speech: october 19: a partial bibliography ... - sec.gov · october 19: a partial bibliography ......

TRANSCRIPT

USSecurities and Exchange Commission lAJw~WashingtonD C 20549 (202) 272-2650 ~~U~

October 19A Partial Bibliography

We are fast approaching the first anniversary of the stock markets 508 point decline and the journalistic jungledrums are signalling a festschrift of epic proportions In order to respond in a systematic manner to several inquiriesmy staff and I have prepared a partial bibliography of materials related to the events of last October 19 and the subsequent policy response

The bibliography is not exhaustive and in particular omits the hundreds of newspaper and magazine articles discussing the events of October 19 That literature is simply too vast easily to be culled and listed There are also likely to be substantial omissions from the bibliographyof academic materials because this literature is growing at a rapid pace

Enclosed with this bibliography is a copy of Professor (and former Commissioner) Roberta Karmels article The Rashomon Effect in the After-The-Crash studies 21 J Sec amp Commod Reg 101 (June 22 1988) While I do not agree with all of Professor Karmels assessments her article is perhaps the most balanced review of the many market studies that have appeared to date For those of you who are not Japanese movie bUffs Rashomon is Kurosawas epic film in which four witnesses provide four widely divergent descriptions of the same event In light of the many inconsistencies among the market studies Professor Karmels reference to Rashomon is both literate and apt

Further lest you think I am being too objective in this endeavor I also enclose copies of three pieces I have written analyzing the events of October 19

Joseph A Grundfest Commissioner

Enclosures

This reference appears originally to be attributable to E Blumenthal Rashomon Returns Probing Reality Anew NY Times Mar 20 1988 Sec 2 at 5 col 1 Those of you who are Japanese movie aficionados may wish to contemplate whether the conflicting analyses might not better support a reference to Zatoichi the blind samurai

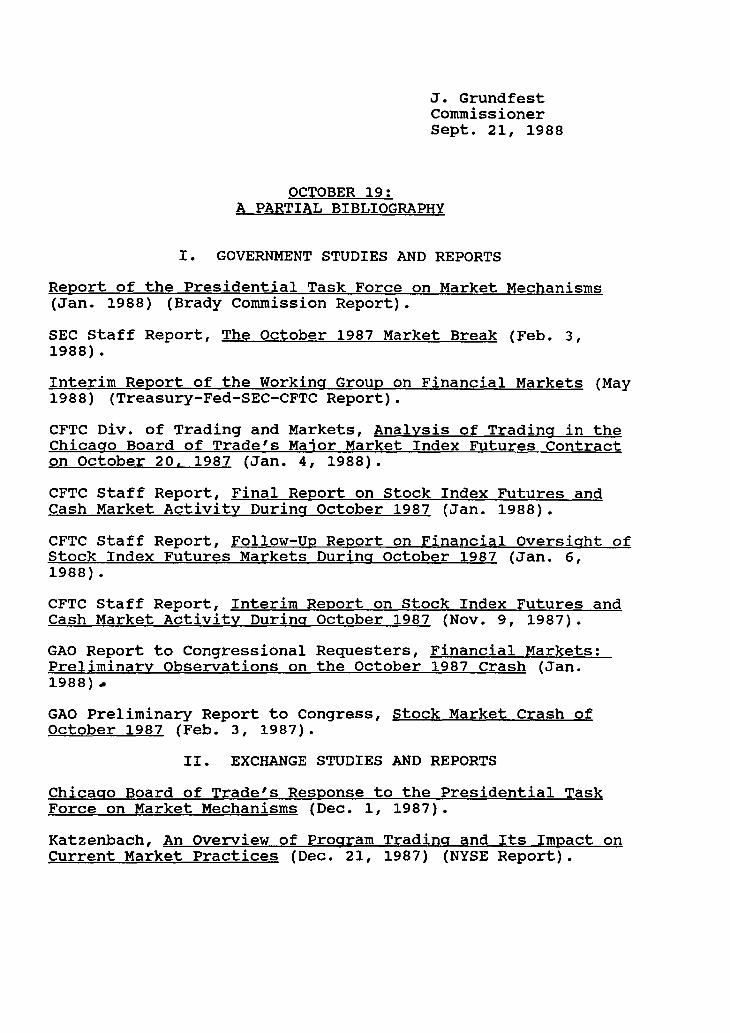

J GrundfestCommissionerSept 21 1988

OCTOBER 19A PARTIAL BIBLIOGRAPHY

I GOVERNMENT STUDIES AND REPORTSReport of the Presidential Task Force on Market Mechanisms(Jan 1988) (Brady Commission Report)SEC Staff Report The October 1987 Market Break (Feb 31988)

Interim Report of the Working Group on Financial Markets (May1988) (Treasury-Fed-SEC-CFTC Report)CFTC Div of Trading and Markets Analysis of Trading in thechicago Board of Trades Major Market Index Futures Contracton October 20 1987 (Jan 4 1988)

CFTC Staff Report Final Report on Stock Index Futures andCash Market Activity During October 1987 (Jan 1988)

CFTC Staff Report Follow-Up Report on Financial Oversight ofStock Index Futures Markets During October 1987 (Jan 61988)

CFTC Staff Report Interim Report on Stock Index Futures andCash Market Activity During October 1987 (Nov 9 1987)

GAO Report to Congressional Requesters Financial MarketsPreliminary Observations on the October 1987 Crash (Jan1988)

GAO Preliminary Report to Congress Stock Market Crash ofOctober 1987 (Feb 3 1987)

II EXCHANGE STUDIES AND REPORTSChicago Board of Trades Response to the Presidential TaskForce on Market Mechanisms (Dec 1 1987)

Katzenbach An Overview of Program Trading and Its Impact onCurrent Market Practices (Dec 21 1987) (NYSE Report)

bull

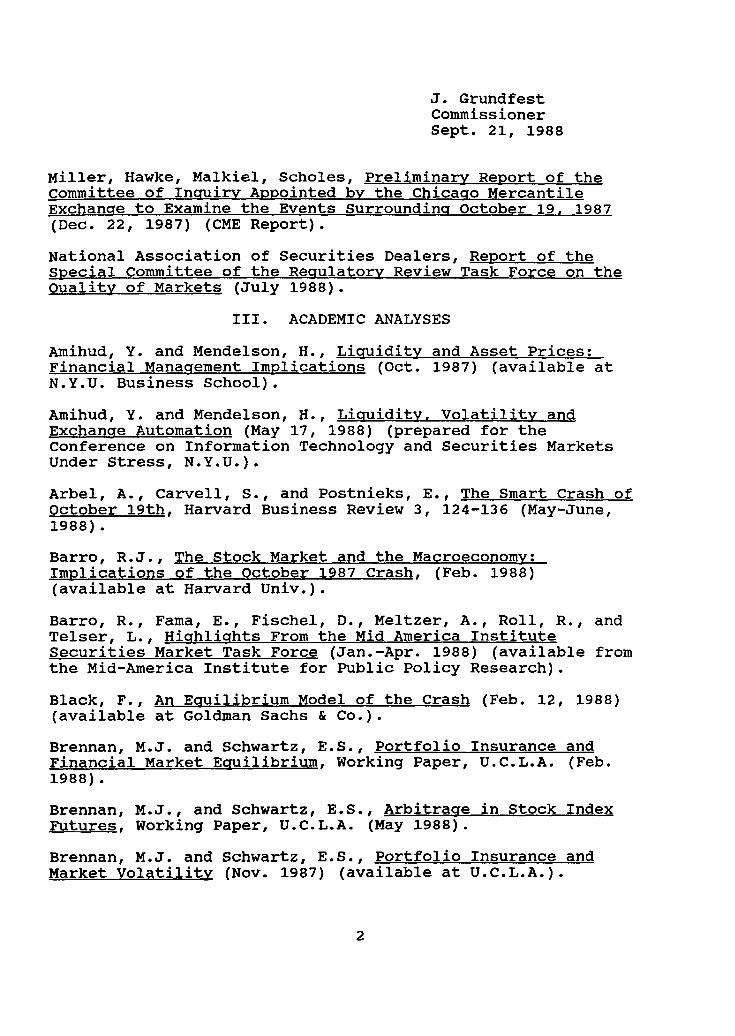

J Grundfest Commissioner Sept 21 1988

Miller Hawke Malkiel Scholes Preliminary Report of the committee of Inquiry Appointed by the Chicago Mercantile Exchange to Examine the Events Surrounding October 19 1987 (Dec 22 1987) (CME Report)

National Association of Securities Dealers Report of the Special committee of the Regulatory Review Task Force on the Quality of Markets (July 1988)

III ACADEMIC ANALYSES

AmihUd Y and Mendelson H Liquidity and Asset Prices Financial Management Implications (Oct 1987) (available at NYU Business School)

Amihud Y and Mendelson H Liquidity Volatility and Exchange Automation (May 17 1988) (prepared for the Conference on Information Technology and Securities Markets Under Stress NYU)

Arbel A Carvell S and Postnieks E The Smart Crash of October 19th Harvard Business Review 3 124-136 (May-June1988)

Barro RJ The Stock Market and the MacroeconomyImplications of the October 1987 Crash (Feb 1988) (available at Harvard Univ)

Barro R Fama E Fischel D Meltzer A Roll R and Telser L Highlights From the Mid America Institute Securities Market Task Force (Jan-Apr 1988) (available from the Mid-America Institute for Public Policy Research)

Black F An Equilibrium Model of the Crash (Feb 12 1988) (available at Goldman Sachs amp Co)

Brennan MJ and Schwartz ES Portfolio Insurance and Financial Market Equilibrium Working Paper UrCLA (Feb1988)

