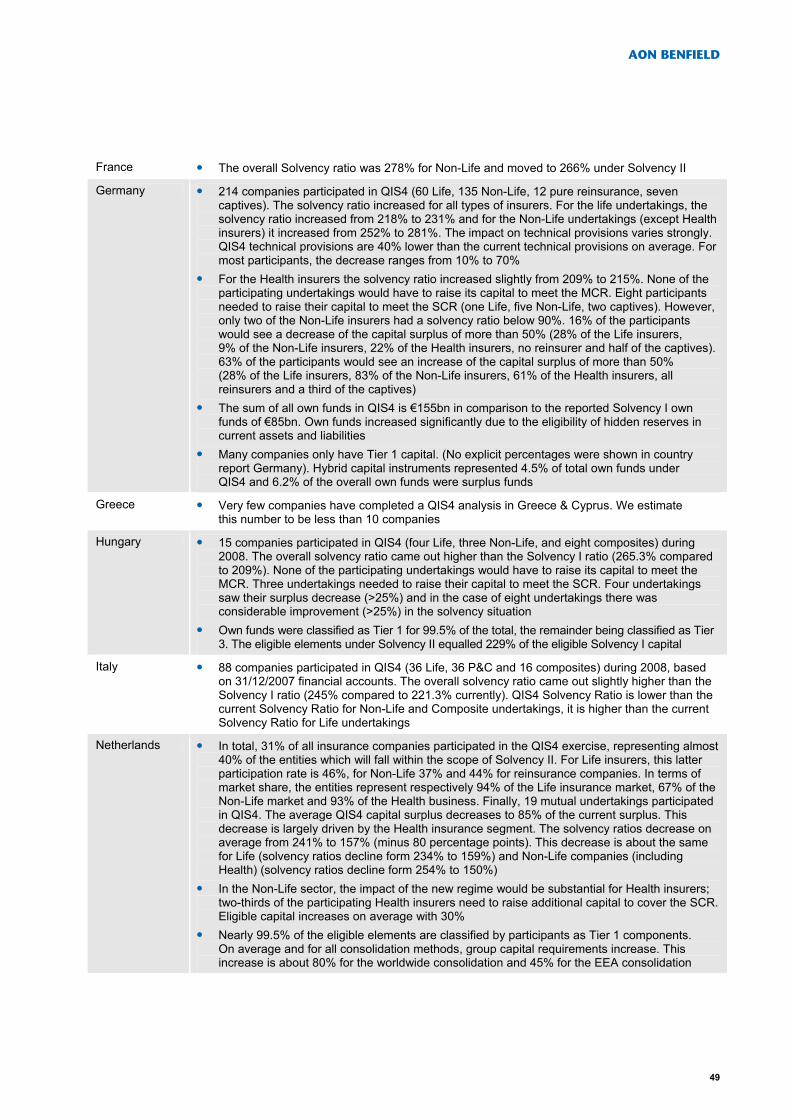

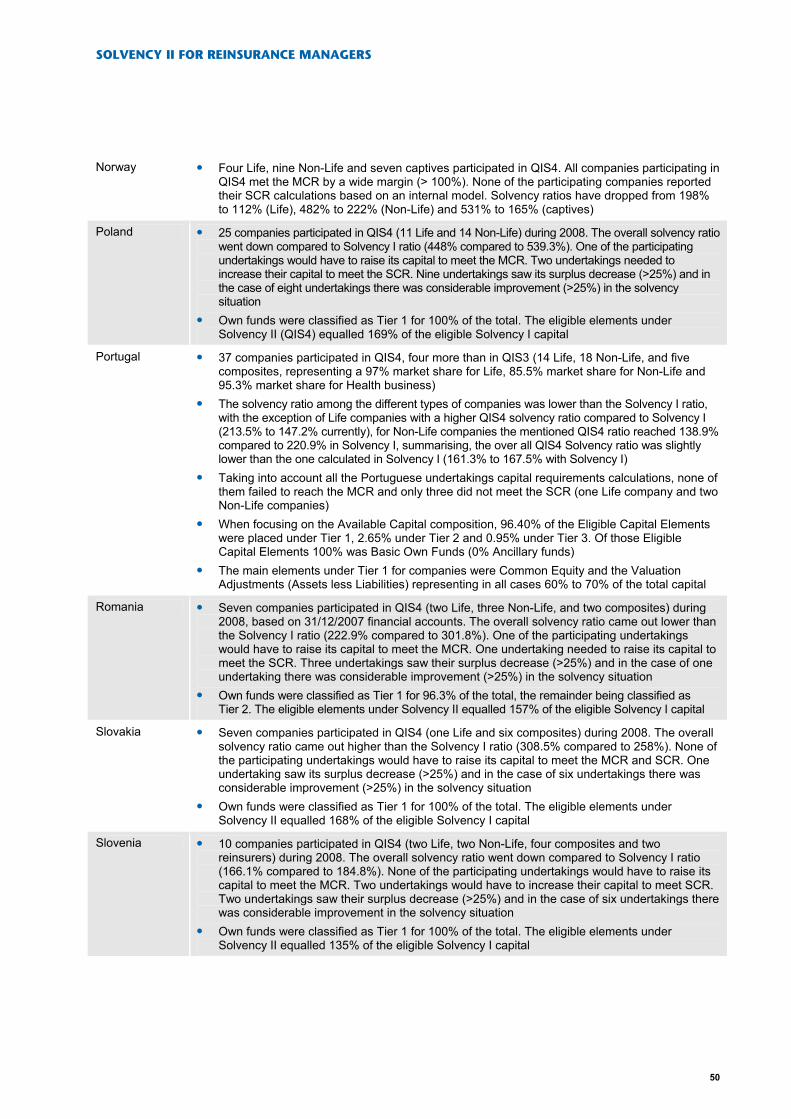

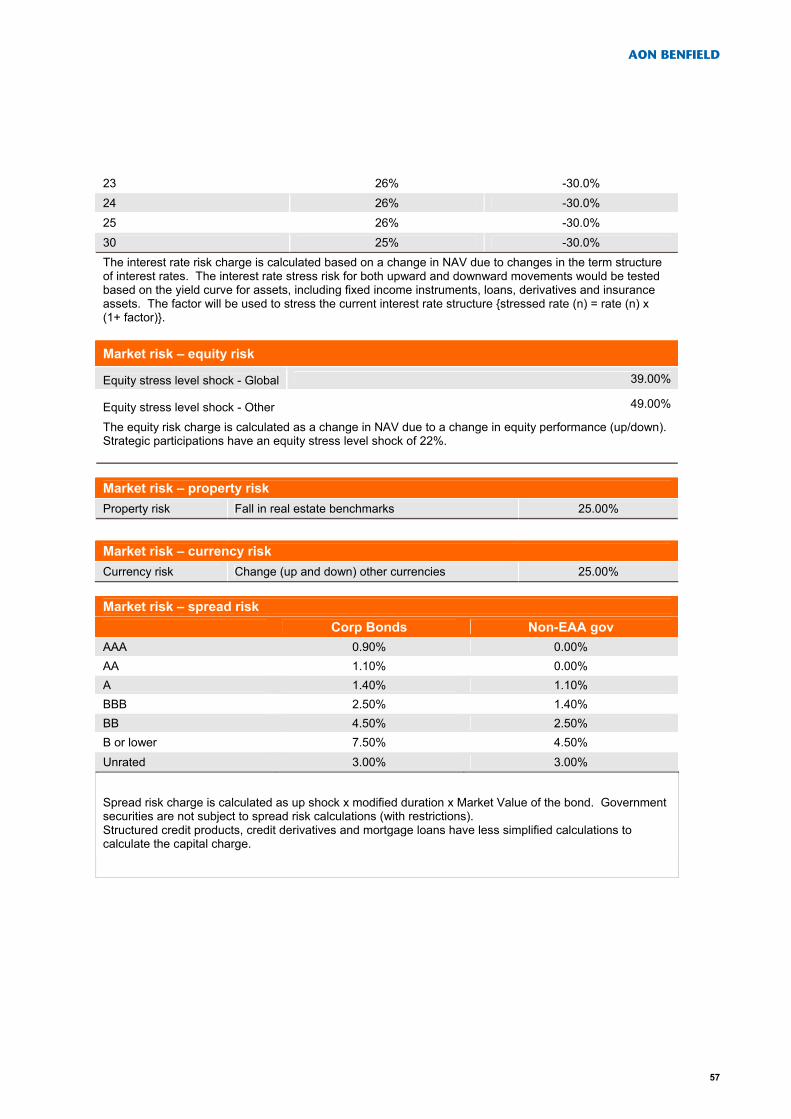

solvency ii for reinsurance managers - aon...

