solar water heating techscope market readiness … · techscope market readiness assessment:...

TRANSCRIPT

SOLAR WATER HEATING TECHSCOPE MARKET READINESS ASSESSMENT: MAURITIUS & SEYCHELLES

January 2015

Page | 1

ACKNOWLEDGEMENTS Prepared by Meister Consultants Group for Joya Bhandari of Green Environment & Energy

Consultants and Tony Imaduwa of Seychelles Energy Commission with support from IRENA

Renewable Energy Policy Advice Network and the Clean Energy Solutions Center

SUPERVISION AND COORDINATION Victoria Healey, Clean Energy Solutions Center

Yao Zhao, International Renewable Energy Agency

LEAD AUTHOR Jeremy Koo

CONTRIBUTING AUTHORS Wilson Rickerson and Emily Chessin

CONTRIBUTORS Denise Bonne, D.B. Supplies

Michèle Martin, Sustainability for Seychelles

Guilly Moustache, Seychelles Energy Commission

Harry Savy, Sun Heat Supplies

Page | 2

Table of Contents INTRODUCTION .......................................................................................................................................................................... 5

MAURITIUS ................................................................................................................................................................................ 7

PARAMETER I: SOLAR WATER HEATING SUPPORT FRAMEWORK ................................................................. 8

1.1.1 Solar Water Heating Heating Targets ........................................................................................................ 9

1.1.2 Financial Incentives for System Installation............................................................................................. 9

1.1.3 SWH Loan Programs ...................................................................................................................................... 10

1.1.4 Building Mandates ........................................................................................................................................... 10

1.1.5 Outreach Campaigns ...................................................................................................................................... 11

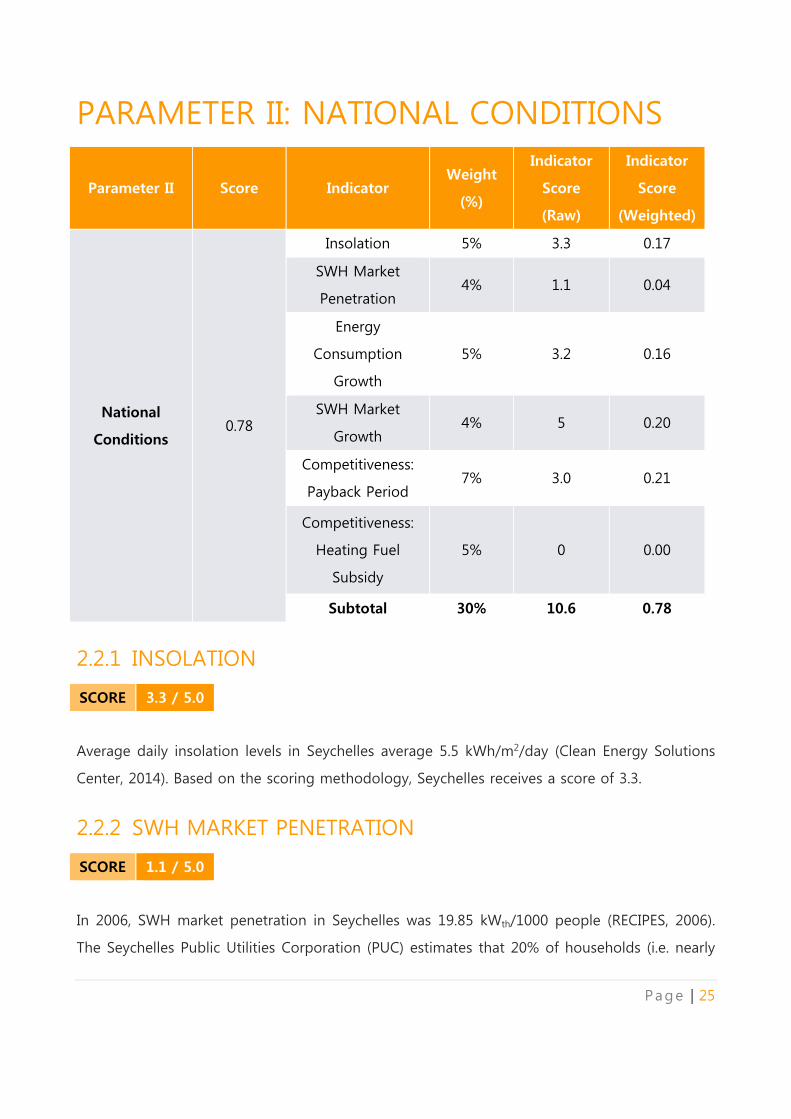

PARAMETER II: NATIONAL CONDITIONS ................................................................................................................ 12

1.2.1 Insolation ............................................................................................................................................................. 12

1.2.2 SWH Market {enetration ............................................................................................................................... 13

1.2.3 Residential Energy Consumption Growth ............................................................................................. 14

1.2.4 SWH Market Growth ...................................................................................................................................... 14

1.2.5 Payback Period .................................................................................................................................................. 15

1.2.6 Competitiveness: Heating Fuel Subsidy ................................................................................................. 16

PARAMETER III: FINANCING .......................................................................................................................................... 17

1.3.1 Country Credit Rating .................................................................................................................................... 17

1.3.2 Access to Finance ............................................................................................................................................. 17

PARAMETER IV: BUSINESS CLIMATE .......................................................................................................................... 18

1.4.1 Business Climate ............................................................................................................................................... 18

1.4.2 Domestic Manufacturing .............................................................................................................................. 19

1.4.3 Product Certification ....................................................................................................................................... 19

1.4.4 Installer Certification ....................................................................................................................................... 20

1.4.5 Industry Association ........................................................................................................................................ 20

SEYCHELLES ............................................................................................................................................................................. 21

PARAMETER I: SOLAR WATER HEATING SUPPORT FRAMEWORK .............................................................. 22

2.1.1 Solar Water Heating Targets ...................................................................................................................... 22

2.1.2 Financial Incentives for System Installation.......................................................................................... 23

2.1.3 SWH Loan Programs ...................................................................................................................................... 23

2.1.4 Building Mandates ........................................................................................................................................... 24

2.1.5 Outreach Campaigns ...................................................................................................................................... 24

Page | 3

PARAMETER II: NATIONAL CONDITIONS ................................................................................................................ 25

2.2.1 Insolation ............................................................................................................................................................. 25

2.2.2 SWH Market Penetration .............................................................................................................................. 25

2.2.3 Residential Energy Consumption Growth ............................................................................................. 26

2.2.4 SWH Market Growth ...................................................................................................................................... 26

2.2.5 Competitiveness: Payback Period ............................................................................................................. 27

2.2.6 Competitiveness: Heating Fuel Subsidy ................................................................................................. 28

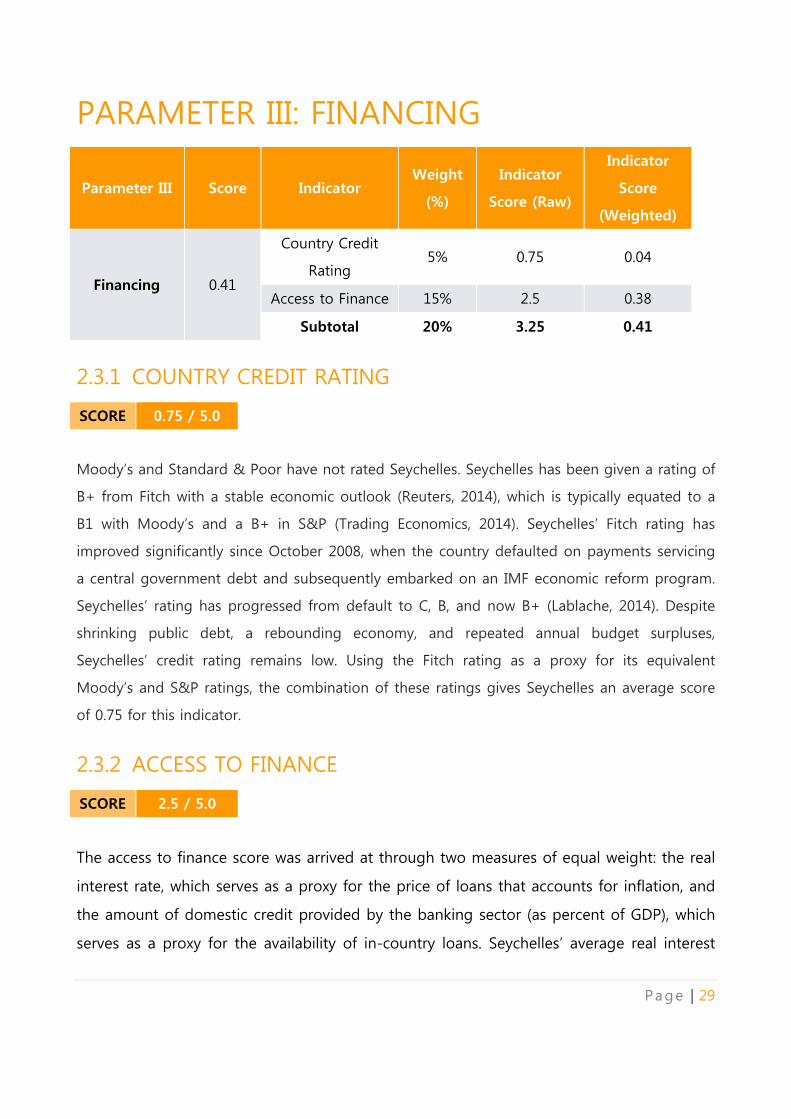

PARAMETER III: FINANCING .......................................................................................................................................... 29

2.3.1 Country Credit Rating .................................................................................................................................... 29

2.3.2 Access to Finance ............................................................................................................................................. 29

