southern perspectives - mississippi state university

TRANSCRIPT

S O U T H E R NP e r s p e c t i v e s

EconomicImpact ofForestry

and ForestProducts in

the RuralSouth

VIEWS from the Director...

Alabama � Arkansas � FloridaGeorgia � Kentucky � Louisiana

Mississippi � North CarolinaOklahoma � Puerto Rico

South Carolina � TennesseeTexas � Virgin Islands � Virginia

VOLUME 3, NUMBER 2

SUMMER 1999

Meeting the Challenges of the Rural SouthThrough Land-Grant Scholarship and Outreach Education

he South is one of the fastest growing re-gions of the country. The 13-state area southof Kentucky and stretching from Virginia

to Texas is experiencing increased population, de-velopment, and importance. The South also has aprominent and economically important forest basethat supplies much of the U.S. with wood prod-ucts and helps support many rural communities.

In recent years, the Southern forest has becomemore strategically important for the nation�s sup-ply of forest products. Changes in timber avail-ability in other regions have tipped wood demandtoward the South. Accordingly, standing timberprices have increased, harvesting and reforestationhave accelerated and forestland has increased invalue. In addition, many Southern states have ex-perienced a boom of forest products industry de-velopment with associated economic impacts.

Studies have projected that the South will continueto be an important timber-producing region well

Putting forests on the economic and rural development radarscreenBob DanielsMississippi State University

T into the next century. The promise of excellentmarkets for Southern forest products in the futurepresents the region with a significant economicopportunity, if landowners can be shown how andwhy to increase timber production on the South�smillions of forest acres. At the same time, there arequestions of wildlife habitat, water quality protec-tion and many others that must be considered.How can the South capture the economic gainsthat are forecasted while protecting the quality ofthe environment?

The job of capturing this economic opportunityrequires the cooperation of many players. To date,the task of telling forestland owners about this op-portunity has been left to foresters, but economicand rural developers have a part to play in this op-portunity for our region. �Growing what we have�has long been a principle of economic development.In the current situation with the South�s forests,this principle can and should be applied.

continued

It is a well understood fact that the long-term healthof any community is closely linked to the strengthand diversity of its economic sector. That is whyso many rural communities are exploring a vari-ety of strategies to further expand the economicbase. In some cases, the approach has entailed theenhancement of businesses and industries that cur-rently exist in these localities. In other instances,the effort has been focused on promoting entre-preneurial, home-based, and micro-business activi-ties. And in still other situations, showcasing theareas� natural amenities�through eco-tourism,farm tourism, and recreational efforts�have provenquite effective.

In this issue of Southern Perspectives, we showcasea sector of our Southern economy that has been,and will continue to be, a major force in the eco-nomic well-being of countless families and com-munities in the rural South�its forest system. Theauthors offer strong evidence to support their idea

that the forest community has contributed signifi-cantly to the welfare of many rural areas of theregion. As such, forestry can not be overlooked incurrent and future efforts to advance the region�srural development and economic developmentagendas.

With this issue of the SRDC newsletter, I will havecompleted two years as director of the Center. It ishard to believe how quickly time has passed. I wantto take this time to offer words of appreciation tothe many land-grant faculty and administrators,non-land-grant rural development colleagues, andcountless others who have supported our effortsover the past two years. We look forward to work-ing with you on the many exciting rural develop-ment opportunities that await all of us in the South.

Bo BeaulieuDirector

SOUTHERN Perspectives

2 SOUTHERNPerspectives Volume 3, Number 2

How can one discuss the future of the South without ad-dressing forests, especially given the importance of forests inthe Southern region? Greater cooperation is needed betweenforestry interests and economic/rural development organiza-tions. If the goal is rural development, and the rural South islargely forested, then there must be common ground for theseinterest groups to work together. If the goal is economic de-velopment and the forest is a source of raw material for manu-facturing there must also be common ground. If the forestindustry is to remain important in the South helping to sus-tain the forest is an economic development issue.

That is the focus of this theme issue of Southern Perspectives.How can closer relationships between economic/ rural de-velopers and the forestry community be developed? What

continued from page 1

hile numbers only tell part of thestory of the Southern forestry

economy, the importance of this particu-lar industry to rural communities is evi-dent by reviewing a few key statistics. In1996 for example, the industry employedmore than 550,000 directly in the lumber,wood products, pulp and paper, and pa-perboard sectors and hundreds of thou-sands indirectly. The value of shipmentsof these products was more than $100 bil-lion. Timber is the highest valued crop ineight Southern states and ranks among thetop three agriculture crops in all of the 13Southern states. [5]

Forest industries also rank among the topthree manufacturing industries in each ofthe Southern states and have higher eco-nomic multipliers than most other indus-tries. These industries tend to locate neartheir resource base and therefore are animportant factor in the rural economywhere they are located. [3] Add to thesefigures the hundreds of millions of dol-lars and thousands of jobs associated withSouthern forests, such as hunting, hiking,

Economic impact offorestry and forestproducts in the ruralSouthWilliam G. HubbardUniversity of Georgia

W

filters, carbon sequestration, archeologicalsites, and places for our youth to learnabout natural resources.

A vast, privately-held resourceRecent studies by the USDA Forest Ser-vice estimate that the Southern forest re-source covers more than 200 million acres.This accounts for close to 30 percent ofthe total U.S. forestland and 56 percent of

kind of information do economic developers need to be betterengaged with forestry? What information is available and whatis not? What do foresters need to know about economic devel-opment to be better partners in the effort? Can existing stateorganizations interface more often regarding forests? Whattraining is needed? What discussions need to begin? What or-ganizations should have common objectives? We want to ex-plore these questions and begin a regional dialogue about howforestry interests and economic developers can work togetherto maintain and enhance an economically important timberbase that also provides the quality of life inputs so vital for lifein the South.

Bob Daniels is an Extension Forestry Specialist in the Department of Forestry atMississippi State University.

fishing, alternative forest products (pinestraw, mushroom production, etc.), forestmanagement (reforestation activities, seed-ling production, prescribed burning, roadbuilding, etc.), and tax generation, and thedollar impact of our Southern forest re-source is simply astounding. In addition,our Southern forests provide a number ofenvironmental and social benefits, such asnon-game wildlife, watersheds and water

Figure 1. Land cover in the U.S. South

*Estimated for the 18 counties in eastern Oklahoma and the 43 counties in eastern Texas covered by theUSDA Forest Service forest survey.

SOUTHERN Perspectives

SOUTHERN 3PerspectivesSummer 1999

dominant force in our rural Southerneconomy.