TRANSCRIPT

SOLVENCY II FOR REINSURANCE MANAGERS Key Discussion Points For Non-Life Insurers

1

July 2010 2nd edition

SOLVENCY II FOR REINSURANCE MANAGERS

2

About Aon Benfield As the industry leader in treaty, facultative and capital markets, Aon Benfield is redefining the role of the reinsurance intermediary and capital advisor. Through our unmatched talent and industry-leading proprietary tools and products, we help our clients to redefine themselves and their success. Aon Benfield offers unbiased capital advice and customized access to more reinsurance and capital markets than anyone else. As a trusted advocate, we provide local reach to the world’s markets, an unparalleled investment in innovative analytics, including catastrophe management, actuarial, and rating agency advisory, and the right professionals to advise clients in making the optimal capital choice for their business. With an international network of more than 4,000 professionals in 50 countries, our worldwide client base is able to access the broadest portfolio of integrated capital solutions and services. Learn more at aonbenfield.com.

AON BENFIELD

Contents Solvency II – What Does it Mean to You and How Can We Help?

10 Key Facts 4 The 4 Ways We Are Helping Our Clients 5 The 3 Key Questions for Clients 5 Frequently Asked Questions by Reinsurance Departments on Solvency II 6

Solvency II – Discussion Papers Executive Summary 8 Solvency II: Can It Deliver? 10 Treatment of Reinsurance in the Solvency II Capital Requirement 13 Reinsurance Under Solvency II – an Exceptional Source of Capital 17 The Impact of Solvency II on Risk Calibration 21 Impact of Non-Proportional Reinsurance on Solvency II Capital 25 S2Metrica – a New Tool for a New World of Regulation 34 The Rating Agency Perspective 36 Challenges for a Captive Audience 39 IFRS and Solvency II – The Wobbling Road to Divergence? 42

Country Overviews 46

Glossary 54

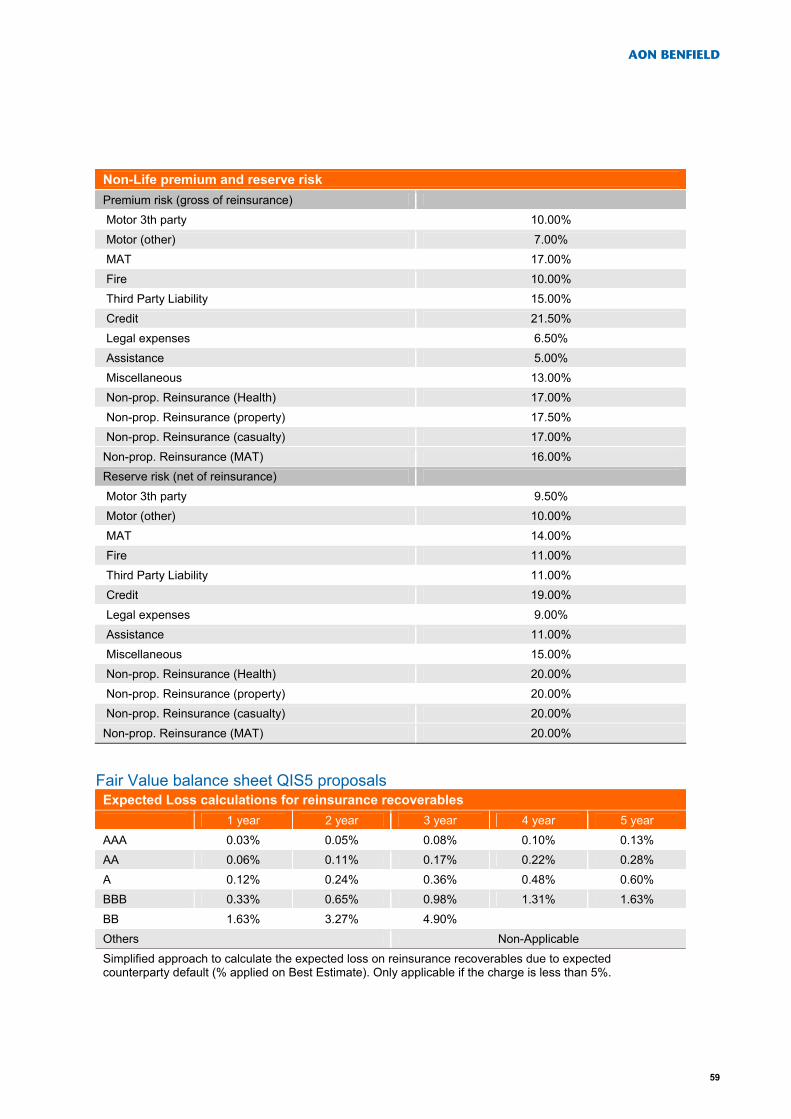

Table of QIS5 parameters 56

Contacts 61

3

SOLVENCY II FOR REINSURANCE MANAGERS

Solvency II – 10 key facts 1. Solvency II is a law replacing Solvency I (1973) which is being introduced by the Committee of

European Insurance and Occupational Pensions Supervisors (CEIOPS) to harmonise insurance risk management practices across Europe.

2. It is expected to take effect in October 2012 but re/insurers across the European Union should take action now if they want to be compliant in time for its inception.

3. Solvency II is a risk-based approach to required capital that demands insurers develop robust risk management practices. It is regarded as state-of-the-art by regulators globally.

4. Solvency II is similar to the Basel II banking regulation by way of its three-pillar approach – Pillar 1 being the quantitative calculation of required and available capital; Pillar 2 the qualitative justification to the regulator (own risk and solvency assessment), and Pillar 3 the disclosure requirements to all stakeholders.

5. For the first time, insurance companies will report on a Fair Value basis, which will impact balance sheet valuations of reinsurance assets and liabilities. Reinsurance assets will be valued on a (discounted) best estimate basis, allowing for an expected loss and accounting for reinsurer ratings.

6. Under Solvency II, all re/insurers will be required to calculate a regulatory capital amount based on a Standard Formula (using standard parameters or company-specific parameters), or an alternative capital amount based on a partial internal model or a full internal model.

7. Natural and man-made catastrophe risk is calculated in the Standard Formula via a complex spreadsheet based on CRESTA zone exposures (natural catastrophes) or via scenarios (man-made catastrophes). Output from commercial catastrophe models will only be accepted through a (partial) internal model. Insurers will be able to apply their own existing (catastrophe) reinsurance programme and will have to show the regulator how they apply this to arrive at net exposures. Both proportional and non-proportional reinsurance for insurance companies are adequately reflected in the Standard Formula for cat risk. Companies with material cat exposures outside the EU will be forced into a partial internal model.

8. The risk and capital mitigating effect of reinsurance in the ‘required capital’ calculation will be allowed only if the reinsurance counterparty has a Solvency II ratio above 100% (or equivalent if supervised by a Solvency II-equivalent regulatory system). Non-Solvency II-equivalent counterparties require a minimal rating of BBB (stable) provided by an external rating agency.

9. Although the Solvency II framework directive was approved in April 2009, there is still uncertainty regarding the calculation of required capital and the allowance of available capital. A QIS5 exercise will take place between August and November 2010 to analyse CEIOPS’ 15 April 2010 proposal. The results of this exercise will be used to finalise the Level 2 implementation measures that, together with the Solvency II Directive, will form the final legal framework.

10. Solvency II is likely to result in a significant increase in regulatory capital for most companies in the market. This is especially true for reinsurers, owing to the nature of the business they underwrite. Some of this increase will be offset by an increasing amount of available capital as a result of Fair Value estimates of liabilities, including discounting. Overall, we estimate that the average solvency ratio for the Non-Life industry will reduce from about 250% (Solvency I) to about 140%.

4

AON BENFIELD

The 4 ways we are helping our clients 1. Reinsurance optimisation: We optimise our clients’ reinsurance programmes so that their capital

requirements are brought in line with the risk appetite and the capital structure of the company.

2. Capital advisory: We guide our clients through the calculation of their Solvency II capital requirement under the Standard Formula in order for them to be fully compliant and knowledgeable, and have their systems ready by 2012. In addition, we perform sensitivity analyses to help them better understand the key drivers of required capital under the new framework.

3. Internal model development: Together with Aon Benfield’s sister division, Aon Global Risk Consulting (AGRC), we help our clients to design and implement an internal model which allows their company to gain insight into the risk and capital position of its balance sheet in a Fair Value world. We can assist in calibration and provide market benchmark data. We compare these results to those that would be achieved under the Standard Formula and assess the impact of their business decisions on capital. We provide a soundboard for specific issues regarding Solvency II and calibration.

4. Risk advice via Aon Global Risk Consulting: We advise our clients on how to derive value from embedding risk management within an organisation, and support them in their Pillar 3 reporting requirements to regulators.

The 3 key questions for our clients • Can I produce my Solvency II Fair Value balance sheet on a quarterly basis, and do I have the

sufficient quality of historical data valued on a one-year Fair Value basis? • Should I use an internal model and how can it help me to calculate the Solvency II capital

requirement, Own Risk and Solvency Assessment (ORSA), risk limits, and Solvency II disclosures? • How do I ensure that my current reinsurance programme is optimised to reduce my capital

requirements under the new Solvency II regime?

5

SOLVENCY II FOR REINSURANCE MANAGERS

FAQs by reinsurance departments on Solvency II 1. Will surplus decrease from Solvency I to Solvency II and can reinsurance help the situation?

We expect that the surplus, or Solvency Ratio, for Non-Life insurers (Available Capital / Required Capital) will fall from around 250% on average under Solvency I to around 140% under Solvency II.