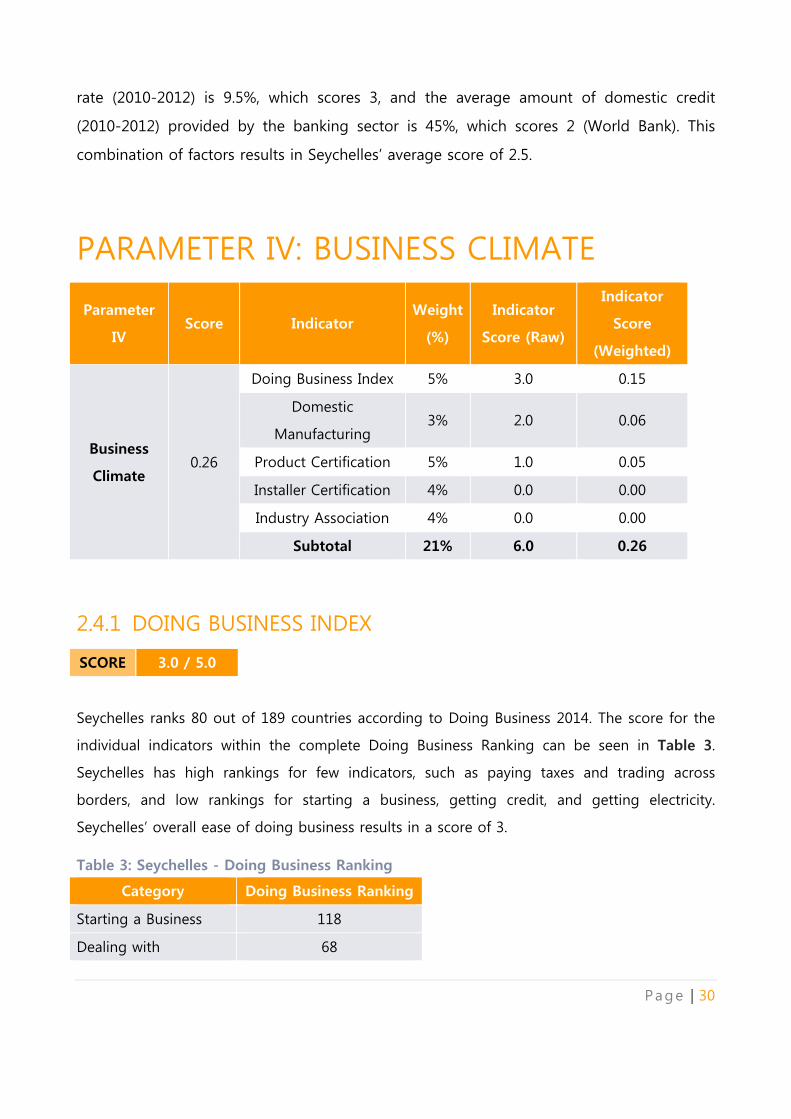

PARAMETER IV: BUSINESS CLIMATE .......................................................................................................................... 30

2.4.1 Doing Business Index ..................................................................................................................................... 30

2.4.2 Domestic Manufacturing .............................................................................................................................. 31

2.4.3 Product Certification ....................................................................................................................................... 31

2.4.4 Installer Certification ....................................................................................................................................... 32

2.4.5 Industry Association ........................................................................................................................................ 32

APPENDIX I: Summary of Country Techscope Scores ............................................................................................ 33

Mauritius ... ............................................................................................................................................................................. 34

Seychelles . ............................................................................................................................................................................. 35

APPENDIX II: SWH Financing in Mauritius .................................................................................................................. 36

Introduction........................................................................................................................................................................... 37

Status of Mauritius SWH Scheme ............................................................................................................................... 37

Alternative financing schemes ...................................................................................................................................... 38

Background on PROSOL ............................................................................................................................................. 38

A PROSOL for Mauritius? ........................................................................................................................................... 39

BIBLIOGRAPHY ......................................................................................................................................................................... 43

Page | 4

INTRODUCTION Small island development states (SIDS) face significant energy challenges. Costly fossil fuels

imports can burden national budgets and inhibit economic development. Indigenous

renewable energy resources can reduce import dependence, while creating important local

business and employment opportunities. Solar water heating (SWH) systems can be highly cost

effective in island settings with high fuel prices, and countries such as Barbados and Cyprus

have had well-documented success with SWH market development. Beyond Barbados and

Cyprus, however, little is known about the current status and lessons learned from the SWH

markets in most SIDS. Initiatives to increase SWH uptake in islands will benefit from efforts to

share information and best practices among SIDS in a standardized manner.

The International Renewable Energy Agency (IRENA) has launched the Global Renewable

Energy Islands Network (GREIN) in order to support islands increase their renewable energy

supply. In 2014, representatives from Mauritius and the Seychelles approached IRENA within

the context of GREIN to conduct an analysis of their SWH markets as a foundation for future

policy development. In response, IRENA’s Renewable Energy Policy Advice Network (REPAN)

and the Clean Energy Solutions Center (CESC) provided resources to conduct a SWH market

study for both countries using the Solar Water Heating TechScope Market Readiness

Assessment methodology (“the TechScope”).

The TechScope was developed under the Global Solar Water Heating (GSWH) Market

Transformation and Strengthening Initiative, which is a joint undertaking by the United Nations

Environment Programme (UNEP) and the United Nations Development Program (UNDP) and is

funded by the Global Environmental Facility (GEF). The goal of the initiative is to develop,

strengthen, and accelerate the growth of the SWH sector. In pursuit of this goal, the UNEP

funded the development of the TechScope as a replicable, high-level, and publicly available

methodology to evaluate the SWH market in various countries. The TechScope uses four

parameters composed of 18 indicators, developed in consultation with a network of

international SWH and renewable energy experts, to benchmark and evaluate SWH markets in

different countries.

The four parameters analyzed in the TechScope methodology are:

Page | 5

I SWH Support Framework

II National Conditions

III Financing

IV Business Climate

The indicators and parameters are weighted to construct a “snapshot” of a given country’s

SWH market, reflected in an overall score of 0 to 5. The TechScope assigns the following

broad labels for scoring:

Score of 0-2: SWH enabling environment is “emerging” and could likely benefit from

additional support to accelerate SWH market growth.

Score of 2-3: SWH enabling environment is “good” with the SWH market positioned

for increased growth.

Score of 3-4: SWH enabling environments are considered to be “strong” and are likely

ready to attract investment.

Score of 4-5: SWH conditions are “very strong” – policy, market, financial, and business

conditions are aligned to support SWH and market growth is likely to be rapid.

This report summarizes the results of the TechScope analysis for Mauritius and the Seychelles.

In addition to the Market Readiness Assessment, the SWH incentive schemes in Mauritius are

analyzed and compared to the Tunisian PROSOL SWH scheme. This overview is included in

Appendix II.

The full Solar Water Heating TechScope Market Readiness Assessment can be accessed online

here: http://www.in.undp.org/content/dam/india/docs/EnE/solar-water-heating-techscope-

market-readiness-assessment.pdf.

Page | 6

Overall Score 3.42 / 5.0

MAURITIUS

Summary: The SWH market in Mauritius has

experienced average annual growth of 40%

over the past five years, from 16.3 MWth in

2008 to 109.8 MWth in 2013. Mauritius’s

overall TechScope score is 3.42, which will be

discussed in detail in the sections below in

order to provide greater insight into the

SWH TechScope Market Readiness

Assessment for Mauritius.

General Information (2013)

Population 1,296,303

GDP US$11,938,403,909

Total installed solar

thermal (flat plate and

evacuated tube

collectors)

109.8 MWth

Parameter Score

Solar Water Heating Support Framework 1.20 / 1.45

National conditions 0.94 / 1.50

Financing 0.63 / 1.00

Business Climate 0.65 / 1.05

P age | 7

PARAMETER I: SOLAR WATER HEATING

SUPPORT FRAMEWORK

Parameter I Score Indicator Weight

(%)

Indicator

Score (Raw)

Indicator

Score

(Weighted)

SWH

Support

Framework

1.20

SWH Targets 5% 0.0 0.00

Financial Incentives

for System

Installation

8% 5.0 0.40

SWH Loans

Programs 7% 5.0 0.35

Building Mandates 5% 5.0 0.25

Outreach

Campaigns 4% 5.0 0.20

Subtotal 29% 20.0 1.20

In April 2007, the Republic of Mauritius adopted the “Outline of the Energy Policy 2007-2025 –

Towards a Coherent Energy Policy for the Development,” which provided for a comprehensive

study of the Mauritian energy sector, jointly funded by the European Commission and United

Nations Development Programme (UNDP)/United Nations Environment Programme (UNEP).

The final report was adopted by the government in December 2008 and was developed into

the “Republic of Mauritius Long-Term Energy Strategy 2009-2025,” released on October 20,

2009. Concurrently, in July 2008, the Republic of Mauritius established the Maurice Ile Durable

(MID) Fund to finance sustainable development on the island and transform Mauritius into a

model for sustainable development for Small Island Developing States (SIDS).

With the establishment of the MID Fund, the government built upon an existing loan scheme

established in 1992 through the Development Bank of Mauritius (DBM) for solar water heaters

(SWH) by setting up the SWH Scheme to provide outright grants to residents to install

household SWHs. Phase 1 of this scheme was launched in 2008 and provided grants of

Page | 8

Rs10,000 (about $315 USD) per SWH system (MID, 2013). Pursuant to a goal of achieving 35%

renewable energy by 2025, the SWH Scheme aimed to increase the number of domestic SWHs

from 25,000 in 2008 to 50,000 by the end of 2009 (Republic of Mauritius Long-Term Energy

Strategy 2009-2025, 2009). Phase 1 enabled 24,000 households to benefit from the scheme at

a cost of Rs250 million (about $7.9 million USD). Although the scheme lacked quality control

infrastructure, such as registered lists of suppliers and installers and warranty requirements

(MID, 2012), public interest exceeded expectations, and by the end of Phase 1, the Scheme

had a backlog of over 20,000 applicants. SWH Scheme 2 was officially launched on December

27, 2011 with tighter quality requirements. Following the successful funding and installation of

14,600 new SWH systems in Phase 2, SWH Scheme 3 was launched immediately, providing

grants to 19,762 recipients. Approximately 60,000 households have purchased SWHs with the

support of incentive and loan schemes.

1.1.1 SOLAR WATER HEATING HEATING TARGETS

SCORE 0.0 / 5.0

The Long-Term Energy Strategy 2009-2025 and Energy Strategy 2011-2025 Action Plan

proposed additional policies and incentives “to promote solar water heating systems to

achieve in a short-to-medium term the target of 50% households and businesses.” However,

this action is no longer listed in the Energy Strategy Action Plan updated 22 April 2014. As a

result, Mauritius receives a score of 0 for this indicator.

1.1.2 FINANCIAL INCENTIVES FOR SYSTEM INSTALLATION

SCORE 5.0 / 5.0

As of end of 2013, the MID Fund and DBM have provided nearly Rs 600 million (over $12

million USD) in grants to nearly 60,000 households for purchasing and installing new SWH

systems. Though the most recent phase of the SWH scheme has concluded, design of phase 4

is under way. As discussed above, applications have continually exceeded available funds

during the Schemes (MID, 2013).

As a result of this program, Mauritius receives a score of 5 for this indicator.

Page | 9

1.1.3 SWH LOAN PROGRAMS

SCORE 5.0 / 5.0

Since 1992, the Development Bank of Mauritius has provided a concessionary interest rate on

loans for the purchase of solar water heaters from registered suppliers for domestic use. This

SWH loan provides up to Rs 35,000 ($1,100 USD) in funding with an annual interest rate of 9%

over 7 years and has been accessed by approximately 9,000 households (J. Bhandari, personal

communication, October 7, 2014). Grant recipients are able to apply for this loan facility under

modified terms (Rs 15,000 with annual interest of 7.5-8.5%), though the DBM has not kept

records on how many households received both grants and loans (MID, 2012).

Additional loan facilities and incentives exist alongside the MID and DBM schemes. The

Agence Française de Développement (AFD) partnered with four local banks to lend €40 million

(Rs 1.61 billion) to fund 104 renewable energy and energy efficiency projects. An additional €

60 million is allocated for investment through 2017, which may help finance larger SWH

projects at the commercial and industrial level (Agence Française de Développement, 2014).

The Mauritius Commercial Bank has also offered free SWHs to customers taking out housing

loans in excess of Rs 1 million ($31,400 USD) (MCB Group, 2014).

Due to Mauritius’s active SWH loan programs, the country earns a score of 5 for this indicator.

