social care, health and wellbeing directorate

TRANSCRIPT

Social Care, Health and Wellbeing Directorate

Charging Policy for Home Care

and Other Non-Residential Services

To be read in conjunction with the: Care and Support (Charging and Assessment of Resources) Regulations 2014 and Care and Support Statutory Guidance

Issue Date:

11 April 2016

Review Date:

April 2017

Owner:

Policy and Standards Team

Policy&[email protected]

The document links in this policy are available in other formats.

Please contact [email protected] or telephone on 03000 416161

Charging policy for home care and other non-residential services 2

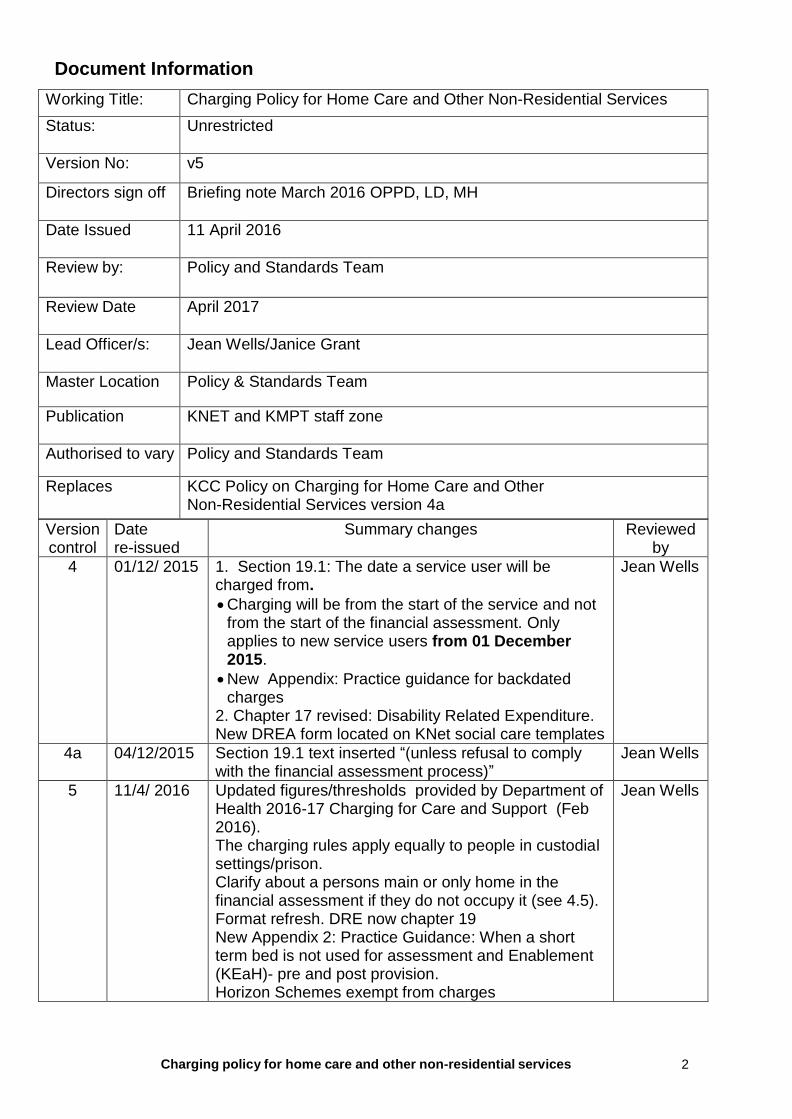

Document Information

Working Title: Charging Policy for Home Care and Other Non-Residential Services

Status: Unrestricted

Version No: v5

Directors sign off Briefing note March 2016 OPPD, LD, MH Date Issued 11 April 2016

Review by: Policy and Standards Team

Review Date April 2017

Lead Officer/s: Jean Wells/Janice Grant

Master Location Policy & Standards Team

Publication KNET and KMPT staff zone

Authorised to vary Policy and Standards Team

Replaces KCC Policy on Charging for Home Care and Other Non-Residential Services version 4a

Version control

Date re-issued

Summary changes Reviewed by

4 01/12/ 2015 1. Section 19.1: The date a service user will be charged from.

Charging will be from the start of the service and not from the start of the financial assessment. Only applies to new service users from 01 December 2015.

New Appendix: Practice guidance for backdated charges

2. Chapter 17 revised: Disability Related Expenditure. New DREA form located on KNet social care templates

Jean Wells

4a 04/12/2015 Section 19.1 text inserted “(unless refusal to comply with the financial assessment process)”

Jean Wells

5 11/4/ 2016 Updated figures/thresholds provided by Department of Health 2016-17 Charging for Care and Support (Feb 2016). The charging rules apply equally to people in custodial settings/prison. Clarify about a persons main or only home in the financial assessment if they do not occupy it (see 4.5). Format refresh. DRE now chapter 19 New Appendix 2: Practice Guidance: When a short term bed is not used for assessment and Enablement (KEaH)- pre and post provision. Horizon Schemes exempt from charges

Jean Wells

Charging policy for home care and other non-residential services 3

References

Legislation

Care Act 2014 Click here

The Care and Support (Charging and Assessment of Resources) Regulations 2014.

Click here

Care and Support Statutory Guidance Annex B (Treatment of capital) Care and Support Statutory Guidance Annex C (Treatment of income) Care and Support Statutory Guidance Annex E (Deprivation of assets)

Click here

Department of Health 2016-2017. Social Care: Charging for Care and Support

Upper Capital Limit £ 23,250

Lower Capital Limit £ 14,250

Lower Rate Attendance Allowance (AA) £ 55.10

Personal Independence Payment (PIP) standard care component £ 55.10

Personal Independence Payment (PIP) standard mobility component £ 21.80

Disability Living Allowance (DLA) standard care component £ 55.10

Disability Living Allowance (DLA) standard mobility component £ 21.80

Minimum Income Guarantee Rates (LAC(DH)(2016) Click here

Other references

KCC Adult Social Care Supporting Carers Policy on KNet Click here

Booket: Your Guide: To charging for care provided in your own home and support in the community” (the blue book) on www.Kent.gov.uk

