smes, trade and sustainable growthcepr.org/sites/default/files/events/jansen.pdf · contribution of...

TRANSCRIPT

Marion Jansen, Chief Economist, ITC

At: The Third CEPR-Modena Conference on Growth in Mature Economies: Revisiting the Contribution of Openness 11-12 May 2015

SMEs, Trade and Sustainable

Growth

SMEs: different definitions, different weights

in the economy

There is no universally

accepted definition of Small

and Medium Sized

Enterprise.

In OECD countries, SMEs

represent: Over 95 per cent of the number

of firms

Around 60-70 per cent of

employment

… but the picture differs

across countries

2

r ist

it er d iet

r i desh

h i d h

d i

pt i

3

SMEs: Who are they and how do they

perform in global markets?

Internationalizing: market power,

bargaining power

Local SMEs and Global Policies

SME productivity and

internationalization

SME, Trade and Growth:

What matters: being connected,

meeting standards and challenging the

superstars

4

SMEs: who are they and how to

the perform in global markets?

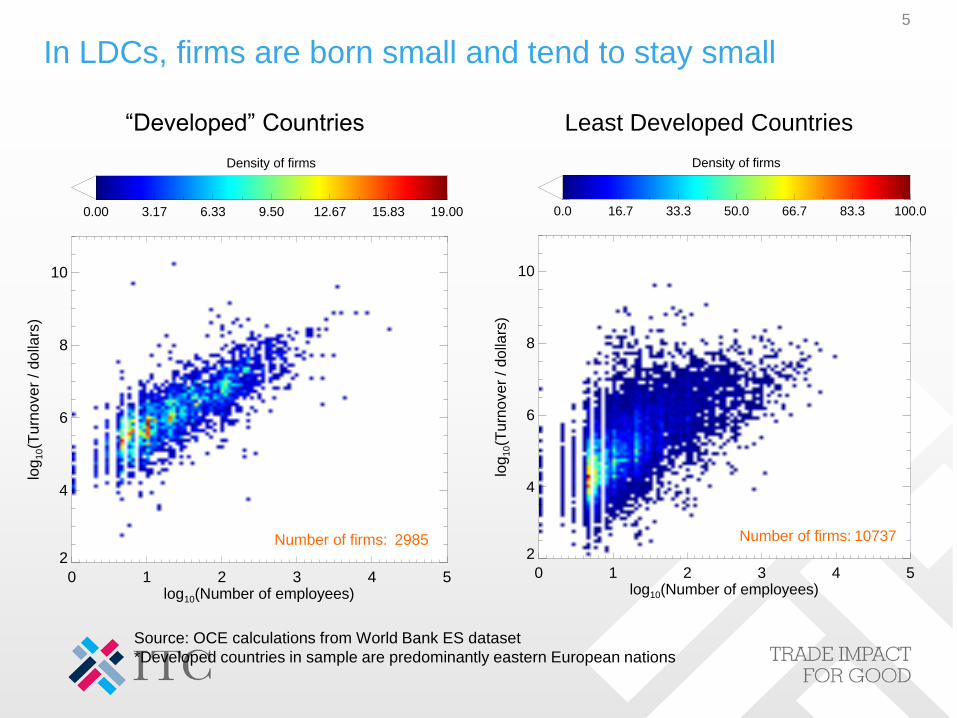

In LDCs, firms are born small and tend to stay small

5

Source: OCE calculations from World Bank ES dataset

*Developed countries in sample are predominantly eastern European nations

Least Developed Countries“De e ped” C u tries

0 1 2 3 4 5log10(Number of employees)

2

4

6

8

10

log

10(T

urn

ove

r /

do

llars

)

0.00 3.17 6.33 9.50 12.67 15.83 19.00

Density of firms

Number of firms: 2985

0 1 2 3 4 5log10(Number of employees)

2

4

6

8

10

log

10(T

urn

ove

r /

do

llars

)

0.0 16.7 33.3 50.0 66.7 83.3 100.0

Density of firms

Number of firms: 10737

Theory predicts it, data confirm it: exporters tend to be larger

in size than non-exporters

6

Source: OCE calculations from World Bank ES dataset

*‘ xp rter’ is defi ed s fir ith % r re f s es exp rted (direct p us i direct)

