social security current reform proposals: how they would affect people with disabilities consortium...

TRANSCRIPT

Social Security

Current Reform Proposals: How They Would Affect People With Disabilities

Consortium for Citizens with Disabilities June 1, 2011

Social Security

Background on the Social Security Programs

June 2011 Consortium for Citizens with Disabilities 2

Social Security 54.2 million people receive

Social Security benefits from the retirement, disability, and survivors programs

More than one-third of all monthly checks go to non-retired individuals

June 2011 Consortium for Citizens with Disabilities 3

Social Security Insurance Retirement – insures against poverty

after worker retires Includes retirees with disabilities Spouses, including those with disabilities Disabled Adult Children

Example of people with increased reliance on Social Security benefits Parents of children with disabilities with

reduced earnings and savings due to care giving

June 2011Consortium for Citizens with

Disabilities 4

Social Security Insurance (continued) Survivors – provides benefits to dependents

after an insured individual (worker, disability insurance or retirement insurance beneficiary) dies Minor children and spouses of

deceased workers and retirees Disabled widow(ers) Disabled adult children

June 2011 Consortium for Citizens with Disabilities

5

Social Security Insurance (continued)

Disability – insures against loss of ability to work due to disability

Disabled workers, their spouses and children, including disabled adult children

Essential protection Millions of families face disability Adults with serious disabilities have very low

employment rate Poverty rates twice as high for workers with

disabilities as other groups who receive Social Security

Equals half or more of TOTAL family income for about half of disabled worker beneficiaries

June 2011Consortium for Citizens with

Disabilities 6

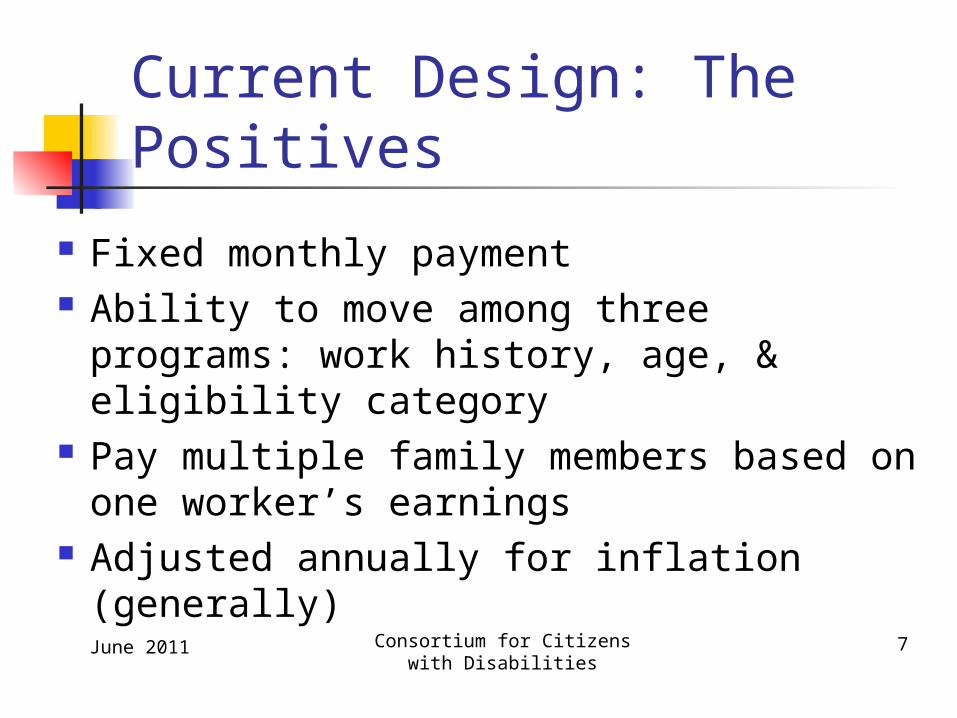

Current Design: The Positives

Fixed monthly payment Ability to move among three programs:

work history, age, & eligibility category Pay multiple family members based on

one worker’s earnings Adjusted annually for inflation

(generally) June 2011 Consortium for Citizens with

Disabilities7

Social Security

Background on Financing and Long-Term

Solvency Consortium for Citizens with

DisabilitiesJune 2011 8

Social Security & the Deficit

National groups examining ways to reduce deficit, including Social Security changes

