southern africa roundtable on making finance work for africa may 7-9, zambezi sun hotel,...

TRANSCRIPT

Southern Africa Roundtable on Making Finance work for Africa

May 7-9, Zambezi Sun Hotel, Livingstone, Zambia

Finance and Technology – What are the opportunities?

By

Stephen Mwaura Nduati

Central Bank of Kenya

Enabling Environment for Mobile Banking in Africa2

Introduction• Access Challenges:

• Financial Services – Kenya, Tanzania, Zambia, South Africa

• Mobile Telephones - Kenya

• Growth in Bank Branches and in ATM Services - Kenya

• Local Money Transfer Services – Kenya

• Enabling Environment for Mobile Banking

• Regional Payment System Initiatives

• Way forward

Enabling Environment for Mobile Banking in Africa3

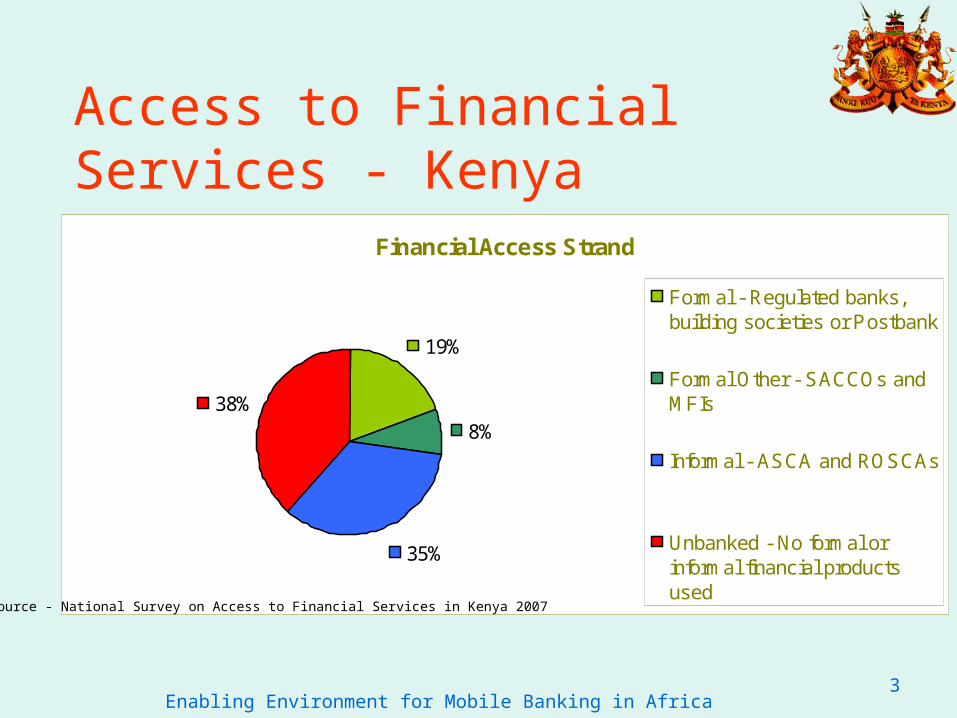

Access to Financial Services - Kenya