1.1.4 BUILDING MANDATES

In its Long-Term Energy Strategy 2009-2025, Mauritius outlined proposals to enact SWH

requirements for some buildings and general energy efficiency codes for all buildings. The

Energy Strategy 2011-2025 Action Plan outlined a requirement that 50% of hot water supplied

to new large buildings be sourced from solar water heaters. As of April 2014, the Energy

Services Division of the Ministry of Energy and Public Utilities is implementing this national

directive.

Mauritius receives a score of 5 for this indicator.

SCORE 5.0 / 5.0

Page | 10

1.1.5 OUTREACH CAMPAIGNS

SCORE 5.0 / 5.0

The MID Fund has implemented a number of outreach programs to promote its range of

sustainability programs. These programs include community outreach and awareness raising

campaigns including, student-targeted sustainability awareness programs, and press

conferences for new SWH Schemes (Mahomed 2013; “Talking Points,” 2011; Virahsawmy,

2011). While many of these outreach programs were not specifically related to SWH, surveys in

the Continuous Multipurpose Household Survey in 2009 found that nearly 83% of households

were aware of the SWH scheme and nearly 92% were aware of the energy saving campaign

conducted by the Ministry of Public Utilities and Central Electricity Board in the previous year.

For these outreach programs, Mauritius receives a score of 5 for this indicator.

Page | 11

PARAMETER II: NATIONAL CONDITIONS

Parameter II Score Indicator Weight

(%)

Indicator

Score (Raw)

Weighted

Score

(Weighted)

National

Conditions 0.94

Insolation 5% 3.9 0.19

SWH Market

Penetration 4% 1.6 0.06

Energy Consumption

Growth 5% 4.2 0.21

SWH Market Growth 4% 5.0 0.20

Competitiveness: LCOE

Comparison/Payback

Period

7% 4.0 0.28

Competitiveness:

Heating Fuel Subsidy 5% 0 0.00

Subtotal 30% 21.7 0.94

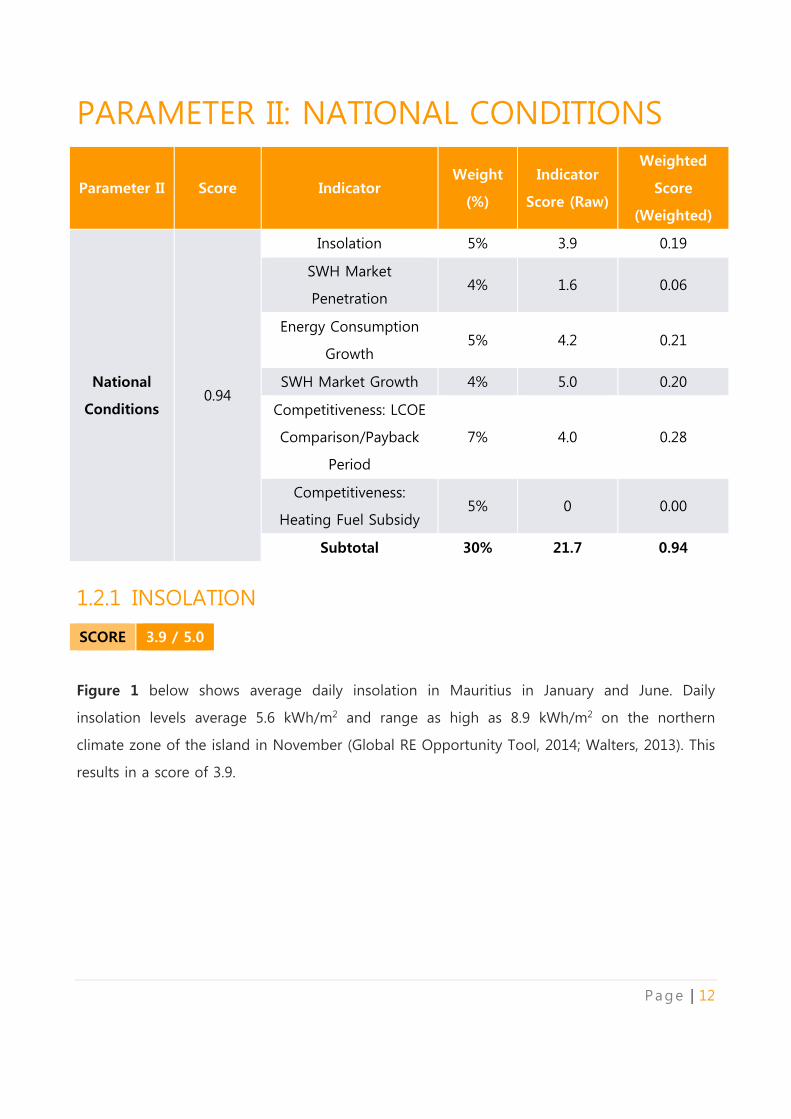

1.2.1 INSOLATION

SCORE 3.9 / 5.0

Figure 1 below shows average daily insolation in Mauritius in January and June. Daily

insolation levels average 5.6 kWh/m2 and range as high as 8.9 kWh/m2 on the northern

climate zone of the island in November (Global RE Opportunity Tool, 2014; Walters, 2013). This

results in a score of 3.9.

Page | 12

Figure 1: Daily Insolation in Mauritius (kWh/m2/day)

Source: Mauritius Meteorological Services, 1985-2000

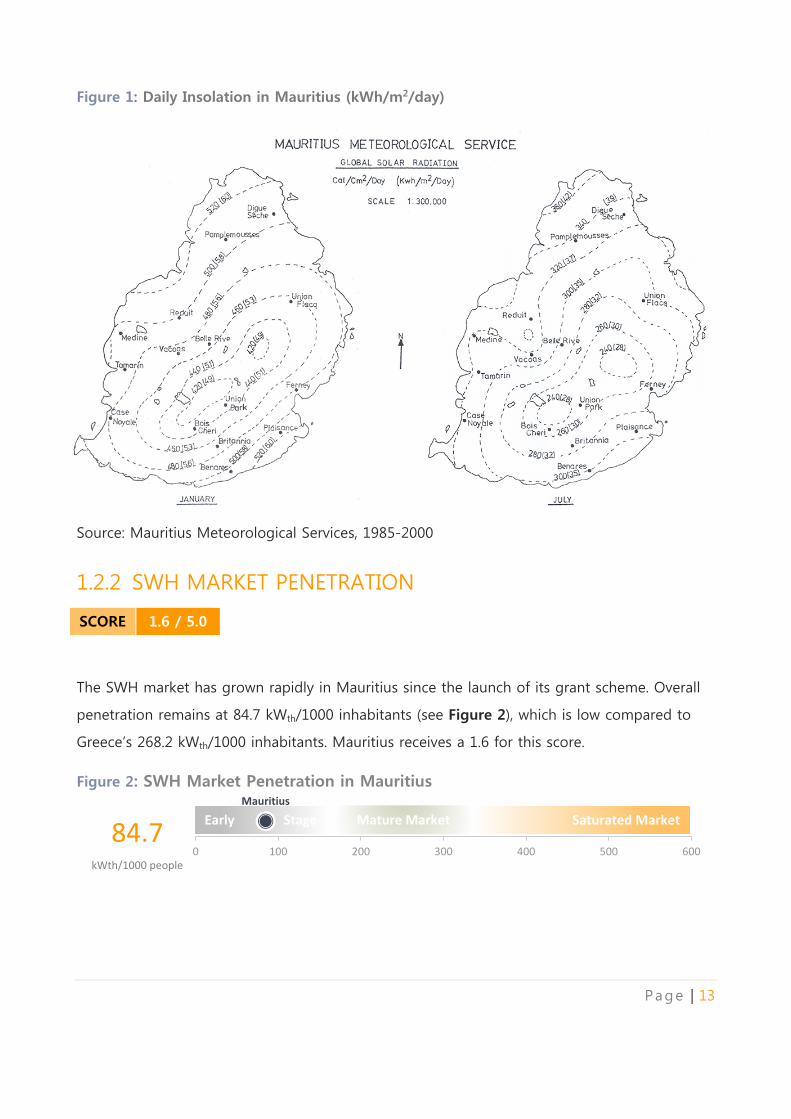

1.2.2 SWH MARKET PENETRATION

SCORE 1.6 / 5.0

The SWH market has grown rapidly in Mauritius since the launch of its grant scheme. Overall

penetration remains at 84.7 kWth/1000 inhabitants (see Figure 2), which is low compared to

Greece’s 268.2 kWth/1000 inhabitants. Mauritius receives a 1.6 for this score.

Figure 2: SWH Market Penetration in Mauritius

84.7

kWth/1000 people

Mature Market Saturated Market Early Stage

Mauritius

0 100 200 300 400 500 600

Page | 13

1.2.3 RESIDENTIAL ENERGY CONSUMPTION GROWTH

SCORE 4.4 / 5.0

According to IEA statistics, residential energy consumption in Mauritius has grown overall

during the five year period of 2006-2011 (Figure 3), although annual growth rates have

ranged from negative growth to growth as high as 4.4%. Mauritius has a 5-year average

residential energy consumption growth rate of 2.1%. This results in a score of 4.4.

Figure 3: Residential Energy Consumption in Mauritius

1.2.4 SWH MARKET GROWTH

SCORE 5.0 / 5.0

The SWH market in Mauritius has grown rapidly during the past five years, from 16.3 MWth in

2008 to 109.8 MWth in 2013 (Figure 4). The number of households using SWH grew from

approximately 13,000 in 2004 to 41,842 in 2011 to over 88,000 by the end of 2013.1 Significant

growth has also occurred in the commercial sector, particularly in hotels and the tourism

sector. The 5-year average market growth rate is 40%. Mauritius receives a score of 5.

1 See comment in 2b of TechScope inputs in accompanying spreadsheet for more information.

100

105

110

115

120

125

2007 2008 2009 2010 2011 2012

Ktoe

Page | 14

Figure 4: SWH Installed Capacity in Mauritius

1.2.5 PAYBACK PERIOD

SCORE 4.0 / 5.0

SWH system costs. Evacuated tube collectors imported from China account for the vast

majority of the residential SWH market in Mauritius (Elahee & Beeharry, 2013; Statistics

Mauritius, 2014). According to data gathered for the MID Fund Phase 2 assessment, the

average collector size is 15 tubes and the typical tank size is 150-200 liters (Walters, 2013). A

survey of 24 Chinese collectors with 15 tubes yielded an average collector aperture area of

1.43 m2 (Solar Rating & Certification Corporation, 2014). The average system cost is around

US$1000 (including installation) and SWHs obtained through government incentive programs

must be guaranteed for at least 7 years.

Retail energy prices. In Mauritius, nearly 60% of domestic hot water systems are powered by

liquefied petroleum gas (LPG) (Digest of Energy and Water Statistics, 2011). The SWH Scheme

2 assessment found that among grant recipients who replaced existing water heaters with

SWH, 77% were replacing LPG-fueled systems (Walters, 2013). It is assumed that SWH

competes against the subsidized price of LPG, which was Rs330 ($10.37 USD) per 12 kg bottle

or Rs27.5 ($0.86 USD) per kg (State Trading Corporation, 2014). 1 kg of LPG yields 12.5 kWh,

translating to $0.069/kWh.2

2 The average residential rate of electricity is $0.18/kWh, which would greatly reduce the payback period

for those replacing electric heating systems with solar water heating systems.