Social Security did NOT cause the deficit Cutting benefits will NOT solve budget

crisis Cutting benefits will deepen financial

crisis for many people with disabilities June 2011

Consortium for Citizens with Disabilities 9

Social Security & the Deficit

Social Security did NOT cause the deficit: It is self-funded By law, it can only spend money

dedicated to the program No borrowing authority

June 2011 Consortium for Citizens with Disabilities 10

June 2011 Consortium for Citizens with Disabilities 11

Social Security’s Finances It is NOT a crisis Social Security does face a long-term financing shortfall

Only modest changes are needed to address shortfall

Current & Future Surplus

Surplus = invested assets or Trust Fund reserves

$2.6 trillion by end 2010 Will continue to grow 2011-2022 Projected to reach $3.7 trillion by

2022 June 2011

Consortium for Citizens with Disabilities 12

Projected Shortfall Over 75 Years

Less than 1 percent of Gross Domestic Product (GDP)

Another measure = 2.22 percent of taxable payroll

Previous Trustees’ forecasts = similar projection

June 2011Consortium for Citizens with

Disabilities 13

June 2011Consortium for Citizens with

Disabilities 14

Future Projections

Pay 100% of scheduled benefits 2011 Trustees Report: until 2036

Pay reduced benefits (if no action taken) 2011 Trustees Report: 77% of

scheduled benefits starting 2037

Social Security

Background: How Social Security Benefits

Are Calculated

Consortium for Citizens with DisabilitiesJune 2011 15

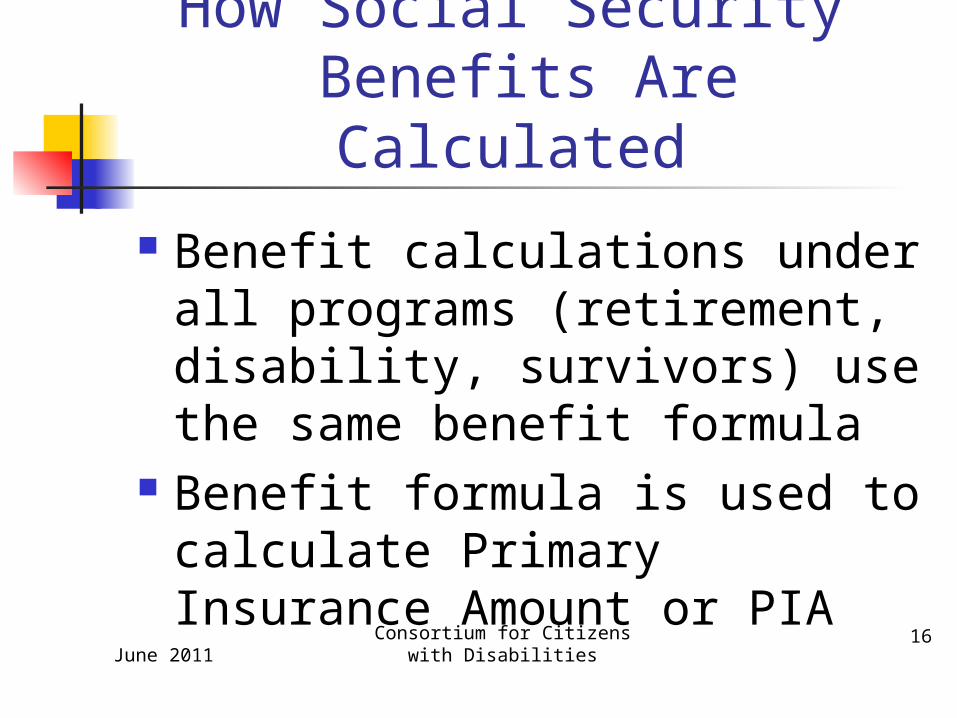

How Social Security Benefits Are Calculated

Benefit calculations under all programs (retirement, disability, survivors) use the same benefit formula