Financial Access Strand

19%

8%

35%

38%

Formal - Regulated banks,building societies or Postbank

Formal Other - SACCOs andMFIs

Informal - ASCA and ROSCAs

Unbanked - No formal orinformal financial productsused

Source - National Survey on Access to Financial Services in Kenya 2007

Enabling Environment for Mobile Banking in Africa4

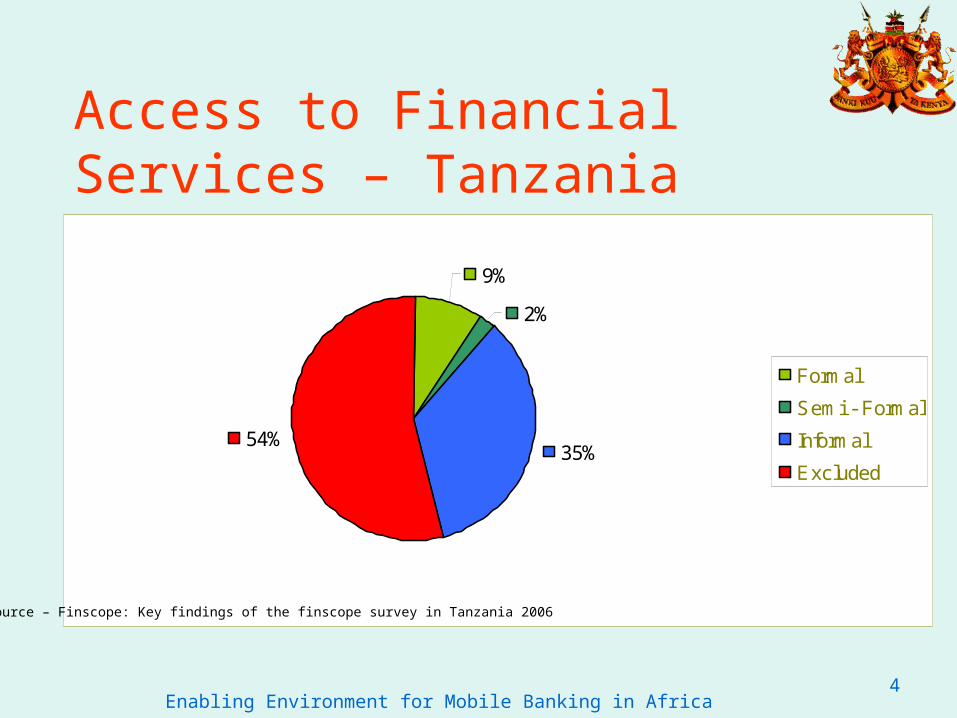

Access to Financial Services – Tanzania

9%

2%

35%54%

Formal

Semi - Formal

Informal

Excluded

Source – Finscope: Key findings of the finscope survey in Tanzania 2006

Enabling Environment for Mobile Banking in Africa5

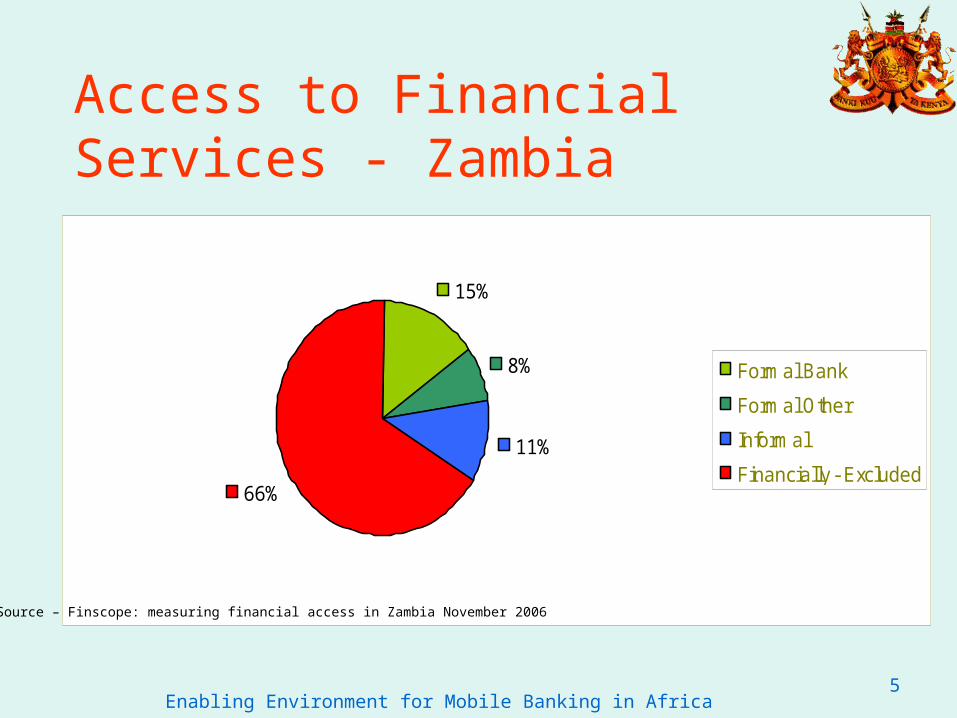

Access to Financial Services - Zambia

15%

8%

11%

66%

Formal Bank

Formal Other

Informal

Financially - Excluded

Source – Finscope: measuring financial access in Zambia November 2006

