sovereign debt panel june 6, 2012 jeffrey frankel harpel professor institute for global law &...

TRANSCRIPT

Sovereign Debt PanelSovereign Debt Panel

June 6, 2012June 6, 2012

Jeffrey FrankelJeffrey FrankelHarpel ProfessorHarpel Professor

Institute for Global Law & Policy, Harvard Law SchoolInstitute for Global Law & Policy, Harvard Law School

Most experience with sovereign debt Most experience with sovereign debt problems during our lifetimes arose problems during our lifetimes arose

in developing countriesin developing countries

Recycling of petrodollars after 1974 -Recycling of petrodollars after 1974 - ended in the international debt crisis of 1982 -ended in the international debt crisis of 1982 - and the Lost Decade of growth in Latin America,and the Lost Decade of growth in Latin America,

until the write-downs of the Brady Plan: 1989- .until the write-downs of the Brady Plan: 1989- .

Emerging market inflows in 1990sEmerging market inflows in 1990s ended in the Mexican peso crisis of 1994, ended in the Mexican peso crisis of 1994, East Asia crisis of 1997-98 East Asia crisis of 1997-98 (private debts), and(private debts), and

Russia Russia 1998 1998 & & Argentina Argentina 20012001 devaluations devaluations & defaults.& defaults.

Most Emerging Market countries learned from Most Emerging Market countries learned from the sovereign debt crises of the 1980s & 1990s.the sovereign debt crises of the 1980s & 1990s.

But many leaders in advanced economies But many leaders in advanced economies failed to do so.failed to do so.

They thought it could never happen to them.They thought it could never happen to them.

Most notably, leaders of euroland,Most notably, leaders of euroland, even after the periphery countrieseven after the periphery countries

violated the deficit & debt ceilings violated the deficit & debt ceilings of Maastricht and the SGP;of Maastricht and the SGP;

And even after the Greek crisis hit in late 2009 !And even after the Greek crisis hit in late 2009 !

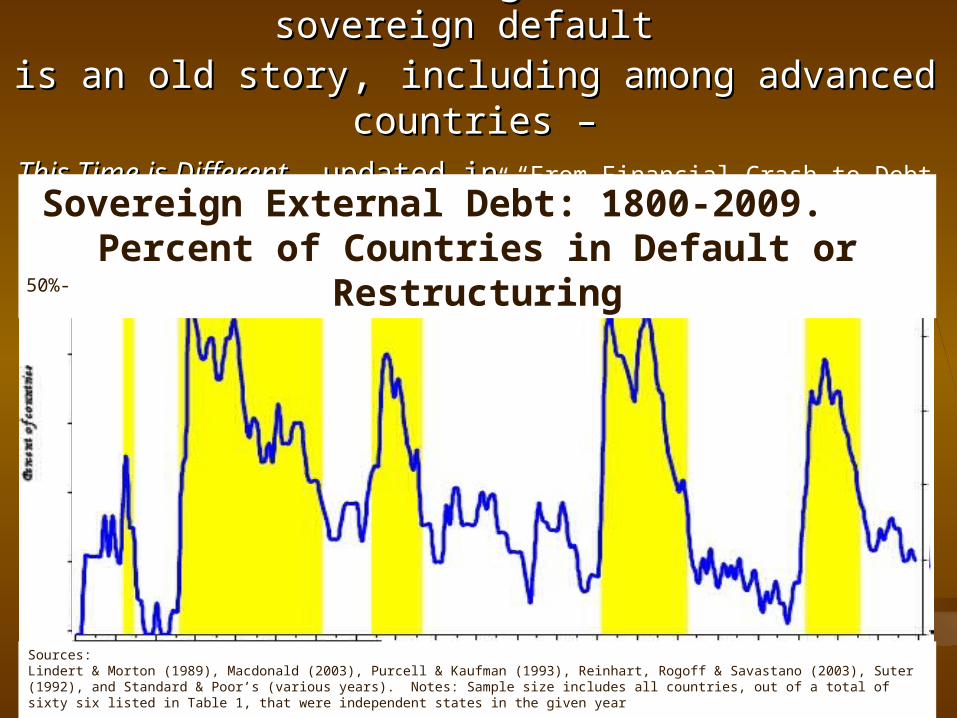

But Reinhart & Rogoff remind us: But Reinhart & Rogoff remind us: sovereign default sovereign default