Brennan MJ and Schwartz ES Arbitrage in Stock Index Futures Working Paper UCLA (May 1988)

Brennan MJ and Schwartz ES Portfolio Insurance and Market Volatility (Nov 1987) (available at UCLA)

2

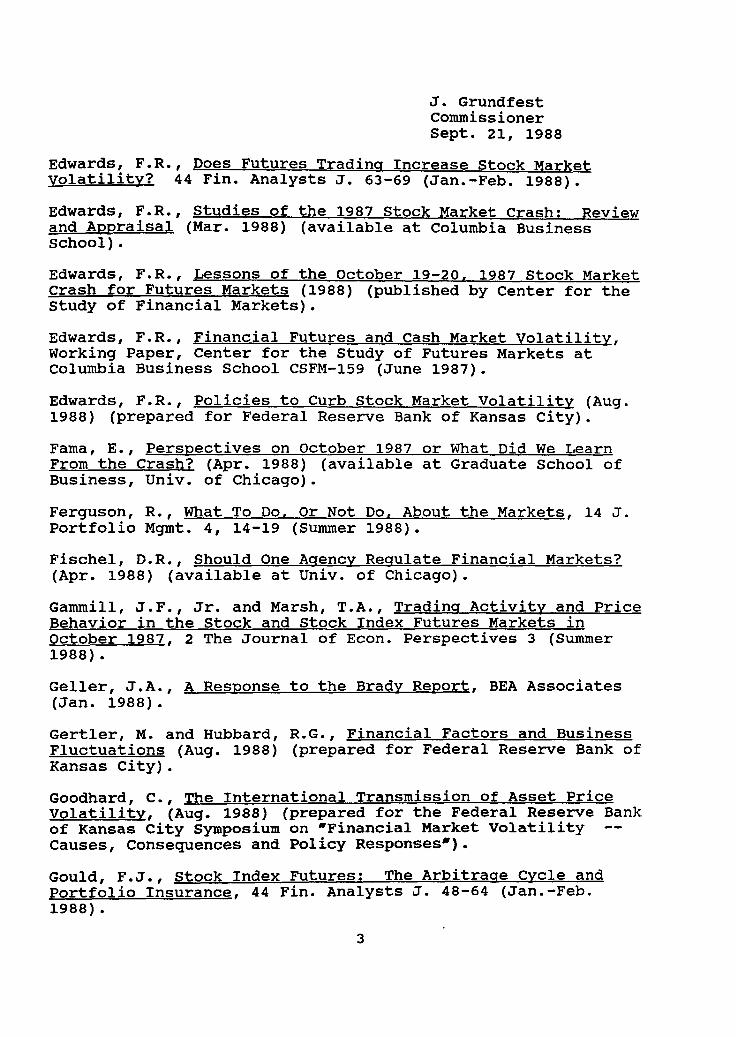

J Grundfest Commissioner Sept 21 1988

Edwards FR Does Futures Trading Increase Stock Market volatility 44 Fin Analysts J 63-69 (Jan-Feb 1988)

Edwards FR Studies of the 1987 Stock Market Crash Review and Appraisal (Mar 1988) (available at Columbia Business School)

Edwards FR Lessons of the October 19-20 1987 Stock Market Crash for Futures Markets (1988) (published by Center for the Study of Financial Markets)

Edwards FR Financial Futures and Cash Market Volatilityworking Paper Center for the Study of Futures Markets at columbia Business School CSFM-159 (June 1987)

Edwards FR Policies to Curb stock Market Volatility (Aug1988) (prepared for Federal Reserve Bank of Kansas city)

Fama E Perspectives on October 1987 or What Did We Learn From the Crash (Apr 1988) (available at Graduate School of Business Univ of Chicago)

Ferguson R What To Do Or Not Do About the Markets 14 J Portfolio Mgmt 4 14-19 (Summer 1988)

Fischel DR Should One Agency Regulate Financial Markets (Apr 1988) (available at Univ of Chicago)

Gammill JF Jr and Marsh TA Trading Activity and Price Behavior in the Stock and Stock Index Futures Markets in October 1987 2 The Journal of Econ Perspectives 3 (Summer1988)

Geller JA A Response to the Brady Report BEA Associates (Jan 1988)

Gertler M and HUbbard RG Financial Factors and Business Fluctuations (Aug 1988) (prepared for Federal Reserve Bank of Kansas City)

Goodhard C The International Transmission of Asset Price Volatility (Aug 1988) (prepared for the Federal Reserve Bank of Kansas City Symposium on -Financial Market VolatilityCauses Consequences and Policy Responses)

Gould FJ Stock Index Futures The Arbitrage Cycle and Portfolio Insurance 44 Fin Analysts J 48-64 (Jan-Feb1988)

3

J Grundfest Commissioner Sept 21 1988

Greenwald B and Stein J The Task Force Report TheReasoning Behind the Recommendations 2 Journal of Econperspectives 3 (Summer 1988)

Grossman SJ Program Trading and Stock and Futures PriceVolatility 8 J Futures Mkts 413-419 (Aug 1988)

Grossman SJ An Analysis of the Implications for Stock andFutures Price Volatility of Program Trading and DynamicHedging Strategies 61 J Bus 275 (1988)

Grossman SJ Program Trading and Market Volatility AReport on Interday Relationships 44 Fin Analysts J 18(July-Aug 1988)

Grossman SJ and Miller MH Liquidity and MarketStructure 43 J Fin (forthcoming 1988)

Hale DO Is the Stock Market Crash of 1987 Comparable to1929 or 1893 or Will There be a New Jazz Age Before the NextDepression Kemper Financial Services (Nov 1987)

Hale DO Is the US Stock Market Overvalued or Should USShares be Valued on the Basis of Japanese Interest RatesKemper Financial Services (1987)

Haraf WS Lessons of the Stock Market Crash What We HaveLearned About the Securities Markets and Their Regulation TheAEI Economist (May 1988)

Harris L Nonsynchronous Trading and the SampP 500 Stock-Futures Basis in October 1987 (Dec 22 1987) (availablethrough the School of Business Administration Univ ofSouthern California)

Harris L The October 1987 SampP stock-Futures BasisWorking Paper Los Angeles Univ of Southern California (May1988)

Harris L SampP 500 Futures and Cash Stock Price VolatilityWorking Paper Los Angeles Univ of Southern California(Oct 1987)

Heston Je New Options strategies Rising out of PortfolioInsurance Ashes Futures 36-39 (June 1988)

4

J Grundfest Commissioner sept 21 1988

Hill JM Portfolio Insurance Past Present and FutureKidder Peabody amp Co (Mar 1988)

Hill JM and Jones FJ Equity Trading Program Trading Portfolio Insurance Computer Trading and All ThatFinancial Analysts Journal 29-38 (July-Aug 1988)

Karmel RS The Rashomon Effect in the After-The-Crash studies 21 J Sec amp Commodities Reg 101-108 (June 22 1988)

Kawaller IG Koch PD and Koch TW Price Volatilityand Volume Effects on Feedback Between SampP 500 Futures Prices and the SampP 500 Index Working Paper New York ChicagoMercantile Exchange (Feb 1988)

Kleidon AW Arbitrage Nontrading and Stale Prices October 1987 (Apr 1988) (Graduate School of BusinessStanford Univ)

Kyle AS and Marsh TA Computers and the Crash I Is Technology the Problem or the Solution Institutional Investor 6-7 (June 1988)

Klye AS and Marsh TA Computers and the Crash II How the Systems Performed Institutional Investor 8-9 (June 1988)

Leland H On the Stock Market Crash and Portfolio Insurance Working Paper Univ of California at Berkeley(Dec 1987)

Leland H and RUbinstein M Comments on the Market Crash six Months After 2 Journal of Economic Perspectives 3 (Summer 1988)

Mackay RJ ed After the Crash (American Enterprise Institute 1988)

Mackinlay CA and Ramaswamy K Index-Futures Arbitrage and the Behavior of Stock Index Futures Prices Working PaperUniv of Pennsylvania (Apr 1988)

Malkiel BG The Brady Commission Report A Critique 14 J Portfolio Mgmt 9 (Summer 1988)

Marshall JM Draft Critiques of the Brady Report (Apr 14 1988) (School of Business Administration Univ of San Diego)

5

J Grundfest Commissioner Sept 21 1988

Meiselman 01 Double Deficits Tight Money and the Stock Market Crash (Nov 18 1987) (comments delivered at the meeting of the Financial Products Advisory Committee of the Commodity Futures Trading Commission)

Merrick JJ Jr Fact and Fantasy About Stock Index Futures Program Trading Bus Rev 13-25 (Sept-oct 1987)

Merrick John J Jr Hedging with Mispriced Futures (forthcoming in Journal of Finanical and QuantitativeAnalysis)

Miller MH Financial Innovations and Market VolatilityWorking Paper University of Chicago (Mar 1988)

Peake JW Mendelson M and Williams RT Jr Black Monday Market Structure and Market Making (Jan 29 1988) (presented at Electronic Fin Mkts Conference at the Salomon Brothers Center for the Study of Fin Mkts New York univ)

Roll R The International Crash of October 1987 (Apr 5 1988) (available at Anderson Graduate School of ManagementUCLA)

RUbinstein M Portfolio Insurance and the Market Crash Fin Analysts J 38-47 (Jan-Feb 1988)

Rutz RD Intermarket Cross-Margining The Myth and the Reality (Mar 23 1988) (available at the Board of Trade Clearing Corp in Chicago)

SChwert WG Why Does Stock Market Volatility Change Over Time Working Paper University of Rochester (Oct 1987)

Shiller RJ Portfolio Insurance and Other Investor Fashions as Factors in the 1987 Stock Market Crash (Feb 25 1988) (available at Yale Univ)

