soalci insuanr ce in figures 2016 - forsakringskassan.se

TRANSCRIPT

Social Insurance in F

igures 2016

Social Insurance in Figures 2016

Social Insurance in Figures 2016Social insurance is an integral part of the lives of most people. It is of great importance, not just for peoples’ security and well-being, but also for the country’s economy. In 2015, the expenditure on the allow-ances and benefits administered by Försäkringskassan amounted to a total of SEK 225 billion, which corresponds to 5 per cent of Sweden’s gross domestic product (GDP).

Each year, Försäkringskassan publishes the report Social Insurance in Figures, which uses statistics and comments to present a number of allowances and benefits within the framework for the social insur-ance administered and paid by Försäkringskassan. These allowances and benefits are presented in tables, charts and diagrams based on the areas scope and financing of social insurance; registered insured persons; financial security for families and children; financial security in the event of disability; financial security in the event of illness; and other payments. Social Insurance in Figures 2016 also includes a thematic chapter about work injury insurance, which celebrates its centenary in 2016.

FK 141 ISBN 978-91-7500-393-1

Försäkringskassan (Swedish Social Insurance Agency) 2016ISSN: 2000-1703ISBN: 978-91-7500-393-1FK 141Design: Folke JohanssonGraphic production: Kristina MalmIllustrations: Lottie PetterssonPrinters: Lenanders Grafiska AB, 2016Translation: Språkservice Sverige AB, 2016Typeface: Neue Haas Grotesk, Chronicle

Försäkringskassan (Swedish Social Insurance Agency) SE-103 51 StockholmSwedenTel: +46 8 786 90 00E-mail: [email protected] further information about social insurance, please see www.forsakringskassan.se

Social Insurance in Figures 2016 can be ordered from the website www.forsakringskassan.se, and costs SEK 120 excluding VAT, postage and packing.

Foreword

Each year, Försäkringskassan publishes Social Insurance in Figures, which uses statistics and comments to present a number of allowances and benefits that are administered by Försäkringskassan.

Social insurance is an integral part of the lives of most people. It is of great importance, not just for peoples’ security and well- being, but also for the country’s economy. The total expenditure on the allowances and benefits administered by Försäkringskassan amounted to around SEK 225 billion in 2015, or 5 per cent of Sweden’s gross domestic product (GDP).

This year sees the anniversary of Sweden’s oldest social insurance, the work injury insurance. We want to commemorate this with a special thematic chapter that illustrates the development of work injury insurance during 100 years.

Many employees at Försäkringskassan have participated in the work with Social Insurance in Figures 2016. Erik Ahlmark and Olof Lundgren have written the chapter about the financial scope of social insurance, Vedrana Milosevic the chapters about financial security for families and children and financial security in the event of disability, and Ulrik Lidwall the chapters about registered insured persons, financial security in the event of illness and other payments. Fanny Jatko wrote this year’s thematic chapter on the centenary of work injury insurance and is the overall editor of the publication.

Stockholm, May 2016

Ann-Marie Begler Director-General

Contents

Thematic chapter – 100 years of Work Injury Insurance 8

Financial Scope of Social Insurance 26Social security expenditures 26Financing social insurance 30

Registered insured persons 32

Financial security for families and children 34Parental benefit 34Equality bonus 39Temporary parental benefit for care of children 40Temporary parental benefit in connection with birth or adoption 42Temporary parental benefit for contact days 43Temporary parental benefit in connection with the death of a child 44Pregnancy benefit 45Child allowance 46Maintenance support 48Housing allowance 50

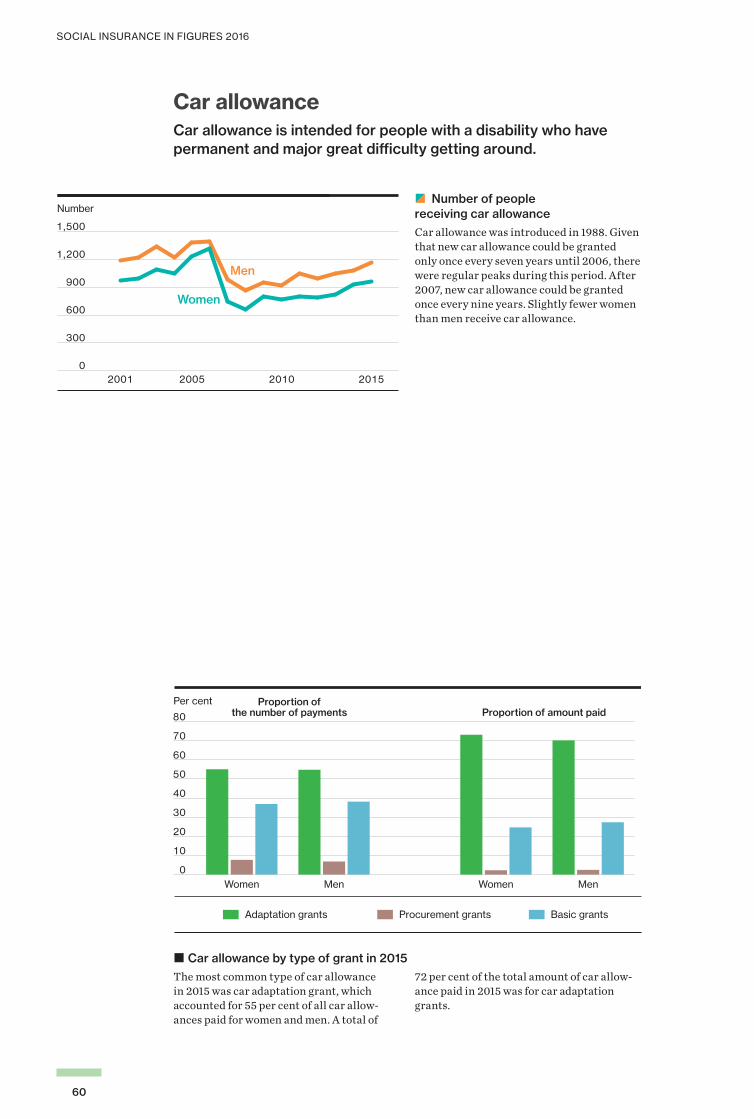

Financial security in the event of disability 52Childcare allowance 52Disability allowance 56Attendance allowance 58Car allowance 60

Financial security in the event of illness 62Sickness cash benefit 62Vocational rehabilitation 66Activity compensation and sickness compensation 68Benefit for care of closely related persons 73Housing supplement for people receiving activity compensation or sickness compensation 74Work injury compensation 76

Other payments 78Dental care 78Activity grants and development allowance 82Introduction benefit, supplementary introduction benefit and introduction benefit for housing 84

SOCIAL INSURANCE IN FIGURES 2016

6

Introduction

Swedish social insurance aims to provide financial security during all stages of life and covers all persons who live or work in Sweden. The parts of social insurance administered by Försäkringskassan include mainly allowances and benefits paid to families with children, persons who are sick and persons with disabilities. As of January 2010, the Swedish Pensions Agency administers allowances and benefits paid to old age pensioners. These allowances and benefits are not included in this publication.

The total expenditures on social insurance in 2015 amounted to around SEK 225 billion, or 5 per cent of Sweden’s gross domestic product (GDP). Just over half of the expenditures were to persons who were sick and persons with disabilities, one third to children and families, and the remaining part to other payments, mainly within the labour market area and for administration.

Social Insurance in Figures 2016 provides an overall description of the allowances and benefits administered by Försäkringskassan. Social insurance is described in tables, charts and diagrams based on the areas scope and financing of social insurance, registered insured persons, financial security for families and children, financial security in the event of disability, financial security in the event of illness, and other payments. Among the indicators presented for many benefits and allowances are the number of recipients, the amount paid and average compensation. In order to put the statistics in context, each benefit and allowance is accompanied by a box that briefly describes the applicable rules. Social Insurance in Figures 2016 also includes a thematic chapter about work injury insurance, which celebrates its centenary this year.

Insured persons have varying needs of social insurance, and utilise it in different ways. For this reason, the statistics are reported by sex and age, and in some cases by region and county of birth.

A PDF version of Social Insurance in Figures 2016 and a diagram document with links to the underlying statistics may be downloaded from Försäkringskassan’s website, www.forsakringskassan.se. Further statistical information is also available on Försäkringskassan’s website for statistics and analysis, www.forsakringskassan.se/statistik. Questions about statistics may also be asked by email to [email protected].

SOCIAL INSURANCE IN FIGURES 2016

7

How to Read the Report

Each benefit and allowance included in Social Insurance in Figures 2016 is accompanied by a box that briefly describes the applicable rules. The box is intended to help readers to put the statistics into context and describes the rules for the year to which the statistics related, that is for the year 2015. In those cases where the rules have changed during the year, the rules that applied most recently during the year in question are shown. Further information about the rules is available on Försäkringskassan’s website, www.forsakringskassan.se.

The term “days” consistently refers to net days – for example, two days of 50 per cent compensation are regarded as one net day.

Income-related daily compensation for sickness benefit, pregnancy benefit, parental benefit, etc., is calculated by multiplying the compensation level (75 or 80 per cent) by a conversion factor (0.97 in 2015). The Riksdag sets the conversion factor. Thus, income-related daily compensation is just under 75 or 80 per cent of the sickness benefit qualifying income.

