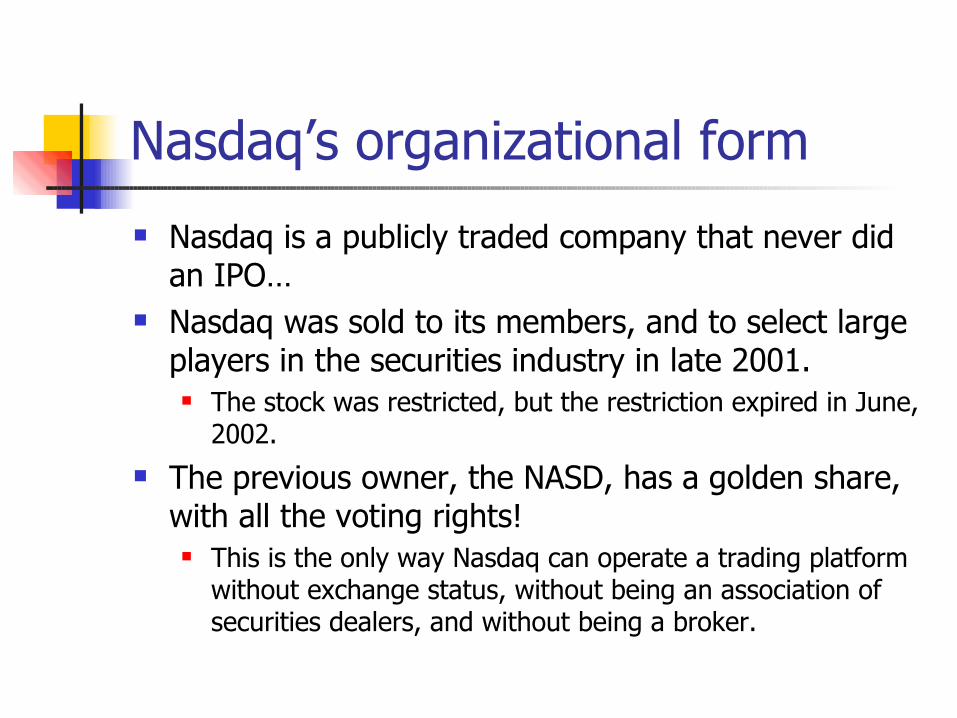

Nasdaq’s organizational form

Nasdaq is a publicly traded company that never did an IPO…

Nasdaq was sold to its members, and to select large players in the securities industry in late 2001. The stock was restricted, but the restriction expired in June,

2002. The previous owner, the NASD, has a golden share,

with all the voting rights! This is the only way Nasdaq can operate a trading platform

without exchange status, without being an association of securities dealers, and without being a broker.

Nasdaq’s stock: NDAQ (OTCBB)