Reinsurance is an efficient way to reduce both earnings volatility and capital requirements, and it will play a more important role under Solvency II than Solvency I – reinsurance credit is much more explicit than it used to be except for quota share reinsurance, for which the effect is largely unchanged.

2. Will the Solvency II regime really begin in October 2012?

Recent comments by some European regulators suggest it may be delayed – but only slightly. We would expect that Solvency II will apply from 1 January 2013, and so 2013 will be the first year for the new rules, and reporting will start based on Q1 2013 figures.

3. Will QIS5 be the last QIS exercise?

In its cover note accompanying the QIS5 technical specifications, the European Commission (EC) explicitly states that the exercise is designed to ‘test the impact of the new regime’. The current QIS5 specifications are less onerous than the proposals made by CEIOPS, and were welcomed by the industry, which feared that the proposals made by CEIOPS in its ‘final advice’ would lead to a dramatic increase in required capital (especially for Life-oriented companies). Since its release in mid-April, sharp comments were raised by CEIOPS (threatening the use of capital add-ons), rating agencies, and investment bankers, that the current proposal was too soft. Certainly, the elements defining Own Funds (VIF, deferred tax assets, hybrids and intangibles) and its classification of the different Tiers, were said to be overly generous to the industry, and would increase the volatility of available capital. This would harm the sector since it would not lead to greater transparency, which would have a knock-on effect on the cost-of-capital the industry is valued on.

The EC is trapped with the timeframe of the Level 2 implementation measures which have to be delivered by early 2011. This does not provide any room for future QIS exercises other than to fine-tune or test the Level 2 implementation measures. We assume that in the current QIS5 exercise enough data will be gathered from the industry to test the likely impact not only of the current proposal but also any modifications that the EC might suggest in its final advice. This is why it is extremely important that the participation rate in QIS5 is significant and provides an adequate representation of the market (although the 60% participation rate seems ambitious – 3,000 insurers vs. the 1,061 that participated in QIS4). It does seem likely that CEIOPS or the EC will push for a dry run on Solvency II in 2011 to test the final proposal one year before the legislation is enacted.

4. Can Aon Benfield assist in calibration of the Undertaking Specific Parameters?

Aon Benfield has an impressive market share across Europe and is heavily engaged with many clients on the calibration of Undertaking Specific Parameters, utilising our vast market knowledge in a confidential manner.

5. How will catastrophe reinsurance programmes impact required capital under Solvency II?

Under the Standard Formula approach, the required capital for natural and man-made catastrophe risk will be calculated through standardised catastrophe scenarios per country (based on CRESTA zone exposures or using man-made scenarios) or, if not relevant, by using a factor approach (a function of net premiums).

6

AON BENFIELD

In the first approach, the resulting figures will be gross of reinsurance and so re/insurers can subsequently apply their reinsurance programme to the calculation. The onus will be on the re/insurer to document and explain to the regulator how the net capital figure was derived. In this way, we would expect the mitigating effect of catastrophe reinsurance to be relatively well accounted for.

However, the most accurate approach will be to use an internal model as this will allow the re/insurer not only to reflect their true exposures (based on street level data if available) but also to adequately calculate the mitigating effect of all possible reinsurance programmes.

6. Can ReMetrica be used to build an authorised Solvency II internal model?

ReMetrica is the best platform for building a full or partial internal Non-Life capital model. Using the ReMetrica platform, Aon Benfield has developed S2Metrica – a tool that offers re/insurers insight into the benefits of an internal model at minimal cost. Essentially the tool uses the QIS4 spreadsheet to build the framework for an internal model, allowing the user to change a number of parameters, such as the reinsurance programme and asset mix. Updates on future Standard Formula templates will be taken into account into new releases of S2Metrica.

The output from S2Metrica is very straightforward and highlights the difference in capital requirement under the Standard Formula versus an internal model. The user can also compare results by Line of Business and review Profit & Loss accounts for different return periods. S2Metrica also contains an Economic Scenario Generator (ESG).

The tool allows companies to decide where to focus their efforts in building partial internal models.

7. What solutions are being provided by the reinsurance market for capital relief?

The most capital efficient reinsurance products include non-proportional catastrophe covers and traditional excess of loss contracts. We also see an increased interest in proportional reinsurance (quota share), even though it is not always the most efficient economically. Given that capital is now based on volatility of assets and liabilities and how both sides of the balance sheet interact, re/insurers will also be considering Loss Portfolio Transfers (LPTs), Adverse Development Covers (ADCs), Out-Of-The-Money Stop Loss solutions, and surplus relief transactions for Life insurers, to name but a few. Hedging of asset risk exposure will also gain importance. Aon Benfield has dedicated teams focusing on each of these solutions and their benefits under Solvency II.

8. Will commercial catastrophe models still matter under Solvency II?

They most certainly will, and the role of Aon Benfield as “the” catastrophe modelling expert in the market will become significantly more important for the following two reasons:

(i) Insurers will develop and seek approval for an internal model under Solvency II. Commercial catastrophe models provide a more adequate assessment of the exposure to catastrophe risk, as unlike the Standard Formula, they take more factors into account than just sum assured and CRESTA zones. Varying data quality, adequate damage functions and the specific characteristics of a client portfolio are important factors that can cause significantly different results. Therefore most insurers will seek to develop a tailored model that provides more relevant results.

(ii) Companies will be required to explain the output of their catastrophe models to the regulator, in line with Pillar 2 (quantitative requirements by the regulator). Even if companies do not submit an internal model for natural catastrophe exposure, they will still have to explain their understanding of these risks to the regulator. Aon Benfield’s unsurpassed knowledge around the strengths and weaknesses of each of the commercially available catastrophe models will prove invaluable to our clients in these discussions.

7

SOLVENCY II FOR REINSURANCE MANAGERS

Executive summary These days, the Solvency II Directive seems to be full of contradictions.

Although both CEIOPS and the European Commission (EC) have now proposed their views on the Level 2 guidance, the expected outcome of the Level 2 implementation measures due in Q1 2011 is less clear than ever before.ItisindeeddisappointingtoseethediscrepancybetweentheCEIOPSandECreportsinAprilonhowtheStandardFormulawillimpactcapitalrequirements.We can only hope that the data retrieved from the QIS5 exercise will be of sufficient quality and granularity that it can also be used to test the final Level 2 advice the EC will have to provide by early 2011, since it is everybody’s expectation that the current QIS5 technical specifications will be subject to change.

It is indeed remarkable to see how the EC has taken a much softer stance than CEIOPS on capital requirements, and in particular on capital quality. Solvency II should not be the regulatory system that drives the market to massive capital increases – especially given how the industry proved itself resilient to the recent financial crises – but it should aim to become a regulatory framework that is respected by the financial markets and is used internally to drive capital decisions.

Notwithstanding this controversy, the industry seems to welcome the EC’s ‘QIS5 technical specifications’, which, by just using the average of QIS4’s and CEIOPS’ factors (e.g. for Asset Risk and for Premium and Reserve risk), represents a significant compromise compared to the factors proposed by CEIOPS.

For non-proportional reinsurance, the new Standard Formula looks particularly flawed. CEIOPS and the EC each came up with their own approach to calculate the net-to-gross ratio, and we will prove in this document that both approaches are completely missing the point.

The deadline for implementation is approaching fast, and we see little appetite by the EC to change the current timing. CEIOPS is pushing the industry to participate in QIS5, a major exercise to test the current proposals which takes place between August and November 2010, but there is so much uncertainty that many insurers are reluctant to give it more than their ‘best efforts plus a bit’. There are indeed considerable doubts about the insurance industry’s current readiness for Solvency II, as many companies are apparently adopting a ‘wait and see’ approach at present.Unlike some regulators, few insurers are able to hire an extra 100 people specifically to address the Solvency II regime.

It is not the supervisor’s intention to send a shockwave through the re/insurance industry that could destroy many business plans by imposing extremely onerous capital requirements. Some serious questions come to mind: Will there be sufficient investor appetite to pump more capital into an industry that could deliver substandard returns? Will Solvency II (or rather the Standard Formula) lead to more earnings volatility? Does the current implied market volatility of insurers compare well with the real volatility? If we take just take one example of a Fair Value assessment by the insurance industry – namely the 2009 Market Consistent Embedded Value (MCEV) report by a major European insurer – which should be the best indicator of the ‘fair’ value of the business, the figure doubled in 2009 after being halved in 2008, which makes it very hard to reward management on the value of the business since the change in value that is due to management action is very limited while the volatility is huge. Although the value for Life businesses is largely driven by asset risk, we would expect a matched (and hedged) balance sheet to have less volatility.

The whole Solvency II system hinges on the credibility of the regulators, which should be responsible for training the industry. However, it appears that most of them are seriously struggling to keep up. How many regulators understand the true model and calibration-related issues they are asking from the re/insurance companies they are supervising? Regulators should be staffed and trained to allow for internal model approval within a period of six months. How many regulators in the EU are currently ready to take up this exercise? If regulators go by the book, we cannot see how they will cope with Pillars 1, 2 and 3. The only way forward seems to be a pragmatic approach focusing on what really matters for insurers – namely providing adequate insurance cover to clients at a reasonable price and with sufficient security.