-

20

40

60

80

100

120

2009 2010 2011 2012 2013

MW

th

Page | 15

Based on RETScreen analysis, the simple payback period for a SWH system in Mauritius is 4.3

years, assuming a household receives both a MID Fund grant and a DBM loan. This results in a

score of 4.

1.2.6 COMPETITIVENESS: HEATING FUEL SUBSIDY

SCORE 0.0 / 5.0

The retail price of LPG is fixed by the Government of Mauritius. In 2012, the Mauritius State

Trading Corporation (STC) spent over Rs716 million ($22.6 million USD) subsidizing the import

and sale of 67,893 metric tons of LPG at 32% below cost (STC, 2013). These subsidies reduce

the competitiveness of solar water heating systems. Mauritius receives a score of 0 for this

indicator.

Page | 16

PARAMETER III: FINANCING Parameter

III Score Indicator Weight (%)

Indicator

Score (Raw)

Indicator Score

(Weighted)

Financing 0.63

Country

Credit Rating 5% 2 0.10

Access to

Finance 15% 3.5 0.53

Subtotal 20% 5.5 0.63

1.3.1 COUNTRY CREDIT RATING

SCORE 2.0 / 5.0

Mauritius has a high per capita GDP relative to other African countries and has maintained a

relatively low government debt-to-GDP ratio (World Bank). Mauritius has maintained steady

annual GDP growth for over 30 years and is ranked by the World Bank as an upper middle

income country. Mauritius received a credit rating of Baa1 from Moody’s, which results in a

score of 2.

1.3.2 ACCESS TO FINANCE

SCORE 3.5 / 5.0

The access to finance score was arrived at through two measures of equal weight: the real

interest rate, which serves as a proxy for the price of loans that accounts for inflation; and

domestic credit provided by the banking sector (as a percentage of GDP), which serve as a

proxy for the availability of in-country loans. The combination of price and availability

create a measure for access. Mauritius’ average real interest rate (2011-2013) is 5.7%,

resulting in a score of 3. The average domestic credit (2011-2013) provided by the

banking sector (as percent of GDP) is 113.9%, resulting in a score of 4. This combination of

factors results in Mauritius’ score of 3.5.

Page | 17

PARAMETER IV: BUSINESS CLIMATE

Parameter IV Score Indicator Weight

(%)

Indicator

Score

(Raw)

Indicator

Score

(Weighted)

Business

Climate 0.65

Doing Business Index 5% 5.0 0.25

Domestic

Manufacturing 3% 4.0 0.12

Product Certification 5% 1.5 0.08

Installer Certification 4% 5.0 0.20

Industry Association 4% 0.0 0.00

Subtotal 21% 11.0 0.65

1.4.1 BUSINESS CLIMATE

SCORE 5.0 / 5.0

Mauritius ranks 20 out of 185 countries according to Doing Business 2014. The scores for the

individual indicators within the Doing Business Rank can be seen in Table 1 below. Mauritius is

the highest ranking African country and has high rankings for certain indicators, such as

protecting investors, paying taxes, trading across borders, and starting a business. Overall,

Mauritius’s ranking results in a score of 5.

Table 1: Mauritius - Doing Business Ranking

Category Doing Business Ranking

Starting a Business 19

Dealing with Construction Permits 123

Getting Electricity 48

Registering Property 65

Getting Credit 42

Protecting Investors 12

Paying Taxes 13

Page | 18

Trading Across Border 12

Enforcing Contracts 54

Resolving Insolvency 61

1.4.2 DOMESTIC MANUFACTURING

In the TechScope assessment, Manufacturing Value Added (MVA) is used as a proxy for how

well positioned a country is for manufacturing. In 2013, Mauritius had a MVA as percentage of

GDP of approximately 15%, which is close to the global average of (~17%). As of 2014, there

are approximately 40 domestic companies in Mauritius that supply solar collectors and

components that are registered with the Development Bank of Mauritius for the MID Fund

SWH Scheme and the DBM’s SWH loan (MID, 2012). However, it is unclear to what extent

these suppliers are involved in assembly or manufacturing. Official import data from 2008-

2013 shows that at approximately 15% of imported SWHs were in completely knocked down

condition and required assembly, but the condition of other imported SWHs was not specified.

Mauritius therefore receives a score of 4, though it remains unclear how applicable this

indicator is to SWH suppliers in Mauritius.

1.4.3 PRODUCT CERTIFICATION

Mauritius continues to build its SWH standards and certification infrastructure as the MID Fund

SWH Scheme progresses.

Standards. The Mauritius Standards Bureau adopted a Mauritian Standard for SWH based

on European SWH standard EN 12976 (EN-MS-12976) on February 13, 2010. Many

domestic suppliers objected, claiming that the added cost of conforming to the stringent

EU standards would make SWHs unaffordable to most households; fewer than 5 out of 40

registered suppliers claimed to provide any models that achieved the standard, and these

models were more expensive and limited in supply. As a result, EN-MS-12976 is not legally

enforced and was not included in the MID Fund SWH Scheme. Instead, a set of prescriptive

minimum standards were adopted, including requirements for safety, collector material,

SCORE 4.0 / 5.0

SCORE 1.5 / 5.0

Page | 19

tank material, and warranty. New standards may be developed in the future that are more

appropriate for a developing country and adaptable to the needs of the Mauritian climate,

particularly with regards to cyclones (MID, 2012).

Testing. As of October 2014, the Mauritius Standards Bureau has no equipment for testing

SWH compliance. All testing of compliance with SWH standards must be undertaken

abroad.

Certification and labeling. According to the Mauritian Standard for SWH, all SWH

products must be tested abroad to achieve EU standards, and each model must receive a

Certificate of Conformity from an ILAC-accredited lab. As previously discussed, EN-MS-

12976 is not enforced and was not incorporated into any of the government incentive

schemes. Ultimately, only 2 out of 40 registered suppliers attempted to conform to the

standard and achieve certification. A new, binding set of standards and domestic testing

facilities will be necessary in order to provide certification for the SWHs sold in Mauritius.

Based on the current status of standards and certification, Mauritius receives a score of a 1.5.

1.4.4 INSTALLER CERTIFICATION

SWH installers who wish to participate in the MID Fund SWH Scheme must be certified by

demonstrating that they have taken a prescribed course at the Mauritius Institute of Training

and Development, or any equivalent course approved by the MITD (MID, 2012). As a result,

Mauritius receives a score of 5 for this indicator.

1.4.5 INDUSTRY ASSOCIATION

The Sustainable Energy Society of Southern Africa (SESSA) was formed in 1974 as a National

Section of the International Solar Energy Society and includes a Mauritian constituency. It is

unclear, what share of Mauritian solar thermal companies take part in SESSA, or to what extent

Mauritian companies even participate in SESSA. There are no other industry associations in the

region. As a result, Mauritius currently receives a score of 0.

SCORE 5.0 / 5.0

SCORE 0.0 / 5.0

Page | 20

Overall Score 1.8 / 5.0

SEYCHELLES

Summary: The solar thermal market in

Seychelles has grown an average of ~17%

annually over the last five years, from 1.7

MWth in 2006 to approx. 7.4 MWth in 2014.

Seychelles’ overall TechScope score is 1.8,

which will be discussed in detail in the

sections in order to provide greater insight

into the SWH TechScope Market Readiness

Assessment for Seychelles.

General Information (2013)

Population 89,173

GDP US$ 1,268,018,738

Total installed solar

thermal (flat plate and

evacuated tube

collectors)

7.4 MWth

Parameter Score

SWH Support Framework 0.35 / 1.45

National Conditions 0.78 / 1.50

Financing 0.41 / 1.00

Business Climate 0.26 / 1.05

Page | 21

PARAMETER I: SOLAR WATER HEATING

SUPPORT FRAMEWORK

Parameter I Score Indicator Weight

(%)

Indicator

Score (Raw)

Indicator

Score

(Weighted)

Solar Water

Heating

Support

Framework

0.35

SWH Targets 5% 0.0 0.00

Financial Incentives

for System

Installation

8% 0.0 0.00

SWH Loans

Programs 7% 5.0 0.35

Building Mandates 5% 0.0 0.00

Outreach

Campaigns 4% 0.0 0.00

Subtotal 29% 5.0 0.35

Seychelles, a group of islands in the Indian Ocean, is almost entirely dependent on imported

fossil fuels. The global oil price spike in 2007-2008 and subsequent global recession damaged

the Seychelles economy, and inflation reached 37% in 2008 (World Bank). In an effort to

reduce its fossil fuel dependence, Seychelles passed the Energy Act in December 2012. The Act

created policies to support renewable electricity generation but did not contain provisions to

support solar water heating.

2.1.1 SOLAR WATER HEATING TARGETS

SCORE 0.0 / 5.0

As of November 2014, Seychelles did not have targets for SWH. Seychelles receives a score of

0 for this indicator.

Page | 22

2.1.2 FINANCIAL INCENTIVES FOR SYSTEM INSTALLATION

SCORE 0.0 / 5.0

In 2010, the Seychelles government enacted a Goods and Services Tax (GST) exemption for all

renewable energy-related equipment and technology (Seychelles Revenue Commission, 2010).

While the Seychelles GST is fairly high (15%), tax exemptions typically do not have a significant

impact on market development unless paired with other financial incentives (see TechScope

Section 2.2).

The Seychelles government, in collaboration with the United Nations Development Programme

(UNDP), the Global Environment Facility (GEF), and domestic partners, launched a financial

rebate scheme of 35% on any solar PV system up to 3 kilowatt peak in May 2014 (“New

Schemes,” 2014). This rebate scheme does not include SWH, and it is unknown if SWH will be

eligible for the rebate scheme at a later date. Seychelles receives a score of 0 for this indicator.

2.1.3 SWH LOAN PROGRAMS

SCORE 5.0 / 5.0

In 2014, the Seychelles government, in collaboration with the UNDP, GEF, and International

Finance Corporation launched the Seychelles Energy-Efficiency and Renewable Energy

Programme (SEEREP), which will provide loans of up to SCR100,000 (approx. $7,100 USD3) at a

concessionary interest rate of 5% to households for purchasing energy efficiency and

renewable energy equipment, including home appliances, solar PV, and SWH (Ministry of

Finance, Trade and Investment, 2014).4 SEEREP will run for three years and aims to target

11,000 households in the first two years. Seychelles receives a score of 5 for this indicator.

3 An exchange rate of 14.11 SCR to 1 USD, representing the average exchange rate for the month of November

(Mataf, 2014), is used throughout this report. 4 The Central Bank of Seychelles’ average lending interest rate is over 11%. The concessionary rate of 5% is backed

by government subsidies of SCR1 million (approx. $71,000).

Page | 23

2.1.4 BUILDING MANDATES

SCORE 0.0 / 5.0

Seychelles has not established SWH building mandates. As a result, Seychelles receives a

score of 0 for this indicator.