ExportersNon exporters

0 1 2 3 4 5log10(Number of employees)

2

4

6

8

10

log

10(T

urn

ove

r /

do

llars

)

0 31 62 92 123 154 185

Density of firms

Number of firms: 40734

0 1 2 3 4 5log10(Number of employees)

2

4

6

8

10

log

10(T

urn

ove

r /

do

llars

)

0.0 5.7 11.3 17.0 22.7 28.3 34.0

Density of firms

Number of firms: 8726

si e is the “ r ” i the ser ices sect r

7

Source: OCE calculations from World Bank ES dataset

ServicesManufacturing

0 1 2 3 4 5log10(Number of employees)

2

4

6

8

10

log

10(T

urn

ove

r /

do

llars

)

0.0 15.7 31.3 47.0 62.7 78.3 94.0

Density of firms

Number of firms: 26299

0 1 2 3 4 5log10(Number of employees)

2

4

6

8

10

log

10(T

urn

ove

r /

do

llars

)

0 17 34 52 69 86 103

Density of firms

Number of firms: 18440

SME contribution to exports differs

significantly across EU countries

8

Cernat et al. (2014)

SME contribution to exports differs

significantly across EU countries

9

From Cernat et al. (2014)

10

A “Quic Wi ” i er s f Growth and Inclusiveness?

Strengthening SMEs

SME Characteristics: Productivity and wages

11

• SMEs are generally less

productive than large

firms

• The gap is larger in

developing economies

Relative Productivity & Wage Gaps in Selected South American

and OECD Countries (Large firms=100)

Source: Adapted OECD-ECLAC, 2013, p. 47

0 20 40 60 80 100

France

Spain

Germany

Peru

Chile

Brazil

Argentina

Medium Firm Small Firm

Micro Firm Wage Gap - Micro

Wage Gap - Small Wage Gap - MediumFrom McDermott and Pietrobelli, ITC, forthcoming

SME Characteristics: Productivity and wages

12

• SMEs are generally less productive than large firms

• The gap is larger in developing economies

• A similar pattern is observed with wages

• Working with SMEs will be a challenge, but thereare large gains to be made

Relative Productivity & Wage Gaps in Selected South American

and OECD Countries (Large firms=100)

Source: Adapted OECD-ECLAC, 2013, p. 47

0 20 40 60 80 100

France

Spain

Germany

Peru

Chile

Brazil

Argentina

Medium Firm Small Firm

Micro Firm Wage Gap - Micro

Wage Gap - Small Wage Gap - MediumFrom McDermott and Pietrobelli, ITC, forthcoming

13

Exports Matter for SME Productivity and so do Imports

Internationalizing:

Trade matters for productivity

14

Firms engaging

in trade are more

productive than

firms not

engaging in trade

(no exports, no

imports), with the

exception of

offshore firms

that do not import

Fir s’ pr ducti it d i ter ti tr de status, Tunisia 2000-2010

All firms

Firms with more than one

employee

All Manufact

uring

Non

Manufact

uring

Services

Non exporting and importing firms 0.992*** 0.992*** 0.828*** 0.607*** 1.352***

(0.006) (0.006) (0.001) (0.012) (0.007)

Onshore firms exporting and non importing 0.314*** 0.031*** 0.268*** 0.471*** 0.0532***

(0.021) (0.021) (0.031) (0.053) (0.034)

Onshore firms exporting and importing 1.434*** 1.434*** 1.232*** 1.14*** 1.895***

(0.006) (0.006) (0.013) (0.016) (0.011)

Offshore firms and non importing -0.847*** -0.849*** -0.904*** -0.771*** -0.645***

(0.010) (0.010) (0.017) (0.085) (0.017)

Offshore firms and importing 0.566** 0.566*** 0.382*** 0.920*** 0.909***

(0.005) (0.005) (0.012) (0.095) (0.016)

