south africa, november 2013 - glencoresource: wood mackenzie, ame, company websites, glencore...

TRANSCRIPT

South Africa, November 2013

This presentation has been prepared by Glencore Xstrata plc ("Glencore").

Forward looking statements

This document contains statements that are, or may be deemed to be, “forward looking statements” which are prospective in nature. Such statements are qualified in their entirety by the inherent risks and uncertainties surrounding future expectations. Forward-looking statements are not based on historical facts, but rather on current predictions, expectations, beliefs, opinions, plans, objectives, goals, intentions and projections about future events, results of operations, prospects, financial condition and discussions of strategy.

By their nature, forward looking statements involve known and unknown risks and uncertainties, many of which are beyond Glencore’s control. Forward looking statements are not guarantees of future performance and may and often do differ materially from actual results. Important factors that could cause these uncertainties include, but are not limited to, those discussed in Part III: “Risk Factors” of the pre-listing statement issued by Glencore on 31 October 2013, and under “Principal risks and uncertainties” in section 1.7 of Glencore’s Annual Report 2012 and “Risks and uncertainties” in Glencore’s Half-Yearly Results 2013.

Neither Glencore nor any of its associates or directors, officers or advisers, provides any representation, assurance or guarantee that the occurrence of the events expressed or implied in any forward looking statements in this document will actually occur. You are cautioned not to place undue reliance on these forward looking statements which only speak as of the date of this document. Other than in accordance with its legal or regulatory obligations (including under the UK Listing Rules and the Disclosure and Transparency Rules of the Financial Conduct Authority and the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited), Glencore is not under any obligation and Glencore and its affiliates expressly disclaim any intention, obligation or undertaking to update or revise any forward looking statements, whether as a result of new information, future events or otherwise. This document shall not, under any circumstances, create any implication that there has been no change in the business or affairs of Glencore since the date of this document or that the information contained herein is correct as at any time subsequent to its date.

No statement in this document is intended as a profit forecast or a profit estimate and no statement in this document should be interpreted to mean that earnings per Glencore share for the current or future financial years would necessarily match or exceed the historical published earnings per Glencore share.

This document does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for any securities. The making of this document does not constitute a recommendation regarding any securities.

2

A JSE listing for Glencore

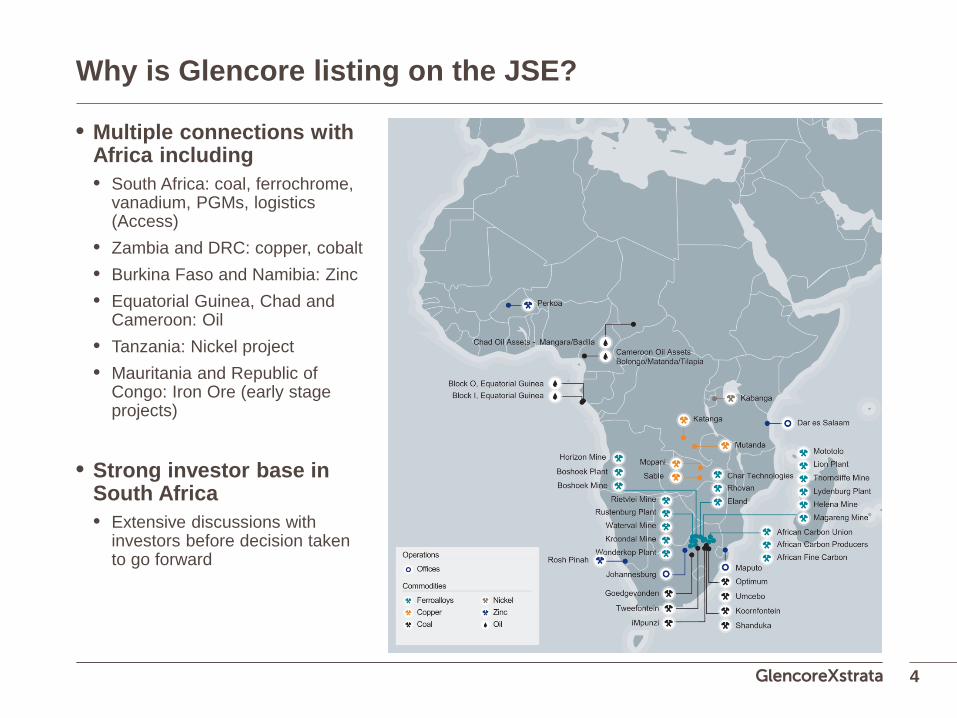

Why is Glencore listing on the JSE?

• Multiple connections with Africa including • South Africa: coal, ferrochrome,

vanadium, PGMs, logistics (Access)

• Zambia and DRC: copper, cobalt • Burkina Faso and Namibia: Zinc • Equatorial Guinea, Chad and

Cameroon: Oil • Tanzania: Nickel project • Mauritania and Republic of

Congo: Iron Ore (early stage projects)

• Strong investor base in

South Africa • Extensive discussions with

investors before decision taken to go forward

4

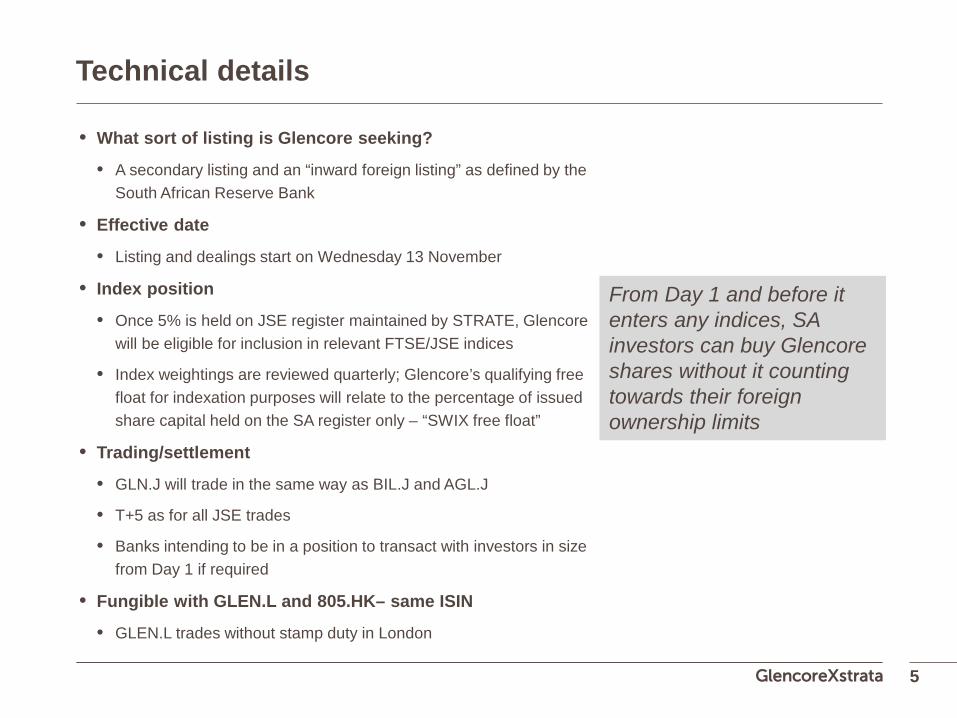

Technical details

• What sort of listing is Glencore seeking?