Click here

Domiciliary Charge Advice letter” on KNet click here

Wellbeing Charge Practice Guidance on KNet Click here

Finance Referral Form on KNet Click here

Disregard -Exceptional form on KNet (charging and finance) Click here

Individual Disability Related Expenditure form (click here

Charging policy for home care and other non-residential services 4

CONTENTS PAGE

1 Introduction 1.1 People who cannot be charged 5 1.2 Services that are chargeable 1.3 Services that are not chargeable 1.4 Enablement (KEaH)- pre and post provision 1.5 Charging exceptions 1.6 A person lacking mental capacity to consent to a

financial assessment 2 Benefit Maximisation 7

3 Summary of how the charge is calculated 7 4 Assessing capital 8

5 Personal injury payments 9

6 Deprivation of assets 10 7 Person with assets more than the upper capital limit 10 8 Person with assets very close to the upper capital limit 10 9 Person with assets below the upper capital limit 10 10 Person with assets below the lower capital limit 10 11 Assessing income 11 12 Couples assessment 12 13 Failure to apply for benefits 13

14 Verification 13 15 Minimum income guarantee 13 16 Working out the income available for charging 14 17 Working out the cost of chargeable services 15 18 Determining the charge 15 19 Disability related expenditure assessment 15 20 Charges-start date 19 21 Optional extras 19 22 Voluntary contributions 20

23 When a person dies 20 24 Wellbeing charge 20

Appendix 1: Practice guidance for backdated charges 21 Appendix 2: Practice Guidance: Short term beds Enablement (KEaH)- pre and post provision 23

Charging policy for home care and other non-residential services 5

1. Introduction The Care Act 2014 provides a single legal framework for charging for care and support under sections 14 and 17. It enables a local authority to decide whether or not to charge a person when arranging to meet a person’s care and support needs or a carer’s support needs. The charging rules apply equally to people in custodial settings/prison. Whilst prisoners have restricted access to paid employment and benefits (and earnings in prison are to be disregarded for the purposes of the financial assessments), any capital assets, savings and pensions will need specific consideration.

The Care and Support Statutory Guidance issued under the Care Act, Annex B, C and E sets out guidance for the treatment of capital; income when conducting a financial assessment in all circumstances and how to respond when a person deliberately deprives themselves of assets.

Regulations state that a charge must not reduce the person’s income below the minimum income guarantee specified in the Care and Support (Charging and Assessment of Resources) Regulation 2014. Earnings must be completely disregarded. In the case of a direct payment, charge is deducted before the direct payment is made to the person, i.e. they are paid Net1 of their financial contribution. Regulations specify that a carer cannot be charged for any provision made directly to the person needing care (replacement care). It would be the person needing care who would be charged, not the carer. Where KCC is meeting the needs of a carer by providing a service directly to a carer, KCC has currently exercised its discretion not to charge the carer. See Supporting Carers Policy for further details. Regulations specify the services which must always be provided free of charge and the persons to whom services must always be provided free of charge. The lists below show which people and services are chargeable and which are not.

1.1 People are not charged when:

receiving NHS Continuing Healthcare;

receiving intermediate care/enablement services (first 6 weeks);

receiving services provided under Section 117 of the Mental Health Act (1983);

receiving certain war pensions;

suffering from variant Creutzfeldt-Jakob disease2;

1.2 Services that are chargeable

personal care provided at home and away from the home;

care and support provided in custodial settings/prison;

community support services;

respite care provided in the home or other setting3 ;

day care (except grant-funded).

1. A net direct payment is allocated after any appropriate charges have been subtracted.

2 A degenerative neurological disorder that is incurable and invariably fatal. Evidence same strain that causes bovine spongiform

encephalopathy (BSE or 'mad cow disease'). 3 If respite in one of KCC’s own residential units or KCC contracts directly with a residential home for the respite, residential

charging rules apply.

Charging policy for home care and other non-residential services 6

1.3 Services that are not chargeable

information and advice;

advocacy;

assessment services (including financial assessment);

preparation of a care and support plan

community equipment (aids and minor adaptations to a property)4

enablement (eg Kent Enablement at Home/KEaH) – up to six weeks5

intermediate care – up to six weeks;

Technology Enabled Care Services (TECS) eg telecare, GPS devises etc;

transport;

grant funded day care;

grant funded employment services;

services provided directly for the carer to meet their eligible needs6;

Kent Pathway Service (LD)- up to 12 weeks;

Kent Enablement and Recovery Service (MH) – up to 12 weeks;

Early Intervention in Psychosis Service - up to 12 weeks. (After 12 weeks or if service user requires long term support (e.g. annual gym membership), then service will be chargeable).

Horizon Schemes7

NB: For Mental Health financial assessments, these are offered as a joint face-to-face assessment with the Mental Health team.

1.4 Enablement (KEaH)- pre and post provision If a person remains with OPPD/KEaH because there is no alternative service after the period of enablement (which was a not chargeable up to 6 weeks), in these circumstances, the person to be informed that the service is chargeable (subject to a financial assessment) from KCC until another provider becomes available. Equally, if a person is waiting for the KEaH service to be available, a person may receive or continue to receive a chargeable service whilst waiting for the enablement provision to start.

Note: This is an in house chargeable service, not enablement. See Appendix 2 for full details.

1.5 Charging: Exceptional Discretionary Disregards

The charging policy allows for an exceptional disregard when it is reasonable for a charge to be waived. Use “Disregard Exceptions” Form on KNet templates to apply for a disregard and approval sought from the appropriate delegated authority. A person may have exceptional expenditure, which makes it difficult to pay the assessed charge. For example – debt repayments, cost of transport, expenses not fully covered by the

Disability Related Expenditure disregard8

4 Care and Support (Charging and Assessment of Resources) Regulations (3)(3) define an aid for the purpose of assisting with

nursing at home, or aiding daily living and a minor adaption if the cost of making the adaptation is £1000 or less 5 Care and Support (Charging and Assessment of Resources) Regulations (3) (3) programme of care and support; specified

period of time; purpose to assist an adult to maintain or regain the ability to live independently in their own home. 6 Currently, KCC has exercised its discretion not to change the carer. See Supporting Carers Policy for further details.

