southwest california legislative council march agenda

TRANSCRIPT

MEETING AGENDA Monday March 21, 2016

Realtor House, 26529 Jefferson Ave, Murrieta

Presiding: Don Murray, Chair

2016 Strategic Initiatives Budget & Tax Reform / Job Creation and Retention / Healthcare / Infrastructure & The Environment/ Public Safety

Call to Order, Roll Call & Introductions: 12:00 p.m. Chair Report Agenda Items

Legislative Report #3 Action

1. SBX1-2 (Huff) Greenhouse Gas Reduction Fund. 2. AB-1591 (Frazier) Transportation funding. 3. AB-2049 (Melendez) Bonds: transportation. 4. AB-1749 (Mathis) California Environmental Quality Act: exemption: recycled water pipelines. 5. SB-789 (Wieckowski) Sale of water by local public entities: excise tax. 6. AB-2277 (Melendez) Local government finance: property tax revenue allocation: vehicle

license fee adjustments. 7. SBX2-2 (Hernandez) Medi-Cal: managed care organization tax. Information

Speaker John Kelliher Calvary Bible Fellowship v. Riverside County Action Speaker and Chamber Announcements Information Our lunch sponsor The French Valley Cafe Thank You

Adjourn – Next Meeting April 18, 2016

Follow us on :

The Southwest California Legislative Council Thanks Our Partners:

Southwest Riverside Country Association of Realtors

Metropolitan Water District of Southern California

Elsinore Valley Municipal Water District CR&R Waste Services

Abbott Vascular

Temecula Valley Chamber of Commerce Murrieta Chamber of Commerce Lake Elsinore Valley Chamber of

Commerce Wildomar Chamber of Commerce

Menifee Valley Chamber of Commerce Perris Valley Chamber of Commerce

Commerce Bank of Temecula Valley California Apartment Association

Southwest Healthcare Systems Temecula Valley Hospital

EDC of Southwest California Paradise Chevrolet Cadillac

The Murrieta Temecula Group

Southwest California Legislative Council

Southwest California Legislative Council

Lake Elsinore Chamber of Commerce Menifee Valley Chamber of Commerce

Murrieta Chamber of Commerce Perris Valley Chamber of Commerce

Temecula Valley Chamber of Commerce Wildomar Chamber of Commerce

Meeting Minutes

Monday, February 22, 2016

2016 Chair: Don Murray Legislative Consultant: Gene Wunderlich

Directors Attendance:

Adam Ruiz Brad Neet Carl Johnson Denee Burns Dennis Frank Don Murray Gene Wunderlich

Greg Morrison Joan Sparkman John Kelliher Judy Gugliemana Matt Buck Michael Garrison

Chamber Executives/Guests Attendance:

Alice Sullivan Andy Abeles Balden Singh Vij Ben Benoit Brenda Dennstedt Cheri Zamora Cindy Espinoza

Connie Lynch Danielle Coats Debbie Herrera Debbie Kosum Doug McAllister Eric Cox

Jeff Bott Kimberly Niebla Laura Turnbow Mario Herrera Maryann Edwards Michelle Runnells Morris Myers Patrick Ellis Pattie Arct Randy Jole Sunday Sayles Tom Stinson

Southwest California Legislative Council

Meeting called to order at: 12:09 pm by Chair Don Murray 1. Approval of Minutes Action Motion was made to approve the minutes and to approve the revised 2016 Policy Platform. Motion was seconded and carried.

2. Legislative Items Action 1. AB1713 (Eggman) Sacramento-San Joaquin Delta: Peripheral Canal. This bill would prohibit the construction of a

peripheral canal unless expressly authorized by an initiative voted on by the voters of California on or after January 1, 2017, and would require the Legislative Analyst’s Office to complete a prescribed economic feasibility analysis prior to a vote authorizing the construction of a peripheral canal. Motion to OPPOSE AB 1713 seconded and carried.

2. AB 1866 (Wilk) High-Speed Rail Bond Proceeds: Redirection: Water Projects. This bill would provide that no further bonds shall be sold for high-speed rail purposes pursuant to the Safe, Reliable High-Speed Passenger Train Bond Act for the 21st Century, except as specifically provided with respect to an existing appropriation for high-speed rail purposes for early improvement projects in the Phase 1 blended system. This bill, subject to the above exception, would require redirection of the unspent proceeds for use in retiring the debt incurred form the issuance and sale of those outstanding bonds and would also require the net proceeds of other bonds to fund capital expenditures for water projects. Motion to SUPPORT AB 1866 seconded and carried.

3. SB 940 (Vidak) High-Speed Rail Authority: Eminent Domain; Right of First Refusal. This bill would declare the intent of the Legislature to enact legislation that would establish a right of first refusal for landowners to reacquire land that was taken for high-speed rail through eminent domain, if the land is later determined to not be necessary for high-speed rail. Motion to SUPPORT SB 940 seconded and carried.

4. AB 21 (ABX-21) (Obernolte) Environmental Quality: Highway Projects. This bill would prohibit a court in a judicial

action or proceeding under CEQA from staying or enjoining the construction or improvement of a highway unless it make specified findings. (1) The project presents an imminent threat to the public health and safety. (2) The project site contains unforeseen important Native American artifacts or unforeseen important historical, archaeological, or ecological values that would be materially, permanently, and adversely affected by the project unless the court stays or enjoins the project. (c) If the court finds that paragraph (1) or (2) of subdivision (a) is satisfied, the court shall only enjoin those specific activities associated with the project that present an imminent threat to public health and safety or that materially, permanently, and adversely affect unforeseen important Native American artifacts or unforeseen important historical, archaeological, or ecological values. Motion to SUPPORT AB 21 seconded and carried.

5. SCA 10 (Huff) Legislative Procedure “Budget Accountability and Transparency Act of 2015.” This measure would authorize a committee to hear or act upon a bill before 31 days have passed following the bill’s introduction if the bill, in the form to be considered by the committee, has been in print and published on the Internet for at least 15 days. This measure would also prohibit either house of the Legislature from passing a bill until it has been made available to the public, in print and on the Internet, for at least 72 hours before a vote on the measure, except for certain bills that address a state of emergency declared by the Governor. Motion to SUPPORT SCA 10 seconded and carried.

6. AB 1788 (Melendez) Legislature: Legislative Employee Whistleblower Protection Act. This bill would prohibit interference with the right of legislative employees, as defined, to make protected disclosures of ethics violations and would prohibit retaliation against legislative employees who have made protected disclosures. This bill would establish a procedure for legislative employees to report violations of the prohibitions to the Legislature. The bill would also impose civil and criminal liability on a person who interferes with a legislative employee’s right to make a protected disclosure or who engages in retaliatory acts, as specified. Motion to SUPPORT AB 1788 seconded and carried.

7. SB 876 (Liu) Homelessness. The bill would afford persons experiencing homelessness the right to use public spaces without discrimination based on their housing status and describe basic human and civil rights that may be exercised without being subject to criminal or civil sanctions, including the right to use and to move freely in public spaces, the right to rest in public spaces and to protect oneself from the elements, the right to eat in any public space in which having food is not prohibited, and the right to perform religious observances in public spaces, as specified. Because the bill would require local agencies to perform additional duties, it would impose a state-mandated local program. Motion to OPPOSE SB 876 seconded and carried.