• A secondary listing and an “inward foreign listing” as defined by the South African Reserve Bank

• Effective date

• Listing and dealings start on Wednesday 13 November

• Index position

• Once 5% is held on JSE register maintained by STRATE, Glencore will be eligible for inclusion in relevant FTSE/JSE indices

• Index weightings are reviewed quarterly; Glencore’s qualifying free float for indexation purposes will relate to the percentage of issued share capital held on the SA register only – “SWIX free float”

• Trading/settlement

• GLN.J will trade in the same way as BIL.J and AGL.J

• T+5 as for all JSE trades

• Banks intending to be in a position to transact with investors in size from Day 1 if required

• Fungible with GLEN.L and 805.HK– same ISIN

• GLEN.L trades without stamp duty in London

5

From Day 1 and before it enters any indices, SA investors can buy Glencore shares without it counting towards their foreign ownership limits

Sector overview

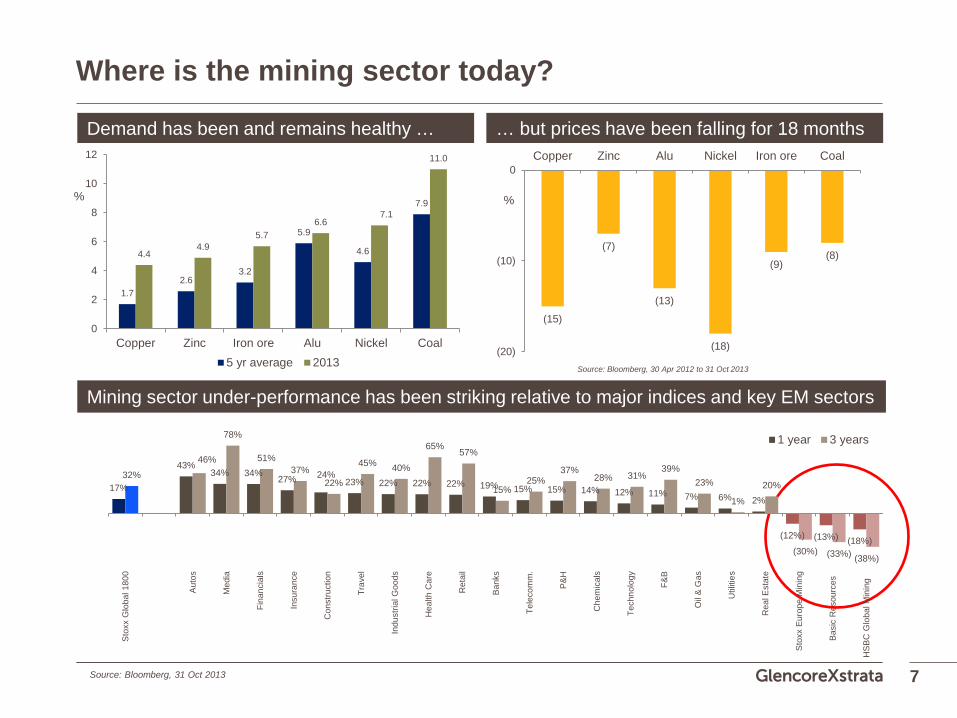

Where is the mining sector today?

7

1.7 2.6

3.2

5.9

4.6

7.9

4.4 4.9

5.7 6.6

7.1

11.0

0

2

4

6

8

10

12

Copper Zinc Iron ore Alu Nickel Coal5 yr average 2013

(15)

(7)

(13)

(18)

(9) (8)

(20)

(10)

0Copper Zinc Alu Nickel Iron ore Coal

Source: Bloomberg, 30 Apr 2012 to 31 Oct 2013

% %

Source: Bloomberg, 31 Oct 2013

Demand has been and remains healthy … … but prices have been falling for 18 months

Mining sector under-performance has been striking relative to major indices and key EM sectors

17%

43% 34% 34%

27% 24% 23% 22% 22% 22% 19% 15% 15% 14% 12% 11% 7% 6% 2%

(12%) (13%) (18%)

32%

46%

78%

51% 37%

22%

45% 40%

65% 57%

15% 25%

37% 28% 31%

39% 23%

1%

20%

(30%) (33%) (38%) -60.00%

-40.00%

-20.00%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Sto

xx G

loba

l 180

0

Aut

os

Med

ia

Fina

ncia

ls

Insu

ranc

e

Con

stru

ctio

n

Trav

el

Indu

stria

l Goo

ds

Hea

lth C

are

Ret

ail

Ban

ks

Tele

com

m.

P&

H

Che

mic

als

Tech

nolo

gy

F&B

Oil

& G

as

Util

ities

Rea

l Est

ate

Sto

xx E

urop

e M

inin

g

Bas

ic R

esou

rces

HS

BC

Glo

bal M

inin

g

1 year 3 years

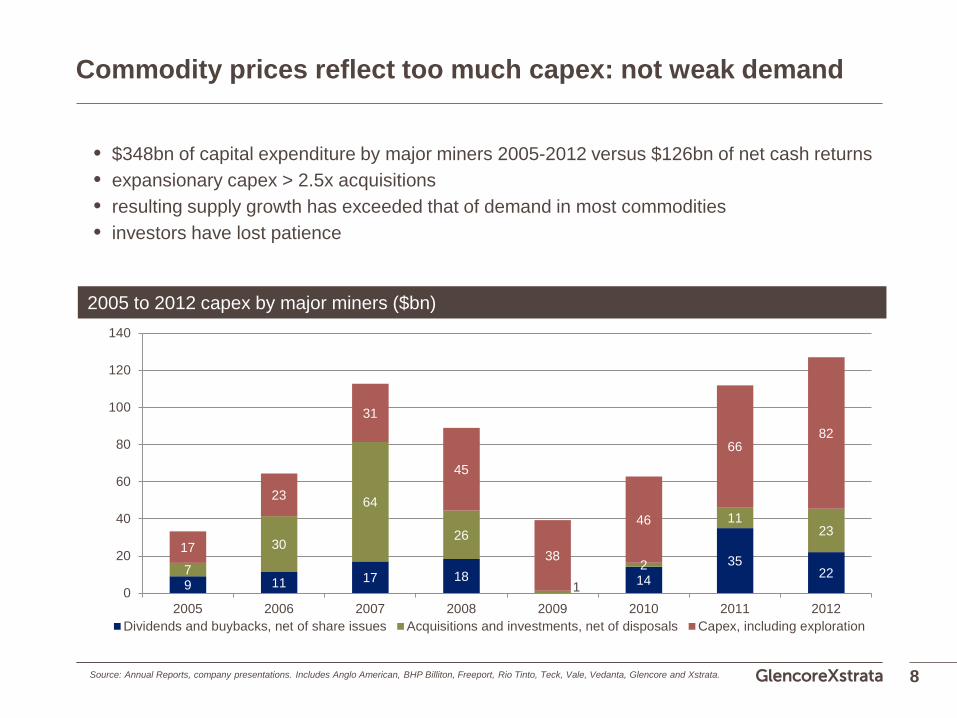

Commodity prices reflect too much capex: not weak demand

• $348bn of capital expenditure by major miners 2005-2012 versus $126bn of net cash returns • expansionary capex > 2.5x acquisitions • resulting supply growth has exceeded that of demand in most commodities • investors have lost patience

8

2005 to 2012 capex by major miners ($bn)

9 11 17 18 14 35

22 7

30

64

26

1 2

11 23

17

23

31

45

38

46

66 82

0

20

40

60

80

100

120

140

2005 2006 2007 2008 2009 2010 2011 2012Dividends and buybacks, net of share issues Acquisitions and investments, net of disposals Capex, including exploration

Source: Annual Reports, company presentations. Includes Anglo American, BHP Billiton, Freeport, Rio Tinto, Teck, Vale, Vedanta, Glencore and Xstrata.