is an old storyis an old story, , including among advanced countries –including among advanced countries –This Time is DifferentThis Time is Different, updated in , updated in “From Financial Crash to Debt Crisis,” 2010

Sovereign External Debt: 1800-2009. Percent of Countries in Default or

Restructuring50%-

Sources:Lindert & Morton (1989), Macdonald (2003), Purcell & Kaufman (1993), Reinhart, Rogoff & Savastano (2003), Suter (1992), and Standard & Poor’s (various years). Notes: Sample size includes all countries, out of a total of sixty six listed in Table 1, that were independent states in the given year

Some defaulters, since the Napoleonic War

Sources: S & P; Kenneth Rogoff & Carmen Reinhart; http://jongoodwin.com/2010/04/15/die-rechnung/

Which governments have defaulted?

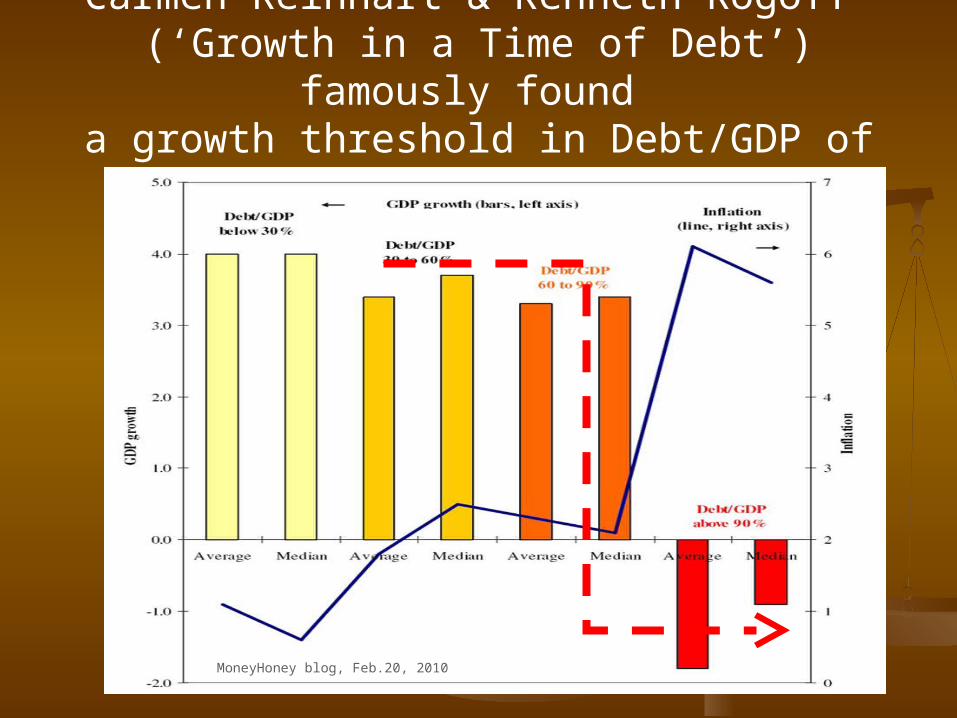

Carmen Reinhart & Kenneth Rogoff (‘Growth in a Time of Debt’) famously found

a growth threshold in Debt/GDP of 90%

MoneyHoney blog, Feb.20, 2010

7

The historic role reversalThe historic role reversal Debt levelsDebt levels among rich countries among rich countries (debt/GDP ratios ≈ 80%) (debt/GDP ratios ≈ 80%)

are now more than twice those of emerging marketsare now more than twice those of emerging markets and rising rapidly.and rising rapidly.