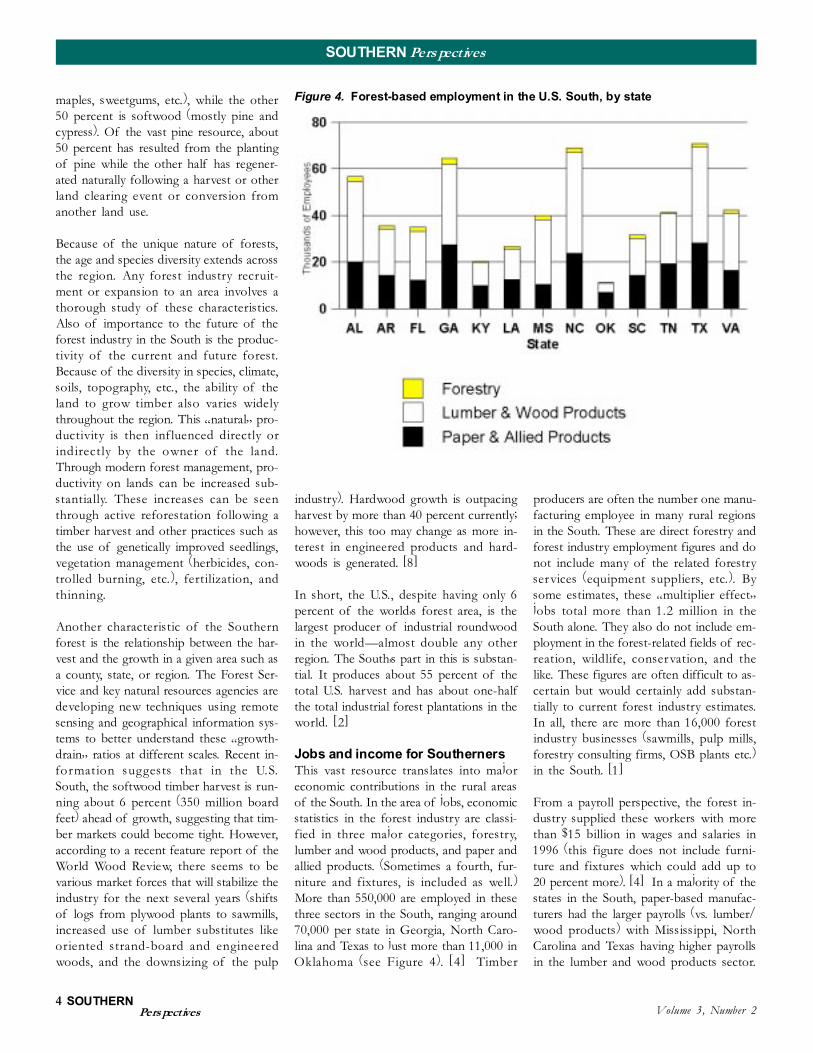

It also is helpful to look at the relative sizeand comparative numbers of these own-erships because the management theselandowners undertake and the goals andobjectives they hold are often correlatedwith the number of acres they own. Ofthese five million landowners, less than 1percent own more than 1,000 acres whileclose to 74 percent own less than 20 acres.Another 20 percent own between 20 and100 acres and the final 5 percent controlbetween 100 and 1000 acres. From an acre-age perspective, roughly 32 percent of thesouthern forests are held in tracts of 100acres or less, 25 percent are between 100and 1,000 acres, and 43 percent are in tractsmore than 1,000 acres. What these last twosets of statistics tell researchers is that thereare relatively few owners owning a major-ity of the resource. The remaining owner-ships are fragmented and tend to getsmaller and smaller. In 1978, the Southhad an estimated 3.9 million landowners.Today it is estimated there are more than4.9 million, ranging from more than700,000 in North Carolina to just under150,000 in Louisiana (see Figure 3). [7]

Forest characteristics and timbersupply summarizedWhat does this vast resource look like?The millions of acres in the South are apatchwork of natural and planted stands.They hold hundreds of different speciesfrom oaks and maples to Southern pineslike longleaf, slash, and loblolly. TheUSDA Forest Service, with assistance fromthe state forestry agencies, have undertakenperiodic inventories of our Southern for-est. These inventories are done on a state-by-state basis and vary widely from thewestern part of the region to the easternand from the north to the south. It is sucha diverse region because of its climate,soils, and topography that many naturalresource professionals separate it into threesubregions: the coastal plain, the pied-mont, and the mountains. Approximately50 percent of the forests in these regionsare considered hardwood (�Hardwood� isa broad grouping that consists of hundredsof kinds of trees like oaks, hickories, elms,

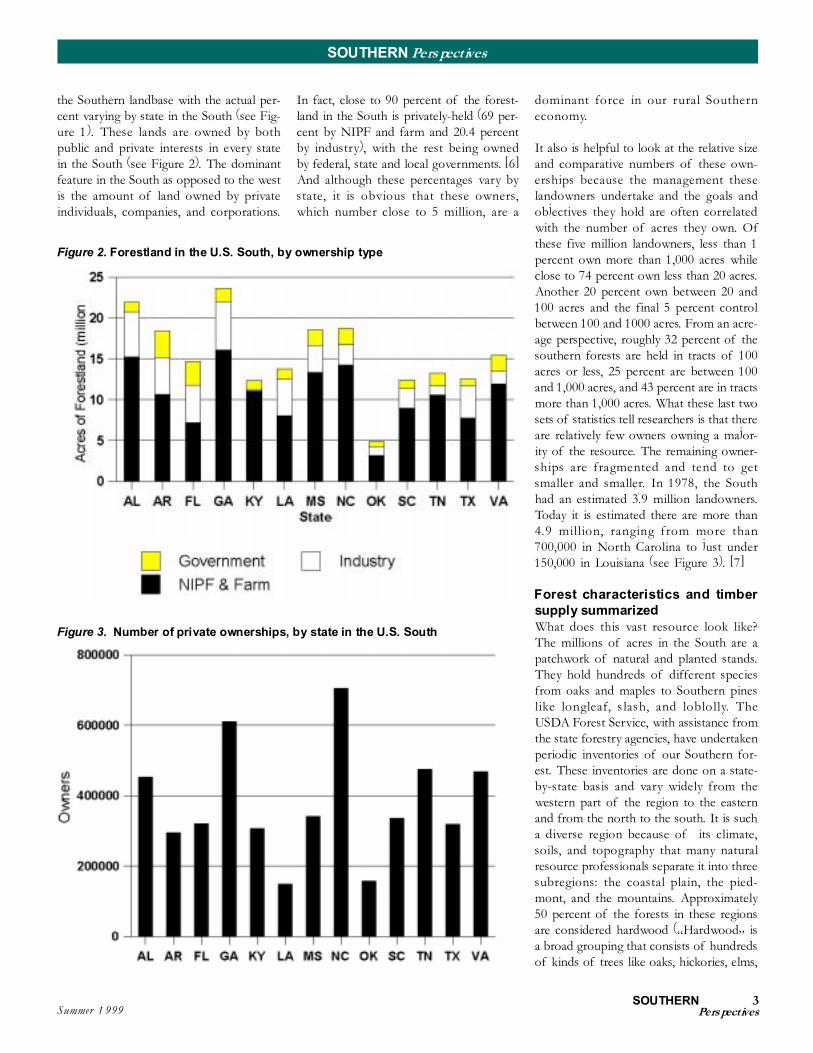

Figure 2. Forestland in the U.S. South, by ownership type

Figure 3. Number of private ownerships, by state in the U.S. South

the Southern landbase with the actual per-cent varying by state in the South (see Fig-ure 1). These lands are owned by bothpublic and private interests in every statein the South (see Figure 2). The dominantfeature in the South as opposed to the westis the amount of land owned by privateindividuals, companies, and corporations.

In fact, close to 90 percent of the forest-land in the South is privately-held (69 per-cent by NIPF and farm and 20.4 percentby industry), with the rest being ownedby federal, state and local governments. [6]And although these percentages vary bystate, it is obvious that these owners,which number close to 5 million, are a

SOUTHERN Perspectives

4 SOUTHERNPerspectives Volume 3, Number 2

maples, sweetgums, etc.), while the other50 percent is softwood (mostly pine andcypress). Of the vast pine resource, about50 percent has resulted from the plantingof pine while the other half has regener-ated naturally following a harvest or otherland clearing event or conversion fromanother land use.

Because of the unique nature of forests,the age and species diversity extends acrossthe region. Any forest industry recruit-ment or expansion to an area involves athorough study of these characteristics.Also of importance to the future of theforest industry in the South is the produc-tivity of the current and future forest.Because of the diversity in species, climate,soils, topography, etc., the ability of theland to grow timber also varies widelythroughout the region. This �natural� pro-ductivity is then influenced directly orindirectly by the owner of the land.Through modern forest management, pro-ductivity on lands can be increased sub-stantially. These increases can be seenthrough active reforestation following atimber harvest and other practices such asthe use of genetically improved seedlings,vegetation management (herbicides, con-trolled burning, etc.), fertilization, andthinning.