7 Horizon schemes are: Shepway: Newman House, Canterbury: Denmark House, Monson Court, Thanet: Library House.

8 See chapter 19 for more details about DREA

Charging policy for home care and other non-residential services 7

1.6 People Lacking Mental Capacity to Consent

Where a person lacks capacity, they may still be assessed as being able to contribute towards the cost of their care. People who lack mental capacity to give consent to a financial assessment and who do not

have a legal representative* with authority to be involved in their affairs, may require the

appointment of a property and affairs deputyship.

* It must be established whether the person has any of the following people with legal powers to

act on their behalf:

enduring power of attorney (EPA); lasting power of attorney (LPA) for property and affairs; lasting power of attorney (LPA) for health and welfare; property and affairs deputyship under the court of protection; or any other person dealing with that person’s affairs (e.g. someone who has been given

appointee-ship by the Department for Work and Pensions (DWP) for the purpose of benefits payments).

A person who does not have any of the above people with authority to be involved in their affairs, family members can apply for a property and affairs deputyship to the Court of Protection or KCC can apply if there is no family involved in the care of the person.

2. Benefit maximization A person should have their benefits maximised at the same time as the financial assessment is carried out. This may be in the form information and advice in line with the Equality Act 2010 requirements under the Care Act 2014.

It is KCC policy to help a person claim all their entitled benefits. The take up of welfare benefits is very important for the following reasons:

to maximise the income of persons, which has a direct effect upon their living standards, dependency levels and participation in society;

to maximise income for the authority. KCC needs the contributions that a person makes to ensure we are able to continue to help as many people as possible with the limited resources that are available;

the take up of certain benefits is monitored by Central Government, who use this information, amongst other factors, to inform the level of funding a local authority receives.

There are a small number Senior Benefit Officers who are based across the county. Senior Benefit Officers provide advice, information and support to persons with complex benefit issues including appeal representation. They only undertake work for people with a chargeable service and people supported by mental health teams.

3. Summary of how the charge is calculated In the financial assessment, resources should only be treated as income or capital but not both. 3.1 Firstly, a person is assessed to see how much capital (savings and other assets) they have (excluding the value of their main or only home see 4.5 for other details). If they have more

Charging policy for home care and other non-residential services 8

than the upper capital limit they will be expected to pay the full cost of their care. Also, they will not be entitled to a direct payment from KCC if their charge is the the same amount as the cost of their service, thereby reducing any direct payment to nil. 3.2 A person with assets between the upper and lower capital limits will pay what they can afford from their income, plus a means-tested contribution from their assets A tariff income is applied for a person who has capital between lower capital limit and upper capital limit (see section 11 Assessing Income for more details). After certain amounts have been deducted from this income they will be left with an amount that is “available” for charging (also known as “disposable income”). 3.3. A person with assets below the lower capital limit will pay only what they can afford from their income. (See section 11, 15, 16 for more details about assessing income, Minimum Income Guarantee and working out available income for charging). 3.4 Resources should only be treated as income or capital but not both. If a person has saved money from their income, then those savings should normally be treated as capital. However they should not be assessed as both income and capital in the same period. Therefore in the period when they are received as income, the resource should be disregarded as capital.

3.5 The actual charge is worked out by comparing 100% of the available income to the cost of their care/personal budget. The charge is whichever is the lower figure.

3.6 If the person is one of a couple9, then a couple’s assessment is offered to see if this results in a lower charge. This is only used if it results in a lower charge. (NB: a local authority has no power to assess couples or civil partners according to their joint resources).

3.7 Once the Financial Assessment Form (FAF) has been completed by the Financial Assessment Officer or the person/financial agent, the Assessment Officer calculates the charge and adds to SWIFT. The notes below give further detail of each stage in the calculation.

4. Assessing Capital A capital asset is normally defined as belonging to the person in whose name it is held- the legal owner. Where ownership is disputed, KCC finance must seek written evidence to prove where the ownership lies. If a person states they are holding capital for someone else, evidence should be obtained of the arrangement, the origin of the capital and intentions for its future use and return to its rightful owner.

4.1 In order to determine the amount of capital owned by a person, the following are added together:

all sources of capital held solely by a person;

half of any capital jointly owned unless there is strong evidence why this should not happen and a different apportionment be used.

4.2 Generally speaking, the capital assets taken into account are those that can be realised, for example:

money in bank, building society, post office;

premium bonds;

9 Partner and couple (living together) has the same meaning as in the Income Support Regulations.

Charging policy for home care and other non-residential services 9

national savings;

stocks and shares (valued according to the latest FT index – Finance will assist);

investment bonds that can be realised, unless they have Life Assurance attached);

ISAs etc.

4.3 If an asset is taken into account as capital then any actual income from that capital asset is ignored. Instead, the tariff income rules apply (see section 11 below - Assessing Income).

4.4 Capital that has been used to purchase Income Plans such as annuities, which cannot be realised, are not taken into account as capital. Instead, the actual income generated from them is taken into account as income.

4.5 Capital to be disregarded

the value of the property which is the persons main or only home10

;

the surrender value of an annuity or life assurance/endowment policy; personal possessions, antiques etc;

funds held in trust or administered by a court o r d e r for vaccine damage, compensation funds, criminal injury, personal injuries etc. See section 5 on Personal Injury payments below;

arrears of benefits. These should, however, be taken into account as income in a retrospective charging assessment (see section on retrospective charging below);

capital of any partner (if capital is held in joint names it should be divided in two unless there is strong evidence why this should not be the case).

Note: any actual income from disregarded capital is taken into account as income, for example income from Personal Injury payments – see below.

5. Personal Injury Payments11

5.1 Capital disregarded Where a person has been awarded damages in consequence of a personal injury to that person and the sum is

held in trust or;

administered on behalf of that person by the court or;

only able to be disposed of by the direction of the court.

the amount shall be fully disregarded from the calculation of the person’s capital. Note:

1) For the first 52 weeks, the capital must be disregarded unless specifically identified by the courts to pay for care. NB: even if it is for care, it must be disregarded if it is in a trust or administered by the Court.

10

KCC has exercised its discretion, if the person does not occupy their home and, for example has moved in with their daughter,

the persons home/s are still disregarded in the assessment of capital, but any income generated from the property (e.g. has rented

it out) will be taken into account when assessing income. 11

In the case of ZYN v Walsall MBC [2014] EWHC 1918 (Admin) the High Court has ruled that capital derived from personal

injury damages which is held by a Court of Protection appointed deputy is disregarded for means testing purposes.