Nasdaq revenue sources

ATSs/ECNs

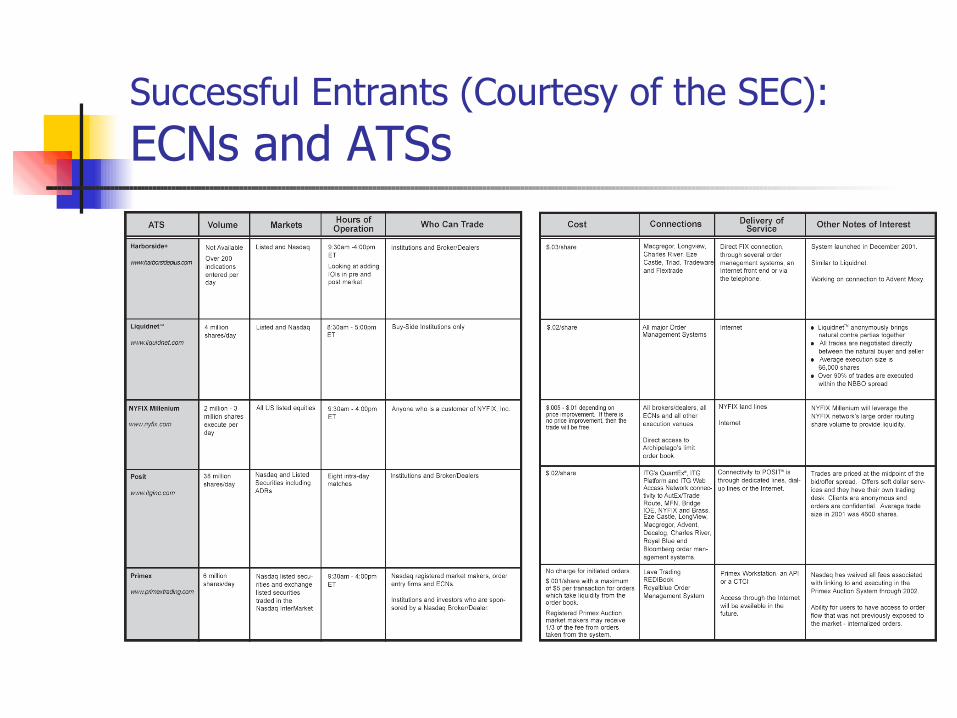

Successful Entrants (Courtesy of the SEC):ECNs and ATSs

Successful Entrants (Courtesy of the SEC):ECNs and ATSs

Source: http://www.capis.com/research/ecn_2002.pdf

Successful Entrants (Courtesy of the SEC):ECNs and ATSs

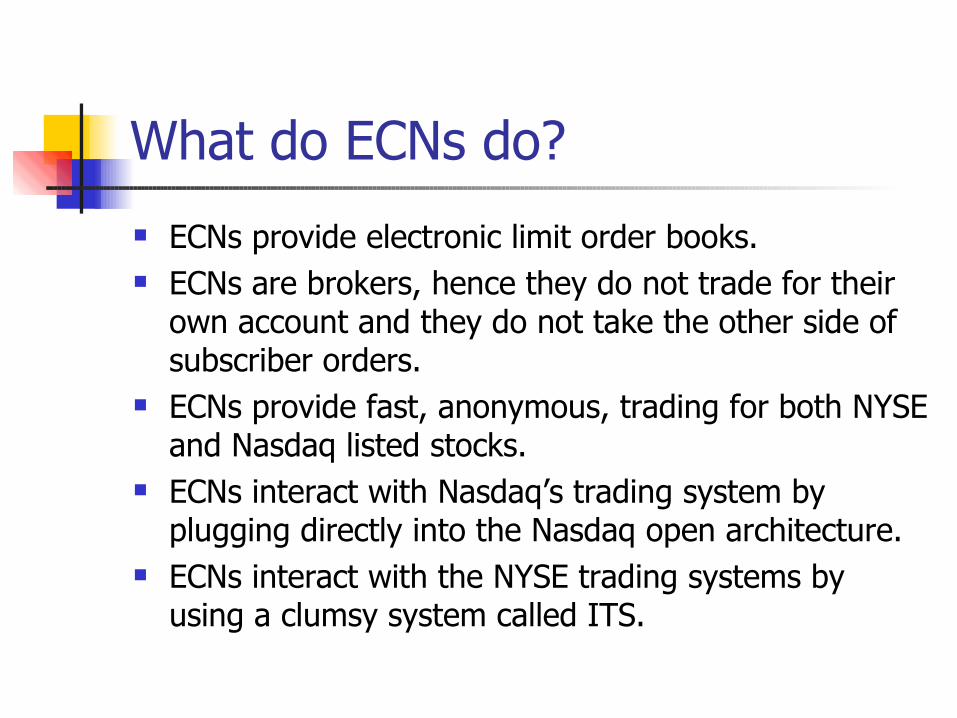

What do ECNs do?

ECNs provide electronic limit order books. ECNs are brokers, hence they do not trade for their

own account and they do not take the other side of subscriber orders.

ECNs provide fast, anonymous, trading for both NYSE and Nasdaq listed stocks.

ECNs interact with Nasdaq’s trading system by plugging directly into the Nasdaq open architecture.

ECNs interact with the NYSE trading systems by using a clumsy system called ITS.

How do ECNs make money?

ECNs charge subscribers an access fee. ECNs pay a liquidity rebate to standing limit orders

that get filled. ECNs charge marketable orders for consuming

liquidity. ECNs have also recently started benefiting from profit

sharing schemes. In return for printing their trades on one of the US regional

exchanges (NSX, BSX), they have negotiated to obtain a share of the resulting market data revenue.

ECNs cannot get listing fees.