N 336806 326572 105114 30712 190313

R2 0.200 0.200 0.213 0.18 0.298

From Bhagdadi, ITC, forthcoming

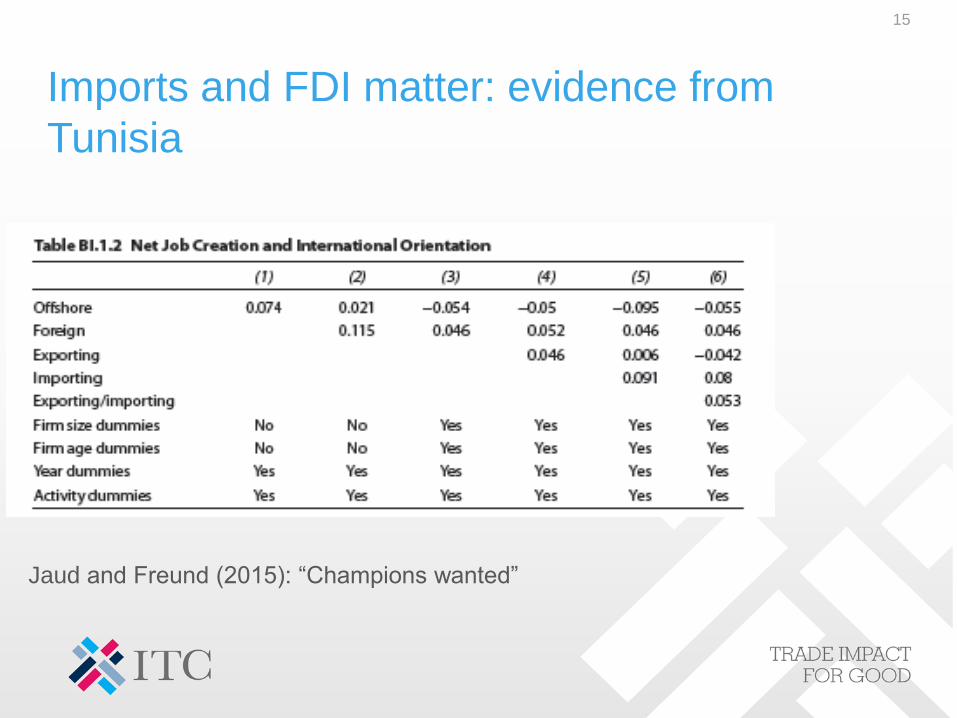

Imports and FDI matter: evidence from

Tunisia

15

Jaud d Freu d ( ): “Ch pi s ted”

Being connected to value chains

matters: evidence from Italy

16

From Giovanetti et al. (2014)

17

Market power and bargaining power

Internationalizing:

Extent of pricing to market: firm size,

efficie c d … r et p erPTM implies that firms react to shocks in the

bilateral exchange-rate by adjusting their FOB

export price in the home currency, rather than by

passing through shocks to consumer prices.

18

(Higher vulnerability

when PTM low: e.g., in

Sweden only a handful

of textile companies

that went bankrupt

during the recent

financial crisis had less

than 50 employees

(Pal et al. 2013))

Bargaining power within value chains

19

Ruffier (forthcoming)

Harvie et al (2010) show that moving up the

value chain (in 7 Asean country and China)

is notably facilitated by:

Higher labour productivity

Higher foreign ownership share

ICT as core business

Having acquired production knowledge

Initial level of supplier capacity will

determine:

the governance approach within the

chain

and will determine gains captured by

suppliers

Gains at the bottom of the chain

are not necessarily high

20

Meeting standards, being connected and challenging the superstars

What matters:

Who challenges the superstar or

“Zid e ith ut te ”

21

From Jaud d Freu d ( ): “Ch pi s ted”

What SMEs ask for: information and

access to finance

22

Source: ITC survey (2015)

SMEs and regulation/standards

Meeting standards or complying with regulation is increasingly a

prerequisite to trade: but compliance is costly.

23

ITC NTM surveys

Results

24Variable Coefficient (Std. Err.)Equation log of competitiveness

Firm-level capacity (readiness to export)

Account 0.147 (0.049)

Dummy for production internationally certified 0.263** (0.041)

Dummy for license issued by foreign company 0.167*** (0.044)

Dummy for company having an Email address 0.503** (0.087)

Dummy for firm having its website 0.194** (0.049)

Credit 0.091* (0.042)

Training 0.166** (0.043)

Variable Coefficient (Std. Err.)

Equation probability of exporting

Firm-level data: determinants of productivity

Account -.233 (0.175)

Dummy for production internationally certified 0.749** (0.079)

Dummy for license issued by foreign company 0.148† (0.087)

Dummy for company having an Email address 0.695** (0.164)

Dummy for firm having its website 0.349** (0.089)

Credit 0.025 (0.080)

Training 0.247** (0.079)

I. Current efficiency

II. Connectivity

III. Capacity to

change

Determinants of international

competitiveness

25

26

A break or the third wave of globalization?