Some emerging markets have earned credit ratings Some emerging markets have earned credit ratings higher than some so-called advanced countries,higher than some so-called advanced countries, and interest rate spreads that are lower..and interest rate spreads that are lower..

Over the last decade some emerging market countries Over the last decade some emerging market countries finally developed finally developed countercyclicalcountercyclical fiscal policies: fiscal policies:

They took advantage of the boom years 2003-2007 They took advantage of the boom years 2003-2007 to run budget primary to run budget primary surpluses and cumulate reservessurpluses and cumulate reserves .. By 2007, Latin America had reduced its debt to 33% of GDP, By 2007, Latin America had reduced its debt to 33% of GDP,

as compared to 63 % in the United States.as compared to 63 % in the United States.

And so were able to respond to global recession of 2008-09 .And so were able to respond to global recession of 2008-09 .

But weaker in advanced economies.But weaker in advanced economies.

World Economic Outlook, IMF, April 2012

Public finances since 2001have become much stronger in EMs

Public finances since 2001have become much stronger in EMs

Ratio of public debt to GDP among advanced countriesis the highest since the end of WW II

Source: Carlo Cotarelli “Making Goldilocks Happy,” IMF, Apr. 20, 2012

Country creditworthiness is now inter-shuffledCountry creditworthiness is now inter-shuffled““Advanced” countries Advanced” countries (Formerly) “Developing” countries(Formerly) “Developing” countries

AAA Germany, UKAAA Germany, UK Singapore, Hong KongSingapore, Hong Kong

AA+ AA+ US, FranceUS, France

AA AA BelgiumBelgium ChileChile

AA-AA- JapanJapan ChinaChina

A+A+ KoreaKorea

AA Malaysia, South AfricaMalaysia, South Africa

A-A- Brazil, Thailand, BotswanaBrazil, Thailand, Botswana

BBB+BBB+ Ireland, Italy, Spain Ireland, Italy, Spain

BBB-BBB- IcelandIceland Colombia, IndiaColombia, India

BB+BB+ Indonesia, PhilippinesIndonesia, Philippines

BBBB PortugalPortugal Costa Rica, JordanCosta Rica, Jordan

BB Burkina FasoBurkina Faso

SDSD GreeceGreece

S&P ratings, Feb.2012 updated 4/25/2012

World Economic Outlook, IMF, April 2012

One indication of improved EM creditworthiness:One indication of improved EM creditworthiness: EM sovereigns used to have to pay higher interest rates EM sovereigns used to have to pay higher interest rates

than many US corporates (BB), but now pay less.than many US corporates (BB), but now pay less.

12

Spreads for Greece, etc., were near zero, 2001-07,Spreads for Greece, etc., were near zero, 2001-07,but then shot up in 2008 and, esp., 2010-12.but then shot up in 2008 and, esp., 2010-12.

Market Nighshift Nov. 16, 2011

It’s not just the It’s not just the levellevel of debt/GDP that matters of debt/GDP that matters

but the risk of getting stuck on an explosive path, but the risk of getting stuck on an explosive path, with ever-rising debt/GDPwith ever-rising debt/GDP because of high primary deficit or interest rates because of high primary deficit or interest rates

(or low growth), (or low growth), combined with risk of a sudden deteriorationcombined with risk of a sudden deterioration

from a worsening of global financial conditions from a worsening of global financial conditions or a decline in export markets, or a banking crisis.or a decline in export markets, or a banking crisis.

