southern copper overview and highlights · 1 copper contained in reserves based on us$1.20 per...

TRANSCRIPT

SOUTHERN COPPER

Overview and Highlights

May, 2008

Safe Harbor Statement

This presentation contains ‘‘forward-looking statements,’’ as defined by federal securities laws, withrespect to our financial condition, results of operations and business, and our expectations or beliefsconcerning future events. These statements include words such as, but not limited to, ‘‘expect,’’‘‘anticipate,’’ ‘‘believe,’’ ‘‘intend,’’ ‘‘plan,’’ ‘‘seek,’’ ‘‘forecast,’’ ‘‘estimate,’’ ‘‘continue,’’ ‘‘may,’’ ‘‘will,’’‘‘would,’’ ‘‘could,’’ ‘‘likely,’’ and similar expressions. These forward-looking statements reflectmanagement’s current expectations and assumptions regarding future events and operating andmanagement s current expectations and assumptions regarding future events and operating andfinancial performance and are based on currently available information. However, actual results aresubject to risks and uncertainties, which could cause actual results to differ materially from thosecontained in the forward-looking statements.

Many risks and uncertainties are inherent in the copper industry. Others are more specific to ouroperations. Additional information about risks and uncertainties that could affect our future resultsare contained in our SEC filings, including our reports on Forms 8-K, 10-Q, and 10-K and aregistration statement on Form S-3 relating to our proposed public offering of common stockregistration statement on Form S-3 relating to our proposed public offering of common stock.

