south america - regional economic drivers and their global impact on the global therm process market

TRANSCRIPT

South AmericaRegional Economic Drivers and their Global Impact in the Thermal Processing Market – South America

Thomas D. Kreuzaler SECO/WARWICK do Brasil Ltda.

Jundiaí, São Paulo, Brasil

The SECO/WARWICK Group

History of SECO/WARWICK Brazil 1986 - Founded as ENGEFOR, São Paulo/SP, Brasil 1989 – furnaces for PTFE curing 1990 – License agreement with ABBOTT furnaces, USA 1991 – First continuous atmosphere sintering furnace 2000 – Steam blackening service for selected customers 2008 – construction of new plant with 5.000 m2 in Jundiaí/SP 2008 – moving 70 km from Sao Paulo City to Jundiaí/SP 2013 – SECO/WARWICK acquired 100 % of the shares of

ENGEFOR, renamed to SECO/WARWICK do Brasil Ltda.

Since 2013 – transfer of technology and productknow-how from the Group entities to Brazil

Factory in Brasil SECO/WARWICK do Brasil Ltda. in Jundiai/SP, Brazil

South America Regional Economic Drivers and their Global Impact in the Thermal Processing Market– South America

Size of South American Market – General Comments

Main Driving Industries Thermal Processing in the region

Business Conditions

Threads and Opportunities South America

Summary

South America in comparison I Large Industrial Market Sizes (USA, EU, China, India, South America w/o Japan)

Contrary to the others South America is not aharmonized and homogenous market!

Selected Markets’ GDP in106 US$

IMFFC2016 / Apr. 15

World Bank2015

United Nations2014

USA 18.558.130 18.460.646 17.348.072

European Union 16.477.211 18.460.646 18.518.430

China 11.383.030 10.866.444 10.430.590

India 2.288.720 2.073.543 2.054.941

South America 3.064.982 3.677.952 4.496.299

South America in comparison II Large Industrial Market Sizes (USA, EU, China, India, South America – without Japan)

Selected Markets’ share in % oftotal selection

IMFFC2016 / Apr. 16

World Bank2015

United Nations2014

USA 36% 34% 33%

European Union 32% 34% 35%

China 22% 20% 20%

India 4% 4% 4%

South America 6% 7% 9%

South America map

South America in detail IMarket sizes South America (GDP in 106 US$)

Country IMF FC2016 World B. 2015 UN 2014

Brazil 1.534.780 1.774.725 2.346.523

Argentina 437.856 548.055 543.490

Chile 235.419 240.216 258.062

Peru 178.643 192.084 201.809

Paraguay 26.804 30.881 30.958

Uruguay 53.145 57.471 57.471

Bolivia 33.983 32.996 32.996

Ecuador 94.014 100.917 100.917

Colombia 253.240 292.080 377.740

Venezuela 185.611 371.337 509.968

Trinidad e Tobago 23.816 28.883 28.069

Guyana 3.335 3.097 3.086

Suriname 4.336 5.210 5.210

South America in detail II Market sizes South America (% GDP of total GDP South America)

Country IMF FC2016 World B. 2015 UN 2014

Brazil 50,1% 48,3% 52,2%Argentina 14,3% 14,9% 12,1%Chile 7,7% 6,5% 5,7%Peru 5,8% 5,2% 4,5%Paraguay 0,9% 0,8% 0,7%Uruguay 1,7% 1,6% 1,3%Bolivia 1,1% 0,9% 0,7%Ecuador 3,1% 2,7% 2,2%Colombia 8,3% 7,9% 8,4%Venezuela 6,1% 10,1% 11,3%Trinidad e Tobago 0,8% 0,8% 0,6%Guyana 0,1% 0,1% 0,1%Suriname 0,1% 0,1% 0,1%

> 70%> 90% incl.