The way that daily compensation is calculated depends on whether it is based on the hour/day (such as temporary parental benefit) or calendar day (such as parental benefit). As a result, even though the maximum compensation is based on 7.5 times the price basic amount for temporary parental benefit and 10 times the price basic amount for parental benefit, the average daily amount for temporary parental benefit may exceed the average daily amount for parental benefit.

Data can change during the course of a particular matter for benefits and allowances that cover a longer period of time. For example, the diagnosis can change over time for ongoing cases of sickness benefit. Information about diagnosis comes from the most recent entries in Försäkringskassan’s systems.

Due to retroactive decisions, reassessments, withdrawals, etc., statistics downloaded at different times from Försäkringskassan’s data warehouse may differ slightly. Thus, information about the number of recipients reported may, for example, differ slightly from what is reported in other contexts.

The diagram entitled “Proportion of the population receiving sick-ness or activity compensation by region of birth in December 2015” has been age-standardised. Given that the occurrence of illness changes with age, the age structures of the various regions of birth are important to consider. Age standardisation involves adjusting the age structure such that it is independent of region of birth.

SOCIAL INSURANCE IN FIGURES 2016

8

Thematic chapter – 100 years of Work Injury Insurance – From industrialisation to service society

Work injury insurance is Sweden’s oldest social insurance. The Industrial Accident Insurance Act was instituted in 1916. The insurance arose from the changes and the insecurity that came with industrialisation, where hazardous working environments and accidents in the workplace were common. Pursuant to this act, employers were obliged to provide insurance for their employees, which meant that in principle all workers were insured for accidents at work.

Work injury insurance 1916–2016This chapter begins by describing the histor-ical development of work injury insurance, with particular focus on the societal changes that have influenced the policy design. Most

of the statistics in this chapter relate to annuities (see the fact box), which represent the most significant compensation paid from work injury insurance. As there are limitations on the information available in Försäkringskassan’s data warehouse, most of the statistics relate to data from the early 2000s until today.

Annuity

Annuity is compensation for loss of earnings that can be granted to individuals who have an approved work injury claim. There are two types of annuities paid from work injury insurance. Annuities as compensation in the event of work injury for loss of earnings, and survivor annuities to provide compensation to survivors if a person dies from a workplace injury.

SOCIAL INSURANCE IN FIGURES 2016

9

Emergence during industrialisationWhen the Industrial Accident Insurance Act was introduced in 1916, it was based on the employer’s insurance obligation and thus came to essentially encompass all workers. The act meant that a worker who was involved in an accident in the workplace received compensation equivalent to two thirds of their lost earnings. The act also included the reimbursement of medical expenses and compensation for survivors in the event of a work injury resulting in death. Employers were responsible for paying out sick pay for the first 35 days. This was motivated by the fact that a forthcoming general and compulsory sickness insurance

would provide compensation for shorter cases of sickness. A few years later, the insurance was expanded to include compensation for accidents occurring on the way to or from work, so-called commuting accidents. In 1929, accident insurance was supplemented with the Act on Insurance for Certain Occupational Diseases. The insurance thus came to encompass some of those diseases caused by hazardous substances such as arsenic, mercury and lead, which some work-ers at the time could frequently come into contact with during work.

National sickness insurance makes an entranceIt was not until 1955 that Sweden established a universal sickness insurance and a new occupational injury insurance (Occupational Injury Insurance Act). The new occupational injury insurance regulated accidents in the workplace, commuting accidents and certain work-related illnesses. Compensation under the Occupational Injury Insurance Act was calculated partly on the basis of the insured party’s annual earnings before the injury and also on the extent in reduction of work ability. In this way, financial compensation was given for both loss of earnings and for the medical disability caused by the work injury.

When occupational injury insurance was introduced, a coordination period was launched, which meant that the person who sustained the work injury received compen-sation according to the rules for sickness insurance during the first 90 days. This meant that a large proportion of the work injuries that had previously been regulated by work injury insurance now came to be regulated through the national sickness insurance. This system in which work injury insurance acts as a complement to public sickness insurance becomes established and will be further strengthened in later devel-opments within the emergence of various types of social insurance.

Insured through collective agreementsIn the early 1970s, the labour market par-ties reached an agreement on collectively agreed security insurances for employees that would complement the general work injury insurance. These insurances meant that workers who suffered injury through accidents at work, or on the way to or from

work, would be compensated according to tort law principles. This was true regard-less of whether it was the employer or the employee who had caused the injury. Later, these security insurances have been supple-mented with compensation for work-related diseases.

SOCIAL INSURANCE IN FIGURES 2016

10

More injuries classified as work injuriesIn 1977, the Work Injury Insurance Act was introduced. This new act contained a rule of evidence to the effect that accidents at work and other injuries caused by the harmful effects of the work should be seen as work injuries unless there were compelling reason not to do so. The idea was that the insurance and not the injured person should bear the cost in the event there was a lack of scientific evidence concerning causality within an area. Unlike previous legislation, compensa-tion was calculated solely on the basis of the claimant’s ability to earn income through gainful employment, and the compensation was equivalent to the loss of earned income up to an income threshold of 7.5 times the price basic amount. How the law should be interpreted was disputable, and in the 1980s, many work

injury claims were appealed to the insurance courts. Many of the insurance offices’ deci-sions were amended after judicial review, which meant a change in practice, which in turn led to a more generous interpretation of the work injury insurance regulations. In the 1980s, the number of approved work injuries increased and insurance costs rose. In the first half of the 1980s, work injury compensation accounted for approx-imately 0.2 percent of the gross domestic product (GDP), and in 1986 this ratio had increased to 0.8 per cent of the GDP. This development also affected the cost of sick-ness insurance due to the fact that the com-pensation from sickness insurance was paid out as underlying benefits in work injury cases, for example, as work injury sickness cash benefit.

The term work injury is more narrowly definedIn the early 1990s, Sweden experienced a sharp recession with high unemployment. As a consequence, the financial base for social insurance was affected, as there was a drop in taxes and fees being paid by fewer in gain-ful employment. In connection with this, the legislators elected to review the work injury insurance. In 1992, the coordination period with sickness insurance was extended, and 1993 saw the abolishment of compensation for medical care, medicine, medical treat-ments and the special work injury sickness cash benefit.

The term work injury was more nar-rowly defined and the new rule of evidence meant that there should be a high degree of probability that a factor in the work-place, a so-called harmful effect, could give rise to the disease of the insured party. Furthermore, there should be predominant grounds supporting the assertion that there was a causal link between the work injury and the harmful effect. Consequently, a requirement was introduced stipulating that a factor’s harmful basis should be able to be proven based on established research.

Fewer work injury cases examinedIn the early 2000s, the legislature assessed that the application of the 1993 law had been too restrictive and that the requirements for a disease to be accepted as a work injury were too stringent. Therefore an alleviation of the evidentiary requirement in assessing work injury was introduced in 2002. The evidentiary requirement was reduced from the previous level requiring a high degree of probability to it being sufficient that predom-inant grounds existed for the assertion that the injury or disease was caused by the work. In 2003, a requirement was introduced stipulating that, for an assessment to begin, a written application for compensation from work injury insurance must be submitted. The legislator had assumed that the alle-viation of the evidentiary requirement would lead to an increased number of applications

for compensation relating to work injury; instead, the trend has gone in the opposite direction with fewer applications since the early 2000s. 2008 saw a sickness insurance reform which had a further impact on the appli-cation of the work injury insurance. One change was that the time-limited sickness compensation was removed and the criteria for receiving permanent sickness com-pensation were tightened. Applications for compensation from work injury insurance in the form of an annuity have often been made in conjunction with individuals having been granted sickness compensation. As fewer people have been granted new sickness com-pensation since the regulatory changes in 2008, this has meant that fewer work injury cases have been assessed.

SOCIAL INSURANCE IN FIGURES 2016

11

Changes in regulations governing work injury insurance

1916 The Industrial Accident Insurance Act is instituted.

1920 Compensation is provided for accidents while travelling to and from work.

1929 The Act on Insurance for Certain Occupational diseases is instituted.

1955 The National Sickness Insurance Act and the Occupational Injury Insurance Act are instituted. In connection with this, a 90-day coordination period between sickness insurance and occupational injury insurance is introduced.

1977 The Work Injury Insurance Act is instituted. The new insurance entailed the introduc-tion of a general definition of injury and elevated levels of compensation.

1993 The term work injury is more closely defined and fewer benefits are included in the insurance. The right to work injury sickness cash benefit essentially no longer applies.

2002 An alleviation of the evidentiary requirement in assessing work injury is introduced.

2003 A requirement is introduced stipulating that a written application must be submitted for compensation from work injury insurance.

2008 Changes are implemented within sickness insurance and the regulations on who is entitled to sickness compensation are tightened.

2011 The Social Insurance Code is instituted and replaces the Work Injury Insurance Act.

A detailed description of regulatory changes is found in the publication Förändringar inom socialförsäkrings- och bidragsområdena 1968-01-01–2015-09-01 [Changes within social insurance 01/01/1968–01/09/2015] which is published at www.forsakringskassan.se/statistik.