Enabling Environment for Mobile Banking in Africa6

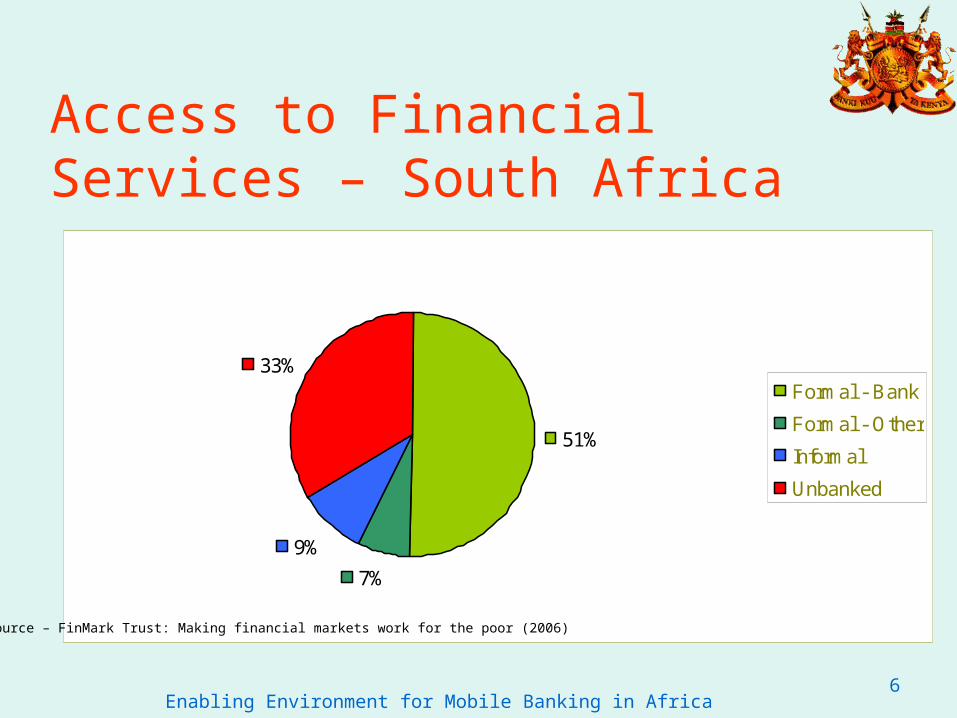

Access to Financial Services – South Africa

51%

7%

9%

33%Formal - Bank

Formal - Other

Informal

Unbanked

Source – FinMark Trust: Making financial markets work for the poor (2006)

Enabling Environment for Mobile Banking in Africa7

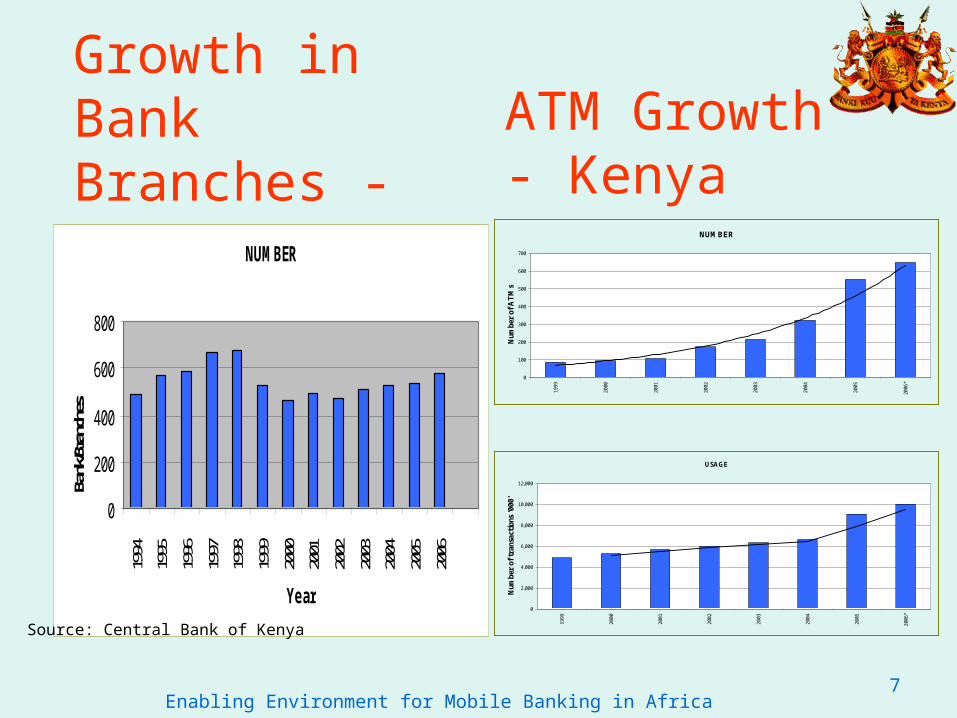

Growth in Bank Branches - Kenya

NUMBER

0

200

400

600

800

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Year

Bank

/Bran

ches

NUMBER

0

100

200

300

400

500

600

700

1999

2000

2001

2002

2003

2004

2005

2006

*

Num

ber

of A

TM

s

USAGE

0

2,000

4,000

6,000

8,000

10,000

12,000

1999

2000

2001

2002

2003

2004

2005

2006

*

Num

ber

of t

rans

acti

ons

'000

'