2.1.5 OUTREACH CAMPAIGNS

SCORE 0.0 / 5.0

The government has held some stakeholder workshops discussing SEEREP and other proposed

sustainability plans and has given briefings to local non-governmental organizations like the

National Consumers Forum on SEEREP (Civil Society in Seychelles, 2014). The Seychelles Energy

Commission is also engaged in general sustainability awareness outreach that includes but

does not focus on solar water heating. Seychelles receives a score of 0 for this indicator since

there has not yet been a dedicated solar water heating outreach program supported by the

government or by partners organizations.

Page | 24

PARAMETER II: NATIONAL CONDITIONS

Parameter II Score Indicator Weight

(%)

Indicator

Score

(Raw)

Indicator

Score

(Weighted)

National

Conditions 0.78

Insolation 5% 3.3 0.17

SWH Market

Penetration 4% 1.1 0.04

Energy

Consumption

Growth

5% 3.2 0.16

SWH Market

Growth 4% 5 0.20

Competitiveness:

Payback Period 7% 3.0 0.21

Competitiveness:

Heating Fuel

Subsidy

5% 0 0.00

Subtotal 30% 10.6 0.78

2.2.1 INSOLATION

SCORE 3.3 / 5.0

Average daily insolation levels in Seychelles average 5.5 kWh/m2/day (Clean Energy Solutions

Center, 2014). Based on the scoring methodology, Seychelles receives a score of 3.3.

2.2.2 SWH MARKET PENETRATION

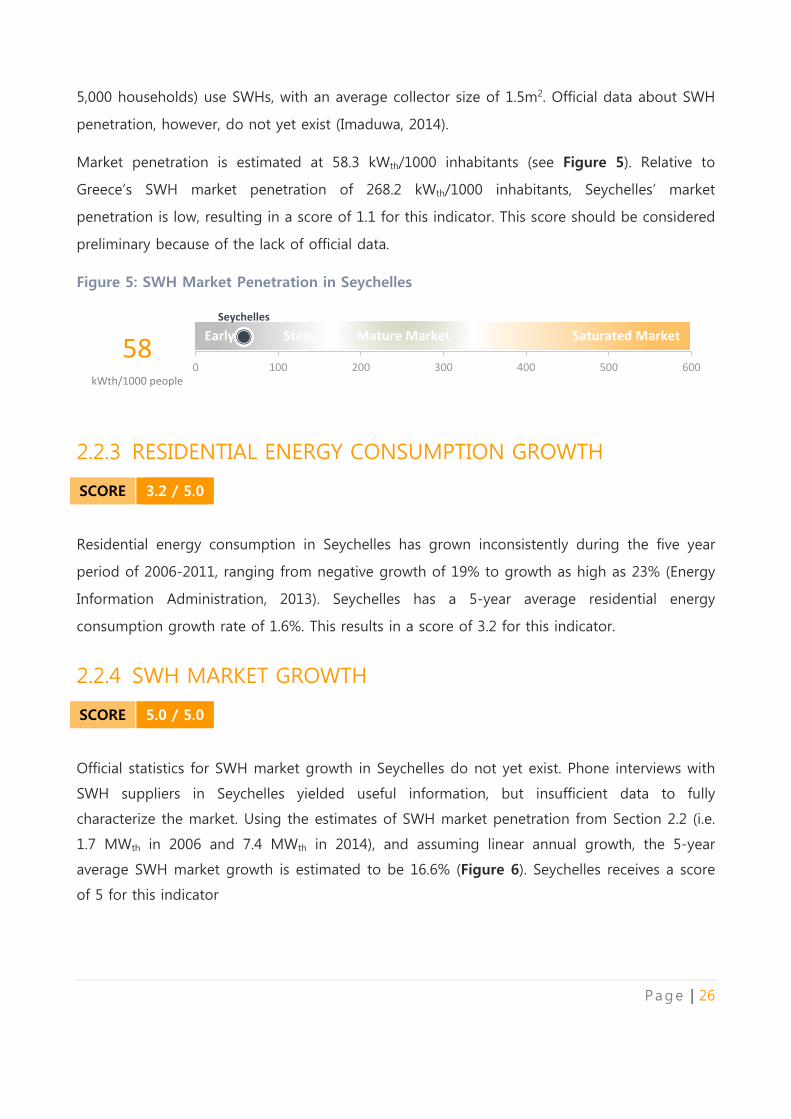

SCORE 1.1 / 5.0

In 2006, SWH market penetration in Seychelles was 19.85 kWth/1000 people (RECIPES, 2006).

The Seychelles Public Utilities Corporation (PUC) estimates that 20% of households (i.e. nearly

Page | 25

5,000 households) use SWHs, with an average collector size of 1.5m2. Official data about SWH

penetration, however, do not yet exist (Imaduwa, 2014).

Market penetration is estimated at 58.3 kWth/1000 inhabitants (see Figure 5). Relative to

Greece’s SWH market penetration of 268.2 kWth/1000 inhabitants, Seychelles’ market

penetration is low, resulting in a score of 1.1 for this indicator. This score should be considered

preliminary because of the lack of official data.

Figure 5: SWH Market Penetration in Seychelles

58

kWth/1000 people

2.2.3 RESIDENTIAL ENERGY CONSUMPTION GROWTH

SCORE 3.2 / 5.0

Residential energy consumption in Seychelles has grown inconsistently during the five year

period of 2006-2011, ranging from negative growth of 19% to growth as high as 23% (Energy

Information Administration, 2013). Seychelles has a 5-year average residential energy

consumption growth rate of 1.6%. This results in a score of 3.2 for this indicator.

2.2.4 SWH MARKET GROWTH

SCORE 5.0 / 5.0

Official statistics for SWH market growth in Seychelles do not yet exist. Phone interviews with

SWH suppliers in Seychelles yielded useful information, but insufficient data to fully

characterize the market. Using the estimates of SWH market penetration from Section 2.2 (i.e.

1.7 MWth in 2006 and 7.4 MWth in 2014), and assuming linear annual growth, the 5-year

average SWH market growth is estimated to be 16.6% (Figure 6). Seychelles receives a score

of 5 for this indicator

Mature Market Saturated Market Early Stage

Seychelles

0 100 200 300 400 500 600

Page | 26

Figure 6: SWH Installed Capacity in Seychelles

2.2.5 COMPETITIVENESS: PAYBACK PERIOD

SCORE 3.0 / 5.0

SWH system costs. In order to calculate the economic performance of typical SWH systems,

data was gathered from a range of different sources (e.g. interviews, reports, and regional

benchmarks). Evacuated tube collectors imported from China account for the majority of solar

water heaters in Seychelles, although installers also import systems from Australia and other

jurisdictions. System sizes and prices (not including installation) reported during interviews are

listed in Table 2. Installation cost estimates range from SCR1500 ($106 USD) to SCR3500 ($248

USD), depending on system size and installation location.

Table 2: Seychelles – SWH System Sizes and Prices

SWH Tank Size SWH System Price

100L SCR12500 ($886 USD)

180L SCR19000 ($1347 USD)

300L SCR27000 ($1914 USD)

Installers reported that 5-year warranty and after sales service are standard for units sold. Since

0

2

4

6

8

2006 2007 2008 2009 2010 2011 2012 2013 2014

MW

th

(Assumed year-on-year growth)

Page | 27

data on typical tank size is not available and specific information on the models sold by

suppliers was not available, data gathered from Mauritius were used as a proxy for system

sizing. The typical SWH sold in Seychelles is therefore assumed to have a 180 liter tank and

cost $1500 USD (including installation).

Retail Energy Prices. In Seychelles, the vast majority of water heaters are electric (Imaduwa,

2014). The analysis assumes that solar water heating competes against electricity, which has an

average retail rate of US$ 0.12/kWh (PUC, 2014).

Based on RETscreen analysis, the payback period is 7.4 years and results in a score of 3. As

discussed below, retail electricity prices in the Seychelles will increase as a result of pending

rate reform – which will improve the economic performance of SWH over time.

2.2.6 COMPETITIVENESS: HEATING FUEL SUBSIDY

SCORE 0.0 / 5.0

While the government of Seychelles has eliminated subsidies in the commercial and residential

sectors for LPG, subsidies for other fossil fuels remain (Laporte, 2013). The subsidies are

indirect; the parastatal Seychelles Petroleum Company (SEYPEC) supplies fuel to the Public

Utility Corporation (PUC) and Seychelles Public Transport Corporation (SPTC) at subsidized

rates. These subsidies amounted to SCR56.1 million ($427,000 USD) in 2012 (Laporte, 2012).

Utility tariffs are in the process of being rebalanced to reflect the cost of production, with

domestic electricity rates projected to more than double by 2022 (Laporte, 2013; PUC, 2014).

Seychelles receives a score of 0 for this indicator because of its energy subsidies, although the

competitiveness of SWH will improve as tariffs are rebalanced over the next decade.

Page | 28

PARAMETER III: FINANCING

Parameter III Score Indicator Weight

(%)

Indicator

Score (Raw)

Indicator

Score

(Weighted)

Financing 0.41

Country Credit

Rating 5% 0.75 0.04

Access to Finance 15% 2.5 0.38

Subtotal 20% 3.25 0.41

2.3.1 COUNTRY CREDIT RATING

SCORE 0.75 / 5.0

Moody’s and Standard & Poor have not rated Seychelles. Seychelles has been given a rating of

B+ from Fitch with a stable economic outlook (Reuters, 2014), which is typically equated to a

B1 with Moody’s and a B+ in S&P (Trading Economics, 2014). Seychelles’ Fitch rating has

improved significantly since October 2008, when the country defaulted on payments servicing

a central government debt and subsequently embarked on an IMF economic reform program.

Seychelles’ rating has progressed from default to C, B, and now B+ (Lablache, 2014). Despite

shrinking public debt, a rebounding economy, and repeated annual budget surpluses,

Seychelles’ credit rating remains low. Using the Fitch rating as a proxy for its equivalent

Moody’s and S&P ratings, the combination of these ratings gives Seychelles an average score

of 0.75 for this indicator.

2.3.2 ACCESS TO FINANCE

SCORE 2.5 / 5.0

The access to finance score was arrived at through two measures of equal weight: the real

interest rate, which serves as a proxy for the price of loans that accounts for inflation, and

the amount of domestic credit provided by the banking sector (as percent of GDP), which

serves as a proxy for the availability of in-country loans. Seychelles’ average real interest

Page | 29

rate (2010-2012) is 9.5%, which scores 3, and the average amount of domestic credit

(2010-2012) provided by the banking sector is 45%, which scores 2 (World Bank). This

combination of factors results in Seychelles’ average score of 2.5.