Work injury insurance in transitionIn summary, the design of work injury insur-ance has undergone substantial changes in the hundred years since the insurance has existed. From having been an acci-dent insurance, a subsequent inclusion of work-related diseases broadened the scope of the insurance. The formulation of the evidentiary requirement in establishing the connection between the injury and the work has had a major impact on which claims have been approved as work injuries. According to the 1977 Act, an accident at work and other injuries caused by the harmful effects of the work should be seen as work injuries unless there is compelling reason not to do so. The act thus contained a presumption of causality, which meant that more illnesses and injuries could be viewed as work injuries. The pendulum then swung in the opposite direction with the 1993 legislation, which required the harmfulness of a factor to have been established based on scientific evidence. According to current legislation, there should be predominant grounds supporting the assertion that the injury or disease was caused by the work in order for compensation from work injury insurance to be considered.

The form of compensation from the insurance has also been changed. Occupational injury insurance provided compensation both for loss of earnings and based on the degree of medical disability caused by the work injury. Later on, insur-ance only provided compensation for eco-nomic loss of income. In the legislation from 1977, lost income due to work injury was also compensated in the event of shorter cases of sickness. Since the 1990s, work injury insur-ance is to a greater extent coordinated with sickness insurance. During the 2000s, there were several changes that affected how many work inju-ries Försäkringskassan came to investigate. Firstly, there was a requirement that a writ-ten application be submitted for compensa-tion from work injury insurance. Secondly, sickness insurance was reformed, which included more stringent requirements for the granting of sickness compensation, i.e. previously disability pension. Work injury insurance, which from the start was seen as a complement to sickness insurance, has in the course of time become increasingly coordinated with sickness insurance benefits.

SOCIAL INSURANCE IN FIGURES 2016

12

Reported work injuriesEmployers and self-employed individuals who become aware that a work injury has occurred are obligated to report this to Försäkringskassan in accordance with the provisions of the Social Insurance Code. The Swedish Work Environment Authority is responsible for the monitoring of reported work injuries and uses this data as a basis for the work to prevent illnesses and accidents in the workplace. Work injuries are divided into work accidents, work-related diseases and

accidents occurring on the way to or from work (so-called commuting accidents). Work accidents are injuries that have arisen in conjunction with a brief and unexpected event. Work-related diseases means that there have been harmful factors in the work environment that have given rise to disease. Some examples of such harmful factors include heavy or repetitive work, vibrations, noise, chemical substances or psychologi-cally stressful working conditions.

1 The data on the number of reported work accidents resulting in absence in 2014 is still preliminary, and the number is expected to rise by about 4 per cent.

Source: Occupational Injuries 2014, Statistical Report 2015:1, Swedish Work Environment Authority

� Reported work injuries per 1,000 gainfully employed persons 1980–2014, employees and self-employed personsThe number of work injuries has varied over time, and the development should be understood in terms of the structural trans-formation of the labour market that has been underway since the late 1980s. During this period the industrial structure has changed, with a fall in employment within goods pro-duction and increased employment within the service sector. Furthermore, there was a recession in the early 1990s that led to a declining number of hours being worked by gainfully employed individuals, which may have affected the number of work injuries. Changes to the work injury insurance and sickness insurance may in and of itself have influenced the propensity to report work-related injuries. A clear example is that the number of reported work-related diseases increasing sharply in 1993, which can be explained by the transitional rules

introduced in connection with the term work injury being more narrowly defined in 1993. Another example, occurring during the early 1990s, is the sharp reduction in the number of reported work accidents with sickness absence in relation to the number of gainfully employed women and men. This development can also be linked to the more stringent definition of work injury and to the fact that the right to work injury sickness cash benefit was essentially discontinued at this time. In recent years, the number of work accidents without sickness absence has increased for both women and men in rela-tion to the number of gainfully employed workers. The number of accidents on the way to or from work, so-called commuting acci-dents, has remained stable since the 1980s.

0

5

10

15

20

25

30

35

40

141005009590851980141005009590851980

Reported per 1,000Women Men

Work-related diseases Commuting accidentsWork accidents with absence

Work accidents without absence1

SOCIAL INSURANCE IN FIGURES 2016

13

Injury type Women Men Total

Work accidents with absence1 13,168 18,089 31,257

Work accidents without absence 34,394 26,869 61,263

Work-related diseases 7,208 4,809 12,017

Commuting accidents 6,431 3,268 9,699

Older cases2 431 495 926

Total 61,632 53,530 115,162

1 The data on the reported work accidents resulting in absence is still preliminary and is expected to rise by about 4 per cent.

2 This category includes those reports that concern occupational injuries that have occurred more than two years before the date the report was submitted.

Source: Occupational Injuries 2014, Statistical Report 2015:1, Swedish Work Environment Authority

� Reported work injuries in 2014In 2014, almost 115,200 work injuries were reported to Försäkringskassan. Of these reports, 53 per cent concerned work accidents not resulting in sickness absence and 27 per cent concerned work accidents resulting in sickness absence. Reports that concerned work-related diseases consti-tuted 10 per cent and commuting accidents represented 8 per cent of the incoming reports of work injuries in 2014. There are gender differences in reported work injuries. In 2014, reported work accidents without sickness absence were more common among

women (56 per cent) than men (44 per cent). Reported work accidents with sickness absence were more common among men (58 per cent) than women (42 per cent). There are no clear answers as to the cause of these gender differences in reported work injuries. It may partly reflect differences in the working environment that women and men work in. It can also be linked to differ-ences in the propensity of small and large workplaces to submit reports, and between different sectors and industries in which men and women are gainfully employed.

SOCIAL INSURANCE IN FIGURES 2016

14

Forms of compensation from work injury insuranceOnly a small portion of the work injuries reported to Försäkringskassan lead to the injured party then applying for compensa-tion from work injury insurance. However, a large proportion of people reporting work injury receive compensation from sickness insurance in the form of sickness cash bene-fit during the acute illness period. Under current legislation, work injury insurance encompasses individual life

annuities, reimbursement of dental expenses, costs for medical care abroad and compensation for special aids. The area of expenditure for work injury insurance also includes compensation for survivors and funeral assistance. As of 1 January 2010, these benefits are administered by the Swedish Pensions Agency.

� Work injury insurance expenditures excluding administration 2007–2015Work injury insurance expenditures are closely connected to the design of the insur-ance. Since the early 2000s, expenditures for work injury insurance have declined. Expenditures fell from SEK 5.3 billion in 2007 to SEK 3.1 billion in 2015, representing a decrease of 42 per cent. In 2015, work injury insurance expendi-tures constituted 1.4 per cent of the total social insurance expenditures. This year, the annuities under current legislation

accounted for 85 per cent of the total expenditures for work injury insurance. The annuities under the Work Injury Insurance Act and other older regulations accounted for 11 per cent of the expenditures. The group “Other forms of compensation” primarily includes reimbursement of dental expenses and costs for medical care abroad. These forms of compensation only constituted 4 per cent of work injury insurance expendi-tures in 2015.

SEK billion

0

1

2

3

4

5

6

201520142013201220112010200920082007

Annuities under current legislation

Annuities under older legislation

Other forms of compensation

SOCIAL INSURANCE IN FIGURES 2016

15

Individual life annuity – the most significant compensationThe largest compensation paid from work injury insurance is individual life annu-ity, which accounted for 96 per cent of the work injury insurance expenditure in 2015. This form of compensation first comes into question when the work injury has resulted in a reduction in the ability to earn income from employment that is experienced for more than one year (see the fact box). The purpose of this compensation is for the insured party who suffers a loss of income due to a work injury to receive compensation that allows them to be able to remain in the same financial situation as if the injury had not occurred. The level of compensation is determined by the income that the insured party had prior to the injury and the income they are expected to have after the injury. In many cases, the insured party has a diminished work capacity that has also entitled them to compensation from sickness insurance. The individual life annuity is then coordinated

with other social insurance benefits and the annuity is paid out for the difference. Individual life annuity can also be paid out if a person, due to a work injury, has switched to a job that gives them a lower income or has participated in vocational rehabilitation measures.

Individual life annuity

To be eligible for an individual life annuity, the ability to earn income through work must have been reduced by at least one fifteenth for at least one year. The loss of income must also be at least one quarter of the price basic amount for one year (SEK 11,075 in 2015). There is an upper limit, which means that the disbursed annuity may not exceed 7.5 times the price basic amount (equivalent to SEK 333,750 in 2015).

See the Regulations box on page 77 for more information on current regulations.

Individual life annuity is often paid over a long periodThe right to compensation from work injury insurance is assessed based on different statutory provisions, depending on when the injury occurred or when the disease first pre-sented itself. In order for the right to entitle-ment to be assessed under the Occupational Injury Insurance Act, the injury must have been sustained prior to 1977. According to the Occupational Injury Insurance Act, individual life annuity is a benefit paid out for life. Individual life annuity under current legislation (Work Injury Insurance Act and

after) is normally paid out until and includ-ing the month before the annuitant turn 65 years old. This means that an individual life annuity is a benefit that a person injured at work can receive for many years, and the majority of individual life annuities dis-bursed today were granted decades ago. The following section describes how the prevalence of individual life annuities has evolved over time, and their distribution based on current or older legislation and gender.