8

AON BENFIELD

Let’s also consider some positives: Solvency II should increase transparency (Pillar 3); it will improve risk management (Pillar 2), and it will create a more solid and underbuilt capital base (Pillar 1). Many companies are planning to use internal capital models, which would be much more representative than the Standard Formula, and which would lead in most cases to significantly lower capital requirements (much more in line with expectations) and thus acceptable solvency ratios. Our S2Metrica software tool can ensure that companies hit the ground running.

In this document we have collected a number of articles written by global experts within the Aon organisation.

The first section precedes this executive summary and provides a good overview of the key points insurers should be aware of with regard to the Solvency II regime.

The second section contains many stand-alone articles that can be read independently of each other:

• Solvency II: Can It Deliver? We show how capital requirements compare under different systems and conclude that volatility is likely to increase under a Fair Value approach.

• Treatment of Reinsurance in the Solvency II Capital Requirement. If you want to get up to speed quickly on Solvency II implications from a reinsurance perspective, this is the article to dive in to.

• Reinsurance Under Solvency II – an Exceptional Source of Capital. Several reinsurance solutions exist to optimise your capital position and earnings volatility in a Solvency II context.

• The Impact of Solvency II on Risk Calibration. An article that appeared in InsuranceERM and that describes the debate between calibrating to ultimate data versus the one-year approach. Auditability of parameters and process is a key concern for regulators.

• Impact of Non-Proportional Reinsurance on Solvency II Capital. This article compares CEIOPS’ net-to-gross ratio with the AMICE proposal from the EC. Neither makes sense, and the solution should be a partial internal model or Standard Formula with Undertaking Specific Parameters that reflects an insurer’s current reinsurance programme.

• S2Metrica – a New Tool for a New World of Regulation. It is possible to simplify building a full or partial internal capital model for Solvency II. Our S2Metrica tool will quickly make that clear.

• The Rating Agency Perspective. Which will be larger, the Solvency II capital requirement or the rating agency version? Rating agencies will surely continue to play their role.

• Challenges for a Captive Audience. Captives can be efficient risk transfer vehicles but they seem to have been forgotten in the progress of Solvency II. Can all captives afford to build internal models?

• IFRS and Solvency II – the Wobbling Road to Divergence? At some point IFRS will also dictate Fair Value liabilities. However, current discussions between the IASB and the FASB seem to be diverging. Will the end result be compatible with the Solvency II Fair Value approach?

We end the document by summarising factual QIS4 information and our recent discussions with regulators on a per country basis, and provide a glossary of Solvency II jargon.

Despite concerns, we believe that Solvency II represents an important step forward for the European Union and the insurers therein, as well as for the global re/insurance industry in general, where individual jurisdictions will be striving to attain Solvency II ‘equivalence’ status in order to maintain a steady flow of business with their EU peers. The re/insurance industry may have been relatively unaffected by the financial crisis compared to the losses suffered by other financial institutions, but this doesn’t mean it should cease to strive for a system that should ultimately enhance its long term stability. A common, risk sensitive platform will provide even greater assurance to the end customer, while allowing enough flexibility for insurers to continue to innovate to the benefit of the industry and their clients.

We see reinsurance, and to some extent the capital markets, playing a more important role as the most efficient way for the re/insurance industry to transfer volatility at an attractive cost of capital.

Enjoy the read.

9

SOLVENCY II FOR REINSURANCE MANAGERS

Solvency II: can it deliver? When Solvency I was introduced in Europe in 1973, capital was not a concern for European insurers – there were enough buffers in the balance sheet to manage earnings and produce stable results. However, accounting rules have since evolved and with the imminent introduction of Solvency II and IFRS Phase II, earnings volatility is now a key concern of most CEOs.

Much has been written over the past few years about the potential ramifications of Solvency II across the European Union, and while some of the text has been conjecture, we are now within touching distance of a solid framework and the reality of what the protocol will mean for thousands of insurers across the continent.

The impact of Solvency II on the reinsurance community has been less well documented, but it is certainly a topic worth exploring. Under Solvency II, reinsurance will no longer be seen as budgeted expense, but as an efficient form of intelligent risk transfer that can significantly benefit insurers’ Return on Equity (RoE), as well as reducing their earnings volatility.

Although the Solvency II Framework Directive was agreed in 2009, the so-called Level 2 implementation measures are still undecided. These implementation measures are extremely important since they will operationalise the Directive and will define the final parameters and methodologies to calculate the required and available capital. CEIOPS conducted a thorough exercise in close collaboration with the insurance industry during 2009 to obtain a first working proposal for these Level 2 implementation levels. This proposal was adjusted by the European Commission (EC) and a new Level 2 document has been created which will form the basis for the QIS5 exercise that will take place from August to November 2010. The conclusions from QIS5 will be published by the end of April 2011, and will be used to make amendments to the final Level 2 proposal that will be delivered by the EC in early 2011.

QIS5 will provide a good insight into the amount of work it will take for insurance companies to become Solvency II compliant by year end 2012, and it is also the first test that will reflect the revised capital charges after the recent financial crisis.

The new proposal from the EC differs from the work produced by CEIOPS in 2009/10, and the following graph compares the effect of all the various proposals that have been discussed so far.

Evolution of capital requirements for a Non-Life insurance company (based on actual case study)

0.050.0

100.0150.0200.0250.0300.0350.0400.0450.0

Solvency I

S&P BBB

QIS 4 SF

QIS 4 SF (USP premium)

SF CP's January 2010

SF CEIOPS 04/10

SF (USP premium) CEIOPS 04/10

QIS 5 04/10

QIS 5 04/10 USP premium

Internal model

Available

Required

Capital reliefthroughreinsurance

Source: Aon Benfield

10

AON BENFIELD

The graph details the various options of calculating Solvency II required capital. Note that the QIS5 available capital, for reasons of practicality, has not been recalculated and is similar to QIS4 although the quality of the available capital (Tier 1 to Tier 3) will be different (e.g. profit from tacit renewals and multi-year contracts can be included). In particular, for Life insurers there are some serious differences in opinion between CEIOPS and the EC in relation to the tiering of capital, e.g. the treatment of Value of In-Force (sometimes known as In-Force Cash Flows). This discussion will also be relevant for Non-Life lines of business with high persistency rates. In this paper we will not dwell on the tiering of capital. For people interested in this discussion, we would refer to equity research by Citi which goes into a lot more detail on this topic.

Solvency I Provided as a reference number S&P BBB Provided as a reference number QIS4 SF Standard Formula result under the 2008 QIS4 conditions QIS4 SF (USP premium) Standard Formula result under the 2008 QIS4 conditions with premium standard

deviations replaced by Undertaking Specific Parameters (pre-described method) SF Consultation Papers January 2010

Standard Formula result using the parameters released by the Consultation Papers prior to January 2010

SF CEIOPS 04/10 Standard Formula result using the parameters from the CEIOPS April 2010 calibration of Non-Life premium and reserve risk standard deviations

SF (USP premium) CEIOPS 04/10

Standard Formula with premium standard deviations replaced by Undertaking Specific Parameters (using Consultation Paper75 method 1)

QIS5 SF Standard Formula result according to QIS5 based on the QIS5 technical specifications

QIS5 SF (USP premium) Standard Formula result according to QIS5 based on the QIS5 technical specifications with premium standard deviations replaced by Undertaking Specific Parameters

Internal model The result of an internal model that fully covers the risk mitigating effects of the reinsurance programme in place and management actions

Under the current Standard Formula proposed for QIS5, the insurer’s solvency ratio would fall significantly, as per our specific example, from about 250% under Solvency I to about 115% under Solvency II (versus an estimated industry average of 140%) – which seems rather punitive given that no pure insurer failed during the financial crisis. While raising additional capital will be one way for insurers to maintain business volumes, a second option is to transfer risk and thus reduce capital requirements significantly. This can be achieved through an effective and appropriate reinsurance programme that would allow insurers to pursue growth opportunities rather than stagnate.

Across Aon’s various divisions we have teams of colleagues analysing the potential impact of Solvency II on our clients’ businesses and offering advice on the most appropriate risk transfer initiatives. We have been looking at how we can simplify their Solvency II workloads, and have created a new tool, S2Metrica, which assists them in creating an internal model in a very short timeframe.

Insurers will also be able to model their existing reinsurance programme, and assess its efficiency under Solvency II. Seeing the QIS5 proposal, it is unclear if non-proportional reinsurance will be adequately reflected in the final Level 2 Standard Formula except for catastrophe risk, and so many insurers may face higher capital requirements than would be a true reflection of their exposures. Therefore, and in addition to our role as a reinsurance intermediary, we are helping our clients with their internal models and simplifying the whole Solvency II universe for them in order to obtain a well-balanced (partial) internal model providing credit in line with the risk that is transferred.