ATM Growth - Kenya

Source: Central Bank of Kenya

Enabling Environment for Mobile Banking in Africa8

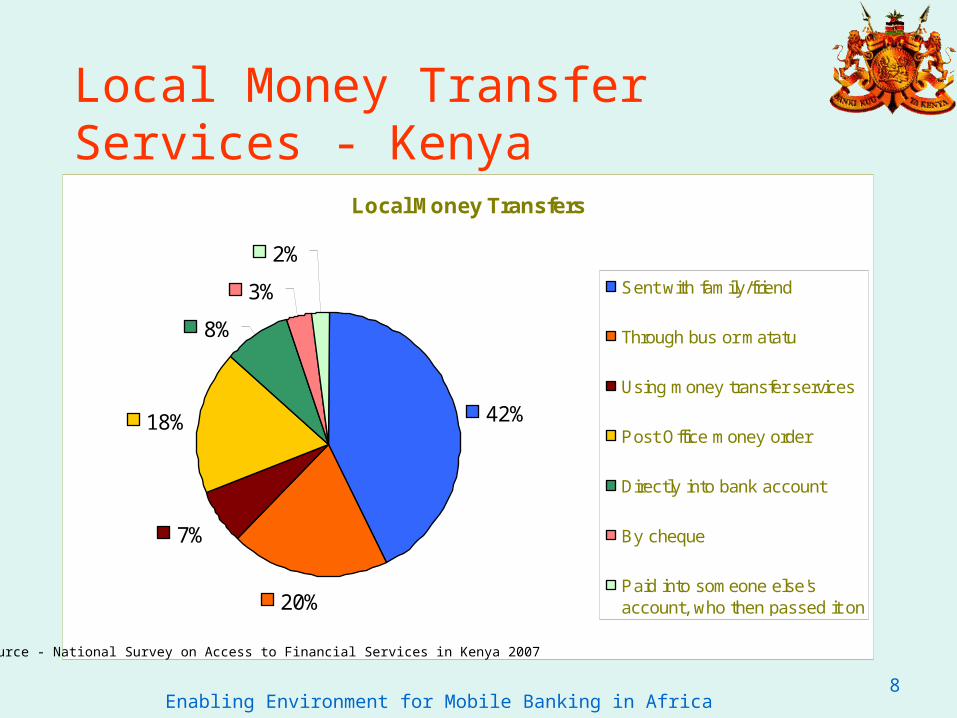

Local Money Transfer Services - Kenya

Local Money Transfers

42%

20%

7%

18%

8%

3%

2%

Sent with family/friend

Through bus or matatu

Using money transfer services

Post Office money order

Directly into bank account

By cheque

Paid into someone else'saccount, who then passed it on

Source - National Survey on Access to Financial Services in Kenya 2007

Enabling Environment for Mobile Banking in Africa9

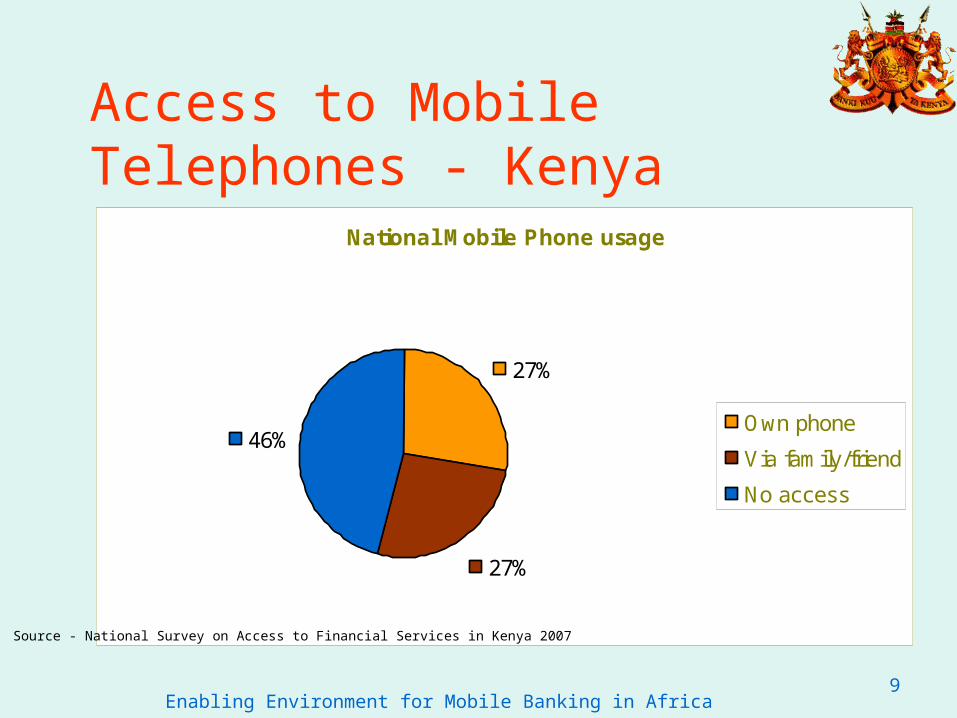

Access to Mobile Telephones - Kenya