1

I. Introduction

Management Presenters

Presenters TitleGenaro Guerrero

Raúl Jacob

Executive VP and CFO

Manager of Financial Planning & IR

3

Corporate Structure

75.1%

Public Float

24.9%

99.29 % 99.95 %

SCC Peru Branch Minera México

4

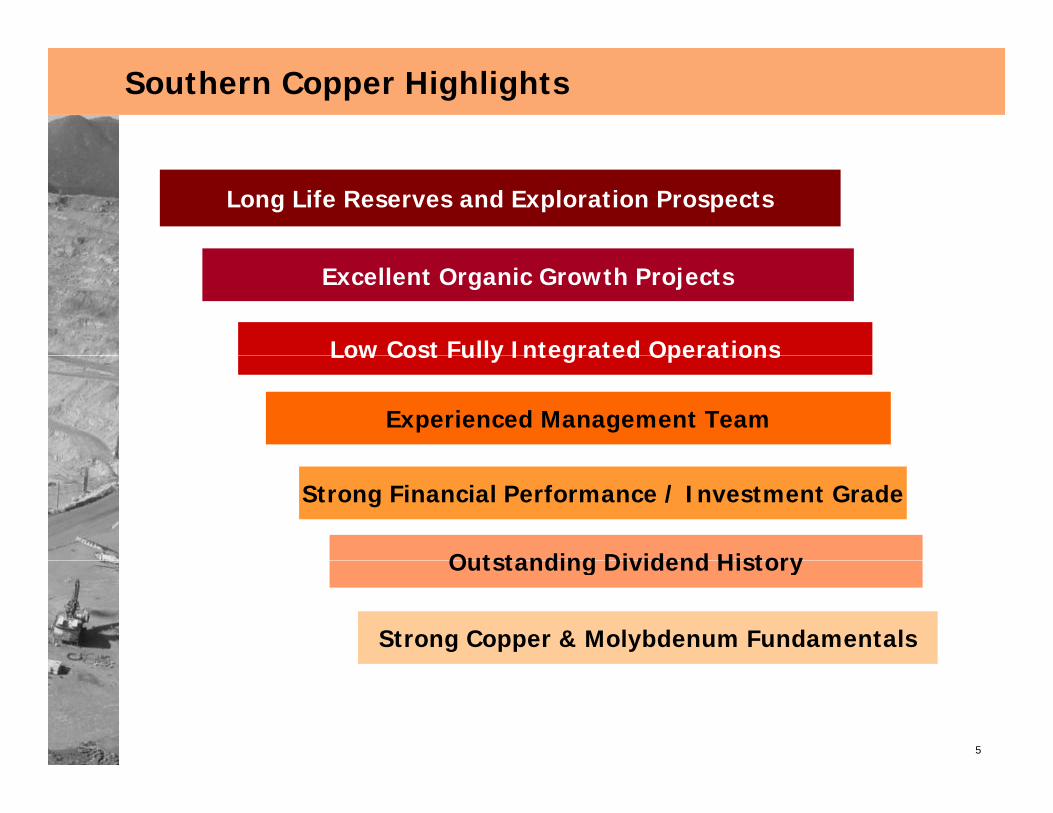

Southern Copper Highlights

Long Life Reserves and Exploration Prospects

Excellent Organic Growth Projects

Low Cost Fully Integrated OperationsLow Cost Fully Integrated Operations

Experienced Management Team

Outstanding Dividend History

Strong Financial Performance / Investment Grade

Outstanding Dividend History

Strong Copper & Molybdenum Fundamentals

5

Southern Copper Business Strategy

L ld l d l tiLeverage our world-class reserves and exploration

prospects

– Develop portfolio of value enhancing projects

Low cost, pure copper play

– Strategic investments focused on cost reduction

– Increase copper production, reserves and continue exploration

Investment grade capital structure with focus on cash flow

generationgeneration

– Return excess capital to investors

St k h d t k i ti

6

– Stock repurchase program and stock appreciation

Copper Price Trends

Strong underlying fundamentals with potential to change the long-term g y g p g gaverage of copper prices

Real Copper Price Trends (US producer) (in US$1998)

1900—1933 1934—1973 1974—2002 Today1

$ $ $ $Technological advances

Economies of scale reduce unit costs and real prices

Construction programs after WWII

US consumer boom

Substitution/conservation reduce Cu consumption

Shift from manufacturing to service economies

Increased demanddriven by China and emerging nations

Low inventories

Average: US$2.13/lb Average: US$1.61/lb Average: US$1.36/lb Current Price: US$3.54