Another characteristic of the Southernforest is the relationship between the har-vest and the growth in a given area such asa county, state, or region. The Forest Ser-vice and key natural resources agencies aredeveloping new techniques using remotesensing and geographical information sys-tems to better understand these �growth-drain� ratios at different scales. Recent in-formation suggests that in the U.S.South, the softwood timber harvest is run-ning about 6 percent (350 million boardfeet) ahead of growth, suggesting that tim-ber markets could become tight. However,according to a recent feature report of theWorld Wood Review, there seems to bevarious market forces that will stabilize theindustry for the next several years (shiftsof logs from plywood plants to sawmills,increased use of lumber substitutes likeoriented strand-board and engineeredwoods, and the downsizing of the pulp

industry). Hardwood growth is outpacingharvest by more than 40 percent currently;however, this too may change as more in-terest in engineered products and hard-woods is generated. [8]

In short, the U.S., despite having only 6percent of the world�s forest area, is thelargest producer of industrial roundwoodin the world�almost double any otherregion. The South�s part in this is substan-tial. It produces about 55 percent of thetotal U.S. harvest and has about one-halfthe total industrial forest plantations in theworld. [2]

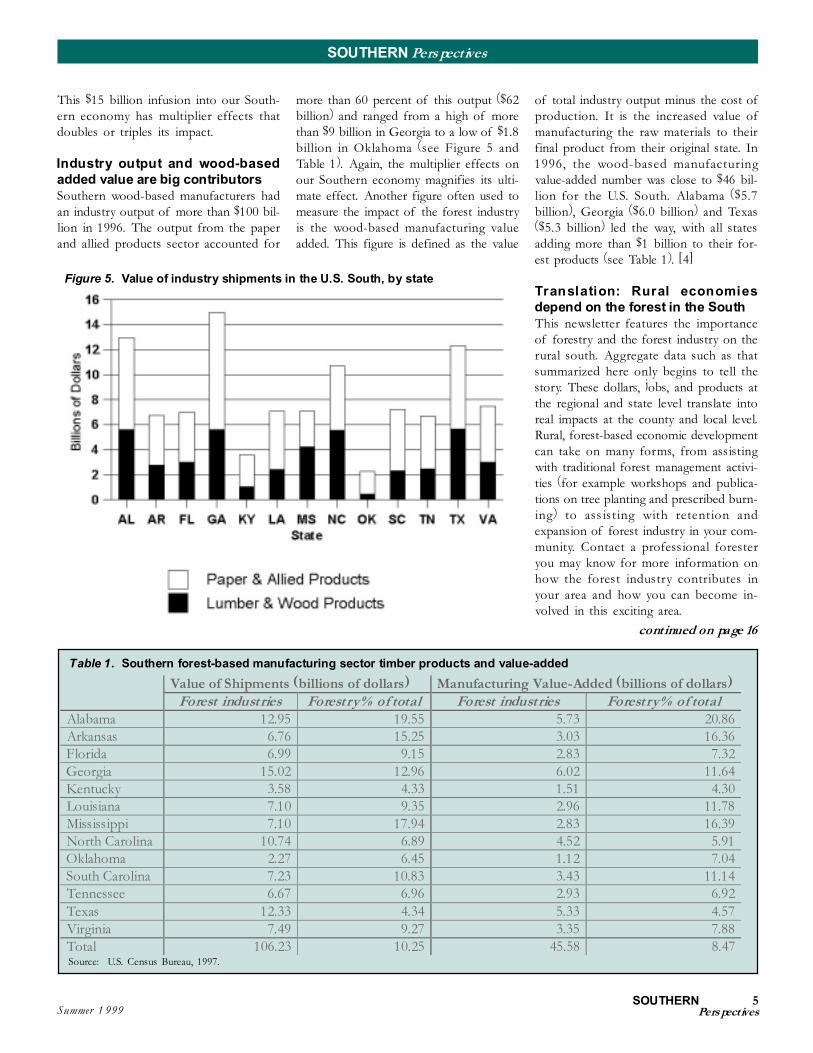

Jobs and income for SouthernersThis vast resource translates into majoreconomic contributions in the rural areasof the South. In the area of jobs, economicstatistics in the forest industry are classi-fied in three major categories, forestry,lumber and wood products, and paper andallied products. (Sometimes a fourth, fur-niture and fixtures, is included as well.)More than 550,000 are employed in thesethree sectors in the South, ranging around70,000 per state in Georgia, North Caro-lina and Texas to just more than 11,000 inOklahoma (see Figure 4). [4] Timber

producers are often the number one manu-facturing employee in many rural regionsin the South. These are direct forestry andforest industry employment figures and donot include many of the related forestryservices (equipment suppliers, etc.). Bysome estimates, these �multiplier effect�jobs total more than 1.2 million in theSouth alone. They also do not include em-ployment in the forest-related fields of rec-reation, wildlife, conservation, and thelike. These figures are often difficult to as-certain but would certainly add substan-tially to current forest industry estimates.In all, there are more than 16,000 forestindustry businesses (sawmills, pulp mills,forestry consulting firms, OSB plants etc.)in the South. [1]

From a payroll perspective, the forest in-dustry supplied these workers with morethan $15 billion in wages and salaries in1996 (this figure does not include furni-ture and fixtures which could add up to20 percent more). [4] In a majority of thestates in the South, paper-based manufac-turers had the larger payrolls (vs. lumber/wood products) with Mississippi, NorthCarolina and Texas having higher payrollsin the lumber and wood products sector.

Figure 4. Forest-based employment in the U.S. South, by state

SOUTHERN Perspectives

SOUTHERN 5PerspectivesSummer 1999

This $15 billion infusion into our South-ern economy has multiplier effects thatdoubles or triples its impact.

Industry output and wood-basedadded value are big contributorsSouthern wood-based manufacturers hadan industry output of more than $100 bil-lion in 1996. The output from the paperand allied products sector accounted for

more than 60 percent of this output ($62billion) and ranged from a high of morethan $9 billion in Georgia to a low of $1.8billion in Oklahoma (see Figure 5 andTable 1). Again, the multiplier effects onour Southern economy magnifies its ulti-mate effect. Another figure often used tomeasure the impact of the forest industryis the wood-based manufacturing valueadded. This figure is defined as the value

of total industry output minus the cost ofproduction. It is the increased value ofmanufacturing the raw materials to theirfinal product from their original state. In1996, the wood-based manufacturingvalue-added number was close to $46 bil-lion for the U.S. South. Alabama ($5.7billion), Georgia ($6.0 billion) and Texas($5.3 billion) led the way, with all statesadding more than $1 billion to their for-est products (see Table 1). [4]

Translation: Rural economiesdepend on the forest in the SouthThis newsletter features the importanceof forestry and the forest industry on therural south. Aggregate data such as thatsummarized here only begins to tell thestory. These dollars, jobs, and products atthe regional and state level translate intoreal impacts at the county and local level.Rural, forest-based economic developmentcan take on many forms, from assistingwith traditional forest management activi-ties (for example workshops and publica-tions on tree planting and prescribed burn-ing) to assisting with retention andexpansion of forest industry in your com-munity. Contact a professional foresteryou may know for more information onhow the forest industry contributes inyour area and how you can become in-volved in this exciting area.

Figure 5. Value of industry shipments in the U.S. South, by state

Table 1. Southern forest-based manufacturing sector timber products and value-added

Source: U.S. Census Bureau, 1997.

continued on page 16

Value of Shipments (billions of dollars) Manufacturing Value-Added (billions of dollars)Forest industries Forestry % of total Forest industries Forestry % of total

Alabama 12.95 19.55 5.73 20.86Arkansas 6.76 15.25 3.03 16.36Florida 6.99 9.15 2.83 7.32Georgia 15.02 12.96 6.02 11.64Kentucky 3.58 4.33 1.51 4.30Louisiana 7.10 9.35 2.96 11.78Mississippi 7.10 17.94 2.83 16.39North Carolina 10.74 6.89 4.52 5.91Oklahoma 2.27 6.45 1.12 7.04South Carolina 7.23 10.83 3.43 11.14Tennessee 6.67 6.96 2.93 6.92Texas 12.33 4.34 5.33 4.57Virginia 7.49 9.27 3.35 7.88Total 106.23 10.25 45.58 8.47

SOUTHERN Perspectives

6 SOUTHERNPerspectives Volume 3, Number 2

t the turn of the century, the origi-nal forests of the South werelogged. Many people have seen

the old photographs of logging in South-ern forests but most people don�t considerthe dynamics of wealth generated fromtimber, then and now�and its relation-ship to economic and rural development.