Charging policy for home care and other non-residential services 10

2) After 52 weeks, the capital may be taken into account unless held in a trust or administered by the court. Staff must be provided with the originals of trust documents etc. and if necessary take advice from Legal Services.

5.2 Income

Income from a personal injury trust, including those administered by a Court, must be fully disregarded.

6. Deprivation of Assets 6.1 When undertaking or reviewing a financial assessment, there may be circumstances that suggest that a person may have deliberately deprived themselves of assets or decreased their overall assets in order to reduce the amount they are charged towards their care. 6.2 It is up to the person to prove they no longer have the asset. If they are not able to, the financial assessment will treat them as if they still had the asset. 6.3 In such cases, KCC may either charge the person as if they still possessed the asset or, if the asset has been transferred to someone else, seek to recover the lost income from charges from that person. However, KCC cannot recover more than the person gained from the transfer.

7. Person with Assets in Excess of the Upper Capital Limit12 7.1 The Care Act places a statutory duty on local authorities to arrange care and support for a person with eligible needs with more than the upper capital limit if the person requests. This duty only extends to non-residential care (local authority discretion for residential care). These persons are not entitled to receive any financial assistance from KCC and may pay the full cost of their care and support until their capital falls below the upper capital limit.

7.2 All available options should be discussed with the person, their carer and/or family as appropriate. In addition, safeguarding issues should be considered. If a person does decide to arrange, contract and pay directly to a private provider, it must be explained that KCC will not be involved in the day-to-day management of that care or financial matters concerned with the service provided.

8. Person with Assets Very Close to Upper Capital Limit 8.1 Where an person chooses to self- fund their care, it should be explained that if they return to KCC for assistance with the funding of their care they would be re-assessed using the eligibility criteria and that may mean we would not fund all of the privately purchased care.

9. Person with Assets Below the Upper Capital Limit Below this level, a person can seek means-tested support. KCC will undertake a financial assessment of the person’s assets and will make a charge based on what the person can afford to pay.

12

See reference section at the beginning of this document

Charging policy for home care and other non-residential services 11

10. Person with Assets Below the Lower Capital Limit13 In the financial assessment, capital below the lower capital limit is disregarded in the assessment of what a person can pay. A person with assets below the lower capital limit will pay only what they can afford from their income. (See section 11, 15, 16 for more details about assessing income, Minimum Income Guarantee, working out available income).

11. Assessing Income Only the income of the cared for person can be taken into account in the financial assessment. Where the person receives income as one of a couple, the starting assumption is that the cared for person has an equal share of the income, taking into account the implications for the cared for person’s partner.

11.1 All income (except disregarded income see 11.2 below) paid to the person should be included in the assessment. Information about the main forms of income to be included and those to be disregarded is held by the Assessment Officer who uses it to calculate the charge. It should be noted that a number of new benefits have come into effect in recent years, most notably Personal Independence Payment (PIP) which replaces Disability Living Allowance (DLA). However, some current DLA claimants remain in receipt of the old benefit and so both types of benefits are referenced in this policy document.

11.2 When assessing incomes, the following should be noted14

Income from the following sources to be fully disregarded:

direct payments;

guaranteed income payments made to Veterans under the Armed Forces Compensation Scheme;

mobility component of Disability Living Allowance;

mobility component of Personal Independence Payments;

all earnings including earnings from ‘permitted work’

earnings in prison;

working tax credit as this tops up low wages;

all income paid in respect of children– Child Benefit, Child Tax Credit, amounts paid with Income Support for Children (from April 2004 these amounts are being transferred to Child Tax Credit but this process has not been completed so some people will still be receiving them);

amounts in Income Support, Employment Support Allowance or Pension; credit paid in respect of mortgage interest.

In addition:

any capital between the lower capital limit and the upper capital limit, it is assumed that for every £500 (£250 for residential charging purposes) of capital or part thereof, the person is able to afford to contribute £1 per week towards the cost of their care. This will be added to their weekly income when assessing their weekly charge;

pension credit – only include the Guarantee Credit, not the Savings Credit.

13

See reference section at the beginning of this document 14

Also refer to “Annex C: Treatment of income” in the Care and Support Statutory Guidance. Types of income that must be

disregarded in the means test are listed in Schedule 1, Part 1, of the charging regulations.

Charging policy for home care and other non-residential services 12

Savings credit disregard;

attendance allowance (AA), PIP/DLA (Care Component (and equivalents) should be taken into account only up to the lower rate of AA15 and standard rate of PIP/DLA (Care Component). This should be the case even if they receive the higher rate of these benefits.

the Carers' Premium/Addition must be deducted from the Income Support/ESA or Pension Credit before dividing it in two;

war pensions and war widows pensions should be disregarded except for the following elements: - Constant Attendance Allowance (CAA) – Exceptionally Severe Disablement Allowance (ESDA). These elements are similar to AA/PIP/DLA (Care Component) and are paid instead of them – they should therefore be taken into account – to the value of lower rate AA;

income from tenants living in a second home should be fully taken into account;

private insurance towards the cost of non-residential services – these may be provided to supplement the services arranged by KCC or may meet part or all of the charge levied by us. These payments should be disregarded in the assessment of income;

amounts sometimes paid with Incapacity Benefit/ESA, Retirement Pension etc. for dependent partner should be disregarded.

12. Couple/partner Assessments16 12.1 The financial assessment should only take into account the income and capital of the person and not that of their partner. In KCC this is called a ‘half-couple’ assessment. Retirement Pensions, Occupational Pensions etc. are usually paid in respect of one person only and so should be attributed to whoever’s name they are in. Certain benefits, however, are paid in respect of the couple and should therefore be divided in two, e.g. Pension Credit and Income Support. (NB: a local authority has no power to assess couples or civil partners according to their joint resources). Example (figures for illustrative purposes) Mr & Mrs Smith

Mr Smith receives £110.15 State Retirement Pension (SRP) Mrs Smith receives £66.00 SRP + Attendance Allowance (AA) of £55.10.