Early Warning indicators:Early Warning indicators: compositioncomposition of capital inflows of capital inflows

Fx-denominated, ST, bank loans vs. Fx-denominated, ST, bank loans vs. FDI, equity & contracts with automatic adjustment FDI, equity & contracts with automatic adjustment

provisions.provisions. Plus real currency overvaluation & fx reserves Plus real currency overvaluation & fx reserves (for peggers)…(for peggers)…

Quality of fiscal policy-makingQuality of fiscal policy-making

Fundamentally: Quality of institutions.Fundamentally: Quality of institutions. This does not mean “tough” rules – This does not mean “tough” rules –

like SGP, debt ceiling or BBA – which lack enforceability.like SGP, debt ceiling or BBA – which lack enforceability.

Better would be structural budget targets (Swiss) Better would be structural budget targets (Swiss) with forecasts from independent experts (Chile).with forecasts from independent experts (Chile).

One third of developing countries since 2000 have One third of developing countries since 2000 have graduated from pro-cyclical spending to countercyclical,graduated from pro-cyclical spending to countercyclical,

even while US, UK & euro countries have forgotten even while US, UK & euro countries have forgotten how to run countercyclical fiscal policy,how to run countercyclical fiscal policy,

and instead enact fiscal expansion in booms and instead enact fiscal expansion in booms & contraction after recessions.& contraction after recessions.

15

Procyclical fiscal policy Procyclical fiscal policy

Definition: Definition:

Governments raise spending or cut taxes in booms; Governments raise spending or cut taxes in booms;

and are then forced to retrench in downturns,and are then forced to retrench in downturns,

thereby exacerbating economic upswings & downswings.thereby exacerbating economic upswings & downswings.

EE..gg., ., the the correlation between spendingcorrelation between spending & & GDP was GDP was positivepositive..

Historically, this has been true in developing countries Historically, this has been true in developing countries Especially among commodity-producersEspecially among commodity-producers and in Latin America.and in Latin America.

Correlations between Govt. Spending & GDP1960-1999

pro

cyc

lic

al

G always used to be pro-cyclical for most developing countries.

cou

nte

rcyc

lic

al

Adapted from Kaminsky, Reinhart & Vegh, 2004, “When It Rains It Pours”

Pro-cyclical spending

Counter-cyclical spending

}

In the last decade, about 1/3 developing countries

switched to countercyclical fiscal policy:Negative correlation of G & GDP.

Frankel, Vegh & Vuletin (2012)

pro

cyc

lical

cou

nte

rcyc

lical

Correlations between Govt. Spending & GDP2000-2009

To summarize the fiscal role reversal,To summarize the fiscal role reversal,

Many important emerging markets have, Many important emerging markets have, so far this century, achieved:so far this century, achieved: Lower debt levels than advanced economies;Lower debt levels than advanced economies; improved credit ratings;improved credit ratings; lower sovereign spreads; andlower sovereign spreads; and less procyclical fiscal policies.less procyclical fiscal policies.

Rules and optimism bias in official forecastsRules and optimism bias in official forecasts

Fiscal rules are the current fashion. Do they help?Fiscal rules are the current fashion. Do they help?

The SGP has utterly failedThe SGP has utterly failed The Fiscal Compact will be no better.The Fiscal Compact will be no better.

As in the US: As in the US: Gramm-Rudman-HollingsGramm-Rudman-Hollings Debt ceiling legislationDebt ceiling legislation Balanced Budget Amendment, if we had one.Balanced Budget Amendment, if we had one.

Optimism bias in forecasts is Optimism bias in forecasts is worseworse among the € countries among the € countries supposedly subject to the budget rules of the SGP,supposedly subject to the budget rules of the SGP, presumably because official forecasters feel pressure to announce presumably because official forecasters feel pressure to announce

they are on track to meet budget targets even if they are not.they are on track to meet budget targets even if they are not. When euro country deficits strayed above the 3% GDP limit, When euro country deficits strayed above the 3% GDP limit,

governments would adjust their forecasts, but not their policies. governments would adjust their forecasts, but not their policies.

http://ksghome.harvard.edu/~jfrankel/http://ksghome.harvard.edu/~jfrankel/Blog: Blog: http://content.ksg.harvard.edu/blog/jeff_frankels_weblog/

Writings by the speaker on fiscal policy:

• “On Graduation from Procyclicality,” with C.Végh & G.Vuletin, 2012. NBER WP 17619, Nov. 2011. Summarized in "Fiscal Policy in Developing Countries: Escape from Procyclicality," Vox.eu, June 23, 2011.