SOCIAL INSURANCE IN FIGURES 2016

16

Data is presented from 1986 because from this year statistics are available on the number of disbursed individual life annuities following coordination with other social insurance benefits. The statistics for individual life annuities under current legislation also include annuities based on national personal injury protection. These annuities regulate compensation for injuries during, for example, military or rescue service, and constitute a small part of the total individual life annuities.

zy Individual life annuities in December 1986–2015The number of individual life annuities under the Occupational Injury Insurance Act has decreased since the mid-1980s. In December 1986, 90,300 annuities were paid out, which can be compared to December 2015 when the number had decreased to 26,700. This decrease reflects the fact that this compensation can only apply for such occupational injuries incurred prior to 1977. The number of individual life annuities under current legislation (the Work Injury Insurance Act and subsequent legislation) increased sharply from the mid-1980s. During the period 1986–1991, there were a high number of work injury cases assessed with a high approval rate. The number of

annuities paid out peaked in December 1995 with 99,200 annuities. Since then the number has decreased. This reflects the tightening of legislation introduced in 1993, which led to fewer injuries being categorised as work injuries according to the insurance parameters. Between 2002 and 2003 there was a small increase of annuities, which can be attributed to the alleviation of the eviden-tiary requirement in the assessment of work injury, as introduced at that time. However, since 2003 the number has decreased again, and by December 2015 there were just under 37,000 disbursed individual life annuities under current legislation.

NumberWomen Men

0

20,000

40,000

60,000

80,000

100,000

120,000

1510050095901986 1510050095901986

Annuities under current legislation

Annuities under the Occupational Injury Insurance Act

SOCIAL INSURANCE IN FIGURES 2016

17

Gender differences in disbursed individual life annuitiesThere are gender differences in terms of how many individual life annuities that are paid out to women and to men. Of those individual life annuities under the older legislation (Occupational Injury Insurance Act) that were disbursed in December 2015, 90 per cent were paid to men. This percent-age has remained largely unchanged since the 1980s. The fact that the majority of the individ-ual life annuities linked to older legislation are paid to men should be understood in terms of what the labour market in Sweden was like when work injury insurance was under development. The Occupational Injury Insurance Act evolved from an accident insurance and mainly encompassed those accidents that could occur in hazard-ous working environments within industry. Only specific diseases were covered by the insurance. These were mainly diseases that could be linked to contact with hazardous substances (such as lead and mercury) or dangerous radiation. Sweden has, and has had, a gender-segregated labour market, and there has been a greater proportion of men working within industries with hazardous work environments that provided the basis for the earliest work injury insurance.

The individual life annuities linked to current legislation (Work Injury Insurance Act and after) are not character-ised by such extreme gender differences. Unlike previ-ous legislation the current legislation also encompasses work injuries in the form of work-related diseases to a greater extent. Women’s employment has increased significantly since the 1970s, but the labour market is still gender-segregated. A large proportion of today’s gainfully employed women work within professions where there may be a greater risk of work injury in the form of work-related diseases due to repet-itive and long-term exposure, rather than manifest accidents. Examples worth men-tioning in this context include those work injuries due to mental and physical strain that can occur within health and social care professions. Despite the fact that current legislation covers work injuries in the form of work acci-dents, work-related diseases and commuting accidents, there are still gender differences in the number of individual life annuities disbursed. In December 2015, 58 per cent of the individual life annuities under current legislation were paid out to men.

SOCIAL INSURANCE IN FIGURES 2016

18

Fewer decisions on individual life annuities When Försäkringskassan receives an application concerning an individual life annuity, it is first checked whether the injury or illness has involved a sufficiently large loss of income to qualify the insured party for compensation. If the insured party meets the requirements, there is then an assessment of whether there are predominant grounds to support the assertion that the accident or illness was caused by the work and is thus to be considered a work injury. There are statistics presented below on those applications concerning an individual

life annuity where Försäkringskassan has decided that the injury has involved a suffi-ciently large loss of income and that there are predominant grounds supporting the asser-tion that the injury was caused by the work and is thus to be considered a work injury. The statistics on approval decisions for an individual life annuity are broken down by injury type (work accidents, work-related diseases and commuting accidents) and diag-nosis group.

The statistics are based both on decisions in conjunction with the initial assessment of work injury and decisions relating to already approved work injuries. On the basis of the underlying statistical data, it is not possible to report all first-time decisions separately.

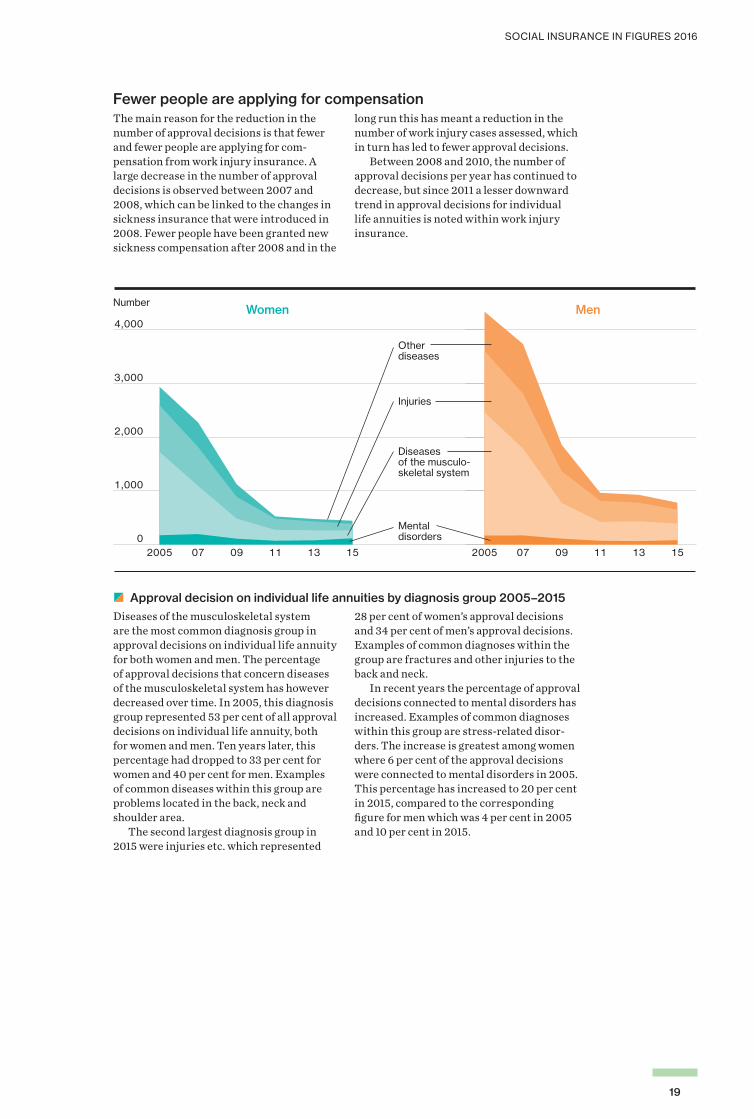

zy Approval decisions on individual life annuities by injury type 2005–2015Since the mid-2000s, the number of approval decisions in the assessment of an individual life annuity has decreased. In 2005, 7,300 approval decisions were made regarding an individual life annuity, which can be compared with 2015 when 1,200 approval decisions were registered. During the same period, the number of refusals in assessments of entitlement to an individual life annuity decreased from 12,600 (in 2005) to 900 (in 2015). The total number of assessments of entitlement to an individual life annuity have thereby decreased during the period in question. Since 2005, a larger proportion of the deci-sions on an individual life annuity in which the applicant is denied are connected to the fact that the formal requirements regarding reduced work ability and loss of income are not met, and thus a work injury assessment is not carried out. In 2005, there were 3,044 rejections where a work injury assessment

had not been carried out, and in 2015 this number had increased to 3,885. Over time, women have received a larger proportion of approval decisions than men with regard to applications concerning an individual life annuity connected to commuting accidents. In 2015, commut-ing accidents represented 23 per cent of the approval decisions issued to women, compared to the corresponding 11 per cent for men. Compared with women, men have received a larger proportion of approval deci-sions that have related to work accidents. In 2015, work accidents constituted 46 per cent of men’s approval decisions and 36 per cent of women’s approval decisions. The percentage of approval decisions that concern work-related diseases is almost equal for women and men. They represented 41 per cent of women’s and 42 per cent of men’s approval decisions in 2015.