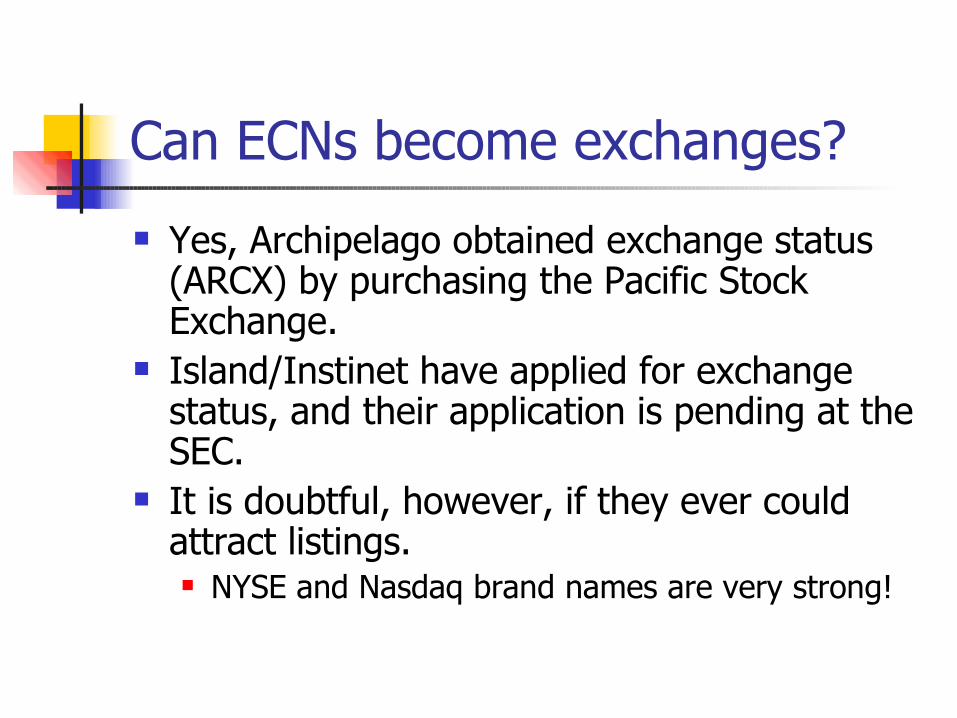

Can ECNs become exchanges?

Yes, Archipelago obtained exchange status (ARCX) by purchasing the Pacific Stock Exchange.

Island/Instinet have applied for exchange status, and their application is pending at the SEC.

It is doubtful, however, if they ever could attract listings. NYSE and Nasdaq brand names are very strong!