• "Over-optimism in Forecasts by Official Budget Agencies and Its Implications," Oxford Review of Economic Policy Vol.27, Issue 4, 2011, 536-562. NBER WP 17239; Summary in NBER Digest, Nov.2011.

• “A Solution to Fiscal Procyclicality: The Structural Budget Institutions Pioneered by Chile,” forthcoming, Fiscal Policy and Macroeconomic Performance, 2012. Central Bank of Chile WP 604, Jan.2011.

• “A Lesson From the South for Fiscal Policy in the US and Other Advanced Countries,” Comparative Economic Studies. 53, no.3, Sept.2011. HKS RWP11-014. Short version, India Planning Commission Workshop on Restoring Inclusive Growth, Oct. 2010.

• “Snake-Oil Tax Cuts,” 2008, Economic Policy Institute, Briefing Paper 221. HKS RWP 08-056

• “The ECB’s Three Big Mistakes,” VoxEU, May 16, 2011.• "Let Greece Go to the IMF," Jeff Frankel’s blog, Feb.11, 2010.• “‘Excessive Deficits’: Sense and Nonsense in the Treaty of Maastricht;

Comments on Buiter, Corsetti and Roubini,” Economic Policy, Vol.16,1993.

AppendicesAppendices 1) Sovereign spreads1) Sovereign spreads

2) The example of Greek debt2) The example of Greek debt And the euro crisisAnd the euro crisis

3) Institutions 3) Institutions for countercyclical for countercyclical fiscal policy fiscal policy

4) US debt woes4) US debt woes

Copyright 2007 Jeffrey Frankel, unless otherwise noted

WesternAsset.com

Bpblogspot.com

↑ Spreads shot up in 1990s crises,• and fell to low levels in next decade.↓

Spreads rose again in Sept.2008 ↑ , • esp. on $-denominated debt • & in E.Europe.

World Bank

Sovereign spreads

Sovereign spreads depend on risk perceptions,Sovereign spreads depend on risk perceptions,as reflected in the VIX as reflected in the VIX

(option-implied volatility of US stock market)(option-implied volatility of US stock market)

Laura Jaramillo & Catalina Michelle Tejada, IMF Working Paper, 2011

Risk on

Riskon

Riskoff

Appendix 2:The example of Greek debt

The Greek budget deficitThe Greek budget deficitnevernever got below the 3% of GDP limit, got below the 3% of GDP limit,

nor did the debt ever decline toward the 60% limitnor did the debt ever decline toward the 60% limit

25

Even Greece’s Even Greece’s primaryprimary budget deficit budget deficithas been far in excess of 3% since 2008has been far in excess of 3% since 2008

26

Source: IMF, 2011.I. Diwan, PED401, Oct. 2011

Optimism bias in official forecasts, Optimism bias in official forecasts, continuedcontinued

Fiscal rules are the current fashion. Do they help?Fiscal rules are the current fashion. Do they help? Example of failure of fiscal rules Example of failure of fiscal rules

in the presence of official forecast bias in the presence of official forecast bias

The Greek government projected The Greek government projected in 2000 that its budget deficit would shrinkin 2000 that its budget deficit would shrink below 2% of GDP one year in the future and below 2% of GDP one year in the future and below 1% of GDP two years into the future, and below 1% of GDP two years into the future, and that it would swing to surplus 3 years into the future. that it would swing to surplus 3 years into the future.

The actual deficit: 4-5% of GDPThe actual deficit: 4-5% of GDP, , well above the 3%-of-GDP ceiling.well above the 3%-of-GDP ceiling.