Southwest California Legislative Council

3. Guest Speakers: Thomas Freeman; Riverside County EDA, Foreign Trade & Military Affairs Information Thomas Freeman gave a report on the March Air Force Base. Budget was cut for the defense department, which means less resources. Since the air force has the oldest technology, jobs are needed to modernize fleet. Keep a look out a for defense bills. 4. Speaker and Chamber Announcements Information Senator Jeff Stone Reported by Maryann Edwards: Brief overview of bills and announcements. Assemblymember Melissa Melendez Reported by Mario Herrera: Legislative update Assemblymember Marie Waldron Reported by Tom Stinson: Legislative update City of Temecula Report by Randy Jole on the French Valley Interchange Project City of Wildomar Reported by Ben Benoit: Update on city’s lawsuit Lake Elsinore Chamber Report by Kim Cousins on upcoming events Menifee Valley Chamber Report by Michelle Runnells on upcoming events Murrieta Chamber Report by Patrick Ellis on upcoming events Temecula Valley Chamber Report by Alice Sullivan on upcoming events. Wildomar Chamber Report by Judy Guglielmana on upcoming events 6. Today's Lunch Sponsor The Shamrock Irish Pub & Eatery Adjournment – Next Meeting March 21, 2016 Motion to adjourn at 1:15 p.m.

Southwest California Legislative Council

Legislative Item #1 Action

SBX1-2 (Huff) Greenhouse Gas Reduction Fund.

Introduced by Senator Huff (Two year bill) (Coauthors: Senators Anderson, Bates, Berryhill, Fuller, Gaines, Moorlach, Morrell, Nguyen, Nielsen, Runner,

Stone, and Vidak)

Recommended action: SUPPORT Presentation: Gene Wunderlich

Summary: Existing law requires all moneys, except for fines and penalties, collected by the State Air Resources Board from the auction or sale of allowances as part of a market-based compliance mechanism relative to reduction of greenhouse gas emissions to be deposited in the Greenhouse Gas Reduction Fund.

Existing law continuously appropriates 60% of the annual proceeds of the fund to various purposes, including high-speed rail, transit and intercity rail capital, low-carbon transit operations, and affordable housing and sustainable communities.

This bill would exclude from allocation under these provisions the annual proceeds of the fund generated from the transportation fuels sector. The bill would instead provide that those annual proceeds shall be appropriated by the Legislature for transportation infrastructure, including public streets and highways, but excluding high-speed rail.

This bill appropriates Greenhouse Gas Reduction Fund (GGRF)monies generated from transportation fuels to transportation infrastructure, excluding highspeed rail.

Arguments in Favor: Over the next 10 years, the state faces a $59 billion shortfall to adequately maintain the state highway system in a basic state of good repair.

Similarly, cities and counties face a $78 billion shortfall over the next decade to adequately maintain the existing network of local streets and roads.

Since the State Air Resources Board imposed the cap-and-trade tax on gasoline production in January 2015, the Governor’s budget is projecting that $2.7 billion will be available from the Greenhouse Gas Reduction Fund in the fiscal year that begins July 1. That figure is more than double the amount that was available last year.

Revenue has surged because cap-and-trade now applies to transportation fuels, the source of roughly 40 percent of the state’s carbon emissions.

The Legislative Analyst’s Office projects that the imposition of cap-and-trade on transportation fuels will raise $1.9 billion this year. This revenue is raised by taxing consumers (through a pass-through increased cost of gasoline) and should be used to repair our streets and roads.

Investing in our streets and roads will end traffic gridlock and improve mobility, which, in turn, will reduce greenhouse gases in the state.

Description:

AB 32: The Global Warming Solutions Act of 2006

Existing law (AB 32, Núñez, Chapter 488, Statutes of 2006) requires the state Air Resources Board (ARB) to develop a plan to reduce emissions to 1990 levels by 2020. It also requires ARB to ensure that programs to reduce greenhouse gas (GHG) emissions are targeted, to the extent feasible, to the most disadvantaged communities in the state. AB 32 authorizes ARB to deposit any fees paid by GHG emission sources into the GGRF. Existing law (AB 1532, Pérez, Chapter 807, Statutes of 2012) specifies that GGRF revenues must be used to facilitate the achievement of GHG emissions reductions.

Existing law specifies that ARB may include market-based compliance mechanisms in the AB 32 regulations, and requires that these mechanisms maximize additional environmental and economic benefits for California, as appropriate. The Scoping Plan approved by ARB in 2008 outlined a suite of measures aimed at achieving AB 32 goals. Average emissions data in the Scoping Plan broken down by sector reveal that transportation accounts for almost 40%

Southwest California Legislative Council

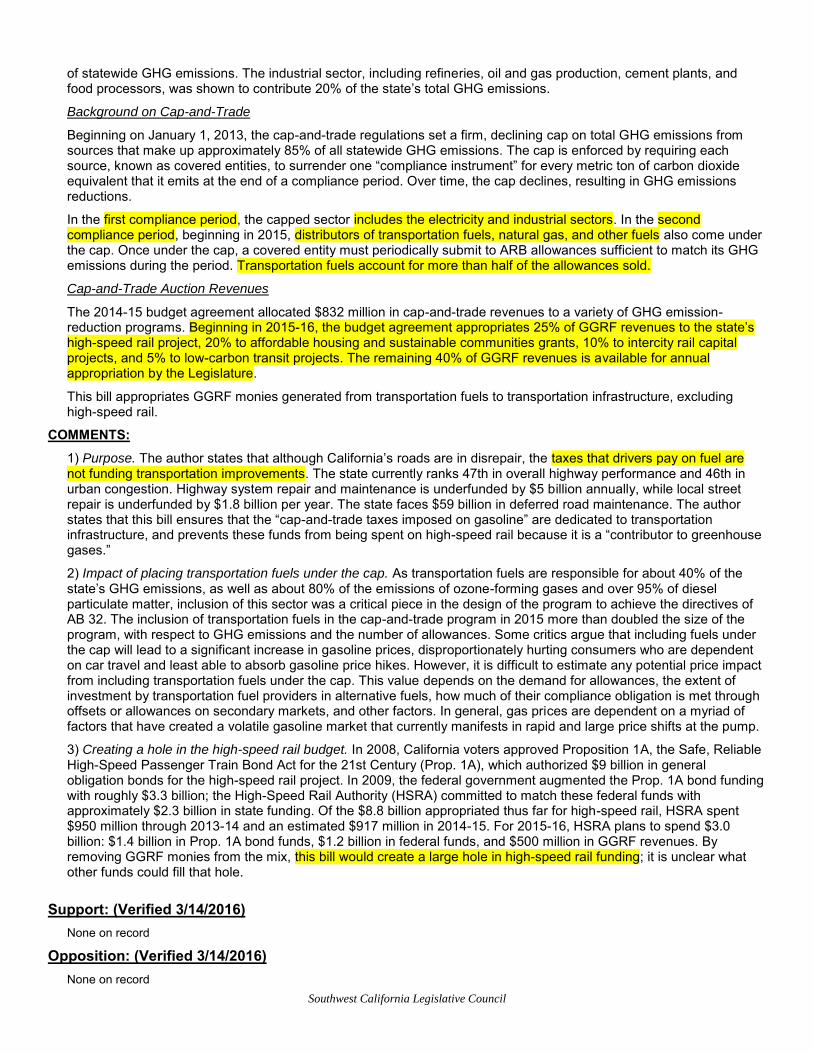

of statewide GHG emissions. The industrial sector, including refineries, oil and gas production, cement plants, and food processors, was shown to contribute 20% of the state’s total GHG emissions.