Early signs that the situation may be improving

• Commodities are a key pre-requisite for growth and improving living standards

• Current prices threaten long term supply security in key commodities

• Shareholders have made their priorities clear

• Senior management changes in 2012/3 have enabled enhanced recognition of the issues

• Signs that major producers may be altering their approach

• Shareholders also have a vital active role to play in the evolution towards genuinely sustainable supply/demand balances in commodities and the achievement of appropriate risk/return parameters

• But

• 2011 and 2012 were record years for capex

• Need for constant vigilance

9

Glencore today

Glencore – a unique business model ..

Exploration

Mining / producing

Processing / refining

Logistics

Marketing & trading

Traditional miners Traders

Exploration

Mining / producing

Processing / refining

Logistics

Marketing & trading

Major presence across the entire value chain

11

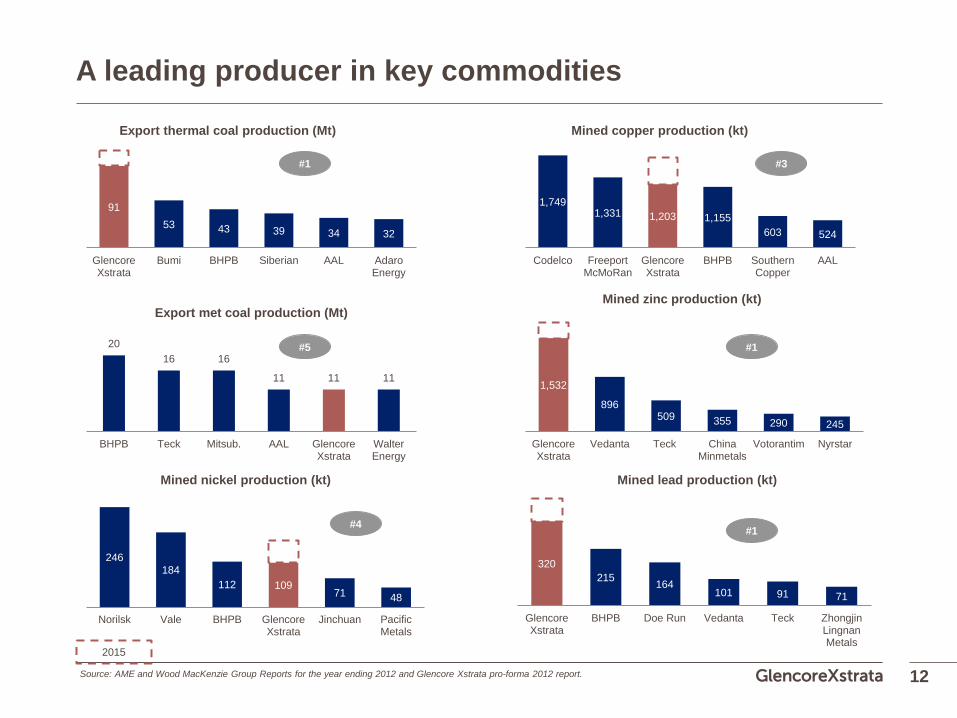

91 53 43 39 34 32

GlencoreXstrata

Bumi BHPB Siberian AAL AdaroEnergy

A leading producer in key commodities

12

20 16 16

11 11 11

BHPB Teck Mitsub. AAL GlencoreXstrata

WalterEnergy

Export met coal production (Mt)

1,749 1,331 1,203 1,155

603 524

Codelco FreeportMcMoRan

GlencoreXstrata

BHPB SouthernCopper

AAL

1,532

896 509 355 290 245

GlencoreXstrata

Vedanta Teck ChinaMinmetals

Votorantim Nyrstar

246 184

112 109 71 48

Norilsk Vale BHPB GlencoreXstrata

Jinchuan PacificMetals

320 215 164

101 91 71

GlencoreXstrata

BHPB Doe Run Vedanta Teck ZhongjinLingnanMetals

Source: AME and Wood MacKenzie Group Reports for the year ending 2012 and Glencore Xstrata pro-forma 2012 report.

#1

#5

#4

#3

#1

#1

Export thermal coal production (Mt) Mined copper production (kt)

Mined zinc production (kt)

Mined nickel production (kt) Mined lead production (kt)

2015

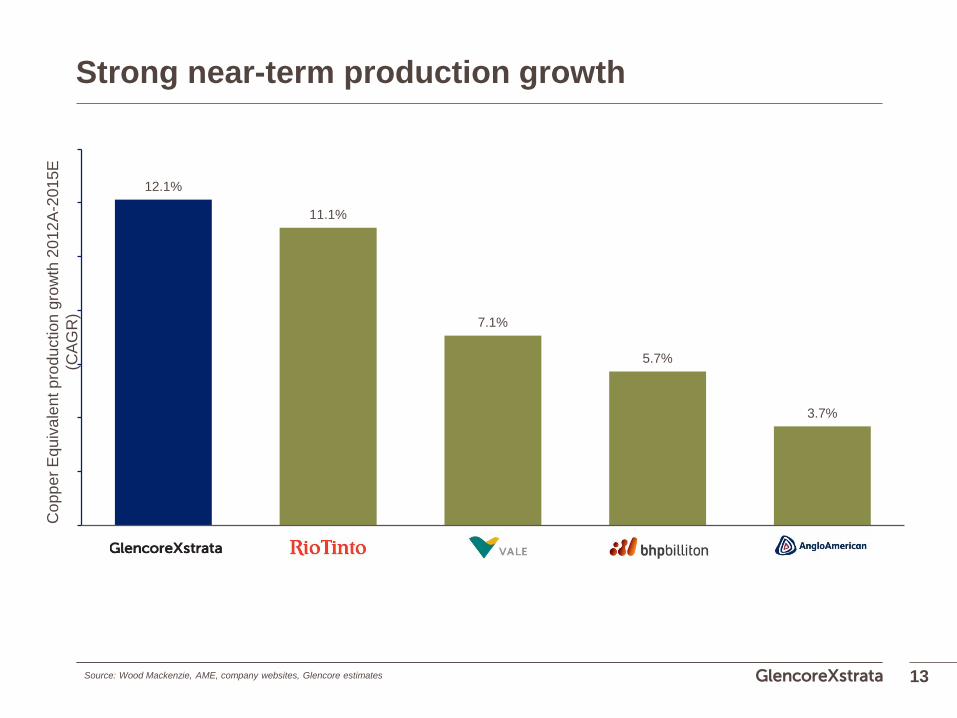

Strong near-term production growth

13 Source: Wood Mackenzie, AME, company websites, Glencore estimates

Cop

per E

quiv

alen

t pro

duct

ion

grow

th 2

012A

-201

5E

(CA

GR

)