11

SOLVENCY II FOR REINSURANCE MANAGERS

The Solvency II regime will also increase the need for insurers to understand solvency capital relief when valuing reinsurance. It will become more important and more challenging than has been the case historically to purchase the optimal reinsurance structure in line with Solvency II’s balance sheet risk management approach. Chief risk officers will have an important role to manage risks according to the insurer’s risk appetite and risk tolerance, and ensure that the risk risk transfer policy encapsulates all business risks. Across Europe there is a trend of more risk managers appearing, but the formal CRO role is still to be filled for many Continental European insurers.

Solvency II will impact each re/insurer differently. The real value in understanding the regulatory capital saving from particular reinsurance contracts will be from dissecting each individual company’s balance sheet. Although some broad trends have become apparent from the Standard Formula, there will be opportunities for companies to fine tune their balance sheets to optimise capital efficiency.

Catastrophe exposure is often a key driver in the regulatory capital calculation. Under QIS4, Non-Life companies could derive their catastrophe risk capital charge using one of three options: a factor based approach, a scenario based approach based on regional scenarios, and a personalised scenario based approach. This will change under QIS5, and companies will be forced to choose between standardised scenarios and a factor based method. A Catastrophe Task Force has been established to ensure that the calibration of the scenarios is harmonised. Personalised scenarios, which effectively mean using the commercial catastrophe models, can only be taken into account via a partial internal model. We fear that under QIS5, there will still be a discrepancy between the real catastrophe risk exposure and the simulated exposure from the Standard Formula. However, using efficient reinsurance, companies should still be able to manage their catastrophe risk exposure in line with their overall risk appetite. The design of the catastrophe component in the Standard Formula is created in such a way that it will allow for all risk mitigating effects of reinsurance (even multiline stop loss will be allowed) and hence limiting the catastrophe exposure in the capital calculation to the aggregate limit net of reinsurance. Re/insurers will have to explain and document to the regulator how they moved from the gross capital requirement to the net capital requirement.

For other Non-Life risks, non-proportional reinsurance has been introduced in the current proposal of the QIS5 technical specifications, but it is uncertain whether and how this will be the case in the final Level 2 guidance. Where companies have extensive non-proportional reinsurance programmes and want to benefit from the possible capital relief, a (partial) internal model or applying the Standard Formula with Undertaking Specific Parameters can offer an alternative. Although some companies may respond by buying less non-proportional reinsurance when limited credit is given and only buy more where they achieve full regulatory capital benefit, we believe this is a short-term view and not supported by economic risk management principles. Indeed, reinsurance purchasing for many companies will continue to be influenced or even determined by rating agency requirements rather than economic capital views.

In a Fair Value world, both available and required capital will become more volatile. History proves that this has always been the case. The only difference that Solvency II will bring is that the figures will need to be calculated and disclosed. How investors will look at insurance companies in a Solvency II era is still unclear and will depend on whether the volatility disclosed is higher or lower than what is currently assumed by the markets. Solvency II will certainly bring capital – and all the elements that can create or destroy it – to the people in a much more harmonised way than in the past. For sure, this will have an impact on management, the product department, the reinsurance department, the actuaries, and – due to its one-year risk approach – also to accountants who will favour the balance sheet to balance sheet approach. In fact, Solvency II will touch all those involved in the insurance business.

12

AON BENFIELD

Treatment of reinsurance in the Solvency II Capital Requirement The principles behind Solvency II are about understanding the risks inherent in the business and understanding how those risks contribute to the capital requirement.

Reinsurance is a tool for transferring risks and hence reducing overall volatility. Depending on the type of reinsurance and the loss-capacity that is transferred, it can have an effect on the volatility of earnings and on the capital the company should hold in order to maintain a sufficient level of solvency or target an adequate rating.

The various options provided under Solvency II to calculate the Standard Capital Requirement (SCR) do not always encompass reinsurance to its full extent.

Companies using the Standard Formula Under the recent QIS5 disclosure for Non-Life risks, the Standard Formula includes a Premium & Reserve component, a Lapse and a Cat component. All components allow including the risk and capital mitigating effect of reinsurance – but not to the same extent.

The Premium & Reserve risk component is conceptually built on a volume and a risk measure (Standard Deviation). The higher the volume and the more risk, the higher the capital requirement will be:

• The volume measure is defined on the Fair Value of outstanding net claim liabilities and next year’s expected net premiums1. Since reinsurance (through ceded premium or a share in the technical provisions) reduces the net exposure, the volume measure is immediately impacted and hence a direct impact on the required capital is introduced.

• The impact reinsurance might have on the risk measure is less obvious and depends on the type of reinsurance. In the current proposal the risk measure is pre-defined both for reserve risk and for premium risk (based on extensive research on European data) on a gross basis. The reserve risk component is netted down to reflect the risk mitigating effect of reinsurance on the development of reserves. This netting procedure was carried out on an average European basis (assuming an average reinsurance programme is protecting prior year liabilities). The premium risk is netted down with a ratio NCRi/GCRi that is calculated on the companies’ data, and which should reflect the risk mitigating effect of non-proportional reinsurance.

The current proposal therefore recognises that both proportional (by reducing the volume measure) and non-proportional reinsurance (by reducing the volume and the risk measure) have a risk-mitigating effect that should be reflected in the Standard Formula. The methodology that has to be used to calculate NCRi/GCRi is, however, still under discussion. The options provided by CEIOPS and by the European Commission (AMICE proposal) are described later in this section.

Perhaps somewhat less logical is the fact that for two companies with the same risk profile, the higher the reserves (technical provisions), the higher the required capital. Although theoretically there should be no difference in the best estimate reserves of similar companies, in practice we observe ranges of about 20% around the best estimate, primarily due to different views on assumptions. Thus a company that is more conservative in calculating its technical provisions, will have a higher capital requirement. This is also the case under Solvency I.

1 The Net premium definition is considered from a Fair Value perspective and not anymore from an accounting perspective (essentially expected pure premium without profit loading).

13

SOLVENCY II FOR REINSURANCE MANAGERS

The Cat component in the Standard Formula covers both natural and man-made catastrophe scenarios. For various reasons, the calculation process will differ from the one used in QIS4:

• Regional scenarios in QIS4 where not always detailed in the same manner by all regulators, leaving room for cherry-picking. The scenarios focused on individual events rather than a possible accumulation of several medium-sized events. Guidance was required on how to integrate all scenarios (since it is unreasonable to assume that all scenarios would impact the undertaking simultaneously).

• Personalised scenarios were considered to be complex, difficult for regulators to judge, and tailored to individual company needs. These were therefore transferred to (partial) internal models.

The Standard Formula will be based on scenarios provided by the Catastrophe Task Force. The final scenarios will be delivered by June 2010 but a first set of events and perils have already been included in the QIS5 technical guidance. The final aim is to have this list updated once every three years. These scenarios, covering both natural and man-made events, will be detailed per peril or event on a gross basis. In case the event is defined as a market event, the market share will be used to derive the company specific loss.

In order to calculate the net effect, a pre-described method is provided but this methodology will probably be expanded by more practical guidance by the Cat Task Force. In case the catastrophe loss is protected by a pool or national arrangement, the effect of this cover should also be taken into account.

Due to its construction around individual catastrophe events, the Cat risk component in the Standard Formula facilitates the use of proportional and non-proportional reinsurance much more than in the Premium & Reserve component. Aggregate limits & stop loss protections can also be used but the user will have to explain how he has arrived at the net estimation. Clearly, due to the aggregation technique of man-made and natural catastrophes, the possible impact of the scenarios on multiple lines of business, and the introduction of accumulation of events, this net calculation will be a challenging exercise for each reinsurance department that has a aggregate limit protecting their balance sheet exposure.

All these considerations will certainly be welcomed by insurance companies and captives. Due to the inclusion of multiple events in the scenarios, insurers will receive credit for purchasing reinsurance contracts with reinstatements. Solvency II also states that the capital requirement for a particular Line of Business (LOB) cannot exceed the aggregate limit (= net retention, taking into regard the policy limit and the reinsurance limit including the cost of reinstatements). The formula includes, however, a requirement that if one has an aggregate cover in addition to a specific cover for a certain LOB, the aggregate limit cannot always be taken into account to cap the catastrophe event since it might lead to double counting.

In two cases, a factor based method (factors applied on net premium per LOB) will have to be calculated:

• As an interim solution, when there are no standardised scenarios available or are not relevant and a partial internal model is not proportional;

• On a permanent basis, in cases that are clearly specified (e.g. miscellaneous LOB).

Examples of non-relevance of the Standard Scenarios could be:

• Material exposure outside the EU. • Material inwards non-proportional reinsurance. • The scenarios have a footprint (or in general, risk characteristics) which is not applicable

to the company’s exposure (e.g. local risks not corresponding to CRESTA zone aggregates).

Alternatively, higher quality data could be a reason for companies to use a partial internal capital model for calculating the capital requirement in relation to their catastrophe exposure.

14

AON BENFIELD

As part of their ORSA, companies should evaluate whether the standardised scenarios and the range of possible outcomes are applicable to their portfolio. The limitations of such scenarios should be covered as well in the ORSA. In the extent that the risks covered in the scenario deviate significantly from their risk profile, the alternative methods shall be chosen (factor or partial internal model). This will most likely be the case for numerous captives.