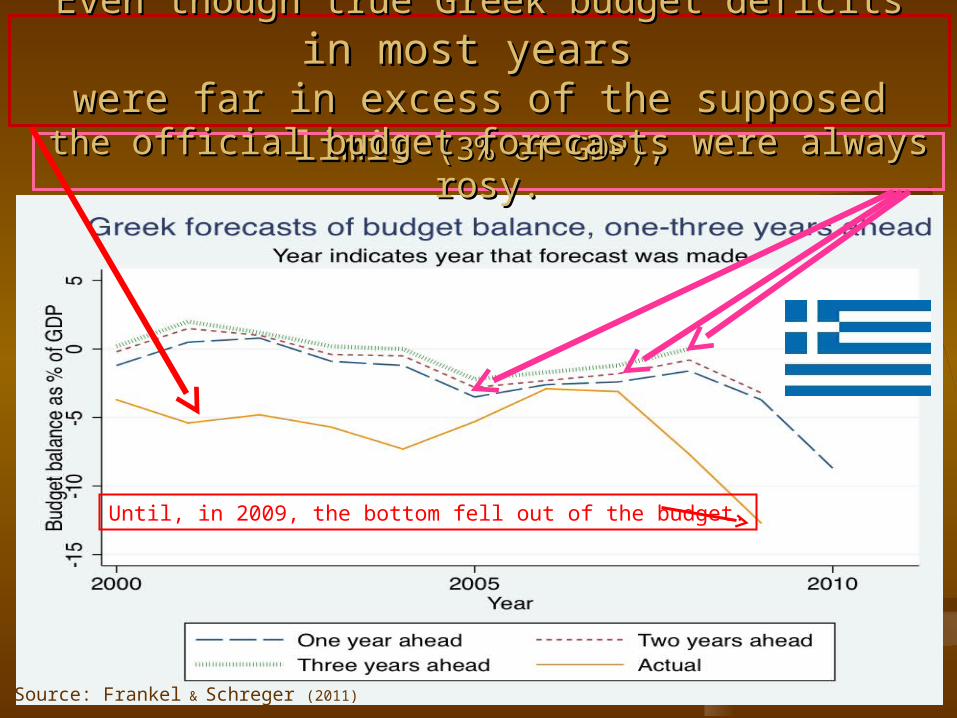

Even though true Greek budget deficitsEven though true Greek budget deficits in most years in most years were far in excess of the supposed limit were far in excess of the supposed limit (3% of GDP),(3% of GDP),

28Source: Frankel & Schreger (2011)

the the official budget forecasts were always rosy.official budget forecasts were always rosy.

Until, in 2009, the bottom fell out of the budget.

Appendix 3: Countries with good institutional quality tend Appendix 3: Countries with good institutional quality tend to be the ones that have attained countercyclical fiscal policyto be the ones that have attained countercyclical fiscal policy

Copyright 2007 Jeffrey Frankel, unless otherwise noted

API-120 - Macroeconomic Policy Analysis I Professor Jeffrey Frankel, Kennedy School of Government, Harvard University

Frankel, Vegh & Vuletin (2012)