Shiller RJ Causes of Changing Financial Market VolatilityYale University (1988) (prepared for Federal Reserve Bank of Kansas City)

Shiller RJ Investor Behavior in the October 1987 Stock Market Crash Survey Evidence (Nov 1987) (available at Yale Univ)

6

J Grundfest Commissioner sept 21 1988

stoll HR and Whaley RE Volatility and Futures MessageVersus Messenger J Portfolio Mgmt 20-22 (Winter 1988)

Stoll HR and Whaley RE Stock Index Futures and options Economic Impact and Policy Issues (Jan 1988) (available at Owen Graduate School of Management Vanderbilt Univ)

stoll HR and Whaley RE Program Trading and the MondayMassacre (Nov 4 1987) (available at Vanderbilt Univ)

Telser LG An Exorcism of Demons (Feb 1988) (available at Univ of chicago)

Tosini Paula A Stock Index Futures and stock Market Activity in October 1987 Financial Analysts Journal 28-37 (Jan-Feb 1988)

VI LEGISLATIVE PROPOSALS

HR 3597 Leach 11387 Agriculture Banking Finance amp Urban Affairs Energy and Commerce To require the Fed to establish minimum margin requirements on certain types of instruments

HR 3594 Jones 11287 Agriculture To amend the commodity Exchange Act to authorize a joint study of market volatility

HR 4997 Markey 6788 Energy and Commerce To transfer regulatory authority over stock index futures and options on stock index futures to the SEC to authorize the Fed to establish margin requirements with respect to such instruments to give the SEC emergency authority over the futures markets and to require reporting by large traders

HR 5265 English 9888 Agriculture To amend the Commodity Exchange Act by transferring to the CFTC authorityover options trading

S 1847 Heinz 11487 Banking Housing amp Urban Affairs To amend the Federal Reserve Act to authorize the Fed to set margin requirements for certain financial instruments

7

J Grundfest Commissioner Sept 21 1988

S 2256 Proxmire 33188 Banking Housing amp Urban Affairs To provide for intermarket coordination between the stock market and the futures markets and the establishment of the Intermarket Coordination Committee consisting of the Chairman of the Fed the SEC and the CFTC

V SEC LEGISLATIVE PROPOSALS

Transmitted to the Hill June 24 1988 Regarding (a)emergency authority for the Commission (b) large trader reporting (c) reporting of information concerning financial or operational risks within holding company systems (d)enhanced authority for the Commission and the CommodityFutures Trading Commission to facilitate development of an integrated clearance and settlement system

Transmitted to the Hill July 6 1988 Regardingcomprehensive regulation of margins for securities and related futures equity index products

Transmitted to the Hill July 7 1988 Regarding amendingfederal securities laws and the Commodity Exchange Act to provide the Commission with regUlatory authority over equityrelated instruments

8

THE REVIEW OF

1OlllBrrraquoJ 4 ~SiCURITIES 8r COMMODITIES_------ R~~Y~T~9N bull

AND REGULATIONS AFFECTING THE SECURiTIESAND FUTURES INDUSTRIES

PUBLISHED BY STANDARD amp POORS CORPORATION

Vol 21 No 12 June 22 1988

THE RASHOMON EFFECT IN THEAFTER-THE-CRASH STUDIES

In Their Reports Governmental and Self-Regulatory Bodies Blamed EachOther for the Chaos in the Markets and Reached Incompatible ConclusionsThe Author Analyzes These Reports and Gives Her Recommendations

Roberta S Kannel

The 508-polnt decline in the Dow Jones Industrial Average(DJIA) on Black Monday October 19 1987 was histori-cally unprecedented Not only was this one day 226 dropin stock prices almost double the 12 8 dechne in the GreatCrash of 1929 but it climaxed an eight-week decline of983 68 points 1 Furthermore on Terrible Tuesday October20 1987 the stock market nearly closed because of theinability of specialists and other market-makers to continuetrading 2 Although the market break may have been due to adramatic change in investor perceptions of economic devel-opments the precipitous nature of the decline raised seriousquestions about market structure in particular index-relatedtradmg

The immediate political reaction to the market crash was aplethora of governmental and seU-regulatory organization(SHO) studies The first study to be published was onecommissioned by the New York Stock Exchange (NYSE)before the crash3 The next day a committee of inquiryappointed by the Chicago Mercantile Ezchanqe (CME)pubhshed a report 4 Shortly thereafter the report of a blue-ribbon presidenbal committee headed by Nicholas Bradywas publisheds The two federal agencies directly con-cerned with requlatinQ the trading markets the Securitiesand Exchange Commission (SEC) and the CommodityFutures Trading Commission (CFTC) issued lIaffreports The U S General Accounting Office (GAO) also

ROBERTA S KARMEL IS a poftlSeN of Law at Booklyll Ltzgt Scllool and aparM of Krllt Drylaquo d WatII litYeNk Cy SIItis a pwbilc dITtcteNof tiltNrlaquo York Stock ExchangrllIt and afomrcommssloM oftltr Secunues andExchangr CommlSsloII

rushed to issue a report7 All of these and other reports thenled to conqreuional inquiries and testimony whichundoubtedly will generate further ltudies Whether mean-ingful action to prevent another crash will be taken by anadministration committed to deregulation or a Conqrellfacing an election is problematic

I Welb Farlo Investment Advi$ors AlIQtomy of a INcM Tilt Rolt ofIndrx-Rtlattd Tadlllg ill tiltMaktts RttOTdFall Nov 9 1987 at I

2 J Siewant D Henzberl Temble TwtsdaYHow tiltStock MQfktt AlmostDulllttgtattd a Day AftO tM Crasll WaU Street JOIImalNov 20 1987 atIcol I

3 N deB Kalzenbach All OvtTYitWof Pogram TradIng And Its Impact Oil

ct1It MoktI PDCtiUS (Dec 211987) [Kalzenbach Report)4 MH Miller JD Hawke B Malkieland M ScbolesPnlNUYR~ponof

tM Commltttt of Inqwiry AppolIItd by tM CME to ElQmine EwlltsSWrrowndlll Oct~ 19 1987 (Dec 22 1987) [CME Report)

s Repon of tM PtsidtlItial Task FOfU 011 Maktt 1rattius (Jan 8 1988)CCH Special Repon No 1267 (Jan 12 1988) [Brady Report)

6 Report by tbe DlYIsionoC Market Rqulallon oC the US Secvrilles andElIcbanae Commission Tilt Oct~ 1987 MQfut Bnak (Feb 1988) [SECReport) Division oC Economic Analysis and DivisionoC TradlDl and MarketsFinal Report on Stock Indell FutllteS and Casb Market AetJYllYdurinlOctober 1987 to the US CommodJly Fulures Tradlnl CommllllOll (Jan1988) ICFTC Final Report) Division of Tradin and Markets oC theCommodity Futures Tradinl Commissioa FillQltCalFollow-Up Rtpon 0fI

FiflQ1ltiolOvtslIt of Stock Indu FwtlUtsMQfktts dII Octobtr 1987(Jan 6 1988) [CFTC FoIlowUp Report) Divisioa of EconoIlUc AnalystS andthe DivisionoCTradlnland Marketslllltrim IUpon Oft Stock llIdu Fwtwnsand Casll MQfut Activity dwrill Octobtr 1987 to tM Us CommodityFwtlUtsTad CorruruSSIOll(Nov 9 1987) [CFTC Interim Report)

7 US General Accountin Office RtpOIt10 COIIgrtsSIOIfQllUqWtsttTsFIIQClal Maktts htlImlNUY ObsrTYatlOllS011 tM Ott~ 1987 Crasll (Jan1988) [GAO Report]

IN THIS ISSUEThe Hashomon Effect in the After-the-Crash Studies

p n1

bull

The purpose of this article 1Sto review the most importantrecommendahons in these reports and to assess the pros-pects for requlatory reform of the securities and hnancralfutures markets Generally the after-the-crash studies con-tam two contradictory conclusions first that since the stockand futures markets are in effect a sinqle market they shouldbe better 1nteqrated and made more efficient and secondthat since the market in derivahve products has underminedthe pnmary market these markets should be either unlinkedor chanqed to prevent a further erosion of the capitalformation function of the stock market

All observers aqree that reform is necessary and con-tinued uncoordinated regulation by competing regulators isa recipe for greater catastrophe However there is no agree-ment on what new regulatory mechanisms should be devel-oped or what qovernmental authority should impose solu-tions on the marketplace The great political and economicinterests at stake seem stronger than the public interestespecially since the fear of tampering with the market is asstrong as the fear of doing nothing Yet the market crisis ofOctober 1987 was at least in part a result of defects in thedesign of ftnancial products by government regulators and itis unlikely that the market can correct these deficiencieswithout government intervention

In Akira Kurosawas classic Japanese film Rashomonthere are four wildly incompatible accounts of the same rapeand murder (or seduction and suicide) The word Rasho-mon has since come into the English language to connotethe slbjective nature of truth All of the after-the-crashstudies are biased This does not malte any of them wrongbut it does make them incompatible Whether the Rashomoneffect permeating these studies makes structural reform ofthe markets impossible probably depends on the futurebehavior of the markets themselves

FACTUAL ANALYSIS

There is little dispute concerning the bare facts of themarket decline What is disputed is the cause of the marketsvolatility and the proposals for changing market structureDuring October 1987 the securities and financial futuresmarkets experienced an extraordinary surge of volume andprice volatility On August 25 1987 the DnA index of 30NYSE stocks reached an intra-day high of 274665 OnOctober 19 1987 the DJIA declined 508 32 points and byits low point on October 20 it had declined to 170872 orover 1000 points (37) from its August 25 high