Background on Cap-and-Trade

Beginning on January 1, 2013, the cap-and-trade regulations set a firm, declining cap on total GHG emissions from sources that make up approximately 85% of all statewide GHG emissions. The cap is enforced by requiring each source, known as covered entities, to surrender one “compliance instrument” for every metric ton of carbon dioxide equivalent that it emits at the end of a compliance period. Over time, the cap declines, resulting in GHG emissions reductions.

In the first compliance period, the capped sector includes the electricity and industrial sectors. In the second compliance period, beginning in 2015, distributors of transportation fuels, natural gas, and other fuels also come under the cap. Once under the cap, a covered entity must periodically submit to ARB allowances sufficient to match its GHG emissions during the period. Transportation fuels account for more than half of the allowances sold.

Cap-and-Trade Auction Revenues

The 2014-15 budget agreement allocated $832 million in cap-and-trade revenues to a variety of GHG emission-reduction programs. Beginning in 2015-16, the budget agreement appropriates 25% of GGRF revenues to the state’s high-speed rail project, 20% to affordable housing and sustainable communities grants, 10% to intercity rail capital projects, and 5% to low-carbon transit projects. The remaining 40% of GGRF revenues is available for annual appropriation by the Legislature.

This bill appropriates GGRF monies generated from transportation fuels to transportation infrastructure, excluding high-speed rail.

COMMENTS:

1) Purpose. The author states that although California’s roads are in disrepair, the taxes that drivers pay on fuel are not funding transportation improvements. The state currently ranks 47th in overall highway performance and 46th in urban congestion. Highway system repair and maintenance is underfunded by $5 billion annually, while local street repair is underfunded by $1.8 billion per year. The state faces $59 billion in deferred road maintenance. The author states that this bill ensures that the “cap-and-trade taxes imposed on gasoline” are dedicated to transportation infrastructure, and prevents these funds from being spent on high-speed rail because it is a “contributor to greenhouse gases.”

2) Impact of placing transportation fuels under the cap. As transportation fuels are responsible for about 40% of the state’s GHG emissions, as well as about 80% of the emissions of ozone-forming gases and over 95% of diesel particulate matter, inclusion of this sector was a critical piece in the design of the program to achieve the directives of AB 32. The inclusion of transportation fuels in the cap-and-trade program in 2015 more than doubled the size of the program, with respect to GHG emissions and the number of allowances. Some critics argue that including fuels under the cap will lead to a significant increase in gasoline prices, disproportionately hurting consumers who are dependent on car travel and least able to absorb gasoline price hikes. However, it is difficult to estimate any potential price impact from including transportation fuels under the cap. This value depends on the demand for allowances, the extent of investment by transportation fuel providers in alternative fuels, how much of their compliance obligation is met through offsets or allowances on secondary markets, and other factors. In general, gas prices are dependent on a myriad of factors that have created a volatile gasoline market that currently manifests in rapid and large price shifts at the pump.

3) Creating a hole in the high-speed rail budget. In 2008, California voters approved Proposition 1A, the Safe, Reliable High-Speed Passenger Train Bond Act for the 21st Century (Prop. 1A), which authorized $9 billion in general obligation bonds for the high-speed rail project. In 2009, the federal government augmented the Prop. 1A bond funding with roughly $3.3 billion; the High-Speed Rail Authority (HSRA) committed to match these federal funds with approximately $2.3 billion in state funding. Of the $8.8 billion appropriated thus far for high-speed rail, HSRA spent $950 million through 2013-14 and an estimated $917 million in 2014-15. For 2015-16, HSRA plans to spend $3.0 billion: $1.4 billion in Prop. 1A bond funds, $1.2 billion in federal funds, and $500 million in GGRF revenues. By removing GGRF monies from the mix, this bill would create a large hole in high-speed rail funding; it is unclear what other funds could fill that hole.

Support: (Verified 3/14/2016)

None on record

Opposition: (Verified 3/14/2016) None on record

Southwest California Legislative Council

Status: Active - Committee on Transportation & Infrastructure Development Vote: majority Appropriation: no Fiscal Committee: yes Local Program: no

Senate Floor votes: Assembly floor votes:

Legislative Item #2 Action

AB1591 (Frazier) Transportation funding.

Recommended action: OPPOSE Presentation: Gene Wunderlich

Summary: Existing law provides various sources of funding for transportation purposes, including funding for the state highway system and the local street and road system. These funding sources include, among others, fuel excise taxes, commercial vehicle weight fees, local transactions and use taxes, and federal funds. Existing law imposes certain registration fees on vehicles, with revenues from these fees deposited in the Motor Vehicle Account and used to fund the Department of Motor Vehicles and the Department of the California Highway Patrol. Existing law provides for the monthly transfer of excess balances in the Motor Vehicle Account to the State Highway Account.

This bill would create the Road Maintenance and Rehabilitation Program to address deferred maintenance on the state highway system and the local street and road system. The bill would require the California Transportation Commission to adopt performance criteria to ensure efficient use of the funds available for the program. The bill would provide for the deposit of various funds for the program in the Road Maintenance and Rehabilitation Account, which the bill would create in the State Transportation Fund, including revenues attributable to a $0.225 per gallon increase in the motor vehicle fuel (gasoline) tax imposed by the bill, including an inflation adjustment as provided, an increase of $38 in the annual vehicle registration fee, and a new $165 annual vehicle registration fee applicable to zero-emission motor vehicles, as defined.

The bill would continuously appropriate the funds in the account for road maintenance and rehabilitation purposes and would allocate 5% of available funds to counties that approve a transactions and use tax on or after July 1, 2016, with the remaining funds to be allocated 50% for maintenance of the state highway system or to the state highway operation and protection program, and 50% to cities and counties pursuant to a specified formula. The bill would impose various requirements on agencies receiving these funds. The bill would authorize a city or county to spend its apportionment of funds under the program on transportation priorities other than those allowable pursuant to the program if the city’s or county’s average Pavement Condition Index meets or exceeds 85.

Existing law provides for loans of revenues from various transportation funds and accounts to the General Fund, with various repayment dates specified.

This bill would require the Department of Finance, on or before March 1, 2016, to compute the amount of outstanding loans made from specified transportation funds. The bill would require the Department of Transportation to prepare a loan repayment schedule and would require the outstanding loans to be repaid pursuant to that schedule to the accounts from which the loans were made, as prescribed. The bill would appropriate funds for that purpose from the Budget Stabilization Account. The bill would require the repaid funds to be transferred to cities and counties pursuant to a specified formula.

The Highway Safety, Traffic Reduction, Air Quality, and Port Security Bond Act of 2006 (Proposition 1B) created the Trade Corridors Improvement Fund and provided for allocation by the California Transportation Commission of $2 billion in bond funds for infrastructure improvements on highway and rail corridors that have a high volume of freight movement, and specified categories of projects eligible to receive these funds. Existing law continues the Trade Corridors Improvement Fund in existence in order to receive revenues from sources other than the bond act for these purposes.

The bill would deposit the revenues attributable to a $0.30 per gallon increase in the diesel fuel excise tax imposed by the bill into the Trade Corridors Improvement Fund.

Southwest California Legislative Council

Existing law specifies projects eligible for funding from the Trade Corridors Improvement Fund, including, among other things, projects for truck corridor improvements, including dedicated truck facilities, or truck toll facilities.

This bill would include truck parking among the truck corridor capital improvements eligible to be funded and would authorize the expenditure of moneys in the fund for certain system efficiency improvements, including the development, demonstration, and deployment of promising Intelligent Transportation System applications. The bill would require the California Transportation Commission, in evaluating potential projects to be funded from the fund, to give priority to projects demonstrating one or more of certain characteristics.