12.1%

11.1%

7.1%

5.7%

3.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

GlencoreXstrata Rio Tinto Vale BHP Billiton Anglo American

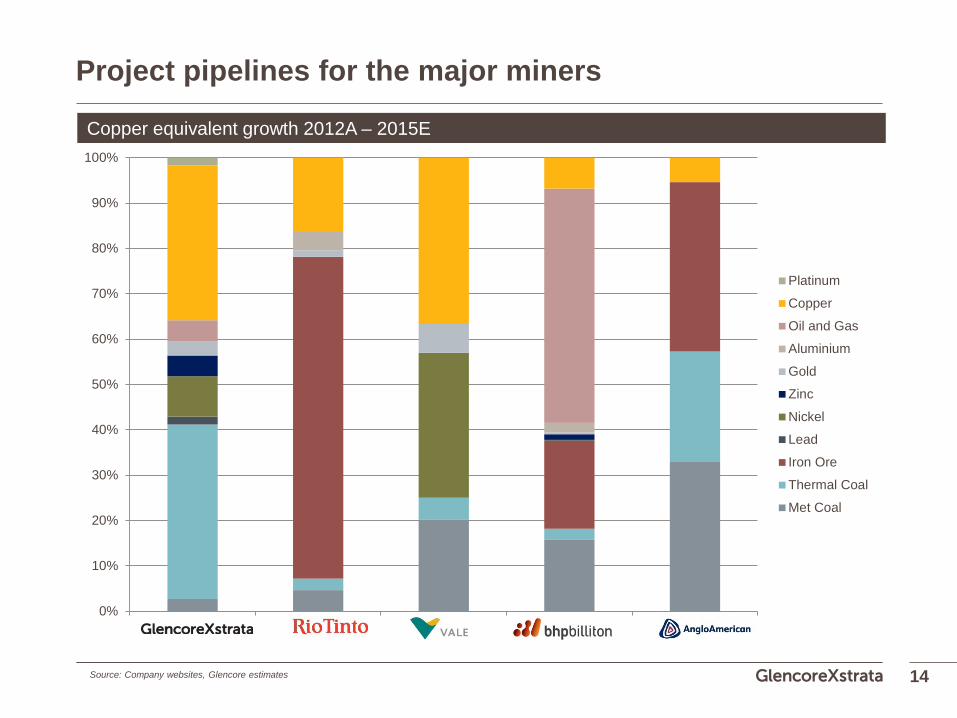

Platinum

Copper

Oil and Gas

Aluminium

Gold

Zinc

Nickel

Lead

Iron Ore

Thermal Coal

Met Coal

Project pipelines for the major miners

14

Copper equivalent growth 2012A – 2015E

Source: Company websites, Glencore estimates

Q1 Q2 Q3 Q4

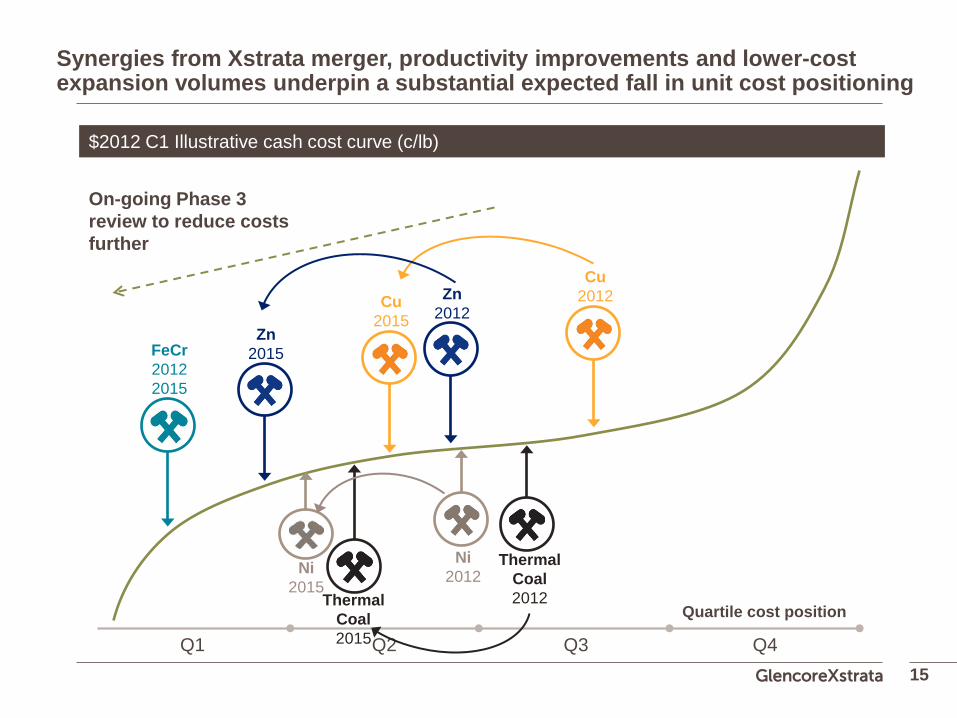

Synergies from Xstrata merger, productivity improvements and lower-cost expansion volumes underpin a substantial expected fall in unit cost positioning

15

$2012 C1 Illustrative cash cost curve (c/lb)

Quartile cost position

FeCr 2012 2015

Zn 2015

Zn 2012

Cu 2012 Cu

2015

Ni 2012 Ni

2015

Thermal Coal 2012 Thermal

Coal 2015

On-going Phase 3 review to reduce costs further

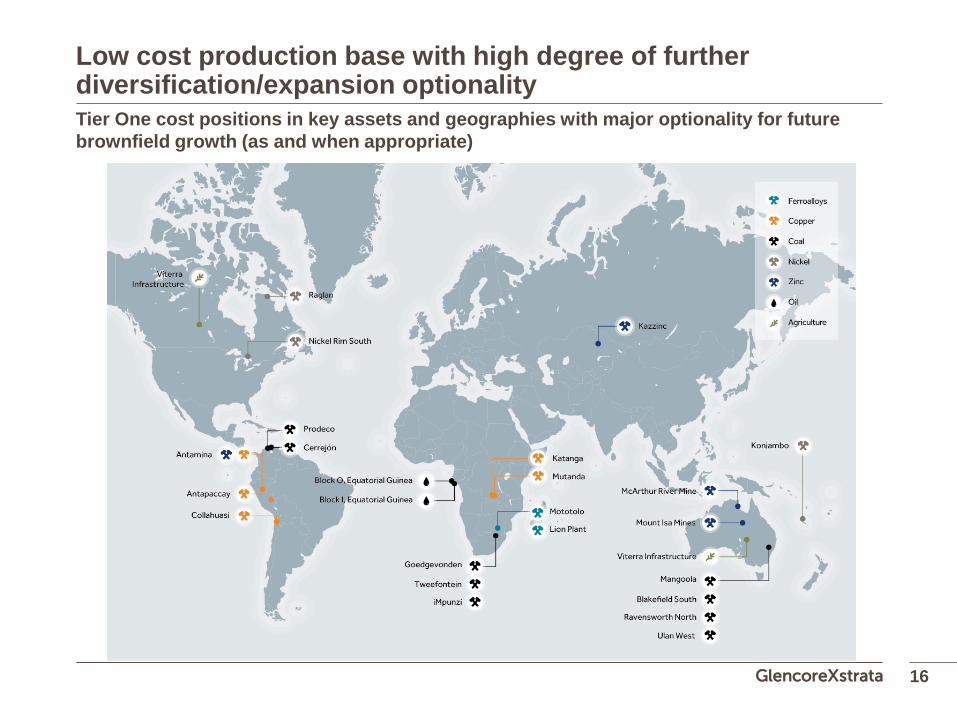

Low cost production base with high degree of further diversification/expansion optionality