The mdex futures markets also expenenced largedechnes Pnces for the SampP 500 December futures contract(SPZ) on the CME underwent more eztreme fluctuationsthan the underlying stocks Durinq October 1987 the SPZtraded allevels as low as 18100 down 44 equivalent tothe DJIAdropping to 144353 Further althouqh the theoret-ical value of index futures normally is at a shght premium tothe cash price from October 19 to 28 the price relationshipbetween futures and stocks was inverted wilh the futurestradIng at large d1scounts to stocksIO

On October 20 1987 there was continued volatility butprice movements resembled a roller coaster As a resultaround midday the securities and futures markets reached apoint when heavy sell pressure overwhelmed marketmaltingcapacity in both the securities and futures markets At aboutnoon trading in a large number of NYSE securities washalted and most derivative markets ceased trading 11 TheChicago Board Options Exchange Inc (CBOE) sus-pended trading at 1145 am based on its rule that tradingon the NYSE must be open in at least 80 of the stockswhich constitute the options index it trades At 1215 pmthe CME announced a trading suspension in reaction toindividual stock closings on the NYSEand the rumor of theimminent closing of the NYSEitself12 Another reason stocksceased to trade was the fear of a widespread credit break-down due to (unfounded) rumors of financial failures bySOmeclearinghouses and major market participants

Just after noon on October 20 however the marketabruptly turned around From 1220 to 100 the DJIA gainedaround 118 points and maintained a 10227 point recoveryfor the day During an interval of about 20 minutes beqin-Ding around 1230 pm the Major Market Index Man(MMI) futures contract traded on the Chicago Board ofTrade (CBT) staged an extraordinary 9O-pointrally risingfrom a discount of about 60 points to a 12-point premium II

The MMIis based on 20 blue-chip stocks 16 of which are inthe DJIAI The CBT had permitted the MMI to continuetradinq because 17 of the 20 stocks in the MMI hadremained open for trading and it had been the only stock

8 E Blumenthal RasliolflOll Relunu hobil RetJIily AMW N Y TilllClMar 20 988 12 at S col I-

9 SEC Report at 2-1-0 (d It 2-22 CFTC Intcnm Report at 231t SEC Report at 22012 CFTC rtnal Report at 10S-06 Brady Report at 4013 SEC Report at 2-~2-2t14 DivisD 01Tndma ud Markets Commodity FutufCI Tradin8 COIMllSSIOD

AlIII1ysbof Major Marlcelilldex FulUUS Co1tttKIOIIOclobe 20 1987 (Jan4 988) at t

Page 102

COPTlghle 1988 by Slalldard amp Poors Cop Reproductio i hole 0 parI unetly forbidde holll wnue pemiSSIOItof 1Mpublish~rs All riglisreserved Published IU a monm (excepl mOltIMy i July alld AuPSI) b Slalldad amp Poors Corp SubscnpllOlt ratlaquo SJ78y SubscrlpllOll OJfiu 25Broodway j~ York tV Y ()()()4 pounddllona OJfice 26 Broaday Nrw York N Y 10004

June 22 1988

bull

Index futures contract tradmq from approximately 1235p rn to 1 05 p m 15 Because of Ihe unusual nature of the MMIpnce move on Terrible Tuesday the CrTC conducted anlDveshgahon into possible manrpulativa acbvity and foundno reasonable indication that any manipulation occurred 16

The volume on October 19 was as extraordinary as thedecline in prices a record of 604 rmllion shares worth justunder $21 billion I The volume on October 20 was an evenhigher 6137 million shares During the weeks of October19 and 28 NYSE share volume reached peak levels at twiceprevious records and volume each day during the periodremained at previous record levels I

CAUSES OF THE CRASH

The vanous studies agree that there was no single causefor the crash and economic factors were significant TheBrady Comr-iission pointed out that the decline was trig-gered by an unexpectedly high merchandise trade deficitwhich pushed interest rates to new high levels and pro-posed tax legislation which led to the collapse of stocks of anumber of takeover candidates20 The CME report pointedout that during 1987 economic fundamentals wealtenedacross the world measured In terms of GNP growth and asharp rise in interest rates but world equity prices continuedto rise to historic hIgh levels In most countries21 The Katzen-bach Report observed that after a consensus formed thatAugust 1987 was a market peak investor sentiment waserpecting a correction and before Black M~nday price-earnings ratios were hovering at unusually high levelsaveraging 23 times earnings22

The SEC report clessihed the fundamental factors thatmarket partlclpanls interviewed by the staff thought hadtnggered changes in investor perceptions These were (1)nsing interest rates (2) US trade and budget deficits (3)overvaluation of stock prices during 1986 and the first eightmonths of 1987 and (4) declines in the value of the USdollar23 A tax bill reported out of the House Ways andMeans Committee that would have severely taxed deduc-tions for interest on debt used to finance takeover activitywas also cited as a possible cause of the crash In addition toinvestor concerns about trade and budget deficits deprecia-tion of the dollar and inflation the CFTC Interim Reportcited increased tensions m the Persian Gulf u

As might be expected from report as politically motivatedand sensitive as the after-the-crash studies none discuss themacroeconomic reasons for the crash or attempt to assignany responsibility to Congress or the administration for thenations debtor condition in both the public and privatesectors And policy makers have done little to fix the

June 22 1988

underlying economic causes of the market crash The policychanges necessary to correct the global budget and tradeimbalances have not been made25 leveraging and specula-tion have not been curbed in the secunties or futuresmarkets 26 Instead government officials and the erchangeshave asked whether trading in derivative products causedthe crash Their answers have been wildly incompatible

The Brady Report concluded that stocks and derivativeproducts-stock inder futures and stock options-constituteone market but the failure of these market segments toperform as one market contributed to the violence of themarket break in October 1987 which brought the financialsystem to a near breakdown27 This study was thereforecritical of the NYSEs prohibition on the use by broker-dealers of the automated DOT system to execute indexarbitrage orders for their own accounts because this prohi-bition disconnected the futures and stock markets TheCITC in its Interim Report similarly blamed the NYSEsclosing of the DOT system to arbitrage programs for pricedisparities between the futures and cash markets2I andfound that futures-related tradinq was not a major part ofNYSE volume during the week of October 19 Indeed theCITC (rather contradictorily) suggested that absent thehedging facility provided by the futures market the stockmarket decline might have been greater

The CITC Final Report was firm in its conclusion thatIt]he wave of selling thai engulfed the global securitiesmarkets on October 19 was not initiated by tradinq in indexproducts nor did it principally emanate from such trad-inga On the contrary the CITC blamed the sellinq ofnearly 175 million shares of stock by one mutual fundduring the first half-hour of trading on October 19 for settinqoff the selling wave on that day and also singled out portfolioinsurance sell programs Morover the CITC asserted that anexamination of the trading data does not provide empirical15 Id at 3 A1tboulh thii tradlnl wu in ChicalO the ume IS stated in eastern

time16 Id at 1417 Brady Report at 3618 SEC Rcpon at 22019 Id at 101 Befon October 19 the IOC1lriUCI indllStry wu skepllcal of the

possibility of a 450-milhonshare day before 1990 TCitimony of John JPhelan Jr bull ChaIrman NYSE before the Senate Comm on BanlanlHousma and UrbaJI Alrairs Feb S 1918 at 3

20 Brady Report at Y

21 CME Report at 622 Katrenbach Rcport at 1923 SEC Rcport at 3924 CITC Interim Report at 42S A Sina~ AlIOth Mrdo MoNlay Til QlusllOff Is Nor If bwr W1I

NY TirnCIApr 3191813 at 3 col I26 Sec B E Garcia Mwell 01 rll Moluts FITst QsuJ Glir Co_ From

StoclcsoITo~ Tarprs Wan St J bullApr 1 1988aI2ScoI 227 Brady Report at 5928 CITC Intcnm Report at 6329 CITe Final Report at 81

Page 103

-~-

support for the theory that hedging m the futures market and index arbitraqe achvities mteracted to cause a technical downward pnce spiral of stock pnces

The SEC on the other hand while concedmg that futures trading and strateg1es involvmq the use of futures were Dot the sale cause of the market break found that the existence of futures on stock indexes and the use of the various strateqies involving proqram tradinq (ie index arbitrage index substitution and portfolio insurance) were a significant factor in accelerating and exacerbatinq the declines3QThis conclusion was based on the SECs obser-vation of three dramatic trends resulting from tradinq in derivative index products first stock index futures have supplemented and often replaced the stock market as the primary price discovery mechanism for stock price levels second the availability of futures strateqies has qreatly increased the velocity and concentration of stock tradinq and third these strategies have increased the risks incurred by stock specialists and strained their ability to provide liquidity to the stock market

Not surprisingly the commodity futures and stock exchanges also differed in their views concerning the role of derivative products in the market break The CME Commit-tee of Inquiry found no evidence that futures margins either caused the 1987 increase in equity prices or exacerbated the crash31 Further index arbitrage did not appear to have played a major role Instead of leadinq the stock market decline the futures market was a net absorber of sellinq pressure Further althouqh portfolio insurance was a con-tributor to sellinq users learned that continuous and smooth ent prices are not obtainable when a collective mass move to an ent occurs This flaw havinq been exposed in the view of the Committee excessive use of this strategy will no longer be a problem

The Katzenbach Report was more circumspect but dis-cussed the importance of the psychological effect of futures trading strateqies It noted that no major or unanticipated financial or political crisis occurred on or immediately before Black Monday

The ablNlnce of such a emu malees explanation more diffi-cult limply because 11suggests a market fragility beyond our anticipation To the enent the futures market with ita huge daily volumel and claims to hquidity encouraqed institu tional ilIveltorl to rely upon it as a quick elCape from too much equity ilIvestment it may have contributed to the quick fall of pricessa