National Mobile Phone usage

27%

27%

46%Own phone

Via family/friend

No access

Source - National Survey on Access to Financial Services in Kenya 2007

Enabling Environment for Mobile Banking in Africa10

Enabling Environment for Mobile Banking

• What is m-payment and m-banking?• Why is m-payments and m-banking relevant?• Emerging experiences & models• Policy Framework• Possible roles for policy makers• Enabling environment policy balance• Key concerns (certainty, security issues,

competition)

Enabling Environment for Mobile Banking in Africa11

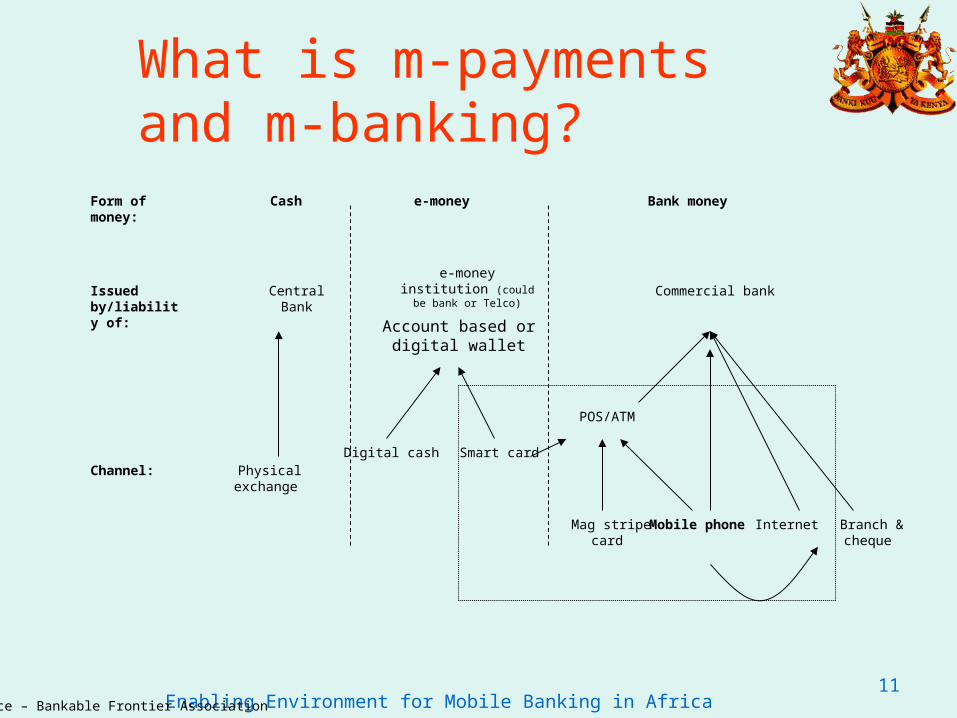

What is m-payments and m-banking?