In addition they receive Pension Credit (PC) as a couple. Pension Credit received is £54.70. This should be divided in two giving each person £27.35. So if Mrs Smith was the service user her income would be:

£66.00 SRP £27.35 half of PC £55.10 AA

£148.45

15

See reference section at the beginning of this document 16

Partner and couple has the same meaning as in the Income Support Regulations: Partner as a member of a couple i.e. a man

and woman who are married to each other and are members of the same household; (b) a man and woman who are not married to

each other but are living together as husband and wife; (c) two people of the same sex who are civil partners of each other and are

members of the same household; or (d) two people of the same sex who are not civil partners of each other but are living together

as if they were civil partners, and for the purposes of paragraph (d), two people of the same sex are to be regarded as living

together as if they were civil partners if, but only if, they would be regarded as living together as husband and wife were they

instead two people of the opposite sex.

Charging policy for home care and other non-residential services 13

12.2 If the person’s partner is willing to disclose his/her income and capital, a joint financial assessment can be carried out to determine whether they would be better off assessed as a couple. A person is most likely to benefit from this if their pa r tne r has a much lower income than they have. The result of a couple’s assessment is only used if it results in a lower charge.

13. Failure to apply for benefits 13.1 If it is clear that a person is entitled to a means-tested benefit such as Income Support, Employment Support Allowance (income based) or Pension Credit it will be expected that they apply for this. If they fail to do so within one month of being advised, it will nevertheless be assumed they have this income. This will not apply in the following circumstances:

to benefits like Attendance Allowance and Personal Independence Payment/Disability

Living Allowance as there is never any guarantee that these will be awarded;

if the person is under 20 and the reason they have not applied for ESA is because they still live with their family and it was decided the family as a whole would be better off if the parents carried on claiming for the young person (meaning the young person could not claim ESA).

14. Verification 14.1 The person's income and /or capital must be verified. It is not sufficient for the person to simply state that they are in receipt of certain benefits and/or have savings/capital. Verification is sought either from the Department for Work and Pensions or from bank/income statements from the person/representative.

15. Minimum Income Guarantee (Protected Income Level) 15.1 Because a person who receives care and support outside a care home will need to pay their daily living costs such as rent, food and utilities, the charging rules must ensure they have enough money to meet these costs. After charging, a person must be left with the Minimum Income Guarantee (MIG) as set out in the Care and Support (Charging and Assessment of Resources) Regulation 2014. At present, KCC only need to apply this test if a person has less than upper capital limit. 15.2 In addition, where a person receives benefits to meet their disability needs that do not meet the eligibility criteria for local authority care and support, the charging arrangements should ensure that they keep enough money to cover the cost of meeting these disability-related costs. Click here for (LAC(DH)(2016) for the MIG rates for 2016/17.

Note the Enhanced Disability Premium is added whether in reality the Service User is entitled to it or not.

16. Working out the income available for charging 16.1 This is a straightforward calculation. From the person’s total assessable income, you should deduct the following:

the appropriate Minimum Income Guarantee /Protected Income Level;

any weekly l oan re pa ym en t f o r OT adap ta t ions ( this does not include repayments

Charging policy for home care and other non-residential services 14

on private loans);

any Supporting People charge paid by the person. This is not the cost of the Supporting People Service but the amount actually paid by the person. Nearly everyone will be exempt from this charge and not pay anything;

any rent paid (i.e. After Housing Benefit taken off) – note that due to welfare reform changes, some persons of working age may get less Housing Benefit and therefore have to pay some/more rent; In most cases, you need to verify rent paid. The only exceptions would be where a person pays an amount to a relative they live with. In these cases, the figure should be accepted if it appears reasonable, and as long as you don’t include an amount for food. It should also be a figure in proportion to the number of people in the household;

any Council Tax paid (i.e. after Council Tax Support taken off);

costs related to leasehold properties – e.g. service charges, ground rent - owner-occupied sheltered flats often come into this category (i.e. after any benefit paid for this has been taken off);

any costs related to a mortgage (i.e. after any benefit paid for this has been taken off). Mortgage costs that can be allowed include:

- Interest on loans for home purchase and essential repairs/improvements;

endowment premiums, buildings insurance, capital repayments;

standard Disability Related Expenditure Disregard of £17 per week. This should be given to every person regardless of which benefits they receive.

16.2 Those persons who are in receipt of a disability benefit may opt for an individual DRE (Disability Related Expenditure Disregard) assessment. See section 19 below.

16.3 After all the above deductions you will be left with a figure that is income available for charging. This figure (100% of it since 12 December 2011) will then be used to work out the cost of chargeable services.

17. Working out the cost of chargeable services The cost of chargeable services should be provided by the Case Manager/Care Coordinator or, as is more often the case, obtained from SWIFT.

17.1 What to do if the person receives less than the agreed amount of service.

Persons who pay the full cost of their service should have their charge reduced for each half hour less service they receive in any week (Monday-Sunday). Persons whose charge is based on their income should only see a reduction in their charge if the cost of their service falls below their usual charge. In this case, their charge should reduce to the cost of their service.

Case Managers/Care Coordinators are responsible for updating SWIFT with details of missed service in any one week. The SWIFT system will then work out whether an adjustment to the charge needs to be made.

18. Determining the charge 18.1 The charge for single people and one of a couple (half-couple): The person will be charged either 100% of the income they have available for charging or the cost of their

Charging policy for home care and other non-residential services 15

service/Personal Budget whichever is the lesser figure. 18.2 If there is a charge for one person in a couple then they should be offered a couple’s assessment to see if this will reduce the charge. This should only be used if this results in a lower charge.

19. Disability Related Expenditure Note: Case Manager relates to Case Manager, Care Manager, Care Coordinator or Social Worker. 19.1 Disability Related Expenditure (DRE) is expenditure incurred as a direct result of a person’s disability or medical condition. It is expenditure over and above what a non-disabled person would spend. 19.2 Councils are required by the Care Act 2014 and its associated guidance and regulations to offer a Disability Related Expenditure Assessment (DREA) to anyone who is in receipt of disability-related benefits when these are taken into account in the charging assessment. 19.3 Disability benefits for the above purpose are: • Attendance Allowance • Disability Living Allowance Care Component (middle or higher rates only) • Personal Independence Payment Care Component (standard or enhanced rates only). • Constant Attendance Allowance. • Exceptionally Severe Disablement Allowance.