Existing law requires all moneys, except for fines and penalties, collected by the State Air Resources Board from the auction or sale of allowances as part of a market-based compliance mechanism relative to reduction of greenhouse gas emissions to be deposited in the Greenhouse Gas Reduction Fund. Existing law, to the extent moneys are transferred to the Trade Corridors Improvement Fund from the Greenhouse Gas Reduction Fund, requires projects funded with those moneys to be subject to all of the requirements of existing law applicable to the expenditure of moneys appropriated from the Greenhouse Gas Reduction Fund, including, among other things, furthering the regulatory purposes of the California Global Warming Solutions Act of 2006. Existing law continuously appropriates 10% of the annual proceeds of the fund to the Transit and Intercity Rail Capital Program.

This bill would, beginning in the 2016–17 fiscal year, instead continuously appropriate 20% of those annual proceeds to the Transit and Intercity Rail Capital Program, thereby making an appropriation, and, transfer 20% of those annual proceeds to the Trade Corridors Improvement Fund.

Existing law, as of July 1, 2011, increases the sales and use tax on diesel and decreases the excise tax, as provided. Existing law requires the State Board of Equalization to annually modify both the gasoline and diesel excise tax rates on a going-forward basis so that the various changes in the taxes imposed on gasoline and diesel are revenue neutral.

This bill would eliminate the annual rate adjustment to maintain revenue neutrality for the gasoline and diesel excise tax rates. This bill would, beginning July 1, 2019, and every 3rd year thereafter, require the board to recompute the gasoline and diesel excise tax rates based upon the percentage change in the California Consumer Price Index transmitted to the board by the Department of Finance, as prescribed.

Existing law requires the Department of Transportation to prepare a state highway operation and protection program every other year for the expenditure of transportation capital improvement funds for projects that are necessary to preserve and protect the state highway system, excluding projects that add new traffic lanes. The program is required to be based on an asset management plan, as specified. Existing law requires the department to specify, for each project in the program, the capital and support budget and projected delivery date for various components of the project. Existing law provides for the California Transportation Commission to review and adopt the program, and authorizes the commission to decline and adopt the program if it determines that the program is not sufficiently consistent with the asset management plan.

This bill, on and after February 1, 2017, would require the commission to make an allocation of all capital and support costs for each project in the program, and would require the department to submit a supplemental project allocation request to the commission for each project that experiences cost increases above the amounts in its allocation. The bill would require the commission to establish guidelines to provide exceptions to the requirement for a supplemental project allocation requirement that the commission determines are necessary to ensure that projects are not unnecessarily delayed.

Support: (Verified 3/14/2016)

None on record

Opposition: (Verified 3/14/2016)

None on record

Status: Active - Referred to Committees. on Transportation. and Revenue & Taxation

Vote: 2/3 Appropriation: yes Fiscal Committee: yes Local Program: no Senate Floor votes: Assembly floor votes:

Southwest California Legislative Council

Legislative Item #3 Action

AB2049 (Melendez) Bonds: transportation.

Recommended action: SUPPORT Presentation: Gene Wunderlich

Introduced by Assembly Member Melendez (Coauthors: Assembly Members Travis Allen, Baker, Gallagher, Harper, Jones, Patterson, and Wilk)

Summary: Existing law, the California High-Speed Rail Act, creates the High-Speed Rail Authority to develop and implement a high-speed rail system in the state. Existing law, the Safe, Reliable High-Speed Passenger Train Bond Act for the 21st Century, approved by the voters as Proposition 1A at the November 4, 2008, general election, provides for the issuance of $9 billion in general obligation bonds for high-speed rail purposes and $950 million for other related rail purposes. Article XVI of the California Constitution requires measures authorizing general obligation bonds to specify the single object or work to be funded by the bonds and further requires a bond act to be approved by a 2/3 vote of each house of the Legislature and a majority of the voters.

This bill would provide that no further bonds shall be sold for high-speed rail purposes pursuant to the Safe, Reliable High-Speed Passenger Train Bond Act for the 21st Century, expect as specifically provided with respect to an existing appropriation for high-speed rail purposes for early improvement projects in the Phase I blended system. The bill, subject to the above exception, would require redirection of the unspent proceeds received from outstanding bonds issued and sold for other high-speed rail purposes prior to the effective date of these provisions, upon appropriation, for use in retiring the debt incurred from the issuance and sale of those outstanding bonds. The bill, subject to the above exception, would also require the net proceeds of other bonds subsequently issued and sold under the high-speed rail portion of the bond act to be made available, upon appropriation, to fund projects in the State Transportation Improvement Program and the State Highway Operation and Protection Program, and to fund projects eligible for funding from the Trade Corridors Improvement Fund. The bill would make no changes to the authorization under the bond act for issuance of $950 million for rail purposes other than high-speed rail. These provisions would become effective only upon approval by the voters at the next statewide general election.

This bill would declare that it is to take effect immediately as an urgency statute.

Support: (Verified 3/14/2016)

None on record Opposition: (Verified 3/14/2016)

None on record

Status: Active - Committee on Transportation

Vote: 2/3 Appropriation: no Fiscal Committee: yes Local Program: no

Senate Floor votes: Assembly floor votes: Legislative Item #4 Action

AB1749 (Mathis) California Environmental Quality Act: exemption: recycled water pipelines.

Recommended action: SUPPORT Presentation: Gene Wunderlich

Southwest California Legislative Council

Summary:

Existing law, the California Environmental Quality Act (CEQA), requires a lead agency, as defined, to prepare, or cause to be prepared, and certify the completion of, an environmental impact report on a project that it proposes to carry out or approve that may have a significant effect on the environment or to adopt a negative declaration if it finds that the project will not have that effect. CEQA also requires a lead agency to prepare a mitigated negative declaration for a project that may have a significant effect on the environment if revisions in the project would avoid or mitigate that effect and there is no substantial evidence that the project, as revised, would have a significant effect on the environment. CEQA exempts from its requirements projects consisting of the construction or expansion of recycled water pipeline and directly related infrastructure within existing rights of way, and directly related groundwater replenishment, if the project does not affect wetlands or sensitive habitat, and where the construction impacts are fully mitigated, and undertaken for the purpose of mitigating drought conditions for which a state of emergency was proclaimed by the Governor on a certain date. CEQA provides that this exemption remains operative until the state of emergency has expired or until January 1, 2017, whichever occurs first.

This bill would extend that date to January 1, 2022.

Providing:

(1) The project is approved or carried out by a public agency for the purpose of mitigating drought conditions for which a state of emergency was proclaimed by the Governor on January 17, 2014, pursuant to Chapter 7 (commencing with Section 8550) of Division 1 of Title 2 of the Government Code.

(2) The project consists of construction or expansion of recycled water pipeline and directly related infrastructure within existing rights of way, and directly related groundwater replenishment, if the project does not affect wetlands or sensitive habitat, and where the construction impacts are fully mitigated consistent with applicable law.

Description:

CEQA includes various statutory exemptions, as well as categorical exemptions in the CEQA Guidelines. In June 2015, SB 88, a drought relief budget trailer bill, added the exemption amended by this bill. At the time, the project cited as the reason for the exemption was a large water recycling project proposed by the Santa Clara Valley Water District consisting of multiple pipelines, groundwater recharge ponds, injection wells, and related facilities. According to the water district, the exemption has not been used and the entire proposed project may not be eligible for the exemption.

Arguments in Favor: SB 88 provided much needed assistance in the way of establishing projects designed to mitigate the effects of the current and future droughts. However, the established exemption date is not conducive to accomplishing the necessary projects needed for a continuation of the drought emergency. If the current sunset date arrives without change, then future drought mitigation projects will not come to fruition due to complex CEQA regulation.