Few people realize that the wealth gener-ated by cutting the South�s original tim-ber went to a relative few companies andindividuals because the land was largelyowned by government, logging companiesor large landowners. By contrast, today,private, non-industrial owners hold most(70 percent) of the South�s forestland.When timber is harvested on these lands,the receipts go directly into family bankaccounts. These funds from timber salesare used to build new houses, repair andrenovate older homes, purchase new carsand trucks, send children to college, fi-nance retirements, and for many otherpurposes that greatly improve the qualityof life for rural and town residents. Thishas been true for many years, but its im-pact has been enhanced in the last 20 yearsbecause Southern timber values have in-creased significantly. On an annualizedbasis, Southern pine sawtimber prices in-creased at 4 percent real per year from 1977to 1995. [3] This economic impact hasbeen felt all across the region.

In addition, Southern forest productsmarkets have been good for many yearsand are projected to continue to be com-petitive for many more. [4, 2] This meansthat the economic potential for growingtrees in the South is excellent. The eco-nomic development community shouldnot overlook this source of rural wealthand economic development. Every acre offorestland in the region is a potential

The importance of forest management and timber harvests in local economies:A Mississippi exampleBob DanielsMississippi State University

A

source of revenue to improve the localeconomy and the lives of the owners.

This is why economic and rural develop-ers should become more involved withforest management and reforestation in theSouth. Managing forestland to its greatestproductive level is economic development.Promptly reforesting harvested forestlandsalso is economic development becausekeeping the land in full timber produc-tion boosts frequency and value of tim-ber sales. Additionally, productive land hasgrowing value for wildlife leases and otherincome-generating activities. And theseactivities can measure favorably with othermore traditional economic developmentefforts.

An exampleMississippi is an agricultural state in theheart of the Southern region. As in otherSouthern states, forests occupy a large per-centage of the land area, and private non-industrial owners hold most of that land.Mississippi has a timber severance tax thatis paid at the county level according tovolume of timber harvested. Therefore,using timber severance tax data from theMississippi State Tax Commission, thevolume of timber products harvested canbe determined. By using average prices fortimber products, we can estimate the valueof timber harvested and delivered annu-ally for each Mississippi county. [1] Thesetimber values make it possible to comparethe values of timber harvests with otheragricultural crops being produced in eachcounty and to get a larger picture of theimportance of forest products at the locallevel.

In 1997, timber was the second most valu-able agricultural crop produced in Missis-sippi with a delivered value (delivered tothe first point of processing, like logs tothe sawmill yard) of $1.31 billion. Theonly agricultural product of greater valuewas poultry and eggs at $1.43 billion.

Mississippi has a total of 82 counties. Tim-ber was the most valuable agricultural cropin 49 counties, the second most valuablein 17 counties and third most valuable in2 counties in 1997. Figure 1 shows theMississippi counties where timber produc-tion was among the top three most valu-able agricultural crops in that county for1997. In all, 68 counties of 82 (83 percent)had timber as an important part of its ag-ricultural economy. In the 49 countieswhere timber was the most valuable agri-cultural crop the values ranged from a lowof $5.0 million to a high of $39.2 million.

Maps like Figure 1 have been developedfor every year since 1990 and the patternof timber values is consistent. Table 1shows the number of Mississippi countieswhere timber ranked among the top threeagricultural crops for the years 1990-1997.For any year between 1990 and 1997, tim-ber was the most valuable agricultural cropin 35 to 51 counties and among the topthree crops in 65 to 70 counties out of 82.While timber values may be a small partof the local economy in a county likeHinds, where Jackson (Mississippi�s larg-est city) is located, in more rural countiestimber is a very important part of the lo-cal economy.

The delivered value of timber is useful torank crops in local county economies butthe standing or stumpage value is thevalue actually received by the landownerfor the timber sold. This is the amountthat goes into the family bank accountfrom the timber sale. In 1997, the esti-mated standing timber value collected byall Mississippi landowners for their tim-ber was $1.02 billion. In counties wheretimber was among the top three agricul-tural crops for that year, the county stand-ing timber values ranged from a low of$4.0 million to a high of $32.3 million. Incounties where timber was the most valu-able crop, the standing timber income tocounty landowners averaged $13.2 million.This means that in the 49 Mississippicounties where timber was the top crop,Managing forestland to its greatest productive level is economic

development.

SOUTHERN Perspectives

SOUTHERN 7PerspectivesSummer 1999

activities are generating similar incomes in local economies inmost Southern states. And they could generate more becausemany forest owners do not manage their forestland.

What it all meansGiven the prospect of the location of a manufacturing plantthat would pay $13 million annually in wages in their countyor area, most economic development officers would be veryactive trying to assist the business prospect so that the plantwould locate in their area. This is as it should be. However,forestry today is producing significant economic effects in hun-dreds of counties across the South. In many local areas the ef-forts of local economic and rural developers are needed to helpperpetuate and increase the economic impacts of forest manage-ment.

A guiding principle of economic and rural development is to�grow what you have.� The opportunity exists for many ruralareas to increase the productivity of their forestland and increasethe income of local economies and landowners because demandfor Southern forest products is expected to rise in the future. Inaddition, planning for the region�s future requires considerationof the Southern forest that will be a source of wood to supplyour industry, and provide recreation, wildlife, water and manyother benefits. Promoting forest management, reforestation af-ter timber harvest and the principle of keeping forestland pro-ductive for generations are very legitimate economic and ruraldevelopment activities in the South. These efforts are also neededbecause of the local economic importance of forestry in Missis-sippi and in many other rural areas across the South.

New relationships between forestry organizations and economicand rural development organizations are needed to tap the addi-tional economic potential in the southern forest and conserveother forest benefits. By working together, foresters and eco-nomic developers can create a forest that serves the economicand social needs of the South for the future.

References[1] Daniels, Bob. 1998. 1997 Harvest of Forest Products. Mississippi State Exten-sion Service, Market Note. October, 1998:10.

[2] Ince, Peter J. 1994. Recycling and Long-Range Timber Outlook. BackgroundResearch Report 1993 RPA Assessment Update. USDA Forest Service. ResearchPaper FPL-RP-534.

[3] Stewart, Peter, J. and Jeffrey Wikle. 1996. Estimating Timber Supply andDemand Over the Next 5 Years. Forest Landowner Vol. 55, No.4:5-11.

[4] USDA Forest Service. 1988. The South�s Fourth Forest: Alternatives for theFuture. Washington DC: Forest Resource Report No. 24:512.

Bob Daniels is an Extension Forestry Specialist in the Department of Forestry atMississippi State University

Table 1. Number of Mississippi counties where timberproduction was economically important, by year, 1990-1997

Figure 1. Timber production rank by county, 1997

the results of past forest management generated an average of$13.2 million in income for landowners who sold timber.

All Southern states don�t have access to tax records that allowestimation of timber receipts by county but the situation de-scribed here for Mississippi is not unique. Forest management

Rank Compared to OtherAgricultural Crops

Year #1 #2 #3 Total

1990 42 23 2 671991 35 27 3 651992 42 20 6 681993 50 15 3 681994 42 26 2 701995 46 20 3 691996 51 16 2 691997 49 17 2 68

SOUTHERN Perspectives

8 SOUTHERNPerspectives Volume 3, Number 2

here does one begin when incorporating forest-basedeconomic development into the rural economic

developer�s tool kit? Many find the myriad of informa-tion and training in this development arena overwhelming anddifficult to ascertain. A number of researchers, policy makers,and practitioners have written on this topic. A summary of asome of these articles may help in understanding forest-basedeconomic development strategies, as well as information andtraining needs of today�s rural economic development special-ist.

According to Syme and Duke, conventional economic develop-ment strategies have been unsuccessful in rural areas due to aninappropriate set of assumptions. [2] These include the beliefthat 1) farming is still the major industry in rural areas; 2) therural sector is a separate entity, not connected to the overalleconomy or society; and 3) many rural areas do not have viablepolitical solutions.