Form of money:

Issued by/liability of:

Channel:

Cash e-money Bank money

Central Banke-money institution (could be bank or Telco) Commercial bank

Physical exchange

Digital cash Smart card

Mag stripe card Mobile phone Internet

POS/ATM

Branch & cheque

Account based or digital wallet

Source – Bankable Frontier Association

Enabling Environment for Mobile Banking in Africa12

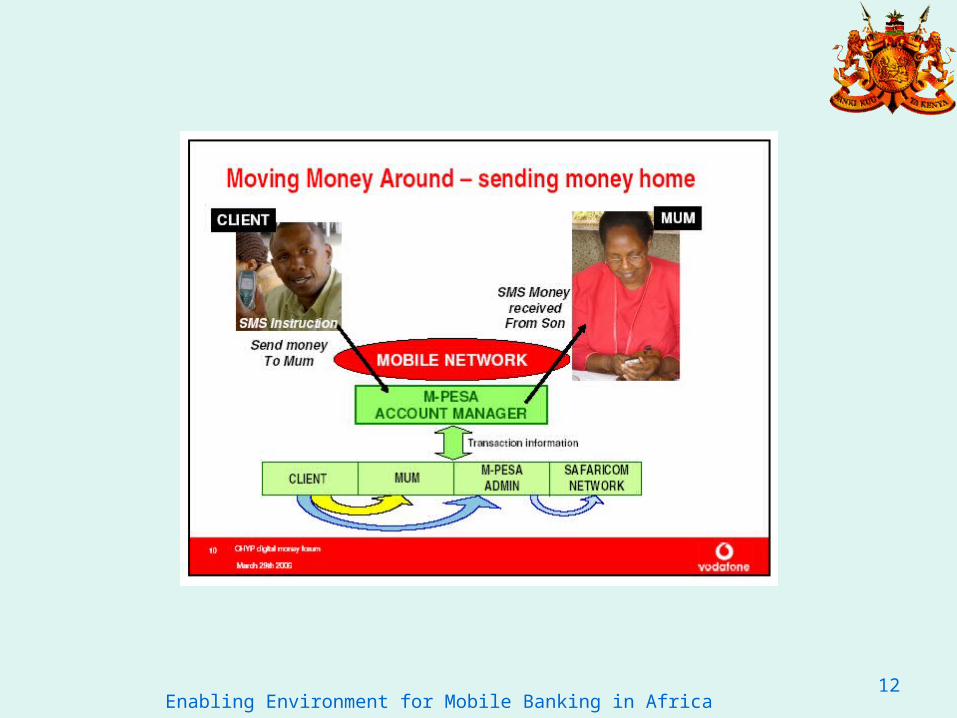

Enabling Environment for Mobile Banking in Africa13

Which model? Macro

payment

$/Eu10

Micro payment

Remote Local

Source: Mobey Forum WP v1.1

Traditionally, bank driven

(linked to deposit account or credit card)

Telco driven

(linked to pre-paid account)

Enabling Environment for Mobile Banking in Africa14

Why is m-payments and m-banking especially relevant? • Broadens access to financial services:

Unbanked with cell phone: SA 20%+Rural coverage and penetration increasing

• Leapfrogging access to e-banking • Focal point to assess and consider general

development issues in the retail banking system

• Enhancement of safety, security & efficiency• Positive impact on social & economic growth

Enabling Environment for Mobile Banking in Africa15

Emerging Experiences & models• Europe:

• Collapse of Simpay & other models• Nordic region most advanced

• Asia:•Japan:

•DoCoMo: FeliCa 10m by end 2005•Korea:

•10m enrolled from 2003 onwards•Philippines

• SMARTmoney: 2.5m/ 20m customers (2000) • Globe G-Cash: 1.2m (2004)