Benefit formula is used to calculate Primary Insurance Amount or PIA

June 2011Consortium for Citizens with

Disabilities16

How Social Security Benefits Are Calculated (continued) Calculated based on the

earnings of the worker Worker must have enough

credits, or “quarters of coverage,” to be eligible

Must have paid in 40 quarters or 10 years to be fully insured

June 2011Consortium for Citizens with

Disabilities17

How Social Security Benefits Are Calculated (continued) Younger workers qualify under

the disability or survivor programs with fewer credits

Exact number of quarters required is dependent on the age of the worker at the time of disability or death

June 2011Consortium for Citizens with

Disabilities18

How Social Security Benefits Are Calculated (continued) Social Security benefit amount is

based on the worker’s average earnings over their years of work

Retirement Benefit: Based on 35 years “Zero years” included if less than 35

years Lowest years “dropped” out (if more

than 35)June 2011

Consortium for Citizens with Disabilities

19

How Social Security Benefits Are Calculated (continued)

Disability and survivors benefits: Number of years based on age of worker at onset of disability or death Use “elapsed” years

The number of full calendar years since the person turned 21

If age 47 or over – get 5 “dropped” years Under age 47 – get 4 or less “dropped”

yearsJune 2011

Consortium for Citizens with Disabilities

20

How Social Security Benefits Are Calculated (continued) Once earnings determined, SSA

“indexes” the person’s earnings Done to update earnings to current

levels Reflects earnings increases in average

wage levels for each year Calculation results in Average

Indexed Monthly Earnings or AIME June 2011

Consortium for Citizens with Disabilities

21

How Social Security Benefits Are Calculated (continued)

Plug AIME into benefit formula Formula Replaces Percentage of AIME – Current

Formula (2011) 0-$749 = Replace 90% $749-$4517 = Replace 32% $4517 and up to taxable max = Replace 15%

Dollar amounts at which replacement percentage changes ($749, $4517) are known as “bend points”

June 2011 Consortium for Citizens with Disabilities

22

How Social Security Benefits Are Calculated (continued)

Bend points change every year Replacement percentages in

formula set by statute and do not change unless Congress changes them

June 2011 Consortium for Citizens with Disabilities

23

How Social Security Benefits Are Calculated (continued)

This calculation determines Primary Insurance Amount (PIA):

Retirement Program Get full PIA as monthly benefit if retire at your Full

Retirement Age (FRA) – also sometimes referred to as Normal Retirement Age (NRA)

Benefit is reduced if retire before then – amount of reduction based on how long before reach full retirement age begin to collect benefits

Youngest age at which benefits can be collected is known as Early Retirement Age or ERA June 2011 Consortium for Citizens with

Disabilities24

How Social Security Benefits Are Calculated (continued) Disability and survivors benefits are

calculated as if someone retires at FRA Based on the full PIA Not reduced regardless of age at which

disability onset or death occurs PIA is also plugged into another

formula to determine “family maximum” to determine benefits of family members

June 2011 Consortium for Citizens with Disabilities

25

Benefits Are Modest Under Current Formula

June 2011Consortium for Citizens with

Disabilities 26

Benefits Are Large Percent of Income for Lower Income Retirees

June 2011Consortium for Citizens with

Disabilities 27

Proposals and Options for Achieving Long-Term

Solvency of the Social Security Programs

June 2011Consortium for Citizens with

Disabilities 28

June 2011Consortium for Citizens with

Disabilities 29

Possible Options: Solvency

Two approaches, but could combine options from each:

Cut benefits Increase revenue

What Is Needed to Achieve Long-Term Solvency

Often looked at as a percentage of payroll

As stated earlier: Need revenue increases or benefit cuts = to 2.22% of taxable payroll to make up shortage

Will explain how much of the shortfall each option will solve (as available)

June 2011 Consortium for Citizens with Disabilities 30

Major Reform Proposals to Date

National Commission on Fiscal Responsibility and Reform – known as Bowles/Simpson Recommendations of Co-Chairs only Commission Member Representative Jan

Schakowsky (D-IL) also made recommendations

Bipartisan Policy Center Debt Reduction Taskforce – known as Rivlin/Domenici

June 2011 Consortium for Citizens with Disabilities 31

Specific Proposals: Benefit Cuts

June 2011 Consortium for Citizens with Disabilities

32

Proposal 1: Change the Benefit Formula

Achieve program savings by changing the replacement percentages in the benefit formula

Can be done: Progressively: Change the replacement

percentages for top earners only (i.e., decrease the percentage)

Regressively: Change the replacement percentages for all earners

June 2011 Consortium for Citizens with Disabilities

33

Proposal Specifics: Bowles/Simpson

Bowles/Simpson (new formula) $0-$9,000 = 90% replacement $9,000 - $38,000 = 30% $38,000 - $64,000 = 10% $64,000 - max = 5%

Based on annual earnings rather than AIME Results in benefit cuts for everyone with

average annual earnings over $9,000 Restores 0.86% of taxable payroll or 39% of

shortfall

June 2011Consortium for Citizens with

Disabilities 34

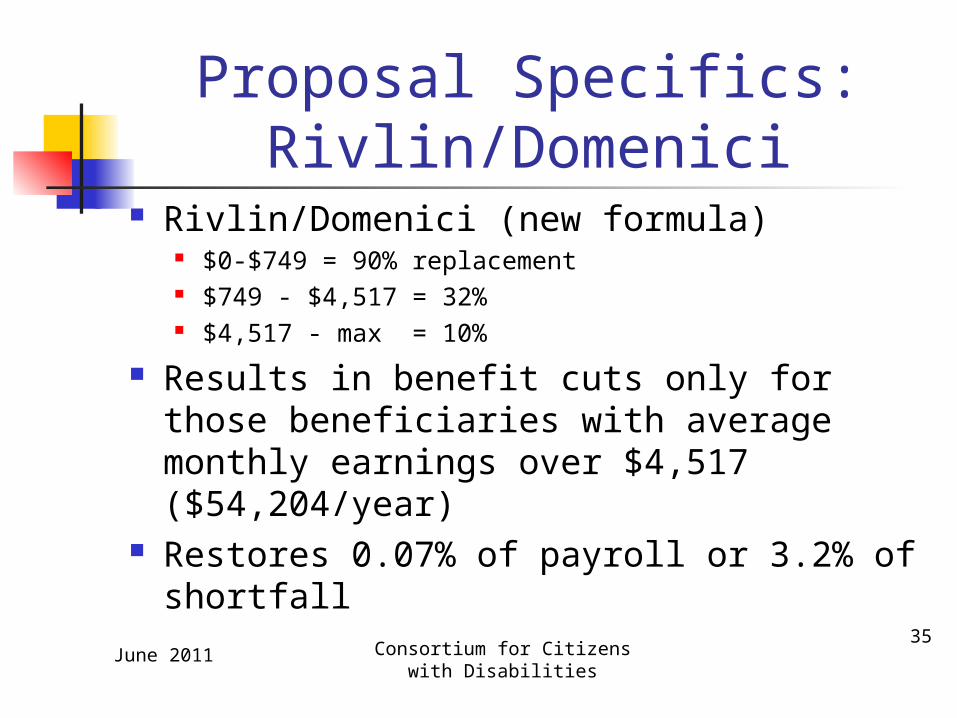

Proposal Specifics: Rivlin/Domenici

Rivlin/Domenici (new formula) $0-$749 = 90% replacement $749 - $4,517 = 32% $4,517 - max = 10%