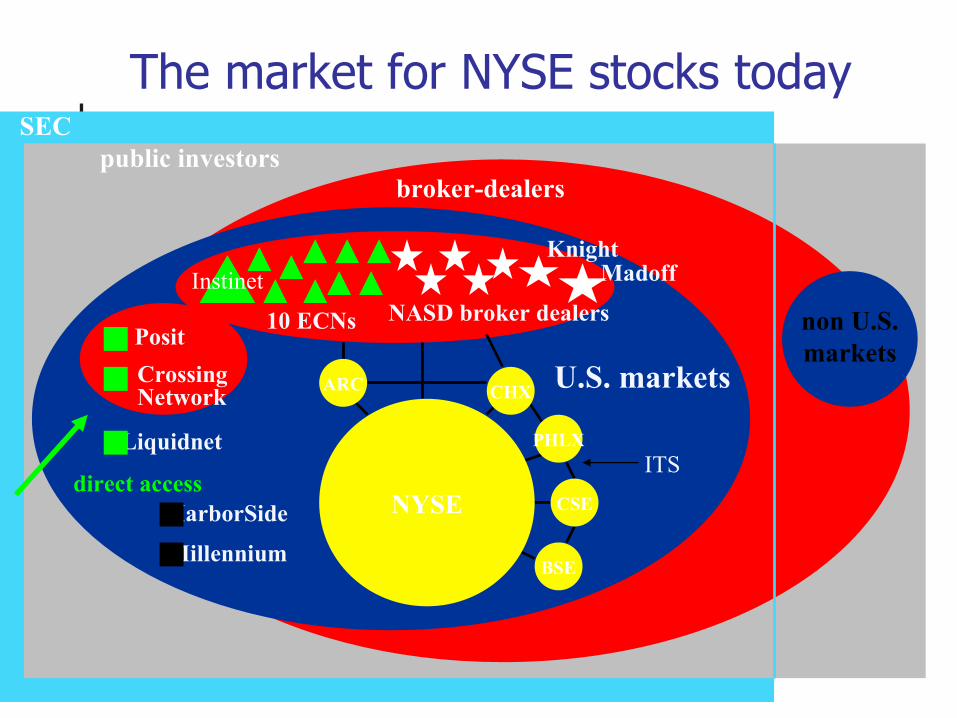

The market for NYSE stocks today

broker-dealerspublic investors

SEC

U.S. markets

direct access

non U.S.markets

Instinet

10 ECNs NASD broker dealers

ARC

NYSE CSE

PHLX

CHX

BSE

ITS

KnightMadoff

Liquidnet

Millennium

HarborSide

Posit

CrossingNetwork

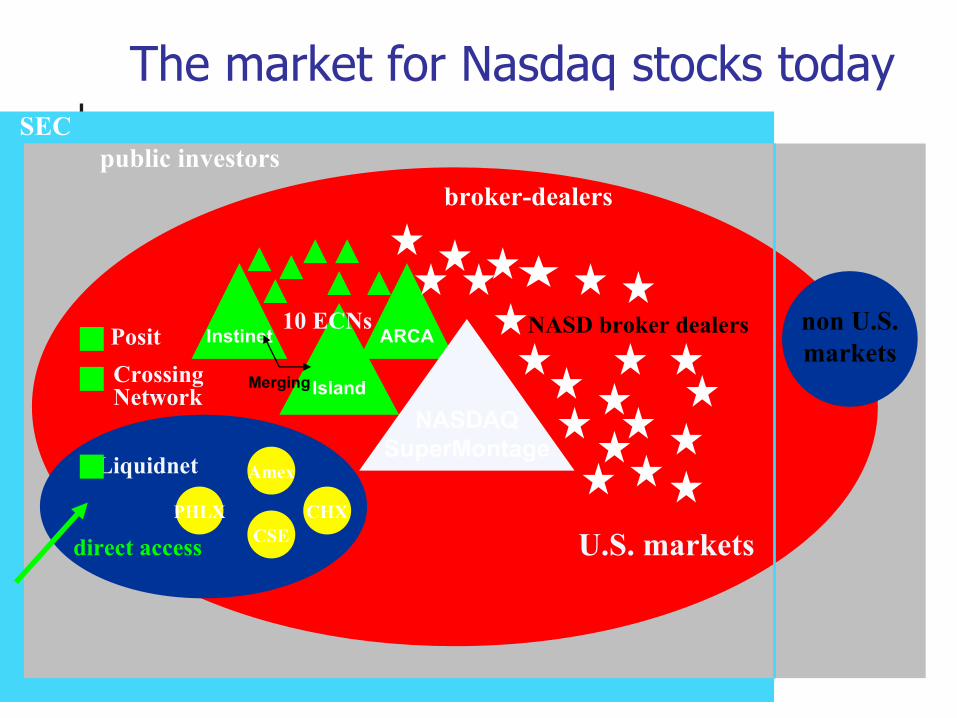

The market for Nasdaq stocks today

broker-dealers

public investorsSEC

non U.S.markets

CHX

direct access

Posit

CrossingNetwork

Liquidnet

U.S. markets

Island

ARCAInstinet

NASDAQSuperMontage

10 ECNs

Amex

CSEPHLX

Merging

NASD broker dealers

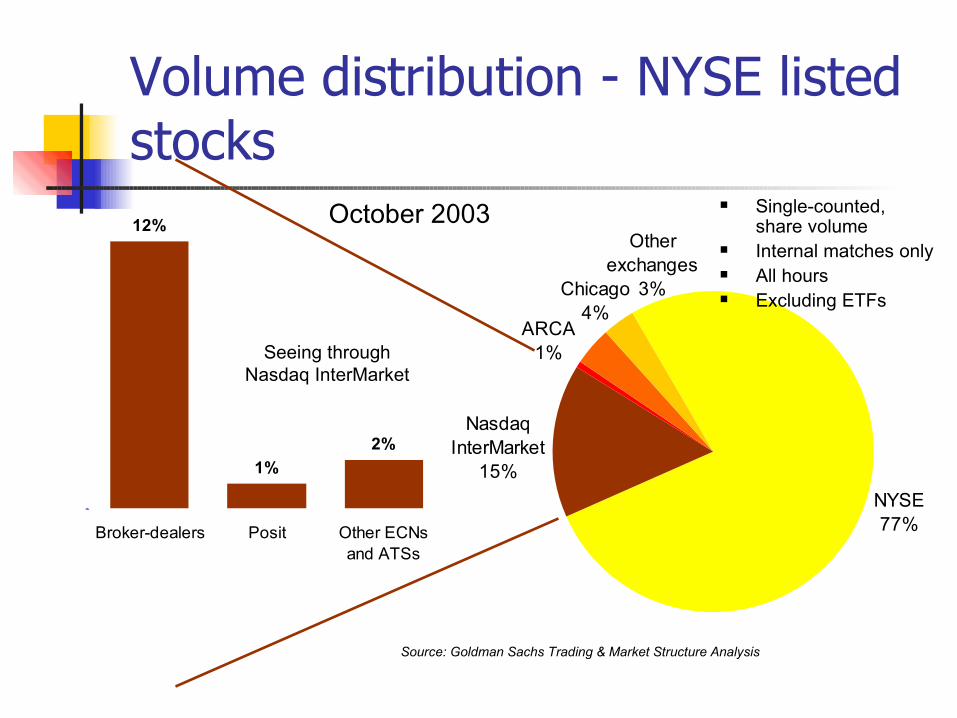

Volume distribution - NYSE listed stocks

Source: Goldman Sachs Trading & Market Structure Analysis

Other exchanges

3%

Nasdaq InterMarket

15%

NYSE77%

ARCA1%

Chicago4%

2%

1%

12%

0%

Broker-dealers Posit Other ECNsand ATSs

Seeing through Nasdaq InterMarket

Single-counted, share volume

Internal matches only All hours Excluding ETFs

October 2003

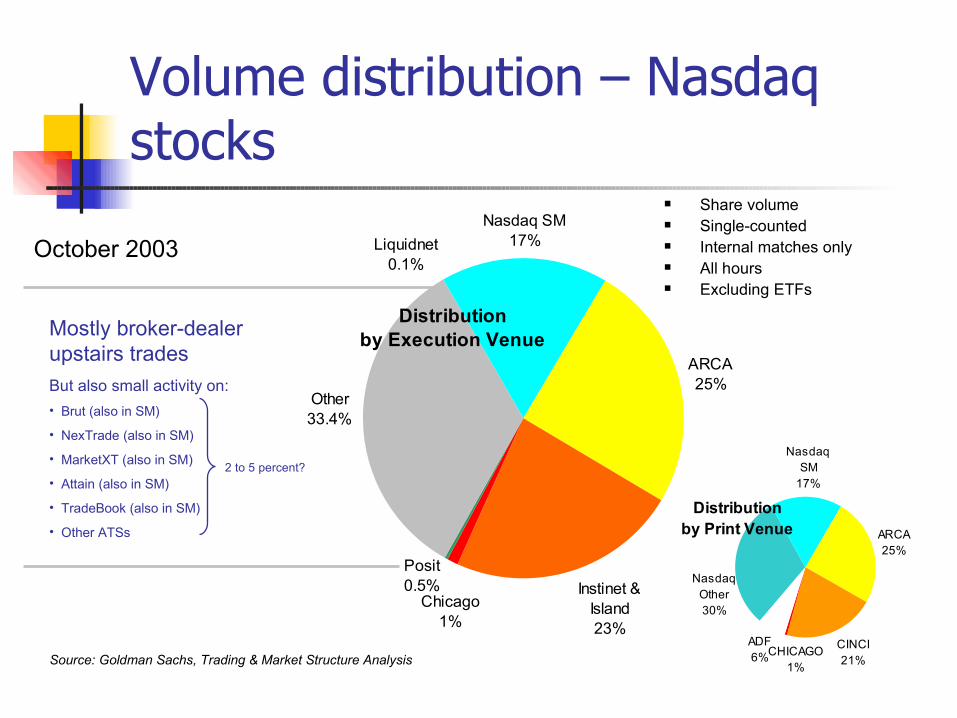

Volume distribution – Nasdaq stocks

Distributionby Print Venue

Nasdaq SM

17%

ARCA25%

CINCI21%

ADF6%

Nasdaq Other30%

CHICAGO1%

Distribution by Execution Venue

Nasdaq SM17%

ARCA25%

Liquidnet0.1%

Instinet & Island23%

Posit0.5%

Chicago1%

Other33.4%

October 2003