Arguments in Opposition: No evidence that CEQA is an unreasonable impediment to recycled water projects. A review of CEQA notices submitted to the Office of Planning and Research (OPR) shows that recycled water projects have been routinely approved via exemption or negative declaration. This bill exempts pipeline projects within existing rights of way. All such projects are exempt under current law if they are under one mile. In addition, categorical exemptions are available for maintenance, replacement and reconstruction of existing public utility facilities, involving negligible or no expansion of capacity. This bill is operative only during the current drought state of emergency, but projects necessary to prevent or mitigate an emergency can be exempted via CEQA, as well as via the Governor's broad authority under the Emergency Services Act.

There's no record that the SB 88 exemption has been used to date and no evidence of its necessity or effect on any particular project. Given the lack of a record, and the fact that the original sunset was only 18 months, a 5-year extension seems excessive. If the committee feels an extension is warranted, it may wish to consider a shorter extension, as well as the addition of conditions consistent with other exemptions approved by the committee, such as prohibiting impacts on protected species or cultural resources, requiring the lead agency to hold a public hearing and adopt mitigation measures for potential construction impacts, and requiring the notice of exemption to be filed with OPR.

Support: (Verified 3/14/2016) California Chamber of Commerce

Southwest California Legislative Council

Opposition: (Verified 3/14/2016) Clean Water Action California Natural Resources Defense Council Sierra Club California

Status: Active - Committee on Natural Resources

Vote: majority Appropriation: no Fiscal Committee: yes Local Program: yes

Senate Floor votes: Assembly floor votes:

Legislative Item #5 Action

SB789 (Wieckowski) Sale of water by local public entities: excise tax.

SB 789, as amended, Wieckowski. Driver’s license suspension: restricted privilege. Sale of water by local public entities: excise tax.

Recommended action: OPPOSE Presentation: Gene Wunderlich

Summary:

The California Constitution prohibits the Legislature from imposing taxes for local purposes, but allows the Legislature to authorize local governments to impose them.

This bill would authorize a local public entity that supplies water at retail or wholesale for the benefit of persons within the service area or area of jurisdiction of that public entity to impose, by ordinance, an excise tax on an excessive user of water, at a rate not to exceed 300% of the purchase price of the water, if the ordinance proposing the tax is approved by 2/3 of the electors voting on the measure and the revenue from the tax is equally distributed between the public entity and the State Water Resources Control Board for water conservation efforts within the jurisdiction of the public entity.

Arguments in Favor:

A local public entity that supplies water at retail or wholesale for the benefit of persons within the service area or area of jurisdiction of that public entity may impose, by ordinance, an excise tax on an excessive user of water, at a rate not to exceed 300 percent of the purchase price of the water, if both of the following conditions are met:

(1) The ordinance proposing that tax is approved by two-thirds of the electors voting on the measure pursuant to Article XIII C of the California Constitution.

(2) The revenue from the tax is equally distributed between the public entity and the State Water Resources Control Board for local water conservation efforts within the jurisdiction of that public entity. The local water conservation efforts may have cobenefits with other regions in the state.

(b) A tax imposed pursuant to this section may be in addition to any other tax authorized by this division.

Arguments in Opposition:

The bill is unconstitutional and unworkable. There is no definition of “excessive user of water” therefore; no practical way to determine who or what constitutes an excessive user of water. Several classes of water users exist such as residential, agricultural, commercial, industrial and institutional. Each uses water in varying ways and at varying prices depending on their water purveyors and necessary water treatment. Many already pay based on volume or contract amounts. Many business such as restaurants, food processors, grocery stores, medical clinics, etc. use water for health and safety purposes which may not be altered without another agency’s approval. Also, in some instances only a master water meter exists for several units without the ability to measure individual unit’s usage.

Southwest California Legislative Council

Farmers and ranchers, some who receive municipal water for irrigation, have made significant improvements in recent years in water use efficiency and spent billions of dollars statewide on more efficient irrigation systems. How will excessive water use be determined for them?

Prop 218 added Article XIII C and D to the California Constitution and, in general, the intent was to ensure that all taxes and most charges on property owners were subject to voter approval. It also clarified the definition of a “special tax” and sought to curb perceived abuses in the use assessments and property-related fees, especially the use of fees and assessments to for general governmental services rather than property-related services.

This would clearly be a special tax, thus the 2/3’s vote requirement.

Furthermore, current law was just amended to allow local agencies to increase their fines for violation of water conservation programs from $1,000 per incident to up to $10,000 per violation and an additional $500 per day the violation of water conservation program requirements occurs.

Support: (Verified 3/14/2016)

None on record Opposition: (Verified 2/16/2016)

None on record

Status: Active - Committee process

Vote: majority Appropriation: no Fiscal Committee: yes Local Program: no Senate Floor votes: Assembly floor votes:

Legislative Item #6 Action

AB2277 (Melendez) Local government finance: property tax revenue allocation: vehicle

license fee adjustments.

Introduced by Assembly Member Melendez (Coauthor: Assembly Member Linder)

Recommended action: SUPPORT Presentation: Gene Wunderlich

Summary: Existing property tax law requires the county auditor, in each fiscal year, to allocate property tax revenue to local jurisdictions in accordance with specified formulas and procedures, and generally provides that each jurisdiction shall be allocated an amount equal to the total of the amount of revenue allocated to that jurisdiction in the prior fiscal year, subject to certain modifications, and that jurisdiction’s portion of the annual tax increment, as defined.

Existing property tax law also requires that, for purposes of determining property tax revenue allocations in each county for the 1992–93 and 1993–94 fiscal years, the amounts of property tax revenue deemed allocated in the prior fiscal year to the county, cities, and special districts be reduced in accordance with certain formulas. It requires that the revenues not allocated to the county, cities, and special districts as a result of these reductions be transferred to the Educational Revenue Augmentation Fund in that county for allocation to school districts, community college districts, and the county office of education.

Beginning with the 2004–05 fiscal year and for each fiscal year thereafter, existing law requires that each city, county, and city and county receive additional property tax revenues in the form of a vehicle license fee adjustment amount, as defined, from a Vehicle License Fee Property Tax Compensation Fund that exists in each county treasury. Existing law requires that these additional allocations be funded from ad valorem property tax revenues otherwise required to be allocated to educational entities.

Southwest California Legislative Council

This bill would modify these reduction and transfer provisions for a city incorporating after January 1, 2004, and on or before January 1, 2012, for the 2016–17 fiscal year and for each fiscal year thereafter, by providing for a vehicle license fee adjustment amount calculated on the basis of changes in assessed valuation.

Support: (Verified 3/14/2016)

None on record Opposition: (Verified 3/14/2016)

None on record

Status: Active - Referred to Committee on Local Government

Vote: majority Appropriation: no Fiscal Committee: yes Local Program: yes Senate Floor votes: Assembly floor votes:

Legislative Item #7 Information

SBX2-2 (Hernandez) Medi-Cal: managed care organization tax. Approved by Governor March 01, 2016. Filed with Secretary of State March 01, 2016

Presentation: Gene Wunderlich

Summary: Existing law establishes the Medi-Cal program, administered by the State Department of Health Care Services, under which health care services are provided to qualified low-income persons. The Medi-Cal program is, in part, governed and funded by federal Medicaid program provisions. Under existing law, one of the methods by which Medi-Cal services are provided is pursuant to contracts with various types of managed care plans. Existing law, until July 1, 2016, imposes a sales tax on sellers of Medi-Cal managed care plans.