What next:

Trade to GDP elasticity has gone

down

Fernandes, Mattoo and

Ruta (2014):

Trade to GDP elasticity

increased in the 1990s

but then went down

again.

27

SCI val addedSCI employment

VARIABLES (1) (2) (3)(4) (5) (6)

1990s 0.00490 -0.00296 0.00896* -0.00526

2000s 0.000579 0.00491 0.00846* 0.000418

Asia 0.00671 0.0103 0.00561 -0.00790

LAC 0.00630 0.0195* -0.00133 -0.00262

Europe_Other 0.0382*** -0.00365 0.0197** -0.00906

Other 0.0125 0.0289 0.00149 0.0192***

1990s_Asia -0.00575 0.0249*

2000s_Asia -0.00916 0.0171

1990s_LAC -0.0173 0.00726

2000s_LAC -0.0261** -0.00211

1990s_Europe_Ot

her 0.0731*** 0.0602***

2000s_Europe_Ot

her 0.0219 0.0252*

1990s_Other -0.0322 -0.0326***

2000s_Other -0.0208

GDP/cap -0.00818*** -0.00386 -0.00442 -0.00581*** -0.00315* -0.00290

Constant 0.0603*** 0.0460*** 0.0469*** 0.0453*** 0.0438*** 0.0449***

Observations 217 217 217 128 128 128

R-squared 0.096 0.200 0.324 0.136 0.196 0.339

Fiorini et al., (forthcoming)

But China has already started to

move up the value chain

Kaplinski (2011), ILO (2010), recent news on the largest

global speed train producer being Chinese; Also,

simulations suggest that India will be the largest global

provider of skilled workers by 2030.

28

There is evidence that industrialized country

producers moved up the value chain when China

integrated in world markets (e.g. Montfort et al.,

2008, for Belgium)

=> But what will happen in industrialized

countries when China itself moves up the value

chain ???

29

Wh t’s h ppe i the p ic

(research) front?

Increased interest in trade support institutions

Concern about Basel financial rules

Increased demands for more

information/transparency on NTMs

The B20 Task Force on SMEs and

Entrepreneurship

TSIs and SMEs

30

Log of exports of goods and services per capita versus the log of TPO budgets per capita (Lederman, Olarreaga & Payton 2006).

Trade Support Institutions and SMEs

Increase in quantitative research in recent years, e.g.

Lederman, Olarreaga & Payton (2006)

IDB /Christian Volpe Martincus

Olivier Cadot

Fernandes and Mattoo (2014)

Two questions regarding the design of the institutions/interventions:

Nature of public/private collaboration

“Targetting”:Fernandes and Mattoo (2014) find that four year after receiving assistance exports of small firms declined by 65%, while exports of large firms were only 6% higher. However, the exports of medium-sized firms increased by 57%.

31

Concern about new global financial

rules

32

Source: Bank of Japan (2014)

x p e: ccess t fi ce b s d r e fir s i J p . … (is there

eed f r i cre sed “ ter ti e fi ci ”?

Increased demands for more

information/transparency on NTMs

Eg:

EU-wide firm level data collection on firm perceptions of NTMs

EU funded research network (PRONTO) on NTMs

… W O r de F ci it ti A ree e t, t b t ddress

procedural obstacles related to NTMs

33

B20 Task Force on SMEs and

Entrepreneurship

Four major themes:

Access to Markets

Access to Finance

Access to Talent and Entrepreneurship

Innovation

Creation of a World SME Forum?

34

Summing Up

SMEs represent significant share of economic in terms of GDP and employment

There has been an increased interest in SMEs at the policy level in recent years

Firm level data sets make it possible to analyze SME performance empirically: increased and different types of research studies

Three bottlenecks for SME growth are highlighted in literature and policy debate around SME internationalization:

Access to information (including role of TSIs)

Access to finance

Fixed costs related to (implementation of) NTMs

Numerous questions remain, including:

What is the relevance of power relationships notably within GVCs

How to deal with heterogeneity within the SME group (e.g. small vs. medium)

35