real prices Industrialization of Japan led to rising real prices

to service economies

Processing efficiency lowers costs

Low inventories

Supply disruptions

New projects: Low ore grades and delays

$3 00

$3.50

$4.00

$4.50

$1.50

$2.00

$2.50

$3.00

US$

/lb

$0.00

$0.50

$1.00

1900 1907 1914 1921 1928 1935 1942 1949 1956 1963 1970 1977 1984 1991 1998 2005

33 years 40 years 29 years

2006 2007 2008

7

Source: USGS, Thomson Financial DatastreamNote:1 Average as of March 31st, 2008

II. Overview of Operations

i

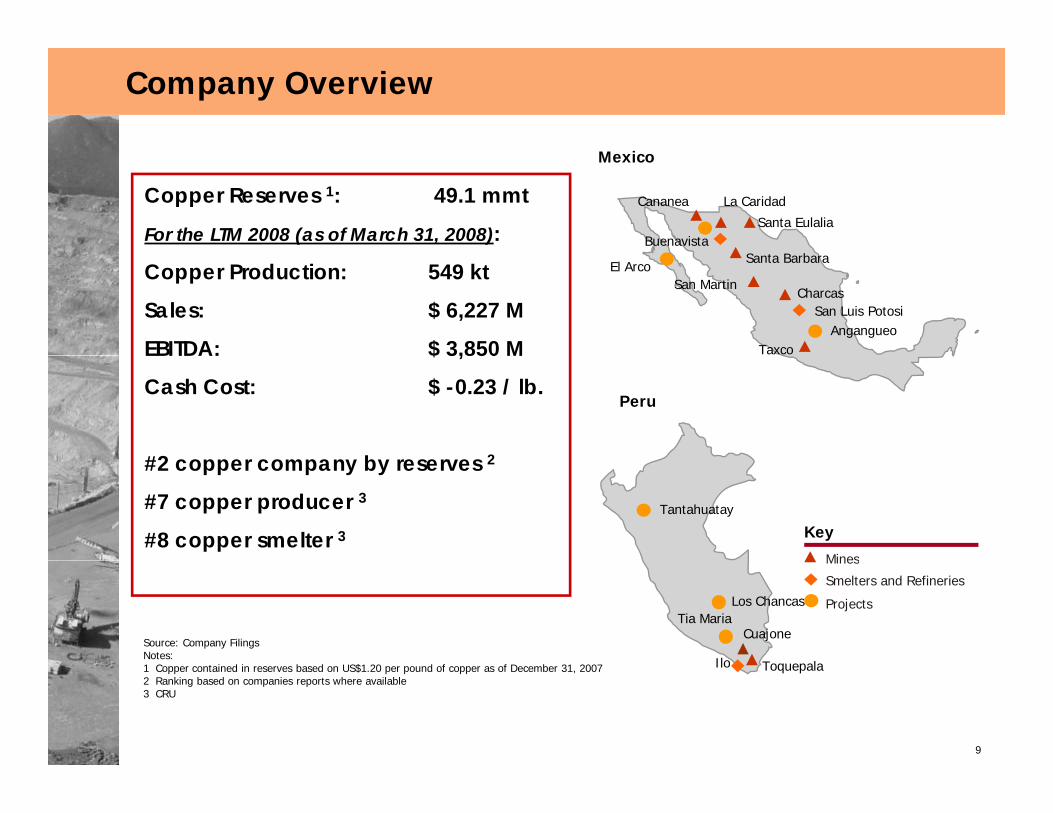

Company Overview

Mexico

La Caridad

S b

Santa Eulalia

Cananea

Buenavista

Copper Reserves 1: 49.1 mmt

For the LTM 2008 (as of March 31, 2008):Santa Barbara

Charcas

Taxco

San Luis Potosi

El Arco

Angangueo

Copper Production: 549 kt

Sales: $ 6,227 M

EBITDA: $ 3,850 M

San Martin

Peru

EBITDA: $ 3,850 M

Cash Cost: $ -0.23 / lb.

#2 b 2

Mines

Key

#2 copper company by reserves 2

#7 copper producer 3

#8 copper smelter 3Tantahuatay

Ilo

Cuajone

T l

Los Chancas

Mines

Smelters and Refineries

ProjectsTia Maria

Source: Company FilingsNotes:

9

Ilo Toquepala1 Copper contained in reserves based on US$1.20 per pound of copper as of December 31, 20072 Ranking based on companies reports where available3 CRU

SCC MinesTotal copper production in 2007 amounted to 592 kt

Copper production 1: 99 kt

– 17% of total

Copper production 1: 125 kt

– 21% of total

Cananea — Mexico La Caridad — Mexico

– 35% SX-EW 2, 65% mill 3

Reserves 4: 19 Mt

– 39% of totalSilver production: 0.8 M Oz

– 18% SX-EW 2, 82% mill 3

Reserves 4: 5.2 Mt

– 10% of totalMolybdenum production: 6.2 ktp

Gold production: 6.9 k Oz

y p

Silver production: 1.9 M Oz

Gold production: 4.2 k Oz

Toquepala PeruCuajone Peru

Copper production 1: 182 kt

– 31% of total– 100% mill 3

Copper production 1: 178 kt

– 30% of total– 21% SX-EW 2, 79% mill 3

Toquepala — PeruCuajone — Peru

Reserves 4: 9.1 Mt

– 18% of totalMolybdenum production: 3.8 kt

Silver production: 2 2 M Oz

,Reserves 4: 15.7 Mt

– 32% of totalMolybdenum production: 6.2 kt

Silver production: 2 0 M Oz

10

Silver production: 2.2 M Oz

Gold production: 4.9 k Oz

Silver production: 2.0 M Oz

Gold production: 2.4 k OzSource: SCC1 Production includes copper in concentrate and SX-EW cathodes2 Solvent Extraction / Electrowinning process3 Mill: A plant in which ore is treated and metals are recovered or prepared for smelting4 Copper price of $1.20 / lb used to calculate reserves

SCC Metallurgical Complexes Three main metallurgical complexes

Caridad – Mexico Ilo – Peru

Copper Smelter

Electrolytic Copper Refinery

Copper Smelter

Copper Refineryy pp y

Precious Metal Refinery

Rod Plant

Sulfuric Acid Plant

pp y

Precious Metals Refinery

Sulfuric Acid Plant

San Luis Potosi – Mexico

Total copper smelting capacity:

– 2,200 kt per year in concentrate feed, standard equivalent of 640 thousandSan Luis Potosi – Mexico

Electrolytic Zinc Refinery

Copper Smelter

Sulfuric Acid Plant

standard equivalent of 640 thousand tons of contained copper

Total copper refinery capacity:

– 580 kt per year in refined cathode

l i l fi iSulfuric Acid Plant Total precious metals refinery capacity:

– Silver: 19.4 M oz

– Gold : 117 K oz

Total zinc refinery capacity:

11

Total zinc refinery capacity:

– 105 kt per year in refined zinc

Total sulfuric acid capacity:

– 2,796 kt per year

Long Life Reserves

First largest copper reserves of any publicly traded companyg pp y p y p y

Copper Reserves SCC Copper Reserves Sensitivity

42.1

49.150.3

40

50

60

rves

(Mt)

69.9

6070

rves

(Mt)

42%

8.710.2

16.517.322.9

25.6

10

20

30

Cop

per R

eser 49.1

38.2

102030405060

er C

onta

ined

in re

ser

29%

2006

2007

SEC

Source: SCCSourc Annual Rep 10K 10K 20F Annual Rep 20F Reserve Rep Annual Rep Annual Rep

0

Cod

elco

SC

C

FCX

BH

P B

illito

n

Ang

loA

mer

ican

Rio

Tin

to

Xst

rata

Ant

ofag

asta

CV

RD

-Inco

010

0.90 1.20 2.664Copper prices ($/lb)

Cop

pe

Source: SCCSourc Annual Rep. 10K 10K 20F Annual Rep. 20F Reserve Rep. Annual Rep. Annual Rep.

Period 06/12/31 07/12/31 07/12/31 07/06/30 07/12/31 07/12/31 07/06/30 07/12/31 06/12/31

Cu Price N/A $1.20 $1.20 $2.00 N/A $2.31 N/A N/A N/A

12

Low Cost of Operations

SCC’s cash cost is in the bottom quartile of global copper producers

0.6

Low Cost Drivers

q g pp p

Net Operating Cash Costs (1)

High quality reservesStrong by-product credits (1)

-0.17

0.160.03

0.18

0.44

0

0.2

0.4

(US$

/lb)

Strong by product credits – molybdenum (18% of revenues) – zinc (6% of revenues)– silver (4% of revenues)– gold & others (3% of revenues)

-0.23

-0.4

-0.22003 2004 2005 2006 2007 LTM 2008

g ( )Significant low cost SX-EW production (2)

– 94 kt or 12% of copper production in 2007Large scale minesManagement focus on cost efficiencyCash Cost per Pound Produced, excluding

By-Product Credits Cost by Elements (1)

Other11%

Operating Materials

16%1.28

1.481.40

1 01

1.50

1.80

Maintenance17%

Labor

Fuel13%

1.010.85

0.74

0.00

0.30

0.60

0.90

1.20

(US

$/lb

)

13

Source: Southern Copper Notes: (1) Includes by-product credits.

Notes:(1) LTM as of March 31, 2008(2) Solvent Extraction / Electrowinning process.

Labor16% Energy

27%

2003 2004 2005 2006 2007 LTM 2008

Geographic and Product Diversification

SCC has broad geographic and product diversification

2007 SCC Revenue by Product

g g p p

2007 SCC Revenue by Market

Zinc6%

Silver4%

Other3%

Peru2%

Asia9% Latin America

19%

Molybdenum18%

Europe24%

United StatesCopper

69%

Mexico20%

United States26%

14

Experienced Management Team

SCC’s team has an average of 30 years experience with the Companyg y p p y

As a result of the SCC–MM merger, the management teams of both companies have been

seamlessly integratedGermán Larrea

Chairman of the BoardChairman of the Board

Oscar González RochaCEO SCC &

President - Peru

Xavier García de Quevedo

Genaro Guerrero

VP-Finance (CFO)

Vidal Muhech

VP - Environmental

Armando Ortega

General Counsel

Mario Vinageras

VP - Commercial

Gabino Paez

VP - Human Resources

QCOO SCC &

President - Mexico

SCC is fully compliant with the Sarbanes-Oxley Act

Strong corporate governance provisions

– one class of shares

( )

– one class of shares

– pro-rata number of independent directors (4 of 13)

– Special Nominating Committee for independent directors

– Audit Committee for independent accountants, and to review internal audit procedures,

