southern africa services exports 20 th february 2008 tralac conference, cape town dr. nick...

TRANSCRIPT

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Southern Africa Services Exports

20th February 2008

TRALAC Conference, Cape Town

Dr. Nick Charalambides

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Context

ServicesLiberalisation

Export competitivenessAgic, Manufacture

ServicesExports

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Overview

• Where are there opportunities?

• What is happening at country level?

• What are the key drivers of services exports?

• Where is there most scope for “home grown” producers?

• What are the constraints for services exports?

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Global TrendsUS$ billions

0

500

1000

1500

2000

2500

3000

1996 2005

Travel

Transport

Commercial

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

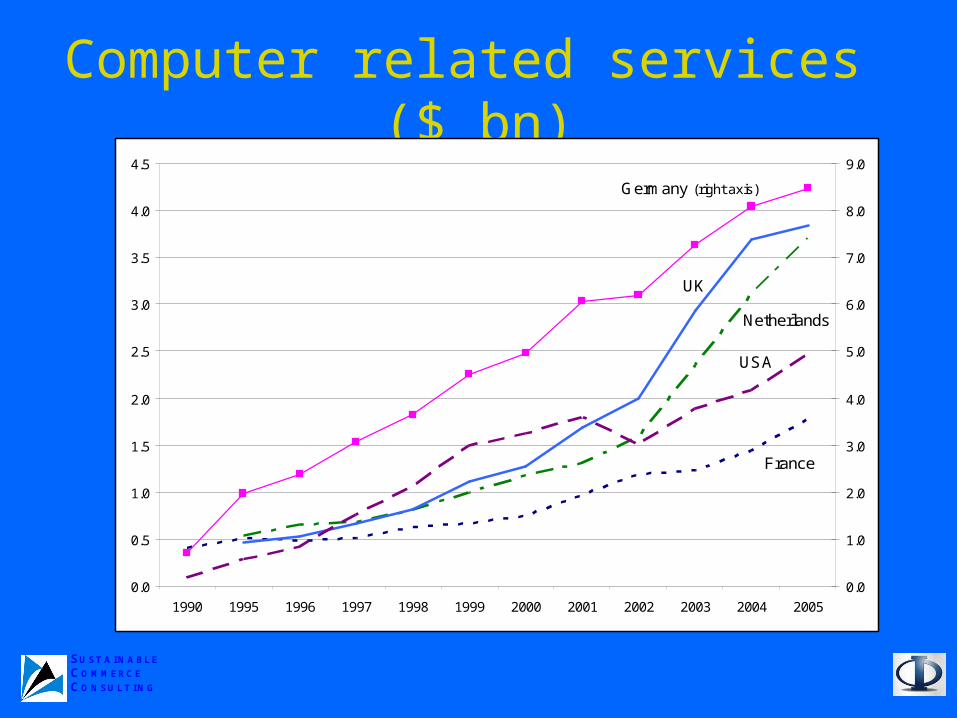

Computer related services ($ bn)

France

Netherlands

UK

USA

Germany (right axis)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1990 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Not only India

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Services exports: Botswana

0.0

5 000.0

10 000.0

15 000.0

20 000.0

25 000.0

30 000.0

35 000.0

Pu

la m

illio

n

Exports of services

Exports of goods

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Services exports: Mauritius

60.5%21.8%

11.9%

1.6%

1.5%

1.3%Travel

Transportation

Other business services

Communicationsservices

Computer andinformation services

Financial services

Construction services

Insurance services

Personal, cultural,

Health

Education

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Key drivers of exports?

• Characteristics of services: Often intangible– Brand and Reputation– Network of established customers

• FDI has been fundamental in many export success stories

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

FDI and Services Exports

• E.g. of Mauritius the key exporting sectors of tourism, offshore banking and BPO, foreign firms account for 84%, 90%, and 80% respectively of total employment

• Botswana: In tourism, Of the 331 enterprises licensed and operating between March 1997 and February 2001, more than two thirds were foreign

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

FDI and Services Exports: Ireland

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Opportunities for Home Grown?

• High technical content, low operational risk

• Regional Approach?– Education– Financial services– Construction (S.A. Madagascar)– Business services

• Niche? Where might the edge be?

TTTT SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Mobile phone boom in Africa

Source : ITU, 2006

1998

120

80

40

0

Million users, from 1998 to 2005

Fixed phone

Internet

Mobile phone

2005

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

M applications?

• The fortune at the bottom of the pyramid:– Wizzit, MPESA, Smartswitch– Trade @ Hand– Too often donor driven

• Tailor made content

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Constraints: Market Access

• Barriers vary greatly by sector, mode, by country• But OECD markets are generally open to CRS,

ITES (banking, accountancy, professional)– Challenges generally relate to second order issues

• Data protection (Domestic)• MRA• Visas (Business Travel Card)

• Regional: many constraints

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Constraints: Business

• Reputation and Profile

• Market information: 48% of Mauritian owned enterprises find market information a serious constraint; 23% for foreign owned. Services Export Help Desk

• Skilled labour

• Need for fast adaptation of regulation

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Constraint to Opportunity

• Regional centres of excellence

• Mutual recognition

• Regional labour market

• …Build and share expertise

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Liberalisation not sufficient

• High costs of business services

• But:– “We are at the “end of the road” (Namibia)– Sectors are already open but there is little

investment (Lesotho), – New entrants have not lowered prices by

much (Mozambique)

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Regulation is key to your competitive edge

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Some challenges

• Why is Botswana, Swaziland not exporting advertising, BPO, legal services… to the most important hub of economic activity in southern African

• … which is one hour away by plane

• What opportunities are there in the region?

• Where is the edge for local entrepreneurs?

SU ST A IN ABLE C O MMERC E C O N SU LT IN G

Thank you