Source – Bankable Frontier Associates

Enabling Environment for Mobile Banking in Africa16

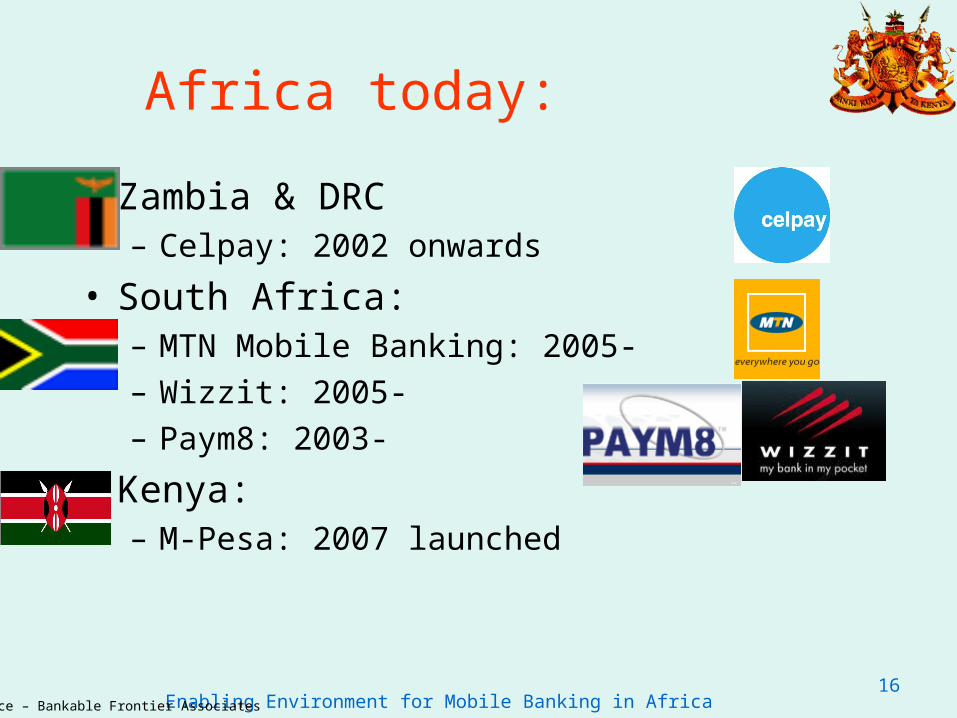

Africa today:

• Zambia & DRC– Celpay: 2002 onwards

• South Africa: – MTN Mobile Banking: 2005- – Wizzit: 2005- – Paym8: 2003-

• Kenya: – M-Pesa: 2007 launched

Source – Bankable Frontier Associates

Enabling Environment for Mobile Banking in Africa17

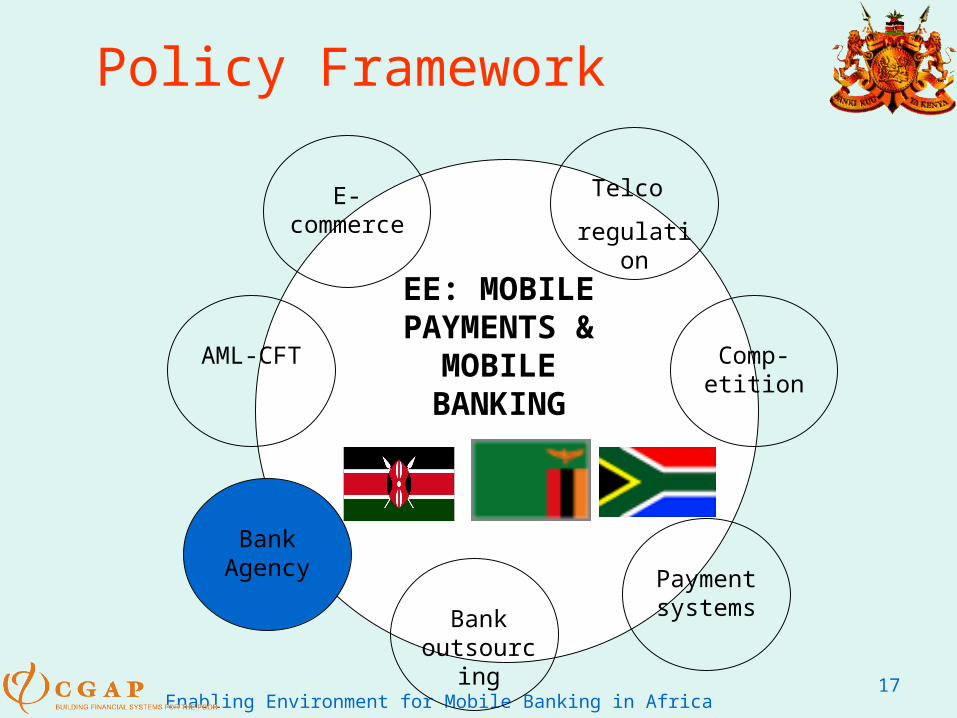

Policy Framework

E-commerce

AML-CFT

Bank Agency Payment

systemsBank outsourcing

Comp-etition

Telco

regulation

EE: MOBILE PAYMENTS &

MOBILE BANKING

Enabling Environment for Mobile Banking in Africa18

Key Concerns - Certainty

There should be sufficient certainty around electronic contracting to protect both parties

Issues: • Repudiation risk• UNCITRAL model laws• Advanced digital signatures

Enabling Environment for Mobile Banking in Africa20

Competition

“The consumer should have the freedom to choose bank, mobile operator and handset and change them independently” Mobey Forum White Paper 2003, Customer Proposition