16

Tier One cost positions in key assets and geographies with major optionality for future brownfield growth (as and when appropriate)

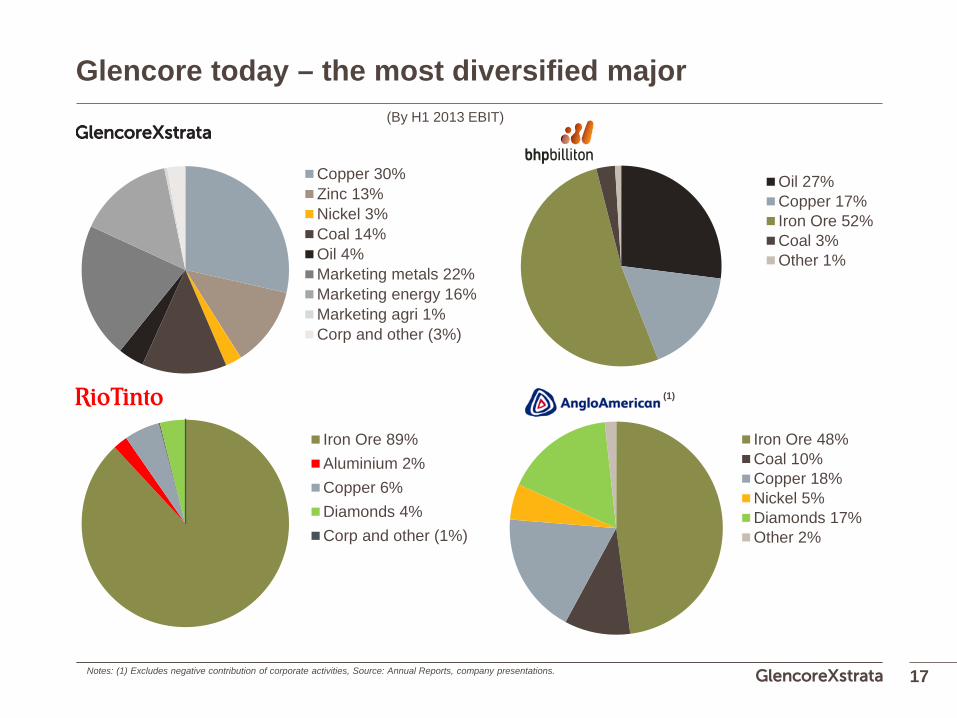

Glencore today – the most diversified major

17

Oil 27%Copper 17%Iron Ore 52%Coal 3%Other 1%

Iron Ore 89%Aluminium 2%Copper 6%Diamonds 4%Corp and other (1%)

(By H1 2013 EBIT)

Iron Ore 48%Coal 10%Copper 18%Nickel 5%Diamonds 17%Other 2%

Rio Tinto:

BHP:

Anglo American (1)

Copper 30%Zinc 13%Nickel 3%Coal 14%Oil 4%Marketing metals 22%Marketing energy 16%Marketing agri 1%Corp and other (3%)

Notes: (1) Excludes negative contribution of corporate activities, Source: Annual Reports, company presentations.

Our philosophy and parameters on capital allocation are clear

• Successful capital allocation is key in this sector • High capital intensity • Investment horizon of decades

• Greenfield projects are disproportionately risky • Multiple uncertain forecast factors combined with long lead times • Many extreme environment, infrastructure and engineering challenges that compound risk • Precise forecasting is almost impossible hence average 35% project over-runs • Often entail material and protracted negative cash flows • Glencore prefers brownfield and bolt-on M&A

• Growth good but must be right kind/time/place • Need to satisfy demand growth and enable increasing profits/dividends • Need to take account of market balance • Focus on retaining diversification by geography and commodity • Acceptable risk adjusted RoE/IRR (as defined) • Look for industrial/marketing synergies • Attractive payback profile

18

Glencore is focused on returns on capital and to shareholders

• Glencore managers are shareholders • Glencore considers total impact of expansions on

returns • Majors lack projects in some of our core

commodities • Ability to shape own destiny via synergies and

portfolio review • Strong cash flow potential from existing

operations • Abundant brownfield options in portfolio once

prices and other factors provide the appropriate incentive to invest

• Access to high-yielding bolt-ons • Commitment to return excess capital to

shareholders

19

"Glencore will have a diversified and defensive asset base with an increasingly strong cost curve position. With our strong balance sheet and cash flow, I am pleased to remind investors of our commitment to return cash to shareholders.” Ivan Glasenberg, Chief Executive of Glencore at the Glencore investor day, 10 September 2013

A strong board

20

• Complies with the UK Corporate Governance Code

• Uniquely strong ownership culture

• Search continuing for permanent new Chairman and additional board members

• Shareholders will continue to be consulted

Anthony Hayward Interim Chairman and Senior Independent Director

Independent Non Executive Directors Executive Directors

CEO Ivan Glasenberg

ED Peter Coates

• 40 years of experience in the resource industry

• Member of the Boards of Santos and Amalgamated Holdings

INED William Macaulay

• Chairman and CEO of First Reserve

• Chairman of Dresser-Rand and Director of Weatherford International

INED Peter Grauer

• Chairman of Bloomberg

• Director of Davita Healthcare Partners

• Member of the International Business Council of the WEF

INED Leonhard Fischer

INED John Mack

• Member of the International Business Council of the WEF, NYC Financial Services Advisory Committee and Shanghai International Financial Advisory Council