Other problems include the lack of economic and social data onrural areas, the presence of organized opposition, and the lackof unified support for new rural development programs. Theystate that specific forest-based economic development strategieshave not been formulated.

These researchers developed a market-oriented strategic approachfor forest-based economic development in rural sectors of SouthCarolina. A heavily-forested rural area (two-county subregion)was targeted for analysis. This region has a large timber resource,but has only a small volume of forest products manufacturingwithin or near the subregion. The subregion�s objectives, re-sources, and capabilities were analyzed in depth. Potential mar-kets for wood products that could be manufactured in the sub-region were identified and analyzed. Target markets and theirhighest-potential wood products were selected, based on theirbest fit with the subregion�s capabilities. The researchers thenformulated a unique strategy for carrying out the forest-basedeconomic development program in the subregion, based on at-tracting a planned set of wood products processing businesses tocreate a manufacturing network.

The market-oriented methodology they incorporated includedsix basic steps.

The researchers believe this approach is applicable in other loca-tions in the South. The proposed manufacturing network, in-cluding both new and existing forest-related businesses, focusedon specific product businesses and provided an opportunity formember firms to gain and sustain a competitive advantage againstcompetitors outside the network.

Linking forest-based economic development and rural development: A reviewof the literatureWilliam G. HubbardUniversity of Georgia

W

Another way of looking at strategy development in an area is toask crucial questions with relation to forest-based economic de-velopment. According to Vlosky, the basic information needssurrounding this type of development can be grouped into fivecategories. These are resource assessments, industry structure,product/market strategy, economic impacts and social interac-tions. [4] An example of some of the critical questions is shownfor each category.

Rural development specialists working closely with forest prod-ucts, and forestry experts should be able to answer these ques-tions and those of a more localized nature.

In a related fashion, the Midwest Research Institute was com-missioned to look at natural resource strategies for rural eco-nomic development. [3] The study looked at various factors ofimportance to forest-based economic development. A list of dataneeds was devised by the principal investigators of the study.These included:

1. Commercial timber acreage. Acreage within the county orwithin a multi-county area that corresponds to the economicdevelopment organization�s service area is going to be needed.

1. A specific rural subregion appropriate for forest productmanufacturing consideration was selected for analysis anddevelopment.

2. An in-depth situational analysis was conducted that iden-tified the capabilities, resources, characteristics, and overalleconomic development objectives of the subregion in re-lation to potential expansion of the forest products in-dustry.

3. Potential markets for wood products that might be pro-duced in the subregion were identified and analyzed.

4. The current and future competitive environments relatedto the potential markets were analyzed.

5. High-potential markets and their wood product needs,which had the best fit with the subregion�s resources andcapabilities, were selected as target markets.

6. Alternative forest-related economic development strate-gies were assessed and a strategy was formulated for thesubregion.

Market-oriented methodology [2]

SOUTHERN Perspectives

SOUTHERN 9PerspectivesSummer 1999

Getting these data by species or forest typeor by age classes is even more useful. Insome situations, the data may be neededwithin a fixed radius area or a variable ra-dius area.

2. Timber ownership patterns. The acre-age and percent distribution of publiclyowned, industry-owned and private, non-industrially owned forest land will beneeded.

3. Timber volumes. Volume by species,ownership category, and-if available-byproduct class and quality would be desir-able.

4. Timber growth. Growth data by spe-cies and land ownership, as well as datashowing growth trends over time, are im-portant.

5. Timber mortality and drain. Losses,by species and ownership, plus trends overtime should be known.

6. Wood-using industries. The numberof industries in the area, their productsand competitors, and current and pro-jected wood consumption should be docu-mented.

7. Proximity to population centers. Aswith many other enterprises, the popula-tion centers are where much of the de-mand for your resources will originate.

8. Proximity to markets. Markets for for-est products may or may not be associ-ated with population centers. Railroads,waterways, and highways are major con-siderations in forest products transporta-tion and marketing systems.

9. Other demographic data. Are thereany unique characteristics about thepeople within the population centers nearyour rural area? Find out as much as youcan about the population to which youwill be marketing.

10. Transportation systems. What trans-portation systems are available in yourarea? This is an important considerationin developing secondary wood processing

industries. Transportation access may dic-tate the type of Industries that you are ableto attract.

11. Demand for potential products or ser-vices. In some cases, population and de-mographic information may not di-rectly translate to demand for products,particularly if the products and servicesare unique to the area. As you speculateon possible economic development activi-ties, you may find the need for more struc-tured market survey research to determinepotential demand.

12. Soil types and productivity potentialfor alternative crops. If you are consider-ing land use enterprises with specific soilrequirements, be certain you find out ifthose soil types exist in your area. Oftensoil types and soil productivity play a

major role in determining the success ofalternative land uses.

The report also gives examples of datasources and how the source might varyin, certain situations.

1. Various forestry-related statistics foryour county (timber volumes, acreage,ownership, and other data) should be avail-able from your local state agency forester,or a University Extension Forester. Thesedata originate from the U.S. Forest Ser-vices� forest inventory and analysis units.Local state agency foresters will likely haveaccess to these published inventory data,but if not, they will be able to help youaccess the Information by contacting theForest Inventory and Analysis Officewhich covers your state (also available onat http://www.srsfia.usfs.msstate.edu).

Basic information needs

Resource Assessmentu �Is the availability of timber resources a barrier to the development of the

value-added secondary forest products industry?�u �Is the focal region located within reasonable transporting distance of signifi-

cant standing timber inventory?�u �What are the trends: ownership, forestland acreage, growing stock, growth/

removals, sawtimber, diameter classes, species, etc.�

Industry Structureu �What is the structure of the established primary and secondary forest prod-

ucts industry base?�u �What types of manufacturing processes and equipment do current compa-

nies use?�u �Is there the presence of sawmills, dry kilns, millwork plants, OSB produc-

tion which could support significant development?�u �Are companies able to compete in the markets they serve?�u �How have these companies which have grown and prospered done so? (Ex-

ploiting specialty niches, cutting costs, etc.)�

Products/Marketu �What is the product mix of the companies?�u �What are the current markets and customer bases? (Both domestic and

export)?�u �What is the quality and level of acceptance in current markets?�u �What is the distribution reach?�

Economic Impactsu �What economic impacts result from forest-based industry development?�u �What are the ramifications at the community, regional, and state levels?�

SOUTHERN Perspectives

10 SOUTHERNPerspectives Volume 3, Number 2

2. Demographic data should be availablefrom several sources including the Exten-sion Service, Chamber of Commerce, andothers. Much of the data will originatefrom national sources such as the Depart-ment of Commerce.

3. Soils data will be available through theUSDA Natural Resource ConservationService. Soil survey reports are publishedfor many counties in the United States.These reports include information on pro-ductivity potential for various crops andtrees.

4. Assistance on marketing informationand feasibility studies should be availablefrom state economic development offices,the Cooperative Extension Service, anduniversity departments and centers. If notdirect assistance, at least good referrals toother community development organiza-tions should be available from thesesources.

5. Assistance on production and man-agement of various crops, products, andresources will be available from your statedepartment of agriculture.

Another area of interest to those in forestand natural resource management and inthe rural development field is the types oftraining and education useful in forest-based economic development. Smith, Al-derman and Hammett assessed the eco-nomic development community inVirginia to evaluate forest-based trainingneeds. [1] According to the authors, �Itwas felt that this group may not be awareof the importance of the forest productsindustry to Virginia and that by identify-ing their training needs, educational pro-

grams could be developed to assist theiractivities.� A survey was mailed to 450individuals involved in economic devel-opment throughout Virginia. More than60 percent of respondents indicated thatbusiness recruitment was their primaryresponsibility. Fifty-eight percent re-sponded that the forest products indus-try was not a targeted area for them. Themost important training areas for eco-nomic developers included value-addedmanufacturing, local forest resource in-formation, local production characteris-tics, and the availability of financial re-sources for forest-based development.Other areas included new forest productstechnology, retention and expansion,wood products, domestic wood products,niche products/markets, evaluating wood-based enterprises and forest-based recre-ational activities. When asked the bestway to present information to economicdevelopers, respondents stated personalvisits, conferences, regional/local work-shops and classroom instruction were thebest methods. The results of their studyin Virginia will lead to targeted extensionprogramming to the economic develop-ment community in Virginia.�

In conclusion, the time for closer work-ing relationships between the natural re-sources community and the rural devel-opment community is now.Opportunities for expansion, recruitmentand improvement in the forest-based eco-

nomic development sector are high. A vastresource with an opportunistic, educatedwork force can result in a higher qualityof life for our Southern rural communi-ties. One of the first steps is to determinethe key players in the county or region ofinterest. These can be found by circulat-ing in both networks. Examples includethe Extension Service, the land-grant uni-versity, other colleges and technical insti-tutes, state forestry and natural resourceagencies, private forest industry, forestryconsultants, state and local rural develop-ment councils, and economic developmentoffices at the state or local level.