The intention is to allow the person to keep enough benefit to pay necessary disability or medical condition related expenditure to meet any needs that are not being met by the local authority.

19.4 The Kent County Council “non-residential charging policy” allows a person with less than the upper capital limit, a standard disability related disregard of £17 per week. If a person who is on a disability benefit believes they have DRE of more than £17 per week, they can request an individual assessment. If the figure arrived at is higher than the £17 standard disregard, then the higher figure is used. If lower, the £17 standard figure is used. See Fig 2 and 3 para 19.8.for illustration. 19.5 All claims for additional DRE in excess of the £17 per week require approval and authorisation by the budget holder (e.g. OPPD/MH Service Manager/LD Locality Team Manager).

19.6. Who Completes the Assessment? 19.6.1 DRE should be evidenced in the care and support plan however, flexibility is needed when calculating the amount allowed. DRE should not be limited to what is necessary for care and support, for example, above average heating costs should be considered (see 19.9 for more details) 19.6.2 If the person provides evidence of extra expense incurred as a result of their disability or medical condition, the Case Manager should discuss this with them during their needs assessment. 19.6.3 The Case Manager should ensure the person understands that if they request a DREA, clearly evidenced expenditure above £17 per week only will affect their charge. Details, including the amount of any DRE, are passed to the Assessment Officer in finance so that this figure can be taken into account when the charge is calculated (see Fig 2 para 19.8).

Charging policy for home care and other non-residential services 16

19.6.4 If DRE is only evident or raised at the financial assessment stage, then the Assessment Officer in finance to inform the Case Manager of the amount claimed. 19.6.5 It is the Case Manager responsibility to seek approval and authorisation from the budget holder before agreeing the amount and signing the DREA form (click here for link). Until the amounts been agreed, the standard amount of £17 per week will be used to calculate the charge and charging will start immediately to avoid a loss of income. 19.6.6 If an increased level of DRE is agreed, the charge is reassessed and the higher level of DRE will apply from the start of the service or when the persons assessed, unless the person only requested an individual DRE at a later date (except in cases of unreasonable delays).

Fig 1: Flowchart showing who should carry out the Disability Related Expenditure Assessment

DREA raised at Needs Assessment DREA raised at Financial Assessment

CM completes DREA AO Contacts CM to request they undertake a DREA or take part in a joint assessment. This will then be agreed by the CM

CM informs AO if the amount is more than £17.00

If more than £17.00, AO uses this for financial assessment

AO uses this for Financial Assessment

CM = Case Manager AO = Assessment Officer (Finance)

Whoever carries out the assessment, they are responsible for ensuring that the person produces documentary evidence of any expenses to be allowed.

19.7. Suitable disability related expenditure Disability related expenditure will only be made where those costs are:

met entirely by the person;

specifically relate to the disability or medical condition in question and

exceed what a person without the disability or medical condition would reasonably be expected to spend.

Expenditure is unlikely to be approved where:

the person is receiving a personal budget that already incorporates some of the identified disability related expenditure;

any additional disability related services or equipment provided by the NHS – such as physiotherapy, chiropody, incontinence pads, and transport – or are facilitated by or provided through the County Council.

19.8. Examples of Disability Related Expenditure

In assessing disability related expenditure, the following should be included. However this list is not intended to be exhaustive and any reasonable additional costs directly related to a person’s disability should be included when they are not incorporated in a personal budget, direct payment, provided by the NHS or provided/facilitated through the County Council:

Charging policy for home care and other non-residential services 17

a) Payment for any community alarm system. b) Costs of any privately arranged care services required, including respite care. c) Any additional costs needed to meet the person’s needs because of disability or medical

condition, for example:

day or night care which is not being arranged by the local authority;

specialist washing powders or laundry;

additional costs of special dietary needs due to illness or disability;

special clothing or footwear, for example, where this needs to be specially made; or additional wear and tear to clothing and footwear caused by disability;

additional costs of bedding, for example, because of incontinence;

any heating costs (see 19.9 below) or metered costs of water, above the average levels for the area and housing type,

reasonable costs of basic garden maintenance, cleaning, or domestic help, if necessitated by the person’s disability and not met by the local authority;

purchase, maintenance, and repair of disability-related equipment (e.g. wheelchairs, powered bed, turning bed, powered reclining chair hoists, stair lifts) when not supplied or facilitated by the County Council (i.e. privately purchased);

internet access for example for blind and partially sighted people;

other transport costs17 necessitated by illness or disability over and above the mobility component of DLA or PIP.

As stated above, the expenditure claimed must be over and above what a non-disabled person would incur and be directly related to the person’s disability or medical condition.

Fig 2:

Example 1: disability related expenditure (Reference: Care and Support Statutory Guidance Disability Related Expenditure Annex C: Treatment of Income) Zach is visually impaired and describes the internet as a portal into the seeing world – in enabling him to access information that sighted people take for granted. For example, he explains that if a sighted person wants to access information they can go to a library, pick up a book or buy an appropriate magazine that provides them with the information they need. The internet is also a portal into shopping. For example without the internet if Zach wanted to shop for clothes, food or a gift he would have to wait until a friend or family member could accompany him on a trip out, he would be held by their schedule and they would then have to explain what goods were on offer, what an item looked like, the colour etc. and would inevitably be based on the opinion and advice of said friend. A sighted person would be able to go into a shop when their schedule suits and consider what purchase to make on their own. The internet provides Zach with the freedom and independence to do these things on his own. The Internet access costs £5 per week and he has no other disability related expenditure. Because the cost of the internet is less than the £17 he already receives from KCC for DRE, he will receive £17 only. (Note there must be clear evidence that this is related to his disability need)

17

It may be reasonable for a council not to take account of claimed transport costs – if, for example, a suitable, cheaper form of

transport, e.g. council- provided transport to day centres is available, but has not been used: ref Care and Support Statutory

Guidance: Annex C Treatment of Income paragraph 38(xv).

Charging policy for home care and other non-residential services 18

Fig 3:

Example 2: disability related expenditure

Zach has internet access and has other DRE costs to help with basic private domestic help and gardening. These costs are £15 per week. This means his total disability related expenditure is £20 (£5 internet and £15 basic help). This means that his DRE is in excess of the £17 he already receives, so he will receive the £20 only (not £17 plus £20).