Analysis of the drivers in TP Mining and Metallurgy

Oil & Gas

Energy

Cars, Trucks and Automotive

Agricultural and Construction machinery

Aerospace & Defense

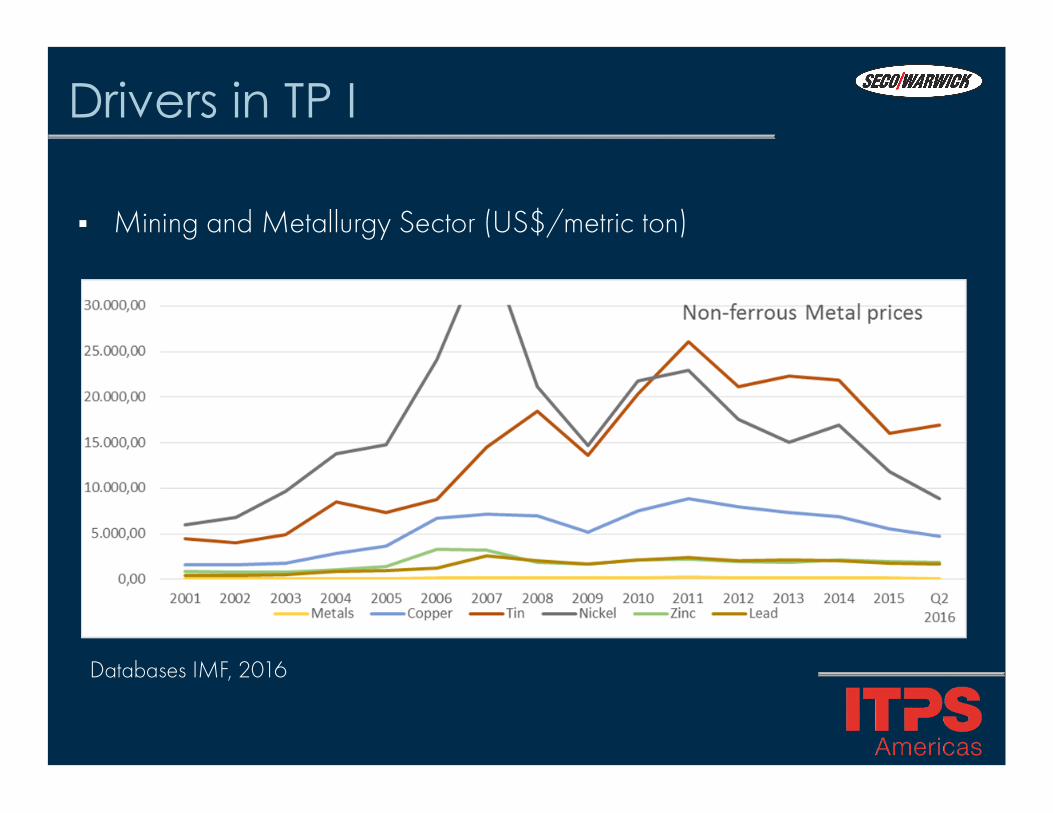

Drivers in TP I Mining and Metallurgy Sector (US$/metric ton)

Databases IMF, 2016

Drivers in TP II Mining and Metallurgy (US$/metric ton)

Databases IMF, 2016

Drivers in TP IIIMining & Metallurgy

Sector is suffering from lower worldwide demand

South America’s countries are suffering especially from the deteriorated ore prices in their balance of trade and budget incomes

Low competitiveness, unfortunate business environment (infrastructure, political conditions e.g.) and high energy prices are a hurdle for increased activities in smelting and refining of metals

Government programs for increased industrial activity have issues with funds

Drivers in TP IV Oil and Gas

Databases IMF, 2016

Drivers in TP VOil & Gas

Sector is suffering from lower worldwide demand

Oil prices are partially lower than oil production cost (Brazil pre-saldeep sea production at max. 70 US$/barrel e.g.)

High oil price of the past caused creation of various inefficiencies in South American Companies, which need to be repaired (undergoing)

Price increase in the future will accelerate the industrial activities quickly

Government funds are suffering from low budget income

Drivers in TP VIEnergy

Due to reduced industrial activities the total demand has been decreased and the supply situation has been improved

High energy cost like in Brazil and Argentina are a hurdle for energy intense industries

Most energy programs are government driven (nuclear, solar and wind energy programs) and suffer from funding

Private investors will be attracted by changes in business conditions

Demand of population will increase certainly

Drivers in TP VII Cars Production

ACEA Worldwide Production 2014/2015

Passenger cars 2014 % of total 2015 % of total

China 17.820.434 24,73% 19.172.731 26,03%North America 17.723.441 24,60% 18.241.366 24,76%Europe 13.795.840 19,15% 14.036.608 19,06%South Asia 12.341.029 17,13% 11.942.164 16,21%Japan/Korea 5.872.427 8,15% 6.096.689 8,28%South America 3.041.644 4,22% 2.642.480 3,59%Middle East/Africa 1.454.528 2,02% 1.526.183 2,07%WORLD 72.049.343 100,00% 73.658.221 100,00%