This bill, on July 1, 2016, and until July 1, 2019, would establish a new managed care organization provider tax, to be administered by the State Department of Health Care Services. The tax would be assessed by the department on licensed health care service plans, managed care plans contracted with the department to provide Medi-Cal services, and alternate health care service plans (AHCSP), as defined, except as excluded by the bill. The bill would require the department to determine for each health plan using the base data source, as defined, specified enrollment information for the base year. By October 14, 2016, or within 10 business days following the date upon which the department receives approval for federal financial participation, whichever is later, the bill would require the department to commence notification to the health plans of the assessed tax amount due for each fiscal year and the dates on which the installment tax payments are due for each fiscal year.

This bill would establish applicable taxing tiers and per enrollee amounts for the 2016–17, 2017–18, and 2018–19 fiscal years, respectively, for Medi-Cal enrollees, AHCSP enrollees, and all other enrollees, as defined. The bill would require the department to request approval from the federal Centers for Medicare and Medicaid Services as necessary to implement this bill. The bill would authorize the department to implement its provisions by means of provider bulletins, all-plan letters, or similar instructions, and to notify the Legislature of this action.

This bill would establish the Health and Human Services Special Fund in the State Treasury, into which all revenues, less refunds, derived from the taxes imposed by the bill would be deposited into the State Treasury to the credit of the fund. Interest and dividends earned on moneys in the fund would be retained in the fund, as specified. The bill would continuously appropriate the moneys in the fund to the State Department of Health Care Services for purposes of funding the nonfederal share of Medi-Cal managed care rates for health care services furnished to specified persons, thereby making an appropriation.

Existing law imposes a gross premiums tax of 2.35% on all insurers, as defined, doing business in this state, as set forth in the California Constitution. For purposes of the Corporation Tax Law, existing law sets forth items specifically excluded from gross income.

Southwest California Legislative Council

This bill would provide that the qualified health care service plan income, as defined, of health plans that are subject to the managed care organization provider tax would be excluded from the definition of gross income for purposes of taxation under the above provisions, as specified. The bill would reduce the gross premiums tax rate from 2.35% to 0% for those premiums received on or after July 1, 2016, and on or before June 30, 2019, for the provision of health insurance paid by health insurers providing health insurance that has a corporate affiliate, as defined, that is a health care service plan or health plan that is subject to the managed care organization provider tax imposed under the bill, as specified. The bill would require the State Department of Health Care Services to annually report specified information to the Franchise Tax Board with regard to these provisions. The bill would authorize the board to implement these provisions and would exempt the board from the administrative rulemaking process.

Existing law provides that when the laws of another state or foreign county impose certain taxes or other amounts on California insurers, or their agents or representatives, the same taxes or other amounts are imposed in this state upon the insurers, or their agents or representatives, of the other state or country doing business in this state.

The bill would prohibit the Insurance Commissioner from considering the reduction of the gross premiums tax rate under this bill in any determination to impose or enforce a tax under those retaliatory tax provisions.

The bill would provide that these provisions become operative on the later of July 1, 2016, or on the date the Director of Health Care Services certifies in writing that federal approval necessary for receipt of federal financial participation has been obtained.

This bill would include a change in state statute that would result in a taxpayer paying a higher tax within the meaning of Section 3 of Article XIII A of the California Constitution, and thus would require for passage the approval of 2/3 of the membership of each house of the Legislature.

Analysis:

From CalChamber:

We are pleased to SUPPORT SBX2 15 (Hernandez) and ABX2 20 (Bonta), which preserve critical funding for the state’s Medi-Cal program without undermining the affordability of commercial health care purchased by employers, families, and individuals.

When the federal Centers for Medicare and Medicaid Services (CMS) issued guidance in 2014 indicating that California’s existing MCO tax, which generates approximately $1 billion a year for the state’s Medi-Cal program, did not comply with the federal rules governing provider taxes and could not be renewed in 2016, policymakers were left with a difficult task. Any replacement proposal would have to raise enough revenue to offset the expiring tax and prevent a reduction in Medi-Cal provider reimbursements, but would also need to apply broadly to most, if not all, health care plans without creating unreasonable disparities between them that might generate pressure in the commercial health insurance marketplace to increase costs for California purchasers. We believe this proposal sufficiently meets these important goals.

Together these bills present a comprehensive solution that is a win-win for California. For this reason, we are pleased to SUPPORT SBX2 15 (Hernandez) and ABX2 20 (Bonta).

MCO Health Care Tax Swap/Reduction Information (AB 2X 15, AB 2X 20)

Restructures the state’s method of taxing health care service plans by establishing a Managed Care Organization (MCO) Tax to replace (hence, swap) the existing tax that has been deemed to violate federal regulations, changes the Gross Premiums Tax rate from 2.35% to 0% for certain qualifying health plans, exempts certain qualifying health plans from Corporations Tax, and prohibits the Insurance Commissioner from enforcing any tax under a retaliatory tax provision.

When taken in its entirety, the bill will provide a net positive of over $100 million to the commercial health plan market, will draw down more than $1.2 billion in federal matching funds each year to pay for Californians’ health care needs, and should not result in premium increases for health plan enrollees. As of 2015, California receives only $0.68 back from the federal government for every dollar paid by a Californian in federal taxes, so bringing federal dollars back to California to help pay for mandatory healthcare expenses is a practical way to free up funding for other key state priorities, including $300 million for the Developmentally Disabled fund which had been cut by Gov. Brown. MAJOR STATE REVENUE GAIN. The bill provides $1.3 billion in net savings to the state for 2016-17, $1.3 billion in 2017-18, and $1.4 billion in 2018-19.