0

1,000

2,000

3,000

4,000

151413121110090807062005 151413121110090807062005

Work-related diseases

Work accidents

Commuting accidents

NumberWomen Men

SOCIAL INSURANCE IN FIGURES 2016

19

Fewer people are applying for compensationThe main reason for the reduction in the number of approval decisions is that fewer and fewer people are applying for com-pensation from work injury insurance. A large decrease in the number of approval decisions is observed between 2007 and 2008, which can be linked to the changes in sickness insurance that were introduced in 2008. Fewer people have been granted new sickness compensation after 2008 and in the

long run this has meant a reduction in the number of work injury cases assessed, which in turn has led to fewer approval decisions. Between 2008 and 2010, the number of approval decisions per year has continued to decrease, but since 2011 a lesser downward trend in approval decisions for individual life annuities is noted within work injury insurance.

zy Approval decision on individual life annuities by diagnosis group 2005–2015Diseases of the musculoskeletal system are the most common diagnosis group in approval decisions on individual life annuity for both women and men. The percentage of approval decisions that concern diseases of the musculoskeletal system has however decreased over time. In 2005, this diagnosis group represented 53 per cent of all approval decisions on individual life annuity, both for women and men. Ten years later, this percentage had dropped to 33 per cent for women and 40 per cent for men. Examples of common diseases within this group are problems located in the back, neck and shoulder area. The second largest diagnosis group in 2015 were injuries etc. which represented

28 per cent of women’s approval decisions and 34 per cent of men’s approval decisions. Examples of common diagnoses within the group are fractures and other injuries to the back and neck. In recent years the percentage of approval decisions connected to mental disorders has increased. Examples of common diagnoses within this group are stress-related disor-ders. The increase is greatest among women where 6 per cent of the approval decisions were connected to mental disorders in 2005. This percentage has increased to 20 per cent in 2015, compared to the corresponding figure for men which was 4 per cent in 2005 and 10 per cent in 2015.

NumberWomen Men

0

1,000

2,000

3,000

4,000

15131109072005 15131109072005

Mentaldisorders

Injuries

Otherdiseases

Diseases of the musculo-skeletal system

SOCIAL INSURANCE IN FIGURES 2016

20

The proportion of approvals in work injury assessments has increasedDuring the period 2005–2015, the per-centage of approvals has increased in relation to the number of work injury

assessments carried out in total. In 2005, Försäkringskassan determined that 28 per cent of the assessed cases where women had applied for an individual life annuity fulfilled the requirements to be classified as work injuries. The correspond-ing proportion in 2015 was 50 per cent. For men, the corresponding trend for approval frequency indicates an increase from 46 per cent in 2005 to 64 per cent in 2015.

Approval rate for individual life annuity

The calculation of approval rate for individual life annuity only includes those decisions where Försäkringskassan has been able to determine that a sufficiently large loss of income can be linked to the injury. The ability to earn income through work must have been reduced by at least one fifteenth for at least one year. The loss of income must also be at least one quarter of the price basic amount for one year.

Largest percentage increase in approvals for mental disordersThe highest percentage of approvals in work injury assessments goes to women and men who apply for an individual life annuity due to injuries of external causes. In 2015, the approval rate was 75 per cent in those work injury assessments where women have applied for an individual life annuity in connection with injuries. The corresponding figure for men was 84 per cent. The greatest increase in approval rate is observed for the mental disorders. In 2015,

the approval rate was 55 per cent among those work injury assessments where women had applied for an individual life annuity in connection with these diagno-ses. This can be compared with 2005 when the corresponding approval rate was only 13 per cent. However, mental disorders only represent a small part of the total number of approval decisions for individual life annuity applications.

SOCIAL INSURANCE IN FIGURES 2016

21

Age distribution among persons with an individual life annuityThe following section describes those indi-viduals who have an individual life annuity, broken down by age and the legislation pursuant to which they were granted an individual life annuity. In a description of the age distribution among those persons with an individual life annuity it is relevant to consider whether the recipients have been granted annuity based on current or former legislation. Persons granted an individual life annu-ity under the Occupational Injury Insurance

Act receive this compensation for the rest of their life. For persons born 1938 or after, an individual life annuity is paid according to current legislation until and including the month before the annuitant turn 65 years old. In 2003, regulatory changes were made for persons born 1937 or before who had guaranteed annuity under the Work Injury Insurance Act. These individuals generally have low annuities and will get to keep their individual life annuities past the age of 65.

The statistics for persons with an individual life annuity under current legislation also include those persons who have annuities based on national personal injury protection. The majority of the persons over 65 who have an individual life annuity under current legislation have guaranteed annuity under the Work Injury Insurance Act.

zy Annuitants in December 2015 by age and legislationIn December 2015, there were over 26,100 persons who had an individual life annuity under former legislation. Among these, the majority were men (89 per cent) and only a small proportion of the annuitants were women (11 per cent). The persons who receive annuity under former legislation have incurred a work injury prior to 1977 and have often received this compensation for a long time. Over 25,800 persons had an individual life annuity under current legislation in December 2015. Among these recipients

there was a more even gender distribution, with 47 per cent women and 53 per cent men. A large proportion of the insured indi-viduals who have an annuity are older. Just under 8 per cent of those who have an indi-vidual life annuity under former legislation (Occupational Injury Insurance Act) were under 65 years old in 2015. Fifteen years ago (2001) the corresponding figure was 25 per cent. Only 4 per cent of the annuitants with compensation under current legislation were under 45 years old in December 2015. The corresponding proportion in 2001 was 10 per cent.

0

1,000

2,000

3,000

4,000

5,000

6,000

90–

85–89

80–84

75–79

65–74

60–64

55–59

50–54

45–49

–44

90–

85–89

80–84

75–79

70–74

65–69

60–64

55–59

50–54

45–49

–44

NumberFormer legislation* Current legislation

Women

Men

Age, year* Occupational Injury Injurance Act

SOCIAL INSURANCE IN FIGURES 2016

22

Many receive compensation from sickness insurance when they are granted an annuityWork injury insurance is in many ways a complement to public sickness insurance. A large proportion of the persons applying for compensation from work injury insurance in the form of an annuity have received benefits from sickness insurance after the work injury occurred. In direct connection to the work injury, they may have been sick-listed and received compensation from sickness insurance in the form of sickness cash ben-efit. If the injury has led to a sustained reduc-tion in work ability, they may have received compensation in the form of activity com-pensation or sickness compensation. If they

have been granted activity compensation or sickness compensation, this can be seen as a signal that it is time to apply for an annuity, based on the fact that this compensation first comes into question when the work injury has resulted in a reduction in the ability to earn income from employment. Sustained means that this reduction is experienced for more than one year. The following section presents statistics on the proportion of people who had received compensation from sickness insurance when they were granted an individual life annuity for the first time.

The data relates to individual life annuities under current legislation.

zy Proportion of annuitants who were receiving compensation from sickness insurance at the first time they were granted an individual life annuityThe graphs show the proportion of those people who were granted an individual life annuity for the first time and who, at the time of application, were receiving compen-sation from sickness insurance in the form of sickness cash benefit, sickness compen-sation or activity compensation. A large percentage of these persons were receiving compensation from sickness insurance at the time of application, but the percentage has decreased during the period 2005 to 2015. Prior to 2010, it was more common that the claimant was receiving compensation in the form of sickness compensation. The per-centage of persons who were receiving com-pensation in the form of sickness cash ben-efit when they applied for an individual life annuity decreased between 2005 and 2010 but has subsequently increased. This reflects the changes in sickness insurance that were introduced in 2008, wherein time limits on

sickness cash benefit were introduced, while at the same the criteria for receiving sickness compensation were tightened and temporary sickness compensation was abolished. Among women, 66 per cent received compensation from sickness insurance when they applied for an individual life annuity for the first time in 2015. Approximately the same number were receiving compensation from sickness insurance in the form of sick ness cash benefit (34 per cent) as were receiv ing activity compensation or sickness compen-sation (32 per cent). Among men there was 57 per cent receiving compensation from sickness insurance when they applied for an individual life annuity for the first time in 2015. A higher number were receiving compensation from sickness insurance in the form of sickness cash benefit (35 per cent) than were receiving compensation in the form of sickness compensation (23 per cent).

Per centWomen Men

0

20

40

60

80

100

151413121110090807062005 151413121110090807062005

Activity- or sickness compensation

Sickness cash benefit

SOCIAL INSURANCE IN FIGURES 2016

23

Persons who have an individual life annuity and are gainfully employedIndividuals who have a work injury that has resulted in a loss of income can be granted an individual life annuity. An individual life annuity may come into question if the injured party cannot work to the same extent as before or if they, due to the injury,

have been compelled to change job and the new job involves a lower income than the job in which they got injured. The following section presents statistics for persons who have an individual life annu-ity and are gainfully employed.

The statistics for persons with an individual life annuity under current legislation also include those persons who have annuities based on national personal injury protection. The estimate regarding occupational distribution is based on whether persons with an individual life annuity were registered in Statistics Sweden’s (SCB) Occupational Register (according to SSYK96) in November 2013

zy The occupational distribution between working annuitants and the total working population age 18–64, in January 2014According to one estimate, 45 per cent of men aged 18–64 with an individual life annu-ity (under current legislation) were gainfully employed in January 2014. The correspond-ing figure for women was 33 per cent. By comparing the occupational distribution between working annuitants and the occu-pational distribution of the entire working population, it is evident that certain profes-sions are over- or under-represented among those who have an individual life annuity. Of female annuitants who were gain-fully employed in January 2014, 35 per cent worked within the field of service, care and sales. This was a slightly higher percentage compared to all working women in Sweden (32 per cent). Other occupations that were more common for female annuitants than for working women in total were administra-tion and customer service work.