• Senior advisor to Morgan Stanley

CEO of Glencore since 2002

29 years with Glencore

• CEO of Genel Energy plc • Member of the European advisory Board of AEA

CEO of RHJ International and former CEO of Winterthur

Member of the Board of Julius Baer Gruppe

Finance update

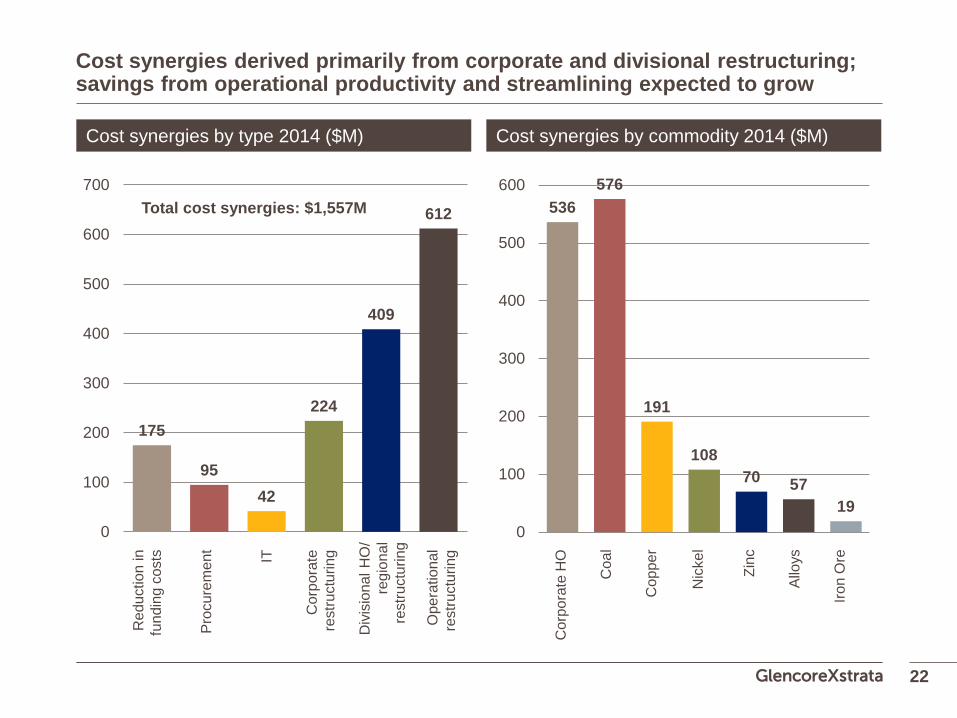

Cost synergies derived primarily from corporate and divisional restructuring; savings from operational productivity and streamlining expected to grow

175

95 42

224

409

612

0

100

200

300

400

500

600

700

Red

uctio

n in

fu

ndin

g co

sts

Proc

urem

ent IT

Cor

pora

te

rest

ruct

urin

g

Div

isio

nal H

O/

regi

onal

re

stru

ctur

ing

Ope

ratio

nal

rest

ruct

urin

g

22

536 576

191

108 70 57

19 0

100

200

300

400

500

600

Cor

pora

te H

O

Coa

l

Cop

per

Nic

kel

Zinc

Allo

ys

Iron

Ore

Cost synergies by type 2014 ($M) Cost synergies by commodity 2014 ($M)

Total cost synergies: $1,557M

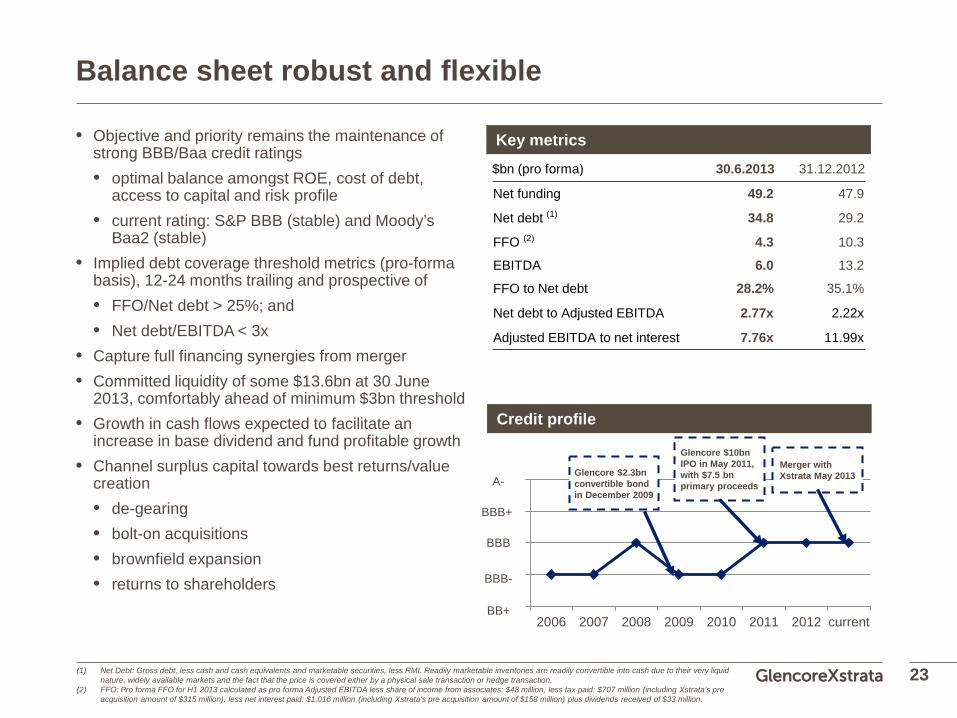

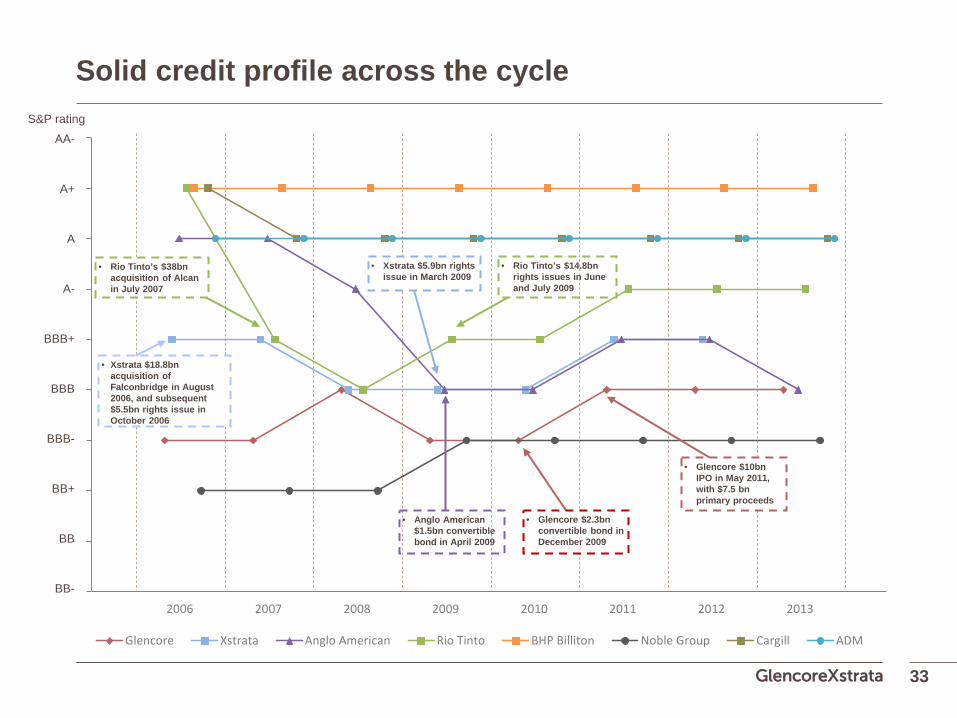

Balance sheet robust and flexible

• Objective and priority remains the maintenance of strong BBB/Baa credit ratings • optimal balance amongst ROE, cost of debt,

access to capital and risk profile • current rating: S&P BBB (stable) and Moody’s

Baa2 (stable) • Implied debt coverage threshold metrics (pro-forma

basis), 12-24 months trailing and prospective of • FFO/Net debt > 25%; and • Net debt/EBITDA < 3x

• Capture full financing synergies from merger • Committed liquidity of some $13.6bn at 30 June

2013, comfortably ahead of minimum $3bn threshold • Growth in cash flows expected to facilitate an

increase in base dividend and fund profitable growth • Channel surplus capital towards best returns/value

creation • de-gearing • bolt-on acquisitions • brownfield expansion • returns to shareholders

23

2

3

4

5

6

2006 2007 2008 2009 2010 2011 2012 current

BBB

BB+

BBB+

BBB-

A-

Glencore $10bn IPO in May 2011, with $7.5 bn primary proceeds

Glencore $2.3bn convertible bond in December 2009

Merger with Xstrata May 2013

$bn (pro forma) 30.6.2013 31.12.2012

Net funding 49.2 47.9

Net debt (1) 34.8 29.2

FFO (2) 4.3 10.3

EBITDA 6.0 13.2

FFO to Net debt 28.2% 35.1%

Net debt to Adjusted EBITDA 2.77x 2.22x

Adjusted EBITDA to net interest 7.76x 11.99x

Key metrics

(1) Net Debt: Gross debt, less cash and cash equivalents and marketable securities, less RMI. Readily marketable inventories are readily convertible into cash due to their very liquid nature, widely available markets and the fact that the price is covered either by a physical sale transaction or hedge transaction.