References[1] Smith, Robert, Delton Alderman and A.L.Hammett. 1999. �Evaluating Forest-Based EconomicDevelopment Training Needs in Virginia.� Forest Prod-ucts Journal Volume 49. Number 4:19-23.

[2] Syme, John H. and Charles R. Duke. 1994. �Mar-ket-oriented strategy for forest-based rural economicdevelopment.� Forest Products Journal Volume 44.Number 5:10-16.

[3] Thomas, Margaret G. 1990. Natural ResourceStrategies for Rural Economic Development. Mid-west Research Institute, Kansas City Missouri:36.

[4] Vlosky, Richard. 1997. �A Primer on Forest-Based Economic Development Planning.� Paper pre-sented at the 1997 Southern Forest-Based EconomicDevelopment Academy. Birmingham, Ala.

William G. Hubbard is Southern Regional ExtensionForester and is based at the University of Georgia.

The time for closer working relationships between the naturalresources community and the rural development community is now.Opportunities for expansion, recruitment, and improvement in theforest-based economic development sector are high.

USDA Forest Service initiates two-year study of Southern forest sustainability

The forests of the Southern United States supply 15 percent of the world�s timber from its 214 million acres. Questions havebeen raised over the past 10 years about how sustainable this amount of cut can be. To help answer these questions, the ForestService, in conjunction with other federal agencies and the Southern Group of State Foresters, will conduct a study over thenext two years of the region�s forested resources. The study will have broad implications for the non-industrial private land-owner because those land make up nearly 70 percent of the study area. Work will begin this summer. For more informationabout the study, visit the Forest Service�s web site at http://www.fs.fed.us.

SOUTHERN Perspectives

SOUTHERN 11PerspectivesSummer 1999

Responding to various federal, state, and local needs and opportunities, a multi-agency task force organized a three-day courseforest-based economic development. More than 100 natural resource, rural development, private sector representatives, and othersattended the academy. They heard from professionals in the various fields of study and application surrounding forestry and ruraldevelopment. Presentations were given on developing a forest-based economic development plan, the importance of forestry in thesouth, the sociological aspects of the Southern forest and its inhabitants, accessing and utilizing forest-resource information, andmany other topics. States brought teams of individuals representing the state forestry agency, the state extension service, the stateresource conservation and development agency, the Forest Service and others. They met throughout the Academy to develop astate plan of action. Since 1998, a number of states have held their own workshops and forest-based economic developmentactivities. A follow-up survey and web site are planned to continue the dialogue at the regional level. For more information, contactBill Hubbard at [email protected].

PublicationsBinkley, Clark S., Charles Raper and Courtland L. Washburn.

1996. Institutional Ownership of US Timberland. Jour-nal of Forestry Vol 94 No. 9 p. 21-28.

Birch, Thomas W. 1997. Private Forestland Owners of theSouthern United States, 1994. USDA Forest Service,Northeastern Forest Experiment Station, Resource Bul-letin NE-137. 195 pp.

Dangerfield, Coleman and Bill Hubbard. 1998. �ForestrySituation and Outlook with Implications for Agricul-ture, 1998.� Paper prepared for presentation at the Ex-tension Southern Agricultural Outlook Conference, At-lanta, Georgia, October 29, 1998. 35 p. (available at http://www.forestry.uga.edu/abstracts/fso98.html).

Hubbard, William G. and Frederick W. Cubbage. 1998. For-ests & the Southern Economy. Forest Landowners As-sociation Technical Report. 4 p. (for copies call 1-800-325-2954).

Kelly, L. Michael. 1996. �The benefits of viewing timber asan investment.� Forest Landowner. Vol. 55 No. 2. p. 51-70. March/April.

Moulton, Robert J. and Thomas W. Birch. 1995. �SouthernPrivate Forest Landowners: A Profile.� Forest Farmer Vol.54 No. 5. pp 44-46. September/October.

Southern Forest-Based Economic Development Council.1998. Forests of the South. 24 p.

Vlosky, Richard P. and N. Paul Chance. 1996. �An Analysisof State-Level Economic Development Programs Target-ing the Wood Products Industry.� Forest Products Jour-nal. Volume 46. Number 9:23-29.

Vlosky, Richard P. and N. Paul Chance. 1997. �Forest Prod-ucts Industry and Rural Economic Development: ThePolicy Makers Perspective.� Working Paper #15. Louisi-ana Forest Products Laboratory. LSU Agricultural Cen-ter. Baton Rouge, LA. 16 p.

Wear, David N., Robert Abt and Robert Mangold. 1998.�People, Space and Time: Factors That will Govern ForestSustainability.� In Transcripts 63rd North American Wild-life and Natural Resources Conference. Pp. 340-360.

State-level economic importance fact sheets have been devel-oped for most states. Contact your Extension Forester,state forester or state forestry association to see if they haveone for your state.

Web sitesAmerican Forest & Paper Association State Economic

Impact Statementshttp://www.afandpa.org/Congressional/eis/index.html

The Southern Forest-Based Economic DevelopmentCouncil

http://www.southernforests.org

Southern Region Extension Forestry (for connections to stateforestr y schools, extension services, forestr y associations andforestr y agencies as well as other links)

http://www.uga.edu/soforext

U.S. Census Bureau Annual Survey of ManufacturersCenstats: An Electronic Subscription Service

http://tier2.census.gov/asm/asm.htm

The USDA Forest Service�Southern Regionhttp://www.r8web.com

For more information & assistance

Report on the Southern Forest-Based Economic Development AcademyBirmingham, Ala., October 1997

SOUTHERN Perspectives

12 SOUTHERNPerspectives Volume 3, Number 2

he forests of the South are very im-portant to the life and the economyof the region. Southern forests will

play an important role in the region�s fu-ture but conflicts over their use may arise.As forest planning is integrated into eco-nomic and rural development planning forthe region, planners should be aware ofthe forces currently changing the South-ern forest. This listing of forces affectingthe South�s forests is not intended to beall-inclusive but is offered to give those out-side the forestry community some insightinto current changes that are impactingone of the region�s greatest resources.

Increasing demand, positivemarkets and changing utilizationIn the past three decades, the South hasexperienced increased demand for its woodproducts, especially pine products. Pricesfor standing timber in the South have risenmarkedly in the past 20 years. This hascaused significant economic and industrialdevelopment in the forest industry inmany southern states.

Strong demand for Southern timber is pro-jected to continue for several decades. Thiscontinued demand outlook is a force thatis attracting capital and helping forest land-owners and others to see the economicadvantages of forest management invest-ments. The economics of pine forestry andthe Conservation Reserve Program havealready helped shift thousands of acres ofmarginal cropland to forest use. Favorableprojected economic returns have begun toincrease the intensity of forest manage-ment and attract non-traditional forestinvestors to the region. The use of inten-sive forest management practices such asreforestation with genetically improvedseedlings, wider spacing, more frequentharvests, and the use of herbicides and fer-tilizers is increasing.

As markets become more competitive fortimber, new technologies for utilizingsmaller trees and under-used species aredeveloping. Products such as orientedstrand board (OSB), laminated veneer lum-ber (LVL) and others now occupy marketniches that would not have been practical20 years ago. The application of technol-ogy to all areas of the forest products in-dustry is a continuing trend.