pro

cyc

lical

→

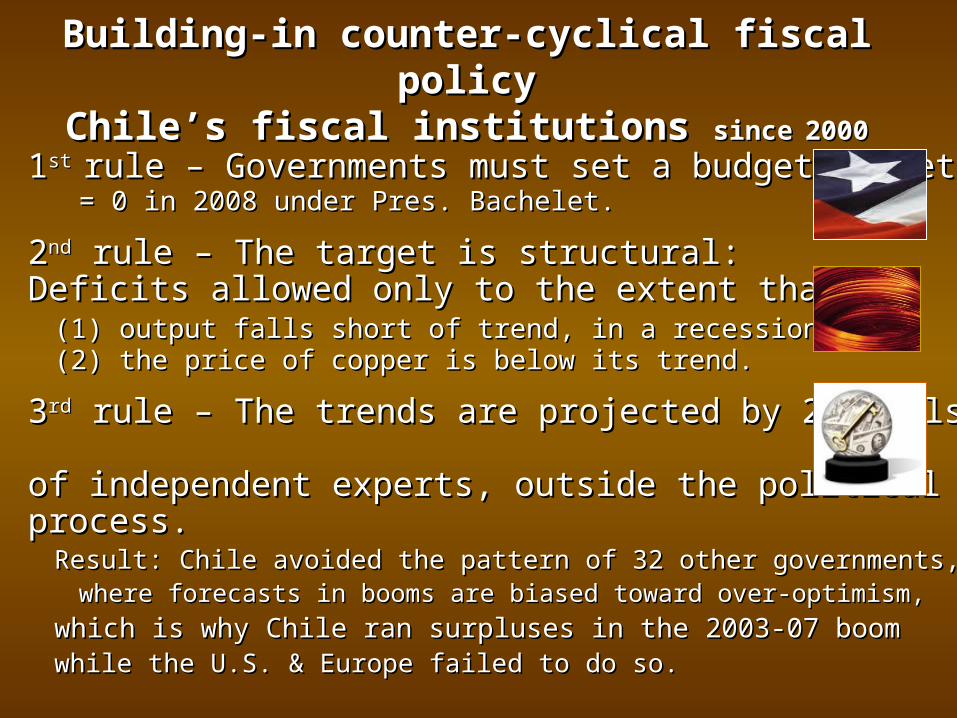

Building-in counter-cyclical fiscal policyBuilding-in counter-cyclical fiscal policyChile’s fiscal institutions Chile’s fiscal institutions sincesince 20002000

11st st rule – Governments must set a budget targetrule – Governments must set a budget target= 0 in 2008 under Pres. Bachelet. = 0 in 2008 under Pres. Bachelet.

22ndnd rule – The target is structural: rule – The target is structural: Deficits allowed only to the extent thatDeficits allowed only to the extent that

(1) output falls short of trend, in a recession, or(1) output falls short of trend, in a recession, or(2) the price of copper is below its trend.(2) the price of copper is below its trend.

33rdrd rule – The trends are projected by 2 panels rule – The trends are projected by 2 panels of independent experts, outside the political process.of independent experts, outside the political process.

Result: Chile avoided the pattern of 32 other governments, Result: Chile avoided the pattern of 32 other governments, where forecasts in booms are biased toward over-optimism,where forecasts in booms are biased toward over-optimism,

which is why Chile ran surpluses in the 2003-07 boomwhich is why Chile ran surpluses in the 2003-07 boomwhile the U.S. & Europe failed to do so.while the U.S. & Europe failed to do so.

Appendix 4: US deficit woesAppendix 4: US deficit woes

The US has mismanaged its finances The US has mismanaged its finances as badly as Europe.as badly as Europe. The US doesn’t have the excuse of 17 legislatures,The US doesn’t have the excuse of 17 legislatures, just two deadlocked political parties.just two deadlocked political parties.

It is a long-term problem:It is a long-term problem: i) Future deficits in “entitlement spending”i) Future deficits in “entitlement spending”

social security & Medicare.social security & Medicare.

ii)ii) Current budget deficits since 1981 Current budget deficits since 1981 Steps in 1990s to restore surplus worked,Steps in 1990s to restore surplus worked, but were reversed in 2001.but were reversed in 2001.

The US national debt as a share of GDPThe US national debt as a share of GDPSource: CBO, MarchSource: CBO, March

One political obstacle, above all othersOne political obstacle, above all others

One of the two political parties is dominated by a One of the two political parties is dominated by a minority who say fiscal balance is urgent, yet also say it minority who say fiscal balance is urgent, yet also say it can be done entirely by cutting domestic spending:can be done entirely by cutting domestic spending: They want to cut taxes & raise military spending They want to cut taxes & raise military spending

at the same time as eliminating the deficit,at the same time as eliminating the deficit, which is mathematically impossible.which is mathematically impossible.