The most common occupational cate-gory for male annuitants in January 2014 was building and manufacturing work (28 per cent). The corresponding percentage among the total number of employed men was 17 per cent. Other occupations that were more common among annuitants than among the working population as a whole included work without the requirement of special vocational training, as well as mechanical manufacturing and transport work. Some professions were clearly overrepre-sented among annuitants, which may reflect differences in working conditions between different professions. The occupations that require higher levels of education are instead under-represented among gainfully employed people with an individual life annuity.

0 5 10 15 20 25 30

Work without the requirement of special vocational training

Mechanical manufacturing and transport workers, etc

Building and manufacturing workers

Agricultural, horticultural, forestry and fishery workers

Service, care and shop sales workers

Administration and customer service clerks

Occupations requiring higher education qualifications or equivalent

Occupations requiring advanced level of higher education

Managers

051015202530Per cent

Women Men

Working population

Working annuitants

Working population

Working annuitants

SOCIAL INSURANCE IN FIGURES 2016

24

Regional variations in the proportion of people with an individual life annuityThe following section presents statistics on the regions in Sweden with the largest proportion of persons with an individual life annuity in the 16–64 age group.

zy Annuitants per 1000 registered insured individuals in Sweden 16–64 years, in December 2015 by regionIn December 2015 there were 2.7 women and 3.9 men with an individual life annuity per 1,000 registered insured individuals in Sweden. There are regional variations in the proportion of those insured who have an individual life annuity under current legis-lation. Västerbotten, Dalarna and Värmland stand out as counties with a relatively higher percentage of people with an individual life annuity, both for women and men.

Stockholm County stands out with a lower percentage of people with an individual life annuity under current legislation. In most counties, there is a higher proportion of men than women who have an annuity. Some counties with a higher proportion of male annuitants include Norrbotten, Gotland and Kalmar. The counties of Jönköping and Östergötland instead have a higher propor-tion of female annuitants.

1.8–2.5

2.6–3.3

3.4–4.1

4.2–5.0

1.0–1.7

2.9–4.1

4.2–5.4

5.5–6.7

6.8–8.1

1.6–2.8

Women Men

SOCIAL INSURANCE IN FIGURES 2016

25

Possible explanations for geographical differencesThere are several possible explanations for these geographical differences in the propor-tion of people with an individual life annuity under current legislation. One such expla-nation could be differences in industrial structure and socio-economic composition between the counties. Another is that the labour market is and has been different in different parts of Sweden. It is therefore pos-sible that there have been more work injuries in certain geographical areas. Before Försäkringskassan became a government agency in 2005, work injury insurance was handled at various county insurance offices. Some of the geographical

differences may therefore be linked to possi-ble differences in the processing and assess-ment of the right to compensation between different insurance offices. However, it is important to remember that today’s regional variations in the proportion of those insured who have an individual life annuity reflects were in the country the people who currently have an individual life annuity now reside. This cannot be equated with an analysis of geo-graphical differences in the granting of work injury compensation. To investigate whether there have been such differences in granting requires additional analysis.

SOCIAL INSURANCE IN FIGURES 2016

26

Financial Scope of Social Insurance

Social security expendituresSocial insurance expenditures are defined here as expenditures on allowances and benefits administered by Försäkringskassan in 2015; that is mainly allowances and benefits paid to families with children, people who are sick and people with disabilities.

� Social insurance expenditures (excluding administration) adjusted to the CPI for 2015Social insurance expenditures for the benefits administered by Försäkringskassan in 2015 amounted to SEK 225 billion, while administration costs for these benefits were just over SEK 8 billion, giving total expendi-tures of just over SEK 233 billion. Since 1980, expenditures (at fixed prices) have increased by 49 per cent. Expenditures declined between 1992 and 1998, primarily due to amended rules, such as reduced compen-sation levels and the adoption of a sick pay period and waiting period. The increase in expenditures starting in 1999 was partially due to rapid increases in sickness cash ben-efit and sickness compensation. A national old age pension contribution – according to which the government pays pension entitle-ments for people with sickness cash benefit, parental benefit, etc. – was introduced in 1999. The decrease in expenditures after 2006 was due primarily to reductions in sickness cash benefit and sickness compen-sation. Expenditures on sickness cash ben-efit rose again during the period 2011–2015 while expenditures on sickness compensa-tion continued to decline.

� Social insurance expenditures (excluding administration) as a proportion of GDPSocial insurance payments represent a considerable proportion of GDP. In 2015, these payments corresponded to 5.4 per cent of GDP. Since 2011, no great changes have occurred and the level is the lowest in 35 years.

SEK billion

0

50

100

150

200

250

20152010200520001995199019851980

Per cent

0

2

4

6

8

10

20152010200520001995199019851980

SOCIAL INSURANCE IN FIGURES 2016

27

Expenditures per expense area/benefit, SEK million 2013 2014 2015

Financial security for families and childrenParental benefit 29,552 30,091 30,816

Temporary parental benefit 6,321 6,655 6,841

Pregnancy benefit 568 601 627

Equality bonus 280 307 343

Child allowance 24,723 25,220 25,764

Housing allowance 4,533 4,958 4,940

Childcare allowance 3,147 3,295 3,548

Maintenance support 3,283 3,258 3,492

Adoption allowance 15 14 15

Total 72,420 74,399 76,386

Financial security in the event of illness or disabilitySickness cash benefit 26,247 30,548 34,718

Rehabilitation allowance 1,363 1,426 1,568

Benefit for care of closely related persons 169 178 182

Supplementary housing allowance 105 89 88

High-cost protection for employers 55 60 78

Dental care 5,191 5,217 5,263

Healthcare abroad 781 489 457

Activity and sickness compensation 47,722 46,139 45,717

Housing supplement 4,517 4,689 4,832

Disability allowance 1,317 1,331 1,353

Work injury compensation1 3,831 3,610 3,397

Car allowance 368 315 280

Attendance allowance 27,107 28,589 29,784

Grants to county councils 1,000 978 681

Grants for the sick-listing process 2,297 2,077 2,063

Other forms of compensation2 43 40 38

Total 122,112 125,773 130,498

Other paymentsActivity grant 15,905 14,519 14,175

Introduction benefit 1,666 2,685 3,667

Family benefit for conscripts 21 20 20

Other 6 4 4

Total 17,598 17,228 17,866

Administration 8,171 8,285 8,293

Total 220,302 225,685 233,0441 Includes expenditures on claim SWEDINT.2 Includes expenditures on compensation within the state personal injury protection (formerly bodily injury)

and expenditures on disease carrier benefit.

� Social insurance expenditures 2012–2015 in SEK million (current prices)Despite a decrease in expenditures on sick-ness allowance, expenditures on financial security in the event of illness and financial security in the event of disability increased gradually between 2013 and 2015. The rea-son was a relatively large increase in sickness cash benefit paid. Expenditures on financial

security for families and children have increased throughout the period, due in part to a higher birth rate. Within the category other payments, expenditures on activity grants dominated. This benefit is paid to people who participate in labour market programmes.

SOCIAL INSURANCE IN FIGURES 2016

28

� Breakdown of expenditures 2015 (SEK million)Just over half of social insurance expendi-tures (56 per cent or around SEK 130 billion) was paid to people who were sick and people with disabilities. Families with children received one third of the expenditures

(33 per cent or around SEK 76 billion). In addition, there are some other benefits, pri-marily within the labour market area (SEK 18 billion). The remainder were expenditures on administration (SEK 8 billion).

� Expenditure areas as a proportion of GDPExpenditures on sickness and disabilities increased during the latter part of the 1980s, but then declined from just over 7 per cent of GDP in 1989 to just under 4 per cent of GDP in 1998. The decline was partly due to less sickness absence, the introduction of the sickness pay period, the reduction in compensation levels and the fact that the county council took over responsibility for the cost of medications. Expenditures

in relation to GDP rose between 1998 and 2003 due to increased sickness absence. Thereafter, expenditures have declined again. Compensation to families and chil-dren increased as a proportion of GDP at the beginning of the 1990s due to increases in the birth rate. During the second half of the 1990s, expenditures declined again as a proportion of GDP and have thereafter remained stable at around 2 per cent.

Administration , 8,293

Other payments, 17,866

Other sickness/disability, 10,134

Attendance allowance, 29,784

Work injury compensation, 3,397Housing allowance, 4,832

Activity/sickness compensation, 45,717 Sickness insurance2, 36,635

Other payments to families, 8,503

Maintenance support, 3,492

Child allowance, 25,764

Parental insurance1, 38,627

1 Parental insurance, equality bonus, temporary parental insurance and pregnancy allowance.2 Sickness benefit, rehabilitation benefit, benefit for care of closely related persons and high-cost protection for employers.

Sickness and disability Families and children Other payments Administration

Per cent

0

1

2

3

4

5

6

7

8

20152010200520001995199019851980

Families and children

Sickness and disability

Other payments

SOCIAL INSURANCE IN FIGURES 2016

29

� Public transfers as a proportion of GDP in 2013 in Sweden and other European countriesApart from social insurance, public transfers also include unemployment compensation and financial assistance. There are big differ-ences in how different countries use public transfers and direct services in order to meet

the needs within the social insurance sys-tem. Examples of direct services which are not included in this summary are tax credits and subsidised pre-school places.