(2) FFO: Pro forma FFO for H1 2013 calculated as pro forma Adjusted EBITDA less share of income from associates: $48 million, less tax paid: $707 million (including Xstrata’s pre acquisition amount of $315 million), less net interest paid: $1,016 million (including Xstrata’s pre acquisition amount of $158 million) plus dividends received of $33 million.

Credit profile

Capital efficient business model

• Application of Glencore’s capital-efficient business model • Glencore run by owners for the benefit of all shareholders • maintain flexible but efficient balance sheet – strong BBB/Baa

• Marketing remains highly capital efficient • low capex and equity requirements

• Strong track record of capital efficiency in industrial assets • value-based, often contrarian and opportunistic approach to investments • lower risk brownfield and bolt-on M&A • divisions responsible for sourcing investments

• Centralised capital allocation process to ensure discipline • Comprehensive assessment of value, based on returns and risks

• focus continues to be on RoE and cash flow • trading and industrial assets access separate pools of capital • focus on high returns, forecastability and appropriate risk-return trade-off

• On-going optimisation of the asset portfolio

24

Glencore’s flexible capital model

• Two distinct pools of capital centrally funded and allocated • Marketing • Industrial

• Marketing: ~$20bn of capital employed • working capital average turnover cycle of ~35 days • target for 80% debt-funded • Marketing debt is frequently refreshed; average duration of debt facilities versus use is a highly

conservative 20x • 2013 earnings benefit from Viterra and Xstrata • target RoE is 40%-65%

• Industrial: ~$100bn of capital employed • target of 30-40% debt-funded; or < 3x Net Debt/EBITDA • target RoE is 20-25% for new capital/projects • earnings to fully benefit from ramp-up of Koniambo, Antapaccay, E&P, African copper belt, Prodeco,

etc • portfolio optimisation will also boost returns on equity

25

Strong cash flow potential confirmed

• Material cash flow growth remains on track for 2013-2015 • commissioning of existing organic growth projects • full earnings from recent bolt-on acquisitions • at least $2bn of merger synergies from 2014 • Phase 3 to come

• Capex confirmed to decline materially from 2013 • large Xstrata capex commitments for 2013 and 2014 come to an end • total capex now expected to fall to $12bn/$8bn/$6bn in 2013/2014/2015 • sustaining capex confirmed at $4bn range • anticipated divestment of Las Bambas at minimum of capital costs incurred at the time of sale

• Base dividend to remain competitive with sector while growth phase completes • …. and to be reviewed after that, adjusted to reflect expected future cash flows, leverage and asset

disposal processes underway • in addition, excess capital will be returned to shareholders in most efficient manner

26

Appendices

How does Glencore find the best investment opportunities?

• Trusted relationships with over 7,000 suppliers and customers • existing supply and credit relationships • Glencore often first call for any investment opportunities

• Marketing activities and relationships provides unique insight • market view enables decisive decision making • product, asset quality and operational matters evident to Glencore • proven ability to spot and deliver on optionality around assets • examples include: Colombian, Australian and South African coal, African copper belt, Kazzinc

• Decades of experience at sourcing and integrating deals • unlike some peers, there is, deliberately, little or no rotation of senior personnel

between divisions • No pressure to grow for strategic reasons

• managers are owners • assets built upon opportunistic deals • divisions have multiple existing options to grow efficiently without M&A

28

Our values

29

• Entrepreneurialism • Our approach fosters the highest level of professionalism,

personal ownership and entrepreneurial spirit in all our employees while never compromising on the safety and well-being of our people. This is important to our success and the superior returns we aim to achieve for all our stakeholders

• Simplicity • We aim to achieve our key deliverables as a path to

industry-leading returns, while maintaining a clear focus on excellence, quality, sustainability and continuous improvement in everything we do

• Safety • Our first priority in the workplace is to protect the health and

well-being of all our workers. We take a proactive approach to health and safety; our goal is continuous improvement in preventing occupational disease and injuries

• Responsibility • We recognise that our work can have an impact on our

society and the environment. We care profoundly about our performance in compliance, environmental protection, human rights and health and safety

• Openness • We value relationships and communication based on

integrity, co-operation, transparency and mutual benefit, with our people, our customers, our suppliers, governments and society in general

30

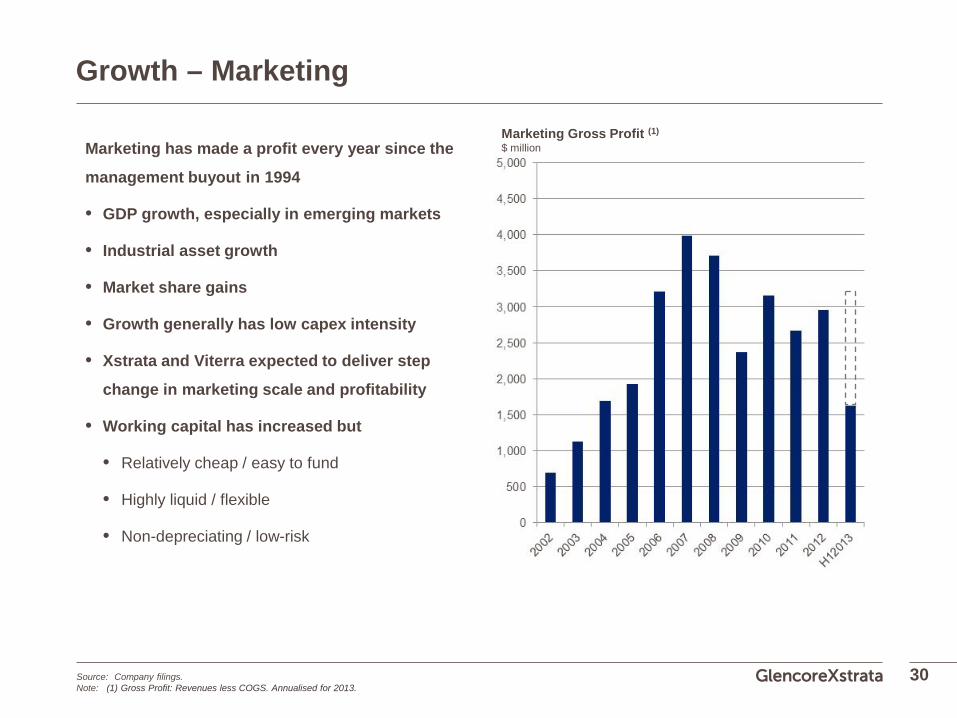

Growth – Marketing

Marketing has made a profit every year since the

management buyout in 1994

• GDP growth, especially in emerging markets

• Industrial asset growth

• Market share gains

• Growth generally has low capex intensity

• Xstrata and Viterra expected to deliver step

change in marketing scale and profitability

• Working capital has increased but

• Relatively cheap / easy to fund

• Highly liquid / flexible

• Non-depreciating / low-risk

Marketing Gross Profit (1) $ million

Source: Company filings. Note: (1) Gross Profit: Revenues less COGS. Annualised for 2013.