Companies using the Standard Formula with Undertaking Specific Parameters Companies with sufficient historical data might conclude that the standard parameters may not fit their portfolio and hence lead to an overstated capital requirement. Under certain conditions, such companies can replace certain parameters from the Standard Formula with Undertaking Specific Parameters (USP):

• Non-Life Premium and Reserve Risk. • Health (not similar to Life) Premium and Reserve Risk. • Health (similar to Life) Revision risk. • Life Revision risk. Indeed, under the Standard Formula approach described above, the (risk) parameters used for calculating companies’ SCR:

• Are calculated on a pan-European basis. • Assume that changes in loss-ratios over time (used in the calibration process) were triggered by

the volatility in losses and not by premium rates (and hence no allowance was made for the possible effects of underwriting cycles).

• Are independent of the size of the company and hence assume that large, medium and small insurance portfolios will all show the same volatility of loss ratios and technical provisions as time goes by.

• Assume an average historical inflation. • Do not always reflect the true impact of reinsurance on the capital (only the effect of working layers

is taken into account for a limited time period of three years under the CEIOPS proposal). In order to be allowed to use USP, supervisory approval is required and supervisors will focus on the quality of data and the (pre-described) techniques used to recalculate the parameters in the Standard Formula based on the company data. The replacement of the standard parameters in the Standard Formula has to be justified by demonstrating that the estimation based on the internal data is more appropriate for the company's risk profile than using the standard market assumptions.

Historical net loss-ratios used in the calculation are allowed to be recalculated on an as-if basis, hence reflecting the current reinsurance programme. At least five years of historical Fair Value calculated loss-ratios have to be available in order to obtain supervisory approval and, in case the data is influenced by a cycle, the full cycle should be included in the calculation. This will certainly limit the use of this technique in the early years when Solvency II becomes active, unless companies begin to prepare themselves.

Large to medium companies with an adequate history of calculating best estimate provisions and a procedure to compare these against experience (as required by the Solvency II Directive), will benefit the most from this USP-approach since the current risk measures in the Standard Formula are probably more tailored to smaller portfolios, which can benefit less from diversification benefit as only best estimates will be allowed in the calculation process.

15

SOLVENCY II FOR REINSURANCE MANAGERS

Companies using partial or full internal models Solvency II encourages companies to understand the true volatility in their balance sheets and the risks that are taken during underwriting. It therefore encourages companies to have (partial or full) internal models. These models should be designed and managed in such a way that risk mitigating techniques (such as reinsurance) can be analysed in terms of their impact on company performance and capital position. By using a partial or full internal model, companies can calculate the full benefit of their reinsurance purchases.

Solvency II goes beyond the pure calculation of the capital required and encourages reinsurance managers to develop and use coherent approaches to analyse reinsurance and implement capital efficient buying strategies that go beyond buying reinsurance according to a pre-defined budget.

Solvency II also encourages considering risk on an enterprise-wide level. This implies that reinsurance managers will be forced to think less in terms of silo based strategies, but more in terms of enterprise-wide capital strategies that can be filtered down to defining capital efficient, class by class, layer by layer reinsurance solutions.

As a result, reinsurers may find they need to become more flexible. The reinsurance market will change and companies will realise that they need more reinsurance in some areas and less in others. If not for regulatory purposes, reinsurance buyers have a strong economic incentive to improve their modeling techniques that will ensure all reinsurance purchases make optimum use of their capital.

This is in line with Aon Benfield’s current integrated capital solutions strategy, and our strategy since 1994 to buy reinsurance as a means of transfering volatility and reducing required (regulatory and rating agency) capital at a cost below a client’s internal cost of capital.

The Consultation Paper (CP) proposals from CEIOPS were never demanding on partial or internal model requirements, but the current QIS5 proposal does require that companies that have material amounts of non-proportional catastrophe inwards reinsurance, or have material amounts of catastrophe exposure outside the EU, apply for partial internal model approval.

Many insurers are enquiring about an internal model. Their nervousness is mostly related to uncertainty about the final Level 2 and Level 3 advice from the EC, and the concern that regulators might not approve the model (because of resource constraints or disagreement on the criteria) so that the Standard Formula would still be the constraint.

16

AON BENFIELD

Reinsurance under Solvency II – an exceptional source of capital In the recent QIS 5 publication of 6 July, the principles below have changed slightly. However, the new text is unclear and the QIS 5 annexes seem to differ at times to the technical specifications.

Risk tolerance Whether reinsurance or capital market covers are bought to cover peak risk for a single line of business, a stop-loss programme protecting the whole book at remote attachment points, or a programme protecting the more frequent losses, they express the risk tolerance the management is (or is not) willing to take on its insurance risks. Those risks that are not in line with the risk tolerance are ceded to the reinsurance market or to the capital markets, and due to the diversification effects the reinsurer or the investors can generate on these risks, it can be done at an attractive price, making it a win-win situation for both parties involved in the transaction.

When the risk is transferred to the external market, the technical insurance risk is replaced by a counterparty risk, but what if the counterparty defaults and it is not able to continue to provide protection?

With this in mind, the regulator has put constrains on the quality of the counterparty and the risk mitigating effects of reinsurance.

Allowance of reinsurance mitigating techniques In the described methodologies to calculate the Solvency Capital Requirement (Standard Formula, Standard Formula with Undertaking Specific Parameters or full/partial internal model), reinsurance is allowed as a risk and capital mitigating technique (reducing the SCR) subject to certain conditions. CEIOPS has chosen to establish a principle-based approach to decide whether a reinsurance contract can be considered in the calculation of the SCR. This should facilitate the ongoing development and evolution of reinsurance risk mitigation techniques.

• Principle 1: Effective risk transfer. The entire relationship between cedant and reinsurer (including legal relationship) should be considered in order to verify whether risk is indeed being transferred. In the case that basis risk is involved (e.g. parametric catastrophe bond), the impact of the cover in the reduction of the SCR shall only be considered when the company is able to demonstrate that the basis risk is not material compared to the mitigation effect. If sufficient risk is transferred then the remaining basis risk shall also be taken into account as an offsetting factor in the SCR calculation.

• Principle 2: Economic effect over legal form. The economic effect of the transaction will be more important than the legal or accounting form. The SCR shall reflect a reduction in capital requirements commensurate with the extent of risk transfer through reinsurance and an appropriate treatment of any corresponding risks that are acquired in the process (e.g. counterparty default risk).

• Principle 3: Legal certainty, effectiveness and enforceability. The risk mitigation should be legally enforceable in all relevant jurisdictions. If reinsurance is used to reduce capital requirements, the SCR should be increased to allow for the possibility that reinsurance protection will not be renewed on expiry or will be renewed on adverse terms. This could be a potential issue for Loss Occurring contracts since they do not always provide protection for the full exposure period that is considered within Solvency II (e.g. in the case of multi-year contracts).

• Principle 4: Valuation. The design of the standard SCR calculation shall recognise reinsurance as a risk mitigation technique in such a way that there is no double counting (e.g. through overlapping local and umbrella covers). Where the reinsurance risk mitigation technique actually increases risk, the SCR shall be increased.

• Principle 5: Credit quality of the provider of the reinsurance risk mitigation instrument. – Reinsurance bought at entities that are Solvency II compliant and which have a solvency ratio

(own funds / SCR) below 100% should not be recognised as risk mitigating.

17

SOLVENCY II FOR REINSURANCE MANAGERS

– Reinsurance bought with entities that are not Solvency II compliant but have an equivalent regulatory system, a likewise approval will be required: reinsurance risk mitigation in the calculation of the SCR is only allowed if the equivalent Solvency ratio of the counterparty is greater than 100%.

– Reinsurance bought with entities that are not Solvency II compliant nor operate under an equivalent regulatory system, will have to have (or demonstrate the capability) at least a BBB (stable) financial strength rating with a regulated rating agency. The rating agency should be compliant with the Regulation on Credit Rating Agencies.

– SPVs will also be subject to limitations, and additional reporting requirements are defined in order to ensure that the supervisor of the SPV has all the information required to make an approval decision in line with Solvency II Level I. Only supervisors can give approval.

It is important to note that for European reinsurers and reinsurers operating in a Solvency II equivalent system, the Solvency ratio will prevail over the financial strength rating.

Counterparty default risk (e.g. introduced by means of reinsurance) Insurance companies can be subject to various forms of counterparty default risk. Most of the default risk is embedded in the investment book (corporate bonds, credit spreads…) but in addition, reinsurance introduces a counterparty default risk to the reinsurer (both to the claims he is covering as to the protection he is providing). Also, policyholders and intermediaries (unpaid premium) cause a counterparty default risk.

The counterparty default capital calculation in the Standard Formula was largely criticised after QIS4 due to the technical difficulties in the calculation approach and the minor effect it had where the portfolio was well diversified with counterparties (both in number of counterparties as well as in their ratings). Many adjustments and simplifications were made in the new formula that will be tested in QIS5 but unfortunately the financial crisis has also shown that counterparty default has characteristics of tail dependency which impacts the framework of the Standard Formula. Both the structure and the scope of the counterparty default calculation have substantially changed in QIS5 compared to QIS4, and the effects of the crisis are clearly visible. New features in the QIS5 counterparty risk module are as follows:

• Some contracts (mostly Life) offer policyholder guarantees that are provided by third parties (e.g. investment bank Lehman Brothers). If the insurance company is held liable for these guarantees, in case of default of the third party the guarantees should be treated like derivatives in the calculation of the counterparty default risk module.