One might have expected the GAO to be objective in determining the claims of Chicaqo and New Yorkto the truth about the market decline However the GAO declined to

Page 104

take any position on the role of futures in the market break Rather the GAO stated

The preclle eHect index arbitrage portfolio insurance and other LDied Iradulq tlal8Qlu had = tbe 508 pomt declme on Monday October 19 may be debaled IIdoel seem clear however that the relabonslup between futurel pncel and cash market pnces wlucb wal aHected at vanoul times on October 19 and on other daYI of the period by the tradiDq Itrateqiel and by market chlrupbo~ bad lOme effect on mveslorl perception of eventa II

THE ONE MARKET ONE REGULATOR HYPOTHESIS

The Brady Report posited the theory that from an ec0-

nomic viewpoint the markets for stocks stock index futures and stock options although traditionally viewed as separate markets are in fact one market 34 The problems of October 19 however could to a larqe extent be traced to the failure of these market segment to act as one

The SEC and CITC were more tentative in their views about how linked the futures and cash markets are perhaps because the observation that these are a sinqle market seems inevitably to lead to the conclusion that they need only one regulator in Washington Accordinq to the CITC the mar-ket are interchangeable but only up to a point

(WJhile lOme may consider the lIIock market as a market for iIlv8ltinq and the futures a market for hedqiDq or initiatiDq portfoho readjuslmenll major inlhtutional iIlvellloCland bro-kerdealers vie the cash and future marketl as interchanqeable for Ihort-term implementation of their port folio d8Cisio~ lubject to coDsiderabonl of relative transac-tion COIta market liquidity and market valueJI

The SEC has taken the position that the securities and derivative markets ar8 linked or unified but each market appropriately has its own distinctive products req-ulations procedures and systems of tradinq

A position on whether the markets are one or several hal important ramifications with reqard to recommendations on regulatory consolidation In the view of the Brady Commis-sion one market mandates one aqency for intermarket

30 SEC Report at 3- 31 CME Report at 55 32 Kauenbacb Report at 2 33 GAO Report at 49 34 Brady Report at 69 35 CFTC Final Repon at 138 36 Testimony or David S beler Chairman SEC before the Us Senate

Comm 011 Bankin Housin and Urban Alrain Securities and Exchane Commission RecommendatlOll5 RClardlDllbc October 1987 Market Break

Feb 3 988 at 5 (SEC RecommendatlOnsl

June 22 1988

Issues37 The Brady Commission discussed but did not endorsethe possibility of either making the SEC the central regulator for stocks stock index futures and options or of JOIntSEC-CITC responsibility through merger or other-WIseand It rejected the idea of a new regulatory body Finally the Brady Commission recommended the Federal ReserveBoard (FRB) as the most experienced indepen-dent and respected candidate to act as an intermarket agency However Alan Greenspan Chairman of the FRB Immediatelydeclined this honor stating that the FRBdid not havesufficient expertise to be effective and that it would be unfortunate to encourage the perception that a federal safety net extends to the securities markets or clearing corpora-tlons38 Mr Greenspan then said that coherence of federal oversightover equities could be achieved through merger of the relevant portions of the CITC with the SEC or a joint oversight authority comprised of the SEC the CFTC and perhaps the FRBor the Treasury

As might be expected the CITC defended the regulatory statusquo stating that the overall regulatory system worked effectively to prevent a broader crisis 39 Accordingly there was no need for any major structural change in those systems Although it gave the nod to interagency coordina-non the CFTC criticized the NYSE for lack of coordination on October 19 in the closing of trading in individual stocks and on October 20 in the possible closing of the entire market 40

The SEC divided on the question of regulatory consolida-tion By a split 3-2 vote the SEC recommended that it be given final regulatory authority for equity-related products with respect to critical intermarket decisions such as trading halts and antimanipulative and front-runninO rules41 In the SECs view the FRBhas insufficient expertise with respect to both the equity and the futures markets to assume such jurisdiction except as to determining marqin levels The SEC additionally recommended that its authority to review proposed indez futures be expanded to include review of both new and existing contracts and to permit consideration of the impact of these products on the oIdeIly operation of the stock market

The GAO did not tacltle this difhcult political issue Although ur91n9 better intermaIlret regulation the GAO said at this point we cannot recommend any single vehicle for achieving it 42 The GAO did howeveI wge some involvement by the FRBwhile declining to endorse or reject the Brady Commissions recommendabon that the FRB be the coordinator of mtermarket ISsues

June 22 1988

EFFICIENCY AND HARMONIZATION

There was one stand that was not too controversial for the GAO to take 11criticized the NYSE for not forecasting 6oo-share-volume days or having computer systems to han-dle such volume Another efficiency reform the GAO recom-mended was cooperative contingency planning 11likewise criticized the SEC for insufficient oversight of the NYSEs automated order-processing systems

The SEC did ezamine and analyze a variety of issues relating to systems efficiency of the NYSEand other market-placeso and recommended certain systems enhancements to expand the capacity of the NYSEto meet increased liquidity demands Other SEC recommendations aimed at increas-ing the efficiency and liqUidity of the securities markets included increased specialist capital and improved clear-ance and settlement procedures including same-day com-parisons The CFTC also focused on the improvement of reporting procedures by the continuous input of trade dataO and recommended various improvements in the relation-ships between banks and clearing firms In particular the CFTC cited the need for reforms to assure that variation margin transfers in volatile markets are not impeded

Inefficiencies leading to illiquidity in the over-the-counter (OTC) markets for which the National Associa-tion of Securities Dealers Inc (NASD) is the self-regula-tor were also examined by the Brady Commission and the SEC The Brady Commission noted that durinO the week of October 19 some OTC marketmakers formally withdrew hom making markets and others did not answer their phones- The SEC was more specific in its criticisms of trading in the National Association of Securities Dealers Automated Quotations (NASDAQ) system which is the third largest securities market in the world in terms of dollar volumeC7 The SEC concluded that the system simply

37 Brady Report al 59 38 Teslimony of Alan Greenspan Chairman Board of Governors of lbe Federal

Reserve System before lbe Senate Comm on Bankutamp HousiDampand Urban MalIS Feb 2 1988 al 22-23

39 CFTC Final Reportal 190 40 CFTC ChairmaD Wendy Gramm reiteraled tbese themes al the Annual

Futures Industry Associatioo Conference on Manb 9-12 1988 Sec Rq L Rep (BNA) Vol 20 at 434 (Mar 181988)

41 SEC Recommendations at 30 This spilt bas continued as lbe SEC bas formulaled leJislative recommendations SEC To Sk E_r~NY Power10

RlSlon FIIU Orlkrly MtuUIs Sec Rq L Rep (BNA) Vol 20 al 831 (JIIDC 3 1988)

42 GAO Report at 100 43 SEC Report Cb 7 44 SEC RCCOIIlDIendatioosal 8-9 45 CFTC Final Report al 195-96 46 Brady Report at 50 47 SEC Report aI9-1 nl

Page lOS

ceased to provide an effective pncing mechanism for many leading NASDAQ secunhes due to the inordinate number 01 locked and crossed markets coupled wIth the large num-ber of delayed last sale reports

The SEC also criticized the abandonment of the NASD small order execution system (SOES) Anhcipating this cnticism the NASD made its own recommendations for improved NASDAQ and SOES performance by proposing amendments to its regulations applicable to NASDAQ mar-ket makers The amendments would serve to ensure that Investors orders are executed in a timely manner in a falling market with high volume and that NASDAQ marketmakers fulfill their obligations to trade for their own accounts on a continuous basis even in extraordinary markets Without commenting on these proposals the SEC suggested some further reforms including increasing the size of public quotations by NASDAQ marketmakers from 100 to 1000

Failures in the options markets also came under scruhny The Brady Commission concluded that options market makers did not play an important role in stabilizing their own market and may have marginally added to the pressure in other marketsso The SEC was also critical of lack of continuity and pricing anomalies in the option markets on October 19 and 20 and nade a number of specific reform recommendations including changes in opening rotation procedures improvements in small-order execution sys-tems and upgraded communications between the CBOE and NYSES1

An anomaly between equity marketplace rules and the rules of derivative product marketplaces that received some attention was short sale regulation The SECs short sale ruleS2 prohibits persons from selling stocks short at a price below the last sale price (minus tick) or when the last trade involves a change in price that was a minus tick Such restrictions have never been imposed on options or futures53

That presents the potential for greater speculative selling in derivative products than can occur in the stock market and also the possibility that downside risk can be transferred to the stock market The SECs short sale rule has thus been undermined Both the Brady Commission and the SEC recommended that short sale regulation be revisited from an intermarket perspective

With regard to market unification the Brady Commission went further than the SEC or CITC and recommended that clearing systems be unified to reduce financial risk and information systems be established to monitor transactions and conditions in related markets In addition the Brady Commission recommended the harmonization of margin requirements to control speculation and financial leverage

Page 106

and the formulahon and implemenlahon of CHCUltbreaker mechanisms to protect the market system

CIRCUIT BREAKERS

Traditionally securihes exchanges have curbed volatility by relyinq on marqin and short sale regulation and com-modities exchanges have curbed volatility by relymq on price and position limits54 Since the October crash both stock and futures exchanges have raised margins for index products but not much 55 In addition the NYSEimposed a parhal ban on index arbitrage whenever the DJIA rises or falls 50 points in one day- When this collar is breached arbitrageurs must execute trends manually instead of usinq the automated DOT system of the NYSE

The Brady Commission recommended the installation of intermarket circuit breakers 57 The SEC however de-murred since price and position limits have lonq been anathema oJWall Street which believes that a continuous agency-auction market is best for investors- This contro-versy has continued