Results in benefit cuts only for those beneficiaries with average monthly earnings over $4,517 ($54,204/year)

Restores 0.07% of payroll or 3.2% of shortfall

June 2011 Consortium for Citizens with Disabilities

35

Impact on People with Disabilities

Any change to the benefit formula that decreases the replacement percentages will result in benefit cuts to people with disabilities in all benefit programs – retirement, disability, survivors

June 2011 Consortium for Citizens with Disabilities

36

Other Possible Formula Changes Resulting in Benefit

Cuts Increase the number of years

used in calculating the AIME Change from wage indexing to

price indexing when calculating the AIME

Not included in proposals discussed today

June 2011 Consortium for Citizens with Disabilities

37

Proposal 2: Change the Retirement Age Current FRA (full retirement age) –

66 for current retirees – up from 65 Under current law, gradually being

raised to 67 for all people born after 1960

Current ERA (early retirement age) 62 for all retirees Not set to increase under current law

June 2011 Consortium for Citizens with Disabilities

38

Proposal Specifics Bowles/Simpson

Raise NRA to 68 by 2050 and 69 by 2075 Raise ERA to 63 by 2075 Restores 0.34% of taxable payroll or 15.3% of shortfall

Rivlin/Domenici Does not include an increase in the retirement age per se Indexes new benefits for longevity instead Replacement rate will be 99.7% of benefits the year before Restores 0.48% of taxable payroll or 21.6% of shortfall

June 2011 Consortium for Citizens with Disabilities

39

Raising the Retirement Age

Is a Benefit Cut

June 2011 Consortium for Citizens with Disabilities

40

Impact on People with Disabilities

Benefit cut for workers with disabilities who work until they reach retirement age or who retire early

Benefit cut for people receiving family benefits from a retired worker

June 2011 Consortium for Citizens with Disabilities

41

Impact on People with Disabilities (continued)

No direct effect on people receiving benefits under disability program but: Disability applications already increasing due to

current law increase in retirement age Raising the ERA:

Leaves people with disabilities in their early 60s, but who do not meet the stringent requirements for Disability Insurance (DI) program, without Social Security insurance coverage

Will cause more workers to apply for DI benefits Will increase the administrative workload, processing time for

disability applications, and delay in benefit awards

June 2011 Consortium for Citizens with Disabilities

42

Proposal 3: Change the Cost of Living Adjustment Formula Current law provides for an annual Cost

of Living Adjustment or COLA for benefits under all programs

Helps protect the value of benefits against inflation

Current COLA is based on the change in the CPI-W (Consumer Price Index for Urban Wage Earners and Clerical Worker)

There was no COLA for 2010 or 2011

June 2011 Consortium for Citizens with Disabilities

43

Proposal 3: Cost of Living Adjustment Formula (cont)

Reform proponents argue that the current measure overstates inflation

Propose to change to another measure known as the “chained CPI” Generally finds a smaller increase in the cost of

living year to year Bases its rate on “substitution effect”

When prices on a particular item go up, people will substitute other less expensive items in their place (e.g. if steak prices rise, a person will buy hamburger instead)

June 2011 Consortium for Citizens with Disabilities

44

Proposal Specifics Bowles/Simpson

Change to “Chained CPI” Restores 0.50% taxable payroll or

22% of shortfall Rivlin/Domenici

Change to “Chained CPI” Restores 0.49% taxable payroll or

22% of shortfall

June 2011 Consortium for Citizens with Disabilities

45

Why the Chained CPI Is Not More Accurate

More applicable to higher income earners Can’t substitute hamburger for steak if already

only eating hamburger or no meat Not applicable to many seniors or people

with disabilities Majority of expenses are to meet basic needs

Underestimates expenses like medical care on which people with disabilities and seniors spend a larger percentage of their income