• Off-balance sheet guarantees, letters of credit, and letters of comfort provided by an insurance company which depend on the credit quality of the counterparty, will need to be taken into account. In case the counterparty approaches default, the guarantee will turn into a liability and therefore these instruments are included in the Standard Formula module of counterparty default calculation.

• The model structure also includes a random shock variable that affects all counterparties due to a similar event (e.g. financial crisis, major catastrophe).

• Observed recovery rates of defaulted securities like CDOs are substantially lower than assumed under QIS4.

• The look-through-approach (available in QIS4) is not allowed anymore. Where reinsurance was centralised and risks (partly) retroceded, the operating companies could calculate the counterparty default risk charge using the rating of the retrocessionaires for the share of the recoverables that were retroceded (look-through-approach). Where the risk was fully transferred (100% retroceded) it implied that the operating companies could use the rating of the external counterparties, implicitly assuming that capital flows within the group were unrestricted. The financial crisis has shown that the above is certainly not the case in times of distress and therefore these approaches will not be allowed in QIS5.

18

AON BENFIELD

The new proposed framework makes a distinction between Type 1 and Type 2 exposures:

• Type 1 exposures include all counterparties that can be individualised and where an external rating is likely to be available. These include counterparties from reinsurance arrangements, securitisations, derivatives, cash at bank, deposits, called up but unpaid capital, letters of credit, initial funds, guarantees, and letters of comfort which the company has provided and which depend on the credit standing of the counterparty.

• Type 2 exposures include grouped, diversified counterparties which are usually unrated. These include receivables from intermediaries and policyholder debtors.

Normal counterparty default calculations only focus on the loss that the insurer’s balance sheet would take in the case of counterparty default. However, a defaulting reinsurance company has a double effect on an insurer’s balance sheet. On the one hand, the share that the reinsurer had in the insurer’s outstanding gross claims becomes unrecoverable (if not protected by deposits); on the other hand, the protection he was providing (and its possible reducing effect on the SCR the insurance company had to hold) is not available anymore, which results in an increase in SCR for the insurance company.

The Standard Formula tries to capture all of the above elements in a different approach for Type 1 and Type 2 exposures (less complex for Type 2 than Type 1). Calculations for Type 1 exposures will have to be done per counterparty (or grouped in similar classes with similar probabilities of default), so it will be important for the reinsurance administration to manage counterparty exposures on an individual basis, keeping track of historical commutation (e.g. reinsurance companies that are sold to other reinsurance companies) and whether these belong to the same group. Each Type 1 counterparty will have to be assigned a probability of default and these will be based on information received from rating agencies which will have to detail the accompanying probability of default together with the rating they have given to the counterparty. In instances where a counterparty does not have a rating, it will have to rely on its published Solvency ratio to derive a probability of default. If this is impossible, a probability of default of 10% (corresponding to an S&P rating between B and CCC) will be assigned.

If collateral is provided in relation to the exposure of the counterparty, it can be used to reduce the counterparty default risk under the condition that the custodian holding the collateral is independent from the counterparty and the collateral is valued using a risk-adjusted approach (bearing in mind the market risk attached to the collateral and the credit risk from its exposure to the custodian). As long as the custodian is bankruptcy-removed, it would mean that 85% of the collateral can be used to reduce the counterparty default risk.

Finally, the methodology used to calculate the risk for Type 1 exposures takes into account the number of counterparties involved in the counterparty default risk. Having an exposure to a limited number of counterparties is being penalised in the formula. Without going into detail, one could say that the capital requirement for a well diversified portfolio of recognised capitalised reinsurers can be 40% lower than a portfolio of less diversified counterparties.

The impact of the changing balance sheet on reinsurance under Solvency II In a Solvency II world, reinsurance will not only affect the SCR calculation, but also the balance sheet. Reinsurance assets need to be valued on a Fair Value basis, which includes a best estimate approach for reinsurance recoverables. Given that the reinsurance recoverables might stem from various accident years, all protected by different reinsurance programmes, this calculation will most likely be a non-linear one. The best approach to consider all the options that are embedded in the reinsurance contracts (e.g. stability clause) is to calculate the reinsurance recoverables using a stochastic approach. This is the only approach that will guarantee that the best estimate derived from this approach is truly a best estimate in line with the Solvency II requirements. Practicality and materiality will probably force most companies to use a more simplified approach to calculate the best estimate cash flow of reinsurance recoverables. The Fair Value calculation should also reflect a reduction of the obtained (discounted) best estimate, due to the potential default of the counterparty. Certainly, for long-term liability covers, this might cause a concern if not all historic counterparties have (or no longer have) an adequate rating.

19

SOLVENCY II FOR REINSURANCE MANAGERS

The market value margin will have a direct impact on companies’ net assets. If a company has no proper methodology to calculate the market value margin, it will have to fall back to the simplifications, which have been defined very conservatively (e.g. 8% for MTPL, 10% for GTPL). Companies with an efficient reinsurance programme protecting prior year liabilities should have a much lower MVM since they can use their net exposure in the calculation of the MVM. This will however only be the case if the MVM is calculated in a sophisticated manner taking into account prior year reinsurance programmes.

With Solvency II taking effect in October 2012 as currently planned, some companies will see a step change in the size of the net assets on their Solvency II balance sheet. Rather than looking to raise capital to fund this shortfall, companies may consider reinsurance options to reduce their capital requirement. The types of reinsurance that companies will consider will depend on the specific balance sheet changes that affect them most.

Companies that have been writing particular lines for many years may consider retrospective reinsurance solutions like Loss Portfolio Transfers or Adverse Development Covers on existing reserves to reduce their capital requirement to reduce ‘dead capital’. Other companies that write capital intensive lines may consider purchasing more traditional reinsurance. Also, several companies have been moving towards more enterprise-wide contracts and aggregate reinsurance solutions e.g. Out-Of-The-Money Stop Loss covers.

One thing is for sure, the market is changing.

20

AON BENFIELD

The impact of Solvency II on risk calibration Many companies have invested in building internal models to cover their balance sheet risks over the past few years, sometimes driven by regulatory requirements (e.g. ICA in the UK), and sometimes driven by management or rating. The Solvency II framework introduces the one-year risk framework which might affect the model architecture or the calibration process on these existing models.

Actuaries are puzzled by the one-year risk concept, and existing internal models need to be adjusted to bring them in line with the Solvency II Directive. Meanwhile, managers fear that the theoretical framework will not be in line with the way they have been running their businesses long before Solvency II was spotted on Google.

But is Solvency II actually that different from standard business practices?

Decomposing Article 101 The Fair Value balance sheet is one of the cornerstones of Solvency II, and its impact is not restricted only to the calculation of Fair Value assets and liabilities. The concept of market value margin (MVM), and the related one-year risk approach in the calculation of the Solvency Capital Requirement (SCR), find their origin in this Fair Value-driven approach: re/insurance companies should have enough capital on their balance sheets to cover the risks that can emerge over a 12-month timeframe and allow for a (theoretical) transfer of all (contractual) liabilities at the end of this balance-sheet period. This means that companies have to be able to calculate the impact of such shocks on their end-of-year balance sheets, and value these in such a way that they can be transferred to a third party.

Article 101 of the Solvency II Directive defines the calculation of the SCR and is written in a very concise way, but when one begins to distil the various concepts introduced, it appears to be far more challenging than at first glance. Certainly, for those companies interested in developing a partial or full internal model, a proper understanding of Article 101 and its consequences on model architecture and calibration-related issues is crucial. If one reads carefully, one can separate:

• The ‘shock’ period – this is the period over which a shock is applied to a risk. In Article 101 this is defined as one year. Therefore, only shocks or risks that can occur over the preceding 12 months need to be considered, whether these are shocks that affect the investments (e.g. a change in credit defaults) or shocks that affect the liabilities (e.g. a windstorm).

• The ‘effect horizon’ – the period over which the shock that is applied to a risk will impact the company’s balance sheet. For instance, should a change in legislation become effective during the shock period, this will have a consequence on future claim payments and will impact the valuation of the liabilities. In this case, the effect horizon is the ultimate time horizon of the policy obligations. Likewise, a change in dividend yield will not only have an impact on the dividend expected for the coming 12 months, but will also impact future dividends and hence the valuation of the asset. In Article 101, this definition is included in the valuation of the basic own funds, which are defined as the excess of Fair-Value assets over Fair-Value liabilities.

• The ‘exposure basis’ – this is the exposure that one needs to take into account when applying the shock. In Article 101, this is defined as the existing in-force liabilities at the opening balance sheet, plus the expected exposure from new business written over the subsequent 12 months. In most cases, the exposure basis will include exposure beyond the shock period. This particular exposure does not need to be shocked any more, but the possible impact from the shock occurring during the 12-month period needs to be included in the revaluation of the net assets.