19.9 Heating Costs

The difference between standard cost and the actual cost incurred because of disability or medical condition is the amount that is allowed for DRE. For example if the standard cost of heating is £1,157 and a person can evidence £1,203 the disability related amount is £46. See Fig. 4 for current figures sourced from National Association of Financial Assessment Officers. Fig 4:

2016/17 Figures18 Single person - Flat/Terrace £1,143 Couple – Flat/Terrace £1,508 Single person – Semi Detached £1,214 Couples – Semi Detached £1,600 Single – Detached £1,477 Couples – Detached £1,947

20. Charges

20.1 Charging will be from the start of the service and not from the start of the financial assessment. A person will not be charged before a financial assessment is completed (unless refusal to comply with the financial assessment process). The financial referral and assessment should be completed as soon as possible to avoid people being faced with large unexpected bills. Where any arrears of charges are due, people should be given a reasonable length of time in which to pay. If the person has difficulty paying the invoice in one go, they will be expected to contact KCC Debt Recovery to arrange payment over a longer period. It is expected charges will not be backdated for more than 12 weeks BUT this can, in exceptional circumstances be extended, such as where a person/family deliberately do not cooperate. Detailed practice guidance in Appendix 1 link here

20.2 Following benefits maximisation the person’s income is increased Typically, this involves the receipt of Attendance Allowance or Disability Living Allowance (Care Component) /Personal Independence Payment (Care Component) but it could involve any benefit including Income Support, Income- related ESA and Pension Credit. This will be backdated to the date it was applied for and logically so should an increased charge if this applies, provided the person was informed of the revised exact amount to be charged, should the increase occur.

Example to illustrate benefit maximisation and retrospective charging

1 January - service or Direct Payment starts; person is assessed as being nil charge because of their income - they are not on Attendance Allowance. On same day an application is logged

18

Source: National Association of Financial Assessment Officers: standard rate.

Charging policy for home care and other non-residential services 19

with DWP for AA (they send out forms and as long as returned within 6 weeks, the award will run from 1 January).

7 April – person informed that awarded AA which he/she starts being paid. H e / she also receives a cheque for arrears of AA going back to 1 January. H e / she may now have a charge, as her income is higher. This should be backdated to 1 January.

20.3 A reduction in charge

If the person is assessed as needing a reduction in their charge and this should have applied from an earlier date, then the reduction will be backdated to the date of the change.

21. Optional Extras

21.1 Some persons may wish to purchase services in addition to their care packages/personal budget e.g. extra time to polish brasses, shine windows etc. This additional help may well be purchased from the same agency and may well be provided by the same home carer who visits for social services – this is often at the person’s express wish.

21.2 In these cases it is important to give the person something in writing that states clearly what is provided by KCC at the subsidised rate (unless full cost) and what is purchased privately at full cost. It should also state that service arranged privately will not be invoiced or paid through KCC TDM19. The private element will NOT appear anywhere on the FAF and will NOT be included in the calculation of the charge for non-residential services.

22. Voluntary Contributions

22.1 A small number of persons insist, on principle, on paying more than the assessed charge, perhaps even as a condition of accepting services. It remains the case to allow voluntary contributions in excess of the assessed charge in these instances. Such agreements should be confirmed in writing with an explanation of the voluntary nature of the additional contribution and a reminder of the opportunity for the person to request reassessment and review the arrangement at any time.

23. What to do when an person receiving services dies 23.1 Following a suitable period, discussions should take place with the next of kin/representative about collecting any outstanding charge. 23.2 A decision to waive or write off any charge in these circumstances must be agreed b y the Assistant Director.

24. Wellbeing Charge 24.1 The Wellbeing Charge is a contribution that tenants living in extra care settings make towards the cost of the background 24 hour support that is available in the event an emergency that occurs. Everyone who enters an extra care scheme should be advised of the Wellbeing Charge.

19

Trans Data Matching System which is an automated payment system to providers

Charging policy for home care and other non-residential services 20

24.2 All people moving into an extra care scheme must have a financial assessment to determine their contribution to the cost of the Wellbeing Charge and their care and support. This applies both to people who meet the eligibility criteria and to those who do not. 24.3 The Wellbeing Charge is NOT part of someone’s personal care package, however the charge will be considered as part of the assessed charge for the care package (if they have one), and therefore the assessed contribution will only include one financial contribution towards the cost of the care package together with the Wellbeing Charge. 24.4. If two people move to an extra care scheme and both have eligible social care needs, the Wellbeing Charge is split equally. If only one person has a social care need, then the person will pay the full Wellbeing Charge. If that person moves out or dies, the remaining person (regardless if they have a social care need) will assume full responsibility for the Wellbeing Charge. 24.5 The charge is £15 for most extra care housing schemes (exceptions apply). For full details, see Wellbeing Charge practice guidance on KNet.

Charging policy for home care and other non-residential services 21

Appendix 1: Backdated charges (reference section 20) 1. Introduction

1.1 The legal framework covering charging was replaced by Section 14 of the Care Act 2014, the Care and Support (Charging and Assessment of Resources) Regulations 2014 and the accompanying Statutory Guidance. 1.2 Neither the Act, Regulations nor Guidance stated anything explicit about backdating of charges. In the absence of anything concrete to go on, local authorities have been attempting to get clarity from the Department of Health about whether they can backdate charges 1.3 The DoH has now provided clarity over the backdating issue in that local authorities have the power to levy charges from the date when it starts to incur costs to meet a person’s care and support needs. 1.4 KCC has taken the decision, effective from 01/12/15, that home care and other non-residential services charges will be backdated from the date services began and not the start of the financial assessment. 1.5 This means that backdated charges apply to both residential and non-residential care, provided certain safeguards are in place. Financial referral and assessment should be carried out as soon as possible and people should be given reasonable length of time to pay backdated charges if necessary.

2. Practice guidance

To this end, the steps below must be followed in order to avoid service users being faced with large and unexpected bills and, if required, having the opportunity to ask to pay off the arrears more slowly.