PARAMETER IV: BUSINESS CLIMATE

Parameter

IV Score Indicator

Weight

(%)

Indicator

Score (Raw)

Indicator

Score

(Weighted)

Business

Climate 0.26

Doing Business Index 5% 3.0 0.15

Domestic

Manufacturing 3% 2.0 0.06

Product Certification 5% 1.0 0.05

Installer Certification 4% 0.0 0.00

Industry Association 4% 0.0 0.00

Subtotal 21% 6.0 0.26

2.4.1 DOING BUSINESS INDEX

SCORE 3.0 / 5.0

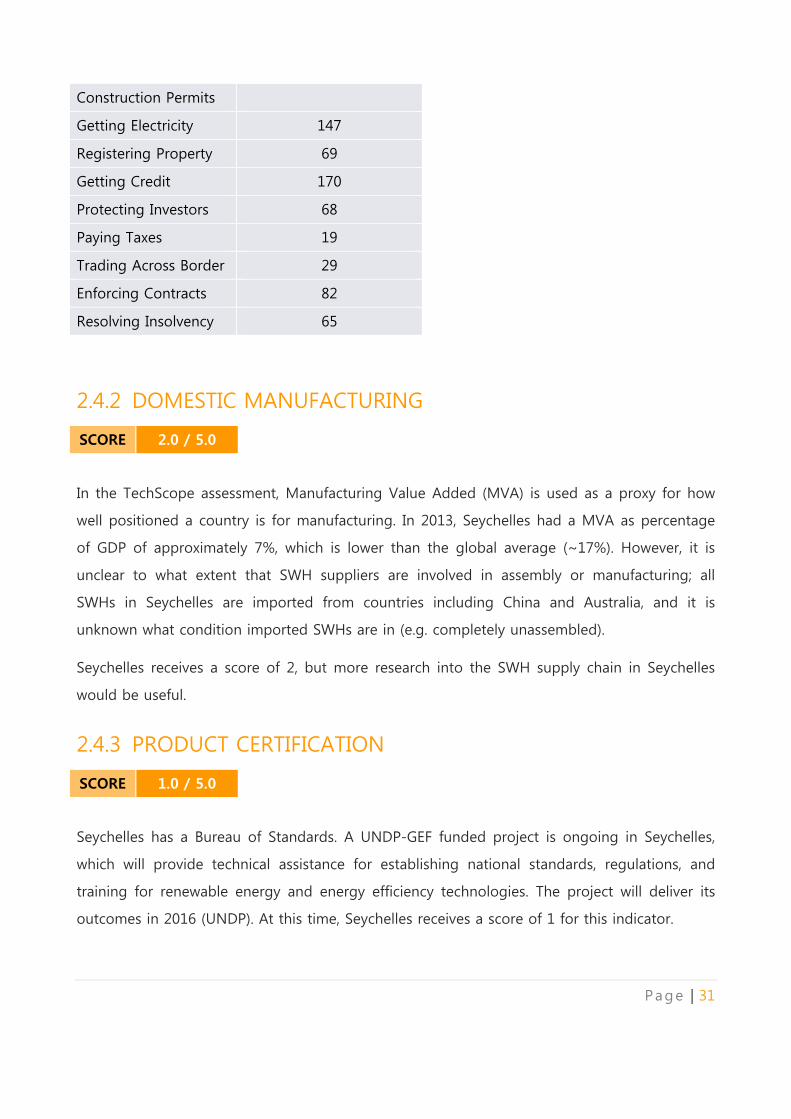

Seychelles ranks 80 out of 189 countries according to Doing Business 2014. The score for the

individual indicators within the complete Doing Business Ranking can be seen in Table 3.

Seychelles has high rankings for few indicators, such as paying taxes and trading across

borders, and low rankings for starting a business, getting credit, and getting electricity.

Seychelles’ overall ease of doing business results in a score of 3.

Table 3: Seychelles - Doing Business Ranking

Category Doing Business Ranking

Starting a Business 118

Dealing with 68

Page | 30

Construction Permits

Getting Electricity 147

Registering Property 69

Getting Credit 170

Protecting Investors 68

Paying Taxes 19

Trading Across Border 29

Enforcing Contracts 82

Resolving Insolvency 65

2.4.2 DOMESTIC MANUFACTURING

SCORE 2.0 / 5.0

In the TechScope assessment, Manufacturing Value Added (MVA) is used as a proxy for how

well positioned a country is for manufacturing. In 2013, Seychelles had a MVA as percentage

of GDP of approximately 7%, which is lower than the global average (~17%). However, it is

unclear to what extent that SWH suppliers are involved in assembly or manufacturing; all

SWHs in Seychelles are imported from countries including China and Australia, and it is

unknown what condition imported SWHs are in (e.g. completely unassembled).

Seychelles receives a score of 2, but more research into the SWH supply chain in Seychelles

would be useful.

2.4.3 PRODUCT CERTIFICATION

SCORE 1.0 / 5.0

Seychelles has a Bureau of Standards. A UNDP-GEF funded project is ongoing in Seychelles,

which will provide technical assistance for establishing national standards, regulations, and

training for renewable energy and energy efficiency technologies. The project will deliver its

outcomes in 2016 (UNDP). At this time, Seychelles receives a score of 1 for this indicator.

Page | 31

2.4.4 INSTALLER CERTIFICATION

SCORE 0.0 / 5.0

Although government agencies are beginning to certify solar PV installers, it is unclear if

installer certification for SWH will become available (Amesbury, 2014). Seychelles receives a

score of 0 for this indicator.

2.4.5 INDUSTRY ASSOCIATION

SCORE 0.0 / 5.0

There are no solar thermal or renewable energy industry associations currently active in

Seychelles. Seychelles receives a score of 0 for this indicator.

Page | 32

APPENDIX I SUMMARY OF COUNTRY TECHSCOPE SCORES

Page | 33

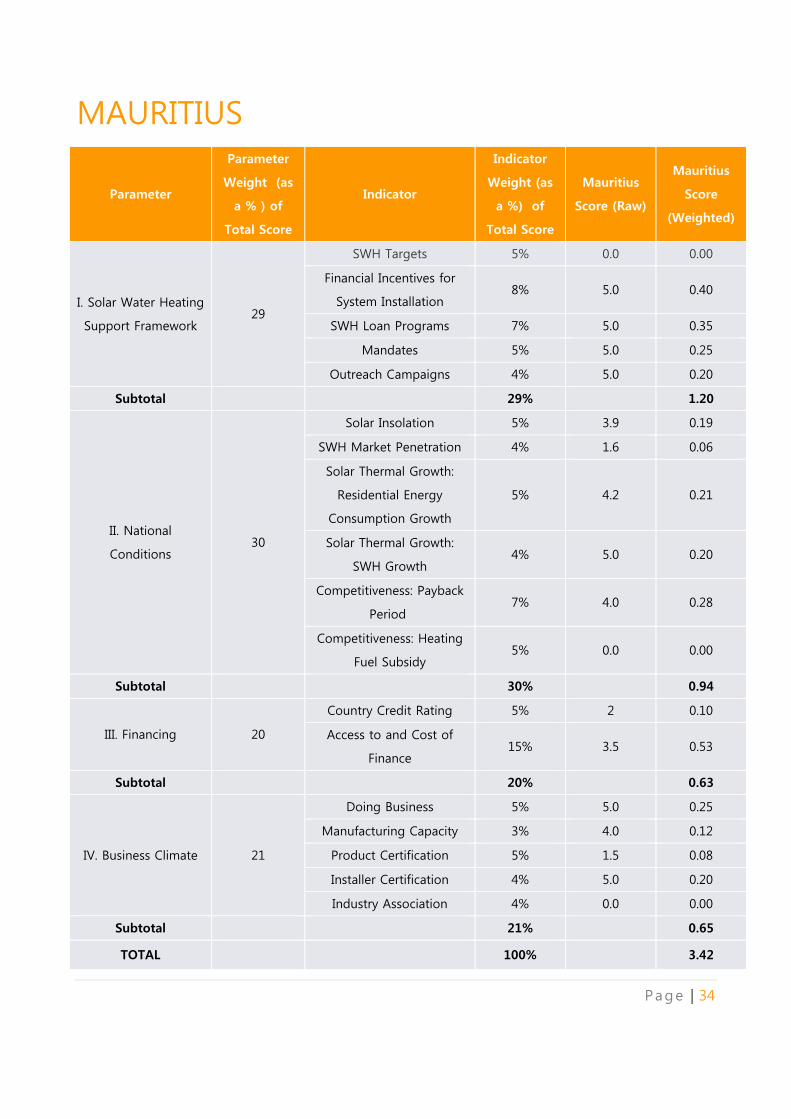

MAURITIUS

Parameter

Parameter

Weight (as

a % ) of

Total Score

Indicator

Indicator

Weight (as

a %) of

Total Score

Mauritius

Score (Raw)

Mauritius

Score

(Weighted)

I. Solar Water Heating

Support Framework 29

SWH Targets 5% 0.0 0.00

Financial Incentives for

System Installation 8% 5.0 0.40

SWH Loan Programs 7% 5.0 0.35

Mandates 5% 5.0 0.25

Outreach Campaigns 4% 5.0 0.20

Subtotal 29% 1.20

II. National

Conditions 30

Solar Insolation 5% 3.9 0.19

SWH Market Penetration 4% 1.6 0.06

Solar Thermal Growth:

Residential Energy

Consumption Growth

5% 4.2 0.21

Solar Thermal Growth:

SWH Growth 4% 5.0 0.20

Competitiveness: Payback

Period 7% 4.0 0.28

Competitiveness: Heating

Fuel Subsidy 5% 0.0 0.00

Subtotal 30% 0.94

III. Financing 20

Country Credit Rating 5% 2 0.10

Access to and Cost of

Finance 15% 3.5 0.53

Subtotal 20% 0.63

IV. Business Climate 21

Doing Business 5% 5.0 0.25

Manufacturing Capacity 3% 4.0 0.12

Product Certification 5% 1.5 0.08

Installer Certification 4% 5.0 0.20

Industry Association 4% 0.0 0.00

Subtotal 21% 0.65

TOTAL

100% 3.42

Page | 34

SEYCHELLES

Parameter

Parameter

Weight (as

a % ) of

Total Score

Indicator

Indicator

Weight (as

a %) of

Total Score

Seychelles

Score (Raw)

Score

(Weighted)

I. Solar Water Heating

Support Framework 29

SWH Targets 5% 0.0 0.00

Financial Incentives for

System Installation 8% 0.0 0.00

SWH Loan Programs 7% 5.0 0.35

Mandates 5% 0.0 0.00

Outreach Campaigns 4% 0.0 0.00

Subtotal 29% 0.35

II. National

Conditions 30

Solar Insolation 5% 3.3 0.17

SWH Market Penetration 4% 1.1 0.04

Solar Thermal Growth:

Residential Energy

Consumption Growth

5% 3.2 0.16

Solar Thermal Growth:

SWH Growth 4% 5 0.20

Competitiveness: Payback

Period 7% 3.0 0.21

Competitiveness: Heating

Fuel Subsidy 5% 0 0.00

Subtotal 30% 0.78

III. Financing 20

Country Credit Rating 5% 0.75 0.04

Access to and Cost of

Finance 15% 2.5 0.38

Subtotal 20% 0.41

IV. Business Climate 21

Doing Business 5% 3.0 0.15

Manufacturing Capacity 3% 2.0 0.06

Product Certification 5% 1.0 0.05

Installer Certification 4% 0.0 0.00

Industry Association 4% 0.0 0.00

Subtotal 21% 0.26

TOTAL

100% 1.80

Page | 35

APPENDIX II SWH FINANCING IN MAURITIUS

Page | 36

INTRODUCTION The state of the solar water heater market in Mauritius is strong, driven by the three phases of

the Maurice Ile Durable SWH Scheme. A quarter of households are now equipped with SWHs

and SWHs are becoming more popular in commercial and industrial applications, particularly

in Mauritius’ water-intensive tourism sector. As with all previous phases of the SWH Scheme,

Phase 3 was over-enrolled, with only 19,700 households receiving grants out of over 42,000

applicants (MID, 2013). Interest in SWH remains high with over 60% of households owning or

expressing interest in purchasing a SWH, and the vast majority of households are aware of the

major renewable energy and energy efficiency initiatives the government has undertaken over

the past five years (Digest of Energy and Water Statistics, 2012).