On March 18 1988 the President appointed a Working Group on financial Markets (Working Group) comprised of the Chairmen of the SEC CITC and fRB and the Secretary of the TreasurySlThe Working Group was given a mandate to agree within 60 days on intermarket mechanisms to prevent another crash The only concrete proposal put forward in the Working Groups Report was a circuit breaker mechanism whereby all stock and futures would close for one hour if the DJIA falls 250 points and for two hours if the DJIA falls 400 pointseoWhile this recommendation is not as

48 NASD Notice to Membcn 87-77 (Nov 20 1987) 49 SEC Report at 9-27 50 Brady Report at 5 51 SEC Report at 8-2~-2352 Rule 10a-1 under tbe Securities Excbanlc Act of 193453 SEC Rcport at 3-2454 Kauenbacb Report at 14-18 See lenerally R S Karme1 MarKlII UfIIlII and

MaritI VolalllY NYLJ bull Feb 18 1986 at 1ClOI 1 55 NYSE Inro Memo No 87-36 (Oct 26 1987) Amu Rais~s MarKill

RftllAiretrllllls lOt Broad MaritI lndu 00111 Sec Rcg L Rep (BNA) Vol 19 at 1655 (Oct 30 1987) See SEC CFTC CommissiolWs Oppos~

Higlu MGTfiIllJor Sloeic lNkJC FIAIIA~S Sec Rea L Rep (BNA) Vol 20 at 288 (Feb 261988)

56 KG Salwen Bil Board VOltS10Cwb 50_ Prolam Tad~s Wall St J bull Feb 5 1988 at 4 col 1 AlIo the ClOmmoditlesexchanges have impoied some ICW price liIIutl See S McMurray CBOT 10 lmpos~ Daily Pric~ 1mII 01

SOIM COIlDdI wan Sl J bull Nov 24 1987 at 2 ClOI 3 C1IicafOMc Says

CFTCChGnd Daily Pna Ismu Wall St J Mar 281987 at 24 col 2 57 Brady Report at 66-47 69 58 SEC Report at 3-23-324 59 Wltilt HOIll~ Iss_ Ord~ O~ailll WOIkg GrolAP 011 FillGMial MaruII

Sec Rea L Rep (BNA) Vol 20 at 452 (Mar 25 1988) 60 Intenm Report or tbe Worklnll Group on Fanancial MarkelS submitted to the

President or the UnIted States (May 1988) at App A

June 22 1988

drashc as some earlier tnal balloons it remains controversial for a number of reasons

Fast closmq the markets is hardly a step in the direction

of greater efficiency or harmonization The real criticism of marketrnakers in all the after-the-crash studies was that markets evaporated in the face of adversity While regula-hon cannot compel marketmakers to risk their capital into

bankruptcy in a rapidly falling market system-wide circuit breakers that close the markets would put a stamp of approval on market failure Secondly there is not at present a clear legislative basis for closing all public markets at once and even more importantly for preventing institutions

Irom trading in the third fourth or overseas markets when

the regulated markets are closed Moreover when the DJIA

approaches a limit it is likely that all investors will try to sell at once and institutions are far more likely than individuals

to succeed in doing so

The NYSE collar of 50 points on index arbitrage tradlng

through the automated DOT systemSI has also proven contro-versial and there are differences of opinion on whether this

circuit breaker has increased or lessened volatility62 Propo-nents of index arbitrage are essentially saying that the

futures and cash markets in stocks should be continuously

allgned but this very alignment transforms the futures

merket mto a lower cost pricing mechanism for stoclcs63 The

NYSE collar can be criticized for being ineffective since

once the 50-point limit is reached manual inde1l arbitrage

can continue However an outright ban on index arbitrage

would tend to disconnect the futures and cash markets This

would make pricing of index products less efficient but would tend to preserve the primacy of the pncing mecha-nism in the stock markels

By criticizing mechanisms for disconnecting the futures

and cash markets and instead urging intermarket circuit breakers to halt all trad1ng the Brady Commiss1on accepted

the commodihzation of the stock marlcet In the absence of physical delivery of stocks comprising the indexes however 1t is specious to argue that the futures markets are limply

performing a customary price discovery function Further-more unless margin levels between the primary and deriva-bve markets are harmonized this will inject greater leverage

and speculeuon Ulto the securities markets than have been

permitted smce the 1930s when the federal secunties laws

were passed

BASKETS

After institutional investors became attracted to index-ation-that is inveshng in the entire market or market segments-the ability to hedge by USlDg mdpx futures had

June~198l

an obvious appeal 64 All the after-the-crash studies recog-nize the leqitimacy of stock index trading for hedg1ng and

none recommend the ebohnon of index futures

These products have been designed to ht w1th1n the

confines of the Shad-Johnson Accord55 which in the

absence of agreement between the congressional commit-tees with oversiqht over the SEC and CITC spilt up jurisdic-tion over options and financial futures between the SEC and

CITC One necessary characteristic of a CITC-regulated

index product is lack of physical delivery- Further all commodities must be approved for trading by the CITC so

new products are designed to meet CFTC specifications67

Although after the Shad-Johnson Accord the SEC was

given authority to object to CITC approval of new index

products the SEC cannot block such approval Its recom-mendations would give it not only veto power over new index

products but also authority to compel the redesigning of old

products Implicit in the SECs request for such authority is

the suggestion that index futures pose a danger to the equity

markets The CITC however claims that index futures are

beneficial to the markets

The most Slgnificant proposal for changing the way in

which the primary and derivative markets interact is the

creation of baskets of stoclcs that would trade as a unit Alternatively index futures could be redesigned with a

physical delivery option These suggestions were contained

in the Katzenbach Report70 and the SEC Report71 The idea

for such a product is to ampHord institutional investors the

opportunity to do index investing and portfolio hedging in a

manner that does not involve the leveraqe currently at play

in the marketl

CONCLUSION

All observers agree that stock marlcet tradinq during the

week of October 19 was a debacle The markets officially

61 Index arbllrale doe5 not deal in pnee dlscrepanaes between ClljIlIYalenllCrms bul depends on tbe yield spread between an indell flltllres contract and 115

IInderlyinl sccunlles Many believe tbis form of proaram tradlnl Intensifies market volalduy Testimony or John J Phelan Jr Cbalrman NYSE before the Scnale Comm on Banking Housing and Urban MaIn Feb S 1918 at 13-14

62 See S McMllrray TJlJ~rs SQy ClUbs Ell4Clrd St1~ tM Ctult Havlaquo

Slaquo~Md Stock lUluts PItlp WaIlSI JApr IS1988p S7col3See also Ka1ZCnbacbReport al 29

63 See B T Byrne TM Stock 11IdFutllns lUlut 117-24 (1987) 64 Ka1ZCnbacbRcpon at 8-9 6S See GAO Report al 28 66 SEC Recommendations at 28 67 See TA RIWO R~plQtjotl 0 tlt~ Cooduj~s Fulurrs QIId OplOllS

lUlws III ~147 (1987) 68 SEC Recommendauons at 30 69 CITC Intenm Rcpon at S3-SS 70 Katzcnbacb Report II 29 71 SECReponaI3-J7-3-18

Page 107

stayed open but they were neither hquid nor continuousTheycame withm a heirs breadth ofclosmq completely andmany mdividual stocks and denvahve products did nottrade The enhre hnancial system was 10 jeopardy

In their after-the-crash studies regulators and self-regula-tors blamed one another for the chaos in the markets It ismteresting how little any of the studies focused on theoutside forces that caused the crash-serious macroeco-nomic problems on the one hand and institutional investorson the other According to the Brady Report a handful ofmstitutions did the trading that drove the markets down onOctober 19 and 2072 Although these institutions are eitherSEC-regulated mutual funds or pension funds regulated bythe Department of Labor curbs on index arbitrage or portio-lio insurance by these institutions has not been suggested

It is not surprising that the commissioners of the SEC andCFTC failed to blame the administration that appointed themfor economic policies that led to an historic stock marketdrop Further the congressional committees that have over-sight over the SEC and CFTC have fomen bulld rather thanresolved the jurisdictional problems dividing these agen-cies and the markets they regulate It also is not surpnsingthat the stock and commodities markets have refrained fromblaming their own customers and members for the marketcrash Ironically the principal users and member firms ofthese exchanges are the same organizations The economicand political battle for supremacy in pricing that is at theheart of the after-the-crash controversies is between theexchange floor members

If the markets remain volatile but not dangerously so it ispossible that some modest structural reforms will be agreedon to link trading more closely in the primary and derivativemarkets although the minimalist nature of the WorkingGroup Report makes even modest changes questionableSerious and Significant reform is very unlikely in the

Page 108

absence of pohtical change 1nWashlngton or a greater crisisin the economy and the markets

One lesson of Rashomon is that truth 19 hidden anduncertain but the frailty of human nature is a commoninqredient tll tragedy In WashIngton New Yorltor Chicagothere is at present no political leadership strong enough toconfront the truth scattered about in the after-the-crashstudies and to enforce a solution to the many problemsplaguing the markels The ultimate victims are likely to bethe corporations that need capital and pension fund benefi-ciaries whose life savings are at risk

The problems of the capital markets are only symptoms ofpolitical malaise and general financial disorder Clearlysecunties and commodities regulation should be integratedeither by merging the SEC and the CFTC or differentlydividing the responsibilities they now share over the cashand futures markets for securities Further the leverage andvelocity in the markets should be reduced either throughrevision of the margin requirements or otherwise For this tohappen stringent regulation of the financial markets mustregaIn political respectability Further the campaign contri-buhons which flowto presidential candidates and memberof the congressional oversight committees for the SEC andthe CFTC must be recognized as serious impediments toreform In addition attention should be given to what regula-tion is needed to change the destructive trading habits ofinstitutional investors which transcend such shibboleths asprogram trading