Attractive investment returns inSouthern forestsIncreased prices and projected strong re-gional demand for timber has made invest-ments in forest management attractivethroughout the region. Published real ratesof return on pine plantations often exceedreturns on many traditional investments.Forest industry and many private non-in-dustrial landowners are now using inten-sive forest management methods to boostyields and shorten growing cycles. Inten-sive forest management is becoming in-creasingly common and forestland priceshave increased in many areas. In addition,leasing for hunting and other alternativeforest uses contributes to the income fromforestland for owners in many areas.

Financial institutions ownershiptrendThe returns on Southern timberland in-vestments and uniquely-suited long-terminvestment objectives have created an eco-nomic rationale for financial institutionsto own timberland. These financial insti-tutions include banks, insurance compa-nies, pension funds, foundations and uni-versity and other endowments. Financialinstitution ownership of southern forest-land has grown rapidly in the past 15 years.It has been reported that more than 60institutions own more than 1.6 millionacres at an estimated value of more than$3 billion. This shifting ownership trend,

among others, has caused some forestproducts firms to begin reexamining thestrategic role of their timberland holdings.Several forest products companies havemoved to �monetize� their timberlandholdings in various ways. For example, in1997, Georgia Pacific separated its timber-lands business into a new operating group,The Timber Company, and issued a letterstock that exclusively reflects the perfor-mance of that group. These developmentsillustrate the changing ownership charac-teristics and add a new dimension to thediverse pool of private forestland owner-ship in the South.

Changing private non-industrialownersThe South had an estimated 4.9 millionforest landowners in 1994. That was a 28percent increase in the number of ownerssince 1978. More than half own less than10 acres. Most are private, individual own-ers and the top three groups are white-col-lar workers, retirees and blue-collar work-ers, respectively. Taken together thesegroups comprise 72 percent of the South�sprivate forest owners and own 45 percentof the forestland. Individuals 55-years-oldor older own 47 percent of the forestlandin the South.

The fragmenting of larger forested tractsinto smaller parcels is increasing in theSouth. Development of forestland forother uses and dividing family ownershipsamong heirs are contributing factors.These changes could have important im-pacts on timber production in the com-ing years.

Environmental concernThe concern among the public for pro-tection of the environment is well knownand this may be even greater in the South.Most Southern states have enacted volun-tary best management practices (BMPs)that are used by loggers to protect waterquality and to prevent erosion during har-vesting operations. Additionally, the

Bob DanielsMississippi State University

Forces driving Southern forest changes: Insights for rural developers

T

As forest planning is integrated into economic and rural developmentplanning for the region, planners should be aware of the forcescurrently changing the Southern forest.

SOUTHERN Perspectives

SOUTHERN 13PerspectivesSummer 1999

American Forest and Paper Association member companies ini-tiated the Sustainable Forest Initiative (SFI) in 1995 to insureenvironmental sustainability on member company lands andencourage such practices by owners of private, non-industriallands. The SFI also includes annual reporting to the public onenvironmental performance. However, there are environmentalorganizations in the South that advocate greater restrictions ontimber harvesting and certification of forest products. Balanc-ing the economic use and protection of the privately-owned,Southern forest may be an area of future conflict but resolutionof such conflicts will be a focal issue for the region.

The interaction of these forces (and others) in the coming de-cades will have significant impact of the economy and quality

of life in the south, especially in the rural South. Organizationsand individuals concerned with the region�s future should notoverlook the forest resources sector that has important local im-pacts throughout the region. Forest use has impacts on local land-owners, forest and other industries, county budgets, local schoolfunding, roads and bridges, and many other aspects of life. Toperpetuate the benefits of the Southern forest, new alliances thatpromote greater cooperation and information exchanged betweenregional development organizations, academia, and the forestrycommunity are needed. These new alliances will be increasinglyimportant to insure the productivity of the Southern forest ofthe future.

Bob Daniels is an Extension Forestry Specialist in the Department of Forestry atMississippi State University.

Linking Community Development with National Forest Planning and Management in the SouthDonald E. Voth, Martin Jardon, Cindy McCauley, Zola K. Moon, and Irene FrentzUniversity of Arkansas

Available from the Southern Rural Devel-opment Center, this report discusses theeffects of devolution on economic and ru-ral development in communities in theSouth. The report defines and describesforest-dependent communities, points outchallenges and disadvantages they face, dis-cusses the evolving relationship betweenthe USDA Forest Service and rural andcommunity development programs andhow public involvement is important tothe forest planning process, and providessome strategies for collaborative planningand recommendations for future pro-grams.

This report is one of a five-part seriesfunded in part by the Economic ResearchService, USDA (Cooperative Agreement#43-3AEN-3-80145) to address current andemerging topics of concern to State RuralDevelopment Councils, land-grant insti-tutions, and other rural development en-tities located in the South.

The other reports in the series include:u The Changing Nature of Work inthe South: The Polarization of

Tomorrow�s WorkforceMelissa A. Barfield and Lionel J.Beaulieu, Southern RuralDevelopment Center, MississippiState University (July 1999)u Land Prices and the ChangingGeography of Southern Row-CropAgricultureJames. C. Hite, Emily J. Terrell, andKang Shou Lu, Strom ThurmondInstitute of Government and PublicAffairs, Clemson University (July1999)u Great Expectations: From Welfareto Work in the SouthDeborah M. Tootle, Louisiana StateUniversity (August 1999)u The Telecommunications Act of1996: Its Implementation in the U.S.SouthJohn Allen and Erin L.V. Koffler,University of Nebraska-Lincoln(September 1999)

For more information about these reportsor to receive a copy, contact the SouthernRural Development Center, Box 9656,

Mississippi State, MS 39762, 662-325-3207,662-325-8915 (fax), [email protected]. When publication is complete, thereports will be available on the SRDC website at http://www.ext.msstate.edu/srdc.

Private, individual owners comprise 72 percent ofthe South�s private forest owners and own 45percent of the forestland. Individuals 55-years-old

State Rural Development Councils/ERS report available

Preparing an article for submis-sion to Southern Perspectives?Please contact us prior to prepar-ing your article so that we canprovide you with a style sheet.The SRDC is endeavoring tomake this publication conform toa basic format for numbers, capi-talization, reference/endnotestyle, etc. Contact the Center at601-325-3207 or [email protected] for a copy of thestyle sheet.

14 SOUTHERNPerspectives

ONSchedule

SERA-IEG 19 ConferenceThe Changing Rural Health System: Education forConsumers and Providers (formerly Rural Health andSafety)October 11-13Nashville, Tenn.

The Southern Extension Research Activity (SERA) Informa-tion Exchange Group (IEG) meets on an ongoing basis to dis-cuss issues of mutual interest.

The conference will be held at the Embassy Suites Airport.Rates are $109 per night for a single and $119 for a double. Forreservations, contact the hotel at 800-EMBASSY or 615-871-0033.

To register for the conference or for more information aboutSERA-IEG 19, contact the Southern Rural Development Cen-ter, Box 9656, Mississippi State, MS 39762, 662-325-3207, 662-325-8915 (fax), [email protected].

Helping Small Towns SucceedOct. 14-18Snow King ResortJackson Hole, Wy.

This conference is designed as an introductory course in com-munity development. Participants will take part in sessionson time and stress management, managing community con-flict, understanding personality differences, and leadership char-acteristics and practices.

The conference will be held at the Snow King Resort in Jack-son Hole, Wy. A block of rooms has been reserved in the nameof the �Heartland Center.� Rates are $79 per night. To makereservations, contact the resort at 800-522-5464 or 307-733-5200.

Registration is $750 until September 17. After September 17,registration is $850. A $100 deposit will hold your reservationuntil the pre-registration deadline. Full registration must bereceived by the deadline to receive the $100 discount.

To register or for more information, contact the HeartlandCenter for Leadership Development, 941 �O� St., Suite 920,Lincoln, NE 68508, 402-474-7667, 800-927-1115, 402-474-7672(fax), http://www.w4.com/heartland.