As planning for Phase 4 of the SWH scheme continues, it may be time to ask – are direct

grants still necessary to drive growth in the market? Given Mauritius’s current support

mechanisms for SWH including an increasing number of available financing mechanisms, a

high degree of public awareness and strong SWH TechScope score of 3.42, additional

incentives may not be required to stimulate the SWH market. However, despite these favorable

conditions, previous experiences demonstrate that SWH purchases drop off precipitously in

between SWH Schemes. In addition, 16% of households surveyed in 2012 reported being

deterred from purchasing SWH by cost. Non-renewal of an additional, well-publicized

financing scheme could result in the rapidly-growing SWH market to slow to a crawl.

STATUS OF MAURITIUS SWH SCHEME In January 2014, oversight of the SWH Scheme was transferred to the National Habitat Fund

Committee (NHFC) under the Ministry of Finance and Economic Development. NHFC is

currently reassessing the procedures of the scheme in order to address the recommendations

presented in the Phase 2 assessment conducted for the MID Committee. Though the report

recognized the significant accomplishments of the SWH scheme, it determined that 15% of

Page | 37

systems purchased through grants were installed, but not properly connected and made four

primary recommendations to improve the scheme:

1) Require and incentivize installers and suppliers to ensure proper connection and operability

of installed SWHs in order to receive grant funding;

2) Build a customer feedback system into the scheme to identify and revoke the registration of

SWH providers who consistently fail to meet the scheme’s requirements;

3) Target and prioritize households with electric water heaters to maximize cost and emissions

savings;

4) Take shading and collector orientation and tilt into account in future reviews (Walters,

2013).

In addition to making adjustments to the scheme’s procedures, observers have suggested that

NHFC develop an alternative, more cost-efficient financing mechanism.

ALTERNATIVE FINANCING SCHEMES IRENA has questioned whether Mauritius could augment its SWH grant scheme with elements

of the PROSOL financing scheme in Tunisia.

BACKGROUND ON PROSOL

The PROSOL scheme, launched in 2005, involved both the financial sector and the state-owned

utility in the provision of subsidized loans to end users. Initially PROSOL was a more complex

scheme that involved suppliers functioning as indirect lenders and guarantors for the

consumers. In 2007, a more streamlined procedure was adopted where consumers are granted

a loan from the bank and repay the loan to the utility through their electricity bills. This

procedure is often called on-bill financing and is becoming increasingly popular in the United

States: at least 20 states have implemented or are in the process of implementing on-bill

financing programs, many of which are supported by state legislation (Bell, Nadel, and Hayes,

2011). The state-owned utility assumes the responsibility of guarantor, and serves the role of a

stable, creditworthy entity that can secure lower loan interest rates and extended loan terms

(Menichetti & Touhami, 2007).

Page | 38

A PROSOL FOR MAURITIUS?

As mentioned in section 1.1.1.3, the Development Bank of Mauritius (DBM) has provided a

SWH loan since 1992. However, less than 10% of households that use SWHs have utilized the

loan facility, and the majority of the loans were issued after the SWH grant scheme was

introduced in 2008/2009. Additional research should be conducted on the reasons for low

uptake rate of the loan. This section assumes that adjustments to loan program design may

make the loan more attractive. Table 4 below compares the current SWH loan program in

Mauritius with the PROSOL scheme, as well as the SEEREP loan program recently introduced in

Seychelles. The table provides basic information about each of the three loan programs. As

can be seen in the table, the PROSOL program has a lower interest rate which may be

attributable to the on-bill financing structure.

Table 4: Comparison of SWH Loan Programs in Mauritius, Seychelles and Tunisia

DBM SWH Loan SEEREP (Seychelles) PROSOL (Tunisia)

Start year 1992 2014 2005

Amount Rs 35,000 ($1,100 USD) SCR 100,000 ($7,414 USD) 750 TND ($416 USD) for 200L

950 TND ($527 USD) for 300L

Loan

duration Up to 7 years 1-5 years 5 years

Interest rate 9% 5% 7% for phase 1, 5-6.5% for phase 2

(monthly market rate + 1.2%)

Eligibility

Individuals/household

owners purchasing a SWH

from a registered supplier

All households purchasing

renewable energy

technology and energy

efficient appliances/devices

Residential utility customers purchasing a

SWH from certified suppliers

Outcome ~9,000 recipients (1992-

present) Unknown

Over 119,000 systems (355,350 m2)

installed (2005-2010), ~140,000 m2

installed in 2011/12

Distinct

features

• Interest rates subsidized

(projected cost in first

year: SCR 1 million/

$75,000 USD)

• Combined with subsidies for lower

interest rates (compared to 12-13% for

similar consumer loans) and capital

costs (200 TND/$111 USD for 200L, 400

TND/$222 USD for 300L)

• Customer pays only the administrative

costs of obtaining a SWH and monthly

loan payments, collected by the utility

Page | 39

(STEG), which acts as a loan guarantor

• In the event of non-payment, STEG

suspends electricity supply to customer

PROSOL has been a successful program. Due to the strong results of the initiative, the

government of Tunisia has adopted an ambitious goal of installing 900,000 m2 of SWH

capacity by 2016 (Trabacchi, Micale, & Frisari, 2012). The success of PROSOL could be

replicated in Mauritius, and the use of on-bill financing could lower the cost of capital and

make the loan program more attractive.

Table 5: Comparison of Tunisia and Mauritius Economy

Tunisia Mauritius

Population (2013) 10,886,500 1,296,303

GDP (2013) $47,128,700,683 $11,938,403,909

PPP per capita (2013) $11,092 $17,200

Domestic credit provided

by banking sector (% of

GDP) (2010-12)

83.0% 113.9%

Country credit rating Ba3 (Moody’s) Baa1 (Moody’s)

Primary fuel for

residential heating LPG (subsidized) LPG (subsidized)

SWH market penetration 41.1 kWth/1000

people

84.7 kWth/1000

people

In some respects, both the financial sector and SWH market are stronger in Mauritius than in

Tunisia (see Table 5). While SWH market penetration is higher in Mauritius, there are still

significant opportunities for growth, given the large number of individuals waitlisted in each

previous SWH Scheme. Mauritius has also laid much of the non-financial groundwork needed

to continue developing the SWH market, including government-led public awareness

campaigns, installer quality requirements, and incentive schemes to “jumpstart” early stage

market growth.

Page | 40

A PROSOL-like scheme for Mauritius would not increase the amount of or access to capital,

which is already relatively strong in Mauritius compared to other SIDS. Rather, the convenient,

reliable cash flow from the utility serving as an enforceable collection agent would reduce risk

to lenders and allow for more favorable loan terms for consumers. Loan default rates in on-bill

financing programs in the United States have typically been less than 2% (Bell et al, 2011),

comparable to or lower than the default rate for other forms of consumer credits, which

ranged from 1.0% to 4.8% between 2009 and 2014 (S&P Dow Jones Indices, 2014). Moreover,

the PROSOL model would create a unified scheme that could synergize the previously-

separate grant and loan programs: smaller government grants could reduce the size of

monthly loan payments and increase the attractiveness of SWHs to the public.

Typical barriers to implementing on-bill financing often lie with the utility involved: the utility

may lack the capacity and resources to serve as a lending institution, assume additional

financial risk on behalf of its customers, and integrate on-bill financing into its billing system

(ACEEE, 2012). If loans were continued to be disbursed by the Development Bank of Mauritius

with the Central Electricity Board (CEB) only serving as a collection agent, financial risk to the

utility would be averted. Additional support would need to be provided by the government to

ensure the CEB has the human, financial, and technical resources to manage an on-bill

financing program and overhaul its billing program if necessary. In addition to addressing

utility-related barriers, the government will need to continue public outreach and education

campaigns to ensure that consumers understand the changes to and benefits of the program.

Though a PROSOL-like scheme would require additional resources to strengthen the CEB to

overcome barriers to implementation, such a scheme could help increase SWH uptake,

particularly in the numerous households that have refrained from purchasing SWHs due to

excessive upfront costs, despite the SWH grant scheme. If the government were able to

successfully assist the CEB in building the capacity needed to administer an on-bill financing

tool for SWHs, such a tool could be easily adapted for other renewable energy and energy

efficiency financing programs in support of Mauritius’ larger sustainability goals.

While the potential results of a PROSOL-like scheme are high and the conditions favorable, a

key difference between Mauritius and Tunisia remains in the area of technological standards

and regulations. As mentioned in 1.1.4.3 and in the introduction of this section, Mauritius does

not enforce any standards for SWHs beyond prescriptive minimum standards and warranty

Page | 41

requirements that suppliers must meet to participate in the SWH incentive programs. By

contrast, Tunisia has implemented a more comprehensive SWH standards regime, including an

accreditation scheme for both suppliers and installers, SWH certification and performance

labeling, and required equipment guarantees and after-sales service contracts (Traacchi et al.,

2012. Given the quality and connection problems noted by the 2013 MID committee study, it

will be important for the Mauritian government to:

• Strengthen SWH standards and regulations and develop a procedure for enforcement.

• Build quality assurance mechanisms (e.g. incentives or penalties) into the loan and

grant programs to ensure suppliers and installers have properly connected installed

SWHs.

If these steps are taken, a PROSOL-like scheme could prove a more cost-efficient financing

scheme for driving growth in the Mauritian SWH market, transferring a grant-based SWHs

market to a more sustainable credit-based market.

Page | 42

BIBLIOGRAPHY

Agence Française de Développement (2014). SUNREF: Green Lending Scheme Mauritius.

Retrieved September 26, 2014 from http://www.eu-africa-infrastructure-

tf.net/attachments/gefior-project-leaflet.pdf

American Council for an Energy-Efficient Economy. (2012, April). On-bill Financing for Energy

Efficiency Improvements. Retrieved November 5, 2014 from

http://www.aceee.org/files/pdf/toolkit/OBF_toolkit.pdf

Amesbury, April. (2014, May 3). Seychelles new solar energy scheme gives 35 percent rebate

on PV systems. Seychelles News Agency. Retrieved October 15, 2014 from

http://www.seychellesnewsagency.com/articles/384/Seychelles+new+solar+energy+sche

me+gives++percent+rebate+on+PV+systems

Bell, C.J., Nadel, S., & Hayes, S. (2011, December). On-bill Financing for Energy Efficiency

Improvements: A Review of Current Program Challenges, Opportunities, and Best

Practices. Report Number E118, Prepared for the American Council for an Energy-

Efficient Economy. Retrieved November 4, 2014 from

http://www.arkansasenergy.org/media/266/ACEEE%20On-

Bill%20Financing%20EE%20Improvements%20Dec%202011%20E118.pdf

Central Electricity Board (2010, December). Domestic tariff (as from 1st December 2010).