Yet reform of financial regulation will not balance thefederal budget rectify the trade deficit or even increase thesavings rate Until the Country begins to address thesefundamental economic problems greater stability in thestock market is a vain hope

72 Brady Report at

June 22 1988

bull

bull

uSSecurities and Exchange CommissionWashingtonDC 20549 (202) 272-2650

WOULD MORE REGULATION PREVENTANOTHER BLACK MONDAY

Remarks tothe CATO Institute Policy Forum

Washington DC

July 20 1988

Joseph A GrundfestCommissioner

[M~~[6~)~

The views expressed herein are those of Commissioner Grundfestand do not necessarily represent those of the Commission otherCommissioners or Commission staff

WOULD MORE REGULATIONPREVENT ANOTHER BLACK MONDAY

Remarks to the CATO Institute Policy ForumJuly 21 1988

Joseph A Grundfest

Its a pleasure to be here this afternoon to deliver anaddress on such a noncontroversial topic Governmentregulators in Washington DC have a well deserved reputationfor danding around difficult issues and not giving straightanswers to simple questions Well Id like to prove that Imnot your typical Washington DC regulator and give you astraight answer to the question Would more regulationprevent another Black Monday The answer is an unequivocableyes no and maybe The answer also depends on what you meanby more regulation and why you believe the market declined onBlack Monday with that issue cleared up Id like to thankall of you for attending and invite you to join the receptionbeing held immediately after this speech Thank you verymuch Its been a pleasure

Actually the question of whether more regulation couldprevent another Black Monday is not as difficult as it seemsif you keep three factors in mind First it is important todistinguish between fundamental factors that initiated orcontributed to the decline and regulatory or structuralfactors that may have unnecessarily exacerbated the declineRegulators at the securities and Exchange Commission can donothing to control or change fundamental factors To the

2

extent we attempt to prevent the market from adjusting tochanged fundamentals we are certain to generate far moremischief than good In this regard the opening line of theHypocratic Oath primum non nocere first do no harm shouldI believe be tattooed inside the eyelids of all governmentregulators to keep us from falling prey to the false butcomfortable idea that regulatory intervention can countermandfundamental market forces Regulatory hubris can be adangerous disease

Second once we have put aside the false notion thatregulation can prevent a market adjustment caused by changesin fundamentals it becomes important to isolate and defineaspects of the markets behavior on Black Monday that werelegitimately attributable to imperfections in the regulatoryand institutional environment On this score it is importantto recognize that none of our markets--equities options orfutures--covered themselves with glory on October 19 Theevidence suggests that many market systems buckled under theweight of massive information failures that were caused inpart by a substantial peak load problem These informationfailures exacerbated liquidity problems that would haveexisted naturally in a rapidly moving and high volume marketand contributed some volatility that could have been avoided

While it is impossible to define with precision exactlyhow much of Black Mondays 50S-point decline was attributableto fundamental factors and how much was attributable to

3

institutional and regulatory factors sUbject to governmentintervention it is my personal highly sUbjective and easilyrefuted estimate that about 200 to 250 Dow points of thedecline could have been avoided by a regulatory policy thatimproved information flows enhanced liquidity and expandedmarket capacity

Third it is absolutely critical to reject Ludditeconceptions of our markets as computer crazed automataProgram trading index arbitrage futures markets optionsmarkets and several other useful innovations in our capitalmarkets have been dangerously and incorrectly blamed for BlackMondays events We have often been warned not to confuse themessage with the messenger Nonetheless some participants inthe policy debate have a perfectly rational incentive tocontinue to confuse the message with the messenger in order toforestall technological progress that threatens traditionaltrading mechanisms that generate substantial rents for certainmarket participants Put more bluntly some people are makingmoney off the system as it operates today and measuresdesigned to make our markets more efficient by improvinginformation expanding capacity and enhancing liquidity arenot necessarily in everyones personal financial bestinterests

Each of these three factors provides enough material foran extended address so in the minutes allotted me I will nothave an opportunity to develop each of them in full

4

Accordingly I hope you will forgive me if I condense theexplanation a bit and occasionally skip abruptly from topic totopic

Fundamentals Cant Be Regulated Perhaps the mostinteresting consensus that has developed in the wake of BlackMonday is that the markets decline was at a minimumtriggered by fundamental-developments in the world economyThis consensus was recently described in an excellent addressby Ms Consuela washington Counsel of the House Committee onEnergy and commercelI Ms Washington pointed out how theBrady commission the SEC staff report the Chairman of theFed the CFTC and several market observers with widelydifferent perspectives on the events of October 19 includingFelix Rohatyn of Lazard Freres and Franklin Edwards ofColumbia University all agree that the decline was triggeredby changes in the macroeconomic environment that induced asharp revaluation of equity values because of changed investorexpectations Among the more frequently mentioned causes ofthe decline were adverse interest and exchange ratedevelopments an antitakeover tax proposal adopted by theHouse Ways and Means Committee and poor merchandise tradefigures

lICM Washington The Crash ofAssessment of Its significanceTimes International Conference(July 6 1988)

October 1987--A WashingtonAddress Before the FinancialBlack Monday--Nine Months After

5

Recently I had the opportunity to engage in privatediscussions with members of the international banking andbusiness communities and was quite intrigued to hear someviews that are not often expressed in the us policy debateMany of these foreign leaders perceived October 1987 as adangerous period in which major goverments were attempting tocontrol interest and exchange rates at levels that wereinternally inconsistent and at odds with changing macro-economic conditions and expectations In this environmentwith semi-pegged exchange and interest rates the equitymarkets turned out to be the major equilibrating forcethrough which the worlds capital markets could expressthemselves From this perspective the depth of the marketdecline may have been exacerbated by efforts to preventnecessary price movements in other major capital markets

Research by Professor Richard Roll of UCLA is broadlyconsistent with this non-US internationalist perspective~Professor Roll points out among other things that all theworlds capital markets declined sharply on or about October19 Of the 23 major world markets the US had the fifthsmallest decline--put another way the US had the fifth bestperformance The US market was not the first to declinesharply--the decline appears to have started with non-JapaneseAsian markets on October 19 their time and then followed the

1JR Roll ~The International Crash of October 1987 inBlack Monday and the Future of Financial Markets (Dow Jones-Irwin) (forthcoming)

6

sun to Europe the Americas and Japan The data also show nolink between computer directed trading and the extent of themarket decline Professor Roll concludes that -the globalnature of the October crash seems to suggest the presence ofsome underlying cause but it debunks the notion that somebasic institituional defect in the us was the cause and italso seems inconsistent with a US-specific macroeconomicevent-

Foreign business leaders also seem a bit amused by theorgy of analysis that has followed in the wake of the crashWith the exception of the Hong Kong market which shut itselfdown for the week of October 19 and suffered seriousconsequences both because of that shutdown and because of manyflaws in its internal processes no other market in the worldhas put itself to the degree of second-guessing finger-pointing and financial psychoanalysis as has the unitedstates While I firmly believe that the broad and searchinganalyses in the wake of the crash has been helpful I wasquite intrigued by a foreign perspective that we are overdoingit with analyses studies commissions task forces reportsand recommendations Foreigners appear much more willing toaccept the view that October 19 was a bad reaction thatresulted from adverse international macroeconomic events andthat little is to be gained by micro-economic tinkering withthe market To me this is a fascinating difference inperspective particularly to the extent it emanates from

7

foreign countries that experienced larger equity declinesthan the united states

Information capacity and Liquidity To the extent thatregulatory and institutional factors exacerbated the marketsdecline on October 19 the culprits can I believe beidentified as information failures capacity constraints andliquidity traps These three problems are all interrelated andcompounded each other on October 19 to make a bad day worse

In a nutshell and highly simplified form there weresubstantial periods of time on October 19 when traders did nothave accurate information on current prices and the status oforders that they had already entered If you wanted to tradeyou didnt know what price to expect and if you had enteredan order you didnt know for quite a while the price at whichyour order was executed Part of this problem wasattributable to the speed with which the market was movingbut part was also caused by capacity constraints thatprevented accurate information flows between customers andmarket floors In this environment traders were being askedto trade blind and it is no surprise to find that underthese circumstances traders backed away from the market orif they were willing to trade they demanded premia for therisk of trading in such an informationless environment Theinformation problems that led investors to back away from themarket removed liquidity from the market at the precise time

8

it was most in need and thereby exacerbated an alreadydifficult situation

The information problems grew worse on the 20th whenfears began to spread over the solvency of some major marketparticipants The concern was that the futures clearinghouseswere late in making substantial payments to large investmentbanks Because of the perceived credit risk associated withtrading with these institutions and in doing business withthe clearinghouses more participants backed away from themarket again at the very time that liquidity was needed mostThe institutions involved were all solvent but thatinformation could not be promptly and credibly signalled tothe market Thus an information failure related to creditstatus further exacerbated the liquidity problems present inthe marketplace

Accordingly to the extent that regulatory intervention~can improve information expand capacity and enhanceliquidity those steps seem to me to be the most logical andproductive measures for the government and marketplaces toconsider

position Limits An Example of A Regulation that MayHave Removed Information and Thereby Harmed the Market Toillustrate how regulatory constraints may have exacerbated themarkets decline Id like to focus on a relatively unknownregulatory constraint that may have had an impact on themarkets performance on Black Monday position limits onindex options

9

Purchasers of portfolio insurance seek to shift the riskassociated with the possibility that the stock market mightfall in excess of some pre-determined amount They attempt toprevent such losses by engaging in dynamic hedging strategiesthat involve selling into declining markets and buying intorising markets