Prevents any sort of deal like 1990Prevents any sort of deal like 1990 which slowed spending growth which slowed spending growth

& raised taxes during the 1990s& raised taxes during the 1990s..

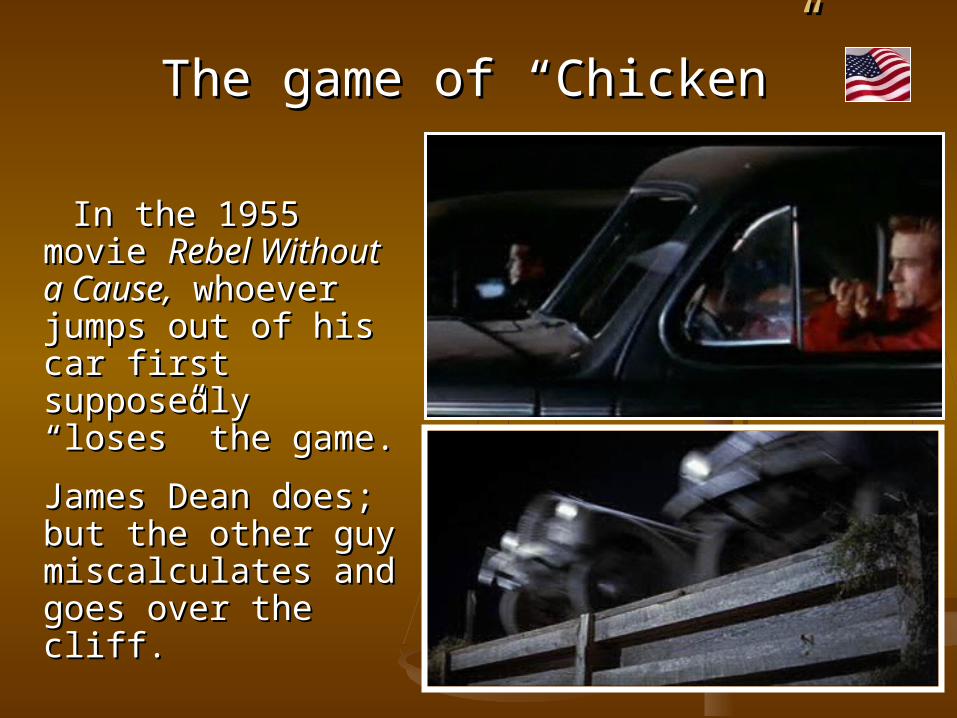

The game of “ChickenThe game of “Chicken””

In the 1955 movie In the 1955 movie Rebel Rebel Without a Cause,Without a Cause, whoever jumps out of whoever jumps out of his car first supposedly his car first supposedly “loses” the game.“loses” the game.

James Dean does; James Dean does; but the other guy but the other guy miscalculates and goes miscalculates and goes over the cliff.over the cliff.

The debt-ceiling game of “chicken”The debt-ceiling game of “chicken”

In the summer of 2011, “fiscal conservatives” recklessly In the summer of 2011, “fiscal conservatives” recklessly threatened government default threatened government default if their demands were not met.if their demands were not met. The resulting political dysfunction led S&P The resulting political dysfunction led S&P

to downgrade US bonds from AAA to AAto downgrade US bonds from AAA to AA ..

A last-minute solution postponed A last-minute solution postponed the deadline to the end of 2012:the deadline to the end of 2012: If no action is taken then, (i) all tax cuts expire, If no action is taken then, (i) all tax cuts expire,

(ii) all discretionary spending is cut drastically, & (ii) all discretionary spending is cut drastically, & (iii) the debt ceiling law is probably violated anyway.(iii) the debt ceiling law is probably violated anyway.

I.e., a return of the stand-off:I.e., a return of the stand-off: => Danger of recession => Danger of recession andand default ! default !