0

50

100

150

200

250

300

0

5

10

15

20

25

30

Q105

Q205

Q305

Q405

Q106

Q206

Q306

Q406

Q107

Q207

Q307

Q407

Q108

Q208

Q308

Q408

Q109

Q209

Q309

Q409

Q110

Q210

Q310

Q410

Q111

Q211

Q311

Q411

Q112

Q212

Q312

Q412

Q113

Q213

Current capital employed CCI Index (rebased to 100)

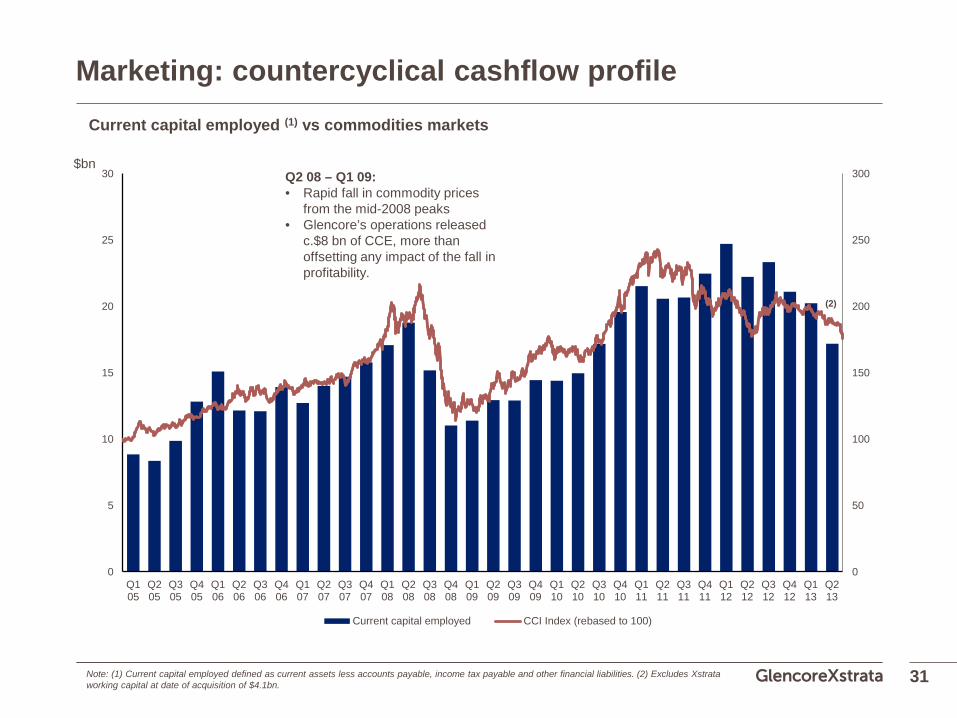

Marketing: countercyclical cashflow profile

31

$bn Q2 08 – Q1 09: • Rapid fall in commodity prices

from the mid-2008 peaks • Glencore’s operations released

c.$8 bn of CCE, more than offsetting any impact of the fall in profitability.

Current capital employed (1) vs commodities markets

Note: (1) Current capital employed defined as current assets less accounts payable, income tax payable and other financial liabilities. (2) Excludes Xstrata working capital at date of acquisition of $4.1bn.

(2)

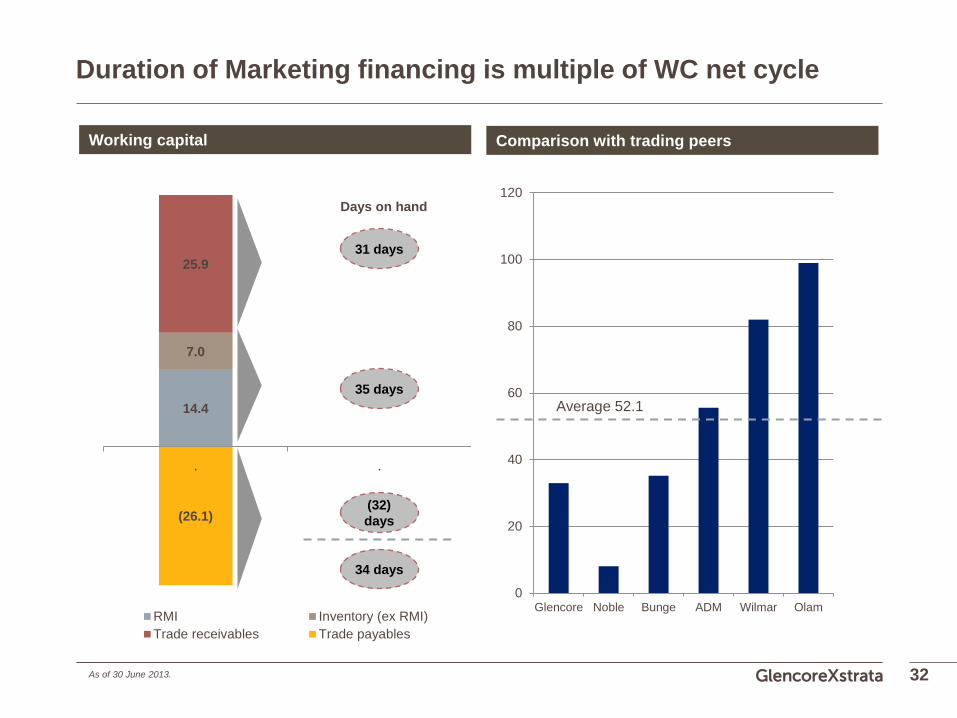

14.4

7.0

25.9

(26.1)

-30

-20

-10

0

10

20

30

40

50

. .

RMI Inventory (ex RMI)Trade receivables Trade payables

Duration of Marketing financing is multiple of WC net cycle

32

Working capital Comparison with trading peers

Days on hand

31 days

35 days

(32) days

34 days

0

20

40

60

80

100

120

Glencore Noble Bunge ADM Wilmar Olam

Average 52.1

As of 30 June 2013.

Solid credit profile across the cycle

33

0

1

2

3

4

5

6

7

8

9

2005 2006 2007 2008 2009 2010 2011 2012 2013

Glencore Xstrata Anglo American Rio Tinto BHP Billiton Noble Group Cargill ADM

S&P rating

• Anglo American $1.5bn convertible bond in April 2009

• Rio Tinto’s $14.8bn rights issues in June and July 2009

• Xstrata $18.8bn acquisition of Falconbridge in August 2006, and subsequent $5.5bn rights issue in October 2006

• Rio Tinto’s $38bn acquisition of Alcan in July 2007

• Xstrata $5.9bn rights issue in March 2009

• Glencore $2.3bn convertible bond in December 2009

• Glencore $10bn IPO in May 2011, with $7.5 bn primary proceeds

BB-

BB

BB+

BBB-

BBB

BBB+

A-

A

A+

AA-

Q&A