Southwest California Legislative Council

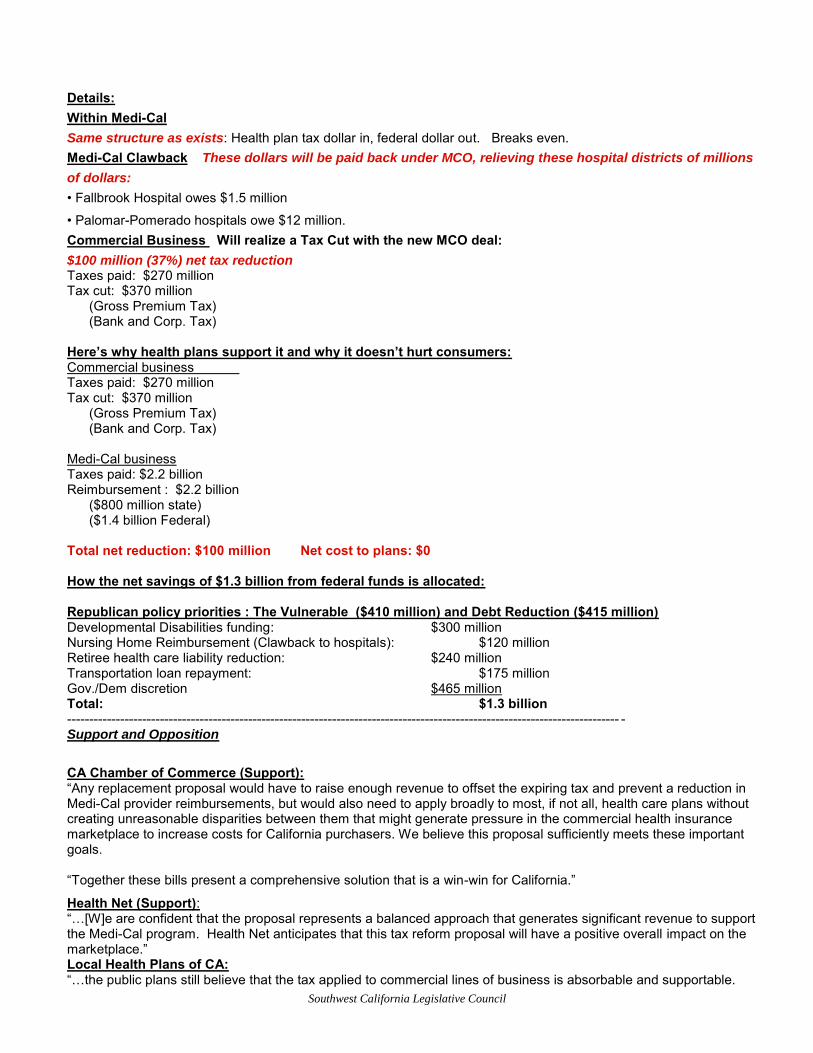

Details: Within Medi-Cal Same structure as exists: Health plan tax dollar in, federal dollar out. Breaks even. Medi-Cal Clawback These dollars will be paid back under MCO, relieving these hospital districts of millions

of dollars: • Fallbrook Hospital owes $1.5 million

• Palomar-Pomerado hospitals owe $12 million. Commercial Business Will realize a Tax Cut with the new MCO deal: $100 million (37%) net tax reduction Taxes paid: $270 million Tax cut: $370 million (Gross Premium Tax) (Bank and Corp. Tax) Here’s why health plans support it and why it doesn’t hurt consumers: Commercial business Taxes paid: $270 million Tax cut: $370 million (Gross Premium Tax) (Bank and Corp. Tax) Medi-Cal business Taxes paid: $2.2 billion Reimbursement : $2.2 billion ($800 million state) ($1.4 billion Federal) Total net reduction: $100 million Net cost to plans: $0 How the net savings of $1.3 billion from federal funds is allocated: Republican policy priorities : The Vulnerable ($410 million) and Debt Reduction ($415 million) Developmental Disabilities funding: $300 million Nursing Home Reimbursement (Clawback to hospitals): $120 million Retiree health care liability reduction: $240 million Transportation loan repayment: $175 million Gov./Dem discretion $465 million Total: $1.3 billion ----------------------------------------------------------------------------------------------------------------------------- - Support and Opposition

CA Chamber of Commerce (Support): “Any replacement proposal would have to raise enough revenue to offset the expiring tax and prevent a reduction in Medi-Cal provider reimbursements, but would also need to apply broadly to most, if not all, health care plans without creating unreasonable disparities between them that might generate pressure in the commercial health insurance marketplace to increase costs for California purchasers. We believe this proposal sufficiently meets these important goals. “Together these bills present a comprehensive solution that is a win-win for California.”

Health Net (Support): “…[W]e are confident that the proposal represents a balanced approach that generates significant revenue to support the Medi-Cal program. Health Net anticipates that this tax reform proposal will have a positive overall impact on the marketplace.” Local Health Plans of CA: “…the public plans still believe that the tax applied to commercial lines of business is absorbable and supportable.

Southwest California Legislative Council

Kaiser (Neutral): “…[w]e are confident the proposal is a balanced approach that will not negatively affect our purchasers…”and will “have a positive overall impact on the health care market.” CA Association of Health Plans (Support): “The MCO tax bills include two tax relief provisions that eliminate current taxes on health plans and insurers. These tax cuts, coupled with other safeguards, protect the affordability of health care coverage.” Blue Shield of CA (Support): “BSC has thoroughly reviewed this legislation and the accompanying fiscal model and are confident that the proposal represents a valuable package of tax reforms for health care consumers. In total, this tax reform will lower the total tax burden on consumers of health coverage and insurers, while protecting a vital funding source for the Medi-Cal program.

Howard Jarvis Taxpayers Association (no position): (See letter attached) “Arguments are being made that this tax is an extension of the 2013 version and no Republicans voted for that proposal, thereby no Republicans should vote for this version either. However, the two proposals are not the same. The 2013 version included a broad sales tax increase on Medi-Cal plans that the 2016 plan does not include. Instead, the 2016 model contains two broad-based tax reductions in both the Gross Premiums Tax (GPT) and the Bank and Corporation tax (B&C) which, in theory, should be revenue neutral for the health plans and ratepayers.” National Federation of Independent Business: “Neutral.” CalTax: “No position.” CIGNA (Oppose): “Unfortunately, the most recent MCO tax proposal creates substantial competitive market advantages for some California plans at the expense of others.” Anthem Blue Cross (Support): “The bill, which is the product of months of negotiations between health plans and the Brown Administration, successfully balances the need to protect $1.1B in Medi-cal funding with the need to control costs and maintain competition in the commercial market.

Support (Verified 2/26/2016)

Anthem Association of Regional Center Agencies Barton Health Bay Area Council Blue Shield of California Brea Chamber of Commerce California Association of Health Facilities Developmental Services Conference California Association of Health Plans California Chamber of Commerce California Disability Services Association California Hospital Association California Respite Association California State Association of Counties California State Council on Developmental Disabilities California Supported Living Network Cal-TASH Coalinga Regional Medical Center Community Regional Medical Center Developmental Services Network Disability Rights California Easter Seals Disability Services Eastern Plumas Health Care Educate.Advocate. Family Resource Centers Network of California George L. Mee Memorial Hospital Health Access California Health Net

IDA California Jewish Home of San Francisco Kaweah Delta Health Care District Kern Valley Healthcare District Lanterman Coalition Mayers Memorial Hospital District Modoc Medical Center Mountains Community Hospital Local Health Plans of California Los Angeles Area Chamber of Commerce Motion Picture & Television Fund North Orange County Chamber Orchard Hospital Palomar Health People First of California Rancho Cordova Chamber of Commerce ResCoalition Seneca Healthcare District Service Employees International Union Sharp HealthCare SoCal Association of People Supporting Employment First Sonora Regional Medical Center Southwest California Legislative Council Tahoe Forest Hospital District The Alliance The Arc California United Cerebral Palsy California Collaboration Western Center on Law & Poverty

Opposed (Verified 2/26/2016) Cigna

Southwest California Legislative Council

Senate Floor votes: Aye: Roth No: Morrell, Stone

Assembly floor votes: Aye: Jones, Linder, Mayes, Medina, Waldron No: Melendez

Calvary Bible Fellowship v. Riverside County Action

Requested action: SUPPORT Riverside County Presentation: John Kelliher

Background:

On February 10, 2016, Calvary Bible Fellowship sued Riverside County, challenging the validity of the zoning ordinances that serve as the foundation to Temecula Valley Wine Country. Calvary operates a small church in the heart of Wine Country. They began operations in 1996 - without a permit, and in contradiction to ordinances - and then appealed to the County for an exception. Despite significant opposition from Wine Country interests, the County granted a permit as a non-conforming use - albeit with mitigating conditions which observers note that Calvary has failed to comply with. Calvary has, for several years, pursued a major expansion from 7.4 acres to approximately 30 acres, with a Costco-sized (80,000 square feet) auditorium, major school facilities, and more than 500 parking spaces. During the last Wine Country zoning update, the County carved out a "donut hole" that included only the 30 acres owned by Calvary, leaving the Calvary issue undecided. After a recent legal decision made it apparent that Calvary's expansion would likely not be permitted, Calvary sued. Calvary's expansion has been opposed by the Temecula Valley Winegrowers Association, the Board of Visit Temecula Valley, and by various other organizations and community leaders - including 11 Temecula Valley Citizens of the Year. In addition to the general concern for incompatible consumption of limited Wine Country land, specific concerns include traffic surges onto two lane roads, likely future limits on normal pest control activities within a substantial radius of the project, and potential threats to wine sales by surrounding wineries due to school proximity. The suit essentially challenges the concept of an Agriculture Preserve, a proven and effective method of incubating a wine region by staving off suburban development. As a comparison, Napa County initiated the nation's first Ag Preserve in 1968. The Napa Preserve was initially controversial, facing substantial opposition. Over the year, it withstood legal challenges, won over detractors to become overwhelmingly supported, and has expanded to include 91% or County land. In contrast, Temecula's Wine Country zone comprises a tiny fraction - about 0.5% - of Riverside County land. Consequently, industry leaders consider any large parcels within the zone to be extremely scarce and extremely valuable in adhering to the stated purpose of the Wine Country zone

Argument in Support (Maintain Wine Country Ordinance)

A lawsuit threatens to weaken the foundation of not only Wine Country, but also the entire Temecula Valley tourism industry. Whether the County chooses to defend, or settle (for budgetary reasons), could have a significant long term impact on the industry's goal to develop the region's tourism industry.

Argument in Opposition (Support Calvary lawsuit)

A request has been made to the Calvary Bible Fellowship for comment and/or speaker. As of this date there has been no response. A copy will be forwarded to you if available. (Link to 21 page complaint)

Requested Action: Letter of Support for the County to contest the lawsuit, and maintain the Wine Country ordinance.

Southwest California Legislative Council

County delays action on repealing Wine Country church ordinance

Riverside County had agreed to repeal the ordinance as part of a lawsuit settlement. County staff needs more time, a spokesman says.

BY AARON CLAVERIE / STAFF WRITER Published: June 7, 2015 Updated: June 8, 2015 10:38 a.m.

FRANK BELLINO , STAFF PHOTOGRAPHER

The Riverside County Board of Supervisors has delayed action on the repeal of an ordinance considered beneficial to Calvary Chapel Bible Fellowship, a nondenominational church nestled in the heart of Temecula Valley Wine Country.

The county agreed to repeal the ordinance – which removes a time limit for how long businesses can operate as legal nonconforming uses – as part of the settlement of a lawsuit filed by Protect Wine Country, a coalition of growers, winery owners and tourism executives opposed to the church’s expansion plans.

County spokesman Ray Smith said Thursday that consideration of the ordinance was postponed to give staff members time to add more information to the report for the board. He did not disclose the nature of that information.

Consideration of the ordinance could be brought up at the June 16 meeting or the meeting on June 30, he said.

The ordinance targeted by Protect Wine Country was approved in the summer of 2014.The group filed a lawsuit a month later in a bid to get it repealed. According to a report for the board, the ordinance removed time limits on how long a business could operate when land use or zoning is changed.

Under the previous rules, the business would have to apply for an extension at the end of a specified time frame. There would be no fiscal impact associated with the repeal and the old time limits would be restored. Critics of the church’s expansion plans say the ordinance benefits Calvary Chapel because it was permitted in the late 1990s when churches were allowed in Wine Country. Subsequent zoning banned churches from the vast majority of the region, turning the church into a legal nonconforming use.

Ray Falkner, one of the leaders of Protect Wine Country, said repeal of the ordinance would require the church to at least seek an extension of its operating permit. This possibly would trigger a review by the county that could call into question the church’s entire operation, including the traffic impacts on Rancho California Road. “Calvary Chapel isn’t in compliance with the initial conditions they were issued,” he said.

Robert Tyler, an attorney representing Calvary Chapel, said he doesn’t think the repeal would change anything for the church. “The intent of 18.8 (the section that addresses time limits) clearly is not to tell a church they can only be on their property for a certain time,” he said.

The county last year approved a new zoning plan for the entirety of Wine Country, an 18,000-acre swath that stretches south across Temecula Parkway. But that plan doesn’t include the 30 acres owned by Calvary Chapel. Protect Wine Country has filed suit to get the “doughnut hole” in the plan removed. That lawsuit may be heard by a judge sometime later this year.

The church’s expansion plans call for building an auditorium designed to accommodate 936 people, nearly double the capacity of the existing sanctuary. The structure and parking would go on 23 acres to the north of the developed 7-acre church campus, which is east of Calle Contento.

Southwest California Legislative Council

Calvary Chapel Sues for Religious Ban in 'Wine Country'

10:30AM EST 2/11/2016 LORI SANADA/ADVOCATES FOR FAITH & FREEDOM

Calvary Wine Country opened its doors in 1996 when churches were once allowed to locate in the 17,900-acre Wine Country region—an area equal to 28 square miles. (ccbf.net)

Calvary Chapel Bible Fellowship filed a complaint in federal court against the County of Riverside, California, based on the United States Constitution and the Religious Land Use and Institutionalized Person's Act of 2000.

Calvary Chapel Bible Fellowship, commonly known as "Calvary Wine Country," is located in the region of California known as the Temecula Wine Country. Calvary Wine Country opened its doors in 1996 when churches were once allowed to locate in the 17,900 acre Wine Country region—an area equal to 28 square miles. However, soon after Calvary Wine Country was approved, the County banned churches from the Temecula Wine Country, leaving Calvary Wine Country as a nonconforming use. Now, Calvary's ability to expand its facilities for its flourishing congregation in the Wine Country is uncertain at best. Calvary Wine Country plans to remain in the Wine Country and to build a larger sanctuary on its 28-acre adjacent property. However, the county's zoning ordinances still ban churches and Calvary Wine Country is the only church in the Temecula Wine Country. Meanwhile, the County permits special occasion facilities, wineries, hotels, resorts, restaurants and many other tourist related uses in the Wine Country. Calvary's Pastor Clark Van Wick said, "It's a tragedy to see our religious liberty eroded in this country where men and women have fought and died to protect our liberty. It's un-American to see churches outlawed like we're seeing here in the neighborhood I've lived in for 27 years." "This is a classic case for the federal religious land use law that protects churches and requires that zoning authorities treat religious assemblies on equal terms to other nonreligious assemblies," said Robert Tyler, managing partner of Tyler & Bursch, LLP and counsel for Calvary Wine Country. He further commented, "Calvary Wine Country has long desired to just be a good neighbor, to work cooperatively with the county and to provide a place of worship for the thousands of residents that live in the Wine Country." Unfortunately, Calvary Wine Country has been the target of litigation by a "loose" organization named Protect Wine Country. Calvary Wine Country has had to fight a neighboring vintner, a special interest group, and other politically influential wineries just to continue its right to exist on its own property. Robert Tyler commented, "It is ironic that Father Junipero Sera, the 'Father of California Wine,' planted the first known vineyard in California at the San Diego Mission de Alcala and vineyards graced the California Missions for many years. Today, however, Riverside County has determined that a church is no longer compatible with vineyards and has banned all religious assemblies from the Temecula Wine Country." Calvary Wine Country is represented by Advocates for Faith & Freedom in association with Tyler & Bursch, LLP. Robert Tyler filed one of the first lawsuits under the Religious Land Use and Institutionalized Persons Act of 2000 on behalf of the Elsinore Christian Center in Lake Elsinore, California. That suit resulted in a successful resolution wherein the City paid more than $1.6 million in settlement. Robert's firm, Tyler & Bursch, LLP, has become one of the nation's premier firms for handling religious land use cases on behalf of churches.