• A ‘risk profile’ – this is the distribution function from which the required capital will be derived. In Article 101, this is defined as the basic own funds. In an internal model it will therefore be crucial to calculate the movement of the basic own funds over a period of 12 months, allowing for a proper valuation at the end of this 12-month period, in line with the exposure the company is expecting to write.

21

SOLVENCY II FOR REINSURANCE MANAGERS

• A ‘risk measure’ – this is the statistical risk measurement applied on the risk profile. This has been set to the value-at-risk approach (VaR).

• The ’risk tolerance level’ – 99.5%.

Impact on internal model kernel When reading the Directive, it would seem that generating an internal model that models excess of assets over liabilities is straightforward, but as soon as one gets into the details, one realises that, among the 80 Consultation Papers (CPs) published so far by the Committee of European Insurance and Occupational Pensions Supervisors (CEIOPS), there is very little guidance on how the requirements can actually be achieved.

A proper understanding of all these elements can make a major difference in the resulting SCR and the way the internal model can be used within the company to define a risk-limit structure and to assist in capital-related issues that management is facing.

The whole idea to focus on a balance-sheet perspective was probably welcomed by those with an accounting background, and it will also facilitate discussions between valuation-related aspects of Solvency II and future International Financial Reporting Standards (IFRS). For most actuaries, however, this approach, and the consequences it brings in terms of calibration of risks, has come as a surprise and is still creating confusion.

Historically, actuaries have calculated premium and reserve-related risks from an ultimate perspective, considering all the shocks that might occur over the lifetime of the liabilities. Now that the regulatory regime becomes truly risk sensitive and regulators’ work becomes more important, does this approach suddenly become less appropriate?

Risk-takers tend to calculate risks not only up to the end of the first year, but until the full development of risks. This is normal since the price should cover the full risk period, not only the first 12 months. The MVM is the glue that combines both visions, but this tends to be so technical that many people lose themselves in over-complicated calculation processes.

Is there actually so much difference between this one-year and ultimate approach? This really depends from which angle you look at the problem. Capital requirements calculated from a one-year risk approach will, in most cases, be lower than when calculated on an ultimate perspective. However, when one looks at the problem from a calculation point of view, the approach taken between a one-year or ultimate basis does not necessarily need to be that different.

The AISAM-ACME study on Non-Life long-tail liabilities in October 2007 raised the alarm that only a few members were aware of the inconsistency that existed between their assessment on an ultimate basis and the Solvency II one-year approach. Since then a number of algorithms have been described in actuarial literature to calculate risks from a one-year perspective. This seems to give the impression that ultimate and one-year are two different approaches. A much more logical approach is to calculate the risks to ultimate and then introduce a second process: How much of the risk (=deviation from the expected value) can be realistically measured over the first 12 months, over the first 24 months, etc., until, at ultimate, all the risk can be measured.

This second process is called the emergence of risk process. Take for example a reinsurer writing long-tail business. The change in the view of the expected ultimate cost of claims over one year could be negligible, but the actual ultimate cost of claims after all liabilities have been extinguished could be very different from the opening view. In this case, the SCR covers the risks emerging during the first 12 months and the implications these might have on the end-of-year valuation, but the MVM covers the risks associated with the settling of liabilities beyond this 12-month period. Or, to be even more precise, the SCR covers the capital required to cushion the risk for the first 12 months, whereas the MVM covers the cost to attract capital to cushion the risk beyond the 12-month period.

22

AON BENFIELD

Example of development table of best estimate ‘ultimate loss ratios’

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 20051993 107.5% 107.5% 115.0% 115.0% 102.6% 95.3% 78.7% 74.4% 78.4% 70.8% 70.4% 66.6% 64.1%1994 107.5% 100.0% 112.5% 112.5% 93.9% 81.6% 80.7% 79.3% 68.3% 63.4% 61.2% 59.6%1995 107.5% 105.0% 120.0% 110.0% 88.0% 84.5% 82.7% 80.7% 80.1% 76.3% 73.6%1996 107.5% 112.6% 112.5% 105.0% 103.5% 101.9% 93.3% 97.9% 96.8% 92.8%1997 112.5% 115.0% 115.0% 115.0% 115.0% 106.7% 110.3% 112.9% 109.9%1998 115.0% 105.0% 110.0% 122.5% 127.5% 142.5% 150.0% 162.5% σ (U,prem,lob)

1999 110.0% 107.0% 105.0% 105.0% 110.0% 140.0% 145.0% = 19,51%2000 105.0% 100.0% 100.0% 107.5% 115.0% 142.5%2001 107.5% 97.5% 97.5% 92.5% 95.0%2002 σ (U,prem,lob) = 13,97% 75.0% 75.0% 70.0% 67.5%2003 70.0% 70.0% 67.5%2004 72.5% 67.5%2005 80.0%

The above table shows the various ultimate loss ratio calculations (measured at different positions in time) per development period for a reinsurer who writes non-proportional business. When considering only the risk that emerges over the first 12 months, the loss-ratio seems to be quite stable across the various accounting years. This probably finds its reason in the fact that not much information is available, and most is based on estimates. Only through the development, information becomes available and the true ultimate loss-ratio (and its movement over time) becomes visible.

As an example the (premium risk) standard deviation suggested in Consultation Paper75 (method 1) was calculated based on the observed ultimate loss-ratio in its first year of development (13.97%) and based on the last known ultimate loss-ratio (19.51%). Clearly, the risk that emerges over the first 12 months is much lower than when considered from an ultimate perspective. The example clearly demonstrates the importance of the various definitions introduced by the Fair Value concept, not only on the calculation of the SCR but also on the MVM. Needless to say, a proper MVM calculation will be important for those companies writing long-tail re/insurance.

Risk emergence patterns Using risk emergence patterns to bridge the link between one-year and ultimate is probably welcomed not only by actuaries but also by management. Actuaries do not have to change their traditional way of working. In order to come up with one-year risk parameters for reserve or premium calculation they can remain working on an ultimate basis, but an additional process will need to be added to derive appropriate parameter inputs for a Solvency II-type calculation. In their expression of the risk appetite, management might not only be interested in covering the capital for the one-year period, but might also be interested in the level of capital required to cover the full run-off.

Emergence of risk through the development period

t=0

t=1 t=2 t=3 (ultimate)

SCR(t=0|t=0) SCR(t=1|t=0) SCR(t=2|t=0)

The above example shows the emergence of risk at the end of various 12-month periods, each showing the position of the ultimate view of loss given a certain ‘state of the world’.

23

SOLVENCY II FOR REINSURANCE MANAGERS

Impact on calibration The Solvency II framework has been established to protect policyholders, and the one-year SCR + MVM approach is an appropriate way of doing so. Companies should be aware, however, that calculating SCR based on an ultimate perspective will lead to a much higher than required capital requirement that provides greater policyholder protection than the regulator is aiming for. Calibration of insurance risk on a total balance sheet approach itself is a quite challenging exercise – certainly in the case where one tries to cover all aspects of the technical insurance both on a gross and net level:

• Premium modelling: large loss, attritional loss, natural catastrophe loss, man-made catastrophe. • Reserve modelling: large loss, attritional. • Counterparty default modelling. The one-year approach and the implications it has on the calibration process creates an additional requirement. But certainly from a use-test perspective, it is much better to re-use existing processes (which mostly deal with ultimate calculations) and append these to introduce the one-year risk approach. The aspects of risk emergence are not restricted to reserve risk only (as is currently discussed in most actuarial literature) but also have important implications on attritional and large loss premium risk modelling, certainly because the emergence of reserving risk between these different capabilities needs to be undertaken on a consistent basis. The icing on the cake is deriving a proper net-of-reinsurance position of the SCR where a clear link with all ultimate calculations is still auditable.

The impact of reinsurance on the risk profile of a company will therefore need to be reconsidered since it will have an effect on multiple levels:

• The SCR – this will be the effect that will be most visible in future Solvency II related capital calculations.

• MVM – reinsurance can protect the business for the full run-off of the claim, and hence will also have an impact on the MVM calculation.

• ORSA (Own Risk and Solvency Assessment) – management should not only look at the capital required to cover the first 12 months but assume a going-concern point of view. In the end, besides some small examples, the insurer tends to take the risk on its balance sheet until it is settled.

24

AON BENFIELD

Impact of non-proportional reinsurance on Solvency II capital Summary When CEIOPS published its methodology for applying non-proportional reinsurance in the Standard Formula in early April 2010, it raised quite a number of eyebrows since it was not discussed in any Consultation Paper (CP). Even greater was the surprise when a week later, the EC published the draft QIS5 rules containing a different methodology developed in conjunction with AMICE – the Association of Mutual Insurers and Insurance Cooperatives in Europe.

On 30 April, Aon Benfield presented its view on both approaches to CEIOPS and the industry; unfortunately, our conclusion was (and still is) not very encouraging. Based on a real example, we can only deduce that both approaches are completely missing their purpose. Neither approach provides adequate capital benefit for non-proportional reinsurance. Perhaps it is time to return to the approach that Aon Benfield suggested in February 2008 to the EC, which suggested granting capital benefit for non-proportional reinsurance in function of the retentions, limits and reinstatement in relation to the company’s overall risk exposure.