June 2011 Consortium for Citizens with Disabilities

46

Impact on People with Disabilities

Change in COLA will result in a benefit cut for all people receiving benefits under all Social Security programs

Effect is cumulative The longer a person receives benefits the greater the

benefit cut will be People receiving disability benefits tend to receive

benefits longer than people who receive benefits under other programs

Value of benefits no longer adequately protected from inflation

June 2011 Consortium for Citizens with Disabilities

47

Proposals to Address Long-Term Solvency:

Revenue Enhancements

June 2011Consortium for Citizens with

Disabilities48

Current Revenue Design Almost every worker pays in – some state

and local workers do not Current FICA Tax Rate: 12.4% of earnings

6.2% paid by employee 6.2% paid by employer

Earnings taxed are capped at $106,800 – adjusted annually

Only earnings in the form of wages are taxed – dividends and capital gains are not

June 2011 Consortium for Citizens with Disabilities

49

Interest Revenue Two sources of revenue to the

Social Security Trust Funds: FICA Taxes Interest earned on money in Trust

Funds Trust Funds invested in U.S.

Treasury bonds Steady return with no risk

May 2011Consortium for Citizens with

Disabilities 50

Proposal 1: Raise or eliminate the cap on earnings Historically, 90% of total earnings

have been taxed Currently, only about 83% of

earnings taxed Lower percentage due in large part to

earnings cap amount increases lagging behind growth in income of high earners

June 2011 Consortium for Citizens with Disabilities 51

Proposal Specifics Phase in increase in cap to capture

90% of wages Bowles/Simpson – by 2050

Restores 0.67% of payroll or 30.2% of shortfall Rivlin/Domenici – over 38 years

Restores 0.60% of payroll or 27% of shortfall

June 2011 Consortium for Citizens with Disabilities 52

Proposal Specifics (continued) Eliminate cap on employers and

keep cap for employees the same Rep. Schakowsky – 74% of shortfall

eliminated based on 2010 Trustees Report (not provided as percent of payroll)

June 2011 Consortium for Citizens with Disabilities

53

Proposal 2: Increase FICA Rates

Current Rate: 12.4% (6.2% employee; 6.2% employer)

Immediately increase by 1.1% on each – 7.3% each Restores 2.09% of payroll or 94.1% of shortfall

Medium earner with $43,451 annual earnings – increase of $478 a year or $9.19/week

Not included in any current proposalJune 2011 Consortium for Citizens with

Disabilities 54

Proposal 2: Increase FICA Rates (continued)

Gradually increase by 1% over 20 years starting in 2015– 7.2% each by 2035 Restores 1.39% of taxable payroll or 63% of

shortfall Average earner in 2015 with $53,085

annual earnings – increase of $26.50 a year or $.50/week

Not included in any current proposalJune 2011 Consortium for Citizens with

Disabilities 55

Proposal 3: Require Uncovered Workers to Contribute Almost all U.S. workers pay into the

Social Security system Currently 8 states have more than half

their state and local workers not covered by the Social Security system and who don’t pay FICA contributions

Are covered by public pensions instead

June 2011 Consortium for Citizens with Disabilities 56

Proposal Specifics Have all newly hired state and local

workers be covered and pay in Bowles/Simpson – by 2020

Restores 0.16% of payroll or 7.2% of shortfall Rivlin/Domenici – by 2020

Restores 0.16% of payroll or 7.2% of shortfall Note: in 75th year would be -.12% of payroll when

state and local workers begin to collect benefits

June 2011 Consortium for Citizens with Disabilities 57

Proposal 4: Eliminate tax free status of cafeteria

plans People currently pay FICA taxes on

401(k) contributions but not on flexible spending accounts Health Savings Account Dependent Care Savings Account Transit Savings Accounts