Issues: • Number portability• Platform access

– Movilpago case (Spain, 2000)

Enabling Environment for Mobile Banking in Africa21

Possible roles for policy makers

• Regulator

• Supervisor

• Standard setter

• Information gatherer

• Facilitator

• Coordinator

Enabling Environment for Mobile Banking in Africa22

Enabling environment:Policy balance

Stability of the financial system

Consumer protection

& choice

Efficiency

Broader access

Financial

integrity

Enabling Environment for Mobile Banking in Africa23

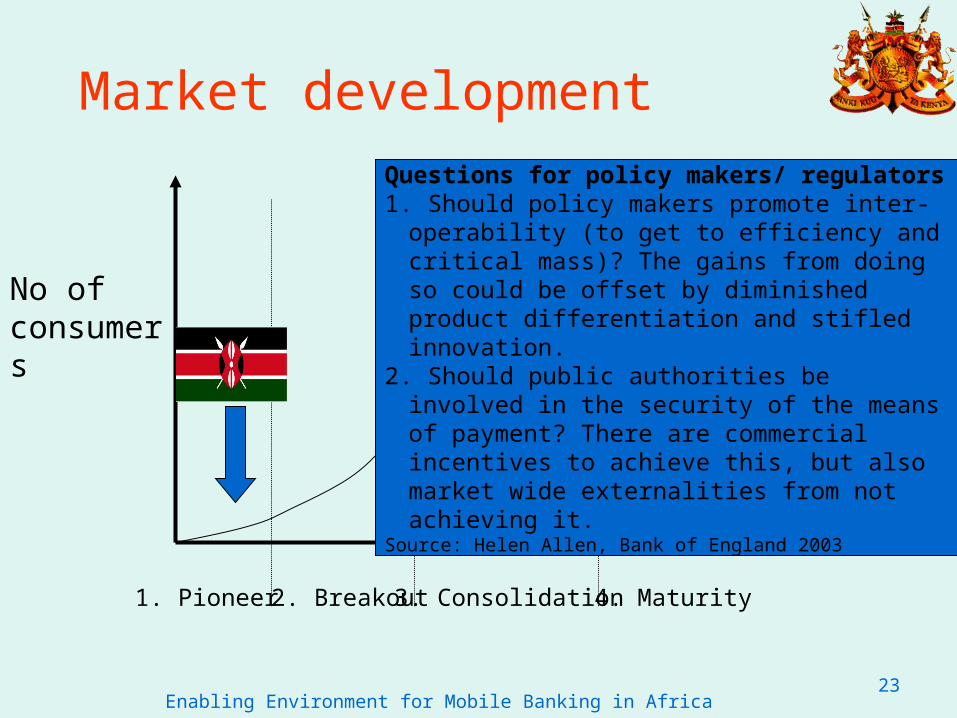

No of consumers

1. Pioneer 2. Breakout3. Consolidation4. Maturity

Market development

Questions for policy makers/ regulators1. Should policy makers promote inter-operability (to

get to efficiency and critical mass)? The gains from doing so could be offset by diminished product differentiation and stifled innovation.

2. Should public authorities be involved in the security of the means of payment? There are commercial incentives to achieve this, but also market wide externalities from not achieving it.

Source: Helen Allen, Bank of England 2003

Enabling Environment for Mobile Banking in Africa24

Regional Payment and Settlement Systems Initiatives

• Enhance regional financial stability and promotion of regional economic development through – East African Payment System Harmonization Committee and MAC directives on:– Cross Border Settlement model for the region– Harmonization of oversight benchmarks– Internet payments, e-commerce and e-banking

• BIS guidelines on Risk Management principles for e-banking• Management and supervision of Cross Border e-banking

activities

Enabling Environment for Mobile Banking in Africa25

Way Forward• Way forward:

– Appreciation that the payment system will remain dynamic – • New opportunities, • Market requirements and • Technological developments

– Enactment of e-legislation [e-transactions, communications & information]

– Enactment of AML and CFT Legislation– Enactment of Modern Payment System Legislation (Large

Value payment systems (RTGS), Retail payment system)– Enhancement of Regulatory Capacity to ensure that safety and

efficiency are maintained and that the following Questions are continuously addressed:-

• Why Regulate?• How?• When?

Enabling Environment for Mobile Banking in Africa26

Are we ready for the transformation?