Retrieved September 24, 2014 from http://ceb.intnet.mu/tariffs/domestic.asp

Clean Energy Solutions Center. Global RE Opportunity Tool (Beta Version): A tool for

policymakers and energy analysts. Retrieved September 17, 2014 from

http://maps.nrel.gov/global_re_opportunity

Country energy information Seychelles. (2006, September). RECIPES. Retrieved from

http://www.energyrecipes.org/reports/genericData/Africa/061129%20RECIPES%20countr

y%20info%20Seychelles.pdf

Page | 43

Credit Rating – Countries – List. (2014, December 16). Trading Economics. Retrieved December

16, 2014 from http://www.tradingeconomics.com/country-list/rating

Development Bank of Mauritius. (2012). Solar Water Heater Loan Scheme. Retrieved September

15, 2014 from http://dbm.mu/node/64

Elahee, M.K., & Beeharry, M.A.H. (2013). Solar Water Heating: The Case of Mauritius. Prepared

for the European Conference on Sustainability, Energy and the Environment 2013.

Retrieved from http://www.iafor.org/offprints/ecsee2013-

offprints/ECSEE2013_Offprint_0040.pdf

Fitch Upgrades Seychelles to ‘B+’; Outlook Stable. (2014, August 8). Reuters. Retrieved October

2, 2014 from http://www.reuters.com/article/2014/08/08/fitch-upgrades-seychelles-to-b-

outlook-s-idUSFit71662020140808

Imaduwa, T. (2014, September 23). Interview.

International Energy Agency. (2013). Mauritius: Balances for 2012. Retrieved from

http://www.iea.org/statistics/statisticssearch/report/?year=2012&country=MAURITIUS&p

roduct=Balances

International Monetary Fund. (2013, April). Mauritius 2013 Article IV Consultation. Retrieved

September 19, 2014 from http://www.imf.org/external/pubs/ft/scr/2013/cr1397.pdf

Lablache, John. (2014, August 9). Seychelles rating upgraded to B+ says Fitch Ratings.

Seychelles News Agency. Retrieved October 15, 2014 from

http://www.seychellesnewsagency.com/articles/1142/Seychelles+rating+upgraded+to+B

+says+Fitch+Ratings

Laporte, Pierre. (2012, December 4). Budget Address 2013 by the Minister for Finance, Pierre

Laporte. Retrieved from http://www.sib.gov.sc/index.php/info-centre/general-

info/events/95-budget-address-2013-by-the-minister-for-finance-pierre-laportev

Page | 44

Laporte, Pierre. (2013, December 10). Budget Speech 2014 (English). Retrieved from

http://www.statehouse.gov.sc/uploads/downloads/filepath_29.pdf

Mahomed, O. (2013). Maurice Ile Durable [PDF document]. Retrieved from

http://www.gov.mu/portal/sites/mid/file/UNESCO%20AT%20TICADV%20-

%201%20june%202013.pdf

Maurice Ile Durable. (2013). Solar Water Heater Scheme 3. Retrieved September 16, 2014 from

http://www.gov.mu/portal/sites/mid/SolarScheme.htm

Maurice Ile Durable. (2012). Solar Water Heater Scheme Phase 2 FAQs. Retrieved September

16, 2014 from

http://www.gov.mu/portal/sites/mid/file/FAQs%20Solar%20Water%20Heater%20Scheme.

Mauritius. Ministry of Environment and Sustainable Development. (2011, June). Talking points

for interactive session of Hon. Minister of Environment and Sustainable Development.

Retrieved September 19, 2014 from

http://environment.gov.mu/English/Documents/speeches/11.06.08%20Meeting%20Stude

nts%20WED.docx

Mauritius. Ministry of Energy & Public Utilities. (2009). Republic of Mauritius Long-Term Energy

Strategy 2009-2025. Retrieved September 15, 2014 from

http://www.sids2014.org/content/documents/68Energy%20Strategy.pdf

Mauritius. Ministry of Energy & Public Utilities. (2011). Energy Strategy 2011-2025 Action Plan

– Updated. Retrieved September 19, 2014 from

http://publicutilities.gov.mu/English/DOCUMENTS/PLAN2806.DOC

Mauritius. Ministry of Energy & Public Utilities. (2014). Energy Strategy 2011-2025 Action Plan

– Updated (as at 22 April 2014). Retrieved October 22, 2014 from

http://publicutilities.gov.mu/English/DOCUMENTS/ENERGY-STRATEGY.PDF

Mauritius. Parliament. (2012). The Building Control Act of 2012. Retrieved September 19, 2014

from

Page | 45

http://environment.gov.mu/English/MUELEX/Documents/coastal/buildingcontrolact%202

012.pdf

Mauritius Standards Bureau. (2010, October). Communiqué on a Mauritian Standard for Solar

Water Heater. Retrieved from http://msb.intnet.mu/English/Pages/Communiqu%C3%A9-

on-a-Mauritian-Standard-for-Solar-Water-Heater.aspx

Mauritius. State Trading Corporation. (2013). Financial Statements (Audited) Year Ended 31

December 2012. Retrieved October 22, 2014 from

http://stc.intnet.mu/downloads/finalaccounts/FinancialStatements2012.pdf

Mauritius. State Trading Corporation. (2014). Retail Price of All Commodities. Retrieved October

14, 2014 from http://stc.intnet.mu/news/pricesofcommodities.html

MCB Group. (2014). Initiative 175. Retrieved October 10, 2014 from

http://www.mcbgroup.com/en/group/community/initiative-175

Members and Partners come together for NATCOF Workshop. (2014, June 25). Civil Society in

Seychelles. Retrieved October 15, 2014 from http://www.civilsociety.sc/?p=2423

Menichetti, E., & Touhami, M. (2007). Creating a credit market for solar thermal: the PROSOL

project in Tunisia. Prepared for the UNEP, Division of Technology, Industry and

Economics

Moody’s Investors Service. (2013, June 27). Moody's: Mauritius's Baa1 rating supported by

increasing economic diversification and resilience. Retrieved September 19, 2014 from

https://www.moodys.com/research/Moodys-Mauritiuss-Baa1-rating-supported-by-

increasing-economic-diversification-and--PR_276746

New scheme to make it cheaper to invest in photovoltaic systems. (2014, May 3). Seychelles

Nation. Retrieved October 2, 2014 from http://www.nation.sc/article.html?id=241554

Page | 46

Rickerson, W., Chessin, E., Veilleux, N., Wilson, H., Crowe, J. (2014). Solar Water Heating

TechScope Market Readiness Assessment. Prepared for UNEP, Division of Technology,

Industry and Economics, Global Solar Water Heating Initiative.

Seychelles. Ministry of Finance, Trade and Investment. (2014). Seychelles Budget 2014

Highlights. Retrieved from

http://www.statehouse.gov.sc/uploads/downloads/filepath_28.pdf

Seychelles. National Assembly. (2012). Energy Act, 2012. Retrieved October 17, 2014 from

http://www.seylii.org/files/Act%2011%20of%202012%20Energy%20Act,%202012.pdf

Seychelles. National Bureau of Statistics. (2013, December). Seychelles in figures. Retrieved

October 17, 2014 from http://www.statehouse.gov.sc/uploads/downloads/filepath_67.pdf

Seychelles. Public Utilities Corporation. (2014, November). Impact of tariff revision. Retrieved 16

December 2014 from http://www.puc.sc/pdfs/impact-of-tariffs-revision.pdf

Seychelles Revenue Commission. SI 34 of 2010 - Goods and Services Tax, SI 34 (2010).

Retrieved from http://www.src.gov.sc/resources/SI/SI34of2010.pdf

Solar Rating & Certification Corporation. Ratings Summary Page. Retrieved October 8, 2014

from https://secure.solar-rating.org/Certification/Ratings/RatingsSummaryPage.aspx

S&P Dow Jones Indices. (2014). S&P/Experian Consumer Credit Default Composite Index.

Retrieved November 5, 2014 from http://us.spindices.com/indices/specialty/sp-experian-

consumer-credit-default-composite-index

Statistics Mauritius. (2014). Detailed Trade data. Retrieved October 10, 2014 from

http://statsmauritius.gov.mu/English/Pages/DetailedTradedata.aspx

Statistics Mauritius. Ministry of Finance and Economic Development (2012, December). Digest

of energy and water statistics – 2011. Retrieved from

http://statsmauritius.gov.mu/English/StatsbySubj/Pages/DigestEnergy.pdf

Page | 47

Statistics Mauritius. Ministry of Finance and Economic Development (2013, October). Digest of

energy and water statistics – 2012. Retrieved from

http://statsmauritius.gov.mu/English/Publications/Documents/Regular%20Reports/energ

y%20and%20water/Digest-EnergyWaterStats2012.pdf

Trabacchi, C., Micale, V., Frisari, G. (2012, June). San Giorgio Group Case Study: Prosol Tunisia.

Prepared by Climate Policy Initiative for the San Giorgio Group. Retrieved from

http://climatepolicyinitiative.org/wp-content/uploads/2012/08/Prosol-Tunisia-SGG-Case-

Study.pdf

United Nations Development Program. (2014). Project document: Promotion and up-scaling of

climate-resilient, resource efficient technologies in a Tropical Island Context

United Nations Industrial Development Organization. (2013). Statistical Country Briefs.

Retrieved from http://www.unido.org/en/resources/statistics/statistical-country-

briefs.html

US Dollar to Seychelles Rupee Converter. (2014, December 17). Mataf. Retrieved 16 December,

2014 from https://www.mataf.net/en/currency/converter-USD-SCR

US Energy Information Administration. (2010). Electricity prices for households for selected

countries. Retrieved from http://www.eia.gov/countries/prices/electricity_households.cfm

US Energy Information Administration. (2013). International energy outlook 2013 (DOE/EIA-

0484(2013)). Washington, DC: US Department of Energy

Virahsawmy, Devanand. (2011, December). Press conference on solar water heater scheme

(phase II). Retrieved September 19, 2014 from

http://www.gov.mu/portal/sites/mid/file/Brief%20on%20SWH%20Phase%202.pdf

Walters, T. (2013, August 29). Maurice Ile Durable Fund: An Assessment of Phase 2 of the Solar

Water Heating Scheme. Prepared for the Maurice Ile Durable Committee

World Bank. (2013). Doing Business 2014: Understanding Regulations for Small and Medium-

Size Enterprises. Washington, DC: World Bank Group. DOI: 10.1596/978-0-8213-9984-2.

Page | 48

World Bank. (2014). Mauritius. Retrieved September 16, 2014 from

http://data.worldbank.org/country/mauritius

World Bank. (2014). Seychelles. Retrieved September 16, 2014 from

http://data.worldbank.org/country/seychelles

World Economic Forum. (2014). Global Competitiveness Report 2014-15. Retrieved from

http://reports.weforum.org/global-competitiveness-report-2014-2015/rankings

Page | 49