15

accounting and financial controls

– independent director oversight of any potential related party transactions

– Compensation and stock incentive plan committees

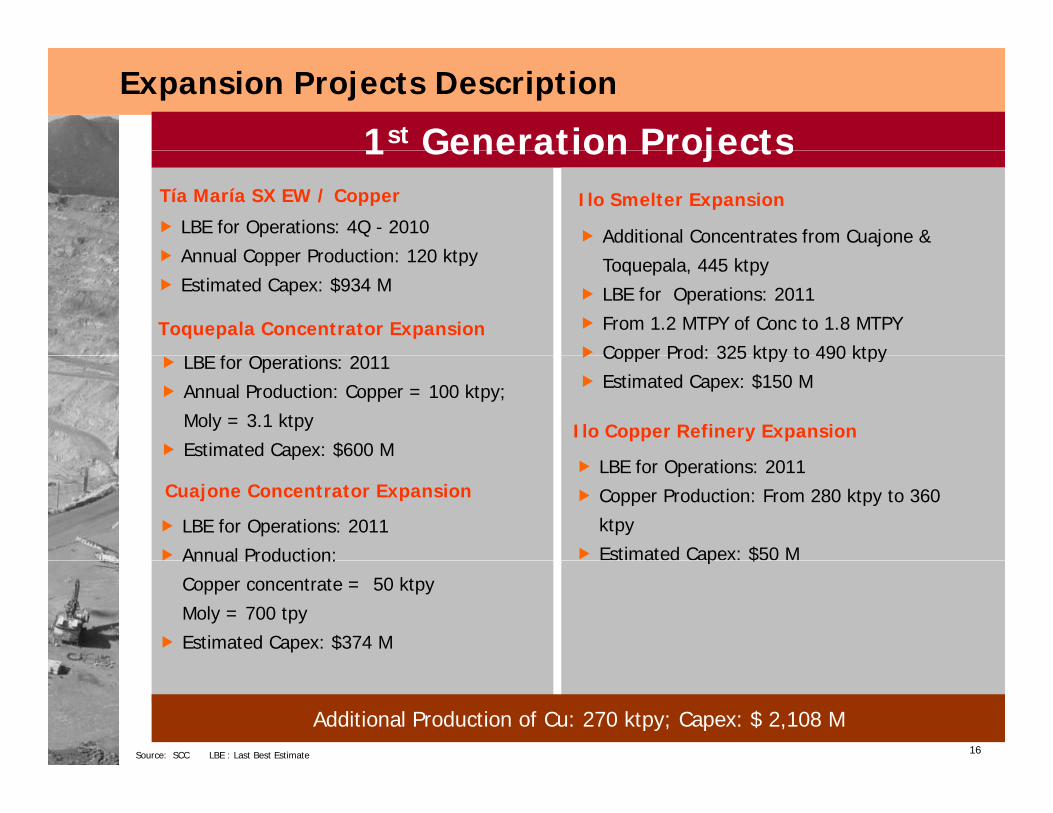

Expansion Projects Description

1st Generation Projects1 Generation Projects

LBE for Operations: 4Q - 2010

Annual Copper Production: 120 ktpy

Tía María SX EW / Copper Ilo Smelter Expansion

Additional Concentrates from Cuajone & Annual Copper Production: 120 ktpy

Estimated Capex: $934 M

Toquepala Concentrator Expansion

LBE f O i 2011

Toquepala, 445 ktpy

LBE for Operations: 2011

From 1.2 MTPY of Conc to 1.8 MTPY

Copper Prod: 325 ktpy to 490 ktpyLBE for Operations: 2011

Annual Production: Copper = 100 ktpy;

Moly = 3.1 ktpy

Estimated Capex: $600 M

Copper Prod: 325 ktpy to 490 ktpy

Estimated Capex: $150 M

Ilo Copper Refinery Expansionp $

LBE for Operations: 2011

Copper Production: From 280 ktpy to 360

ktpy

Estimated Capex: $50 M LBE for Operations: 2011

Annual Production:

Cuajone Concentrator Expansion

p $Annual Production:

Copper concentrate = 50 ktpy

Moly = 700 tpy

Estimated Capex: $374 M

16Source: SCC LBE : Last Best Estimate

Additional Production of Cu: 270 ktpy; Capex: $ 2,108 M

III. Financial Overview

Financial Summary

(US$ MM) 2003 2004 2005 2006 2007 LTM 20084(US$ MM) 2003 2004 2005 2006 2007 LTM 20084

Copper Price (LME) US$ per pound 0.81 1.30 1.67 3.05 3.23 3.44Income Statement:Net Revenues $1,577 $3,097 $4,089 $5,460 $6,086 $6,227COGS 992 1,334 1,635 2,020 2,122 2,176Gross Margin 584 1,762 2,454 3,440 3,964 4,050G g 58 ,76 , 5 3, 0 3,96 ,050SG&A 64 72 81 88 98 99EBITDA 493 1,702 2,335 3,316 3,766 3,850EBITDA Margin 31% 55% 57% 61% 62% 62%EBIT 326 1,482 2,071 3,054 3,497 3,575Interest Expense 117 106 109 113 123 122Net Income 84 982 1,400 2,038 2,216 2,230Balance Sheet Statement:Cash & Equivalents $352 $710 $876 $1,023 $1,409 $1,473Total Assets 4,491 5,319 5,688 6,376 6,581 6,778Total Debt 1 1,671 1,330 1,172 1,528 1,450 1,450Total Liabilit ies 2,386 2,494 2,349 2,696 2,716 2,760Total Shareholders' Equity 2,023 2,814 3,326 3,667 3,848 4,001Cash Flow Statement:Capital Expenditures 2 $65 $228 $471 $456 $316 $281Free Cash Flow 3 (0.1) 944 1,193 1,604 2,388 2,376( )Key Credit RatiosNet Debt / EBITDA 2.7x 0.4x 0.1x 0.2x 0.01x -0.01XEBITDA / Interest Expense 4.2 16.0 21.4 29.3 30.6 31.6

1 Includes short-term and long-term debt including current portion2 Includes capitalized stripping costs until 2005

18

2 Includes capitalized stripping costs until 20053 Free Cash Flow defined as net cash from operating activities less capital expenditures4 LTM as of March 31, 2008

Solid Financial Performance

Among the highest EBITDA margins and strongest leverage ratios in the g g g g gmetals & mining industry

2007 EBITDA Margin (%) Net Debt/ 2007 EBITDA (x)

62%

72%

SCC

Antofagasta -0.7x

-0.02xSCC

Antofagasta

46%

51%

FCX

BHP Billiton

0.5x

0.4x

AngloAmerican

BHP Billiton

42%

44%

Rio Tinto

Anglo American

1.0x

0.7x

Xstrata

FCX

e ca

39%

41%

Xstrata

CVRD - Inco

3.2x

2.7x

Rio Tinto

CVRD - Inco

19

Source: SCC; Company Reports

Focus on Total Return to Investors

Disciplined approach to creating shareholder value

Current Dividend Yield1 (%) 3-Year Share Price Performance1 (%)

p pp g

3 5%

6.3%

7.6%

Antofagasta

SCC

Anglo American

328%

439%

448%

Xstrata

SCC

CVRD

1.4%

1.7%

3.5%

Freeport

BHP Billiton

Antofagasta

In 2007, SCC paid US$2 Billi

291%

328%

333%

Antofagasta

Rio Tinto

Xstrata

1.3%

1.3%

Rio Tinto

Xstrata

US$2 Billion

US$6.80 per share

218%

242%

BHP Billiton

Freeport

0.5%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0%

CVRD 190%

0% 100% 200% 300% 400% 500%

Anglo American

20

Source: Bloomberg; Company FilingsNote:1 Regular and special dividends declared over last twelve months by record date

divided by current share price as of March 31, 2008 (SCC = US$103.83)1 As of March 31, 2008

Capital Expenditure Forecast (US$M)

$107

$1,200$1,085$1,070

$107

$199

$800

$1,000

$137 $

$333$213

$60

$45

$116

$226

$950 $965

$400

$600$471 $456 $500

$316$137 $121 $112$45$56$40

$143$230

$120 $120 $120

$328$226

$135$380

$127

$120$181

$0

$200$247

$316

2008- 2011 = US$ 2,108 M in First Generation Development

$02005A 2006A 2007A 2008E 2009E 2010E 2011E

All Other Projects

21Source: SCC

$ , p

US$ 480 M in Other Equipment Replacement Investments

SCC Debt Amortization ScheduleMillions of USD as of March 31, 2008

$1 000$1,000

SCC is evaluating the best financing option for its

j tprojects.

$150

$56

$200

$10$10$10 $10 $10$10$56

2008 2009 2010 2011 2012 2013 2015 2028 2035

22

Mitsui Yankee Bonds 10 & 30 year Bonds

SOUTHERN COPPER

Overview and Highlights

May, 2008