Southern Institute for Rural DevelopmentNovember 8-12Athens, Ga.

Participants in this conference will receive two A points to-ward CED recertification by the American Economic De-velopment Council.

For registration information, contact David P. Mills at theUniversity of Georgia, 912-329-4825, [email protected],or Martha A. Schoonmaker at Georgia Tech, 404-894-0332,[email protected].

Entrepreneurial Education and Training ConferenceNovember 11-12

Haywood Community College, Clyde, N.C. (for ARC countiesin Kentucky, North Carolina, South Carolina, Virginia, andWest Virginia)For information on the conference in Clyde, N.C., contactNC REAL Enterprises, 115 Market St., Suite 320, Durham,NC 27701, 919-688-7325, 919-682-7621 (fax) http://www.ncreal.org.

November 18-19Birmingham, Ala. (for ARC counties in Alabama, Mississippi,Tennessee, and Georgia)For information on the conference in Birmingham, Ala., con-tact the Southern Rural Development Center, Box 9656, Mis-sissippi State, MS 39762,662-325-3207, 662-323-8915 (fax),[email protected].

Professional Agricultural Workers ConferenceDecember 5-7Tuskegee, Ala.

With the theme �Global Food Security: Exploring the NexusBetween Domestic and International Strategies,� this confer-ence will allow participants to review and discuss topics onimproving the quality of rural life for people in the Southand the nation as a whole.

Conference organizers are soliciting papers and posters onthe conference theme. For information, contact PAWC Con-ference Coordinator, Tuskegee University, Milbank Hall,Tuskegee, AL 36088 before October 15.

continued on page 16

SOUTHERN 15Perspectives

ON Schedule

This conference tar-gets extension pro-gram leaders in theSouth. The objec-tives of the confer-ence are to increasecommun ica t i on

and planning, to development a commonunderstanding, to improve programmingthrough sharing ideas and resources, andto identify current important issues to theSouth and their implications for currentand future programs.

Charles Laughlin is the new administrator of the U.S. Depart-ment of Agriculture�s Cooperative State Research, Education,and Extension Service. He had been the dean and director ofthe College of Tropical Agriculture and Human Resources atthe University of Hawaii-Manoa since 1996. Prior to his ap-pointment at UHM, he was the director of the Colorado Agri-cultural Experiment Station at Colorado State University forfour years. In past years, he has served in research areas in Geor-gia, Mississippi, Michigan, and Florida. His international expe-rience includes work in Brazil, the Philippines, Thailand, Ma-laysia, and Nepal. Laughlin is a former member of the Board ofDirectors for the Southern Rural Development Center. He re-ceived his bachelor�s degree in horticulture from Iowa State Uni-versity, his master�s in agronomy from the University of Mary-land, and his doctorate in plant pathology and physiology fromVirginia Tech.

Dan Kugler is interim director of Economic and CommunitySystems for USDA�s Cooperative State, Research, Education, andExtension Service. With a background in agricultural econom-ics, he comes from the Plant and Animal Sciences unit ofCSREES where he headed Products and Processing and was re-sponsible for staffing and leadership of agricultural engineering,small farms, agricultural industrial materials, and food science.He replaces Bob Koopman, who left CSREES for a positionwith the International Trade Commission. A permanent direc-tor should be chosen in the next nine months.

Virginia Caples, who has served as 1890 administrator of Ala-bama A&M University since 1996, has been appointed adminis-trator of 1890 extension programs at the university. She succeeds

NAMES in the News

Chinella Henderson who now serves as associate director. Caplesreceived her doctorate in home economics and family environ-ment from Iowa State University.

Vernon L. Jones, associate research professor at Langston Uni-versity in Oklahoma, recently was appointed administrator for1890 extension programs for the university. He succeeds MarvinBurns, who now serves as dean of the School of Agricultureand Applied Sciences. Jones received his doctorate in agronomyfrom the University of Illinois.

Edward A. Hiler has been appointed director of the Texas Agri-cultural Extension Service. Hiler also serves as vice chancellorfor Agriculture and Life Sciences and dean of the College ofAgriculture and Life Sciences at Texas A&M University. He re-ceived his doctorate in agricultural engineering from the OhioState University. Chester P. Fehlis, former associate director ofTAES, is now deputy director. He received his doctorate in agri-cultural education from Texas A&M.

Kriton Hatzios, former chair of the Department of Plant Pa-thology, Physiology, and Weed Science at Virginia Tech, is nowdirector of the Virginia Agricultural Experiment Station andassociate dean for research in the College of Agriculture and LifeSciences at Virginia Tech. He received his bachelor�s degree inagriculture from the Aristotelian University of Thessaloniki,Greece and his doctorate from Michigan State University.

August 29-September 1Biloxi, Miss.

Southern Region Program Leadership Conference

The conference will be held at the GrandCasino Bayview Hotel, 280 Beach Boule-vard in Biloxi, Miss. A block of rooms hasbeen reserved in the name of the �South-ern Rural Development Center.�

Rates are $85 per night for a single and$95 for a double. Rooms will be helduntil July 30. After this date, rooms willbe confirmed on an as available basis. Tomake reservations, contact the hotel at 800-354-2450 or 228-386-1924.

The registration fee is $100 and includesbreaks, two luncheons, and conferencematerials. Registration deadline is August13. For registration information, contactthe Southern Rural Development Center,Box 9656, Mississippi State, MS 39762,662-325-3207, 662-325-8915 (fax) [email protected]. Any cancella-tions must be received by August 20.

SOUTHERN Perspectives

16 SOUTHERNPerspectives Volume 3, Number 2

NONPROFIT ORG.

U.S. Postage

PAID

Permit No. 39

Mississippi State, MS

A quarterly newsletter published by

Southern Rural Development CenterBox 9656, 410 Bost Extension BuildingMississippi State, MS 39762Phone: 662-325-3207Fax: 662-325-8915http://ext.msstate.edu/srdc/

Lionel J. “Bo” Beaulieu, DirectorDenise M. Cosper, Editor(Send comments [email protected].)

SOUTHERNPerspectives

Mississippi State University does not discriminateon the basis of race, color, religion, nationalorigin, sex, age, disability, or veteran status.

Box 9656Mississippi State, MS 39762

The conference will be held at the Tuskegee University Kellogg Conference Center. Ablock of rooms has been reserved under �PAWC� until November 19. Rates are $70per night. To make reservations, contact the center at 334-727-3000.

Registration is $165 ($110 for retirees and students). For information, contact LouiseHerron, PAWC Finance Committee, Tuskegee University, 112 Campbell Hall, Tuskegee,AL 36088, 334-727-8334, 334-727-4451 (fax).

[5] USDA Forest Service. 1988. The South�s FourthForest: Alternatives for the Future. Washington, DC:Forest Resource Report No. 24:512.

[6] USDA Forest Service. 1993. Forest Resources ofthe United States, 1992. Fort Collins, CO: GeneralTechnical Report RM-234:133.

[7] USDA Forest Service. 1996. Private ForestlandOwners of the Southern United States, 1994.Radnor, PA. Resource Bulletin NE-138:195.

[8] World Wood Review. 1999. �Timber Supply Nota Problem: Feature Report.� Volume 6, No. 1. Janu-ary 1999.

William G. Hubbard is Southern Regional ExtensionForester and is based at the University of Georgia.

continued from page 5

References[1] American Forest & Paper Association. 1999.State Economic Impact Statements. (http://www.afandpa.org/Congressional/eis/index.html).

[2] Cubbage, Frederick W. and Robert C. Abt. 1998.�Southern Timber Supply: Implications for the For-estry Sector.� Forest Landowner Volume 57, Num-ber 4:27-31.

[3] Syme, John H. and Charles R. Duke. 1994.�Market-oriented strategy for forest-based rural eco-nomic development.� Forest Products Journal Volume44. Number 5:10-16.

[4] U.S. Census Bureau. 1998. Annual Survey ofManufacturers. Censtats: An Electronic Subscrip-tion Service (http://tier2.census.gov/asm/asm.htm).

continued from page 14