Per cent

Social exclusion (social assistance)Sickness

UnemploymentFamilies and childrenDisability

Survivors

Old age

0 2 4 6 8 10 12 14 16 18 20

Italy*France*AustriaBelgiumDenmark*PortugalNetherlands*FinlandCyprusSpain*Germany*United Kingdom*SerbiaSlovenia*SwitzerlandSweden*LuxembourgHungaryNorwayCroatiaCzech RepublicIrelandMaltaIcelandBulgariaSlovakia*Lathvia*EstoniaRomaniaLithuania*

* Preliminary figuresGreece and Poland did not report statistics on public transfers for 2013. Source: Eurostat

SOCIAL INSURANCE IN FIGURES 2016

30

Financing social insuranceSocial insurance is financed by contributions, taxes, compensation from municipalities, etc.

� Social insurance income and expenditures in 2015 (SEK million)In 2015, the income from social insurance contributions was SEK 122 billion. In addi-tion, government funds (taxes) covered SEK 95 billion of the expenditures. Compensation from municipalities, child support debtors and similar financed just under 3 per cent of the expenditures. The amounts presented under payments in the table also include

government old age pension contributions. Among the types of insurance financed by contributions, work injury insurance, sickness cash benefit and sickness com-pensation generated a surplus of just under SEK 1 billion in 2015. Meanwhile, parental insurance and sickness insurance generated a deficit of just over SEK 11 billion.

Income Expenditures Surplus/ deficit Contrib- Statutory Other Total Pay- Admin- Total utions taxes ments and istration old age pension contribution

Parental insurance1 39,099 – – 39,099 38,000 1,036 39,036 63

Child allowance – 26,130 – 26,130 25,764 366 26,130 –

Housing allowance – 5,222 – 5,222 4,940 281 5,222 –

Childcare allowance – 3,803 – 3,803 3,548 255 3,803 –

Maintenance support – 2,612 1,236 3,847 3,492 356 3,847 –

Sickness insurance2 64,365 11,670 – 76,035 82,979 4,229 87,208 –11,173 3

Grants to county councils – 681 – 681 681 – 681 –

Grants for the sick-listing process – 2,063 – 2,063 2,063 – 2,063 –

Dental care – 5,406 – 5,406 5,263 144 5,406 –

Healthcare abroad – 559 – 559 457 102 559 –

Disability allowance – 1,469 – 1,469 1,353 116 1,469 –

Activity grant 14,175 662 – 14,838 14,175 662 14,838 –

Introduction benefit – 3,717 – 3,717 3,667 50 3,717 –

Work injury compensation 4,508 – – 4,508 3,397 191 3,588 920

Car allowance – 318 – 318 280 38 318 –

Attendance allowance – 25,213 4,894 30,107 29,784 323 30,107 –

Housing supplement – 4,971 – 4,971 4,832 139 4,971 –

Other forms of compensation – 82 – 81 77 5 82 –

Total 122,147 94,577 6,130 222,854 224,751 8,293 233,044 –10,190

1 Includes parental benefit and temporary parental benefit, but in this table, pregnancy benefit, which is usually included in parental insurance, is included in the sickness insurance as it is financed by the sickness insurance contribution.

2 Includes sickness cash benefit, rehabilitation benefit and other rehabilitation compensation, sickness and activity compensation, pregnancy benefit, benefit for care of closely related people and high-cost protection for employers.

3 The difference between sickness insurance contributions and the expenses that they are to finance by law.

SOCIAL INSURANCE IN FIGURES 2016

31

Contribution rate (%) 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Old age pension contribution1 10.21 10.21 10.21 10.21 10.21 10.21 10.21 10.21 10.21 10.21

Survivor pension contribution1 1.7 1.7 1.7 1.7 1.7 1.17 1.17 1.17 1.17 1.17

Sickness insurance contribution

– Employer’s contribution 8.64 8.78 7.71 6.71 5.95 5.02 5.02 4.35 4.35 4.35

– Self-employed person’s social security contribution 9.61 9.61 7.93 6.93 6.04 5.11 5.11 4.44 4.44 4.44

Parental insurance contribution1 2.2 2.2 2.2 2.2 2.2 2.2 2.6 2.6 2.6 2.6

Work injury contribution1 0.68 0.68 0.68 0.68 0.68 0.68 0.3 0.3 0.3 0.3

Labour market contribution

– Employer’s contribution 4.45 4.45 2.43 2.43 4.65 2.91 2.91 2.91 2.91 2.64

– Self-employed person’s social security contribution 1.91 1.91 0.5 0.5 2.11 0.37 0.37 0.37 0.37 0.1

General payroll tax1 4.4 4.4 7.49 7.49 6.03 9.23 9.21 9.88 9.88 10.15

Total employer’s contribution 32.28 32.42 32.42 31.42 31.42 31.42 31.42 31.42 31.42 31.42

Total self-employed person’s social security contribution 30.71 30.71 30.71 29.71 28.97 28.97 28.97 28.97 28.97 28.97

1 Employer’s and self-employed person’s social security contribution have the same expenditure rate.

� Statutory contributions to social insurance in per cent of the contribution baseThe base for social insurance contributions consists of the payroll expense for employees and self-employed people. Employers and self-employed people pay the contributions. Certain changes in the contributions have been offset by corresponding changes to the general payroll tax (a contribution that is not linked to any special social insurance benefit or allowance). Total payroll taxes were thus

stable at just over 32 per cent until 2009. The sickness insurance contribution was lowered by one percentage point at that junc-ture, while other contributions remained unchanged. As a result, the total contribu-tion declined by one percentage point. The contribution rates were unchanged in 2015 compared to 2014.

SOCIAL INSURANCE IN FIGURES 2016

32

Registered insured persons

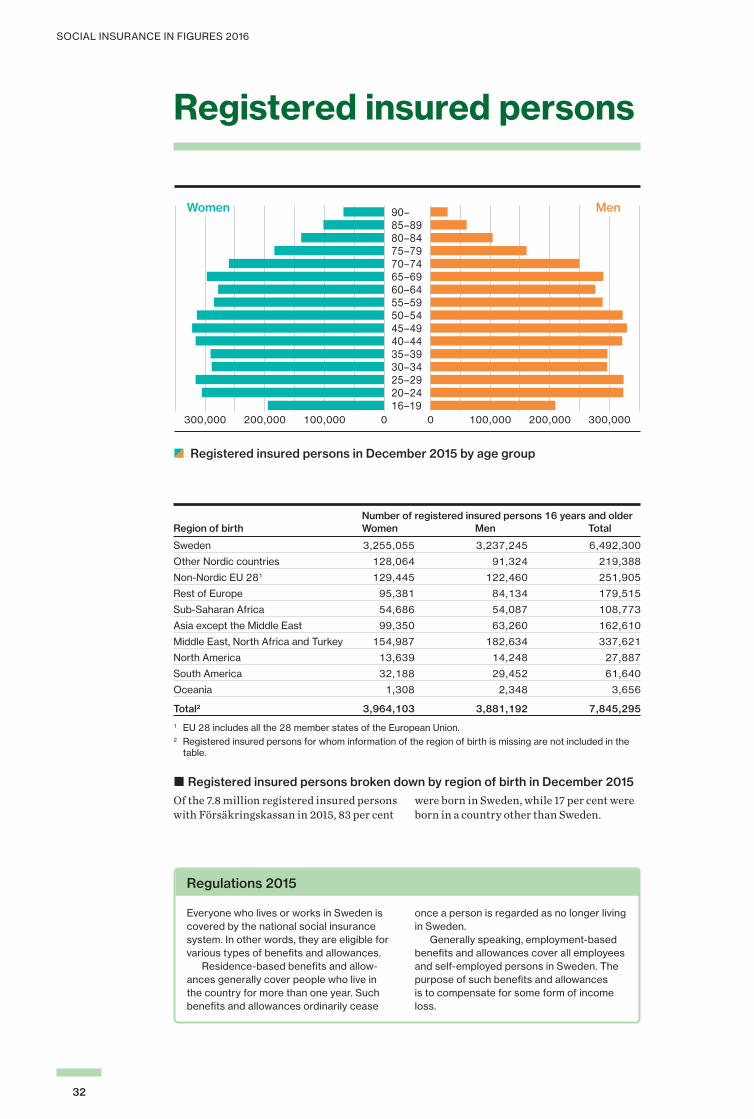

zy Registered insured persons in December 2015 by age group

Number of registered insured persons 16 years and older Region of birth Women Men Total

Sweden 3,255,055 3,237,245 6,492,300

Other Nordic countries 128,064 91,324 219,388

Non-Nordic EU 281 129,445 122,460 251,905

Rest of Europe 95,381 84,134 179,515

Sub-Saharan Africa 54,686 54,087 108,773

Asia except the Middle East 99,350 63,260 162,610

Middle East, North Africa and Turkey 154,987 182,634 337,621

North America 13,639 14,248 27,887

South America 32,188 29,452 61,640

Oceania 1,308 2,348 3,656

Total2 3,964,103 3,881,192 7,845,295

1 EU 28 includes all the 28 member states of the European Union.2 Registered insured persons for whom information of the region of birth is missing are not included in the

table.