These techniques at their root are no different -fromstop-loss trading rules that have been with us for decadesFor example suppose you have a $3 million portfolio in theequity market when the Dow is at 2500 and you want insurancethat you will be out of the market when the Dow hits 2200 Asimple dynamic hedge that provides just such an insuranceprogram would have you sell $1 million in stock when the Dowhits 2400 $1 million when the Dow hits 2300 and your last $1million when the Dow hits 2200 By following this very simpleset of stop loss rules you can insure yourself againstlosses that result from markets dropping below 2200--providedof course that the markets do not gap downward or become soilliquid that you cant execute your trades close to therequired prices which is what occurred on October 19

The relationship between portfolio insurance which isoften reviled as the demon that spooked the market into acrash and stop loss selling which is often described as a

I

conservative strategy suitable for small investors seeking tominimize their market risk is an important one because ithelps demystify portfolio insurance It also helps point out

10

consistently with some research findings by Professor RobertShiller of Yale UniversityJI that the market may have beensusceptible to profit-taking in a stop-loss formregardless of the existence of formal portfolio insuranceprograms I could expand on this theme but it would take mefar afield from the topic I want to address--the relationshipbetween portfolio insurance index option position limits andBlack Monday

To connect these pieces of the puzzle it is important tounderstand that there is a market substitute for portfolioinsurance when it is practiced as a dynamic hedge Thatsubstitute involves the purchase of a put option on aportfolio Whether a dynamic hedge is cheaper or better thanpurchasing a put option is an interesting question and Iwould argue that in an equilibrium with SUfficiently informedmarket participants the price of a dynamic hedge will at themargin equal the price of an equivalent put There ishowever an important informational difference betweenportfolio insurance practiced through dynamic hedgingtechniques and portfolio insurance practiced through putoption transactions As pointed out in a prescient August1987 article by Professor Sanford Grossman of Princeton

1JR Shiller Portfolio Insurance and Other Investor Fashionsas Factors in the 1987 Stock Market Crash (Feb 25 1988)(unpublished paper)

11

university~ dynamic hedge strategies provide substantiallyless information to the market than do put strategies Whenan investor buys a put option he signals to the world that hewould like to shift downside risk and the premium he pays forthat put measures the price that the market demands forshifting that risk In contrast dynamic hedging is notpublicly announced and it is not priced per se in any ~ante market transaction Thus an argument can be made thatthe market would have been less susceptible to destabilizingprice shocks that result from the unexpected use of stop lossorders or portfolio insurance if more investors had relied onput option strategies rather than dynamic hedge strategies

The problem however is that large institutions wereeffectively prohibited from relying on the options market asan effective hedge because SEC-approved exchange regulationsimposed position limits that limited the amount of insurancean institution could obtain through the option market2j Asone commentator put it unless and until position limits areeliminated the SampP 500 Index option cannot rival the SampP 500futures contract for portfolio insurance business~ ThUS

~S Grossman An Analysis of the Implications for Stockand Futures Price Volatility of Program Trading and DynamicHedging Strategies National Bureau of Economic Research(Working Paper 2337 Aug 1987)2jSee ~ Chicago Board Options Exchange Options Clearingcorporation Rule 244 (position Limits) (Jan 29 1988)~GL Gastineau The Options Manual 308 (3d ed 1988)Accord JG Cox and M Rubinstein options Markets 98 (1985)

12

regulatory position limits had the unfortunate side effect offorcing risk shifting activity away from options marketswhich would have provided greater information to all marketparticipants about the demand for downside equity risk hedgesand toward dynamic hedging strategies that do not provideequivalent information to the marketplace

Beware of Luddites Not all market observers agreehowever that the proper response to October 19 lies inimproving information expanding capacity and increasingliquidity There are policYmakers and market participants whodistrust recent innovations such as futures and optionsmarkets and program trading Their response to the marketsproblems would involve turning back the hands of time andfreezing our markets in a 1950-ish environment in which theprevailing ethos is that stocks are bought and sold one at atime based on fundamental assessments of the issuersunderlying prospects

As an initial matter I doubt that our equity marketsever truly worked that way and even if they did there is noreason to try to revert to that world even if we could undodecades of change The theory and practice of finance has inthe past 20 years experienced a revolution as profound asthose in biotechnology superconductivity and other areas ofhigh technology We know now that portfolios have propertiesthat are very different from simple aggregates of individualstocks We know now that it often makes perfect logical sense

13

to trade portfolios as portfolios (or baskets) and not asindividual securities

Moreover todays institutional investors are so largethat it is often impractical for them to make investmentdecisions on a stock-by-stock basis These large fundsenhance their returns not by picking General Motors overGeneral DYnamics or General Electric but by smart sectoralallocations among equities long bonds short bonds realestate venture capital and other broad investment classesIn this environment institutions have no rational choice butto trade portfolios as portfolios

These two forces--the growth of new informationsuggesting that it is smart to trade portfolios as portfoliosand the growth of large institutions that as a practicalmatter have to trade portfolios as portfolios--have combinedto change the demand for transactions services in the equitymarket unfortunately the supply of transactions services onthe equity side of the market did not keep pace with theevolution in demand because the New York stock Exchange onOctober 19 and till today trades equity on a stock-by-stockbasis and not as a portfolio This imbalance between the formof supply of transactions services and the form of demandcarries several adverse consequences for the operation of ourcapital markets which I dont have time to detail today

To put the problem in a laYmans perspective howeverId like to propose the following analogy Suppose you wanted

14

to bUy or sell a basket of stocks in todays equity marketAs a practical matter the basket would be broken down into aseries of say 400 individual securities transactions on thefloor of the exchange and if someone wanted to bUy exactlythe same basket that you had just sold he would also have toengage in 400 transactions on the floor of the exchange Ifwe operated our used Volkswagon markets according to the sameplan vw sellers would drive their autos onto dealers lotswhere the cars would be stripped down to fenders doors andengine blocks and when a buyer walked onto the lot the dealerwould reassemble the VW from the fenders doors and engineblocks If that doesnt seem like a particularly wise way tobuy and sell VWs I suggest that it may also not be the wisestway of buying or selling market baskets of equities

Fortunately recent developments suggest that the NewYork stock Exchange is actively exploring basket tradingmechanisms and I hope we will see substantial progress inthis direction in the near future

Conclusion In sum regulators can help prevent anotherBlack Monday but only if they act to remove existingimpediments in the market process by improving informationflows increasing capacity and enhancing liquidity We mustunderstand that the structure of demand for transactionsservices ischanging rapidly and that unless we innovatevigorously there is a substantial risk that we will damage ourdomestic financial service industry Unfortunately there are

15

many who believe that the answer to the markets problems liesin nostalgia for the past They would have us turn back thehands of time and urge measures designed to return the marketto the good old days of the 1950s 1960s and 1970sWell upon careful reflection I think youll find that thoseold days may not have been so good for everyone involved soeven if we could return to the past we might not want to go

More to the point however nostalgia is not a viablesolution to the markets problems The future lies ininnovation in innovations that adapt markets and regulationsto changing patterns of demand and technology To the extentthat we can achieve pro-competitive innovation throughregulation regulation can help prevent another Black MondayTo the extent we try to hold back inevitable processes ofchange or use the regulatory mechanism in an effort toprevent markets from adjusting to changed fundamentalsregulation is more likely to cause or exacerbate the nextBlack Monday

The choice is ours We still have an opportunity to getit right

uSSecurities and Exchange CommissionWashington D C 20549 (202) 272-2650

Observations on Black MondayBefore

The Federal Reserve Bank of ChicagoConference on Bank structure

and competition

May 12 1988

Joseph A GrundfestCommissioner

[N]~~[p6~~~

The views expressed herein are those of CommissionerGrundfest and do not necessarily represent those of theCommission other Commissioners or Commission staff

Federal Reserve Bank of ChicagoConference on Bank structure

COMMISSIONER GRUNDFEST Thank you very much Its apleasure to be here this afternoon to address so manydistinguished and unindicted members of the financialcommunity

(Laughter)As many of you may have noticed the political and

ethical scene in Washington often generates controversy andrecent events can charitably be described as suggesting alack of candor among politicians Because this is such anintimate group of several hundred people Id like to sharewith you an acid test useful to determine whether somebody inWashington is telling the truth You can imagine how valuablethis tool is so Im going to insist that we keep this littlesecret among ourselves

What Ive discovered is that if a person is moving hishand in a circular direction over his chin something likethis odds are hes not lying If a person moves his handwith a vertical motion over either cheek again he isprobably not lying And if you observe a horizontal moppingof the brow the odds again are that the person is not lying

However as soon a persons lips start to move all betsare off

(Laughter)

2

This rule has worked well for me and I hope it will workwell for you Please use the rule with great discretion andremember that you have all promised to keep it a secret

The experience of the past few months has taught me thatthe world moves faster than I type which may not be sayingvery much for those of you who have seen me at the wordprocessor Accordingly ~ have adapted my speechifying styleso that I now work without a prepared text my staffcomplains that this practice reminds them of a trapeze artistworking without a net but they appreciate the suspense itadds to their job and are gratified that they need not try toguess what I want to say

The subject of my talk this afternoon is at oncephilosophical and practical I would like to explore therelationship between reality and perceptions of reality asreflected in the current policy debate over regulation of ourcapital markets The distinction between that which is realand that which is perceived is quite important when dealingwith Congressmen regulators and other Washingtonprofessionals because the policy process is generallydominated by perceptions not realities If perception andreality happen to overlap that can be a happy coincidenceIf however the two diverge the real danger is that policywill be guided far more by perception than by reality

3