Drivers in TP VIII

ACEA Worldwide Production 2014/2015

Commercialvehicles 2014 % of total 2015 % of total

China 6.335.620 34,26% 5.653.601 31,31%North America 3.726.981 20,16% 4.016.421 22,25%Europe 2.919.493 15,79% 3.186.779 17,65%South Asia 2.309.728 12,49% 2.367.733 13,11%Japan/Korea 1.732.786 9,37% 1.701.478 9,42%South America 968.787 5,24% 683.214 3,78%Middle East/Africa 497.423 2,69% 445.787 2,47%WORLD 18.490.818 100,00% 18.055.013 100,00%

Comercial Vehicles Production

Drivers in TP IX Car & Trucks Production

OICA Worldwide Production 2014/2015, *FC2016 various sources

2014 2015 FC 2016*World 89.776.465 90.780.583 91.500.000

ARGENTINA 617.329 533.683 500.000BRAZIL 3.146.386 2.429.463 2.200.000

COLOMBIA 71.137 78.070 100.000ECUADOR 5.986 4.800 5.000VENEZUELA 19.759 18.300 15.000

TOTAL SOUTH AMERICA 3.860.597 3.064.316 2.820.000% of WORLD 4,30% 3,38% 3,08%

Drivers in TP XCars & Trucks

Declining production in Brazil as major producer/market and adaptation of production capacities radiates to all countries in South America

Reduced demand due to economic crisis in Brazil, Argentina and Venezuela

Expectation, that 2016 bottom line of demand has been hit

Production nationalizing programs (Autoinovar e.g.) require companies to invest in local production lines for imported parts

Slight improvement expected in 2017, middle term the market will return strongly due to its infrastructure demands

Drivers in TP XIAgricultural & Construction machines

Agricultural business is growing continuously and will reach new record in export in 2016

Demand in agriculture is constantly growing, but smaller companies are depending on government funding

Construction business in infrastructure has been reduced due to funding issues of government

Construction demand in private sector has lower demand due to crisis situation

BRAZIL Export 2014 Export 2015 DifferenceAgricultural 06.768 mioUS$ 06.863 MioUS$ +1,4%Other 10.726 mioUS$ 09.920 mioUS -7,5%

Brazilian Agricultural Ministry, 2016

Drivers in TP XIIAerospace & Defense EMBRAER introduced new models, FC 2016 positive, but most of the

parts are imported and the company is undergoing now a corruption investigation (“Board members approved bribes”)

SAAB Viken fighter program Brazil from 2017 with local content Investment and modernization of Defense forces suffer from government

funding A lot of smaller companies and suppliers on the path of

internationalization and standardizing. Initiatives launched.

Commercial plane deilveries 2015 2016 FCBoeing 762 planes Airbus 635 planes EMBRAER 101 planes

Drivers in TP XIIIDrivers summary

Commercial plane deilveries 2016 2017 2018+Mining and Metallurgy () Oil & Gas Energy () Cars, Trucks and Automotive () Agricultural and ConstructionMachinery

Aerospace & Defense

Business Conditions IIMD World Competitiveness Report 2016

The IMD World Competitiveness Scoreboard presents the 2016 overall rankings for 61 economies and is issued by the IMD institute in Lausanne/CH (www.imd.org). Criterias: Economic performance (83 criteria), What are the

macro-economics of the economy? Government efficiency (73 criteria) – Do government

policies are conducive to competitiveness? Business efficiency (71 criteria) - Does national

environment encourage companies to perform innovative, profitable and responsible?

Infrastructure (115 criteria) - Do basic, technological, scientific and human resources meet the need of the business?

Business Conditions IIIMD competitiveness report on selected countries

0 20000 40000 60000 80000 10000061 - Venezuela

57 - Brazil55 - Argentina

54 - Peru51 - Colombia

45 - Mexico41 - India36 - Chile

26 - Japan25 China Mainland

12 - Germany10 - Canada

3 - USA

Summary and OutlookSummary

South America’s global impact on the thermal processing market is marginal, this could change if positive signs for 2017/2018 lead to considerable growths numbers

Brazil and Argentina will remain for some time the most important economies and regional motors for the further development

Political scenarios and the corresponding business ambience are very important and are improving in the recent past

In 2016 the share of the big drivers (automotive, mining and metallurgy) is declining in South America, other (aerospace, agriculture) are not yet capable of compensating this

OutlookThreads

Overcapacities, low competitiveness and “bad economic culture” will continuously be a hurdle for substantial growth

Politic instability take the industry and foreign investments at risk

Only slowly and on a long term (2020+) the industry will return to growth

Opportunities

Political culture changes and higher commodities prices will improve the conditions rapidly

Growing internal demand in the countries will require fast growing industrial production

Investors confidence will increase investments in infrastructure and industry

Export will develop significantly Changes are quickly