� Registered insured persons broken down by region of birth in December 2015Of the 7.8 million registered insured persons with Försäkringskassan in 2015, 83 per cent

were born in Sweden, while 17 per cent were born in a country other than Sweden.

Regulations 2015

Everyone who lives or works in Sweden is covered by the national social insurance system. In other words, they are eligible for various types of benefits and allowances. Residence-based benefits and allow-ances generally cover people who live in the country for more than one year. Such benefits and allowances ordinarily cease

once a person is regarded as no longer living in Sweden. Generally speaking, employment-based benefits and allowances cover all employees and self-employed persons in Sweden. The purpose of such benefits and allowances is to compensate for some form of income loss.

0 100,000 200,000 300,00016–1920–2425–2930–3435–3940–4445–4950–5455–5960–6465–6970–7475–7980–8485–8990–

0100,000200,000300,000

MenWomen

SOCIAL INSURANCE IN FIGURES 2016

33

Number of registered insured persons Estimated percentage 19–64 years with sickness cash benefit Region of qualifying income birth Women Men Total Women Men Total

Sweden 2,220,021 2,322,348 4,542,369 90 89 90

Other Nordic countries 66,648 52,528 119,176 83 82 82

Non-Nordic EU 28 90,171 85,802 175,973 82 85 83

Rest of Europe 78,250 69,272 147,522 80 84 82

Sub-Saharan Africa 45,797 44,637 90,434 75 73 74

Asia except the Middle East 87,136 51,505 138,641 78 80 79

Middle East, North Africa and Turkey 129,041 152,182 281,223 70 75 73

North America 11,051 11,798 22,849 78 81 80

South America 27,542 25,343 52,885 83 85 84

Oceania 1,129 2,150 3,279 78 83 82

Total 2,756,786 2,817,565 5,574,351 88 88 88

The number of insured persons expected to have sickness cash benefit qualifying income is estimated here on those who have pensionable income that comes to at least 24 per cent of the price basic amount (excluding those who receive income-related activity or sickness compensation and those who do not have sickness cash benefit qualifying income but receive parental benefit at the guarantee level).

� Estimated proportion of insured people aged 19–64 with sickness cash benefit qualifying income at the beginning of 2015A larger proportion of those born in Sweden are expected to have sickness cash benefit qualifying income than those born abroad. Of those born in Sweden, 90 per cent were eligible for sickness cash benefit, pregnancy benefit, temporary parental benefit and other income-related daily compensation. A total of 70 per cent of women and 75 per cent of men born in the Middle East, North Africa and Turkey were entitled to sickness cash benefit qualifying income. The main reason that the proportion was lower for people born in certain regions of the world outside

Sweden is that they tend to have less of a foothold in the labour market. Figures for the proportion of insured people who were entitled to sickness cash benefit qualifying income are inexact; the reason being that the assessment was performed when a person applied for income-related daily compensa-tion. Thus, the data is based on an estimate that proceeds from information about pen-sionable income.

Regulations 2015

Insured people entitled to sickness cash benefit qualifying income are those expected to earn at least 24 per cent of the price basic amount every year from gainful employment. That corresponded to sickness cash benefit qualifying income of just under SEK 10,700

in 2015. Having the right to sickness cash benefit qualifying income is a basic prerequi-site for entitlement to sickness cash benefit, pregnancy benefit, temporary parental benefit and other income-related daily compensation.

SOCIAL INSURANCE IN FIGURES 2016

34

Financial security for families and children

Parental benefitThe purpose of parental benefit is to make it easier to combine parenthood with work or studies.

zy Parental benefit daysThe birth rate increased in the early 2000s, as did the number of parental benefit days. Quite a few changes occurred during the period with respect to the number of days and the amount of compensation. In 2015, parental benefit was paid for more than 53 million days, of which 74 per cent to women. Men accounted for an increased proportion of days during the period. From having received parental benefit for just over 14 per cent of the total days in 2001, by 2015 this amounted to 26 per cent.

zy Average number of parental benefit days at various ages for children born in 2007Most days of parental leave for children born in 2007 were during their first three years and were taken by women. After that age, there was no difference between women and men.

Number

0

10,000,000

20,000,000

30,000,000

40,000,000

2015201020052001

Women

Men

Number

Women

Men

Childs age, year

0

50

100

150

200

250

87654321

SOCIAL INSURANCE IN FIGURES 2016

35

� Proportion of days of parental benefit taken by men per county in 2015Men took 26 per cent of all parental ben-efit days in 2015. Men accounted for the most days (just short of 31 per cent) in Västerbotten County and fewest days (just short of 24 per cent) in Skåne County. The differences between the various munici-palities were quite large in many counties. For example, men accounted for a greater proportion of days in Umeå, Uppsala, Lund and other municipalities with large uni-versity towns than in sparsely populated municipalities. Men’s proportion of days of parental benefit is partially a function of the number of days taken by women. Thus, the men of two counties may differ in terms of their proportion of total days but not with respect to the average number of days per child, and the difference in proportions is then depend-ent on the number of days taken by women varying between counties.

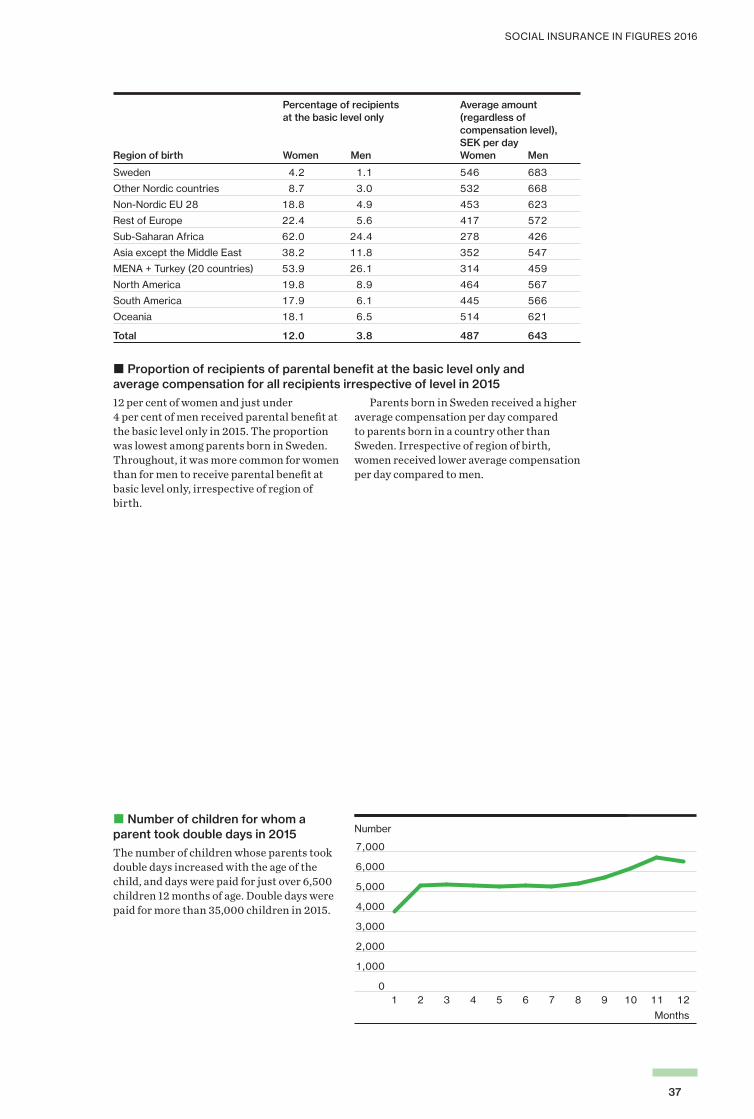

zy Proportion of recipients of parental benefit at the basic level only in 2015The proportion of recipients who received parental benefit at the basic level only declined until the age of 50, and then began to rise again. A total of 12 per cent of women and 4 per cent of men received parental ben-efit at the basic level only because they did not meet the requirements for income-re-lated parental benefit.

A total of 92 per cent of women and 75 per cent of men aged 19 and younger received parental benefit at the basic level only in 2015. However, few recipients of parental benefit were in this age group.

25.3–26.6

23.9–25.2

26.7–28.0

28.1–29.4

29.5–30.9

Women

Men

Per cent

0

20

40

60

80

100

55–50–5445–4940–4435–3930–3425–2920–24–19Age, year

SOCIAL INSURANCE IN FIGURES 2016

36

Number of children Percentage of children for whom parental benefit was paid Age Girls Boys Girls Boys

0 45,699 48,901 82 82

1 54,911 57,958 96 96

2 41,977 44,351 74 74

3 31,787 33,570 56 55

4 30,299 32,011 53 53

5 31,927 33,805 54 54

6 33,104 35,338 57 58

7 34,035 36,622 60 61

8 32,119 33,990 57 57

Total 335,858 356,546 65 65

� Children whose parents received parental benefit in 2015The parents of 82 per cent of children born in 2015 (age 0 in the table) received parental benefit during the year. The proportion declined after the child’s second birthday.