2.1 The case/care manager will prepare the Care and Support Plan with the service user and will give the service user:

“Your Guide: To charging for care provided in your own home and support in the community” (the blue book), explaining the financial assessment process is to work out how much they can afford to pay for their care and support. Kent.gov.uk link here-charges for care and support

and

“Domiciliary Charge Advice letter” (located on KNet templates), reading through the content of the letter with the service user, providing the opportunity to seek clarification click here.

2.2 The case/care manager will explain to the service user who to contact if they are facing serious financial hardship to discuss what options are available.

2.3 The case/care manager must update SWIFT as soon as possible (finance are not able to progress a financial assessment until the information is on the system unless a Direct Payment has been requested). If there is an unavoidable delay to update SWIFT with the provision (e.g. a delay contracting with a provider), charges will not be backdated for more than 12 weeks (unless exceptional circumstances). Delay in putting forward financial assessments will be monitored.

Charging policy for home care and other non-residential services 22

2.4 A referral to be sent to finance within 3-5 days the service has commenced. It is important that a referral for a financial assessment is carried out as soon as possible, in order to avoid the service user being faced with large unexpected bills if they were assessed as able to pay for their care and support (Finance referral link here) 2.5 On receipt of the finance referral, a Finance Assessment Officer will arrange to complete the financial assessment with the service user/representative with 10 days of receipt of the referral. 2.6 Following the financial assessment, the service user is sent a letter from finance outlining their charge, when it will run from and that if the arrears cannot be paid off in one go, they should contact Debt Recovery (03000 411032 or [email protected] to arrange to pay this off over a longer period. 2.7 The Finance Assessment Officer will notify the case/care manager of the charge and by secure email to the case/care manager, send a copy of the financial assessment and the letter. The case/care manager will record the charge amount (per week) on the Care and Support plan under “My Contribution”, arrange for the service user to receive and sign the final plan and, file the financial documentation in the case file. 2.8 The first Kent care invoice will be sent out which will include charges back to the date services began. If the service user is set up on Direct Debit, there will be a gap of at least 10 days before any money is deducted from their account. 2.9 The service user/representative may contact Debt Recovery about their Kent care invoice to discuss paying the backdated amount over a longer period. This will be agreed on case-by-case bases. In general, charges should not be backdated for more than 12 weeks BUT this can, in exceptional circumstances, be extended, such as where a person/family deliberately does not cooperate.

Charging policy for home care and other non-residential services 23

Appendix 2:

1. Short Term Beds

1.1 Short term bed when not used as assessment bed

Where no appropriate package of care is available from a Home Care provider and a Short Term Bed is used. The case/care manager must:

Apply the normal process for application of a residential placement

Be clear, in writing, with the person/ their carer that this arrangement is temporary and that if the Care and Support Plan is updated the STB (charging and other) arrangements may be changed. This can be clarified within the Care and Support Plan as the way the individual’s outcomes are being met.

Ensure a financial assessment is completed.

2. Enablement (OPPD KEaH)- pre and post service 2.1 Use of chargeable homecare where KEaH is not available

In some circumstances a lack of capacity in KEaH means that a person who is in need of an Enablement service is not able to do so. In these circumstances a person may be provided with a chargeable service whilst they wait for the Enablement provision to start.

The chargeable service should be entered on Swift.

A referral for financial assessment should be sent.

The charging policy allows for an exceptional disregard to be made where the Case Manager thinks it is reasonable for the charge to be waived. The “Disregard-exceptions” form on KNet should be completed and submitted to the Service Manager or Assistant Director. The individual should be advised in writing that the disregard is subject to review, this should be noted in the Care and Support Plan.

Where a disregard is applied this should be reviewed weekly as it may become apparent that the service is becoming more of a permanent arrangement.

Where an individual is in receipt of an existing KCC service and no KEaH provision is available the person will continue with the chargeable service and will continue to pay their contribution until Enablement becomes available.

2.2 Use of KEaH (post Enablement) where a non-KCC provider is not available

Therefore an in house chargeable service that is not enablement

A person who has been in receipt of Enablement from KEaH, has ongoing eligible needs as determined at final review and so appropriate for moving to a chargeable service, is subject to a financial assessment and to paying a contribution to the cost of their care from the date the chargeable service starts.

A person who continues to receive a service from KEaH following the end of their period of Enablement because there is no alternative ongoing service is subject to the Charging for non-residential care policy as they would be if they moved to another provider. The unit costs (service cost) will be calculated using the cost setting guidance.

Charging policy for home care and other non-residential services 24

1. The person is referred to KEaH for a period of Enablement.

2. The KEaH Supervisor reviews the person and agrees the period of Enablement is complete, and the person has on-going care needs.

3. The Supervisor advises the person their period of Enablement is complete, determines their eligible needs applying the eligibility criteria and discusses ongoing care, explaining this is subject to the KCC charging policy. The Supervisor gives the person the “Your Guide: To charging for care provided in your own home and support in the community” (the blue book) and the “Domiciliary Charging letter (for KEaH only)” (located on KNet templates), reading through the content of the letter with the person, providing the opportunity to seek clarification.

4. The Supervisor will refer to Purchasing (ACT) to commission appropriate package of care (email sent).

5. Purchasing confirm to KEaH Locality Organiser or Supervisor that a care package is not available due to lack of capacity and the person will need to continue with the in-house provider (KEaH) until a suitable package can be sourced.

6. The KEaH supervisor informs the person that there is no alternative provider available and that they will continue to receive care and support from the KCC in-house provider (KEaH) until another provider becomes available. They advise the person that this will be a chargeable service and confirm the date they will transfer from the Enablement service to a chargeable service. Charging will commence five days from the date the person is assessed as completing their Enablement provision and referred to Purchasing.

7. Purchasing/ACT allocate the person to a Case Manager and refer the person for a financial assessment.

8. Five days after the person starts to use the in-house provider (KEaH) as a chargeable service (see point 6 above), the Purchasing team will update Swift to change provision from non-chargeable to chargeable (so that an invoice can be raised if the person has a contribution).

9. KEaH continue to provide a chargeable service until a suitable care provider can be sourced or the person no longer requires a service, whichever is sooner. ACT will ensure the person is reviewed to source a suitable provider as soon as possible.

The same process detailed above applies for self-funders who ask KCC to meet their needs and/or arrange a package of care for them.