June 2011 Consortium for Citizens with Disabilities 58

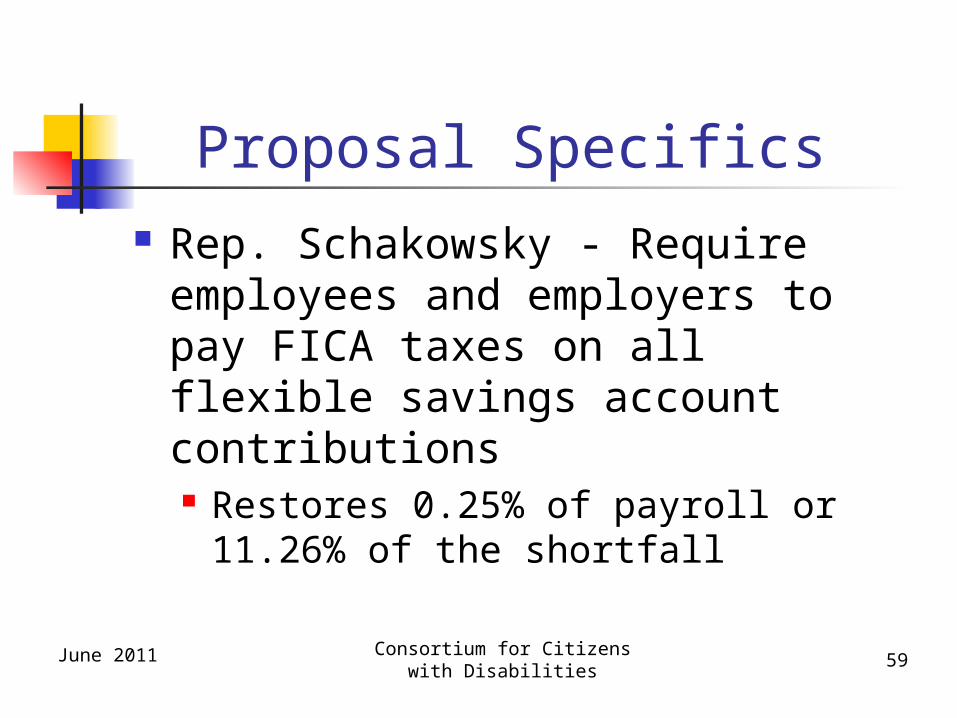

Proposal Specifics Rep. Schakowsky - Require

employees and employers to pay FICA taxes on all flexible savings account contributions Restores 0.25% of payroll or 11.26%

of the shortfall

June 2011 Consortium for Citizens with Disabilities 59

Revenue Changes: Impact on People with Disabilities Workers with disabilities would have

less take home pay if: FICA rates for employees increased They have earnings above current

taxable maximums and the cap is raised No direct impact on people with

disabilities receiving benefits under any of the Social Security programs

June 2011 Consortium for Citizens with Disabilities

60

June 2011Consortium for Citizens with

Disabilities 61

Principles for Achieving Long-Term Solvency of

the Social Security Programs

General Principles Social Security is NOT in crisis Social Security changes should not be included in

deficit reduction legislation The Social Security programs should not be

included in proposals that cap overall federal spending

Modest premium contribution adjustments, rather than benefit cuts, should be used to address long-term solvency of the Social Security programs

June 2011 Consortium for Citizens with Disabilities

62

June 2011Consortium for Citizens with

Disabilities 63

Principles (continued)

Do not change basic design based on payroll taxes

Preserve as social insurance for disability, survivors & retirement

Guarantee monthly benefits adjusted for inflation

Preserve current & future benefits Restore program’s long term funding

For More Information

To find fact sheets regarding Social Security and disability, links to helpful resources, or to access a recording of this webinar, please visit

www.disabilityandsocialsecurity.org

June 2011Consortium for Citizens with

Disabilities 64

Webinar Sponsors

This webinar has been sponsored by the Consortium for Citizens with Disabilities. Funding was provided through a grant administered by the National Academy of Social Insurance and provided by the Ford Foundation.

June 2011 Consortium for Citizens with Disabilities 65