Share volume Single-counted Internal matches only All hours Excluding ETFs

Mostly broker-dealer upstairs trades

But also small activity on:

• Brut (also in SM)

• NexTrade (also in SM)

• MarketXT (also in SM)

• Attain (also in SM)

• TradeBook (also in SM)

• Other ATSs

2 to 5 percent?

Source: Goldman Sachs, Trading & Market Structure Analysis

Why have ECNs been successful in Nasdaq but not the NYSE? Nasdaq built its business model on “open architecture.”

Nasdaq made it easy for ECNs/ATSs to link into the Nasdaq trading platform.

The links were fast, which reduced the double jeopardy problem. Order flow externality is weak (all orders are displayed, limited if

any disadvantage from not trading in Nasdaq systems) The NYSE built its business model on defending its market

share. The NYSE made it difficult to trade NYSE listed stocks away from

NYSE trading systems. ITS is antiquated, and extremely slow, exacerbating the double

jeopardy problem. Order flow externality is strong (floor broker orders, non-displayed

liquidity significant, disadvantage from trading off-exchange)

What are the current issues?

On February 26, 2004, the SEC submitted a new market structure proposal, Regulation NMS, for comment.

Trade through rule Fast versus slow markets?

Intermarket Access ITS is antiquated and needs updating!

Sub-penny Pricing Market Data